Evolution of the North American Beef Industry By Larry Martin, Kevin Grier, and Simon Dessureault George Morris Centre November 2004 Presented to the Saskatchewan Agrivision Corporation Inc. and Canadian Western Agribition seminar on November 22, 2004

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Evolution of the North American Beef Industry By Larry Martin, Kevin Grier, and Simon Dessureault

George Morris Centre November 2004

Presented to the Saskatchewan Agrivision Corporation Inc. and Canadian Western Agribition seminar on November 22, 2004

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 2

Table of Contents Evolution of the North American Beef Industry................................................................. 3 1. Evolution of the North American Beef Industry......................................................... 3

Statistical Overview of the Canadian Beef Industry ....................................................... 3 The Cow Herd - History and Trends........................................................................... 3 Composition and Geographic Distribution of Cattle Inventory .................................. 6

Marketing and Structural Change ................................................................................... 7 Beef and Cattle Marketing Channels .......................................................................... 7 Structure and Consolidation ...................................................................................... 10

2. The Challenge ............................................................................................................... 14 Building Blocks to Success�It Starts With the Consumer Meat Case ........................ 14

Successful Meat Cases .............................................................................................. 16 3. What Can the Cattle Industry Do? ............................................................................ 18 4. Future Opportunities for the Canadian Industry ....................................................... 22 5. Conclusions ............................................................................................................... 26

Paper made possible by:

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 3

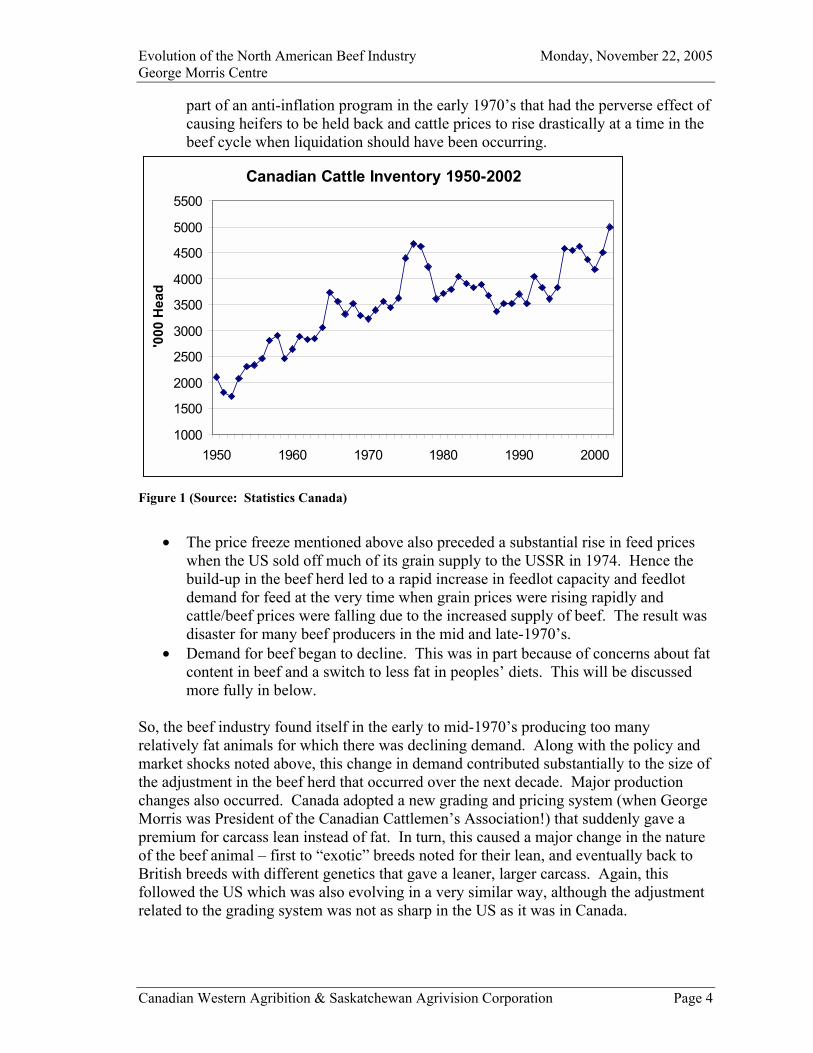

Evolution of the North American Beef Industry This paper focuses on the evolution of the Canadian beef industry. It compares and contrasts it to the US industry. The slide set that accompanies it has more detail on aspects of the comparison. But the paper addresses what has occurred in the cow-herd and production of beef since the middle of the 20th century, changes in geographic concentration, as well as concentration of production among farmers and packers. It also addresses changes in marketing channels and demand for beef. From the recent history of the industry and an assessment of its future opportunities, a number of lessons are addressed regarding the challenges facing it in the future. Finally, we identify some suggestions for ways it can take advantage of the opportunities. 1. Evolution of the North American Beef Industry Statistical Overview of the Canadian Beef Industry This section of the paper provides a statistical overview of the changes and patterns in the Canadian cattle industry. Its purpose is to provide perspective on the industry�s current size and future potential. The Cow Herd - History and Trends Canadian cattle inventory has been in an upward trend since 1987. But in fact, as illustrated by Figure 1, this is the third of three growth stages in the herd since 1950. During the first stage, the three beef cycles from 1950 until the mid-1970�s, the beef cow herd tripled. The last of those cycles took beef cow inventories to extreme cyclical highs that were not reached again until 2004 in Canada. The first stage in Canada roughly paralleled the US (Figure 2), which saw rapid growth until 1975. This was a period of rapid industrial development in North America, with rising personal incomes, a substantial share of which was spent on beef by consumers who saw beef as the preferred source of protein. It was also characterized by relatively low grain prices that were also falling in real terms (ie after adjusting for inflation). The combination of strong demand and falling feed prices led the beef industry through its rapid growth during those three decades. In some ways, it also sewed the seeds of the second stage of growth, which began in the mid-1970�s and lasted in Canada for about a decade, or one beef cycle. In this phase, the beef herd declined by about 40% in both countries. Several factors contributed to this adjustment:

• The sheer size to which the Canadian and US herds were �overbuilt� in the mid-1970�s. This was exacerbated by an ill-advised �price freeze� on retail beef as

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 4

part of an anti-inflation program in the early 1970�s that had the perverse effect of causing heifers to be held back and cattle prices to rise drastically at a time in the beef cycle when liquidation should have been occurring.

Canadian Cattle Inventory 1950-2002

1000

1500

2000

2500

3000

3500

4000

4500

5000

5500

1950 1960 1970 1980 1990 2000

'000

Hea

d

Figure 1 (Source: Statistics Canada)

• The price freeze mentioned above also preceded a substantial rise in feed prices

when the US sold off much of its grain supply to the USSR in 1974. Hence the build-up in the beef herd led to a rapid increase in feedlot capacity and feedlot demand for feed at the very time when grain prices were rising rapidly and cattle/beef prices were falling due to the increased supply of beef. The result was disaster for many beef producers in the mid and late-1970�s.

• Demand for beef began to decline. This was in part because of concerns about fat content in beef and a switch to less fat in peoples� diets. This will be discussed more fully in below.

So, the beef industry found itself in the early to mid-1970�s producing too many relatively fat animals for which there was declining demand. Along with the policy and market shocks noted above, this change in demand contributed substantially to the size of the adjustment in the beef herd that occurred over the next decade. Major production changes also occurred. Canada adopted a new grading and pricing system (when George Morris was President of the Canadian Cattlemen�s Association!) that suddenly gave a premium for carcass lean instead of fat. In turn, this caused a major change in the nature of the beef animal � first to �exotic� breeds noted for their lean, and eventually back to British breeds with different genetics that gave a leaner, larger carcass. Again, this followed the US which was also evolving in a very similar way, although the adjustment related to the grading system was not as sharp in the US as it was in Canada.

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 5

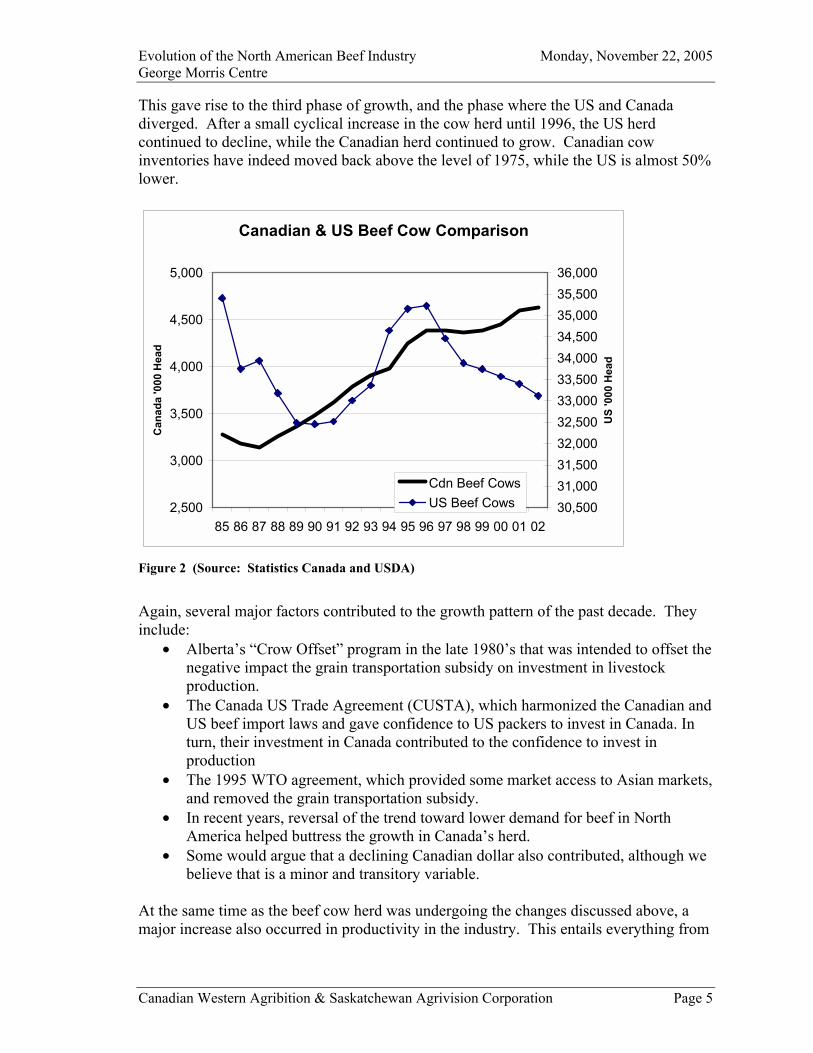

This gave rise to the third phase of growth, and the phase where the US and Canada diverged. After a small cyclical increase in the cow herd until 1996, the US herd continued to decline, while the Canadian herd continued to grow. Canadian cow inventories have indeed moved back above the level of 1975, while the US is almost 50% lower.

