A FINAL PROJECT REPORT ON “EVA AS A FINANCIAL PERFORMANCE MEASUREMENT TOOL IN CASE OF SMALL MEDIUM SCALE ENTERPRISES ” In partial fulfillment of the requirement for the degree Of Master of Business Administration Specialization- Finance Submitted By: Gourav Sharma 94512236916 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

A

FINAL PROJECT REPORT

ON

“EVA AS A FINANCIAL PERFORMANCE MEASUREMENT TOOL IN CASE OF SMALL

MEDIUM SCALE ENTERPRISES”

In partial fulfillment of the requirement for the degree

Of

Master of Business Administration

Specialization- Finance

Submitted By:

Gourav Sharma

94512236916

Submitted To:

Dr. Navjot Kaur

(2009-2011)

1

ACKNOWLEDGEMENT

I am extremely thankful to Dr. NAVJOT KAUR, Faculty Guide,

GIAN JYOTI INSTITUTE OF MANAGEMENT AND TECHNOLOGY,

for her timely guidance and support throughout the Final Report work. In the

course of carrying out the Project work she help me out to understand the

various terms and working of economic value added as performance

measurement tool for small & medium scale enterprises.

Finally I am indebted to our other faculty members, my friends who

gave their full-fledged co-operation for successful completion of my project.

It was an indeed a learning experience for me.

Name of the Student: Gourav Sharma

Enrollment No.: 94512236916

2

Introduction

3

1.1 Introduction

EVA is a value based financial performance measure, an investment decision tool and a

performance measure reflecting the absolute amount of shareholder value created. It is

computed as the product of the “excess return” made on an investment or investments

and the capital invested in that investment or investments. EVA is the net operating

profit minus an appropriate charge for the opportunity cost of all capital invested in an

enterprise or project. It is an estimate of true economic profit, or the amount by which

earnings exceed or fall short of the required minimum rate of return investors could

get by investing in other securities of comparable risk (Stewart, 1990).

EVA is not new. Residual income, an accounting performance measure, is defined to be

operating profit with a capital charge subtracted. Thus, EVA is a variant of residual

income, with adjustments to how one calculates income and capital. Stern Stewart

& Co, a consulting firm based in New York, introduced the concept of EVA as a

measurement tool in 1989, and trademarked it. The EVA concept is often called

Economic Profit (EP) to avoid problems caused by the trade marking. EVA is so popular

and well known that all residual income concepts are often called EVA even though they

do not include the main elements defined by Stern Stewart & Co (Pinto, 2001). Up to

1970 residual income did not get wide publicity and it was not the prime

performance measure for companies (Makelainen, 1998). However, in the 1990’s,

the creation of shareholder value has become recognized as the ultimate economic

purpose of a corporation. Firms focus on building, operating and harvesting new

4

businesses and/or products that will provide a greater return than the firm’s cost of

capital, thus ensuring maximization of shareholder value. EVA is a strategy

formulation and a financial performance management tool that helps companies make a

return greater than the firm’s cost of capital. Firms adopt this concept to track their

financial position and to guide management decisions regarding resource allocation,

capital budgeting and acquisition analysis.

Economic Value Added simply balances a company's profitability against the capital it

employs to generate this profitability. If a company's earnings, after tax, exceed the cost

of the capital employed in the business, EVA is positive. Market studies have indicated

that a company that continually generates an increasingly positive EVA will be rewarded

by a higher stock price. A definition of EVA is net operating profit after taxes (NOPAT),

less an internal charge for the capital employed in the business (i.e., opportunity cost of

capital).

Many of the traditional corporate performance measures have been found to poorly

correlate, or even conflict, with management's primary objective of maximizing the

market value of a firm's stock. Now, there are several new measures in the financial

world that attempt to align the behaviors of an organization with its stockholders'

interests. One measure that has received a great deal of notice and acceptance is

Economic Value Added (EVA), developed by Joel M. Stern and G. Bennett Stewart III of

Stern Stewart & Co.

Implementation of one of these measures, such as EVA, can fundamentally change the

behavior of an entire organization. The new measure focuses the behavior of individuals

throughout all parts of the organization in a way that is better aligned with creating

stockholder wealth. Because performance compensation incentives are based upon the

new measure, employees and stockholders mutually benefit.

The financial function is uniquely qualified to take a leadership role in communicating an

understanding of the new measure. Main challenge is to gain a deep understanding of the

underlying principles of the measure and to communicate them in a meaningful way to all

5

parts of the organization. There can be pitfalls in translating the theory to practice, but

there is an opportunity to provide the appropriate counsel.

Economic Value Added (EVA) has become all the rage in the investing world. Stern

Stewart has gone so far as to trademark the concept, though many academics challenge it

as a knock-off of residual income. Stern Stewart has, however, been very successful

touting the measure as the best measure of business performance and management

discipline. Fortune Magazine annually publishes a list of top companies complete with

and EVA numbers and rankings, crediting the measures for the creation (or destruction)

of shareholder wealth. The Journal of Applied Corporate Finance annually publishes the

EVA for the Stern Stewart Performance 1000, citing EVA as "the critical driver of a

company's stock performance". Successful corporations are increasingly turning to EVA

to measure performance. General Electric, AT&T, Chrysler, and Compaq use EVA for

financial analysis. Coca Cola's late CEO, Roberto Goizueta, acknowledged the value of

EVA and declared "You only get richer if you invest money at a higher rate than the cost

of the money to you" (Fisher, 1995). In turn, investors and analysts are now scrutinizing

company EVA just as they have historically observed EPS and PE ratios. Academic

articles relating EVA success stories and promoting adoption of the measure abound

(Blair, 1996; Byrne, 1994; Carr, 1996; Copeland and Meenan, 1994; Gressle, 1996; Tully

1993; Stern 1990; Rice, 1996; Pallerito, 1997; Martin, 1996).

As described by Stern Stewart, EVA is net operating profit minus an appropriate charge

for the opportunity cost of all capital invested in an enterprise. In effect, it estimates the

economic profit (or loss) of a company's operations. Traditional accounting measures

such as EPS and ROA measure economic performance, but ignore the cost of the capital.

Including the cost of capital, as EVA does, reveals whether any economic value was

created. This forces management to focus on managing the company's assets as well as

creating income.

How does EVA promote shareholder interests? First, it clearly specifies to management

that the primary financial objective of the company is to create shareholder wealth.

Secondly, it emphasizes continuous improvement in the company's EVA as the basis for

6

increased shareholder wealth. Assuming the efficient market hypothesis holds, stock

price reflects the company's current performance; therefore, the level of EVA isn't

important, but changes in that level are. Management focus on these two issues can result

in dramatically increasing EVA.

Rising EVA has been purported to cause stock price to rise, therefore satisfying

shareholder interests. Does a relationship between EVA and stock return really exist?

James Meenan, CFO of AT&T's long distance business believes that it does. According

to Meenan, his company's EVA and stock price have had an almost perfect correlation

since 1984 (Fortune, 1993). Detractors are not as enthusiastic. Corporate strategy expert

Gary Hamel argues that while EVA is a good place to start, it is not an adequate way to

measure a company's wealth creation (Hamel and Lieber 1993). In 1995, Daniel Saint of

Chrysler stated, "as a single period measure of financial performance, I believe EVA's

contribution is minimal and not much different from return on equity or other traditional

accounting measures" (Kramer and Pushner, 1997). In truth, empirical evidence

supporting the relationship between EVA and stock return is sketchy at best.

1.2 What is Performance Measurement (PM)?

Investors measure overall performance of a firm as a whole to decide whether to invest in

the firm or to continue with the firm or to exit from it. In order to achieve goal

congruence, managers’ compensation is often linked with the performance of the

responsibility centers and also with firm-performance. Therefore selection of the right

measure is critical to the success of a firm. To measure performance of a firm one needed

a simple method for correctly measuring value created/ enhanced by it in a given

time frame. All the current metrics trade off between the precision in measuring the value

and its cost of measurement. In other words, each method takes into consideration the

degree of complexities in quantifying the underlying measure. The more complex is the

process, the more is the level of subjectivity and cost in measuring the performance of

the firm. There is a continuous endeavor to develop a single measure that captures

the overall performance, yet it is easy to calculate.

