Exchange Rate “Fundamentals” FIN 40500: International Finance

Exchange Rate “Fundamentals” FIN 40500: International Finance.

Dec 22, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Exchange Rate “Fundamentals”

FIN 40500: International Finance

Economic models represent an attempt to explain various phenomena with observable variables.

Economic Model

Exogenous Variables

Endogenous Variables

These variables are what we are trying to explain

These variables are what we are taking as “given”

An economic model is simply a set of assumptions

Lets start with a simply one…

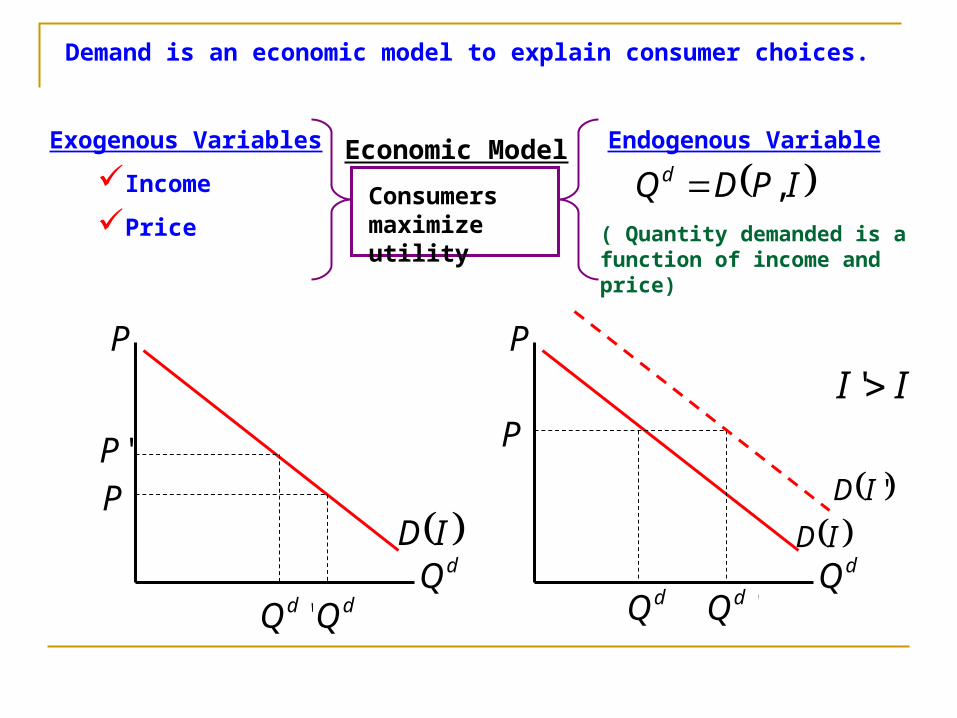

Demand is an economic model to explain consumer choices.

Exogenous Variables

Income

Price

Economic Model Endogenous Variable

Consumers maximize utility

IPDQd ,( Quantity demanded is a function of income and price)

dQ ID

dQ

P

ID 'ID

II 'P

P'P

'dQ dQ

P

'dQdQ

Equilibrium models use supply and demand to explain price

Exogenous Variables

Income

Costs

Economic Model Endogenous Variable

Price adjusts to clear the market

( Price is a function of income and costs)

CIPP ,

CS

ds QQ

dQ ID

P

P

sd QQ

IPDQd ,

CPSQ s ,

Ultimately, the point is to use the economic model to pricing function that we can estimate empirically

CS

dQ ID

P

P

sd QQ

CICIP 210,

Parameters to be estimated

(+) (+)

Once we have an estimated pricing function, we can use it to forecast

1121101 tttt CIP

Forecasts for income and costs

General Equilibrium Models try to explain multiple prices simultaneously using multiple markets

PepsiCoke PCIPP ,,

IPPDQ PepsiCokedCoke ,,

CokePepsi PCIPP ,,

IPPDQ PepsiCokedPepsi ,,

CPPDQ PepsiCokesCoke ,, CPPDQ PepsiCoke

sPepsi ,,

CS

dQ ID

P

P

sd QQ

CS

dQ ID

P

P

sd QQ

Home Currency (M) Pays no interest, but needed to buy goods

Domestic Bonds (B) Pays interest rate (i)

