ANNUAL REPORT 2008 Everyday Malls Primed For Growth

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

a n n u a l r e p o r t 2 0 0 8

Everyday MallsPrimed For Growth

CONTENTS

01 CorporateProfile-AboutLMIRTrust02 OurVision03 OurMission04 GroupFinancialHighlights

Delivering Performance

08 LetterToUnitholders10 TheBoardOfDirectors12 ManagementTeam14 TrustStructure15 CorporateInformation

Delivering Quality

18 PortfolioSummary20 PortfolioReview-RetailMalls23 PortfolioReview-RetailSpaces25 PortfolioLocationMap

Reaching Out To Customers

28 MarketReport34 FinancialReview36 CapitalManagement37 RiskManagement40 OperationReview44 InvestorRelations&Communications45 CorporateGovernance

FINANCIALS

52 FinancialContents104 StatisticsOfUnitholdings107 RelatedPartyTransactions

L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8 • 0 1

CORPORATePROFILe-ABOUTLMIRTRUST

Everyday Malls primed For defensive Growth

Lippo-Mapletree Indonesia Retail Trust (“LMIRTrust”), the first real estate investment trust (“ReIT”)in Singapore to provide exposure to Indonesia’sgrowing retail sector, is focused on enhancingshareholdervaluethroughactiveassetenhancementandsoundfinancialmanagementthatensuresteadyanddefensiveincomeforinvestors.

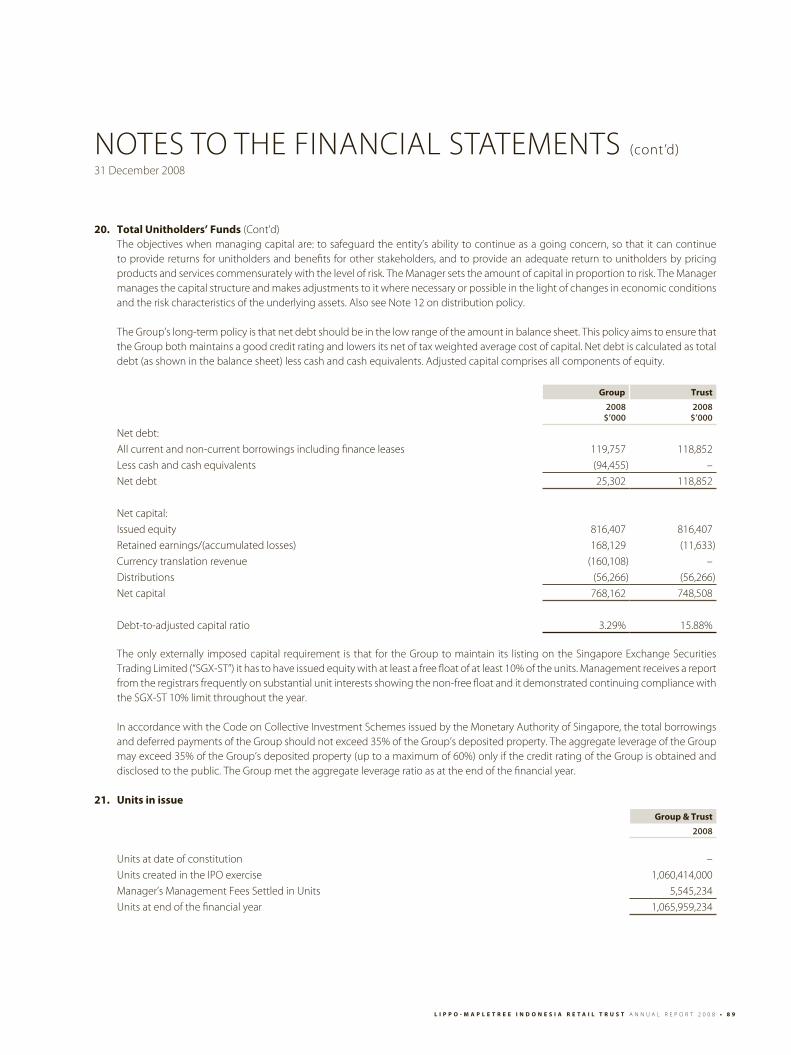

LMIR Trust’s portfolio comprises eight high-qualityretail malls and seven retail spaces located withinothermallswithacombinednetlettablearea(“nLA”)of402,632sqm1andvaluationofS$830million2asatDecember31,2008.Strategicallylocatedwithinlargeurban middle-class population catchment areas inGreater Jakarta, Bandung and Medan, LMIR Trust’sportfolio properties are everyday malls popularwith middle-to-upper-middle-income domesticconsumers in Indonesia. Top tenants include well-known international and domestic retailers andbrandnames, such as Matahari Department Store,Hypermart,GiantHypermarket,GramediaBookstore,Starbucks,Giordano,FitnessFirst,SportsStationandStudio21Cinema.

Since its listing on november 19, 2007, LMIR Trusthas undertaken prudent acquisition to prime thevastpotentialof itsportfolio for long-termgrowth.ThisincludedtheacquisitionofSunPlaza,alandmarkretailmallinMedan,thethirdmostpopulouscityinIndonesiaafterJakartaandSurabaya.To-date,LMIRTrust’s malls and retail spaces continue to enjoy astrongaverageoccupancyrateof95.7%comparedtothe84.6%3industryaverage.

Going forward, LMIR Trust will look towardsfocusingonorganicgrowththroughproactiveassetmanagementtomaintainitsstrongoccupancy.

About the Sponsor and the Manager

TheSponsorofLMIRTrustisPTLippoKarawaciTbk,Indonesia’s largest listedpropertycompanyandaninternationally recognised corporation with a trackrecord and dominant position within the propertyindustryinIndonesia.

TheManager,Lippo-MapletreeIndonesiaRetailTrustManagementLtd, is incorporatedinSingaporeand60.0% indirectly owned by the Sponsor and 40.0%ownedbyMapletreeManagementPte.Ltd,awholly-ownedsubsidiaryoftheMapletreeGroup,aleadingrealestatecompanyinSingaporewithanassetbaseofS$4.5billioncomprisingoffice,logistics,industrial,retailandlifestyleproperties.

1 As at December 31, 2008.2 Valuation from Knight Frank as at November 30, 2008.3 Cushman & Wakefield Indonesia Q4 Market Review.

Ekalokasari Plaza.

0 2 • L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8

To be the premier retail REIT in Asia, creating and utilising scale

whilst leading the way in innovation and quality. We aim to create

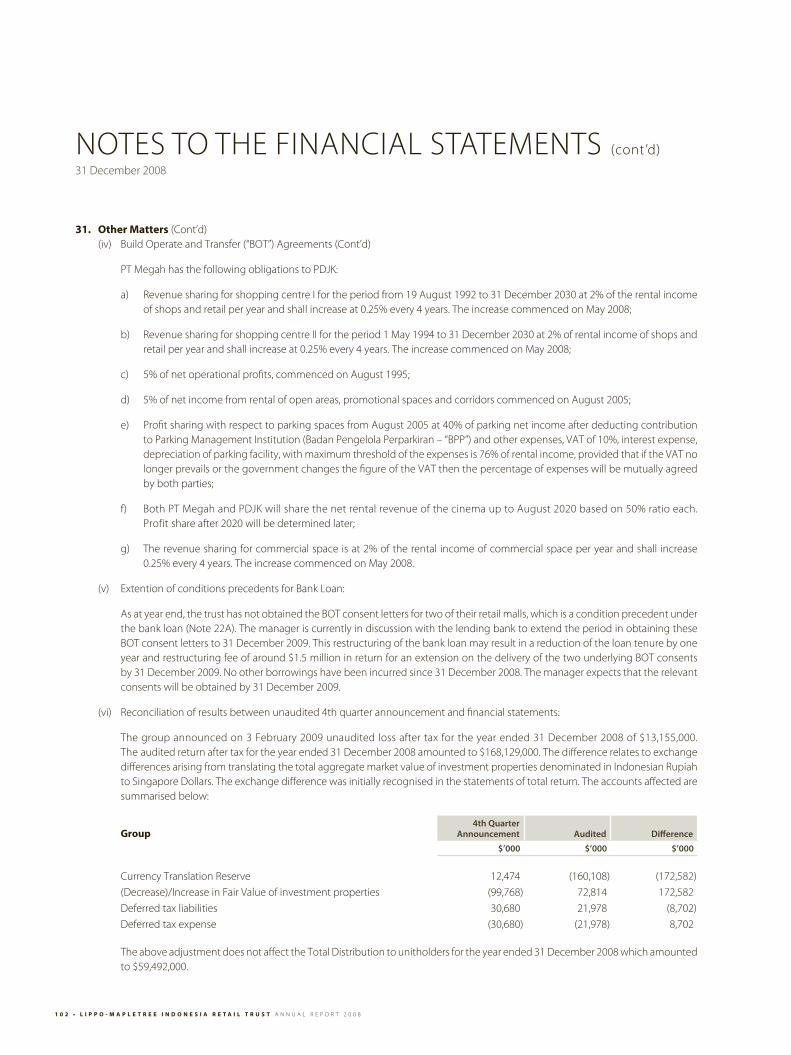

long term value for stakeholders by providing access to high

growth malls as well as strong economic and consumer growth.

OURVISIOn

Istana Plaza. Ekalokasari Plaza.

L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8 • 0 3

OURMISSIOnWe are committed to:

• delivering regular and stable distributions to Unitholders

• growing our portfolio by way of investments in retail and/or retail related assets

• enhancing returns from existing and future properties

• achieving long-term growth to provide Unitholders with capital appreciation on their investments

Outdoor dining.

0 4 • L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8

GROUPFInAnCIALHIGHLIGHTS

Summary of FY20081 results

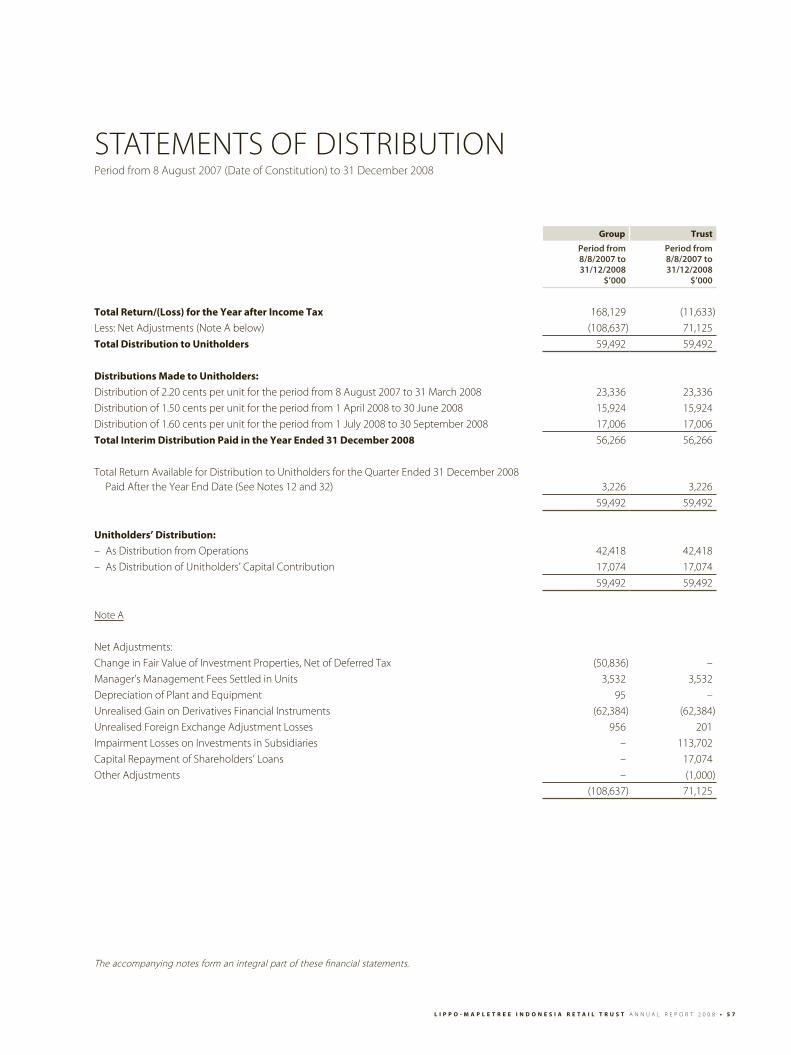

2008

Actual S$’000 Forecast S$’000 Change %

GrossRevenue 101,761 94,202 8%

PropertyOperatingexpenses (13,464) (5,942) 127%

netPropertyIncome 88,297 88,260 0%

DistributableIncome 59,492 68,863 14%

DistributionPerUnit(cents) 5.60 6.48 14%

LMIRTrustrecordedgrossrevenuesofS$101.8millionfortheFinancialYear2008endedDecember31,2008(“FY2008”),whichwasaboveforecast,mainlyduetothecontributionfromSunPlaza,whichwasacquiredonMarch31,2008.

Property operating expenses for FY2008 cameto S$13.5 million. The unfavourable increase of$7.5 million compared to forecast is due mainly toallowance for impairment charge on outstandingreceivables of S$7.0 million comprising outstandingrentfromwholesalertenants.

Distribution to unitholders for FY2008 is S$59.5million, which is S$9.4 million below forecast.This is mainly due to impairment charge for theoutstandingreceivablesof$7.0millionasexplainedabove,andthewritingoffofthearrangementfeeofS$2.8millionforthebalanceS$225millionloantobesyndicatedin2009.ThistranslatesintoaDPUof5.60centsforFY2008.

notwithstandingthechallengingeconomicclimate,LMIR Trust still managed to achieve high averageoccupancyof95.7%,abovetheindustryaverageof84.6%.LMIRTrust’sgearingof12.4%iswellwithintheaggregateleveragelimitassetoutintheguidelinesforrealestateinvestmenttrustsinAppendix2oftheCode on Collective Investment Schemes issued bythe Monetary Authority of Singapore. LMIR Trust’sportfolio is well diversified with no single propertyaccountingformorethan21%oftotalnetpropertyincome. Tenant diversification is balanced with nosingle trade sector accounting for more than 17%oftotalnLA,whichprovidesstability inthecurrenteconomicclimate.

For 2009, LMIR Trust will focus on organic growththrough proactive asset management to maintainstrong occupancy, balanced property and tenantdiversificationacrossitsretailmallsandspaces.Assetacquisitionsareunlikely.

1 FY 2008 includes private trust period from 8 August 2007 to 18 November 2007 and public trust from 19 November 2007 (“Listing Date”) to 31 December 2008.

