Turkey’s Economic & Political Outlook June 3, 2014 Mehmet Şimşek Minister of Finance 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Turkey’s Economic & Political Outlook

June 3, 2014

Mehmet Şimşek

Minister of Finance

1

Is political stability at stake?

Low growth – the new normal?

Is the pick-up in inflation temporary?

Turkey’s soft spot - getting fixed?

Questions of Interest

2

Is political stability at stake?

3

Importance of Political Stability

4

v

A Virtuous Cycle

Political Stability

5

15 Months

139 Months

0

20

40

60

80

100

120

140

Average Lifetime of Governments during 1950-2002 AK Party Governments Since 2002

1923-2002

Average Lifetime of

Governments: 17 months

2002-14

Political Stability

2023 Vision

Local Election Results

Source: Anadolu Agency

AK PARTY: Justice and Development Party

CHP: Republican People’s Party

MHP: Nationalist Movement Party

BDP: Peace and Democracy Party

( %

)

38,8

23,1

16,1

5,7

16,3

45,5

27,8

15,2

4,2

7,3

0

5

10

15

20

25

30

35

40

45

50

AK PARTY CHP MHP BDP Others

2009

2014

6

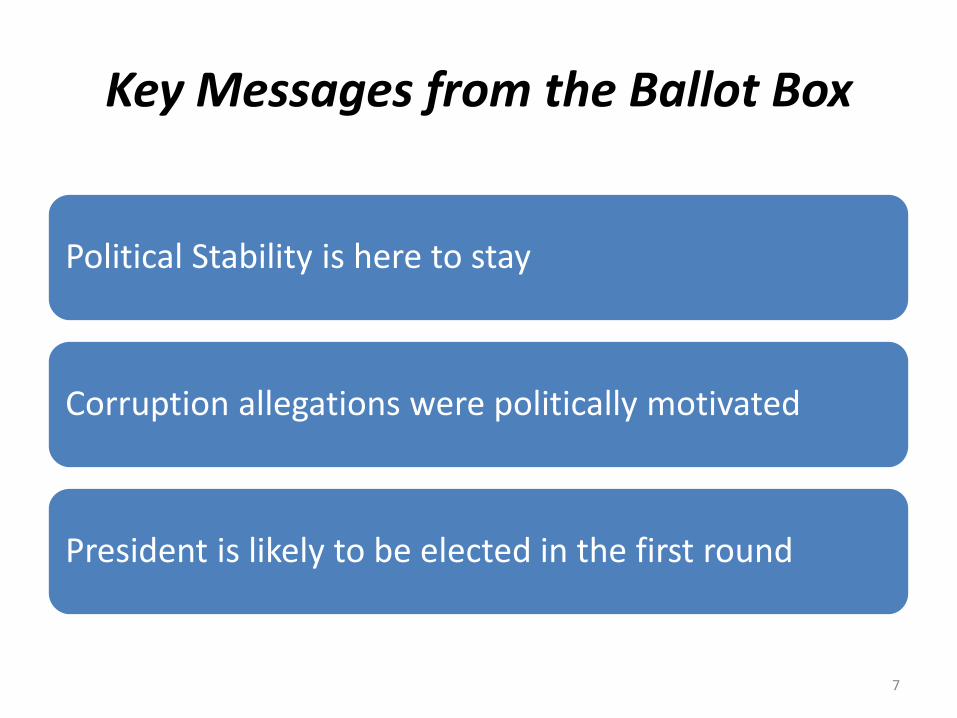

Key Messages from the Ballot Box

Political Stability is here to stay

Corruption allegations were politically motivated

President is likely to be elected in the first round

7

2 More Elections Ahead

Presidential

• August 2014

Parliamentary

• June 2015

8

Low growth – the new normal?

9

Real GDP

Source: Turkstat, Eurostat

120

100,0

85

90

95

100

105

110

115

120

Q1

-08

Q2

Q3

Q4

Q1

-09

Q2

Q3

Q4

Q1

-10

Q2

Q3

Q4

Q1

-11

Q2

Q3

Q4

Q1

-12

Q2

Q3

Q4

Q1

-13

Q2

Q3

Q4

Rea

l GD

P (

20

07

Q4

=1

00

, s.a

.)

10

Real GDP: Turkey vs AMs

Source: Turkstat, Eurostat

120

98

100,0

106

85

90

95

100

105

110

115

120

Q1

-08

Q2

Q3

Q4

Q1

-09

Q2

Q3

Q4

Q1

-10

Q2

Q3

Q4

Q1

-11

Q2

Q3

Q4

Q1

-12

Q2

Q3

Q4

Q1

-13

Q2

Q3

Q4

Rea

l GD

P (

20

07

Q4

=1

00

, s.a

.)

TURKEY

US

Euro Area

11

12

Real GDP: Turkey vs EMs

Source: TURKSTAT, IMF

168,8

100,0

152,8

153,0

180,4

159,0

143,8

95

105

115

125

135

145

155

165

175

185

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Turkey Emerging & Developing Europe

LatAm. & the Caribbean Developing Asia excl. China & India

Russia South Africa

TURKEY

Rea

l GD

P (

20

02

=10

0)

Upside

• Stronger external demand

• EU pulling out of recession

• Arab Spring becoming less disruptive

• TL depreciation

Downside

• Tighter financial conditions

• Geopolitical tensions

Growth Outlook

13

Softer Domestic Demand

14 Source: Turkstat, BRSA

(In

dex

) (A

nn

ua

l, %)

0

5

10

15

20

25

30

35

40

45

55

60

65

70

75

80

85Ja

n-0

8

Ap

r-0

8

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Consumer Confidence Total Credit Growth (rhs)

15 Source: Bloomberg, Turkstat

Ind

ex (

mo

nth

ly)

(6 m

on

th ro

lling

)

20

22

24

26

28

30

32

34

36

30

35

40

45

50

55

60

65

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Eurozone Manufacturing PMI Turkey's Exports to Europe (rhs)

External Demand

Manufacturing Output

16 Source: Turkstat, CBT

100

80

85

90

95

100

105

110

115

120

125

130

55

60

65

70

75

80

85

90

95

100

105

110

115

120Ja

n-0

8

Ap

r-0

8

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Real Sector Confidence Index (s.a.) Industrial Production (rhs) (s.a.)

PMI remaining above 50

17 Source: HSBC

51,1

30

35

40

45

50

55

60

Jan

-07

Ap

r-0

7

Jul-

07

Oct

-07

Jan

-08

Ap

r-0

8

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

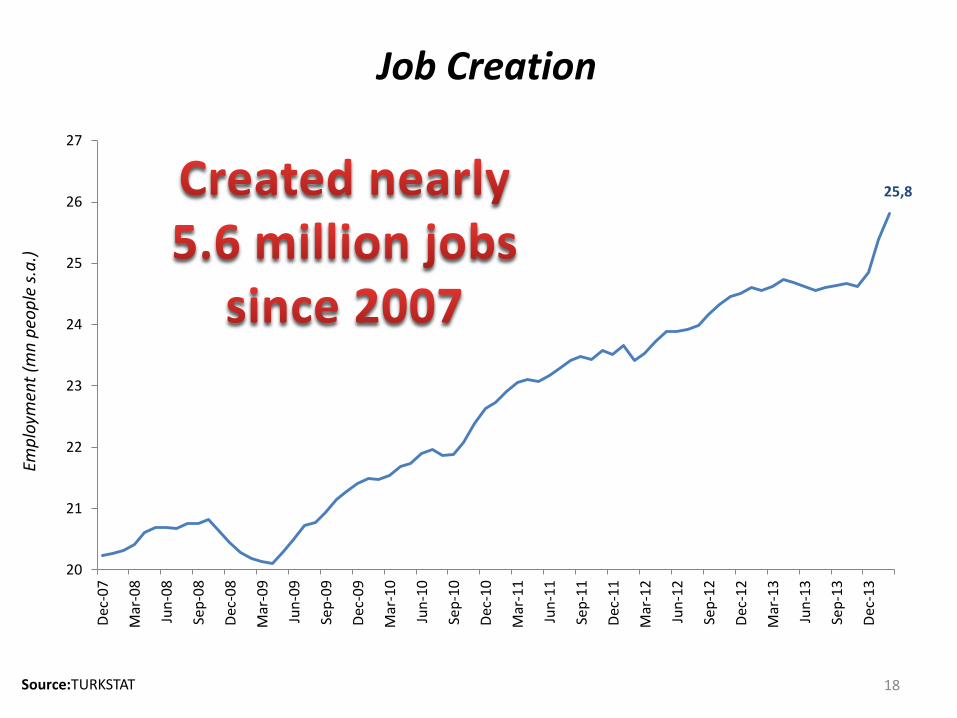

Job Creation Em

plo

ymen

t (m

n p

eop

le s

.a.)

