Exemplar for internal assessment resource Accounting for Achievement Standard 90977 Exemplar for Internal Achievement Standard Accounting Level 1 This exemplar supports assessment against: Achievement Standard 90977 Process financial transactions for a small entity. An annotated exemplar is an extract of student evidence, with a commentary, to explain key aspects of the standard. It assists teachers to make assessment judgements at the grade boundaries. New Zealand Qualifications Authority To support internal assessment from 2014 © NZQA 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Exemplar for internal assessment resource Accounting for Achievement Standard 90977

Exemplar for Internal Achievement Standard

Accounting Level 1

This exemplar supports assessment against:

Achievement Standard 90977

Process financial transactions for a small entity.

An annotated exemplar is an extract of student evidence, with a commentary, to explain key aspects of the standard. It assists teachers to make assessment judgements at the grade boundaries.

New Zealand Qualifications Authority

To support internal assessment from 2014

© NZQA 2014

Exemplar for internal assessment resource Accounting for Achievement Standard 90977

Grade Boundary: Low Excellence

1. For Excellence, the student needs to comprehensively process financial transactions for a small entity. This means correctly entering financial transactions impacting on all financial elements in the accounting records of the entity, including the consistently correct treatment of GST, non-GST, cash and electronic transactions and consistently following good accounting practice.

The student has completed three source documents. The bank reconciliation process has been completed accurately. The student entered transactions in the cash receipts journal (1) and cash payments journal (2). Good accounting practice has consistently been followed in the cash journals. Column totals and sundry column items have been accurately posted from the journals to ledger accounts. All ledger accounts have been correctly balanced. A chart of accounts has been applied to ledger accounts. Good accounting practice has been consistently followed in the ledger accounts (3). The trial balance was completed accurately. For a more secure Excellence, the student could:

• correct the single GST calculation error in the cash receipts journal (1) • use the account names provided in the resource material in the particulars

columns of the journals (1) (2).

`

© NZQA 2014

PENE’S PIZZA’s CASH JOURNALS

CASH RECEIPTS JOURNAL

Date Particulars Ref Receipts Bank GST received

Pizza sales

Catering sales

Sundry

May 14 Pizza sales 2997.00 300.00 2697.00

Catering sales 1440.00 187.83 1252.17

Shop equipment 450.00 4887.00 58.70 391.30

Pizza sales EFT 2520.00 328.70 2191.30

Catering sales EFT 1107.00 3627.00 144.39 962.61

May 28 Pizza sales 3,600.00 469.57 3130.43

Catering sales 342.00 44.61 297.39

Commission received 540.00 4482.00 70.44 469.56

Additional Capital DC 13500.00 13500.00

Pizza sales EFT 1800.00 234.79 1565.21

Catering sales EFT 1080.00 2880.00 140.87 939.13

May 30 Interest received BS 18.00 18.00

$29394.00 $1979.90 $9583.94 $3451.30 $14378.86

CASH PAYMENTS JOURNAL

Date Particulars Ref Bank GST paid Purchases Drawings Wages Sundry May 10 Purchases EFT 3060.00 399.13 2660.87

