Expanding into Biopharmaceuticals Vamsi Chavakula Sungshik Kim David Liu Radhika Marathe

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Expanding into Biopharmaceuticals

Vamsi Chavakula

Sungshik Kim

David Liu

Radhika Marathe

2

Executive Summary

The pharmaceutical industry is in total more profitable than any other industry in

the United States. The highly lucrative payoffs are countered by heavy risks associated

with drug research and development, which may take as many as ten years in a product

life cycle. In addition, companies must deal with securing FDA approval for their

products, which may provide yet another barrier to producing a pharmaceutical product.

Pfizer is currently the largest pharmaceutical company in this industry, accruing

revenues of $51.3 billion in 2006. Known for its innovative medicines, Pfizer has brought

a number of successful drugs to the market, including Viagra, Celebrex, and Lipitor,

currently the top selling drug in the world. However, it faces a myriad of competitors in

the industry with over 200 major companies vying for the production of the next so-

called “blockbuster drug.” In addition, the market game is changing as new technologies

such as biopharmaceuticals threaten to displace traditional medications. In light of this

competition, we recommend that Pfizer take the following actions:

o expand its efforts to lobby the government to protect its interests, including

stricter regulation of new companies to discourage entry into the pharmaceutical

industry and the biotech pipeline, extension of patents on existing exclusive

drugs, and stricter enforcement of patent infringements.

o extend its resources in biotech by focusing on excelling in an ophthalmology

niche and then using this as a focal point to expand into related fields in biotech

through its existing synergies and efficient sales and marketing arm.

3

Table of Contents

Introduction

4

Biotech as the Future for Pharmacy

6

Porter’s Six Forces Analysis

8

Strengths, Weaknesses, and Opportunities

13

Threats and Competition

15

Suggested Strategies

18

Conclusion

24

Appendix

25

References

28

4

Introduction

Pfizer is the largest pharmaceutical company in the world – it was named by Fortune

Magazine as the fifth-best “wealth-creator” in America. Currently Pfizer places primary

focus on the development of chemical compounds into therapeutic drugs and health

products for humans and animals. It can divert revenue from these two divisions, as well

as from the smaller consumer health care division (with products such as Schick razors,

Trident gum, and over-the-counter medications like Sudafed) into any of the other

divisions for growth and investment.

Pfizer has grown over the years to an extent through internal development and

licensing, but primarily through acquisitions and mergers to solidify its position in a

given concentration or begin expansion into a new therapeutic area - for example, in 2003

Pfizer merged with Pharmacia to broaden Pfizer’s product line, increase revenue, and

make research and development more efficient. The new company then works to trim the

fat by eliminating redundant practices and creating synergies between the existing

operations of subsidiaries. Through this expansion, the company now offers

pharmaceuticals in over 40 different categories of diseases/conditions. The company has

remained successful by allocating a vast amount of resources (over $5 billion a year) into

its research and development unit, more than any of its competitors. In addition, the

company has spent on the same order of revenue on marketing of drugs, causing some of

their products (such as Lipitor, Claritin, and Viagra) to become household names.

With its merger with Pharmacia in 2003, Pfizer acquired its first biotech facility in St.

Louis. The company has a relatively small pipeline for these biotech drugs – in contrast

to its role as a leading company in the pharmaceutical business, Pfizer as a late entrant

5

into biotech is still far behind prominent competitors such as Roche, Johnson & Johnson,

and Amgen, the industry leader. Biotech promises to be the future of medicinal therapy

for the world (see next section) and will likely become an increasingly important facet to

success in the pharmaceutical industry. Pfizer is far behind in the game – what can the

company do in order to aggressively move into this emerging field?

6

Biotech as the Future for Pharmacy

Currently the entire pharmaceutical industry seems to be favoring the shift from

ordinary organic molecule treatments to biotech solutions.

“The basic science underlining all biopharmaceutical drugs is that every living

cell in the human body contains DNA (deoxyribonucleic acid) and contained within them

are genes. Cells are able to perform their functions because of the instructions encoded

within the genes… These genes are then isolated and duplicated on a large scale to

produce the desired protein, which is then extracted, purified and used for the production

of the biopharmaceutical or biotech drugs, as they have come to be known.” (A.N.

