RUSSIA Author: Simone Tremonte Market research:

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

RUSSIA

Author: Simone Tremonte

Market research:

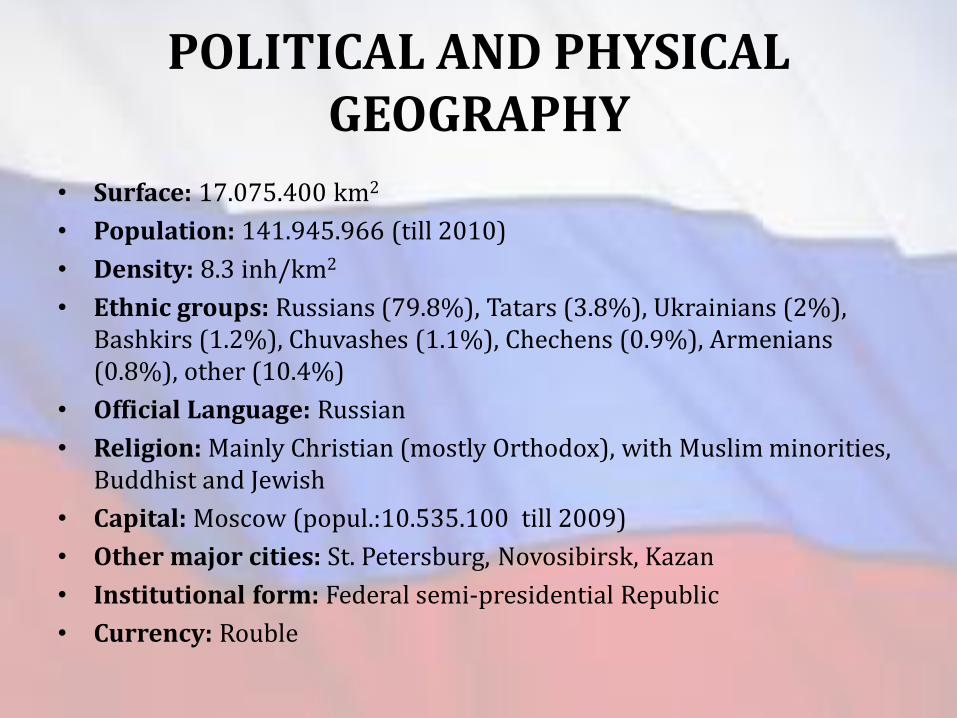

POLITICAL AND PHYSICAL GEOGRAPHY

• Surface: 17.075.400 km2

• Population: 141.945.966 (till 2010)

• Density: 8.3 inh/km2

• Ethnic groups: Russians (79.8%), Tatars (3.8%), Ukrainians (2%), Bashkirs (1.2%), Chuvashes (1.1%), Chechens (0.9%), Armenians (0.8%), other (10.4%)

• Official Language: Russian

• Religion: Mainly Christian (mostly Orthodox), with Muslim minorities, Buddhist and Jewish

• Capital: Moscow (popul.:10.535.100 till 2009)

• Other major cities: St. Petersburg, Novosibirsk, Kazan

• Institutional form: Federal semi-presidential Republic

• Currency: Rouble

SHORT HISTORICAL BACKGROUND

• Early periods: VIII century

Novgorod Republic

• 882 – 1054: Kievan Rus‘

• 1054 – 1245: Setting-up of further Principalties (Basis of the modern Russia)

• Grand Duchy of Moscow:

1245 – 1380: Mongol supremacy

1380 – 1478: Moscow dominion under Ivan III (The Great)

