2005 Annual Report Center for Pacific Basin Studies Federal Reserve Bank of San Francisco CPBS FRBSF

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

2005 Annual Report

Center for Pacific Basin StudiesFederal Reserve Bank of San Francisco

CPBSFRBSF

Center for Pacific Basin Studies 2005 Annual Report

�

Contents

From the Director ....................................................2

A Monetary Policymaker’s Passage to India .......................................................3FRBSF President and CEO Janet L. Yellen External Imbalances and Adjustmentin the Pacific Basin: Conference Summary .........7 Reuven Glick and Mark Spiegel

Does Europe’s Path to Monetary Union Provide Lessons for East Asia? ............................ 11Reuven Glick

A Look at China’s New Exchange Rate Regime ....................................................................15Mark Spiegel

What If Foreign Governments Diversified Their Reserves? ......................................................19Diego Valderrama

To Float or Not to Float? Exchange Rate Regimes and Shocks .............................................23Michele Cavallo

Other Programs ....................................................27

Center Staff ............................................................28

Visiting Scholars ...................................................29

Center Working Papers .......................................30

Center Staff Pacific Basin Publications ...............32

CPBS Pacific Basin Notes ....................................35

Other Recent Articles and Working Papers .......36

Participation in the Center’s Programs ..............39

About the Center

Since 1974 the Pacific Basin program of the Federal Reserve Bank of San Francisco has promoted coop-eration among central banks in the Pacific Basin and enhanced public understanding of economic policy issues in the region. In 1990 the Center for Pacific Basin Studies was established by the Bank within its Economic Research Department to open the program to greater participation by researchers in other central banks, universities, research institutes, and interna-tional organizations. The Center’s mission is to further international understanding of major Pacific Basin monetary and economic policy issues. The Center’s programs are designed to carry out this mission through staff research, its visiting scholar program, its international network of research associates, and international conferences.

Center for Pacific Basin Studies 2005 Annual Report

�

From the Director

Mark M. SpiegelVice President

International Researchand Director

Center for Pacific Basin Studies

In 2005, the FRBSF Center for Pacific Basin Studies (CPBS) confronted the large and growing U.S. current account deficit in two scholarly conferences. Explor-ing this topic was of particular interest to the Center, because of its implications for the U.S. economy and because of the important role Asia plays in it, as the U.S. has traditionally run a large bilateral current account deficit with countries in that region. The U.S. current account balance has deteriorated significantly over the last fifteen years. In 1991, it was in surplus. Since then, it has swelled to more than 6 percent of GDP, the highest such ratio in 40 years.

In February 2005, the CPBS and U.C. Berkeley’s Clausen Center for International Economics co-spon-sored a symposium on this issue entitled “The Revived Bretton Woods System: A New Paradigm for Asian De-velopment?” The symposium provided an opportunity for leading economists to discuss the sustainability of international trade patterns. This issue was revisited in our Annual Conference “External Imbalances and Adjustment in the Pacific Basin,” held in September 2005. Details of both the symposium and the confer-ence, including links to the relevant research material, are included in this report.

The year also included an official visit by FRBSF President Janet Yellen and Federal Reserve Board Governor Donald Kohn to India. These trips by Federal Reserve officials enhance ties with policymakers in the

country and increase the Federal Reserve’s knowledge of those regions, which aids in conducting policy asso-ciated with ensuring global stability and carrying out the 12th District’s banking supervision responsibilities. Below, we include President Yellen’s report on her Indian experience.

The remainder of this report summarizes the Center’s research on Pacific Basin topics in 2005. Cen-ter staff conducted studies on a diverse set of topics. Center activities this year also included a weeklong seminar conducted jointly with the World Bank on monetary policy and financial issues in Paris. This seminar is geared towards senior policymakers, and reflects a long-running partnership in community outreach with the World Bank.

The Center disseminates its studies through vari-ous channels. Pacific Basin research results are initially issued in the FRBSF Working Paper series, with the intention of eventual external publication in academic journals or the FRBSF Economic Review. Shorter analy-ses are distributed as “Pacific Basin Notes” through the FRBSF Economic Letter series. The Center’s publica-tions can be accessed through its website at www.frbsf.org/economics/pbc/.

The CPBS continues to expand its activities and community outreach programs. We are broadening our already active visiting scholar program to focus on scholars doing work with policy implications for the Asian region. I would like to thank everyone for their contributions to the Center’s activities during the past year, particularly my colleague, Reuven Glick, who co-organized the Annual Conference with me, and Andrew Rose of U.C. Berkeley, who joined the two of us in organizing the symposium on behalf of the Clausen Center. I would also like to thank Sylvia Papa for her continued excellent administrative assistance on behalf of the Center. I look forward to continued participation from all of you in the future.

Center for Pacific Basin Studies 2005 Annual Report

�

Janet YellenPresident and

Chief Executive Officer

An overview of India’s economy�

India’s economy is booming. Since 1991, economic growth has averaged about 6%, and in the last two or three years it has grown even faster—around 8%—mak-ing India, along with China, among the fastest growing countries in the world. Per capita GNP is still very low but has been rising impressively.

The service sector in India accounts for more than 50% of total output—an unusually large share for a developing country—and its growth has been consis-tently strong. In the industrial sector, growth has been more variable, but it has picked up noticeably in the past two years. The agricultural sector is a major con-cern to Indian policymakers. It accounts for roughly 20% of India’s output and employs 60% of the popula-tion. In recent years, farm income growth has slowed due to weak productivity growth. This sector has also been held back by inadequate roads and storage facili-ties. Clearly, improving performance in agriculture is a key to increasing the welfare of the bulk of India’s people, who are not fully sharing in the country’s over-all growth.

India’s business climate is improving, and one con-crete sign is that foreign capital is finally flowing in—

A Monetary Policymaker’s Passage to India

though not at anything like the scale into China—after a long history of hostility to foreign involvement in the economy.

The single most important reason for stronger growth is economic liberalization. The process dates back to the mid-1980s, following many years of being a highly closed, highly regulated economy based on self-sufficiency and modeled on Soviet-style central planning. In 1991, further reforms were undertaken in the wake of a balance of payments crisis related to massive fiscal deficits. The government began to lib-eralize inward capital controls, institute banking re-forms, and lift trade barriers, further spurring growth. This reform process is continuing.

Our perception is that the broad path of reform is firmly established, though the pace or details may vary with changes in government. In the elections of May 2004, the Bharatiya Janata Party—which was pro-reform—was replaced by a coalition led by the Congress Party. While this coalition has slowed the pace of liberalization, promising to focus on poverty alleviation and rural reforms, it is not backsliding, and several of the government officials we talked with seemed to be aware of the need for more progress in privatizing state enterprises and otherwise encourag-ing private markets.

The most visible example of the success of India’s economy and of unfettered market processes is the IT (information technology) sector. India’s advantages as an IT center include its abundance of English-language speakers, strong technical education system, and professional talent with programming and manageri-al experience. Government policies have also played a

FOOTNOTES:

�This article summarizes President Yellen’s report on her trip to India in November 2005.

Center for Pacific Basin Studies 2005 Annual Report

�

key role, as the service sector generally is less heavily regulated, less taxed, and less dependent on physical infrastructure. Many of the IT sector representatives we met expressed confidence that this sector will con-tinue to attract the business of U.S. companies looking for opportunities to outsource some of their activities.

The direct importance of IT services for India’s overall growth is easily exaggerated—currently, the sector accounts for approximately 3% of GDP and em-ploys less than 1% of the workforce. But its success has had a very significant positive demonstration effect. In particular, it has created pressure for reform in other sectors, as Indian businesspeople have become more aware of profit opportunities to be exploited both at home and abroad. This is a fundamental change from earlier periods when Indian producers sought govern-ment protection from domestic and import competi-tion. The success of this sector has strengthened the conviction that Indian industries can excel at compet-ing in world markets and has generated a palpable in-crease in confidence about the economy’s future.

Restraints on growth

Though liberalization has progressed, many regu-lations still discourage and distort growth, and much reform remains to be implemented. For example, de-spite declines in import tariffs, India remains a rela-tively closed economy. Its ratio of exports plus im-ports to GDP is between 25% and 30%, well below the levels of other countries in Asia. In addition, although approval for foreign direct investment is easier, such investment is still wholly prohibited in some sectors, such as retailing, agriculture, and railroads.

