Moments That Matter Finding the Extraordinary in the Ordinary insights.fb.com October 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Moments That MatterFinding the Extraordinary in the Ordinary

insights.fb.comOctober 2015

2 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

TABLE OF CONTENTS

INTRODUCTION

ONCE- OR A-FEW-TIMES-IN-A-LIFETIME MOMENTS

The “Got Engaged” and “Just Married” Moments

The “We Had a Baby!” Moment

The “I Need a New Car” Moment

The “I’m Moving” Moment

ONCE-A-YEAR MOMENTS: A YEAR OF EXTRAORDINARY

EVERYDAY MOMENTS

The Cooking and Baking Moment

The Lost Phone Moment

The “I Need a New Phone” Moment

The Moment of Entertainment Discovery

The Multiscreening Moment

—The Watercooler Moment

—The Bingewatching Moment

The Shopping Moment

MULTIPLE-TIMES-A-DAY MOMENTS

How Our Brains Process Mobile vs. TV Moments

CONCLUSION

03

05

05

08

13

19

23

31

31

33

36

38

41

41

43

45

47

48

49

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 3

INTRODUCTION

Finding the Extraordinary in the OrdinaryWe are marketers participating in arguably the most important medium shift in marketing since the first television ad for Bulova watches in 1941. Mobile has delivered us from a mass media world to a personally relevant one—from a world in which marketers would buy TV, magazine and radio ads as a way to reach people based purely on context to a world in which marketers can reach individuals based not just on demographics but also on passions, behaviors, interests and so on. It’s driven the shift from a world of appointment-driven media ruled by rigid 15-, 30- and 60-second frameworks to a world of anytime/anywhere media.

And thanks to mobile, we’re moving from fewer bigger, longer moments manufactured by the media and marketing industry—moments like soap operas, the “Seinfeld” finale and pivotal sports games—to a time when people are manufacturing and consuming their own and each other’s moments en masse—every minute, every day, 365 days a year. From meals to memes, from first steps to first jobs and from moving on to moving up, millions of people go on Facebook and Instagram to share—and share in—these types of moments every day.

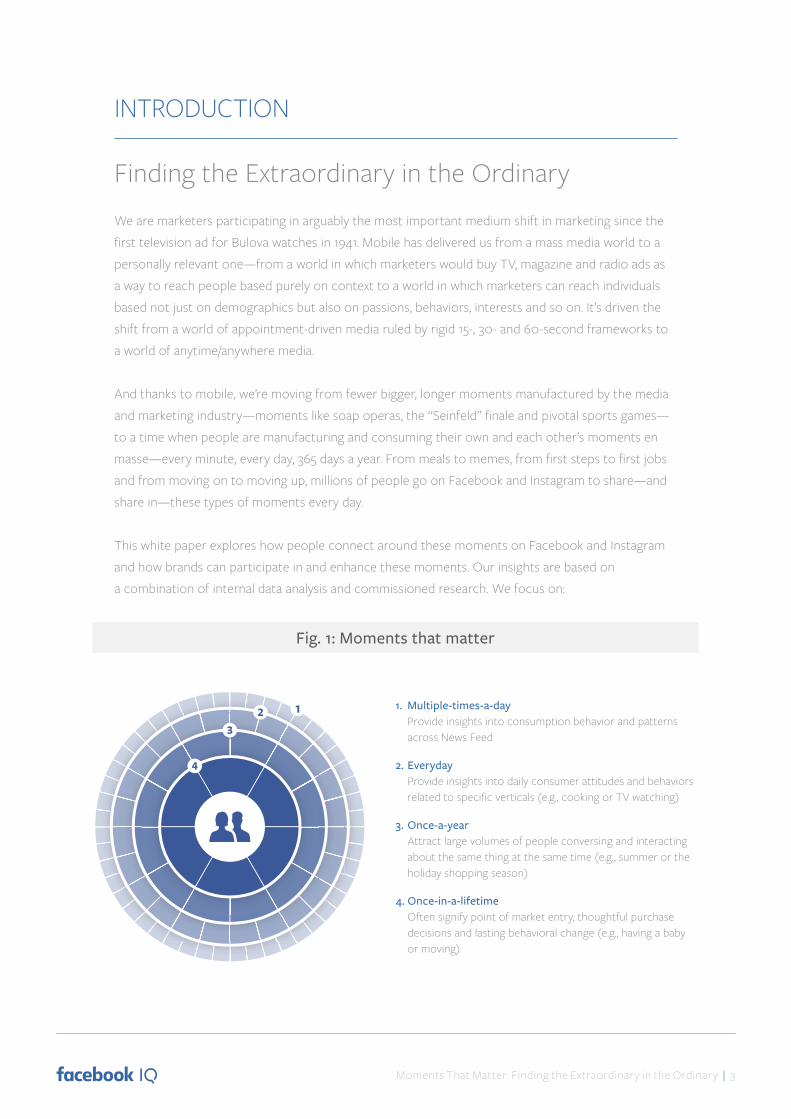

This white paper explores how people connect around these moments on Facebook and Instagram and how brands can participate in and enhance these moments. Our insights are based on a combination of internal data analysis and commissioned research. We focus on:

Fig. 1: Moments that matter

1. Multiple-times-a-day Provide insights into consumption behavior and patterns across News Feed

2. Everyday Provide insights into daily consumer attitudes and behaviors related to specific verticals (e.g., cooking or TV watching)

3. Once-a-year Attract large volumes of people conversing and interacting about the same thing at the same time (e.g., summer or the holiday shopping season)

4. Once-in-a-lifetime Often signify point of market entry, thoughtful purchase decisions and lasting behavioral change (e.g., having a baby or moving)

4 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

People have always had these moments in their lives. But marketers never had the opportunity to take part—until mobile. Mobile has given us the opportunity to capitalize on these very important, highly personal and uniquely relevant moments. It has never been easier to find the right people or the right moments.

In a breath,* there are a million moments of mobile discovery happening on Facebook and Instagram—that’s well over 20 trillion moments of mobile discovery each year.1 On the surface, some of these moments may feel ordinary. But dig deeper, and they belie extraordinary insights. Insights like …

For new parents, feeding time is Facebook time. People are friendlier in summer, accepting more friend requests than in any other season of the year. People are cooks on the weekdays, but they are gourmets on the weekends.

It’s a simple yet powerful idea: if we can understand more about the moments that matter to people—the magnitude, motivation and meaning of each moment—we can deliver experiences that matter more to them. We hope you use this white paper to explore and uncover how to leverage these ordinary moments to make your brand extraordinary.

1. Facebook internal data, Mar 2015. *A breath is measured as 3–5 seconds.

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 5

ONCE- OR A-FEW-TIMES-IN-A-LIFETIME MOMENTS

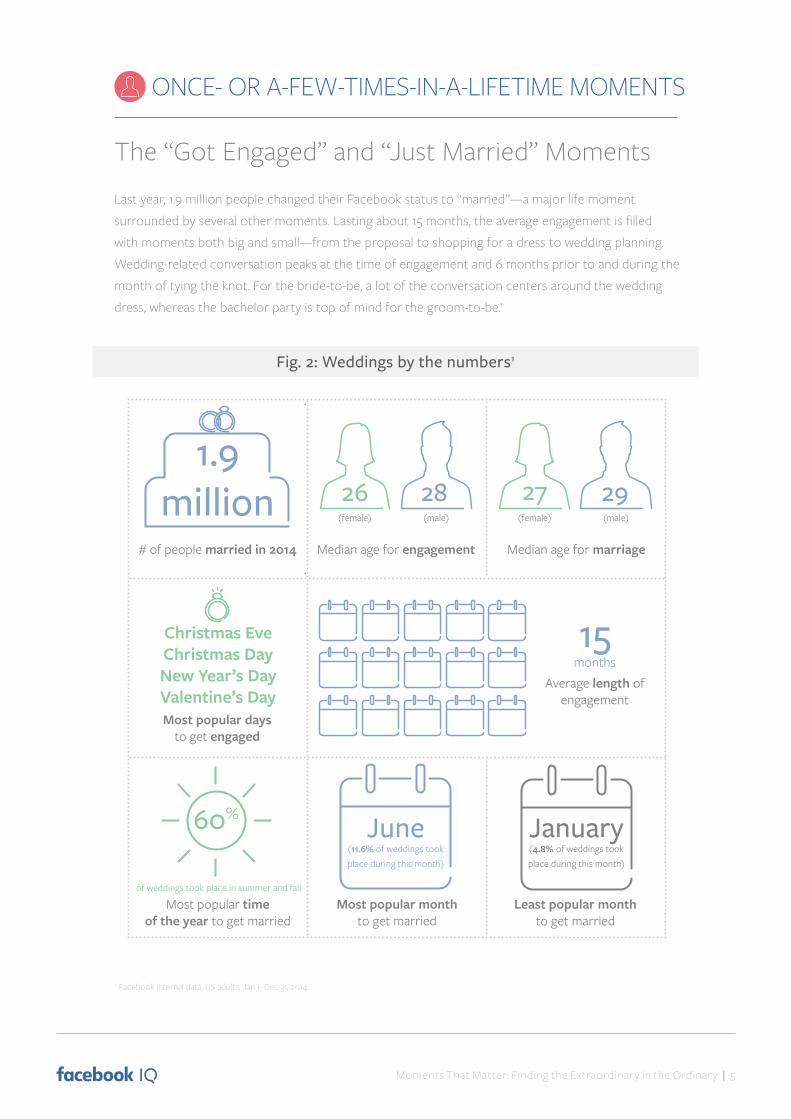

The “Got Engaged” and “Just Married” MomentsLast year, 1.9 million people changed their Facebook status to “married”—a major life moment surrounded by several other moments. Lasting about 15 months, the average engagement is filled with moments both big and small—from the proposal to shopping for a dress to wedding planning. Wedding-related conversation peaks at the time of engagement and 6 months prior to and during the month of tying the knot. For the bride-to-be, a lot of the conversation centers around the wedding dress, whereas the bachelor party is top of mind for the groom-to-be.1

Fig. 2: Weddings by the numbers1

# of people married in 2014

1.9million

Median age for engagement Median age for marriage

(female) (male)

Most popular daysto get engaged

Average length of engagement

Most popular timeof the year to get married

Most popular monthto get married

Least popular monthto get married

27 29

Christmas EveChristmas DayNew Year’s DayValentine’s Day

(female) (male)

26 28

June(11.6% of weddings took place during this month)

January(4.8% of weddings took place during this month)

60%

15months

of weddings took place in summer and fall

1. Facebook internal data, US adults, Jan 1–Dec 31, 2014.

Fig. 2: Weddings by the numbers1

6 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

Top Categories as per Keywords

Fig. 3: Finance-related conversation1

12 11 10 9 8 7 6 5 4 3 2 1

Wed

ding

mon

th

1 mon

th a

fter w

eddi

ng

2 m

onth

s afte

r wed

ding

3 m

onth

s afte

r wed

ding

Bride

Groom

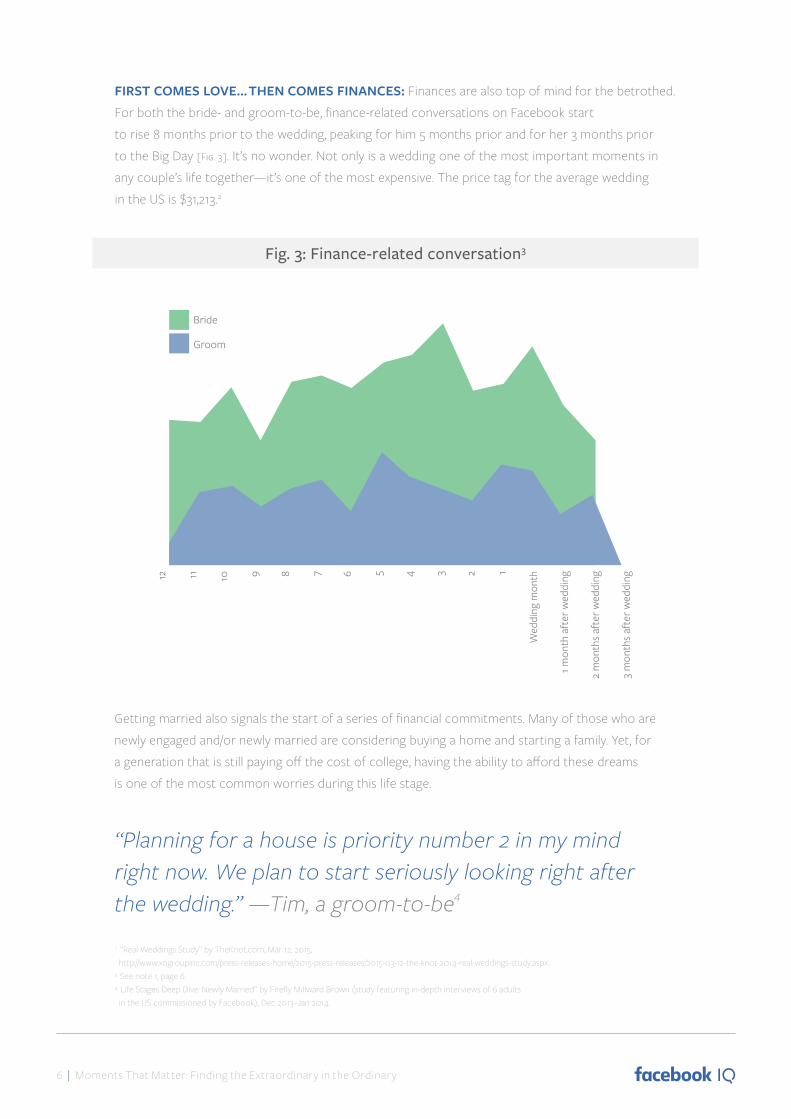

FIRST COMES LOVE… THEN COMES FINANCES: Finances are also top of mind for the betrothed. For both the bride- and groom-to-be, finance-related conversations on Facebook start to rise 8 months prior to the wedding, peaking for him 5 months prior and for her 3 months prior to the Big Day [Fig. 3]. It’s no wonder. Not only is a wedding one of the most important moments in any couple’s life together—it’s one of the most expensive. The price tag for the average wedding in the US is $31,213.2

Getting married also signals the start of a series of financial commitments. Many of those who are newly engaged and/or newly married are considering buying a home and starting a family. Yet, for a generation that is still paying off the cost of college, having the ability to afford these dreams is one of the most common worries during this life stage.

