Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Expert Group onHousehold Income

Statistics

The Canberra International ExpertGroup on Household IncomeStatistics met between December1996 and May 2000 to developstandards on conceptual andpractical issues related to theproduction of household incomedistribution statistics. The aimwas to improve national andinternational statistics in this field.These recommendations are theculmination of the Group’s work.They will be of interest both to datacompilers and to data analysts aswell as to a wide range of users ofthese important statistics.

ISBN 0-9688524-0-8

cover.p65 2/14/2001, 3:56 PM1

Expert Group onHousehold Income

Statistics

The Canberra group

Final Reportand

Recommendations

Ottawa 2001

ISBN 0-9688524-0-8

Table of contents

The Canberra Group iii

Ackowledgements ............................................................................... ix

Preface .................................................................................... xi

SUMMARY ................................................................................... xiiiChapter 1 Introduction ............................................................................................................. xiiiChapter 2 The income concept ................................................................................................. xiiiChapter 3 Other conceptual issues ........................................................................................... xivChapter 4 From concept to practice ......................................................................................... xivChapter 5 Comparing income distributions over time .............................................................. xvChapter 6 Income dynamics ...................................................................................................... xvChapter 7 Data Presentation ..................................................................................................... xviChapter 8 Robustness assessment reporting ............................................................................. xviChapter 9 Issues for the future ................................................................................................. xvi

CHAPTER 1 Introduction ................................................................. 11.1 Aim of these guidelines .......................................................................................................... 11.2 Why is income distribution important? ............................................................................... 21.3 Economic well-being .............................................................................................................. 3

1.3.1 Income .................................................................................................................... 31.3.2 Change in value of net worth ...................................................................................... 41.3.3 Value of stock of net worth ......................................................................................... 4

1.4 Household income as a microeconomic and a macroeconomic concept ........................... 51.5 Historical background ........................................................................................................... 6

CHAPTER 2 The Income Concept ................................................ 112.1 Introduction .................................................................................................................. 112.2 Towards a definition of income ........................................................................................... 11

2.2.1 Historical background .............................................................................................. 112.2.2 The micro approach .................................................................................................. 12

2.2.2.1 Cash income .............................................................................................. 13Property income ........................................................................................ 13Cash transfers ............................................................................................ 13Deductions ................................................................................................ 14

2.2.2.2 Beyond cash income ................................................................................. 15Income in kind .......................................................................................... 15Changes in net worth ................................................................................ 15

2.2.3 Reconciling the micro and macro approaches .......................................................... 152.3 Income versus capital accumulation ................................................................................... 16

2.3.1 Current and capital transfers ..................................................................................... 162.3.2 Capital/holding gains ................................................................................................ 17

2.4 The components of income and its aggregates .................................................................. 172.4.1 Introduction .............................................................................................................. 172.4.2 Total income and its components ............................................................................. 19

2.4.2.1 Employee income ..................................................................................... 192.4.2.2 Income from self-employment .................................................................. 192.4.2.3 Income from rentals .................................................................................. 192.4.2.4 Property income ........................................................................................ 202.4.2.5 Current transfers received ......................................................................... 202.4.2.6 Total income .............................................................................................. 22

2.4.3 Disposable income .................................................................................................... 22

Table of contents

iv The Canberra Group

Table of contents2.4.3.1 Current transfers paid ................................................................................ 222.4.3.2 Disposable income .................................................................................... 22

2.4.4 Adjusted disposable income and social transfers in kind ......................................... 222.4.4.1 Social transfers in kind ............................................................................. 22

2.4.5 Choosing between income measures ........................................................................ 242.4.5.1 Total, disposable and adjusted disposable income ................................... 242.4.5.2 Cash only or cash and non-cash income ................................................... 25

2.5 Extension to consumption and accumulation .................................................................... 252.5.1 Introduction .............................................................................................................. 252.5.2 Household consumption expenditure ....................................................................... 25

2.5.2.1 Inter-household transfers .......................................................................... 262.5.2.2 Voluntary transfers between households and other units .......................... 27

Transfers to charities ................................................................................. 27Lotteries and gambling ............................................................................. 27Non-life insurance ..................................................................................... 28

2.5.3 Holdings gains and losses ......................................................................................... 28

CHAPTER 3 Other Conceptual Issues ......................................... 313.1 Introduction .................................................................................................................. 313.2 Accounting period ................................................................................................................ 313.3 Statistical units .................................................................................................................. 32

3.3.1 Introduction .............................................................................................................. 323.3.2 Definitions of statistical units ................................................................................... 33

3.3.2.1 Unattached individuals - Persons not in families: ..................................... 333.3.2.2 Households ............................................................................................... 34

Definition .................................................................................................. 34Impact on the income sharing assumption ............................................... 34Practical measurement implications ......................................................... 35Associating persons with dwellings: ........................................................ 35Definition of a dwelling: ........................................................................... 36

3.3.2.3 Broadly defined families ........................................................................... 36Definition .................................................................................................. 36Impact on the income sharing assumption ............................................... 36

3.3.2.4 Nuclear families ........................................................................................ 36Definition .................................................................................................. 36Impact on the income sharing assumption ............................................... 36

3.3.3 Choice of unit and the measurement of income ....................................................... 373.3.3.1 Owner-occupied housing .......................................................................... 373.3.3.2 Goods and services provided to employee as part of employment

package ..................................................................................................... 373.3.4 Recommendations for harmonised statistical units .................................................. 383.3.5 Equivalence scales .................................................................................................... 403.3.6 Population weighting ................................................................................................ 41

3.4 Use of price indices ............................................................................................................... 423.5 Use of Purchasing Power Parities ....................................................................................... 43

CHAPTER 4 From Concepts to Practice ...................................... 454.1 Introduction .................................................................................................................. 454.2 Data availability .................................................................................................................. 47

4.2.1 Introduction .............................................................................................................. 474.2.2 The metasurvey ......................................................................................................... 474.2.3 The results ................................................................................................................. 48

4.2.3.1 Employee income ..................................................................................... 48

Expert Group on Household Income Statistics

The Canberra Group v

4.2.3.2 Income from self-employment .................................................................. 484.2.3.3 Income from rentals .................................................................................. 494.2.3.4 Property income ........................................................................................ 494.2.3.5 Current transfers received ......................................................................... 494.2.3.6 Deductions of current transfers paid ......................................................... 494.2.3.7 Social transfers in kind ............................................................................. 504.2.3.8 Other items ................................................................................................ 50

4.2.4 Conclusions .............................................................................................................. 504.3 Assessing the validity of income distribution results ......................................................... 51

4.3.1 Introduction .............................................................................................................. 514.3.2 Imperfections and ambiguities in income data ......................................................... 51

4.3.2.1 Incomplete coverage of the population ..................................................... 524.3.2.2 Other groups who may be excluded from surveys are: ............................ 524.3.2.3 Representativeness of sample ................................................................... 534.3.2.4 Inaccurate income data on those who are represented in the dataset ....... 534.3.2.5 Other imperfections in income data .......................................................... 55

4.3.3 Results sensitive to equivalence scales ..................................................................... 564.3.4 Price indices .............................................................................................................. 57

4.4 Options for choice of a practical definition ........................................................................ 584.4.1 Producing comparable estimates .............................................................................. 584.4.2 Experiences from the Luxembourg Income Study (LIS) ......................................... 594.4.3 A practical definition of income for international comparisons ............................... 604.4.4 Towards a more complete income definition ............................................................ 62

4.4.4.1 Property Income, Self-Employment Income and Own AccountProduction ................................................................................................. 63

