Evaluation and future of road toll concessions Presented by PricewaterhouseCoopers Advisory S.p.A. to ASECAP 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Evaluation and future of road toll concessions

Presented byPricewaterhouseCoopers Advisory S.p.A. to ASECAP

2014

Table of Contents

1 Introduction 5 1.1 Aim of the Study 5 1.2 Sources of information 5 1.3 Structure of the Study 5

2 Description of the typical toll concession scheme 7 2.1 What is a road toll concession 7

3 Description of the ASECAP network 10 3.1 Presentation of ASECAP 10 3.2 Concession models applied to networks operated by ASECAP members 11 3.3 Value added of the road toll concession 22 3.4 Conclusions 38

4 Issues and Risks 40 4.1 Risk allocation between Concession Authority and Concessionaire 40 4.2 Unforeseeneventsaffectingriskallocation 45 4.3 Aspectsaffectingsocialacceptabilityoftollsystems 49 4.4 Casesofevolutions/divergencesintheinterpretationofthecontracts 50 4.5 Conclusions 52

5 Forms of funding 54 5.1 Alternativeformsofroadtolling 54 5.2 OverviewofthefinancialinstrumentstosupporttransportinfrastructureinEurope 59 5.3 Conclusions 62

6 TheEuropeanlegislativeframeworkaffectingtheconcessionsector 64 6.1 EUlegislativeinitiativesinthetransportsector 64 6.2 Stateaidlegislation 69 6.3 Conclusions 70

7 Conclusions and recommendations 71 7.1 Advantagesofroadtollconcessionscheme 71 7.2 Recommendations 72

Annexes 73AnnexI.Applicationofthedirective1999/62/ECintheASECAPmembers’network 73Annex II List of sources 75

Evaluation and future of road toll concessions / Final Report // 3

Key figures*

“ The Concession Model represents the most flexible tool to finance, build and manage road infrastructure ”

26 billion Toll revenues

187Companies

48.265,01Km in operation

27.346ETC lanes

26.660.884ETC subscribers

*Source: ASECAP 2014 Statistical Bulletin

Evaluation and future of road toll concessions / Final Report 4 //

1. Introduction

1.1 Aim of the Study

In a fragmented context characterized by a largenumberofEUinitiativesthatmightaffectthetolledroad concession schemes, the aim of the study is:

• to clarify what a road concession is, •shedmorelightonissuesconcerningconces-

sions as well as bottlenecks for the develop-ment of road infrastructures,

•highlightthebenefitsoftheconcessionsche-mesandtheconditionsforensuringtheirpro-per implementation across Europe.

1.2 Sources of information

TheStudyisbasedondataandinformationgathe-red through desk research and a performancesurvey.

Thedeskresearchinparticularanalyzedandcom-pared several sources to allow a full and coherent overview of toll concession schemes in Europe. These sources are:

• Reports and publications from ASECAP and from its members,

• Data and statistics elaborated by relevant ins-titutions (for a full list of sources see Annex 3),

• Further input from interventions, feedbacks and discussions on specific matters whichtookplaceduringtheAthensASECAPStudyDays (26-28 May 2014).

In addition to the desk research, in March 2014, a Performance survey was addressed to all ASECAP

memberstogatherallno-publiclyavailableinforma-tionrelatedtotollsystemsandconcessionregimes.More in detail, the Performance survey aimed at obtaining an overview and an exhaustive unders-tandingofthetopicsregardingtollroadconcessioncontractsand it gatheredopinions,bestpracticesand recommendations on future development of concession schemes in European countries.

1.3 Structure of the Study

ThisHandbookconsistsofthefollowingchapters:• Chapter 2 provides a description of the typical concessionmodeldefiningitsmainfeaturesandprovidingadefinitionbothatEuropeanlevelandat ASECAP member level.• Chapter 3 providesageneral overviewof theconcession models applied to networks ope-rated by ASECAPmembers (i.e. national legalframework, the obligations of the Concessio-naireandthefinancialaspectsrelatedtotollingmechanisms). This section also provides data andinformationwithregardtotheperformanceof the motorway network in concession (i.e. length of network built, toll equipment, trafficvolumes and safety) and considerations about the socio economic relevance of toll concession schemesatlocalandregionallevel.• Chapter 4isaimedatprovidingaclearunders-tanding of the issues and risks endangering acorrect application of the road concession tool through the assessment of possible impactsspecificsituationsmighthaveontheconcessionschemes.

Evaluation and future of road toll concessions / Final Report // 5

1. Introduction

• Chapter 5isaimedatdepictingthealternativeforms of funding (i.e. direct tolling, indirecttollingandshadowtolling)andatintroducingthe existing financial instruments to supporttransport infrastructure in Europe.

• Chapter 6 is aimed at providing the legisla-tive framework at European level with direct or indirect impacts on road toll concession models. In particular, this section describes thelegislationinforcewithregardtothepast,recent and upcoming EU legislative initia-tives relevant for the development of the road toll sector.

• Chapter 7 isaimedatprovidingconcreteele-ments and recommendations to support the concession model as the most flexible toolfor constructing,maintaining and operating anetworkforagivenperiod.

• Annex I provides an overview of the implemen-tationoftheEurovignettesysteminASECAPmembers’network.

• Annex II provides the questionnaire formatlaunched in the context of the Performance Survey 2014.

• Annex III provides the list of relevant sources investigatedinthecontextofthedeskanalysis.

Evaluation and future of road toll concessions / Final Report 6 //

2 Description of the typical toll concession scheme

Nowadays governments are constantly lookingfor ways to develop their road networks and other transport links tomeet citizenseconomic,politicaland social needs. New motorways are expensive and governments are often unable or unwilling tocommit fiscal spending on roads. The scarcity ofpublic resourceshasbrought to theapplicationofnewmodels for thefinancingandmanagementoftolled roads, ranging from thecollectionof tolls tothe recourse toprivate financeviamore “sophisti-cated”concessionmodels.EachmodelenvisagesadifferentlinkbetweentheState-whichistheownerof the road network - and the Company - which has to carry out the roadmanagement and operationactivities.

At the European level, nowadays such link can have differentprofiles:

• Road toll concession scheme;•DirectcontrolbytheState(byspecificAgen-

cies as well);• Public-Private Companies.

2.1 What is a road toll concession

In general, a concession is a kind of public–pri-vate partnership (PPP) under which a public au-thority (Concession Authority) grants specific longtermrightstoaprivateorsemi-publicorganisation(Concessionaire), to construct, overhaul, maintain and operate an infrastructure. On the basis of the agreementbetweenagovernmentoritsentitiesandaprivate firm, theConcessionaire iscommitted touse all utility assets conferred and has the responsi-bility for all operations and investments, while asset ownership remains with the authority and the assets revert to the authority at the end of the concession period.

In the context of a concession agreement, theConcessionaire typically obtains its revenues direc-

tly from the consumer in the form of a toll and/or from the public authority in the form of payments calculated on the basis of the traffic observed onthe motorway.

Three mechanisms for obtaining revenues areavailable:

1. Direct road tolling: the public authority dele-gates the construction, funding and mana-gement of a road to a managing company,which carries out the work at its expenses. The company collects tolls from the users (dis-tance-basedcharge)toreimbursetheinvest-ment and to cover maintenance costs (see alsoparagraph5.1.1).

2. Indirect road tolling: the public authority dele-gatestheconstruction,fundingandmanage-mentofaroadtoamanagingcompany,whichcarries out the work at its expenses. Users pay a toll to the public authority, usually on the basisofa“vignette”(time-basedcharge).Theoperator is remunerated by the public autho-rity, typically on the basis of availability pay-ments(seealsoparagraph5.1.2).

3. Shadow toll system: the public authority dele-gatestheconstruction,fundingandmanage-mentofaroadtoamanagingcompany.Thecompany collects no toll from the users, for whom the infrastructure is free (see also para-graph5.1.3).Thecompanyisdirectlyremune-ratedbythepublicawardingauthority.

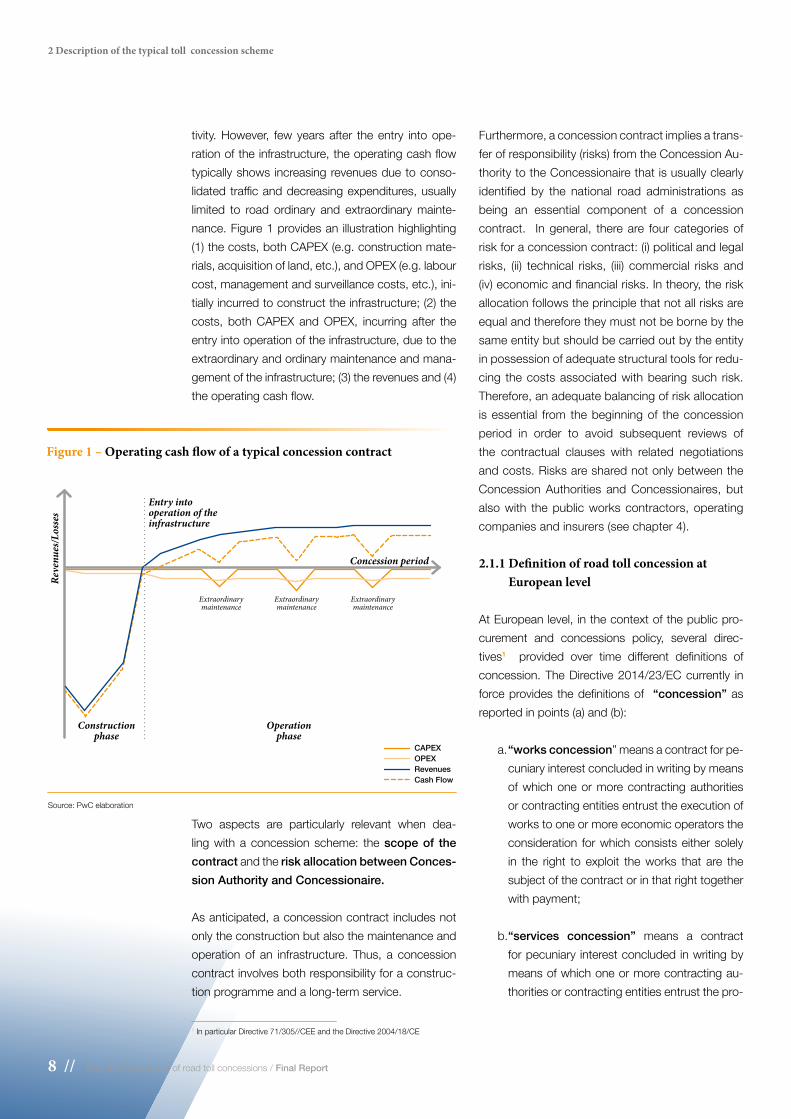

From the perspective of the Concessionaire, the operatingcashflowofatypicalconcessioncontractshows losses in the initial phase, typically from the beginningoftheconcessioncontracttillthefirstyearsof operations, due the capital expenditures (CAPEX) andoperatingexpenses(OPEX)intheconstructionphaseand to thestart-upphaseof the tollingac-

Evaluation and future of road toll concessions / Final Report // 7

2 Description of the typical toll concession scheme

tivity. However, few years after the entry into ope-rationoftheinfrastructure,theoperatingcashflowtypicallyshows increasingrevenuesduetoconso-lidatedtrafficanddecreasingexpenditures,usuallylimited to road ordinary and extraordinary mainte-nance.Figure1providesanillustrationhighlighting(1)thecosts,bothCAPEX(e.g.constructionmate-rials,acquisitionofland,etc.),andOPEX(e.g.labourcost,managementandsurveillancecosts,etc.),ini-tially incurred to construct the infrastructure; (2) the costs, bothCAPEX andOPEX, incurring after theentry into operation of the infrastructure, due to the extraordinary and ordinary maintenance and mana-gementoftheinfrastructure;(3)therevenuesand(4)theoperatingcashflow.