L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8 • 0 5

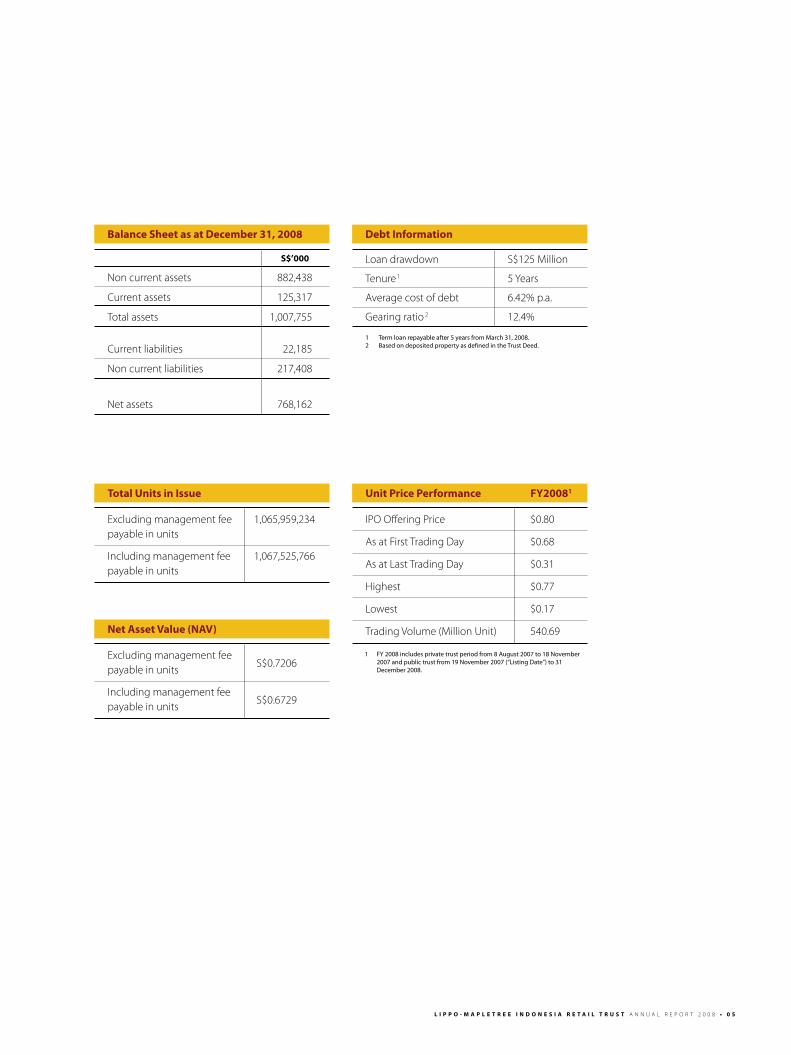

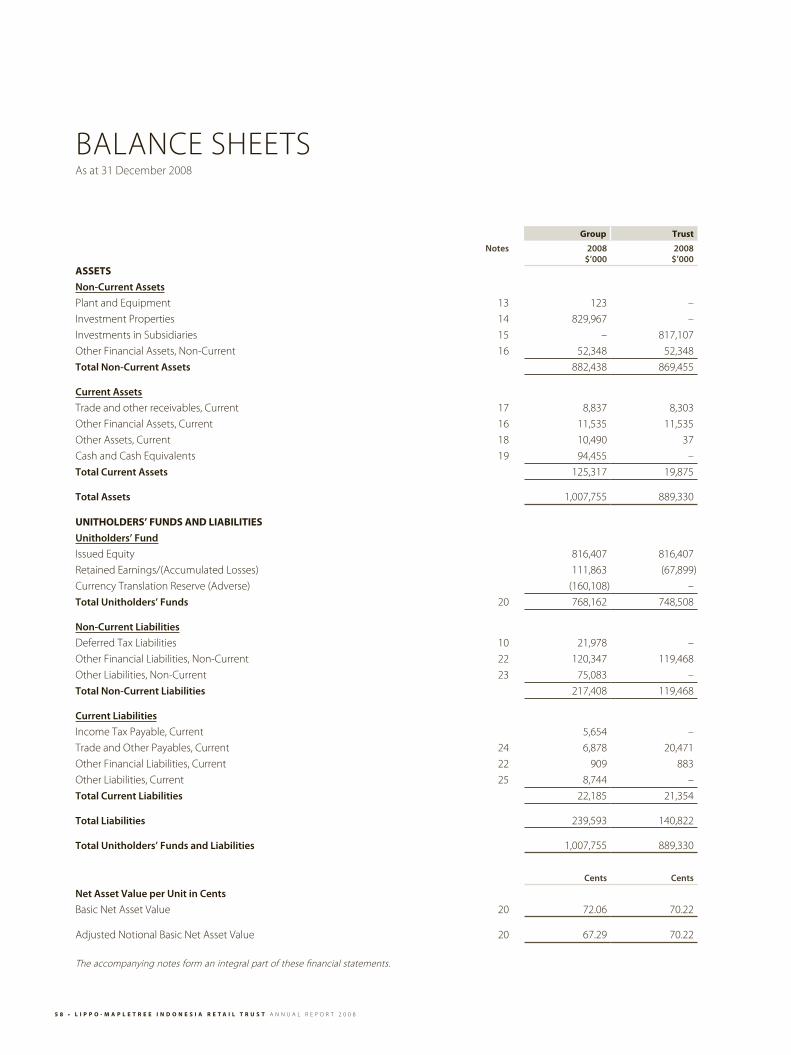

Balance Sheet as at december 31, 2008

S$’000

noncurrentassets 882,438

Currentassets 125,317

Totalassets 1,007,755

Currentliabilities 22,185

noncurrentliabilities 217,408

netassets 768,162

debt Information

Loandrawdown S$125Million

Tenure1 5Years

Averagecostofdebt 6.42%p.a.

Gearingratio 2 12.4%

1 Term loan repayable after 5 years from March 31, 2008.2 Based on deposited property as defined in the Trust Deed.

Total units in Issue

excludingmanagementfee 1,065,959,234 payableinunits

Includingmanagementfee 1,067,525,766 payableinunits

Net Asset Value (NAV)

excludingmanagementfee payableinunits S$0.7206

Includingmanagementfee payableinunits S$0.6729

1 FY 2008 includes private trust period from 8 August 2007 to 18 November 2007 and public trust from 19 November 2007 (“Listing Date”) to 31 December 2008.

unit price performance FY20081

IPOOfferingPrice $0.80

AsatFirstTradingDay $0.68

AsatLastTradingDay $0.31

Highest $0.77

Lowest $0.17

TradingVolume(MillionUnit) 540.69

dELIVErING pErFOrMANCE prudent capital management and proactive

asset enhancement has been the cornerstone

of LMIr Trust’s performance. It is a strategy that

has yielded high occupancy, balanced property

and tenant diversification across LMIr Trust’s

retail malls providing for resilient, stable earnings.

0 8 • L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8

DearUnitholders

OnbehalfoftheBoardofDirectorsofLippo-MapletreeIndonesiaRetailTrustManagementLtd,managerofLMIRTrust,wearepleasedtosharewithyouthekeymilestones and progress that LMIR Trust has madeintheFinancialYearendedDecember31,2008.

Year in reviewFY2008 was a historical year which sawunprecedented volatility in the global financialmarkets. Indonesia’s economy displayed resilienceinthefaceoftheglobaldownturn,registeringGDPgrowth of 6.1%1 for FY2008, helped by increasedgovernmentfiscalexpenditureandlowerinflation.

AsatSeptember2008,thetotalretailspaceinJakartaincreasedslightlyby0.27millionsquaremetresto3.37millionsquaremetresfrom3.10millionsquaremetresinJune2008.Theoveralloccupancyratefortheindustryheldsteadyat84.6%2asatDecember31,2008.

LMIR Trust’s resilient operational performance forFY2008wassupportedbyourportfolioofdefensivesuburbanmallsandretailspacesstrategicallylocatedin high population urban middle-class catchment

LeT TeRTOUnITHOLDeRS

areas in Greater Jakarta, Bandung and Medan, asoundbalancesheetandstrongmanagementteam.

FY2008 witnessed LMIR Trust’s maiden acquisitionof Sun Plaza, one of the largest shopping centresin Medan, north Sumatra at a purchase price ofapproximatelyS$146.73million,whichincreasedourtotalportfolionLAbyapproximately20%sinceourIPO.AsatDecember31,2008,ourtotalnLAstandsat402,632sqm.

Against the challenging backdrop of high inflationandslowdownindiscretionaryconsumerspending,grossrevenuesinFY2008cametoS$101.8million,8%higher than forecasted due mainly to contributionfromtheacquisitionofSunPlaza.

However, property operating expenses for FY2008washighatS$13.5million,duemainlytoallowancefor impairment of S$7.0 million in outstandingreceivables comprising outstanding rent fromwholesaler tenants. In addition, we wrote off S$2.8million of arrangement fee and the correspondinglegal fee of S$0.5 million relating to the balanceS$225 million loan to be syndicated in 2009. Weundertooktheseasmeasuresofprudencegiventheincreasingly challenging credit environment. DPUcameto5.60centsforFY2008.

Although we had to contend with an increasinglychallenging economic climate, our retail mallsachievedahighaverageoccupancyrateof95.7%asatDecember31,2008,which isabovethe industryaverageof84.6%2.

LMIR Trust contended with challenging macro-economic conditions in

FY2008 and emerged financially stable with low gearing, defensive and

steady revenues and a well-balanced, diversified portfolio of retail properties

located within high population urban middle-class catchment areas.

1 Thomson Reuters, February 18, 2009.2 Cushman & Wakefield Indonesia Q4 Market Review.3 Purchase price of the Singapore Companies which own the Indonesian Company which wholly own Sun Plaza.

Ms Viven Gouw Sitiabudi, CEO and Mr Tan Bar Tien, Chairman.

L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8 • 0 9

Capital ManagementLMIRTrustbenefitsfromanoptimalcapitalstructurein the face of the tightening credit market. As atDecember 31, 2008, LMIR Trust’s gearing ratioremainsataconservative12.4%,whichisbelowtheaggregateleveragelimitassetoutintheguidelinesfor ReITs in Appendix 2 of the Code on CollectiveInvestment Schemes issued by the MonetaryAuthorityofSingapore.Ourcurrentgearingismainlyfrom a S$125 million loan with a five-year tenureandall-in interest rateof6.42%p.a. Duetoadelayin getting the consents from BOT (Build OperateTransfer) grantors for two of LMIR Trust’s malls toenterintotheloandocuments,Manageriscurrentlyin discussion with the lending bank to extend theperiod in getting these BOT consents to the endof the year. This restructuring of the current S$125million five year loan, may result in a reduction oftheloantenurebyoneyearandrestructuringfeeofaroundS$1.5millioninreturnforanextensiononthedelivery of the two underlying BOT consents by 31Dec2009.nootherborrowingshavebeenincurredsinceDecember31,2008.Weexpectthattherelevantconsentswillbeobtainedbytheendof2009.

We will continue to focus on prudent capitalmanagement strategy by conserving cash throughtightcontrolsoveroperatingandcapitalexpenditure.

Asset enhancement progressWe are pleased to report positive progress of ourasset enhancement initiatives (AeI). Our AeI plansaredesignedtoaddvaluetoourexistingmallsandincrease shopper traffic to maximise their growthpotentialfromIndonesia’sexpandingurbanmiddle-classsegment.

IstanaPlaza’sAeIisprogressingwiththeconversionofaniceskatingrinkintonewcafeterias,restaurantsand an expanded food court. About 653 sqm ofadditional nLA will be derived from the 950 sqmproposedarea.

Goingforward,wewillcontinuetolookatachievingan optimal balance between AeI and a need toconservecash,forgreaterfinancialflexibility.

defensive earnings in uncertain timesLMIR Trust’s property portfolio comprises retailmallsandretailspaces locatedin Indonesia’smajorcities with large urban middle-class populationcatchmentareasthatareeasilyaccessibleviamajortransportation routes and highways. The strongaverageoccupancyoftheproperties,coupledwithwelldiversifiedtenantmixwherenoparticulartrade

sectoraccountsformorethan17%oftotalnLAandnosinglepropertyconstitutesmorethan21%oftotalnetpropertyincome,ensuresdefensiveearningsfortheTrustduringthecurrentuncertaintimes.

The main shopper traffic at our retail malls andspaces comprises Indonesia’s domestic urbanmiddle-incometoupper-middle-incomeconsumersegments,whichhavegreaterresiliencetoinflationin consumer staple prices. LMIR Trust’s malls arealsodeemedas“everydaymalls”fordailyessentials,foodoutletsandfamilyentertainment.Whilstthesedefensive qualities provide stability to LMIR Trust’sincome and cashflow, we will continue to monitordevelopments inthemacroeconomicenvironmentandtheirpotentialimpactonourbusiness..

update on utilisation of IpO proceedsLMIRTrustraisedgrossproceedsofS$848.3millionupon listing. This amount has been fully appliedfor payment of the purchase consideration for theacquisitionofalltheordinarysharesandredeemablepreference shares of the Singapore companies(which in turn owns the Indonesian companieswhichwhollyowntheretailmallsandretailspacesinIndonesia),andtheissuecostsrelatedtotheIPO.

OutlookWe anticipate 2009 to be a challenging year,with retail space demand expected to weakenand competition among landlords to intensify. Inaddition,rentaltrendsinIndonesiaareexpectedtocomeunderpressure.Ourstrategyistocontinuetofocusonorganicgrowth,whilstexercisingprudenceinassetenhancementsandacquisitions.Inaddition,throughproactiveassetmanagement,wewilldoourutmosttomaintaingoodoccupancyandbalancedpropertyandtenantdiversificationacrossour retailmallsandspacesforsteady,defensiveearnings.

AcknowledgementsLMIR Trust’s resilient performance is due to theunrelenting support provided by its tenants,shoppers, business partners and employees. Onbehalf of the Board of Directors, we are privilegedto extend our sincere thanks and appreciation tothemandtoyou,ourUnitholders,foryourinvaluablecontribution,beliefandconfidenceinourbusiness.

Mr Tan Bar Tien Ms Viven Gouw Sitiabudinon-executive ChiefexecutiveOfficer&Chairman executiveDirector

1 0 • L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8

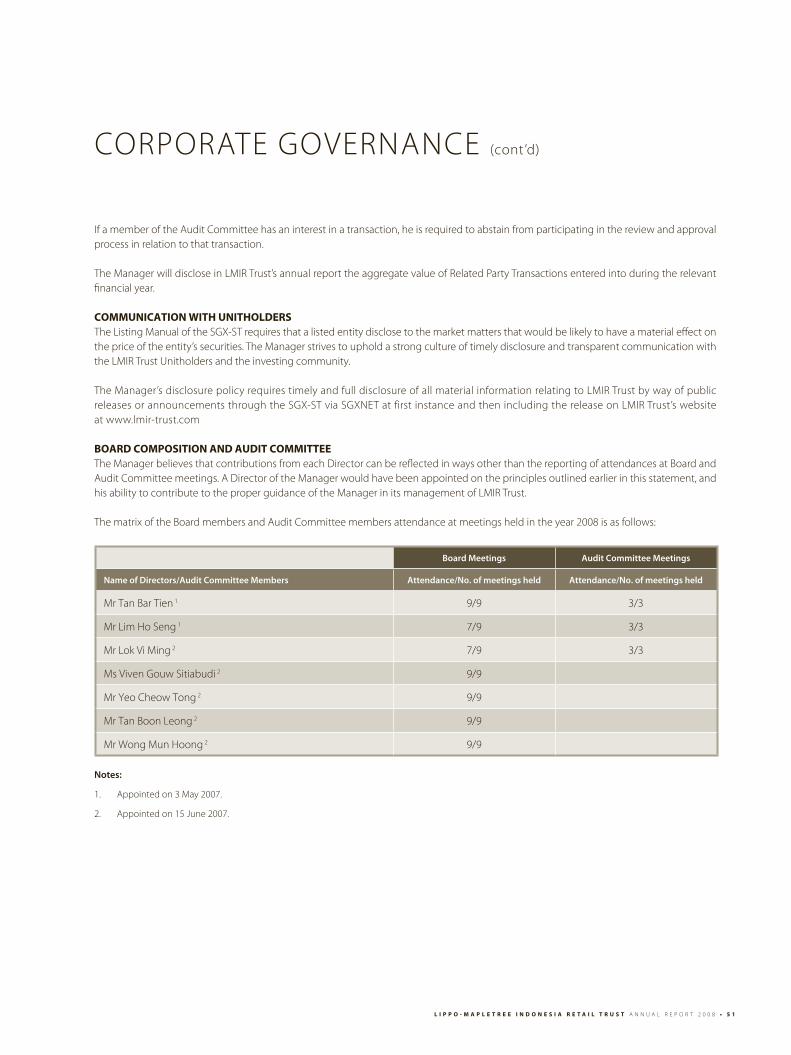

THeBOARDOFDIReCTORS

From top left to bottom right :

Mr Tan Bar TienMs Viven Gouw Sitiabudi Mr Lim Ho SengMr Lok Vi MingMr Yeo Cheow TongMr Wong Mun HoongMr Tan Boon Leong

L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8 • 1 1

Mr Tan Bar TienChairmanIndependent Non-Executive Director

MrTan BarTien is a lawyer with 30 years of practice andextensive experience in various aspects of law includingcorporate law, property law and litigation matters. MrTan has represented clients in transactions in relation tocompleted properties and properties under constructionand is familiar with real estate matters such as propertymortgages, sale and purchase of properties, constructionloansanddeveloper’sprojects, includingtheconstructionofpropertiesonaprogressivebasis.MrTangraduatedfromtheUniversityofSingaporein1976withadegreeinBachelorofLaws(Honours),andwasadmittedasanAdvocateandSolicitoroftheHighCourtofSingaporeinJanuary1977.

Mr Lim Ho SengIndependent Non-Executive Director

MrLimHoSenghasover20yearsofexperienceintheretailindustry and was formerly the Chief executive Officer ofnTUCFairpriceCooperativeLtd,whichhas investments inreal estate and leases retail spaces to other retail tenants.MrLimwaspreviouslyadirectorofTampinesMallPteLtd,whichwassubsequentlyacquiredbyCapitaMallTrust,andiscurrentlytheChairmanofBakerTechnologyLimited.HeisaFellowof the InstituteofCertifiedPublicAccountantsofSingapore,the InstituteofCertifiedPublicAccountants,Australia,theAssociationofCharteredCertifiedAccountantsandtheInstituteofCharteredSecretariesandAdministrators,UnitedKingdomandtheSingaporeInstituteofDirectors.

Mr Lok Vi MingIndependent Non-Executive Director

MrLokViMingisapartnerandheadoftheAviationPracticeGroup at M/s Rodyk & Davidson. Appointed as a SeniorCounsel in 2005, Mr Lok is an internationally renownedaviationlawyerwhohasbeenfeaturedineuromoneyLegalMedia’sGuideandGuidetotheWorld’sLeadingInsuranceandReinsurancelawyersandalsointheInternationalWho’sWho of Aviation lawyers 2005. Mr Lok is a Fellow of theSingapore InstituteofArbitratorsandhasbeenappointedto the Regional Panel of Arbitrators with the SingaporeInternationalArbitrationCentre.

Mr Lok graduated with a Bachelor of Law (Honours) fromthenationalUniversityofSingaporein1986.

Ms Viven Gouw SitiabudiExecutive Director of the Board and Chief Executive Officer

Ms Viven Gouw Sitiabudi has more than 20 years ofexperience inmanagement,marketingandsalesandwasthePresidentDirectoroftheSponsor.Underherstewardshipinthepastthreeyears,theSponsorhasbecomethelargestlistedpropertycompanyinIndonesia.Shehasbeenintegralin identifyingtheopportunity for theSponsorto invest inretail properties (the strata malls and the planned leasedmalls),enhancingexistingassetsandensuringthedeliveryoftheSponsor’sdevelopmentprojects,whichspanacross

a variety of real estate sectors, including urban/township,residentialclusters,condominium,hospitalsaswellashotelprojects, throughout Indonesia. Ms Sitiabudi graduatedfromtheUniversityofnewSouthWales,Australia in1977withadegreeinComputerScienceandStatistics.

