Page 1 of 10 F No. AERA/20010/MYTP/BIAL/2011-12 Airports Economic Regulatory Authority of India Minutes of the Stakeholder Consultation Meeting held on 22.07.2013 (Consultation Paper No. 14/2013-14) A Stakeholder Consultation meeting was convened by the Authority on 22.07.2013 at 1500 hrs. in the Conference Room, 1 st Floor, AERA Building, Administrative Complex, Safdarjung Airport, New Delhi to elicit the views of the stakeholders on the Consultation Paper No. 14/2013-14 (i.e., the Consultation Paper) issued by the Authority setting out its tentative position in respect of the determination of tariff for aeronautical tariffs services in respect of Bengaluru International Airport (BIA), Bengaluru for the 1 st Control Period (from 01.04.2011 to 31.03.2016). The list of the participants is enclosed at Annexure – I. 2.1 Chairperson, AERA welcomed the participants and requested Shri Bhaskar, Sr. Director – Finance & Support Services, Bengaluru International Airport (BIAL) to present his proposal. Shri Bhaskar, thanked the Authority for the efforts taken in bringing out a comprehensive Consultation Paper on the subject. 2.2 Shri Bhaskar thanked the Authority for the opportunity to present its views in relation to the Consultation Paper and stated that BIAL was making this presentation to put forth its views on the proposals in the consultation paper and their implication on BIAL’s finances. Shri Bhaskar indicated that BIAL will submit their detailed responses to the consultation paper. 2.3 The presentation made by Shri Bhaskar is at Annexure – II wherein, inter-alia, the following was highlighted – 2.3.1 Bangalore being the capital of Karnataka and India’s first largest metropolitan city, is also known as a silicon valley of Asia. It is home to many successful brand in the IT-ITES, BPO & KPO services world-wide and is also India’s aviation, with the presence of institution such as HAL, ISRO, DRDO and NAL. 2.3.2 The annual traffic in the past was 11.5 million passengers which has reached 17 million passengers annually as on date. BIAL envisages traffic growth upto 35 million passengers and above in the future. 2.3.3 Terminal 2 development has features such as: Airside flexibility + Efficiency Integrated with Terminal 1 Compact + Cost Efficient Terminal Design Swing Capability and Terminal Flexibility Reduced Walking Distances Flexibility for Future Growth

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Page 1 of 10

F No. AERA/20010/MYTP/BIAL/2011-12 Airports Economic Regulatory Authority of India

Minutes of the Stakeholder Consultation Meeting held on 22.07.2013

(Consultation Paper No. 14/2013-14)

A Stakeholder Consultation meeting was convened by the Authority on 22.07.2013 at 1500 hrs. in the Conference Room, 1st Floor, AERA Building, Administrative Complex, Safdarjung Airport, New Delhi to elicit the views of the stakeholders on the Consultation Paper No. 14/2013-14 (i.e., the Consultation Paper) issued by the Authority setting out its tentative position in respect of the determination of tariff for aeronautical tariffs services in respect of Bengaluru International Airport (BIA), Bengaluru for the 1st Control Period (from 01.04.2011 to 31.03.2016). The list of the participants is enclosed at Annexure – I. 2.1 Chairperson, AERA welcomed the participants and requested Shri Bhaskar, Sr. Director – Finance & Support Services, Bengaluru International Airport (BIAL) to present his proposal. Shri Bhaskar, thanked the Authority for the efforts taken in bringing out a comprehensive Consultation Paper on the subject. 2.2 Shri Bhaskar thanked the Authority for the opportunity to present its views in relation to the Consultation Paper and stated that BIAL was making this presentation to put forth its views on the proposals in the consultation paper and their implication on BIAL’s finances. Shri Bhaskar indicated that BIAL will submit their detailed responses to the consultation paper. 2.3 The presentation made by Shri Bhaskar is at Annexure – II wherein, inter-alia, the following was highlighted –

2.3.1 Bangalore being the capital of Karnataka and India’s first largest metropolitan

city, is also known as a silicon valley of Asia. It is home to many successful brand in the IT-ITES, BPO & KPO services world-wide and is also India’s aviation, with the presence of institution such as HAL, ISRO, DRDO and NAL.

2.3.2 The annual traffic in the past was 11.5 million passengers which has reached 17 million passengers annually as on date. BIAL envisages traffic growth upto 35 million passengers and above in the future.

2.3.3 Terminal 2 development has features such as:

Airside flexibility + Efficiency

Integrated with Terminal 1

Compact + Cost Efficient Terminal Design

Swing Capability and Terminal Flexibility

Reduced Walking Distances

Flexibility for Future Growth

Page 2 of 10

Passenger Experiences + Garden Integration: a 21st Century Terminal in a Garden and

Innovative and Iconic Design

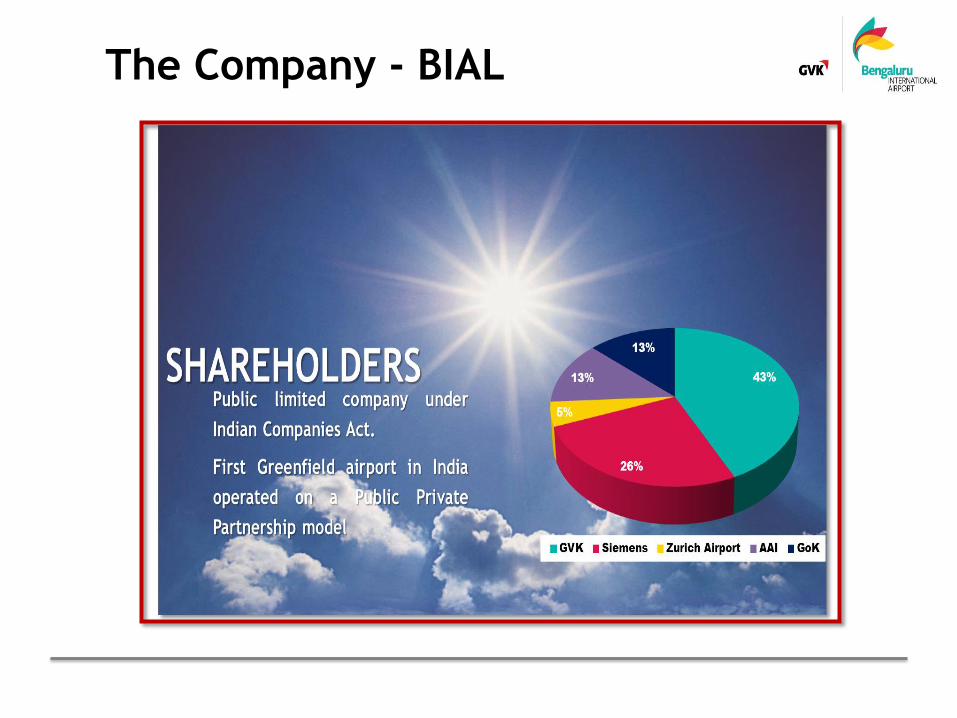

2.3.4 BIAL is a public limited company under Indian Company Act and First Green Field Airport operated on a Public Private Partnership model.

2.3.5 There are 33 airlines operating to Bengaluru Airport, amongst which 6 are domestic passenger airlines, 19 are international airlines, 1 domestic cargo airline and 7 international cargo airlines. The domestic traffic constitute 80% while international traffic contributes to 20% of the total traffic.

