Welcome To OUR Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

WelcomeTo OUR

Presentation

2

TOPICSME investment activities & disbursement process : A comparative study on SME activities of EXIM Bank of Bangladesh Ltd.

3

AIMThe aim of our presentation is to provide a clear idea about the SME investment procedures of EXIM Bank Limited and their position in SME banking among the competitors.

4

ContentsIntroductory Part

◦ Introduction

◦Objectives of the report

◦ Scope of the study

◦ Limitation of the study

Organizational Part

◦Organizational overview

◦Mission, Vision & Objectives

◦Management of EXIM Bank Limited

◦Organizational structure

◦ EXIM Bank subsidiaries

◦ Products & services

◦ Financial Performances of EXIM Bank Ltd.

Actual Task Part

o Job Part

◦Definition of SME as per Bangladesh Bank

◦ SME history of EXIM Bank Ltd.

◦ Importance of SME

◦ Types of SME Investment

◦ Terms & Condition of SME Loan

◦ Procedures of SME Loan

◦ SME Investment process Flow chart

◦Disbursement of SME Investment

◦ Sector-wise SME Distribution

5

Contents◦ Analysis of SME Credit Scheme

of Five Different Banks currently Available in Bangladesh

◦ Financial Aspects

◦ RATIO

◦ Summary of Findings & Analysis, Financial Aspects

Research Part

oMaterial

◦Hypothesis Development

◦Hypotheses Testing

◦Graphical representation

◦ Findings

◦ Recommandation

◦ Conclusion

6

Introduction

7

Objective of the ReportBroad Objective

1. How EXIM Bank Ltd operates SME banking operation around the country through its network.

2. To review the SME banking of Bangladesh.

Specific Objectives

◦ To analyze the SME investment processing activities.

◦ To know the disbursement and recovery procedures of SME investment.

◦ To know the enterprise selection criteria to provide SME investment.

◦ To know the terms and conditions of SME investment.

◦ To conduct a comparative analysis of SME banking in EXIM Bank and four other private commercial banks.

8

Scope of the study◦ Concept of SME and its impact in overall economy of Bangladesh.

◦ Importance of SME banking in context of Bangladesh.

◦ Entrepreneurship development situation through SME banking.

◦ Small entrepreneurs of rural – urban spectrum are enjoying the EXIM Bank investment facility without the presence of bank at rural area.

◦ The report focuses on the comparative analysis of SME Banking of EXIM Bank with four other private commercial banks.

Limitation of the study◦Data from EXIM Bank is highly confidential for the outside people and we had no

authority to use the core banking software.

◦As the duration of the internship program is three months and the process of this program is job rotation, so we didn’t get sufficient time in each department to understand their activities.

◦ Since the bank personals where very busy, they could provide us little time.

◦ Banking sector is a very vast sector where we have a little knowledge about it which limits our report.

9

Organizational part

10

Quotes

“Together Towards

Tomorrow”

Md. Nazrul Islam Majumder Chairman

11

Organizational Overview◦EXIM Bank was established under the leadership of Late Mr.

Shahjahan Kabir .

◦The bank starts functioning from 03 August, 1999 with its name as Bengal Export Import Bank Limited.

◦On 16 November, 1999 it was renamed as Export Import of Bangladesh Limited.

◦EXIM Bank's footprint has grown to 80 branches.

◦EXIM Bank provides necessary funds for executing various programs in the process of economic development.

12

Mission, Vision & Objectives

Mission

To be the most caring and customer friendly and service oriented bank.

To create a technology based most efficient banking environment for its customer.

To ensure ethics and transparency in all levels.

To ensure sustainable growth and establish full value of the honorable shareholders.

Vision

◦ Believes in togetherness with its customers.

◦ To achieve the desired goal, there will be pursuit of excellence at all stages.

◦ Bank’s strategic plans and networking will strengthen its competitive environment.

13

Cont…Objectives

◦ Building a strong customer focus and relationship based on integrity, superior service.

◦ To provide high quality financial services.

◦ To perform social responsibility for a happy future.

◦ To encourage the new entrepreneurs for investment and thus to develop the country’s industry sector and contribute to the economic development.