Mr Yeo Cheow TongNon-Executive Director

Mr Yeo Cheow Tong has been a prominent figure inthe Singapore political landscape for over 20 years andhad previously held different ministerial positions in theSingapore government such as Minister of Transport,Minister of Health, Minister for Community Development,Minister for Trade and Industry and Minister for theenvironment. He is currently a Member of Parliament forHongKahGroupRepresentationConstituencyandsitsonthe panel of advisers for Lippo Group, Raffles educationCorporation as well as that for the University of ChicagoGraduate School of Business. In addition, he holds theposition of chairman of the Board of Governors of RafflesUniversity,andisalsoadirectorofKillyInvestPteLtd.MrYeograduatedfromtheUniversityofWesternAustraliain1971withaBachelor’sdegreeinengineering.

Mr Tan Boon LeongNon-Executive Director

Mr Tan Boon Leong has 32 years of experience in thereal estate industry and is currently the Chief OperatingOfficer of Mapletree Investments Private Limited. He isalso a director of Mapletree Logistics Trust ManagementLtd and chairs the Asset Control Group for VivoCity, thelargest retail mall in Singapore. He has also worked withtheInlandRevenueAuthorityofSingapore(IRAS)wherehewasinvolvedinthevaluationofrealestateinSingaporeandheldtheappointmentsofTaxDirector(TechnicalServices—Property)andHeadofPropertyandValuationServices.Heis currently a member of the Valuation Review Board ofSingapore.MrTanwasaColomboPlanscholarandstudiedurbanvaluation(realestate)attheUniversityofAuckland,newZealand.

Mr Wong Mun HoongNon-Executive Director

Mr Wong Mun Hoong is the Chief Financial Officer ofMapletreeInvestmentsPteLtdwhereheisresponsibleforFinance,Treasury,CorporatePlanning& InvestorRelations,Risk Management and InformationTechnology. He is alsoadirectorofMapletreeLogisticsTrustManagementLtd.MrWonghasover14years’investmentbankingexperienceinAsia,thelast10yearsofwhichwerewithMerrillLynch&Co,whichincludedstintsinSingapore,HongKongandTokyo,and where he was a Director and Head of its SingaporeInvestment Banking Division. Mr Wong graduated witha Bachelor of Accountancy (Honours) from the nationalUniversity of Singapore in 1990. He is a non-practisingmember of the Institute of Certified Public Accountantsof Singapore. He holds the professional designation ofChartered Financial Analyst from the CFA Institute of theUnitedStates.

Standing from left to right :

Ms Rita Yovita SantosaMr Rudi Chuan Hwee HiowMs Viven Gouw SitiabudiMr Leigh V Regan

MAnAGeMenTTeAM

1 2 • L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8

Ms Viven Gouw SitiabudiExecutive Director of the Board and Chief Executive Officer

Ms Viven Gouw Sitiabudi is responsible for the overallmanagement and planning of the strategic direction ofLMIRTrust,aswellasoverseeingitsday-to-dayoperations,asChiefexecutiveOfficer.PleaserefertoBoardofDirectorssectionforfurtherdetailsofMsVivenGouwSitiabudi’sprofile.

Mr rudi Chuan Hwee Hiow Chief Financial Officer, Investor Relations Manager and Compliance Officer

Mr Rudi Chuan Hwee Hiow brings with him extensiveexperienceincorporatefinanceintheproperty, industrial,logisticsandconsumersectors.Priorto joiningLMIRTrust,he was the Senior Vice President (Finance & Accounting)withMacquariePacificStarPrimeReITManagementLimitedwhere he was in charge of finance and finance-relatedduties,humanresource,informationtechnologyaswellasservingastheco-companysecretary.MrChuanisacertifiedpublicaccountantandhasbeenamemberoftheInstituteof Certified Public Accountants of Singapore since 1988.He graduated in 1981 from the University of Otago, newZealand,withaBachelorofCommercedegreeinAccountingandholdsaMaster’sdegreeinBusinessAdministrationfromtheStateUniversityofnewYork,Buffalo.

Mr Andreas Kartawinata(not in the picture)Asset ManagerMrAndreashasovertwentyyearsofexperienceinallphasesof leasing, management, marketing and sales, includingbuildingateamofpropertyprofessionals,marketresearch,market planning, product management, advertising,promotion,salesandpropertymanagement.MrKartawinataisalsothePresidentoftheAssociationofShoppingCentresofJakarta—Indonesiafortwoconsecutiveperiods,namely2003-2007and2007-2010.MrKartawinatahasparticipatedin internationaleventssuchassittingasapanelistontheCouncil of Asian Shopping Centre Seminar in Malaysia(2005) and Indonesia (2006). Mr Kartawinata graduatedfrom Institute Technology of Bandung with a major inelectro-techniqueengineering.

L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8 • 1 3

Ms rita Yovita SantosaAsset Manager

Ms. Rita Yovita Santosa has more than 10 years ofexperience in the real estate industry covering the areaof property management and maintenance; marketingand lease management; property development andspecial project management; and asset enhancementprogram,negotiationsandacquisitions.Shepreviouslyheldappointmentsas theGeneralManagerofLippoKarawaci-AssetenhancementDivisionandSpecialProjectSpecialistof Lippo Bank-Asset Management Group. She holds anInternationalCouncilofShoppingCentersCertificatefromUniversityofShoppingCentersandattendedtheIndonesiaShoppingCentersSeminar&CongressattheAssociationofIndonesiaShoppingCenters.

Mr Leigh V reganInvestment Manager

MrLeighVReganbringswithhim24yearsofprofessionalinvestmentmanagementexperience,spanningareassuchas retail property leasing, management and operations inIndonesiaandAustralia.PriortoLMIRTrust,MrReganwasChiefOperatingOfficeroftheUS$250millionSenayanCityMixedUseProject inJakarta, Indonesia. HehadalsoheldseniorappointmentsatQueenslandInvestmentCorporationandJonesLangLaSalleinAustralia.MrReganholdsCertifiedPracticingAccountant(CPA)andCertifiedShoppingCentreManager(CSMA)professionalqualificationsinadditiontoaBachelorofBusinessfromRMIT,Australia.

1 4 • L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8

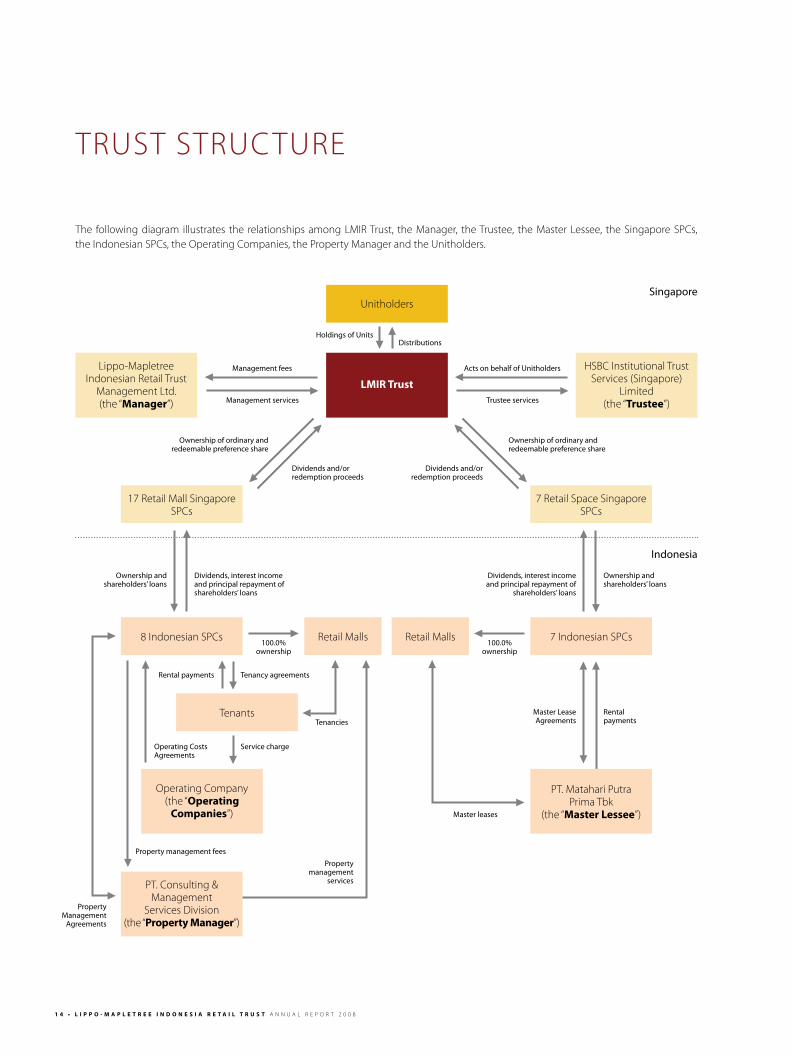

TRUSTSTRUCTURe

The followingdiagram illustrates the relationshipsamongLMIRTrust, theManager, theTrustee, theMasterLessee, theSingaporeSPCs,theIndonesianSPCs,theOperatingCompanies,thePropertyManagerandtheUnitholders.

LMIr Trust

Lippo-MapletreeIndonesianRetailTrust

ManagementLtd.(the“Manager”)

HSBCInstitutionalTrustServices(Singapore)

Limited(the“Trustee”)

Unitholders

17RetailMallSingaporeSPCs

7RetailSpaceSingaporeSPCs

8IndonesianSPCs 7IndonesianSPCsRetailMalls RetailMalls

Indonesia

PT.MatahariPutraPrimaTbk

(the“Master Lessee”)

Tenants

OperatingCompany(the“Operating

Companies”)

Singapore

Management services

Management fees

Holdings of UnitsDistributions

Trustee services

Acts on behalf of Unitholders

Ownership of ordinary and redeemable preference share

Dividends and/or redemption proceeds

Ownership of ordinary and redeemable preference share

Dividends and/or redemption proceeds

Ownership and shareholders’ loans

Dividends, interest income and principal repayment of shareholders’ loans

Dividends, interest income and principal repayment of

shareholders’ loans

Ownership and shareholders’ loans

100.0% ownership

100.0% ownership

Rental payments Tenancy agreements

Tenancies

Service chargeOperating Costs Agreements

Property management fees

Property Management

Agreements

PT.Consulting&Management

ServicesDivision(the“property Manager”)

Property management

services

Master Lease Agreements

Rental payments

Master leases

L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8 • 1 5

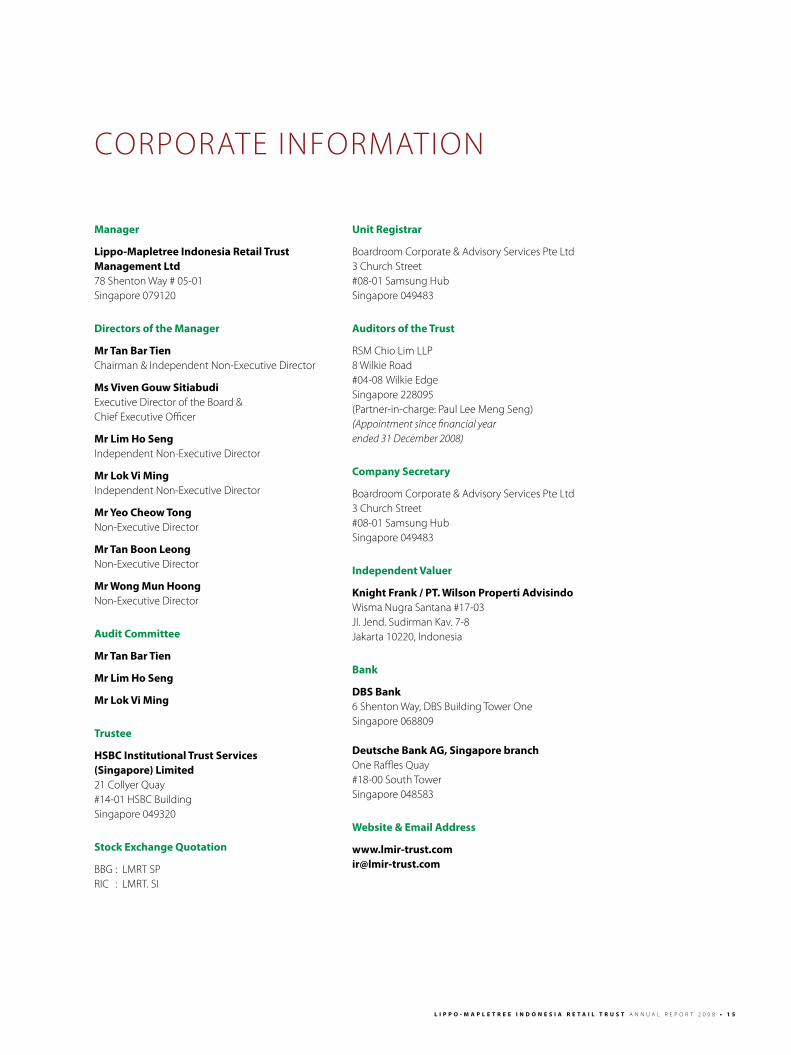

CORPORATeInFORMATIOn

Manager

Lippo-Mapletree Indonesia retail Trust Management Ltd78ShentonWay#05-01Singapore079120

directors of the Manager

Mr Tan Bar TienChairman&Independentnon-executiveDirector

Ms Viven Gouw SitiabudiexecutiveDirectoroftheBoard&ChiefexecutiveOfficer

Mr Lim Ho Seng Independentnon-executiveDirector

Mr Lok Vi MingIndependentnon-executiveDirector

Mr Yeo Cheow Tongnon-executiveDirector

Mr Tan Boon Leongnon-executiveDirector

Mr Wong Mun Hoongnon-executiveDirector

Audit Committee

Mr Tan Bar Tien

Mr Lim Ho Seng

Mr Lok Vi Ming

Trustee

HSBC Institutional Trust Services (Singapore) Limited21CollyerQuay#14-01HSBCBuildingSingapore049320

Stock Exchange Quotation

BBG: LMRTSPRIC : LMRT.SI

unit registrar

BoardroomCorporate&AdvisoryServicesPteLtd3ChurchStreet#08-01SamsungHubSingapore049483

Auditors of the Trust

RSMChioLimLLP8WilkieRoad#04-08WilkieedgeSingapore228095(Partner-in-charge:PaulLeeMengSeng)(Appointment since financial year ended 31 December 2008)

Company Secretary

BoardroomCorporate&AdvisoryServicesPteLtd3ChurchStreet#08-01SamsungHubSingapore049483

Independent Valuer

Knight Frank / pT. Wilson properti AdvisindoWismanugraSantana#17-03Jl.Jend.SudirmanKav.7-8Jakarta10220,Indonesia

Bank

dBS Bank 6ShentonWay,DBSBuildingTowerOneSingapore068809

deutsche Bank AG, Singapore branch OneRafflesQuay#18-00SouthTowerSingapore048583

Website & Email Address

dELIVErING QuALITY LMIr Trust’s portfolio properties are “everyday”

high quality retail malls and spaces located

in Indonesia’s major cities within large urban

middle-class population catchment areas. Tenants

comprise well known international and domestic

retailers and brandnames hugely popular with

middle-to-upper-middle-income consumers.

