Pasquale Tridico Jean Monnet Chair in European integration Studies Professor of Labour Economics Department of Economics University Roma Tre [email protected] European Governance and Crisis Responses

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Pasquale Tridico

Jean Monnet Chair in European integration Studies

Professor of Labour Economics

Department of Economics

University Roma Tre

European Governance and Crisis

Responses

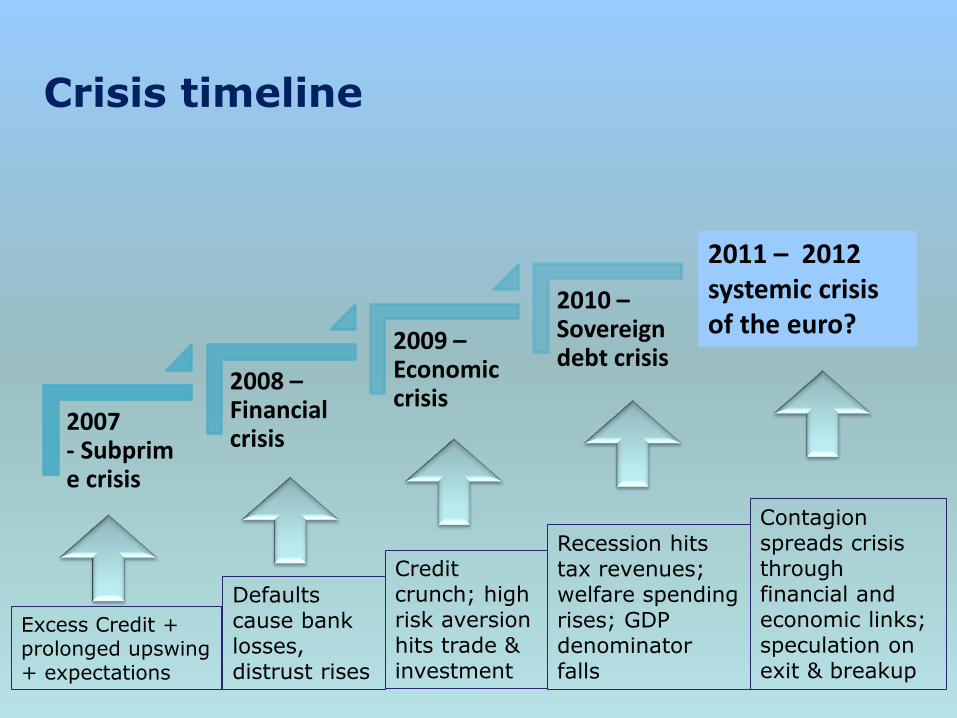

Crisis timeline

2007 - Subprime crisis

2008 – Financial crisis

2009 – Economic crisis

2010 – Sovereign debt crisis

2011 – 2012 systemic crisis of the euro?

Excess Credit + prolonged upswing + expectations

Defaults cause bank losses, distrust rises

Credit crunch; high risk aversion hits trade & investment

Recession hits tax revenues; welfare spending rises; GDP denominator falls

Contagion spreads crisis through financial and economic links; speculation on exit & breakup