“Planning for a house is priority number 2 in my mind right now. We plan to start seriously looking right after the wedding.” —Tim, a groom-to-be4

2. “Real Weddings Study” by TheKnot.com, Mar 12, 2015, http://www.xogroupinc.com/press-releases-home/2015-press-releases/2015-03-12-the-knot-2014-real-weddings-study.aspx.3. See note 1, page 6.4. Life Stages Deep Dive: Newly Married” by Firefly Millward Brown (study featuring in-depth interviews of 6 adults in the US commissioned by Facebook), Dec 2013–Jan 2014.

Fig. 3: Finance-related conversation3

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 7

Insights and Implications ACT AS A FINANCIAL ADVISOR AND BUILD LIFETIME VALUE: During this life stage, couples are focused on finances—whether it’s because of the cost of the wedding and the honeymoon or because it’s a time when they’re planning their futures. Brands can help the newly engaged and newly

married set their financial and life goals and map out what it would take to reach them. They also

have an opportunity to build a long-term relationship by reaching couples when they are making big

purchases together for the first time (e.g., home, car, furnishings, appliances and Internet and cable

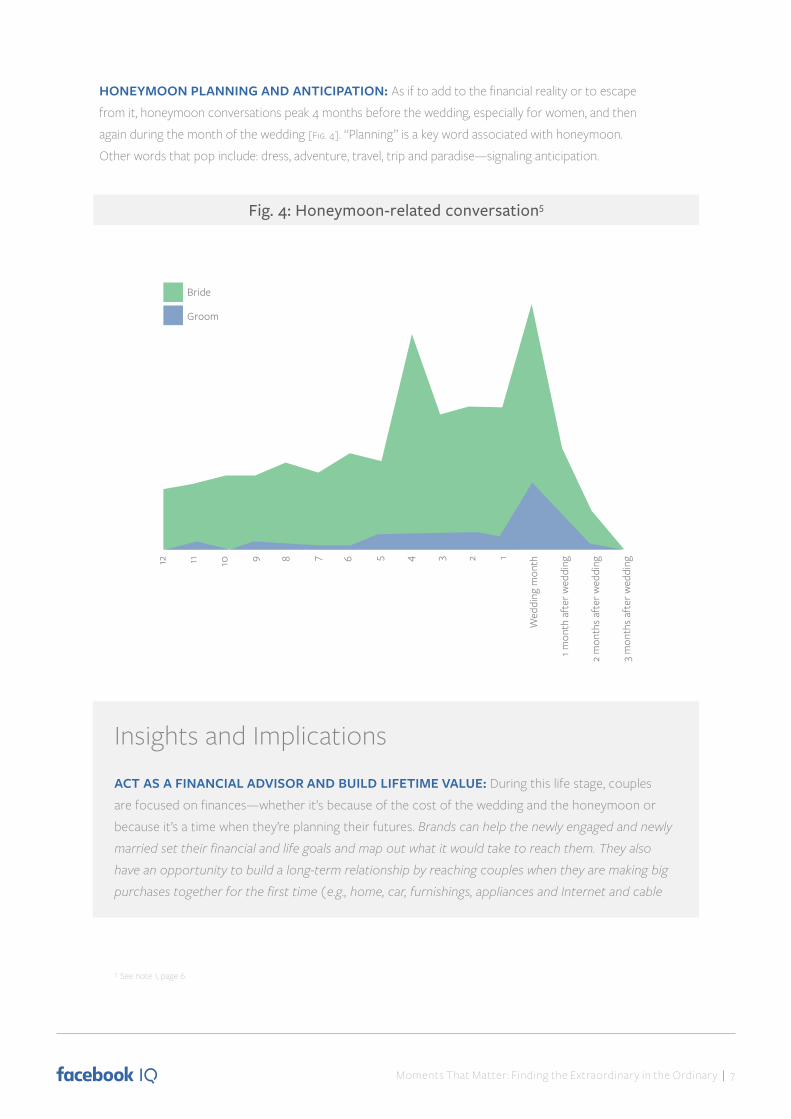

HONEYMOON PLANNING AND ANTICIPATION: As if to add to the financial reality or to escape from it, honeymoon conversations peak 4 months before the wedding, especially for women, and then again during the month of the wedding [Fig. 4]. “Planning” is a key word associated with honeymoon. Other words that pop include: dress, adventure, travel, trip and paradise—signaling anticipation.

5. See note 1, page 6.

Top Categories as per Keywords

Fig. 4: Honeymoon-related conversation1

Bride

12 11 10 9 8 7 6 5 4 3 2 1

Wed

ding

mon

th

1 mon

th a

fter w

eddi

ng

2 m

onth

s afte

r wed

ding

3 m

onth

s afte

r wed

ding

Groom

Fig. 4: Honeymoon-related conversation5

8 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

TV subscriptions) and then building loyalty and retention programs to ensure consideration

and conversion during subsequent key decision points.

DON’T FORGET THE PARENTS: The average couple is in their 20s, likely cash-strapped and receiving help with expenses. According to The Knot, on average, the bride’s parents contribute 43%, the groom’s parents contribute 12% and the bride and groom contribute 43% of the total wedding budget (others account for the remaining 2%). This creates potential for brands

to connect with the parents of the bride- and groom-to-be with targeted messaging.

BE A PART OF THE CONSIDERATION AND ANTICIPATION: Chatter data indicate that there are 2 phases ahead of the honeymoon: the actual planning of the trip and then the anticipation. Travel brands can take advantage of these key moments, first as couples determine their

destination and then as they prepare to head off into the sunset as newlyweds.

The “We Had a Baby!” MomentFrom the birth announcement to sleepless nights to all of their child’s “firsts,” being a parent becomes a collection of moments for new moms and dads. With the average new parents spending anywhere from $4,000 to $10,000 on their baby before the end of their child’s first year,1 brands can connect and earn their way into new parents’ trusted circle by providing advice and motivations along the way through the device that is most accessible—the mobile phone.

PARENTHOOD MEANS MOBILEHOOD: With a baby in their arms and a phone in their hands, mobile is new parents’ connective tissue to the wider world. New parents spend 1.4X more time on Facebook mobile than non-parents. Moms primarily drive the increase in mobile activity, spending 1.5X more time on Facebook mobile than non-moms, though new dads also spend 1.1X more time on Facebook mobile than non-dads.2

Living in a world that can sometimes feel chaotic, mobile is a medium new moms and dads can readily consume. Mobile devices help new parents stay connected and informed, capture and share their kids’ key milestones and retain their sense of identity.

FEEDING TIME IS FACEBOOK TIME: Parents’ first mobile session of the day starts early. New parents are active on Facebook in the wee hours, starting their first mobile sessions as early as 4am and peaking at 7am. By 7am, 56% of new parents on mobile have visited Facebook for their first mobile session of the day. Comparatively, 45% of non-parents have logged into Facebook by 7am.2 It seems that feeding time is Facebook time [Fig. 5].

1. Survey conducted by Babycenter and The Bump’s Annual Pregnancy and Baby Study: http://www.babycenter.com/0_by-the-numbers-key-stats-from-our- moms-and-money-survey_1744466.bc, http://www.dailymail.co.uk/femail/article-2044921/How-new-parents-spend-4-000-born--experts-warn-bassinets- baby-wipe-warmers-waste-money.html. 2. Facebook internal data, US adults, Jan–Apr 2015. Based on 1.6 million new moms and 925,000 new dads. Each segment is a result of self-reported and inferred data combined with a proprietary method of assessing affinity. Parents having a child under the age of 1 are the “New Parents” affinity segment. Non-parents are defined as those who do not belong to the New Parents affinity segment.

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 9

Fig. 5: New parents’ fi rst mobile sessions of the day on Facebook vs. non-parents160%

55%

50%

45%

40%

35%

30%

25%

20%

15%

10%

5%0%

% of people who have been on Facebook mobile (accumulated)

56%

45%

4 am

5 am

6 am

7 am

Non-parents New parents

SHARENTING: “Sharenting” has been defined by Urban Dictionary as “when parents share too much of their children’s information, pictures and private moments online, mostly on Facebook.” 4 Indeed, new moms and dads overindex on all Facebook activity—status updates, photo posts, video posts, etc.—except check-ins. This increase in activity is driven primarily by new moms, particularly

3. See note 2, page 9.4. Urban Dictionary, http://www.urbandictionary.com/define.php?term=Sharenting.

Fig. 5: New parents’ first mobile sessions of the day on Facebook vs. non-parents3

10 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

New moms New dads New momsages 18-34

New dadsages 18-34

Status updates 2.6x 1.7x 2.6x 1.8x

Links 2.2x 1.4x 2.3x 1.5x

Photos 2.9x 1.6x 3.0x 1.7x

Videos 5.0x 2.0x 5.5x 2.0x

Check-ins -1.3x -1.5x -1.3x -1.6x

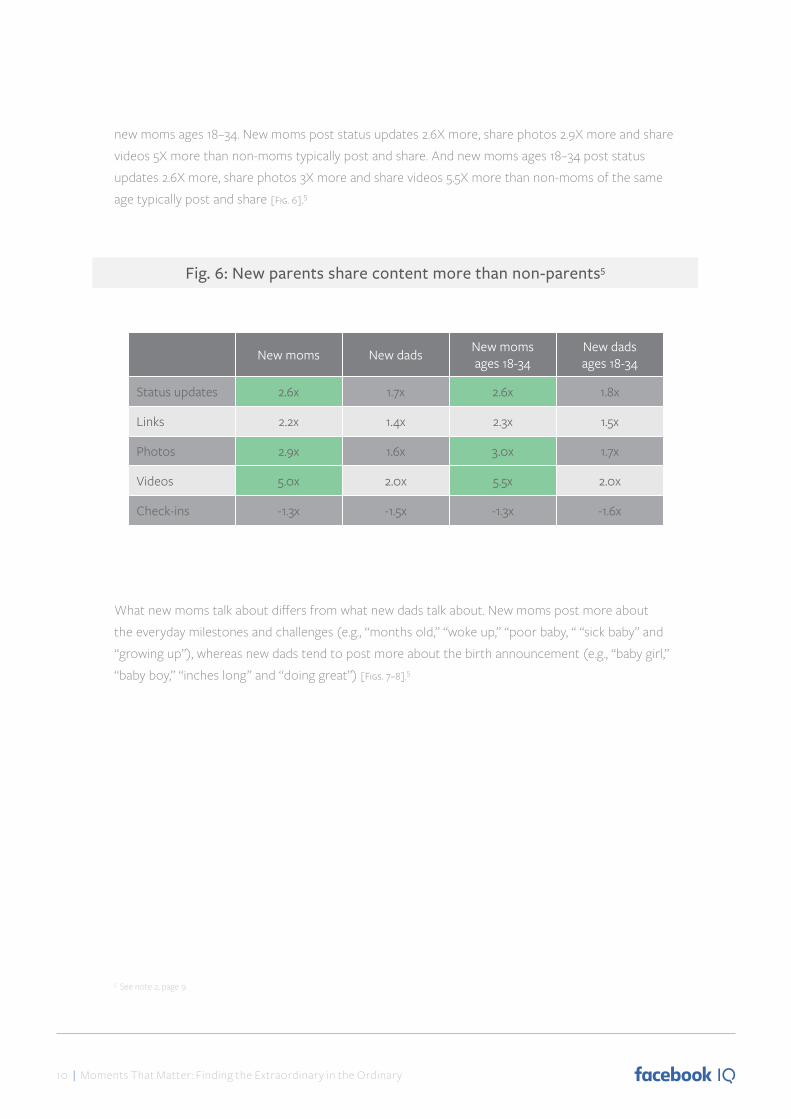

Fig. 6: New parents share content more than non-parents1

new moms ages 18–34. New moms post status updates 2.6X more, share photos 2.9X more and share videos 5X more than non-moms typically post and share. And new moms ages 18–34 post status updates 2.6X more, share photos 3X more and share videos 5.5X more than non-moms of the same age typically post and share [Fig. 6].5