While liberalization has been critical to India’s eco-nomic growth, two other factors also have played a role in recent years—stimulative fiscal policy and stimulative monetary policy. Both are a matter of some macroeconomic concern. In the case of fiscal policy, government deficits are huge. Combined central and

state fiscal deficits have been around 8-9% of GDP in recent years. The fiscal situation has constrained pub-lic infrastructure investment and crowded out private investment. The deficit also undermines reforms in other areas, such as the financial sector, because the government is always concerned about finding buy-ers for the debt. Complicating matters is the concern about how the new government will finance its social programs, such as a guarantee of limited employment to a member of every household.

In the case of monetary policy, inflation has now risen to around 4%. Demand is being fed in part by rapid growth in consumer spending fueled by con-sumer credit. Higher oil prices are also a factor. To ad-dress the inflation problem, the Reserve Bank of India raised the short-term policy rate in 2005.

Higher oil prices are a concern to India above and beyond their inflationary impact. Since India is a ma-jor oil importer, higher oil prices are a hit to real in-come, and the burden tends to fall disproportionately on India’s poor. To shield Indian households, only a fraction of the price hikes for fuel have been passed on to consumers. The difference has been absorbed by oil marketing companies, most state-owned, which has necessitated government subsidies. The subsidies create a further burden for government finances.

In the view of most private and public sector representatives with whom we spoke, the number one barrier to sustainable growth at the recent ac-celerated pace in India is infrastructure, particularly transportation and power. The government has made some progress in improving airports, seaport facili-ties, and roadways. In fact, The New York Times (2005) did a four-part article on the construction of a major highway around India, dubbed “The Golden Quad-rilateral.” Nonetheless, problems remain. The power sector faces even more severe problems related to in-adequate capacity and substantial distribution losses, estimated to be as high as 40%. The government’s

Center for Pacific Basin Studies 2005 Annual Report

�

ability to undertake needed investments to improve the country’s infrastructure is limited by fiscal problems, as I mentioned. As a result, there is increasing focus on greater private sector involvement through public-pri-vate partnerships in the development and management of ports and power generation facilities.

Another factor restraining growth in India is a sys-tem of labor market regulations that restricts flexibility in firing as well as restrictive business regulations more generally. In the view of the experts from the multilat-eral institutions and the Indian business leaders with whom we met, these regulations are a barrier to signifi-cant expansion of India’s manufacturing sector, which is necessary to create more jobs in the economy for less-skilled workers. According to World Bank measures (2006), India’s degree of labor market flexibility and general business climate rank very low in comparison to many other developing countries, including China. India’s textile industry, which employs 30 million peo-ple, has been one of the more highly regulated sectors and is still dominated by many small businesses. As a result, this industry, unlike China’s, was not well posi-tioned to gear up in response to the end of the multi-fi-ber quotas on exports to industrial countries. Although Indian companies have found ways around the labor laws by outsourcing production to the unorganized sector, greater labor flexibility is important to the abil-ity of the economy to achieve scale economies and gen-erate more jobs.

India’s banking sector

As noted, the health of the banking sector and the state of bank supervision and regulation were a focus of our trip, which is natural, given our Bank’s responsi-bilities in assessing the quality of home country super-vision of foreign banks operating in the United States. Prior to 1991, the banking system in India was char-acterized by weak asset quality, low profitability, and limited transparency due to directed lending and regu-

latory forbearance. However, things have improved considerably. Nonperforming loan levels have been falling in India and are now in the 4-5% range, and bank capital is adequate.

Two concerns relating to the health of the banking sector have, however, attracted concern. First, there is concern that aggressive retail loan growth may lead to future asset quality problems. I noted earlier that India is experiencing a credit boom, and it is possible that lending standards may be declining, which could lead to higher nonperforming loans in the future.

A second concern relates to the banking system’s high level of exposure to long-term government bonds. Although government bonds have fallen to less than 30% of the banking system’s assets—from nearly 40%—this level remains high and entails risks as inter-est rates continue to rise.

An important feature of India’s banking system is that, as in China, state ownership of banks is high. Overall, state-owned entities account for close to three-fourths of total financial system assets.

Indian private banks are flourishing. They have ad-opted relatively stronger risk-management processes, using technology effectively and developing new fi-nancial products. The most successful of these banks are ICICI and HDFC, which continue to increase mar-ket share and compete successfully with both state-owned and foreign banks.

Foreign banks would like to expand in India, but ownership remains restricted. To date, there are rough-ly 30 foreign banks operating in India, but they repre-sent only 7% of total assets. The Reserve Bank of In-dia understands the benefits that an increased foreign banking presence can bring to the financial sector, but it is committed to giving Indian banks a cushion of time to prepare for increased competition. Reforms to foreign ownership policy were announced earlier this year but they do not materially change the way foreign banks can operate until 2009.

Center for Pacific Basin Studies 2005 Annual Report

�

Conclusion

On a fact-finding trip to India, it would be impossi-ble, and, indeed, a huge waste, to ignore what glimps-es of Indian life and culture one might get. Though we visited only three cities, we were struck by the diz-zying beauty and the dizzying disparities that India has long been known for. We were lucky enough to see the serene magnificence of the Taj Mahal. Another manmade wonder—more of the 21st century than of the 17th—was a technology campus, for all the world like any such facility you might see in Silicon Valley.

But en route to both, we saw other faces of India—shan-ties, roads clogged not just with cars, but with pedes-trians, peddlers, pushcarts, cows, goats, even a caravan of camels. Scenes like these are not only unforgettable, they are also emblematic of the challenges the country faces. Our visit raises my hopes that India will remain on the path of liberalization, with the ultimate goal of improving the economic well-being of its people.

ReferenceWorld Bank. 2006. Doing Business in 2006: Creating Jobs. Washington, DC.

Center for Pacific Basin Studies 2005 Annual Report

�

librium model of the U.S. and the rest of the world to estimate the magnitude of dollar depreciation neces-sary to eliminate the U.S. current account deficit. Fo-cusing only on the relative price effects of currency change, they calculate that a devaluation of as much as 30% is necessary to achieve this goal. These estimates are sensitive to assumptions about key parameters, particularly the degree of substitutability of traded and nontraded goods. For example, a lower substitut-ability implies that a greater depreciation is required to induce a shift of resources out of nontradables and into tradables production. Obstfeld and Rogoff note that currency and price changes are only part of the adjustment mechanism through which the U.S. trade imbalance will be reduced; other factors, such as the relative growth of foreign output, matter as well. They also point out that it is difficult to determine when the adjustment to the U.S. current account will begin and whether it will be rapid or slow.

The ongoing U.S. trade deficits have contributed to the buildup of U.S. net international liabilities. Since the early 1980s, the U.S.’s net international investment position has swung from a creditor position of more than 5% of GDP to a debtor position amounting to 22% of GDP. This situation has raised concerns about the extent to which the U.S. can continue to accumulate foreign liabilities. Pierre-Olivier Gourinchas of U.C. Berkeley and Hélène Rey of Princeton University ana-lyze how a depreciation of the dollar affects the U.S. net international investment position through two channels, trade and finance. Through the “trade chan-nel,” a depreciation makes U.S. goods more competitive

The U.S. current account balance on international transactions in goods and services has deteriorated significantly over the last fifteen years. Since recording a small surplus in 1991, it has swelled to a deficit in 2005 of more than 6% of GDP, the highest such ratio in over 40 years. In the past, other countries with a cur-rent account deficit above 5% of GDP have typically faced worsening borrowing terms, either in the form of reduced borrowing opportunities or increased inter-est charges. By that standard, some would argue that the U.S. is overdue for such adjustments, including a significant fall in the value of the dollar.

This year’s Pacific Basin Conference brought togeth-er seven papers examining the U.S. current account deficit and its implications, with special emphasis on the prominent role of Asian countries, which accounted for over 40% of the overall U.S. trade deficit in 2004.

The U.S. current account and net international investment position

Maurice Obstfeld of U.C. Berkeley and Kenneth Rogoff of Harvard University use a small general equi-

External Imbalances and Adjustment in the Pacific Basin: Conference Summary

�

FOOTNOTES:

� This article summarizes the papers presented at the conference on “External Imbalances and Adjustment in the Pacific Basin” held at the Federal Reserve Bank of San Francisco on September 22-23, 2005, under the sponsorship of the Bank’s Center for Pacific Basin Studies. The papers are listed at the end and are available at http://www.frbsf.org/economics/conferences/0509/agenda.pdf

Reuven GlickGroup Vice PresidentInternational Research

Mark SpiegelVice PresidentInternational Researchand DirectorCenter for Pacific Basin Studies

Center for Pacific Basin Studies 2005 Annual Report

�

than foreign goods, encouraging a switch of world consumption towards U.S. goods, improvement of the trade balance, and lessening of the accumulation of foreign liabilities. Second, through the “financial chan-nel” dollar depreciation affects the dollar value of U.S. financial assets and liabilities denominated in foreign currencies.