Source:TURKSTAT 18

25,8

20

21

22

23

24

25

26

27

Dec

-07

Mar

-08

Jun

-08

Sep

-08

Dec

-08

Mar

-09

Jun

-09

Sep

-09

Dec

-09

Mar

-10

Jun

-10

Sep

-10

Dec

-10

Mar

-11

Jun

-11

Sep

-11

Dec

-11

Mar

-12

Jun

-12

Sep

-12

Dec

-12

Mar

-13

Jun

-13

Sep

-13

Dec

-13

Unemployment & Labor Participation Rate

Source:TURKSTAT

44

45

46

47

48

49

50

51

52

8

9

10

11

12

13

14

15

16Ja

n-0

8

May

-08

Sep

-08

Jan

-09

May

-09

Sep

-09

Jan

-10

May

-10

Sep

-10

Jan

-11

May

-11

Sep

-11

Jan

-12

May

-12

Sep

-12

Jan

-13

May

-13

Sep

-13

Jan

-14

Unemployment Rate Labor Force Participation Rate (rhs)

(s.a., %

) (s.a

., %

)

19

Is the pick up in Inflation Temporary?

20

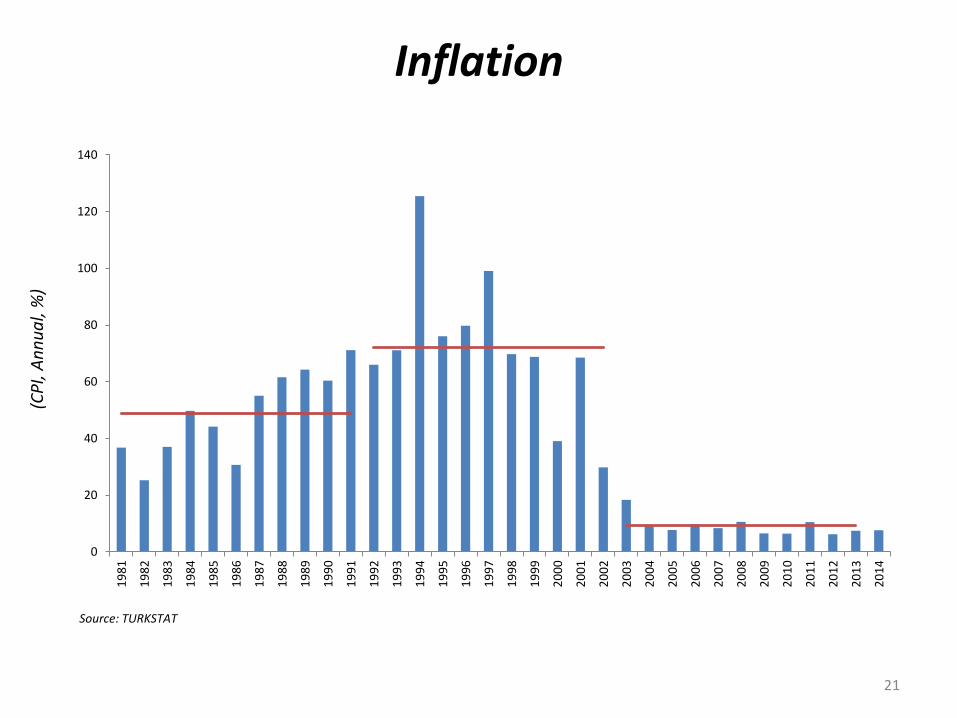

Inflation

0

20

40

60

80

100

120

140

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Source: TURKSTAT

(CP

I, A

nn

ua

l, %

)

21

2014 Inflation: Target vs Forecast

Energy prices

0.1 ppt

Deterioration in pricing behavior

0.3 ppt

Tax hikes

0.5ppt

Food prices

0.6 ppt

Exchange rate depreciation

0.8 ppt

Inflation Target: 5.3 % (2014-16 Medium Term Program)