Aditya, Technical Insights, Frost & Sullivan).

One of the primary reasons for the shift in research paradigm is that current drugs

are proving to have limitations both in efficiency and effectiveness. One of the issues

confronting organic molecule treatments is the problem of drug delivery. Physiologically,

it is very difficult to ensure that an organic chemical drug acts on only a desired location

in the body, because it can never be determined how effectively the drug will reach its

target organs. This is the issue of drug delivery, and current research for solutions to this

dilemma are being sought after in the biotech world because it is believed that by

utilizing protein therapies, the body’s natural transport and recognition systems can be

harnessed to ensure that the drug acts on only the appropriate targets, and that significant

amounts of the drug are able to reach the target organ. Through the use of biologically

synthesized molecules, such as hormones and proteins that are naturally produced by the

body, it is hoped that greater drug efficacy is achieved. In addition, most organic

7

chemicals work in the body by acting as homologs (having similar structural properties)

to certain compounds in the body. Biotech seeks to manufacture the desired biological

molecules exactly and introduce them as the treatment substance. Examples such as

artificial insulin and lab synthesized clotting factors serve as examples as to how

conditions that were untreatable by conventional treatments are now being unlocked.

At this time, it seems that there are three areas of focus by the pharmaceutical

industry in the biotech market. The first are of research is novel drug delivery systems, as

mentioned above. Nanoparticles and various drug introduction systems are being studied

in order to more effectively deliver treatment to damaged targets, while preventing the

actions of the drug anywhere else. Hence, this field strives to improve the specificity of

drugs and thereby reduced adverse side effects.

Another field of study utilizes modified proteins to accurately detect contaminants

in small fluid samples. Such products have applications not only in human fluids such as

blood, but can be utilized to analyze environmental samples such as water contamination

levels, or gasoline purity levels.

Finally, biotech firms are concentrating on medical devices such as heart assist

devices, and other electronic devices that will improve the functioning of impaired

organs. This field is still very young, and significant improvements are yet to be seen.

Overall, the field of biotechnology offers faster and more efficient solutions to the

pharmaceutical industry than were previously possible with conventional chemical

molecule treatment with the benefit of reduced side effects. It would be unwise for Pfizer

not to consider expansion into this new and developing field.

8

Porter’s Five (Six) Forces Analysis

Buyer Bargaining Power

o Little bargaining power for individuals who end up consuming the drugs because

there are few alternatives for any specific drug and the individuals are not

associated in any way (to form any kind of union, etc.), which may gain some

bargaining power.

o Pharmacies also have little bargaining power because they merely sell what the

individuals demand (especially when the product is recommended by a doctor).

o However, HMO’s and other health insurance agencies have significant amounts

of bargaining power because they can choose not to subsidize certain drugs

(deeming them unnecessary) or they can subsidize certain drugs more than others.

Often a HMO will have a partnership with certain companies to favor that

company’s drugs.

Supplier Bargaining Power

o Chemical plants and material suppliers such as Aldrich have very little bargaining

power. Prior to the expiration of a patent, the cost of actually producing a brand

name drug is very low compared to the retail price of the drug, as seen in the

many-fold drop in price when a comparable generic is released. Even when a

generic drug is released, there are still a number of suppliers to choose from; the

resources required to produce the pharmaceuticals are not restricted to a limited

set of suppliers.

9

o The pharmaceutical companies for security, integration, and quality control

reasons however often own these suppliers.

o Individual scientists that work for a pharmaceutical company such as Pfizer have

very little bargaining power since they sign away the intellectual rights to any

discovered product while working for the company.

o However, if a group of scientists independently, either in an institution or small

company, make a discovery, that institution or company can have a potentially

large amount of bargaining power for that discovery.

o The institution will often license the right to the discovery while small companies

often merge with the buyer.