4.4.4.2 Net Imputed Rent for Owner-Occupied Dwellings. ................................. 634.4.4.3 Social Transfers In-Kind. .......................................................................... 644.4.4.4 Capital gains ............................................................................................. 66

CHAPTER 5 Comparing Income Distributions Over Time .......... 695.1 Introduction .................................................................................................................. 695.2 Impact of measurement error ............................................................................................. 705.3 Issues for the data originator .............................................................................................. 715.4 Issues for secondary dataset producers .............................................................................. 725.5 Issues for the end user .......................................................................................................... 74

5.5.1 Detecting Trends ....................................................................................................... 745.5.2 Significance of Changes ........................................................................................... 775.5.3 Trends versus episodes ............................................................................................. 78

CHAPTER 6 Income Dynamics ..................................................... 816.1 Introduction .................................................................................................................. 816.2 The relative advantages and disadvantages of longitudinal surveys ............................... 816.3 International examples of longitudinal income surveys ................................................... 83

6.3.1 Survey of Labour and Income Dynamics ................................................................. 836.3.2 Panel Study of Income Dynamics ............................................................................ 846.3.3 Survey of Income and Program Participation ........................................................... 846.3.4 European Community Household Panel Survey ...................................................... 84

6.4 Some applications of longitudinal surveys ......................................................................... 846.4.1 Labour Market Dynamics ......................................................................................... 856.4.2 Family Economic Mobility ....................................................................................... 866.4.3 Low income dynamics .............................................................................................. 86

Table of contents

Table of contents

vi The Canberra Group

CHAPTER 7 Data Presentation ..................................................... 897.1 Introduction .................................................................................................................. 897.2 Units of analysis and classification ..................................................................................... 897.3 Summary measures of income level: the mean and the median ...................................... 927.4 Measures of income dispersion ........................................................................................... 93

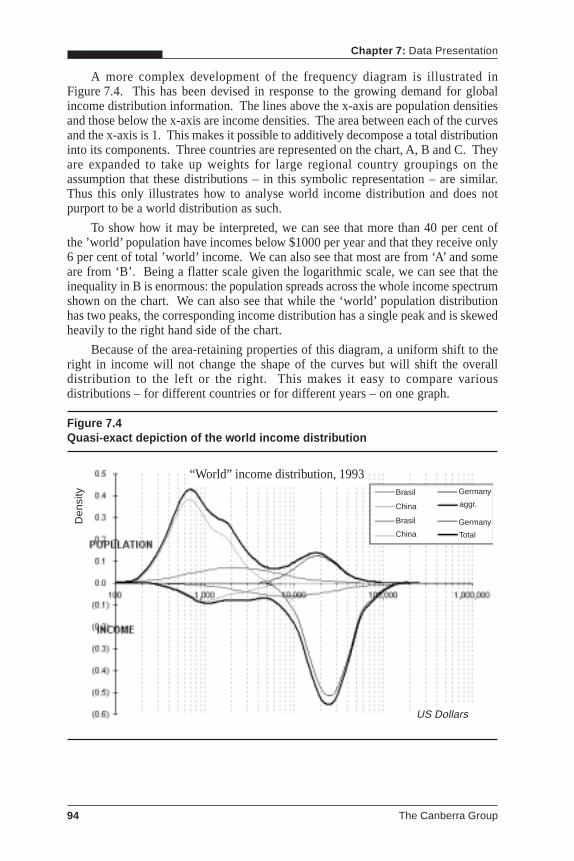

The frequency diagram .......................................................................................................... 937.4.1 The Lorenz curve ...................................................................................................... 957.4.2 The Gini coefficient .................................................................................................. 967.4.3 Quantile groups ........................................................................................................ 977.4.4 Other summary measures ....................................................................................... 101

7.5 Income composition ........................................................................................................... 102

CHAPTER 8 Robustness Assessment Reporting ..................... 1038.1 Introduction ................................................................................................................ 1038.2 Guiding principles .............................................................................................................. 103

Robustness of income distribution results to data imperfections ........................... 105

CHAPTER 9 Issues for the Future9.1 Introduction ................................................................................................................ 1079.2 Where next for household economic well-being? ............................................................ 108

9.2.1 Transfers within and between households .............................................................. 1089.2.2 Relationships between income, expenditure and wealth ........................................ 1099.2.3 Non-monetary income from household production ............................................... 110

9.3 Challenges for income measurement from economic transformation ........................... 1129.3.1 Changing role of the public and private sectors ..................................................... 1129.3.2 Informal sector ........................................................................................................ 113

Appendix 1 Definitions of the Components of Income ............ 1151. Employee income ................................................................................................................ 115

1.1 Cash wages and salaries ......................................................................................... 1151.2 Tips and bonuses .................................................................................................... 1151.3 Profit sharing including stock options .................................................................... 1161.4 Severance and termination pay ............................................................................... 1161.5 Allowances payable for working in remote locations etc, where part of1.6 Employers’ social insurance contributions ............................................................. 1171.7 Goods and services provided to employee as part of employment package .......... 118

2. Income from self-employment ........................................................................................... 1182.1 Profit/loss from unincorporated enterprise ............................................................. 1182.2 Royalties ................................................................................................................ 1192.3 Income from goods and services produced for barter ............................................ 1202.4 Goods produced for home consumption ................................................................ 1202.5 Income less expenses from owner-occupied dwellings .......................................... 120

3. Income less expenses from rentals, except rent of land .................................................. 1214. Property income received .................................................................................................. 122

4.1 Interest received less interest paid .......................................................................... 1224.2 Dividends received ................................................................................................. 1234.3 Rent from land ........................................................................................................ 123

5. Current transfers received ................................................................................................. 1235.1 Social insurance benefits from employers’ schemes .............................................. 1245.2 Social insurance benefits in cash from government .............................................. 1255.3 Universal (ie not means-tested) social assistance benefits in cash

from government .................................................................................................... 1255.4 Means-tested social assistance benefits in cash ...................................................... 126

Table of contents

Expert Group on Household Income Statistics

The Canberra Group vii

5.5 Regular inter-household cash transfers received .................................................... 1265.6 Regular support received from non-profit institutions including charities ............. 127

6. Total Income ................................................................................................................ 1277. Deductions from Income of Current Transfers Paid ....................................................... 128

7.1 Employers’ social insurance contributions ............................................................. 1287.2 Employees’ social insurance contributions ............................................................. 1287.3 Taxes on income ..................................................................................................... 1297.4 Regular taxes on wealth .......................................................................................... 1307.5 Regular inter-household cash transfers ................................................................... 1307.6 Regular transfers to non-profit institutions including ............................................. 131

8. Disposable Income .............................................................................................................. 1319. Social Transfers in Kind (STIK) Receivable ................................................................... 13110. Adjusted Disposable Income ............................................................................................. 132

APPENDIX 2 Reconciliation of micro-macro conceptsand terminology ...................................................... 133

1. Introduction ................................................................................................................ 1331.1 Type of income or means of payment .................................................................... 133

2. Receipts in cash (Column A) ............................................................................................. 1342.1 Income from involvement in production ................................................................ 1342.2 Property income ...................................................................................................... 1362.3 Transfers 1372.4 Taxes on income, wealth etc. .................................................................................. 141

3. Receipts in kind (Column B) ............................................................................................ 1424. Receipts of forced saving (Column C) .............................................................................. 142

4.1 Employers’ social insurance contributions ............................................................. 1424.2 Property income ...................................................................................................... 1434.3 Pension fund adjustment ......................................................................................... 1434.4 Capital gains ........................................................................................................... 144