Canadian & US Beef Cow Comparison

2,500

3,000

3,500

4,000

4,500

5,000

85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02

Can

ada

'000

Hea

d

30,50031,00031,50032,00032,50033,00033,50034,00034,50035,00035,50036,000

US

'000

Hea

d

Cdn Beef CowsUS Beef Cows

Figure 2 (Source: Statistics Canada and USDA)

Again, several major factors contributed to the growth pattern of the past decade. They include:

• Alberta�s �Crow Offset� program in the late 1980�s that was intended to offset the negative impact the grain transportation subsidy on investment in livestock production.

• The Canada US Trade Agreement (CUSTA), which harmonized the Canadian and US beef import laws and gave confidence to US packers to invest in Canada. In turn, their investment in Canada contributed to the confidence to invest in production

• The 1995 WTO agreement, which provided some market access to Asian markets, and removed the grain transportation subsidy.

• In recent years, reversal of the trend toward lower demand for beef in North America helped buttress the growth in Canada�s herd.

• Some would argue that a declining Canadian dollar also contributed, although we believe that is a minor and transitory variable.

At the same time as the beef cow herd was undergoing the changes discussed above, a major increase also occurred in productivity in the industry. This entails everything from

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 6

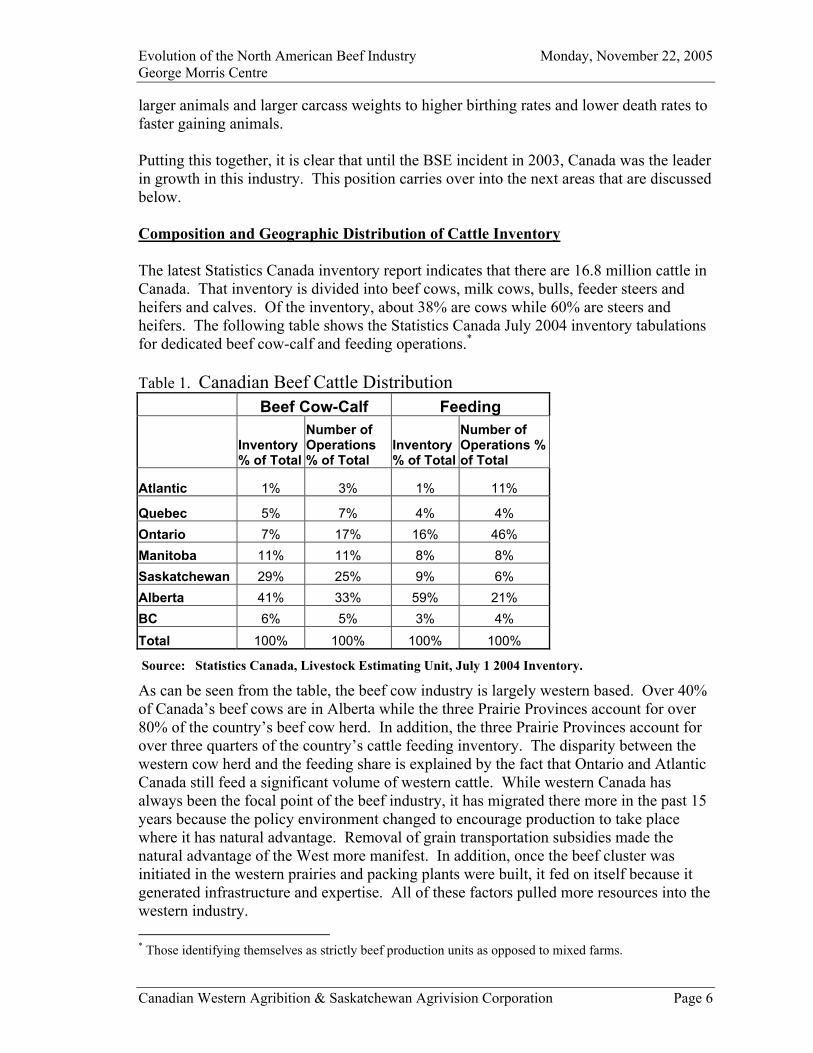

larger animals and larger carcass weights to higher birthing rates and lower death rates to faster gaining animals. Putting this together, it is clear that until the BSE incident in 2003, Canada was the leader in growth in this industry. This position carries over into the next areas that are discussed below. Composition and Geographic Distribution of Cattle Inventory The latest Statistics Canada inventory report indicates that there are 16.8 million cattle in Canada. That inventory is divided into beef cows, milk cows, bulls, feeder steers and heifers and calves. Of the inventory, about 38% are cows while 60% are steers and heifers. The following table shows the Statistics Canada July 2004 inventory tabulations for dedicated beef cow-calf and feeding operations.* Table 1. Canadian Beef Cattle Distribution Beef Cow-Calf Feeding

Inventory % of Total

Number of Operations % of Total

Inventory % of Total

Number of Operations % of Total

Atlantic 1% 3% 1% 11%

Quebec 5% 7% 4% 4% Ontario 7% 17% 16% 46% Manitoba 11% 11% 8% 8% Saskatchewan 29% 25% 9% 6% Alberta 41% 33% 59% 21% BC 6% 5% 3% 4% Total 100% 100% 100% 100%

Source: Statistics Canada, Livestock Estimating Unit, July 1 2004 Inventory.

As can be seen from the table, the beef cow industry is largely western based. Over 40% of Canada�s beef cows are in Alberta while the three Prairie Provinces account for over 80% of the country�s beef cow herd. In addition, the three Prairie Provinces account for over three quarters of the country�s cattle feeding inventory. The disparity between the western cow herd and the feeding share is explained by the fact that Ontario and Atlantic Canada still feed a significant volume of western cattle. While western Canada has always been the focal point of the beef industry, it has migrated there more in the past 15 years because the policy environment changed to encourage production to take place where it has natural advantage. Removal of grain transportation subsidies made the natural advantage of the West more manifest. In addition, once the beef cluster was initiated in the western prairies and packing plants were built, it fed on itself because it generated infrastructure and expertise. All of these factors pulled more resources into the western industry. * Those identifying themselves as strictly beef production units as opposed to mixed farms.

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 7

It is of interest to note that the west�s share of the cow herd has not changed over the longer term. In 1970 the west�s share (including BC) was approximately the same as it is in 2004. What has changed is the share of feeding in the west versus Ontario. Historical data on feeding inventory is not available but there are indications of the shift based on slaughter data. During the mid-1980�s Ontario�s slaughter was approximately one and a half times greater than its current slaughter. Furthermore, based on data sets that were once collected by Agriculture Canada, that slaughter was fuelled by nearly 200,000 head per year of slaughter and feeder cattle that were shipped from west to east. That flow is significantly smaller today. So, as has been the case in the US, finishing in Canada moved closer to the concentration of feeder animals and forage, likely because of the relative cost of transporting them vs providing forage and feed. The disparity between the shares of inventory and shares of operations also reveals a lot about the sizes of operations. For example, Ontario has 16% of the feeding inventory but 46% of the feeding operations. Contrast that with Alberta at 59% and 21%. Clearly, Alberta�s feeding operations are much larger than Ontario�s. This reveals another aspect of the evolution that is similar to the US � larger operations have sprung up because of the economies of size they provide. In Canada, Statistics Canada reports that there were 6.4 million cows on hand as of July 1, 2004. It is important to note that in addition to beef cows, the total Canadian cow herd also includes 1.1 million, or 17% were dairy cows. While the beef industry is western based, the dairy herd is more eastern based. Eastern Canada is the home to nearly 80% of the country�s dairy cow herd. With regard to the packing industry, it is noted that in 2002, nearly 77% of the total Canadian cattle slaughter occurred in the west and 71% was in Alberta alone. With regard to slaughter breakdown, the west accounted for nearly 79% of steer and heifer slaughter with Alberta alone accounting for 76%. Cow slaughter was more evenly based between east and west. Quebec slaughtered about 31% of the cows in the country while Alberta handled 46%. The composition of the slaughter between east and west reflects the geographic distribution of dairy versus beef cows. Marketing and Structural Change Beef and Cattle Marketing Channels Feeder cattle marketing is largely a domestic endeavor with reltatively few exports. For example in 2002, Statistics Canada tallied 5.2 million calves in the summer inventory report. That same year, the USDA reported just 487,000 imported feeder cattle or less than 10% of the total inventory. Even that tally was inflated by the severe western drought. In normal years, feeder exports just amounted to around 100,000 head. Given the large concentration of feedlots in Alberta (see table 1) and the resulting demand for feeder cattle, the overwhelming share of western feeder cattle are marketed to feedlots in Alberta. Based on Ontario�s relatively large share of cattle on feed relative to its cow