14

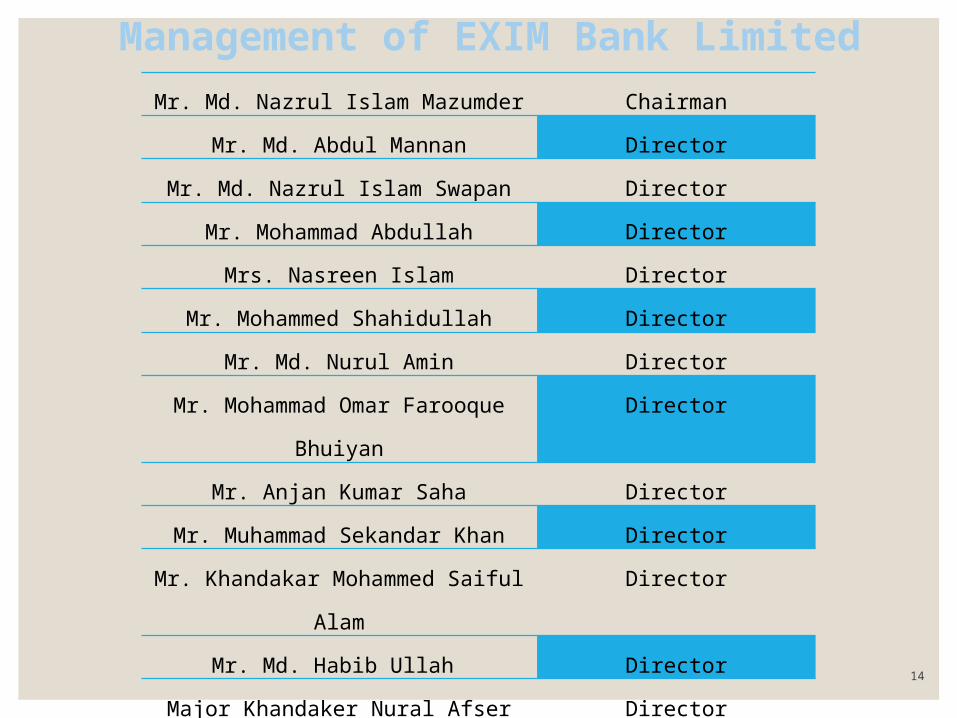

Management of EXIM Bank LimitedMr. Md. Nazrul Islam Mazumder Chairman

Mr. Md. Abdul Mannan Director

Mr. Md. Nazrul Islam Swapan Director

Mr. Mohammad Abdullah Director

Mrs. Nasreen Islam Director

Mr. Mohammed Shahidullah Director

Mr. Md. Nurul Amin Director

Mr. Mohammad Omar Farooque

Bhuiyan

Director

Mr. Anjan Kumar Saha Director

Mr. Muhammad Sekandar Khan Director

Mr. Khandakar Mohammed Saiful

Alam

Director

Mr. Md. Habib Ullah Director

Major Khandaker Nural Afser (Retd) Director

Lt Col (Retd) Serajul Islam Director

Mr. Ranjan Chowdhury Director

Dr. Mohammed Haider Ali Miah Managing Director

15

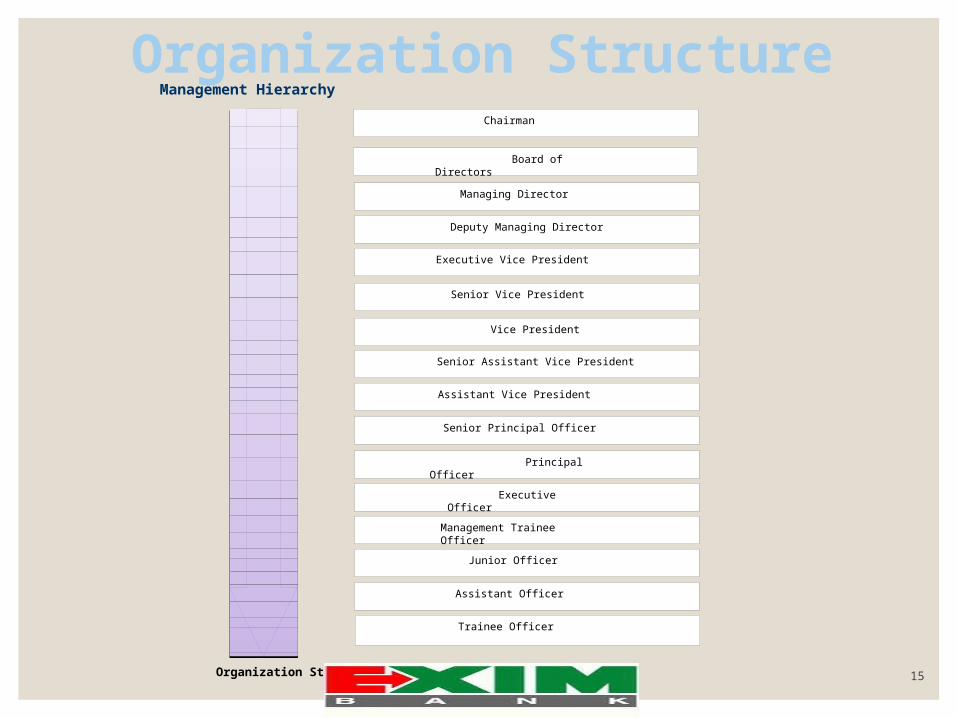

Organization StructureManagement Hierarchy

Organization Structure

Chairman

Board of Directors

Managing Director

Deputy Managing Director

Executive Vice President

Senior Vice President

Trainee Officer

Vice President

Senior Assistant Vice President

Assistant Vice President

Senior Principal Officer

Principal Officer

Executive Officer

Management Trainee Officer

Junior Officer

Assistant Officer

16

EXIM Bank Subsidiaries

17

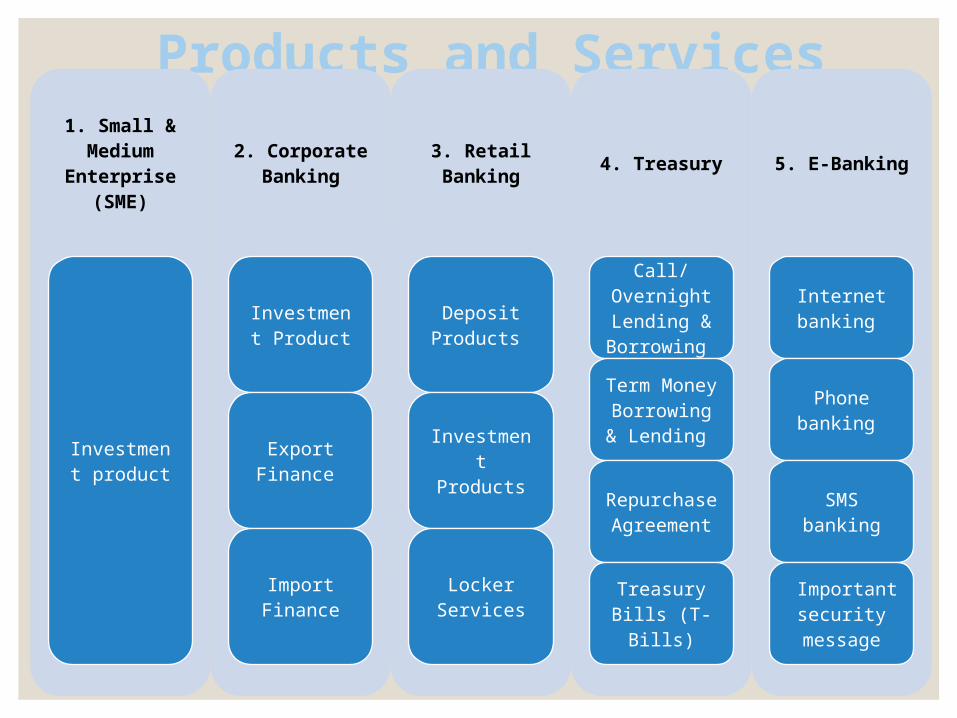

Products and Services1. Small & Medium

Enterprise (SME)

Investment product

2. Corporate Banking

Investment Product

Export Finance

Import Finance

3. Retail Banking

Deposit Products

Investment Products

Locker Services

4. Treasury

Call/Overnight Lending & Borrowing

Term Money Borrowing & Lending

Repurchase Agreement

Treasury Bills (T-Bills)

5. E-Banking

Internet banking

Phone banking

SMS banking

Important security message

18

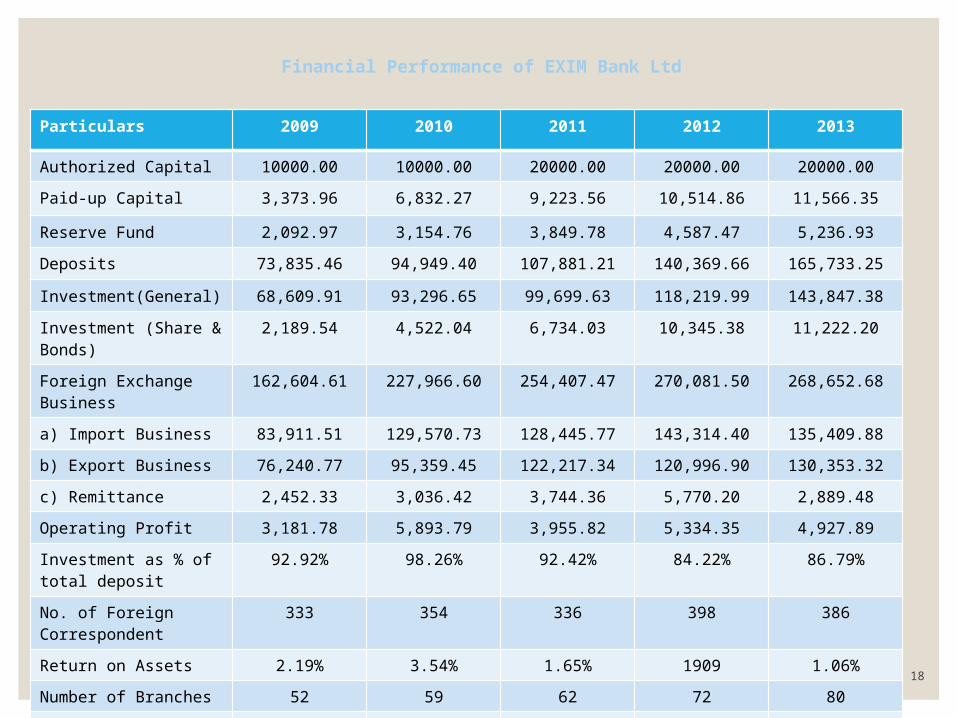

Financial Performance of EXIM Bank Ltd

Particulars 2009 2010 2011 2012 2013

Authorized Capital 10000.00 10000.00 20000.00 20000.00 20000.00

Paid-up Capital 3,373.96 6,832.27 9,223.56 10,514.86 11,566.35

Reserve Fund 2,092.97 3,154.76 3,849.78 4,587.47 5,236.93

Deposits 73,835.46 94,949.40 107,881.21 140,369.66 165,733.25

Investment(General) 68,609.91 93,296.65 99,699.63 118,219.99 143,847.38

Investment (Share & Bonds)

2,189.54 4,522.04 6,734.03 10,345.38 11,222.20

Foreign Exchange Business

162,604.61 227,966.60 254,407.47 270,081.50 268,652.68

a) Import Business 83,911.51 129,570.73 128,445.77 143,314.40 135,409.88

b) Export Business 76,240.77 95,359.45 122,217.34 120,996.90 130,353.32

c) Remittance 2,452.33 3,036.42 3,744.36 5,770.20 2,889.48

Operating Profit 3,181.78 5,893.79 3,955.82 5,334.35 4,927.89

Investment as % of total deposit

92.92% 98.26% 92.42% 84.22% 86.79%

No. of Foreign Correspondent

333 354 336 398 386

Return on Assets 2.19% 3.54% 1.65% 1909 1.06%

Number of Branches 52 59 62 72 80

Number of Employees 1440 1686 1724 1.45% 2229

19

Actual tASK Part

20

Job Part

Internship Experience

◦We got the opportunity to work as an intern in the Garib-e-Newaz branch of EXIM Bank Ltd and the duration of our internship was 11th September to 11th December 2014.

Experience Regarding Personal Improvement

◦ Time management

◦ Formal dress code

Practical Working Experience

21

Duties and Responsibilities

◦ Update information of SME & Account opening files in checklist.

◦ Update information of these files in central database using “T-24” a software that is currently EXIMBL using.

◦ Finally used to update these data in net server and used to make report to project manager at the end of work.

Specification Contributions

◦ We have updated and made report of approximate 5,000 files.

◦ We have given different ideas which helped our project manager to continue the project in right fashion which saved time and labor as well.

◦ Being a responsible member of the project we have saved for EXIM Bank Ltd. by finding an important SME investment file from archive of EXIM Bank limited.