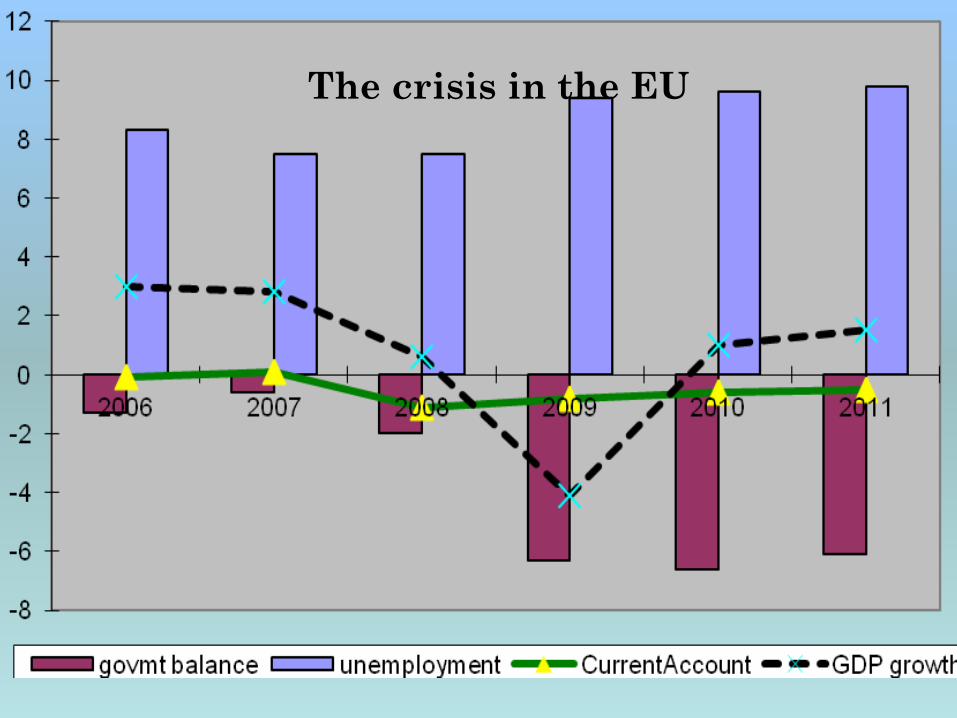

The crisis in the EU

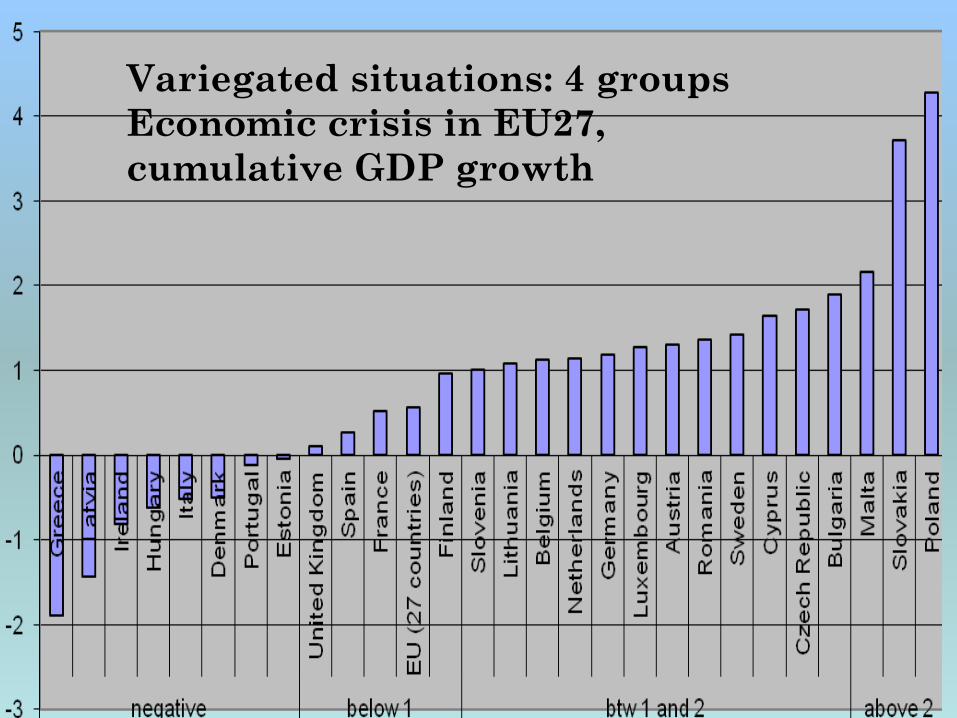

Variegated situations: 4 groups

Economic crisis in EU27,

cumulative GDP growth

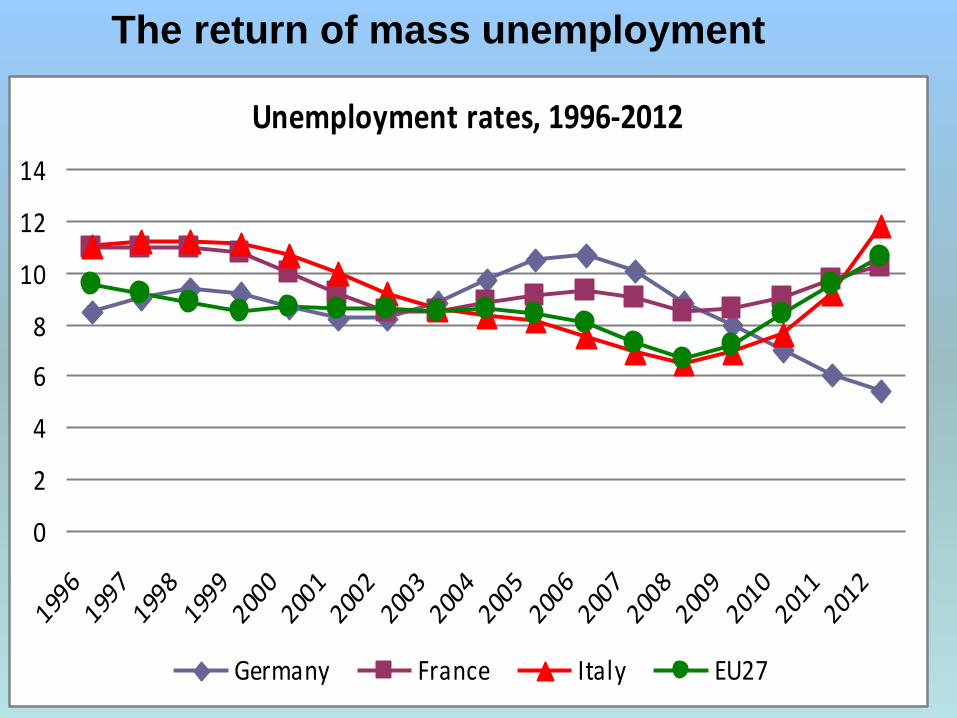

Unemployment rates, 1996-2012

0

2

4

6

8

10

12

14

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Germany France Italy EU27

The return of mass unemployment

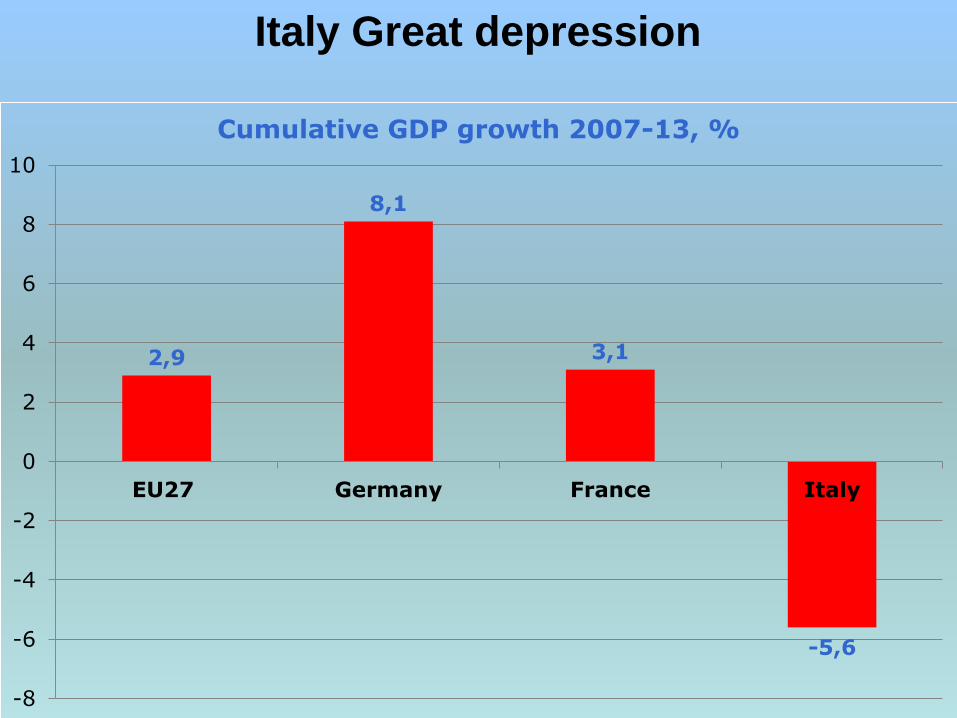

2,9

8,1

3,1

-5,6

-8

-6

-4

-2

0

2

4

6

8

10

EU27 Germany France Italy

Cumulative GDP growth 2007-13, %

Italy Great depression

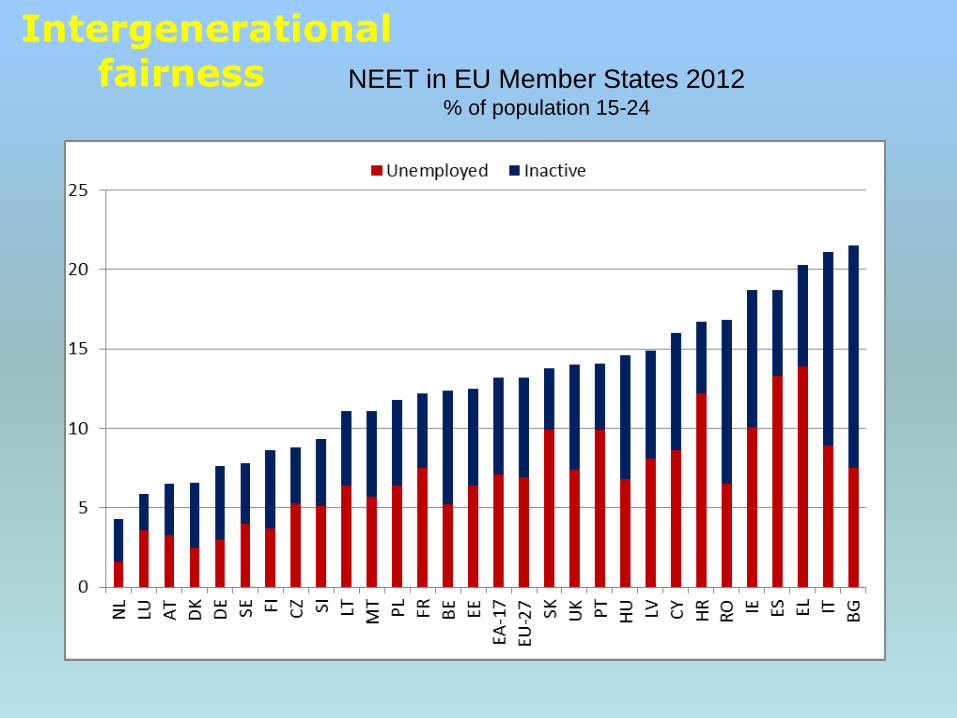

Intergenerational fairness NEET in EU Member States 2012

% of population 15-24

The crisis …

• Building up of a dangerous leverage/debt cycle in

the (global) financial system

• &

• Emerging macro-economic imbalances in the euro

area in the years preceding the financial crisis

• &

• Flaws in the systemic design of EMU

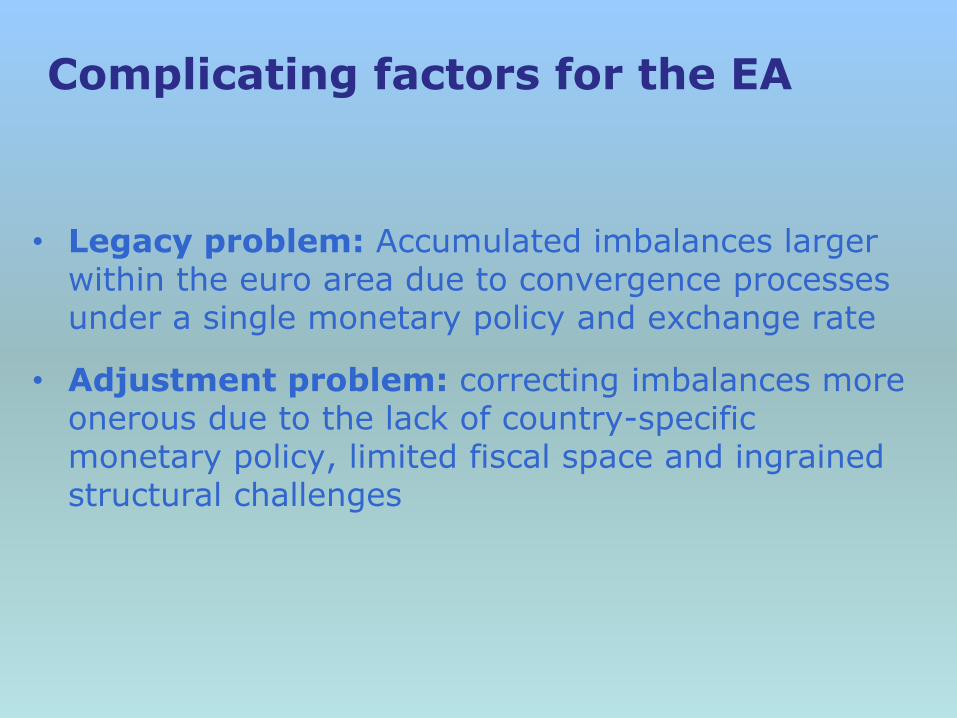

• Legacy problem: Accumulated imbalances larger within the euro area due to convergence processes under a single monetary policy and exchange rate

• Adjustment problem: correcting imbalances more onerous due to the lack of country-specific monetary policy, limited fiscal space and ingrained structural challenges

Complicating factors for the EA

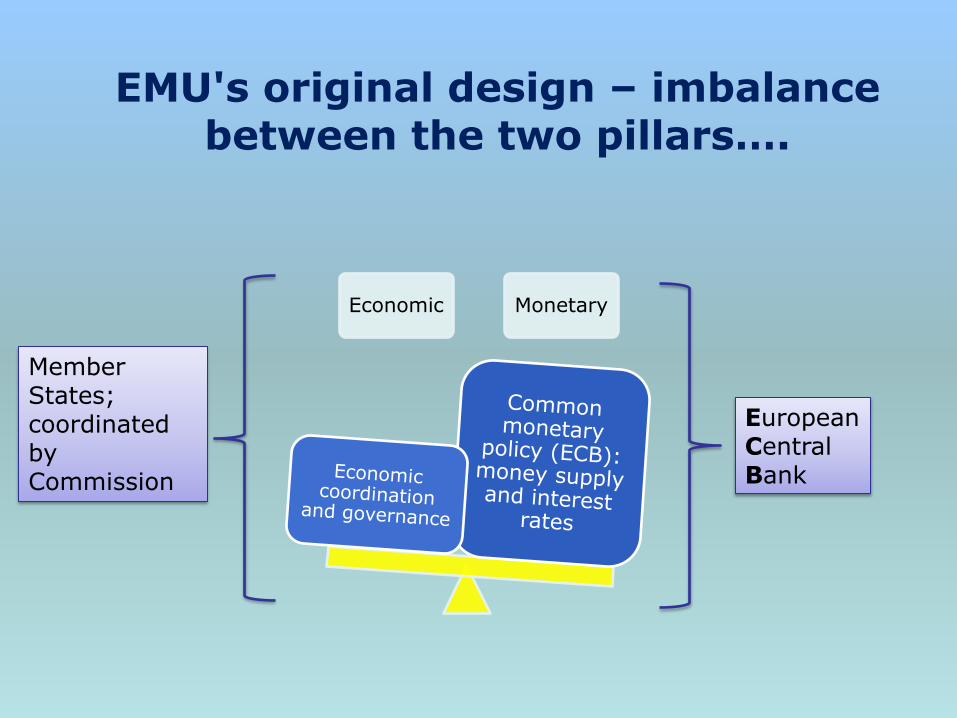

EMU's original design – imbalance between the two pillars….

Economic Monetary

European Central Bank

Member States; coordinated by Commission

• No formal lender of last resort or other quasi-fiscal capacity to deal with sovereign liquidity and solvency crises

• Missing an integrated financial framework for banking supervision and resolution, esp. of cross-border banking giants

• No surveillance and coordination tools apart from SGP and (non-binding) Broad Economic Policy Guidelines (BEPGs).

