A CASE STUDY OF THE EUROPEAN DAIRY INDUSTRY EXPLORING THE RELATIONSHIP BETWEEN FIRM CHARACTERISTICS AND CORPORATE SOCIAL RESPONSIBILITY STRATEGY Sven Thomassen Final report

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

i

A CASE STUDY OF THE EUROPEAN DAIRY INDUSTRY

EXPLORING THE RELATIONSHIP BETWEEN FIRM CHARACTERISTICS

AND CORPORATE SOCIAL RESPONSIBILITY STRATEGY

Sven Thomassen Final report

ii

Exploring the relationship between firm characteristics and corporate social responsibility strategy in the European dairy industry Gerardus Lambertus (Sven) Thomassen Registration No: 941216-829-020 MST-80436 (MSc Thesis Management Studies) Business, Management and Organisation Group (BMO) Wageningen University and Research Supervisor: dr. W.J.J. (Jos) Bijman Co-supervisor: dr. V. (Vincent) Blok Credits: 36 ECTS Date: 02 – 07 – 2019 Version 4.0 Cover picture: (NIBC, n.d.) Disclaimer: this product is produced by a student of Wageningen University as a part of the course MST-80436. This is not an official publication of Wageningen University or Wageningen University and Research and the content herein does not represent any formal position or representation by Wageningen University. Copyright Ó 2019. All rights reserved. No part of this publication may be reproduced or distributed in any form of by any means, without the prior consent of the author.

iii

Preface This research was facilitated by the Business, Management and Organisations Group (BMO) located at Wageningen University and Research. The supervision was provided by dr. W.J.J. (Jos) Bijman (Wageningen University and Research) being my supervisor and dr. V. (Vincent) Blok (Wageningen University and Research) being my co-supervisor. The findings of this report are entirely the responsibility of G.L. (Sven) Thomassen and cannot be considered as an expression of Wageningen University and Research. Acknowledgements During the 6 months this research has been conducted, I was offered the possibility to develop my research skills. I would like to thank all the people involved who supported me during this journey, especially my supervisor and co-supervisor.

iv

Abstract Corporate social responsibility (hereafter CSR) is a widely known concept in management literature since the emergence of it in the early fifties. Firms can be motivated for several reasons to implement CSR in their corporate strategy, among which the increase of corporate reputation. Although this might be the case, firms encounter difficulties during the implementation of CSR in their corporate strategy. In order to understand why the implementation of CSR is hampered, this study aimed to explore the relationship between firm characteristics and CSR strategy. This study explored this relationship specifically for the European dairy industry, due to the high percentages of cooperatives and lack of industry specific research. A multiple case study design was employed to investigate 11 European dairy firms. The relationship was explored firstly by constructing a theoretical background by reviewing literature. Afterwards a content analysis of the corporate reports was conducted to obtain firms’ CSR strategies. The literature review revealed three firm characteristics which were related to CSR. These characteristics are firm size, corporate governance and ownership. By the use of different metrics, the relationship between these characteristics and CSR strategy was explored. Results suggest that firm size, corporate governance and ownership are related to the amount disclosed by the firms on CSR. Although this might be the case, results should be interpreted carefully due to limitations of the sample (e.g size). To conclude, the results of this study indicate that firm size, corporate governance and ownership have an influence on the CSR strategies of European dairy firms.

v

Executive summary Corporate social responsibility (hereafter CSR) is a widely known concept in management literature since the emergence of it in the early fifties. Within the concept of CSR, firms acknowledge and take responsibility for their impact on society. Firms can be motivated for several reasons to implement CSR in their corporate strategy, among which the increase of corporate reputation and decrease of production costs. Although this might be the case, firms encounter difficulties by implementing CSR activities in their corporate strategy. The implementation process might be hampered due to several reasons, among which the unclear relationship between CSR and firms’ financial performance. However, literature also indicates that other factors might influence the integration process of CSR into the overall corporate strategy. To be more specific, literature indicated that firm characteristics may be related to CSR strategy. Creating better understanding on this specific topic, could results in better alignment between CSR and the firm’s overall strategy. As a consequence, performance of CSR activities could be improved. An increase of the performance of CSR might be crucial for managers to persuade firm’s stakeholders to invest in CSR activities.

In order to explore this relationship, this study selected 11 European dairy firms. The European dairy industry is particularly interesting because current literature lacks industry specific research. Furthermore, the high percentages of cooperatives could lead to interesting results. The aim of this study is thus to explore the relationship between firm characteristics and CSR strategy in the context of the European dairy industry. In order to achieve this, firms’ corporate reports were analysed via a content analysis. Before the content analysis was conducted, scientific articles on CSR, CSR strategy and CSR disclosure were consulted. The literature review indicated that there is no consensus yet on a common definition. This is caused by the complex and dynamic nature of CSR. This might enable firms to formulate CSR in their own distinctive way. Furthermore, reviewed literature on CSR disclosure revealed that, based on legitimacy and stakeholder theory, three firm characteristics were found relevant to investigate in the context of the European dairy industry.

The three firm characteristics are firm size, corporate governance and ownership. Firm size was operationalised via the annual dairy turnover. Results suggests that firm size is positively related to CSR strategy. Corporate governance was operationalised via three metrics namely, number of board members, percentage of female board members and percentage of independent board members. Results of this study suggest that all three metrics are positively related to CSR strategy. Lastly, ownership was operationalised via ownership structure and ownership identity. Results suggest that, only for the private firms, ownership structure is positively related to CSR strategy. Cooperatives were not included in this analysis since cooperatives are by definition dispersed. Results regarding ownership identity suggest that private firms disclose more on average than cooperatives. Although these trends were obtained, one has to bear in mind that due to the limitations of the research design, results should be interpreted carefully. Related to the results, it is worthwhile to mention the differences between private firms and cooperative. The differences in terms of CSR disclosures, might be explained by the fact that cooperatives are less equipped in communicating their CSR strategy to stakeholders. If cooperatives fail to communicate their CSR strategy, it might have implications for their legitimacy in society and eventually their competitive position within the dairy industry. Therefore, it might be interesting for managers of the cooperatives to investigate how they could improve their CSR disclosure. Furthermore, it might be interesting for both the private firms and cooperatives to reflect upon their corporate governance structure. As this study indicates that certain board compositions might influence the CSR disclosure and thus the ability of firms to legitimize their behaviour via CSR. All in all, this study tried to explore the relationships between firm characteristics and CSR strategy and, thereby revealed that these characteristics might explain why firms face issues regarding the implementation of CSR.

vi

Table of Content

1. Introduction ............................................................................................................................................... 7 1.1 Introduction ................................................................................................................................................. 7 1.2 Research questions ...................................................................................................................................... 8

2. European dairy industry ............................................................................................................................. 9

3. Literature Review ..................................................................................................................................... 12 3.1 Corporate social responsibility strategy ..................................................................................................... 12 3.2 Corporate social responsibility disclosure .................................................................................................. 15 3.3 Firm characteristics .................................................................................................................................... 20

3.3.1 Firm size ............................................................................................................................................. 20 3.3.2 Corporate governance ........................................................................................................................ 22 3.3.3 Ownership .......................................................................................................................................... 24

3.4 Conceptual framework ............................................................................................................................... 25

4. Methodology ............................................................................................................................................ 27 4.1 Study design ............................................................................................................................................... 27 4.2 Data collection methods ............................................................................................................................ 27 4.3 Data analysis methods ............................................................................................................................... 28 4.4 Objects under study ................................................................................................................................... 29 4.5 Operationalization ..................................................................................................................................... 30

4.5.1 Corporate Social Responsibility Strategy ............................................................................................ 30 4.5.2 Firm characteristics ............................................................................................................................ 31

5. Results ..................................................................................................................................................... 34 5.1 Corporate social responsibility strategy ..................................................................................................... 34 5.2 Firm characteristics .................................................................................................................................... 34

5.1.1 Firm size ............................................................................................................................................. 35 5.1.2 Corporate governance ........................................................................................................................ 36 5.1.3 Ownership .......................................................................................................................................... 40

6. Discussion ................................................................................................................................................ 45 6.1. Comparing results with proposition .......................................................................................................... 45 6.2 Limitations .................................................................................................................................................. 47

7. Conclusion ................................................................................................................................................ 49 7.1 Conclusion .................................................................................................................................................. 49 7.2 Contributions, future research and implications ....................................................................................... 50

References ................................................................................................................................................... 51

Appendices .................................................................................................................................................. 58

7

1. Introduction

1.1 Introduction

Bangladeshi microentrepreneurs and the Danish dairy firm Arla Foods are on first sight unrelated business entities. However, from 2019 onwards they are collaborating to tackle the malnutrition in the rural areas of Bangladesh. Arla Foods started this collaboration to ensure that their product, Dano Daily Pushti, could reach the target customers. These are the residents of rural Bangladesh, which are hard to reach due to limited distribution networks and poor infrastructure (myNewsDesk, 2019). Arla Foods had to find solutions for these limitations, since 70% of the target customers are residing in the rural and remote areas of Bangladesh (myNewsDesk, 2019). To deal with these challenges, Arla Foods employed 200 local women also known as the Pushti-ambassadors. These ambassadors are responsible for delivering the product, while simultaneously educating people about health and milk nutrition (myNewsDesk, 2019). This example illustrates that Dano Pushti is not only produced to make a profit, but also to solve nutritional issues in the rural areas of Bangladesh.