Inflation Forecast: 7.6%

22

CBRT’s Inflation Outlook

23

Inflation is to resume downward trend as base effects fade

Source: CBRT

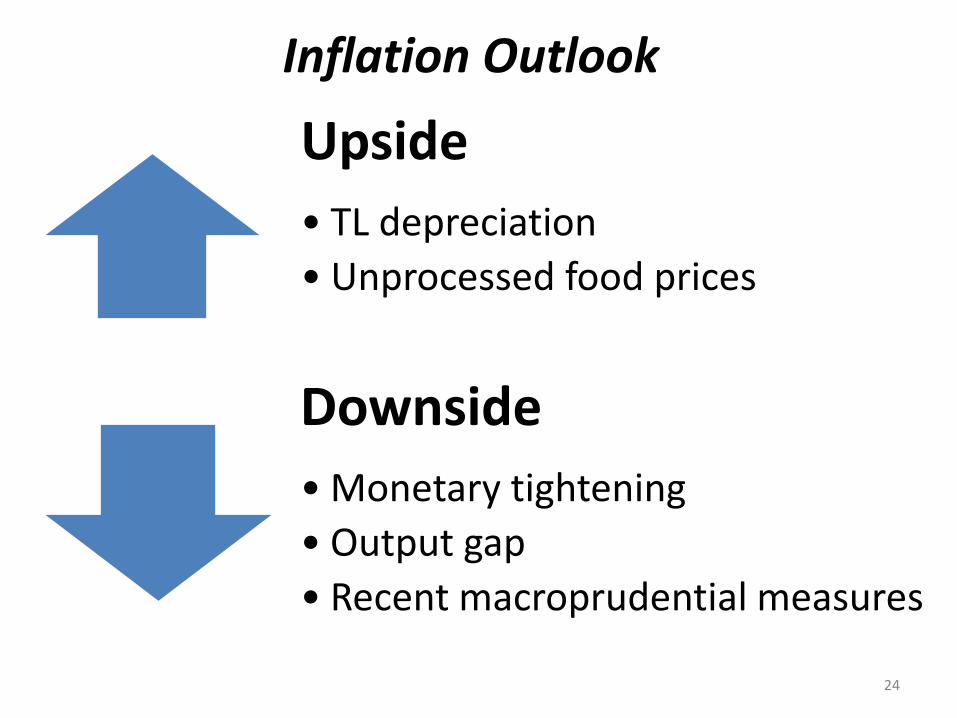

Upside

• TL depreciation

• Unprocessed food prices

Downside

• Monetary tightening

• Output gap

• Recent macroprudential measures

Inflation Outlook

24

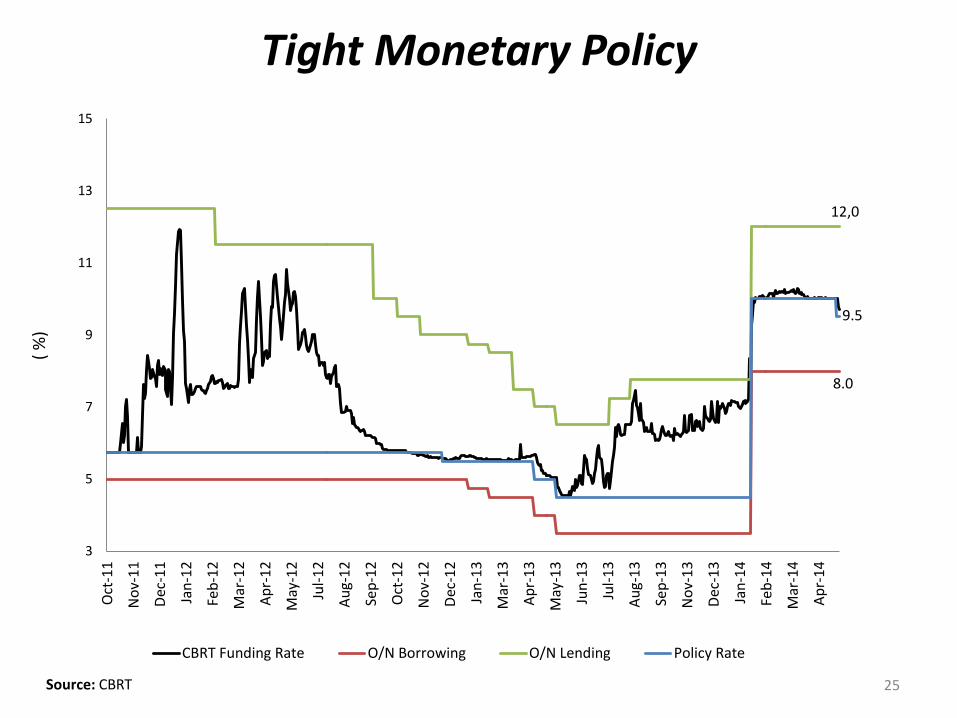

( %

) Tight Monetary Policy

Source: CBRT 25

8.0

12,0

9.5

3

5

7

9

11

13

15O

ct-1

1

No

v-1

1

Dec

-11

Jan

-12

Feb

-12

Mar

-12

Ap

r-1

2

May

-12

Jul-

12

Au

g-1

2

Sep

-12

Oct

-12

No

v-1

2

Dec

-12

Jan

-13

Mar

-13

Ap

r-1

3

May

-13

Jun

-13

Jul-

13

Au

g-1

3

Sep

-13

No

v-1

3

Dec

-13

Jan

-14

Feb

-14

Mar

-14

Ap

r-1

4

CBRT Funding Rate O/N Borrowing O/N Lending Policy Rate

( %

)

26 Kaynak: TCMB

Interest Rates on Turkish Lira Bank Loans

7

9

11

13

15

17

19

21

23

25

27

29Ja

nu

ary-

08

Ap

ril-

08

July

-08

Oct

ob

er-0

8

Jan

uar

y-0

9

Ap

ril-

09

July

-09

Oct

ob

er-0

9

Jan

uar

y-1

0

Ap

ril-

10

July

-10

Oct

ob

er-1

0

Jan

uar

y-1

1

Ap

ril-

11

July

-11

Oct

ob

er-1

1

Jan

uar

y-1

2

Ap

ril-

12

July

-12

Oct

ob

er-1

2

Jan

uar

y-1

3

Ap

ril-

13

July

-13

Oct

ob

er-1

3

Jan

uar

y-1

4

Ap

ril-

14

Personal Vehicle Housing Commercial

Macroprudential Measures

• Single limit for all credit cards

• Higher minimum payment

• Limit on # of installments

Credit card loans

• Higher risk weighting for consumer loans

Consumer loans

• Compulsory advance payment

• Term limit for vehicle and consumer loans

Auto & other consumer loans

• Lower risk weighting for SME & export credits

Other Loans

27

28 Source: CBRT

Credit Growth 1

3 w

eek

mo

vin

g a

vg.(

%. y

/y)

* Credit Growth is adjusted for exchange rate movements

12,1

0

5

10

15

20

25

30

35

40

45

Jan

-11

Mar

-11

Ap

r-1

1

Jun

-11

Au

g-1

1

Oct

-11

Dec

-11

Feb

-12

Mar

-12

May

-12

Jul-

12

Sep

-12

No

v-1

2

Jan

-13

Mar

-13

Ap

r-1

3

Jun

-13

Agu

-13

Oct

-13

Dec

-13

Feb

-14

Ap

r-1

4

Turkey’s Soft Spot – Getting Fixed?

29

Current Account Deficit

Source: CBRT 30

(12

Mo

nth

Ro

llin

g, U

SD b

n)

-80

-60

-40

-20

0

20

40

Jan

02

Jul 0

2

Jan

03

Jul 0

3

Jan

04

Jul 0

4

Jan

05

Jul 0

5

Jan

06

Jul 0

6

Jan

07

Jul 0

7

Jan

08

Jul 0

8

Jan

09

Jul 0

9

Jan

10

Jul 1

0

Jan

11

Jul 1

1

Jan

12

Jul 1

2

Jan

13

Jul 1

3

Jan

14

Current AccountCurrent Account excluding EnergyCurrent Account excluding Energy and Gold

Net Gold Exports

• 2011: -$4.8 billion

• 2012: +$5.7 billion

• 2013: -$11.8 billion

• 2014 Jan-Mar: $1.7 billion

Factors behind high C/A Deficit (2011-13)

Strong domestic demand

Euro crisis

High energy prices

Arab Spring

31

Upside • Geopolitical tensions

• Higher energy prices

Downside

• Faster recovery in Europe

• More stable MENA

• Softer domestic demand

• Exchange rate weakness

• Falling gold imports

• Higher tourism revenues

Outlook for C/A Deficit

32

Should we be worried about Open FX Positions?

33

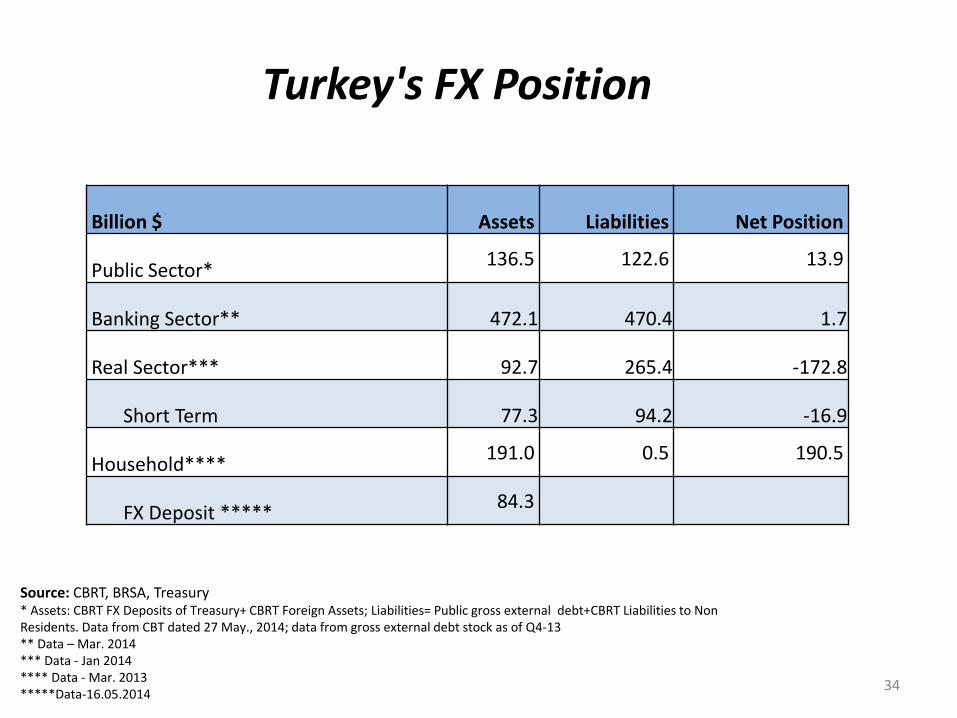

Turkey's FX Position

Source: CBRT, BRSA, Treasury * Assets: CBRT FX Deposits of Treasury+ CBRT Foreign Assets; Liabilities= Public gross external debt+CBRT Liabilities to Non Residents. Data from CBT dated 27 May., 2014; data from gross external debt stock as of Q4-13

** Data – Mar. 2014

*** Data - Jan 2014 **** Data - Mar. 2013

*****Data-16.05.2014

Billion $ Assets Liabilities Net Position

Public Sector* 136.5 122.6 13.9

Banking Sector** 472.1 470.4 1.7

Real Sector*** 92.7 265.4 -172.8

Short Term 77.3 94.2 -16.9

Household**** 191.0 0.5 190.5

FX Deposit ***** 84.3

34

Firms

Source: CBRT

No FX Loans 63%

FX Loan w/ export earning

25%

FX Loan w/o export earning

12%

9,500 firms

Total net sales at 71% of GDP

35

Firms: SMEs and Large Companies

Greater amount of FX debt belongs to LARGE COMPANIES

80% out of the 57% of large companies w/ FX debt have export earnings

Source: CBRT 36

Households: Low Leverage

Source: CBRT, ECB

(Ho

use

ho

ld L

iab

iliti

es, %

of

GD

P, J

un

e 2

01

3)