5. Own account production of goods and owner occupied dwellings (Column D) ........... 1445.1 Own account production ........................................................................................ 1445.2 Owner occupied housing ........................................................................................ 144

6. Own account production of services (Column E) ............................................................ 1457. Social transfers in kind (Column F) ................................................................................. 1458. Corresponding outgoings (Column G) ............................................................................. 1469. Introducing income aggregates ......................................................................................... 146

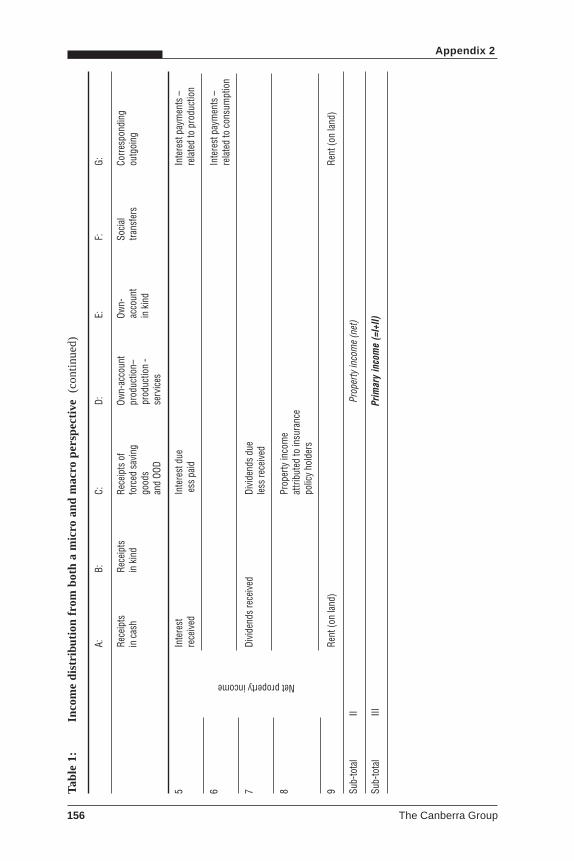

9.1 Primary income ....................................................................................................... 1479.2 Total income, disposable income and adjusted disposable incomme .................... 148

10. Extending the table to consumption and accumulation .................................................. 14810.1 Consumption expenditure ....................................................................................... 14910.2 Saving 15210.3 Accumulation entries .............................................................................................. 152

11. Reconciliation with SNA/macro aggregates ..................................................................... 15312. Conclusion ................................................................................................................ 154

APPENDIX 3 Purchasing Power Parities ..................................... 1611. What is a Purchasing Power Parity? .................................................................................... 1612. How is a PPP calculated? ..................................................................................................... 1613. Periodicity ................................................................................................................ 1624. Updating PPPs ................................................................................................................ 1625. Which PPP? ................................................................................................................ 1636. Representativity and comparability ..................................................................................... 164

Table of contents

Table of contents

viii The Canberra Group

7. PPPs for different income groups? ....................................................................................... 1648. Conclusion ................................................................................................................ 166

APPENDIX 4 Availability of Income Data .................................... 167

APPENDIX 5 Robustness of National Accounts Estimates ....... 1791. Overview ................................................................................................................ 1792. The output measure .............................................................................................................. 1793. The income measure ............................................................................................................ 1804. The expenditure measure ..................................................................................................... 1815. Reconciling the three measures ............................................................................................ 182

APPENDIX 6 Robustness Assessment Report for IncomeDistribution Data ..................................................... 183

Appendix 7 Extract from “Recommendations of the TaskForce on Statistics on Social Exclusionand Poverty,” Eurostat, 1998 .................................. 191

Requirements for a First Release or Press Notice and for Statistics in Focus ................................. 191Requirements for more detailed reports .......................................................................................... 192Compendium, anthology or omnibus publications ......................................................................... 193

Bibliography ................................................................................. 195

List of Tables and FiguresTable 2.1 Definitions of income ............................................................................................. 18Table 2.2 Extension of definition of income to consumption and accumulation .................. 30Table 3.1 Canberra Group recommendations for harmonised statistical units ...................... 38Table 4.1 Components of disposable income ......................................................................... 61Appendix 2Table 1 Income distribution from both a micro and macro perspective ........................... 155Table 2 Extension to consumption and accumulation ....................................................... 159Appendix 4Table 1 Income Component code list ................................................................................ 168Table 2 Summary of Income Component Data Collection ............................................... 172

Chapter 5Figure 5.1 Inequality in country X: an illustration of three pitfalls ......................................... 75Figure 5.2 Trends in Income Inequality: Gini Coefficients in country Y ................................ 76Figure 5.3 Trends in Income Inequality: Gini Coefficients (1986=1) in country Z ................ 77Figure 5.4 Trends in Income Inequality (Gini coefficients)Percentage

Change per Year and Absolute Change per Year: 1979-97 ..................................... 78Figure 5.5. Trend in Income Inequality: Gini Coefficients (1983=1) in country H ................. 79

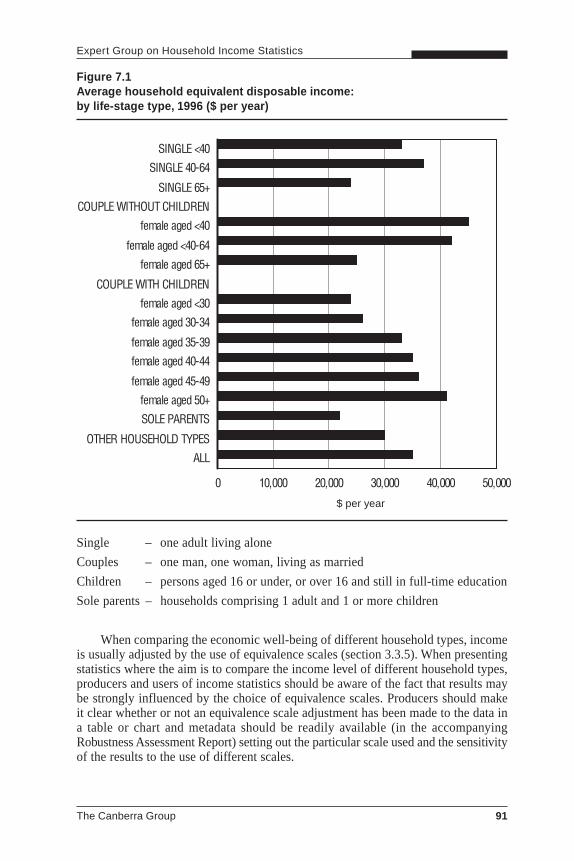

Chapter 7Figure 7.1 Average household equivalent disposable income: by life-stage type,