Wages AP 4500.00 4500.00

Rates DD 585.00 76.31 508.69

Drawings EFT 630.00 630.00

Electricity EFT 216.00 28.17 187.83

May 14 Drawings EFT 360.00 360.00

Shop equip. 135 4950.00 645.65 4304.35

Wages AP 1980.00 1980.00

Purchases EFT 2880.00 375.66 2504.34

May28 Water DD 180.00 23.48 156.52

Telephone EFT 108.00 14.09 93.91

May 30 Bank fees BS 27.00 27.00

Insurance AP 450.00 58.70 391.30

$19926.00 $1621.19 $5165.21 $860.86 $5634.78 $5669.60

1

2

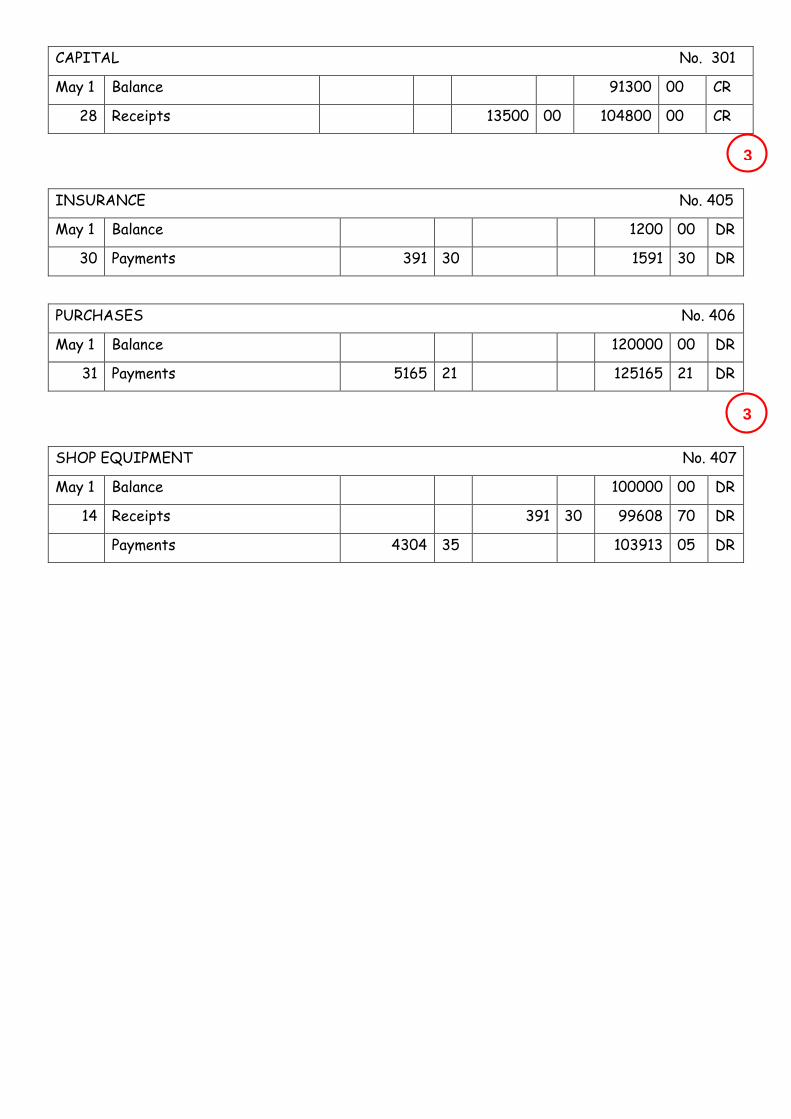

CAPITAL No. 301

May 1 Balance 91300 00 CR

28 Receipts 13500 00 104800 00 CR

INSURANCE No. 405

May 1 Balance 1200 00 DR

30 Payments 391 30 1591 30 DR

PURCHASES No. 406

May 1 Balance 120000 00 DR

31 Payments 5165 21 125165 21 DR

SHOP EQUIPMENT No. 407

May 1 Balance 100000 00 DR

14 Receipts 391 30 99608 70 DR

Payments 4304 35 103913 05 DR

3

3

Exemplar for internal assessment resource Accounting for Achievement Standard 90977

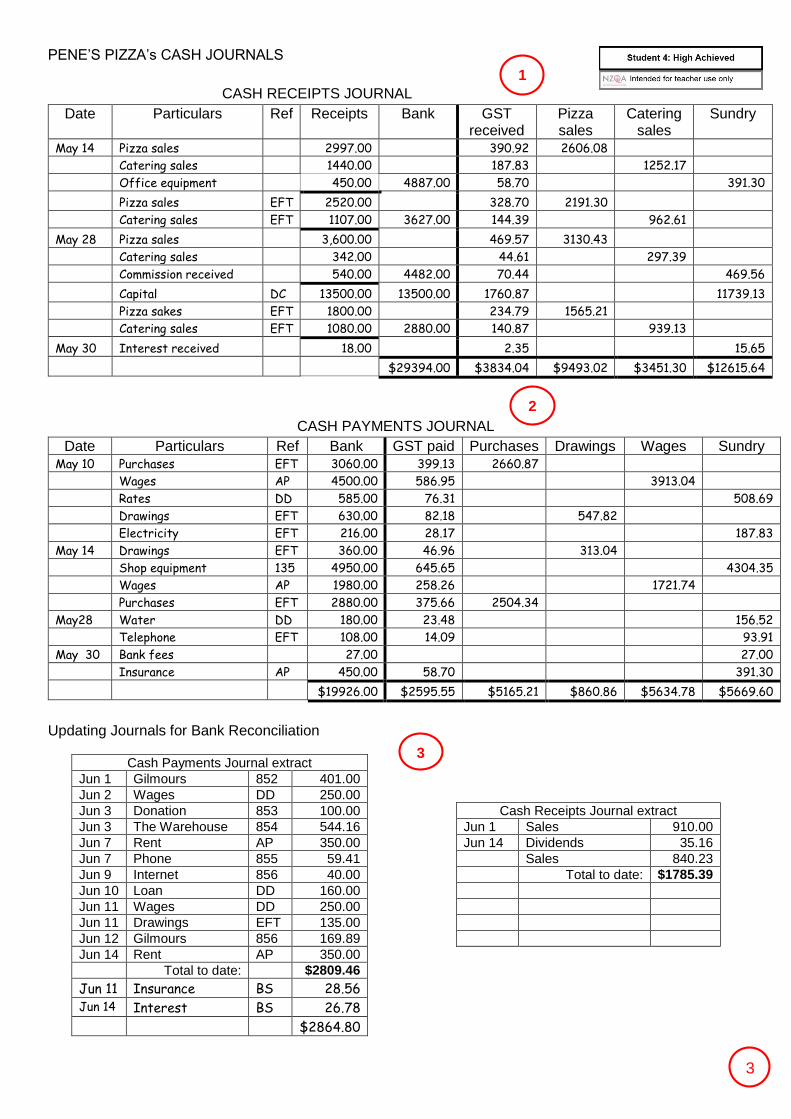

Grade Boundary: High Merit

2. For Merit, the student needs to process financial transactions in depth for a small entity. This means correctly entering financial transactions in the accounting records of the entity, including the correct treatment of GST, non-GST, and cash and electronic transactions, following good accounting practice The student has completed three source documents. The student entered transactions in the cash receipts journal (1) and cash payments journal (2). Good accounting practice has consistently been followed in the cash journals. The bank reconciliation process has been completed (3). Column totals and sundry column items have been posted from the journals to ledger accounts. All ledger accounts have been correctly balanced. A chart of accounts has been applied to ledger accounts. Good accounting practice has been consistently followed in the ledger accounts (4). The trial balance was completed accurately. To reach Excellence, the student could:

• record the electronic transfer of capital in the bank column (1) • in the reconciliation process, enter interest received in the cash receipts

journal rather than the cash payments journal (3) • use the GST-exclusive figure for the entry in the water account (4).