22

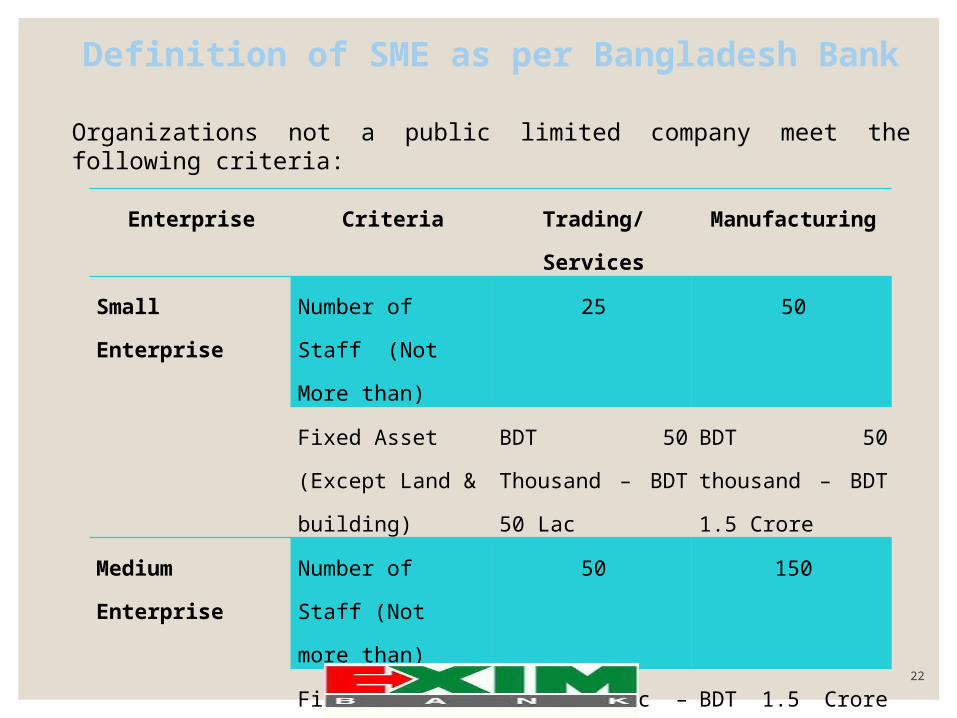

Definition of SME as per Bangladesh Bank

Organizations not a public limited company meet the following criteria:

Enterprise Criteria Trading/

Services

Manufacturing

Small

Enterprise

Number of Staff

(Not More than)

25

50

Fixed Asset

(Except Land &

building)

BDT 50 Thousand

– BDT 50 Lac

BDT 50 thousand

– BDT 1.5 Crore

Medium

Enterprise

Number of Staff

(Not more than)

50 150

Fixed Asset

(Except Land &

building)

BDT 50 Lac – BDT

1 Crore

BDT 1.5 Crore –

BDT 20 Crore

23

SME History of EXIM Bank

◦ EXIM Bank Ltd. has successfully made a mark in creating platform for small and medium entrepreneur.

◦Discharging over 7,000 crore taka in SME loan and helping fulfillment of more than thousand dreams that change hundreds and thousands of lives every day.

◦ The bank has incorporated double bottom line approach in its operation –

1) Making profit by mobilizing fund from urban to rural areas.

2) Performing social responsibility by creating an entrepreneurial class.

24

Importance of SME

25

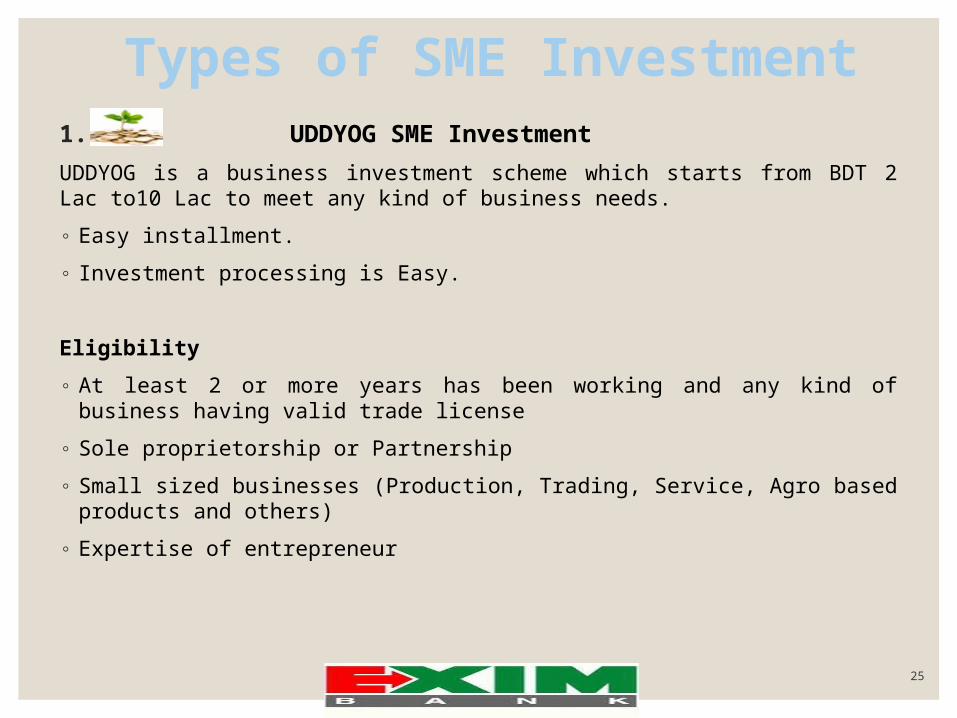

Types of SME Investment1. UDDYOG SME Investment

UDDYOG is a business investment scheme which starts from BDT 2 Lac to10 Lac to meet any kind of business needs.

◦ Easy installment.

◦ Investment processing is Easy.

Eligibility

◦ At least 2 or more years has been working and any kind of business having valid trade license

◦ Sole proprietorship or Partnership

◦ Small sized businesses (Production, Trading, Service, Agro based products and others)

◦ Expertise of entrepreneur

26

Types of SME Investment2. ABALAMBON SME Loan

ABALAMBAN is a small scaled business investment scheme for operating and extending small and medium level business and industries.

◦ Facility of repayment at a time or installments according to the return of business

◦ As low as 10% interest rate

◦ Provide investment facility in a easiest way

Eligibility

◦ At least 3 years has been working and any kind of business having valid trade license.

◦ Those who have land/building/property.

◦ Expertise of entrepreneur

◦ Annual transaction and income

27

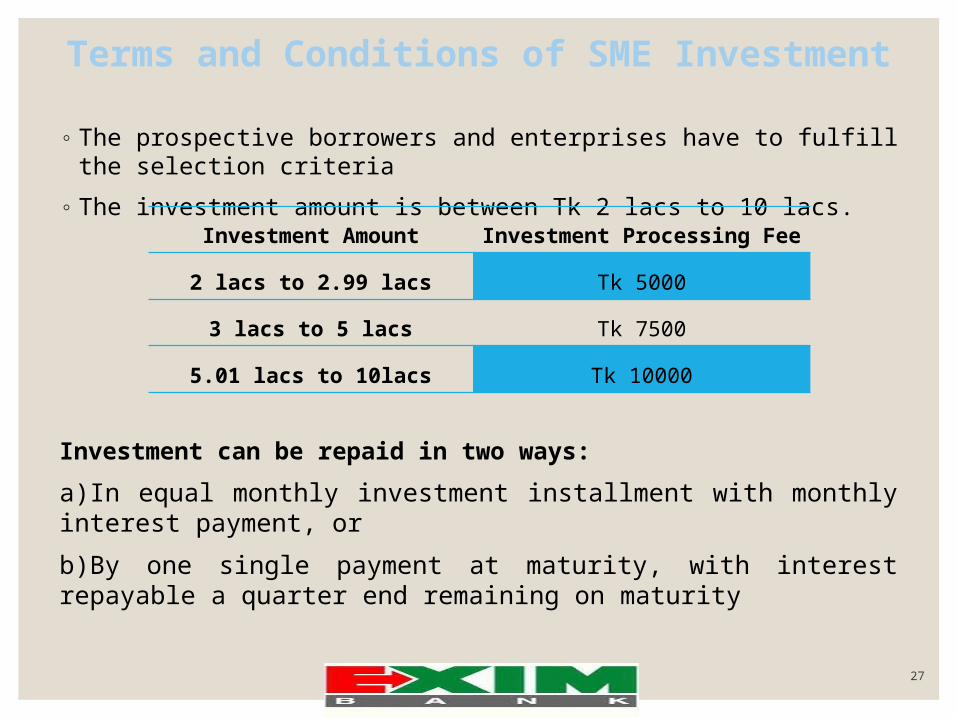

Terms and Conditions of SME Investment

◦ The prospective borrowers and enterprises have to fulfill the selection criteria

◦ The investment amount is between Tk 2 lacs to 10 lacs.