1478: Indipendence under the Moscow supremacy

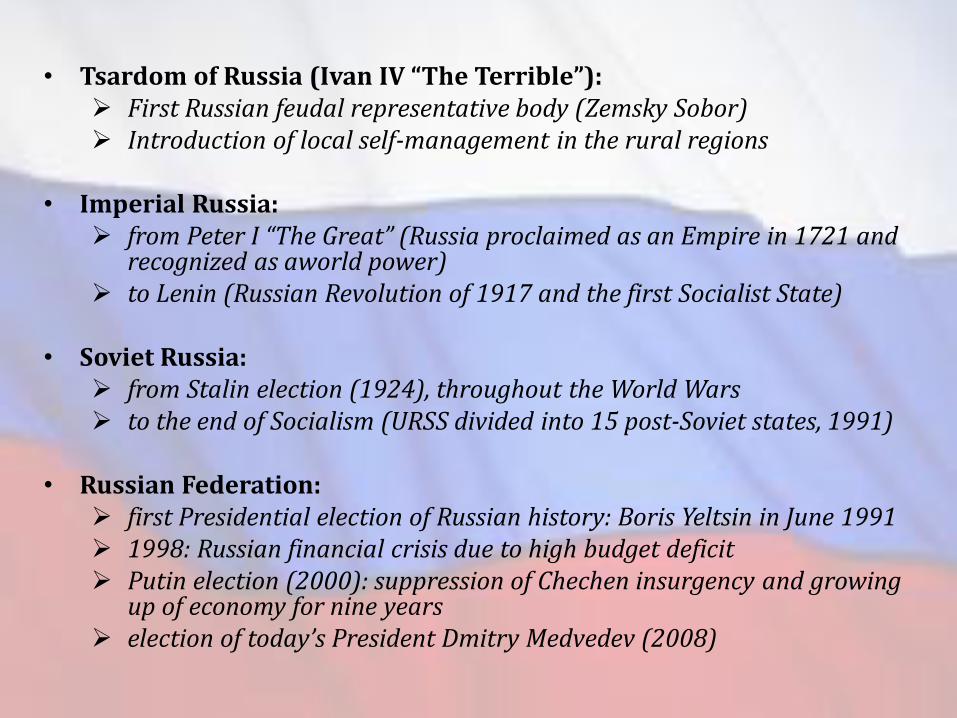

• Tsardom of Russia (Ivan IV “The Terrible”): First Russian feudal representative body (Zemsky Sobor) Introduction of local self-management in the rural regions

• Imperial Russia:

from Peter I “The Great” (Russia proclaimed as an Empire in 1721 and recognized as aworld power)

to Lenin (Russian Revolution of 1917 and the first Socialist State) • Soviet Russia:

from Stalin election (1924), throughout the World Wars to the end of Socialism (URSS divided into 15 post-Soviet states, 1991)

• Russian Federation:

first Presidential election of Russian history: Boris Yeltsin in June 1991 1998: Russian financial crisis due to high budget deficit Putin election (2000): suppression of Chechen insurgency and growing

up of economy for nine years election of today’s President Dmitry Medvedev (2008)

GOVERNMENT AND POLITICS

• Government: Federal semi-presidential republic

• President: Dmitry Medvedev

• Prime Minister: Vladimir Putin (Independent, but leader of

UR)

• Chairman of the Federation Council: Sergey Mironov (FR)

• Chairman of the State Duma: Boris Gryzlov (UR)

• Legislature: Federal Assembly

• Upper House: Federation Council

• Lower House: State Duma

Main information till April 2010

• Russia is in a phase of slow rising in updating military and economic

power , inside the country and all over the world

this requires:

stability in political and economic relations with Europe

• April 2010: strategic nuclear arms treaty START 2

normalization of relations between the USA and Russia

IMPORTANT:

Relations with China: opportunities for energy trade and already become the biggest market for Russian imports