No FX exposure

65

23

20 40 60 80 100 120 140

DenmarkNetherlands

IrelandUnited Kingdom

PortugalSweden

SpainFinland

Euro AreaGreece

MaltaGermany

FranceLuxembourg

BelgiumAustria

ItalyEstoniaPoland

Czech RepublicLatvia

SloveniaHungarySlovakia

LithuaniaTurkey

37

Banks: Safe & Sound

Ca

pit

al A

deq

ua

cy R

ati

o, %

2002 Mar-14

17,6

2,8

NP

L R

ati

o o

f Lo

an

s (%

)

15,7

0

5

10

15

20

25

Jan

-08

May

-08

Sep

-08

Jan

-09

May

-09

Sep

-09

Jan

-10

May

-10

Sep

-10

Jan

-11

May

-11

Sep

-11

Jan

-12

May

-12

Sep

-12

Jan

-13

May

-13

Sep

-13

Jan

-14

Legal Rate: %8

Target Rate 12%

Source: BRSA 38

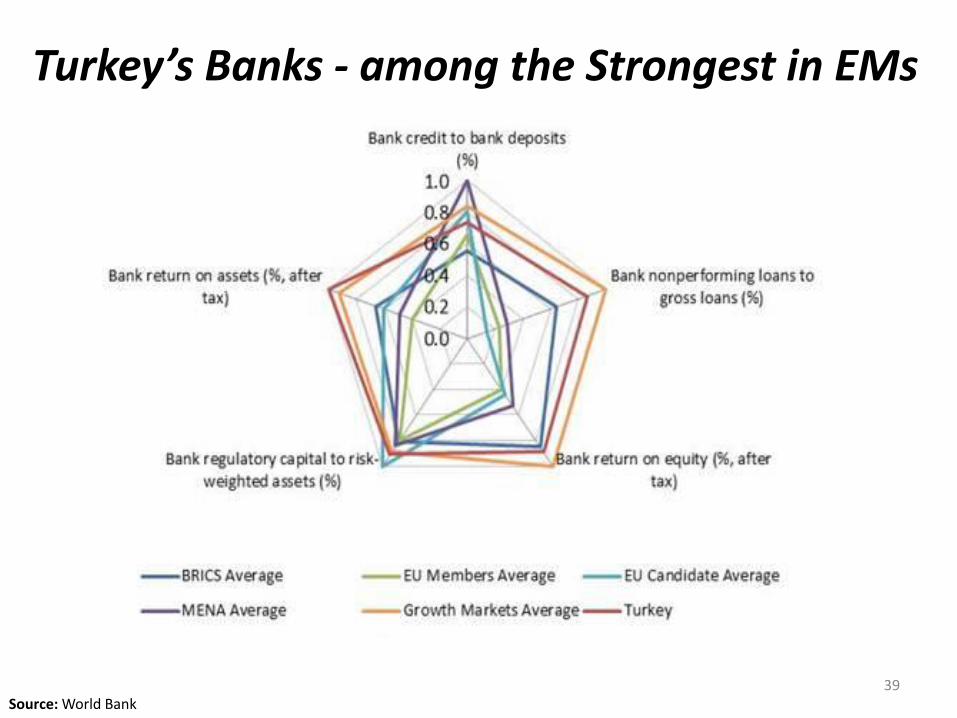

Turkey’s Banks - among the Strongest in EMs

39 Source: World Bank

Source: World Bank, IMF, BRSA

Banking Sector: Able to Absorb Shocks

Arm

Br

Bul

Col

Cro

Egy

Fr

Gre

Indo

Ire

Ita

Latv

Leb

Lith

Mex

Phil

Pol

Rom Rus

Serb

SoAf

Sp

Tu

Ukr

Venz

8

10

12

14

16

18

20

22

0 50 100 150 200 250

Private Credit/GDP (%)

CA

R (

%)

40

Fiscally:

Room to Manoeuvre

41

10,8

7,9

4,1

0,1

-1,3

0,2

1,6

5,5

3,0

0,4 1,0 1,0 1,1

-2,0

0,0

2,0

4,0

6,0

8,0

10,0

12,0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Maastricht Criteria: 3%

Achieved Maastricht Criteria except 2009

Source: Ministry of Development

Bu

dg

et D

efic

it-t

o-G

DP,

%

Low Deficit

42

Budget Deficit (2014) B

ud

get

Def

icit

-to

-GD

P, %

Source: IMF, OECD, Ministry of Development

3,9

2,9

2,3

1,1

0,5

1

1,5

2

2,5

3

3,5

4

4,5

OECD EU-28 EMs Turkey

43

44

Upside

• Conservative revenue assumptions

• Outperformance in non-tax revenues

• Improving tax compliance

Downside

• Weaker domestic demand

• Higher VAT rebates

Fiscal Outlook

Source: IMF

Fiscal Strength in EMs G

ross

Pu

blic

Deb

t (

%, G

DP

)

Fiscal Deficit (%, GDP)

Arm

Br

Bul

Col

Cro

Fr

Hun

Indo

Ire

Latv

Lith Mex Phil

Pol

Rom

Rus

Serb Slvk

Slov

SoAf

Sp

Tu

0

20

40

60

80

100

120

140

0 1 2 3 4 5 6 7 8 9

45

74,0

67,7

59,6

52,7

46,5

39,9 40,0

46,1

42,3

39,1 36,2 36,3

33,0

25

30

35

40

45

50

55

60

65

70

75

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Lower Public Debt D

ebt-

to-G

DP,

%

Satisfying Maastricht Criteria since 2004

Maastricht Criteria: 60%

Source: Treasury 46

Public Debt (2014)

Source: IMF, OECD, Treasury

Deb

t-to

-GD

P, %

111,1

89,0

33,3 33,0

20

30

40

50

60

70

80

90

100

110

120

OECD EU-28 EMs Turkey

47

Details of Treasury Guarantee Scheme

$3bn cap under 2014 Budget Law

PPPs under guarantee

• 3rd Bridge

• Euroasia Tunnel

• Gebze-Izmir Highway

Minimum 20% equity

In the case of default

• Max. 85% of total FX liabilities are guaranteed

• Defaulting parties’ assets to be transferred to the state 48

Priorities & Reform Agenda

49

Chapter- 1

Enhancing Human Capital Stock

Local & Renewable

Energy

Reducing Informal Economy

50

Enhancing Human Capital Stock

51

Source: Ministry of Finance

Share of Education Budget (%

)

52

Investment Incentives in Education Sector

18% VAT down to 8%

50% tax relief on CIT & PIT for exports in education

PIT and CIT exemption for 5 years on proceeds gained from education services

5th zone incentives for investments in pre-schools, elementary, secondary and high schools

Allocation of public real estate to investors

53

Gross Schooling Rates

Source: Ministry of Development 54

12 Years of Mandatory Education

Austral.

Austria

Belg.

Canada

Chile

Czech R.

Den.

Estonia

Finland

France

Italy

Japan

Lux

Mex

New Zeal.

Poland

Port.

Spain Switz.

TURKEY

UK

USA

6

7

8

9

10

11

12

13

14

9,5 9,7 9,9 10,1 10,3 10,5 10,7 10,9 11,1 11,3 11,5

Ave

rag

e Ye

ars

at

Sch

oo

l of

Pop

’n o

ver

25

Yea

rs

Income per Capita (PPP, log)

Source: OECD 55

2002

91.1 girls per 100 boys

2012

101.8 girls per 100 boys

Improving Girls’ Education

56

Source: OECD

76 74

47

51

38

46

30

35

40

45

50

55

60

65

70

75

80

Science Math

2006 2009 2012

Enhancing Human Capital Stock: PISA Results, Gap b/w Turkey & OECD

57

Improving Quality of Education

With Fatih Project, we are providing our children with

Broadband Internet Access

Smart Boards

Tablet PCs

Other Information Technology Tools

58

Local & Renewable Energy

59

High Dependence on Energy Imports

72%

Total Energy

92%

Oil

98%

Natural-Gas

60

Source: TURKSTAT, Bloomberg

Energy Import Bill (B

rent, $

pb

l) En

erg

y Im

po

rts

(Bill

ion

Do

llars

)