…and an incomplete architecture

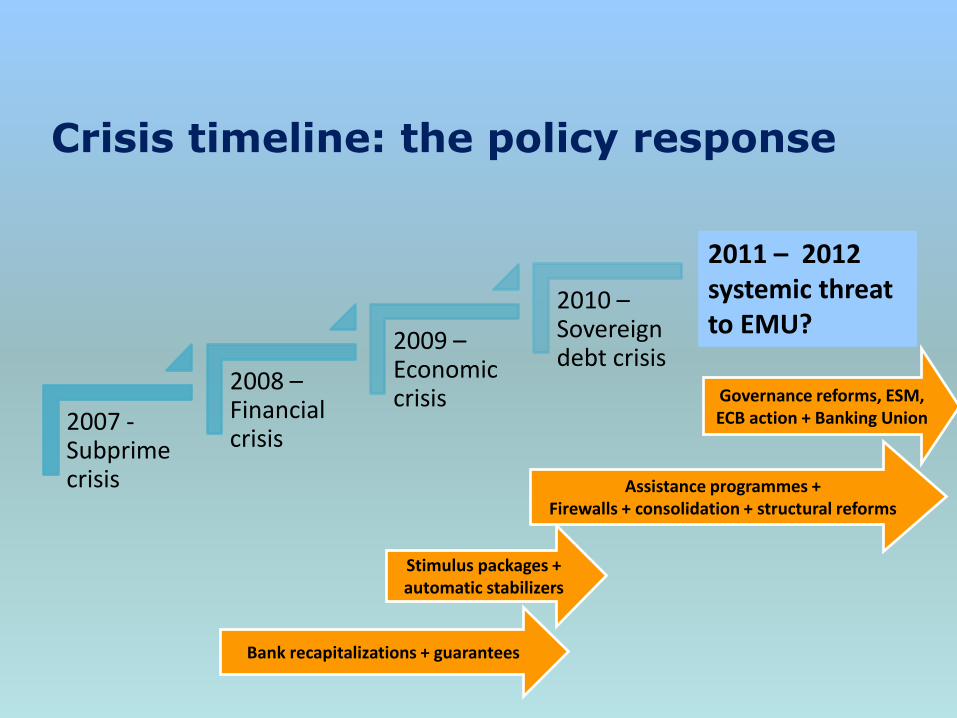

Crisis timeline: the policy response

2007 - Subprime crisis

2008 – Financial crisis

2009 – Economic crisis

2010 – Sovereign debt crisis

Stimulus packages + automatic stabilizers

2011 – 2012 systemic threat to EMU?

Assistance programmes + Firewalls + consolidation + structural reforms

Bank recapitalizations + guarantees

Governance reforms, ESM, ECB action + Banking Union

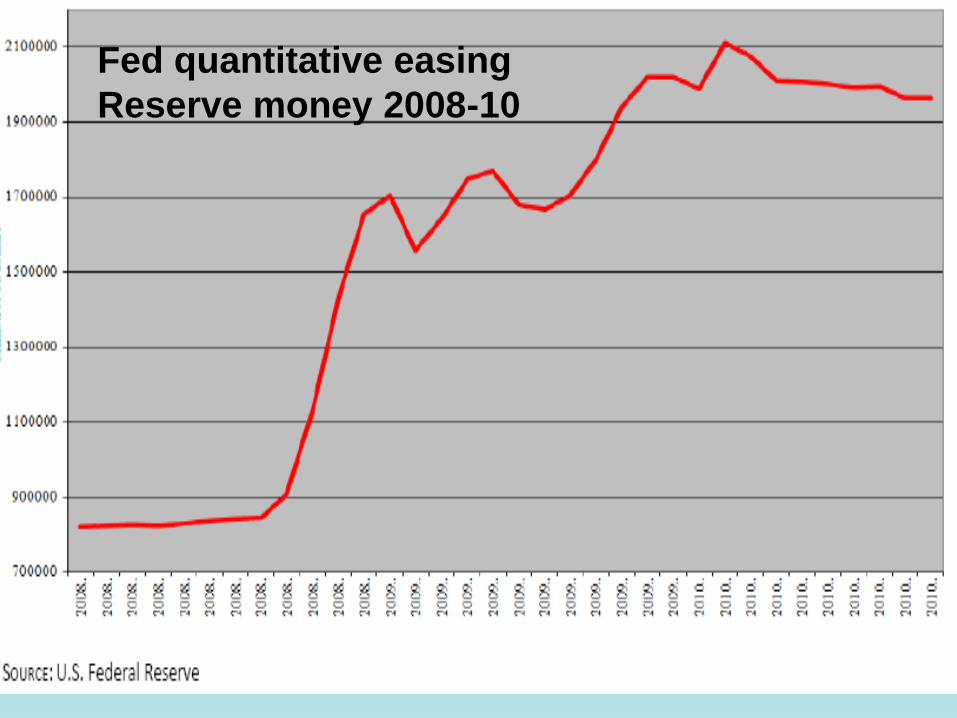

Fed quantitative easing

Reserve money 2008-10

0

1

2

3

4

5

6

2006 2007 2008 2009 2010

Fed

ECB

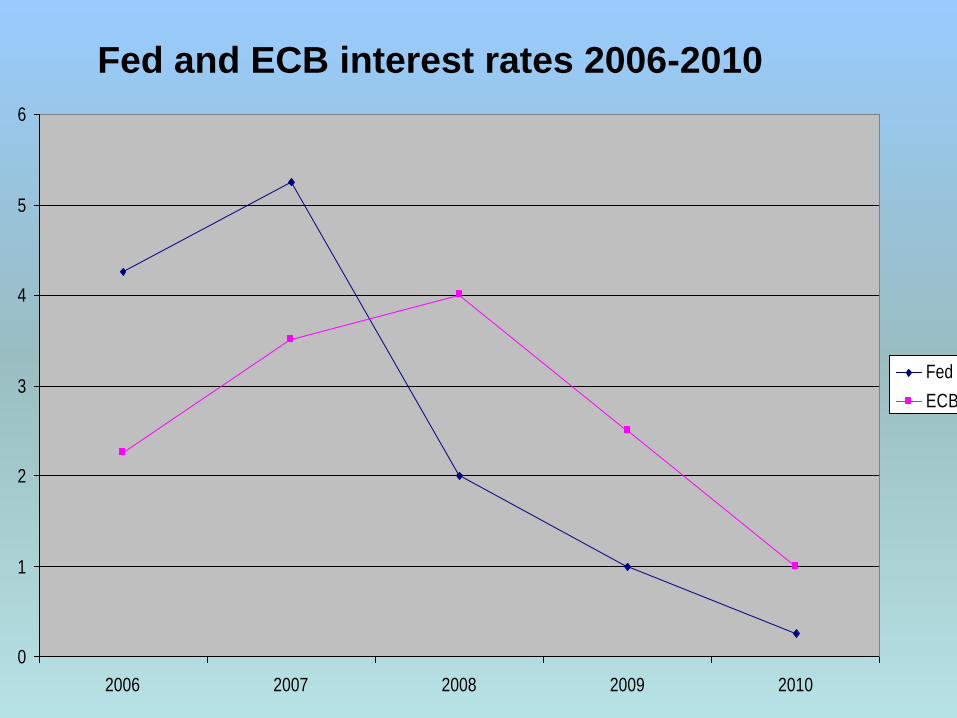

Fed and ECB interest rates 2006-2010

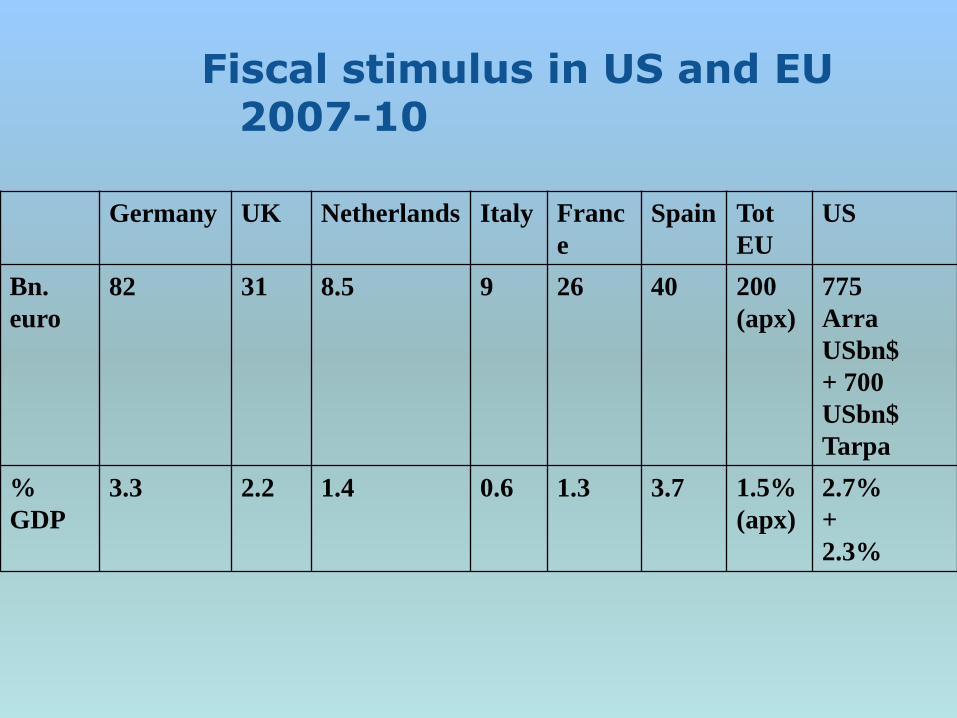

Fiscal stimulus in US and EU 2007-10

Germany UK Netherlands Italy Franc

e Spain Tot

EU US

Bn.

euro 82 31 8.5 9 26 40 200

(apx) 775

Arra

USbn$

+ 700

USbn$

Tarpa

%

GDP 3.3 2.2 1.4 0.6 1.3 3.7 1.5%

(apx)

2.7%

+

2.3%

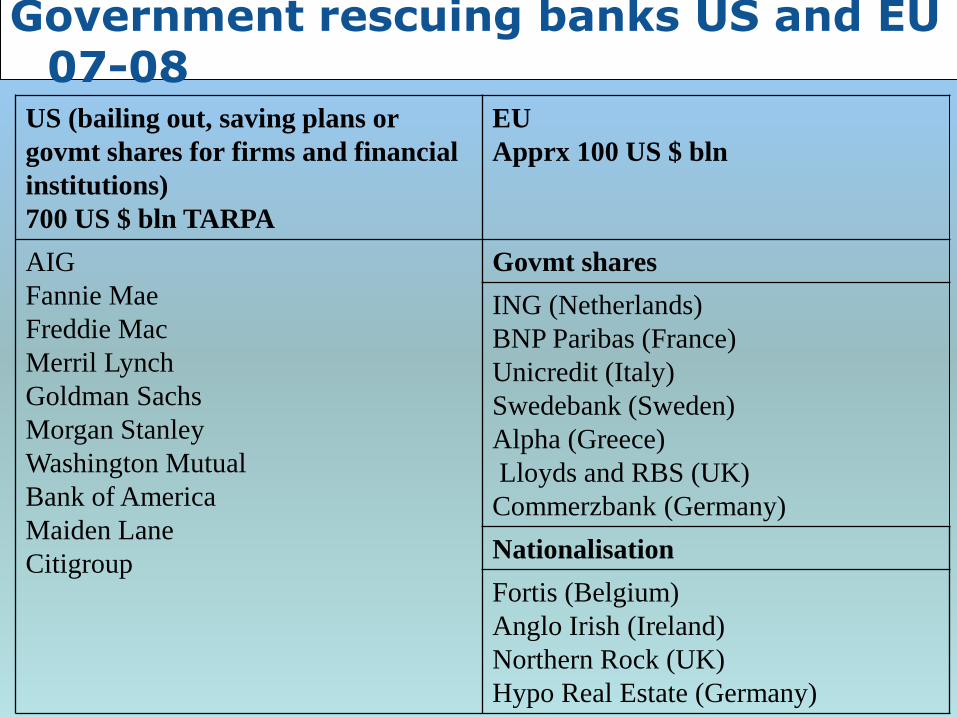

Government rescuing banks US and EU 07-08

US (bailing out, saving plans or

govmt shares for firms and financial

institutions)