The principle that firms should not only look at profits, but also have to consider their impact on society, is at the essence of corporate social responsibility (hereafter CSR). To be more precise, CSR can be defined as “the responsibility of enterprises for their impacts on society” (European Commission, 2011, p. 6). Literature indicates that CSR is not only a concept that is proposed by academics, but is demanded by society as well (Bernstein, 2000, as cited in Carroll & Shabana, 2010). Adding to that, the public believes that profits should be sacrificed in order to enable firms to improve the situation of disadvantaged stakeholders (Bernstein, 2000, as cited in Carroll & Shabana, 2010).

But why should or should not firms create, implement and execute CSR activities? Friedman argued that it is not the responsibility of the firm to be concerned about social issues (Carroll & Shabana, 2010). He believed that legislation and governments have to take responsibility for solving social issues. Another argument against CSR, is that firms will make themselves less competitive globally (Carroll & Shabana, 2010). Literature also established numerous motivations in favour of CSR among which that it strongly influences firm’s reputation (Vilanova, Lozano, & Arenas, 2009), it increases the price of products (Trudel & Cotte, 2009), and it decreases the production costs (Sprinkle & Maines, 2010). Adding to that, Bhattacharya and Sen (2004, p. 9) stated that “not only doing good is the right thing to do, but it also leads to doing better”. Implementing CSR within the corporate strategy can thus be beneficial for both society and firms. In order to create CSR activities which are in line with corporate strategy, firms formulate CSR strategies. CSR strategy can be defined as the long-term direction of the responsibilities of enterprises regarding their impact on society. Although literature indicates that pursuing CSR activities could have positive implications for firms, firms encounter difficulties by integrating CSR activities into their overall corporate strategy (Vilanova et al., 2009). McWilliams & Siegel (2001) explain these integration issues, by the unclear relationship between CSR and firm’s financial performance. Solving the implementation issues could reduce the misalignment between CSR activities and overall corporate strategy. As a result, alignment between CSR activities and overall corporate strategy could lead to greater impact of these CSR activities on firm’s results (Marín, Rubio, & de Maya, 2012). To optimise the effect of CSR strategies, this study explores how CSR strategies could be influenced. To be more precise, this study focuses on the relationship between firm characteristics and CSR strategy. Firm characteristics are selected as explaining variable, since literature indicates that for example firm size (Graafland, Van de Ven, & Stoffele, 2003) and ownership (Dam & Scholtens, 2013) explain differences in firm’s CSR strategy. Even though a vast amount of literature is already existing on the relationship between firm characteristics and CSR, specific studies for the European dairy industry were not identified. Besides the lack of industry specific research, the dairy industry is more interesting than other industries due to the high percentage of cooperatives (EDA, 2017), which might lead to interesting results.

In order to assess firm’s CSR strategy, one could use different types of sources such as corporate reports, interviews and news articles. This study used corporate reports to obtain firm’s CSR strategy, since these reports are a fruitful source of information (Lu & Abeysekera, 2014). In order to

8

make CSR tangible and measurable, literature on CSR disclosure was employed. CSR disclosure is defined as the process of providing information designed to discharge social accountability via annual reports, special publications or reports or even socially oriented advertising. This study reasons that, by investigating corporate reports, the CSR strategy of the firms could be obtained. Even though this study is aware of a gap between CSR disclosure and CSR strategy, one could argue that differences have become smaller in recent years due to higher levels of scrutinization by society. Literature on CSR disclosure revealed that the legitimacy and stakeholder theory are commonly used to explain firm’s motivations to participate in CSR (Tagesson, Blank, Broberg, & Collin, 2009). Therefore, these theories were used as a theoretical foundation to select the firm characteristics. The three firm characteristics selected for this study, are firm size, corporate governance, and ownership. By conducting this research, this study aims to reveal whether firm characteristics are related to CSR strategy in the context of the European dairy industry.

This report is structured as follows: a description of the European dairy industry is presented in chapter 2, while the literature on CSR, CSR disclosure, and the firm characteristics is reviewed in chapter 3. The research design, data collection and data analysis methods are presented in chapter 4, followed by the results in chapter 5. The results are presented in chapter 6, as well as the limitations of this study. Lastly, conclusions and recommendations for future research are presented in chapter 7.

1.2 Research questions

The objective of this research is to broaden the understanding of the relationship between firm characteristics and corporate social responsibility strategies of European dairy firms. In order to accomplish this, the following central research question is formulated:

What is the influence of firm characteristics on corporate social responsibility strategy of European dairy firms?

In order to answer the central research question, sub-questions are formulated. The sub questions are structured in two parts, including a theoretical part and an empirical part. This study answers the following research questions: Theoretical sub research questions

- What is a corporate social responsibility strategy? - What is corporate social responsibility disclosure? - Which firm characteristics can influence corporate social responsibility strategy?

Empirical sub research questions

- What is the influence of firm size on the corporate social responsibility strategy of European dairy firms?

- What is the influence of corporate governance on the corporate social responsibility strategy of European dairy companies?

- What is the influence of ownership on the corporate social responsibility strategy of European dairy firms?

9

2. European dairy industry This chapter presents an overview of the European dairy industry. An overview is necessary, to fully understand and recognize the dynamics of this industry. Statements made in this chapter, should be seen as a framework in which all dairy firms have to act.

The European dairy industry is a major contributor to the European trade balance as more than 10-billion-euro surplus is created by more than 12,000 dairy processing firms (EDA, 2018). Therefore the dairy industry can be seen as the economic backbone of rural Europe (EDA, 2018). This is demonstrated in Table 1, in which 20 global dairy firms are ranked according to their turnover. The 10 European dairy firms are highlighted in this table. Table 1. Global dairy industry 2017

Company name Country Legal Form Turnover dairy products (in billion €)

Milk intake (in billion kg)

Added Value (in euro/kg milk intake)

Nestlé Switzerland Private 21.4 13.7 1.56 Lactalis France Private 17.7 19.6 0.90 Danone France Private 15.5 8.6 1.43 Dairy Farmers of America USA Cooperative 13.0 29.2 0.45 Fonterra New Zeeland Cooperative 13.0 29.2 0.51 Friesland-Campina Netherlands Cooperative 12.0 13.6 0.88 Arla Foods Denmark Cooperative 10.3 13.9 0.74 Saputo Canada Private 9.6 9.8 0.98 Yili China Private 8.8 7.2 1.22 Mengniu China Private 7.8 6.4 1.22 Dean Foods USA Private 6.7 9.4 0.71 Unilever Netherlands Private 6.2 (est) n.a. n.a. DMK Germany Cooperative 5.8 8.1 0.72 Kraft Heinz United States

of America Private 5.5 n.a. n.a.

Meiji Japan Private 5.1 n.a. n.a. Sodiaal France Cooperative 5.1 4.9 1.04 Savencia France Private 4.9 4.1 1.20 Müller Germany Private 4.5 (est) 4.6 0.98 Agropur Canada Cooperative 4.5 6.3 0.71 Schreiber Foods USA Private 4.4 4.5 0.98

Source: adapted from Bijman and Hanisch (2018, p. 16)

At the European dairy farms, a total of 168.3 million tonnes of milk is produced of which the majority of 163 million ton is cow milk (Eurostat, 2017). The produced milk originates from ewes (2.8 million tonnes), goats (2.3 million tonnes) and buffalos (0.3 million tonnes) (Eurostat, 2017). The European milk production constitutes more than twenty per cent of the total global milk production, as 170.1 million tonnes (Eurostat, 2017) of milk were produced in Europe of the globally produced 811.9 million tonnes of milk in 2016 (Food and Agricultural Organization, 2017). In order to process all the raw milk, the dairy industry employs more than 300,000 people across Europe (EDA, 2018). A small amount of the milk is used for on-farm purposes and the majority of the produced milk is transported to dairy processing firms who use it to create products for consumption such as drinking milk, cheese, whey, butter and milk powder (Eurostat, 2017). In terms of exports, 18.74 of the 69.39 million tonnes of traded dairy products, were produced in Europe. (EDA, 2018). By exporting these products, the dairy industry employs another 45,000 people (Rabobank, 2016). The main export markets for the European dairy industry are China, Mexica and Russia with respectively 7.5, 4.3 and 4.1 million tonnes of exported dairy products (Rabobank, 2016).