Investment can be repaid in two ways:

a)In equal monthly investment installment with monthly interest payment, or

b)By one single payment at maturity, with interest repayable a quarter end remaining on maturity

Investment Amount Investment Processing

Fee

2 lacs to 2.99 lacs Tk 5000

3 lacs to 5 lacs Tk 7500

5.01 lacs to 10lacs Tk 10000

28

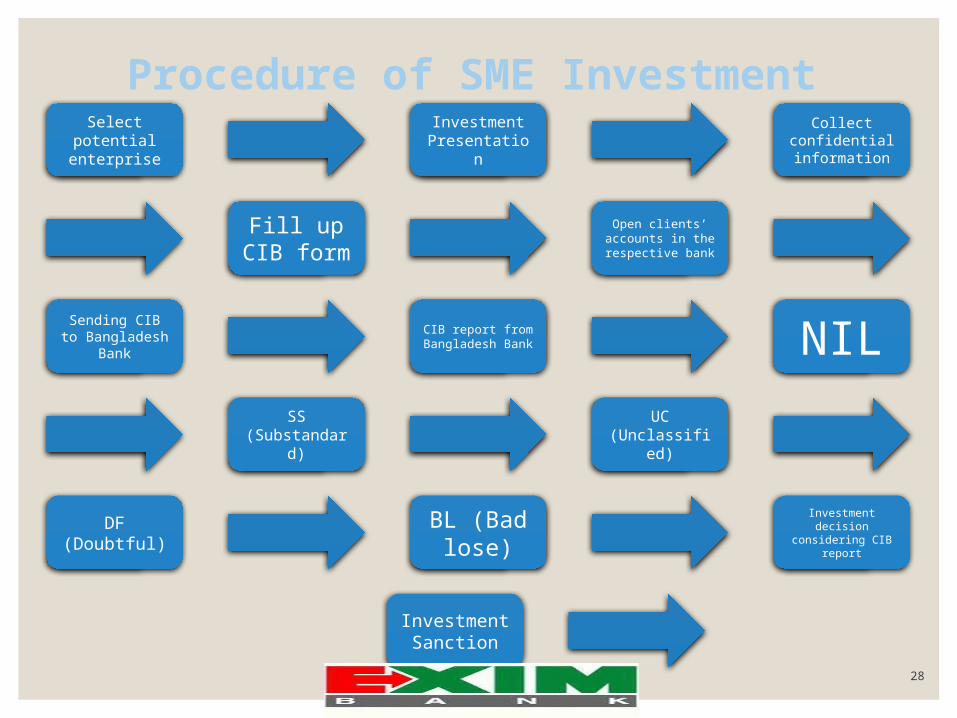

Procedure of SME Investment Select

potential enterprise

Investment Presentation

Collect confidential information

Open clients’ accounts in the respective bank

Fill up CIB form

Sending CIB to Bangladesh

Bank

CIB report from Bangladesh

Bank NILUC

(Unclassified)

SS (Substandard

)

DF (Doubtful)

BL (Bad lose)

Investment decision

considering CIB report

Investment Sanction

29

SME Investment Process Flow

30

Disbursement of SME Investmenta) Pre Disbursement Manual

Activities

◦ Prepare investment file

◦ Charge documents checking

◦ Documents deficiency and problem resolving

◦ Prepare disbursement list

◦ Disbursement of the amount

Message sent to the unit office

MBS (Millennium Banking System) entries for disbursement:

◦ Initial ID generation

◦ Investment account opening

◦ Cost center assign Security details set-up Guarantor details set-up Loan other details set-up

◦ Risk fund collection

◦ Activision of the loan Loan sanction details set-up Repayment timetable set-up and

printing Loan activation Disbursement and voucher print Disbursement voucher posting