Rivalry

o For a drug that is within its period of exclusivity, the company that distributes it

can exercise monopoly pricing since it is the only drug available to treat a certain

condition.

o This patent tends to reduce competition between pharmaceutical industries during

this phase. However, companies can try to subvert the patent law by developing a

similar drug to treat the health condition that goes about the problem in a different

manner; this will undercut the monopoly and increase the rivalry between the

companies.

o Several companies have prescription drugs in a specific category such as second-

generation painkillers or prescription stomach acid reducing drugs – these

products can usually be substituted with one another, increasing the rivalry in this

market.

10

o Price competition is not particularly strong in this industry due to pressure from

insurance companies and government regulation. Price cutting will not increase

revenues or units sold significantly because each drug possesses a unique set of

attributes, i.e. targets and side effects. In general, such drugs are prescribed by

physicians who will not factor price into their decision of which drug a patient

should receive. In other words, Pfizer should not expect a great increase in

revenue or units sold due to a price cut – considering the rival response, Pfizer

should not consider price slashing as a viable strategy for future growth.

o In addition, a number of companies can have the same type of drugs in

development. For highly publicized types of drugs, such as those designed to cure

AIDS, this increases the rivalry, as it soon becomes a race to whoever can patent

the drug first.

New Entrants/Barriers to Entry

o There are a number of barriers to entry, which is what contributes to making the

pharmaceutical industry and the biotech pipeline very profitable.

o However, these high profits are what drive entry, which is made all the more

attractive if there is a good product.

o With a specific type of drug already on the market, a competitor will need time to

research and develop its own version of that drug and patent any technological

advances that arise during this phase. It also requires a talented group of lawyers

to create the patents and be prepared to litigate in order to enforce them.

o In addition, the competitor will need to prove to doctors, hospitals, and health care

professionals that the product is as good, if not better, than the original product.

11

o With regards to a new type of drug, a company first needs a marketable product,

which means either a successful and large research and development team, or

quite a bit of serendipity.

o A large amount of capital ($800 million on average to bring a drug into the

market) and time are necessary to take the drug from its conceptual stage to the

final production and distribution. This includes animal and human testing, passing

government regulations (FDA approval), and convincing people that the product

is both effective and necessary.

o In addition, existing pharmaceutical companies can lobby the government against

new entrants to make it more difficult to gain access to the drug market. Pfizer has

one of the largest lobbying arms in the industry today and should be able to

exercise this muscle further to keep entrants out.

o A new entrant lacks the strong brand name and reputation, as well as the

necessary connections that could help to facilitate this process and reduce cost.

They also lack the economies of scale and distribution networks already in place

for existing players in the industry.

o Again, the company will require a group of lawyers to protect this novel drug

from encroachment.

Substitutes

o When a drug is in its period of exclusivity, there aren’t (by definition) many

viable substitutes.

12

o On occasion, a similar drug will be released within a few years, but often the only

substitutes are alternative medicinal therapies (such as standard Asian therapies

such as Ayurveda and acupuncture), surgery, or other medical procedures.

o Once the period of exclusivity has ended, there are a variety of substitutes as

generic drugs come into the picture. Prolonging this exclusivity period then is a

desirable strategy to keep a pharmaceutical company profitable.

Complements

o For a specific drug, the main complement is whatever the drug is designed to

treat, prevent, or cure, whether it is a disease, an illness, an injury, or a side effect

caused by another drug.

o If the health issue is capable of mutation, the complements can include related

drugs since an increase in a drug’s usage could lead to immunity to that particular

drug, resulting in the increased usage of a related drug (e.g. the high turnaround

time associated with AIDS drugs).

o In general, complements also include well-educated doctors, favorable

government policies (thus the necessity for strong lobbying), and insurance

companies including Medicare.

13

SWOT Analysis of Pfizer

Strengths

o As the current leader in the pharmaceutical industry, Pfizer has a number of

advantages. It has a strong and large sales force that is capable of effectively

marketing their products.

o The company also has a strong reputation in the industry, which confers a three-

fold advantage – a) it eases the approval process by the FDA, b) makes the drug

more likely to be recommended by doctors and approved by insurance carriers,

and c) gives Pfizer an edge when trying to convince others to license new

products to it.

o By holding the top position in the industry, Pfizer has the most fluid capital to

reinvest into research (about $5 billion per year), take risks in high return type

products, or outbid rivals on a crucial product.

o In addition, Pfizer already has large research facilities and production capabilities,

while also spending the most in research and development of new products.