Two aspects are particularly relevant when dea-lingwithaconcessionscheme: thescope of the contract and the risk allocation between Conces-sion Authority and Concessionaire.

As anticipated, a concession contract includes not only the construction but also the maintenance and operation of an infrastructure. Thus, a concession contract involves both responsibility for a construc-tionprogrammeandalong-termservice.

Furthermore, a concession contract implies a trans-fer of responsibility (risks) from the Concession Au-thority to the Concessionaire that is usually clearly identified by the national road administrations asbeing an essential component of a concessioncontract. Ingeneral, thereare fourcategoriesofriskforaconcessioncontract:(i)politicalandlegalrisks, (ii) technical risks, (iii) commercial risks and (iv)economicandfinancialrisks.Intheory,theriskallocation follows the principle that not all risks are equalandthereforetheymustnotbebornebythesame entity but should be carried out by the entity inpossessionofadequatestructuraltoolsforredu-cing thecostsassociatedwithbearingsuch risk.Therefore,anadequatebalancingofriskallocationisessential from thebeginningof theconcessionperiod in order to avoid subsequent reviews ofthe contractual clauses with related negotiationsand costs. Risks are shared not only between the Concession Authorities and Concessionaires, but alsowith thepublicworkscontractors,operatingcompanies and insurers (see chapter 4).

2.1.1 Definition of road toll concession at European level

At European level, in the context of the public pro-curement and concessions policy, several direc-tives1 provided over time different definitions ofconcession. The Directive 2014/23/EC currently in forceprovidesthedefinitionsof “concession” as reported in points (a) and (b):

a. “works concession” means a contract for pe-cuniaryinterestconcludedinwritingbymeansofwhichoneormorecontractingauthoritiesorcontractingentitiesentrusttheexecutionofworks to one or more economic operators the consideration for which consists either solely in the right to exploit theworks that are thesubjectofthecontractorinthatrighttogetherwith payment;

b. “services concession” means a contract forpecuniaryinterestconcludedinwritingbymeansofwhichoneormorecontractingau-thoritiesorcontractingentitiesentrustthepro-

Figure 1 – Operating cash flow of a typical concession contract

Source: PwC elaboration

1 In particular Directive 71/305//CEE and the Directive 2004/18/CE

Reve

nues

/Los

ses

Entry intooperation of theinfrastructure

Concession period

Operation phase

Construction phase

Extraordinary maintenance

Extraordinary maintenance

Extraordinary maintenance

CAPEX OPEX Revenues Cash Flow

Evaluation and future of road toll concessions / Final Report 8 //

2 Description of the typical toll concession scheme

visionandthemanagementofservicesotherthan the execution of works referred to in point (a) to one or more economic operators, the consideration of which consists either solely intherighttoexploittheservicesthatarethesubjectofthecontractorinthatrighttogetherwith payment.

Incaseofroadmotorways,thedefinitionofconces-sion schemes could be related to works concession and/orservicesconcession(seeparagraph2.1.2).

2.1.2 Definition of road toll concession in ASECAP member European Countries

Thereisnotauniquemodelofroadtollconcession,and,asaconsequence,notauniquedefinition.Asexample,thetablebelowreportsthedifferentdefi-nitions provided by ASECAP members.

Thedifferentdefinitionsofroadtollconcessioncanbereferredbothtothedefinitionofworkconcessionand service concession contained in the Directive 2014/23/EC.

Table 1 – Definition of road toll concession in the European countries*

Country Definition

Austria InAustria,the“concession”(legalstatus:ususfructuscontract,Fruchtgenussvertrag)betweentheRepublicofAustriaandASFINAGisdefinedbyacontractbetweenthesetwoentitiesandbyfurtherspecificlaws:ASFINAGisentitledtocollecttollontheentireAustrianMotorwaynetwork(levelofthetollratesbeingapprovedbytheState).Inreturnforthetollcollected,ASFINAGisobligedtofinance,build,maintainandoperatetheAustrianhighwayandmotorwaynetwork.

France A concession is a tool for State authorities to fund, maintain, exploit and develop an infrastructure network.Throughtheconcession,theStatedelegatetothecontractingpartnertheresponsibilitytobuildandoperatetheinfrastructurebearingtherisksassociated.Remunerationofthepartnerisprovidedthroughtollcollection.

Greece In Greece a concession is a tool for State authorities to complete and maintain the motorway networkthroughthetollscollected.

Hungary InHungary, a concession is a tool developedbyprivate investors, financed through availabilitypayment received directly from the State, to build, maintain, improve and operate the infrastructure.

Italy “Publicworksconcessions”arecontracts,withfinancialclauses,writtenandregistered,regardingthe solely execution,or thedetailedconstructiondesignand theconsequent execution,or thefinaldesignandthedetailedconstructiondesignandtheexecutionofpublicworks,andofworksstructurallyanddirectlyconnectedtothem;andtheirfunctionalandfinancialoperation.

Poland A concession is a type of contract between the State and the private entrepreneur, whereby the Concessionaireagreestocarryoutthesubjectoftheconcessionforremuneration,whichistherighttousethesubjectoftheconcessionwiththerighttocollectthebenefits(tolls).

Slovenia AconcessionisabilaterallegalrelationshipbetweenthestateandpublicentityasthegrantorandanylegalentityastheConcessionaire,inwhichtheawardingauthoritygrantstotheConcessionaireaspecialorexclusiverighttoperformpublicserviceorotheractivityinthepublicinterest,whichmay include the construction of facilities and devices that are partly or wholly in the public interest.

Spain A concession is a mixed contract of public works and public service operations.Through the concession, theConcessionaire, chosenbymeansof a public tender, operates apublicservice,suchasplacinganinfrastructurefortravelandroadtransportationatthedisposalofindividuals, and on the other, the Concessionaire occupies and uses an asset of public domain for the operation of that service.

*ThetablereportsdefinitionsfromASECAPmemberswhichprovideditinthecontextofthePerformanceSurvey2014.

Evaluation and future of road toll concessions / Final Report // 9

M E R M É D I T E R R A N É E

M E R

T Y R R H É N I E N N E

M E R

É G É E

M E R

N O I R E

MA N C H E

M E R

D U N O R D M E RB A

L T I QU

E

M E RB L A

N

CH

E

M E R

D E B A R E N T SO C É A N G L A C I A L

A R C T I Q U E

OC

ÉA

NA

TL

AN

TI

QU

E

ME R

A D R I A T I Q U E

Ljubljana

Bratislava

Beograd

Moscou

London

Praha

Lisboa

Warszawa

Amsterdam

Oslo

Rabat

Roma

Dublin

Budapes t

Athinai

Paris

Madrid

Copenhague

Zagreb

Wien

Berlin

Danemark

Royaume-Uni

Irlande

Allemagne

Pays-Bas

France

Italie

Espagne

Grèce

Portugal

Pologne

RépubliqueTchèque

Hongrie

Norvège

Serbie

Croatie

Slovaquie

Slovénie

Autriche

Maroc

Russie

ASECAP Full MemberASECAP Associate MemberASECAP Network as for 01.01.2013 ASECAP Network in constructionToll Bridges,Tunnels and Roads

3 Description of the ASECAP network

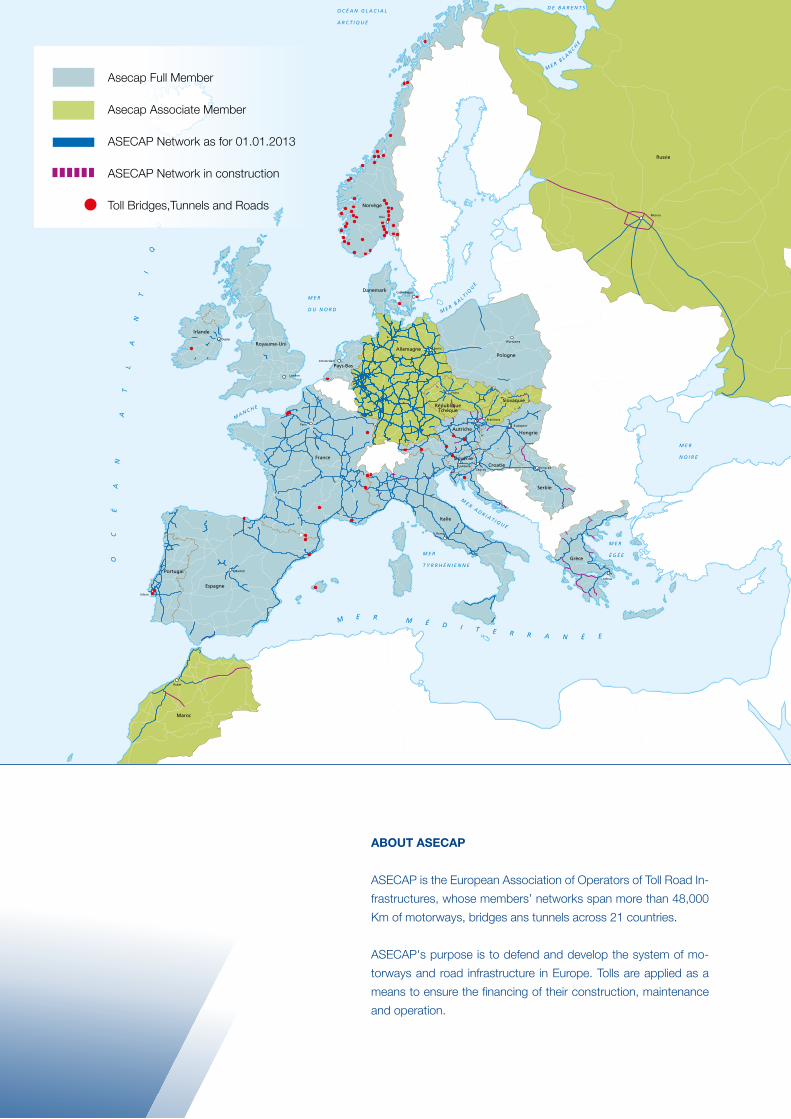

3.1 Presentation of ASECAP

ASECAP is the European Association of Opera-torsofTollRoad Infrastructures,whosemembers’networks in 2014 span over 48,000 km of mo-torways,bridgesand tunnelsacross21countries,managedby187companies.