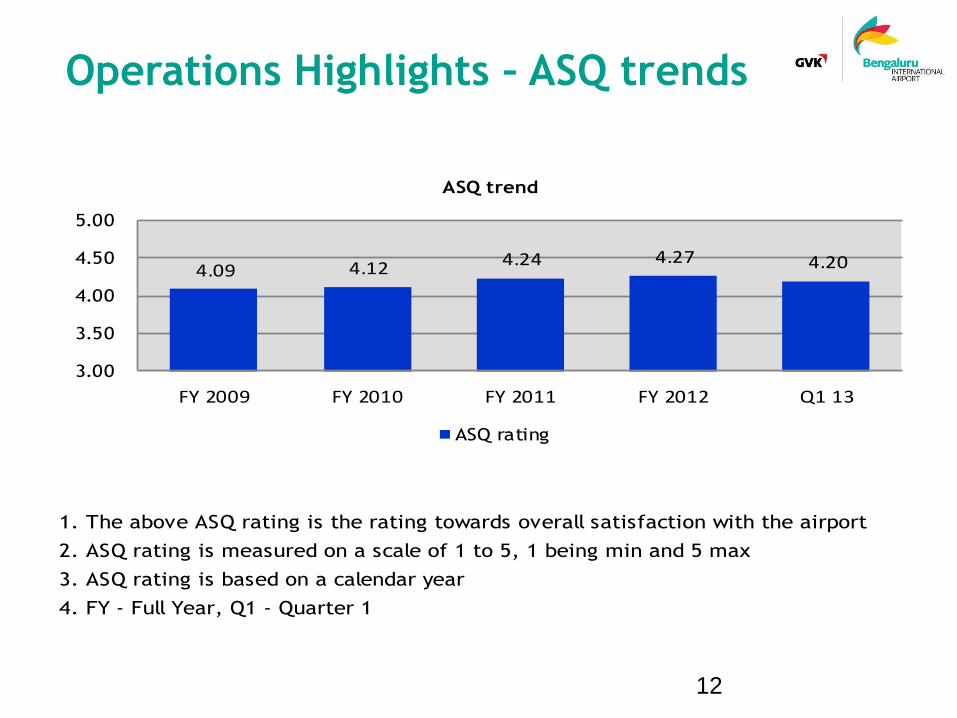

2.3.6 The ASQ trend has been in the range of 4.09 to 4.20 from FY 2009 to first

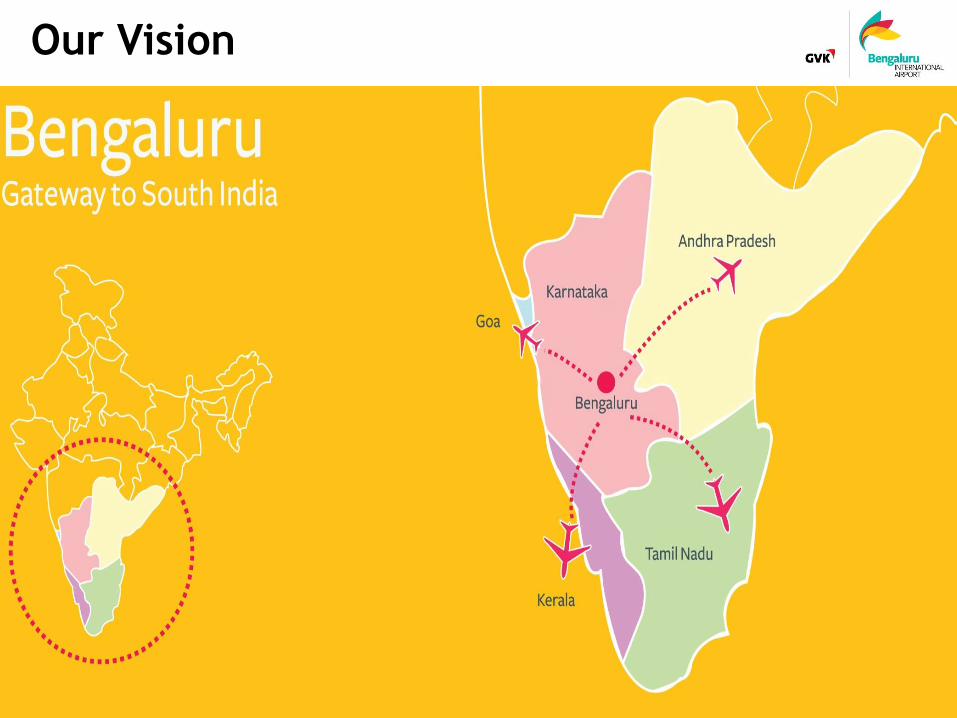

quarter of 2013. 2.3.7 BIAL has a view to make Bengaluru Airport the Gateway to South India since it is

well connected with other South Indian cities in terms of Trade and Culture.

2.4 The other issues highlighted by Shri Bhaskar regarding the airport project were as below: 2.4.1 BIAL project being the first PPP Project, involved conceptualization and

crystallization of many concepts during execution of Concession and other project agreements – many terms as per these agreements were defined and some were implied.

2.4.2 The Initial UDF approvals by MoCA on adhoc basis were approved under dual till in respect of international UDF and hybrid/Shared till in respect of domestic UDF.

2.4.3 Regarding the proposals contained in the consultation paper, Shri Bhaskar enumerated the response of BIAL which, inter-alia, include low profits envisaged in Consultation Paper, Exposure to BIAL in terms of failure to comply with covenants of Loan agreements, inadequate funds affecting future expansion. He stated that even on regular operations of the airport, the average return to shareholder for 1st control period is 9.33% in spite of cost of equity assured by AERA @ 16%. He stated that this does not compensate or take into account the risks taken by the promoters in developing a Greenfield airport. He stated that Financial close, one of the conditions precedent in the Concession Agreement, was achieved on an express understanding that BIAL would have an equity internal rate of return of 21.66%. Shri Bhaskar , therefore, submitted that the proposed return on equity is not only contrary to the fulcrum of the arrangements arrived at between BIAL and the State of Karnataka, but also a clear disincentive that affects future expansion. Further, Rs. 649 Crores of additional equity infusion requirement will also have effect on future expansion.

Page 3 of 10

2.4.4 Shri Bhaskar stated that in view of the traffic growth projections, future expansion is viz.2ndTerminal & 2ndRunway etc. are required for involving capacity creation.

2.4.5 Shri Bhaskar stated that a growing airport has requirement of Cash and hence fulcrum of growing airport is adequate Cash flow . Thus, generation of adequate Cash / funds is requirement of BIAL. While stating that presently, airport is faced with an arbitral award wherein BIAL is required to pay Rs.301 Crores together with interest, he stated that single Till approach is not appropriate for growing airports. He indicated that in view of proposed Single Till mechanism, BIAL cannot go ahead with additional capacity creation due to constraints such as, no additional equity infusion due to inability of promoters to infuse additional equity, difficulty in raising additional debt, failure to comply with financial covenants (DSCR & DSRA), cash flow constraints,(meager cash flow of Rs. 10 Crores)and low internal accruals.

2.4.6 As regards means of financing for future expansion, Shri Bhaskar brought out that additional Equity Infusion of Rs. 649 cr is required and GoI and GoK, as well as private promoters, have expressed their inability to infuse additional equity. While stating that the Shareholders Agreement mandates minimum shareholding of state promoters at 26%, he stated that infusion of additional equity by private promoters only, as contemplated by Authority, will have an adverse effect on the shareholding of state promoters. He emphasized that Land monetization, in the current market situation, may not generate enough funds to fund airport expansion and added that proposed land value adjustment is a disincentive for land monetization as it reduces internal accruals that are otherwise available for expansion. He, therefore, submitted that dual till regulation will ensure adequate internal resources for funding airport expansion.