7

Each metric of performance claims its superiority over others. Performance of a firm is

usually measured with reference to its past record and the performance of other

firms with comparable risk profile. The various performance metrics currently in use are

based on the returns on investment generated by the business entity . Therefore to

reach a meaningful conclusion, returns generated by the firm in a particular year

should be compared with returns generated by assets with similar risk profile

(cross sectional analysis). Similarly return on investment for the current period should be

compared with returns generated in past (time series analysis). A firm creates value only

if it is able to generate return higher than its cost of capital. Cost of capital is the

weighted average cost of equity and debt (WACC).

The performance of a firm gets reflected on its valuation by the capital market. Market

valuation reflects investor’s perception about the current performance of the firm

and also their expectation on its future performance. They build their expectations

on the estimated growth of the business in terms of return on capital. This

results in incongruence between current performance and the value of the firm. Even

if the current performance is better in relative terms, poor growth prospects adversely

affects the value of the firm. Therefore any metric of performance, to be effective,

should be able to not only capture the current performance but also should be able to

incorporate the direction and magnitude of future growth. Therefore the robustness of a

measure is borne out by the degree of correlation the particular metric has with respect

to the market valuation. Perfect correlation is impossible because as shown by empirical

researchers, fundamentals of a company cannot fully explain its market capitalization;

other factors such as speculative activities, market sentiments and macro-economic

factors influence movement in share prices. However the superiority of a performance

metric over others lies in providing better information to investors.

Metrics of performance have a very important and critical role not only in evaluating the

current performance of a firm but also in achieving high performance and growth in the

future. The metrics of performance have a variety of users, which include all the

stakeholders whose well being depends on the continued well being of the firm. Principal

stakeholders are the equity holders, debt holders, management, and suppliers of material

8

and services, employees and the end-users of the products and services. Value creation and

maximization depends on the alignment of the various conflicting interests of these

stakeholders towards a common goal. This means maximization of the firm value without

jeopardizing the interests of any of the stakeholders. Any metric, which measures the

firm value without being biased towards any of the stakeholders or particular class

of participants, can be hailed as the true metric of performance. However it is difficult, if

not impossible, to develop such a metric. Most of the conventional performance measures

directly relate to the current net income of a business entity with equity, total assets, net

sales or similar surrogates of inputs or outputs. Examples of such measures are return on

equity (ROE), return on assets (ROA) and operating profit margin. ROA measures the

asset productivity and operating profit margin reflects the margin realized by the firm

at the market place. The net income figure in itself is dependent on the operational

efficiency, financial leverage and the ability of the entity to formulate right strategy

to earn adequate margin in the market place.

It is important to note that none of these measures truly reflect the complete picture

by themselves but have to be seen in conjunction with other metrics. These

measures are also plagued by the firm level inconsistencies in the accounting

figures as well as the inconsistencies in the valuation methods used by

accountants in measuring assets, liabilities and income of the firm. Accounting

valuation methods are in variance with the methods that are being used to value

individual projects and firms. The value of an asset or a firm, which is a collection

of assets, is computed by discounting future stream of cash flows. The net present

value (NPV) is the surplus that the investment is expected to generate over the cost of

capital. Measures of periodical performance of a firm, which is the collection of assets

in place, should follow the same underlying principles. Economic value added (EVA) is

a measure that captures the valuation principles.

Historically, PM systems was developed as a means of monitoring and maintaining

organizational control, which is the process of ensuring that an organization pursues

strategies that lead to the achievement of overall goals and objectives (Nanni, et al 1990).

9

PM plays a vital role in every organization as it is often viewed as a forward-looking

system of measurements that assist managers to predict the company's economic

performance and spot the need for changes in operations. In addition, PM can provide

managers, supervisors and operators with information required for making daily

judgments and decisions. PM is increasingly used by organizations, as it enables them to

ensure that they are achieving continuous improvements in their operations in order to

sustain a competitive edge, increase market share and increase profits.

1.3 Traditional measures

Accounts for the costs associated with capital and help firms spot areas in which capital

is being invested unprofitably. Although these financial data have the advantage of being

precise and objective, the limitations are far greater, making them less applicable in

today's competitive market. Organisations, that have adopted the traditional PM, have

experienced great difficulty in trying to fit the measures with increasing new business

environment and current competitive realities.

While the traditional financial metrics are value-based, they are nonetheless lagging

indicators. They offer little help for forward-looking investments, where future earnings

and capital requirements are largely unknown investments such as new product

introductions and capital or new market entry. This will lead to narrow short-term

decision-making based on bottom-line financial results.

On the other hand, most of the criticism of traditional PM stems from their failure to

measure and monitor multiple dimensions of performance, by concentrating almost

exclusively on financial measure (Brignall and Ballantine, 1996). They solely concentrate

on minimizing costs and increasing labour efficiency while neglecting other operational

performance measures such as quality, responsiveness and flexibility (Skinner, 1974)

Therefore focusing on financials to the exclusion of all other factors can produce

distortions such as low cost and high margin productions unnecessarily.

First let us look into the claim of EVA being superior than the conventional

measures such as ROI, ROE and ROA, which are based on the accounting figures. Most

10

of these measures give us the rate of return earned by the firm with respect to capital

invested in the firm. The most important limitation of these measures are derived

from limitations inherent in the measurement of accounting profit. As per current

accounting practices, while historical-cost-based accounting measures are being

used to carry most of the assets in the balance sheet, revenue and expenses (other than

depreciation) are recognized in the profit and loss account at their current value.

Therefore accounting rate of returns do not reflect the true return from an investment

and tend to be biased downwards in the initial years and upward in the latter years.

Similarly as noted by Malkelainen (Esa Malkelainen 1998), distortion occurs basically

due to the historical cost and straight line depreciation schedule used by most

businesses to value their assets. This leads to a bias in these measures due to the

composition of assets of a firm at any given point in time.

By composition he refers to the current nature of the assets, more current the assets are,

the accounting rate of return is closer to the true rate of return. This distortion will not be

significant if there is a continuous stream of investments in assets i.e. the value of the mix

of assets is nearer to the current value of the assets. But the probability, that at any point

of time, a firm should have such a composition of assets is rare, in most cases either the

assets are old or relatively new. This precludes these accounting measures from being

used to reach any meaningful conclusion regarding the true performance of the firm. The

other important limitation of accounting measures is that they ignore the cost of

equity and only consider the borrowing cost. As a result it ignores the risk inherent in the

project and fails to highlight whether the return is commensurate with the risk of

the underlying assets. This might result in selecting projects that produce attractive rate of

return but destroys firm value because their cost of capital is higher than the benchmark

return established by the management. On the other hand accounting measures encourage

managers to select projects that will improve the current rate of return and to

ignore projects even if their return is higher than their cost of capital. Selection of

projects with returns higher than the current rate of return does not automatically

increase shareholders’ wealth. Taking up only those projects, which provide returns

that are higher than the hurdle rate (cost of capital) results in increasing the

11

wealth of the shareholder. Therefore use of ROE, ROA or similar accounting

measures as the benchmark, might result in selection of those projects that though

provide rate of return higher than the current rate of return destroys firm-value. Similarly

use of these measures result in continuing with activities that destroys firm value until the

rate of return falls below the benchmark rate of return.

However, despite the criticisms made on traditional financial measure, many companies

still use them to measure performance. Many organizations, even until the end of 1970s,

operate performance under central control, through large functional department. Thus,

allowing managers to use slow-reacting and tactical management control system such as

'budgets'. These budgeting measures mainly focus on short-term value creation as it only

attempts to control and improve existing operations. However budgeting systems are

inflexible for today's dynamic and rapidly changing environment organizations still

continue to use them. This is because implementing new measures designed to manage

strategy and not control is very difficult.