Foreign Bonds (B*) Pays interest rate (i*), payable in foreign currency

Foreign Currency (M*) Pays no interest, but needed to buy foreign goods

Any international general equilibrium must have at least four commodities

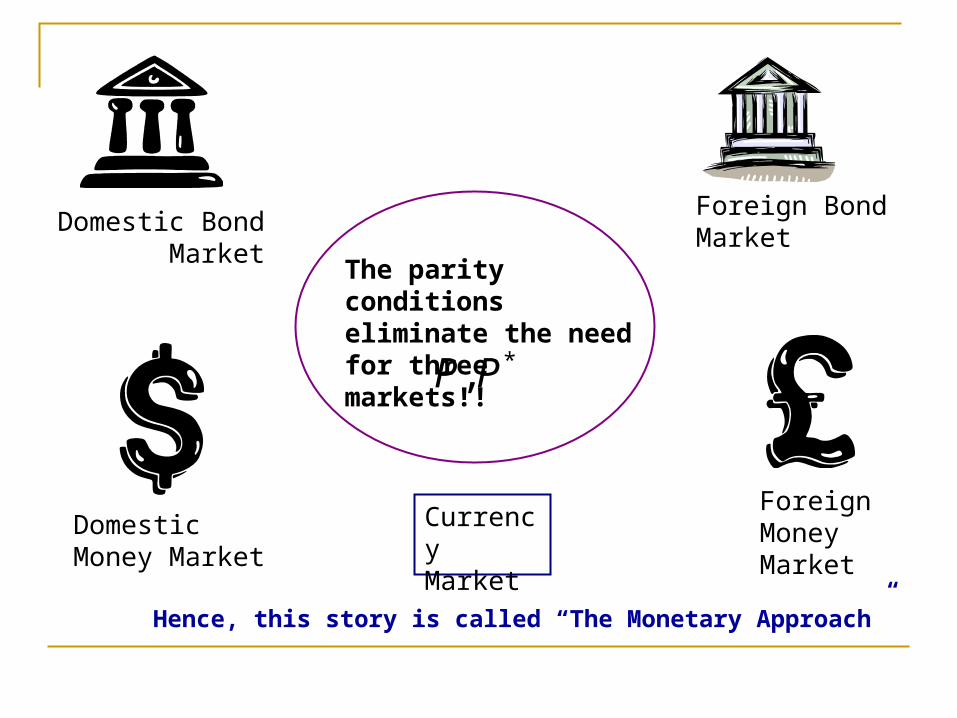

Foreign Bond Market

Domestic Money Market

Domestic Bond Market

Households choose a combination of the four assets for their portfolios

Foreign Money Market

Currency Market

BennyFluffy

Foreign Bond Market

Domestic Money Market

Domestic Bond Market

We need five prices to clear all five markets

Foreign Money Market

Currency Market

eiiPP ,,,, **

Purchasing Power Parity

Currency Markets

Uncovered Interest Parity

*ePP

eEii %*

The parity conditions can make things a lot simpler!

Foreign Bond Market

Domestic Money Market

Domestic Bond Market

Foreign Money Market

Currency Market

The parity conditions eliminate the need for three markets!!

*,PP

Hence, this story is called “The Monetary Approach”