b) Post Disbursement Manual Activities

◦ Repayment schedule sent to unit office

◦ Investment details MBS entry

◦ Document stamp cancellation

◦ Send the investment file to archive

31

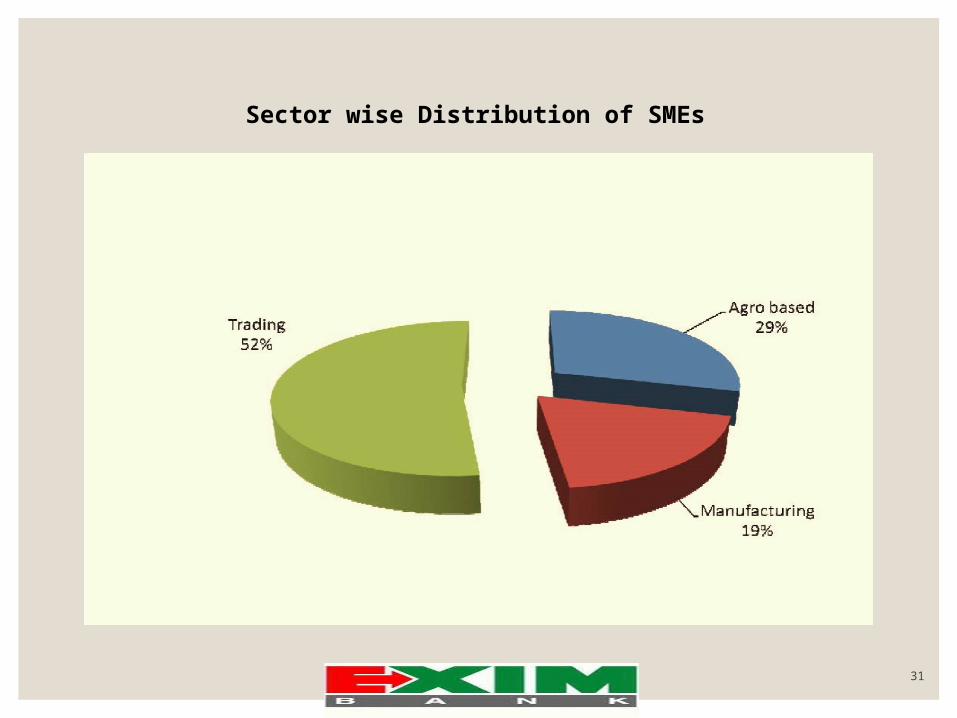

Sector wise Distribution of SMEs

32

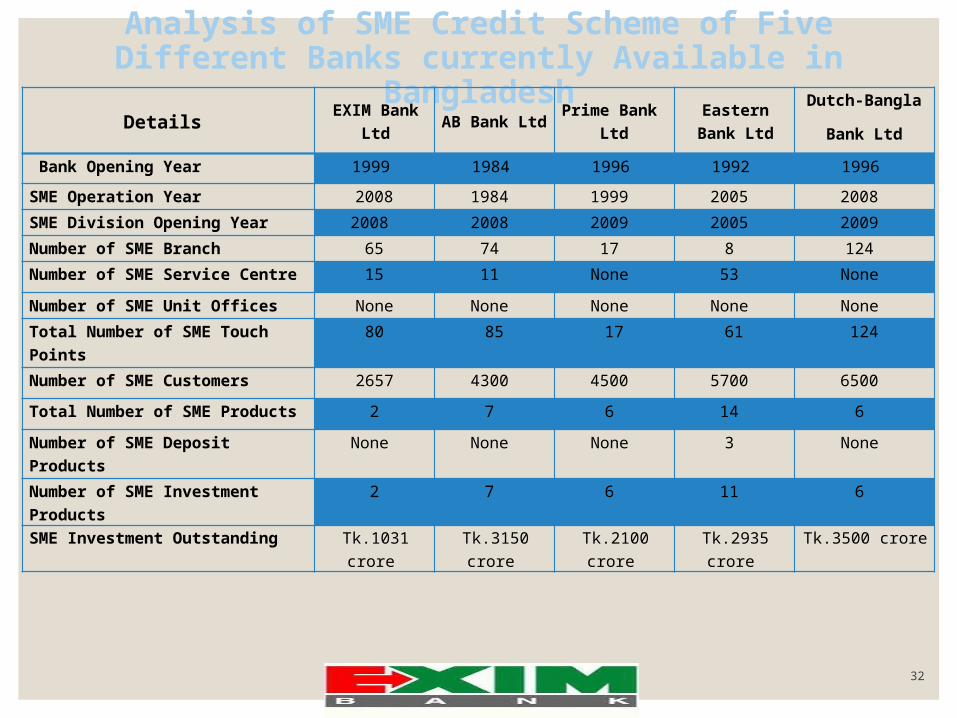

Analysis of SME Credit Scheme of Five Different Banks currently Available in

BangladeshDetails

EXIM Bank Ltd

AB Bank Ltd

Prime Bank Ltd

Eastern Bank Ltd

Dutch-Bangla

Bank Ltd

Bank Opening Year 1999 1984 1996 1992 1996

SME Operation Year 2008 1984 1999 2005 2008

SME Division Opening Year 2008 2008 2009 2005 2009

Number of SME Branch 65 74 17 8 124

Number of SME Service Centre 15 11 None 53 None

Number of SME Unit Offices None None None None None

Total Number of SME Touch Points

80 85 17 61 124

Number of SME Customers 2657 4300 4500 5700 6500

Total Number of SME Products 2 7 6 14 6

Number of SME Deposit Products

None None None 3 None

Number of SME Investment Products

2 7 6 11 6

SME Investment Outstanding Tk.1031 crore

Tk.3150 crore

Tk.2100 crore

Tk.2935 crore

Tk.3500 crore

33

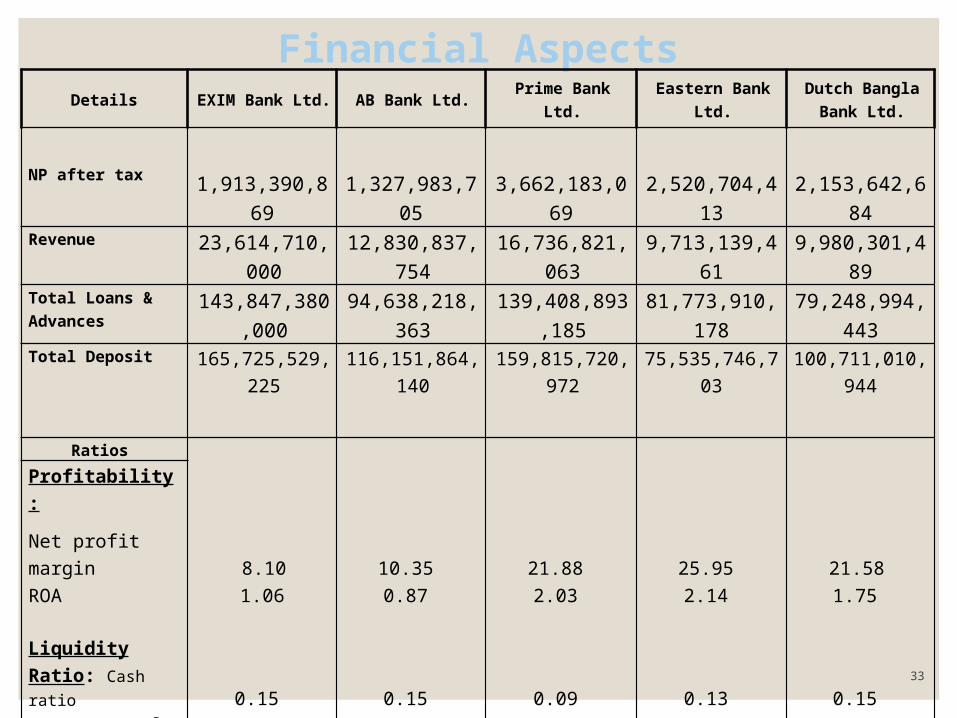

Financial AspectsDetails EXIM Bank Ltd. AB Bank Ltd. Prime Bank Ltd. Eastern Bank Ltd.

Dutch Bangla Bank Ltd.

NP after tax

1,913,390,869

1,327,983,705

3,662,183,069

2,520,704,413

2,153,642,684Revenue 23,614,710,000 12,830,837,754 16,736,821,063 9,713,139,461 9,980,301,489Total Loans & Advances

143,847,380,000 94,638,218,363 139,408,893,185 81,773,910,178 79,248,994,443

Total Deposit

165,725,529,225

116,151,864,140

159,815,720,972

75,535,746,703

100,711,010,944

Ratios

8.10

10.35

21.88

25.95 21.58

Profitability:

Net profit margin ROA 1.06 0.87 2.03 2.14 1.75

Liquidity Ratio: Cash ratio

0.15

0.15

0.09

0.13

0.15

Loans to Total Deposit 0.87 0.81 0.87 1.08 0.79

Loans to Total Asset 0.74 0.62 0.77 0.70 0.65

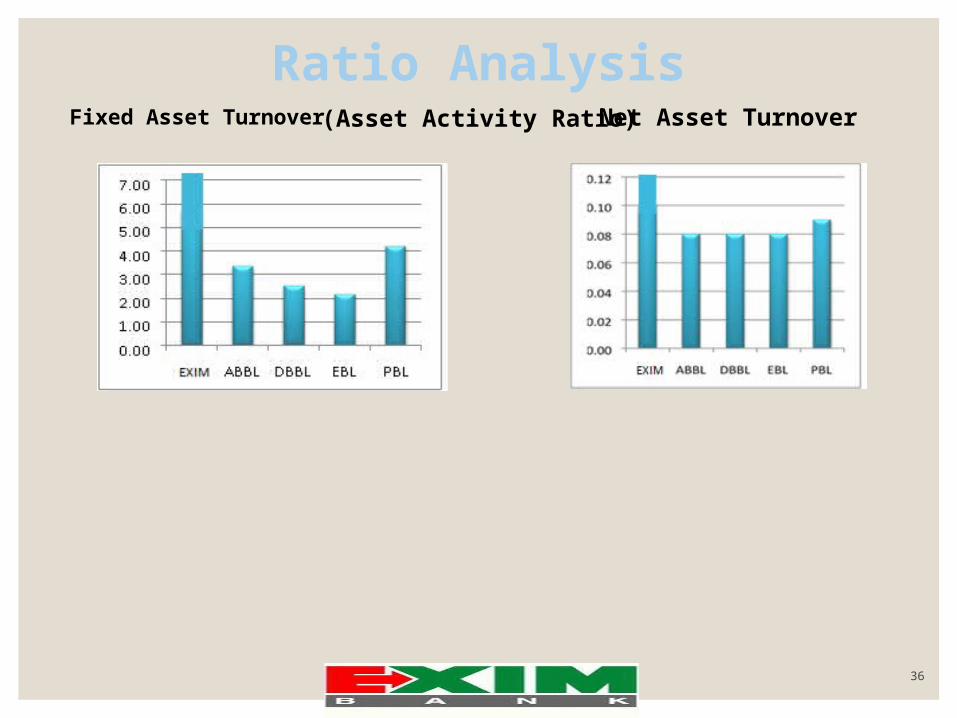

Asset Activity Ratio:

Fixed Asset Turnover

7.42

3.33

4.21

2.18

2.51

Net Asset Turnover 0.12 0.08 0.09 0.08 0.08

34

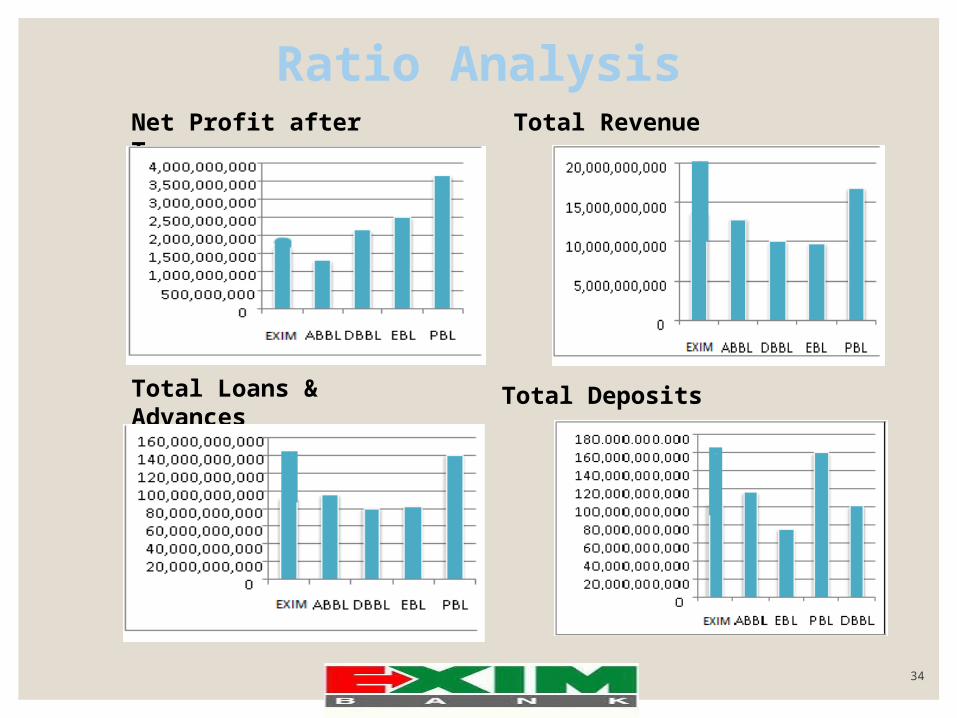

Ratio AnalysisNet Profit after Tax Total Revenue

Total Loans & Advances Total Deposits

35

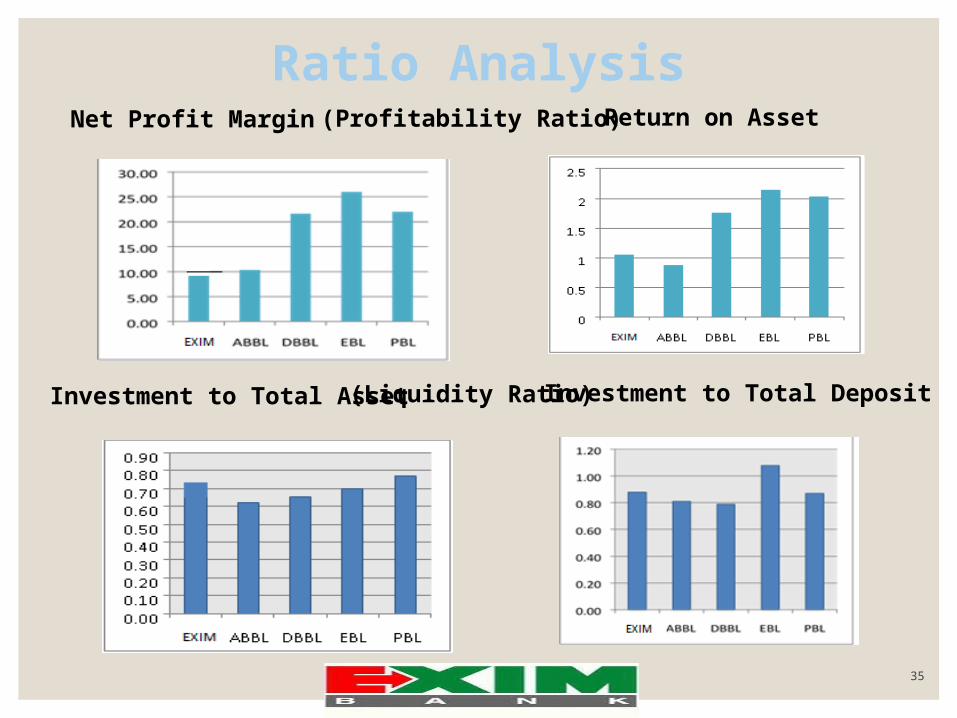

Net Profit Margin Return on Asset

Investment to Total Asset Investment to Total Deposit(Liquidity Ratio)

(Profitability Ratio)

Ratio Analysis

36

Fixed Asset Turnover Net Asset Turnover(Asset Activity Ratio)

Ratio Analysis

37

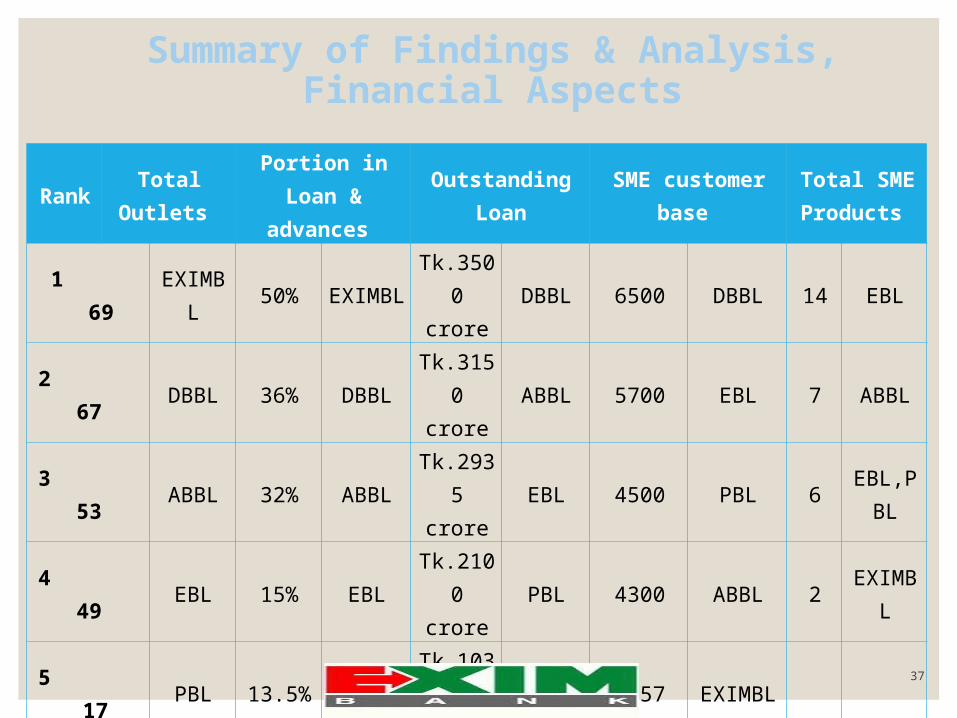

Summary of Findings & Analysis, Financial Aspects

RankTotal

Outlets

Portion in Loan &

advances

Outstanding Loan

SME customer base

Total SME Products

1 69EXIMB

L50%

EXIMBL

Tk.3500 crore

DBBL 6500 DBBL 14 EBL

2 67 DBBL 36% DBBLTk.3150 crore

ABBL 5700 EBL 7 ABBL

3 53 ABBL 32% ABBLTk.2935 crore

EBL 4500 PBL 6EBL,P

BL

4 49 EBL 15% EBLTk.2100 crore

PBL 4300 ABBL 2EXIMB

L

5 17

PBL 13.5% PBLTk.1031 crore

EXIMBL

2657 EXIMBL

38

Research part

39

Research PartProject’s Expenditures

Problem Statement

During our internship we worked specially SME investment of EXIM Bank Limited. SME investment section is most important for any bank. Although the performance of SME investment section of EXIMBL is good, however still some problems are facing by the department. So, we want to find out it and want to give some suggestions. And for this reason we are doing this research.

Particulars Cost (Taka)

Data Collection 800

Transportation 4000

Processing, Printing and

Binding

1600

Total = 6400

40

Materials1. Data collection - a)Primary Data b)Secondary Data

2. Sample - The sample of this study is the all customers of EXIM Bank

limited and some valued clients.

3. Population - Sampling unit or population of our study is existing

customers of EXIM Bank Limited.

4. Sample size - The sample size of my survey is fifty (50) customers of

EXIM Bank Limited. Here, n = sample size = 50

5. Sampling Procedure - To accurately determine the probability,

probability sampling is selected and it is simple random sampling.

6. Analysis of data - Relevant data for this report has been collected

primarily by direct investigation of different records, papers, documents

and different personnel.

41

Hypothesis DevelopmentWith a view of fulfilling the objectives some relevant hypothesis have been formulated for this study:

◦HA: SME investment has positive effect on success of the bank.

◦HA: SME investment has positive impact to increase on the level of EXIMBL’s customer satisfaction.

◦HA: EXIMBLs profit rate is more reasonable for SME investment.

◦HA: EXIMBL provides SME to women entrepreneurs with easy condition.

◦HA: EXIMBLs SME section uses proper system to meet the clients demand.

◦HA: EXIMBLs executives are performing well in the SME investment section.

42

Hypotheses TestingLikert Scale H1 H2 H3 H4 H5 H6

1 = Strongly Disagree

2 3 8 3 4 6

2 = Disagree 6 4 12 7 6 4

3 = Neither Agree Nor disagree

5 9 5 13 10 8

4 = Agree 12 14 10 7 17 20

5 = Strongly Agree 25 20 15 20 13 12

Total 202 193 162 184 179 178

Average 4.04 3.88 3.24 3.68 3.58 3.56

Standard Deviation ( )

1.20 1.19 1.49 1.29 1.22 1.27

Z - Test Value 9.06 8.12 3.52 6.55 6.35 5.89

X

43

1. H0: SME investment has negative effect on success of the bank.

HA: SME investment has positive effect on success of the bank.