Moreover, most companies motivate their worker through reward system. Rewards can

be financial such as cash payments, bonuses or share options and non-financial such as

promotion. Traditionally, employees are rewarded with bonuses at the end of the year

once a specific target has been achieved. However, this reward system causes short-

term’s as employees are seen to narrow down their focus by just targeting the 'rewarded'

goal. They may not take other factors, such as quality and service into consideration.

Hence leading businesses to run without long-term vision.

1.4 EVA (Economic Value Added)

EVA (Economic Value Added) was developed by a New York Consulting firm, Stern

Steward & Co in 1982 to promote value-maximizing behaviour in corporate managers

(O'Hanlon. J & Peasnell. K, 1998). It is a single, value-based measure that was intended

to evaluate business strategies, capital projects and to maximize long-term shareholders

wealth. Value that has been created or destroyed by the firm during the period can be

measured by comparing profits with the cost of capital used to produce them. Therefore,

12

managers can decide to withdraw value-destructive activities and invest in projects that

are critical to shareholder's wealth. This will lead to an increase in the market value of the

company. However, activities that do not increase shareholders value might be critical to

customer's satisfaction or social responsibility. For example, acquiring expensive

technology to ensure that the environment is not polluted might not be of high value from

a shareholder's perspective. Focusing solely on shareholder's wealth might jeopardize a

firm reputation and profitability in the long run.

EVA sets managerial performance target and links it to reward systems. The single goal

of maximizing shareholder value helps to overcome the traditional measure problem,

where different measures are used for different purposes with inconsistent standards and

goal. Rewards will be given to managers who are able to turn investor's money and

capital into profits efficiently. Researches have found that managers are more likely to

respond to EVA incentives when making financial, operational and investing decision

(Biddle, Gary, Managerial finance 1998), allowing them to be motivated to behave like

owners. However this behaviour might lead to some managers pursuing their own goal

and shareholder value at the expense of customer satisfaction.

Unlike simple traditional budgeting, EVA focuses on ends and not means as it does not

state how manager can increase company's value as long as the shareholders wealth are

maximized. This allowed managers to have discretion and free range creativity, avoiding

any potential dysfunctional short-term behaviour. Rewards such as bonuses from the

attainment of EVA target level are usually paid fully at the end of 3 years. This is because

workers' performance is monitored and will only be rewarded when this target is

maintained consistently. Hence, leading to long-term shareholders' wealth.

Cola-Cola is one of the many companies that adopted EVA for measuring its

performance. Its aim, which was to create shareholders wealth, was announced in its

annual report. Coca-Cola CEO Roberto Goizueta accredited EVA for turning Coca-Cola

into the number one Market Value Added Company. Coca-Cola's stock price increased

from $3 to over $60 when it first adopted EVA in the early 1980s. In 1995, Coca-Cola's

investor received $8.63 wealth for every dollar they invested.

13

Most companies refer to stock price increase as an outcome of implementing EVA.

However, empirical studies have found that traditional accounting measure have provided

a similar, or even better result in increasing stock performance (Dodd J and Johns J 'EVA

reconsidered').

EVA is a financial measure based on accounting data and is therefore historical in nature.

It has the same limitations as other traditional accounting measures and cannot

adequately replace all measures within the company especially the non-financial ones.

Due to the historical nature of EVA, manager can benefit in terms of rewards or be

punished by the past history of the organization (Otley, David Performance management

1999). Dodd J and Johns J see the balanced scorecard as one approach to overcome the

potential problem of using a single financial measure such as EVA.

1.4.1 The background of EVA

EVA is not a new discovery. An accounting performance measure called residual income

is defined to be operating profit subtracted with capital charge. EVA is thus one variation

of residual income with adjustments to how one calculates income and capital. According

to Wallace (1997) one of the earliest to mention the residual income concept was Alfred

Marshall in 1890. Marshall defined economic profit as total net gains less the interest on

invested capital at the current rate. According to Dodd & Chen (1996) the idea of residual

income appeared first in accounting theory literature early in this century by e.g. Church

in 1917 and by Scovell in 1924 and appeared in management accounting literature in the

1960s. Also Finnish academics and financial press discussed the concept as early as in

the 1970s. It was defined as a good way to complement ROI-control (Virtanen 1975).

Knowing this background many academics have been wondering about the big publicity

and praise that has surrounded EVA in the recent years. The EVA-concept is often called

Economic Profit (EP) in order to avoid problems caused by the trademarking. On the

other hand the name "EVA" is so popular and well known that often all residual income

concepts are often called EVA although they do not include even the main elements

defined by Stern Stewart & Co. For example, hardly any of those Finnish companies that

have adopted EVA calculate rate of return based on the beginning capital as Stewart has

14

defined it, because average capital is in practice a better estimate of the capital employed.

So they do not actually use EVA but other residual income measure. This insignificance

detail is ignored later on in order to avoid more serious misconceptions. It is justified to

say that the EVA concept, Finnish companies are using corresponds virtually the EVA

defined by Stern Stewart & Co.

In the 1970s or earlier residual income did not got wide publicity and it did not end up to

be the prime performance measure in great deal of companies. However EVA, practically

the same concept with a different name, has done it in the recent years. Furthermore the

spreading of EVA and other residual income measures does not look to be on a

weakening trend. On the contrary the number of companies adopting EVA is increasing

rapidly (Nuelle 1996, Wallace 1997, and Economist). It can only be a guess why residual

income did never gain a popularity of this scale. One of the possible reasons is that

Economic value added (EVA) was marketed with a concept of Market value added

(MVA) and it did offer a theoretically sound link to market valuations. In the times when

investors demand focus on Shareholder value issues this was a good bite. Perhaps also

pertinent marketing by Stern Stewart & Co. had and has its contribution.

In some previous conducted researches, EVA was verified to suffer from the same

accounting distortions as any accounting rate of return (e.g. ROI). Therefore EVA might

in some occasions give somewhat misleading signals of the true value added to

shareholders. In spite of this fact EVA has become a very popular performance measure,

perhaps because applying it has some powerful impacts on organizational behavior.

Unlike conventional profitability measures EVA helps the management and also other

employees to understand the cost of equity capital. At least in big public companies,

which do not have a strong owner, shareholders have often been conceived as a free

source of funds. Similarly, business unit managers often seem to think that they have the

right to invest all the retained earnings that their business unit has accumulated although

the group would have better investment opportunities elsewhere. EVA might change the

attitude in this sense because it emphasizes the requirement to earn sufficient return on all

capital employed.

15

Including capital costs in the income statement helps everybody in the organization to see

the true costs of capital. Rate of return does not work that way because nobody can

explicitly see the costs caused by e.g. inventories, receivables etc. The approaches

showing the consequences of invested capital under the line as profit (with ROI) or over

the line as cost (with EVA) are totally different. That is why organizations tend to

increase their capital turnover after introducing EVA, although they have formerly used

ROI that ought to take into account the capital as well. When calculating EVA, the cost

of equity (and debt) can be subtracted in the income statement earlier than after the net

operating profit. If all the revenues and costs are grouped by functions or by processes,

then it is of course practical to allocate the capital costs to these functions or processes.

The capital costs can also be allocated directly to products. Parts of the capital costs are

variable in nature (inventories, trade receivables) and thus they fluctuate according to the

sales volume. If the true capital costs were not included fully in product costs, then those

cost calculations (for price determination) are misleading. The error is the bigger, the

more capital intensive the production is.