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 8

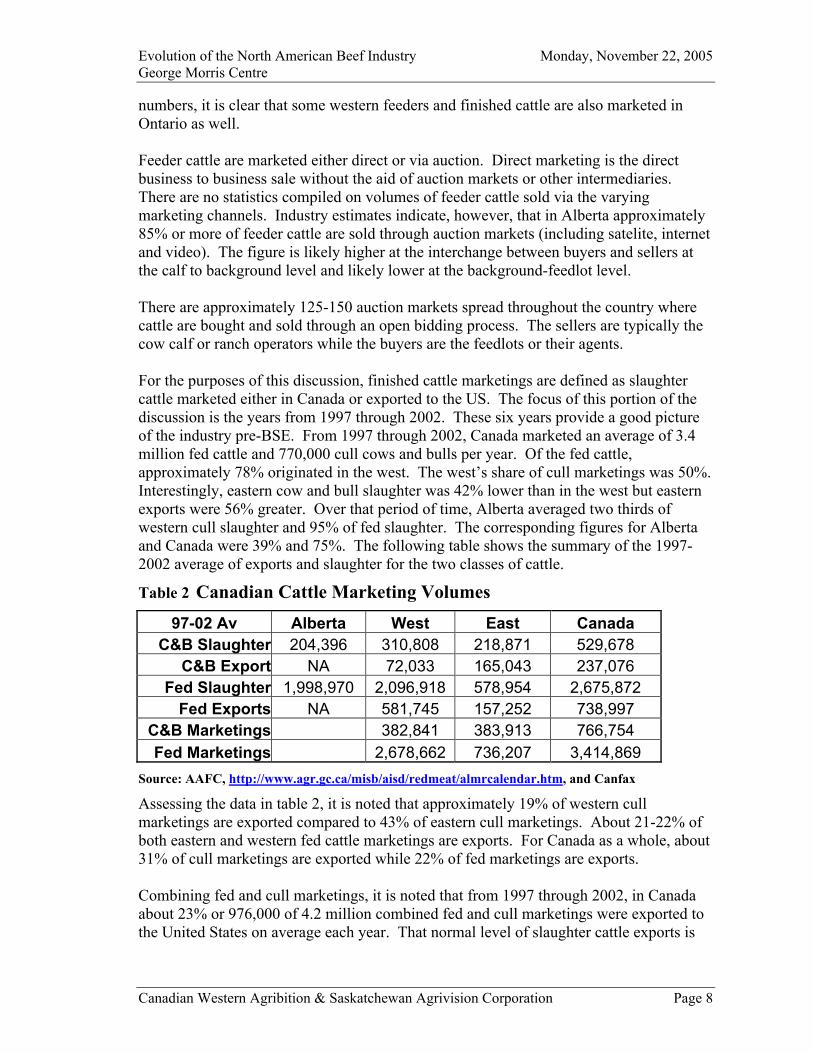

numbers, it is clear that some western feeders and finished cattle are also marketed in Ontario as well. Feeder cattle are marketed either direct or via auction. Direct marketing is the direct business to business sale without the aid of auction markets or other intermediaries. There are no statistics compiled on volumes of feeder cattle sold via the varying marketing channels. Industry estimates indicate, however, that in Alberta approximately 85% or more of feeder cattle are sold through auction markets (including satelite, internet and video). The figure is likely higher at the interchange between buyers and sellers at the calf to background level and likely lower at the background-feedlot level. There are approximately 125-150 auction markets spread throughout the country where cattle are bought and sold through an open bidding process. The sellers are typically the cow calf or ranch operators while the buyers are the feedlots or their agents. For the purposes of this discussion, finished cattle marketings are defined as slaughter cattle marketed either in Canada or exported to the US. The focus of this portion of the discussion is the years from 1997 through 2002. These six years provide a good picture of the industry pre-BSE. From 1997 through 2002, Canada marketed an average of 3.4 million fed cattle and 770,000 cull cows and bulls per year. Of the fed cattle, approximately 78% originated in the west. The west�s share of cull marketings was 50%. Interestingly, eastern cow and bull slaughter was 42% lower than in the west but eastern exports were 56% greater. Over that period of time, Alberta averaged two thirds of western cull slaughter and 95% of fed slaughter. The corresponding figures for Alberta and Canada were 39% and 75%. The following table shows the summary of the 1997-2002 average of exports and slaughter for the two classes of cattle.

Table 2 Canadian Cattle Marketing Volumes

97-02 Av Alberta West East Canada C&B Slaughter 204,396 310,808 218,871 529,678

C&B Export NA 72,033 165,043 237,076 Fed Slaughter 1,998,970 2,096,918 578,954 2,675,872

Fed Exports NA 581,745 157,252 738,997 C&B Marketings 382,841 383,913 766,754 Fed Marketings 2,678,662 736,207 3,414,869

Source: AAFC, http://www.agr.gc.ca/misb/aisd/redmeat/almrcalendar.htm, and Canfax

Assessing the data in table 2, it is noted that approximately 19% of western cull marketings are exported compared to 43% of eastern cull marketings. About 21-22% of both eastern and western fed cattle marketings are exports. For Canada as a whole, about 31% of cull marketings are exported while 22% of fed marketings are exports. Combining fed and cull marketings, it is noted that from 1997 through 2002, in Canada about 23% or 976,000 of 4.2 million combined fed and cull marketings were exported to the United States on average each year. That normal level of slaughter cattle exports is

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 9

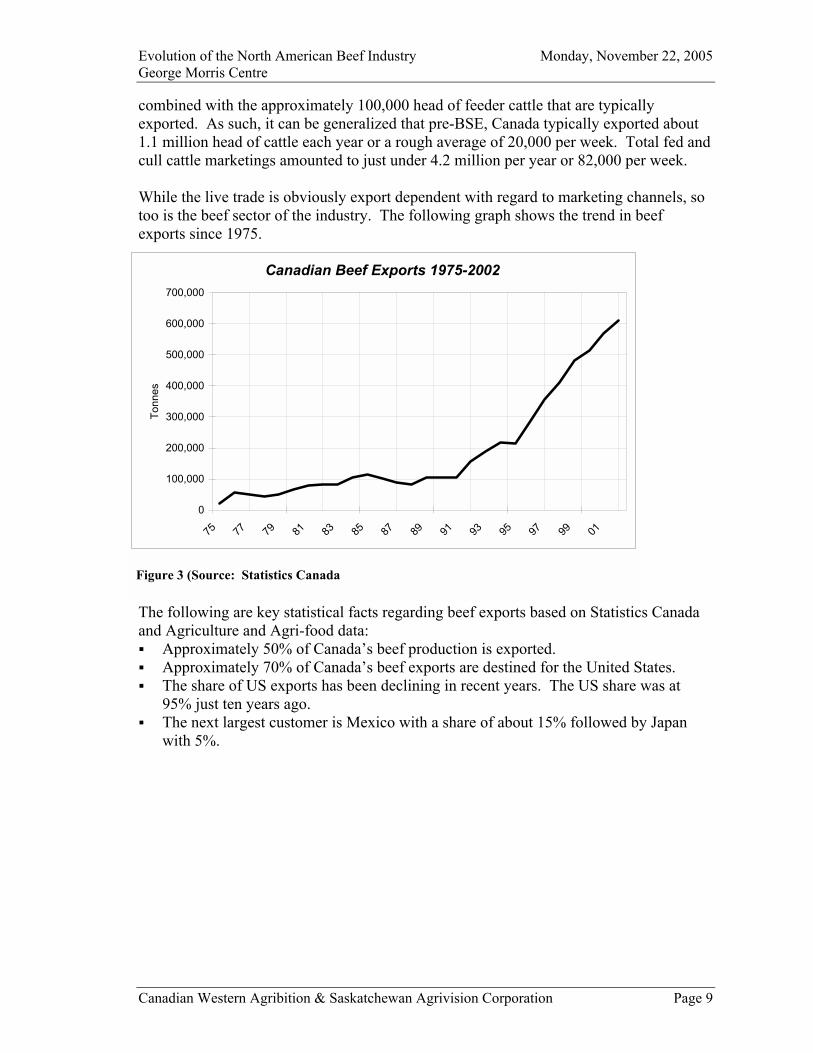

combined with the approximately 100,000 head of feeder cattle that are typically exported. As such, it can be generalized that pre-BSE, Canada typically exported about 1.1 million head of cattle each year or a rough average of 20,000 per week. Total fed and cull cattle marketings amounted to just under 4.2 million per year or 82,000 per week. While the live trade is obviously export dependent with regard to marketing channels, so too is the beef sector of the industry. The following graph shows the trend in beef exports since 1975.

The following are key statistical facts regarding beef exports based on Statistics Canada and Agriculture and Agri-food data: ! Approximately 50% of Canada�s beef production is exported. ! Approximately 70% of Canada�s beef exports are destined for the United States. ! The share of US exports has been declining in recent years. The US share was at

95% just ten years ago. ! The next largest customer is Mexico with a share of about 15% followed by Japan

with 5%.