ASECAP’s purpose is to advocate and developthe system of motorways and road infrastructures inEuropeapplying tollsasameans toensure thefinancing of their construction, maintenance andoperation.

The members of the Association are either full members or associate members:

• 16 full members: ASFINAG (Austria), HUKA (Croatia), SUND & BÆLT Holding A/S (Den-mark), ASFA (France), HELLASTRON (Gree-ce), AKA (Hungary), ITIA (Ireland), AISCAT(Italy), NORVEGFINANS (Norway), N.V. Wes-terscheldetunnel (The Netherlands), AWSA (Poland),APCAP(Portugal),PublicEnterprise«Roads of Serbia» (Serbia), DARS (Slovenia), SEOPAN(Spain),MacquarieMotorwayGroup(UnitedKingdom);

• 5 associate members: Kapsch T.S. (CzechRepublic), TOLL COLLECT GmbH (Germany), Société Nationale des Autoroutes du Maroc (Morocco), AVTODOR (Russia), NDS (Slovak Republic).

Full members are associations of companies or companies holding at least one tolled motorwaysection or a tolled construction in Europe and whose incomederivesprincipallyfromcollectingtollspaidby users.

Associate members are national associations or groups of toll motorways or concession holdersoperating innon-Europeancountriesadjacentanddirectly connected to the European members of the Association by land or by the Mediterranean sea, or–undercertainconditions–companiesinchargeofcollectingadistance-relateduserchargefromtheroad users.

Figure 2 – ASECAP network and members (as for 01.01.2013)

Source: ASECAP

Evaluation and future of road toll concessions / Final Report 10 //

3 Description of the ASECAP network

3.2 Concession models applied to networks operated by ASECAP members2

ASECAP members operate their road networks under a number of different concession schemeswhich can vary mainly on the basis of the nature of the Concessionaire (i.e. private, public or private/public),obligationsoftheConcessionaire(e.g.buil-ding, maintaining, operating, provision of ancillaryservices, etc.) and financial aspects such as themechanism for settling and adjusting tolls. Fol-lowing, is provided a brief description of the legalframework of the concession models, of the obli-gations for theConcessionaireandof thefinancialaspects in each ASECAP full member.

Details concerning specificobligationswith regardtosafetyaredescribedintheparagraph3.2.1.

Austria - ASFINAG

Legal frameworkThe concession company ASFINAG is governedby private law and is 100% owned by the Republic of Austria, i.e. the Concession Authority is identical with the Concessionaire. The usus fructus contract between the Republic of Austria and ASFINAG en-ables ASFINAG to collect tolls on the Austrian pri-mary road network. The concession period of AS-FINAG is unlimited.

ObligationsTheConcessionaireASFINAGhastheobligationtomaintain,operateandfinancethecurrenthighway.Furthermore, it isobligedtobuildnewconcession

sections as set in the Federal RoadAct (BSTG –Bundesstraßengesetz). All expenses are financedfromtheASFINAGbudget.

Financial aspectsThe payment of toll constitutes a contract between ASFINAG and the users, where the user pay for usingtheroadnetworkofASFINAG.Thetollfeeisleviedwitharealtollingscheme(dis-tance dependent > 3,5t maximum gross weight,time-dependent <=3,5t) and on some sections (mainly tunnels) vehicles <= 3,5t also pay distance related toll instead of time-dependent toll.Toll ratesaredeterminedbyapplying theEUEuroVignetteDirective.Thetariffisdistinguishedwiththenumber of axles of a vehicles >3,5 t and the vehicles Euro-emissionclass.ForsomesectionsaccordingtotheEuro-Vignettedirectiveamark-upforcross-fi-nancing of trans-European railway networks is le-vied.Thetariffsforvehicles<3,5tarejustdistingui-shedbetweenmotorbikesandpassengercars,nofurther distinctions are made for these vehicles.

Croatia - HUKA

Legal frameworkMotorway concessions are based on the Public Roads Act and Concession Act as well as on parti-cularConcessionAgreementsbetweenthegrantor(State) and the Concessionaire whereby the State entrusts to the Concessionaire the entire responsi-bilityforbuildingandoperatingthemotorways.

2Source:InformationregardingFullMembersfromPerformanceSurvey2014andTolledinfrastructureswithinASECAP2007

© A

SFIN

AG

© H

UKA

Evaluation and future of road toll concessions / Final Report // 11

3 Description of the ASECAP network

Atthetimetheconcessionshavebeengranted,thelengthoftheconcessionperiodhadbeenfixedat33 years. Reform of the Roads Act dated 2013 re-sulted in extension of the initial duration of conces-sion to maximum 60 years.

ObligationsThe Concessionaire or the motorway company is responsiblefordesigning,financing,building,main-taining,developingandoperatingtheinfrastructure.It has to comply with the location permit issued by the State, to adjust the infrastructure to traf-fic volume, and to provide annex services on themotorway.

Financial aspectsThe Croatian term CESTARINA is a fee paid by the user forusingamotorwaynetworkor facility. It isbasedondistancetravelledandonthecategoryofthevehicle(vehiclesareclassifiedin5categoriesonthebasisofnumberofaxles,heightandweightofthe vehicle).

In accordance with the Roads Act, users in Croatia payonlyformotorwaysandcertainfacilities(bridgeand tunnel); the rest of the road network is free. The tariffisdeterminedinaccordancewithcertaincrite-ria: costs of construction, operations, maintenance anddevelopment of the network, taking also intoaccount the level of GDP.

Inparticular,companiesareentitledtoapplydiffe-rent tariffs based on category, period of the day,parts and stretches of motorways, purpose of the vehicle, and euro emission class of vehicle.

Denmark - SUND & BAELT

Legal frameworkIn Denmark, tolls are collected only for two largebridgelinks:Storebaelt(inDenmark)andOeresund(between Denmark and Sweden). The Sund & Baelt Groupisgovernedbyprivatelawandis100percentownedbytheDanishstate.Theaffiliatedcompaniesareassignedthetaskofconstructingthe linksandlater on to be responsible for their operation.

ObligationsConcessionairesarerequiredtodesign,build,main-tain, improve, and operate the infrastructure.

Financial aspectsThe tolls levied on the users are used to repay loans that were raised for the construction costs and to pay for the operation and maintenance of links. The amount of the toll is determined on the basis of the length/heightof thevehicleand insomecases thenumber of trips. The amount of the toll is related to theconstructionandoperatingcostsand isdrivenby commercial considerations. The toll amount is not adjustedtotrafficvolume.

© S

UN

D &

BAE

LT

Evaluation and future of road toll concessions / Final Report 12 //

3 Description of the ASECAP network

France - ASFA

Legal frameworkThe French motorway system is based on the prin-ciple of the concession of public works and services (constructionandoperation)followingtheLawof18April1955.Theconcessionagreement,backedupbyadetailedspecification,isacontractwherebytheState(thegrantor)entruststoconcessionarycompa-nies,attheirrisk,theentireresponsibilityforbuildingandoperatingthemotorwaysforalimitedperiodoftime. Extension of concession contract is allowed up to1year(forcontractualagreement);extensionover1 year must be approved by a dedicated rule.

ObligationsThe companies are required to finance conduct thedesign of the feasibility study and to build,maintain,develop and operate the infrastructure. They are also obligedtoprovideancillaryservices.However,theyareundernoobligationtoadaptorexpandtheinfrastruc-tureinaccordancewithtrafficvolume,unlessthishasbeenspecificallymentionedintheoriginalspecification.

Financial aspectsIn France, a toll is the payment by the user of a fee for usingaroadinfrastructureornetworktherevenuesofwhicharedirectlyassignedtoalegallyindependententity responsible for the finance, construction,maintenance and operation of that infrastructure. Theuserpaysaccordingtothedistancedriven,thenumberofaxles, theweightof thevehicleand, forrecentlybuilthighways,itsemissionscoefficient.Thetariffisfixedinrelationtothecostsofconstruction,operation and maintenance.

Greece - HELLASTRON

Legal frameworkInGreece, theconcessionsaregenerallygovernedbyprivate lawandownedprimarilyby thegovern-ment. There are also totally private companies in Greece, subject to different legislation. The meanconcession period is 30 years. National rules foresee the possibility to extend the concession contract (up to 3 years) in case the expected internal rate of return (IRR) is achieved.

ObligationsTheConcessionaire isrequiredtomaintainand im-prove the infrastructure, supply annex services and adjustorexpandtheinfrastructureaccordingtotraf-ficvolume.

Financial aspectsThe user pays according to the distance travelledand the number of axles of the vehicle. The toll is determinedbytheoperatingcosts.

© E

IFFA

GE

CEV

M –

Fos

ter+

Partn

ers

– D

. Jam

me

© A

ttiki

Odo

s

Evaluation and future of road toll concessions / Final Report // 13

3 Description of the ASECAP network

Hungary - AKA Zrt.

Legal framework InHungary,theconcessionsaregovernedbypubliclaw. The tenure of the concession is 35 years and itrevertstothegrantingauthorityattheendofthecontract. There is no government guarantee andthe companies are free to determine their own bor-rowing policy. Although the government does notsupply any guarantee, it requires complete trans-parency from the Concessionaire, which operates as a private company. The mean concession pe-riod is 35 years. The national public procurement rulesdonotallowanymodificationtothetermsofthecontract,includingextensionoftheconcessioncontract.

ObligationsInHungary,theConcessionairesarerequiredtofi-nance, build, maintain, improve and operate the in-frastructure. Moreover the company has to adjust orexpandtheinfrastructureaccordingtothetrafficvolume.