10

In order to regulate the European agricultural sector, the Common Agricultural Policy (hereafter CAP) was introduced in 1962. To provide European citizens with affordable food, and to create a fair living standard for the farmers by the means of guaranteed minimum prices (European Commission, 2012). With a guaranteed price for their products, European farmers’ income increased which enabled them to switch from manual production to more sophisticated production techniques. In the seventies, the guaranteed prices eventually led to a milk surplus (European Commission, 2012). In order to reconnected farmers’ production and market demand, and to prevent overproduction, quotas on the milk production were imposed in 1984 (European Commission, 2012). Regulation changed even more in 1992, when the European Commission decided to switch from market to producer support. (European Commission, 2012). As a consequence, price support was replaced by direct payments. These changes were necessary in order to transform the CAP into a market-oriented policy. The milk quota resulted in a gradual decreasing gap between the European and world milk market price. Eventually, the milk quota was abolished in 2015. As a result of the abolishment together with the Russia import embargo, decline in Chinese demand for milk and increase in world milk production, surpluses of milk were created across Europe (Bijman & Hanisch, 2018).

As a consequence of the changes in the CAP, milk prices have become more volatile. Volatility in milk prices especially increased after the adjustment of the intervention prices in 2003 (European Commission, 2017). To illustrate, in the year 2007 the volatility of the milk prices reached 15% whereas an average of 4% volatility was common in the pre-2007 era (European Commission, 2017). Furthermore, prices in the dairy industry have lost their previous seasonal pattern (European Commission, 2017). Comparing the European dairy industry with those of Oceania and the US, it can be observed that the pattern of the volatility follows the same path on a global scale. However, the volatility of the European prices is less pronounced, more smooth and lower compared to Oceania and the US (European Commission, 2017). The increasing volatility can be explained by the continuous reforms of the CAP on the one hand and increasing dependency of European dairy firms on global demand on the other hand (Bijman & Hanisch, 2018).

Besides changes regarding the milk quota, dairy firms have to consider changes in environmental regulation. Because changes in environmental regulations could influence the firm’s strategic decisions. The European Commission (2000) concluded that the European dairy industry mainly impacts the soil, water, biodiversity and non-renewable resources, as these become depleted due to intensification and overuse. To illustrate, dairy cows produce twenty per cent of the yearly methane and are therefore partly responsible for the increasing greenhouse gas emissions (Bijman & Hanisch, 2018). In order to reduce the environmental impact of the European dairy industry, national governments and the European Commission are introducing environmental legislation. For instance, to tackle the increasing levels of nitrate, the European Commission implemented the Nitrates Directive in 1991. In order to achieve this goal, targets and restrictions have been imposed on dairy farmers and Member States have been obliged to report back their progress every four years (European Commission, 2018). As the concerns regarding the environment are increasing, it is expected that regulation to prevent further degradation will become stricter (Bijman & Hanisch, 2018). Not only regulation could be a key driver to reduce the firm’s environmental impact. Sometimes it is a collaboration between multiple stakeholders in society. This can be a collaboration between firms or between firms and governmental agencies, or other stakeholders in society. The Clean and Efficient Agricultural Sectors Covenant is such a collaboration between the Dutch government and agricultural firms, to increase energy efficiency and reduce their greenhouse gas emissions (Ministerie van Landbouw Natuur en Voedselkwaliteit, 2008).

Firms are not only challenged by the threat of stricter regulations, but also stimulated by the ongoing changes in consumer preferences. Whereas products were previously differentiated in a traditional way, in which size and colour are common examples, nowadays other factors have become more important (Saitone & Sexton, 2017). Production location and environmental implications of the production are examples of new differentiating characteristics (Saitone & Sexton, 2017). These characteristics were already existing but have become more prominent differentiation determinants in recent years due to income growth (Saitone & Sexton, 2017) and increasing consumer’ awareness

11

about environmental issues (Loureiro, McCluskey, & Mittelhammer, 2001). These two changes have led to the emergence of a new product category namely, organic food products. Organic food products differ from conventional food products as they limit the use of chemical pesticides and antibiotics and prohibit synthetic fertilizers (European Parliament, 2018). The popularity of organic food products is also growing over the recent years, due to consumers’ concerns about conventional food (Van Loo, Diem, Pieniak, & Verbeke, 2013). Consumers believe that organic food products are both healthier and safer compared to conventional food products. As a results, the organic food sector is the third largest food sector in the European Union (Van Loo et al., 2013).

Changes in regulation and consumer demand, may affect firm’s overall and CSR strategy. For example, the creation of organic food products can be seen as firms’ reactions on changing consumer demand. As stated at the beginning of this chapter, the dynamics of the firm’s environment should be considered to better understand decisions made by managers of European dairy firms. The upcoming chapter elaborates on CSR and the definitional construct of this concept. Furthermore, it elaborates on the CSR disclosure and which firm characteristics are selected for this study.

12

3. Literature Review This chapter reviewed the literature on the definition of CSR, CSR strategy, and CSR disclosure. To be more precise, section 3.1 presents literature on the construction of a CSR definition and elaborates on CSR strategies. Section 3.2 deepens our understanding of firms’ motivations to disclose information on CSR. This is accomplished by explaining and employing legitimacy and stakeholder theory. The theories were used for selecting the three firm characteristics, which is presented in section 3.3. To deal with the three firm characteristics section 3.3 is divided into three subsections, namely firm size (section 3.3.1), corporate governance (section 3.3.2) and ownership (3.3.3).

3.1 Corporate social responsibility strategy

The concept of corporate social responsibility (hereafter CSR) began to emerge in the early fifties of the previous century (Carroll, 1999). Literature found that managers are more dedicated in devoting resources to CSR activities, as this is demanded by multiple stakeholder groups (McWilliams & Siegel, 2001). Adding to that, the European Commission (2008) stated that CSR can be a key determinant in achieving sustainable development and enhancing firm’s innovativeness and competitiveness simultaneously. Therefore, CSR has become a central issue on the agenda of firms across the globe (Perrini, Russo, & Tencati, 2007; Vilanova et al., 2009). Although this might be the case, businesses encounter difficulties by integrating the CSR activities into their overall corporate strategy (Vilanova et al., 2009). In order to understand the CSR and its implications from a business perspective, this section deals with the ongoing discussion regarding the definitional construct of CSR. To properly define CSR, one must understand the origin of the complexity. The remainder of this section elaborates these difficulties in detail to create understanding of the complexity of defining CSR, before defining CSR itself. Sheehy (2014) identified multiple problems which arise when one is defining CSR which will be elaborated in detail. These difficulties include; the multifaceted nature of CSR, ambiguity of issues under consideration and the distinct agendas of the involved actors.

Firstly, CSR is difficult to define due to its multifaceted nature. This implies that CSR is involved in a dynamic and complex system such as the ecological, societal and economic system (Sheehy, 2014). To clarify, the wide variety of systems in which CSR is involved makes it challenging to honour sufficient attention to each system, without excluding systems or imposing contradictions between those systems.

Secondly, CSR is complex due to the inherent ambiguity of the issues under considerations (Sheehy, 2014). Sheehy (2014), identified three layers to explain this ambiguity, by using an example of the working conditions in developing countries. The first layer is identified as the ambiguity regarding the harms that need to be addressed, and regarding whose views should be applied on these harms (Sheehy, 2014). One could raise the questions “Should working conditions be accounted for?” and “Who should set the standards for these conditions?”. The second layer of complexity arises when one aims to solve the issue to what extent issues should be addressed (Sheehy, 2014). Sheehy raises the question, “Should all working conditions be accounted for or only include those which are formulated by the International Labour Organisation?”. The last layer of complexity is about the responsibility of these harms (Sheehy, 2014). In line with his example, the following question could be asked: “Does this responsibility lie solely with producers of the developed countries or with the subcontractors in the developing countries?”. Responsibility is a complex discussion within the CSR debate due to the multiple locations, concerns, authorities, societies and political agendas involved (Sheehy, 2014).

Thirdly, constructing a CSR definition is hampered by the different agendas of actors who are engaged in CSR. Sheehy (2014) identified four actors; businesses, academics, political movements and governments, which are trying to define CSR but hamper this process due to their own agenda. Firstly, firms create specific cases of CSR related to their organization, in order to claim they are representing a socially responsible organisation (Sheehy, 2014). As a result of this claim, firms’ actions must be socially responsible. Firms establish themselves as socially responsible, without these actions being tested for their socially responsible nature. The academics on their turn try to reflect their disciplinary

13

perspectives and priorities, within the definitional construct of CSR. Adding to that, academics try to propose new descriptive definitions (Sheehy, 2014). However, these definitions fail to identify the nature of CSR (Sheehy, 2014). Defining CSR is also hampered by the ongoing battle between political movements. Politicians debate on several themes among which the public-private divide, the role of the government and the place of private enterprise or markets (Sheehy, 2014). Again, the battle between different movements complicates the construction of a CSR definition. Lastly, governments employ CSR as a cheaper alternative to address and solve social and environmental issues in society (Sheehy, 2014). Therefore, governments need a CSR definition which is acceptable to business and motivates behavioural change to achieve the desired results. These four actors illustrate that they all have their own distinct agenda when it comes down to formulating a CSR definition. According to Sheehy (2014, p. 627) “to find or develop a definition which is not focused on one or a few of these factors, issues, actors or solutions is a challenge”. Although constructing a definition is challenging, multiple academics tried to define CSR. The upcoming part elaborates briefly on the present research constructing a CSR definition and its evolution in time.