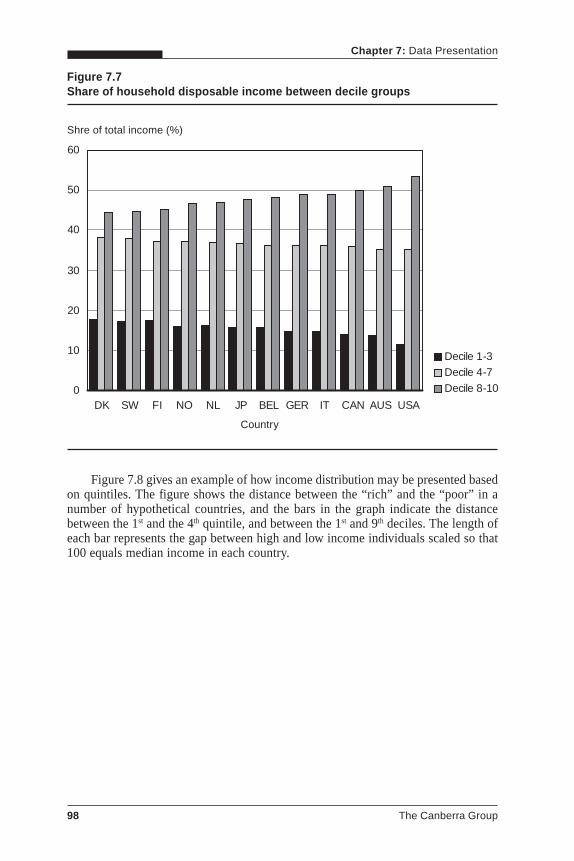

1996 ($ per year) .................................................................................................... 91Figure 7.2 Changes in mean and median household equivalent disposable income ............... 92Figure 7.3 Frequency distribution of income ........................................................................... 93Figure 7.4 Quasi-exact depiction of the world income distribution ........................................ 94Figure 7.5 Lorenz curves for the distribution of equivalent household disposable income .... 95Figure 7.6 Lorenz curves for the distribution of equivalent household disposable income .... 96Figure 7.7 Share of household disposable income between decile groups ............................. 98Figure 7.8 The distance1 between the 1st and the 4th quintiles and the 1st and 9th deciles ........ 99Figure 7.9 Ratios between decile group shares of income (A) and between

decile points (B) ................................................................................................... 100

Table of contents

Ackowledgements

The Canberra Group ix

This report has been made possible through the contributions of all those listed belowwho attended one or more of the four meetings of the Canberra Group. All tookpart as experts in the field of income distribution statistics rather than as membersof a particular organisation though their institutional affiliation (at the time of themeeting(s) they attended) is also given.

Particular thanks are due to the members of the Editorial Review Board whotook responsibility for agreeing the final text with valuable input from members ofthe whole Canberra Group:

Jenny Church (Consultant Editor)Anne Harrison (OECD)Marion McEwin (Australian Bureau of Statistics)Leon Pietsch (Australian Bureau of Statistics)Mike Sheridan (Statistics Canada)Timothy Smeeding (Luxembourg Income Study)Paul Van Der Laan (Statistics Netherlands)Daniel Weinberg (US Bureau of the Census)

A. National organisationsAUSTRALIAAcademy of Social Sciences

Ian CastlesAustralian Bureau of Statistics

Marion McEwinHarry KroonMaureen McDonaldGeorge Sarossy

Commonwealth TreasuryPhil Gallagher

Department of Social SecurityPeter Whiteford

National Centre for Social andEconomic Modelling

Ann HardingUniversity of Melbourne

Duncan Ironmonger

CANADAInformetrica Limited

Michael McCrackenStatistics Canada

Cathy CottonIan MacredieMike SheridanMaryanne WebberStew Wells

CHINAState Statistical Bureau

Qingxin MengTing Shi

FINLANDStatistics Finland

Veli-Matti TörmälehtoPekka Ruotsalainen

Table of contents

x The Canberra Group

GERMANYGerman Institute for Economic Research

Gert WagnerINDIADepartment of Statistics

Prabhakar JoshiITALYBank of Italy

Giovanni D’AlessioJAPANStatistics Bureau

Takehiro FukuiYoshiyuki Kobayashi

KOREANational Statistical Office

Sa-Im WooMALAYSIADepartment of Statistics

Abdul Rahman HasanSaidah Hashim

MEXICOInstituto Nacional de Estadistica,Geografia e Informática

Patricia Méndez CarniadoNETHERLANDSMinistry of Finance

Leo van den EndeStatistics Netherlands

Wim BosBen GrubbenPaul van der LaanPeter MeuwissenJos SchiepersClemens SiermannLourens Trimp

NEW ZEALANDStatistics New Zealand

Dianne MacaskillJohn ScottHelen Stott

NORWAYStatistics Norway

Jon EplandSWEDENStatistics Sweden

Kjell JanssonLeif Johansson

UNITED KINGDOMDepartment of Social Security

Gordon HarrisOffice for National Statistics

Tim HarrisNigel Stuttard

UNITED STATESBureau of the Census

Daniel WeinbergBureau of Labor Statistics

Thesia Garner

B. International agenciesCentre d’Études de Populations, dePauvreté et de Politiques Socio-économiques/International Network for Studies inTechnology, Environment, Alternatives,

Development (CEPS/INSTEAD)Frédéric BergerUwe Warner

Statistical Office of the EuropeanCommunities (EUROSTAT)

Antonio BaigorriAnne ClemenceauPieter EveraersAlfred Franz (Consultant)Eric MarlierLene MejerJohn Walton (Consultant)Christine Wirtz

Inter-American DevelopmentBank (IADB)

José Antonio MejíaInternational Labour Office (ILO)

Marie-Thérèse DupréSylvester Young

Luxembourg Employment Study(LES) at CEPS/INSTEAD

Jean-Yves BienvenueJean-Marie Jungblut

Luxembourg Income Study (LIS)at CEPS/INSTEAD

Paul AlkemadeAnn MorissensTim SmeedingKoen Vleminckx

Organisation for EconomicCo-operation and Development (OECD)

Heinrich BrünggerAnne HarrisonPeter Scherer

United Nations Economic Commissionfor Latin America and the Caribbean(ECLAC)

Juan Carlos FeresPedro Sáinz

The World BankHaeduck LeeMichael Ward

Preface

The Canberra Group xi

T he initiative to organise an International Expert Group on Household IncomeStatistics was taken by the Australian Bureau of Statistics in order to workon the development of statistics on household economic well-being and

particularly on household income. The initiative was a reaction to a growingawareness that, in advancing the quality of their own household income statistics,national statistical offices shared many problems. In particular the comparative OECDstudy on income distribution (Atkinson et al. 1995) triggered off a renewed discussionon the underlying quality and comparability of household income data. Expectationswere that combining forces would help solve conceptual and methodologicalproblems, and would thus result in more relevant and reliable national statistics whichcould also be used for international comparisons on income distribution.

The International Expert Group met for the first time in Canberra, Australia and,taking its name from the venue of the First Meeting, is known as the ‘CanberraGroup’. It follows a now well-established phenomenon of City-named Expert Groupsset up under the auspices of the United Nations Statistical Commission. The traditionstarted with the Voorburg Group on service statistics, which was first set up in 1986and first met in Voorburg, the Netherlands, in January 1987. According to the UnitedNations Statistical Commission the role of City Group is:

• To contribute actively to the development of international standards in theirrespective areas of work, within the framework set by the international workprogramme;

• To exchange best practices in their area of work;

• To produce specific outputs (advice, classifications, manuals) requested by theStatistical Commission.

Objectives of the Canberra GroupThe primary objective of the Canberra Group was to enhance national householdincome statistics by developing standards on conceptual and practical issues relatedto the production of income distribution statistics. Its work was in support of arevision of international guidelines on income distribution statistics. The Group wouldaddress collectively the common conceptual, definitional and practical problems facedby national and international statistical agencies in this subject area and would actas a forum for expert opinions on conceptual and methodological issues and for

Preface

xii The Canberra Group

obtaining endorsement for guidelines. It was hoped that a combined approach tosolving these conceptual and methodological problems would result not only inimproved national statistics, but also in improved data for international comparisonson household income distribution.