700 US $ bln TARPA

EU

Apprx 100 US $ bln

AIG

Fannie Mae

Freddie Mac

Merril Lynch

Goldman Sachs

Morgan Stanley

Washington Mutual

Bank of America

Maiden Lane

Citigroup

Govmt shares

ING (Netherlands)

BNP Paribas (France)

Unicredit (Italy)

Swedebank (Sweden)

Alpha (Greece)

Lloyds and RBS (UK)

Commerzbank (Germany)

Nationalisation

Fortis (Belgium)

Anglo Irish (Ireland)

Northern Rock (UK)

Hypo Real Estate (Germany)

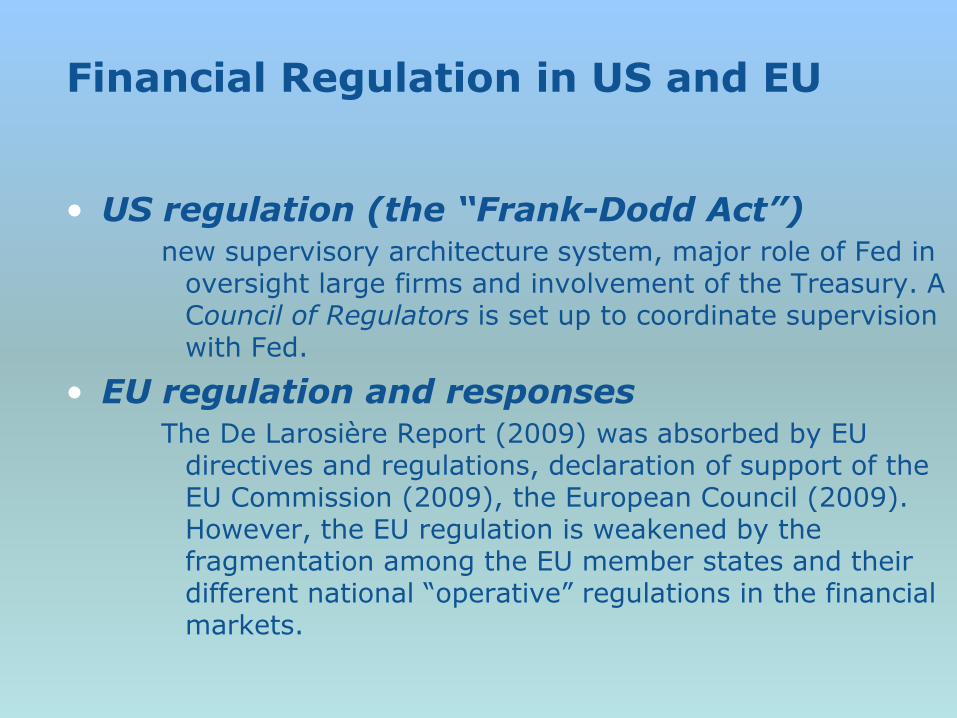

Financial Regulation in US and EU

• US regulation (the “Frank-Dodd Act”) new supervisory architecture system, major role of Fed in

oversight large firms and involvement of the Treasury. A Council of Regulators is set up to coordinate supervision with Fed.

• EU regulation and responses The De Larosière Report (2009) was absorbed by EU

directives and regulations, declaration of support of the EU Commission (2009), the European Council (2009). However, the EU regulation is weakened by the fragmentation among the EU member states and their different national “operative” regulations in the financial markets.

A stronger EU regulation

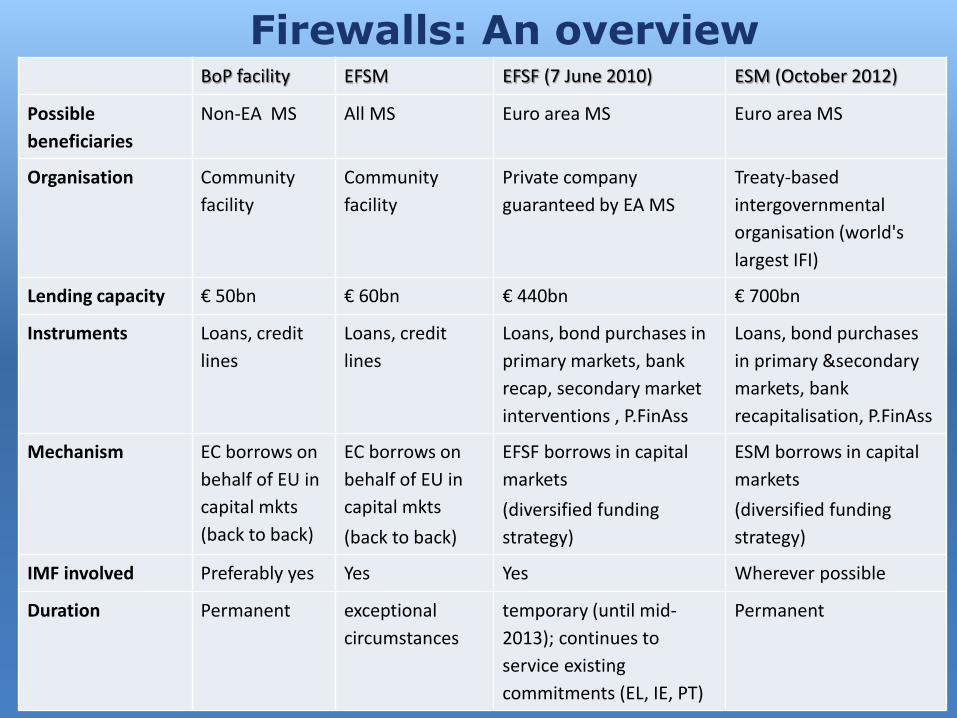

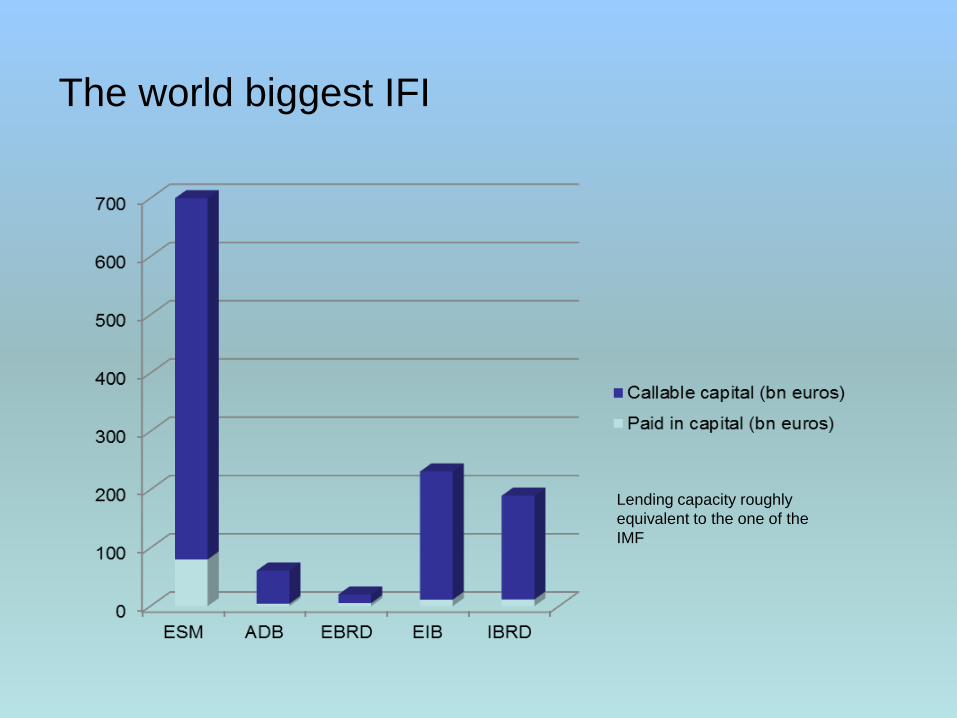

BoP facility EFSM EFSF (7 June 2010) ESM (October 2012)

Possible

beneficiaries

Non-EA MS All MS Euro area MS Euro area MS

Organisation Community

facility

Community

facility

Private company

guaranteed by EA MS

Treaty-based

intergovernmental

organisation (world's

largest IFI)

Lending capacity € 50bn € 60bn € 440bn € 700bn

Instruments Loans, credit

lines

Loans, credit

lines

Loans, bond purchases in

primary markets, bank

recap, secondary market

interventions , P.FinAss

Loans, bond purchases

in primary &secondary

markets, bank

recapitalisation, P.FinAss

Mechanism EC borrows on

behalf of EU in

capital mkts

(back to back)

EC borrows on

behalf of EU in

capital mkts

(back to back)

EFSF borrows in capital

markets

(diversified funding

strategy)

ESM borrows in capital

markets

(diversified funding

strategy)

IMF involved Preferably yes Yes Yes Wherever possible

Duration Permanent exceptional

circumstances

temporary (until mid-

2013); continues to

service existing

commitments (EL, IE, PT)