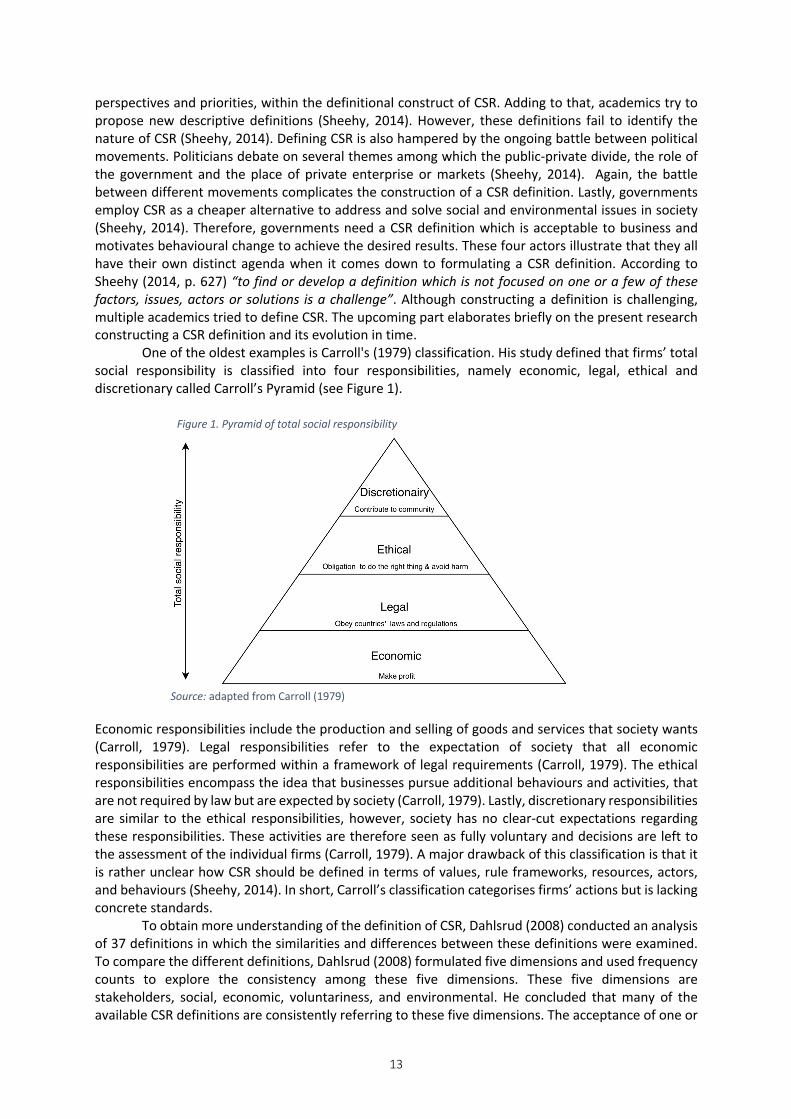

One of the oldest examples is Carroll's (1979) classification. His study defined that firms’ total social responsibility is classified into four responsibilities, namely economic, legal, ethical and discretionary called Carroll’s Pyramid (see Figure 1).

Economic responsibilities include the production and selling of goods and services that society wants (Carroll, 1979). Legal responsibilities refer to the expectation of society that all economic responsibilities are performed within a framework of legal requirements (Carroll, 1979). The ethical responsibilities encompass the idea that businesses pursue additional behaviours and activities, that are not required by law but are expected by society (Carroll, 1979). Lastly, discretionary responsibilities are similar to the ethical responsibilities, however, society has no clear-cut expectations regarding these responsibilities. These activities are therefore seen as fully voluntary and decisions are left to the assessment of the individual firms (Carroll, 1979). A major drawback of this classification is that it is rather unclear how CSR should be defined in terms of values, rule frameworks, resources, actors, and behaviours (Sheehy, 2014). In short, Carroll’s classification categorises firms’ actions but is lacking concrete standards. To obtain more understanding of the definition of CSR, Dahlsrud (2008) conducted an analysis of 37 definitions in which the similarities and differences between these definitions were examined. To compare the different definitions, Dahlsrud (2008) formulated five dimensions and used frequency counts to explore the consistency among these five dimensions. These five dimensions are stakeholders, social, economic, voluntariness, and environmental. He concluded that many of the available CSR definitions are consistently referring to these five dimensions. The acceptance of one or

Figure 1. Pyramid of total social responsibility

Source: adapted from Carroll (1979)

14

a multitude of these dimensions is still troublesome, due to the divers interests of different stakeholders. According to Dahlsrud (2008), the biggest challenge is not to define CSR, but to understand how it is constructed in a context and while incorporating this knowledge into a business strategy. In this line of reasoning, Dahlsrud did not propose a new definition like many scholars are aiming for. To elaborate, a general definition of CSR is not desirable according to Dahlsrud because of the differences between for example countries and firms. To illustrate with Sheehy’s example, it is comprehensible that US firms incorporate labour rights into their CSR strategy. However, it would be remarkable for European firms as these rights are often determined by law. For firms, similar comparisons could be made. For example, the clothing industry emphasizes the improvement of working conditions of labourers in developing countries via initiatives like the Dutch Agreement on Sustainable Garment and Textile (SER, 2019). However, the dairy industry’s main impact on society is its environmental impact due to the production of milk (European Commission, 2000). Furthermore, this example is in line with Sheehy’s first and third implication as both clothing and dairy industry pursue different agendas. One could argue that dairy firms must highlight their efforts to reduce their environmental impact of milk production.

Although Dahlsrud contributed to the knowledge on the definitional construct of CSR, Dahlsrud’s study is limited in two ways. Firstly, the five dimensions identified by Dahlsrud are not tested for their validity (Carroll & Shabana, 2010). Furthermore, Dahlsrud’s study was criticized for the limited time period, namely 1980-2003. Due to the selection of this time frame, it underestimates the true number of definitions (Carroll & Shabana, 2010). As a consequence, Dahlsrud’s study did not include essential definitions constructed by academics outside this time period (Sarkar & Searcy, 2016). Furthermore, previous studies were limited by the use of qualitative analysis. This resulted in subjective results and made it challenging to replicate these studies (Sarkar & Searcy, 2016). To overcome these problems, Sarkar and Searcy (2016) used bibliometric techniques and expanded the time frame to 1953-2014. In their study, they tried to reveal the key dimensions of the CSR and the relationships of these dimension within the CSR definitions. In total 110 definitions, which were obtained via different sources like books, journals and non-academic publications, were analysed. By analysing these definitions, they found six core dimensions of which CSR consists of; economic, ethical, social, stakeholders, sustainability and discretionary (Sarkar & Searcy, 2016). Based on these six core dimensions, they proposed the following definition of CSR;

“CSR implies that firms must foremost assume their core economic responsibility and voluntarily go

beyond legal minimums so that they are ethical in all of their activities and that they take into account the impact of their actions on stakeholders in society, while simultaneously contributing to

global sustainability” (Sarkar & Searcy, 2016, p. 1433) Sarkar and Searcy's conclusions differ from the conclusion drawn by Dahlsrud, as they found that the ethical component is a distinct concern in the CSR debate. This corresponds to Carroll’s definition, as the third was the ethical responsibility. Sarkar and Searcy (2016) concluded therefore that it is essential to incorporate the ethical considerations into a CSR definition since CSR requires firms to behave open, fair and moral. Furthermore, Dahlsrud’s view fundamentally differs from Sarkar and Searcy, as the latter considered it necessary to construct a general definition for CSR, while the opposite holds for Dahlsrud. The difference between these visions also illustrate the problem formulated by Sheehy, in which scholars formulate CSR according to their perspective and agenda. One could conclude that, although academics and scholars try to formulate a unifying description of CSR, they have failed to do so (Sheehy, 2014). This is reinforced by Dahlsrud (2008), as he was unable to develop an unbiased definition since CSR is a social construct. Adding to that, Sarkar and Searcy (2016) stated that the lack of consensus around the definition of CSR has resulted in multiple implications regarding the development, implementation and reporting of social activities. Instead of looking at general CSR definitions, this study tried to reveal whether industry specific literature could give more guidance on defining CSR. This might be the case as the dairy industry might focus on specific areas in their CSR strategy, like environment, as these areas are impacting society

15

greatly. Maloni and Brown (2006) constructed a framework in which CSR elements of the food supply chain are addressed. They constructed a new framework because they stated that different supply chains have to deal with unique CSR dimensions (Maloni & Brown, 2006). By conducting a review on both industry and academic literature, Maloni and Brown (2006) found the following dimensions are occurring in the food supply chain:

- Animal welfare - Biotechnology - Health and safety - Environment - Community - Labour and Human Rights - Fair trade - Procurement

Although these dimensions clarify to a certain extend what CSR encompasses in the food supply chain, it is hard to extrapolate these to all different firms within the food supply chain. The food supply chain encompasses a wide variety of other industries, among which the dairy industry, which is investigate in this study, is one. Since the CSR dimensions are industry-specific, one could argue that the dimensions constructed by Maloni and Brown (2006) are not suitable for the dairy industry. To illustrate, one could reason that animal welfare is more dominating the debate in dairy firms than in fast-mover-consumer-good firms as the former are closer located to the animals. In order to construct a CSR definition specifically for the dairy industry, literature regarding CSR and the dairy industry was consulted. However, current literature could not give any clear direction of specific CSR issues within the context of the dairy industry. As a consequence, it is difficult to formulate CSR definition specifically for the dairy industry.