© NZQA 2014

CASH RECEIPTS JOURNAL

Date Particulars Ref Receipts Bank GST received

Pizza sales

Catering sales

Sundry

May 14 Pizza sales 2997.00 390.92 2697.00

Catering sales 1440.00 187.83 1252.17

Sold old shop equipment 450.00 4887.00 58.70 391.30

Pizza sales EFT 2520.00 328.70 2191.30

Catering sales EFT 1107.00 3627.00 144.39 962.61

May 28 Pizza sales 3,600.00 469.57 3130.43

Catering sales 342.00 44.61 297.39

Commission 540.00 70.44 469.56

Capital DC 13,500.00 17982.00 13500.00

Pizza sales EFT 1800.00 234.79 1565.21

Catering sales EFT 1080.00 2880.00 140.87 939.13

May 30 Interest received BS 18.00 18.00

$29394.00 $2070.82 $9583.94 $3451.30 $14378.86

CASH PAYMENTS JOURNAL

Date Particulars Ref Bank GST paid Purchases Drawings Wages Sundry May 10 Purchases EFT 3060.00 399.13 2660.87

Wages AP 4500.00 4500.00

Rates DD 585.00 76.31 508.69

Drawings EFT 630.00 630.00

Electricity EFT 216.00 28.17 187.83

May 14 Drawings EFT 360.00 360.00

Shop equip. 135 4950.00 645.65 4304.35

Wages AP 1980.00 1980.00

Purchases EFT 2880.00 375.66 2504.34

May28 Water DD 180.00 23.48 156.52

Telephone EFT 108.00 14.09 93.91

May 30 Bank fees BS 27.00 27.00

Insurance AP 450.00 58.70 391.30

$19926.00 $1621.19 $5165.21 $860.86 $5634.78 $5669.60

Updating Journals for Bank Reconciliation

Cash Payments Journal extract

Jun 1 Gilmours 852 401.00

Jun 2 Wages DD 250.00

Jun 3 Donation 853 100.00 Cash Receipts Journal extract

Jun 3 The Warehouse 854 544.16 Jun 1 Sales 910.00

Jun 7 Rent AP 350.00 Jun 14 Dividends 35.16

Jun 7 Phone 855 59.41 Sales 840.23

Jun 9 Internet 856 40.00 Total to date: $1785.39

Jun 10 Loan DD 160.00 Jun 11 Wages DD 250.00 Jun 11 Drawings EFT 135.00

Jun 12 Gilmours 856 169.89

Jun 14 Rent AP 350.00

Total to date: $2809.46

Jun 11 Insurance BS 28.56

Jun 14 Interest BS 26.78

Bank fees BS 12.00

$2850.02

1

2

3

INTEREST RECEIVED No. 401

1/5 Balance 1000 00 CR

31/5 Bank 18 00 1018 00 CR

LOAN No. 201

1/5 Balance 10000 00 CR

COMMISSION RECEIVED No. 402

28/5 Bank 469 56 469 56 CR

PURCHASES No. 106

1/5 Balance 120000 00 DR

31/5 Bank 5165 21 125165 21 DR

TELEPHONE No. 107

28/5 Bank 93 91 93 91 DR

WATER No. 108

28/5 Bank 180 00 180 00 DR

4

4

Exemplar for internal assessment resource Accounting for Achievement Standard 90977

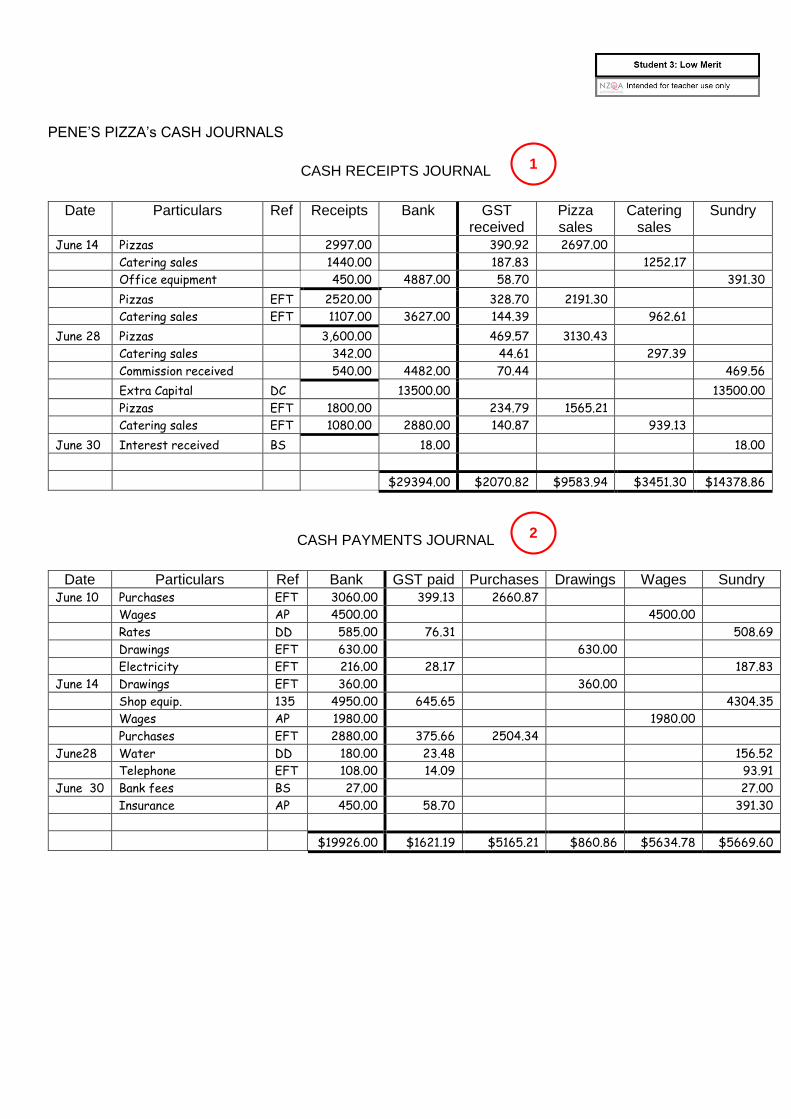

Grade Boundary: Low Merit

3. For Merit, the student needs to process financial transactions in depth for a small entity. This means correctly entering financial transactions in the accounting records of the entity, including the correct treatment of GST, non-GST, and cash and electronic transactions, following good accounting practice. The student has completed three source documents. The student entered transactions in the cash receipts journal (1) and cash payments journal (2). Good accounting practice has been followed in the cash journals. The bank reconciliation process has been accurately completed. Column totals and sundry column items have been posted from the journals to ledger accounts. All ledger accounts have been correctly balanced. A chart of accounts has been applied to ledger accounts. Good accounting practice has been followed in the ledger accounts (3). The trial balance was completed accurately. For a more secure Merit, the student could:

• use the account names provided in the resource material in the particulars column of the cash journals and record transactions for May rather than June (1) (2)

• use the correct account code for the shop equipment account and credit the $13,500 of new equity in the capital account (3).

© NZQA 2014

PENE’S PIZZA’s CASH JOURNALS

CASH RECEIPTS JOURNAL

Date Particulars Ref Receipts Bank GST received

Pizza sales

Catering sales

Sundry

June 14 Pizzas 2997.00 390.92 2697.00

Catering sales 1440.00 187.83 1252.17

Office equipment 450.00 4887.00 58.70 391.30

Pizzas EFT 2520.00 328.70 2191.30

Catering sales EFT 1107.00 3627.00 144.39 962.61

June 28 Pizzas 3,600.00 469.57 3130.43

Catering sales 342.00 44.61 297.39

Commission received 540.00 4482.00 70.44 469.56

Extra Capital DC 13500.00 13500.00

Pizzas EFT 1800.00 234.79 1565.21

Catering sales EFT 1080.00 2880.00 140.87 939.13

June 30 Interest received BS 18.00 18.00

$29394.00 $2070.82 $9583.94 $3451.30 $14378.86

CASH PAYMENTS JOURNAL

Date Particulars Ref Bank GST paid Purchases Drawings Wages Sundry June 10 Purchases EFT 3060.00 399.13 2660.87

Wages AP 4500.00 4500.00

Rates DD 585.00 76.31 508.69

Drawings EFT 630.00 630.00

Electricity EFT 216.00 28.17 187.83

June 14 Drawings EFT 360.00 360.00

Shop equip. 135 4950.00 645.65 4304.35

Wages AP 1980.00 1980.00

Purchases EFT 2880.00 375.66 2504.34

June28 Water DD 180.00 23.48 156.52

Telephone EFT 108.00 14.09 93.91

June 30 Bank fees BS 27.00 27.00

Insurance AP 450.00 58.70 391.30

$19926.00 $1621.19 $5165.21 $860.86 $5634.78 $5669.60

1

2

CAPITAL No. 301

May 1 Balance 91300 00 CR

28 Receipts 13500 00 77800 00 CR

INSURANCE No. 405

May 1 Balance 1200 00 DR

30 Payments 391 30 1591 30 DR

PURCHASES No. 406

May 1 Balance 120000 00 DR

31 Payments 5165 21 125165 21 DR

SHOP EQUIPMENT No. 407

May 1 Balance 100000 00 DR

14 Receipts 391 30 99608 70 DR

Payments 4304 35 103913 05 DR

3

3

Exemplar for internal assessment resource Accounting for Achievement Standard 90977