2.4.7 Shri Bhaskar stated that Clause 4.1 of Land lease deed (LLD) empowers BIAL to

carry out Activities (as defined in Schedule B, which includes both airport and non-airport activities). It additionally empowers BIAL, with approval of KSIIDC, to utilize leased land including for facilitation of substantive further investment in or around the airport. For Activities set out in clause 4.1, such permission is not required. He stated that as per Clauses 3.4 and 3.5 – CA Excluded Area and SSA Excluded Area have been carved out and BIAL will be entitled to retain the same, even without operating the airport, subject to settlement of commercial terms therefor (13.5.2 of CA & 19.4.2 of SSA also reaffirms the above position). He further added that Land lease deed contemplates separation of airport and non-airport activities and does not contemplate cross subsidization. He therefore concluded that Land value adjustment is not in consonance with LLD.

2.4.8 As regards Regulatory Till, Shri Bhaskar stated that promises made to BIAL’s shareholders be respected as the Concession Agreement distinguishes between regulated services and services other than regulated services. Similarly, the State Support Agreement makes a distinction between airport activities and non-airport activities. He stated that tariff determination process is to be in line with

Page 4 of 10

the Airports Infrastructure Policy, in accordance with which the Greenfield airport in Bengaluru was developed. While stressing that Concession Agreement implies dual till, he submitted that Authority is required, under Section 13(1)(a)(vi) of the Act, to consider concessions provided.

2.4.9 Shri Bhaskar highlighted that the fact that in respect of BIA, MoCA had determined ad hoc UDF for international passengers on dual till basis and for domestic passengers on 30% shared till basis. He stated that this indicates that single till was not contemplated and the basis of financing was dual till (please refer Letter issued by ICICI).

2.4.10 He further stated that in respect of BIA, Financial close, as contemplated in the Concession Agreement, took place on the basis of dual till. As financial close was condition precedent for principal provisions of Concession Agreement to come into force, the conclusion that Concession Agreement contemplates dual till is inescapable. While stating that Viability Gap Funding of Rs.350 Crores promised in the SSA was calculated on the basis of dual till, he highlighted that Authority has considered and applied the mandate contained in OMDA in respect of Mumbai and Delhi airports. Likewise, concessions provided by the Central Government under the Concession Agreement in the case of BIA may also be honoured.

2.4.11 As regards Quality parameters, Shri Bhaskar stated that the Authority is proposing both subjective and objective service quality parameters and that under the AERA Act, it is the Central Government’s prerogative to prescribe objective quality parameters. Further, as per the Concession Agreement, BIAL is required to maintain quality as per IATA Global Airport Monitor service standards. Moreover, the Authority is taking into account a large number of quality parameters over which BIAL has no control, such as the time consumed during security check or immigration etc. He therefore concluded that to include such rebate for non-compliance while determining tariff would not only prejudice BIAL‟s interest but also be divergent to the covenants of the Concession Agreement and the AERA Act.

3. In conclusion, Shri Bhaskar requested the Authority to consider their submissions as contained in the presentation and the detailed submissions (which they were to submit in due course) including the following:

Uphold Concession agreement and approve Dual till mechanism for BIAL

Keep land out of regulation in line with Land lease deed

Allow bad debts and discounts for tariff determination

Not to impose new quality parameters

To consider Fuel throughput charges as non-aeronautical as per provisions of Concession agreement

Page 5 of 10

4. Shri Bhaskar also intimated the Authority and stakeholders that BIAL has written to MoCA on certain issues the problems envisaged by them, based on the Consultation Paper issued. 5. The Chairperson thanked requested the participants to state their comments/views in respect of the proposals contained in the CP No. 14/13-14 and the presentation by BIAL. 6. Mr. Malvyn Tan, Assistant Director, International Air Transport Association (IATA) submitted that the Cargo, Ground Handling and Fuel (Into plane) services, regardless of whether concessioned out or otherwise be considered as Aeronautical Service, as defined in the AERA Act and revenue therefrom be treated as aeronautical revenue in the hands of BIAL. He stated that IATA disagrees on Capital Financing to be met through UDF as he felt that in such a case the goal of privatisation through Private sector participation is not achieved. He said that as per IATA’s interpretation of the Concession Agreement does not contemplate UDF accruing to airport financial reserves to be used for financing Capital expansion. He also stated that IATA supports plans for continued investment in Infrastructure growth at the Airport. As regards the requirement of second run way projected by BIAL, Mr. Tan stated that the ATM number of 172000 to be reached by 2017-18 from 105000 in 2009-10 appear to be very an optimistic projection. He stated that this needs to be validly supported by a conducive cost environment and that IATA will consult with BIAL to evaluate if the estimation for requirement of second run way, in 2017-18 needs adjustment. He stated that Bad Debts are not to be considered as opex as per the Authority’s guidelines and hence IATA is not in agreement with Authority’s consideration of Rs. 47.51 crores as allowance for Bad debts. He stated that IATA agrees with Single Till Mechanism. 7. Regarding Concession Agreement implying Dual Till he stated that Concession Agreement would have to be explicit if it required application of Dual Till. He further stated and that Single Till does not cause injury to Airport Operator, except not allowing him to obtain more than fair rate of return on the investment which he would reap under Dual Till. He stated that IATA is strongly against a tariff structure which has a 131% increase in the landing charges for International Flights and stated that a moderate increase rate is needed. He also disagreed with the different Landing, Parking, Housing (LPH) charges for domestic and International Airlines, stating that it is a deviation from ICAO principles. He also stated that the UDF is a revenue enhancing measure and should be a balancing figure but BIAL has considered the International UDF to be fixed at 1700, thereby keeping Domestic UDF as the balancing figure. He also stated that the differential principles adopted in arriving at a ratio of approx. 1:4 in Domestic UDF to International UDF is unfair and, as was submitted by IATA at the time of MIAL consultation, a 1:2 ratio could be considered as a fair ratio. Mr. Tan commented that it is highly unfair that one airline subsidizes another. He supported Authority’s view of incorporating the Common Infrastructure levy (proposed as a new charge by BIAL) with UDF to simplify the tariff structure and not charging it separately. With regard to Pre-control losses, he stated that the Authority does not have retrospective jurisdiction. Prior to establishment of AERA, there was another Regulator in place, viz., the Ministry of Civil Aviation, who had determined UDF in respect of BIAL and hence

Page 6 of 10

that period should be omitted in assessing pre-control period losses. On CGF being considered as Agents or as Third Party concessionaires, he stated that CGF services should be considered as Aeronautical service irrespective of this distinction. He also requested for 3 weeks’ time extension for submission of their views. 8. The Chairperson clarified that the manner of treatment of revenue from cargo, ground handling and fuel facility is the same as was considered in the earlier Consultation Papers, i.e., if airport operator provides these services itself then revenue accruing to it from these services is treated as aeronautical. However, if these services are provided by an independent Third Party Concessionaire (ISP) the the revenue share/royalty etc. accruing to the airport operator from such ISPs is treated as non-aeronautical revenue. However, there may be a need to revisit this issue in the next Control Period. This is because, even when the aeronautical service is provided by the third party concessionaire, it can be said that the aeronautical service in question is “caused” to be provided by the airport operator (through third party concessionaire).