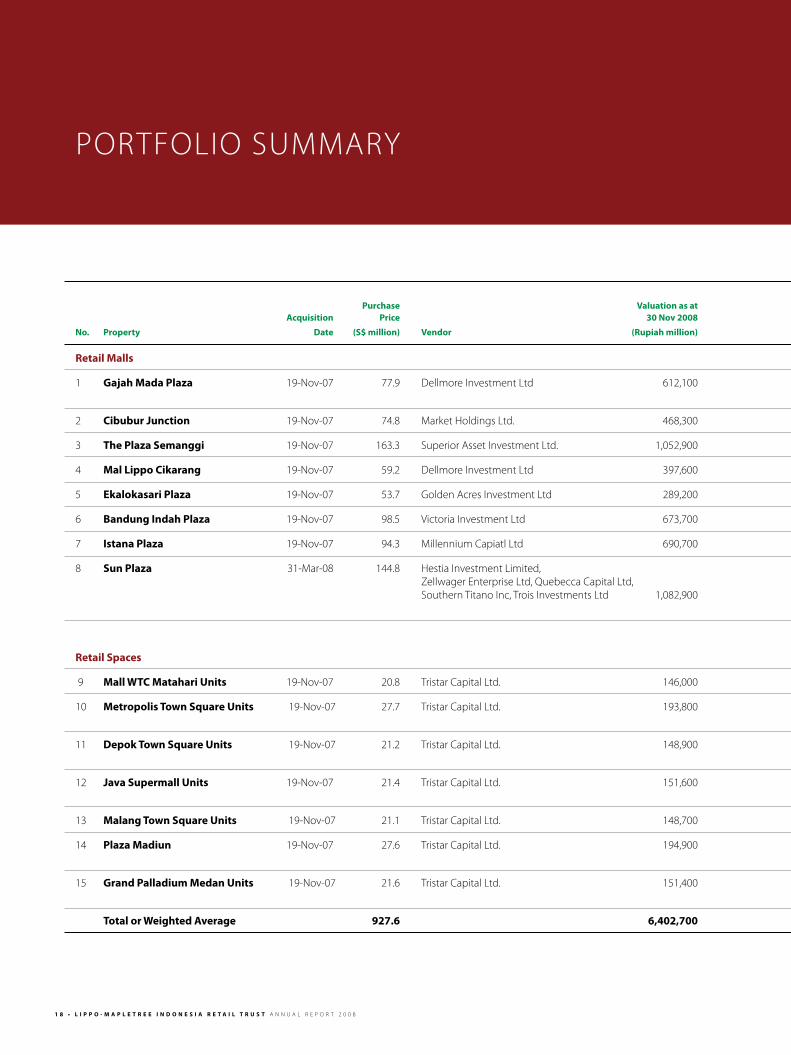

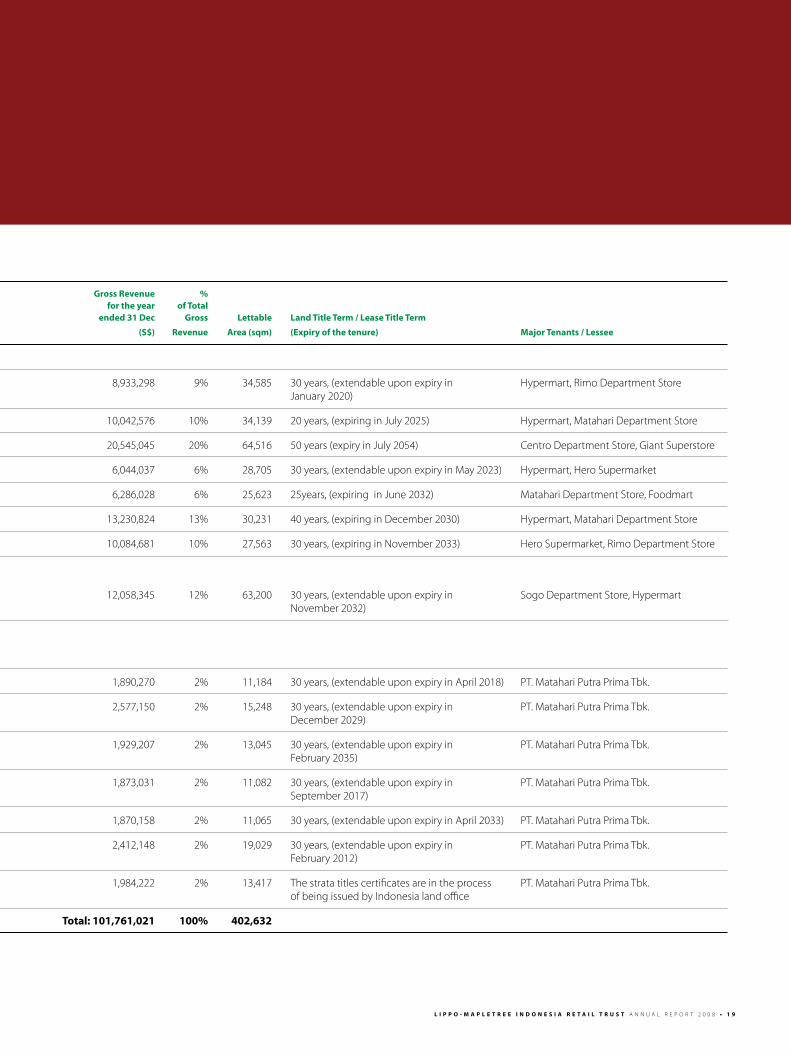

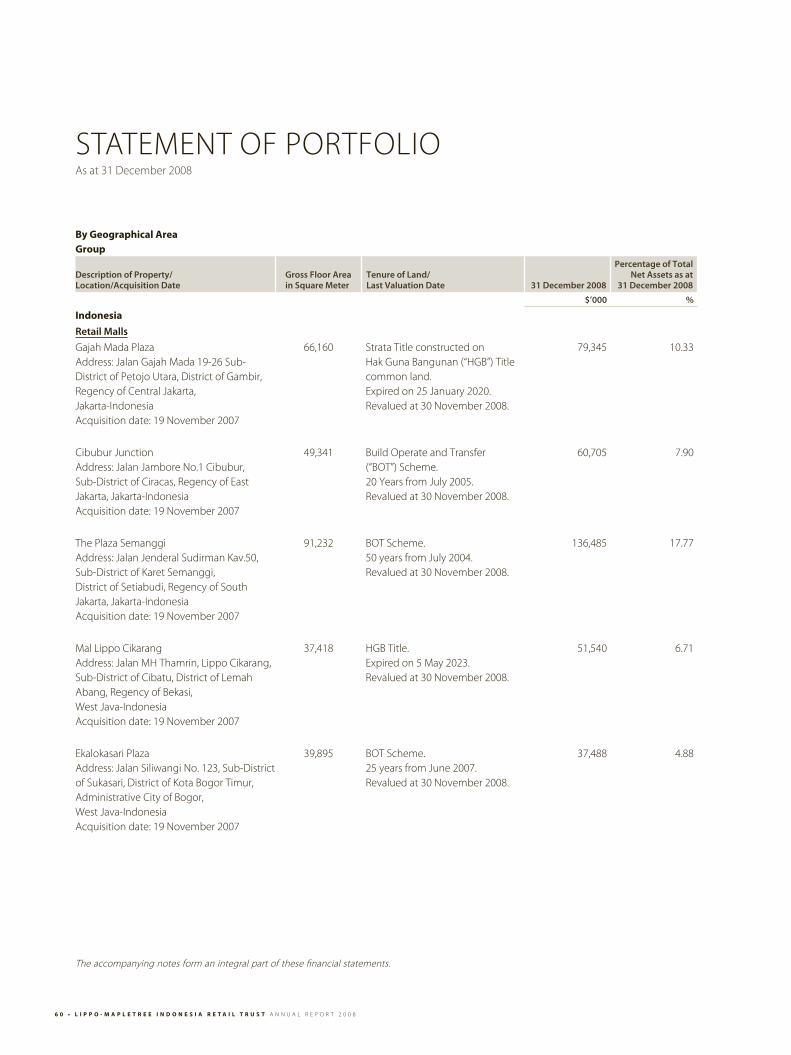

Gross revenue % purchase Valuation as at for the year of Total Acquisition price 30 Nov 2008 ended 31 dec Gross Lettable Land Title Term / Lease Title Term

No. property date (S$ million) Vendor (rupiah million) (S$) revenue Area (sqm) (Expiry of the tenure) Major Tenants / Lessee

retail Malls

1 Gajah Mada plaza 19-nov-07 77.9 DellmoreInvestmentLtd 612,100 8,933,298 9% 34,585 30years,(extendableuponexpiryin Hypermart,RimoDepartmentStore January2020)

2 Cibubur Junction 19-nov-07 74.8 MarketHoldingsLtd. 468,300 10,042,576 10% 34,139 20years,(expiringinJuly2025) Hypermart,MatahariDepartmentStore

3 The plaza Semanggi 19-nov-07 163.3 SuperiorAssetInvestmentLtd. 1,052,900 20,545,045 20% 64,516 50years(expiryinJuly2054) CentroDepartmentStore,GiantSuperstore

4 Mal Lippo Cikarang 19-nov-07 59.2 DellmoreInvestmentLtd 397,600 6,044,037 6% 28,705 30years,(extendableuponexpiryinMay2023) Hypermart,HeroSupermarket

5 Ekalokasari plaza 19-nov-07 53.7 GoldenAcresInvestmentLtd 289,200 6,286,028 6% 25,623 25years,(expiringinJune2032) MatahariDepartmentStore,Foodmart

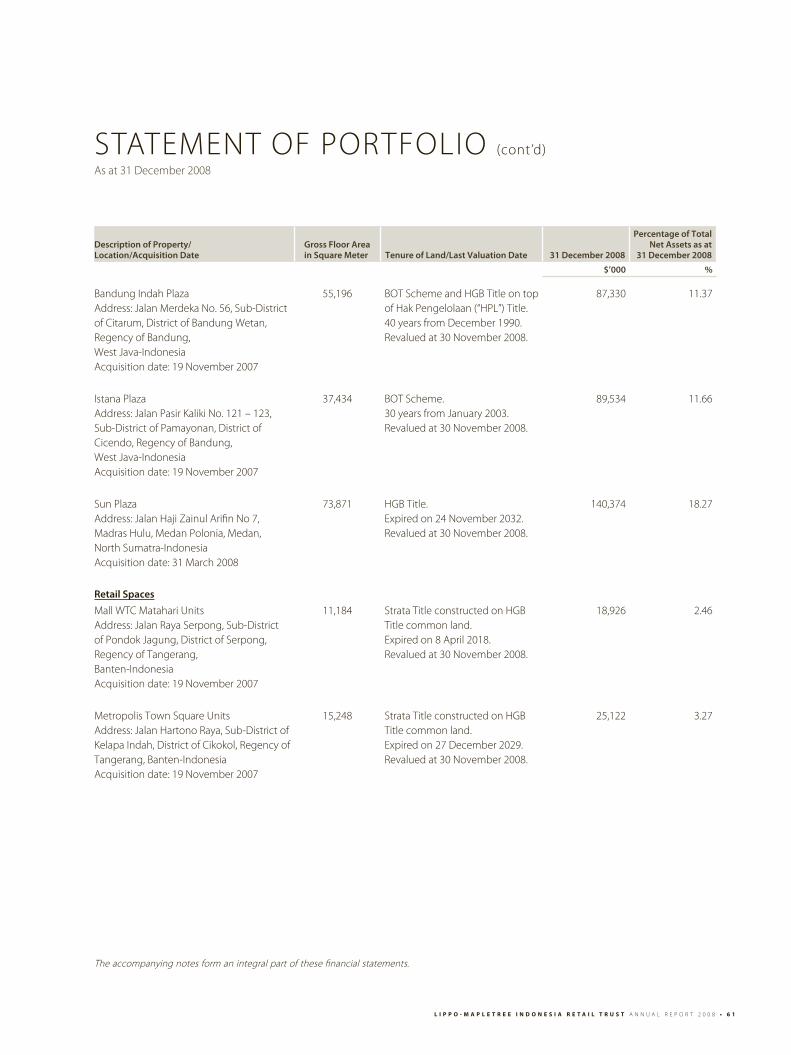

6 Bandung Indah plaza 19-nov-07 98.5 VictoriaInvestmentLtd 673,700 13,230,824 13% 30,231 40years,(expiringinDecember2030) Hypermart,MatahariDepartmentStore

7 Istana plaza 19-nov-07 94.3 MillenniumCapiatlLtd 690,700 10,084,681 10% 27,563 30years,(expiringinnovember2033) HeroSupermarket,RimoDepartmentStore

8 Sun plaza 31-Mar-08 144.8 HestiaInvestmentLimited, ZellwagerenterpriseLtd,QuebeccaCapitalLtd, SouthernTitanoInc,TroisInvestmentsLtd 1,082,900 12,058,345 12% 63,200 30years,(extendableuponexpiryin SogoDepartmentStore,Hypermart november2032)

retail Spaces

9 Mall WTC Matahari units 19-nov-07 20.8 TristarCapitalLtd. 146,000 1,890,270 2% 11,184 30years,(extendableuponexpiryinApril2018) PT.MatahariPutraPrimaTbk.

10 Metropolis Town Square units 19-nov-07 27.7 TristarCapitalLtd. 193,800 2,577,150 2% 15,248 30years,(extendableuponexpiryin PT.MatahariPutraPrimaTbk. December2029)

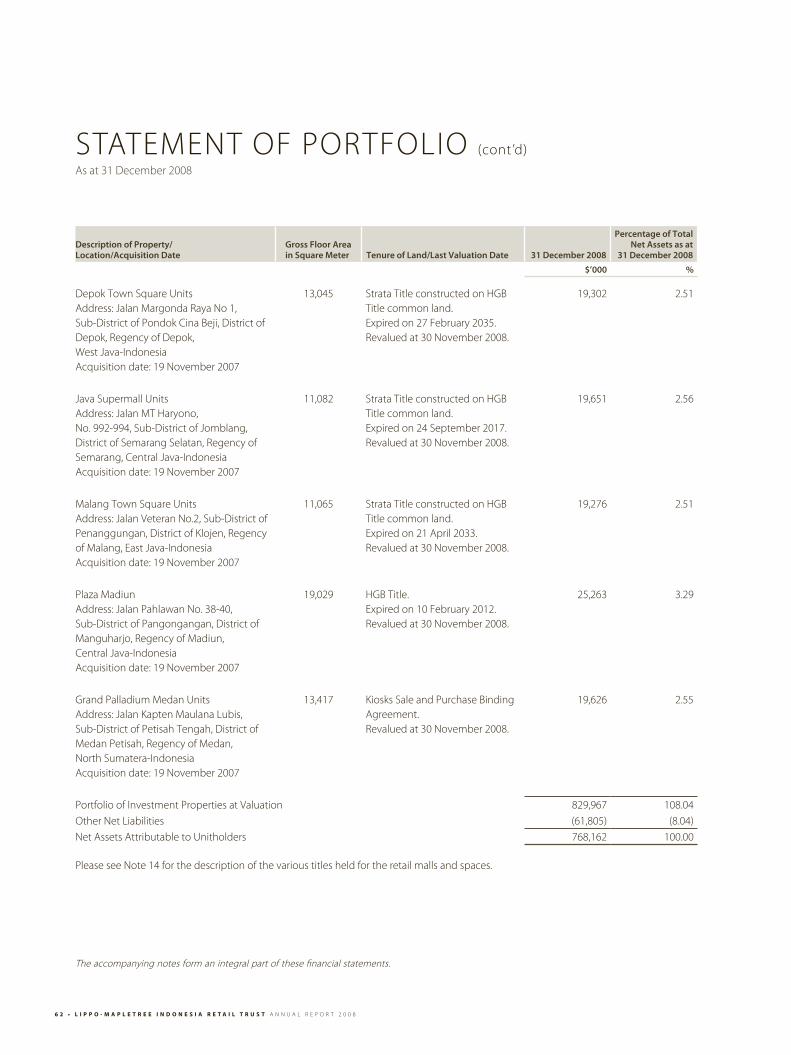

11 depok Town Square units 19-nov-07 21.2 TristarCapitalLtd. 148,900 1,929,207 2% 13,045 30years,(extendableuponexpiryin PT.MatahariPutraPrimaTbk. February2035)

12 Java Supermall units 19-nov-07 21.4 TristarCapitalLtd. 151,600 1,873,031 2% 11,082 30years,(extendableuponexpiryin PT.MatahariPutraPrimaTbk. September2017)

13 Malang Town Square units 19-nov-07 21.1 TristarCapitalLtd. 148,700 1,870,158 2% 11,065 30years,(extendableuponexpiryinApril2033) PT.MatahariPutraPrimaTbk.

14 plaza Madiun 19-nov-07 27.6 TristarCapitalLtd. 194,900 2,412,148 2% 19,029 30years,(extendableuponexpiryin PT.MatahariPutraPrimaTbk. February2012)

15 Grand palladium Medan units 19-nov-07 21.6 TristarCapitalLtd. 151,400 1,984,222 2% 13,417 Thestratatitlescertificatesareintheprocess PT.MatahariPutraPrimaTbk. ofbeingissuedbyIndonesialandoffice

Total or Weighted Average 927.6 6,402,700 Total: 101,761,021 100% 402,632

1 8 • L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8

PORTFOLIOSUMMARY

Gross revenue % purchase Valuation as at for the year of Total Acquisition price 30 Nov 2008 ended 31 dec Gross Lettable Land Title Term / Lease Title Term

No. property date (S$ million) Vendor (rupiah million) (S$) revenue Area (sqm) (Expiry of the tenure) Major Tenants / Lessee

retail Malls

1 Gajah Mada plaza 19-nov-07 77.9 DellmoreInvestmentLtd 612,100 8,933,298 9% 34,585 30years,(extendableuponexpiryin Hypermart,RimoDepartmentStore January2020)

2 Cibubur Junction 19-nov-07 74.8 MarketHoldingsLtd. 468,300 10,042,576 10% 34,139 20years,(expiringinJuly2025) Hypermart,MatahariDepartmentStore

3 The plaza Semanggi 19-nov-07 163.3 SuperiorAssetInvestmentLtd. 1,052,900 20,545,045 20% 64,516 50years(expiryinJuly2054) CentroDepartmentStore,GiantSuperstore

4 Mal Lippo Cikarang 19-nov-07 59.2 DellmoreInvestmentLtd 397,600 6,044,037 6% 28,705 30years,(extendableuponexpiryinMay2023) Hypermart,HeroSupermarket

5 Ekalokasari plaza 19-nov-07 53.7 GoldenAcresInvestmentLtd 289,200 6,286,028 6% 25,623 25years,(expiringinJune2032) MatahariDepartmentStore,Foodmart

6 Bandung Indah plaza 19-nov-07 98.5 VictoriaInvestmentLtd 673,700 13,230,824 13% 30,231 40years,(expiringinDecember2030) Hypermart,MatahariDepartmentStore

7 Istana plaza 19-nov-07 94.3 MillenniumCapiatlLtd 690,700 10,084,681 10% 27,563 30years,(expiringinnovember2033) HeroSupermarket,RimoDepartmentStore

8 Sun plaza 31-Mar-08 144.8 HestiaInvestmentLimited, ZellwagerenterpriseLtd,QuebeccaCapitalLtd, SouthernTitanoInc,TroisInvestmentsLtd 1,082,900 12,058,345 12% 63,200 30years,(extendableuponexpiryin SogoDepartmentStore,Hypermart november2032)

retail Spaces

9 Mall WTC Matahari units 19-nov-07 20.8 TristarCapitalLtd. 146,000 1,890,270 2% 11,184 30years,(extendableuponexpiryinApril2018) PT.MatahariPutraPrimaTbk.