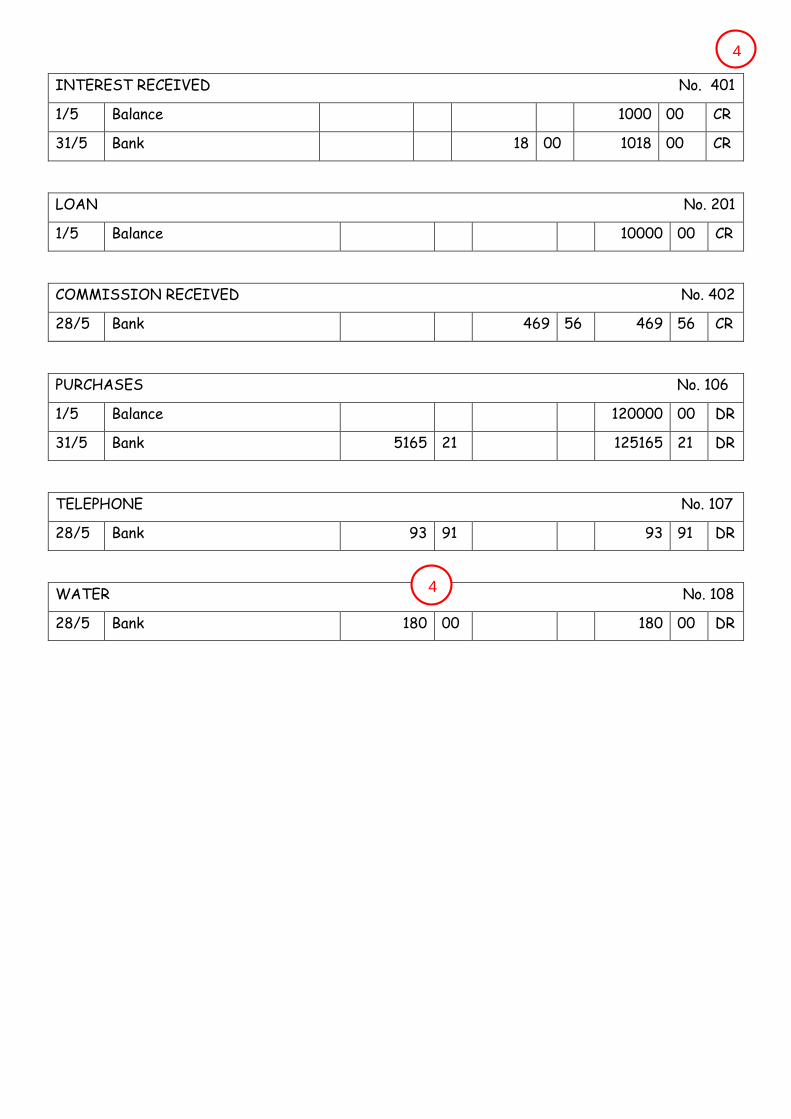

Grade Boundary: High Achieved

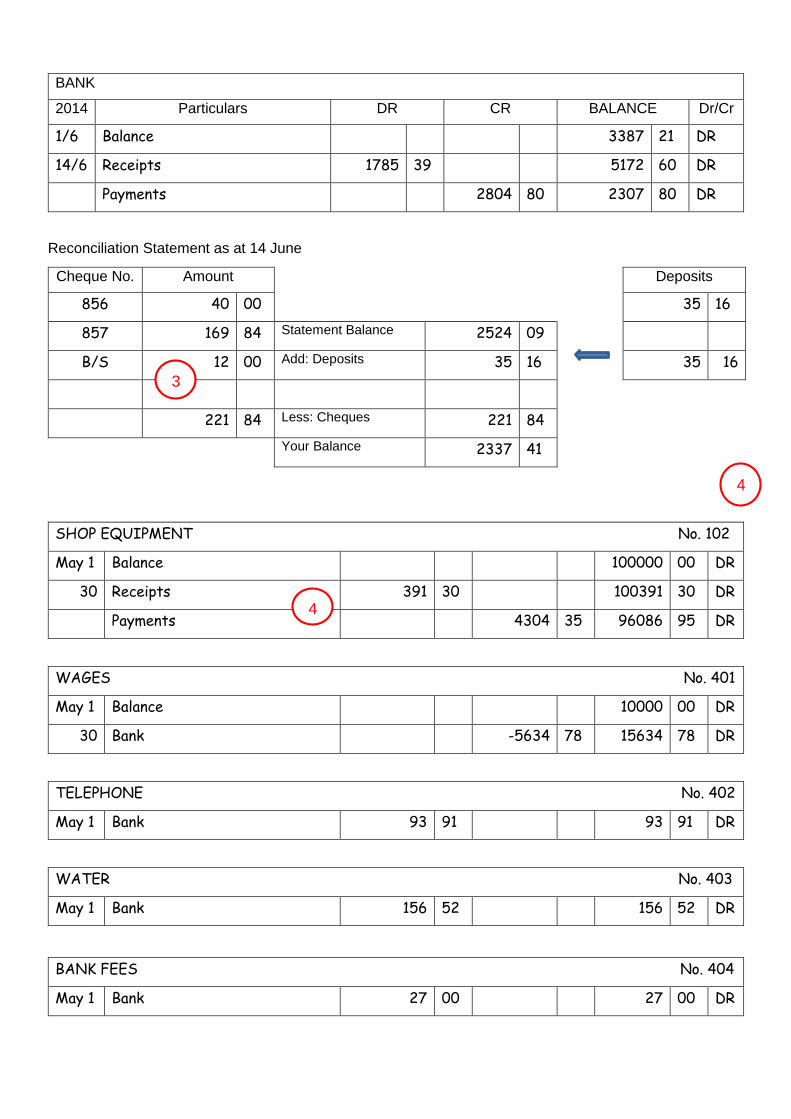

4. For Achieved, the student needs to process financial transactions for a small entity. This means correctly entering transactions in the accounting records of the entity. The student has completed source documents that can be accurately recorded. The student has entered transactions into the cash receipts journal (1) and cash payments journal (2). Good accounting practice has been followed. The student has reconciled the bank statement with journals and their bank account balance is correct on follow through (3). All ledger accounts have been balanced and the chart of account codes has been applied (4). Balances have been transferred to a trial balance. To reach Merit, the student could:

• use the account names provided in the resource material in the particulars columns of the cash receipts journal (1)

• accurately identify non-GST items in both journals (1) (2) • accurately update the journals with items from the bank statement and

enter the bank fee in the cash payments journal rather than on the bank reconciliation (3)

• credit the sale of equipment and debit the purchase in the shop equipment account (4).

© NZQA 2014

PENE’S PIZZA’s CASH JOURNALS

CASH RECEIPTS JOURNAL

Date Particulars Ref Receipts Bank GST received

Pizza sales

Catering sales

Sundry

May 14 Pizza sales 2997.00 390.92 2606.08

Catering sales 1440.00 187.83 1252.17

Office equipment 450.00 4887.00 58.70 391.30

Pizza sales EFT 2520.00 328.70 2191.30

Catering sales EFT 1107.00 3627.00 144.39 962.61

May 28 Pizza sales 3,600.00 469.57 3130.43

Catering sales 342.00 44.61 297.39

Commission received 540.00 4482.00 70.44 469.56

Capital DC 13500.00 13500.00 1760.87 11739.13

Pizza sakes EFT 1800.00 234.79 1565.21

Catering sales EFT 1080.00 2880.00 140.87 939.13

May 30 Interest received 18.00 2.35 15.65

$29394.00 $3834.04 $9493.02 $3451.30 $12615.64

CASH PAYMENTS JOURNAL

Date Particulars Ref Bank GST paid Purchases Drawings Wages Sundry May 10 Purchases EFT 3060.00 399.13 2660.87