61

Developing Local & Renewable Resources

Source: Ministry of Energy and Natural Resources

Electricity Generation Installed Capacity

MW % of Total

Current Installed Capacity (2013) 64,044

- Renewable Energy 25,596 40.0

Power Plants Under Construction 14,338

- Renewable Energy 10,804 75.4

In 3-to-5 years 78,382

- Renewable Energy 36,401 46.4

62

Renewable Energy Outlook O

ver

the

nex

t d

eca

de

in T

urk

ey,

• 20,000 MW, wind power generation

• 3,000 MW, solar power plants

• 600 MW, geothermal power plants

• An energy stock market to be established

63

64

0

6

12

18

24

2010 2011 2012 2013

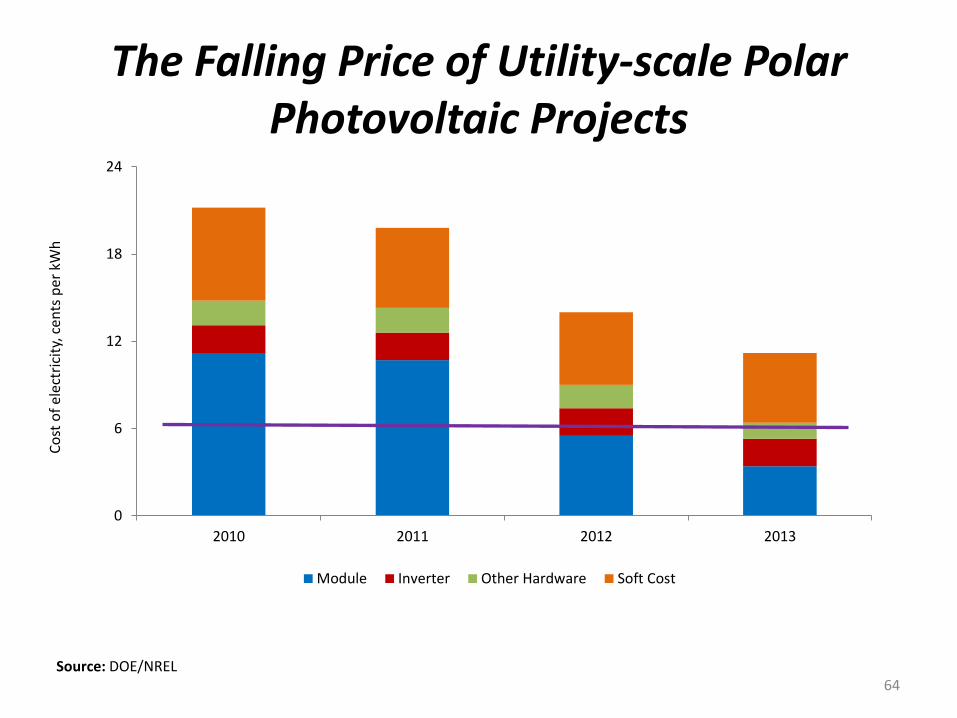

Module Inverter Other Hardware Soft Cost

Co

st o

f el

ect

rici

ty, c

ents

per

kW

h

Source: DOE/NREL

The Falling Price of Utility-scale Polar Photovoltaic Projects

Turkey’s Solar Energy Potential Atlas

65

Building Nuclear Capacity

Akkuyu: JV with Russia

Sinop JV with a Japanese-French consortium

Working on a 3rd plant

66

Improving Energy Efficiency

Industry

20%

Transportation 15%

Construction 30%

67

Combatting Shadow Economy

68

52,1 51,7

50,1

48,2

47,0

45,4

43,5 43,8 43,3

42,1

39,0

36,7

33,8

30

35

40

45

50

552

00

2

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Feb

.-2

01

4

(%, T

ota

l Em

plo

ymen

t)

Informal Employment

Source:TURKSTAT 69

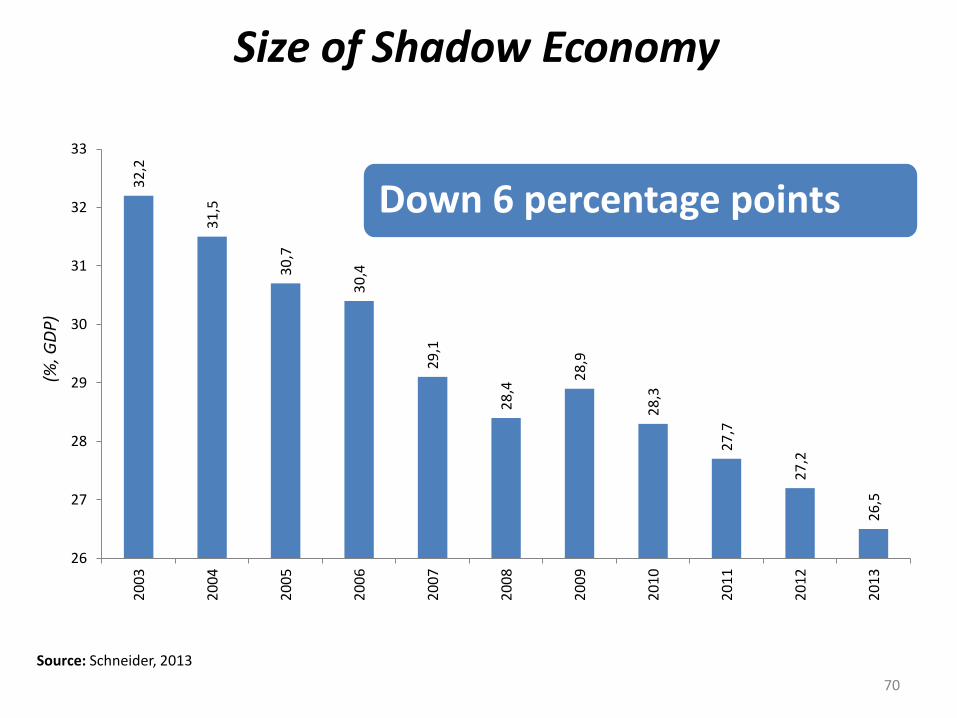

Size of Shadow Economy

32

,2

31

,5

30

,7

30

,4

29

,1

28

,4 2

8,9

28

,3

27

,7

27

,2

26

,5

26

27

28

29

30

31

32

332

00

3

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Source: Schneider, 2013

Down 6 percentage points

70

(%, G

DP

)

Size of Shadow Economy

Source: Schneider, 2013

But still higher than EU average 31

,2

28

,4

28

,4

28

,0

27

,6

26

,5

25

,5

25

,2

24

,3

23

,8

23

,6

23

,1

22

,1

21

,1

19

,0

18

,6

18

,4

16

,4

15

,5

15

,0

13

,9

13

,6

13

,0

13

,0

13

,0

12

,2

9,9

9,7

9,1

8,0

7,5

5

10

15

20

25

30

35

Bu

lgar

ia

Ro

man

ia

Cro

tia

Latv

ia

Esto

nia

TUR

KEY

Lith

uan

ia

S. C

ypru

s

Mal

ta

Po

lan

d

Gre

ece

Slo

ven

ia

Hu

nga

ry

Ital

y

Po

rtu

gal

Spai

n

EU A

vera

ge

Bel

giu

m

Cze

ch R

ep.

Slo

vaki

a

Swee

den

No

rway

Den

mar

k

Fin

lan

d

Ger

man

y

Irel

and

Fran

ce

Un

ited

Kin

gdo

m

Net

her

lan

ds

Luxe

mb

urg

Au

stri

a

(20

13

, %, G

DP

)