Weaknesses

o As the leading pharmaceutical company in the industry, Pfizer also has the largest

overhead cost and must spend a sizeable fraction of its revenues filing and

defending lawsuits on its existing products.

o Although Pfizer has a wide variety of drugs, it is dependent on a handful of drugs

for the majority of its revenues. When patents on these drugs expire, Pfizer will

14

face severe losses in profit unless the company can time the release of a new

product when the patent on an older product runs out. For example Pfizer will

lose exclusive rights for Lipitor production in 2010, which currently accounts for

about 25% of its revenues worldwide. This product timing is largely a function of

research and government approval, which makes it difficult for the company to

plan ahead. To take measures into its own hands, Pfizer must have a strategy for

the development of products and maintain healthy relations with the government.

o As a late entrant into the biopharmaceuticals market, Pfizer enjoys very little

market share and revenue compared to what it generates in traditional

pharmaceutical drugs. Without strategic action, Pfizer risks losing ground on

competitors of comparable size with a mature biopharma portfolio.

o Insurance companies can pressure the company to lower prices on their products

or risk being denied coverage, and therefore use by the final consumer.

Opportunities

o As the baby boomer generation grows older, this graying population will require

an assortment of prescription medicines and services as the average life

expectancy increases due to the improvement in healthcare. By catering to this

demographic, Pfizer can lock in a number of these customers, who will be around

for a while and will be dependent on these therapeutic drugs.

o Pfizer also has an opportunity to expand globally and enter new markets such as

India, China, and South Korea that have a large population base that is expected

to get wealthier and older over the next few years. At present, many of Pfizer’s

drugs are priced outside of the range of the average person in these countries. But

15

with their continued economic success, it is highly possible that all three will

become major markets for pharmaceutical drugs.

o In addition, there are a number of possible alternatives open to Pfizer with regards

to recent scientific discovers, such as gene therapy and stem cell research. Both of

these technologies are still in the development stage and will likely face stiff

cultural opposition, but both represent a possible “next” market.

Threats and Competition

o Pfizer faces a number of threats to its premier market position. High gross profits

across the industry attract entry, which, in principle, is feasible for an entrant with

a novel idea or application.

o Each new entrant into the industry could potentially become a long-term

competitor – for instance, new startups that do not want to merge with a larger

company may grow to competitive size. As an example, Amgen began its entry

into the industry in 1985 and has since become a major rival to Pfizer.

o There is also a long-term threat from generic drugs produced by such companies

as Teva and Barr that creates competition when Pfizer’s drugs come off their

period of exclusivity.

o Established companies can displace Pfizer as market leader in this volatile market.

Below are the strategic positions of Johnson & Johnson and GlaxoSmithKline, the

two next highest revenue-grossing pharmaceutical companies in the industry.

16

Johnson & Johnson

In contrast to Pfizer, Johnson & Johnson, the closest competitor in terms of

revenue, is a multidivisional firm that focuses not only on pharmaceutical drugs and

consumer products, but also places a much higher emphasis on medical devices. It is

independent of any one drug, drug category, or consumer product as it can funnel profits

from any one division into another. The company also has a strong reputation, and most

worrisome for Pfizer, large amounts of operating profits that can be used to diversify or

counter strategic repositioning by Pfizer. Johnson & Johnson is less broad than Pfizer

with regard to product development, instead focusing on the development of drugs in

twelve key categories (as opposed to the nineteen offered by Pfizer) such as Alzheimer’s

disease, oncology, and urology. Inside of this therapeutic area focus, Johnson & Johnson

makes strategic acquisitions to complement existing products and research in these areas,

create synergies, and boost revenue. In addition, Johnson & Johnson expanded into

biopharma through the acquisition of successful firms in the sister industry earlier than

Pfizer, giving it a head start in carving out a niche and taking market share. Although it

may be better known for its consumer products, J&J is in a strong position as the number

two pharmaceutical company and can take Pfizer’s place should it falter.