H0 : µ= 2.5

HA : µ>2.5

n = 50

Here, = 4.04

= 1.20

Zcal = ( - µ)/ ( /√n) = 9.06

At 5% level of significance, follows Z- distribution 0.05 = 1.645

Since Zcal > Ztab the null hypothesis is not accepted. So at 5% level of significance, it can be said that SME investment has positive effect on success of the Bank.

Strongly Disagree

4%

Dis-agree12%

Nei-ther Agree Nor dis-

agree10%

Agree

24%

Strongly

Agree

50%

H1

44

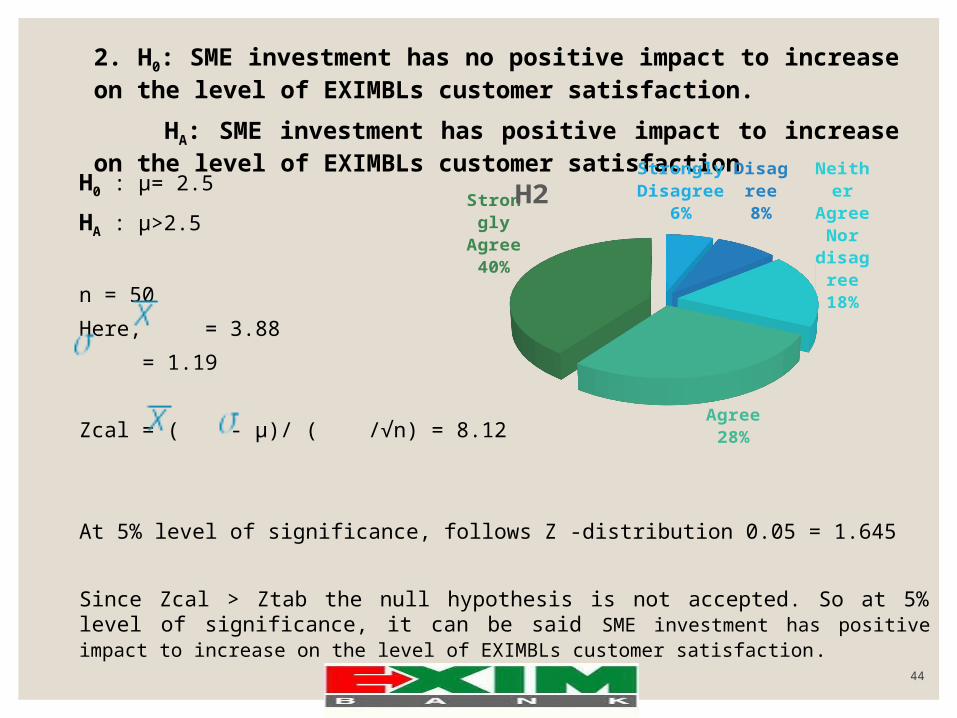

2. H0: SME investment has no positive impact to increase on the level of EXIMBLs customer satisfaction.

HA: SME investment has positive impact to increase on the level of EXIMBLs customer satisfaction

H0 : µ= 2.5

HA : µ>2.5

n = 50

Here, = 3.88

= 1.19

Zcal = ( - µ)/ ( /√n) = 8.12

At 5% level of significance, follows Z -distribution 0.05 = 1.645

Since Zcal > Ztab the null hypothesis is not accepted. So at 5% level of significance, it can be said SME investment has positive impact to increase on the level of EXIMBLs customer satisfaction.

Strongly Disagree

6%Dis-agre

e8%

Nei-ther Agree Nor dis-agre

e18%

Agree28%

Strongly

Agree

40%

H2

45

3. H0 : EXIMBL interest rate is not more reasonable for SME investment.

HA : EXIMBL interest rate is more reasonable for SME investment.

H0 : µ= 2.5

HA : µ> 2.5

n = 50

Here, = 3.24

= 1.49

Zcal = ( - µ)/ ( /√n) = 3.52

At 5% level of significance, follows Z distribution 0.05 =1.645

Since Zcal > Ztab the null hypothesis is not accepted. So at 5% level of significance, it can be said EXIMBL interest rate is more reasonable for SME investment.

Strongly Dis-agre

e16%

Dis-agre

e24%

Neither Agree Nor disagree

10%

Agree20%

Strongly Agree30%

H3

46

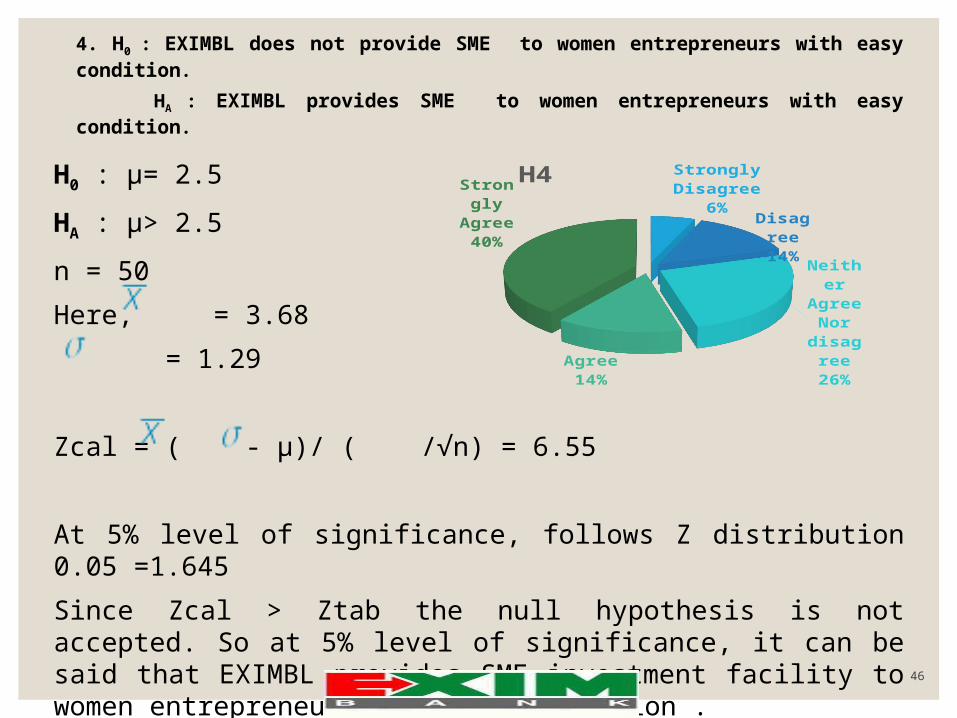

4. H0 : EXIMBL does not provide SME to women entrepreneurs with easy condition.

HA : EXIMBL provides SME to women entrepreneurs with easy condition.

H0 : µ= 2.5

HA : µ> 2.5

n = 50

Here, = 3.68

= 1.29

Zcal = ( - µ)/ ( /√n) = 6.55

At 5% level of significance, follows Z distribution 0.05 =1.645

Since Zcal > Ztab the null hypothesis is not accepted. So at 5% level of significance, it can be said that EXIMBL provides SME investment facility to women entrepreneurs with easy condition .

Strongly Disagree

6%Dis-agre

e14%

Nei-ther Agree Nor dis-agre

e26%

Agree14%

Strongly

Agree

40%

H4

47

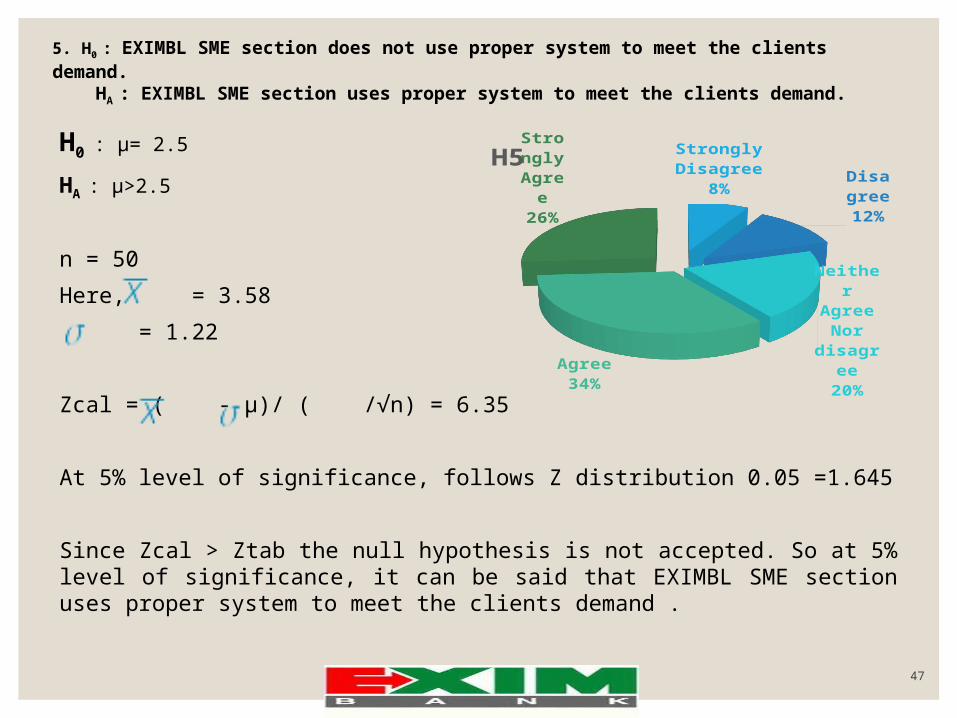

5. H0 : EXIMBL SME section does not use proper system to meet the clients demand. HA : EXIMBL SME section uses proper system to meet the clients demand.