5. See note 2, page 9.

Fig. 6: New parents share content more than non-parents5

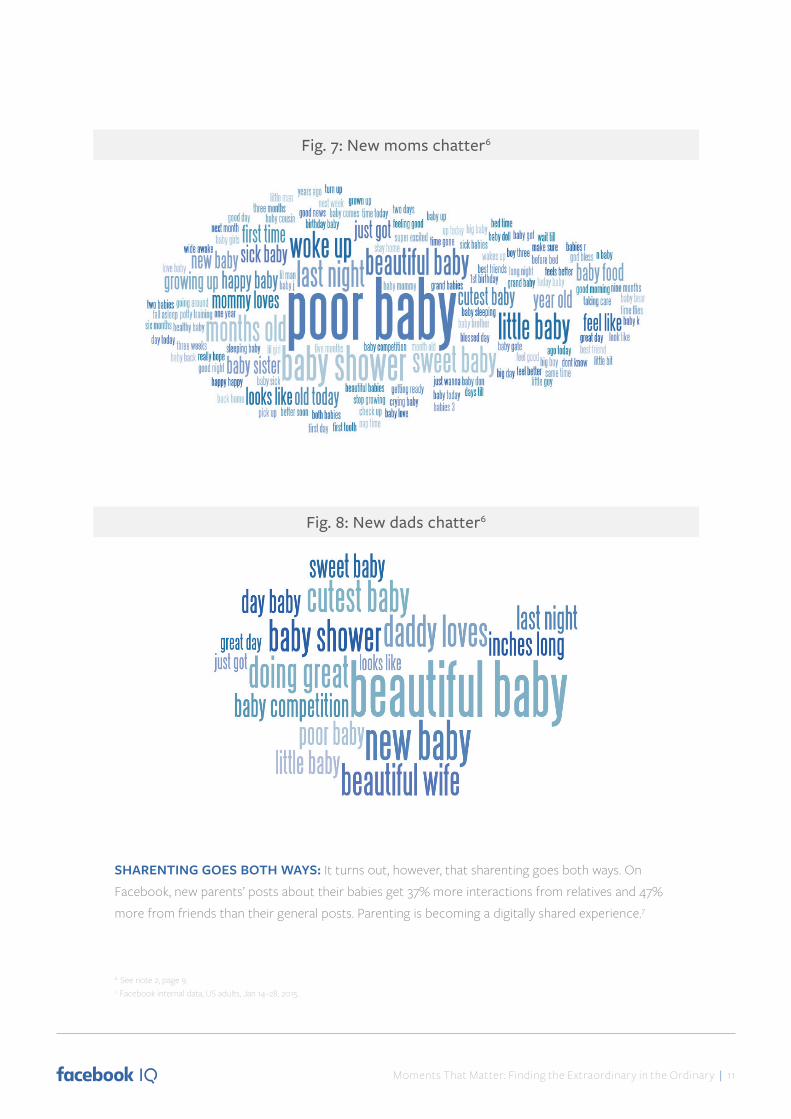

What new moms talk about differs from what new dads talk about. New moms post more about the everyday milestones and challenges (e.g., “months old,” “woke up,” “poor baby, “ “sick baby” and “growing up”), whereas new dads tend to post more about the birth announcement (e.g., “baby girl,” “baby boy,” “inches long” and “doing great”) [Figs. 7–8].5

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 11

SHARENTING GOES BOTH WAYS: It turns out, however, that sharenting goes both ways. On Facebook, new parents’ posts about their babies get 37% more interactions from relatives and 47% more from friends than their general posts. Parenting is becoming a digitally shared experience.7

6. See note 2, page 9. 7. Facebook internal data, US adults, Jan 14–28, 2015.

Fig. 7: New moms chatter6

Fig. 8: New dads chatter6

12 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

8. Ipsos survey data of 7,167 parents in US, UK, AU, BR, MX, CA and DE, Mar–Apr 2015. Results are statistically significant. “Friends” as part of the definition of family includes 2 or more friends.

THE FLUIDITY OF FAMILY: The idea of family is more fluid for new parents than for parents of toddlers and older kids. New parents are more likely to consider relatives and friends in their definition of family than are parents of older kids.8 91% of new parents versus 85% of parents of older kids include extended family members in their definition of family.8 34% of new parents versus 29% of parents of older kids include friends in their definition of family.8

Thanks to technology, we are are shifting back to an extended family structure, albeit one of a more virtual kind. Technology has enabled this family fluidity, allowing new parents to share, connect, inform and ask advice of grandparents, aunts, uncles, cousins and friends both near and far on a regular basis. As parents capture and share their baby’s milestone moments, they in essence invite extended family to help them raise their child. Extended families are now more involved and influential than they have been since the rise of the nuclear family.

Insights and ImplicationsDELIVER “SNACKABLE” CONTENT FOR MOBILE MOMENTS: With a baby in their arms and a phone in their hands, mobile is new parents’ connective tissue to the wider world. Brands

can create bite-sized, image-heavy content and catchy videos that will appeal to harried parents

during stolen moments for self. There are so many moments during the first days and years

of being a parent, and mobile (and Facebook and Instagram) can serve as a gateway to

tips, products and motivations along the way.

SEIZE ISOLATED, QUIET MOMENTS OF PARENTHOOD: Feeding time is Facebook time, with new parents starting their first mobile session of the day in the wee hours. This is an opportunity

for brands to reach new moms and dads at a time when parents can’t be reached elsewhere and

in moments that were never accessible before.

BE A PART OF THE EXTENDED FAMILY: Thanks to technology, extended families are now more involved and influential than they have been since the rise of the nuclear family. Parenting has become a digitally shared experience. Brands can earn their way into this trusted circle in a number of ways. For

instance, brands can help simplify and address the information overload and key questions that arise in

the run-up to and early days and years of parenthood, offering reassurance that everything’s going to be

alright. Brands can also recognize the unique roles played by new moms and dads when speaking to them,

as new moms are involved more in the everyday challenges while new dads focus on the major milestones.

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 13

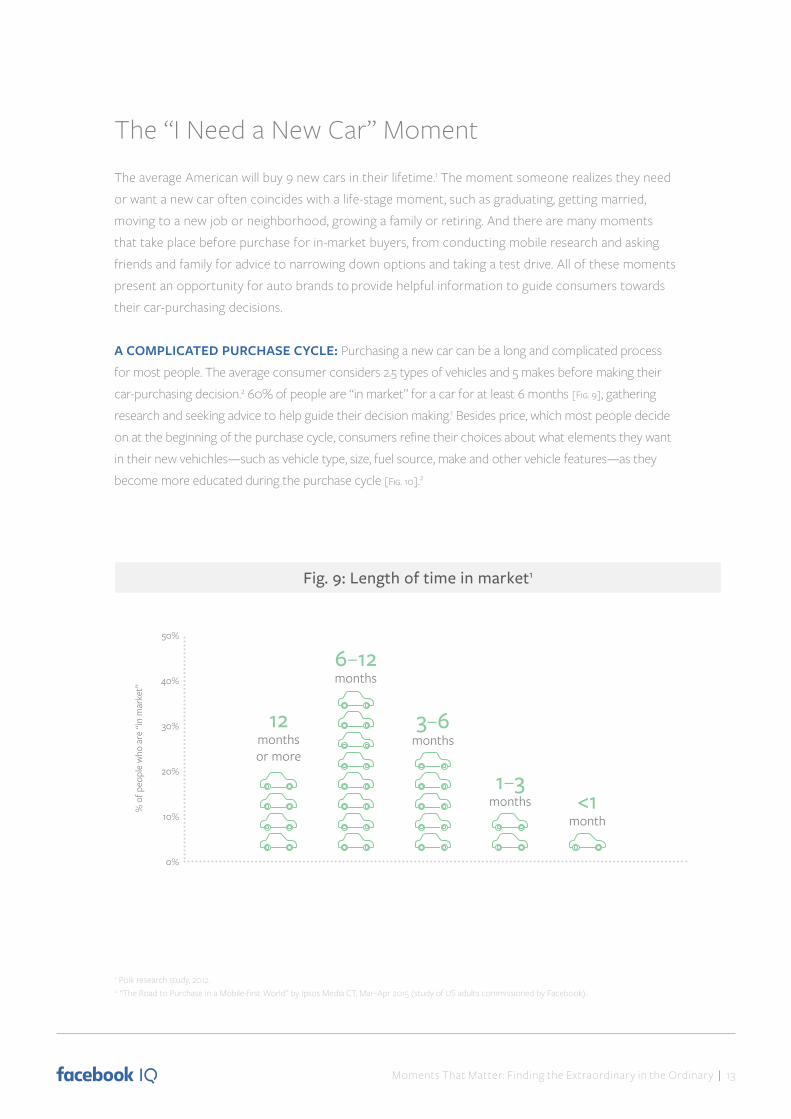

The “I Need a New Car” MomentThe average American will buy 9 new cars in their lifetime.1 The moment someone realizes they need or want a new car often coincides with a life-stage moment, such as graduating, getting married, moving to a new job or neighborhood, growing a family or retiring. And there are many moments that take place before purchase for in-market buyers, from conducting mobile research and asking friends and family for advice to narrowing down options and taking a test drive. All of these moments present an opportunity for auto brands to provide helpful information to guide consumers towards their car-purchasing decisions.

A COMPLICATED PURCHASE CYCLE: Purchasing a new car can be a long and complicated process for most people. The average consumer considers 2.5 types of vehicles and 5 makes before making their car-purchasing decision.2 60% of people are “in market” for a car for at least 6 months [Fig. 9], gathering research and seeking advice to help guide their decision making.1 Besides price, which most people decide on at the beginning of the purchase cycle, consumers refine their choices about what elements they want in their new vehichles—such as vehicle type, size, fuel source, make and other vehicle features—as they become more educated during the purchase cycle [Fig. 10].2

50%

40%

30%

20%

10%

0%

12 monthsor more

6–12 months

3–6months

1–3 months <1

month

% o

f peo

ple

who

are

“in

mar

ket”

Fig. 10: Length of time in market1

1. Polk research study, 2012.2. “The Road to Purchase in a Mobile-first World” by Ipsos Media CT, Mar–Apr 2015 (study of US adults commissioned by Facebook).

Fig. 9: Length of time in market1

14 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

% o

f peo

ple

cert

ain

Fig. 11: Certainty of vehicle elements1

61%

51%

40%39%

32%

69%67%65%64%61%59%

PriceTypeSizeFuel sourceMakeFeatures

Number of months before purchase

6–12 3–6 1–3 Less than 1

61%

3. Respondents who report not being asked advice about cars by others. Average car buyers represent 87% of survey respondents.4. See note 2, page 14.

Fig. 10: Certainty of vehicle elements4

OPPORTUNITY GAP: In the last month before purchase, 59% of average car buyers3 narrow down their choice of vehicle make and type to 1–2 cars.4 Yet this last month is when people say they are exposed to the most ads on digital [Fig. 11].4 This signals an opportunity for marketers to use digital to influence consumers earlier in the purchase cycle, before they decide on features and vehicle choice.

Fig. 12: Claimed ad exposure1

100%

0%

Opportunity

% o

f buy

ers w

ith1-2

car

s in

cons

ider

atio

n

Number of months before purchase

6–12 3–6 1–3 Less than 1

Claimed ad exposure

Offl ine

Desktop

Mobile

71%

35%

21%

43%

27%

50%

35%

68%

60%

42%

71% 71%

Fig. 11: Claimed ad exposure4

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 15

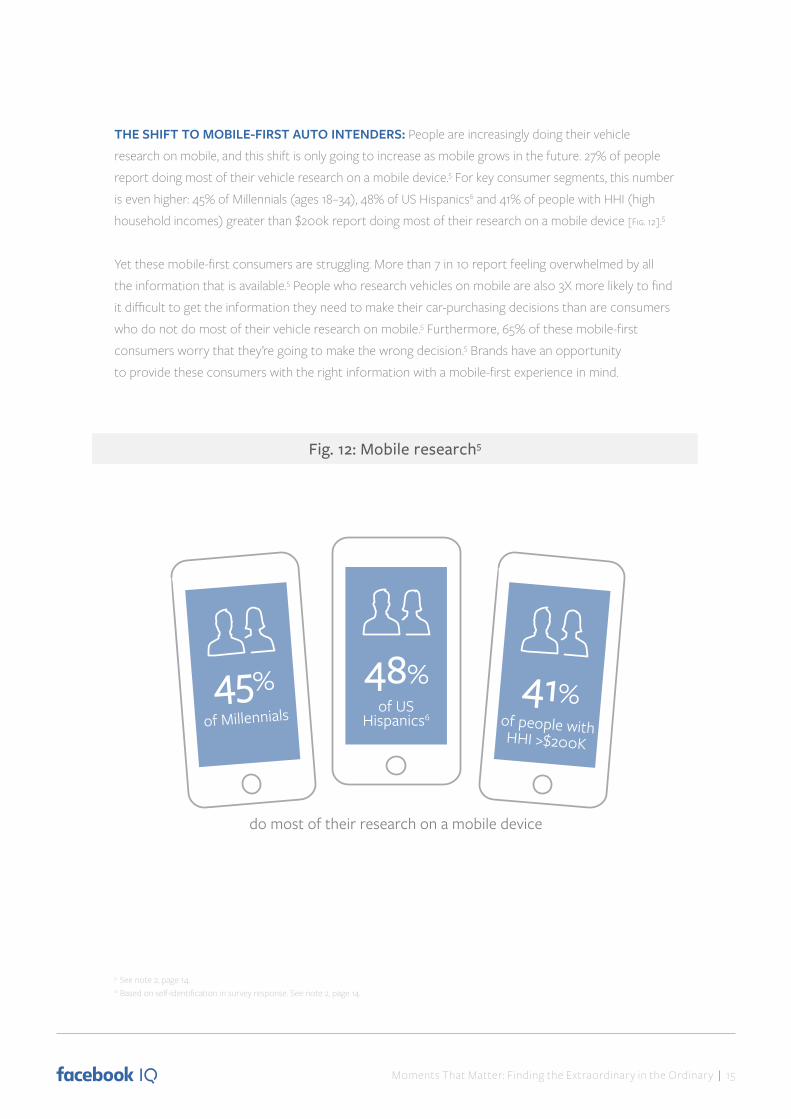

THE SHIFT TO MOBILE-FIRST AUTO INTENDERS: People are increasingly doing their vehicle research on mobile, and this shift is only going to increase as mobile grows in the future. 27% of people report doing most of their vehicle research on a mobile device.5 For key consumer segments, this number is even higher: 45% of Millennials (ages 18–34), 48% of US Hispanics6 and 41% of people with HHI (high household incomes) greater than $200k report doing most of their research on a mobile device [Fig. 12].5

Yet these mobile-first consumers are struggling. More than 7 in 10 report feeling overwhelmed by all the information that is available.5 People who research vehicles on mobile are also 3X more likely to find it difficult to get the information they need to make their car-purchasing decisions than are consumers who do not do most of their vehicle research on mobile.5 Furthermore, 65% of these mobile-first consumers worry that they’re going to make the wrong decision.5 Brands have an opportunity to provide these consumers with the right information with a mobile-first experience in mind.