Taking these arguments together, one could argue whether constructing a CSR definition is necessary at all. As Sheehy (2014) indicated before, CSR itself has a dynamic nature implying that the content of CSR is changing continuously. This is caused by the changing demands and expectations of the economic, environmental and social systems. Therefore, to ensure the relevance of possible CSR definitions, definitions should be dynamic instead of static. However, one could question whether academics and other stakeholders could reach consensus fast enough in order to be relevant and prevent the definition from becoming outdated.

In sum, one could argue that constructing a universally accepted CSR definition is unreachable or even undesirable. It might be more suitable to construct guidelines which indicate the domain of CSR, while allowing industries to formulate their own CSR definitions. In this line of reasoning, this study defines CSR in its broadest way as “the responsibility of enterprises for their impacts on society” (European Commission, 2011, p. 6). A definition is selected to provide this study with guidance on concept of CSR. Relating the definition to the strategy of a firm, CSR strategy in this study is defined as long-term direction of firm’s responsibilities regarding their impact on society. The upcoming section elaborates specifically on CSR disclosure, and how this is related to CSR strategy. Furthermore, it presents two theories which serve as theoretical foundation to select the firm characteristics.

3.2 Corporate social responsibility disclosure

This section presents an overview of the current state of knowledge on the relationship between various determinants and CSR disclosure. CSR disclosure literature was included specifically, since it offers the possibilities to measure CSR strategy. Even though there is a gap between CSR disclosure and CSR strategy, one could argue that differences have become smaller in recent years due to higher levels of scrutiny by society. It is assumed that levels of scrutiny have become higher, especially for firms producing nutritional products, due to scandals like the 2008 baby formula scandal in China and the 2013 horse meat scandal in Europe. To illustrate, Starbuck disclosed several CSR claims, but NGOs were suspicious whether Starbuck actually executed these claims. As a consequence, NGOs started

16

protest efforts against Starbucks causing reputational damages (Maloni & Brown, 2006). To put it differently, disclosing CSR activities while not performing these activities could cause a so-called backfire effect and eventually lead to reputational damages.

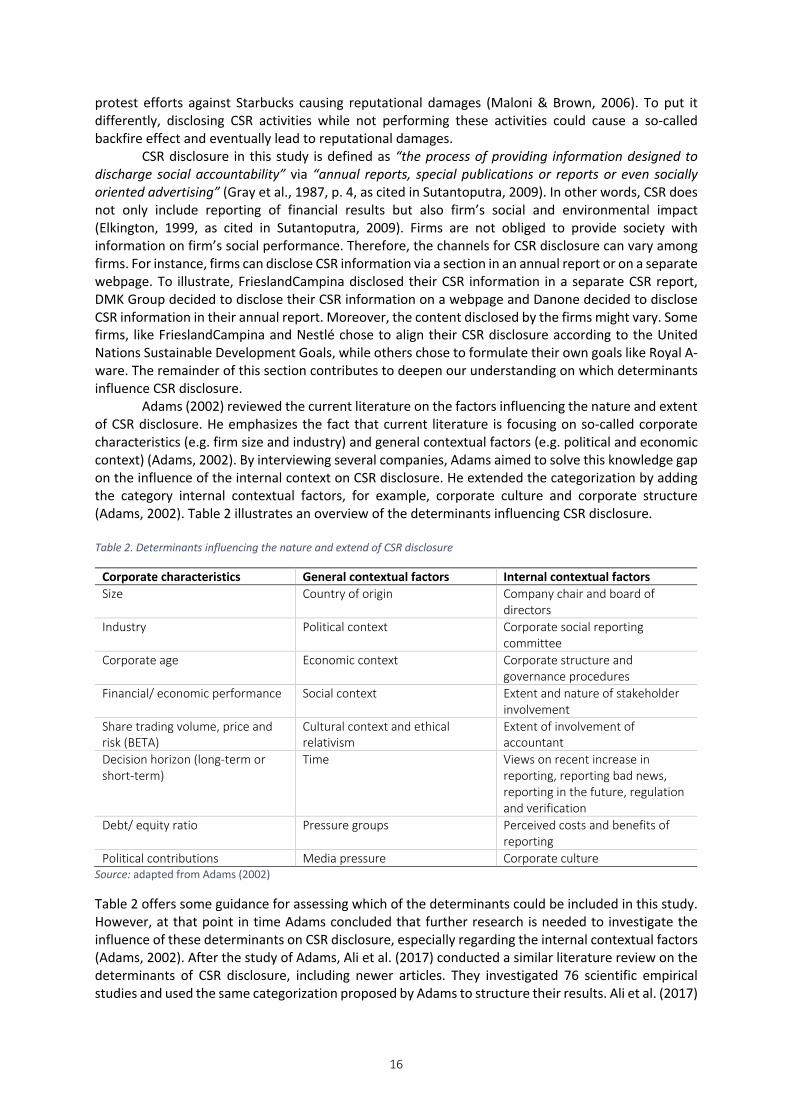

CSR disclosure in this study is defined as “the process of providing information designed to discharge social accountability” via “annual reports, special publications or reports or even socially oriented advertising” (Gray et al., 1987, p. 4, as cited in Sutantoputra, 2009). In other words, CSR does not only include reporting of financial results but also firm’s social and environmental impact (Elkington, 1999, as cited in Sutantoputra, 2009). Firms are not obliged to provide society with information on firm’s social performance. Therefore, the channels for CSR disclosure can vary among firms. For instance, firms can disclose CSR information via a section in an annual report or on a separate webpage. To illustrate, FrieslandCampina disclosed their CSR information in a separate CSR report, DMK Group decided to disclose their CSR information on a webpage and Danone decided to disclose CSR information in their annual report. Moreover, the content disclosed by the firms might vary. Some firms, like FrieslandCampina and Nestlé chose to align their CSR disclosure according to the United Nations Sustainable Development Goals, while others chose to formulate their own goals like Royal A-ware. The remainder of this section contributes to deepen our understanding on which determinants influence CSR disclosure. Adams (2002) reviewed the current literature on the factors influencing the nature and extent of CSR disclosure. He emphasizes the fact that current literature is focusing on so-called corporate characteristics (e.g. firm size and industry) and general contextual factors (e.g. political and economic context) (Adams, 2002). By interviewing several companies, Adams aimed to solve this knowledge gap on the influence of the internal context on CSR disclosure. He extended the categorization by adding the category internal contextual factors, for example, corporate culture and corporate structure (Adams, 2002). Table 2 illustrates an overview of the determinants influencing CSR disclosure. Table 2. Determinants influencing the nature and extend of CSR disclosure

Corporate characteristics General contextual factors Internal contextual factors Size Country of origin Company chair and board of

directors Industry Political context Corporate social reporting

committee Corporate age Economic context Corporate structure and

governance procedures Financial/ economic performance Social context Extent and nature of stakeholder

involvement Share trading volume, price and risk (BETA)

Cultural context and ethical relativism

Extent of involvement of accountant

Decision horizon (long-term or short-term)

Time Views on recent increase in reporting, reporting bad news, reporting in the future, regulation and verification

Debt/ equity ratio Pressure groups Perceived costs and benefits of reporting

Political contributions Media pressure Corporate culture Source: adapted from Adams (2002)

Table 2 offers some guidance for assessing which of the determinants could be included in this study. However, at that point in time Adams concluded that further research is needed to investigate the influence of these determinants on CSR disclosure, especially regarding the internal contextual factors (Adams, 2002). After the study of Adams, Ali et al. (2017) conducted a similar literature review on the determinants of CSR disclosure, including newer articles. They investigated 76 scientific empirical studies and used the same categorization proposed by Adams to structure their results. Ali et al. (2017)

17

also tried to present the differences between developed and developing countries. In the scope of this study, namely European dairy firms, only the results of the developed countries are included. Ali et al. (2017) found that two corporate characteristics are most frequently examined and consistent in results, namely firm size and industry sector. They state that the relationship between firm size and industry and CSR disclosure are strong and significant. Current literature also established a strong relationship between industry and CSR disclosure (Ali et al., 2017). The determinant financial performance and systematic risk characteristics were investigated numerous times, however, these relationships were rather unclear in terms of significance and direction. Furthermore, Ali et al. (2017) investigated literature on the general contextual factors. They found that national context can explain the differences between firms in both the CSR practices and disclosure. The included studies found significant differences in CSR disclosure between the US and European countries, as well as between European countries. Lastly, as was the case during Adams’ literature review, little attention has been paid to the internal contextual factors and their influence on CSR disclosure (Ali et al., 2017). Most studies included in Ali’s analysis, were conducted to reveal executives’ attitude towards CSR disclosure, which was overall positive. The same positive relationship holds between corporate governance and CSR disclosure. Ali et al. (2017) summarized that the included studies explained this positive relationship by the gain of competitive advantage or, enhanced corporate reputation. Summarizing, most of the literature paid attention to firm size, industry sector, profitability, and corporate governance mechanisms and their influence on CSR disclosure (Ali et al., 2017).