Financial aspectsRoadconstructionprojectsarefinancedfromaspe-cialstatefund,dividedbythestatebudget,feededby the tolls pays by users. In case of concession contracts, road construction and operation shall be “pre-financed”bytheConcessionaire,andthestatepays availability fees.

Ireland - ITIA

Legal frameworkIn Ireland, the Public Private Partnership (“PPP”)contracts are awarded to a Concessionaire by the NationalRoadsAuthority(“NRA”)followingacom-petitive bid process.

ObligationsTypically,thePPPcontractsignedwiththeConces-sionaire requires thedesign, building, finance andoperationofthenewmotorway.Itisenvisagedthatthe Concessionaire will recover its initial and on-goingcosts througha combinationof i) subsidiesreceivedfromtheNRAandii)chargingtollsinres-pect of use of the road. In some cases where tolls arenotchargedtothepublic,costsarerecoveredsolely through availability payments received fromthe NRA.

Financial aspectsMaximum base tolls are set out in Bye Laws, which are created for each motorway where tolls are to be charged.Theyareincreasedorreducedbyapplyinga consumer price index each year in accordance withtheByeLaws.Tollsaredifferentiatedontheba-sis of number of axles and time of travel (for certain infrastructures).

3CIPEistheItalianInter-MinisterialCommitteeforEconomicPlanning,anentitysupposedtogiveadvicesandtocoordinatealltheissuesrelatedtotheeconomicandfinancialplanningatNationallevel.

© IT

IA

© A

KA Z

rt.

Evaluation and future of road toll concessions / Final Report 14 //

3 Description of the ASECAP network

Italy - AISCAT

Legal frameworkIn Italy, the concessions are governed by law, bydirectives from CIPE3 and by the concession’scontract. Italian Concessionaires include 100% privately-owned companies as well as companies owned primarily by public authorities (local and re-gionalauthorities)butwithsomeprivatesharehol-ders.Theconcessionisreturnedtothegrantingau-thority at the end of its period of tenure. The mean of concession period is 30 years and extension of the concession contract is allowed only in cases complyingwiththeEuropeanlawsonconcessions.

ObligationsIn Italy, in compliance with the concession contract, the Concessionaires are responsible for: financing,building,maintainingandupgradingtherelevantsec-tionsofmotorway,includingthecollectionoftolls;or-ganisingandmaintainingusers’informationandassis-tanceservices;keepingaccountsasspecifiedbythegrantingauthority;providinggrantingauthoritywiththerelevant information needed to assess the favorable development of the concession, in compliance with the provisions of the concession contract.

Financial aspectsThe toll is a payment made by a user in return for using a specific infrastructure,with reference to theconstruction, maintenance and operation of that in-frastructure. The revenue is directly assigned to a

legally independent body responsible for financing,building,maintaining,andoperatingtheinfrastructure.

The determination of the toll amount is based upon the distance travelled, the number of axles, pollu-tionlevelsfortheAlpinetunnelsonly,andtheheightabovethefirstaxle.Theamountofthetollisrelatedtotheconstructionandoperatingcostsandisnotdriven by commercial considerations.

Norway - Norvegfinans

Legal frameworkTheStateisnotonlyinchargeofplanningbutalsoofbuildingandmaintainingtheroadnetworkinclu-dingmotorways(therearenoroadconcessionairesin Norway). The sector’s companies are only inchargeoffinancingcertaininfrastructuresandcol-lectingtolls.

Obligations Theconcession’sonlyobligationistosupplythene-cessaryfinancingandcollecttolls.

FinancingThe legislativebackground for tollcollection is theRoadAct,inwhichtollsareseenasawaytofinancepublic road projects, and under certain conditions also other infrastructure projects. Each toll project needs approval both locally and in the Parliament. Thetoll’samountisdeterminedbytheStateaccor-dingtotheconstructioncosts.

© A

ISC

AT

© N

orve

gfina

ns

Evaluation and future of road toll concessions / Final Report // 15

3 Description of the ASECAP network

The Netherlands - N.V. Westerscheldetunnel

Legal frameworkThe N.V. Westerscheldetunnel is the company in charge of building,maintaining and operating theinfrastructure (namely the Westerscheldetunnel) in order to recover the costs of the investment and maintenance via the collection of tolls.

In 2033 the infrastructure will be transferred to the Dutch Government.

ObligationsThecompanyisobligedtomaintainandoperatetheinfrastructure.

Financial aspectsAccording to law, theN.V.Westerscheldetunnel isentitledtodeterminetheamountofthetollcharges.Toll is collected as a fee, depends mainly on the len-gthandheightof thevehiclesand isdifferentiatedon the basis of number of axles and Euro standard.

Poland - AWSA

Legal frameworkThe typical concession models applied in Poland aretheprojectfinancemodel,wherethecashflowgenerated from tolls serves the debt repayment(granted for construction), maintenance and ope-ration or projects with public authority support in a form of availability payments to the Concessio-nairesandsecuringthedebtrepayment.Themeanof concession period is 30 years and the extension of concession contract is not allowed.

ObligationsConcessionaires are obliged to identify and orga-nizethefinancing,buildnewroads,orreconstructtheexistingones,bywayofadaptationoftheroadoriginally built by thegovernment, upgrade to therequirementsofamodernmotorway,operateandmaintaintheentiresectionaccordingtothecondi-tionsandrequirementsofConcessionAgreements.

Financial aspectsIn Poland there are both traditional concession schemeoffinancing(paymentbyusertoll)aswellaspublic-private contractswith repaymentsusingavailability scheme. Contrary to tolls collected on the motorway sections run by the State (GDDKiA –RoadAdministration),motorwaytollscollectedbyprivateconcessionariesaredefinedasafeeandaresubject to 23% VAT.

On the A1 Motorway, the level of toll is subject to levelsagreedwith thegovernment in theconces-sion agreement. The A1Motorway tolling systemis“closed”type,meaningthatthepaymentismadeattheendofthejourneyattheexitgates.Thetollamount is determined in function of the rate per km (vehiclecategory)andthedistancedriven.

© A

WSA

© N

.V. W

este

rsch

elde

tunn

el

Evaluation and future of road toll concessions / Final Report 16 //

3 Description of the ASECAP network

Toll rates, which shall not exceed the trash hold as defined in the concession agreement, aredefinedby the Concessionaires on the A2 Motorway (5 categories)andA4Motorway(2categories)andbytheMinisterontheA1Motorway(2categories)andtheA2IIMotorway(5categories).

Ingeneral,tollsratesfollowtherecommendationoftrafficadvisorsforecast.

Portugal - APCAP

Legal frameworkConcessions are governed by private law. Thegrantor isEP -EstradasdePortugalS.A, thena-tional road authority entrusted by the PortugueseGovernment. The concession overs at the end of thecontract,withoutchargesandwithnoreversionfunds.Extendingitisnotallowed.

ObligationsIncompliancewiththeconcessionagreement,theConcessionaires have the obligation of designing,building,maintaining,wideningoflanes(whenappli-cable) and operation (toll collection included). TheConcessionairehastoorganizethetollcollec-tionserviceasefficientlyandsafelyaspossibleandin a way that causes the minimum inconvenience and time loss to motorway users.

Financial aspectsGenerally, each Concessionaire fully finances itsoperationwith financial resources raised or gene-ratedautonomouslythroughtolls.

The amount of the toll is not driven by commercial considerations and is based upon traveled dis-tance,numberofaxlesandvehicle’sheightoverthefirstaxle.

The initial toll isdefinedby theStateaccording totheaveragetariffoftheyearofreferenceonthena-tional toll network. The Concessionaire may revise tollratesonthefirstmonthofeachcalendaryear.

Serbia - PUBLIC ENTERPRISE “Roads of Serbia”

Legal frameworkAll motorways in Serbia are State-owned and PE “Roads of Serbia” is wholly-owned by the State.Currently, there are no concession companies for motorway operation or maintenance in Serbia.

ObligationsPE«RoadsofSerbia» is inchargeofmaintaining,protecting, exploiting, developing and managingstate roadsof Iand IIcategory in theRepublicofSerbia.PE“RoadsofSerbia”isalsoresponsiblefortoll collection on motorways in opened and closed toll-collection systems.

Financial aspectsToll,financialloans,budgetoftheRepublicofSer-bia, other sources pursuant to the Law are the meanstofinancetheconstructionandreconstruc-tion, maintenance and protection of public roads.

© A

PCAP

© P

E “R

oads

of S

erbi

a”

Evaluation and future of road toll concessions / Final Report // 17

3 Description of the ASECAP network

Slovenia - DARS

Legal frameworkIn Slovenia, the concession contract between Re-public of Slovenia (the Concession Authority) and DARSd.d.(thesoleexistingConcessionaire,ajoint-stock company, established by law and 100% State-owned)hasbeensignedfortheentiredurationofthe motorway construction and/or for the period of repaymentobligationsonloansanddebtsecuritiesraised and/or issued to this end, but not lower than 20 years. National rules allow contract extension up to 10 years (maximum duration 50 years).

ObligationsIn accordance with the national law, DARS is in charge of financial engineering, preparing, organi-singandmanagingconstructionandmaintenanceof the motorway network, and is responsible for themanagementofmotorways in theRepublicofSlovenia.

Financial aspectsInSlovenia,thetollisappliedasatollingtool,sinceit is paid directly to the Concessionaire, however, toll tariffsareregulatedbytheGovernment.

DARSd.d.asaConcessionairefinancesall itsac-tivities out of toll (toll represents approx. 94% ofDARS d.d. revenues) and other revenues (leases, overweight load transport, telecommunications,easements).

DARSd.d. only has the right to suggest changesinthetollingpolicyregardingtheamountofthetollper toll categories, Euro-emission classes, timeoftravel etc., but final decision is made by the Go-vernmentof theRepublicofSlovenia–whoapart

from the Concessionaire’s proposal, usually takesinto account also the public opinion and the opinion of the users, mainly domestic haulers. The same goesforthedeterminationofthepriceofvignettes:DARSd.d.canproposechanges,butfinaldecisionis made by the Government.

Spain - SEOPAN

Legal frameworkConcessions are governed by private law. Theawardof a concession takesplace throughapu-blictender,calledtogetherbytheMinistryofPublicWorksonbehalfoftheSpanishStateorbyRegio-nalGovernments.EligibleforawardareSpanishorforeignindividualsandcorporations,withfullcapa-city to act, and that do not incur any prohibition to contract, in accordance with what is established in thePublicAdministrationContractsLegislation.