71

Chapter- 2

Improving Infrastructure

Deepening Capital

Markets

Moving up the Value-Chain

72

Improving Infrastructure

73

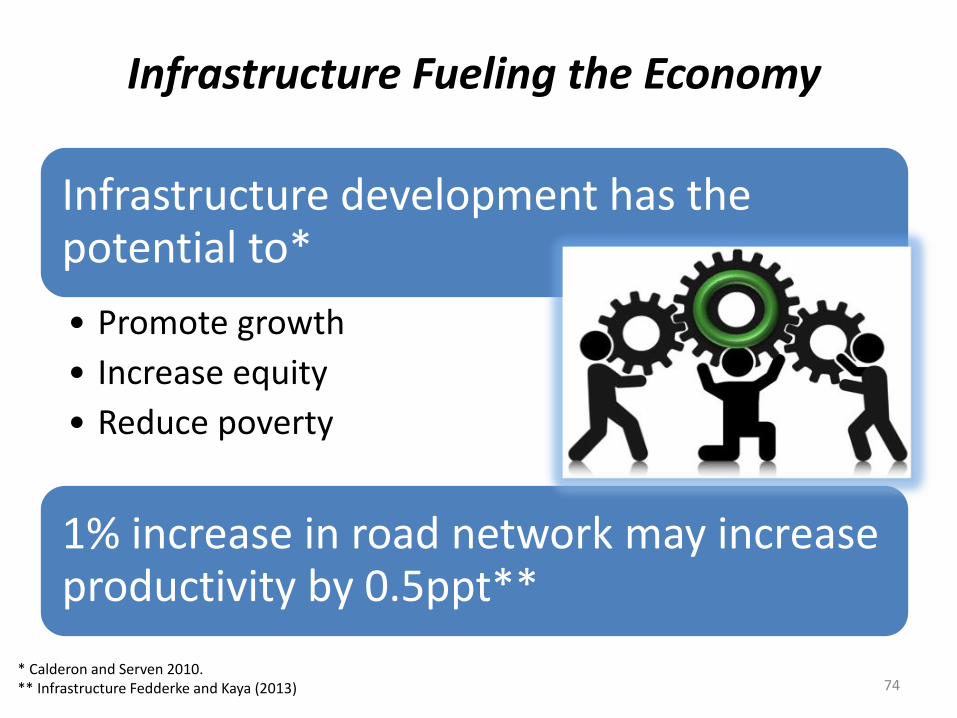

Infrastructure Fueling the Economy

Infrastructure development has the potential to*

• Promote growth

• Increase equity

• Reduce poverty

1% increase in road network may increase productivity by 0.5ppt**

74 * Calderon and Serven 2010. ** Infrastructure Fedderke and Kaya (2013)

1,714 Km

Total of Motorways

4,387 Km

Total of State and Provincial Dual Carriageways

Total: 6,101 Km

January 1, 2003

2,244 Km

Total of Motorways

20,807 Km

Total of State and Provincial Dual Carriageways

Total: 23,051 Km

January 2014

75

İSTANBUL

EDİRNE

ESKİŞEHİR

Polatlı

ANKARA

KONYA

İZMİR

SİVAS

AFYONKARHİSAR

KAYSERİ

BURSA

ERZİNCAN

ERZURUM

KARS

MERSİN ADANA

DİYARBAKIR

ELAZIĞ

MALATYA

ZONGULDAK SAMSUN

Bandırma

VAN

MUŞ

BİLECİK

ÇANKIRI

KIRIKKALE

TEKİRDAĞ

İZMİT

BALIKESİR

AYDIN

DENİZLİ BURDUR

ISPARTA

UŞAK MANİSA

KARAMAN

NİĞDE

OSMANİYE

K.MARAŞ

AMASYA

BATMAN

MARDİN

Yerköy

KARABÜK

Yenişehir

405 km

212 km

533 km

624 km

105 km

Completed (888 km) Under Construction (1796 km)

Bidding Phase (454 km)

Project Phase (354 km)

GAZİANTEP

Çobanbey

76

High Speed Railway Projects

Future Railways Investments

By 2023 $ 45 billion worth of investment

10,000 km worth of new high speed railway network

4,000 km of new conventional line

77

İstanbul

Antalya

İzmir

Gaziantep

Trabzon

Kayseri

Samsun

Erzurum

Kars

Van

Diyarbakır

Malatya

Dalaman

Bodrum

Sivas

Elazığ

Bursa

Ankara

Ağrı

Erzincan

Muş

Batman

Mardin Şanlıurfa

Adana

Konya

Denizli

KKTC THY

THY Pegasus Onur Air SUN Express ATLAS JET

Tokat

Zonguldak

BoraJet

Edremit

Siirt

Gazipaşa

Çorlu

KKTC

Iğdır

Gökçeada

Hatay

Adana Antalya

İzmir

Gaziantep

Trabzon

Kayseri

Ankara

Bursa

Samsun

Erzurum

Kars

Van

Mardin

Malatya

Dalaman

Bodrum

Konya

Sivas

Elazığ

Sinop

Nevşehir

Adıyaman Batman

Çanakkale

Denizli

Eskişehir

Isparta

Kahramanmaraş

Merzifon

Muş Uşak

Ağrı

Tekirdağ

Erzincan

Diyarbakır

Şanlıurfa

İstanbul

Kastamonu

Bingöl

Şırnak

2014 6 Airlines 7 Centers

52 Airports

2003 2 Centers

26 Airports

In domestic lines

the fastest

growing country

in Europe

TURKEY

Flight Points (Domestic Lines)

78

2003 60 Points

SunExpress Pegasus

ATLAS JET Onur Air

2014 236 Points

THY THY

SunExpress

Increase : 294%

79

Flight Points (International Lines)

The 3rd Airport in Istanbul, Largest of All

150 million passengers

An area of 90 million m2

Construction Cost: €10 billion

Rent (25 Years): €22.2 billion

80

Projects of the Century - Under Construction

Tube Tunnel 3rd Bridge

Izmit Gulf Transit Istanbul-İzmir Highway High-Speed Train through

Ankara-Bursa-Istanbul

81

Projects of the Century – Planned

Channel Istanbul

82

Deepening Capital Markets

83

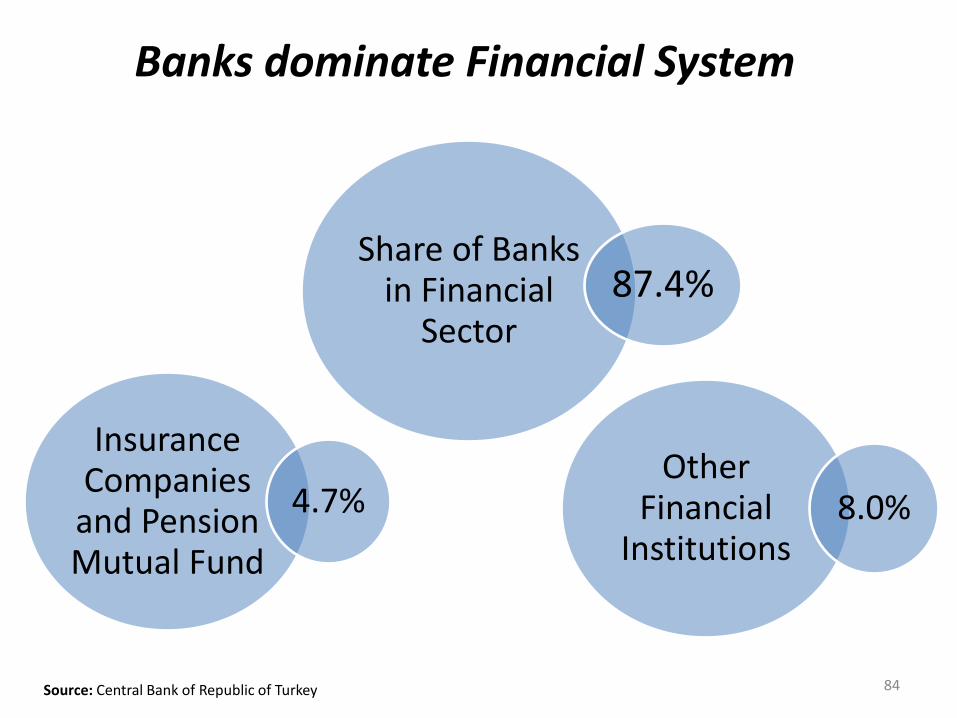

Banks dominate Financial System

Share of Banks in Financial

Sector 87.4%

84 Source: Central Bank of Republic of Turkey

Insurance Companies and Pension Mutual Fund

4.7% Other

Financial Institutions

8.0%

2009 72nd

2014 47th

2018 25th

Global Financial Centers Index

Source: Global Financial Centres Index 15

45 47

60

63

70

75 77

20

30

40

50

60

70

80

Rio de Jeneiro ISTANBUL Warsaw Mauritius Mexico Prague Budapest

(20

14

)