At best EVA can be a new approach to view business. Perhaps the biggest benefit of this

approach is to get the employees and mangers to think and act like shareholders. It

emphasizes that in order to justify investments in the long run they have to produce at

least a return that covers the cost of capital. In other case the shareholders would be better

off investing elsewhere. This approach includes that the organization tries to operate

without lazy or excess capital and it is understood that the ultimate aim of the firm is to

create shareholder value by enlarging the product of positive spread (between return and

cost of capital) multiplied with the capital employed. The approach creates a new focus

on minimizing the capital tied to operations. Firms have so far done a lot in cutting costs

but cutting excess capital has been paid less attention. The power of EVA-approach is

something that most academic studies about EVA and share price correlation fail to trace.

The only way to assess the effects of this approach is to compare two sample groups,

other representing firms that use EVA and other firms that do not.

There are countless individual operational things that create shareholder value and

increase EVA. Often EVA does not directly help in finding ways to improve operational

16

efficiency except when improving capital turnover. Nor does EVA help directly in

finding strategic advantages that enable a company to earn abnormal returns and thus

create shareholder value. It is however often helpful to understand the basic ways in

which EVA and thus the wealth of shareholders can be improved.

Increasing EVA falls always into one of the following three categories:

1) Rate of return increases with the existing capital base. It means that more operating

profits are generated without tying any more capital in the business.

2) Additional capital is invested in business earning more than the cost of capital.

(Making NPV positive investments.)

3) Capital is withdrawn or liquidated from businesses that fail to earn return greater than

the cost of capital.

The first method includes all the countless ways to improve operating efficiency or

increase revenues. Of course increasing rate of return with current operations and new

investments (that is categories 1 and 2) are often linked; in order to improve the

efficiency of ongoing operations, companies often do investments which enhance also the

return on current capital base.

The fact that the wealth of shareholders increase with investments returning more that the

cost of capital (category 2) is probably known in organizations if they also use some kind

of weighted average cost of capital (WACC) and Net present value (NPV) methodology

in investment calculations. This rule is actually completely same as accepting only NPV-

positive investments.

The third category, withdrawing capital, is probably not so widely understood and

applied as the previous ones. It is however also very important to realize that shareholder

value can also be increased if capital is withdrawn from businesses earning less than the

cost of capital. Even if an operation has positive net income, it might pay to withdraw

capital from that activity. It is also kind of withdrawal when access inventories and

17

receivables and thus the capital costs caused by them are reduced without corresponding

decreases in revenues.

These categories and ways to improve EVA might appear to be quite simple. They are

certainly not new ways to improve the position of shareholders. Decreasing cost of

capital is not included in this list of methods. That is because it can not normally be done

without changing line of business and in that way changing business risk. Changing

financial leverage affects WACC only slightly via increased tax shield.

1.4.2 Indian context

In India EVA is being used with impunity. A case at point is the study published by

Economic times (11th December 2000) ,on corporate performance. While computing

EVA it used a flat rate of 15 percent as the cost of capital of all the enterprises included

in the study. The study explains that an average 15 percent interest for both the

years covered by the study is used as it is almost equal to the prime-lending rate

of the commercial bank and financial institution. It is a basic principle of economics

that ‘higher the risk higher is the expected return’. By estimating WACC at 15% this

basic principle is violated. It may be argued that cost of debt should be taken

post-tax and therefore effective cost of equity incorporated in the calculation is higher

than 15 percent. Even if this argument is accepted the computation cannot be defended

because the cost of capital is estimated without using any accepted economic model.

Moreover by using a flat rate, variation in risk profiles of firms have been ignored.

This shows both the popularity of EVA in India and difficulties in measuring the

same. The study has also ignored adjustments in capital and operating income suggested

by proponents of EVA

1.5 ECONOMIC VALUE ADDED – the concept

EVA is the most misunderstood term among the practitioners of corporate finance. The

proponents of EVA are presenting it as the wonder drug of the millennium in overcoming

all corporate ills at one stroke and ultimately help in increasing the wealth of the

18

shareholder, which is synonymous with the maximization of the firm value. The

attractiveness of the EVA lies in its use of cash flow and cost of capital that are

determinant of the value of the firm.

In the process, EVA is being bandied about with utmost impunity by all and

sundry, which includes the popular press. The academic world in its turn has come

up with various empirical studies which either supports the superiority of EVA or

questions the claim of its proponents. Currently the empirical evidence is split almost half

way.

EVA is nothing but a new version of the age-old residual income concept recognized by

economists since the 1770's. Both EVA and ‘residual income’ concepts are based on the

principle that a firm creates wealth for its owners only if it generates surplus over the cost

of the total invested capital. So what is new? Perhaps EVA could bring back the lost

focus on ‘economic surpluses from the current emphasis on accounting profit. In a lighter

vein it can be said that in an era where commercial sponsorship is the ticket to

the popularity of even the concept of god, the concept of residual income has not found a

good sponsor until Stern Stewart and Company has adopted it and relaunched it with a

brand new name of EVA.

Technically speaking EVA is nothing but the residual income after factoring the cost of

capital into net operating profit after tax. But this is only the tip of the iceberg as will be

seen in the next few sections. The paper examines EVA both as a measure of overall

performance and a management philosophy that helps to improve the productivity

of resources.

Mathematically:

EVA= (adjusted NOPAT - cost of capital) x capital employed----- (I)

Or

EVA = (Rate of return - cost of capital) x capital --------- (II)

19

Where;

Rate of Return = NOPAT/Capital

Capital = total assets minus non interest bearing debt, at the beginning of the year

Cost of capital = cost of equity x proportion of equity + cost of debt (1-tax rate)

x proportion of debt in the capital.

The above cost of capital is nothing but the weighted average cost of capital (WACC).

Cost of equity is normally estimated using capital asset pricing model (CAPM) that

estimates the expected return commensurate with the riskiness of the assets.

If we define ROI as NOPAT/capital then the above equation can be rewritten as

EVA= (ROI- WACC) x CAPITAL EMPLOYED----- (III)

Capital being used in EVA calculation is not the book capital, capital is defined as an

approximation of the economic book value of all cash invested in going-concern business

activities, capital is essentially a company’s net assets (total assets less non-interest-

bearing current liabilities), but with three adjustments:

Marketable securities and construction in progress are subtracted.

The present value of non-capitalized leases is added to net property, plant,

and equipment.

Certain equity equivalent reserves are added to assets:

Bad debt reserve is added to receivables.

LIFO reserve is added to inventories.

The cumulative amortization of goodwill is added back to goodwill

R&D expense is capitalized as a long-term asset and smoothly depreciated over

5 years (a period chosen to approximate the economic life typical of an

investment in R&D).

20

Cumulative unusual losses (gains) after taxes are considered to be a long-

term investment.

A firm can motivate its managers to direct their effort towards maximizing the value of the

firm only by, first measuring the firm value correctly and secondly by providing

incentives to managers to create value. Both are interdependent and they complement

each other. Therefore this paper examines the EVA concept from two perspectives, EVA

as a performance measure and EVA as a corporate philosophy.

I shall examine EVA as a performance measure to assess whether it conveys any

additional information to investors over conventional performance measures. In

other words, whether information on EVA leads to better decision by investors.

EVA can lend a helping hand in this connection in two ways: one that it is

inherently flexible and second, it helps generate flexibility within the organization:

1. The EVA concept allows adjustment of various accounting parameters (mentioned in

section on EVA theory) to suit the desired end purpose. There can be various purposes

for which EVA exercise might be carried out such as award of bonus to employees,

relative performance of various divisions, assessment of business as a whole etc. For the

purpose of award of bonus to employees, the focus is on the operational income and

capital employed to generate such income. Various accounting adjustments are made

accordingly. However, for the purpose of assessment of business as a whole, the strategic

investment and its returns also come into picture. While comparing various divisions, the

capital employed and expenses incurred on corporate centre take a back seat Thus, EVA

concept provides flexibility in hands of finance manager in measuring performance. In

the case study discussed later, we have discussed EVA from the point of view of award

of bonus.