The concession for constructionwork and equip-ment followed by the operation of the service will be awarded by Royal Decree, approved by the Cabi-net,attherequestoftheMinistryofPublicWorks,tothe most suitable bid. This Royal Decree sets itself upasthedeclarationofpublicutilitywithregardtoexpropriation. A similar process takes place at a re-gionallevelinthecaseofthoseprojectsunderthecompetenceareaofregionalAdministrations.

TheConcessionairemanagestheservice,purposeof the concession, under the supervision, inspection andcontrol of the awardingAdministration,whichwillbeexercisedbytheGovernment’sDepartmentofNational Toll Road Concessionaire Companies. The Deputy Secretary of the Ministry of Public Works is, atthesametime,theGovernment’sRepresentative

© S

EOPA

N

© D

ARS

Evaluation and future of road toll concessions / Final Report 18 //

3 Description of the ASECAP network

for National Toll Road Concessionaire Companies, asstatedinRoyalDecreeregulatingthestructureofthe Ministry of Public Works.

Generally, the duration of concessions is 40 years for construction concessions (with the possibility of extension until 46 years) and 20 years for operation concessions (with the possibility of extension until 25 years).

ObligationsTheconcessioncompaniesarerequiredtofinance,build, maintain, improve and operate the infrastruc-ture.Theyare required toguarantee thebest ser-vice to the user and keep the motorway in the best conditions.

Financial aspectsThe Concessionaire is committed to structure the financingofthemotorwayusingitsownresourcesorexternalones(lookingintofinancemarket,issuingbonds).

InSpain,atollisthepaymentbyauserforusingaspecificinfrastructureaccordingtothedistancetra-velled and some physical parameter of the vehicle (number of axles and presence of dual tyres).Therearethreetariffcategoriesaccordingtovehicleclassification.

Every year, the concessionaire, previous approval bytheawardingauthority, increasestoll rates.Themethod used to calculate the increase of toll rates onconcessionsawardedisbasedontheprevious’year increase in cost of living, plus the differencebetweentheforecastedandrealtraffics.Thetollratecan be increased every year.

All the revenues collected from the users (except taxes as VAT) are allocated to the Concessionaire who has to invest on the proper maintenance of the roadduringalltheperiodofconcessioncontract.

United Kingdom - Macquarie Motorway Group

Legal frameworkMacquarieMotorwayGroup-MidlandExpresswayLtd has a 53 years concession to build, operate and maintain the M6toll road. At present time, the concession will be held for a further 40 years period after which it will be handed back to the Government.

ObligationsThe company was appointed to build, maintain and operate the M6 toll road.

Financial aspectsTheoperatordefinestolllevelswithamarket-ledap-proach, without any interference from Government. Thereare fivebasic classifications towhichdefinetoll:motorcycle,car,carwithtrailer,lightcommercialvehicles and HGVs. Separate rates apply for wide loadsandslowmovingvehicles.

The table below summarizes themain aspects ofconcessionmodelsandroadchargingpoliciesap-plied in the concessions under ASECAP members management.

© M

acqu

arie

Mot

orw

ay G

roup

Evaluation and future of road toll concessions / Final Report // 19

3 Description of the ASECAP network

Table 2 – ASECAP members: main aspects of concession model, types of payment and charge differentiation

Full members

NO. AND NATURE OF COMPANIES

CONCESSION PERIOD TYPES OF PAYMENT CHARGE DIFFERENTIATION

Public Mixed capital

Private Total Average concession

period

Extensionperiod

Light vehicles

Heavy vehicles

Euro standard

Period of day Axles

Austria 1 1 Unlimited - Distance- based

Distance- based ✓

✓ (Brenner motorway) ✓

Croatia 2 2 4 30 years Maximum60 years

Distance- based

Distance- based ✓ ✓

Denmark 2 2 - - Distance- based

Distance- based ✓ - ✓

France 2 21 23 30 years 1 year4 Distance- based

Distance- based

✓ (selected tunnels)

✓ (selected roads) ✓

Greece 8 8 30 years3 years,

underspecificcondition5

Distance- based

Distance- based - - ✓

Hungary 5 5 35 years No Time-based Time-based - - -

Ireland 9 9 35 years - Distance- based

Distance- based -

✓ (Dublin port tunnel, only

vehicles <3.5t)✓

Italy 2 21 4 27 30 yearsYes, under specific

condition6

Distance- based

Distance- based - - ✓

The Netherlands 1 1 30 years - - Time-based - - -Norway 38 38 - - - - ✓ - ✓

Poland 4 4 30 years No Distance- based

Distance- based - - ✓

Portugal 1 20 21 30 years No Distance- based

Distance- based - - ✓

Serbia 1 1 Unlimited - - - ✓ ✓(day/night) ✓

Slovenia 1 1 20 years 10 years (maxi-mum 50 years) Time- based Distance-

based - ✓ (selected roads) ✓

Spain 3 29 32

- 40 years for construction concessions

- 20 years for operation concessions

- Maximum 46 years for construction concessions

- Maximum 25 years for operation

concessions

Distance- based

Distance- based - - ✓

United Kingdom 1 1 50 years No - Time-based - ✓ ✓

Total 17 24 139 180

Source:ASECAP,nationalreports,PerformanceSurvey2014;EvaluationoftheimplementationandeffectsofEUinfrastructurechargingpolicysince1995-Final(ReportRicardo–AEA/ECDGMOVE);EuropeanCommission

4 Extension over 1 year must be approved by a dedicate rule.5 National rules foresee the possibility to extend the concession contract in case the expected IRR is achieved. 6ExtensionoftheconcessioncontractisallowedonlyincasescomplyingwiththeEuropeanlawsonconcessions.

Evaluation and future of road toll concessions / Final Report 20 //

3 Description of the ASECAP network

3.2.1 Obligations with regard to safety improvements 7

Nowadays, as in the past, concession companies play an important role in the development of the safety level of the road network. As a matter of fact, safety concerns tend to be taken into account since the early stage of a concession scheme. Beyondthe general obligations concerning the construc-tion, maintenance and operation, road concession contracts tend to foresee specific obligations fortheConcessionaireregardingsafety improvementsalong the road network (e.g. pavements mainte-nance,safetybarriers,roadlighting,etc.).Inparticu-lar, the results of the Performance Survey revealed how in six countries (i.e. Austria, Italy, Poland, Slove-nia,GreeceandHungary)thecontractualschemesinforceregularlyforeseeobligationswithregardtosafety improvements.

Further,incaseunexpectedobligationsofthiskindarise(e.g.needtoupgradepavements),therelatedcostsarefundedindifferentwaysamongASECAPmembers:

• in Austria, Italyand Slovenia, such costs are included fully in the tolls paid by users;

• in France and Spain, such costs are fully or partially included in the tolls paid by users;

• in Poland such costs are totally borne by the Concessionaire without compensation;

•inGreecesuchcostsare fundedbygovern-mental authorities.

The relevance given by the public authorities tosafetyconcernsisconfirmedbythemonitoringac-tivity put in place by the ASECAP members. As a matter of fact, the Public Authority in each country monitorsdifferentsafety indicatorsandmakespe-riodicallyonthegroundinspections,inparticular:

• In Austria, the public authority inspects, via on spot inspections and examination of plans and designs,ifASFINAGobeysthesafetyrequire-mentsandobligations..Thenumberofacci-dentsandfatalitiesisahighprioritymatterandmajorpoliticalgoalforthestate/concessiongrantor.

• In Italy,thegrantingauthorityverifiesconstant-ly, by means of inspections, the safeness sta-tus of the motorways, on the basis of many in-dicators,including:thepavementsconditions,the efficiency of the safety barriers, the ligh-ting (where applicable), the compliance withall the technical parameters defined by theprescribed standards, etc. Furthermore, it is stipulatedthatwithintheannualtariffsupdatemechanism, an indicator about levels of safety or accidents has to be taken into account.

• In France, most security improvements are included in “Contrats de plan”, stipulated for a 5 years period and including investments toupgradetheconcessionandtariffincreasestofinancethem.Securityimprovementscouldbefunded by Concessionaires prior the inclusion in a Contrat de plan. Most often, the invest-ments are fully or at least partially compensa-ted later on.

• In Spain, no specific obligations relating tosafety are considered in the toll concessions contracts,nevertheless,thereisageneralobli-gationtokeepandmaintainthemotorwayonthe best conditions, under the strict supervi-sionofthegrantingauthority.Onshadowtollsconcessions, safety is a parameter included in theindicatorsusedtoassessthegoodopera-tion of the road.

• In Poland, the Public Authority monitors/conducts inspection of signing of the mo-torwayforcompliancewithapproveddesign,ongoing maintenance, preparation for wintermaintenance, control infrastructure compo-nents related to the safety, toll collection. Such checks are held several times a year.

• In Slovenia, the safety improvements are definedon thebasisof thenumberof trafficaccidentsthatoccurredonhighwaysandex-pressways. The monitored indicators are num-ber of killed and seriously injured persons.

• In Greece, the Public Authority monitors the conditionofbarriers,thelightinglevel,theas-

7 Source: Performance Survey 2014

Evaluation and future of road toll concessions / Final Report // 21

3 Description of the ASECAP network

phalt surface characteristics (surface friction, regularity, rutting), theconditionofsignsandroadmarkings,equipmentintunnelsetc.Theinspections by the Public Authority are made according to the provisions of the ContractDocuments.

• In Hungary, the Public Authority periodically checks the compliance with a broad spec-trum of technical requirements and legalprovisions applicable for road operation and management.