Meetings and participantsThe Canberra Group was designed to be a flexible working group of experts inhousehold income statistics from both national and international organisations.Members of the Group included representatives from national statistical agencies,government departments and research agencies from Europe, North and SouthAmerica, Asia, Australia and New Zealand as well as from a number of internationalorganisations and research agencies. All members attended as experts rather thanofficial representatives of their organisations. A central tenet of all City Groups isthat their members take part in a personal capacity without necessarily committingtheir employers. At the outset, the Group decided that English should be its soleworking language.

From December 1996 to May 2000 the Canberra Group met four times. Over70 participants from 26 national organisations and 7 international organisations wereinvolved in the work of the Canberra Group (See Acknowledgements page at thefront of this volume). Reports of the First, Second and Third Meeting of the CanberraGroup were published in February 1997, May 1998 and November 1999 respectively(See International Expert Group on Household Income Statistics 1997, 1998 and1999). This document represents the final Report of the Group.

The Group’s work has benefited from contributions from other individuals andorganisations. Professor A B Atkinson (Nuffield College, Oxford) and Mr AndreaBrandolini (Bank of Italy, Research Department) have both made major contributionsto papers discussed by the Group. The discussions of the Expert Group meeting onIncome Distribution Statistics convened by Eurostat in December 1999 provided anadditional forum. The International Association for Research into Income and Wealthhas played a major role both in the birth of the Group as a result of a session onInternational Standards on Income and Wealth Distribution at its 24th GeneralConference at Lillehammer, Norway in August 1996, and in enabling peer reviewof the Group’s outputs at a session at the 26th General Conference in Cracow, Polandin August 2000 when some of the draft chapters of this Report were presented anddiscussed.

Summary

The Canberra Group xiii

Chapter 1 Introduction… sets out the aims of these Guidelines and their intended audience, and describestheir historical background. They are a guide to compilers, and also data analystsand other users, on how to prepare harmonised and comparable statistics on householdincome distribution. The manual represents a synthesis of prevailing ideas and triesto be faithful to the concept of income and its theoretical definition, while takingaccount of the practical difficulties of data collection and presentation.

The main motivation for the production of household income statistics is themeasurement of economic well-being. However, income is not the only way in whichthe concept of economic well-being can be characterised, and this introductorychapter also considers the broader conceptual issues underlying its nature.

Although the Guidelines are primarily aimed at the users and producers of micro-level income statistics, the concept of household income is equally familiar to nationalaccounts practitioners. As in practice the two sets of statistics are rarely produced ina harmonised manner, however, the manual attempts to interpret the differences ofapproach and terminology to what is in fact a single concept.

Chapter 2 The income concept… seeks to establish conceptual groundrules for defining and measuring householdincome, ignoring for the time being considerations of data quality and availability.A hierarchy of components of income is built up which provides definitions of total,disposable and adjusted disposable income, described in more detail in Appendix 1.Appendix 2 reconciles these micro concepts with the macro concepts familiar tonational accountants, demonstrating how the different categories of income can beassembled to meet the needs of different types of analyses coming from the twotraditions.

THE CANBERRA GROUP RECOMMENDS THAT THECONCEPTUAL FRAMEWORK SET OUT IN TABLE 2.1 BE ADOPTEDAS THE FRAMEWORK FOR INCOME DISTRIBUTION ANALYSIS,RECOGNISING THAT NOT ALL OF IT CAN BE IMPLEMENTED FORPRACTICAL PURPOSES.

This chapter also explains how the concept of income is related to those ofhousehold consumption and capital accumulation.

Summary

xiv The Canberra Group

Chapter 3 Other conceptual issues… discusses the other important conceptual issues which have to be resolved beforeincome distribution statistics can be compiled. It is necessary to decide whichstatistical units are to be used and the length of the accounting period to which thestatistics refer. If households are the chosen unit, then the effect of variation in theirsize and composition on their relative needs has to be taken into account. The use ofequivalence scales to adjust for such differences is discussed.

THE CANBERRA GROUP RECOMMENDS THAT THE ACCOUNTINGPERIOD TO BE USED FOR INCOME DISTRIBUTION ANALYSISSHOULD BE ONE YEAR, AND THAT THE HOUSEHOLD, ASDEFINED IN TABLE 3.1, BE ADOPTED AS THE BASIC STATISTICALUNIT, WITH THE OTHER UNITS SET OUT IN TABLE 3.1 ASALTERNATIVES FOR PARTICULAR PURPOSES.

THE GROUP FURTHER RECOMMENDS THAT INCOME SHOULDBE ADJUSTED TO TAKE ACCOUNT OF HOUSEHOLD SIZE, USINGEQUIVALENCE SCALES.

Most comparisons of income distribution statistics across time or betweencountries are made in relative terms using measures which are invariant to absolutelevels of income. However, if income distribution statistics expressed in money termsare to be compared either spatially or temporally, an added consideration is how totake account of price differences in order to compare real incomes. For validcomparisons of real incomes between countries or other geographic areas, the useof Purchasing Power Parities is discussed, and for comparisons within a country theuse of relevant price indices is addressed. Appendix 3 provides background onPurchasing Power Parities.

THE CANBERRA GROUP RECOMMENDS THAT WHEN CROSS-COUNTRY COMPARISONS OF REAL INCOMES ARE TO BE MADE,PURCHASING POWER PARITIES SHOULD BE USED INPREFERENCE TO EXCHANGE RATES.

Chapter 4 From concept to practice… provides an overview of the practical considerations which will determine theparameters for the production of a set of income distribution statistics. These are:

• Availability of data

• Quality of available data

• Purposes for which the statistics are required

The Canberra Group carried out a metasurvey of data availability in 25 countriesfrom all continents, the results of which are summarised here (details may be foundin Appendix 4). This illuminates differences in current practice and the extent to

Expert Group on Household Income Statistics

The Canberra Group xv

which they might allow the development and implementation of a consistentdefinition.

It is not enough that data are available from which income distribution statisticscan be compiled: they must be fit for purpose. This chapter goes on to identify themain sources of error or uncertainty which may underlie income distribution results,and draws on a survey of data quality amongst Canberra Group members to indicatewhich difficulties appear to be widespread. National Accounts aggregates are oneyardstick against which the quality of income distribution statistics may be assessed,though these themselves have some uncertainties as discussed in Appendix 5.

Both data availability and data quality will affect the choice of income definition.The options for choice of a practical income definition are discussed in the contextof making cross country comparisons and are developed based on the experience ofthe Luxembourg Income Study.

THE CANBERRA GROUP RECOMMENDS THAT THE PRACTICALDEFINITION OF INCOME SET OUT IN TABLE 4.1 BE ADOPTED FORUSE IN MAKING INTERNATIONAL COMPARISONS OF INCOME

Priorities are also suggested for the development of a more complete incomedefinition.

Chapter 5 Comparing income distributionsover time

… discusses the consistency requirements for making valid cross-time comparisonswithin a country, as well as the additional difficulty of comparing time trends acrosscountries. In this context guidance is provided for primary data producers; for thecompilers of secondary datasets which bring together time series estimates formultiple nations; and for the researchers and analysts who use both primary andsecondary sources.

THE CANBERRA GROUP RECOMMENDS THAT PRIMARY ANDSECONDARY PRODUCERS OF INCOME DISTRIBUTION STATISTICSBE MORE AWARE OF THE NEEDS OF USERS FOR TIME SERIES DATAAND THAT IMPROVEMENTS IN THE AVAILABILITY OF BOTH DATAAND METADATA BE GIVEN PRIORITY

Chapter 6 Income Dynamics… draws attention to the fact that cross-sectional data have a number of limitationsfor the study of change over time in income distributions. Longitudinal (panel) datahave an important role in providing insight into the way in which households ofdifferent types move within the distribution over time. However, they have drawbacksalso, in terms of attrition bias and cost of collection. Examples of panel surveys andtheir use are presented.