Although the study of Adams (2002) and Ali et al. (2017) summarizes numerous determinants of CSR disclosure, it lacks a theoretical foundation upon which determinants could be selected. In order to select the most relevant determinants, this study took a step back and ask the following question “What is the theoretical foundation for selecting proper firm characteristics?”. In other words, what is the rationale behind disclosing CSR at all. Reviewing the literature, it became clear that two theories were predominantly occurring to explain why firms would disclose CSR (Chan, Watson, & Woodliff, 2014; Tagesson et al., 2009). These two theories are the legitimacy and stakeholder theory. In order to reduce the number of determinants, this study could choose for selecting the legitimacy or stakeholder theory. However, according to Ljungdahl (as cited in Tagesson et al., 2009), these theories should be seen as complementary and not substitutes. Firms are incentivized to disclose CSR related information for multiple reasons which are hard to capture in one theory (Cormier, Magnan, & Van Velthoven, 2005). Moreover, selecting one theory would be problematic since “a comprehensive theoretical framework of the underlying determinants of corporate environmental disclosure is still elusive” (Cormier, Magnan, and Van Velthoven, 2005, p. 6). According to Cormier et al. (2005), one single theory captures CSR disclosure insufficiently since CSR disclosure is not systematic but dynamic, not associated with same-period profitability, related to firm size, subjected to industry-specific effects and subjected to country-specific effects. Tagesson et al. (2009) explained the success of these two theories specifically as a consequence of their system-oriented approach compared to other theories which are more market-oriented. Furthermore, both the legitimacy and stakeholder theory can be considered as more comprehensive theories due to their recognition of the dynamic environment in which organizations evolve (Cormier et al., 2005). To wrap up, from literature one could conclude that current literature did not reach consensus on a universally accepted theoretical framework to explain CSR disclosure, however, researcher did reached consensus on the fact that these theories should be seen as complementary rather than substitutes (Chan et al., 2014). Therefore, this study uses a combination of both the legitimacy and stakeholder theory as a theoretical foundation in order to select the determinants of CSR.

The legitimacy theory is founded on the principle that companies act in a certain way, to legitimize their behaviour to stakeholders formalized via social contracts (Branco & Rodrigues, 2006). The existence of firms is based on the fulfilment of society’s expectations on how firms should conduct their operations (Branco & Rodrigues, 2006). Specifically applied to the case of CSR, firms disclose CSR information to present their socially responsible image and to obtain legitimacy from society (Branco & Rodrigues, 2006). Firms’ legitimacy is not static, but rather dynamic due to the changing expectations of society (Montecchia, Giordano, & Grieco, 2016). As a consequence, firms can lose legitimacy when

18

they are unable to fulfil societies’ dynamic expectations. This can lead to a legitimacy gap, followed by a violation of the social contract and ultimately a loss of legitimacy (Sethi, 1979 as cited in Montecchia et al., 2016). Firms can mitigate the risk of legitimacy loss by aligning their actions with societies’ expectations. Society is possibly informed by firms’ actions via CSR disclosure, due to which disclosing this kind of information can be seen as a strategy to prevent legitimacy loss (Dowling & Pfeffer, 1975; Gray et al., 1995; Suchman, 1995, as cited in Montecchia et al., 2016). Legitimacy loss cannot only be prevented by disclosing firm’s CSR strategy, as firms have to execute these activities due to scrutinization of society. If they decide to disclose but not to execute CSR activities, firms are still risking legitimacy loss as was illustrated at the beginning of this section. Therefore, legitimacy theory provides this study with a theoretical framework to assess the relationship between firm characteristics and CSR.

Another perspective is the stakeholder theory, which uses the perspective of the firm’s stakeholders. Stakeholders can be defined as groups who can affect or are affected by fulfilling organisations’ objectives (Russo & Perrini, 2010). Central to the concept of stakeholder theory is the interaction between firms and stakeholders (Donaldson, Preston, & Preston, 1995). Stakeholder groups are influenced by firm’s business of conduct. However, to seek approval from stakeholders, firms may adjust these decisions. For example, managers might devote more resources to CSR related activities due to the positive response of (multiple) stakeholders (Donaldson & Preston, 1995; Mitchell, Agle, & Wood, 1997 as cited in McWilliams & Siegel, 2001). More general, managers are vital for firms since they balance and meet conflicting demands of multiple stakeholders (Freeman, 1984; Ullmann, 1985, as cited in Chan et al., 2014). Besides, firms depend on external stakeholders since they provide them with resources, that gives stakeholders power over the firm and its behaviour (Chan et al., 2014). Therefore, one could argue that firms need support of all of its stakeholders to achieve long-term success (Van der Laan Smith et al., 2005, as cited in Chan et al., 2014). In order to manage firms’ stakeholders, firms might employ strategic stakeholder management which compromises that firms, in order to be effective, devote attention to those stakeholders that can affect or can be affected by achieving firm’s objectives (Freeman, 1999, as cited in Chan et al., 2014). A possible way to meet stakeholders demands is to develop firm’s reputation as “socially responsible through performing and disclosing CSR activities” (Chan et al., 2014, p. 62). Moreover, if these activities are part of a strategic plan, one could argue that stakeholder power and CSR performance or disclosure are positively related (Chan et al., 2014). Therefore, stakeholder theory provides this study with a useful theoretical framework to assess the relationship between firm characteristics and CSR.

In short one could say that the legitimacy theory entails the interaction with society as a whole, while stakeholder theory focusses on firm’s interactions with stakeholders (Deegan & Blomquist, 2006, as cited in Chan et al., 2014). These theories were used as starting point to select the determinants for this study. Based on the study conducted by Ali et al. (2017), tables were constructed which give an overview of determinants that were investigated in previous studies based on the legitimacy theory (Table 3), stakeholder theory (Table 4), or combination of both (Table 5).

19

Table 3. Determinants of CSR disclosure based on legitimacy theory

Table 4. Determinants of CSR disclosure based on stakeholder theory

Stakeholder theory Study No Authors (year) Determinants 1 Roberts (1992) Financial performance (+)*, systematic risk (-)** 2 Van der Laan Smith et al. (2005) Country (+) 3 Jo and Harjoto (2012) Governance structure (+)

Source: adapted from Ali et al. (2017). Notes: *(+): significant positive correlation OR proof of influence. ** (-): significant negative correlation or proof

Table 5. Determinants of CSR disclosure based on combination of legitimacy and stakeholder theory

Combination of legitimacy theory and stakeholder theory Study No Authors (year) Determinants 1 Gray et al. (1995) Size (+)*, political development (+) 2 Reverte (2009) Size (+), industry (+), financial performance

(o)**, media exposure (+), leverage (o) 3 Taggeson et al. (2009) Size (+), industry (+), financial performance (+),

ownership (govt vs. private) (+) Source: adapted from Ali et al. (2017). Notes: * (+): significant positive correlation OR proof of influence. ** (o): no evidence OR relationship

In order to select determinants for this study, the scope of this study should be taken into account. This study is only interested in determinants which can be identified as firm characteristics. In order to select these types of determinants, firm characteristics must be defined. A characteristic can be defined as “a typical or noticeable quality of someone or something” (Cambridge Dictionairy, 2019a). In that line of reasoning and in the context of firms, this study defined firm characteristics as typical or noticeable feature of a firm. For example, a typical or noticeable feature of a firm could be its size or the industry in which it is positioned. Therefore, determinants which were not categorised as such are

Legitimacy theory Study No Authors (year) Determinants 1 Guthrie and Parker (1989) External pressure (+)* 2 Patten (1991) Size (+), industry (+), financial performance

(o)**, public pressure proxied by size and industry (+)

3 Deegan and Gordon (1996) Size (+), industry (+), env.*** concerns proxied by membership of env. groups (+)

4 Hackston and Milne (1996) Size (+), industry (+), overseas listing (+), financial performance (o)

5 Adams et al. (1998) Size (+), industry (+), country (+) 6 Neu et al. (1998) Shareholder (+), creditors (o), management

attitude (+) 7 Deegan et al. (2002) Media attention to social issues (+) 8 Patten (2002) Size (+) 9 Wilmshurst and Frost (2002) Perceived importance of shareholders (+),

investors (+), local community (+), suppliers (+), customers (+)