3.3 Value added of the road toll

concession

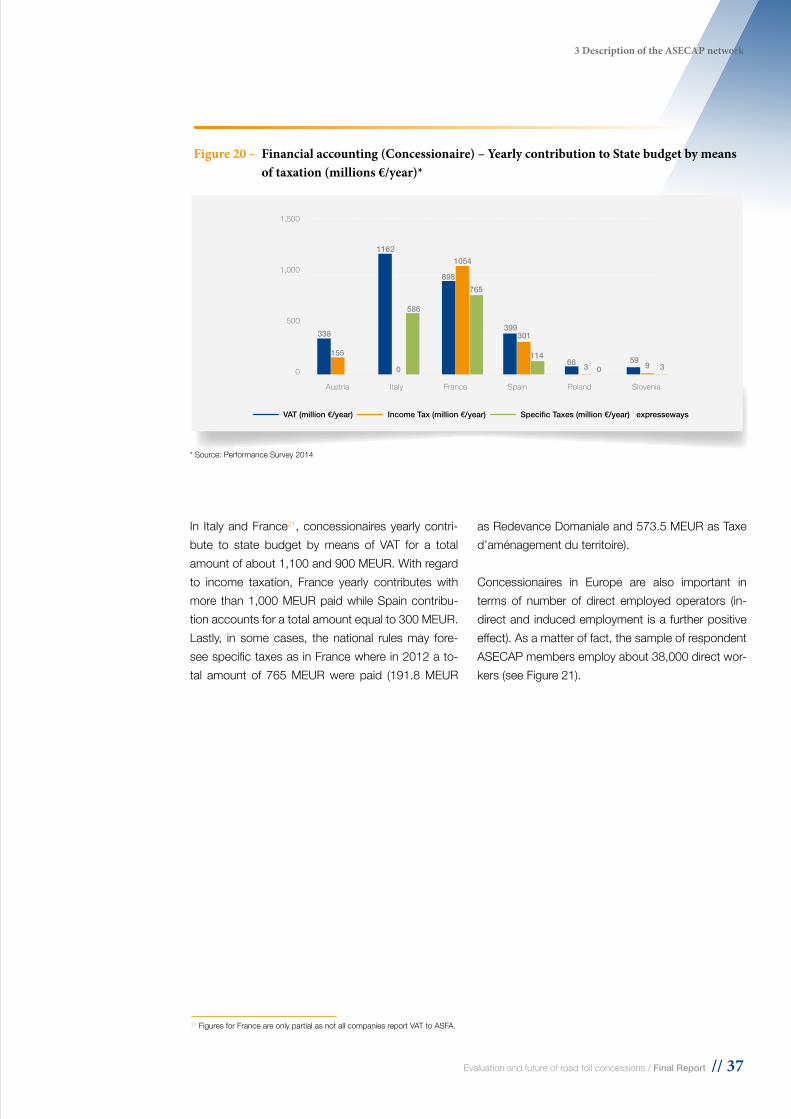

Concessionaires have successfully deployed and operatedtollroadsthroughoutEuropeformorethan50 years. The value added provided by the road toll concession sector can be declined in terms of physi-cal results, such as the development of the network, the share of traffic served and the contribution tothedevelopmentof technology supporting the tolloperation, and in terms of socio economic impacts onthelocalandregionalareas,suchasthereduc-tionoftraveltime,thecontributiontostatebudgetby means of taxation and the creation of new jobs.

3.3.1 Characteristics of ASECAP network: development of the network, share of traffic, safety performance, contribution to the development of technology8

ASECAP members operate more than 55% of the total motorway network in Europe. 775 of the 30,501 km of the ASECAP networks are operated by concessionaires in 5 Countries: France, Italy, Spain,PortugalandAustriaare thecountrieswiththelongestconcessednetwork(asawholetheyarehereinafterreferredtoas‘largernetworks’)

It has to be noted that in Spain the concessed network is less than¼of the national high capa-cityroadnetwork(seetablebelow).Theremainingnetwork –in some cases running in parallel to analreadyexistingtollroad−ismademainlyoftollfree

expresswaysdirectlymanagedbytheStateorRe-gionalGovernments.

Table 3 –Length of ASECAP network

Full members Network length [km]

% on the total national mo-

torway network

Austria 2,177 100%

Croatia 1,289 100%

Denmark 34 3%

France 9,048 78%

Greece 1,659 87%

Hungary 1,145 74%

Ireland 337 37%

Italy 5,814 86%

The Netherlands 20 1%

Norway 911 NA

Poland 468 34%

Portugal 2,943 98%

Serbia 603 100%

Slovenia 607 79%

Spain 3,404 23%

United Kingdom 42 1%

Total 30,501 55%

Source: ASECAP, Performance Survey 2014

Infivecountries (Austria, Denmark, Netherlands, Serbia and Slovenia) motorways (or toll infrastruc-tures)areexclusivelymanagedbytheStatethrough100% controlled companies.

In Croatia, Italy and Portugal some motorways are operated by mixed capital companies, but only in Italy the majority of the concessionaire companies havemixedcapital although, in termsof lengthofthe network, the vast majority is operated by private companies. It seems that also in Croatia this model can be more extensively applied in the future (this subject is currently under examination by the go-vernmentthatisaimingatreducingthepublicsharein motorway O&M). In Portugal just Vialitoral, the companyoperating themotorwaysof theMadeira

8TheanalysescontainedinthissectionreferonlytoASECAPfullmembers,towhomquestionnaireswereaddressed.

Evaluation and future of road toll concessions / Final Report 22 //

3 Description of the ASECAP network

island, is partially owned by a public body (Madeira Region).

In Austria, out of 3 concession companies (ASFI-NAG, GROHAG, Felbertauern AG), just one (ASFI-NAG) operates motorways. The other 2 companies operate toll mountain roads. In this study only ASFI-NAG and its network is taken into account.

In Denmark, the Netherlands, Norway and UK only specific sections of the network are underconcession(i.e.bridges,tunnelsorshortmotorwaylinks).

The Figure below shows the evolution of theconcessed networks in the last 10 years.

10,000

9,000

8,000

7,000

6,000

5,000

4,000

3,000

2,000

1,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Largernetworks

km

1,800

1,600

1,400

1,200

1,000

800

600

400

200

0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Smaller networkskm

Greece

Croatia

Hungary

Norway

SerbiaSloveniaPoland

Ireland

United kingdomThe Netherlands

France

Italy

PortugalSpain

Austria

Source: ASECAP

Figure 3 – Evolution of the ASECAP motorway network

Evaluation and future of road toll concessions / Final Report // 23

3 Description of the ASECAP network

Among the larger networks, the recent sharp in-crease of Portuguese network leaps out imme-diately.In2013,infact,severalregionalmotorwayspreviously operated under shadow tolling andconceded to private companies, turned into real tol-lingconcessions,thereforethenetworkincreasedofabout 1,200 km.

Asharping increaseoccurredalso inGreece after 2009.Inthiscasetheexpansionisduetothefactthatmanyexistingmotorwayspreviouslyoperatedby the State where concessed to private companies.

3.3.1.1 Tolling equipmentInaccordancewiththe‘pay-per-use’principle,mostpartoftheinfrastructureisfinancedbyafeechargedtotheusersandgenerallycollectedattollstations.Vignette9 - or ‘e-vignette’ - systems are currentlyused only in Austria, Hungary and Slovenia (only forlightvehiclesinallthreecountries).

Figuresbelowshowthenumberoftollstationsandlanes for each country, both in absolute and relative terms.

Austria, where a free-flowsystem10 is in operation forheavygoodsvehiclesabove3.5 tonnes, is thecountrywiththehighestdensityoftollstations(i.e.No. of toll stations / km)11.

Amongother countries, besidesUK –where only40kmareinconcession-,othernetworkswithhighdensity of toll stations are Norway, Italy, Croatia and Portugal.

In terms of toll lanes, besides Denmark(twobridgesin concession), UK and the Netherlands (one tun-nel inconcession),countrieswiththehighestden-sity are Austria, Spain and Italy.

In absolute terms, Austria, France and Italy are the countrywiththehighestnumberoftollstationsandlanes.

In the Netherlands and Ireland, almost all toll lanes are ETC type. Other countries with high ETC12 share (more than 75%) are Austria, UK, Denmark and Norway.

Figure 4 – No. of toll stations (as for 01.01.2014)

Source: ASECAP

9Vignetteisaformofroadpricingimposedonvehiclesbasedonaperiodoftimeinsteadoftheusualroadtollmethodbasedondistancetravelled.10Free-flowsystemsallowtollstobepaidwithoutanyneedtochanneltrafficand,aboveall,withoutanyneedtostopthevehicle.Theyconsistofportalsthatcovertheentirelane,onwhichcameras,antennasandclassificationsystemsdetecton-boardunitsand/orvehicleplates.

11Inthiscaseeachportalisconsideredasasingletollstation12 Electronic toll collection

1,000

900

800

700

600

500

400

300

200

100

0

450

400

350

300

250

200

150

100

50

0

Abso

lute

val

ue

Valu

e / k

m (x

1.0

00)

Aust

ria

Cro

atia

Den

mar

k

Fran

ce

Gre

ece

Hun

gary

Irel

and

Italy

The

Net

herla

nds

Nor

way

Pola

nd

Port

ugal

Serb

ia

Slov

enia

Spai

n

Uni

ted

Kig

dom

Value / km (x 1000) Absolute value

Evaluation and future of road toll concessions / Final Report 24 //

3 Description of the ASECAP network

Figure 6 – % ETC/toll lanes (as for 01.01.2014)

Figure 5 – No. of toll lanes (as for 01.01.2014)

Source: ASECAP

Source: ASECAP

6,000

5,000

4,000

3,000

2,000

1,000

0

100

90

80

70

60

50

40

30

20

10

0

1,600

1,400

1,200

1,000

800

600

400

200

0

Abso

lute

val

ue

Valu

e / k

m (x

1.0

00)

Aust

ria

Cro

atia

Den

mar

k

Fran

ce

Gre

ece

Hun

gary

Irel

and

Italy

The

Net

herla

nds

Nor

way

Pola

nd

Port

ugal

Serb

ia

Slov

enia

Spai

n

Uni

ted

Kig

dom

Aust

ria

Cro

atia

Den

mar

k

Fran

ce

Gre

ece

Hun

gary

Irel

and

Italy

The

Net

herla

nds

Nor

way

Pola

nd

Port

ugal

Serb

ia

Slov

enia

Spai

n

Uni

ted

Kig

dom

Value / km (x 1000) Absolute value

%

96

68

78

56

99

55

100

87

36

59

12

42

89

0 0NA

Evaluation and future of road toll concessions / Final Report // 25

3 Description of the ASECAP network

3.3.1.2 TrafficFiguresbelowshowthetrafficevolution inthe last10years.Traffic isexpressedboth in termsofvo-lume(averagedailytraffic–ADT-)anddistancetra-velled (veh-km).

In2013thecountrywiththehighestADTwastheUnited Kingdom (about 40,000 vehicles) , followed by Italy and Austria.

Consideringthenumberofvehiclestravelling,coun-trieswithhighestlevelsareFrance and Italy (more than 75 bn of veh-km per year). All other countries registerlessthan30bnofvehicles-kmperyear.

Trafficisgenerallystronglyinfluencedbyeconomictrend;economicgrowthtendstoleadtoincreased

travel and transport of goods. In a more rapidlygrowingeconomy,agreaterproportionof thepo-pulationislikelytobeworking,hasmoredisposableincome and more products are manufactured which must be transported and for which raw materials must be supplied.

Of course, it may also happen the opposite: in case of economic slump,trafficmovesdownward.Thisis the phenomenon that many European countries areobservingintherecentyears.