Canadian Beef Exports 1975-2002

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

75 77 79 81 83 85 87 89 91 93 95 97 99 01

Tonn

es

Figure 3 (Source: Statistics Canada

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 10

Structure and Consolidation Statistics Canada1 data for January 2004 says that for all of Canada the cow-calf sector features over 70,000 operations of varying sizes with the average size being 120 head. In Alberta, the corresponding numbers are 24,000 operators with an average size of 146 head. In other words, this sector of the industry is very fragmented and diverse. Some operators are full time commercial producers while others are hobby farmers. As with nearly all sectors of the agriculture and food industry, the Alberta and Canadian cattle industry is and has been restructuring to fewer and larger operations. The number of operators is declining and those that remain have become larger. For example in Alberta in January 1996, Statistics Canada counted 27,500 cow calf operations. As of January 2004 that number declined by 13%. With regard to the cattle feeding sector, the vast majority of the industry is centered in Alberta. While the average number of head per operation in Canada is about 380, the Alberta average is closer to 1,500 head. That, however, does not reveal just how concentrated the feeding sector truly is within the west and Alberta. In a practical sense, essentially all of the fed cattle marketed in western Canada are sold by about 200 feedlots in Alberta and less than 10 in Saskatchewan2. The top 20 operations had a total capacity of about 754,000 head in 2003*. Assuming a conservative turnover rate of 2 times per year, this means that the top 20 are capable of marketing well over 1.5 million head per year.** Canfax lists 208 feedlots in 2003 in its compilation of lots in the province for the purpose of the Canadian on-feed report and for its evaluation of total annual capacity. The yards that are included in the Canfax accounting have capacity of 1,000 head or more. Of course there are many other operations that feed and market cattle in Alberta. But of yards over 1,000 head capacity, the top 20 represents less than 10% of the total. Using Canfax data, the total Alberta capacity is estimated to be about 1,545,600 head (Canfax Weekly, Jan 31, 2003). Based on that estimate, the top 20 of the lots (10% of the total) comprise roughly 50% of the total capacity in the province. The 20 largest yards� capacity total has increased by about 38,000 head or 5% compared to the estimated capacity of the top 20 yards two years ago (George Morris estimates). During 2003, prior to the BSE crisis, the total share of the top twenty was expected to increase again. This was due to the fact that the largest operators were close to adding more capacity. The increase in capacity is driven by economies of scale, which in turn results in lower operating costs per head.

1 Statistics Canada Livestock and Animal Products Section 2 Estimate is based on George Morris Centre and Canfax research. * Reference is made to 2003 data in order to provide a pre-BSE overview of the situation. ** Average turnover is likely between 2-3 times per year but there is no definitive source for this information.

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 11

As a final note on the issue of size of operation, and as refelcted in Table 2, it is of interest to note Canfax�s findings on this topic:3

Since the initiation of the Alberta and Saskatchewan cattle on feed report in 1999 Canfax has been able to keep accurate feedlot demographic information. The information includes feedlots that are over 1,000 head one time feeding bunk capacity that are feeding steers and heifers to finish only.

As of January 1, 2002 the total feedlot bunk capacity in Alberta and Saskatchewan was 1,651,400 million head. That�s an additional 73,200 head of bunk space added to these two provinces since January 2001. In Alberta the capacity increase was 72,000 head when compared to the total capacity of 1,578,200 last year. Of this capacity, 131 feedlots are 1,000-5,000 head one-time bunk capacity and account for 21% of the total, 47 lots are between 5,001 and 10,000 and make up 23%. There are 11 feedlots that are from 10,001-15,000 that account for 9% of the total. Ten feedlots are 15,001-20,000 accounting for 12% of capacity and 11 feedlots that are over 25,000 head and represent 35% or 541,000 head of the total available capacity in Alberta.

Saskatchewan increased their one time feeding capacity by 1% when compared to total capacity last year. Saskatchewan consists of 17 feedlots that are 1,000-5,000 head and make up 39% of the bunk capacity, 3 lots are 5,001-10,000 head capacity and account for 17% of total capacity and 3 lots over 10,001 head make up 43% of the total bunk capacity.

In 1991, Alberta�s feedlot demographic data was derived from the National Tripartite Stabilization program. Since that time feedlots in Alberta over 1,000 head capacity have gone from 229 lots to 210 lots in 2002. Over that time those lots were feeding less than a million head in 1991 and more than 2.4 million head in 2001. The number of lots over 10,000 head capacity has risen from 12 lots in 1991 that accounted for 31% of total production to 32 lots in 2002 that account for 57% of production.

The total number of feedlots that have over 1,000 head finishing capacity has been fluctuating over the past few years. In most cases this shift has been a result of higher input costs for finishing cattle, mainly the higher cost of feed and replacement cattle over the past two years. Some operations have chosen to use their pen space differently and focus on other aspects of the cattle industry. These operations would have the pen space available if they ever wanted to resume finishing cattle again. (End of Canfax excerpt)

The basic message of the Canfax excerpt is to illustrate the concentration that is occuring in the Alberta cattle feeding industry. That is lots are getting larger and the major area of growth in the province were those lots that are of the largest size category. 3 January 18, 2002 Canfax weekly report

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 12

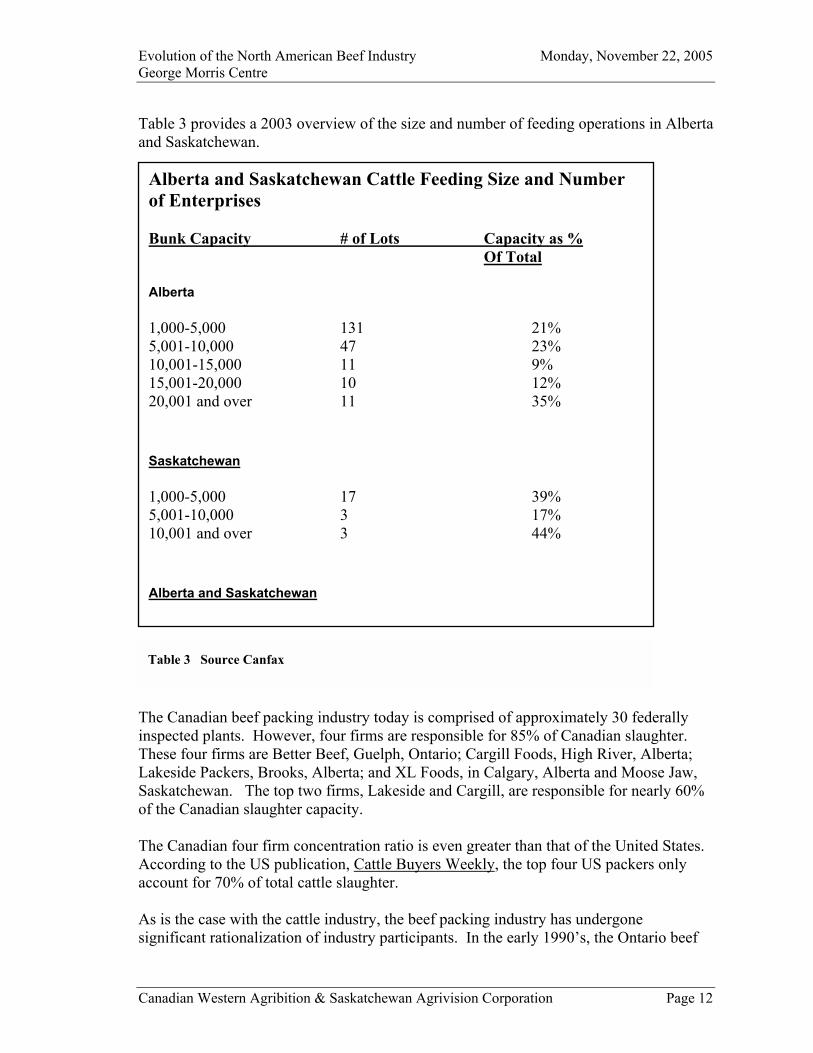

Table 3 provides a 2003 overview of the size and number of feeding operations in Alberta and Saskatchewan.

The Canadian beef packing industry today is comprised of approximately 30 federally inspected plants. However, four firms are responsible for 85% of Canadian slaughter. These four firms are Better Beef, Guelph, Ontario; Cargill Foods, High River, Alberta; Lakeside Packers, Brooks, Alberta; and XL Foods, in Calgary, Alberta and Moose Jaw, Saskatchewan. The top two firms, Lakeside and Cargill, are responsible for nearly 60% of the Canadian slaughter capacity. The Canadian four firm concentration ratio is even greater than that of the United States. According to the US publication, Cattle Buyers Weekly, the top four US packers only account for 70% of total cattle slaughter. As is the case with the cattle industry, the beef packing industry has undergone significant rationalization of industry participants. In the early 1990�s, the Ontario beef

Alberta and Saskatchewan Cattle Feeding Size and Number of Enterprises Bunk Capacity # of Lots Capacity as %

Of Total

Alberta

1,000-5,000 131 21% 5,001-10,000 47 23% 10,001-15,000 11 9% 15,001-20,000 10 12% 20,001 and over 11 35%