Consolidation of trade power in world strategic sector

(production and sale of gold, uranium, and export of arms) Source: PROMEC

MACROECONOMICS DATA

Source: CISSTAT

General economic sight

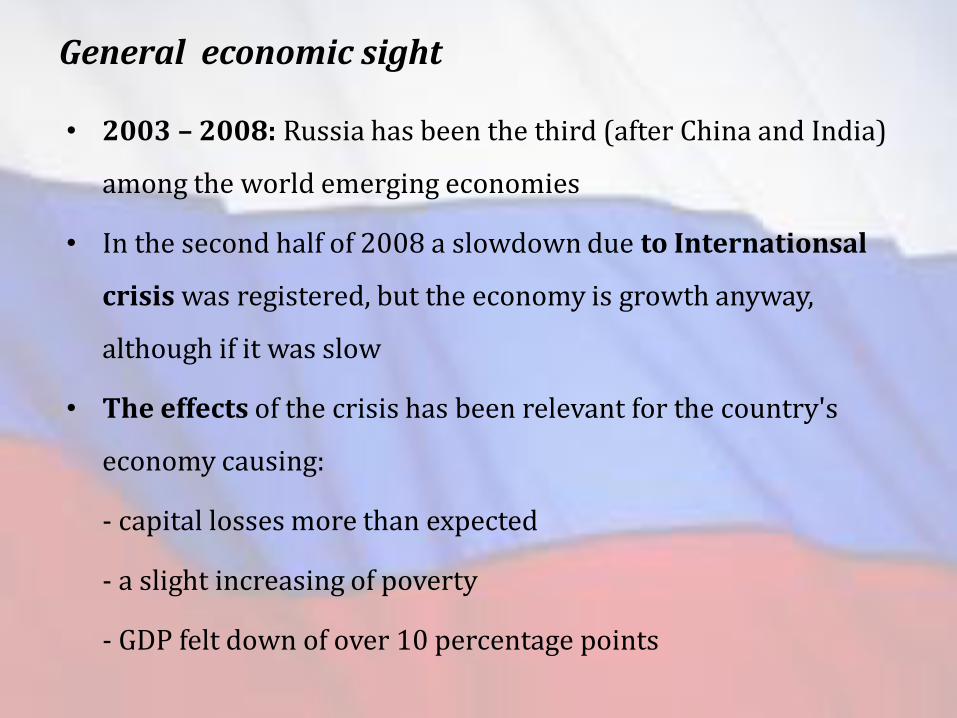

• 2003 – 2008: Russia has been the third (after China and India)

among the world emerging economies

• In the second half of 2008 a slowdown due to Internationsal

crisis was registered, but the economy is growth anyway,

although if it was slow

• The effects of the crisis has been relevant for the country's

economy causing:

- capital losses more than expected

- a slight increasing of poverty

- GDP felt down of over 10 percentage points

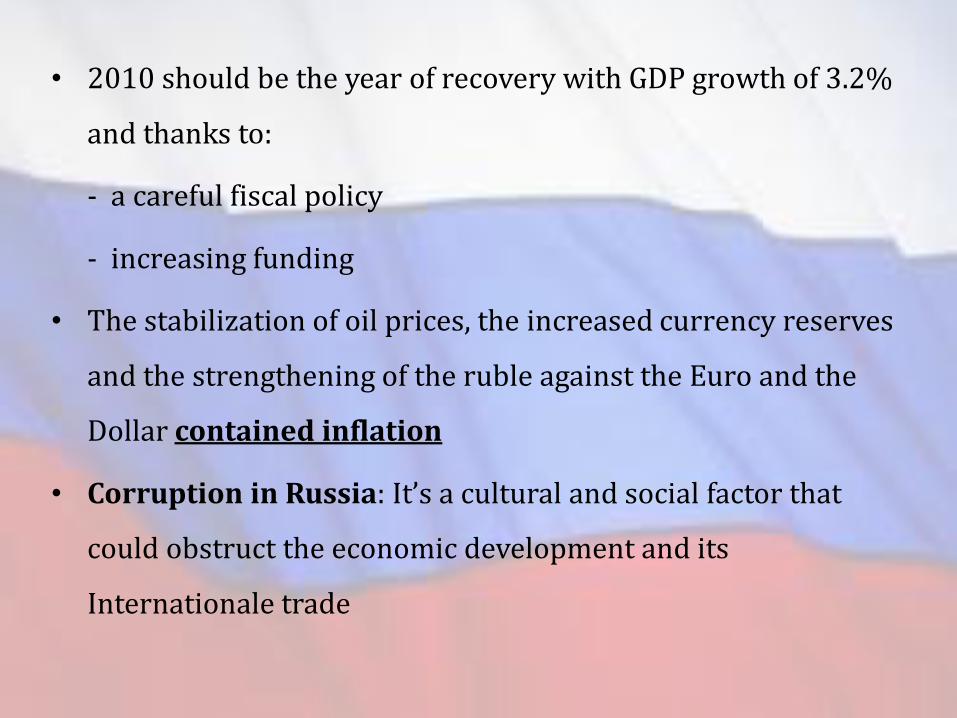

• 2010 should be the year of recovery with GDP growth of 3.2%

and thanks to:

- a careful fiscal policy

- increasing funding

• The stabilization of oil prices, the increased currency reserves

and the strengthening of the ruble against the Euro and the

Dollar contained inflation

• Corruption in Russia: It’s a cultural and social factor that

could obstruct the economic development and its

Internationale trade

Main productive sectors

Mining and extraction of oil (-3.6%), production and distribution of

electricity, gas and water (-6%), manufacturing (-21.1%), construction

(-20.7%), retail and wholesale (-6.2%), financial services (-2.5%),

agriculture (-2.1%), food industry (-2%), carbon-coke production and

petrochemicals (-1.3%), leather goods and footwear (-5.5%), chemical

industry (-13%), plastics (-14.6%), textiles and clothing (-20.7%), metal

industry (-23.1%), wood industry (-23.1%). Despite the declines seen

during the 2009, all sectors show, now in recovery. The crisis remains,

however, for sectors such as transport, in particularly automotive,

mechanical and electrotechnical industry (-31.7%), optical (-36.1%)

Source: ASSOCAMERESTERO Data are referred to the first nine months of 2009

IMPORT-EXPORT

• According to data released by the Federal Customs Service in 2009, the

interchange trade with the rest of the world total has decreased in

36.2% compared to 2008 (source: ICE)

Total imports: mld / e 143.2

Total exports: mld / e 215.1

Main imported products: transport equipment, machinery and

plants(50%)

Main exports: oil, gas, raw materials

Main trading partners

Customers countries: Netherlands (12.2%), Italy (9%), Germany (6.9%),

Turkey (5.9%), Ukraine (5%), China (4.5%), Poland (4.3%)

Related countries: China (12.9%), Germany (12.6%), Japan (6.9%),

Ukraine (6%), USA (5.1%), Italy (4.1%)

Source: The World factbook, CIA; partial data till 2009

Regulation of trade

• Customs clearance and import documents: system

certification and standardization of customs rules and issuance

Licensing is expensive and not very transparent. A step forward

seems to be the formation of the new customs union of EURASES

for the free trafic of goods between the three countries

(Kazakhstan,Russia and Belarus): it concern of unified rules for

customs and fees

• Customs classification of goods: fees Russian nomenclature

customs is organized according to international criteria HTS,

which makes it identical to the EU structure Harmonised System

of tariff nomenclature

• Restrictions on imports: the government significantly raised the

level of customs duties on imports of new cars (25-30%) and

used from 12.01.2009, in order protect local producers. The new

customs duties have a pre-planned nine months. Russia

announced any reduction of duties as soon as the Country will be

part of WTO

• Temporary imports: the system allows a total or partial

exemption from taxes and customs duties, providing

that the goods are re-exported within the prescribed period

by the customs authorities, not to exceeding two years

Fonte: Russian Customs Tariff; Dogana Russa; Rupto (www.rupto.ru); fisconelmondo.it

In order to operate Country Risk: 4/7 (Source: OCSE) Terms of SACE Insurance: unrestricted access