Nevertheless, despite the current economic glo-balcrisis,trafficinsomemotorwaynetworksisstillgrowing (e.g. Austria, +5% in the 3-year period 2010 - 2013; Poland, even +13% from 2012 to 2013).

Figure 7 – Average Daily Traffic (ADT) on the ASECAP network

Source: ASECAP, Performance Survey 2014

45,000

40,000

35,000

30,000

25,000

20,000

15,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Largernetworks

50,000

45,000

40,000

35,000

30,000

25,000

20,000

15,000

10,000

5,000

0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Smaller networks

GreeceCroatia

Hungary

SloveniaPoland

United Kingdom

The Netherlands

France

Italy

PortugalSpain

Austria

DataofDenmark,Ireland,NorwayandGreece(from2009)arenotavailable(onlynumberoftransactionsisregistered).DataofPortugalrefersto7historicalAPCAPmembersDuetoachangeinthemeasuringmethodin2008,dataofAustriafrom2004to2007cannotbecomparedwiththefollowingfigures.

Evaluation and future of road toll concessions / Final Report 26 //

3 Description of the ASECAP network

Figure 8 – Total veh-km travelling on the network (10^6 veh-km) on the ASECAP network

Source: ASECAP, Performance Survey 2014

90,000

80,000

70,000

60,000

50,000

40,000

30,000

20,000

10,000

0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Largernetworks

8,000

7,000

6,000

5,000

4,000

3,000

2,000

2,000

1,000

0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Smaller networks

France

Italy

PortugalSpain

Austria

DataofPortugalrefersto7historicalAPCAPmembers.Data of Norway and Serbia are not available

SloveniaGreece

CroatiaHungary

Poland

United Kingdom

The NetherlandsDenmark

Ireland

3.3.1.3 SafetyOne of the most remarkable features of the service provided by toll motorways is safety. It isunques-tionable that safety is duly taken into account in everystageofamotorway’slifecycle,i.e.planning,constructionandoperatingstage.

Alltolledmotorwayshavespeciallydesignedequip-ment to ensure road safety, such as perimeter fences,anti-glarepanels,lightingattollstationsandsemi-urbanstretches,cutting-edgeoperationalandtrafficmanagementcentres,closed-circuittelevision,traffic data collection systems, 24 hour customercare, SOS posts and meteorological stations and

other safety systems. There are fast road patrols for collectinglostitems,providingearlyassistanceandwarningsofanyaccidentsand there isanefficientwinterservicebasedon24hourmonitoringofroadandweatherconditions.Trafficismadesafeatroadworks sites through early and efficient warnings,roadmarkingandthesettingupofprotectivefencesincludingTMAs(truckmountedattenuators).

Priority isalwaysgiven to thesafetyofpeopleandgoods travelling throughout themotorwayconces-sion network. This concerns both motorists and lorry drivers,whocanrestinfullyequippedservice and parking areas.

Evaluation and future of road toll concessions / Final Report // 27

3 Description of the ASECAP network

Consistent and continuous investments are made by Concessionaires in research and development of new and more efficient technological systemsaimed to improve safety levels. It is worth under-lining thatmany typesof equipment that arenowefficaciously installed in European road and mo-torway networks have been previously developed

bymotorwaycompanies (e.g.safetybarriers, traf-ficcontrolsystems,signsandmarkings,automaticspeed control systems, etc.). An example is descri-bed in the Case Study 1.

Figuresbelowshowroadsafetytrendsofaccidentand fatality rates (i.e. absolute value / veh-km) 14.

Figure 10– Fatality rate 2012

Figure 9– Accident rate 2012

Source: ASECAP, national reports, Performance Survey 2014

Source: ASECAP, national reports, Performance Survey 2014

12.0

10.0

8.0

6.0

4.0

2.0

0.0

0.8

0.7

0.6

0.5

0.4

0.3

0.2

0.1

0

Aust

ria

Cro

atia

Den

mar

k

Fran

ce

Gre

ece

Hun

gary

Irel

and

Italy

The

Net

herla

nds

Pola

nd

Port

ugal

Slov

enia

Spai

n

Uni

ted

Kig

dom

Aust

ria

Cro

atia

Den

mar

k

Fran

ce

Gre

ece

Hun

gary

Irel

and

Italy

The

Net

herla

nds

Pola

nd

Port

ugal

Slov

enia

Spai

n

Uni

ted

Kig

dom

Data refer to accidents with injuriesData of Norway and Serbia are not available

Data of Norway and Serbia are not available

14Itshouldbenotedthattheaccidentrateitishighlyinfluencedbythelocalmethodsofstatisticalsurveys(i.e.themeaningof“accident”maybedifferentbetweenthevariouscountries).Accordingly,foramorereliablecomparison,itisrecommendedtoconsiderthefatalityrates.

Valu

e / 1

00 m

ln v

eh-k

mVa

lue

/ 100

mln

veh

-km

Evaluation and future of road toll concessions / Final Report 28 //

3 Description of the ASECAP network

Source: Performance Survey 2014

Besides Denmark and Netherland, where only short specificroadlinksareunderconcession,thelowestaccident and fatality rates are observed in France.

In 2012, Portugal and Italyhave thehighestacci-dent rates (> 8 accidents/100 mln veh-km) but their fatality rates are on average.Croatia, Greece and Hungaryhavethehighestfatalityrates(>0.4fatali-ties/100 mln veh-km).

Intheperiod2004–2013particularlysignificantim-provementsareobservedinallkeycountries.Higherreduction trend of fatality rate are observed in Aus-tria (-76%), Spain (-57%) and Italy(-49%).France, alreadystartingfromgoodsafetyperformances,fur-ther reduced the fatality rate by 16%.

Sincethedistancetravelledbyvehiclesisafigurera-rely available for other road networks, a reliable com-

Figure 11– Evolution of fatality rate (only larger networks)

0.8

0.7

0.6

0.5

0.4

0.3

0.2

0.1

France

ItalyPortugal

Spain

Austria

15ASFA–Motorwaysafety/Fatalaccidents/Keyfigures(2013)16 APCAP–Asvantagensdeviajaremautoestradas(2013)

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

parison between safety rates on motorway and road network is not feasible. However, few cases have been subject to specific analyses: ASFA (France)15 and APCAP (Portugal)16 estimates that the level of safety on motorways is 4 to 5 timeshigherthanfortherestoftheroadnetwork(thePortuguesecaseisreported in detail in the Case Study 2).

Table 4 compares the evolution of fatalities on the motorways with the rest of the road network in three countries. The performance of the motorway networks is significantlybetter.The roadsafety im-provementisabout10%higheronthemotorways.It is worth to underline that ASECAP network has met the objective of the European Commission to halve the number of fatalities in 10 years, a couple of years before the rest of the network.

Table 4 – Road safety evolution 2002/2012: comparison between No. of fatalities on road and motorway networks

Road network Motorway network

Country 2002 2012 D% 2002 2012 D%

Austria 956 531 -44% 152 59 -61%

France 7,655 3,653 -52% 328 143 -56%

Italy 6,980 3,653 -48% 625 250 -60%Source: European Commission, national reports

Evaluation and future of road toll concessions / Final Report // 29

3 Description of the ASECAP network

The Safety Tutor is a system developed by Autos-trade per l’Italia and made available since 2005 to theItaliantrafficpolicetorecord,onthebasisofthetimespenttocoveragivendistance,theaverage speed of a vehicle.

The Safety Tutor has been installed on stretches of the Italian motorway network with a mortality rate overtheaverage.Itallowsspeedingsanctionstobeissuedautomaticallyanddonotrequire theactualpresenceoftrafficpoliceonthemotorway.

Thevehicles’averagespeedismonitoredinalllanesoverlongsectionsofthemotorway(generally10to25kminlength).Thesystemisoperationalunderall

weatherconditions(fog,rain,etc.)dayandnight.Itcandetectvehiclestravellingwiththeirlightsofforin the emergency lane, twooccurrences that putthe safety of other motorists at risk, for which sanc-tions are particularly severe.

The system, in force on over 2,500 km of the Italian motorway network, has had a significantimpact on reducing average speed (-15%), maximum speed (-25%),and,asaconsequence, accidents rates17:

• Fatality rate: -51% • Injury rate: -27% • Accidents rate: -19%

Figure 12 – Safety Tutor: how it works

Source:Infotraffico.autovie.it

Case Study 1 - The ‘Safety Tutor’ project in Italy

ORA / TIME - 15:05:35TARGA/NUMBER PLATE - AA 000 ZZTIPO/TYPE - AUTOVETURRA

ORA / TIME - 15:15:00TARGA/NUMBER PLATE - AA 000 ZZTIPO/TYPE - AUTOVETURRAVELOCITA / SPEED -

120,00 km >

ORA / TIME - 15:05:30TARGA/NUMBER PLATE - XX 999 YYTIPO/TYPE - AUTOVETURRA

ORA / TIME - 15:10:35TARGA/NUMBER PLATE - XX 999 YYTIPO/TYPE - AUTOVETURRAVELOCITA / SPEED -

180,00 km >SANZIONE/SANCTION

15 km

17Datareferredtothefirst12monthsofoperation.

Evaluation and future of road toll concessions / Final Report 30 //

3 Description of the ASECAP network

Case Study 2 - Benefits to travel on the Portuguese motorway network

APCAP,thePortuguesemotorwayassociation,hasrecently demonstrated the assumption that mo-torways are safer than other roads. This study is contained in the report ‘As vantagens de viajar em autoestradas’(‘Theadvantagesoftravellingonmo-torways’)(June2013).

Just analyzing the recent historical development(Figure below) of traffic and accidents, both onmotorways and national road network, it is plain thatthedifferentialreductionofaccidentsismoresignificantinthemotorwaynetwork.

Figure 13 – Evolution of traffic (blue line) and accidents (green line) on the motorways (left) and other roads (right)

Source: APCAP

Nevertheless APCAP wanted to study in detail this phenomenon and analyzed 10 routes, comparingmotorway trips with those carried out on the ordina-ryroadnetwork.AccidentsandfatalitiesondifferentroutesaresummarizedintheTablebelow.The analysis shows that for all trips, the accident rate on the motorway is lower compared to what

recorded on the alternative road. Sometimes the differencebetweentheaccidentratesinthesetwotypesofrouteisquiteevident,asfortherouteLis-bon - Albufeira, where the fatality rate recorded in alternativeroadismorethan7timeshighertheoneofmotorway.Figurebelowsummarizesgraphicallythese results.