Permanent

Firewalls: An overview

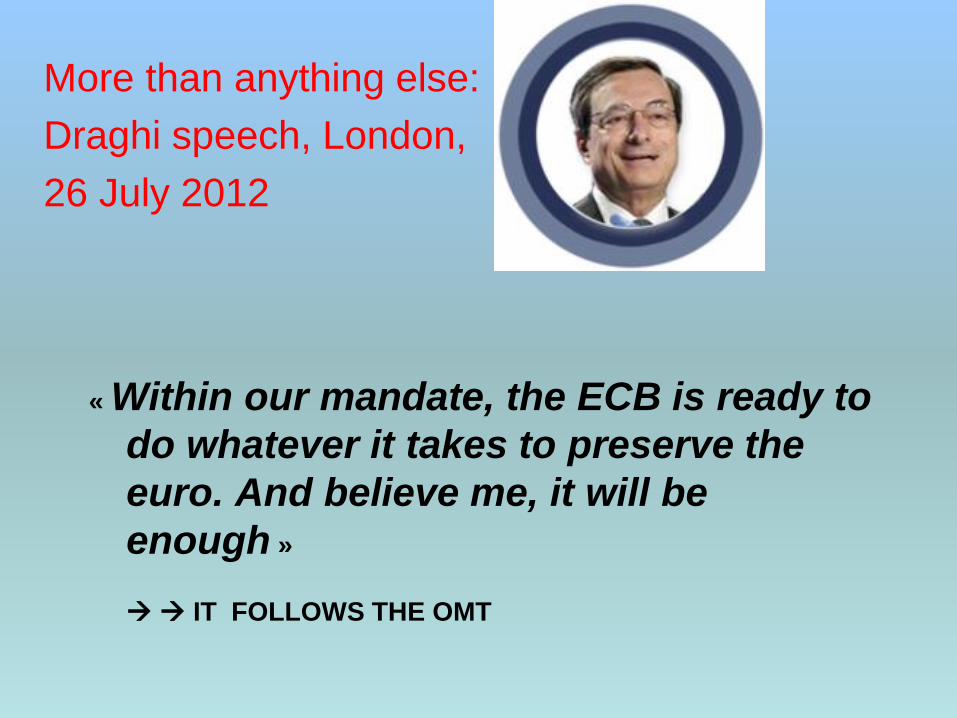

« Within our mandate, the ECB is ready to

do whatever it takes to preserve the

euro. And believe me, it will be

enough »

IT FOLLOWS THE OMT

More than anything else:

Draghi speech, London,

26 July 2012

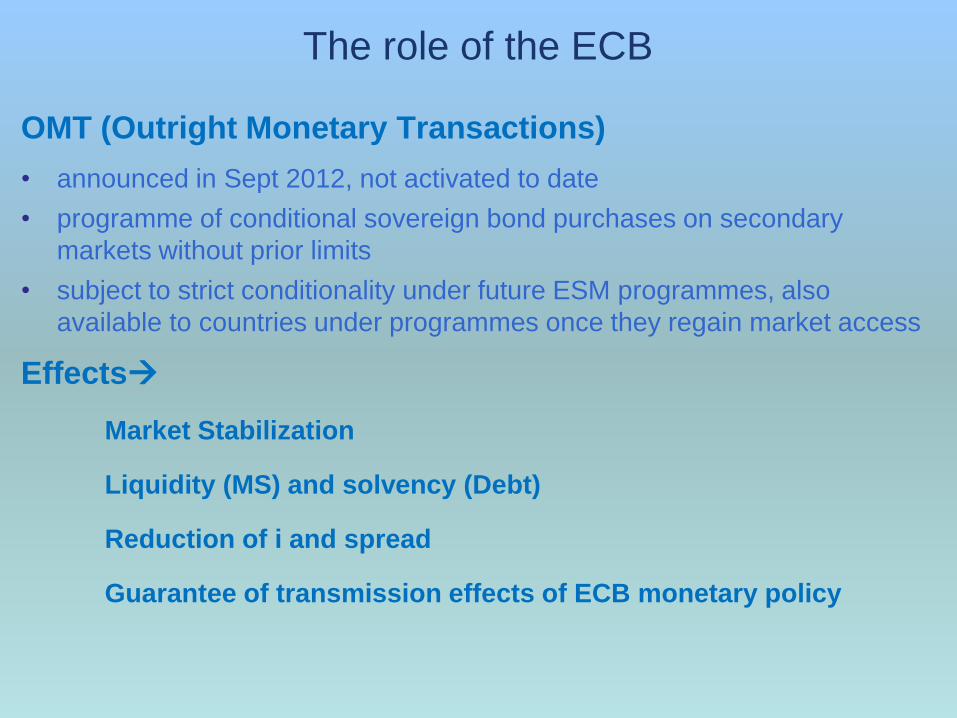

The role of the ECB

OMT (Outright Monetary Transactions)

• announced in Sept 2012, not activated to date

• programme of conditional sovereign bond purchases on secondary

markets without prior limits

• subject to strict conditionality under future ESM programmes, also

available to countries under programmes once they regain market access

Effects

Market Stabilization

Liquidity (MS) and solvency (Debt)

Reduction of i and spread

Guarantee of transmission effects of ECB monetary policy

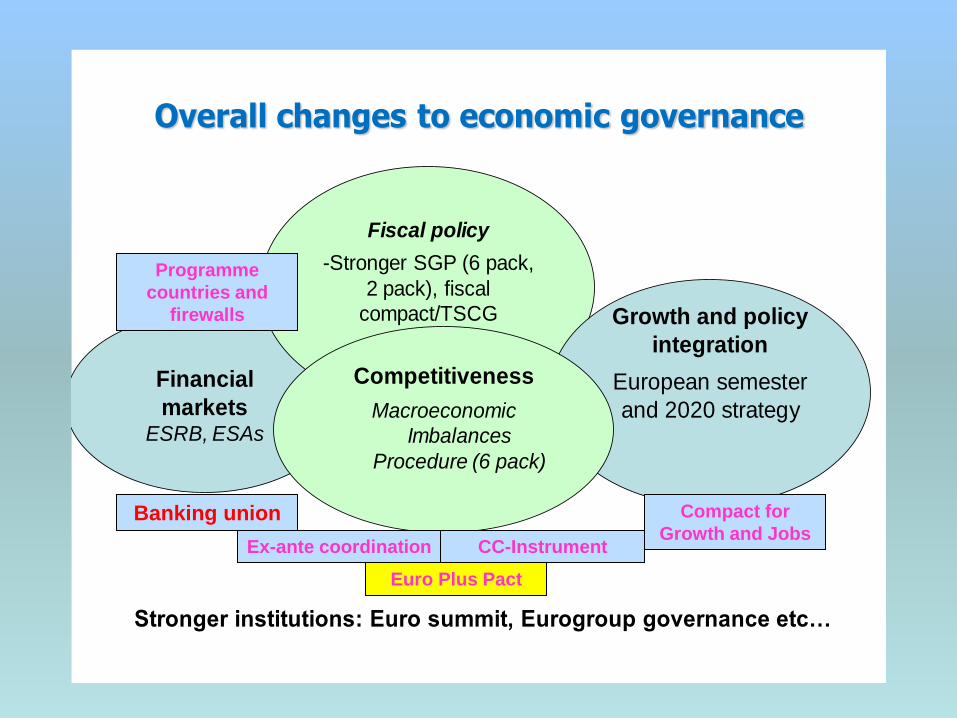

Overall changes to economic governance

Financial

marketsESRB, ESAs

Fiscal policy

-Stronger SGP (6 pack,

2 pack), fiscal

compact/TSCG Growth and policy

integration

European semester

and 2020 strategy

Competitiveness

Macroeconomic

Imbalances

Procedure (6 pack)

Stronger institutions: Euro summit, Eurogroup governance etc…

Programme

countries and

firewalls

Compact for

Growth and Jobs Banking union

Euro Plus Pact

Ex-ante coordination CC-Instrument

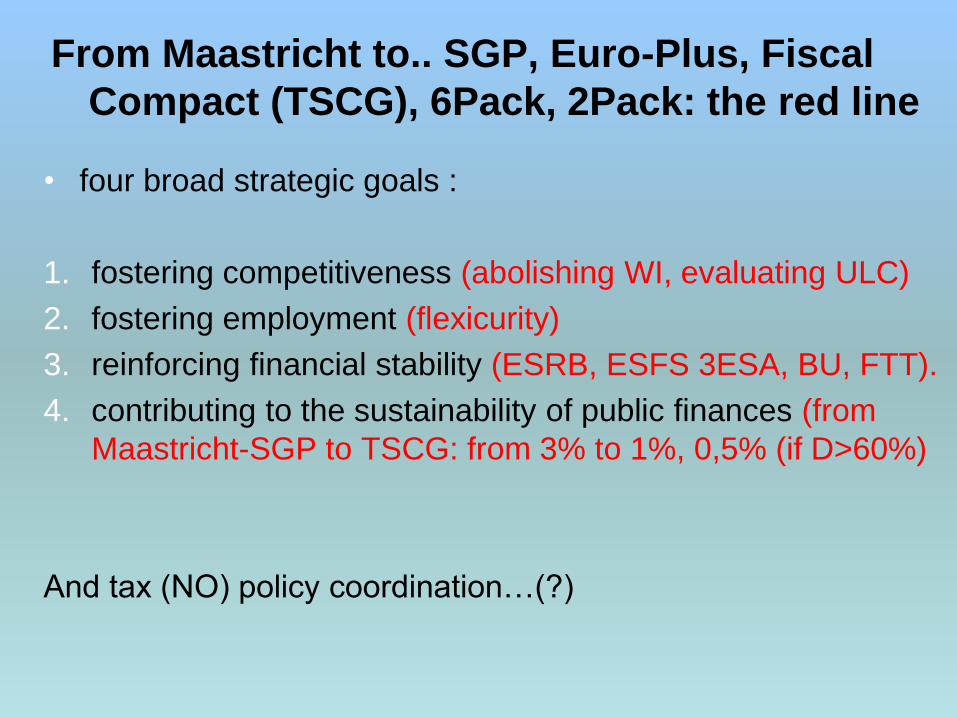

From Maastricht to.. SGP, Euro-Plus, Fiscal

Compact (TSCG), 6Pack, 2Pack: the red line

• four broad strategic goals :

1. fostering competitiveness (abolishing WI, evaluating ULC)

2. fostering employment (flexicurity)

3. reinforcing financial stability (ESRB, ESFS 3ESA, BU, FTT).

4. contributing to the sustainability of public finances (from

Maastricht-SGP to TSCG: from 3% to 1%, 0,5% (if D>60%)

And tax (NO) policy coordination…(?)