Saskatchewan

1,000-5,000 17 39% 5,001-10,000 3 17% 10,001 and over 3 44%

Alberta and Saskatchewan

Table 3 Source Canfax

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 13

packing industry alone had 19 federally inspected plants. Today the Ontario packing industry is comprised of Better Beef and two other smaller plants. The Alberta industry has also lost several packers over the last 10 to 15 years including major industry participants such as Canada Packers, Burns, Dvorkin, and Centennial. The genesis of the industry�s rationalization is two factors: economies of size and declining demand. Economies of size pertain to the reduction in costs associated with larger volumes, more particularly the ability to allocate fixed overhead to larger cattle numbers. Numerous academic studies and research projects in the US have demonstrated the significance of large plants to cost reduction.4 The first plant to demonstrate the impact of economies of size in Canada was the Cargill Foods plant in High River. That plant was built in 1989 and its impact was to almost immediately drive out several other plants in Ontario and Alberta that could not compete on costs. Declining demand also played a role in the industry consolidation, particularly during the 1980�s and early 1990�s. That was simply because as North Americans demanded less and less beef, there was a need for fewer and fewer packers. Furthermore, those that survived needed to be low cost producers. Another point with regard to industry structure and concentration in the Canadian beef packing industry is the issue of ownership. Prior to 1989 with the arrival of Cargill Foods in Alberta, the Canadian beef packing industry was 100% Canadian owned, whereas U.S. firms today control about 60% of the Canadian industry�s capacity - Cargill Inc. of Minnesota owns Cargill and in the mid-1990�s Lakeside Packers was purchase by IBP, which is now owned by Tyson Foods. A final point related to rationalization and concentration is the geographic location of the industry. The nature of the beef packing industry is that it is cheaper to transport boxed beef than it is to transport live cattle. As a result of that fundamental logistical factor, the Canadian beef packing industry is overwhelmingly located in Alberta and Saskatchewan, close to the feedlot operations. The situation is exactly the same in the United States. Beef packers relocated from areas with concentrations of people (like Chicago) to the primary feeding regions of the Texas Panhandle, western Kansas and Nebraska.

4 USDA Packers and Stockyards Administration 1996, Ward, C.E. �Meatpacking Plant Capacity and Utilization: Implications for Competition and Pricing.� Agribusiness.

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 14

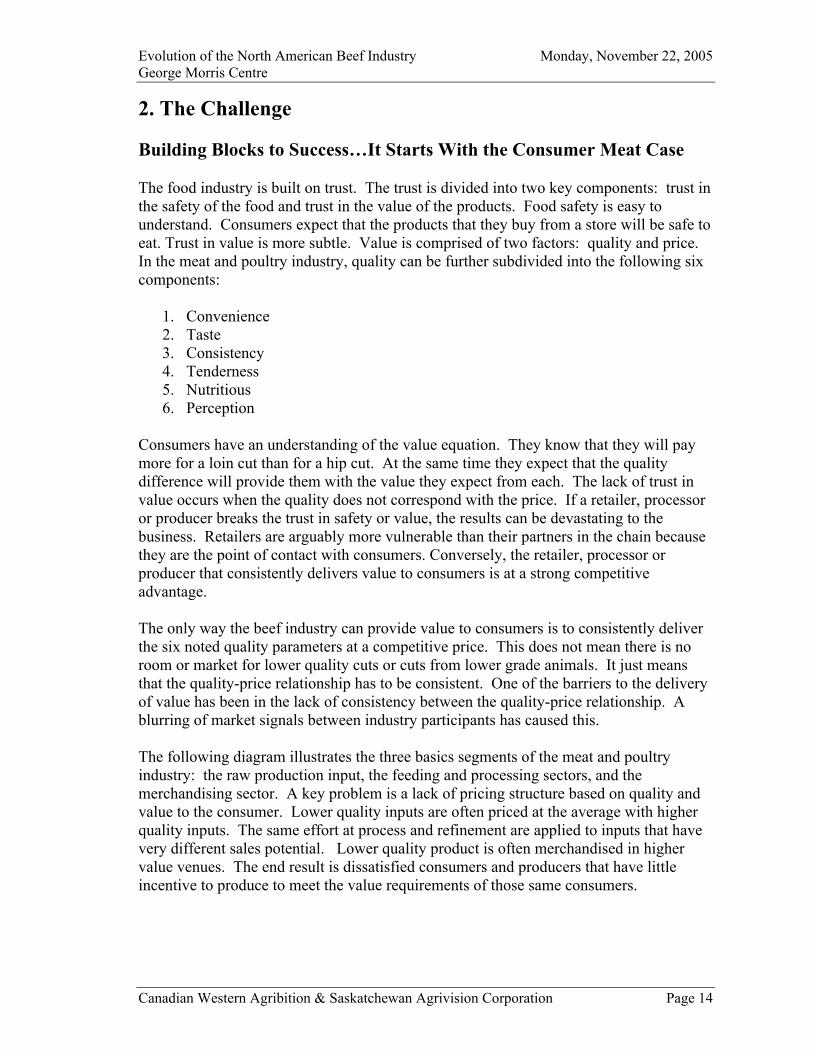

2. The Challenge Building Blocks to Success�It Starts With the Consumer Meat Case The food industry is built on trust. The trust is divided into two key components: trust in the safety of the food and trust in the value of the products. Food safety is easy to understand. Consumers expect that the products that they buy from a store will be safe to eat. Trust in value is more subtle. Value is comprised of two factors: quality and price. In the meat and poultry industry, quality can be further subdivided into the following six components:

1. Convenience 2. Taste 3. Consistency 4. Tenderness 5. Nutritious 6. Perception

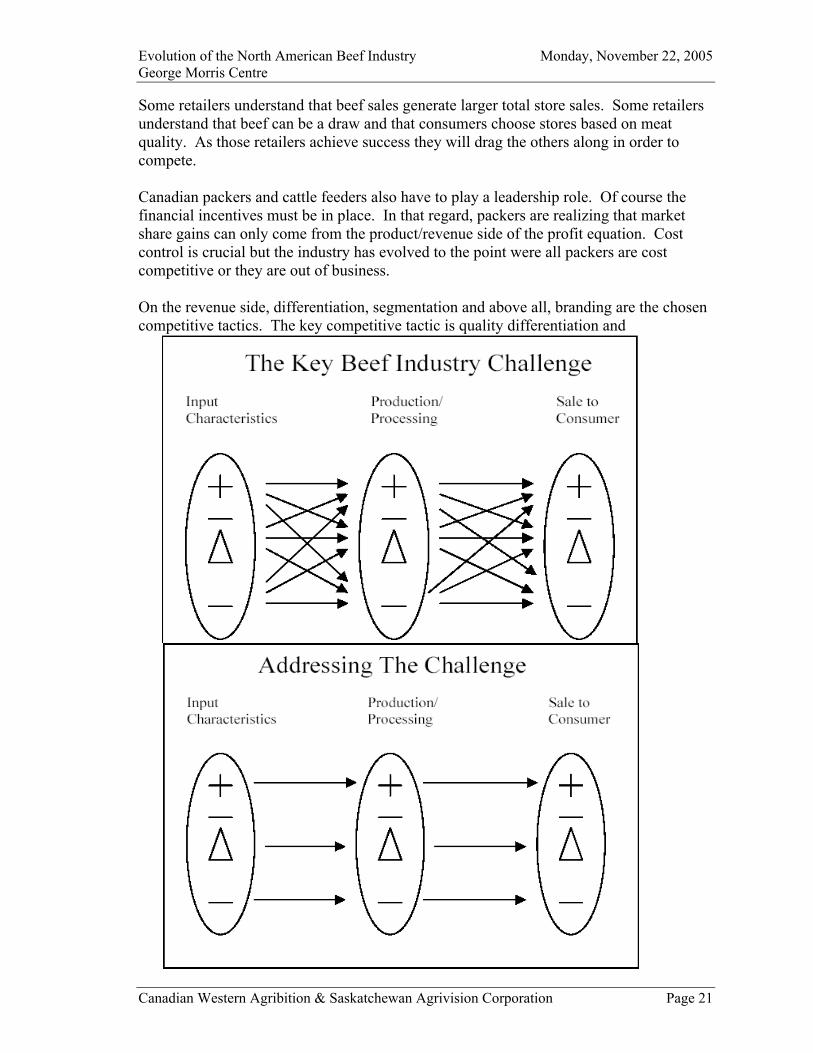

Consumers have an understanding of the value equation. They know that they will pay more for a loin cut than for a hip cut. At the same time they expect that the quality difference will provide them with the value they expect from each. The lack of trust in value occurs when the quality does not correspond with the price. If a retailer, processor or producer breaks the trust in safety or value, the results can be devastating to the business. Retailers are arguably more vulnerable than their partners in the chain because they are the point of contact with consumers. Conversely, the retailer, processor or producer that consistently delivers value to consumers is at a strong competitive advantage. The only way the beef industry can provide value to consumers is to consistently deliver the six noted quality parameters at a competitive price. This does not mean there is no room or market for lower quality cuts or cuts from lower grade animals. It just means that the quality-price relationship has to be consistent. One of the barriers to the delivery of value has been in the lack of consistency between the quality-price relationship. A blurring of market signals between industry participants has caused this. The following diagram illustrates the three basics segments of the meat and poultry industry: the raw production input, the feeding and processing sectors, and the merchandising sector. A key problem is a lack of pricing structure based on quality and value to the consumer. Lower quality inputs are often priced at the average with higher quality inputs. The same effort at process and refinement are applied to inputs that have very different sales potential. Lower quality product is often merchandised in higher value venues. The end result is dissatisfied consumers and producers that have little incentive to produce to meet the value requirements of those same consumers.