2. Not only is EVA concept inherently flexible, but also it induces flexibility in the

organization. The application of concept forces the organization to release/ free the

excess capital employed. This deployment of excess capital provides the much-required

flexibility to finance manager to improve performance. Since application of concept

21

questions every decision harder, it forces the managers to keep exploring options and

encourages keeping the system flexible. This effect is more pronounced in companies

which are in distress, and where restructuring is being carried out.

1.5.1 Implementing EVA

Implementing EVA should be more than just adding one line in the monthly profit report.

EVA affects the way capital is viewed and therefore, it might create some kind of change

in management's attitude. Of course this depends on how shareholder-value-focused the

management is and how the company has been in the past. While implementing EVA

represents some kind of change in the organization, it should be implemented with care in

order to achieve understanding and commitment.

It is vital that group level managers thoroughly understand the characteristics of the

concept, how these characteristics affect control and above all where the Strategic

Business Units (SBUs) stand currently from the viewpoint of these characteristics. Before

implementing EVA to any SBU, the group management ought to assess whether the

business units are currently cash flow generators in mature businesses or companies in

rapidly growing businesses. This assessment should absolutely include careful estimation

of relative age and structure of assets in order to know whether the current accounting

rate of return is over or under estimating the true rate of return. Only then can the concept

be properly tailored to the unique situation of each individual business unit. Group level

managers should also know how to support strategic goals of SBU with EVA and how to

create value with EVA in individual SBU.

At the level of SBU, gaining understanding and commitment are also the most important

issues. First task is to get the support of all the managers, not only of the Managing

Director but also of directors of production and marketing etc. This is achieved with

intense and thorough training. For managerial level, attaining thorough commitment can

be facilitated very much by introducing good incentive plan based on EVA.

Gaining commitment of middle level managers and other employees below the top

management of business unit is also important. Training and some kind of EVA based

22

compensation plans should also be considered with these target groups. Keeping EVA

simple is also viewed as an important feature in successful implementation. In principle,

EVA is simple concept and it should be offered to business units as such.

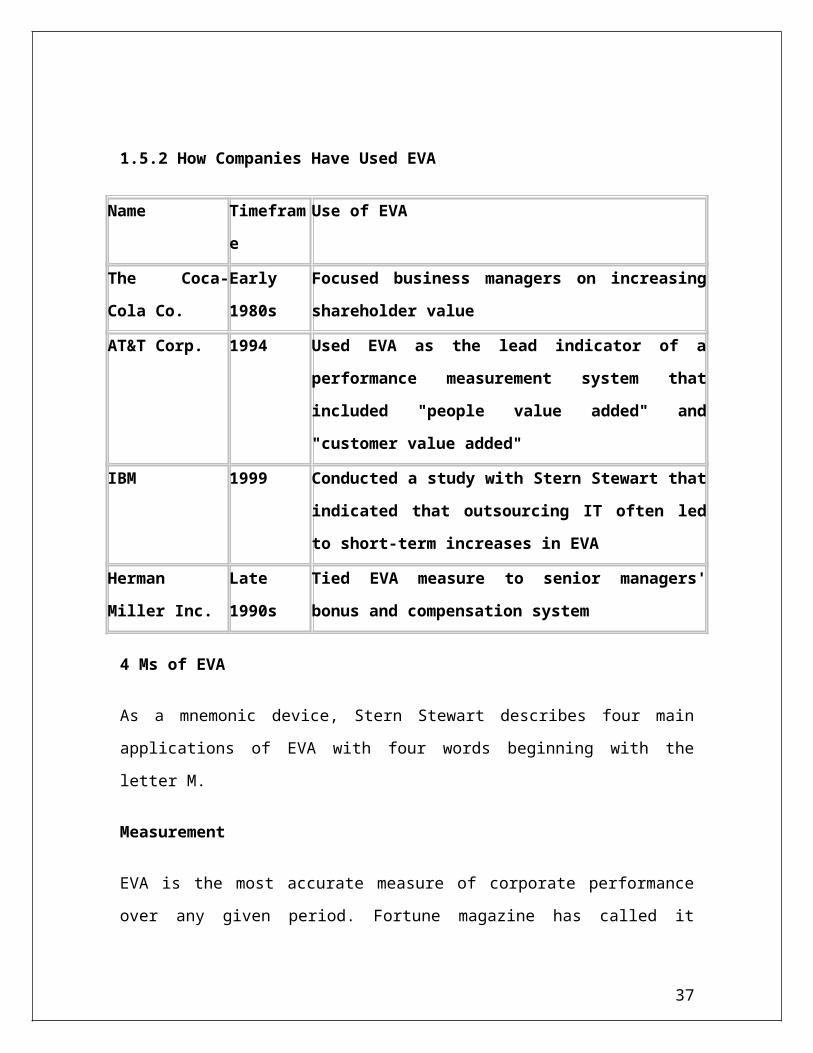

1.5.2 How Companies Have Used EVA

Name Timeframe Use of EVA

The Coca-Cola

Co.

Early 1980s Focused business managers on increasing shareholder

value

AT&T Corp. 1994 Used EVA as the lead indicator of a performance

measurement system that included "people value added"

and "customer value added"

IBM 1999 Conducted a study with Stern Stewart that indicated that

outsourcing IT often led to short-term increases in EVA

Herman Miller

Inc.

Late 1990s Tied EVA measure to senior managers' bonus and

compensation system

4 Ms of EVA

As a mnemonic device, Stern Stewart describes four main applications of EVA with four

words beginning with the letter M.

Measurement

EVA is the most accurate measure of corporate performance over any given period.

Fortune magazine has called it "today's hottest financial idea," and Peter Drucker rightly

23

observed in the Harvard Business Review that EVA is a measure of "total factor

productivity" whose growing popularity reflects the new demands of the information age.

Management System

While simply measuring EVA can give companies a better focus on how they are

performing, its true value comes in using it as the foundation for a comprehensive

financial management system that encompasses all the policies, procedures, methods and

measures that guide operations and strategy. The EVA system covers the full range of

managerial decisions, including strategic planning, allocating capital, pricing acquisitions

or divestitures, setting annual goals-even day-to-day operating decisions. In all cases, the

goal of increasing EVA is paramount.

Motivation

To instill both the sense of urgency and the long-term perspective of an owner, Stern

Stewart designs cash bonus plans that cause managers to think like and act like owners

because they are paid like owners. Indeed, basing incentive compensation on

improvements in EVA is the source of the greatest power in the EVA system. Under an

EVA bonus plan, the only way managers can make more money for themselves is by

creating even greater value for shareholders. This makes it possible to have bonus plans

with no upside limits. In fact, under EVA the greater the bonus for managers, the happier

shareholders will be.

Mindset

When implemented in its totality, the EVA financial management and incentive

compensation system transforms a corporate culture. By putting all financial and

operating functions on the same basis, the EVA system effectively provides a common

language for employees across all corporate functions. EVA facilitates communication

and cooperation among divisions and departments, it links strategic planning with the

operating divisions, and it eliminates much of the mistrust that typically exists between

operations and finance. The EVA framework is, in effect, a system of internal corporate

governance that automatically guides all managers and employees and propels them to

24

work for the best interests of the owners. The EVA system also facilitates decentralized

decision making because it holds managers responsible for-and rewards them for-

delivering value.

1.5.3 The EVA Concept of Profitability

EVA is based on the concept that a successful firm should earn at least its cost of capital.

Firms that earn higher returns than financing costs benefit shareholders and account for

increased shareholder value. In its simplest form, EVA can be expressed as the following

equation:

EVA = Net Operating Profit after Tax (NOPAT) - Cost of Capital

NOPAT is calculated as net operating income after depreciation, adjusted for items that

move the profit measure closer to an economic measure of profitability. Adjustments

include such items as: additions for interest expense after-taxes (including any implied

interest expense on operating leases); increases in net capitalized R&D expenses;

increases in the LIFO reserve; and goodwill amortization. Adjustments made to operating

earnings for these items reflect the investments made by the firm or capital employed to

achieve those profits. Stern Stewart has identified as many as 164 items for potential

adjustment, but often only a few adjustments are necessary to provide a good measure of

EVA.