Gourinchas and Rey argue that recent dollar depre-ciations have generated sizable capital gains and re-duced the U.S. net debt position. In particular, because approximately 70% of U.S. foreign assets are in foreign currencies, while almost all of U.S. foreign liabilities are in dollars, a dollar depreciation on balance reduces the net U.S. international debt position in dollars. In fact, because of substantial valuation effects associated with the dollar depreciations since the end of 2001, the net U.S. debt position has remained roughly constant, de-spite current account deficits in excess of 5% of GDP.

Imbalances in the Pacific Basin region are not lim-ited to international trade. For example, Japan has been running large fiscal deficits during its recent era of sluggish growth. Given the demographic complica-tions associated with the aging of the Japanese popula-tion, Japan is expected to address these fiscal imbal-

ances once its economic growth has proven to be sus-tainable. This raises the question of what a change in Japan’s fiscal policy is likely to mean for the Japanese economy and the pattern of world trade.

Nicoletta Batini, Papa N’Diaye, and Alessandro Rebucci from the International Monetary Fund (IMF) address this question using the IMF’s global econ-omy model. This model divides the world into five blocks—the U.S., Japan, emerging Asia, Europe, and the rest of the world. Batini et al. explore the implica-tions of bringing Japan’s fiscal policy back into bal-ance, both with and without accompanying structural reforms to the Japanese economy. The authors com-pare the results of three scenarios. In the first sce-nario, Japan slowly brings its government into fiscal balance but makes no other changes. In the second, Japan achieves modest productivity growth to accom-pany its fiscal adjustment. In the third, Japan achieves more rapid productivity growth but makes no explicit policy effort to reduce its fiscal budget deficits. The results for the first scenario show that the U.S. current account falls further into deficit; specifically, the de-mand for U.S. goods declines as Japan reduces its de-gree of fiscal stimulus. The other two scenarios, how-ever, demonstrate that enhanced productivity growth can accelerate the pace of fiscal adjustment without exacerbating Japan’s current account imbalance. The policy conclusion, therefore, is that Japan can regain fiscal balance without disrupting the world econo-my, provided it simultaneously pursues reforms that achieve productivity growth.

China’s trade

The U.S. bilateral trade deficit with China reached over $200 billion in 2005. Some have attributed this development to an undervalued currency that makes Chinese goods unduly cheap in world markets, such as the United States. Indeed, since 1994, China has maintained a fixed exchange rate with respect to the

Hélène Rey, Princeton University, presenting her paper, “International Financial Adjustment.”

Center for Pacific Basin Studies 2005 Annual Report

�

U.S. dollar (although a small degree of flexibility was introduced in July 2005).

Yin-Wong Cheung from U.C. Santa Cruz, Menzie Chinn from the University of Wisconsin at Madison, and Eiji Fujii of the University of Tsukuba evaluate the extent to which the renminbi might be undervalued using a variety of criteria, such as purchasing power parity calculations. Because of the vast structural changes in China over time, the calculations depend on the base period used. Cheung et al. find that some approaches imply substantial undervaluation of the renminbi, while others imply little or no undervalu-ation. China’s undervaluation appears to be driven not by competitive reductions in the nominal value of its currency, but rather by greater inflation in the mid-1990s that was not accompanied by an appreciation of the renminbi. Since the late 1990s inflation in China has been comparable to that in the U.S.

China’s accession to the World Trade Organization (WTO) in 2001 entailed several liberalization require-ments, including reductions in its tariffs and capital inflow restrictions as well as harmonization of its cor-porate tax policy on foreign and domestic firms. A year later, China took major steps toward liberalization by agreeing to form a free trade area with the ASEAN na-tions by 2012.

Mesut Saygili and Kar-yiu Wong of the University of Washington evaluate the impact of China’s acces-sion to the WTO and its formation of a free trade area with the ASEAN nations. They develop a model of trade among China, ASEAN, and the rest of the world. They then consider the impact of China’s accession to the WTO, both in isolation and accompanied by the formation of a free trade area with the ASEAN nations. They find that accession to the WTO alone would greatly increase China’s openness, as its imports in-crease and resources previously employed in import-competing industries are transferred to the production of exports. They then examine the combination of Chi-

na’s accession to the WTO and its formation of a free trade area with the ASEAN nations. They again find that China’s trade increases overall, but the pattern of trade is quite different. China’s trade with the rest of the world declines, in favor of increased trade with ASEAN. Overall, both China and the rest of the world are shown to experience modest declines in welfare as a result of the pursuit of both policies, while the ASEAN nations emerge as large winners.

Foreign reserve accumulation

The recent increase in the U.S. trade deficit has been accompanied by large buildups of holdings of U.S. securities by Asian governments. Some have sug-gested that these buildups are motivated by mercan-tilist desires to maintain export competitiveness by keeping exchange rates low; others have argued that they represent a precautionary response to the 1997 Asian financial crisis experience. Joshua Aizenman from U.C. Santa Cruz and Jaewoo Lee from the IMF use a theoretical model to identify testable differences between these two explanations. They find that the empirical patterns followed by foreign reserve build-ups have been more consistent with the precautionary

John Taylor, Stanford University, discusses his experience as Undersecretary of the Treasury for International Affairs.

Center for Pacific Basin Studies 2005 Annual Report

�0

motive hypothesis. In particular, countries with more liberal capital regimes, which would expose them to greater risk of capital outflows, holding all else equal, are shown to hold greater stocks of international re-serves.

Maturity mismatches

“Maturity mismatch,” whereby a country borrows abroad short-term, but invests the borrowed capital in long-term assets, exposes borrowing countries to sig-nificant risk. In the event of a “sudden stop,” where foreign creditors refuse to roll over these short-term obligations, a borrowing country could find itself illiq-uid, compelling it to curtail investment plans and per-haps even liquidate assets prematurely. The contention that the potential for disruptive sudden stops exists has largely been based on the observation that countries that issue short-term debt obligations often experience poorer economic performance. However, this observed correlation may simply reflect the fact that poorly per-forming economies are limited to short-term borrowing by creditors because they are expected to exhibit infe-rior performance.

To assess the role of maturity mismatches in sud-den stop crises, Hoyt Bleakley of U.C. San Diego and

Kevin Cowan of the Inter-American Development Bank use micro data for 3,000 publicly traded firms from a cross-section of 16 emerging market nations, including five in East Asia. Their sample includes firms in countries that experienced high capital ac-count volatility as well as countries that issued large volumes of short-term debt liabilities. Surprisingly, they find no statistically significant difference in the investment response of firms with high and low short-term debt obligations to changes in aggregate short-term capital flows. They do determine that firms with more short-term debt find capital outflows more cost-ly and are sometimes forced to liquidate in the wake of capital outflows, but these outflows do not dispro-portionately affect their investment behavior relative to firms with fewer short-term debt obligations.

Conference papers Aizenman, Joshua, and Jaewoo Lee. “International Reserves: Precautionary versus Mercantilist Views, Theory and Evidence.”Batini, Nicoletta, Papa N’Diaye, and Alessandro Rebucci. “The Domestic and Global Impact of Japan’s Policies for Growth.”Bleakley, Hoyt, and Kevin Cowan. “Maturity Mismatch and Financial Crises: Evidence from Emerging Market Corporations.”Cheung, Yin-Wong, Menzie D. Chinn, and Eiji Fujii. “Why the Renminbi Might Be Overvalued (But Probably Isn’t).”Gourinchas, Pierre-Olivier, and Hélène Rey. “International Financial Adjustment.”Obstfeld, Maurice, and Kenneth Rogoff. “The Unsustainable U.S. Current Account Position Revisited.”Saygili, Mesut, and Kar-yiu Wong. “Unilateral and Regional Trade Liberalization: China’s WTO Accession and FTA with ASEAN.”

J. Bradford Delong, University of California at Berkeley, Ronald McKinnon, Stanford University, and Richard Meese, Barclays Global Investments.

Center for Pacific Basin Studies 2005 Annual Report

��

Reuven GlickGroup Vice President

International Research

In 1999, eleven European countries adopted the euro as their common currency (Greece followed in 2001). This followed a long period of gradually tying their national currencies together more tightly by limiting exchange rate fluctuations among member countries, culminating in the European Monetary Union (EMU). The experience of Europe has raised the question as to whether countries in other regions of the world can and should follow a similar path towards adopting a common currency.