9. He informed that Agency is altogether a different concept as the revenue in the hands of agent becomes revenue of airport and the airport operator becomes the regulated entity. Accordingly, the quantum of revenue to be considered revenue from aeronautical services will have to be determined. He further stated that Pre-financing per se is not against ICAO principles and has been resorted to in different forms in different airports across the world. On ATM Projections he stated that while the comment needs to be reviewed and responded by the Operator, BIAL would have projected the ATM traffic based on a technical evaluation. This can be best reviewed by the statistics wing of the Airport Authority of India (AAI) and commented upon. This will be re-visited based on the comments that may be received and BIAL’s response to it. He stated that Bad Debts and Discounts, though a business reality, are generally not allowed in regulatory tariff determination. But an amount of Rs. 47.51 crores has been proposed by the Authority to be allowed as opex due to actual write off of corresponding dues from M/s Kingfisher Airlines, which, if recovered later, would be claimed back and will then go to reduce the ARR in that year. He stated that the issue of inter-se ratio of Domestic and International UDF is open for comments from the stakeholders basis. On Pre-control losses, Chairperson stated that as MOCA had determined it on ad-hoc basis, the Authority need to consider the pre-control period losses also if the airport operator did not get the fair rate of return on the basis of the ad-hoc UDF determined by the Government (that was the then regulator) The Chairperson stated that though Rs. 1700 was fixed as International UDF as per BIAL’s submission, it has been changed by the Authority in its proposed tariff structure. As regards the second runway and second terminal, as per the Authority’s Guidelines, BIAL is required to conduct user consultation which should be held by BIAL, in which IATA can raise these issues for proper planning of the future expansion in a reasonable manner. The Chairperson reiterated that single till is still maintained as the right approach by the Authority. As regards the request for extension of time, the Chairperson stated that extension will be duly considered based on request from all stakeholders. 10. The representative from MoCA stated that response to Consultation Paper on BIAL will be submitted in due course. He also requested for extension of time for

Page 7 of 10

submission of comments on HIAL Consultation Paper no. 9/2013-14 by 15 days beyond 22.07.2013 (the last date as per CP No. 9/13-14). 11. FIA representative requested BIAL to confirm whether, as per their agreements with the CGF concessionaires, the concessionaires are construed as agents or not. FIA representative requested for the business plan components considered by the Authority in working out the proposals contained in CP No. 14/13-14, to be given in Microsoft Excel for analysis. He also stated that while the Deposit relating to land and interest earned by BIAL on this deposit has been excluded in computation by the Authority, any cost or land relating to the hotel should also be reduced from RAB. He stated that the capitalisation of assets is proposed to the tune of approx. Rs. 2000 crores in the Control period, for which a technical evaluation should be carried out. He stated that the depreciation not should be considered upto 100% of the asset value. Instead, it should be restricted to 90% of the value, as has been specified in the Airport Guidelines. He stated that the detailed Working Capital loan amount workings are not available in the CP No. 14/13-14 and should be reviewed by the Authority for sharing with the stakeholders. The representative also stated that for future expenses, a benchmark cost review should be conducted. He stated that for Non-Aeronautical Revenues, while CPI based increase is given, the detailed computation of the same should also be provided. He also stated that it should be ensured that Advertisement revenue, utility revenue and Rental income is projected considering that with the New Terminal building, additional space will also be available for such activities. He also stated that the LPH rate increase is steep and a moderate increase should be considered. 12. In response, the Chairperson stated that though the Authority had incorporated detailed discussions on various issues in the CP and has uploaded all the relevant documents, the request now made by FIA will be duly considered by the authority. Regarding the issue of concessionaires being treated as Agents of BIAL and the underlying agreement, Chairperson stated that BIAL may respond to the same in writing. On depreciation, the Chairperson stated that it was to lessen, to some extent, maturity mismatch between depreciation and loan repayment that the Authority has proposed depreciation upto 100% of asset value. This would possibly help in Debt repayments and improved DSCR. On technical evaluation of assets to be capitalised, he stated that given the assets that are being capitalized in the current control period, majority of them would have undergone a consultation process. Further, if there is a certification from Chartered Accountant that appropriate due diligence was exercised in awarding tenders etc., the same could be considered.

13. On Working Capital loan, the Chairperson stated that the evaluation of the requirement and quantum of loan is best done by the bankers who are the lenders and thus in the best position to monitor the working capital limits. However, the interest is allowed as a cost, which has been proposed to be trued up on actuals. On efficiency of expenses, he stated that in a Board managed company, the Company’s Board is expected to exercise diligence and review of the spends. Any move towards benchmarking of the costs could be considered in the next Control Period. However, under the current perception, in case an airport operator optimizes costs and achieves operating costs less

Page 8 of 10

than the benchmark, then upon considering the benchmark opex for tariff determination – can be construed unjust enrichment of the airport operator.

14. The operating costs are also proposed to be trued up as requested by the airport operator. Regarding Non-Aeronautical Revenues considered by the Authority, he stated that as the airport is undergoing expansion, accurate estimation of the future revenues has not become feasible. Hence, the Authority has proposed to true it up. Regarding Landing, Parking and Housing charges being steeply increased, he stated that these rates had not been revised for long and hence an increase has been proposed. 15. The representative of Airline Operator Committee (AOC), Bengaluru supported the Authority’s Balanced approach in bringing out the CP. He stated that the increase in charges to be paid by the passengers should be implemented from the date of ticketing, and not from the date of travel, so as to reduce inconvenience to the passengers. He commented that the aeronautical charges are collected in INR and there is increase in rate proposed which is due to foreign exchange fluctuation. On levy of UDF he stated that Indian Airports should compare with other economies such as China, Korea, Japan, Malaysia etc. 16. Chairperson indicated that BIAL may respond on the Foreign exchange fluctuation and the aeronautical tariff rates. 17. The representative of Association of Private Airport Operators (APAOs) stated that, the letter and spirit of the Concession Agreement should be honoured where Dual Till was envisaged. He also stated that reducing the RAB based on value of land monetised by BIAL would reduce the returns to the Airport Operator. On Cost of Equity, he stated that Return on Equity should be commensurate with the risks. He stated that Cost of Equity as has been evaluated by agencies other than NIPFP which is at large variance with CoE evaluated by NIPFP. He also raised concerns on NIPFP’s methodology of computation of CoE. 18. In response to ACO’s comments, the Chairperson stated that the Consultation Paper deals with all the proposals put forth by the Airport Operator including that of Light Touch mechanism and Concession Agreement implying Dual Till. Land in excess of requirements for the airport was given on lease by GoK and Land value adjustment by reduction of RAB is only one of the mechanism of implementing this nexus between lease of land to BIAL (upon acquisition) and its purpose viz. to improve the financial viability of the airport project. However, GoK can suggest any other methodology. He also informed that in the Concession Agreement itself, Independent Regulatory Authority (IRA) was envisaged to be formed to regulate “any aspect of” the airport activities. The Authority is only determining tariffs in respect of services which are aeronautical services as per the AERA Act. On Cost of Equity, he stated that the Authority has elaborated up on various risk mitigation measures in the Consultation Paper which have reduced the risk to a very large extent. He stated that the cost of equity proposed in the CP has adequate and generous allowance for any uncertainties in estimating various parameter that go into its determination.