Recently, the Economic Valued Added method has gained attention worldwide. This

method is intuitively appealing and measures profitability in the way shareholders define

it.

Economic Value Added calculates the actual dollar amount of a business's wealth created

or destroyed in each reporting period. It takes into account the opportunity cost (the

minimum acceptable compensation for investing in a risky asset as opposed to a less

risky market instrument like government bonds) of the company's capital investment and

measures the excess returns over this charge.

25

A positive Economic Value Added indicates that value is being created; so adding to the

intrinsic value of the company by that amount. A negative Economic Value Added, on

the other hand, indicates that value is eroded and the company is now worth less than the

initial capital employed.

Measurement of EVA

Measurement of EVA can be made using either an operating or financing approach.

Under the operating approach, NOPAT is derived by deducting cash operating expenses

and depreciation from sales. Interest expense is excluded because it is considered as a

financing charge. Adjustments, which are referred to as equity equivalent adjustments,

are designed to reflect economic reality and move income and capital to a more

economically-based value. These adjustments are considered with cash taxes deducted to

arrive at NOPAT. EVA is then measured by deducting the company's cost of capital from

the NOPAT value. The amount of capital to be used in the EVA calculations is the same

under either the operating or financing approach, but is calculated differently.

The operating approach starts with assets and builds up to invested capital, including

adjustments for economically derived equity equivalent values. The financing approach,

on the other hand, starts with debt and adds all equity and equity equivalents to arrive at

invested capital. Finally, the weighted average cost of capital, based on the relative values

of debt and equity and their respective cost rates, is used to arrive at the cost of capital

which is multiplied by the capital employed and deducted from the NOPAT value. The

resulting amount is the current period's EVA.

1.6 There are eight steps involve in applying Economic Value Added to value a

company:

Step 1: Determining a period of financial projection. To calculate returns on capital

employed, we first need to estimate the company's earnings; for instance, in the next five

years to 2016. The earnings projection is based on a set of assumptions for future volume

sales growth, finished product prices, government duties and inflation.

26

Step 2: Net operating profit after tax (NOPAT): Net operating profit after tax is

equivalent to the after tax earnings generated by the company (excluding interest

expense). The financing of asset (interest expense) is assumed to be independent of

operating results and is instead reflected in the company's cost of capital.

Step 3: Initial capital employed: The total capital employed at the beginning of each year

is the assets base from which earnings for the year are generated.

Capital employed = Net fixed assets + Working capital

Step 4: Return on capital employed (ROCE) the yearly returns on capital employed are

determined by dividing NOPAT by capital employed at the beginning of each year.

ROCE = NOPAT ÷ Capital employed

Step 5: Weighted average cost of capital (WACC) after calculating the Returns on

Investment (ROI), match them to the cost of capital. The most commonly used cost of

capital is the WACC, which is based on the company's debt equity capital structure.

WACC = Weighted cost of equity + Weighted after tax cost of debt

After tax cost of debt = [Interest payment x (1-tax rate)] ÷ Total borrowings

How big a risk premium required for investing in a company is dependent on how risky

the stock is relative to the broad market; which known as correlation beta. A high beta

implies the stock price is more volatile than the broad market. Therefore, an investor

should require a higher than market average return to compensate for the additional risks.

Conversely, a low beta implies that the stock returns will lag a market rally but will be

more resilient during a sell down.

Step 6: Excess returns over cost of capital

Excess returns (ER) = ROCE - WACC

27

Step 7: Economic Value Added and Market Value Added (MVA)

Economic Value Added = ER x Capital employed

Beyond the projected period of 2016, impute a terminal value (perpetuity); on the basis

that the company is an ongoing business concern (for the stream of future Economic

Value Added, assuming a constant yearly growth of 1%).

The stream of Economic Value Added is then discounted back to present day values

using the WACC calculated previously, the sum of which is the positive value created by

the company's business operations.

MVA = Sum of present value of Economic Value Added stream.

Step 8: Intrinsic value and shareholder value. The intrinsic value for the company is its

initial capital employed enhanced by the positive value created.

Intrinsic market value = Initial capital employed + MVA

And finally,

Shareholder value = Intrinsic market value - Net debt

Fair value per share = Shareholders' value ÷ Number of shares

The company's primary objective would be to maximize Economic Value Added; which

is not necessarily the same as maximizing profits. If the return on an investment is below

its cost of capital, then the company prefers not to make the investment at all (even if the

absolute magnitude of profit is increased).

1.6.1 EVA Calculation and Adjustments

As stated above, EVA is measured as NOPAT less a firm's cost of capital. NOPAT is

obtained by adding interest expense after tax back to net income after-taxes, because

28

interest is considered a capital charge for EVA. Interest expense will be included as part

of capital charges in the after-tax cost of debt calculation.

Other items that may require adjustment depend on company-specific activities. For

example, when operating leases rather than financing leases are employed, interest

expense is not recorded on the income statement, nor is a liability for future lease

payments recognized on the balance sheet. Thus, while interest is implicit in the yearly

lease payments, an attempt is not made to distinguish it as a financing activity under

GAAP.

Under EVA, however, the interest portion of the payment is estimated and the after-tax

amount from it is added back into NOPAT because the interest amount is considered a

capital charge rather than an operating expense. The corresponding present value of

future lease payments represents equity equivalents for purposes of capital employed by

the firm, and an adjustment for capital is also required.

R&D expense items call for careful evaluation and adjustment. While GAAP generally

requires most R&D expenditures to be expensed immediately, EVA capitalizes

successful R&D efforts and amortizes the amount over the period benefiting the

successful R&D effort.

Other adjustments recommended by Stern Stewart include the amortization of goodwill.

The annual amortization is added back for earnings measurement, while the accumulated

amount of amortization is added back to equity equivalents. Goodwill amortization is

handled in this manner because by "unamortizing" goodwill, the rate of return reflects the

true cash-on-yield. In addition, the decision to include the accumulated goodwill in

capital improves the real cost of acquiring another firm's assets regardless of the manner

in which the acquisition is accounted.

While the above adjustments are common in EVA calculations, according to Stern

Stewart, those items to be considered for adjustment should be based on the following

criteria:

29

Materiality: Adjustments should make a material difference in EVA.

Manageability: Adjustments should impact future decisions.

Definitiveness: Adjustments should be definitive and objectively determined.

Simplicity: Adjustments should not be too complex.

If an item meets all four of the criteria, it should be considered for adjustment. For

example, the impact on EVA is usually minimal for firms having small amounts of

operating leases. Under these conditions, it would be reasonable to ignore this item in the

calculation of EVA. Furthermore, adjustments for items such as deferred taxes and

various types of reserves (i.e. warranty expense, etc.) would be typical in the calculation

of EVA, although the materiality for these items should be considered. Unusual gains or

losses should also be examined and eliminated if appropriate. This last item is

particularly important as it relates to EVA-based compensation plans.

1.6.2 EVA at Work

Although economic value added is considered to be the kingpin of value-based metrics, it

won't work in an organization if a CEO doesn't force implementation throughout the

company or if incentive-based compensation isn't offered. And a pure EVA bonus plan

won't necessarily work at the middle and lower levels of a company, making it difficult to

preach the EVA gospel throughout an organization.

Stern Stewart & Co., a New York-based financial consulting firm which has trademarked

the term EVA, promotes the idea that economic value added is a financial performance

measure that comes closer than any other to capturing the true economic profit of an

enterprise. "The formula for EVA looks formidable, but it's really not," says Stern

Stewart vice president Tom Leander. "EVA is net operating profit minus an appropriate

charge for the opportunity cost of all capital invested in an enterprise. In simple terms,

EVA equals net operating profit after taxes — we use the acronym NOPAT."