Fig. 13: Mobile research1

do most of their research on a mobile device

48%of US

Hispanics6

41%of people withHHI >$200K

45%of Millennials

5. See note 2, page 14. 6. Based on self-identification in survey response. See note 2, page 14.

Fig. 12: Mobile research5

16 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

LIFE-STAGE MOMENTS DRIVE PURCHASE: We found that the reason people give for buying a new car (“old car,” “just feel like a new one”) is often not the real reason behind this purchase moment. Instead, it’s life-stage moments that are driving purchases.7 New life stages, such as growing a family, starting a new job or moving, can signal when someone is or will be in the market for a car. These signals can help marketers know when to reach people, upstream in the purchase cycle and before the last month when most consumers have made up their minds.

“Our current vehicle needs to replaced because it’s old and is needing more frequent repairs. Also our children are getting bigger and they don’t all fit as comfortably in the vehicle as when they were babies/toddlers.”7

7. See note 2, page 14.

People who are in new life stages are more likely to do most of their vehicle research on mobile, compared to people who are not in new life stages.7 For instance, new parents and newlyweds are 2.4X more likely to do most of their research on mobile and new homeowners and recent graduates and retirees are 2.1X more likely, compared to people not in these life stages.7

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 17

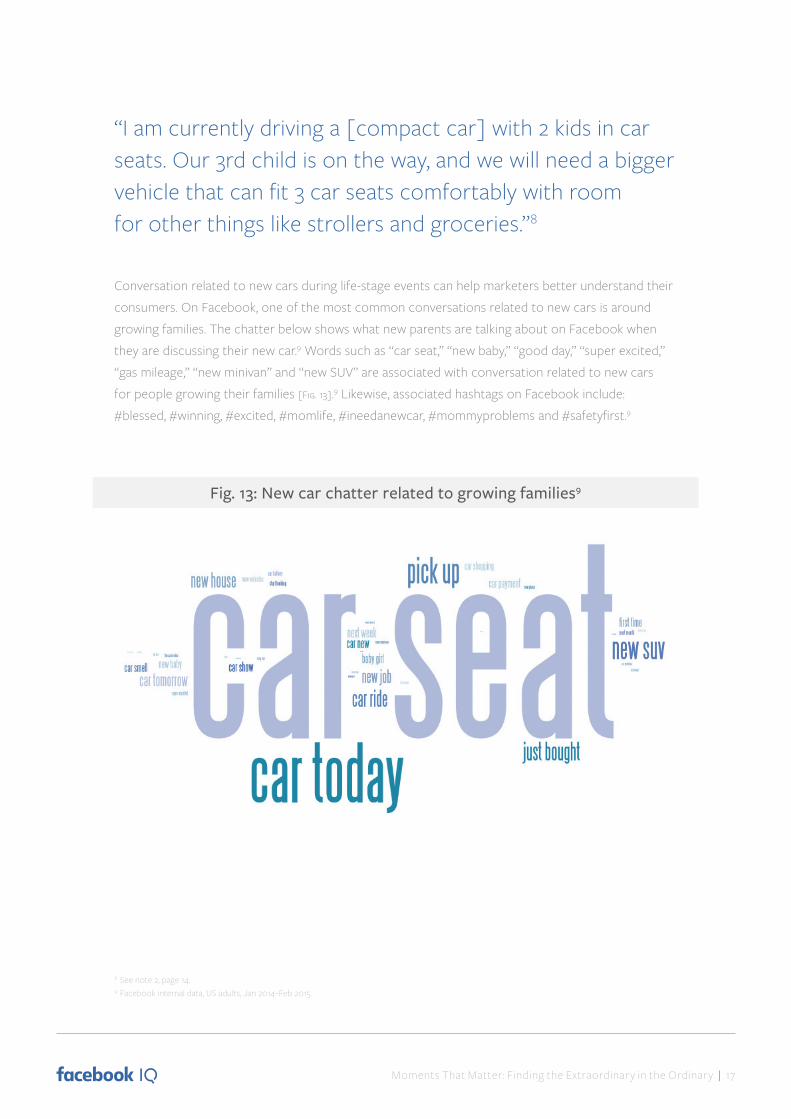

“I am currently driving a [compact car] with 2 kids in car seats. Our 3rd child is on the way, and we will need a bigger vehicle that can fit 3 car seats comfortably with room for other things like strollers and groceries.”8

8. See note 2, page 14.9. Facebook internal data, US adults, Jan 2014–Feb 2015.

Fig. 13: New car chatter related to growing families9

Conversation related to new cars during life-stage events can help marketers better understand their consumers. On Facebook, one of the most common conversations related to new cars is around growing families. The chatter below shows what new parents are talking about on Facebook when they are discussing their new car.9 Words such as “car seat,” “new baby,” “good day,” “super excited,” “gas mileage,” “new minivan” and “new SUV” are associated with conversation related to new cars for people growing their families [Fig. 13].9 Likewise, associated hashtags on Facebook include: #blessed, #winning, #excited, #momlife, #ineedanewcar, #mommyproblems and #safetyfirst.9

18 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

“I am about to start a new job and would like to replace my old truck with a new one.”10

“Recently moved to CA from NYC so didn’t need a car before.”10

Insights and ImplicationsREACH PEOPLE ON DIGITAL EARLIER IN THE PURCHASE PROCESS: By the last month before purchase, the average buyer has narrowed down their vehicle choices significantly. But the last month is when people are exposed to the most digital ads. Brands can use the power of digital to drive

awareness, consideration and intent before buyers make up their minds.

MAKE IT MOBILE: Mobile is where key audiences are doing their vehicle research. But these mobile-first buyers are struggling to find the right information they need to make their car purchase decisions. Brands can design experiences with mobile-first buyers in mind, providing information

in bite-sized, easy-to-digest, highly visual formats. This will be key in attracting key audiences like

Millennials, US Hispanics, people with high household incomes and also future consumers, as mobile

use for auto purchase intenders will only increase.

UNDERSTAND TRIGGERS: Life-stage events, such as having a baby or moving, can signal when someone is or will be in the market for a car. People going through a new life stage are also more likely to do most of their vehicle research on mobile, compared to those who aren’t in a new life stage. Brands can target potential buyers during life-stage events, when they are seeking opinions

and advice from friends and family, and speak to them with their feelings and purchase needs in mind.

10. See note 2, page 14.

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 19

The “I’m Moving” MomentAs people who have recently moved stay connected to their former communities and connect with their new ones, they go online to talk about everything from bubble wrap and packing to their new address and renovations.

Moving is an important point of market entry for many marketers. It signals an opportunity for people to try new things, switch brands and services, learn their local neighborhoods and start anew in many ways. In fact, people who move make moving-related purchases for up to 7 months around their move (3.2 months before, and 3.8 months after)1 and spend around $9,000 per household on goods, services and financial products.2

People who move are more likely to switch brands for baby products, dishwashing detergent and household cleaner and more likely to spend on home entertainment systems, kitchen appliances, laptops, smartphones and digital cameras than people who have not moved.1 It is also more likely that a person who just moved, as compared to someone who has not moved, will purchase a car within 12 months of moving.1

Moving can also present a challenge in reaching people through traditional marketing means, as the move can be the only thing on their minds and their media habits are often disrupted.

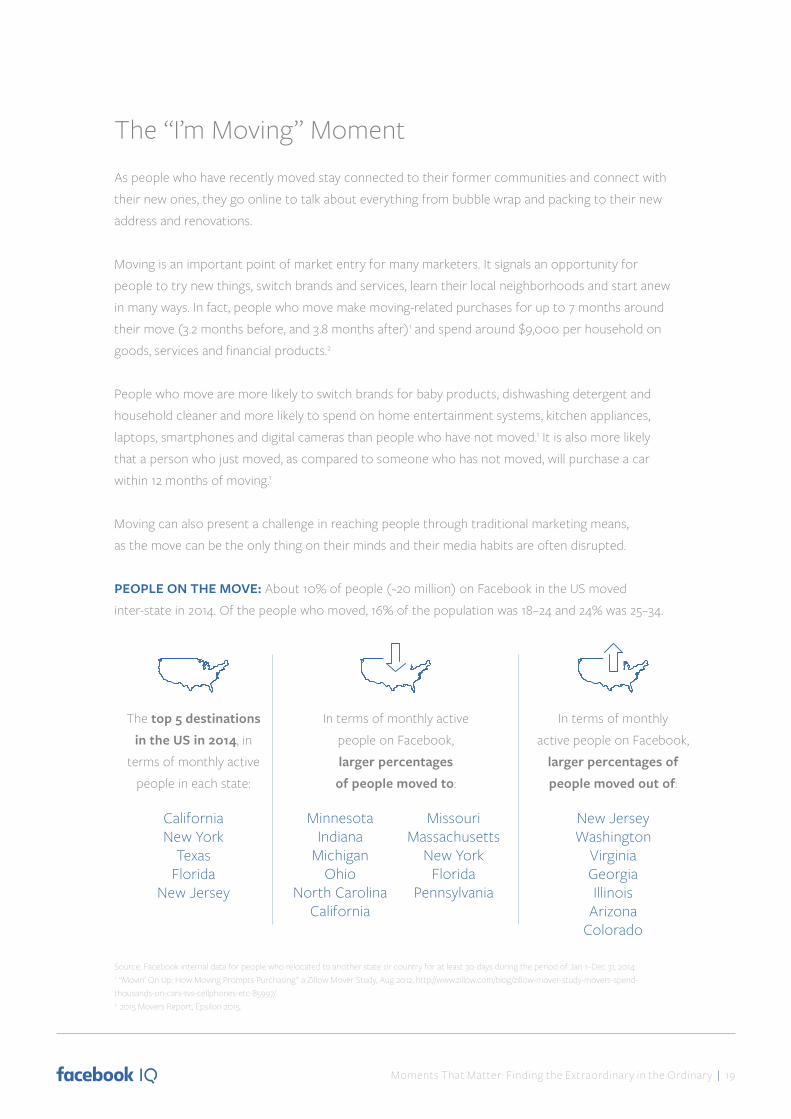

PEOPLE ON THE MOVE: About 10% of people (~20 million) on Facebook in the US moved inter-state in 2014. Of the people who moved, 16% of the population was 18–24 and 24% was 25–34.

Source: Facebook internal data for people who relocated to another state or country for at least 30 days during the period of Jan 1–Dec 31, 2014.1. “Movin’ On Up: How Moving Prompts Purchasing” a Zillow Mover Study, Aug 2012, http://www.zillow.com/blog/zillow-mover-study-movers-spend-thousands-on-cars-tvs-cellphones-etc-85997/.2. 2015 Movers Report, Epsilon 2015.

The top 5 destinations in the US in 2014, in

terms of monthly active people in each state:

CaliforniaNew York

TexasFlorida

New Jersey

In terms of monthly active people on Facebook, larger percentages of people moved to:

In terms of monthly active people on Facebook,

larger percentages of people moved out of:

New Jersey Washington

VirginiaGeorgia Illinois

Arizona Colorado

Missouri Massachusetts

New YorkFlorida

Pennsylvania

Minnesota Indiana

MichiganOhio

North CarolinaCalifornia

20 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

There’s a seasonality to moving, with most people moving in March and April. Unlike older adults, people ages 18–34 move consistently throughout the year.

CHECKING IN AND OUT A NEW CITY: When moving to a new city, people are more open to doing new things as they explore and learn about their new surroundings. Around the time they move, people ages 18+ check in on Facebook 16% more than they normally do. Men (+23%) and people aged 55+ (+31%) help drive the increase in check ins. That’s not the only difference in Facebook activity: around the time they move, people post 24% less video than normal and use the web less as well. Mobile and non-video activities (sharing links, photos, posts and notes) remain stable.

Across the board, people who are moving talk about settling into their new cities and neighborhoods around 4X more than they discuss other topics generally and similar topics during the same time the year before. Also top of mind: real estate agents, packing, moving day, a new address, installations, furniture and housewarmings [Fig. 14].