10 Van Staden and Hooks (2007) - 11 O’Dwyer (2002) Industry (+), management attitude (+) 12 O’Donovan (2002) To manage public relations (+), to present

positive picture of social and environmental performance (+)

Source: adapted from Ali et al. (2017). Notes: *(+): significant positive correlation OR proof of influence. ** (o): no evidence OR relationship. *** env.: environmental

20

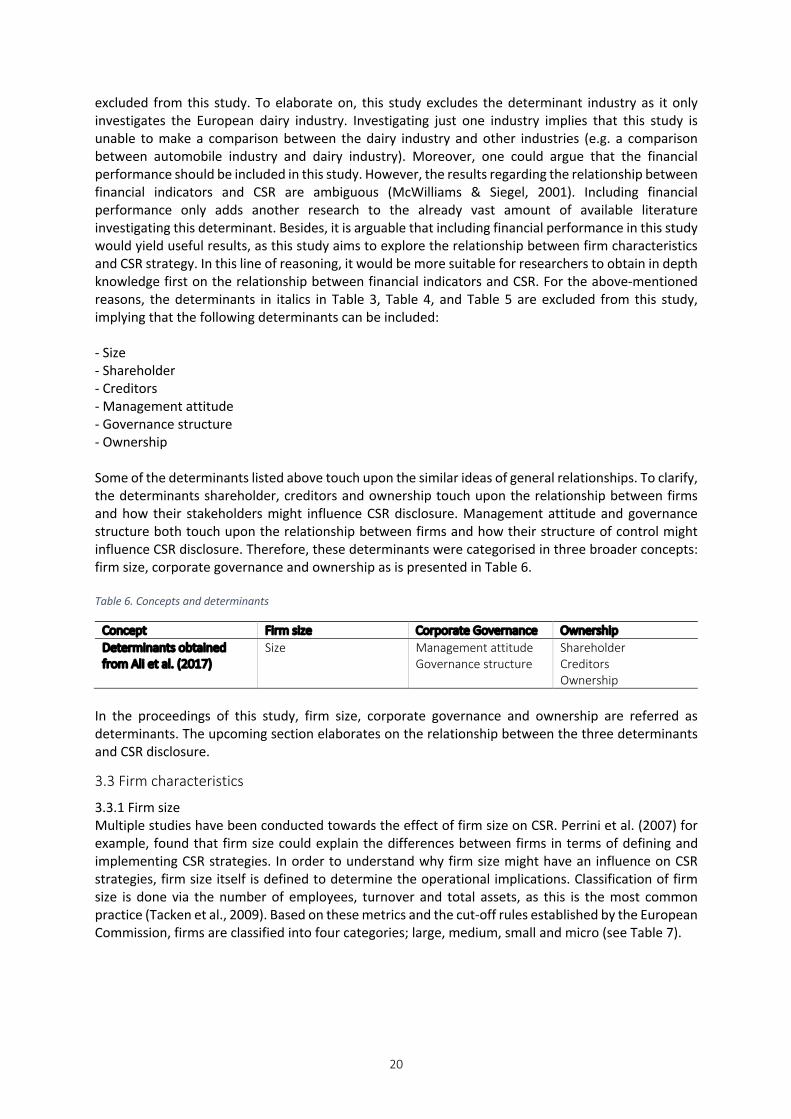

excluded from this study. To elaborate on, this study excludes the determinant industry as it only investigates the European dairy industry. Investigating just one industry implies that this study is unable to make a comparison between the dairy industry and other industries (e.g. a comparison between automobile industry and dairy industry). Moreover, one could argue that the financial performance should be included in this study. However, the results regarding the relationship between financial indicators and CSR are ambiguous (McWilliams & Siegel, 2001). Including financial performance only adds another research to the already vast amount of available literature investigating this determinant. Besides, it is arguable that including financial performance in this study would yield useful results, as this study aims to explore the relationship between firm characteristics and CSR strategy. In this line of reasoning, it would be more suitable for researchers to obtain in depth knowledge first on the relationship between financial indicators and CSR. For the above-mentioned reasons, the determinants in italics in Table 3, Table 4, and Table 5 are excluded from this study, implying that the following determinants can be included: - Size - Shareholder - Creditors - Management attitude - Governance structure - Ownership Some of the determinants listed above touch upon the similar ideas of general relationships. To clarify, the determinants shareholder, creditors and ownership touch upon the relationship between firms and how their stakeholders might influence CSR disclosure. Management attitude and governance structure both touch upon the relationship between firms and how their structure of control might influence CSR disclosure. Therefore, these determinants were categorised in three broader concepts: firm size, corporate governance and ownership as is presented in Table 6. Table 6. Concepts and determinants

Concept Firm size Corporate Governance Ownership Determinants obtained from Ali et al. (2017)

Size Management attitude Governance structure

Shareholder Creditors Ownership

In the proceedings of this study, firm size, corporate governance and ownership are referred as determinants. The upcoming section elaborates on the relationship between the three determinants and CSR disclosure.

3.3 Firm characteristics 3.3.1 Firm size Multiple studies have been conducted towards the effect of firm size on CSR. Perrini et al. (2007) for example, found that firm size could explain the differences between firms in terms of defining and implementing CSR strategies. In order to understand why firm size might have an influence on CSR strategies, firm size itself is defined to determine the operational implications. Classification of firm size is done via the number of employees, turnover and total assets, as this is the most common practice (Tacken et al., 2009). Based on these metrics and the cut-off rules established by the European Commission, firms are classified into four categories; large, medium, small and micro (see Table 7).

21

Table 7. Firm size classification

Firm size Number of employees

and Annual turnover (mil EU)

or Annual balance sheet (mil EU)

Large > 250 and > 50 or > 43 Medium 50 – 249 and 11 - 50 or 11 – 43 Small 10 -49 and 2 – 10 or 2 – 10 Micro < 10 and < 2 or < 2

Source: adapted from European Commission (2019)

Small and medium-sized enterprises (hereafter SMEs) are often characterised as organisations which are internally financed, cash-limited, multitasking, flexible, local and based on informal relationships inside and outside the firm (Marín et al., 2012). On the contrary, large enterprises are externally financed and have rigid organisational structures with formalised processes (Marín et al., 2012). Larger firms are more likely to disclose CSR information since they are more visible to the public. As a consequence, they are subject to higher levels of scrutiny from their stakeholders, compared to SMEs (Marín et al., 2012). Larger firms are more likely to be responsive with respect to environmental and community issues. They are more responsive since they can identify relevant stakeholders and meet their demands more easily (Perrini et al., 2007). Satisfying stakeholder’ demands could positively influence the firms’ competitiveness (Marín et al., 2012). Graafland, Van de Ven and Stoffele (2003) conducted a similar study in which they investigated the influence of firm size on the instruments used to foster ethical behaviour. According to Graafland et al. (2003), larger firms are more visible to the public, which makes responsible production and selling of production relatively more important for larger firms. Furthermore, both Graafland et al. (2003) and Perrini et al. (2007) argue that larger firms can use their economies of scale during the development of ethical instruments, as they are relatively small for large firms. Adding to that, larger firms are more in need to communicate their values and norms to their customers as they often operate in anonymous markets (Graafland et al., 2003). Although these results suggest that firm size is positively related to CSR, Udayasankar (2008) argues that this may be too premature to assume. Udayasankar (2008) argues that attributes should be allocated to the concept firm size, in order to properly explain the effect of firm size on CSR. She identified three dimensions of which firm size might consists of namely, firm visibility, resource access and scale of operations. To put it differently, she proposes that firm size should not be treated as a one-dimensional concept. The dimensions influence firm size each in their own way. For example regarding visibility Udayasankar (2008) stated, that even when firms are rarely visible to the public they can be equally motivated to participate in CSR. Less visible and smaller firms may gain more from participating in CSR initiatives, than highly visible and larger firms, due to a higher marginal utility of CSR for smaller firms (Udayasankar, 2008). Similar to firm’s visibility, Udayasankar (2008) reasoned that resource access can be both hampering and fostering participation in CSR initiatives. Firms which are resources-abundant and often larger, are more prone to invest in CSR because they have the resources to respond to stakeholders’ pressure (Udayasankar, 2008). On the other hand, firms which are resource-scarce and often smaller, perceive CSR initiatives as a strategic option to acquire resources at the expense of competitors (Udayasankar, 2008). Furthermore, larger scale operating firms which are often larger, are more capable of re-organizing and re-allocating resources. Therefore, larger scale operating firms are more likely to implement CSR successfully (Udayasankar, 2008). Some CSR initiatives require large scale operations in order to be socially effective and, therefore, are unattainable for smaller firms (Udayasankar, 2008). On the contrary, smaller firms cannot compete on the basis of economies of scale and, have to pursue a differentiation strategy to gain competitive advantage. CSR might be useful in obtaining a competitive advantage (Jones, 1999, as cited in Udayasankar, 2008). Medium-sized enterprises are less motivated to participate in CSR, because they are not forced by stakeholders due to their low visibility, and because they can resist pressure from stakeholders as they have resources and large scale of operations (Udayasankar, 2008).