Stern Stewart calculates what the economic value added for a company is and then

decides from what business centers the EVA will be calculated. Once the measurement is

made, the firm works with the finance department to show employees how EVA can be

30

used as an internal measure. The next and most obvious step is tying that measurement to

incentive compensation.

"Under classic economic theory, a problem exists in that managers' interests are not

aligned with the interests of the owners," Leander says. "But one of the aspects of EVA is

that managers must think and act like owners of the company. The underlying principle

here is that unless managers are motivated to think and feel like they're owners of the

company, they're not going to create value in a way that benefits shareholders."

EVA is about working smarter, not harder. It's about doing such things as reducing the

number of steps in a work process, reducing cycle times or scrutinizing business

expenses. Economic value added can be improved in three basic ways:

1. Growth: Invest in projects that earn more than the cost of capital. For example,

investing in personal computers, which frequently increase efficiency and justify

a minimal investment?

2. Improved productivity: Increase profits without using additional capital and/or

eliminate business expenses which can help improve income.

3. Divestiture: Eliminate non-strategic assets that do not generate operating profits

greater than the cost of capital. Examples include the reduction of inventory levels

and speeding up cycle times. Many companies which use EVA have found this to

be the most attractive method.

According to Stern Stewart, a key to weaving EVA into the corporate culture is to make

it the focal point for reporting, planning and decision-making. To do that requires two

things: The first is recognizing that, because economic value added is a measure of total

factor productivity, it can and should supersede other financial and operating measures,

resulting in a hierarchy as opposed to a balanced scorecard. The balanced scorecard

results when financial numbers are not the only consideration used to make strategic

decisions. For example, if you're manufacturing a product, a balanced scorecard weighs

factors such as financial impact, quality, customer satisfaction and productivity. If EVA

is merely added to a list of many other performance measures, confusion and unnecessary

31

complexity will remain. The second requirement is that EVA be incorporated into

decision-making processes.

The fact that such high-profile companies as The Coca-Cola Co. and Briggs & Stratton

have achieved considerable success through the implementation of EVA has prompted a

wave of companies to at least consider the strategy. "You have thought leaders in the

marketplace who are touting this much as they would reengineering," says Tom Hertog,

manager of Chicago-based Arthur Andersen Global Best Practices.

"When people come to us, they're looking for the magic bullet, but as is the case with

benchmarking and best practices, there is a whole host of approaches and no single

solution. But the appropriate and consistent application of EVA methodology will yield

results, regardless of what size company you are or what industry you're in."

Arthur Andersen promotes a four-step process for organizations that want to undertake an

economic value added program:

1. Calculation or formulation: How does one measure the return on capital minus the

cost of capital? This is where most of the focus is directed. Certain aspects of the

EVA calculation include determining the number of capital adjustments, the

number of cost of capital factors, the number of cost centers calculating EVA, and

the number of NOPAT (net operating profit after taxes) adjustments

2. Application: How does one apply EVA in his/her organization, in that particular

line of business? For example, if you're a service organization and you don't have

a tangible product, you still need a performance measurement tool such as EVA to

determine the increase or decrease of value. It's important to set a goal for

increasing EVA as expressed as a percentage for the next 12 months, the next one

to three years, and the next three to five years.

3. Implementation or integration: How does one make EVA part of their

organizational culture? This step includes determining the extent of training

needed for management and staff, the methods by which EVA will be

32

communicated throughout the company, and the time it will take for

implementation at various levels in the organization.

4. Interpretation or correlation: How will EVA impact the future of company?

Organizations obviously want to focus on positive change and sometimes use

MVA (market value added) as a measure of interpretation. MVA can be measured

by taking the current market value placed on the company as reflected in its stock

price and then subtracting the capital invested on the balance sheet.

"It comes down to ABO — awareness, buy-in, and ownership," Hertog says. "One or two

people will rise to the champion level and take ownership and drive it. The business unit

controllers will need to get that message from the CFO that they're going to do EVA. The

way you introduce it and integrate it is absolutely critical for it to gain acceptance.

Otherwise, it never happens

1.7 EVA vs. Traditional Performance Measures

The development of the concept of EVA has added flexibility in measurement of

performance. The traditional methods can continue side by side with EVA. Some of the

traditional ways of measuring corporate performance are described here.

1.7.1 Return on Investment (ROI)

Return on capital is a very good and relatively good performance measure. Different

companies calculate this return with different formulae and call it also with different

names like return on invested capital, return on capital employed, return on net assets,

return on assets etc. The main shortcoming with all these rates of return is that in all cases

maximizing rate of return does not necessarily maximize the return to shareholders.

Following example will clarify this statement:

Suppose a group has two subsidiaries X and Y. For both subsidiaries and so for the whole

group the cost of capital is 10%. The group has maximizing ROl as its target. Subsidiary

X has ROl of 15% and the other has ROl of 8%. Both subsidiaries begin to struggle for

the common target and try to maximize their respective ROIs. Company X rejects all the

33

projects that produce a return below the current 15% although there would be some

projects with return 12-13%. Y, in turn, accepts all the projects with return above 8%. For

a reason or another, it does not find very good projects, but the returns of its projects lie

somewhere near 9%.

Suppose that both subsidiaries manage to increase their ROI. The ROI of subsidiary X

increases from 15 to 16% and that of Y increases from 8 to 8.5%. The company's target

to increase ROI has been achieved, but what about the shareholder value. It is obvious

that all the projects of subsidiary Y decrease the shareholder value, because the cost of

capital is more than rate of return (and so the shareholders money would have been better

off with alternative investments). The actions of the better subsidiary are not optimal for

shareholders. Of course shareholders will benefit from the good projects with return

greater than 15% but also all the projects with returns of 10-14% should have been

accepted even though they decrease the current ROl of subsidiary X. These projects still

create and increase the shareholder value.

Hence, the capital can be misallocated on the basis of ROl. ROl ignores the definite

requirement that the rate of return should be at least as high as cost of capital. Further,

ROI does not recognize that shareholder's wealth is not maximized when the rate of

return is maximized. Shareholders want the firm to maximize the absolute return above

the cost of capital and not to increase percentages.

1.7.2 Return on Equity (ROE)

The level of ROE does not tell the owners if company is creating shareholders' wealth or

destroying it. With ROE, this shortcoming is much more severe than with ROI, because

simply increasing leverage can increase the ROE. In other words, decreasing solvency

does not always make shareholders' position better because of the increased financial

risk.

1.7.3 Earning per Share (EPS)

34

EPS is raised simply by investing more capital in business. If the additional capital is

equity (retained earnings) then the EPS will rise if the rate of return of the invested

capital is just positive. For example, let us assume that as on March 31, 2009, company A

has net worth of Rs 50 million and 5 million equity shares. At a profit after tax of Rs 100

million for FY 2009, the EPS would work out to be 20. The entire income can be

ploughed back in the business at a marginal return of 5%. Assuming that the return on

previous net worth remains the same, the profit after tax would be Rs 105 million and

EPS would be 21. Though the performance has gone down, the EPS has increased.

If the additional capital is debt then the EPS will rise if the rate of return of the

invested capital is just above the cost of debt. In reality, the invested capital is a mix of

debt and equity and the EPS will rise if the rate of return on the additional investment is

somewhere between the cost of debt and zero. Therefore EPS is completely inappropriate

measure of corporate performance and still is very common yardstick and even a

common bonus base.

Unlike conventional profitability measures, EVA helps the management and other

employees to understand the cost of equity capital. At least in big companies, which do

not have a strong owner, shareholders have often been perceived as free source of funds.

These flaws are taken care of by the concept of economic value added. The key feature of

this concept is that for the first time any measure takes cares of the opportunity cost of

capital invested in business.