East Asia, with some of the most dynamically grow-ing economies in the world, has long been considered a possible candidate for a regional monetary union. This article addresses three questions that help frame the issue. First, is it desirable for East Asia to adopt a common currency like the euro? Second, does Europe’s experience provide any lessons for East Asia about how to attain a common currency? Third, how does the eco-nomic integration path that East Asia is now following differ from the path Europe followed?

Is a common currency desirable for East Asia?

Joining a monetary union can benefit a country’s economy in a number of ways. First, it eliminates ex-change rate risk with other monetary union members, which facilitates trade among them. Second, it makes price differences in member countries more transpar-ent and, therefore, sharpens competition. Third, it may

increase policy discipline; specifically, an individual country’s central bank may become more credible in its commitment to price stability by delegating authority for monetary policy to a regional central bank. Related to this third benefit, however, is the principal cost of joining a monetary union—by delegating authority for monetary policy to a regional central bank, an individual country’s central bank loses independent monetary policy control and, therefore, the ability to stabilize the economy when it is hit by a shock.

The benefits of joining a monetary union may out-weigh the cost, depending on how great the cost is. Specifically, according to the so-called optimum currency theory, the cost, or the need for independent monetary policy control, is greater when member countries are exposed to different shocks and lesser when they are exposed to the same or similar shocks. One factor that reduces the likelihood of different shocks is high trade integration among member countries. Other consid-erations, such as high labor mobility and a system of intraregional fiscal transfers, also lessen the cost.

Does East Asia satisfy the criteria for a lesser cost to joining a monetary union? Much research has explored this question, and the empirical evidence suggests that this region does, more or less. For example, as Figure 1 shows, East Asian countries do trade a lot with each other. (Note: this figure is adapted from Kawai and Motonishi 2004.) By themselves, countries within the Association of Southeast Asia Nations (ASEAN), which includes Indonesia, Malaysia, Philippines, Thailand, and several other smaller countries, do not trade much with each other; likewise, by themselves, the countries within the Newly Industrialized Economies (NIE) group-ing—Korea, Hong Kong, Taiwan, and Singapore—do not trade much with each other. But taking these emerging countries of East Asia together with China, about 40%

Does Europe’s Path to Monetary Union Provide Lessons for East Asia?

Center for Pacific Basin Studies 2005 Annual Report

��

of trade was intraregional in 2003, up from 20% in 1980. When Japan is included, more than 50% of trade is intra-regional, up from about 35% in 1980. This is comparable to the more than 60% intraregional trade within the European Union (EU).

More supporting evidence for the plausibility of an East Asian currency area comes from looking at the cor-relation of demand and supply shocks. Kwack (2004) and Zhang et al. (2004) recently applied the Blanchard-Quah methodology to identify demand and supply shocks from movements in prices and output. They find evidence of high correlations of demand and supply shocks, although the correlations for Japan and China, the two largest countries in the region, are somewhat lower. Still, in general, the correlations are not much different from those across Europe in the early 1990s (see Bayoumi and Eichengreen 1994). (It should also be noted that these correlations are partly endogenous; that is, the adoption of a monetary union of itself can lead to more trade integration which, in turn, raises the cross-correlations.)

Does Europe’s experience provide any lessons about how to get a common cur-rency?

Though East Asia has moved toward satisfying the optimal currency area criteria, the region remains very different from Europe in ways that make it difficult, if not impossible, to follow the European path. Four differences stand out.

First, East Asian economies have much less in com-mon than European nations generally do in terms of income levels, stages of development, and economic structure. The implication is that achieving any mon-etary arrangement, including a common currency, is much more difficult in East Asia.

Second, East Asia is less economically self-contained than Europe. To be sure, as economies in East Asia have developed, intraregional trade has grown—from about 20%-30% of total exports in the 1980s to about 40%-50% in 2002. But about half of the intraregional trade is trade in raw materials and intermediate components that ultimately are exported outside of the region. For example, they trade chips and hard disks, but they sell the assembled computers in the U.S. and Europe. So, in-directly and directly, East Asian countries still depend much more heavily on exports to countries outside the region. Thus, East Asia must be more concerned than Europe about exchange rate stability against currencies outside the region as well as within the region.

Third, the two regions differ in terms of interest in political integration. In Europe, a monetary union was achievable primarily because it was part of the larger process of political integration. Most European countries share a history of intellectual belief in the benefits of integration and political democracy. The experiences of World War I and II generated a desire to forge deeper political, as well as economic, links in order to prevent a recurrence of country conflicts. These political desires were indispensable for the suc-

Center for Pacific Basin Studies 2005 Annual Report

��

cess of the EMU in particular and the EU more generally. There is no apparent desire for political integration in East Asia, partly because of the great differences among those countries in terms of political systems, culture, and shared history. As a result of their own particular histories, East Asian countries remain particularly jeal-ous of their sovereignty.

The fourth difference is that, in contrast to Europe, East Asian governments appear much more suspicious of strong supranational institutions. Early on, European countries were willing to contemplate compromises of national sovereignty to achieve the goal of greater inte-gration. The European Coal and Steel Community was established way back in 1952 and was given significant power to close down segments of national steel indus-tries. Later came the European Commission, the Euro-pean Parliament (which has very considerable power to shape competition policies, social policies, and so on, for EU member states). All these institutions preceded establishment of the European Central Bank; they were indispensable to providing the popular support for del-egating monetary decisions to a common central bank. In contrast, in East Asia, sovereignty concerns have left governments reluctant to delegate significant authority to supranational bodies, at least so far.

What path is East Asia following towards greater economic integration?

It is not at all clear that East Asia is on a path to a common currency. But it is very clear that it is following a different path from Europe’s.

First, in contrast to Europe, East Asia has not pur-sued formal trade liberalization as its first priority in integrating the region’s economies. Europe pursued formal trade liberalization, first through a customs union and free trade area, well before it focused on monetary cooperation. In East Asia, formal trade liberalization has been slower to materialize. Negotiated trade agreements

generally involve only the smaller countries or bilateral agreements between a large country and a small coun-try; no broad free trade agreements have been achieved among the largest countries in the region, Japan, Korea, Taiwan, and China.

A second key difference is the timing of liberalizing capital accounts. Most European countries did not fully liberalize capital flows until the late 1980s or very early 1990s, after their domestic financial markets were well developed and the integration process was well along. In contrast, many countries in East Asia (China is a no-table exception), liberalized their capital accounts before their financial markets were well developed. This has heightened the region’s vulnerability to destabilizing capital movements, which, if not the cause of the East Asia financial crisis, were at least factors that made it worse. Clearly, capital mobility makes it difficult to sustain either a single currency peg or a common basket currency peg, which some have advocated as a useful stepping stone to an East Asian monetary union.

Third, East Asia does not appear to have an obvious candidate for an internal anchor currency for a coopera-tive exchange rate arrangement. Most successful new currencies have been started on the back of an existing currency, establishing confidence in its convertibility, thus linking the old with the new. In the approach to-wards adoption of the euro, European exchange rates were tied to an internal anchor, the deutsche mark. But the choice of an internal currency anchor is not so clear in East Asia. The yen was an obvious candidate, but Japan’s economic problems over the past decade and wide swings in the yen-dollar exchange rate have lessened its appeal. As for China, its currency is not convertible for capital account transactions and its financial system is not well developed. Moreover, East Asia’s heavy dependence on exports outside the region implies that an external currency anchor now has more merits than an internal anchor.

Center for Pacific Basin Studies 2005 Annual Report

��

Conclusion

Asia’s history and current circumstances—the dif-ferences among its countries, its dependence on extra-regional trade, its political diversity, its lack of strong collective institutions, and its capital mobility—imply that exchange rate stabilization and monetary integra-tion are unlikely in the near term. Nevertheless, East Asia is integrating through trade, even without an emphasis on formal trade liberalization agreements. Moreover, there is evidence of growing financial cooperation in the region, including the development of regional arrange-ments for providing liquidity during crises through bilateral foreign exchange swaps, regional economic surveillance discussions, and the development of re-gional bond markets. These kinds of cooperation do not yet require the same compromises of sovereignty that seem to preclude adopting a common East Asian exchange rate policy.

Finally, it must be acknowledged that the European Monetary Union and the adoption of the euro was a project that was fifty years in the making. In time, East Asia might also proceed along the same path, first with loose agreements to stabilize currencies, followed later by tighter agreements, and culminating ultimately in adoption of a common anchor—and, after that, maybe an East Asia dollar.

References [URL accessed August 2005.]