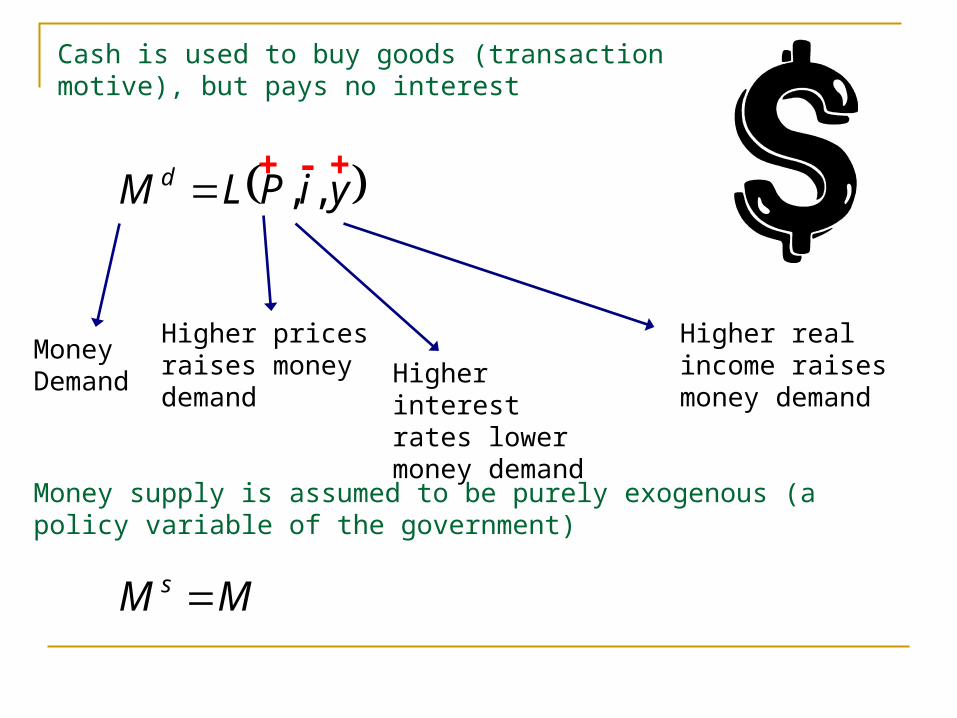

Cash is used to buy goods (transaction motive), but pays no interest

- +

Money Demand Higher interest

rates lower money demand

Higher real income raises money demand

Higher prices raises money demand

+ yiPLM d ,,

Money supply is assumed to be purely exogenous (a policy variable of the government)

MM s

++ - yiL ,M

M

P

P

An equilibrium price level clears the money market (i.e. supply equals demand)

If prices are too high, there won’t be enough money available to buy all the goods and services available

If prices are too low, there is excess money floating around

yiMPP ,,

++ - yiL ,M

M

P

P

An increase in money supply raises the price level

As the government makes more currency available, demand for goods and services increases. This allows suppliers to raise their prices.

At the initial price, there is an excess supply of currency

yiL ,M

M

P

PAn increase in interest rates lowers money demand – this raises the price level (holding money supply fixed)

yiL ,M

M

P

P An increase in real income raises the demand for money – this lowers the price level (holding money supply fixed)

++ - yiL ,M

M

P

P

If we assign a particular functional form to money demand, we can solve for the equilibrium price level analytically.

MM

i

PYM

s

d

1

If we set money supply equal to money demand and solve for price, we get

y

MiP 1

Domestic Money Market Foreign Money Market

PPP

*

*** 1y

MiP

y

MiP 1

*ePP

*

**11y

Mie

y

Mi

We can assume that the foreign money market is identical to the domestic money market. Using PPP and the two Money Market equilibrium conditions, we get the “fundamentals” for a currency

Now, solve for the exchange rate

Relative Money Stocks

Relative Outputs

Relative Interest Rates

*

*

* 1

1

i

i

Y

Y

M

Me

Taking the previous expression and solving for the exchange rate, we get

These are known as currency “fundamentals”

A regression using fundamentals would generally take the form:

tttttttt iiyyMMe *3

*2

*1 %%%%%

Percentage change in exchange rate (dollars per foreign currency) – an increase is a dollar depreciation

Parameters to be estimated

0

0,

2

31

Estimated parameters of this regression are often statistically insignificant:

Implied by the monetary framework

50

100

150

200

250

300

Jan-80 Jan-84 Jan-88 Jan-92 Jan-96

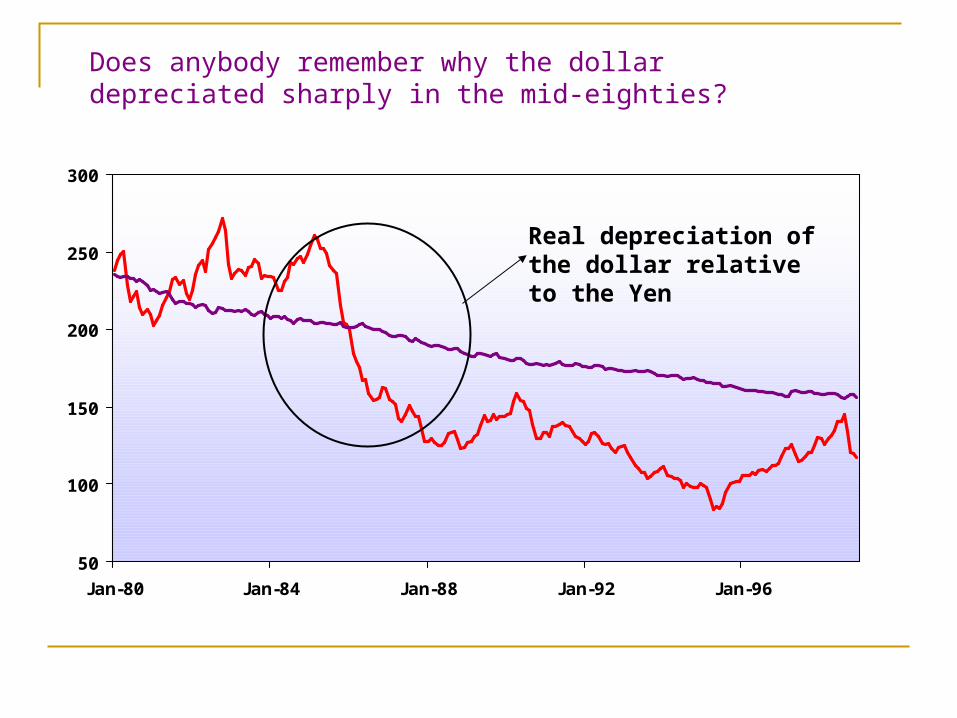

Note that while the “fundamentals” seem to track the general trend of the dollar, they don’t pick up the shorter term movements

Fundamentals

USD/JPY

0.4

0.5

0.6

0.7

0.8

0.9

1

Jan-80 Jan-84 Jan-88 Jan-92 Jan-96

The fact is that fundamentals just don’t exhibit enough variance to explain exchange rate movements in the short term

Fundamentals

USD/GBP

Real Exchange Rate

Recall that PPP often fails in the short run. This is possibly due to trading friction or relative price changes

*

*

* 1

1

i

i

Y

Y

M

MRERe

Real exchange rate changes create a problem…they tend to follow random walks (i.e. unit root processes for you statistics buffs) and are, hence, unpredictable.

50

100

150

200

250

300

Jan-80 Jan-84 Jan-88 Jan-92 Jan-96

Real depreciation of the dollar relative to the Yen

Does anybody remember why the dollar depreciated sharply in the mid-eighties?

Recall that UIP implies that the differences in nominal interest rates reflects expectations of currency price changes (countries with high interest rates should expect their currencies to depreciate

1* % teEiiUncovered Interest Parity

*** %%%%% ttttttt iiyyMMe

1** %%%%%% tttttt eEyyMMe

This incorporates an expectation of the future into the fundamentals

Suppose that expectations are stable (i.e. coincide with future fundamentals

1** %%%%%% tttttt eEyyMMe

211 %% ttt eEfEeEtf

Continue the substitution process forward

21 % tttt eEfEfe

1iitt fEe Today’s currency price depends on

ALL future fundamentals!

Alternatively, its possible for expectations to be destabilizing (i.e. speculative bubbles)

1** %%%%%% tttttt eEyyMMe

2111 %% tttt eENFfEeE

tf

Continue the substitution process forward

211 % ttttt eENFfEfe

11 iit

iitt NFfEe

Some “non-fundamental” factor

A “Bubble” Term!!

*ePP

Why don’t trade deficits matter in the monetary approach? Remember, this framework assumes that PPP and UIP always hold

Trade deficits aren’t a consequence of the price of foreign goods relative to US goods – PPP assures that these prices are the same

Instead, trade deficits are motivated by real interest rates – low interest rates will lower domestic saving and increase domestic spending. This creates a trade deficit.

r

SI ,

wr TGI

SBut with globally integrated capital markets, every country takes the world interest rate as a constant.

Normally, we think of a country’s currency appreciating during an expansion while its trade deficit worsens.

r

SI ,

wr TGI

S Trade deficits are determined in asset markets. Rising income tends to raise investment expenditures and lowers savings – the world interest rate remains unaffected, but the trade deficit worsens

yiL ,M

M

P

P

Meanwhile, in the domestic money market, an increase in income raises money demand and lowers prices

A drop in the domestic price level causes the dollar to appreciate

If commodity prices are free to adjust, then commodity markets/money markets take center stage in currency price determination (PPP)

There is no correlation between trade deficits and currency prices

Volatility in currency markets is created by relative price changes (real exchange rate changes) or speculative behavior

These relative price changes are passed onto nominal exchange rates

The Bottom Line…

Related Documents