GlaxoSmithKline

GlaxoSmithKline plc (GSK) is the third largest pharmaceutical company in the

world – in addition to producing prescription medicines and consumer health care

products like Pfizer and Johnson & Johnson, GSK differentiates itself as a large producer

of vaccines and antibiotics. In 2000, GSK accounted for over a quarter of all vaccine

sales. It has a very large sales force (40,000+), which is capable of ensuring the

17

distribution of GSK products around the globe. The GSK growth strategy has involved

internal development and extension of key products such as Advair for the treatment of

asthma, in-licensing for organic growth with companies such as Merck, and increasing its

pipeline of vaccines (over 20 in development) for a number of conditions. Two other

positions that GSK has taken is aggressive development of HIV/AIDS as well as

investment into genetics and gene sequencing. GSK is also already a player in the biotech

market.

18

Suggested Strategies

Aggressive Lobbying

An effective practice that pharmaceutical companies often employ is lobbying the

government for favorable treatment. Pfizer has spent over $20 million in lobbying

expenses in the past decade in order to protect its interests; these include extension of

patents on existing drugs, tax breaks, protection, and enforcement of its patent laws.

Recipients of these funds have included such politicians as Senator Richard Gephardt, Kit

Bond, and Joseph Lieberman. These grateful politicians are then in place to help the

company once elected to office.

On a number of occasions, Congress has deliberated on the ability of

pharmaceutical companies to extend patents on exclusive drugs, thus denying the

company the ability to enjoy longer periods of high profits with the associated high price

to consumers. Pfizer stands to lose a substantial amount of revenue should measures like

these pass through the House and Senate.

Pfizer should then continue to place heavy emphasis on lobbying politicians by

increasing contributions (within the legal limit) towards causes that would subvert bills

such as these. In addition to the promotion of the enforcement of patent law, Pfizer

should also lobby to make it harder for new entrants to make it into the industry and the

biotech pipeline. This could be through more extensive testing, proof of quality, and

safety for products in the FDA approval process for new companies and stricter

requirements for the assembly of new production facilities. This applies to foreign

competitors as well; it could include strict inspection of facilities abroad and heavy

19

regulation on the packaging and importation of goods. In the past, Pfizer has pressed

politicians for trade sanctions against companies that import cheap generic copies of their

patented drugs – Pfizer should continue this exercise as well as petition the World Health

Organization to uphold the company’s patent law worldwide.

There should be little to no opposition to this strategy from Pfizer’s main

competitors. Since these practices will tend to benefit the entire industry as a whole in

barring access to the market to new players, it will ensure that any competition for market

share will be between entrenched companies.

Pfizer should however refrain from lobbying against existing competitors in the

industry. For instance, if Pfizer were to lobby for stricter government regulation in a

therapeutic focus in which it has little interest, this could antagonize other companies for

which that focus is their specialization (for example, GlaxoSmithKline would be

aggravated if Pfizer were to lobby for greater regulation of vaccines). Pfizer is not the

only company in pharmaceuticals that spends a large amount of operating profit on

lobbying the United States government; Johnson & Johnson, Merck, and Roche are not

far behind. The incited rival response could be detrimental to Pfizer; the other companies

could lobby the government for tighter control of FDA regulation in the cardiovascular

market. This could potentially escalate into a conflict that is harmful for all players

involved. Knowing this, Pfizer should not be the first to throw the stone; rather, by

working to keep new competitors out of the market, it can obtain greater market share

from existing competitors by other means.

20

Specialization

Although Pfizer is the leader in pharmaceuticals, since it was not one of the first

firms to enter the biopharmaceutical industry, its competitors have gained incumbent

advantages and larger market shares. To carve out a niche in the biotech pipeline, Pfizer

should focus on an area that does not have high-density competition. At this point, most

of the major areas or research such as protein, hormone, enzyme, and blood factor

creation for systems such as cardiovascular, central nervous and etc already have a lot of

firms vying for the lion’s share of the market.