Fig. 15: Mentions for people ages 18+

2.8

1.21.0

1.21.0 0.9

1.6 1.6

2.3

1.1 1.1

2.2

1.3

2.0

3.8

1.5

4.2

1.1 1.2

2.01.7

1.2

Chan

ge o

f add

ress

Bubb

le w

rap

Cont

act

New

pho

ne

Dec

orat

ing

Fina

nce

Furn

iture

Hou

sew

arm

ing

Inst

alla

tions

Loan

Mor

tgag

e

Mov

ing

day

Nei

ghbo

rhoo

ds

New

add

ress

New

city

New

frie

nds

New

nei

ghbo

rhoo

d

Repa

ir

Ope

n ho

mes

Pack

ing

Real

est

ate

appr

aisa

l

Reno

vatio

n

Source: Facebook internal data for people who relocated to another state or country for at least 30 days during the period of Jan 1–Dec 31, 2014.

Fig. 14: Increase in mentions for people ages 18+

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 21

However, there are some differences by age and gender. Women ages 18–34 mention housewarming 1.9X more than the same time a year prior (men of the same age mention it only 0.9X more). Men ages 18–34 mention installations 2.7X more than the same time a year prior (women of the same age mention it 1.3X more). Men and women ages 35–54 also care about installations, with men mentioning it 4.1X more and women 2.4X more compared to the same time a year prior. Men 55+ mention renovation 2.1X more than the same time a year prior (women of the same age mention it 1.2X more).

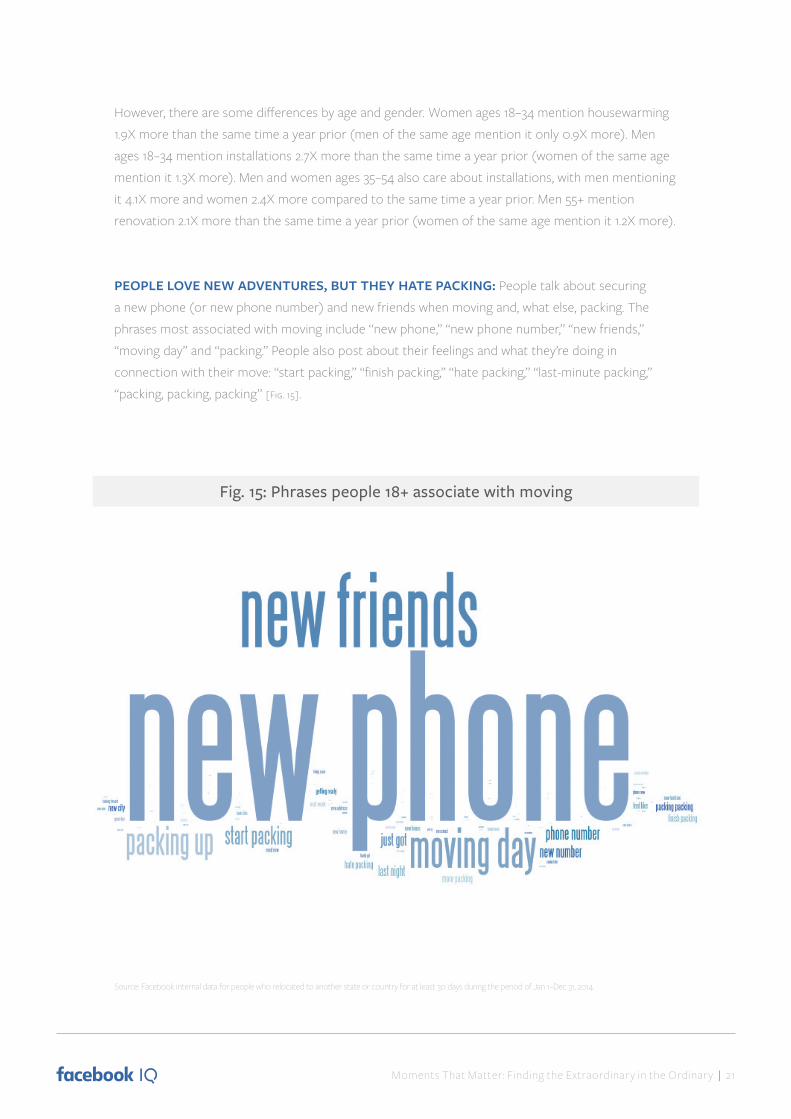

PEOPLE LOVE NEW ADVENTURES, BUT THEY HATE PACKING: People talk about securing a new phone (or new phone number) and new friends when moving and, what else, packing. The phrases most associated with moving include “new phone,” “new phone number,” “new friends,” “moving day” and “packing.” People also post about their feelings and what they’re doing in connection with their move: “start packing,” “finish packing,” “hate packing,” “last-minute packing,” “packing, packing, packing” [Fig. 15].

Fig. 15: Phrases people 18+ associate with moving

Source: Facebook internal data for people who relocated to another state or country for at least 30 days during the period of Jan 1–Dec 31, 2014.

22 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

Insights and Implications SPARK TRIAL: Moving indicates not only a new life stage but also a point of market entry. It’s a period of significant financial investment, with those who’ve moved buying new furniture and home goods, taking on installation and renovation projects, and entertaining friends and family in their new residence. Facebook is not only a place people share these life changes—it is also a place to update to a current address. In that way, Facebook serves as people’s change of address card. Brands can

use Facebook to complement their traditional media and direct-mail efforts to spark trial around

products, services and experiences for new residents.

EXPAND PEOPLE’S WORLDS VIA MOBILE: When people move, they tend to be open to trying new things and meeting new people, as Facebook check-in and chatter data indicate. The mobile phone—likely a new one procured upon moving—and Facebook allow those who’ve moved to readily discover new things and friend new neighbors. Brands can position themselves at the center of this

discovery and provide much-needed familiarity amid the unfamiliar by accelerating the settling-in

process and making a new home feel less foreign.

EMPATHIZE AND ENABLE TO EASE MOVING’S CHALLENGES: Although moving can be one of the most stressful and exciting events in a person’s life, the responsibilities and concerns that come with it vary by gender and generation. Brands can ease the process and position themselves as an ally

in this transition by addressing people’s moving experience in a personalized way. Brands can also add

levity or meaning to what can be an arduous process, poking fun at the universal hatred for packing,

for instance, or making moving a time to reflect on memories made or yet to come.

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 23

ONCE-A-YEAR MOMENTS

January 23, 2015

National Reading Day Stories with Staying Power When people in countries around the world list “10 books that have stayed with you,” friends are 4X more likely to list the same books than 2 random people. And the majority of those books are classic coming-of-age novels—books that many people first encounter as they are themselves growing up. Leverage the power of storytelling: The stories that stick with us tend to be timeless, inspiring tales of facing and triumphing over the challenges of finding ourselves. Identify and tap into the universal stories that already resonate with your audience. Help your audience triumph over their challenges and emerge the hero. Source: “Books that have stayed with us” by Facebook Data Science, Sep 2014. Based on 130,000 status updates

matching “10 books” or “ten books,” appearing in the last 2 weeks of Aug 2014.

JANUARY

Each year is full of extraordinary moments that brands and people can celebrate together. And mobile is allowing people and brands to share—and share in—the festivities to a greater extent than ever before. Holidays and events tend to inspire heightened excitement and heightened spending. And increasingly there’s a season for every reason: brands can always find a reason to celebrate by joining existing festivities or creating their own. Explore how some of the moments play out on Facebook and Instagram and how they can bring extraordinary opportunities to brands.

24 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

February 14, 2015

Valentine’s Day The Best Time to Engage 166,800 people across the US, Canada and the UK changed their status to engaged within 4 days of Valentine’s Day 2014. Engage with the engaged: The weeks following the holiday are the perfect time to reach out to newly engaged couples. Take advantage of the long run-up to connect with newly engaged couples and become a potential partner through the entire wedding journey and beyond. Source: Facebook internal data, US adults, Feb 2014 (accessed Aug 2014).

February 19, 2015

Lunar New Year Capturing the Celebration As people in Hong Kong, Indonesia, South Korea, Malaysia, Singapore, Taiwan and Vietnam traveled and gathered to celebrate the Lunar New Year, mobile photo uploads jumped 20% in 2014. Leverage mobile moments: People capture their holiday moments in photo (and even video) to let the Lunar New Year celebration last all year. Create mobile-friendly content and inspire people to share their celebration— with connections on Facebook and with creativity on Instagram. Source: Facebook internal data, Jan 31–Feb 2, 2014 (accessed Oct 2014).

FEBRUARY

FEBRUARY

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 25

March 2015

Spring Break Unplugged But Always Connected 73% of people ages 18–24 on Facebook in the US say they actively use Facebook while traveling. Guide Millennials on mobile: Wherever they may go, Millennials are only as far away as their mobile phone. Guide Millennials’ journeys by providing the travel inspiration and validation that people seek from their Facebook and Instagram feeds before, during and after their trips. Source: Poll of 845 respondents in the US, selected randomly on Facebook, ages 18–34, Apr 2015

April 5, 2015

Easter Chocolate Tastes Better Shared Socializing is the #1 activity people in Australia, Canada and the US say they will take part in on Easter. And in those countries, the social aspects of the holiday also drive the conversation on Facebook—more so than chocolate or church. Celebrate Easter connections: Easter is only as sweet as the people you share it with. Speak to people’s desire to share the experience of Easter with family and friends to develop creative that resonates widely and deeply. Sources: Poll of respondents in AU, CA and the US, selected randomly on Facebook, ages 18+, Mar 8–11, 2015. Facebook internal data, Apr 5–May 6, 2014 (accessed Mar 2015).

APRIL

MARCH

26 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

May 10, 2015

Mother’s Day Not Just for Moms 77% of US mothers are connected to their sons and daughters on Facebook. And in the US in May 2014, 84 million people joined the Mother’s Day conversation on Facebook. The network of Mother’s Day gift-givers is also larger than ever and includes husbands, parents, siblings, grandkids, friends and godchildren. Expand the occasion: Nearly everyone has somebody they’d like to celebrate on Mother’s Day. Grow your consumer base by targeting the full range of Mother’s Day gift-givers with tailored messaging and relevant offers. Source: Facebook internal data (accessed Feb 2015). “Mother’s Day on Facebook” by Facebook Newsroom, May 2014.

June 17–July 17, 2015

Ramadan The Month of Mobile As people around the world celebrate Ramadan on Facebook, most will connect on mobile rather than desktop: 1.6X more people across Algeria, Bahrain, Egypt, Iraq, Jordan, Kuwait, Lebanon, Morocco, Oman, Qatar, Saudi Arabia, Tunisia and the UAE; 3X more in Malaysia; and 4.3X more in Indonesia. Personalize for the mobile masses: While mobile is helping more people connect at Ramadan, people across countries use a wide range of mobile devices and have different levels of access to mobile data. Use tailored creative and bandwidth targeting to deliver a meaningful mobile message across a broad range of countries, devices and network speeds. Source: Facebook internal data for AE, AL, BH, EG, ID, IQ, JO, KW, LB, MA, MY, OM, QA, SA and TN, Apr–Jul 2014 (accessed on Apr 2015).

MAY

JUNE

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 27

Summer The Rise of Relaction People may think of summer as a season for relaxation, but summer can also be the ultimate call to action. In fact, 46% of people across 12 countries say their #1 summer goal is to get in shape (eat better/exercise more). As people unwind by taking advantage of the many activities that summer has to offer, expect to see the rise of “relaction”—relaxing through action. Make summer count: People will be reconciling their expectation of relaxation with their desire to take advantage of all that summer has to offer. Help people become their best summer selves—whether that means encouraging people to go out or helping them chill out. Source: Poll of 56,356 respondents in CA, DE, ES, FR, HK, IT, JP, KR, MX, TW, UK and US, selected randomly on Facebook, ages 18+, Apr 6–21, 2015.

Summer Mobile Is Our Constant Companion Across 21 countries last summer, 70% of people who connected to Facebook were on mobile. And people share more photos during summer than in any other season—22% more than in spring. Maximize your mobility: As people head out to enjoy their summer adventures, TVs and desktops stay at home, but mobile goes everywhere. Dial up your mobile strategy to reach people consistently—on the beach and beyond. Source: Facebook internal data for BE, CA, DE, DK, ES, FR, HK, IT, JP, KR, MX, NL, NO, PO, PT, SA, SW, TK, TW, UK and US, May–Sep 2014 (accessed Apr 2015).

JUNE-AUGUST

28 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

Summer Making Modern-Day Pen Pals In summer, people across 21 countries accept more friend requests on Facebook than in any other season: 20% more than in spring, 14% more than in winter and 6% more than in fall. Facilitate summer friendships: As people are out and about in summer, they’re also open to making new connections. Develop messaging and activations that inspire new connections and celebrate existing ones—and in doing so, establish ties with the people who matter in a way that lasts well beyond the season itself. Source: Facebook internal data, May–Sep 2014 (accessed Apr 2015).

September 26, 2015

National Family Health + Fitness Day Exercising Mindfulness People in the US talking on Facebook about working out generated a daily average of 22.3 million posts, comments, likes and shares over a month in the US—and “mindful” was one of the top 20 terms driving that conversation. Maximize the moment: Fitness is increasingly as much about moments along the journey as it is about the destination. Support people in achieving a more healthful lifestyle by inspiring them to see the beauty along the journey to their fitness destination—for example, through photos on Facebook and Instagram and hashtags like #fromwherewerun. Source: Facebook internal data, US only, Mar 4–Apr 4, 2015 (accessed Apr 2015).