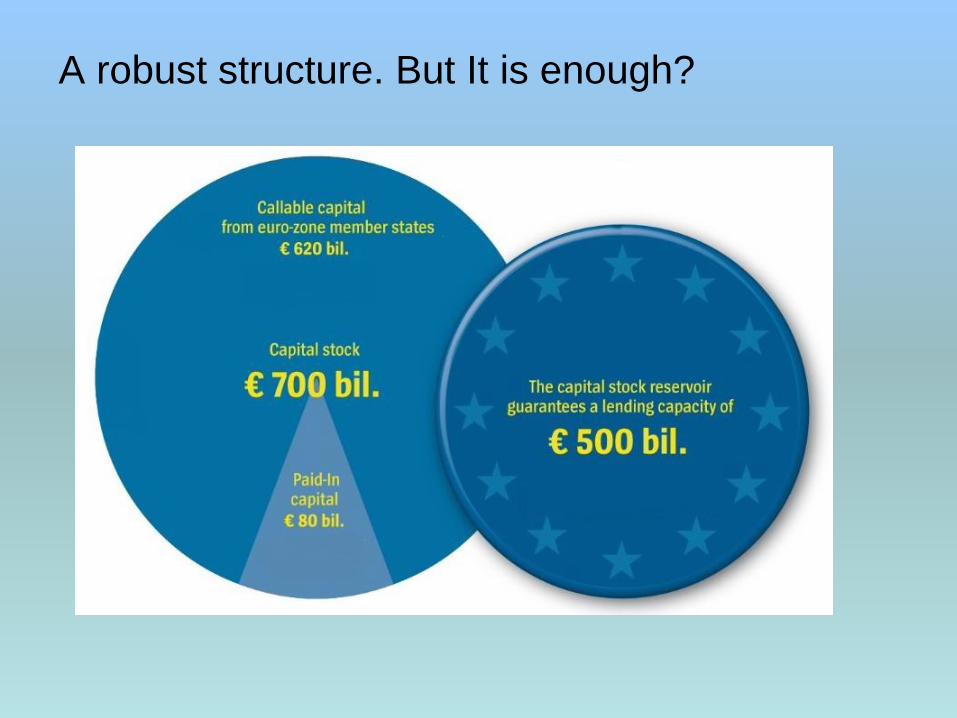

A (quasi)Sovereign protection

A robust structure. But It is enough?

The world biggest IFI

Lending capacity roughly

equivalent to the one of the

IMF

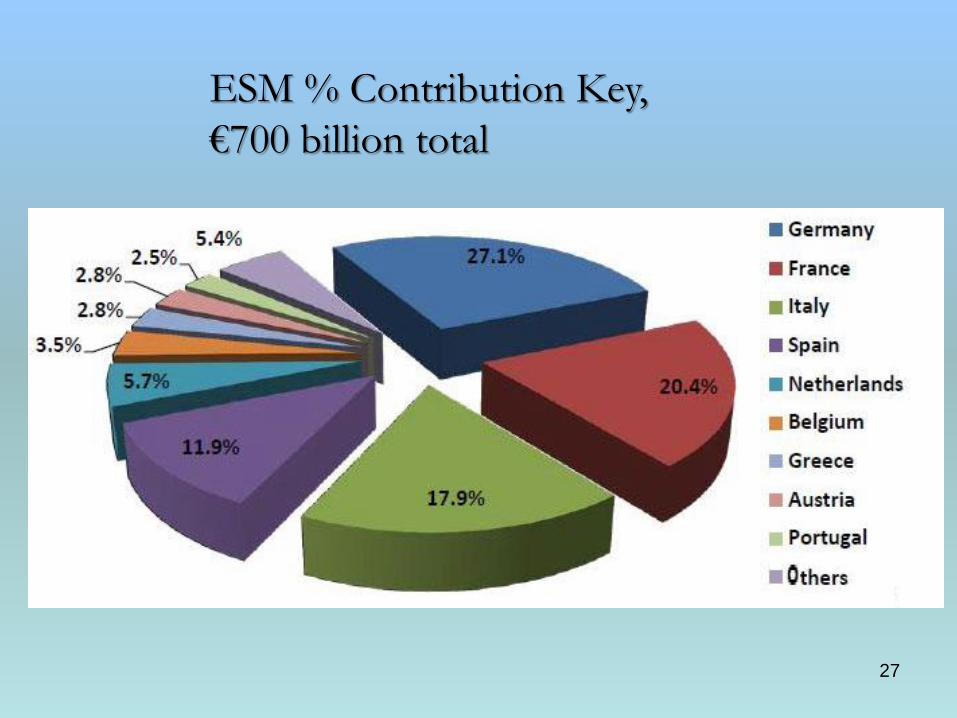

27

ESM % Contribution Key,

€700 billion total

28

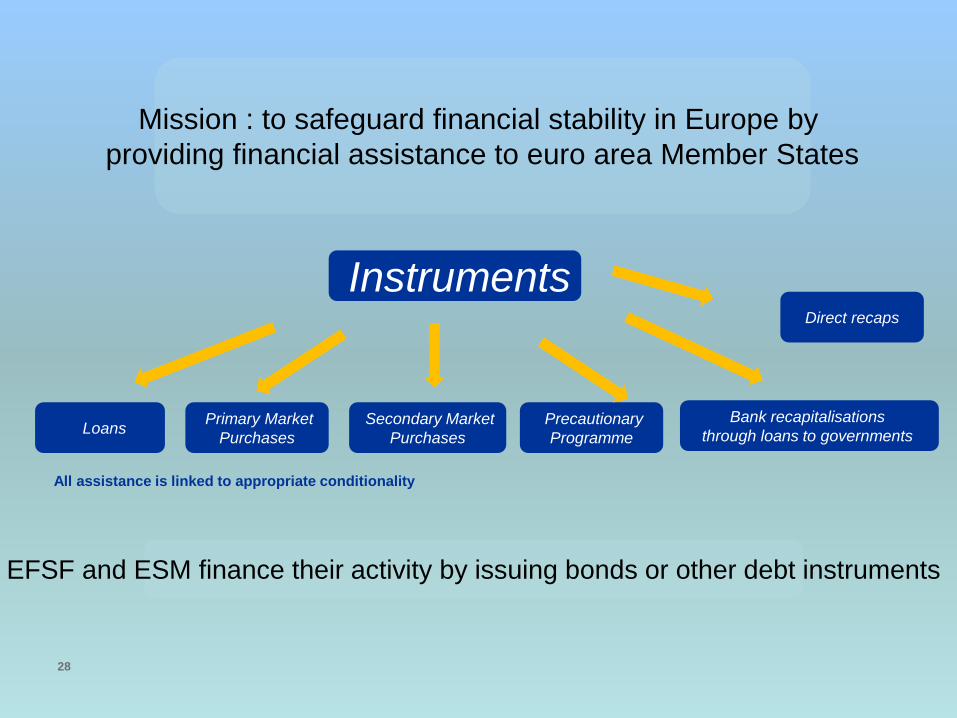

Mission : to safeguard financial stability in Europe by

providing financial assistance to euro area Member States

Instruments

Loans Primary Market

Purchases

Secondary Market

Purchases

Precautionary

Programme

Bank recapitalisations

through loans to governments

All assistance is linked to appropriate conditionality

EFSF and ESM finance their activity by issuing bonds or other debt instruments

Direct recaps

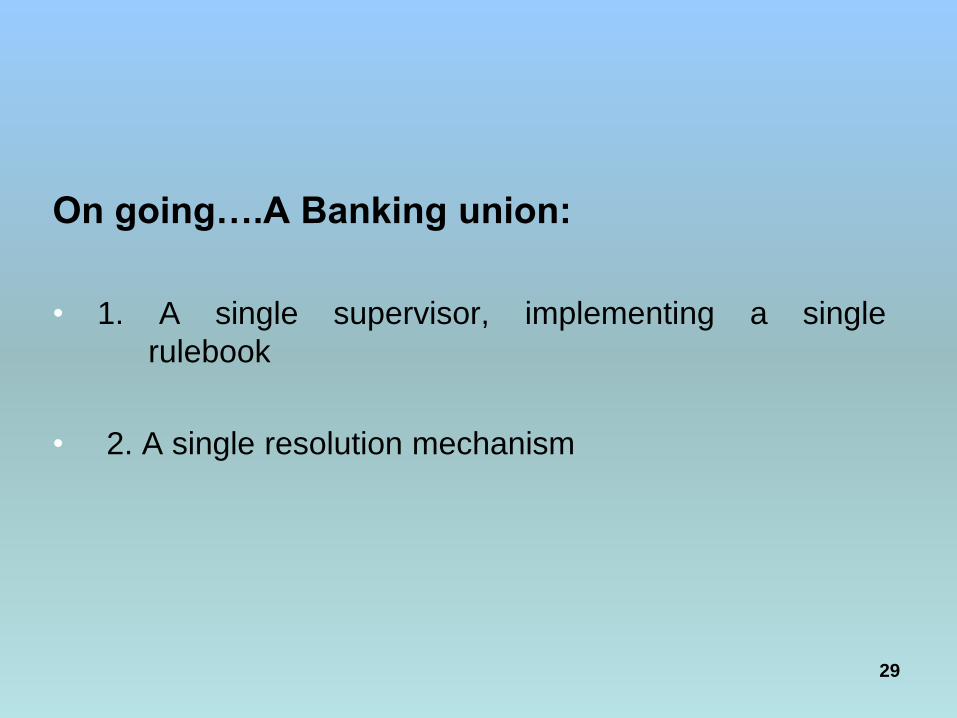

On going….A Banking union:

• 1. A single supervisor, implementing a single

rulebook

• 2. A single resolution mechanism

29

Why a Banking Union?

- To reduce the vicious loop/circle between the Sovereign

Debt and its banks

• cost of bank resolution can sometimes be excessive for one

country in isolation

• the same goes for bank recapitalization

- To improve supervision:

• no more captures

• no more excessive ring-fencing

Distribution of work between ECB and NSAs

- National supervisors assist ECB with preparation and implementation of its

tasks.

- For less significant banks national supervisors take the daily supervisory

decisions.

o Definition based on size (< 30 Bn assets), importance for national

economy (<20% national GDP; in any case 3 most important banks),

significance of cross-border activities

o ECB in charge of 128 banking groups (some strange choices), +/- 85% of

bank assets

o - ECB framework regulation on practical modalities.

The recovery in context

32

forecast

Where do we stand?

Self-defeating fiscal

consolidation?

Picture: The Atlantic

• composition of measures

• credibility

• impact on confidence

• monetary policy

• synchronisation

• Should we stop, ease,

postpone, delay, stretch

fiscal consolidation?

• Annual Growth Survey

• Pursue growth-friendly,

differentiated consolidation

The short-term fiscal multiplier is Yes, it depends on

higher than in normal times.