10 Metropolis Town Square units 19-nov-07 27.7 TristarCapitalLtd. 193,800 2,577,150 2% 15,248 30years,(extendableuponexpiryin PT.MatahariPutraPrimaTbk. December2029)

11 depok Town Square units 19-nov-07 21.2 TristarCapitalLtd. 148,900 1,929,207 2% 13,045 30years,(extendableuponexpiryin PT.MatahariPutraPrimaTbk. February2035)

12 Java Supermall units 19-nov-07 21.4 TristarCapitalLtd. 151,600 1,873,031 2% 11,082 30years,(extendableuponexpiryin PT.MatahariPutraPrimaTbk. September2017)

13 Malang Town Square units 19-nov-07 21.1 TristarCapitalLtd. 148,700 1,870,158 2% 11,065 30years,(extendableuponexpiryinApril2033) PT.MatahariPutraPrimaTbk.

14 plaza Madiun 19-nov-07 27.6 TristarCapitalLtd. 194,900 2,412,148 2% 19,029 30years,(extendableuponexpiryin PT.MatahariPutraPrimaTbk. February2012)

15 Grand palladium Medan units 19-nov-07 21.6 TristarCapitalLtd. 151,400 1,984,222 2% 13,417 Thestratatitlescertificatesareintheprocess PT.MatahariPutraPrimaTbk. ofbeingissuedbyIndonesialandoffice

Total or Weighted Average 927.6 6,402,700 Total: 101,761,021 100% 402,632

L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8 • 1 9

2 0 • L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8

PORTFOLIOReVIeW-ReTAILMALLS

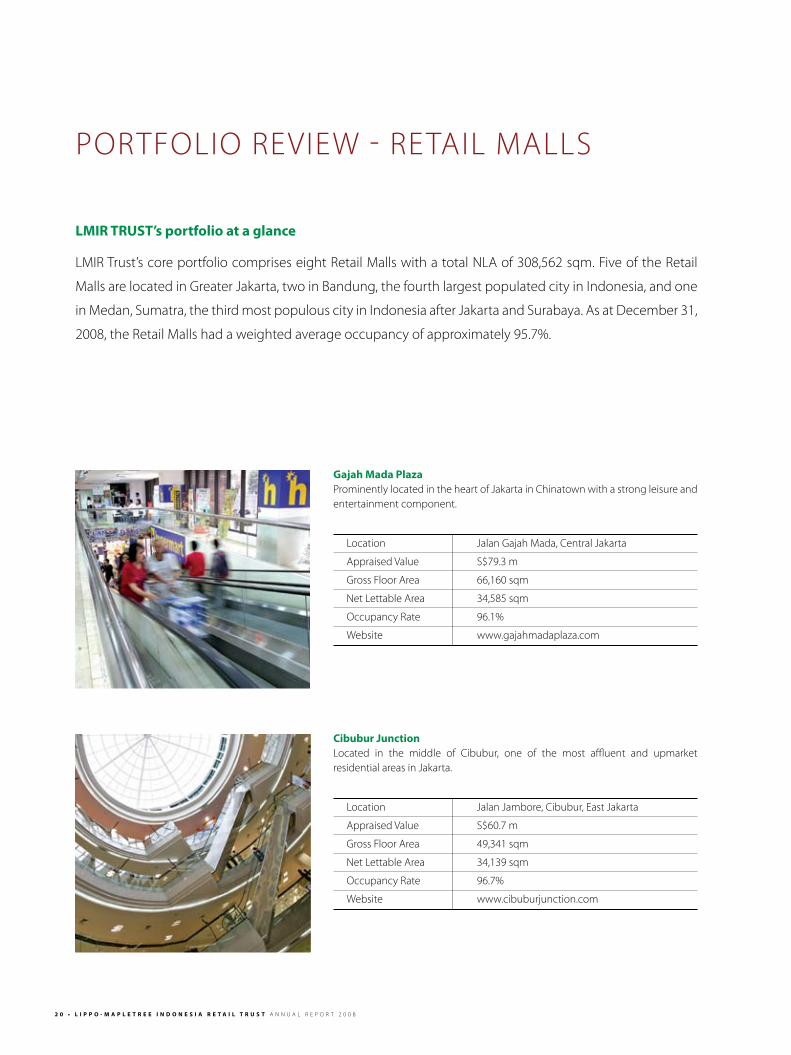

Gajah Mada plazaProminentlylocatedintheheartofJakartainChinatownwithastrongleisureandentertainmentcomponent.

Location JalanGajahMada,CentralJakarta

AppraisedValue S$79.3m

GrossFloorArea 66,160sqm

netLettableArea 34,585sqm

OccupancyRate 96.1%

Website www.gajahmadaplaza.com

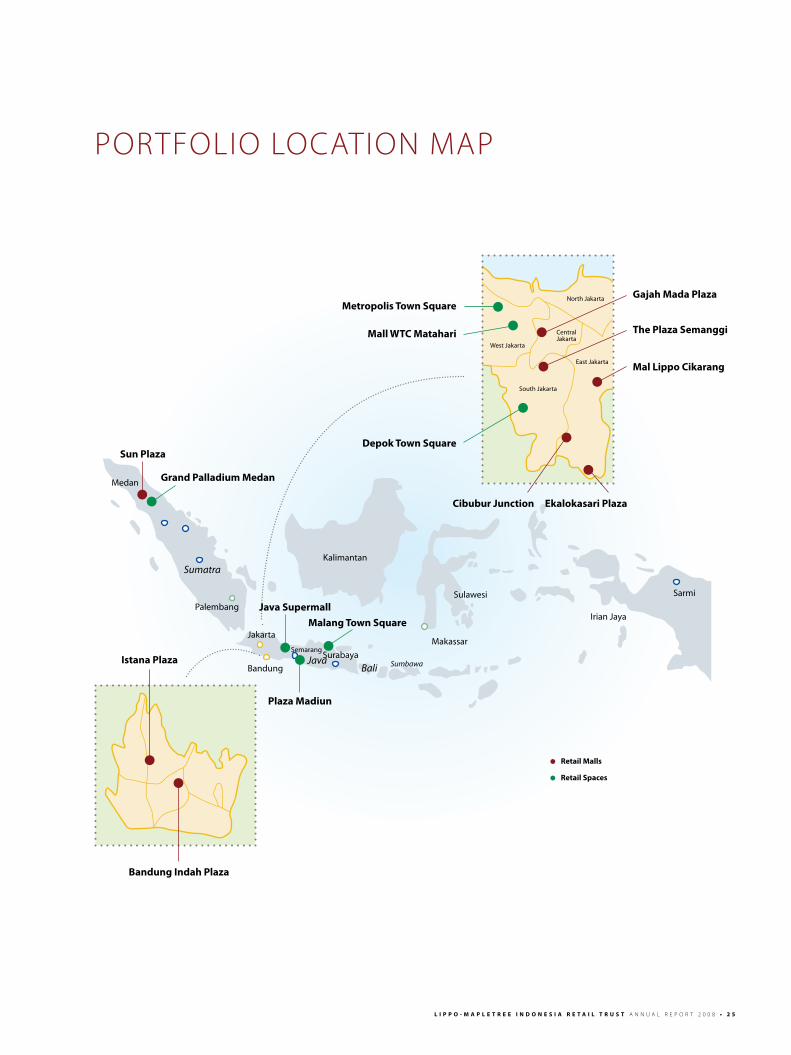

LMIr TruST’s portfolio at a glance

LMIRTrust’scoreportfoliocompriseseightRetailMallswithatotalnLAof308,562sqm.FiveoftheRetail

MallsarelocatedinGreaterJakarta,twoinBandung,thefourthlargestpopulatedcityinIndonesia,andone

inMedan,Sumatra,thethirdmostpopulouscityinIndonesiaafterJakartaandSurabaya.AsatDecember31,

2008,theRetailMallshadaweightedaverageoccupancyofapproximately95.7%.

Cibubur JunctionLocated in the middle of Cibubur, one of the most affluent and upmarketresidentialareasinJakarta.

Location JalanJambore,Cibubur,eastJakarta

AppraisedValue S$60.7m

GrossFloorArea 49,341sqm

netLettableArea 34,139sqm

OccupancyRate 96.7%

Website www.cibuburjunction.com

L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8 • 2 1

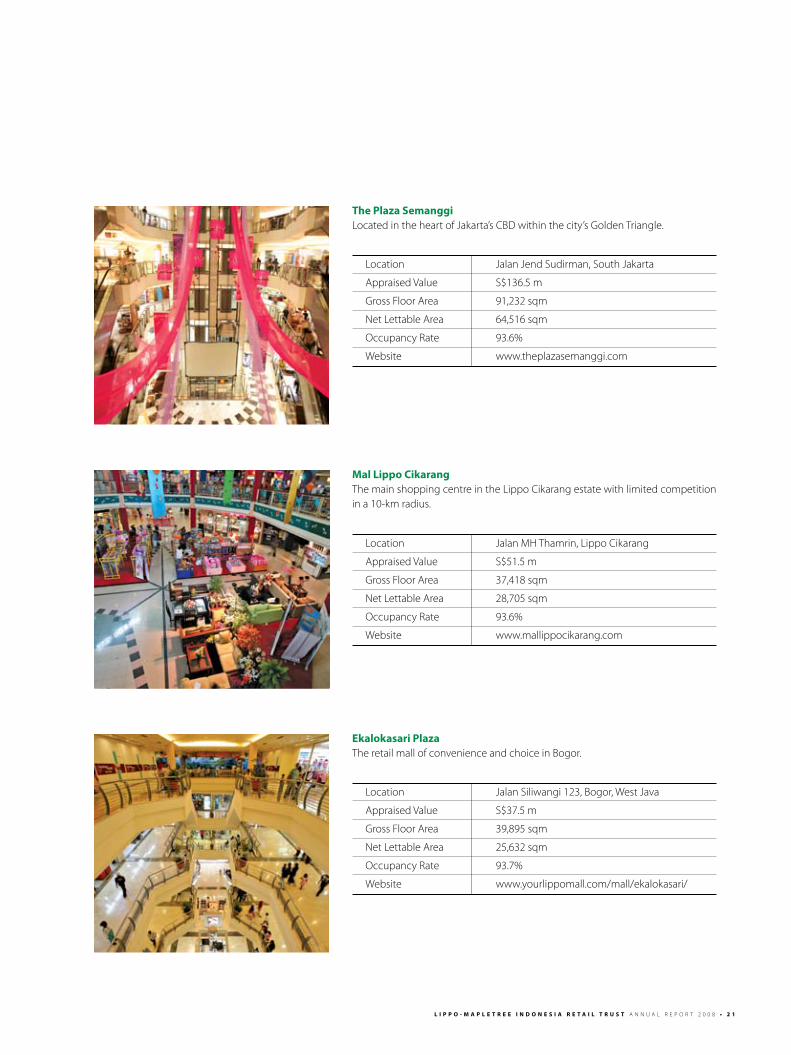

The plaza SemanggiLocatedintheheartofJakarta’sCBDwithinthecity’sGoldenTriangle.

Location JalanJendSudirman,SouthJakarta

AppraisedValue S$136.5m

GrossFloorArea 91,232sqm

netLettableArea 64,516sqm

OccupancyRate 93.6%

Website www.theplazasemanggi.com

Mal Lippo CikarangThemainshoppingcentreintheLippoCikarangestatewithlimitedcompetitionina10-kmradius.

Location JalanMHThamrin,LippoCikarang

AppraisedValue S$51.5m

GrossFloorArea 37,418sqm

netLettableArea 28,705sqm

OccupancyRate 93.6%

Website www.mallippocikarang.com

Ekalokasari plazaTheretailmallofconvenienceandchoiceinBogor.

Location JalanSiliwangi123,Bogor,WestJava

AppraisedValue S$37.5m

GrossFloorArea 39,895sqm

netLettableArea 25,632sqm

OccupancyRate 93.7%

Website www.yourlippomall.com/mall/ekalokasari/

2 2 • L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8

PORTFOLIOReVIeW-ReTAILMALLS(cont’d)

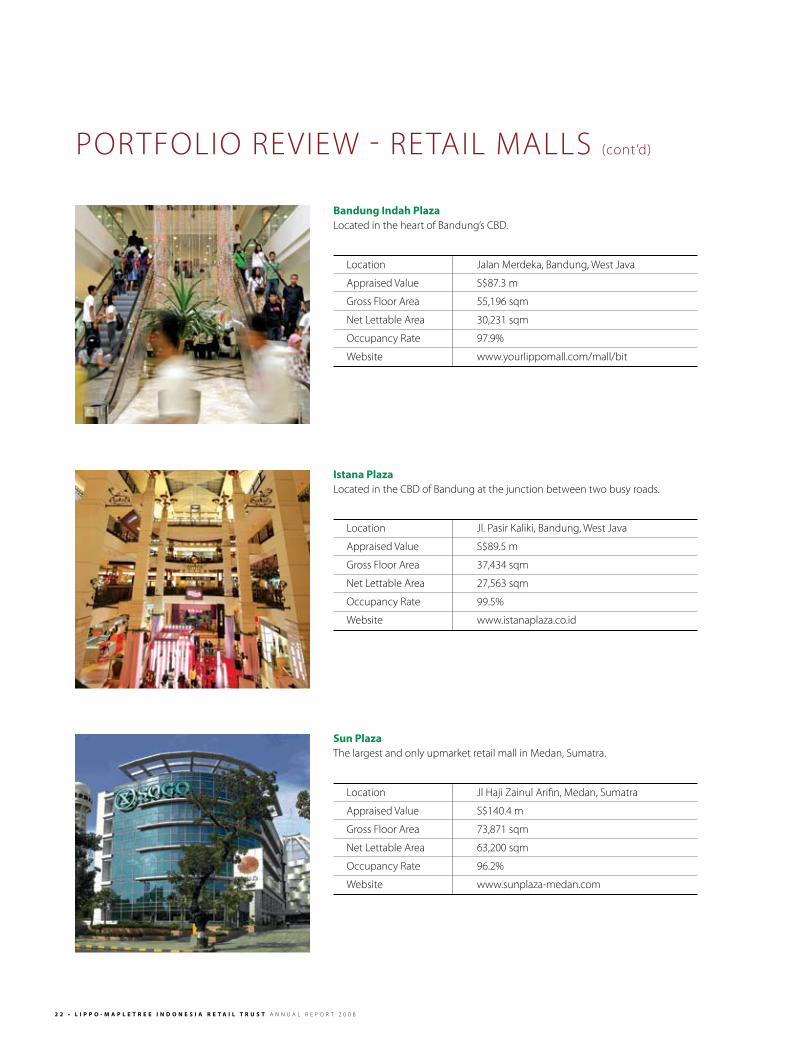

Istana plazaLocatedintheCBDofBandungatthejunctionbetweentwobusyroads.

Location Jl.PasirKaliki,Bandung,WestJava

AppraisedValue S$89.5m

GrossFloorArea 37,434sqm

netLettableArea 27,563sqm

OccupancyRate 99.5%

Website www.istanaplaza.co.id

Sun plazaThelargestandonlyupmarketretailmallinMedan,Sumatra.

Location JlHajiZainulArifin,Medan,Sumatra

AppraisedValue S$140.4m

GrossFloorArea 73,871sqm

netLettableArea 63,200sqm

OccupancyRate 96.2%

Website www.sunplaza-medan.com

Bandung Indah plazaLocatedintheheartofBandung’sCBD.

Location JalanMerdeka,Bandung,WestJava

AppraisedValue S$87.3m

GrossFloorArea 55,196sqm

netLettableArea 30,231sqm

OccupancyRate 97.9%

Website www.yourlippomall.com/mall/bit

PORTFOLIOReVIeW-ReTAILSPACeS

L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8 • 2 3

retail Spaces

TheRetailSpacesoccupyatotalnLAof94,070sqmandarestrategicallylocatedasanchorspaceswithin

retailmalls.ThreeofthesevenRetailSpacesarelocatedwithinGreaterJakartaandfouraresituatedinthe

majorcitiesofSemarang,Medan,MadiunandMalang.

Mall WTC Matahari unitsStrategicallylocatedonthemainroadconnectingtheBSDresidentialestate,thelargestresidentialestateinGreaterJakarta.

Location JalanRayaSerpong,Tangerang,GreaterJakarta

AppraisedValue S$18.9m

netLettableArea 11,184sqm

CurrentUtilisation Hypermart,MatahariDepartmentStoreandTimezone

OccupancyRate 100%

Website www.wtcmatahari.com

Metropolis Town Square unitsAone-stopshoppingmalllocatedalongoneofthemainroadsinTangerang.

Location JalanHartonoRaya,Tangerang,GreaterJakarta

AppraisedValue S$25.1m

netLettableArea 15,248sqm

CurrentUtilisation Hypermart,MatahariDepartmentStoreandTimezone

OccupancyRate 100%

Website www.metropolistownsquare.com

depok Town Square unitsDepokTown Square is located adjacent to the University of Indonesia and hasdirectaccesstoPondokCinarailwaystation.

Location JalanMargondaRaya,Depok,GreaterJakarta

AppraisedValue S$19.3m

netLettableArea 13,045sqm

CurrentUtilisation Hypermart,MatahariDepartmentStore,Timezone

OccupancyRate 100%

Website www.depoktownsquare.com

2 4 • L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8

PORTFOLIOReVIeW-ReTAILSPACeS(cont’d)

Java Supermall unitsLocatedinSemarang,capitalofCentralJavaprovinceandthefifthlargestcityintermsofpopulationinIndonesia.

Location JalanMTHaryono,Semarang,CentralJava

AppraisedValue S$19.7m

netLettableArea 11,082sqm

CurrentUtilisation MatahariDepartmentStoreandFoodmartsupermarket

OccupancyRate 100%

Website -

Malang Town Square unitsConceptualised as an international lifestyle mall, the biggest and mostcomprehensivemallinMalang.