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 15

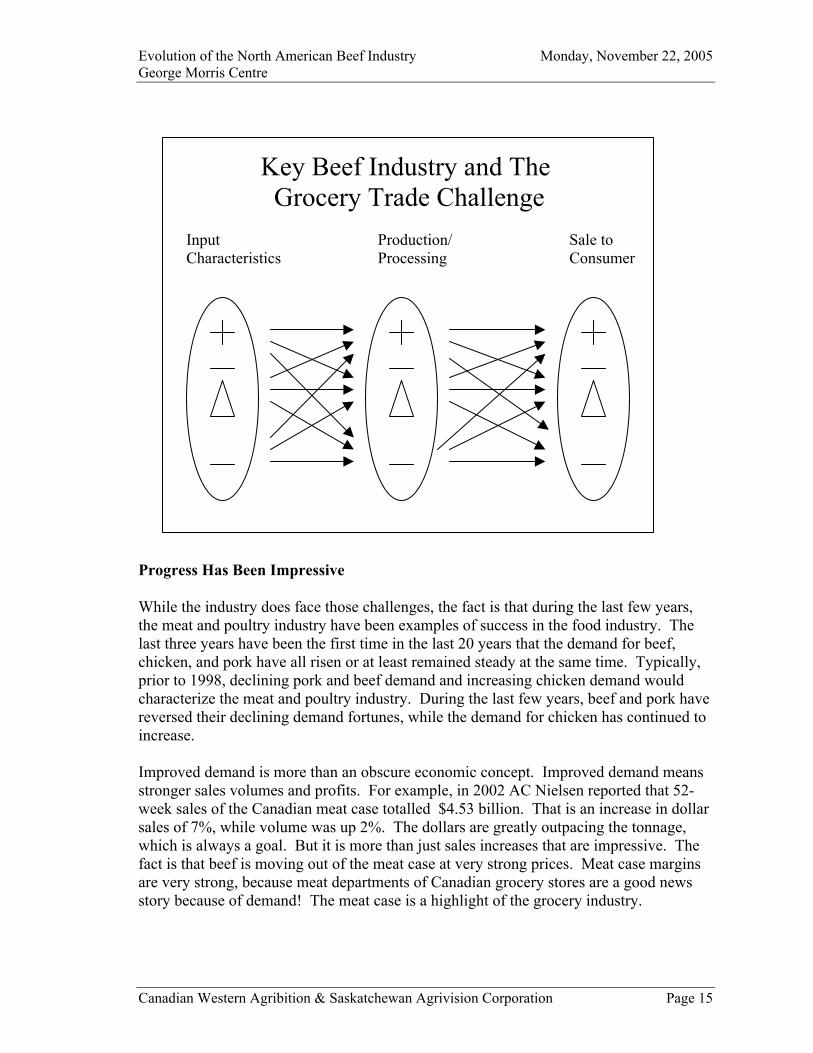

Key Beef Industry and The Grocery Trade Challenge

Input Production/ Sale to Characteristics Processing Consumer

Progress Has Been Impressive While the industry does face those challenges, the fact is that during the last few years, the meat and poultry industry have been examples of success in the food industry. The last three years have been the first time in the last 20 years that the demand for beef, chicken, and pork have all risen or at least remained steady at the same time. Typically, prior to 1998, declining pork and beef demand and increasing chicken demand would characterize the meat and poultry industry. During the last few years, beef and pork have reversed their declining demand fortunes, while the demand for chicken has continued to increase. Improved demand is more than an obscure economic concept. Improved demand means stronger sales volumes and profits. For example, in 2002 AC Nielsen reported that 52-week sales of the Canadian meat case totalled $4.53 billion. That is an increase in dollar sales of 7%, while volume was up 2%. The dollars are greatly outpacing the tonnage, which is always a goal. But it is more than just sales increases that are impressive. The fact is that beef is moving out of the meat case at very strong prices. Meat case margins are very strong, because meat departments of Canadian grocery stores are a good news story because of demand! The meat case is a highlight of the grocery industry.

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 16

In addition, leading grocery chains in Canada and the United States have determined that not only is the meat case a winner, but that the meat case can make the entire store and chain a winner. Some leading retailers have researched the fact that consumers shop their stores because of the meat case. They have determined that if there is a strong meat purchase in the consumer�s shopping cart, chances are that there is going to be multiples of other purchases as well. In other words if there is beef in the purchase, then total purchase is going to be much greater than if there is no beef in the purchase. Successful Meat Cases The point to be made here is that effort in the meat case is effort well spent. It is effort that pays dividends to grocers and by default to the entire industry. So where is the meat case of the future going and what will it look like? To answer that it is necessary to look at the characteristics of current successful meat cases. That will provide an indication of where the entire industry will eventually be going. First of all, the self-serve part of the meat department will be characterized by the following: ! Branded products will proliferate or dominate the case. Brands will be national

and private label. ! All product will be case ready ! There will be a proliferation of �fresh� product that is prepared to some extent

(cooked, seasoned, marinated�) ! The meat case will be more segmented based on quality and end use

Just as importantly, more and more retailers are seeing or will see the pay-off in offering full service sections for the meat department. These full service sections will offer consumers extra effort in the form of in-store preparation and processing (in-store vacuum tumblers). These full service sections will also offer expert advice, as well as sales effort. The bottom line is that retail meat sales and merchandising effort will burgeon. Successful meat cases will be full of value-added offerings focused on convenience and ready to eat. Retailers will �brand the meat case,� with their own merchandising and strategic vision. In short, retailers will become expert meat merchandisers. At the same time, retailers are downloading more and more responsibilities and functions back to processors and packers. Inventory and case management as well as packaging and merchandising are increasingly being pushed back to packers and processors. Concerns regarding the responsibility for product safety and labor requirements have fostered and forced this change. In addition, industry leader Wal-Mart is also aggressively pushing these changes. The fact is that when Wal-Mart starts something, the other competitors follow. The meat case is being treated as a category, much like a packaged good. The category and the processor must prove their value and carry their weight or risk being de-listed.

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 17

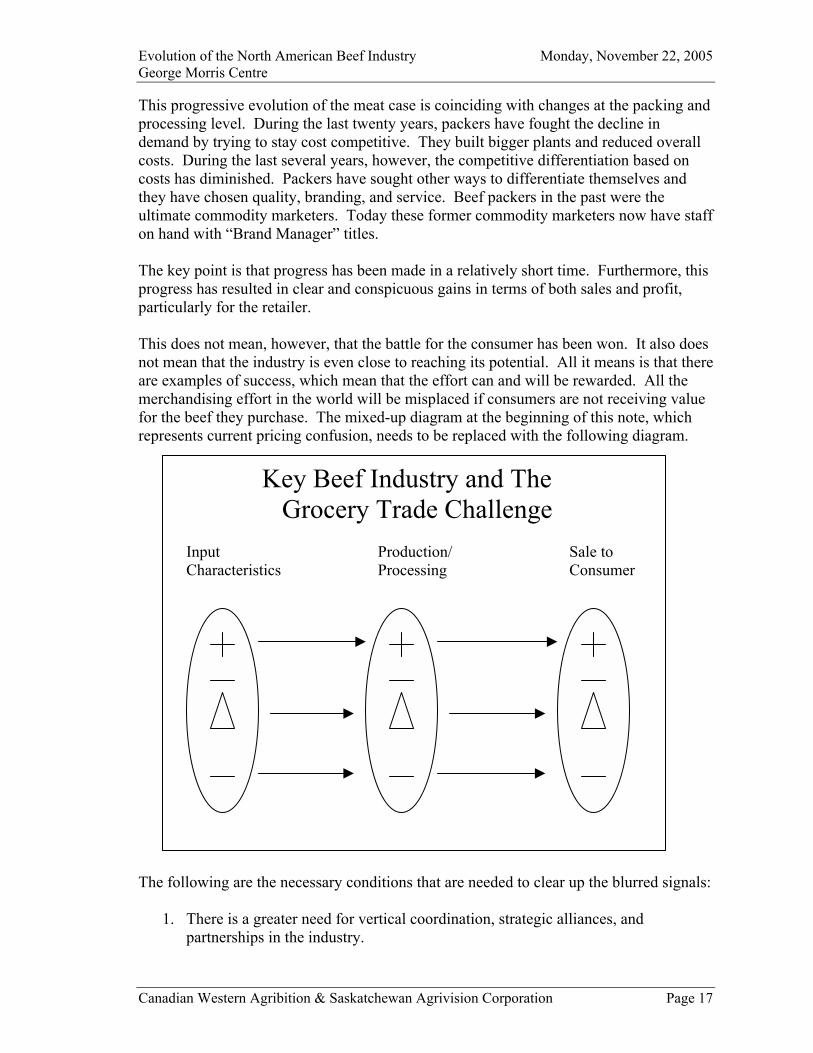

This progressive evolution of the meat case is coinciding with changes at the packing and processing level. During the last twenty years, packers have fought the decline in demand by trying to stay cost competitive. They built bigger plants and reduced overall costs. During the last several years, however, the competitive differentiation based on costs has diminished. Packers have sought other ways to differentiate themselves and they have chosen quality, branding, and service. Beef packers in the past were the ultimate commodity marketers. Today these former commodity marketers now have staff on hand with �Brand Manager� titles. The key point is that progress has been made in a relatively short time. Furthermore, this progress has resulted in clear and conspicuous gains in terms of both sales and profit, particularly for the retailer. This does not mean, however, that the battle for the consumer has been won. It also does not mean that the industry is even close to reaching its potential. All it means is that there are examples of success, which mean that the effort can and will be rewarded. All the merchandising effort in the world will be misplaced if consumers are not receiving value for the beef they purchase. The mixed-up diagram at the beginning of this note, which represents current pricing confusion, needs to be replaced with the following diagram.