1.8 The Utility of EVA: Better Decision-Making

EVA clarifies the concept of maximizing the absolute returns over and above cost of

capital in creating shareholders' wealth. Hence better investment decisions can be taken

with above aim rather than maximizing percentage of ROl. Understanding of EVA

enables monitoring of investment decisions closely not only at the level of corporate but

at line staff as well.

Fosters New Era of Corporate Control

35

EVA points / centres can be created within an organization and these centres would have

capital, revenue and expenditure issue attached to them. It helps identify value drivers

and destroyers. Responsibility of positive EVA can be delegated at these centres. It

questions the decisions harder.

Long-Term Thinking

Perhaps the biggest benefit of this approach is to get employees and managers to think

and act like shareholders. EVA encourages long-term perspective among the managers

and employees of organization. It emphasizes that in order to justify investments in the

long run they have to produce at least a return that covers the cost of capital. In other

case, the shareholders would be better off investing elsewhere. This approach includes

that the organization tries to operate without the luxury of excess capital and it is

understood that the ultimate aim of the firm is to create shareholder value by enlarging

the product of positive spread multiplied with capital employed. The approach creates a

new focus on minimizing the capital tied to operations. Firms have so far done a lot in

cutting costs but cutting excess capital has been paid less attention.

Capital Allocation Tool

EVA is a capital allocation tool inside a company as it sets minimum level of acceptable

performance with regard to the rate of return in the long run This minimum rate of return

is based on average (risk adjusted) return on equity markets. The average return is a

benchmark that should be reached. If a company cannot achieve the average return, then

the shareholders would be better off if they allocated the capital to another industry or

another company.

Bonus System

EVA has provided a platform on which a flexible bonus payment system can be

based. Employees will be paid bonus only when they earn at least equal to the cost of

capital employed. This links the bonus with the end result and forces employees to act

like shareholders. Proponents of bonus systems based on EVA have suggested that

36

bonuses for corporate managers should always be tied to the long-term capital because

short-term EVA can sometimes be manipulated upwards to the cost of long run EVA The

long run can be incorporated into EVA-based bonuses, that is, by banking the bonuses.

This would mean that when EVA is good, the managers earn a certain percentage of it,

but the bonus should not be paid out of them entirely. If the periodic EVA is negative,

then the bonus put in the bank is negative and it decreases the balance already earned.

This exposes the managers partly to the risk the shareholders are used to bear. At the

same time, it gives incentives to good performers and encourages the bad performers to

improve their performance.

For example, manager earns a bonus of an amount X of the annual salary for leading its

centre to a positive EVA to the extent of 10% of capital employed. Out of the entire

bonus, 50% can be paid out and the rest can be banked as entitlement if the next year

EVA is not negative. In case the EVA next year is negative, the banked bonus can be

reduced as disincentive for bad performance.

Flexibility in EVA

Today's business environment is marked by presence of a lot of change drivers like

globalization, an intense competition, etc and the uncertainty surrounding them has

created chaos and confusion in organizations. Consequently, flexibility has assumed key

role in every facet of organization management and finance function, known for its

rigidity, is not too far from application of this paradigm.

1.9 Small and Medium Enterprises (SMEs)

Small and Medium Enterprises (SMEs) are considered engines for economic growth, not

only in India but all over the world. Small and medium enterprises have played a vital

role in the growth of the Indian economy. Small Scale Industry has a 40% share in

industrial output, producing over 8000 value-added products. They contribute nearly 35%

in direct export and 45% in the overall export from the country. They are one of the

biggest employment-providing sectors after agriculture, providing employment to 28.28

million people. They account for 80% of global economic growth.

37

Market conditions have dramatically changed for Indian SMEs after economic reforms.

SMEs are regularly facing new challenges in terms of cost, quality, delivery, flexibility

and human resource development for their survival and growth. In the context of a

dynamic market scenario, they have to formulate their strategies for developing various

capabilities and competencies to satisfy their domestic as well as global customers.

For long-term competitiveness, SMEs have to focus on all aspects of organizational

functions such as assets, strategy development, processes and their performance. In

Punjab the SMEs have not been growing at the pace at which they should have been as

they have been facing a lot of problems.

Small Scale industrial undertaking is defined as an industrial undertaking in which the

investment in fixed assets in plant and machinery whether held on ownership terms on

lease or on hire purchase does not exceed Rs.50 million (Subject to the condition that the

unit is not owned, controlled or subsidiary of any other industrial undertaking). Small and

medium-size enterprises (SMEs) in India play an important role in generating

employment and creating economic wealth. Small-scale industries play a key role in the

industrialization of a developing country. This is because they provide immediate large-

scale employment and have a comparatively higher labor-capital ratio; they need lower

investments, offer a method of ensuring a more equitable distribution of national income

and facilities an effective mobilization of resources of capital and skill which might

other-wise remain unutilized.

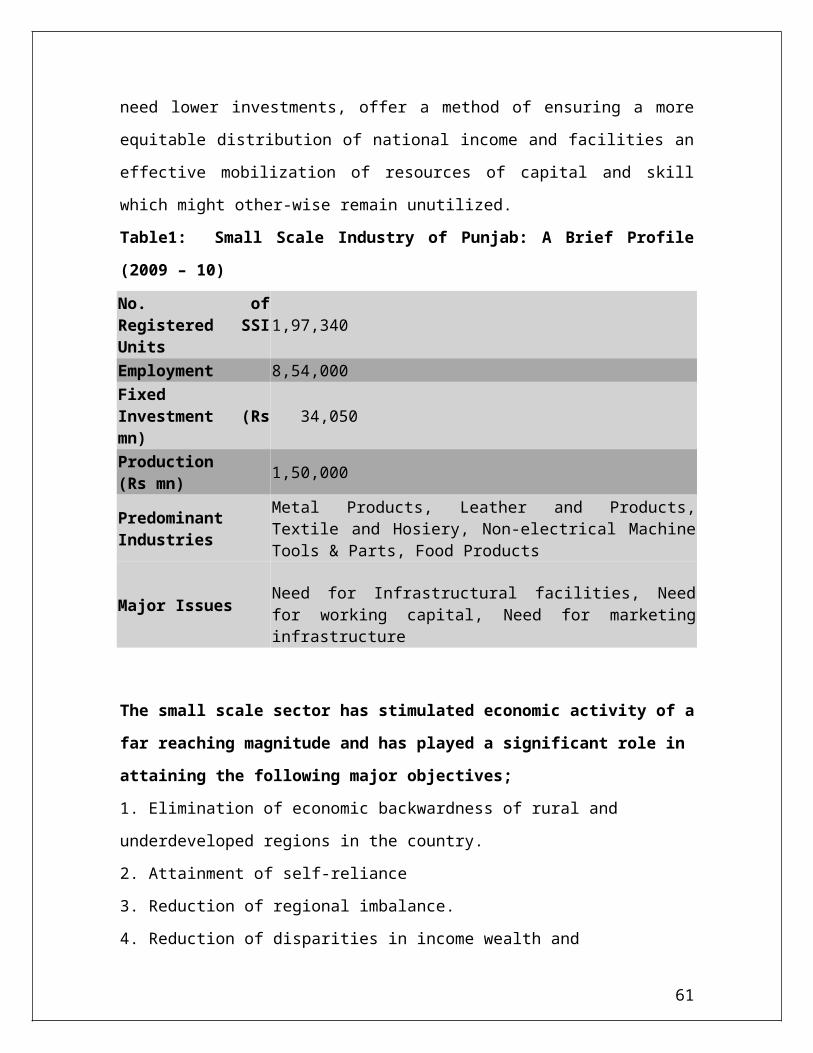

Table1: Small Scale Industry of Punjab: A Brief Profile (2009 – 10)

No. of Registered SSI Units 1,97,340

Employment 8,54,000Fixed Investment (Rs mn) 34,050

Production (Rs mn) 1,50,000Predominant Industries