SEPTEMBER

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 29

September 29, 2015

International Coffee Day The Power of Love On an average day, people around the world talking about coffee generate over 7.5 million interactions on Facebook, with #love as a top hashtag. Married couples overindex on interactions around coffee on Facebook, talking more about coffee than they do about other topics. Brew up the love: It’s more than a functional beverage for the masses—coffee brews up loving feelings that people just want to share on Facebook. Win over your target audience by tapping into this moment of loving indulgence—fueled by a beverage that can be savored alone or with others. Source: Facebook internal data, Sep 3–Oct 3, 2014 (accessed Apr 2015).

October 16, 2015

World Food Day Serving Up the Right Message Nearly half (47%) of the interactions around cooking and baking on Facebook take place on Fridays, Saturdays and Sundays around the world. The cooking and baking conversation “cools” midweek, on Tuesdays and Wednesdays. “Serve” the right messaging at the right time: There are 2 types of cooks in the kitchen: the weekday warrior and the weekend leisure chef. Match the right messaging in News Feed to audience behavior—whether it’s giving people delivery, pre-cooked or oven-friendly-meal solutions to get them over the midweek hump or enticing them with recipes for weekend culinary adventures. Source: Facebook internal data, Mar 2015 (accessed Apr 2015).

SEPTEMBER

OCTOBER

30 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

November 26, 2015

Thanksgiving Giving Thanks for Mobile Last Thanksgiving, over 171 million people participated in the worldwide conversation on Facebook, generating 1.2 billion interactions around Thanksgiving, holiday shopping, Black Friday and Cyber Monday. And 88% of people on Facebook during that time were on mobile. Reach people throughout the season: Mobile is a Thanksgiving holiday essential and an in-hand guide to a successful shopping weekend. Use mobile to reach people throughout the festivities with compelling content and relevant offers that evolve as the holiday’s lifecycle progresses. Source: Facebook internal data, Nov 26–Dec 1, 2014 (accessed Dec 2014).

DECEMBER 2015

Holiday Shopping The Journey of the Year In the UK, 68% of shoppers use their mobile in store. And in the US, among people who accessed their mobile phone in store while holiday shopping, 64% accessed their phone in the store aisle, 44% accessed it in the store parking lot and 28% accessed it in the checkout line. Fuel holiday shopping on mobile: Mobile is the ultimate shopping companion, guiding people towards informed decisions as they express their love through holiday shopping. Reach people throughout the season on mobile, the device on which people continuously discover deals and ideas throughout the store and all throughout their holiday journeys. Sources: “Multi-Channel Shopping” by Research Now (study of UK adults commissioned by Facebook), May 2014. “The Impact of Mobile and Facebook While Shopping” by Millward Brown Digital (survey of 500 US holiday shoppers commissioned by Facebook), Nov 28–Dec 25, 2013.

NOVEMBER

DECEMBER

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 31

EVERYDAY MOMENTS

The Cooking and Baking Moment Food and everything that goes with it—the cooking, the baking, the dining—is always best when shared with others. And now people are extending that experience online, inviting their friends into every facet of the process—from the prep to the plating to the piece de resistance.

Globally, 213 million people generated 1.1 billion interactions (posts, comments, likes and shares) about cooking and baking over a 30-day period. On an average day in the US, there are 18 million posts, comments, likes and shares about cooking and baking on Facebook. And 83% of cooking and baking interactions on Facebook happen on a mobile device in the US.

MOMENTS THAT MAKE A CHEF: Married people interact (post, comment, like and share) about cooking and baking more than single people. People ages 35 and older tended to overindex on posts, comments, likes and shares about cooking and baking more than other topics they discuss on Facebook.

By region, the states with the most interactions around cooking and baking in a 30-day period are:

Source: Facebook internal data, Mar 5–Apr 5, 2015.

Western region: On average, people in California generated 1.7 million interactions each day, 2.7X more than the other general topics discussed by

people in California on Facebook

Midwest region: On average, people in Ohio generated 700k interactions each day, 3X more

than the other general topics discussed by people in Ohio on Facebook

Eastern region: On average, people in Pennsylvania generated

670k interactions each day, 3.1X more than the other general topics discussed by people in Pennsylvania on Facebook

Southern region: On average, people in Virginia generated 430k interactions each day, 3X more than

the other general topics discussed by people in Virginia on Facebook

Fig. 16: Cooking and baking by region

32 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

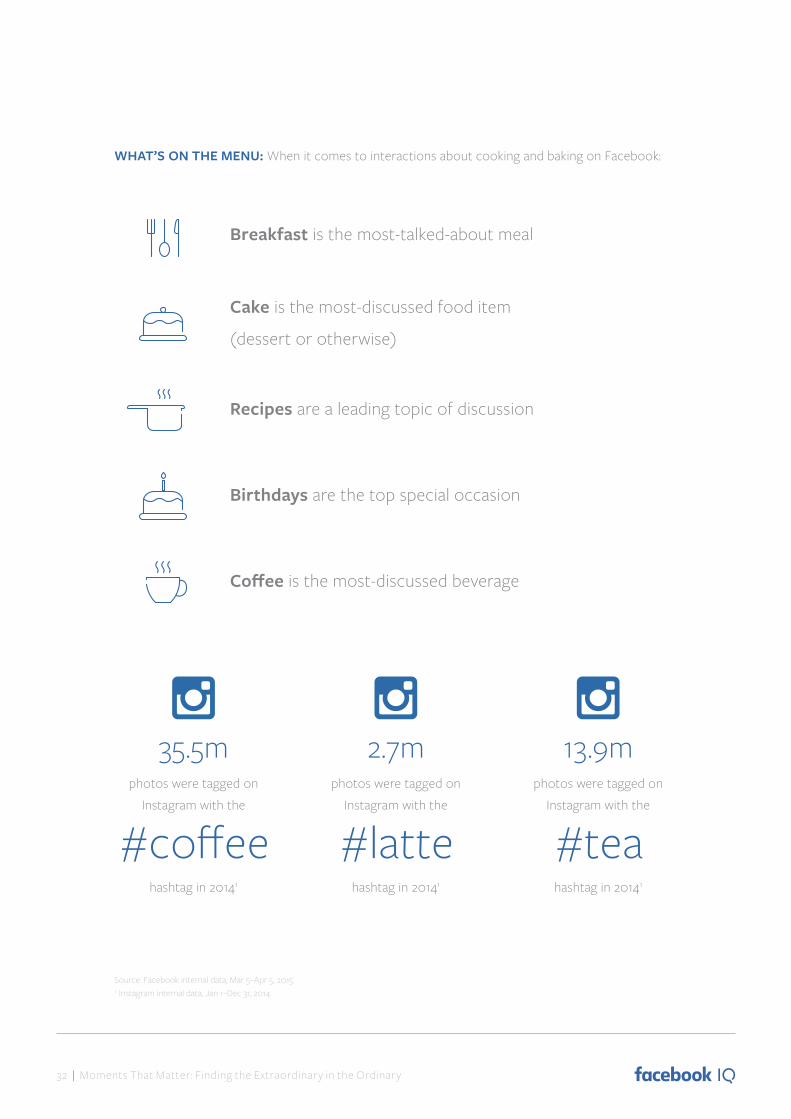

WHAT’S ON THE MENU: When it comes to interactions about cooking and baking on Facebook:

Breakfast is the most-talked-about meal

Cake is the most-discussed food item

(dessert or otherwise)

Recipes are a leading topic of discussion

Birthdays are the top special occasion

Coffee is the most-discussed beverage

35.5m 2.7m 13.9mphotos were tagged on

Instagram with the

#coffee hashtag in 20141

photos were tagged on Instagram with the

#latte hashtag in 20141

photos were tagged on Instagram with the

#teahashtag in 20141

Source: Facebook internal data, Mar 5–Apr 5, 2015.1. Instagram internal data, Jan 1–Dec 31, 2014.

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 33

Insights and ImplicationsMOBILIZE THE HOME COOK: With 83% of cooking and baking interactions happening on a mobile device, brands should create digestible content to appeal to this mobile-minded audience.

PAIR MESSAGES WITH THE RIGHT DAYS: People are cooks on the weekdays, gourmets on the weekends. Whether it’s pre-prepared meals and delivery options to get them over the mid-week

hump or recipes to inspire the weekend chef, brands can adjust marketing to address different

needs on different days.

ENGAGE PEOPLE AS THEY TRANSITION TO NEW LIFE STAGES: As people become more established in their personal and professional lives (transitioning from single to married, for instance), they interact more around cooking and baking topics on Facebook. Brands can tailor content and

messaging to reach people around these times.

DON’T FORGET BREAKFAST: Breakfast is not only the first meal of the day—it is also the most-discussed meal on Facebook. Brands can tap into this meme and/or establish use cases

that go beyond the morning ritual.

The Lost Phone Moment

Our mobile phones are often the one place where everything that matters to us most—names, numbers, meetings, messages, music, photos, apps, ideas and random notes—converge. Many of us consider our mobile phone to be our lifeline to the world. The loss happens to many people at some point in time, reaching across genders, age ranges and cohorts.

And it happens to so many people, so regularly, that on Facebook, the “lost phone” conversation is one that never gets dropped. In one month, in the US, “lost phone” conversation generated 51.2 million interactions (posts, comments, likes and shares). While the conversation tends to peak on Thursdays, it’s definitely happening every day of the week.

MOBILE IS MANDATORY: Even when people post about losing their phone, they usually do it from a mobile device. Over 75% of “lost phone” posts are generated on mobile—over 85% for Millennials ages 18–34. This is a powerful testament to the central role that mobile plays in our lives. Having

Source: Facebook internal data, Mar 5–Apr 5, 2015.

34 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

just lost their phone, many people likely feel more inclined to borrow someone else’s (even a stranger’s) phone, reach for their second phone, dig up an old phone or buy a new phone than to post about their ordeal from a desktop. Mobile has become so integral to life as we know it that when people lose their phone, many will want to replace it the next day—or the same day.

FACEBOOK IS THE ULTIMATE “LOST PHONE” SUPPORT GROUP: When people post about losing their phone, the posts are overwhelmingly negative (understandably)—but the comments posted in response are primarily positive. People are likely coming to Facebook to express their frustration, but the support they get from their friends on Facebook often transforms the conversation into a more positive one, perhaps reminding the newly #phoneless that they are not as alone as they may feel.

Fig. 19: Lost phone: posts vs. comments

Posts

18% Positive

78% Negative

4% Neutral

57% Positive

38% Negative

5% Neutral

“Lost phone”posts recieve

2x morecomments

than average

Comments

PEOPLE TURN TO FACEBOOK TO SHARE ALL FACETS OF THE JOURNEY: Facebook is a place where people turn to vent about their recent phone loss, to request their friends and family’s phone numbers and to share their joy at getting a new phone [Fig. 18].

Source: Facebook internal data, Mar 5–Apr 5, 2015.

Fig. 17: Lost phone: posts vs. comments

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 35

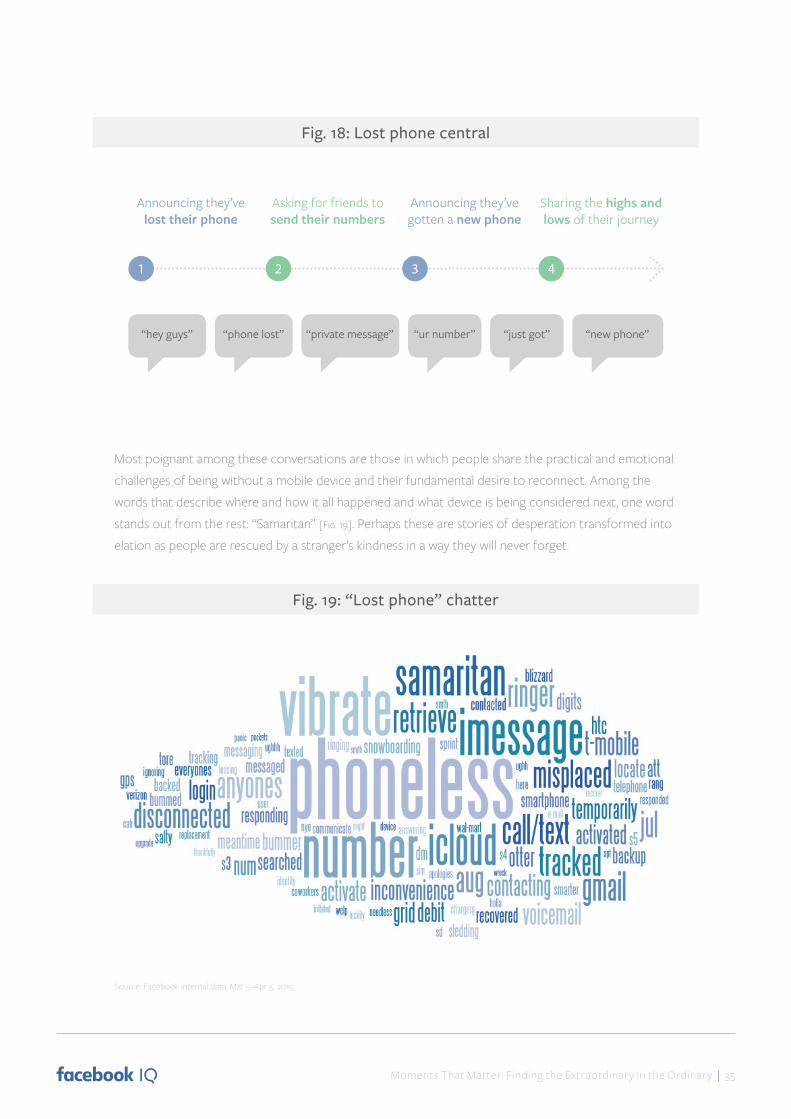

Fig. 20: Lost phone central

Announcing they’ve lost their phone

Asking for friends to send their numbers

Announcing they’ve gotten a new phone

Sharing the highs and lows of their journey

“hey guys” “phone lost” “private message” “ur number” “just got” “new phone”

1 2 3 4

Most poignant among these conversations are those in which people share the practical and emotional challenges of being without a mobile device and their fundamental desire to reconnect. Among the words that describe where and how it all happened and what device is being considered next, one word stands out from the rest: “Samaritan” [Fig. 19]. Perhaps these are stories of desperation transformed into elation as people are rescued by a stranger’s kindness in a way they will never forget.