Fonte: Gabriele 2013

Fonte: Gabriele 2013

Fiscal stance turning broadly neutral

36

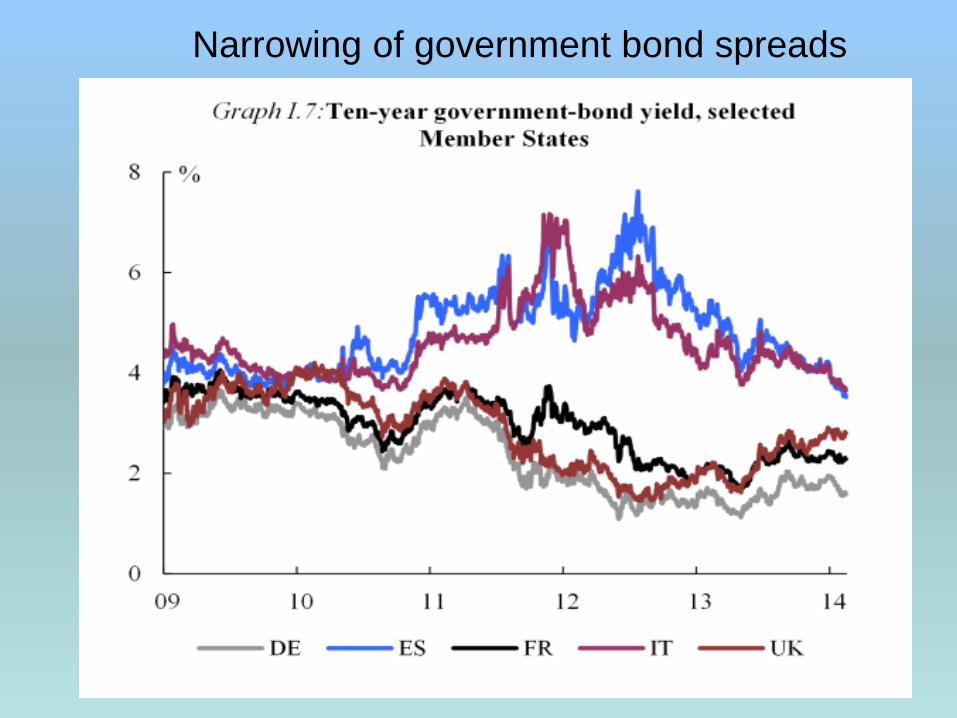

Narrowing of government bond spreads

37

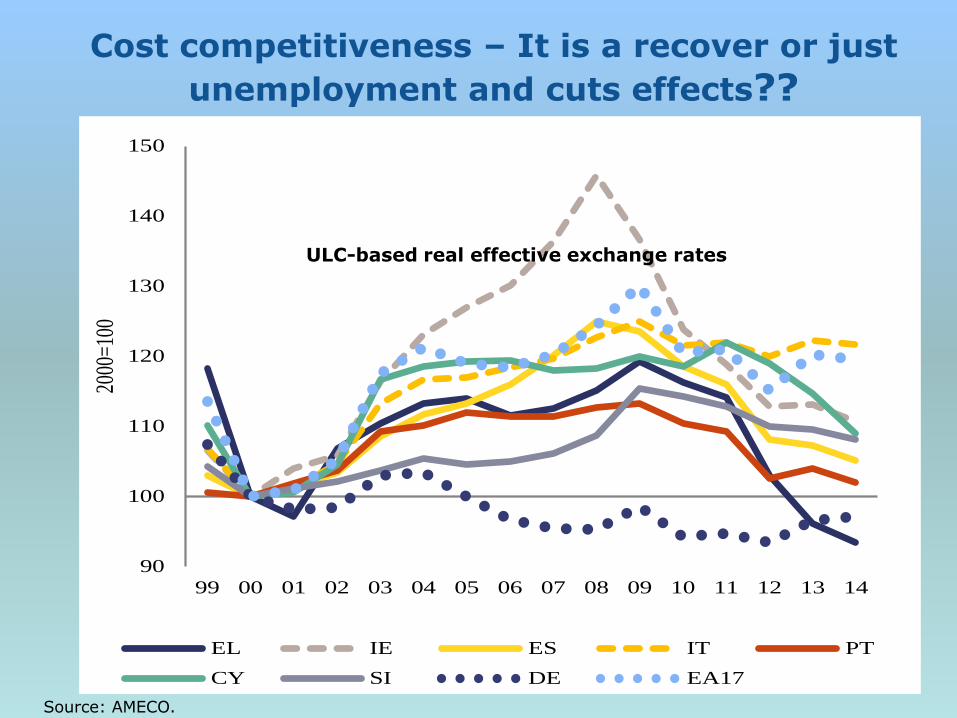

Cost competitiveness – It is a recover or just

unemployment and cuts effects??

38

90

100

110

120

130

140

150

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

2000

=100

EL IE ES IT PT

CY SI DE EA17

ULC-based real effective exchange rates

Source: AMECO.

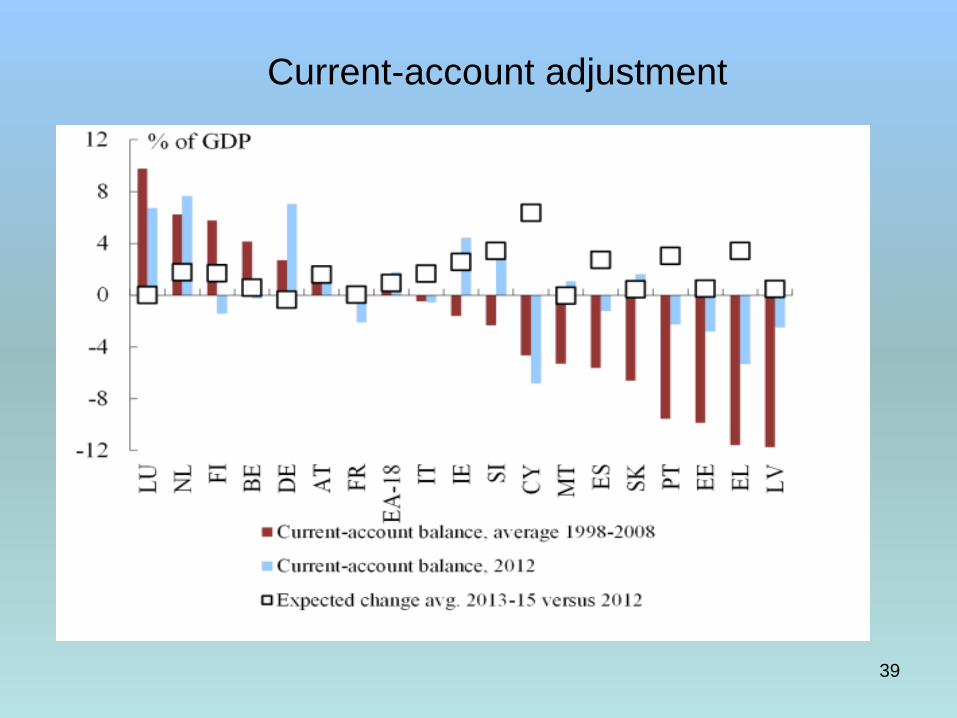

Current-account adjustment

39

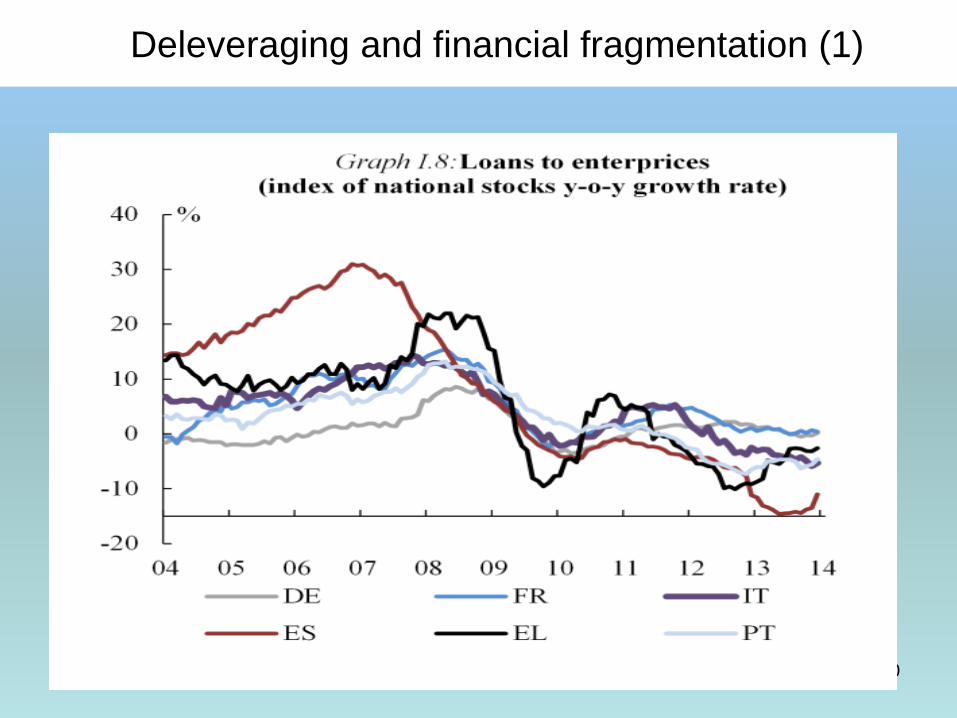

Deleveraging and financial fragmentation (1)

40

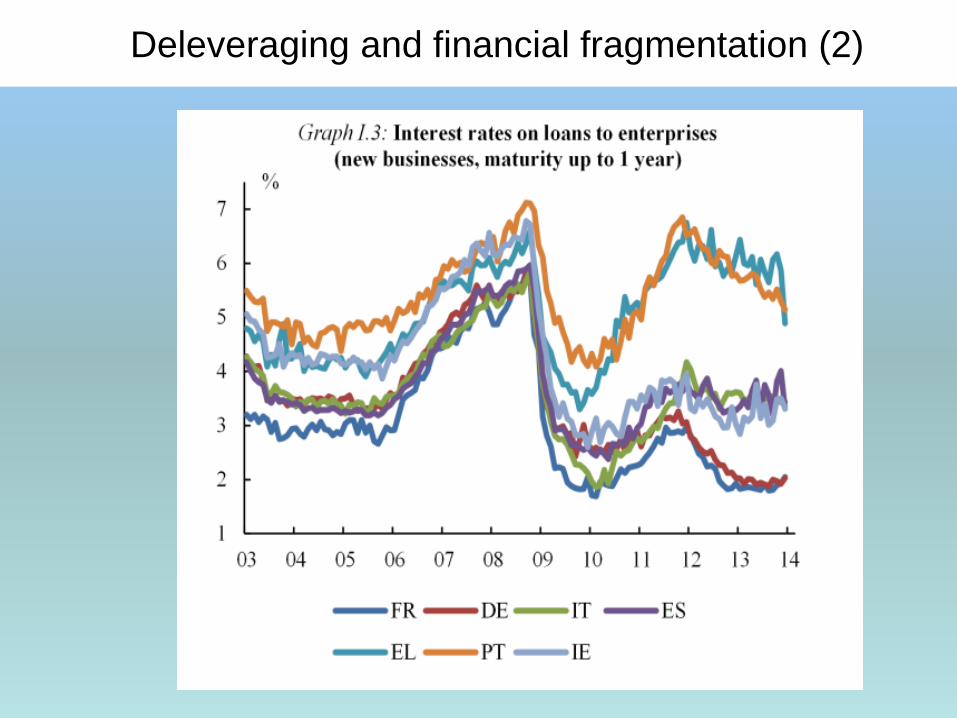

Deleveraging and financial fragmentation (2)