Page 9 of 10

19. The representative of Emirates Airlines reiterated the observations made by IATA. He stated that the Infrastructure expansion will be supported. He also commented that the Airport Operator did not get the Domestic UDF that it requested and hence amount has to be given to fill the balance shortfall. He commented that 131% increase is not acceptable and is nowhere increased in this steep manner. He also commented that 37% of the fee is paid on Ground Handling Services which needs to be looked into. 20. The Chairperson commented that large domestic UDF rates also have to be seen in relation to the cost of tickets, as a matter of “proportionately”. 21. The representative of Government of Karnataka requested for extension of 2 weeks to be given to submit responses. 22. The representative of Bharat Petroleum Company Limited (BPCL) stated that Rs. 1067 of Fuel Throughput fee was a charge levied by the Airport Operator before the tariff was determined by AERA. He stated that this is considered as a pass-through and if this is done to subsidise any other charge, the details may be provided. The representative of Hindustan Petroleum Company Limited (HPCL) endorsed the views of BPCL and stated that tariff revisions made, if any, should be prospective. 23. The representative of Shell Petroleum (Shell) stated that if the Fuel Throughput charge is higher, then it would require higher Working Capital which would in turn need to be met. He further stated that the revised tariffs should be determined in advance or be levied only prospectively. He also stated that suitable mechanism should be worked out to reduce the rate of FTC per Kilo Litre. 24. The representative of Airport Authority of India (AAI) stated that in respect of BIAL, MoCA had granted an ad-hoc UDF, yet Pre-control period losses are being considered by the Authority. However, despite their request, some other airports did not get any ad-hoc UDF. He stated that the Authority should consider the losses to the airport operator in such a case also. He further queried whether the Authority will re-determine the charges proposed in case of BIA during the current control period itself if the land is monetised by BIAL. 25. In response, the Chairperson stated that the current computations consider the gap in funding of Rs. 649 crores being brought in as Equity by the promoters. If this amount is brought in as Equity, then it would not have any impact on proposed tariffs but if any other financing arrangements was made by BIAL, e.g., Land monetisation or any other arrangement, then the computation of tariffs would undergo changes to that extent. He also stated that Para 4.21 of the Consultation Paper elaborates this issue. As regards consideration of pre control period losses for such airports (notably AAI) that did not get any ad-hoc UDF. Chairperson stated that the then regulator (government) may not have felt the need to grant UDF and now the Authority will be unable to go into that question.

Page 10 of 10

26. The representative of Bangalore Chamber of Industry and Commerce stated that the need is felt for expansion of the Airport and that they support the consultative approach followed by BIAL. He stated that in order to retain investor’s confidence, Concession Agreement should be implemented. 27. The representatives of CIAL, MIAL and HIAL stated that they will submit their comments in due course. 28. Chairperson noted that in its presentation BIAL has stated that the average return works out to less than 16%, however, as per the projections regarding the accretion to RAB, BIAL will earn 16% Return on Equity. While considering return on equity, equity includes Retained Earnings. The Chairman observed that the presentation made by Mr. Bhaskar stating that average return came to less than 16% appeared to pertain to the average return on “capital employed”. The Authority’s calculations on Weighted Average Cost of Capital (WACC) was based on the equity return at 16% and the cost of other means of finances taken on actual. The other sources of finance includes Debt, Refundable Security Deposit (as and when obtained), etc. The equity return of 16% is given on the total equity plus retained earnings. However, capital employed represents work-in-progress on which the cost of debt is made available. This cost of debt is much lower than the cost of equity. As and when the capital works in progress get capitalized, they are eligible for weighted average cost of capital that includes the portion of equity as well. The interest during construction is also capitalized and hence to compare the return on the capital employed with equity return is not appropriate. 29. Regarding Equity infusion, Chairperson said the alternate means of funding should be re-examined. He also reiterated that reduction to RAB by value of land monetized is only a mechanism proposed by the Authority. On Greenfield Policy, 2008 and its relevant to agreements executed dated prior to the policy (i.e., 2005 or 2006), he stated that the future policy (unless it is an Act of the Parliament), generally, cannot alter the covenants of an earlier agreement. Only an Act passed by the Parliament can be said to take primacy over any agreements to the extent of repugnancy.

30. There being no more comments from the stakeholders present in the meeting, the chairperson thanked all the stakeholders for participation and expression of their views. He further stated that the Authority will consider request for extension of time for submission of comments. The decision in this regard will be conveyed soon.

31. The meeting ended with a vote of thanks to the Chair.

******

Annexure - I List of Participants : Shri/Smt Airports Economic Regulatory Authority of India :

1. Yashwant S. Bhave, Chairperson - in Chair 2. Capt. Kapil Chaudhary, Secretary 3. C.V. Deepak, OSD-II 4. Radhika R., DGM 5. A.B. Saxena, AGM 6. Praveen Gupta, AGM(Finance) 7. R.K. Gupta, AGM (Finance) 8. Dheeraj Khanna, Manager (Finance) 9. Ravi Pahwa, Bench Officer

Bangalore International Airport Pvt. Ltd.

10. B.Bhaskar, Sr. Director – Finance & Support Services 11. Harimarar, President, Airport Operations 12. Daniel Bircher, Director - Operations 13. Jagdish Prasad Rajguru, Head – Legal 14. Girish Nair, Asst. V. P., Head – Airline Marketing & Aviation Contracts 15. Kirankumar J G, Asst. General Manager – Finance Controlling 16. Anand Kumar, Asst. V. P., Head – Controlling & Regulatory affairs 17. Niranjan Reddy, Head HR 18. Sridhar K. Chari, Secretary, BCIIC 19. R.Nagesh, Deputy General Manager(IPD), KSIIDC 20. Sunil Joshi, Sr. Manager 21. Manu, Consultant

Govt. of Karnataka

22. Vandana Gurnani, Resident Commissioner

Airports Authority of India (AAI)

23. M.Ravi Varma, General Manager-Finance 24. S Samantha, General Manager-Finance 25. R D Vishwakarma, Jt General Manager-Finance

International Air Transport Association (IATA)

26. Amitabh Khosla, Director 27. Malvyn Tan, Assistant Director

Emirates :

28. Guy Hickling, Manager Procurement & Logistics Mumbai International Airport Pvt. Ltd. :

29. Alok Patni, Assistant Manager

GMR Hyderabad International Airport Pvt, Ltd. :

30. Madhukar Dodrajka, General Manager-Finance 31. Gautam Agrawal, Manager

Cochin International Airport Limited:

32. Santhosh J Poovattil, Senior Manager-Finance

Association of Private Airport Operators (APAO) :

33. Satyan Nayar, Secretary General 34. Dr. K.V. Damodharan, Advisor – Regulatory Affairs 35. Pawan Chande, Leigh Fisher, Associate Director

Airfrance:

36. Sanjiv Chawla, Station Manager – Bangalore Airlines Operation Committee

37. Arum Chandra, Station Manager - Bangalore

Federation of Indian Airlines (FIA) :

38. Gaurav Khurana, (BMR Advisors) 39. Jeetu Bairathi, (BMR Advisors) 40. Divya, (JSR)

Bharat Petroleum Corporation Limited

41. N. Anand, Deputy General Manager Business Development-Aviation-HQ 42. Sujith Kumar, Senior Manager Business Information –Aviation

Bharat Stars Services (P) Ltd

43. Partha Sarathi Hindustan Petroleum Corporation Ltd.

44. Indrajit Dasgupta, Chief Manager – Commercial, Aviation SBU 45. R.K.Rai, Chief Manager – Aviation, Aviation SBU

Shell MRPL Aviation Fuels & Services Ltd.

46. V.N. Diwakar, Chief Executive Officer

PKF Sridhar Santhanam

47. Ravi Surya Narayanan, Partner 48. Seetha Lakshmi, Partner 49. Shanta Mani

Deloitte Touche Tohmatsu

50. Pushkar Thakur, Manager 51. Ritesh Sinha, Manager

ICWAI

52. Harpreet Kaur, Project Assistant 53. Seema, Project Assistant 54. Yogendar, Project Assistant

`

AERA Consultation Paper on tariff

determination of BIAL – Presentation

July 22, 2013

Introduction

BIAL thanks the Authority for this opportunity to present its views in

relation to Consultation Paper No.14/2013-14 dated June 26, 2013 (“CP”).

BIAL is making this presentation to put forth its views on certain

proposals in the CP and their implications on BIAL‟s finances.