Bayoumi, Tamim, and Barry Eichengreen. 1994. “One Money or Many? Analyzing the Prospects of Monetary Unification in Various Parts of the World.” Princeton Studies in International Finance No. 76.

Kawai, Masahiro, and Taizo Motonishi. 2004. “Is East Asia an Optimum Currency Area?” Paper delivered at the conference on Financial Interdependence and Exchange Rate Regimes in East Asia sponsored by the Japan Ministry of Finance Policy Research Institute, December 2-3, 2004. http://www.mof.go.jp/english/soken/kiep2005/kiep2005_04.pdf

Kwack, Sung Yeung. 2004. “An Optimum Currency Area in East Asia: Feasibility, Coordination, and Lead-ership.” Journal of Asian Economics 15(1) (February) pp. 153-169.

Zhang, Zhaoyong, Kiyotaka Sato, and Michael McAleer. 2004. “Is a Monetary Union Feasible for East Asia?” Applied Economics 36(10) (June) pp. 1031-1043.

Center for Pacific Basin Studies 2005 Annual Report

��

Mark SpiegelVice President

International Researchand Director

Center for Pacific Basin Studies

On July 21, 2005, after more than a decade of strictly pegging the renminbi to the U.S. dollar at an exchange rate of 8.28, the People’s Bank of China (PBOC 2005a) announced a revaluation of the currency and a reform of the exchange rate regime. The revaluation puts the renminbi at 8.11 against the dollar, which amounts to an appreciation of 2.1%. Under the reform, the PBOC will incorporate a “reference basket” of currencies when choosing its target for the renminbi.

The announcement stated that the changes were made “[w]ith a view to establish and improve the social-ist market economic system in China, enable the market to fully play its role in resource allocation as well as to put in place and further strengthen the managed float-ing exchange rate regime based on market supply and demand.” However, the announcement and subsequent clarifications leave the PBOC with considerable discre-tion over its renminbi target.

In this article, I review several characteristics of the new renminbi regime. I also examine how the renminbi might have moved in the past if this regime had been in place. Because the PBOC provided only guidelines, and not specifics, about the composition and trade weights of the reference basket, I construct three likely indexes and compare their movements with each other and with the bilateral renminbi-U.S. dollar exchange rate. I find that movements in China’s trade-weighted exchange rate indexes over the long term are relatively insensitive

A Look at China’s New Exchange Rate Regime

to currency composition; moreover, when viewed over the previous four to five years, all three indexes exhibit appreciation against the dollar far exceeding the initial 2.1% renminbi revaluation.

The new renminbi regime

According to the July 21 announcement, each day the PBOC will announce its target for the following working day based on that day’s renminbi closing price in terms of a “central parity.” For example, the target may be expressed in terms of the value of the renminbi against the dollar. The following day, the renminbi exchange rate will be allowed to fluctuate against the dollar within a band of plus or minus 0.3% around the announced central parity.

Figure 1 shows the market reaction to the announce-ment by graphing the daily closing values of the ren-

Center for Pacific Basin Studies 2005 Annual Report

��

minbi-dollar exchange rate and the two-month renminbi non-deliverable forward (NDF) rates around the time of the revaluation. Although these forward contracts consti-tute a relatively thin market, they can be considered the best indicator available of the market’s beliefs about the future path of the renminbi-dollar exchange rate. At the end of July 21, the market anticipated further renminbi appreciation, as the two-month NDF renminbi-dollar exchange rates stood below 8 renminbi per dollar.

The apparent market anticipation of additional ap-preciation of the renminbi prompted the PBOC to issue a series of clarifications stating that the initial revalua-tion did not imply further action. The market responded again, as shown by the upward movement in the two-month NDF rate on July 22, but still stood below the current stated peg of 8.11.

Trade-weighted renminbi reference indexes

In a speech on August 10 (PBOC 2005b), the Governor of the PBOC clarified the new exchange rate regime and the components of China’s “reference basket.” He stated that assigned index weights will be selected “…in line with the real situation of China’s external sector devel-opment,” and that “…the basket should be composed of currencies of the countries to which China has a promi-nent exposure in terms of foreign trade, external debt, and foreign direct investment.” Clearly, then, the PBOC has not made any commitment to follow rigidly a trade-weighted currency index peg. However, the Governor did give some guidelines on the country composition of China’s currency basket. Specifically, he suggested that countries whose bilateral trade with China exceeded $10 billion would receive non-negligible weights, and those exceeding $5 billion in total weight would also be considered.

Because the PBOC has not announced the relative weights to be placed on the components of the basket, nor has it made any commitment to keep these weights constant over time, it is impossible to track movements

in an official Chinese trade-weighted currency index. However, using the guidelines, I can construct hypo-thetical but likely indexes and examine what the path of the renminbi-dollar exchange rate would have been since January 2001, if the exchange rate had been rigidly pegged to one of these indexes. According to the IMF Direction of Trade Statistics, 15 economies (excluding Hong Kong) had total trade (exports plus imports) exceeding $10 billion for the year in 2004, which ac-counted for 66% of China’s total trade; 22 countries (again, excluding Hong Kong) had total trade exceeding $5 billion for the year in 2004, which accounted for 69% of China’s total trade. I therefore construct a “narrow” trade-weighted index for China based on trade shares of the 15 countries with trade exceeding $10 billion an-nually, and a “broad” trade-weighted index based on trade shares of the 22 countries with total trade levels exceeding $5 billion in total trade with China. This number is similar to the 23 countries in the European Central Bank’s calculation of the euro area nominal ef-fective exchange rate index.

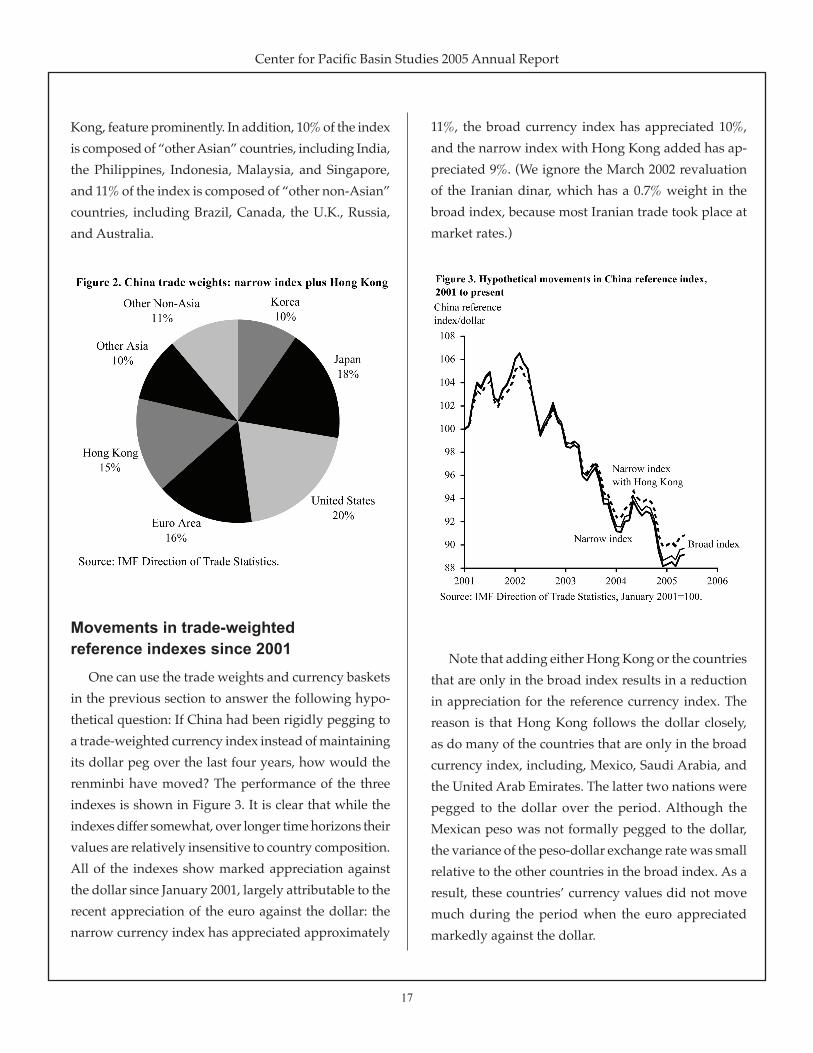

The Governor’s speech did not discuss the inclusion or exclusion of Hong Kong in the currency index, prob-ably because of Hong Kong’s unique political relation-ship with the rest of China. However, the inclusion or exclusion of Hong Kong in a trade-weighted currency index for China could have important implications for two reasons: First, Hong Kong is an important trade partner for China, accounting for 11.7% of total Chinese trade in 2004; second, Hong Kong’s exchange rate is closely pegged to the U.S. dollar, implying that adding the Hong Kong dollar to a trade-weighted currency index would diminish the volatility of the index rela-tive to the U.S. dollar. Based on these considerations, I construct a third index composed of the 15 countries in the narrow index plus Hong Kong.