Summary

xvi The Canberra Group

Chapter 7 Data Presentation… provides a practical guide to presenting complex income distribution statistics ina clear, unambiguous and user-friendly manner, through the provision of a widevariety of examples. The user is warned of some of the pitfalls in presenting andinterpreting income distribution statistics, based on Canberra Group members’experiences.

Chapter 8 Robustness Assessment Reporting… complements the previous chapter, in that when the results of income distributionstudies are presented, they should always be accompanied by full information onthe sources and methods employed, and an assessment of their quality. It providesrecommendations on the forms of reporting which may be appropriate in individualanalyses and at various stages of producing and using income distribution statistics.A template for a robustness assessment report is set out in Appendix 6, andAppendix 7 presents Eurostat recommendations for presenting robustness data forestimates at varying levels of detail.

THE CANBERRA GROUP RECOMMENDS THAT INCOMEDISTRIBUTION STATISTICS BE ALWAYS ACCOMPANIED BYROBUSTNESS ASSESSMENT REPORTS AS SET OUT IN APPENDIX 6,SO THAT USERS MAY JUDGE THEIR FITNESS FOR PURPOSE.

Chapter 9 Issues for the future… draws together a number of issues which the Canberra Group recognise have stillto be resolved and which require further work. Some have already been touched onin earlier chapters – for example, the importance of expenditure and wealth ascomplementary measures of economic well-being. There is also a range ofdevelopments in the world economy which provide conceptual and methodologicalchallenges to the ways in which household income is measured today.

This chapter sets out this future agenda, hoping that others will rise to thechallenges it presents.

THE CANBERRA GROUP RECOMMENDS THAT THESEGUIDELINES BE PERIODICALLY REVIEWED TO ENSURE THATTHE ADVICE IS KEPT UP-TO-DATE WITH DEVELOPMENTS IN THEPRACTICE OF INCOME DISTRIBUTION COMPILATION AND INTHE ECONOMIC AND SOCIAL CONTEXTS IN WHICH THESTATISTICS ARE USED.

Chapter 1

Introduction

The Canberra Group 1

1.1 Aim of these guidelinesThis document is a guide to compilers, and hence data analysts and other users, onhow to prepare harmonised and comparable statistics on income distribution. It is asynthesis of prevailing ideas which tries to reconcile the dual concerns to be faithfulto the conceptual nature of income and its theoretical definition, whilst taking intoaccount the practical difficulties of data collection and compilation including thecosts involved both to the agencies producing the statistics and the householdsproviding the raw material.

The aim is to lay down useful guidelines for understanding the complex natureof income data, set in the context of prevailing ideas and best practices. These reflecthow economic societies are organised and people conduct their lives. Over thepassage of time, with social and political transformation, changes in the role ofgovernment, globalisation and so on, economic issues and priorities will change. Itis thus essential to retain a certain degree of flexibility in developing general standardsfor statistics on this topic. Thus, acknowledging that there is no single concept orset of concepts that fit all circumstances, the guidelines do not attempt to propose adefinitive set of standards for the compilation of income distribution statistics. Ratherthe aim is to give a systematic presentation of all the issues, both conceptual andpractical, which should be considered by producers and users of income distributionstatistics. Where sufficient consensus exists about best practice, recommendationsare made, in the hope that this will contribute in due course to the availability ofmore accurate, complete, and internationally comparable income statistics compiledto common standards. This should in turn lead to greater transparency in theirpresentation, and better informed use of what are inevitably some of the most complexstatistics produced by national and international organisations.

The guide is designed to be pragmatic. It is aimed mainly at those who areresponsible for compiling income distribution statistics, whether primary producers(originators) who collect and analyse data from primary sources or secondaryproducers who take processed data (micro, meso, or summary level) and derive theirown estimates and datasets from them. However, it will be of equal use to researchersand analysts who make use of the outputs from primary and secondary producers,in leading them to a better understanding of the underlying principles of incomedistribution statistics and the pitfalls in their practical implementation.

Chapter 1: Introduction

2 The Canberra Group

1.2 Why is income distribution important?Economic analysts and policy makers identify three main purposes for compilinginformation on income distribution. The first is driven by a desire to understandhow the pattern of income distribution can be related to patterns of economic activityand the returns to labour, capital and land, and to the way in which societies areorganised – ie to theoretical and institutional considerations. The second reflectsthe concern of policy makers to determine the need for both universal and sociallytargeted actions on different socio-economic groups and to assess their impact. Thethird is an interest in how different patterns of income distribution influence householdwell-being and people’s ability to acquire the goods and services they need to satisfytheir needs. These guidelines are driven by the need to produce statistics which fulfilall these purposes.

Producers of income distribution statistics therefore have to address suchquestions as:

• How unequal is the distribution of income in a given country? How does this comparewith earlier years, or with other countries?

• How many ‘poor’ people are there in a given country? How does this compare withearlier years, or with other countries?

• Who are the ‘poor’? Has this changed over time?

• Have the rich become richer? The poor become poorer?

The audience for income distribution statistics is usually less conscious of theambiguities surrounding concepts such as ‘income,’ ‘poor’ and ‘rich’ than are theproducers of the statistics. ‘Income’ may often be thought of by the user in terms ofcash income; the ‘poor’ are those whose lack of income means they are restricted toa low standard of living – i.e. there is an implicit assumption that ‘income’ constraintsare binding on poor people’s consumption - and the ‘rich’ are those who can afforda luxurious lifestyle. Typically, the main focus of interest is on changes over time,with differences between countries coming a close second. Statisticians’ statementsabout incomes are interpreted as statements about the living standards experiencedby different sections of the population; those with the lowest incomes are assumedto have the lowest living standards.

Thus interest in income distribution may be justified either per se as a way tosee how the benefits of national product are distributed across people, or indirectlyas the best proxy for the distribution of economic well-being. In a strictly utilitarianframework, the ideal measure of well-being would be the lifetime utility of a person.A utility measure should reflect differences in leisure as well as all forms of potentialconsumption, including home production and publicly provided goods; it should takeaccount of differences in constraints faced both by people living in the same country,and differences in constraints faced by people in different countries; it should accountfor differences in the ability to smooth income across periods. It is therefore clearthat household income measured over a period of perhaps a year is, at best, a proxyfor this ideal concept. On the other hand, income remains a fundamental determinantof people’s well-being in non-utilitarian frameworks, such as Sen’s capabilityapproach (Sen, 1992).

However, income is not the only way in which the concept of economic well-being can be characterised, and it is therefore useful first to consider the broaderconceptual issues underlying its nature, such as consumption, savings and wealth.

Expert Group on Household Income Statistics

The Canberra Group 3

1.3 Economic well-beingA household’s economic well-being can be expressed in terms of its access to goodsand services. The more that can be consumed, the higher the level of economic well-being, though the relationship between the two is not a linear one. Measuringconsumption might therefore be a way of measuring economic well-being. However,a household may be able to choose not to consume the maximum amount it couldin any given period but to save at least some of the resources it has available. Bysaving, households can accumulate wealth through the purchase of assets which willboth generate income at a later date and serve as a ‘nest-egg’ for spending at a latertime when income levels may be lower, or needs higher, than now. In addition topotentially earning a return for the household, ownership of wealth also affects theirbroader economic power. For example, wealthy households may find it easier togain credit to finance their consumption. Thus to capture the full extent of ahousehold’s economic well-being it is desirable to look at a number of differentaspects of their economic situation including not only income but also levels of wealth(hereafter referred to as level of net worth - assets minus liabilities) and changes inthe value of that wealth.