Pfizer should start out in an area with relatively less competition – we have

identified ophthalmology as a potential market for the company to start its expansion into

biotech. This is for four reasons:

1) None of the top competitors in the biotech market, including Amgen and

Johnson & Johnson have entered this sector of the market.

2) Pfizer already has a pharmaceutical research and development unit in

ophthalmology. Incorporating biotech into this existing research unit will help ease the

company’s entry into the market. Further, Pfizer entered a licensing agreement with

Quark Biotech, an innovative biopharmaceutical developing treatments for diseases of

the kidney and lungs, as well as fibrotic and ischemic diseases of the eye. With their

expertise, Pfizer should be able to quickly gain experience in this niche.

3) For the aging baby boomer generation, retention of sight is of particularly high

importance. By expanding early into ophthalmology and capturing a growing proportion

of potential buyers, Pfizer can lock in a sales blocks for years to come.

4) On the other hand, ophthalmology is not a sufficiently attractive sector of the

biotech market for competitors to enter given that Pfizer has made it the company’s

21

primary focus. While the sector can be profitable, it will not be able to match the margins

for more profitable areas of biotech such as cardiovascular or cancer treatment. If Pfizer

can develop quality treatments that give value to their customer base, it will be difficult

for another company to undercut the incumbent. Given the smaller profit margins, it may

not be profitable for another company to do so. In short, ophthalmology is an attractive

market for one player, but not sufficiently large for two.

Diversification

Pfizer should then begin its expansion conquest of the biotech industry in

ophthalmology. Here they can gain experience in how the industry operates (move right

along the experience curve) and adapt to the different requirements for success as

compared to the traditional pharmaceutical drug industry that it has dominated. During

this time, Pfizer should plan cost-efficient strategies for production and make use of its

existing distribution network to develop economies of scale for their products. As Pfizer

expands in this market sector, Pfizer should take care to impose heavy quality testing on

all of products coming out of the biotech pipeline. This will be to establish a reputation as

a safe manufacturer of biotech products, a distinction that will carry over into other

sectors of the biotech market.

Once Pfizer has solidified its position in the ophthalmology department, it can

begin to look into related fields to enter. By diversifying their biotech product portfolio,

the company can continue its strategy to carve out a place for itself in the biotech

industry, which according to our eight to ten year projected strategy will have huge

payoffs for the company in the years to come.

22

Pfizer would have a three-fold cost sharing advantage when moving into these

related fields. First, the manufacturing facilities will share a number of related multi-

purpose technologies that can be used for the simultaneous production of

biopharmaceutical products. This will place downward pressure on the costs of expansion

since Pfizer already has the production capabilities to handle the expanded drug portfolio.

There will also be a set of educated specialists who can be shared across various areas of

the industry and add their area of expertise to any project that they work on. These cross-

fertilizations will allow for the spread of working ideas (such as a particularly effective

paradigm, i.e. an efficient protein structure, etc.) and efficient practices across the new

frontier of research for Pfizer. Finally, Pfizer has a strong advantage with its large sales

and marketing arm – by announcing its entry into new fields in biotech and flooding the

public with information on their products, Pfizer can make their products known more

effectively than competitors, thus making it more likely that their product will be the one

prescribed.

With its history of acquisitions, Pfizer should also consider acquiring a few

companies that show promising research in the desired field. In this way Pfizer can gain

patents, licenses, and specialized personnel to excel in these new fields, while those

companies gain Pfizer’s expertise in sales and marketing and existing distribution

networks. At this time, Pfizer should also make use of the aggressive lobbying strategy

cited above to make it difficult for additional entrants to make it in the industry while

establishing its leadership. Ultimately, Pfizer should look to the production of proteins to

complement their cardiovascular drugs, at present the most profitable and fastest growing

sector of the pharmaceutical industry.