Trade shares for the third index are shown in Figure 2; by construction China’s main trading partners, the United States, the euro area, Japan, Korea and Hong

Center for Pacific Basin Studies 2005 Annual Report

��

Kong, feature prominently. In addition, 10% of the index is composed of “other Asian” countries, including India, the Philippines, Indonesia, Malaysia, and Singapore, and 11% of the index is composed of “other non-Asian” countries, including Brazil, Canada, the U.K., Russia, and Australia.

Movements in trade-weighted reference indexes since 2001

One can use the trade weights and currency baskets in the previous section to answer the following hypo-thetical question: If China had been rigidly pegging to a trade-weighted currency index instead of maintaining its dollar peg over the last four years, how would the renminbi have moved? The performance of the three indexes is shown in Figure 3. It is clear that while the indexes differ somewhat, over longer time horizons their values are relatively insensitive to country composition. All of the indexes show marked appreciation against the dollar since January 2001, largely attributable to the recent appreciation of the euro against the dollar: the narrow currency index has appreciated approximately

11%, the broad currency index has appreciated 10%, and the narrow index with Hong Kong added has ap-preciated 9%. (We ignore the March 2002 revaluation of the Iranian dinar, which has a 0.7% weight in the broad index, because most Iranian trade took place at market rates.)

Note that adding either Hong Kong or the countries that are only in the broad index results in a reduction in appreciation for the reference currency index. The reason is that Hong Kong follows the dollar closely, as do many of the countries that are only in the broad currency index, including, Mexico, Saudi Arabia, and the United Arab Emirates. The latter two nations were pegged to the dollar over the period. Although the Mexican peso was not formally pegged to the dollar, the variance of the peso-dollar exchange rate was small relative to the other countries in the broad index. As a result, these countries’ currency values did not move much during the period when the euro appreciated markedly against the dollar.

Center for Pacific Basin Studies 2005 Annual Report

��

Caveats

First, the indexes generated are, at best, guesses about the reference trade-weighted currency index China may use. The PBOC has made no commitment to follow such a trade-weighted index peg rigidly, stating that other cur-rent account considerations, such as the share of major currencies in foreign debt and foreign direct investment will also be considered. As such, the movements in the currency index would not necessarily be representative of the desired path for the renminbi under China’s new exchange rate regime, even if the country weights as-signed to the index were appropriate.

Second, it would be inaccurate to argue that the historical movements in the trade-weighted currency index are representative of how the renminbi would have moved over its fixed exchange rate period were it follow-ing such an index. The reason is that, while China’s Asian trading partners are weighted significantly in China’s trade-weighted index, China is also an important trade partner for them. Therefore, Chinese exchange rate policy is likely to influence the path of many Asian exchange rates. Indeed, McKinnon (2005) has recently argued that a number of China’s main Asian trading partners have smoothed their dollar exchange rates in an effort to retain competitiveness against China.

Finally, while it is clear that all of the indexes exhib-ited appreciation over the sample period far exceeding the 2.1% appreciation of the renminbi on July 21, this study does not imply anything about whether or not the renminbi is “undervalued.” In particular, the study is silent on the relative under- or over-valuation of the renminbi on the sample starting date in 2001.

References [URL accessed September 2005.]

McKinnon, Ronald I. 2005. Exchange Rates under the East Asian Dollar Standard. Cambridge, MA: MIT Press.

People’s Bank of China. 2005a. “Public Announce-ment of the People’s Bank of China on Reforming the RMB Exchange Rate Regime,” July 21.People’s Bank of China. 2005b. “Speech of Governor Zhou Xiaochuan at the Inauguration Ceremony of the People’s Bank of China Shanghai Head Office,” August 10. http://www.pbc.gov.cn/english/detail.asp?col=6500&id=82

Center for Pacific Basin Studies 2005 Annual Report

��

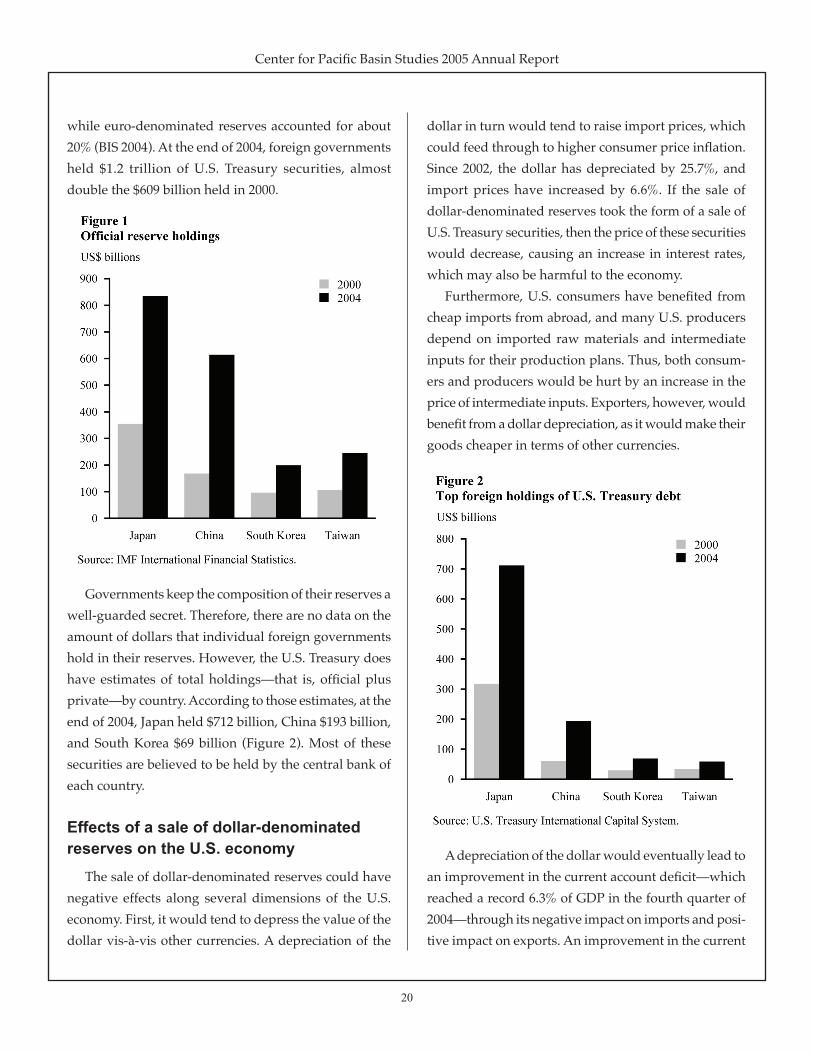

of the major uses of foreign exchange reserves is to intervene in the foreign exchange market in order to influence the value of the domestic currency and to serve as collateral for foreign borrowing. Suppose, for example, that a country wants to see the value of its currency depreciate, so that the cost of its exports will be relatively lower and therefore more attractive to foreign buyers. The government would then buy foreign-de-nominated securities and pay for them with domestic currency, thus leading the domestic currency to depre-ciate. Governments may also intervene in the foreign exchange market to keep the local currency stable rela-tive to another currency in order to reduce the risk of exchange rate fluctuations. By reducing exchange rate risk, foreign governments may promote greater foreign trade and financial flows. A more dramatic use of for-eign reserves may occur when the domestic currency is under a speculative “attack.” Reserves can be used as a “war chest” to defend the local currency and, by extension, the domestic financial systems, in case of future runs on their currency. Following the 1997-1998 Asian financial crises, many East Asian governments moved to accumulate large amounts of reserves to serve as collateral for their domestic financial systems and prevent future currency crises (Figure 1). At the end of 2004, South Korea held over $200 billion in reserves, more than twice the level it held in 2000.

Total worldwide foreign reserves holdings reached $3 trillion at the end of 2004, up from $2.4 trillion in 2003, with the largest holders being Japan, at $834 bil-lion, and China, at $615 billion. Most foreign exchange reserves are held in the form of dollar-denominated securities; one reason for this is that foreign govern-ments like the highly liquid market for U.S. Treasury securities. As of December 2003, dollar-denominated securities accounted for roughly 70% of total reserves,

What If Foreign Governments Diversified Their Reserves?