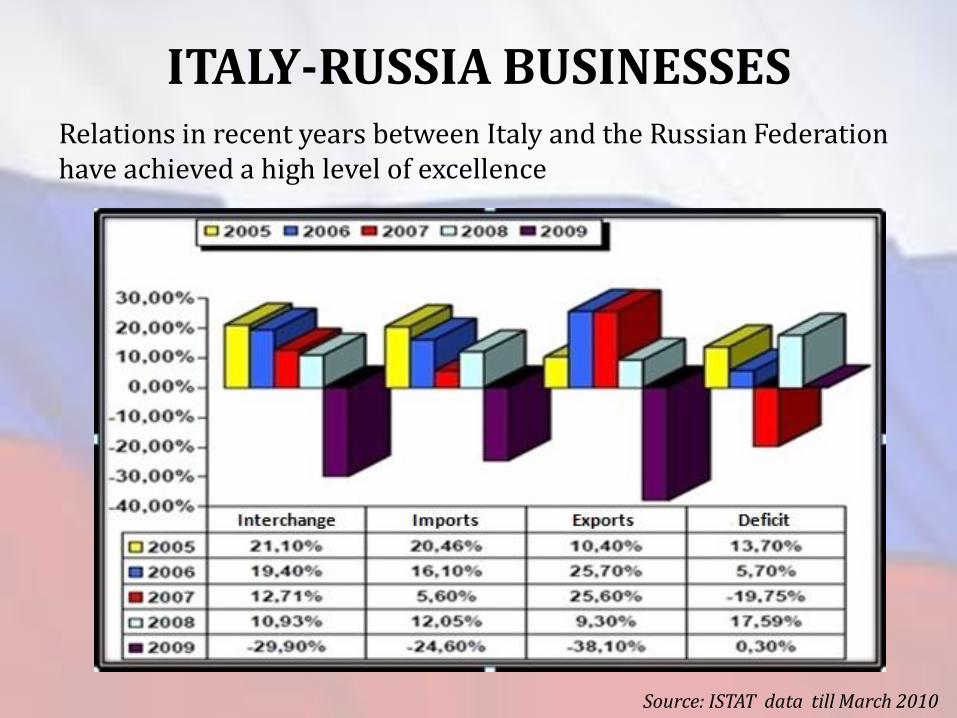

ITALY-RUSSIA BUSINESSES

Relations in recent years between Italy and the Russian Federation have achieved a high level of excellence

Source: ISTAT data till March 2010

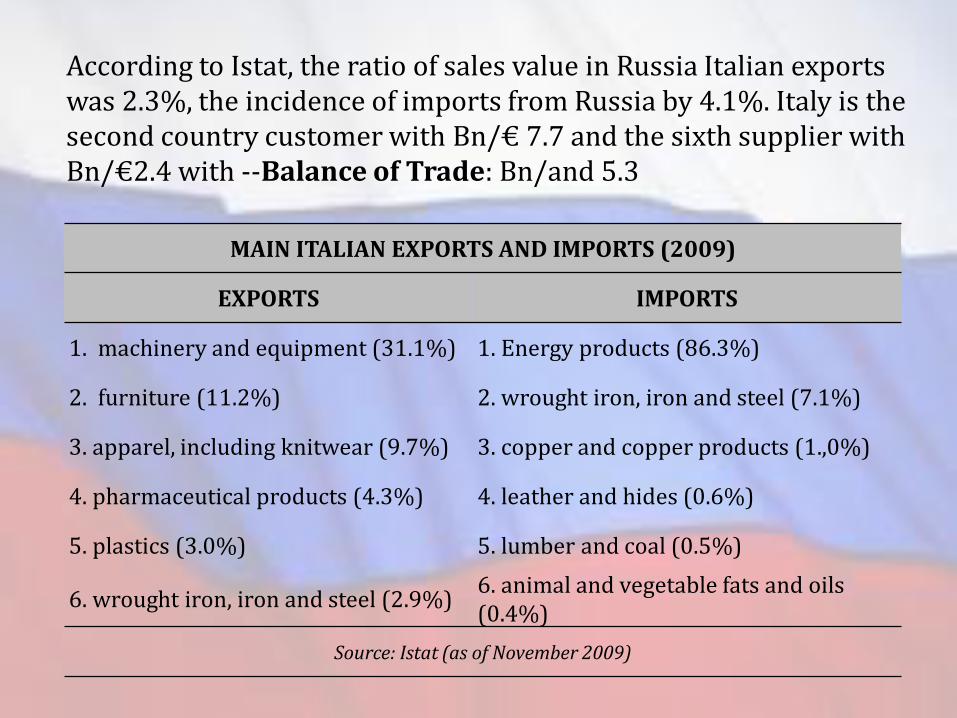

MAIN ITALIAN EXPORTS AND IMPORTS (2009)

EXPORTS IMPORTS

1. machinery and equipment (31.1%) 1. Energy products (86.3%)

2. furniture (11.2%) 2. wrought iron, iron and steel (7.1%)

3. apparel, including knitwear (9.7%) 3. copper and copper products (1.,0%)

4. pharmaceutical products (4.3%) 4. leather and hides (0.6%)

5. plastics (3.0%) 5. lumber and coal (0.5%)

6. wrought iron, iron and steel (2.9%) 6. animal and vegetable fats and oils (0.4%)

Source: Istat (as of November 2009)

According to Istat, the ratio of sales value in Russia Italian exports was 2.3%, the incidence of imports from Russia by 4.1%. Italy is the second country customer with Bn/€ 7.7 and the sixth supplier with Bn/€2.4 with --Balance of Trade: Bn/and 5.3