Wages AP 4500.00 586.95 3913.04

Rates DD 585.00 76.31 508.69

Drawings EFT 630.00 82.18 547.82

Electricity EFT 216.00 28.17 187.83

May 14 Drawings EFT 360.00 46.96 313.04

Shop equipment 135 4950.00 645.65 4304.35

Wages AP 1980.00 258.26 1721.74

Purchases EFT 2880.00 375.66 2504.34

May28 Water DD 180.00 23.48 156.52

Telephone EFT 108.00 14.09 93.91

May 30 Bank fees 27.00 27.00

Insurance AP 450.00 58.70 391.30

$19926.00 $2595.55 $5165.21 $860.86 $5634.78 $5669.60

Updating Journals for Bank Reconciliation

Cash Payments Journal extract

Jun 1 Gilmours 852 401.00

Jun 2 Wages DD 250.00

Jun 3 Donation 853 100.00 Cash Receipts Journal extract

Jun 3 The Warehouse 854 544.16 Jun 1 Sales 910.00

Jun 7 Rent AP 350.00 Jun 14 Dividends 35.16

Jun 7 Phone 855 59.41 Sales 840.23

Jun 9 Internet 856 40.00 Total to date: $1785.39

Jun 10 Loan DD 160.00

Jun 11 Wages DD 250.00

Jun 11 Drawings EFT 135.00

Jun 12 Gilmours 856 169.89

Jun 14 Rent AP 350.00

Total to date: $2809.46

Jun 11 Insurance BS 28.56

Jun 14 Interest BS 26.78

$2864.80

3

1

2

3

BANK

2014 Particulars DR CR BALANCE Dr/Cr

1/6 Balance 3387 21 DR

14/6 Receipts 1785 39 5172 60 DR

Payments 2804 80 2307 80 DR

Reconciliation Statement as at 14 June

Cheque No. Amount Deposits

856 40 00 35 16

857 169 84 Statement Balance 2524 09

B/S 12 00 Add: Deposits 35 16 35 16

221 84 Less: Cheques 221 84

Your Balance 2337 41

SHOP EQUIPMENT No. 102

May 1 Balance 100000 00 DR

30 Receipts 391 30 100391 30 DR

Payments 4304 35 96086 95 DR

WAGES No. 401

May 1 Balance 10000 00 DR

30 Bank -5634 78 15634 78 DR

TELEPHONE No. 402

May 1 Bank 93 91 93 91 DR

WATER No. 403

May 1 Bank 156 52 156 52 DR

BANK FEES No. 404

May 1 Bank 27 00 27 00 DR

4

3

4

Exemplar for internal assessment resource Accounting for Achievement Standard 90977

Grade Boundary: Low Achieved

5. For Achieved, the student needs to process financial transactions for a small entity. This means correctly entering transactions in the accounting records of the entity.

The student has completed three source documents. The student has entered transactions into the cash receipts journal (1) and cash payments journal (2). The student has updated cash journals with items from the bank statement and has updated the bank account balance. Parts of the reconciliation statement have been completed accurately (3). All ledger accounts have been balanced and chart of account codes have been applied (4). For a more secure Achieved the student could:

• use the account names provided in the resource material in the particulars columns of the cash journals (1) (2)

• use the receipts and bank columns in the cash receipts journal to distinguish between cash and electronic receipts (1)

• avoid entering insurance and bank fees in the reconciliation statement as well as the cash payments journal extract (3)

• increase the drawings balance, correctly treat entries in the GST account, and enter debit entries in the water and bank fees accounts (4).

© NZQA 2014

CASH RECEIPTS JOURNAL

Date Particulars Ref Receipts Bank GST received

Pizza sales

Catering sales

Sundry

May 14 Pizza sales 2997.00 390.92 2606.08

Catering sales 1440.00 4437.00 187.83 1252.17

Shop equipment 450.00 450.00 58.70 391.30

Pizza sales EFT 2520.00 328.70 2191.30

Catering sales EFT 1107.00 3627.00 144.39 962.61

May 28 Pizza sales 3,600.00 469.57 3130.43

Catering sales 342.00 3942.00 44.61 297.39

Commission received 540.00 540.00 70.44 469.56

Capital contribution 13,500.00 13500.00 13500.00

Pizza sales EFT 1800.00 234.79 1565.21

Catering sales EFT 1080.00 2880.00 140.87 939.13

May 30 Interest received 18.00 18.00 18.00

$29394.00 $1979.90 $9583.94 $3451.30 $14378.86

CASH PAYMENTS JOURNAL

Date Particulars Ref Bank GST paid Purchases Drawings Wages Sundry May 10 Purchases EFT 3060.00 399.13 2660.87

Wages AP 4500.00 4500.00

Rates paid direct debit DD 585.00 76.31 508.69

Drawings EFT 630.00 630.00

Electricity paid EFT 216.00 28.17 187.83

May 14 Drawings EFT 360.00 360.00

New shop equipment 135 4950.00 645.65 4304.35

Wages AP 1980.00 1980.00

Purchases EFT 2880.00 375.66 2504.34

May28 Water direct debut DD 180.00 23.48 156.52

Telephone paid EFT 108.00 14.09 93.91

May 30 Bank fees 27.00 27.00

Insurance auto payment AP 450.00 58.70 391.30

$19926.00 $1621.19 $5165.21 $990.00 $6480.00 $5669.60

Updating Journals for Bank Reconciliation

Cash Payments Journal extract

Jun 1 Gilmours 852 401.00

Jun 2 Wages DD 250.00

Jun 3 Donation 853 100.00 Cash Receipts Journal extract

Jun 3 The Warehouse 854 544.16 Jun 1 Sales 910.00

Jun 7 Rent AP 350.00 Jun 14 Dividends 35.16

Jun 7 Phone 855 59.41 Sales 840.23

Jun 9 Internet 856 40.00 Total to date: $1785.39

Jun 10 Loan DD 160.00 Interest 26.78 Jun 11 Wages DD 250.00 $1812.17 Jun 11 Drawings EFT 135.00