Location JalanVeteran,Malang,eastJava

AppraisedValue S$19.3m

netLettableArea 11,065sqm

CurrentUtilisation Hypermart,MatahariDepartmentStore,Timezone

OccupancyRate 100%

Website -

plaza MadiunThebiggestmallinMadiun,locatedonPahlawanStreet,amajorroadofthecity.

Location JalanPahlawan,Madiun,eastJava

AppraisedValue S$25.3m

netLettableArea 19,029sqm

CurrentUtilisation MatahariDepartmentStoreandFoodmartsupermarket

OccupancyRate 100%

Website -

Grand palladium Medan unitsLocated within the Medan CBD and surrounded by government and businessofficesandthetownhall.

Location Jl.Kapt.MaulanaLubis,Medan,northSumatra

AppraisedValue S$19.6m

netLettableArea 13,417sqm

CurrentUtilisation Departmentstore,hypermarket,entertainmentandgamecentre

OccupancyRate 100%

Website www.thegrandpalladium.com

L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8 • 2 5

PORTFOLIOLOCATIOnMAP

Grand palladium Medan

plaza Madiun

Sumatra

Bandung

Semarang

JavaSurabayaBali Sumbawa

Sulawesi

Makassar

Irian Jaya

Sarmi

Istana plaza

Bandung Indah plaza

• retail Malls

• retail Spaces

Malang Town SquareJava SupermallPalembang

Jakarta

Kalimantan

Metropolis Town Square

Mall WTC Matahari

depok Town Square

Gajah Mada plaza

The plaza Semanggi

Mal Lippo Cikarang

Cibubur Junction Ekalokasari plaza

West Jakarta

North Jakarta

Central Jakarta

East Jakarta

South Jakarta

Sun plaza

Medan

rEACHING OuT TO CuSTOMErS Strategic asset enhancement initiatives have

extended the NLA of existing malls and added

highly appealing retail concepts that increased

shopper traffic. LMIr Trust will continually

undertake innovative marketing strategies and

active tenant remixing to enhance its properties’

appeal as one-stop destination malls for its

valued customers.

Groceries shopping at our hypermart. Bandung Indah Plaza.

2 8 • L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8

MARKeTRePORT

retail Sector SupplyAmidst the uncertainty of the global crisis whereworldwide retailers announced their businesscontraction, two shopping centers were launchedtakingtheopportunityofyear-endholidays.PejatenVillage belong to Lippo Group and Blok M Squareinitiated by Agung Podomoro Group were thetwo shopping centers that were introduced, bothcomprising a total retail space of around 83,000sq m. Total retail space in Jakarta accounted for3.46millionsqmofwhicharound496,708sqmofretail space only entered in 2008, historically thesecondhighestannualsupplysince2005.Jakartaisstill perceived as an interesting market for retailershighlighted by the progress of under-constructionshoppingcenterswhichwillcometothemarketin

thenearfuturelikeSeasonsCity,PulomasPlace,KojaTradeMallandemporiumPluit.Supplyprojectionin2009 isquiteoptimisticwith retail spaceofaround465,000sqminthepipeline.Besidestheshoppingcenters mentioned above, other centers projectedtocomeon-streamin2009includetheextensionofPlazaIndonesia,GajahMadaSquareandCitiwalkatGajahMada.Meanwhile,AgungPodomoroGroupastheownerofCentralParkcompoundinJalanLetjenS.Parmanannouncedthattheshoppingmallwillbereadybytheendofthisyear.Yet,notalltheunder-constructionshoppingcenterswillarriveonschedule.Again,thecurrentfinancialcrisishasalsoimpactedonsome commercial compounds under construction.KotaKasablankaandtheshoppingmallatGandariahaveputtheirconstructionprogressonhold.Othernew projects in the CBD area were monitoredtocontinuewithprogressbutataslowerpace.

1 3Q08.2 January - December 2008.3 December 2008.

Economics Indicators

Indonesian Economic Indicator

2004 2005 2006 2007 2008

economicGrowth(%YoY) 5.00 5.70 5.50 6.30 6.301

InflationRate(%) 6.40 17.11 6.60 6.59 11.062

exchangeRate(Rp/US$) 8,934 9,695 8,9800 9,124 9,6722

InterestRate-CentralBankRate(%) 7.40 12.75 9.75 8.000 9.253

(Source: Statistics Indonesia, Finance Department, Bank Indonesia).

Other future projects in the DeBoTaBek

area include Tangerang City with sizeable

space of around 50,000 sq m; Mall

Harapan Indah and Alam Sutera Mall.

Cafe Walk at Plaza Semanggi.

L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8 • 2 9

InthegreaterJakartaareaswhichcompriseDepok,Bogor, Tangerang and Bekasi (DeBoTaBek), CityMal Tangerang has been partially operated at theend of December with the opening of Giant as itsanchor tenant. Meanwhile, Taman Topi Square, orabbreviatedasTatos,inBogorhasyettooperateeventhough,asmonitored in thefield, theconstructionhasbeencompleted.Thus,withthe influxof thosetwo shopping centers, the greater Jakarta areareceivedadditionalretailspacewhichaccumulatedtoaround1.72millionsqm.

OtherfutureprojectsintheDeBoTaBekareaincludeTangerangCitywithsizeablespaceofaround50,000sqm;MallHarapanIndahandAlamSuteraMall.Thesethree projects would contribute around 154,420sq m of retail space in 2009 and 2010. TangerangCity will prioritize the shophouse developmentbeforestartingwiththeshoppingcenter.BothMallHarapanIndahandAlamSuteraMallarescheduledtooperatein2010.

Cumulative retail Supply In Jakarta

Source: Colliers International Indonesia - Research Department.

• for lease • for strata-title sale

3,500,000

3,000,000

2,500,000

2,000,000

1,500,000

1,000,000

500,000

02001 2002 2003 2004 2005 2006 2007 1Q08 2Q08 3Q08 4Q08 2009F 2010F

3 0 • L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8

MARKeTRePORT(cont’d)

List Of under Construction retail Centers

In Jakarta

Marketing Expectedretail Name Location Scheme Completion

SeasonsCity Latumenten forStrata-titleSale 2009

PulomasPlace Pulomas forLease 2009

KojaTradeMall Koja forStrata-titleSale 2009

CityWalkatGajahMada GajahMada forLease 2009

PusatGrosirSenenJaya Senen forStrata-titleSale 2009

Rasunaepicentrum(emperiumWalk) RasunaSaid forLease 2009

CentralParkMall S.Parman forLease 2009

PlazaIndonesia(extension) MHThamrin forLease 2009

GrandParagon(GajahMadaSquare) GajahMada forLease 2009

KuninganCity Satrio forLease 2010

KotaKasablanka Kasablanka forLease 2010

ShoppingMallGandaria Gandaria forLease 2010

KernangVillage Kemang forLease 2010

MTHaryonoSquare Otista forStrata-titleSale 2010

CiputraWorld Satrio forLease 2010

Total Space 747,643 sq m

Teraskota Tangerang forLease 2010

MallHarapanIndah Bekasi forLease 2010

TangerangCity Tangerang forStrata-titleSale 2010

AlamSuteraMall Tangerang forLease 2010

Total Space 191,660 sq m

Source: Colliers International Indonesia - Research Department.

L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8 • 3 1

demandQuite a few retailers reported that there was atendencyofdecliningsaleswhencomparedtothesame period last year. Retailers are more cautiouswith relatively weakening purchasing powerfollowing thecurrenteconomicdownturn.Despitenegative sentiment on the current economicsituation,premiumclassbrandsarerelativelystable,in particular those with steady customers. Marks& Spencer, a British-based fashion retailer, cameto Plaza Indonesia while Harvey nicholls enteredGrandIndonesia.PlazaIndonesiawiththeextensionspace of around 35,000 sq m has reported a highcommitment level by various tenants. For someyears,premiummallswhichhavebeentheshoppingdestinationsof loyalandwilling-to-spendshoppersenjoyhighoccupancyandpremiumrentalrates.Ontheotherhand,middletoupperclassretailersprefertooptfortheoperatingmallswithloyalshopperstoassuretheirmarket.

newly operated shopping centers still rely onhypermarkets as the anchor tenant. PejatenVillagesecured Hypermart which is still their own group,while Blok M Square is flanked by Carrefour as theanchor. Other main tenants within the two mallsinclude Matahari as the second anchor for PejatenVillage. Matahari was also present in the shoppingcenters like in Pluit Village (previously known asMegamall Pluit) which was taken over by LippoGroup.InthePluitVillage,Matahariintroducedanewconceptwherebytheycombinedentertainment/lifemusicconceptwithinthestore.Besides,thecorridorswere designed to be bigger than other Mataharioutletstofacilitatethevisitors.ApartfromCarrefourastheanchor,BlokMSquarehassecuredtenantslikeRamayana,BreadTalk,SolariaandHokaHokaBento

On a positive note, despite the weaker marketsentiments,someretailersarestilleyeingIndonesiaas a potential market. South Korea’s Lotte GroupofficiallyacquiredwholesalerMakro,anetherlands-based retailer which has 19 stores in Indonesia, inacquisition worth US$223 million. Other than that,US-based convenience store, 7-eleven announcedits tie-up with Modern Group to enter the market.It is also reported that Lion Superindo, owned bySalim Group, plans to open eight more stores in

2009. Carrefour has been reported to expand withfour stores in 2009 itself. Further to that, Indonesiawith a population of more than 200 million is stillperceived as a lucrative market by Tesco, a UK-basedhypermarketwhichplans toopenoutlets inIndonesiabetween2010-2011.

Theoveralloccupancyrate inJakartawasrelativelystableinthisquarter,standingat88.14%.Theoverallincomingandoutgoingtenantswerequitebalanced,evenwiththeopeningoftwonewshoppingcentersthis quarter.Throughout 2008, the occupancy ratehoveredataround88%.Mostvacantspacegenerallycame from strata-title retail centers (trade centers).InthegreaterJakartaareatheoccupancyrateeasedslightlyto83.29%.

Despiteshowingsignsofbeingabletowithstandtheeconomicstorm,therearelikelysomevictimswithinthis tough time like high-end branded retailerswhose expensive goods will go stale on the shelf.We anticipate a decline in branded sales in 2009.Singapore which has been a mature retail market,for the first ten months of the year had reportedthat retail sales had also grown at a significantlyslower pace of 2.3% YoY compared to the 8.4%growth recorded during the corresponding periodin 2007 (according to a research done by ColliersInternationalSingapore).

3 2 • L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8

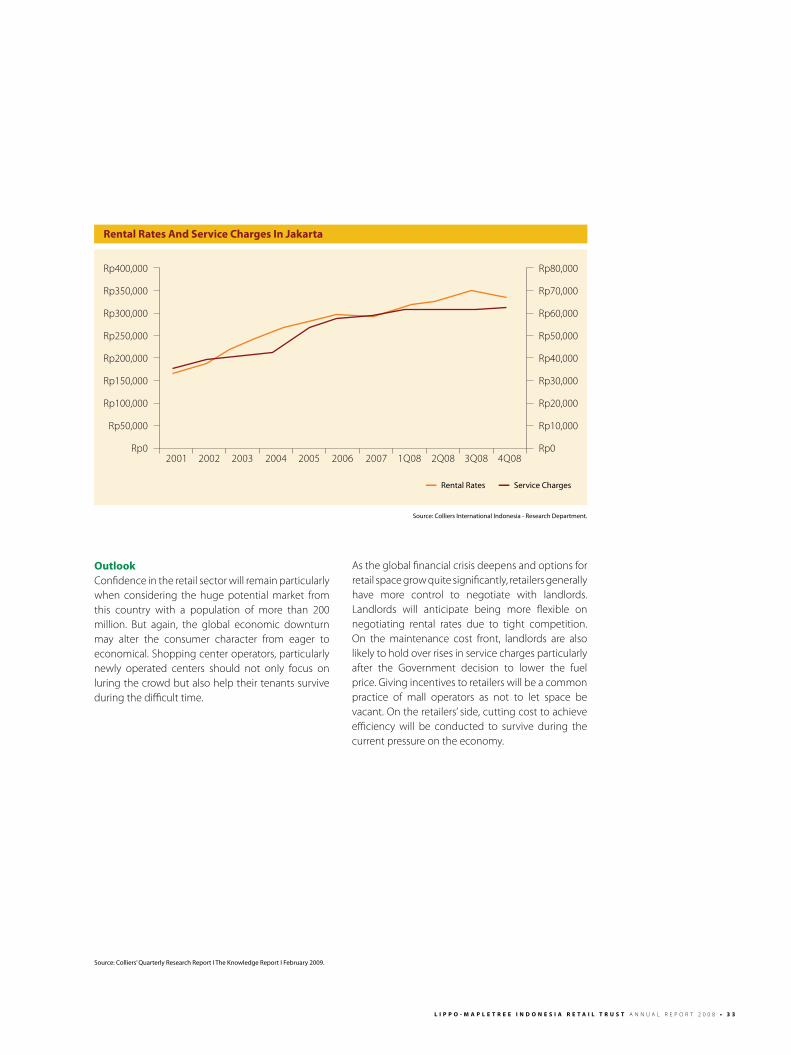

MARKeTRePORT(cont’d)

Asking rental rates And Service ChargesAsking Rental RatesOnaverage,therentalratesinthequarterdroppedby 5 to 6% but this is mostly not because ofadjustments made by landlords. Average askingrentalrateswasdownfromRp354,253/sqm/monthtoRp338,150/sqm/monthin4Q08.ThediscrepancyinQoQrentalrateswasmostlyduetotheavailabilityof retailspaces, forexamplespacesavailable intheprevious quarter were largely of higher rates whilespaces available within this quarter were of lowerrates.Manydevelopersarenowtakingthepositionofnot increasing the rental ratesamid theslowingbusinessenvironmentandtightmarketcompetition.Themeasureofloweringtherentalrateswilldependalotonthelevelofvacantspace.

Shopping malls of premium class maintained thesame asking price as in the previous quarter. Onlythree malls i.e. Plaza Indonesia, Plaza Senayanand eX Plaza offered US$ rates. Other centers mayhave offered US$ rate but pegged at lower thanthe current rate. The average pegged rates withinthe quarter slightly increased to Rp7,176/US$ fromRp7,140/US$afteranupwardadjustmentmadebyLaPiazzabyRp250andDaanMogotMallbyRp500.

In the DeBoTaBek area, a minor downwardadjustment of 5% was recorded for the averageaskingrentalrateswhichstoodatRp259,174/sqm/month.Againtheloweringrateismostlyduetotheavailabilityofspacewithlowerratesascomparedtothepreviousquarter.noneoftheshoppingcentersquotingUS$rateswithinthisareausedthecurrentexchangerates,instead,theaveragepeggedrateforthisareamaintainedatRp6,938/US$.

Service ChargesTherewasnegligibleadjustmentintheservicechargefor the quarter and this maintained the averageservicechargecostatRp62,685/sqm/month.Duringthequarterweonlyrecordedanupwardadjustmentof around 30% by three shopping centers likeTendean Plaza, Ratu Plaza and ITC Cempaka Mas.Othershoppingcenters likeMallKelapaGading,LaPiazza,CitralandMallandDaanMogotMall revisedthepeggedrateswhichcorrectedtheoverallservicechargecost.

There was no revision in the service charge in thegreaterJakartaarea.Thisquarter,theaverageservicechargecostmaintainedrelativelystableatRp52,656/sqm/month.

Cumulative Supply, demand And Occupancy rate

Source: Colliers International Indonesia - Research Department.

• Cumulative Supply (sq m) • Cumulative Demand (sq m) – Occupancy (%)

3,500,000

2,800,000

2,100,000

1,400,000

700,000

02001 2002 2003 2004 2005 2006 2007 2008

100%

80%

60%

40%

20%

0%

L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8 • 3 3

OutlookConfidenceintheretailsectorwillremainparticularlywhen considering the huge potential market fromthis country with a population of more than 200million. But again, the global economic downturnmay alter the consumer character from eager toeconomical.Shoppingcenteroperators,particularlynewly operated centers should not only focus onluringthecrowdbutalsohelptheirtenantssurviveduringthedifficulttime.

Astheglobalfinancialcrisisdeepensandoptionsforretailspacegrowquitesignificantly,retailersgenerallyhave more control to negotiate with landlords.Landlords will anticipate being more flexible onnegotiating rental rates due to tight competition.On the maintenance cost front, landlords are alsolikelytoholdoverrisesinservicechargesparticularlyafter the Government decision to lower the fuelprice.Givingincentivestoretailerswillbeacommonpractice of mall operators as not to let space bevacant.Ontheretailers’side,cuttingcosttoachieveefficiency will be conducted to survive during thecurrentpressureontheeconomy.

rental rates And Service Charges In Jakarta

Source: Colliers International Indonesia - Research Department.

– Rental Rates – Service Charges

Rp400,000

Rp350,000

Rp300,000

Rp250,000

Rp200,000

Rp150,000

Rp100,000

Rp50,000

Rp02001 2002 2003 2004 2005 2006

Rp80,000

Rp70,000

Rp60,000

Rp50,000

Rp40,000

Rp30,000

Rp20,000

Rp10,000

Rp02007 1Q08 2Q08 3Q08 4Q08

Source: Colliers’ Quarterly Research Report I The Knowledge Report I February 2009.