Agreements with Italy

• In 2007 ENI and Gazprom signed an agreement aiming to launch the

study of the gas pipeline project South Stream which would link the

southern regions of Russia to Europe across the Black Sea

• ENI also entered as an intermediary in the Russian gas market, by signing,

in 2008, with the TGK-9, electricity generating Company, a contract to

supply 350 million cubic meters of gas by 2010

• In May 2009, Eni and Gazprom have also finalized an agreement, in order

to increase the capacity transport of South Stream (by 31 to 63 billion

cubic meters)

• The Finmeccanica Group is strengthening its cooperation with Russian

companies in the aerospace, defense and telecommunications

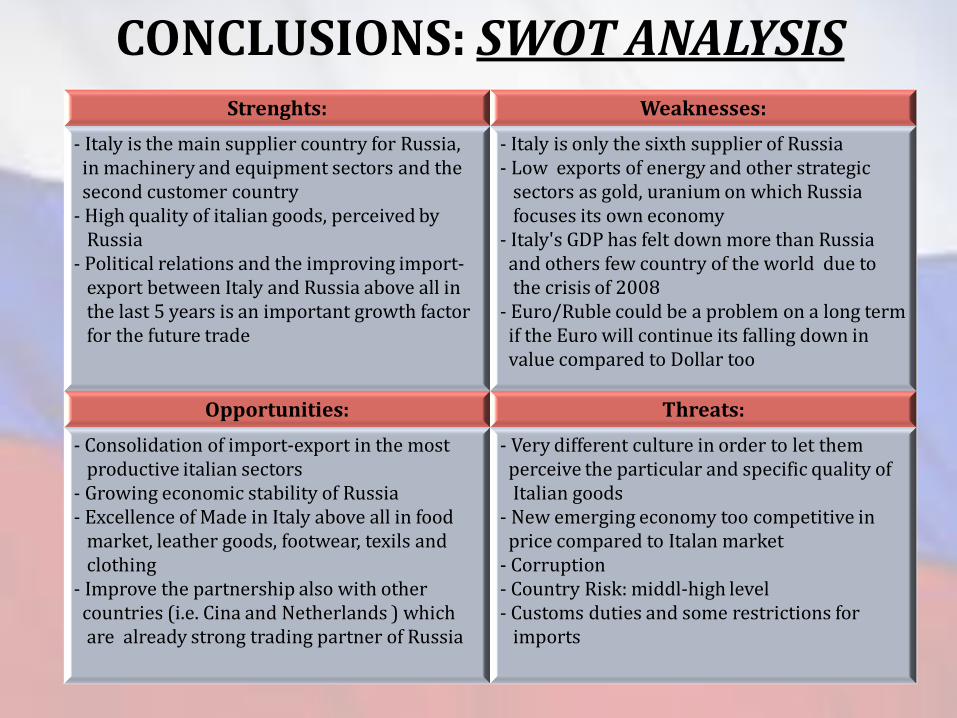

CONCLUSIONS: SWOT ANALYSIS Strenghts: Weaknesses:

- Italy is the main supplier country for Russia, in machinery and equipment sectors and the second customer country - High quality of italian goods, perceived by Russia - Political relations and the improving import- export between Italy and Russia above all in the last 5 years is an important growth factor for the future trade

- Italy is only the sixth supplier of Russia - Low exports of energy and other strategic sectors as gold, uranium on which Russia focuses its own economy - Italy's GDP has felt down more than Russia and others few country of the world due to the crisis of 2008 - Euro/Ruble could be a problem on a long term if the Euro will continue its falling down in value compared to Dollar too

Opportunities: Threats:

- Consolidation of import-export in the most productive italian sectors - Growing economic stability of Russia - Excellence of Made in Italy above all in food market, leather goods, footwear, texils and clothing - Improve the partnership also with other countries (i.e. Cina and Netherlands ) which are already strong trading partner of Russia

- Very different culture in order to let them perceive the particular and specific quality of Italian goods - New emerging economy too competitive in price compared to Italan market - Corruption - Country Risk: middl-high level - Customs duties and some restrictions for imports

Thanks for your attention

Related Documents