23

Since biotech is a broad and growing market with many existing companies,

Pfizer’s competitors will have a difficult time blocking Pfizer’s movement into this

sector. As discussed earlier, cutting prices is not an effective strategy for competition in

this industry. Also, other companies cannot try to dislodge the Pfizer giant by appealing

to the government since Pfizer can lobby in retaliation. What leading competitors like

Johnson & Johnson and Amgen can do is try and lock in a given constituency with their

existing drug/treatment/method rather than trying the new Pfizer version by pushing their

product with their sales team. They can also drive up acquisition costs or purchase the

desired biotech companies themselves in order to block Pfizer’s entry. However, they

cannot keep Pfizer out of a sector of the market completely, and will most likely

accelerate production or increase the allocation of resources into the sector in order to

beat Pfizer to the next product. As long as Pfizer utilizes its unique strengths and

synergies, it will have a strategic advantage that cannot be easily reproduced by its

competitors.

24

Conclusion

Pfizer is standing at the crossroads with its current position. If biotech really is the

future of the industry then the company risks being left behind as competitors extend

their biopharmaceutical portfolios. In order to enjoy the types of revenue and market

share that it currently holds in the next eight to ten years, the company necessarily must

take action to secure its future position.

As such, we have identified ophtamology as a potential cornerstone from which

the company can expand into the biotech market. From this focal point, the company can

use its existing size to spill over into related markets. However, with sizeable competition

in these sectors, it will be important for Pfizer to execute this strategy effectively through

efficient production, strong sales and marketing, and savvy acquisition. Although it may

not be able to completely displace the current biopharmaceutical leaders, Pfizer can use

these strategies to at the very least better its current position in this market. Since success

in biotech implies success in the pharmaceutical drug industry, Pfizer can maintain a

strong role in the production of tomorrow’s treatments for the next generation.