Table 5 – Accident data in selected routes

Route

Accident rate Fatality rate

Road Motorway D % Road Motorway D %

Lisboa - Nazaré 58.5 15.3 -74% 1.1 0.2 -81%

Santarém - Peniche 21.7 7.0 -68% 0.9 0.0 NA

Espinho - Valongo 44.0 13.3 -70% 2.1 0.6 -72%

Cascais - Mem Martins 13.3 10.3 -23% 0.6 0.0 NA

Braga - Apúlia 46.9 5.8 -88% 1.0 0.8 -23%

Lisboa - Tróia 46.6 21.4 -54% 4.1 1.1 -74%

Lisboa - Albufeira 42.7 13.0 -70% 4.7 0.6 -86%

Lisboa - Porto 43.0 12.0 -72% 1.7 0.6 -64%

Porto - Valença 70.0 15.1 -78% 2.6 0.4 -84%

Leiria - Mira 40.2 7.9 -80% 1.4 0.9 -34%

Source: APCAP

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

160140120100806040200C

ircul

açao

Sin

istra

lidad

e

-60%

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Circ

ulaç

ao S

inis

tralid

ade

160140120100806040200

-47%

Evaluation and future of road toll concessions / Final Report // 31

3 Description of the ASECAP network

Case Study 3 – Comparison between toll and non-toll network in Spain

Figure 14 – Comparison of accident (left) and fatality (right) rates between motorways (blue) and other roads (green)

Toll motorways are, in absolute and relative terms, the safest roads of the Spanish road network. In fact, Spain has managed to comfortably exceedthe European Commission’s target of halving thenumber of fatalities in 10 years (from 2001 to 2010), achievinga reductionof61.5% (79.8% ifwe takedata from 2001 to 2012).

Thephysicalandgeometriccharacteristicsoftollmotorways, itsdesignandhigh-qualitymaterialsusedforitsconstruction,itsgoodequipment,theefficient and personalized toll motorway mana-gement,andaregularandperiodicmaintenanceperformed throughout themotorwayconcessionlifecycle,guaranteetheroadsafetystandards.

Case Study 2 - Benefits to travel on the Portuguese motorway network (suite)

Source: APCAP

50454035302520151050

2.5

2

1.5

1

0.5

0

3Xmaior 4X

maior

EN AE EN AE

N° A

ccid

ente

s / 1

08 vkm

s

N° v

ictim

as m

orta

is /

108 v

kms

Figure 15 – Evolution of traffic accidents fatalities in the Spanish road network according to the type of road (1994-2012)

Source: Anuario Estadístico 2012 Ministerio de Fomento

700

600

500

400

300

200

100

0

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

205

34

Tolled motorways Free motorways and expresseways

Evaluation and future of road toll concessions / Final Report 32 //

3 Description of the ASECAP network

Figure 16 – Evolution of traffic accident victims in the Spanish Road Network according to the type of road (1994-2012)

Case Study 3 - Evolution of traffic accidents fatalities in the Spanish road network according to the type of road (1994-2012)

The reduction of fatalities in the State toll road network has been -82.4%, meanwhile a -64.1%

Source: Anuario Estadístico 2012 Ministerio de Fomento

reduction has occurred in free motorway and highways.

9,000

8,000

7,000

6,000

5,000

4,000

3,000

2,000

1,000

0

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Tolled motorways Free motorways and expresseways

The reduction of accidents with victims in the Spani-sh toll motorway network has been -17.3%. Howe-ver, accidents with victims in free motorways and highwayshasincreasedby41.8%.

The table below shows that the toll motorway networkhas,ingeneralterms,adangerousnessrateapproximately half of what the free toll motorways andhighwayshave.

Table 6 – Comparison of dangerousness rate

Toll Motorways Motorways Highways

Fatal accidents rate 0.15 0.26 0.26

Fatalities rate 0.17 0.26 0.29

Dangerousness rate 6.92 12.78 7.5

Evaluation and future of road toll concessions / Final Report // 33

3 Description of the ASECAP network

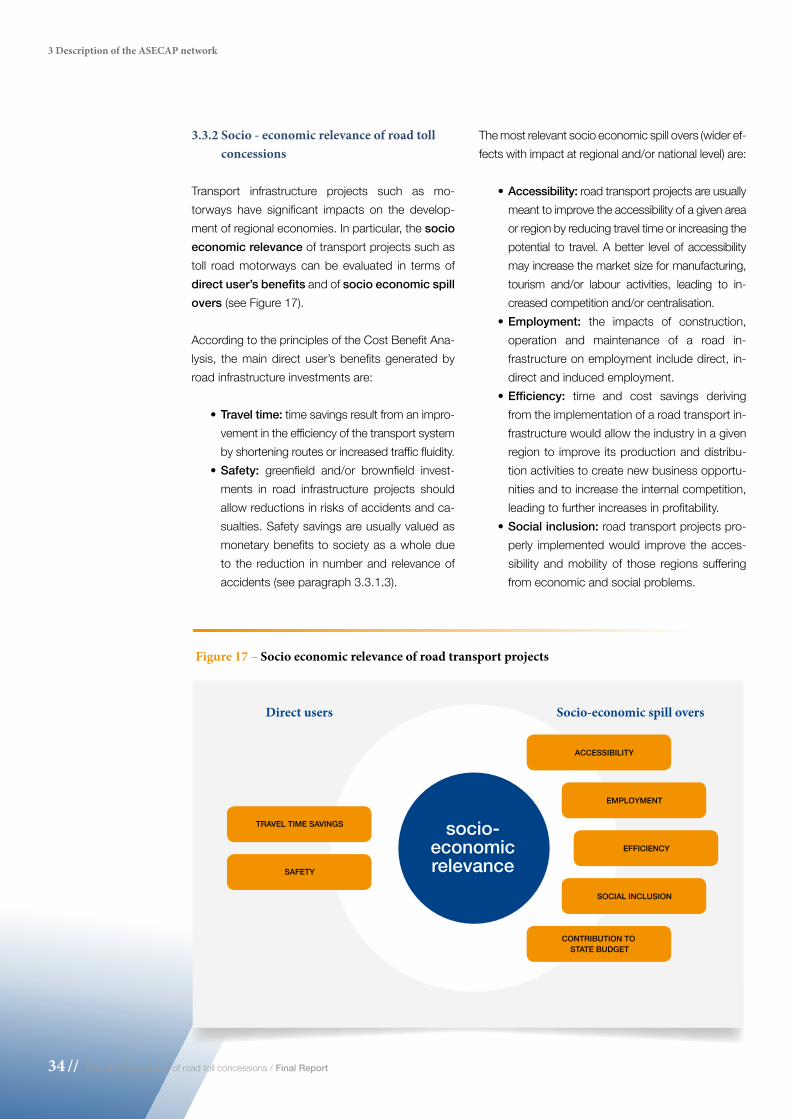

3.3.2 Socio - economic relevance of road toll concessions

Transport infrastructure projects such as mo-torways have significant impacts on the develop-mentofregionaleconomies.Inparticular,thesocio economic relevance of transport projects such as toll road motorways can be evaluated in terms of directuser’sbenefits and of socio economic spill overs(seeFigure17).

AccordingtotheprinciplesoftheCostBenefitAna-lysis, themaindirectuser’sbenefitsgeneratedbyroad infrastructure investments are:

• Travel time:timesavingsresultfromanimpro-vementintheefficiencyofthetransportsystembyshorteningroutesorincreasedtrafficfluidity.

• Safety: greenfield and/or brownfield invest-ments in road infrastructure projects should allow reductions in risks of accidents and ca-sualties.Safetysavingsareusuallyvaluedasmonetarybenefitstosocietyasawholedueto the reduction in number and relevance of accidents(seeparagraph3.3.1.3).

The most relevant socio economic spill overs (wider ef-fectswithimpactatregionaland/ornationallevel)are:

• Accessibility: road transport projects are usually meanttoimprovetheaccessibilityofagivenareaorregionbyreducingtraveltimeorincreasingthepotential to travel. A better level of accessibility mayincreasethemarketsizeformanufacturing,tourism and/or labour activities, leading to in-creased competition and/or centralisation.

• Employment: the impacts of construction, operation and maintenance of a road in-frastructure on employment include direct, in-direct and induced employment.

• Efficiency: time and cost savings derivingfrom the implementation of a road transport in-frastructurewouldallowtheindustryinagivenregionto improve itsproductionanddistribu-tion activities to create new business opportu-nities and to increase the internal competition, leadingtofurtherincreasesinprofitability.

• Social inclusion: road transport projects pro-perly implemented would improve the acces-sibility andmobility of those regions sufferingfrom economic and social problems.

Figure 17 – Socio economic relevance of road transport projects

TRAVEL TIME SAVINGS

SAFETY

ACCESSIBILITY

EMPLOYMENT

EFFICIENCY

SOCIAL INCLUSION

CONTRIBUTION TO STATE BUDGET

socio-economic relevance

Direct users Socio-economic spill overs

Evaluation and future of road toll concessions / Final Report 34 //

3 Description of the ASECAP network

• Contribution to state budget: road infrastruc-tureprojectsgivearelevantcontributiontothenational state budget by means of differentforms of taxation over time, from construction activities to operational ones.

Inordertogiveevidenceoftherelevantcontributionof the road toll concession sector to the development of the road transport network as a whole and to the socio economic improvement at local level, it has tobe investigatedtheyearlyvolumeof investmentsmade by the concessionaires, and the overall contri-butiontostatebudgetandemploymentrateduetothe road concession sector18.

Motorway companies made relevant investments over time in new motorways and in existing onesgeneratingpositive impacts in termsofdirect, indi-rectand inducedvalueaddedat localand regionallevel. Inthefollowingtablesthe investments innewmotorways(seeFigure18)andinexistingones(seeFigure19)inthelast10yearsarereported.

In theperiod2004–2013, the total amountof in-vestments in new motorways with regard to thesample of respondent ASECAP members was about 28,598 MEUR19. Italy is the country that invested more in the reference period: 14,120 MEUR as total amount invested in the reference period.

Further, several ASECAP members planned future investments in new motorways:

• Italy planned investments for about 16,000MEURfortheperiod2013–2020;

• France planned investments for about 1,800 MEUR by 2014;

• Slovenia planned investments for about 320MEURfortheperiod2014–2016;

• Portugal planned investments for about 280 MEUR by 2014;

• Austria planned investments in new and in existing infrastructure for about 4,500 MEURfortheperiod2014–2019.

Figure 18 – Past investments in new motorways in the last 10 years (millions €/year)*

* Source: Performance Survey 2014DataregardingAustriaalsoincludepastinvestmentsinexistingmotorways

2,500

2,000

1,500

1,000

500

0