Source: Facebook internal data, Mar 5–Apr 5, 2015.

Fig. 18: Lost phone central

Fig. 19: “Lost phone” chatter

36 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

Insights and ImplicationsCONNECT WITH THE #PHONELESS ON “LOST PHONE CENTRAL”: Facebook is a place where the “lost phone” conversation is always on and the place that many people visit continuously throughout their “lost phone” journey—from requesting friends’ numbers to asking for advice on which new phone or carrier to switch to. But people move quickly when they lose their phone (as the high number of people posting about lost phones from another mobile device demonstrates). The opportunity for brands is huge, but the window of opportunity is narrow. Brands may only

have a matter of hours to intervene. In order to seize the moment, brands will need to maintain an

“always on” presence so that they are able to play meaningful roles in guiding people’s “lost phone”

journeys—and so that brands are able to build up the goodwill and advocacy that will make them

top of mind when someone asks their network of friends which phones or carriers to consider next.

BE A MODERN-DAY MOBILE SAMARITAN: Nothing’s worse than losing your phone. People turn to their friends and family members on Facebook when it happens. This creates an opportunity for

brands of all kinds to be a modern-day mobile Good Samaritan. Brands can connect with practically

every audience in an extraordinarily meaningful way through the “lost phone” experience—the key

is finding one that is authentic to your brand, whether it’s showing empathy, making light of the

situation or offering solutions to the phone-deprived.

The “I Need a New Phone” MomentThe path to buying a new phone is increasingly paved with hundreds of moments of opportunity. With more people buying new phones out of desire (rather than necessity) and regularly engaging with tech/telco news and content (often months prior to purchase), a growing number of people are essentially always “in market.”

In this journey of continuous consideration, any moment could become the moment of purchase. It just takes the right offer presented at the right time (or a lost phone) to ignite it. To win the sale when it matters, brands must be “always on”—like the people they are trying to connect with. Opportunities for OEMs and carriers to engage the people who matter most in endemic environments are limited, as people will probably visit network, retailer and manufacturer sites only a handful of times as they research. But what about all the moments in between, before and after those visits?

Source: “Path to Purchase for Tech and Telcos” by GfK (study commissioned by Facebook), Oct 2014. Nationally representative group of adult mobile phone/smartphone owners in DE, FR, PL, TK and UK.

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 37

Facebook is woven throughout the journey: many people return to Facebook as they switch between, and even in the middle of, digital activities. Toggling has made Facebook a consistent thread throughout the entire path to purchase. A typical shopper is likely to visit Facebook hundreds of times while approaching purchase. As illustration, during a 24-day consideration period, someone in the market for a new phone visited Facebook 201X, compared to network visits (3X), retailer visits (tech & telco related) (2X), OEM visits (2X) and search visits (23X) [Fig. 20].

Fig. 21: One person’s path to purchase for a new phone

Facebook Is Present Throughout the Journey

The path below illustrates how people in market for a new mobile phonemight visit Facebook along their journey to purchase

201 Facebook visits in total over 24 days

Day 11:15pm

Visits Facebook

2:20pmVisits mobile

carrier website

2:42pmVisits search

engine

2:42pmVisits retailer

website

Day 117:26am - 10amVisits Facebook multiple times

4:52pm - 5:05pmChecks Facebook

9:53pmVisits search

engine

9:53pmVisits

manufaturer website

Day 139:29am

Visits manufaturer

website

Day 199:11pm

Checks Facebook

9:11pmDownloads carrier app

Day 24

Purchases new smartphone

6:41pmChecks

Facebookon new

smartphone

Source: “Path to Purchase for Tech and Telcos” by GfK, Oct 2014 (study commissioned by Facebook). This graphic represents an excerpt from the path of a UK consumer. The study’s respondents must either have bought a phone in the last 2 years, or be open to buying a phone in the next year; own a PC and a smartphone; and be willing to have behavior tracked on qualifying devices.

1 24

It’s important to consider people’s mindsets. People typically visit telco and manufacturers’ sites to accomplish tasks that might be associated with a more “functional” state of mind—for example, conducting device research, checking balances or paying bills. But people go to Facebook to connect and engage in discovery. Many show up with a mind that is open to relevant and interesting news from friends and brands alike.

Source: “Path to Purchase for Tech and Telcos” by GfK (study commissioned by Facebook), Oct 2014. Nationally representative group of adult mobile phone/smartphone owners in DE, FR, PL, TK and UK.

Fig. 20: One person’s path to purchase for a new phone

38 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

Insights and ImplicationsBE PRESENT THROUGHOUT THE JOURNEY: The path to purchase is an ongoing cycle. To ensure

an “always on” presence, brands can seek out the places their audiences are really spending time. By

integrating their message throughout the consideration cycle, brands will be present to accelerate

purchase among an audience that is ready to buy when the moment feels right.

ADAPT TO MOBILE: Why should brands try to create new behaviors when they can leverage existing ones? Mobile manufacturers and operators have an opportunity to leverage the very channel

they created, using mobile to stay close to the people who matter to them. The consistent presence

of Facebook throughout the path to purchase may offer brands additional opportunities to reach

audiences—both broad and targeted—in an engaging environment.

CONNECT TO PEOPLE WITH RELEVANT CREATIVE: Expanding onto new platforms may also mean expanding the way brands approach creative opportunities. Brands may be able to differentiate

themselves from the pack by shifting the focus of messaging from product features to the lifestyle

values of the people they want to connect with. By doing this in a way that is personalized (e.g., with

targeted messaging) and visually appealing (e.g., with photos and video), brands can give people an

ongoing reason to stay committed.

The Moment of Entertainment DiscoveryWhen it comes to entertainment, there are dozens of moments that matter every day. People are discovering entertainment all day, every day. But the nature of how and where people—especially Millennials—are discovering music, movies and TV shows is changing. Where people discover entertainment content is no longer limited to the screens where they consume content— it’s expanding to the screens where they spend their time.

While this development is expected for music, which is heavily consumed on digital devices, Millennials are discovering TV shows and movies more on digital than on the TV screen. This leads to a very important point. Consumption does not equal discovery.

Source: “Entertainment Discovery Study” by Millward Brown Digital (study of US adults commissioned by Facebook), Jan 2015. For the purposes of this research, “entertainment” includes movies, TV shows and music.

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 39

In fact, many people discover entertainment content only digitally [Fig. 22]. The younger the audience, the truer this is.

Fig. 22: Online vs. offl ine discovery

60%

61%

64%

Discover online

TV shows

Movies

Music

Discover offl ine

56% (TV)

50% (TV)

48% (Radio)30% (TV)

18–34

Fig. 23: Online vs. offl ine discovery by age demo

18–34 35–68

31%Online only

23%Online onlyTV / Radio only

21%TV / Radio only

35%

Both TV and online Both TV and online

31% 25%Offl ine total

52% Offl ine total

60% Online total

62% Online total

48%

WHY DIGITAL? People want more than TV and radio can provide. 73% say that the reason for going online to discover is because it’s accessible 24/7, 58% say it gives them more access to resources and 58% say it allows them to get the most up-to-date information. When discovering entertainment information online, 56% say video is the most influential type of content.

PEOPLE GO ON FACEBOOK TO DISCOVER NEW CONTENT: As discovery is moving to digital, people are turning to Facebook to learn about content relevant to their interests. Of those who discover entertainment content on social and video sites, 63% discover music, 66% discover TV shows and 67% discover movies on Facebook. Facebook is also considered a leader in discovery by a factor of 2:1 when compared to other online sources of content [Fig. 23].

Source: “Entertainment Discovery Study” by Millward Brown Digital (study of US adults commissioned by Facebook), Jan 2015. For the purposes of this research, “entertainment” includes movies, TV shows and music.

Fig. 21: Online vs. offline discovery

Fig. 22: Online vs. offline discovery by age demo

40 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

Fig. 24: Facebook as a place for discovery

Facebook Facebook

48% 45%

48%Other online sources Other online sources

Other online sources

“Allows me to connect with information I wouldn’t be

aware of”

“Where information is

relevant to my interests”

“Where I expect to fi nd most new

information”20%

7%

6%

21%

9%

7%

17%

7%

3%

Insights and ImplicationsBE AT THE CENTER OF DISCOVERY: Digital sources of discovery have become as important as (and for some forms of entertainment content more important than) other sources of discovery. For marketers, that means it’s no longer an “either/or” world when it comes to discovery (i.e., either TV or online), it’s a “both/and” world (i.e., both TV and online). And online will increasingly mean mobile, with more entertainment content being consumed on mobile devices. Brands can personalize messaging

across platforms to resonate with different audiences and gain attention at the moment of discovery.

DRIVE VALUE WITH VIDEO: Video is a powerful tool in engaging people online in the discovery of new entertainment content. And it’s come to the mobile phone in earnest, with over 4 billion video views1 a day happening on Facebook, and 75% of those happening on a mobile device.2

Source: “Entertainment Discovery Study” by Millward Brown Digital (study of US adults commissioned by Facebook), Jan 2015.1. Facebook internal data, Mar 2015.2. Facebook internal data, Feb 2015.

Fig. 23: Facebook as a place for discovery

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 41

Entertainment brands should leverage their most compelling asset, video, to capture people’s

attention and convince them to watch a new TV show, listen to a new artist or see a film they

had not previously known about.

EXTEND REACH: As people’s media consumption habits shift, brands have an opportunity to amplify messages across multiple platforms. Brands can use digital to extend the reach offered by

TV and radio—delivering an incremental audience that can’t be found through traditional channels

and driving deeper engagement. This strategy is especially useful in reaching Millennials, some

of whom discover entertainment content online only.

The Multiscreening MomentThe living room has evolved. While multiscreening isn’t new, it is more ubiquitous than ever. Half of US adults use a mobile device (34% a smartphone, 17% a tablet) while watching TV. And 73% are accessing their devices constantly or very often during this time. People are driven to multiscreen while watching TV shows and commercials for a number of reasons. The top reasons: to be productive and to continue to be entertained or to communicate with family and friends.

The Watercooler MomentThe moments people spend watching TV and the shows that people talk about reveal unique insights into people’s passions. We looked at a month’s-worth of conversation around TV shows (from Mar 9–Apr 5) to see how many people were talking, what they were talking about and how [Fig. 24].

Source: “Primetime Live TV and Facebook Usage” by Millward Brown Digital and Firefly Millward Brown, Jan–Feb 2014 (study of US adults commissioned by Facebook).1. Poll of 2,995 respondents in the US, ages 18+, Mar 1-15, 2015.

70% of Millennials use Facebook

while watching a movie or TV1

42 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

Fig.25: TV talk

Facebook hashtags with most engagements

per post from Mar 9–Apr 5, 2015:

#ncisla#ncis#h50

#bluebloods#bigbangtheory

Facebook hashtags with most interactions

from Mar 9–Apr 5, 2015:

#dwts (“Dancing with the Stars”)

#scandal#greysanatomy

#thewalkingdead#rhoa (“Real Housewives of Atlanta”)

Men and women both start the conversation—but women are more likely to continue it

51 million posts, comments,

likes and shares every day

56%

43%

Women

Men

67%

33%

Posts Interactions

80% of the conversation around TV shows happens on mobile

People talking about TV shows inthe US generate, on

average, over

Source: Facebook internal data, Mar 9–Apr 5 2015.