Jun 12 Gilmours 856 169.89

Jun 14 Rent AP 350.00

Total to date: $2809.46

Jun 11 Insurance BS 28.56

Jun 14 Interest BS 26.78

Bank fees BS 12.00

$2850.02

3

1

2

BANK

2014 Particulars DR CR BALANCE Dr/Cr

1/6 Balance 3387 21 DR

14/6 Receipts 1812 17 5199 38 DR

Payments 2850 02 2349 36 DR

Reconciliation Statement as at 14/6/14

Cheque No. Amount Deposits

Internet 40 00 35 16

Gilmours 169 89 Statement Balance 2524 09 26 78

Insurance 28 56 Add: Deposits 61 94 61 94

Bank fee 12 00 2586 03

250 45 Less: Cheques 250 45 Your Balance 2335 58

DRAWINGS No. 502

May 1 Balance 42700 00 DR

31 Payments 990 00 41710 00 DR

GST PAYABLE No. 203

May 1 Balance 7200 00 CR

31 Receipts 1979 90 9179 90 CR

31 Payments 1621 19 7558 71 CR

INSURANCE No. 404

May 1 Balance 1200 00 DR

28 Bank 450 00 1650 00 DR

TELEPHONE No. 405

May 28 Bank 93 91 93 91 DR

WATER No. 406

May 28 Bank 156 52 DR

BANK FEES No. 407

May 28 Bank 27 00 DR

4

3

3

3

4

4

Exemplar for internal assessment resource Accounting for Achievement Standard 90977

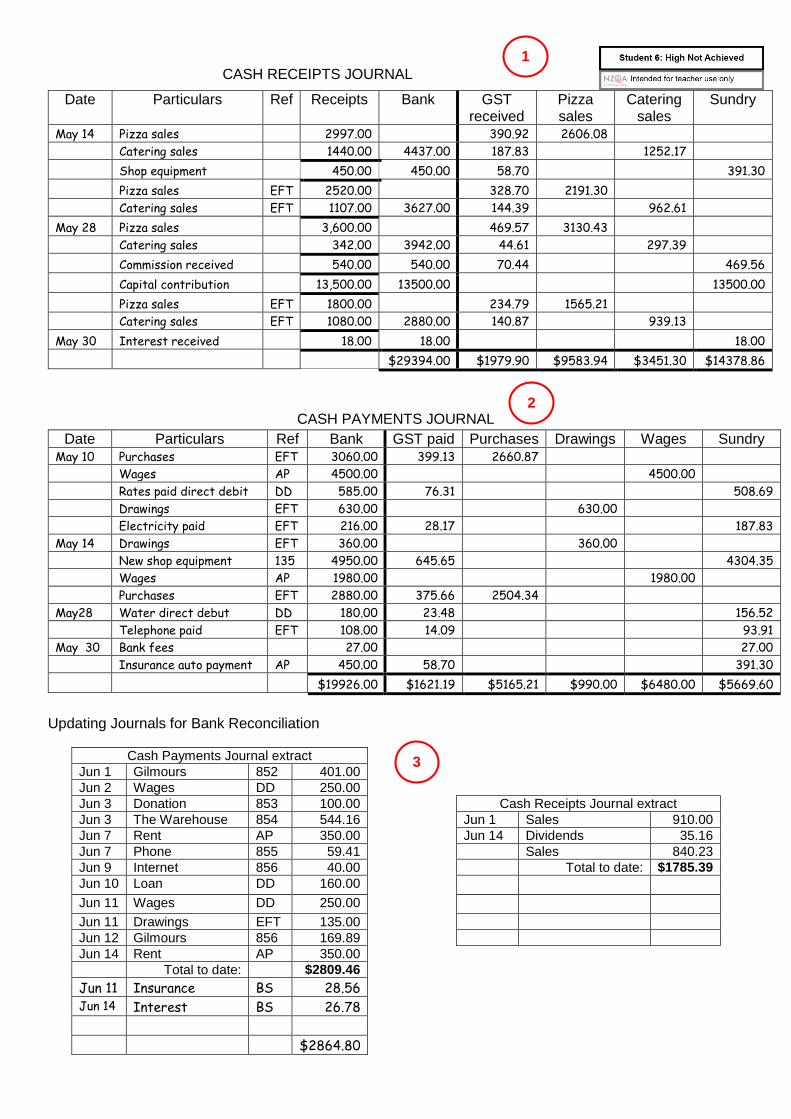

Grade Boundary: High Not Achieved

6. For Achieved, the student needs to process financial transactions for a small entity. This means correctly entering transactions in the accounting records of the entity.

The student has accurately completed the source documents. The student has entered transactions into the cash receipts journal (1) and cash payments journal (2). The student has updated the cash payments journal with items from the bank statement and has updated the bank account balance. The bank reconciliation statement has been processed correctly (3). All ledger accounts have been balanced and chart of account codes have been applied (4). To reach Achieved the student could demonstrate understanding of financial elements by:

• crediting the commission account and debiting the purchases and rates accounts

• entering figures in the debit column in the other expense accounts (4).

© NZQA 2014

CASH RECEIPTS JOURNAL

Date Particulars Ref Receipts Bank GST received

Pizza sales

Catering sales

Sundry

May 14 Pizza sales 2997.00 390.92 2606.08

Catering sales 1440.00 4437.00 187.83 1252.17

Shop equipment 450.00 450.00 58.70 391.30

Pizza sales EFT 2520.00 328.70 2191.30

Catering sales EFT 1107.00 3627.00 144.39 962.61

May 28 Pizza sales 3,600.00 469.57 3130.43

Catering sales 342.00 3942.00 44.61 297.39

Commission received 540.00 540.00 70.44 469.56

Capital contribution 13,500.00 13500.00 13500.00

Pizza sales EFT 1800.00 234.79 1565.21

Catering sales EFT 1080.00 2880.00 140.87 939.13

May 30 Interest received 18.00 18.00 18.00

$29394.00 $1979.90 $9583.94 $3451.30 $14378.86

CASH PAYMENTS JOURNAL

Date Particulars Ref Bank GST paid Purchases Drawings Wages Sundry May 10 Purchases EFT 3060.00 399.13 2660.87