Analysis of economic well-being is usually primarily concerned with thecomparison of the actual or potential living standards of different groups in society,and sometimes between groups in different societies, at a point in time and also overa period of time. Policies to address problems of living standards usually focus onincome in some form or other. In other words, income is normally the most objectiveproxy for economic well-being for policy purposes. Therefore the focus of this reportis on measuring household income. But to be able to define income, and as a reminderthat income is not the only element of economic well-being, the remainder of thissection provides an overview of the relationship between economic well-being andincome, change in the value of net worth, and value of stock of net worth.

The economist’s concept of economic well-being also often encompasses thevalue of leisure time (or the disutility of labour). However, these guidelines assumethat income distribution statistics do not attempt to capture this element.

1.3.1 IncomeIn broad terms, income refers to regular receipts such as wages and salaries, incomefrom self employment, interest and dividends from invested funds, pensions or otherbenefits from social insurance and other current transfers receivable. Large andirregular receipts from inheritances and the like are considered to be capital transfersbecause it is unlikely that they will be spent immediately on receipt and are ‘one-off’ in nature.

Income presents a partial view of economic well-being and represents the regularor recurring receipts side of household economic accounts. It provides a measure ofresources available to the household for consumption and saving. On thedisbursements side of household accounts, consumption expenditure represents theday-to-day purchases that may be financed not only by regular or recurring incomebut also by savings from previous years or by incurring debt. For some households,such as retired households, the running down of capital for consumption mayrepresent a deliberate attempt on their part to even out consumption over a life time.Other groups in the population, such as farmers, may also average out their

Chapter 1: Introduction

4 The Canberra Group

consumption over a number of years while their incomes may show quite widefluctuations over the same period. In such cases, consumption expenditure mayrepresent a better estimate of the household’s sustainable standard of living.

There are difficulties in collecting data on both income and consumptionexpenditure in household surveys. Income is a sensitive issue for many respondentsand non-response or misreporting of some income components may be significant.On the other hand, data on consumption expenditure are often onerous and costly tocollect. In fact, the choice between the income or the consumption expenditureapproach to measuring economic well-being is often made for the analyst by thefact that income data may be more frequently available than data on consumptionexpenditure.

Nevertheless, it should be acknowledged explicitly at the outset that the approachto defining income taken in these guidelines is essentially consumption-based. Apositive resource flow (in money, goods or services) is considered as contributingtowards economic well-being if it increases the recipient’s potential to consume orsave, and a negative flow reduces well-being if it reduces the capacity to consumeor save.

1.3.2 Change in value of net worthWhether data on income or on expenditure are used for measuring economic well-being, the data should ideally be accompanied by some assessment of the change inthe value of the household’s net worth during the accounting period. If the level ofnet worth has increased, the increase will have resulted from saving (the differencebetween income and consumption), from the receipt of capital transfers, or from otherchanges in the value of assets, including capital or holding gains. Such a householdis likely to be better off in the long term than a household with a similar level ofconsumption that has financed this consumption by dissaving, that is, running downassets or incurring a liability. The question of whether the dissaving has beeninvoluntary or has been planned by saving in earlier periods is important in thiscontext.

1.3.3 Value of stock of net worthThe value of the stock of net worth owned by a household is the value of accumulatedassets less liabilities. As already noted, as well as possibly earning a return for thehousehold in the form of income, those households with high levels of net worthmay find it easier to gain credit for consumption or investment or to maximise thechoice of timing for different types of consumption. High levels of net worth canalso affect living standards by the potential for dissaving for consumption either nowor at a later date. For these reasons, it is important to ascertain, if possible, the valueof the household’s net worth to give a complete picture of the household’s commandover economic resources or economic well-being.

At a practical level, the collection of microdata on the assets and liabilities ofhouseholds can often be problematic. Such information may be even more sensitiveto the respondent than that on income and, because transactions are relativelyinfrequent, misreporting may be more prevalent. There are also considerabledifficulties in using data on stocks of wealth and data on transactions or flows in acombined measure of economic well-being. One option is to annuitise the net worthheld by the household and add this (notional) annuity to the flow of income and

Expert Group on Household Income Statistics

The Canberra Group 5

other receipts (Australian Bureau of Statistics, 1995). However, annuitisation of networth requires that a large number of value judgements and assumptions be madein relation to, for example, the period over which the net worth should be annuitised(life of the householder or spouse) and the interest rates to be used. This is not asimple matter, and the complexity suggests that the issue of incorporation of the valueof stocks of household net worth into a broader measure of economic well-beingmight be best treated in a separate study. The measurement of these stocks is thereforenot considered any further in these guidelines. However, the last section of Chapter 2sets out a conceptual framework in which income, consumption and accumulationcan be related to each other.

Ideally, analysis of economic well-being would benefit greatly from theavailability of fully articulated survey or administrative data covering all aspects:income, expenditure, saving, and the value of wealth held. This would enableobservation of the size and nature of the economic resource generated by households,and how they then disposed of it. Many of the uncertainties which exist, for exampleabout how to treat lump sum income receipts which some households might regardas additions to saving but others would spend immediately, would be resolved at themicro level by reference to observed behaviour. No catch-all assumptions wouldhave to be made either across all households or across groups of households.

However, collection of such fully articulated data is highly problematic from apractical point of view. Integrated income and expenditure surveys are conductedin some countries, more often in the developing than in the developed world. Somealso collect data on savings and other capital transactions and on net worth. However,the respondent burden is very high and even when data are collected on all of thesevariables they are rarely fully articulated and can raise as many questions as theyanswer. For example, the accounting period which is optimal, say, for collectingincome information may not be optimal for expenditure or capital transactions,leading to potential inconsistency and error in estimates of saving that are derivedfrom those aggregates. The same may be true of the reporting unit. Compromisechoices have to be made which may increase the ease and accuracy with which datacan be collected but reduce consistency between them. Integrated surveys also imposea heavy burden on respondents particularly in complex economies where even aquestionnaire concentrating only on cash income can take an interview of two hoursor more to administer. They are therefore very costly not just to the commissioningorganisation but also in the opportunity cost to the respondent. They are not thereforeconsidered further in these guidelines as feasible sources of internationallycomparable data.

1.4 Household income as a microeconomic and amacroeconomic concept

One of the major issues to emerge during the discussions of the Canberra Groupwas the existence of two traditions of household income measurement:

• the macro approach, having its roots in national accounts and in particular thestandards laid out in the System of National Accounts (SNA) (Commission of theEuropean Communities et al, 1993);

• the micro approach, having its roots in microeconomics and particularly the studyof poverty and its effect on different socio-economic groups within society.

Chapter 1: Introduction

6 The Canberra Group

The two traditions have tended to develop different terminologies andconventions, and often use different data sources. The difference of approach mightbe characterised in the contrast between the rigorous accounting framework of theSNA and the inherent flexibility of income micro-data.

Notwithstanding the differences of approach, it is important to stress that bothmacro and micro analysts are trying to measure the same concept: household income.Many of the conceptual difficulties encountered in drawing together the guidelineson household income distribution statistics are the same or similar to those faced indeveloping related guidelines such as the SNA. While the decisions made about howor how not to treat specific situations might sometimes be relatively arbitrary, it issensible to adopt a consistent treatment across frameworks whenever possible.