Key Beef Industry and The Grocery Trade Challenge

Input Production/ Sale to Characteristics Processing Consumer

The following are the necessary conditions that are needed to clear up the blurred signals:

1. There is a greater need for vertical coordination, strategic alliances, and partnerships in the industry.

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 18

2. There is also a need for technological advances in screening beef for quality attributes.

3. Technological advances are also needed for traceback for the purposes of safety and pricing.

4. There is also a need for an attitudinal change in the industry to move towards a consumer value focus.

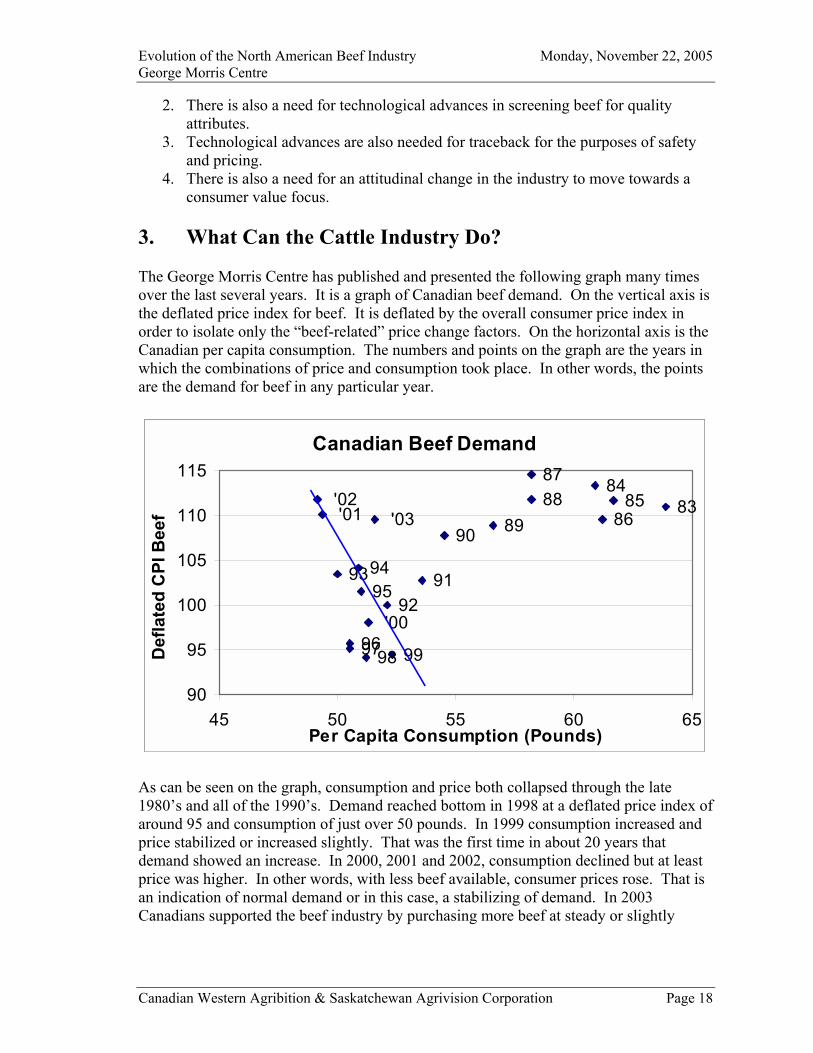

3. What Can the Cattle Industry Do? The George Morris Centre has published and presented the following graph many times over the last several years. It is a graph of Canadian beef demand. On the vertical axis is the deflated price index for beef. It is deflated by the overall consumer price index in order to isolate only the �beef-related� price change factors. On the horizontal axis is the Canadian per capita consumption. The numbers and points on the graph are the years in which the combinations of price and consumption took place. In other words, the points are the demand for beef in any particular year.

As can be seen on the graph, consumption and price both collapsed through the late 1980�s and all of the 1990�s. Demand reached bottom in 1998 at a deflated price index of around 95 and consumption of just over 50 pounds. In 1999 consumption increased and price stabilized or increased slightly. That was the first time in about 20 years that demand showed an increase. In 2000, 2001 and 2002, consumption declined but at least price was higher. In other words, with less beef available, consumer prices rose. That is an indication of normal demand or in this case, a stabilizing of demand. In 2003 Canadians supported the beef industry by purchasing more beef at steady or slightly

Canadian Beef Demand

'03 '02 '01

'00

99989796

959493

9291

90 898887

8685

8483

90

95

100

105

110

115

45 50 55 60 65Per Capita Consumption (Pounds)

Def

late

d C

PI B

eef

Canadian Beef Demand

'03 '02 '01

'00

99989796

959493

9291

90 898887

8685

8483

90

95

100

105

110

115

45 50 55 60 65Per Capita Consumption (Pounds)

Def

late

d C

PI B

eef

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 19

lower price levels. That showed that demand actually increased in a year in which BSE was all over the headlines. There has been a great deal of relief and gratification expressed at the improvement in demand in recent years. This sentiment is justified in light of the fact that the dismal performance of the past appears to have been stopped. At the same time, however, this does not mean that beef demand is strong. By our estimates, beef demand in the last couple of years has only been as good (or as bad) as it was in the mid-1990�s. During the mid-1990�s nobody was happy with beef demand. The quantity consumed of a product typically increases or decreases in response to increases or decreases in price. That is typical demand. An improvement in demand occurs when more is consumed at steady or higher prices. Declining demand occurs when less is consumed at steady or declining prices (see the graph from 1988 to 1998). An increase or decrease in demand is a change in demand. Based on economic research (Kansas State for example), we know that the drivers of beef demand are the following: ! Changes in income (GDP) ! Demographics ! Product attributes/quality ! Prices of substitutes ! Health ! Food Safety The cattle industry has no control over the prices of substitutes such as pork and chicken. The cattle industry also can�t control incomes. The industry is taking steps to make beef even safer through a variety of intensive and exhaustive system-wide measures. In addition, the Beef Information Council is taking steps to research and communicate the health benefits of beef. BIC is also helping to address the demographic challenges of two income households and a lack of product knowledge. These steps include product development and labelling. The product attribute/quality factor, however, remains an ongoing challenge for the industry. Product attributes/quality is associated with issues such as: 1. carcass size 2. tenderness 3. taste 4. consistency 5. meat yields The quality of the beef itself is an area that ultimately determines whether consumers buy the product or an alternative. William T. Hudson and Wayne D. Purcell have reasoned in a 2001 research paper5 that, �In the final analysis, the product that is produced, processed, 5 �Risk Sharing and Compensation Guides for Managers and Members of Vertical Beef Alliances,� William T. Hudson and Wayne D. Purcell, August 2001

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 20

and prepared for consumption needs to fit what consumers want. It is widely known from surveys and focus work that the consumers want a consistent, high-quality eating experience in beef, and they want convenience in preparation. That desire for and willingness to pay for convenience is arguably the primary reason that we have seen a resurgence of steakhouses and steak chains. Consumers have had money in their pockets in the 1990s and they have been willing to pay for the experience and the event of eating out.� Hudson and Purcell also warn, however, that this willingness to pay "has not meant, necessarily, that the beef entrées served at the steakhouses were meeting the needs and desires of consumers. Meat scientists who have conducted three quality audits across the past 10-12 years have concluded that up to 20-25% of the Choice grade steaks and roasts were too tough to chew.� Unfortunately, with regard to product quality, the industry continues to function in an environment that does not encourage a focus on quality. The lets remind ourselves of the linkages diagram which we showed above and which is used again below. The diagram shows the problem and the potential solution. The first input to the ultimate beef sale is the calf. The input can have characteristics that will result in a high or a low quality beef product. The production and processing end of the business are the feeding and packing functions. These functions can also play a quality role in the transformation process. A calf that does not have the basic traits that deliver a high quality beef product cannot be created in the feedlot but it can be improved. Certainly a feedlot or packing plant can take a high quality calf and reduce its eating or consumption quality. The problem as illustrated or perhaps exaggerated by the diagram is the confused price signals in the industry. In other words it is the old argument: as long as the industry buys cattle on averages, quality characteristics are not going to be adequately rewarded or penalized. As long as the industry continues to price on averages, quality will not improve as fast as it needs to improve. Industry leaders, innovators and the Canadian Cattlemen�s Association are aware of these problems. The innovators are taking risks and, at times, enduring the scrutiny and scepticism of their industry partners. The CCA is taking steps to address the challenges through targeted programs. Nevertheless, ultimately the challenge can only be addressed through pricing signals and incentives. A roadblock to addressing this is that beef industry segments have not shown much interest in addressing the problem. Cow-calf operators have consistently demonstrated that they have little or no concern about the product after the sale ring. With some notable exceptions, many major retailers are only interested in buying product cheap. As long as those two bookends of the industry operate in that manner, the pace will be very slow in improving the connection between price and quality. Ultimately the leadership on this issue will have to come from retailers. Without retail there will be no success in branding, segmentation or value-added merchandising of beef. Despite the continued commodity orientation of most retailers, there are signs of movement. Some retailers have understood the importance of a strong beef program.