85

Strengthening the legal framework

Improving physical infrastructure

Simplifying tax system

Providing financial education

Istanbul as a Finance Center

86

Main Objective: Deepening Financial Markets

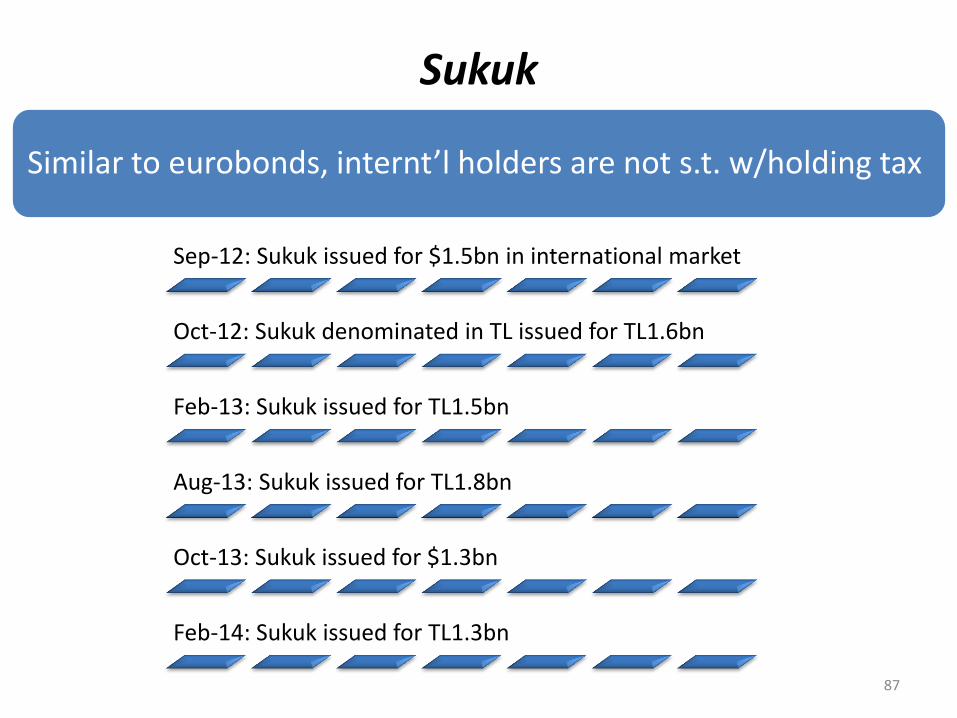

Sukuk

87

Sep-12: Sukuk issued for $1.5bn in international market

Oct-12: Sukuk denominated in TL issued for TL1.6bn

Feb-13: Sukuk issued for TL1.5bn

Aug-13: Sukuk issued for TL1.8bn

Oct-13: Sukuk issued for $1.3bn

Feb-14: Sukuk issued for TL1.3bn

Similar to eurobonds, internt’l holders are not s.t. w/holding tax

Increasing Savings: Private Pensions

25% State Contribution

1.4 million new

participants and TL7.9bn funds since end-2012

88

Support for Start-Ups

Incentives for Biz Angels

Incentives for VCs

89

Moving up the Value-Chain

90

Source: The Scientific and Technological Council of Turkey * % of GDP

R&D Spending*

91

•3.00% 2023

•1.8% 2018

• 0.92% 2012

• 0.53% 2002

Patent Applications

Source: TPI 92

1.874

12.053

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

10.000

11.000

12.000

13.000

2002 2013

Trade Mark Applications (2

01

2, T

ho

usa

nd

)

86

64

54

44 41

20

30

40

50

60

70

80

90

100

110

120

TURKEY France Germany Italy Spain England

108*

Source: Turkish Patent Institute *TURKEY 2013 Data

93

Tax Incentives for R&D

R&D Expenditure

• Corporate income tax relief

• Personal income tax relief

• State contributions to social security premiums

• Exemption from stamp duty

• Capital support for young entrepreneurs

Strengthening the link b/w R&D and Commercial Activities

• 50% tax relief on commercial use of patents, trademarks…

• VAT exemption on patents, trademarks…

94

Since 2008, 155 R&D Centers

Global Investors in Turkey

95

International Companies Operating in Turkey

Source: Ministry of Economy

96

3.212 4.303

6.342

9.092

12.380

16.082

19.097

21.898

25.170

29.529

33.808

37.199 37.737

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.0002

00

2

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Feb

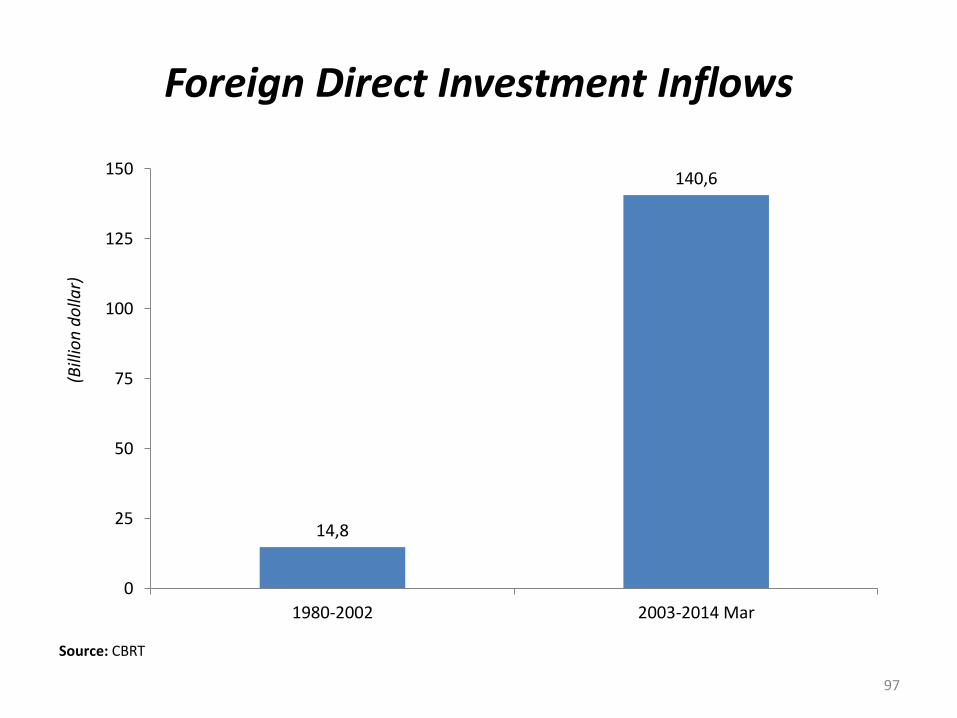

Foreign Direct Investment Inflows

Source: CBRT

(Bill

ion

do

llar)

97

14,8

140,6

0

25

50

75

100

125

150

1980-2002 2003-2014 Mar

Strong Long-Term Prospects

98

Determinants of Long-Term Growth

Quality of Institutions

Demographics

Productivity

99

Improving Quality of Institutions

Corruption Perceptions:

2013: 53rd in 177

2002: 65th in 102

Ease of Doing Business:

2013-14: 69th in 185

2006: 84th in 175

Global Competitiveness: 2013: 44th in 148

2005: 71st in 117

Source: WB, WEF, Transparency International 100

Corruption Perceptions Index (2002)

(65th among 102 countries)

31

44 45

58 59

65 70

73 74

96

20

30

40

50

60

70

80

90

100

Ital

y

Gre

ece

Bra

zil

Mex

ico

Ch

ina

TUR

KEY

Arg

enti

na

Ind

ia

Ru

ssia

Ind

on

esia

Source: Transparency International

101

Corruption Perceptions Index (2013)

(53rd among 177 countries)

Source: Transparency International

53

69 72

80 80

94

106 106

114

127

40

50

60

70

80

90

100

110

120

130

140

TUR

KEY

Ital

y

Bra

zil

Ch

ina

Gre

ece

Ind

ia

Arg

enti

na

Mex

ico

Ind

on

esia

Ru

ssia

102

Within the period of 2005-2012, Turkey has ranked higher than Russia, Argentina and Greece. (71st among 117 countries)

31

35 36

38

43 45

47 48

53 54

57 59

67 68 69 71

30

35

40

45

50

55

60

65

70

75

Po

rtek

iz

Hu

nga

ry

Slo

vak

Rep

.

Ital

y

Po

lan

d

Ind

ia

Gre

ece

Ch

ina

Ru

ssia

Arg

enti

na

Bra

zil

Mex

ico

Ro

man

ia

Ukr

ain

e

Ind

on

esia

TUR

KEY

Source: World Economic Forum

Global Competitiveness Index (2005)

103

(44th among 148 countries)

Source: World Economic Forum

Global Competitiveness Index (2013)

29

38

42 44

49 51

55 56

60 63

64

76 78

84

91

104

25

35

45

55

65

75

85

95

105

Ch

ina

Ind

on

esia

Po

lan

d

TUR

KEY

Ital

y

Po

rtu

gal

Mex

ico

Bra

zil

Ind

ia

Hu

nga

ry

Ru

ssia

Ro

man

ia

Slo

vak

Rep

.