Indeed, the social accounting matrix (SAM) approach to national accounts asset out in the SNA, Chapter XX, typically focuses on the role of people within theeconomy. A SAM will invariably disaggregate the household sector in order to analysethe interrelationship between structural features of an economy and the distributionof income and expenditure among different socio-economic groups. In most SAMstherefore it is necessary to reconcile the macro aggregate of household income withthe micro income statistics on which the disaggregation is based. However, althoughthe intention of the SNA was in fact to include a disaggregation of household incomeby socio-economic group as a standard part of national accounts output, in practicethere are few if any countries who do so on a regular basis.

It can also be argued that most users of household income statistics would expectthe producers to have carried out a reconciliation between the macro aggregate ofhousehold income and the micro income statistics suitably grossed up to populationtotals. Even if this is not possible, at least one should expect to see clear explanationswhen discrepancies are known to exist. It is undoubtedly a considerable dis-serviceto users when two sets of statistics both labeled ‘household income’ appear to producequite different results and, possibly, different implications for social policy.Nevertheless such a reconciliation is rarely carried out by national statistics offices.

There are other practical reasons to try to maximise comparability betweenincome distribution statistics and household income as defined for the nationalaccounts. First, there is a greater likelihood that any datasets collected can be usedfor multiple purposes. Second, statistics compiled under the different frameworkscan be compared as part of a mutual checking process, and users can be confidentthat different sets of statistics can be brought together if so required for analyticpurposes.

Although these guidelines have been produced with the needs of the micro-analyst uppermost, they also draw attention to areas of difference between therecommendations and those of the SNA and how the two may be reconciled. Theintention is to aid understanding amongst micro-analysts of the concerns andconventions of the macroanalysts and thus to build bridges between the two.

1.5 Historical backgroundIncome distribution statistics were first on the agenda of the United Nations StatisticalCommission at its Fourteenth Session in 1966. Subsequently, a system of distributionstatistics was gradually developed by the United Nations Statistical Office, which

Expert Group on Household Income Statistics

The Canberra Group 7

covered income, consumption and accumulation of households and was tied in withboth earlier versions of the United Nations System of National Accounts and thenow obsolete System of Balances of the National Economy (MPS).

The United Nations Statistical Commission adopted a final version of the fullsystem at its Seventeenth Session in 1972. However, the Commission requested thatamendments and simplifications be made in the light of its discussions. A draft ofthe simplified system was presented to the Commission at its Eighteenth Session in1974 and was adopted with a number of reservations. In particular, the Commissionfelt that further simplification was desirable.

After careful consideration, the United Nations Statistical Office concluded thatit would be desirable to combine the full and the simplified versions of the Guidelinesand present them in a single publication. So, the Provisional Guidelines on Statisticsof the Distribution of Income, Consumption and Accumulation of Households werepublished by the Statistical Office of the United Nations in 1977 (M71, UnitedNations, 1977). Their aim was to assist developed and developing countries to collectand disseminate income distribution statistics and to provide for internationalreporting and publication of comparable data. The guidelines emphasised the needto link micro-level income distribution statistics with macro-level national accountingstandards. Surveys of national practices of income distribution statistics werepublished by the United Nations Statistical Office in 1981 and 1985 (United Nations,1981 and 1985).

The 1977 Provisional Guidelines were to be revised concurrently with therevision of the 1968 SNA (eg Norrlof ,1985). The United Nations EconomicCommission for Europe (UNECE) in particular began work on revising the 1977Provisional Guidelines and organised a number of Work Sessions and Seminars onstatistics of household income with this in mind. Special attention was paid to therelevance of the revision of the SNA (eg United Nations, 1989), given that the revisionprocess of the 1968 SNA had led to advances in conceptual thinking about thehousehold sector and about the concept of income in particular. However, due tolimited resources progress in the revision of the 1977 Provisional Guidelines wasslow.

In 1994, with the agreement of the UNECE and the Organisation for EconomicCo-operation and Development (OECD), EUROSTAT, the Statistical Office of theEuropean Communities, undertook to play a major role in the revision of the 1977Provisional Guidelines. The key objective was to update the Guidelines in the lightof the revised SNA and European System of Accounts (ESA) and new developmentssince 1977 relating to household income statistics (eg hidden and informal activities)and to extend and adapt them where appropriate to serve the analytic needs ofeconomic and social policies. However, the geographical scope of the revisedguidelines would initially be the countries of the European Economic Area.

In addition, as a result of the 15th International Conference of LabourStatisticians in October 1993 the Bureau of Statistics of the International LabourOrganization (ILO) took the initiative to improve the measurement of income fromemployment (eg Dupré, 1997). In October 1998, the 16th International Conferenceof Labour Statisticians (ICLS) adopted a Resolution concerning the measurementof employment-related income (ILO, 1998b).

Chapter 1: Introduction

8 The Canberra Group

A general feature of most of these approaches to create international guidelineson income distribution statistics is that they principally started from a macro view,proceeding from the SNA. However, the top-down macro-to-micro approach toconceptual issues provides a very different, and not immediately obvious, perspectivefor most micro-data users. Emphasis on a framework tends to lead to a rigorous andtheoretical approach where flexibility may look like inconsistency. Emphasis onthe practical issues arising from micro-datasets sets great store on the virtues offlexibility at the possible cost of losing sight of an underlying framework.Consequently, framework-based guidelines tend to lack practical advice to theproducers and users of micro-data. This is perhaps the main reason why the 1977Provisional Guidelines were seldom adopted by producers of income distributionstatistics and remained provisional.

In what was thus a virtual vacuum of international consensus on how incomedistribution could and should be measured, concern grew in many countries to developbetter measures of the economic well-being of their populations for national policypurposes. The range of survey and other information expanded, and technologicaladvances considerably improved the possibilities for sophisticated treatment ofcomplex micro-data. At the same time, there was an increasing desire to makeinternational comparisons of such statistics which exposed the lack of consistencyof the available data. At the inter-country level, the Luxembourg Income Study (LIS)was set up in 1983 to address the lack of comparability of household income datafrom different countries. Located in the Centre for Population, Poverty and Socio-Economic Policy Studies in Luxembourg, LIS draws together unit record data froma wide range of countries and attempts to reorganise them to a common set ofconcepts and definitions. However, organisations such as World Bank, United Nationsand OECD all published inter-country comparisons during the 1990s in which thesame country might have very different relative rankings depending on the conceptsand data sources used. Partly in response, the OECD commissioned a cross-nationalstudy of income distribution based on LIS data (Atkinson et al, 1995).

The 24th General Conference of the International Association for Research inIncome and Wealth (IARIW) in August 1996 included a session on InternationalStandards on Income and Wealth Distribution (Smeeding, 1996). This session mainlyfocussed on efforts to revise the 1977 Provisional Guidelines on Statistics of theDistribution of Income, Consumption and Accumulation of Households (UnitedNations, 1977). The session had two keynote papers:

• ‘Towards a Revision of the UN Guidelines on Statistics of the Distribution of Income,Consumption and Accumulation of Households’, actually consisting of three separatecontributions by Lidia Barreiros and Deo Ramprakash (Barreiros and Ramprakash1996), Alfred Franz (Franz, 1996a) and John Walton (Walton, 1996) respectively;

• ‘A Provisional Framework for Household Income, Consumption, Saving and Wealth’,published in June 1995 by the Australian Bureau of Statistics and presented by HarryKroon and Maureen McDonald (Australian Bureau of Statistics, 1995).