3 4 • L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8

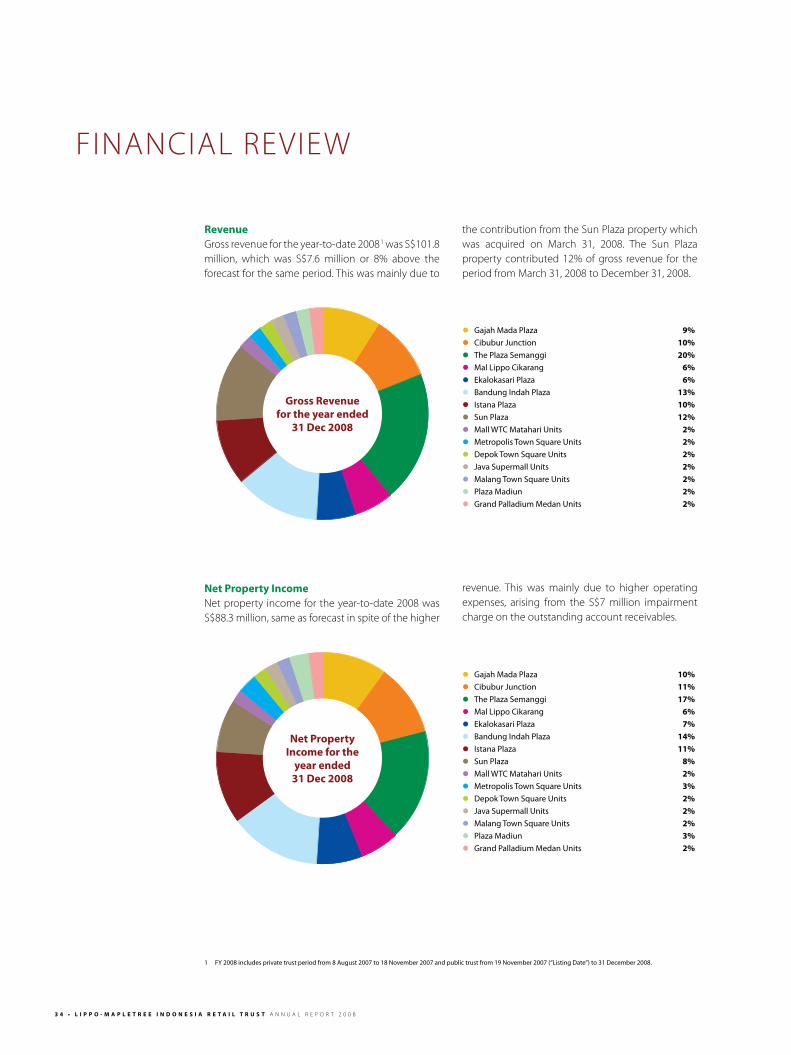

FInAnCIALReVIeW

revenueGrossrevenuefortheyear-to-date20081wasS$101.8million, which was S$7.6 million or 8% above theforecastforthesameperiod.Thiswasmainlydueto

Gross revenue for the year ended

31 dec 2008

• Gajah Mada Plaza 9%

• Cibubur Junction 10%

• The Plaza Semanggi 20%

• Mal Lippo Cikarang 6%

• Ekalokasari Plaza 6%

• Bandung Indah Plaza 13%

• Istana Plaza 10%

• Sun Plaza 12%

• Mall WTC Matahari Units 2%

• Metropolis Town Square Units 2%

• Depok Town Square Units 2%

• Java Supermall Units 2%

• Malang Town Square Units 2%

• Plaza Madiun 2%

• Grand Palladium Medan Units 2%

thecontributionfromtheSunPlazapropertywhichwas acquired on March 31, 2008. The Sun Plazaproperty contributed 12% of gross revenue for theperiodfromMarch31,2008toDecember31,2008.

Net property Income for the

year ended 31 dec 2008

• Gajah Mada Plaza 10%

• Cibubur Junction 11%

• The Plaza Semanggi 17%

• Mal Lippo Cikarang 6%

• Ekalokasari Plaza 7%

• Bandung Indah Plaza 14%

• Istana Plaza 11%

• Sun Plaza 8%

• Mall WTC Matahari Units 2%

• Metropolis Town Square Units 3%

• Depok Town Square Units 2%

• Java Supermall Units 2%

• Malang Town Square Units 2%

• Plaza Madiun 3%

• Grand Palladium Medan Units 2%

Net property Incomenetpropertyincomefortheyear-to-date2008wasS$88.3million,sameasforecastinspiteofthehigher

revenue. This was mainly due to higher operatingexpenses, arising from the S$7 million impairmentchargeontheoutstandingaccountreceivables.

1 FY 2008 includes private trust period from 8 August 2007 to 18 November 2007 and public trust from 19 November 2007 (“Listing Date”) to 31 December 2008.

L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8 • 3 5

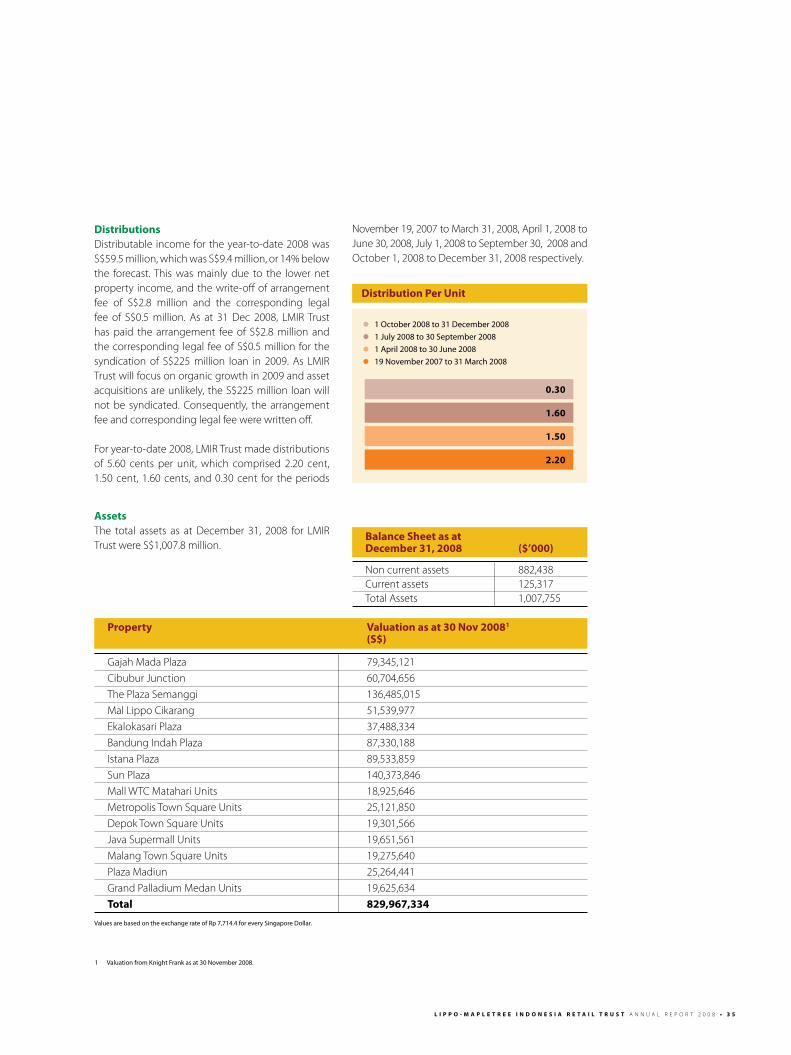

distributionsDistributable incomefortheyear-to-date2008wasS$59.5million,whichwasS$9.4million,or14%belowthe forecast.This was mainly due to the lower netproperty income,andthewrite-offofarrangementfee of S$2.8 million and the corresponding legalfee of S$0.5 million. As at 31 Dec 2008, LMIRTrusthas paid the arrangement fee of S$2.8 million andthecorresponding legal feeofS$0.5millionforthesyndication of S$225 million loan in 2009. As LMIRTrustwillfocusonorganicgrowthin2009andassetacquisitionsareunlikely,theS$225millionloanwillnot be syndicated. Consequently, the arrangementfeeandcorrespondinglegalfeewerewrittenoff.

Foryear-to-date2008,LMIRTrustmadedistributionsof 5.60 cents per unit, which comprised 2.20 cent,1.50cent,1.60cents, and0.30cent for theperiods

AssetsThe total assets as at December 31, 2008 for LMIRTrustwereS$1,007.8million.

1 Valuation from Knight Frank as at 30 November 2008.

• 1 October 2008 to 31 December 2008

• 1 July 2008 to 30 September 2008

• 1 April 2008 to 30 June 2008

• 19 November 2007 to 31 March 2008

distribution per unit

2.20

1.50

1.60

0.30

november19,2007toMarch31,2008,April1,2008toJune30,2008,July1,2008toSeptember30,2008andOctober1,2008toDecember31,2008respectively.

Balance Sheet as at december 31, 2008 ($’000)

noncurrentassets 882,438Currentassets 125,317TotalAssets 1,007,755

Values are based on the exchange rate of Rp 7,714.4 for every Singapore Dollar.

property Valuation as at 30 Nov 20081

(S$)

GajahMadaPlaza 79,345,121CibuburJunction 60,704,656ThePlazaSemanggi 136,485,015MalLippoCikarang 51,539,977ekalokasariPlaza 37,488,334BandungIndahPlaza 87,330,188IstanaPlaza 89,533,859SunPlaza 140,373,846MallWTCMatahariUnits 18,925,646MetropolisTownSquareUnits 25,121,850DepokTownSquareUnits 19,301,566JavaSupermallUnits 19,651,561MalangTownSquareUnits 19,275,640PlazaMadiun 25,264,441GrandPalladiumMedanUnits 19,625,634Total 829,967,334

3 6 • L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8

CAPITALMAnAGeMenT

A prudent capital management strategyTheManagerpursuesaprudentcapitalmanagementstrategy through adopting and maintaining anappropriate gearing level and using an activecurrencyandinterestratemanagementpolicy.

Thisstrategywill:• Optimiseunitholder’sreturns;• Providestablereturnstounitholders;• Maintainflexibilityforworkingandcapital requirements;and• Retainflexibilityinthefundingof futureacquisitions.

100% of loan at fixed interest rateInMarch2008,LMIRTrustdrewdownaS$125million5 year loan for the acquisition of the Sun Plazaproperty.

Thisloanwasfullyhedgedfortheinterestrateriskfor3 year through entering into an interest rate swap,whichfixedtheall-inannualcostofdebtat6.42%.Fixinginterestratehelpstoprotectoverallearningsfrom short term volatility in interest rates. TheManager will continue to work towards deliveringstable and growing returns through sourcingattractivelypricedcapitalandadoptingappropriatehedgingstrategies.

Low gearing level provides stability in current tight credit marketUnder the Property Fund Guidelines, a ReIT isgenerally permitted to borrow up to 35.0% of thevalueofitsDepositedProperty(oruptoamaximumof60.0%ifacreditratingisobtainedanddisclosedtothepublic).

LMIRTrustgearingasat31December2008is12.4%,waybelowthepermitted35%.AsfornowLMIRTrustdoes not intend to make any acquisition. ShouldLMIRTrustintendtomakeanyacquisition,LMIRTrustwillhavesubstantialabilitytoincurindebtednesstofundfutureacquisitions.Ourcurrenttargetgearinglevelisbelow35%onaconsolidatedbasis.debt highlights as at 31 december 2008

Loan $125M

Total debt $ 125 M

Gearingratio1 12.4%

Fixedratedebt 100%

Weightedaverageinterestrate 6.42%p.a.

1 Based on deposited property as defined in trust deed.

L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8 • 3 7

RISKMAnAGeMenT

Risk Management Framework The Manager has developed a comprehensive riskmanagement framework that enables the Boardand Audit committee (“AC”) to review the risksarising from LMIR Trust’s portfolio of assets fromquartertoquarteronaconsistentandsystematicbasis.

The frameworkquantifieskeyproperty-relatedriskssuch as occupancy and rental rates, credit-relatedrisks and financial market risks, including counter-party risks, foreign currency exposure and interestratevolatility.Tenantandindustryconcentrationrisksarealsomonitoredaspartoftheriskframework.

The risk framework is supplemented bycomprehensive and robust internal processes andprocedures that are formalized in the ManagerOrganizational and Reporting Structures, StandardOperating Procedures and Delegation of Authorityguidelines. These cover significant strategic,operationalandfinancialrisks.

The overall risk framework is managed by theManager who reports to the Board and AC on aquarterlybasis.

The internal audit function of the Manager willbe outsourced to a third party. KPMG, who hasbeen appointed, will plan its internal audit workin consultation with management, but worksindependentlybysubmitting itsplantotheACforapprovalatthebeginningofeachyear.

risk Management StrategyProperty,financialmarket,operationalandstrategicrisks and other externalities such as regulatorychanges,naturaldisastersandactofterrorismoccurinthenormalcourseofbusiness.TheManager’sriskmanagementstrategyenablesustobettermanagetheserisksastheyarise.

TheManager’sriskmanagementstrategyisalignedwith its overall business objectives which aim tobalancerisksandreturns inordertooptimizeLMIRTrust’sportfoliovaluesandreturns.

Someofthekeyrisksfacedandhowthesearebeingmonitoredandmanagedaredetailedbelow:

Operational RiskThe Manager has established risk managementstrategy into the day-to-day activities across allfunctions. These include planning and controlsystems, operational guidelines, informationtechnologies systems, reporting and monitoringprocedures.Theriskmanagementsystemisregularlymonitoredandexaminedtoensureeffectiveness.

The risk management framework is designed toensurethatoperationalrisksareanticipatedsothatappropriateprocessesandprocedurescanbeputinplacetoprevent,manage,andmitigateriskswhichmay arise in the management and operation ofLMIRTrust.

Investment Risk As LMIR Trust’s growth is driven by acquisition ofproperties, the risk involved in such investmentactivities is managed through a rigorous set ofinvestment criteria which includes accretionyield, growth potential and sustainability, locationand specifications. The key financial projectionassumptions and sensitivity analysis conducted onkeyvariablesarereviewedbytheBoard.

The potential risks associated with proposedprojects and the issues that may prevent theirsmoothimplementationorprojectedoutcomesareidentifiedattheevaluationstage.Thisenablesustodetermineactionsthatneedtobetakentomanageormitigaterisksasearlyaspossible.

Interest Rate RiskWith the current tight credit market, the Managerwill adopt a proactive strategy to manage the riskassociated with changes in interest rates on anyfutureloanfacilitieswhilealsoseekingtoensurethatLMIR Trust’s ongoing cost of debt capital remainscompetitive.Asat31December2008,100%ofLMIRTrustborrowingshadbeenlockedintofixedinterestrate,throughenteringintointerestrateswapwhichhedgetheexposuretointerestraterisksarisingfromthefloatinginterestrateloan.

3 8 • L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8

RISKMAnAGeMenT(cont’d)

Foreign Exchange RiskLMIR Trust will be subject to foreign exchangeexposure due to changes in foreign exchangerates arising from foreign currency transactionsand balances and changes in fair values from itsinvestmentinIndonesia.ThevalueoftheIndonesianRupiahhasbeensubjecttofluctuationsinthepastandmaybesubjecttofluctuationinthefuture.TheManagerhasapolicytoundertakeforeignexchangehedging of the expected distributions of LMIRTrust to insulate against movements in exchangerates (whether favourable or unfavourable). TheTrustee, as trustee of LMIR Trust, has entered intoforeign exchange hedges equivalent to 100% ofLMIRTrust’sestimateddistributionsforatotaltermof five years, effective as of the Listing Date, andthereafterwillcontinuouslyhedgeonarollingbasissoastoprovideadegreeofcertaintytoUnitholdersthat changes in the exchange rate between theIndonesian Rupiah and the Singapore dollar willnothaveasignificantimpactonthedistributionsinSingaporetoUnitholders.

Credit Risk Creditriskisthepotentialearningsvolatilitycausedby tenants’ inability and/or unwillingness to fulfilltheircontractual leaseobligations.Tominimisetheriskoftenantdefaultonrentalpayment,themanagerhas put in place standard operating proceduresfor debt collection and recovery of debts. Otherthan the collection of security deposits, whichamount to a minimum of three months rental inthe form of cash or bankers guarantee, we alsohaveamonitoring systemanda setofproceduresondebtcollection.

Liquidity Risk The Manager actively monitors LMIR Trust’s cashflow position so as to ensure sufficient liquidreserves terms of cash and credit facilities to meetshorttermobligations.Inaddition,theManageralsoobserves and monitors compliance with the Codeon Collective Investment Schemes issued by theMonetaryAuthorityofSingaporetogovernlimitsontotalborrowings.