BIAL seeks indulgence of the Authority for favourable consideration of its

submissions.

BIAL craves leave to submit detailed responses to the CP.

Bangalore - The face of Global

India

Bangalore is the capital of Karnataka and India’s fifth largest metropolitan city, also known as garden city of India. But

now it has earned yet another name, „silicon valley of Asia‟ and has established itself as a successful brand in the IT-ITES,

BPO & KPO services world-wide. Apart from being India’s information technology hub it has also become India’s aviation

hub. thanks to the presence of prestigious institutions such as Hindustan aeronautics limited, defense research and

development organization, Indian space research organization and national aerospace laboratories, among others.

Yesterday – (11.5 Mio Pax)

WINNER

5

Today (Upto 17 Mio pax)

HOTEL

T1

T2

PARKIN

G

PARKIN

G

PARKIN

G

FORECOURT T1-T2 RAIL STATION

Tomorrow (35 Mio pax & above)

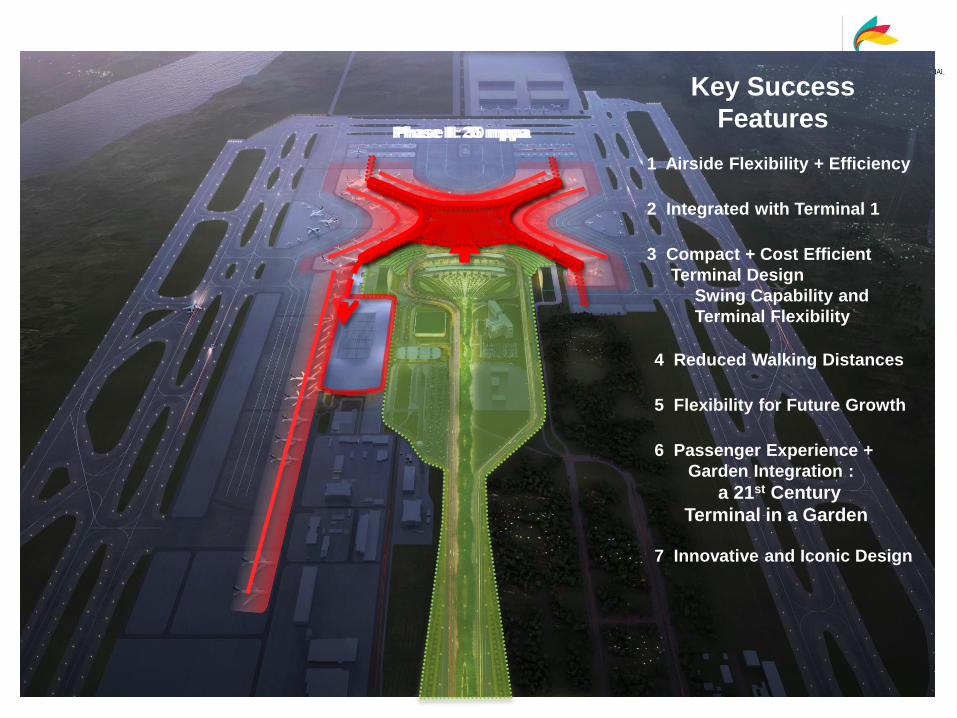

Terminal 2 Development

Phase I: 20 mppa Phase II: 35 mppa Phase III: 50 mppa

1 Airside Flexibility + Efficiency

2 Integrated with Terminal 1

3 Compact + Cost Efficient

Terminal Design

Swing Capability and

Terminal Flexibility

6 Passenger Experience +

Garden Integration :

a 21st Century

Terminal in a Garden

5 Flexibility for Future Growth

4 Reduced Walking Distances

7 Innovative and Iconic Design

Key Success Features

Key Success

Features

The Company - BIAL

Our Values

Efficient

Caring

Engaging

Proactive

Simple

Airline Business

Operations Highlights – ASQ trends

12

4. FY - Full Year, Q1 - Quarter 1

1. The above ASQ rating is the rating towards overall satisfaction with the airport

2. ASQ rating is measured on a scale of 1 to 5, 1 being min and 5 max

3. ASQ rating is based on a calendar year

4.09 4.12 4.24 4.27 4.20

3.00

3.50

4.00

4.50

5.00

FY 2009 FY 2010 FY 2011 FY 2012 Q1 13

ASQ trend

ASQ rating

Our Vision

Gateway to

South India

BLR is in the

center of south

India and also

connected with

other south

Indian cities in

terms of trade

and culture.

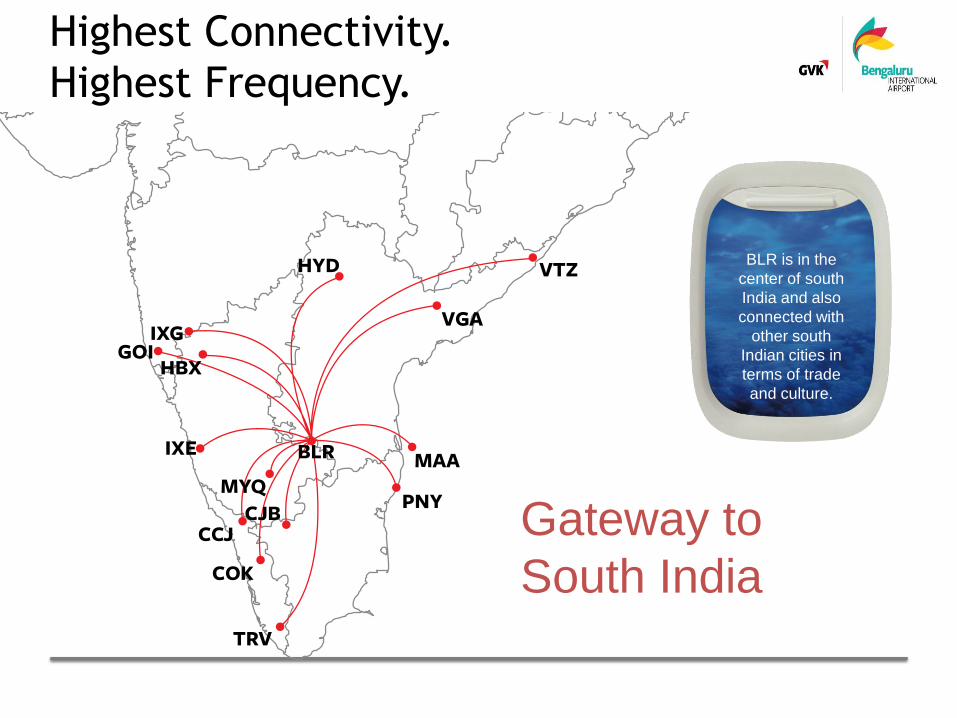

Highest Connectivity.

Highest Frequency.