Diego ValderramaEconomist

World financial markets paid close attention when officials from both South Korea and Japan said that their governments were considering diversifying their hold-ings of foreign reserves (Dougherty 2005 and Koizumi 2005). Many analysts thought these announcements were partly in response to the past depreciation of the dollar; if true, then it seemed likely that those two governments would sell some of their dollar-denominated assets, put-ting further downward pressure on the dollar.

Since then, officials in both countries have insisted that they were not considering any major changes to the policy of reserve holdings. Nonetheless, the potential for a sell-off of dollar-denominated assets by foreign govern-ments has raised some questions about the consequences of such a move. This article attempts to put these issues into perspective. It begins with a review of recent trends in the holdings of such assets by foreign governments and a description of how these governments use them. Then it explores some of the risks the U.S. economy might face if foreign governments sold off large quantities of their dollar-denominated reserves. It concludes with a discussion of some of the costs such a sell-off would pose to foreign countries themselves.

Recent trends in holdings of foreign exchange reserves and how they are used

Foreign exchange reserves are holdings of foreign-denominated securities by foreign governments. One

Center for Pacific Basin Studies 2005 Annual Report

�0

while euro-denominated reserves accounted for about 20% (BIS 2004). At the end of 2004, foreign governments held $1.2 trillion of U.S. Treasury securities, almost double the $609 billion held in 2000.

Governments keep the composition of their reserves a well-guarded secret. Therefore, there are no data on the amount of dollars that individual foreign governments hold in their reserves. However, the U.S. Treasury does have estimates of total holdings—that is, official plus private—by country. According to those estimates, at the end of 2004, Japan held $712 billion, China $193 billion, and South Korea $69 billion (Figure 2). Most of these securities are believed to be held by the central bank of each country.

Effects of a sale of dollar-denominated reserves on the U.S. economy

The sale of dollar-denominated reserves could have negative effects along several dimensions of the U.S. economy. First, it would tend to depress the value of the dollar vis-à-vis other currencies. A depreciation of the

dollar in turn would tend to raise import prices, which could feed through to higher consumer price inflation. Since 2002, the dollar has depreciated by 25.7%, and import prices have increased by 6.6%. If the sale of dollar-denominated reserves took the form of a sale of U.S. Treasury securities, then the price of these securities would decrease, causing an increase in interest rates, which may also be harmful to the economy.

Furthermore, U.S. consumers have benefited from cheap imports from abroad, and many U.S. producers depend on imported raw materials and intermediate inputs for their production plans. Thus, both consum-ers and producers would be hurt by an increase in the price of intermediate inputs. Exporters, however, would benefit from a dollar depreciation, as it would make their goods cheaper in terms of other currencies.

A depreciation of the dollar would eventually lead to an improvement in the current account deficit—which reached a record 6.3% of GDP in the fourth quarter of 2004—through its negative impact on imports and posi-tive impact on exports. An improvement in the current

Center for Pacific Basin Studies 2005 Annual Report

��

account would reduce the amount of additional external borrowing needed to finance this deficit. However, a rapid reversal of the current account may be disruptive to the U.S. economy, as either investment or consumption, or both, would need to contract to close the current account gap (for the argument, see Setser and Roubini 2005).

Diversifying reserves without selling dollar-denominated assets

One source of information on whether there are any instances of diversifying reserves without selling dollar-denominated assets comes from the Bank for Interna-tional Settlements (BIS). The BIS (2005) reports data on the currency composition of deposits of BIS-reporting banks. These deposits include some foreign exchange reserves held outside the home country.

Figure 3 shows that banks in South Korea, Taiwan, and particularly China, have increased the amount of dollar deposits they hold, including holdings of reserves between 2000 and 2004. This is consistent with the data presented previously on the increase of reserves by foreign central banks and the predominance of the dollar as a currency of reserve. Figure 4 shows that while the fraction of dollar-denominated deposits in South Korea and Taiwan has remained mostly stable between 2000 and 2004, China has slowly diversified its holdings away from the dollar during this period. The fact that China increased its total holdings indi-cates that a diversification away from the dollar does not necessarily imply that central banks will sell their dollar-denominated assets. Foreign governments may be able to achieve diversification by purchasing larger amounts of securities denominated in other currencies in the future instead of by selling current holdings of dollar-denominated assets. For example, it is possible that the euro will grow in importance as an international reserve currency as the European Central Bank cements its low-inflation performance and as the euro financial market develops.

A sale of dollar-denominated reserves may be costly to foreign economies

In many Asian countries, economic growth has been led by the export sector, which would be hurt by an appreciation of the local currency vis-à-vis the dollar. In fact, the economies of Japan and South Korea would grow more slowly were it not for their dynamic export sectors. Thus, a significant move away from dollar-denominated reserves would entail significant costs to foreign economies.

A sale of dollar-denominated assets that leads to a large depreciation of the dollar would generate large capital losses for foreign governments, as the value of their assets would drop with respect to their domestic currency. On the other hand, since the United States borrows internationally mostly in terms of dollars and since most of its foreign assets are denominated in foreign currencies, it would receive most of the capital gains, as the value of its liabilities would drop relative to the value of its assets. Tille (2005) estimates that a 10% depreciation of the dollar leads to a valuation loss for foreign economies equivalent to about 4% of U.S. GDP.

Center for Pacific Basin Studies 2005 Annual Report

��

Conclusions

This article posed the question: What if foreign central banks diversified their reserves? The answer has several dimensions. A sale of dollar-denominated reserves would depress the value of the dollar vis-à-vis other currencies, thus raising import prices for U.S. consumers and feeding into higher consumer price inflation. If the depreciation is sudden and leads to a rapid reversal of the current account, it may depress investment and consumption. However, a sale of dollar-denominated securities would also be costly to foreign economies. Foreign governments would be exposed to large capital losses, and an appreciation of their curren-cies would make their exports less competitive. Finally, the case of China makes it clear that if foreign govern-ments want to diversify their holdings of reserves, they can do so not only by selling dollar-denominated secu-rities but also by buying into securities denominated in other currencies.

References [URLs accessed July 2005.]

Bank for International Settlements. 2004. Annual Report. http://www.bis.org/publ/ar2004e.htm

Bank for International Settlements. 2005. BIS Quar-terly Review (March). http://www.bis.org/publ/r_qt0503.htm

Dougherty, Carter. 2005. “Dollar Plunges on Proposal by Korea Bank to Diversify.” New York Times (Febru-ary 23, 2005) sec. C, p. 12, col. 5, national edition.

Koizumi, Junichiro. 2005. Remarks before Japanese Parliament, March 10, 2005.

Setser, Brad, and Nouriel Roubini. 2005. “How Scary Is the Deficit?” Foreign Affairs. (July/August) pp. 194-200.

Tille, Cédric. 2005. “Financial Integration and the Wealth Effect of Exchange Rate Fluctuations.” Mimeo. FRB New York.

Center for Pacific Basin Studies 2005 Annual Report

��

economies may prefer to keep the exchange rate fixed, at least in the short run, to mitigate the costs arising from exchange rate adjustment.

Balance sheet effects

Episodes of large exchange rate adjustments in emerging market economies during the 1990s were characterized by widespread defaults by domestic firms and output contractions. This led many researchers to evaluate how financial conditions affect the impact of exchange rate adjustments on aggregate economic activity.

Financial conditions can influence aggregate de-mand through balance sheet effects on borrowing and investment expenditure. These effects occur when the interest rate at which firms borrow from financial inter-mediaries to finance investment depends on the level of net worth, which is essentially a firm’s gross value of as-sets net of liabilities. Firms with a lower net worth tend to finance a greater share of their investment through debt. Since these firms will be more leveraged, they are less likely to meet their loan obligations in the event of some negative shock to their activity. Consequently, to compensate for the greater expected likelihood of default, lenders will charge these firms a higher risk premium. Therefore, a lower net worth, through an increase in the risk premium, leads to a higher cost of borrowing that, in turn, reduces investment.

When external liabilities are denominated in foreign currencies, as is the case for almost all emerging mar-ket economies, exchange rate depreciation may have negative balance sheet effects. Since domestic firms typically earn their revenues in their domestic currency, depreciation makes these revenues worth less in terms of foreign currency, thereby reducing their capacity to

To Float or Not to Float? Exchange Rate Regimes and Shocks

Michele CavalloEconomist

Many economists argue that a flexible exchange rate regime is preferable to a fixed exchange rate regime because it helps to insulate the domestic economy from adverse external shocks. For example, when export demand declines, a depreciation makes domestic goods more competitive abroad, stimulates an offsetting ex-pansion in demand, and dampens the contraction in domestic economic activity.