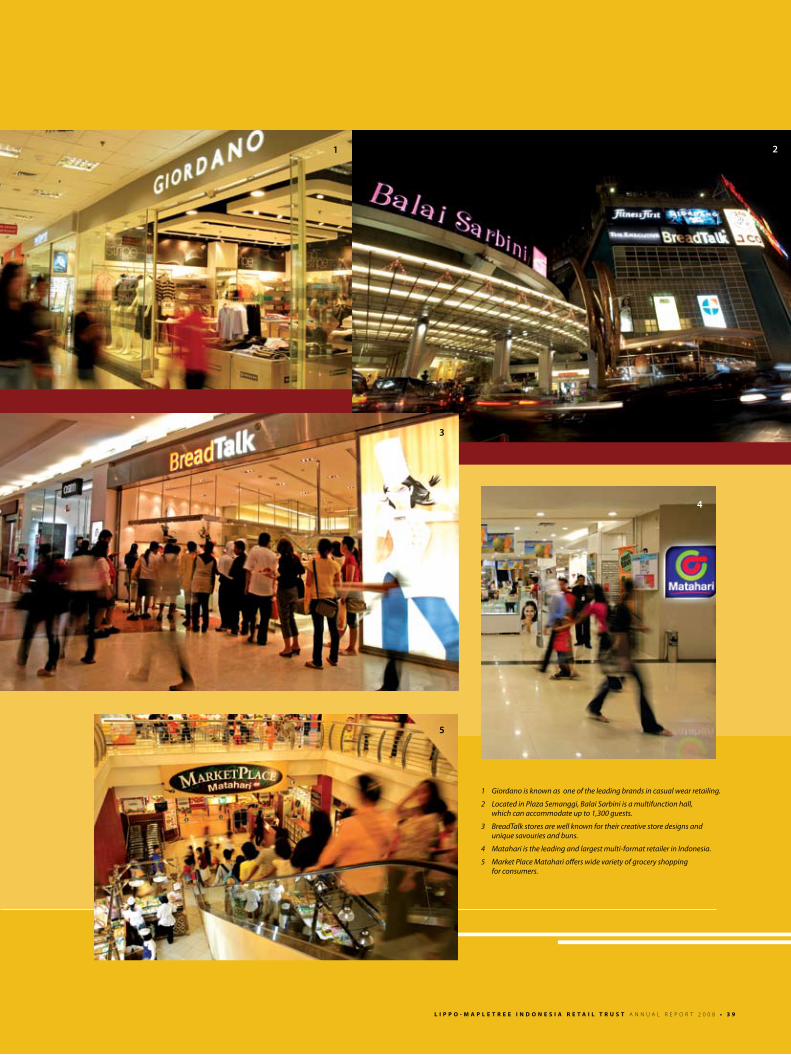

1 Giordano is known as one of the leading brands in casual wear retailing.

2 Located in Plaza Semanggi, Balai Sarbini is a multifunction hall, which can accommodate up to 1,300 guests.

3 BreadTalk stores are well known for their creative store designs and unique savouries and buns.

4 Matahari is the leading and largest multi-format retailer in Indonesia.

5 Market Place Matahari offers wide variety of grocery shopping for consumers.

L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8 • 3 9

1 2

3

4

5

4 0 • L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8

OPeRATIOnReVIeW

Yield Accretive AcquisitionsOn March 31, 2008 LMIR Trust acquired Sun Plaza,oneof thebest shoppingcentres inMedan,northSumatra. At a purchase price of Rp9801 billion(approximatelyS$146.7million)2, theacquisitionwasLMIR Trust’s first since its listing on the Singaporeexchange Securities Trading Limited (“SGX-ST”) innovember2007andincreasedLMIRTrust’sIPOtotalportfolionLAbyapproximately20%.

With a population of over two million, Medan isthe third most populous city in Indonesia (afterJakartaandSurabaya)andcapital cityof thenorthSumatran province. Sun Plaza is a six-level retailmall strategically located in Medan’s commercialdistrict,surroundedbyprominentlandmarksaswellas government and business offices, including thegovernor’soffice,embassiesandmajorbanks,withconvenient accessibility from all parts of Medancity.TheacquisitionofSunPlazahasincreasedLMIRTrust’s presence in Medan, adding to the MatahariretailspacewhichitownsinGrandPalladium.

Builtonalandareaof29,419sqm,withagrossfloorarea of approximately 73,871 sqm and net lettablearea(“nLA”)of63,200sqm,SunPlazawasvaluedatRp1.1trillionbyindependentvaluerKnightFrank/PTWilsonPropertiAdvisindoinnovember2008.

Theacquisitionwas funded20%with internalcashresources and 80% with debt, drawing down fromaS$125milliontermloanfacilityatanall-incostof6.42%p.a.

ThelandonwhichthePropertyisbuiltisheldunderIndonesianHakGunaBangunan(RighttoBuild)titlewhich is valid until november 24, 2032. The HGBTitle is the highest title that can be obtained by acompany incorporated or located in Indonesia. AHGBtitleisgrantedforamaximuminitialtermof30years and may be extended for an additional termnotexceeding20years.Followingexpirationoftheadditional term, a renewal application for the titlemaybemade.

Key Asset Enhancement Initiatives Assetenhancementinitiatives(AeI)wereakeyfocusfortheportfolioduringtheperiodunderreview.ThefollowingisanupdateonsomeoftheAeIundertakenatLMIRTrust’sproperties.

At ekalokasari Plaza in Bogor, asset enhancementworks increased nLA by 5,013 sqm to 25,600 sqmthroughanewlycreatedareathatincludescinema,foodcourt,andgymnasium,andachieveda93.7%occupancyrateasatDecember31,2008.

1 Based on the exchange rate of S$1.00 = RP . 6,682 as at 31 March 2008.2 Purchase price of Singapore Companies which own the Indonesian Company which wholly own the Sun Plaza.

Household shopping at our hypermart.Ekalokasari Plaza.

L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8 • 4 1

Theyearalsowitnessed theopeningofPlangiSky.DiningatThePlazaSemanggi,whichincreasednLAby3,000sqmto61,685sqminFebruary2008.PlangiSkyDiningisanopenairconceptspecialtyfoodandbeverageareaonthe10thfloorwhichhasbecomea landmark dining destination in South Jakarta,offeringawidevarietyofcafeteria-styleoutlets.Themallreached93.6%occupancyrateasatDecember31,2008.

AtIstanaPlazainWestJava,planstoconvertanexistingice skating rink into new cafeterias and restaurantsandanexpandedfoodcourtareproceedingwhere653 sqm of nLA will be converted from the 950sqmproposedareaatestimatedcostsofS$434,000.TargetROIfromthisassetenhancementisexpectedtobeabove30%(netoflossincome),Themallhasa99.5%occupancyrateasatDecember31,2008.

portfolio Lease Expiry profileThe average lease term of LMIR Trust’s tenantsis line with the industry average, with specialtytenants typically on a three-to-five-year averagelease term and anchor tenants on a 10-yearaverageleaseterm.Over30%ofthetenants’ leasesare long-term, extending to 2013 and beyond.Thelargestnumberofleasesdueforrenewalswillbein2013.

LMIRTrust’stenantstypicallypayanadvancerentalofapproximately10%to20%ofthetotalrentpayableforthedurationoftheleaseuponsigningofaleaseagreement. This advance rental payment helps tominimise LMIR Trust’s cash flow volatility due topotentialrentalarrears.

Plangi Sky Dining is an open air concept specialty

food and beverage area on the 10th floor which

has become a landmark dining destination in

South Jakarta, offering a wide variety of cafeteria-

style outlets.

Plangi sky dining.

portfolio Lease Expiry profile

60.0%

50.0%

40.0%

30.0%

20.0%

10.0%

0.0%2009

%ofnLA

2010 2011 2012 2013beyond

11.8%7.6% 8.3% 8.9%

53.3%

OPeRATIOnReVIeW(cont’d)

4 2 • L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8

Average occupancy of LMIRTrust’s malls increasedfrom92.8%asatDecember31,2007to95.7%asatDecember 31, 2008, significantly higher comparedto industry average of 84.6%. The high averageoccupancy combined with its long lease expiryprofileensuresstabilityofincomeforLMIRTrust.

portfolio Income and Trade Sector AnalysisThe retail malls has well-balanced tenantdiversification with no particular trade sectoraccounting formore than17%ofLMIRTrust’s totalnLA,aswellaswidepropertydiversificationwithno

single property accounting for more than 21% ofLMIRTrust’stotalnetpropertyincome,

Top tenants include well-known international anddomesticretailersandbrandnames,suchasMatahariDepartment Store, Hypermart, Giant Hypermarket,Gramedia bookstore, Starbucks, Giordano, FitnessFirst,SportsStationandStudio21Cinema.

Department stores were the largest contributor tonetPropertyIncomeandoccupiedthemostspaceat 17.0% of nLA. Supermarkets and hypermarketswerethesecondlargestcontributortonetPropertyIncomeandoccupied14.0%ofthetotalportfolionLA.Thisindicatesthatthekeysourcesofincomefortheretailmallsarefromtenantsinnon-cyclicalbusinesseswhich draw “everyday” middle-income shoppersandarelessvulnerabletotheeconomicslowdown.

Tenant remixing To Enhance rental IncomeIn order to increase shopper traffic, the Managercontinually undertakes active tenant remixing andseeking to place both locally and internationally-renowned“favourite”specialtybrandstoenhanceitsproperties’appealas“everyday”one-stopdestinationmalls for both discretionary and non-discretionaryconsumer spending. In FY2008, the Managerexperienced upward rental reversions within itsprojections.

Weighted Average Occupancy

Actual Actual prospectus forecast dec 07 dec 08 dec 08 No. Malls (%) (%) (%)

1 BandungIndahPlaza 85.3 97.9 91.9

2 CibuburJunction 93.8 96.7 98.6

3 ekalokasariPlaza 78.0 93.7 91.4

4 GajahMadaPlaza 94.5 96.1 95.9

5 IstanaPlaza 99.4 99.5 99.4

6 MalLippoCikarang 96.1 93.6 98.5

7 ThePlazaSemanggi 96.8 93.6 98.4

8 SunPlaza - 96.2 93.5

LMIr Trust Average 92.8 95.7 96.7

Industry Average 84.6%*

* Cushman & Wakefield, Indonesia Q3 Market Review.

ThaiExpress Restaurant at Istana Plaza.

L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8 • 4 3

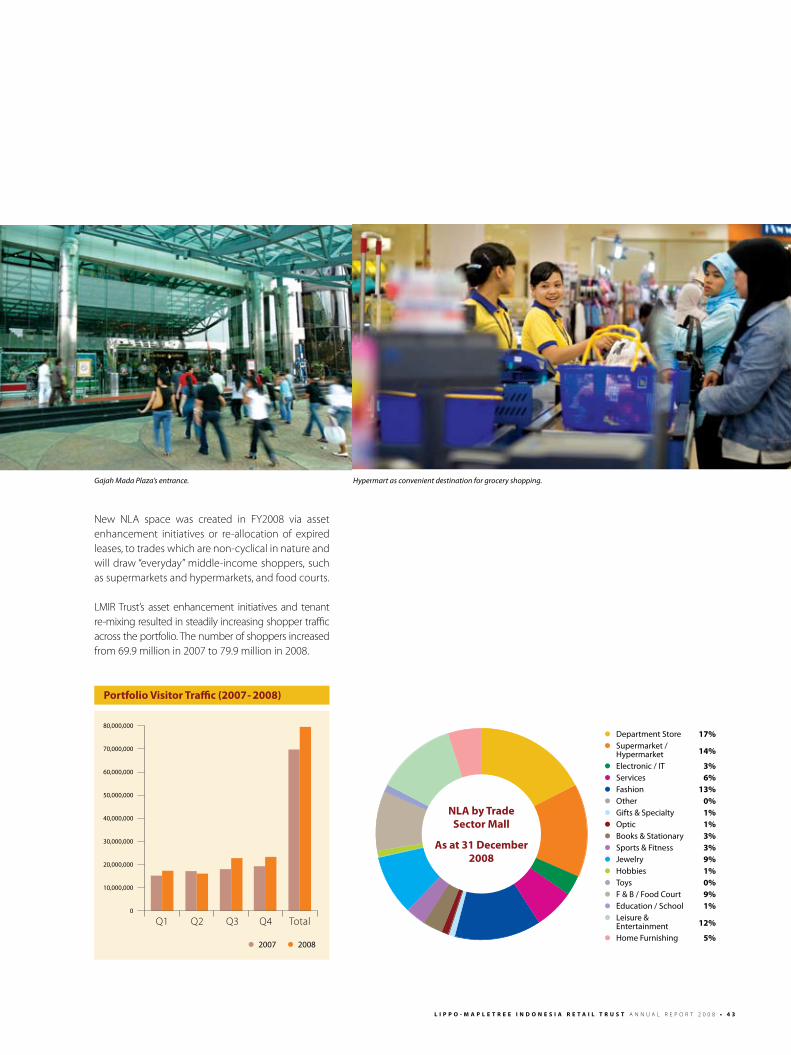

new nLA space was created in FY2008 via assetenhancement initiatives or re-allocation of expiredleases,totradeswhicharenon-cyclicalinnatureandwilldraw“everyday”middle-incomeshoppers,suchassupermarketsandhypermarkets,andfoodcourts.

LMIRTrust’s asset enhancement initiatives and tenantre-mixingresultedinsteadilyincreasingshoppertrafficacrosstheportfolio.Thenumberofshoppersincreasedfrom69.9millionin2007to79.9millionin2008.

NLA by Trade Sector Mall

As at 31 december 2008

• Department Store 17%

• Supermarket / Hypermarket 14%

• Electronic / IT 3%

• Services 6%

• Fashion 13%

• Other 0%

• Gifts & Specialty 1%

• Optic 1%

• Books & Stationary 3%

• Sports & Fitness 3%

• Jewelry 9%

• Hobbies 1%

• Toys 0%

• F & B / Food Court 9%

• Education / School 1%

• Leisure & Entertainment 12%

• Home Furnishing 5%

portfolio Visitor Traffic (2007- 2008)

• 2007 • 2008

80,000,000

70,000,000

60,000,000

50,000,000

40,000,000

30,000,000

20,000,000

10,000,000

0

Q1 Q2 Q3 Q4 Total

Hypermart as convenient destination for grocery shopping.Gajah Mada Plaza’s entrance.

4 4 • L I p p O - M A p L E T r E E I N d O N E S I A r E T A I L T r u S T A n n U A L R e P O R T 2 0 0 8

InVeSTORReLATIOnS&COMMUnICATIOnS

LMIR Trust believes in and practices clear,transparent and consistent investor relations andcommunications practices to disclose pertinentinformation relevant to all stakeholders. For eachquarterlyresultsannouncement,LMIRTrustpreparesinvestor relations packs comprising news releases,and presentation slides highlighting materialinformationonitsfinancialresults,portfolioandassetperformance,marketupdatesandrelevantpropertysector reports. As and when there are significantcorporate developments, such as managementchangesandchangesinshareholdingstructure,theannouncementsarereleasedwithimmediateeffectviaSGX-STinatimelymanner. AllannouncementsarealsomadeavailableonLMIRTrust’swebsite.

Regularone-on-onemeetingsareheldwithanalystsand institutional investors upon the release ofLMIR Trust’s quarterly results and/or the release ofannouncements pertaining to material corporatedevelopments.Atthesemeetings,themanagementteamwillbepresenttoaddressanyqueryorconcernregardingtheseannouncements. Inaddition,uponrequest, conducted toursofLMIRTrust’spropertiescanbearrangedforkeyinstitutionalinvestorstogivethem a first-hand view of LMIRTrust’s high qualityportfolioofproperties.

This annual report marks LMIR Trust’s first officialpublication of its maiden full-year financial yearresults after its initial public offering on the SGX.Going forward, LMIR Trust strives to proactivelyenhanceitsdisclosurestandardsthatwillensureclearand consistent communication to all stakeholdersandtheinvestingpublic.

uNITHOLdEr ENQuIrIESFormoreinformationonLippoMapletreeIndonesiaRetailTrustanditsoperations,pleasecontact:

Financial Calendar

2008 2009 (Tentative)

InterimPeriodResultsAnnouncement April2008 April2009

InterimPeriodDistributiontoUnitholders May2008 May2009

SecondQuarterResultsAnnouncement July2008 July2009

SecondQuarterDistributiontoUnitholders August2008 August2009

ThirdQuarterResultsAnnouncement October2008 October2009

ThirdQuarterDistributiontoUnitholders november2008 november2009

FullYearResultsAnnouncement January2009 January2010

FinalDistributiontoUnitholders February2009 February2010

Lippo Mapletree Indonesia retail Trust Management Ltd78ShentonWay#05-01Singapore079120Tel : +6564109138Fax : +6562206557email : [email protected] : http://www.lmir-trust.com

unitholder depositoryFor depository-related matters such as change ofdetailspertainingtoUnitholder’sinvestmentrecords,pleasecontact:

BoardroomCorporate&AdvisorServicesPteLtd3ChurchStreet#08-01SamsungHubSingapore049483

L i p p o - M a p L e t r e e i n d o n e s i a r e t a i L t r u s t a n n u a l r e p o r t 2 0 0 8 • 4 5

Corporate GoVernanCe

Corporate GoVernanCelippo-Mapletree Indonesia retail trust Management ltd, (the “Manager”) of lippo-Mapletree Indonesia retail trust (lMIr trust) is committed to good corporate governance as it believes that such self-regulatory are essential to protect the interest of the unitholders, as well as critical to the performance of the Manager.

the Manager uses the Code of Corporate Governance (the “Code”) as its benchmark for its corporate governance policies and practices. the following segments describe the Manager’s main corporate governance policies and practices.

tHe ManaGer oF LMir trustthe Manager has general powers of the management over the assets of lMIr trust.

the Manager’s main responsibility is to manage lMIr trust’s assets and liabilities for the benefit of unitholders. the Manager’s key financial objectives is to provide unitholders of lMIr trust with a competitive rate of return for their investment by ensuring regular and stable distributions to unitholders and to achieve long-term growth in net asset value of lMIr trust.

the primary role of the Manager is to set strategic direction and risk management of lMIr trust and give recommendations to HSBC Institutional trust Services (Singapore) limited, as trustee of lMIr trust (the “trustee”), on the acquisition, divestment and enhancement of assets of lMIr trust in accordance with its stated investment strategy.