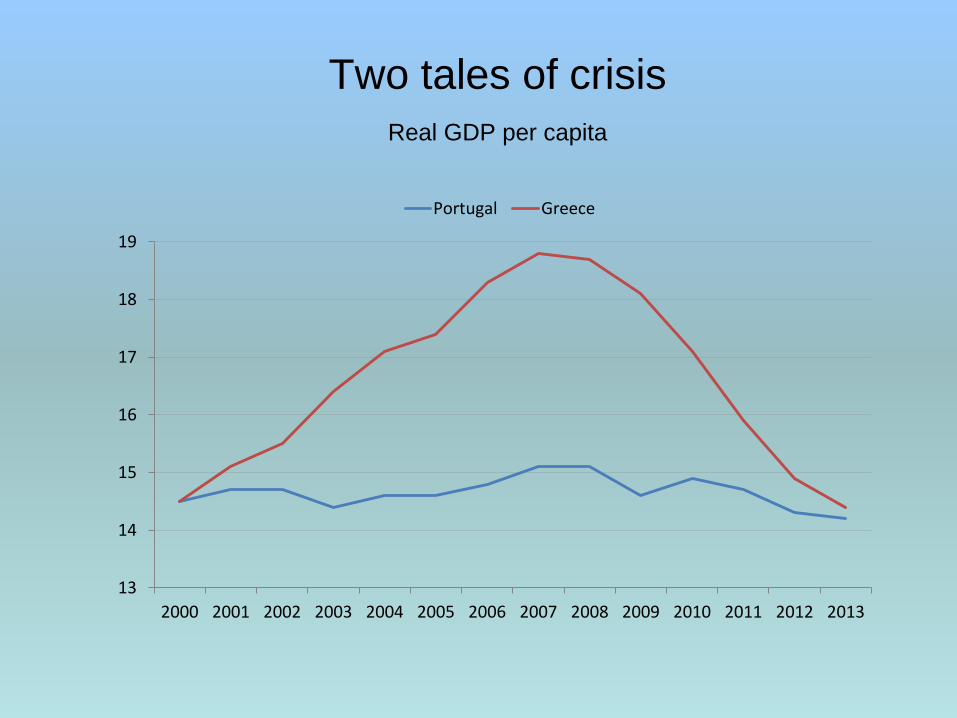

Two tales of crisis

Real GDP per capita

13

14

15

16

17

18

19

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Portugal Greece

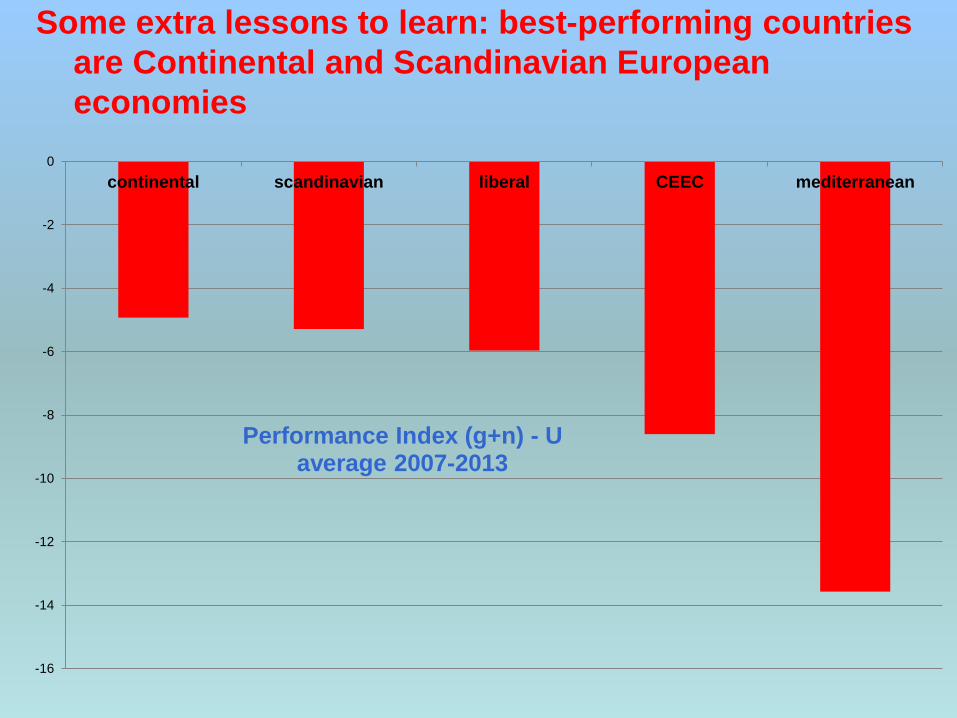

Some extra lessons to learn: best-performing countries

are Continental and Scandinavian European

economies

-16

-14

-12

-10

-8

-6

-4

-2

0

continental scandinavian liberal CEEC mediterranean

Performance Index (g+n) - U average 2007-2013

Lesson 1 to be learned – during the crisis

• In the years of the crisis (2007-13): countries that had

better performance are those that managed not to

retrench the welfare state (before, under the process of

globalisation) and therefore reached the eve of the crisis

in 2007 better equipped in terms of the welfare state.

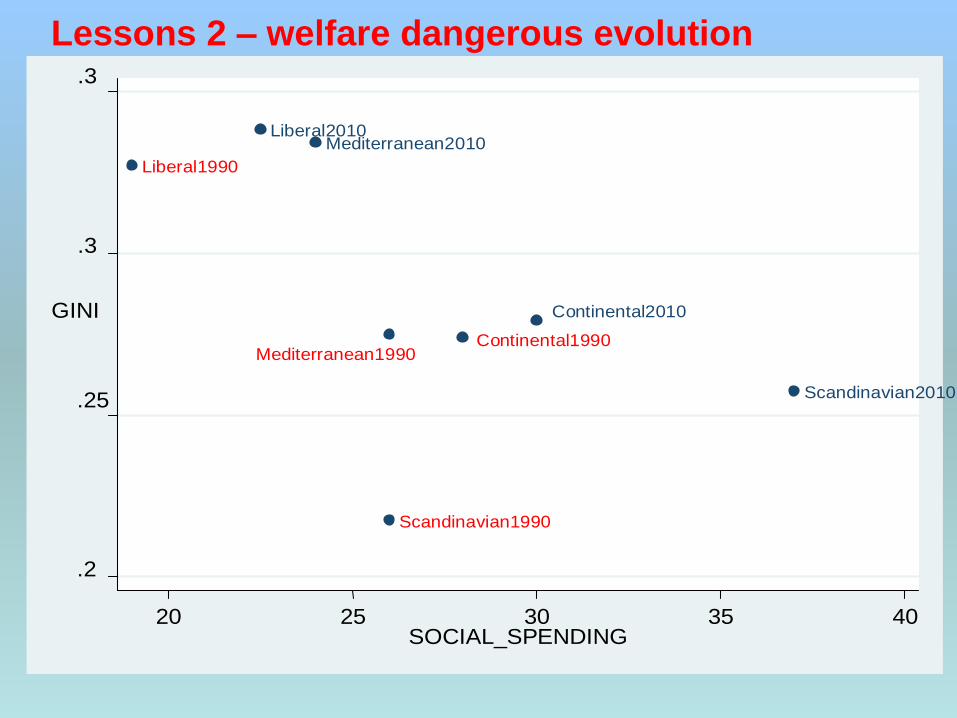

Lessons 2 – welfare dangerous evolution

Continental1990

Scandinavian1990

Liberal1990

Mediterranean1990

Continental2010

Scandinavian2010

Liberal2010 Mediterranean2010

.2

.25

.3

.3

GINI

20 25 30 35 40 SOCIAL_SPENDING

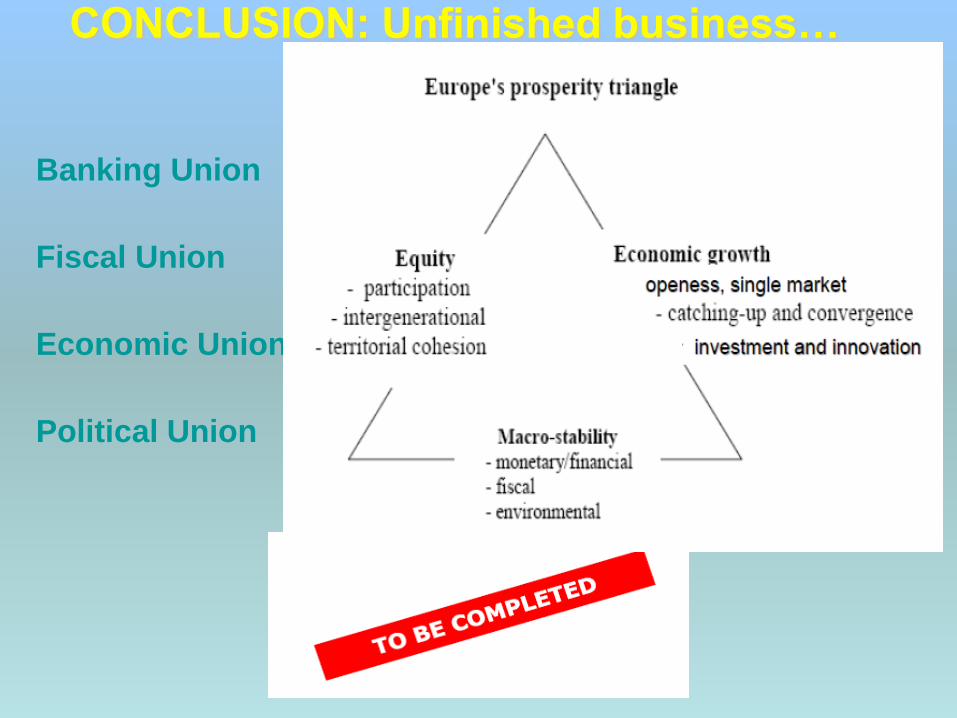

CONCLUSION: Unfinished business…

Banking Union

Fiscal Union

Economic Union

Political Union

Related Documents