22

Taking these arguments together, Udayasankar (2008) reasoned that both small and large firms can be motivated to participate in CSR, and therefore the relationship between firm size and CSR participation is U-shaped (Udayasankar, 2008). The study of Adams, Hill, and Roberts (1998) may indicate the existence of this U-shaped relationship as well, since super-large firms exceeding a 3 billion dollar turnover are disclosing significantly more corporate sustainability issues than their smaller competitors.

Although the Udayasankar’s study gives interesting insights on the concept firm size, it is only conceptual and empirically not validated yet. Besides, the link between firm size and CSR itself is widely recognised and accepted in literature (Brammer & Millington, 2005, as cited in Dam & Scholtens, 2013). Therefore, this study proposes that larger firms are likely to disclose more CSR information since they are facing higher public visibility. Therefore, the following proposition is formulated:

Proposition 1: larger firms disclose more CSR information

3.3.2 Corporate governance Multiple studies have been conducted to investigate whether corporate governance could influence the strategic choices of a firm. This study elaborates firstly on the definition of corporate governance, followed by explaining the differences between corporate governance systems in the dairy industry. Corporate governance can be defined as “the structure and systems of control by which managers are held accountable to those who have a legitimate stake in an organisation” (Johnson, Whittington, & Scholes, 2012, p. 82). These structures and systems can vary per country due to differences in legislation. The biggest difference between European firms in general is the use of a one- or two-tier governance structure. In the case of a one-tier governance structure, the supervisory board is included in the management board, thus control and execution are not decoupled (Kamer van Koophandel, 2019)1. In a two-tier governance structure, the supervisory board is decoupled from the management board. This is illustrated in Figure 2.

Particularly important are the differences in governance between cooperatives and private firms. Looking at the internal governance structure of a traditional cooperative, one can distinguish three entities, namely the General Assembly, the Board of Directors and the Supervisory board (Bijman, Hanisch, & van der Sangen, 2014). In the General Assembly, members of the cooperative elect the members of the Board of Directors. The directors are mandated by the members, to take the majority of the decisions (Bijman et al., 2014). The Supervisory Board monitors and controls the decisions taken by the Board of Directors. Private firms have similar governance structures, however, the General Assembly is replaced by the Shareholder Meeting. A major difference between cooperatives and private firms, is the power of members in the General Assembly, compared to the power of shareholders in the Shareholder Meeting. The General Assemblies often have a one-member-one-vote system (Bijman et al., 2014), while the power of shareholders is often determined via the percentage of holdings within of the firm. As a consequence, power and influence of the owners between private firms and cooperatives differ greatly. 1 The Dutch Chamber of Commerce

Figure 2. Corporate governance structures

23

The study of Marquis and Lee (2013), investigated the impact of organizational structure on strategies pursued by firms. In their study, they focussed on board structure in relation to corporate philanthropy. Corporate contributions are influenced by CEO tenure, director degree centrality, the board size, the percentage of women senior managers, and the percentage of women directors (Marquis & Lee, 2013). They state that shorter CEO tenure is positively and significantly associated with corporate philanthropy, as new CEOs tend to increase expenditure on philanthropy, while the opposite holds for longstanding CEOs (Marquis & Lee, 2013). Also, board size is positively, and significantly related to corporate philanthropy expenditure. A possible explanation given by Marquis, Glynn, and Davis (2007, as cited in Marquis & Lee, 2013), is that peer pressure within the organisation influences organisational strategy. It is important to mention that within larger boards, both the individual peer pressure and opportunities given by members to contribute to philanthropy are higher (Marquis & Lee, 2013). Lastly, Marquis and Lee (2013) found that the percentages of women in senior managers and board of directors, both positively and significantly influences the corporate contributions to philanthropy. This positive relation originates from the fact that women tend to contribute more to philanthropy compared to men (Marquis & Lee, 2013).

Moreover, results found by Webb (2004) indicated that socially responsible firms tend to have larger boards, more women on their boards and more independent board members. Independent board members are persons who are absent of any material conflict of interest (European Commission, 2005). Independent board members positively influence the CSR orientation, as they reduce opportunism and agency costs (Shaukat, Qiu, & Trojanowski, 2016). Independent board members are likely to be more objective and long-term focussed regarding the decision-making process (Shaukat et al., 2016). Furthermore, independent board members emphasize their external environment and legitimacy more than their insider counterparts (Shaukat et al., 2016). In other words, independent board members do not only act in the firms’ best interest, but also include the interests of stakeholders (Haniffa & Cooke, 2005).

In order to make corporate governance tangible, this study selected a number of metrics to reflect corporate governance. This study specifically focusses on the firms’ board to investigate the influence of corporate governance on CSR, as the board is the most important control mechanism of a firm (Hernández-Nicolás, Martín-Ugedo, & Mínguez-Vera, 2019). Hence, the board has the power to influence corporate strategy and thus CSR strategies. The study of Mohamed Adnan, Hay, and van Staden (2018) revealed that board size and board composition are often used metrics to express corporate governance. Board size can be defined as the number of members in the board, while board composition can be operationalised in different ways. This study chose to operationalise board composition via two metrics. Firstly, it operationalised board composition by using the percentage of female board members as this study found that there is a relationship between female representation in the board and CSR. Furthermore, some studies indicate that female representation between private firms and cooperatives might differ. To illustrate, the study of (Hernández-Nicolás et al., 2019) found that cooperatives have on average a slightly higher percentages of female board members (14%) than large firms (10%) and SMEs (8.4%) have on average (Hernández-Nicolás et al., 2019). This could indicate that, if cooperatives have a higher percentage of female board members, cooperatives disclose more information on CSR than private firms. Secondly, corporate governance is measured by using the percentage of independent board members, since literature stated that especially these board members include the perspective of the wider environment reflecting firms’ stakeholders. Based on the reviewed literature, the following propositions are formulated:

Proposition 2a: firms with larger boards disclose more CSR information

Proposition 2b: firms with a higher share of female board members disclose more CSR information

Proposition 2c: firms with a higher share of independent board members disclose more CSR

information

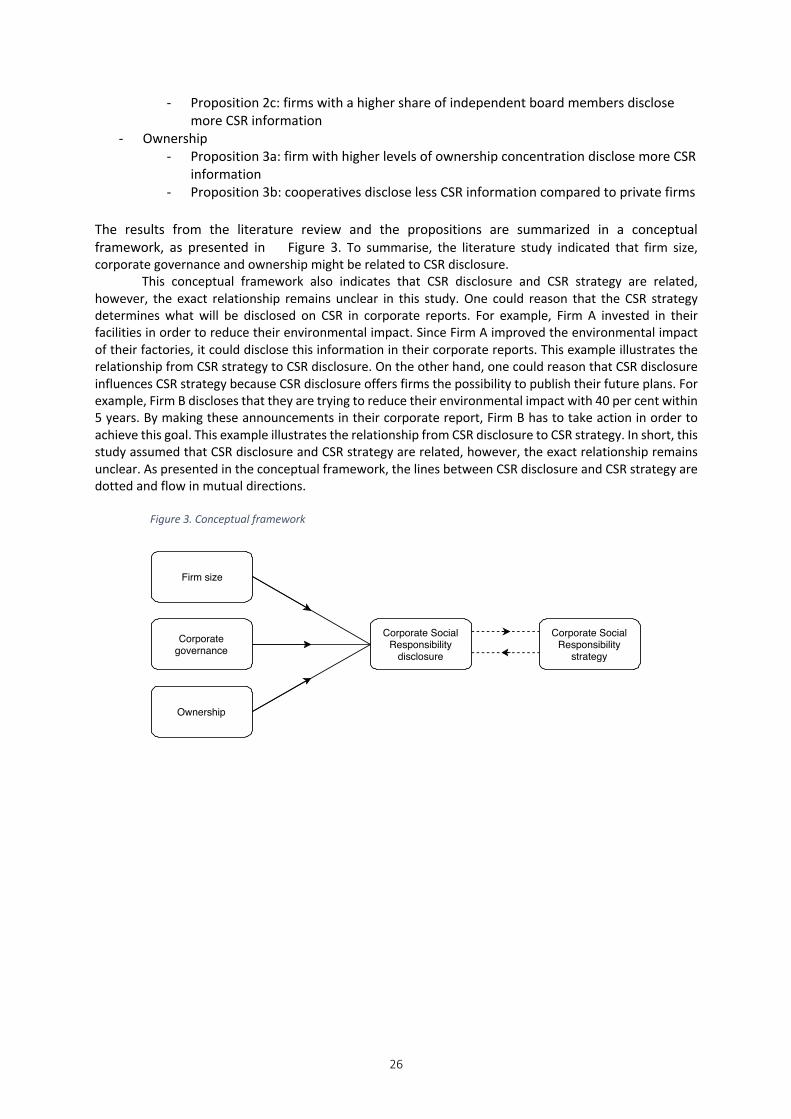

24