BIAL project – Concession & Other project agreements

Being first PPP project, many concepts were conceptualized and

crystallized during execution of above agreements

Many terms were defined and some were implied

Initial UDF approvals by MoCA were on adhoc basis

International UDF – Dual Till basis

Domestic UDF – Hybrid / Shared till basis

BIAL – Pioneer PPP airport project

in India

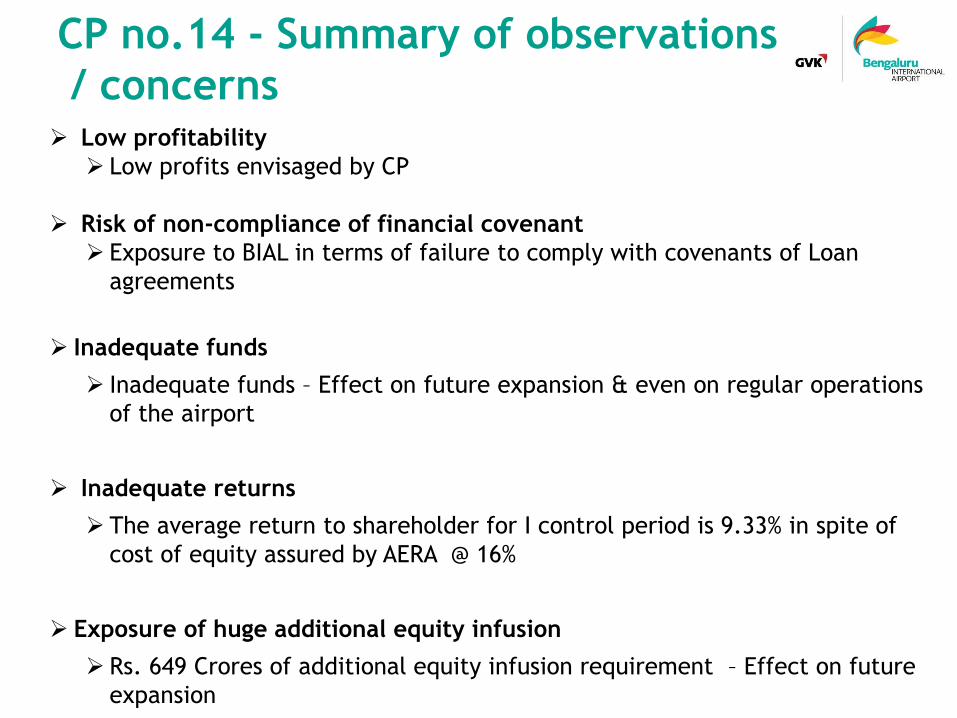

Low profitability

Low profits envisaged by CP

Risk of non-compliance of financial covenant

Exposure to BIAL in terms of failure to comply with covenants of Loan

agreements

Inadequate funds

Inadequate funds – Effect on future expansion & even on regular operations

of the airport

Inadequate returns

The average return to shareholder for I control period is 9.33% in spite of

cost of equity assured by AERA @ 16%

Exposure of huge additional equity infusion

Rs. 649 Crores of additional equity infusion requirement – Effect on future

expansion

CP no.14 - Summary of observations

/ concerns

As per Traffic growth projections, Future expansion - 2nd Terminal & 2nd

Runway etc thereby capacity creation needs pirority

Proposed Single Till mechanism, BIAL cant go ahead with additional

capacity creation due to below constraints:

No additional equity infusion

Inability of promoters to infuse additional equity

Difficulty in raising additional debt

Failure to comply with financial covenants (DSCR & DSRA)

Severe cash flow constraints

Meager cash flow of Rs. 10 Crores which is sufficient for 10 days

expenses of running the airport

Low internal accruals

Future expansion – imminent requirement

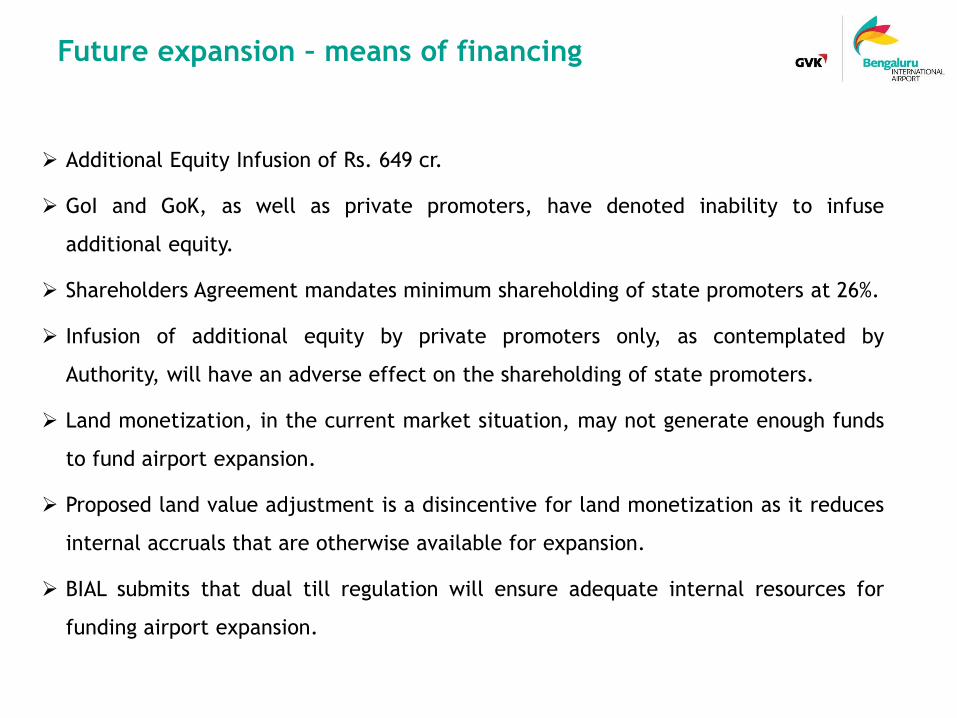

Additional Equity Infusion of Rs. 649 cr.

GoI and GoK, as well as private promoters, have denoted inability to infuse

additional equity.

Shareholders Agreement mandates minimum shareholding of state promoters at 26%.

Infusion of additional equity by private promoters only, as contemplated by

Authority, will have an adverse effect on the shareholding of state promoters.

Land monetization, in the current market situation, may not generate enough funds

to fund airport expansion.

Proposed land value adjustment is a disincentive for land monetization as it reduces

internal accruals that are otherwise available for expansion.

BIAL submits that dual till regulation will ensure adequate internal resources for

funding airport expansion.