Wages AP 4500.00 4500.00

Rates paid direct debit DD 585.00 76.31 508.69

Drawings EFT 630.00 630.00

Electricity paid EFT 216.00 28.17 187.83

May 14 Drawings EFT 360.00 360.00

New shop equipment 135 4950.00 645.65 4304.35

Wages AP 1980.00 1980.00

Purchases EFT 2880.00 375.66 2504.34

May28 Water direct debut DD 180.00 23.48 156.52

Telephone paid EFT 108.00 14.09 93.91

May 30 Bank fees 27.00 27.00

Insurance auto payment AP 450.00 58.70 391.30

$19926.00 $1621.19 $5165.21 $990.00 $6480.00 $5669.60

Updating Journals for Bank Reconciliation

Cash Payments Journal extract

Jun 1 Gilmours 852 401.00

Jun 2 Wages DD 250.00

Jun 3 Donation 853 100.00 Cash Receipts Journal extract

Jun 3 The Warehouse 854 544.16 Jun 1 Sales 910.00

Jun 7 Rent AP 350.00 Jun 14 Dividends 35.16

Jun 7 Phone 855 59.41 Sales 840.23

Jun 9 Internet 856 40.00 Total to date: $1785.39

Jun 10 Loan DD 160.00 Jun 11 Wages DD 250.00 Jun 11 Drawings EFT 135.00

Jun 12 Gilmours 856 169.89

Jun 14 Rent AP 350.00

Total to date: $2809.46

Jun 11 Insurance BS 28.56

Jun 14 Interest BS 26.78

$2864.80

1

3

2

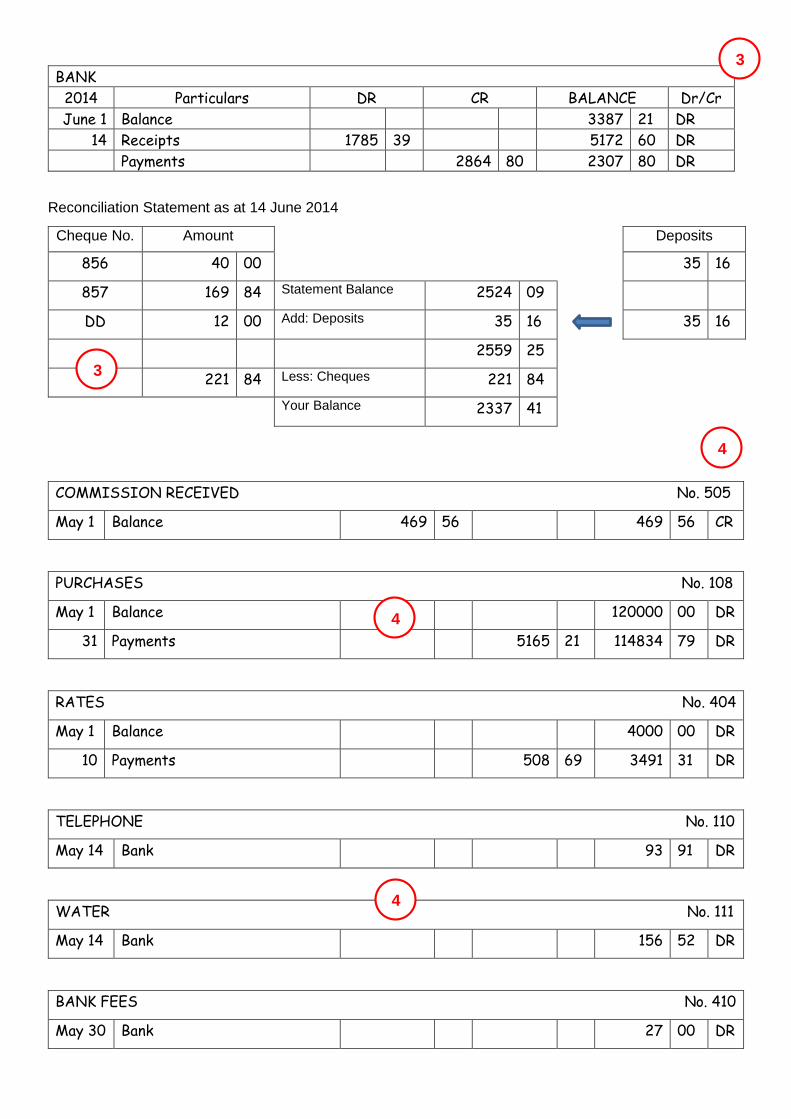

BANK

2014 Particulars DR CR BALANCE Dr/Cr

June 1 Balance 3387 21 DR

14 Receipts 1785 39 5172 60 DR

Payments 2864 80 2307 80 DR

Reconciliation Statement as at 14 June 2014

Cheque No. Amount Deposits

856 40 00 35 16

857 169 84 Statement Balance 2524 09

DD 12 00 Add: Deposits 35 16 35 16

2559 25

221 84 Less: Cheques 221 84

Your Balance 2337 41

COMMISSION RECEIVED No. 505

May 1 Balance 469 56 469 56 CR

PURCHASES No. 108

May 1 Balance 120000 00 DR

31 Payments 5165 21 114834 79 DR

RATES No. 404

May 1 Balance 4000 00 DR

10 Payments 508 69 3491 31 DR

TELEPHONE No. 110

May 14 Bank 93 91 DR

WATER No. 111

May 14 Bank 156 52 DR

BANK FEES No. 410

May 30 Bank 27 00 DR

3

4

4

3

4

Related Documents