H0 : µ= 2.5

HA : µ>2.5

n = 50

Here, = 3.58

= 1.22

Zcal = ( - µ)/ ( /√n) = 6.35

At 5% level of significance, follows Z distribution 0.05 =1.645

Since Zcal > Ztab the null hypothesis is not accepted. So at 5% level of significance, it can be said that EXIMBL SME section uses proper system to meet the clients demand .

Strongly Disagree

8%

Disagree12%

Nei-ther

Agree Nor dis-

agree20%

Agree34%

Strongly

Agree26%

H5

48

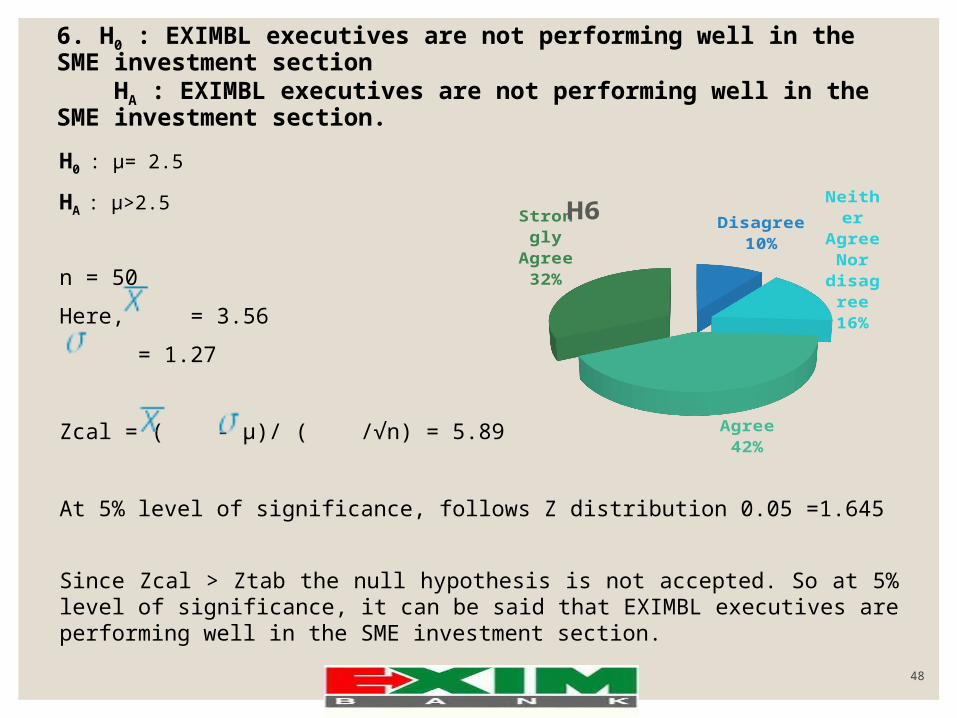

6. H0 : EXIMBL executives are not performing well in the SME investment section HA : EXIMBL executives are not performing well in the SME investment section.

H0 : µ= 2.5

HA : µ>2.5

n = 50

Here, = 3.56

= 1.27

Zcal = ( - µ)/ ( /√n) = 5.89

At 5% level of significance, follows Z distribution 0.05 =1.645

Since Zcal > Ztab the null hypothesis is not accepted. So at 5% level of significance, it can be said that EXIMBL executives are performing well in the SME investment section.

Disagree10%

Nei-ther Agree Nor dis-agre

e16%

Agree42%

Strongly

Agree

32%

H6

49

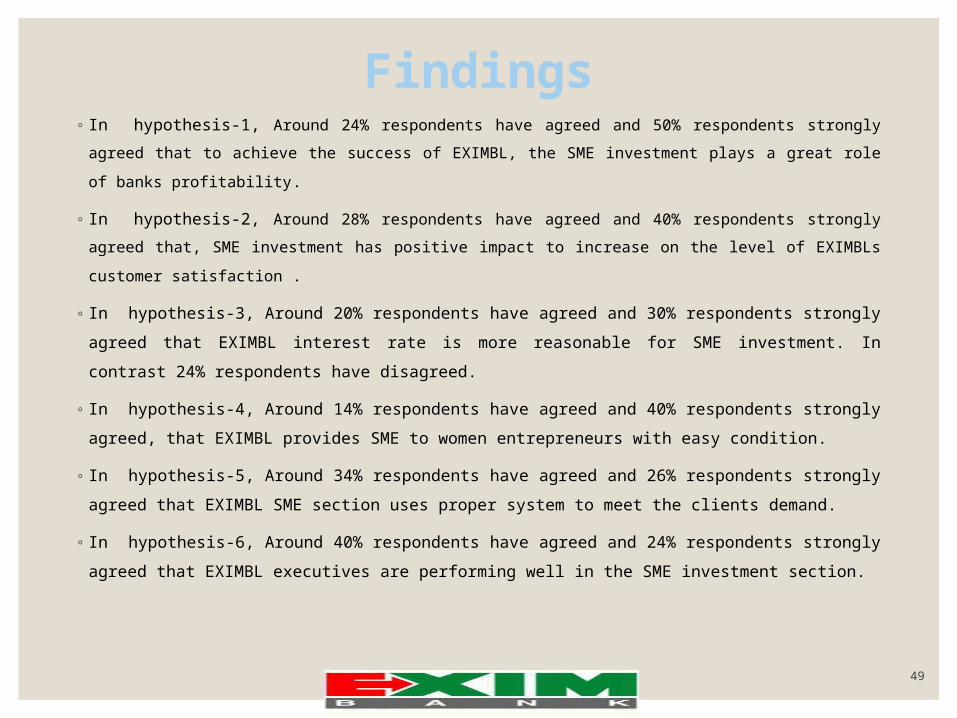

Findings◦ In hypothesis-1, Around 24% respondents have agreed and 50% respondents strongly

agreed that to achieve the success of EXIMBL, the SME investment plays a great role of

banks profitability.

◦ In hypothesis-2, Around 28% respondents have agreed and 40% respondents strongly

agreed that, SME investment has positive impact to increase on the level of EXIMBLs

customer satisfaction .

◦ In hypothesis-3, Around 20% respondents have agreed and 30% respondents strongly

agreed that EXIMBL interest rate is more reasonable for SME investment. In contrast

24% respondents have disagreed.

◦ In hypothesis-4, Around 14% respondents have agreed and 40% respondents strongly

agreed, that EXIMBL provides SME to women entrepreneurs with easy condition.

◦ In hypothesis-5, Around 34% respondents have agreed and 26% respondents strongly

agreed that EXIMBL SME section uses proper system to meet the clients demand.

◦ In hypothesis-6, Around 40% respondents have agreed and 24% respondents strongly

agreed that EXIMBL executives are performing well in the SME investment section.

50

Recommendation1.To achieve the success of EXIMBL, the SME investment plays a great role

of banks profitability. So EXIMBL should more careful on SME Investment.

2. To increase the level of customer satisfaction the bank should provide

incentives SME products and imposed the reasonable interest rate.

3.From the customers feedback the EXIMBLs interest rate is more

reasonable from others because their goal is that less profit more

customer. Even EXIMBL should more careful on their interest rate

because about 24% respondents have disagreed.

4.EXIMBL should focus on encouraging more women entrepreneurs for

SME investment. EXIMBL should also provide investment facility to

women entrepreneurs with easy provision continuously.

51

Cont…5.EXIMBL has their IT departments. So for SME investments they are

applying proper system by using modern technologies like they are

making on line CIB inquiry against SME holders. Sometimes their

network does not work properly in the branch. So they should more

careful about that.

6.The organizational success depends on their employees

performances. The EXIMBL executives providing the best

performances in the SME investment sections. Even EXIMBL should

always monitor the performance of its employees.

52

Conclusion

Do you have

???53

Related Documents