Future expansion – means of financing

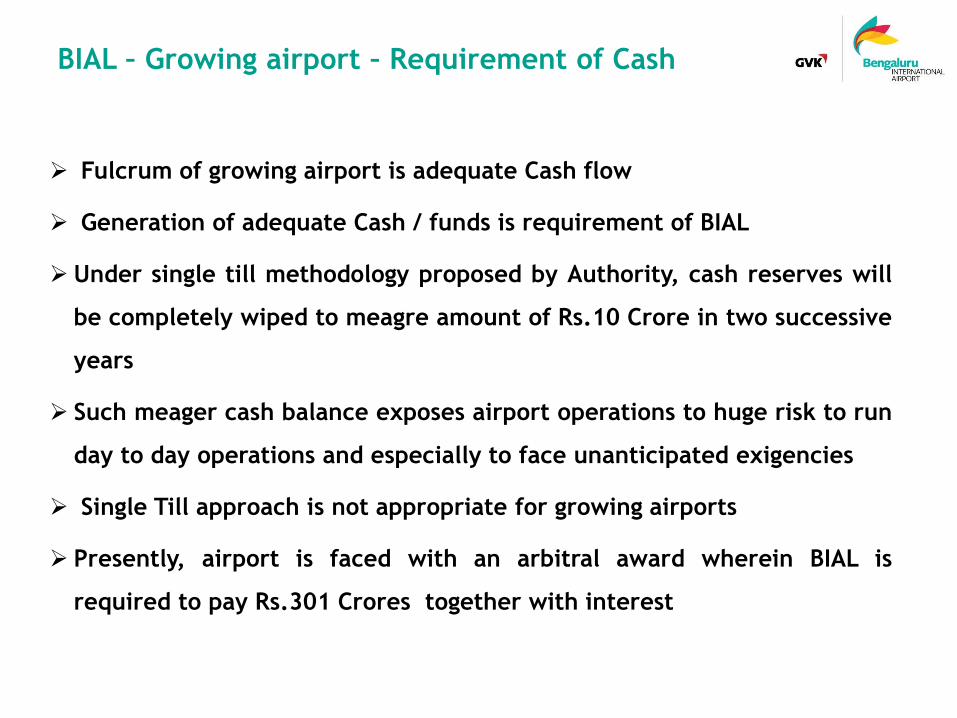

Fulcrum of growing airport is adequate Cash flow

Generation of adequate Cash / funds is requirement of BIAL

Under single till methodology proposed by Authority, cash reserves will

be completely wiped to meagre amount of Rs.10 Crore in two successive

years

Such meager cash balance exposes airport operations to huge risk to run

day to day operations and especially to face unanticipated exigencies

Single Till approach is not appropriate for growing airports

Presently, airport is faced with an arbitral award wherein BIAL is

required to pay Rs.301 Crores together with interest

BIAL – Growing airport – Requirement of Cash

Return on Equity

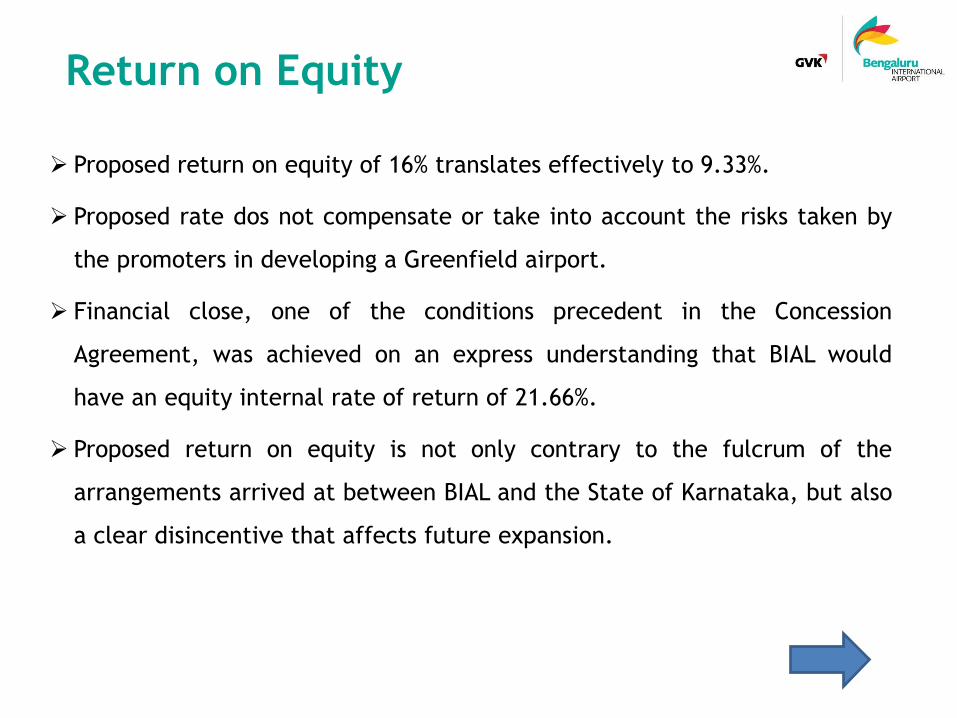

Proposed return on equity of 16% translates effectively to 9.33%.

Proposed rate dos not compensate or take into account the risks taken by

the promoters in developing a Greenfield airport.

Financial close, one of the conditions precedent in the Concession

Agreement, was achieved on an express understanding that BIAL would

have an equity internal rate of return of 21.66%.

Proposed return on equity is not only contrary to the fulcrum of the

arrangements arrived at between BIAL and the State of Karnataka, but also

a clear disincentive that affects future expansion.

Non-Airport activities - Land value adjustment

Land Lease Deed (LLD)

Clause 4.1 of LLD empowers BIAL to carry out Activities (as defined in

Schedule B, which includes both airport and non-airport activities).

Clause 4.2 additionally empowers BIAL, with approval of KSIIDC, to utilize

leased land including for facilitation of substantive further investment in

or around the airport. For Activities set out in clause 4.1, such permission

is not required.

Clauses 3.4 and 3.5 – CA Excluded Area and SSA Excluded Area have been

carved out and BIAL will be entitled to retain the same, even without

operating the airport, subject to settlement of commercial terms therefor

(13.5.2 of CA & 19.4.2 of SSA also reaffirms the above position).

Land lease deed contemplates separation of airport and non-airport

activities and does not contemplate cross subsidization.

Land value adjustment is not in consonance with LLD.

Non-Airport activities - Land value adjustment

Commercial & Operational aspects

Premise that all real estate activity will yield extraordinary profits.

Case in point – Bangalore Airport Hotel is saddled with an arbitration award

of Rs.377 Crore approximately.

Thus, land value adjustment may have adverse effect on BIAL‟s finances.

BIA lacks proper connectivity with the city.

Leased land is not fit for commercial use and requires huge investment in

infrastructure such as roads, utilities etc.

Lease rentals or commercial returns may accrue over a long gestation

period.

Immediate and upfront deduction may thus result in losses and make

commercial utilization of leased land unattractive.

Proposed land value adjustment is a disincentive for commercial

exploitation of land.

Regulatory Till

Promises made to BIAL’s shareholders be respected:

Concession Agreement distinguishes between regulated services and services

other than regulated services.

Similarly, the State Support Agreement makes a distinction between airport

activities and non-airport activities.

Tariff determination process is to be in line with the Airports Infrastructure

Policy, in accordance with which the Greenfield airport in Bangalore was

developed.

Concession Agreement implies „dual till‟.

Authority is required , under Section 13(1)(a)(vi) of the Act, to consider

concessions provided.

Regulatory Till

Ad hoc UDF determination

The fact that MoCA had determined adhoc UDF for international passengers on dual

till basis and for domestic passengers on 30% shared till basis indicates that single

till was not contemplated.

Basis of financing was dual till (please refer Letter issued by ICICI)

Financial close, as contemplated in the Concession Agreement, took place on the

basis of dual till. As financial close was condition precedent for principal

provisions of Concession Agreement to come into force, the conclusion that

Concession Agreement contemplates dual till is inescapable.

VGF of Rs.350 Crore promised in the SSA was calculated on the basis of dual till.

Authority has considered and applied the mandate contained in OMDA in respect

of Mumbai and Delhi airports. Likewise, concessions provided by the Central

Government under the Concession Agreement in the case of BIA may also be

honoured.

Quality parameters - penalties

The Authority is proposing both subjective and objective service quality

parameters.

Under the AERA Act, it is the Central Government‟s prerogative to prescribe

objective quality parameters.

Further, as per the Concession Agreement, BIAL is required to maintain

quality as per IATA Global Airport Monitor service standards.

Moreover, the Authority is taking into account a large number of quality

parameters over which BIAL has no control, such as the time consumed

during security check or immigration etc.

Therefore, to include such rebate for non-compliance while determining

tariff would not only prejudice BIAL‟s interest but also be divergent to the

covenants of the Concession Agreement and the AERA Act.

Request to Authority

We request the Authority to consider our submissions as contained in the

presentation and as well in detailed submissions during consultation process :

Uphold Concession agreement and approve Dual till mechanism for BIAL

Keep land out of regulation in line with Land lease deed

Allow bad debts and discounts for tariff determination

Not to impose new quality parameters

To consider Fuel throughput charges as non-aeronautical as per provisions

of Concession agreement

Thank you

Bangalore International Airport Limited

Alpha 2, Bengaluru International Airport,

Devanahalli,

Bangalore – 560300, India

www.bengaluruairport.com

Related Documents