In reality, however, exchange rate depreciations in many emerging market economies over the past decade typically have been associated with financial distress and output contractions. Consequently, recent research has reconsidered the stabilization properties of a flexible exchange rate regime when exchange rate movements affect financial conditions, and these, in turn, influence economic activity.

This article summarizes some of the findings of these studies and their policy prescriptions for the choice of the exchange rate regime. Some studies find that, in spite of the adverse impact of changing exchange rates on financial conditions and aggregate economic activity, a flexible exchange rate regime is still preferable. Yet, this is difficult to reconcile with the observation that many emerging market economies prefer to avoid exchange rate adjustments. Other studies explain this behavior by showing how changing exchange rates can produce severe financial distress that, in turn, leads to a net loss of wealth. This mechanism explains why emerging market

Center for Pacific Basin Studies 2005 Annual Report

��

service foreign currency debt. The associated reduction in net worth generates an increase in the risk premium on borrowing that dampens investment expenditure and aggregate demand. Therefore, the interaction of balance sheet effects and foreign currency denomination of liabilities can lead exchange rate depreciations to be contractionary and render flexible exchange rate regimes less attractive.

The question is: Are these balance sheet effects large enough to make policymakers prefer a fixed exchange rate regime? Céspedes, Chang, and Velasco (2004) and Gertler, Gilchrist, and Natalucci (2003) address this ques-tion by analyzing the reaction of an emerging market model economy to an adverse external shock, such as an increase in the foreign interest rate. These studies conclude that, even in the presence of balance sheet ef-fects, flexible exchange rates still provide more output stabilization in response to a negative external shock.

For example, consider the effect of an increase in the foreign interest rate above the domestic interest rate. Under flexible exchange rates, this induces a financial outflow and a depreciation of the domestic currency. With liabilities denominated in foreign currency, this channel produces a decrease in net worth. However, there are also positive consequences from the asset side of firms’ balance sheets. Because the depreciation makes domestic goods relatively cheaper, export revenue rises, creating a positive impact on net worth. If this positive effect dominates and net worth rises, the overall effect of depreciation need not be contractionary.

Alternatively, under fixed exchange rates, the central bank must raise the domestic interest rate to match the increase in the foreign interest rate so as to prevent the domestic currency from depreciating. This interest rate rise leads to a decrease in a firm’s net worth because future revenues are worth less in current value terms. As net worth shrinks, the risk premium rises, inducing a contraction in investment spending and output. There-fore, under fixed exchange rates, balance sheet effects

exacerbate the contractionary effects of an increase in the foreign interest rate on investment, aggregate demand, and output.

Some stylized facts

Despite these theoretical arguments in favor of a floating exchange rate policy, many emerging market economies appear averse to exchange rate adjustments. Calvo and Reinhart (2002), notably, report evidence of widespread fear of large exchange rate adjustment in emerging market economies. In addition, Hausmann, Panizza, and Stein (2001) find that this is particularly so for countries that borrow heavily abroad in foreign currency, as they are exposed to the potential for balance sheet deterioration.

Cavallo et al. (2004) find that balance sheet effects are, in fact, at the root of the output contraction in the

Center for Pacific Basin Studies 2005 Annual Report

��

aftermath of an exchange rate adjustment. As shown in Figure 1, they detect a positive relation between the severity of output contractions and an index of intensity of balance sheet effects, where the latter is measured by the product of total real exchange rate (REER) depre-ciation and the ratio of net foreign currency liabilities to output. In addition, they observe that many of the recent exchange rate adjustment episodes in emerging market economies have been characterized by exchange rate overshooting; that is, the degree of exchange rate depreciation in the short run was considerably larger than in the long run. Cavallo et al. (2004) also find that exchange rate overshooting is greater the higher is the ratio of foreign currency debt to GDP, as Figure 2 indicates.

Which exchange rate policy?

Cavallo et al. (2004) formulate a model that relates these stylized facts by recognizing one additional feature of most recent episodes of exchange rate adjustment in emerging market economies; specifically, these countries

also experienced a decline in the confidence of foreign investors that sharply curbed their ability to borrow from abroad.

In their model, exchange rate depreciation produces negative balance sheet effects that interact with the reduced ability to borrow abroad, which, in turn, gen-erates the need to reduce external indebtedness even further. This can be achieved through two channels: reducing imports of foreign goods and selling equity claims in domestic firms to foreign investors. Each channel of adjustment has further effects. The drop in imports induces a further depreciation of the exchange rate that results in exchange rate overshooting, while the sale of domestic assets prompts a decline in do-mestic equity prices (see Aguiar and Gopinath 2005 for evidence on East Asian countries during the late 1990s). Both effects are stronger when the exposure to foreign currency liabilities is larger, as any depreciation creates a greater need to reduce external indebtedness. In addition, they magnify the costs of exchange rate depreciation: exchange rate overshooting interacts with sizable foreign currency liabilities and exacerbates the adverse balance sheet effect of depreciation on output, while the sale of domestic assets at a discount implies a net loss of wealth that permanently affects domestic consumption.

Preventing exchange rate depreciation avoids the negative balance sheet effects and lessens the need to sell off domestic equity assets, but at the cost of mak-ing domestic goods less competitive. This hampers aggregate demand and depresses domestic output. For this reason, as other studies have concluded, a regime of flexible exchange rates may in fact dominate in the long run. In the short run, however, matters can be quite different: in the face of a sharp reduction in the ability to borrow externally, keeping the exchange rate fixed mitigates the disruption caused by the necessary sales of domestic equity assets and the resulting loss of wealth, so that, in this case fixed exchange rates dominate.

Center for Pacific Basin Studies 2005 Annual Report

��

Conclusions

In answer to the question posed in the title, “to float or not to float,” the evidence and the models discussed in this article point to the relevance of foreign currency liabilities in choosing the appropriate exchange rate policies in response to adverse external shocks. Specifi-cally, recent research has found that, even when finan-cial conditions influence aggregate economic activity, flexible exchange rates can be more desirable than fixed exchange rates as a tool to deal with adverse external shocks. However, in emerging market economies these shocks often involve temporarily reduced access to international financial markets. Under such scenarios, a policy of flexible exchange rates can lead to substan-tial costs. Conversely, a policy of fixed exchange rates dampens these costs, and, at least in the short run, can be preferred to an exchange rate adjustment.

References

Aguiar, Mark, and Gita Gopinath. 2005. “Fire-sale FDI and Liquidity Crises.” Review of Economics and Statistics, forthcoming.

Calvo, Guillermo A., and Carmen M. Reinhart. 2002. “Fear of Floating.” Quarterly Journal of Economics 117 (May) pp. 379-408.

Cavallo, Michele, Kate Kisselev, Fabrizio Perri, and Nouriel Roubini. 2004. “Exchange Rate Overshooting and the Costs of Floating.” Mimeo. New York University.

Céspedes, Luis Felipe, Roberto Chang, and Andrés Velasco. 2004. “Balance Sheets and Exchange Rate Policy.” American Economic Review 94 (September) pp. 1183-1193.

Gertler, Mark, Simon Gilchrist, and Fabio M. Natalucci. 2003. “External Constraints on Monetary Policy and the Financial Accelerator.” NBER Working Paper no. 10128. http://papers.nber.org/papers/w10128.pdf

Hausmann, Ricardo, Ugo Panizza, and Ernesto Stein. 2001. “Why Do Countries Float the Way They Float?” Journal of Development Economics 66 (December) pp. 387-414.

Center for Pacific Basin Studies 2005 Annual Report

��

Other Programs

Symposium on “The Revived Bretton Woods System: A New Paradigm for Asian Development?”

The U.S. current account balance has deteriorated significantly over the last fifteen years. In 1991, it was in surplus. Since then, it has swelled to a deficit that in 2005 equaled more than 6 percent of GDP, the highest such ratio in at least 40 years. Some argue that the U.S. trade patterns are overdue for adjustment, which may be accompanied by a fall in the value of the dollar.

This position has been contested by a group of econo-mists who argue that the current pattern is caused by unique conditions, and that continued large U.S. trade deficits need not necessarily lead to a large dollar de-valuation. Instead, they envision an environment where the large U.S. current account deficit can continue to be financed by accumulation of dollar reserves by foreign governments, particularly those in Asia. They argue that Asian governments will be willing to accumulate ever-increasing stocks of U.S. Treasuries in order to maintain export growth in an informal arrangement that mirrors the Bretton Woods system of fixed exchange rates that prevailed internationally in the mid-twentieth century.