25

Appendix

Table 1: Top 10 Global Pharmaceutical Companies

2005 US Revenue (USD billions)

Pfizer Inc 51,300

Johnson & Johnson 50,514

GlaxoSmithKline Plc 39,421

Sanofi-Aventis Group 33,946

Novartis AG 32,212

Roche Holding AG 28,505

AstraZeneca PLC 13,950

Abbott Laboratories 13,338

Merck & Co., Inc 22,012

Bristol-Myers Squibb Company 19,207

Source: Datamonitor

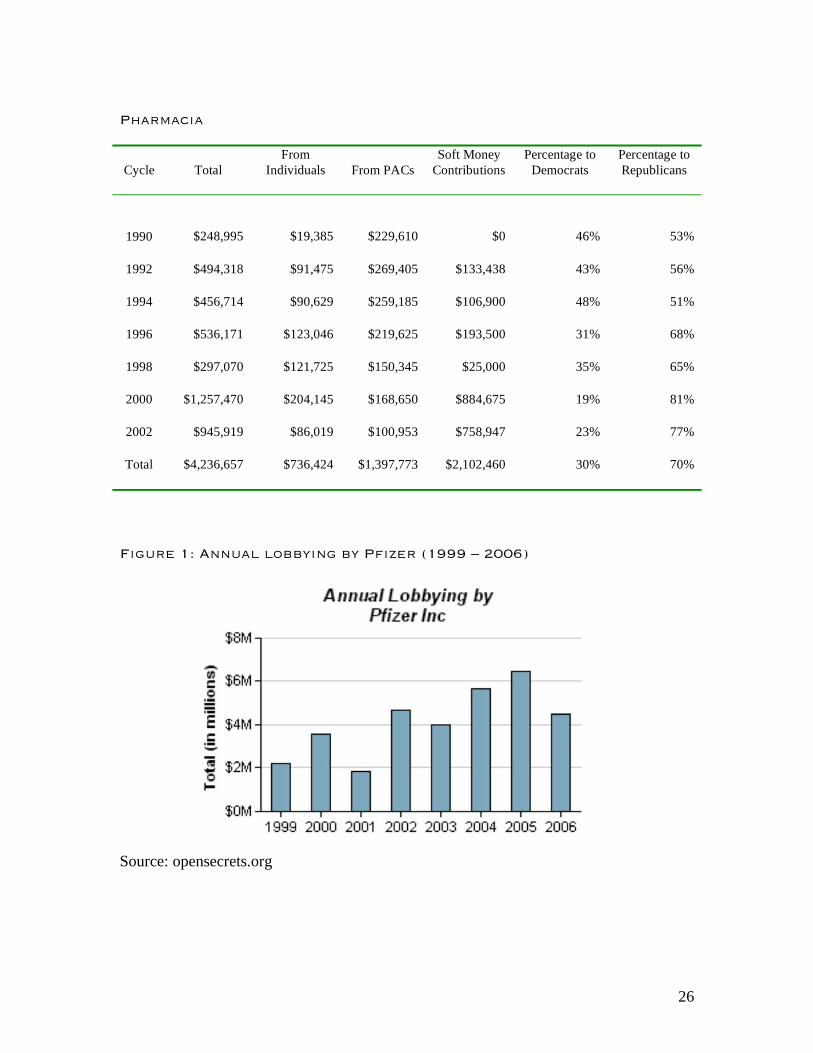

Table 2: Total Contributions to federal Parties by Pfizer &

Pharmacia prior to their merger in 2003 (Source: opensecrets.org)

Pfizer

Cycle Total

From

Individuals

From

PACs

Soft Money

Contributions

Percentage to

Democrats

Percentage to

Republicans

1990 $150,050 $10,250 $139,800 $0 54% 46%

1992 $304,757 $32,180 $190,600 $81,977 39% 61%

1994 $546,903 $41,676 $261,692 $243,535 36% 64%

1996 $888,116 $83,300 $289,100 $515,716 22% 78%

1998 $1,144,310 $85,580 $311,680 $747,050 20% 80%

2000 $2,492,166 $370,379 $562,970 $1,558,817 15% 85%

2002 $1,280,404 $45,140 $396,000 $839,264 21% 78%

TOTAL $6,806,706 $668,505 $2,151,842 $3,986,359 22% 78%

26

Pharmacia

Cycle Total

From

Individuals From PACs

Soft Money

Contributions

Percentage to

Democrats

Percentage to

Republicans

1990 $248,995 $19,385 $229,610 $0 46% 53%

1992 $494,318 $91,475 $269,405 $133,438 43% 56%

1994 $456,714 $90,629 $259,185 $106,900 48% 51%

1996 $536,171 $123,046 $219,625 $193,500 31% 68%

1998 $297,070 $121,725 $150,345 $25,000 35% 65%

2000 $1,257,470 $204,145 $168,650 $884,675 19% 81%

2002 $945,919 $86,019 $100,953 $758,947 23% 77%

Total $4,236,657 $736,424 $1,397,773 $2,102,460 30% 70%

Figure 1: Annual lobbying by Pfizer (1999 – 2006)

Source: opensecrets.org

27

Figure 2: Proportion for Key Pharmaceutical Firms in Biopharma and

traditional Pharmaceutical drugs

Source: pubs.acs.org

28

References

http://www.pfizer.com

http://www.media.pfizer.com/pfizer/download/investors/presentations/shedlarz_presentat

ion_012207.pdf

http://www.datamonitor.com

http://www.wikipedia.com

http://www.pmi.com/cgi-bin/stories.pl?ACCT=104&STORY=/www/story/02-10-

2006/0004279298&EDATE=

http://www.jnj.com

http://www.gsk.com

http://www.corporatewatch.org.uk/?lid=329

http://www.opensecrets.org

http://www.prnewswire.com/cgi-bin/stories.pl?ACCT=104&STORY=/www/story/02-22-

2001/0001433051&EDATE=

http://pubs.acs.org/cen/coverstory/8219/8219biopharma.html

http://www.amgen.com/science/pipe.jsp

http://www.jnj.com/innovations/biotech/partner_biotech_2002.pdf

http://www.accessexcellence.org/RC/VL/GG/biotechnology.html

http://www.pharmabioingredients.com/articles/2006/03/biopharmaceuticals-what-the-

future-holds

http://www.business.com

McAfee, R. Preston. Personal interview. 28 Feb. 2007.

Related Documents