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 21

Some retailers understand that beef sales generate larger total store sales. Some retailers understand that beef can be a draw and that consumers choose stores based on meat quality. As those retailers achieve success they will drag the others along in order to compete. Canadian packers and cattle feeders also have to play a leadership role. Of course the financial incentives must be in place. In that regard, packers are realizing that market share gains can only come from the product/revenue side of the profit equation. Cost control is crucial but the industry has evolved to the point were all packers are cost competitive or they are out of business. On the revenue side, differentiation, segmentation and above all, branding are the chosen competitive tactics. The key competitive tactic is quality differentiation and

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 22

segmentation programs. This means that packers have to have their own brands, private label or other quality programs. This obviously means paying for value through more rigorous systems of premiums and discounts. Whether it is called value-based marketing or another name, ultimately it means that successful or meaningful programs must be based on some sort of multi-dimensional pricing grid. While packers might be able to segregate and sort live-bought cattle for these programs, there is very little in it for cattle feeders. That is, for cattle feeders to actively participate and reap the rewards of quality-based marketing, there is no role for selling on averages or live selling. Canfax notes that in 2002, 19.5% of cattle in Alberta were purchased on a grid or formula basis. That compares to 11% in 1999 and 16% in 2001. That is a strong movement towards grid pricing, especially when the dismal-drought induced economics of cattle feeding are considered. In other words, despite the over-riding challenges of the past year, cattle feeders were still willing to work on value-based selling. Of course there remains a great deal of scepticism among cattle feeders regarding formula pricing. There is the view that the bar keeps getting higher. The concern is that if higher standards become the norm, there is less room for premiums, just discounts. In other words, what was once a premium is now an average. 4. Future Opportunities for the Canadian Industry Future opportunities flow from the foregoing and they can be categorized into at least three: market opportunities; regulatory opportunities: and supply chain opportunities. Let�s turn first to the market opportunities. Market Opportunities The foregoing discussion about the meat case of the future is the starting point. There is no need to repeat it beyond emphasizing that the trend in North America will be toward branded, case ready products that are �fresh processed� and the brands will differentiated based on quality and end use. In other words we are describing a meat industry that sees markets as being segmented and responds to the each market segment with products that have the characteristics desired by the segment. The opportunities lie in creating and being paid for additional value through branding differentiated products. This is something the automobile, textile and fashion industries learned many years ago. The market opportunities will, however, be much greater than is implied by the discussion above because it does not address the export component. At the recent International Meat Conference in Winnipeg, Nancy Morgan of the FAO presented a

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 23

paper that traced world trends in consumption of meat. Two observations characterize her message:

• World meat consumption approximately doubled between roughly 1990 and 2000

• In 1990, 51% of meat consumption was in the industrialized countries. By 2000 the industrialized countries� share of consumption was down to 41%.

We would add two more observations:

• Human population growth rates in most countries are nearing replacement levels, and world population will begin to level off in the next 25 years.

• Real income growth in a number of countries is much higher than in North America.

These four points together suggest a world where most of the growth opportunities for food will be in parts that we have regarded as �developing� and that much of the growth there will be for meat. Because of the income effect, segmented and differentiated products will likely be as or more important than the bulk type because middle and upper income classes in those countries will also desire consistent products with specific characteristics. Regulatory �Opportunities� Now let�s turn to the regulatory opportunities. The word is in brackets because regulation is not an opportunity per se, but rather appropriate regulations are required to obtain market access. In other words, even if a substantial market opportunity exists, the inability to meet regulatory requirements means it�s not available. No one in the world is in a better position to appreciate the consequences of a loss of market access than the Canadian beef industry because of the BSE incident, especially because of Canada�s reliance on the US as a trade destination. And its economic loss results from a (to-date) single occurrence of a non-contagious disease. While some in the US have clearly benefited from Canada�s loss, others have not, especially in terms of capacity utilization and lost export opportunities, because of the US reliance on Canada as a trading partner. If, we forecast above, the industry continues to evolve toward even more reliance on offshore trade, the once-growing integration of the Canadian and US industries will be ever more important. Therefore, one must be concerned that we could face disease outbreaks that are serious threats to human health, and vectors that do not respect international borders may cause them. If this happens, each country�s industry could be threatened by events in the other. At a less dramatic, but still important level, there are irksome differences in regulatory policies in the two countries regarding things like registration of animal health products, quality assessment, etc, many of the differences in which evolved in part as protection from the products of the other.

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 24

In a world where trade is dominant and lost access to offshore markets can be affected by a problem in the neighbouring country, then it is to the advantage of both to work together to make both partners as strong as possible so that market access is maximized. So our suggestion is that Canadian and US beef producers would be well advised to work together to seize the opportunity to establish appropriate regulatory protocols and, to the extent possible to ensure that relatively common and effective rules be put in place that protect human health in both countries and simultaneously maximize our access to offshore markets. In the long term, the industries in both countries will be much stronger by increasing their degree of integration. This must be done in ways that minimize the possibility of people being seriously injured on either side of the border by short-term trade protection measures on the other. Supply Chain Opportunities We focused at length in the previous section on what�s needed to continue to improve the image and demand for beef in the meat case. In this industry, as in all industries, when one starts talks to farmers about developing branded value added products they show little interest because they are convinced that they can�t participate. They feel they can�t participate because the market mechanism they deal with gives them no reward for producing specific characteristics. Hence they tend toward simply producing a commodity at as low a cost as they can. Over the past few years, traceability has become a concept of frequent discussion. We are in better position now in Canada to trace back where a problem got started. It�s now regarded as a strength of the Canadian beef industry. We believe that traceability will soon be the minimum that will need to be done if one is to develop branded meat products. By itself, traceability has been used mainly for identifying problems. There is precious little evidence that anyone is willing to pay much for just that, so it will likely become a cost of doing business � it will add the cost of the trace-back system, but add little value for people in the supply chain. We need to start thinking about the next generation of traceability that will add value by using it to ensure that the characteristics required to differentiate products are there. And we need to do it in the context of a very different concept of a supply chains and approaches to pricing. Randy Westgren of the University of Illinois recently and eloquently distinguished between the ideal supply chain and the way things are. In essence, Westgren argues that supply chains should be mechanisms that provide information on consumer wants to the producing segments, that get products to consumers with the characteristics that fulfill those wants, and send money to the various participants in proportion to the value they create in the final product. This means that there is vertical coordination of the supply chain in ways that provide continuous flows of information from the consumer to all parts of the chain. He also argues that North American supply chains suffer a disconnect � they are not chains, but rather series of unrelated transactions.

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 25

Hence the earlier reference to retailers and cow-calf producers as bookends. The retailer buys from the packer on averages. The packer buys from feedlots on averages, the feedlot buys from cow-calf producers on averages. And we wonder why the final product has problems with consistency of quality and why the cow-calf operator is indifferent to quality. The answer is obvious � the system is designed to produce the results it is producing. If the industry wants to take advantage of differentiation and branding, then it needs to change the system from the current win-lose approach to a win-win. If packers and retailers want to differentiate consistent premium lines, then they need to pay consistent premium prices for the characteristics that provide the premium. To our way of thinking, there are only three approaches to changing the system: someone at the bottom end of the supply chain owns and controls the chain; someone at the top end of the supply chain owns and controls the chain (people at the Sunterra Group say that a major reason they decided to integrate forward was to obtain market information they couldn�t access by selling to a packer on averages); or the chain mutually develops contractual relationships that reward its members for doing the right things right. The current state of the Canadian beef industry is such that it can be poised to move to the latter if they will is there to do it. A relatively small number of producers can produce enough cattle for a shift, or a half a shift. By developing a contract to deliver a fixed quantity of cattle with specific characteristics, packers� costs can be predicted, a market can be built for the final product with those characteristics, and risks and rewards can be shared. We would go further and suggest that the risks and rewards be shared through contract provisions that base price at each level on the value that consumers pay for the final product. We see a number of supply chains with this type of approach in Europe, but few in North America because North American industries tend to continue to want to operate from the scarcity paradigm. If we want to take advantage of differentiation and branding as the demand for meat grows markedly in the future, the disconnect between how supply chains operate and what is required to provide consistent products with the requisite characteristics needs to be broken. Putting this concept together with the previous one about regulation suggests that there will be a growing role in �integrating�, at least in management terms, producers and others in the supply chain, both to achieve what is required for market access in regulation and in developing appropriate supply chains to deliver what consumers want. As the final aspect of this rather utopian picture that is being painted, there is no theoretical reason why, where appropriate, Canadian and US producers should not participate together in supply chains. What stops us from taking advantage of the opportunities of the future are the regulations and mind sets that are in place from the past that were intended to protect us from competition.

Evolution of the North American Beef Industry Monday, November 22, 2005 George Morris Centre

Canadian Western Agribition & Saskatchewan Agrivision Corporation Page 26

5. Conclusions This final section has the intent of summarizing the major conclusions from the papers. Here is what the author thinks are the important takeaways: • The Canadian beef industry has experienced phenomenal growth over the past 50

years. Until the BSE event, the beef industry has to be regarded as one of the great success stories for Canada and for western Canada.

• When we look back over history, it is amazing how completely disruptive

government intervention can be. The US interventions in the early 70�s, and the adjustment in Canada post-CUSTA, post-WTO, and post-Crow are great examples. It underlines the Centre�s perspective that we need better policy.

• The opportunities of the future will be in branding and differentiation, not in bulk low

cost production. Those opportunities can be at least as great in the export market as in the domestic and North American markets.

• To access those opportunities, we need market access as the past year and a half has

shown. To ensure market access, we need good forward looking regulatory policy. And the regulatory policy must be consistent between Canada and the US to optimize our opportunities in the future. It is in the interest of producers in Canada and US to focus their efforts on integrating the two countries� regulatory policies as a way to mitigate risk and to enhance market access.

• If branded products are the future, then quality control will be paramount. If brands

will be based on specific characteristics, then the characteristics need to be delivered. If they are to be delivered, then people in the supply chain need to be rewarded for delivering. The current market mechanism promotes averages, not uniqueness. We need to have much better vertical supply chain control so that the appropriate product gets delivered and the appropriate people get paid appropriately. This will mean either total vertical integration through ownership, or developing dedicated supply chains who do planning and pricing starting from the perspective of the value to the final customer and working back.

Related Documents