Fig. 24: TV talk

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 43

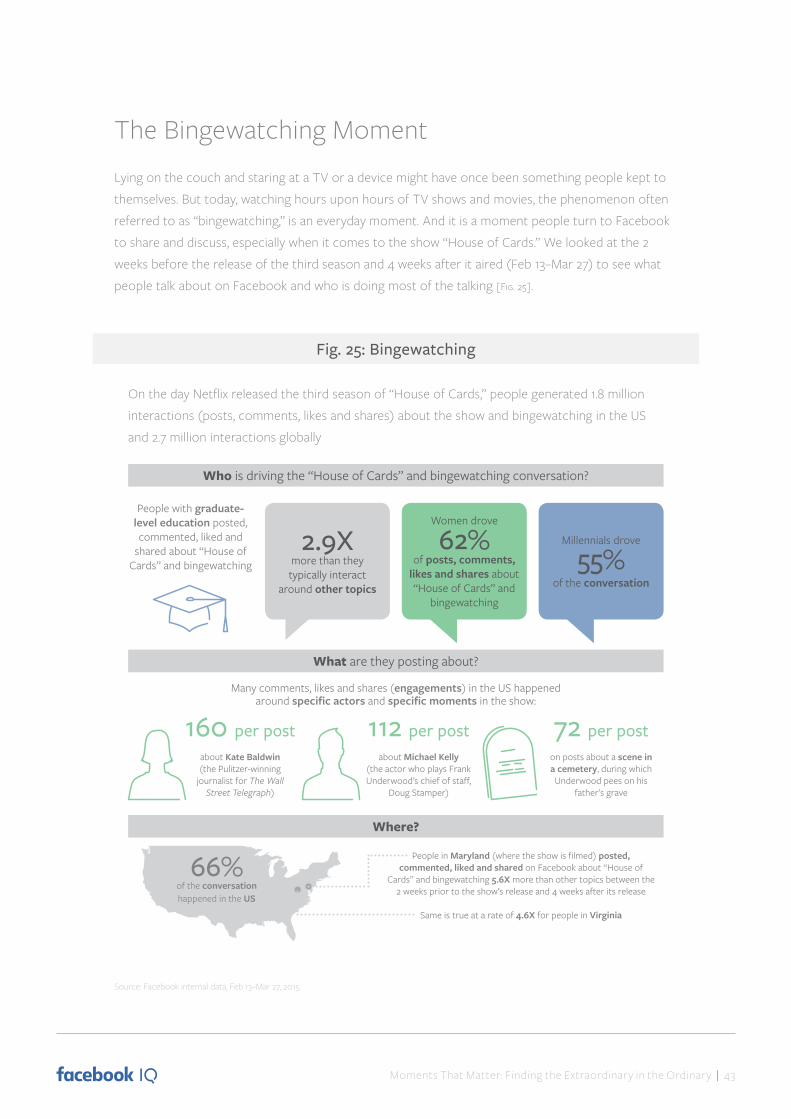

The Bingewatching MomentLying on the couch and staring at a TV or a device might have once been something people kept to themselves. But today, watching hours upon hours of TV shows and movies, the phenomenon often referred to as “bingewatching,” is an everyday moment. And it is a moment people turn to Facebook to share and discuss, especially when it comes to the show “House of Cards.” We looked at the 2 weeks before the release of the third season and 4 weeks after it aired (Feb 13–Mar 27) to see what people talk about on Facebook and who is doing most of the talking [Fig. 25].

Fig.26: Bingewatching

Who is driving the “House of Cards” and bingewatching conversation?

What are they posting about?

Many comments, likes and shares (engagements) in the US happenedaround specifi c actors and specifi c moments in the show:

160 per post

about Kate Baldwin (the Pulitzer-winning

journalist for The Wall Street Telegraph)

112 per post about Michael Kelly

(the actor who plays Frank Underwood’s chief of staff ,

Doug Stamper)

72 per post on posts about a scene in a cemetery, during which Underwood pees on his

father’s grave

Where?

66%of the conversation happened in the US

People in Maryland (where the show is fi lmed) posted, commented, liked and shared on Facebook about “House of

Cards” and bingewatching 5.6X more than other topics between the 2 weeks prior to the show’s release and 4 weeks after its release

Same is true at a rate of 4.6X for people in Virginia

When?

56%of posts about “House of Cards” and bingewatching

happened on Fridays, Saturdays and Sundays

People are most likely to post about “House of Cards” and bingewatching on Fridays

(25%)and least likely on Wednesdays

(9%)

How?

of posts, comments, likes and shares happened on mobile

78%

People with graduate-level education posted, commented, liked and

shared about “House of Cards” and bingewatching

2.9Xmore than they typically interact

around other topics

Women drove

62%of posts, comments,

likes and shares about “House of Cards” and

bingewatching

Millennials drove

55%of the conversation

Source: Facebook internal data, Feb 13–Mar 27, 2015.

Fig. 25: Bingewatching

On the day Netflix released the third season of “House of Cards,” people generated 1.8 million interactions (posts, comments, likes and shares) about the show and bingewatching in the US and 2.7 million interactions globally

44 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

Fig.26: Bingewatching

Who is driving the “House of Cards” and bingewatching conversation?

What are they posting about?

Many comments, likes and shares (engagements) in the US happenedaround specifi c actors and specifi c moments in the show:

160 per post

about Kate Baldwin (the Pulitzer-winning

journalist for The Wall Street Telegraph)

112 per post about Michael Kelly

(the actor who plays Frank Underwood’s chief of staff ,

Doug Stamper)

72 per post on posts about a scene in a cemetery, during which Underwood pees on his

father’s grave

Where?

66%of the conversation happened in the US

People in Maryland (where the show is fi lmed) posted, commented, liked and shared on Facebook about “House of

Cards” and bingewatching 5.6X more than other topics between the 2 weeks prior to the show’s release and 4 weeks after its release

Same is true at a rate of 4.6X for people in Virginia

When?

56%of posts about “House of Cards” and bingewatching

happened on Fridays, Saturdays and Sundays

People are most likely to post about “House of Cards” and bingewatching on Fridays

(25%)and least likely on Wednesdays

(9%)

How?

of posts, comments, likes and shares happened on mobile

78%

People with graduate-level education posted, commented, liked and

shared about “House of Cards” and bingewatching

2.9Xmore than they typically interact

around other topics

Women drove

62%of posts, comments,

likes and shares about “House of Cards” and

bingewatching

Millennials drove

55%of the conversation

Insight and ImplicationRECOGNIZE APPOINTMENT MULTISCREENING: Given that people interact during and after big shows and finales, and since multiscreening is increasingly commonplace, brands can use Facebook to

extend the reach of their TV investment inside and outside of the living room. Brands that provide quality

content and integrate that content across screens that will deliver the most impactful, immersive message.

Source: Facebook internal data Feb 13–Mar 27, 2015.

Fig. 25: Bingewatching cont’d

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 45

The Shopping MomentMobile has become as irresistible as a good deal. In a 30-day period, we learned that when people go on Facebook to talk about shopping, they mostly do so on mobile and discounts and style are top of mind.

Fig.27: Shopping

76%

67%

58%

48%43%

Percentage of posts about shopping on mobile by age group

% o

f pos

ts a

bout

shop

ping

on

mob

ile

18–34 35–44 45–55 55–64 64+Age group

80%

70%

60%

50%

40%

30%

20%

10%

0%

Women in the US generate 79%of posts, comments, likes and

shares about shopping

College graduates generate over half (57%) of posts, comments, likes and

shares about shopping

Married people interact aboutshopping topics 1.5X more than

other topics on Facebook

The majority of posts are on mobile

People turn to mobile for at least 3 out of every 5 posts

about shopping in the US (68%)

Interactions peak on Saturday: People talk about shopping the least on Mondays (13%) and the most on Saturdays (17%)

Ship, Ship, Hooray! Posts about

“#freeshipping”receive the most comments, likes and shares in the US

Top shopping hashtags on Facebook:

#shopping#fashion

#deals#style#sale

#onlineshopping

Most positive sentimentin the US is around:

#socialshopping#deals

#onlineshopping#clearance#discounts

Shopping hashtags on Instagram:

#fashion #ootd

#shopping#fashionista#blackfriday

Source: Facebook internal data, Mar 24–Apr 24, 2015 (accessed May 2015).

Mon Tue Wed Thurs

Fri Sat Sun

79% 57%1.5X

People in the US interact with stories about shoppingtopics 2.4X more than other topics on Facebook

Source: Facebook internal data, Mar 24–Apr 24, 2015.

Fig. 26: Shopping

46 | Moments That Matter: Finding the Extraordinar y in the Ordinar y

Fig.27: Shopping

76%

67%

58%

48%43%

Percentage of posts about shopping on mobile by age group

% o

f pos

ts a

bout

shop

ping

on

mob

ile

18–34 35–44 45–55 55–64 64+Age group

80%

70%

60%

50%

40%

30%

20%

10%

0%

Women in the US generate 79%of posts, comments, likes and

shares about shopping

College graduates generate over half (57%) of posts, comments, likes and

shares about shopping

Married people interact aboutshopping topics 1.5X more than

other topics on Facebook

The majority of posts are on mobile

People turn to mobile for at least 3 out of every 5 posts

about shopping in the US (68%)

Interactions peak on Saturday: People talk about shopping the least on Mondays (13%) and the most on Saturdays (17%)

Ship, Ship, Hooray! Posts about

“#freeshipping”receive the most comments, likes and shares in the US

Top shopping hashtags on Facebook:

#shopping#fashion

#deals#style#sale

#onlineshopping

Most positive sentimentin the US is around:

#socialshopping#deals

#onlineshopping#clearance#discounts

Shopping hashtags on Instagram:

#fashion #ootd

#shopping#fashionista#blackfriday

Source: Facebook internal data, Mar 24–Apr 24, 2015 (accessed May 2015).

Mon Tue Wed Thurs

Fri Sat Sun

79% 57%1.5X

People in the US interact with stories about shoppingtopics 2.4X more than other topics on Facebook

Source: Facebook internal data, Mar 24–Apr 24, 2015.

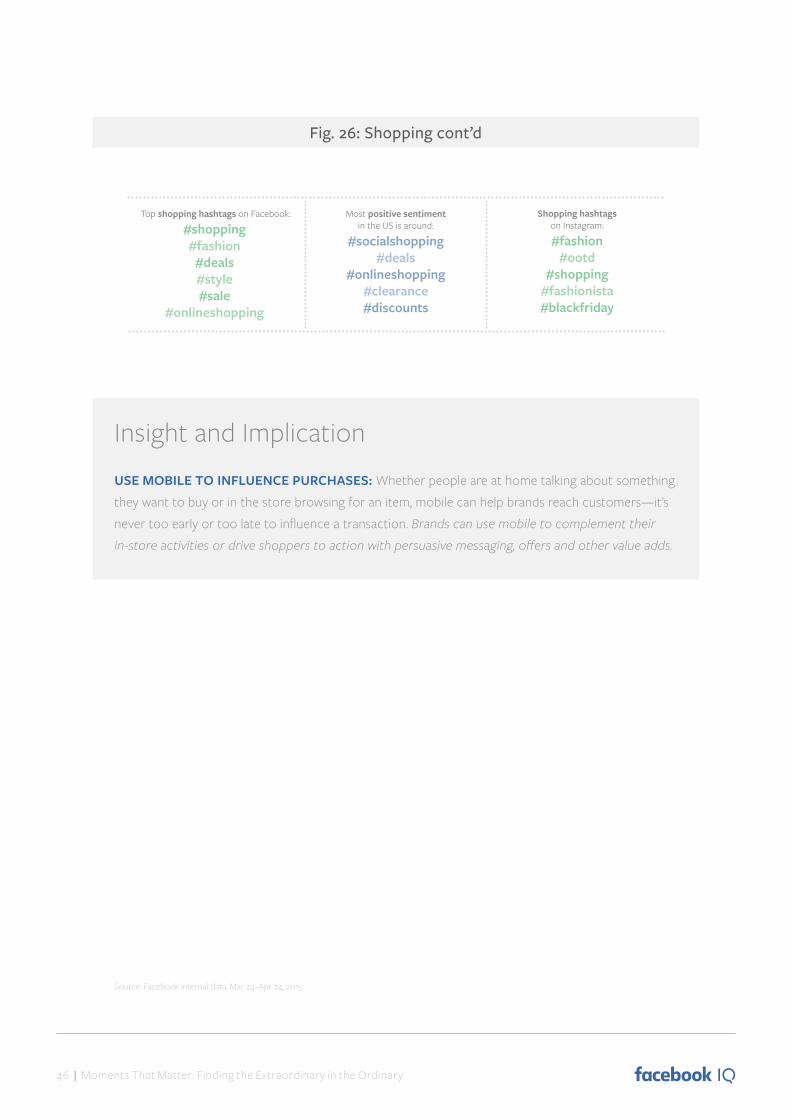

Fig. 26: Shopping cont’d

Insight and ImplicationUSE MOBILE TO INFLUENCE PURCHASES: Whether people are at home talking about something they want to buy or in the store browsing for an item, mobile can help brands reach customers—it’s never too early or too late to influence a transaction. Brands can use mobile to complement their

in-store activities or drive shoppers to action with persuasive messaging, offers and other value adds.

Moments That Matter: Finding the Extraordinar y in the Ordinar y | 47

MULTIPLE-TIMES-A-DAY MOMENTS

Source: Facebook internal data, Jan–Mar 2015.1 Facebook internal data, May 2015.2. Facebook internal data, Mar 2015. 3. Facebook internal data, Q4 2014.

Fig.x: xxxxxxx

On a typical day...

friend requests are sent out on Facebook1

moments (stories viewed on Facebook and Instagram) happen on average1

photos are uploaded daily on Facebook on average3

~280 million

~350 million

~4 billion ~70 millionvideo views happen

on Facebook2photos and videos are posted on Instagram1

~150 billion

A REFLECTION OF A PERSON’S WHOLE LIFE: News Feed is more than just puppies and babies. It’s a window into people’s wider worlds, the place where they are discovering professionally created content that enriches their lives and fills their everyday moments. News Feed reflects a person’s whole life, not just one facet, and encompasses all of that person’s interests.

Insight and ImplicationCONSIDER THE BIGGER PICTURE: Every person’s experience of Facebook is different, but every person’s News Feed is specifically designed to provide them with the most interesting content possible, to feed their lives and fill their moments. Brands can not only learn from what people are