Ukr

ain

e

Gre

ece

Arg

enti

na

104

(84th among 175 countries)

Source: World Bank

Ease of Doing Business (2006)

62

69 70 71

84

93

97

108

111

122

131 132 134

138

60

70

80

90

100

110

120

130

140

Mex

ico

Ital

y

Uru

guay

Ro

man

ia

TUR

KEY

Arg

enti

na

Ru

ssia

Ch

ina

Gre

ece

Bra

zil

Ind

on

esia

Ukr

ain

e

Cro

atia

Ind

ia

105

(69th among 189 countries)

Source: World Bank

Ease of Doing Business (2013)

53

65 69

72 73

88 89 92

96

112 116

120 126 134

20

40

60

80

100

120

140

Mex

ico

Ital

y

TUR

KEY

Gre

ece

Ro

man

ia

Uru

guay

Cro

tia

Ru

ssia

Ch

ina

Ukr

ain

e

Bra

zil

Ind

on

esia

Arg

enti

na

Ind

ia

106

Favorable Demographics

Source: Eurostat

Shar

e o

f 1

5-2

4 y

ears

old

in T

ota

l Po

p. (

%)

16,6

7 9 11 13 15 17 19 21

Spain

Italy

Andorra

Slovenia

Greece

Portugal

Bulgaria

Germany

Czech Republic

Serbia

Switzerland

Ireland

Croatia

Estonia

Latvia

France

Austria

Hungary

Luxembourg

Finland

Netherlands

Ukraine

Poland

Denmark

Sweden

United Kingdom

Slovakia

Norway

Malta

Lithuania

Montenegro

Iceland

Macedonia

Georgia

Moldova

Turkey

Azerbaijan

107

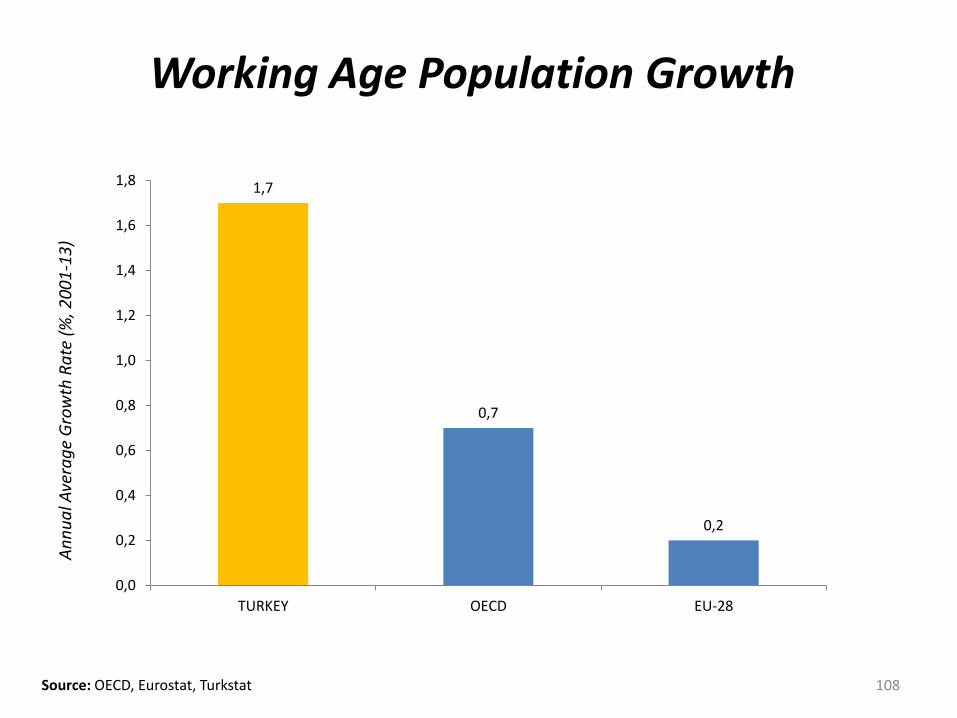

1,7

0,7

0,2

0,0

0,2

0,4

0,6

0,8

1,0

1,2

1,4

1,6

1,8

TURKEY OECD EU-28

An

nu

al A

vera

ge

Gro

wth

Ra

te (

%, 2

00

1-1

3)

Working Age Population Growth

Source: OECD, Eurostat, Turkstat 108

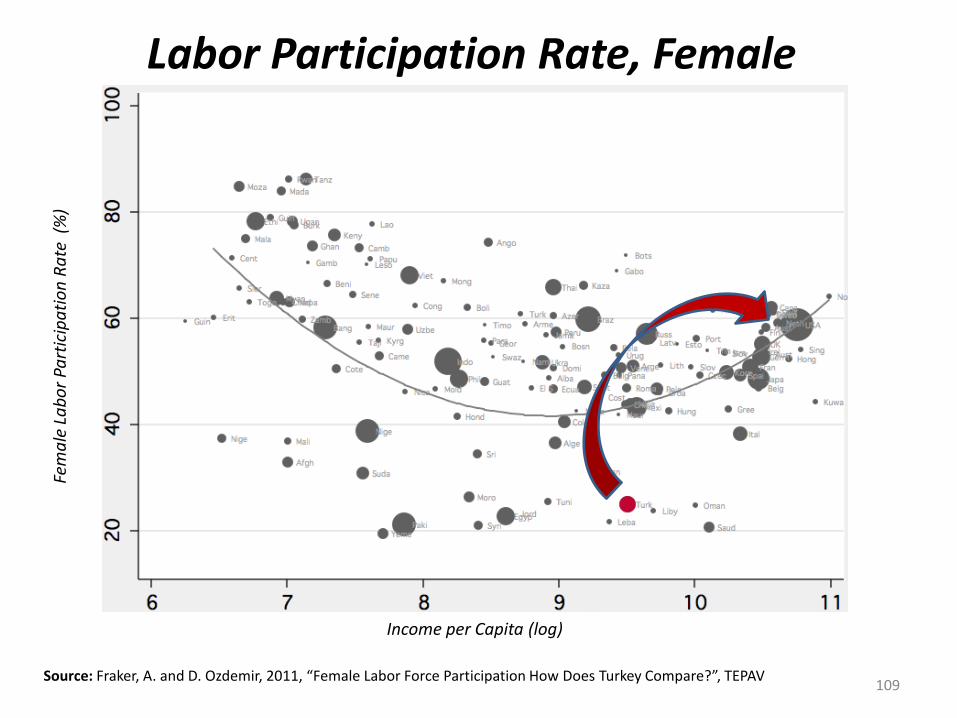

Labor Participation Rate, Female

Source: Fraker, A. and D. Ozdemir, 2011, “Female Labor Force Participation How Does Turkey Compare?”, TEPAV

Fem

ale

La

bo

r Pa

rtic

ipa

tio

n R

ate

(%

)

Income per Capita (log)

109

Source: TURKSTAT, Eurostat, WB

(

20

04

=10

0)

75

80

85

90

95

100

105

110

115

120

125

130

2004 2005 2006 2007 2008 2009 2010 2011 2012

TURKEY South Africa Croatia Hungary

Poland Brazil Russian Federation Indonesia

China Mexico India

TURKEY

Female Labor Participation Rates

110

Labor Participation Rate, Female

Source: Turkstat, OECD 111

(%, F

eb 2

01

4)

23,3

28,7

14,6

24,1

32,3

39,2

70,4

10

20

30

40

50

60

70

80

2004 Total Illeterate Less than highschool

High school Vocational highschool

Higher education

OECD Average: 62,3

Formal Employment rising with Education

112 Source: TURKSTAT

No education

Primary

Lower secondary

Upper secondary

Tertiary

0

10

20

30

40

50

60

70

80

90

100

020406080100

(Informal Employment, %)

(Form

al Em

plo

ymen

t , %)

113

National Employment Strategy, 2014-23

Improving confidence and flexibility in the labor market

Increasing employment of the disadvantaged groups

Improving the relation b/w education & employment

Improving the relation b/w employment & social protection

114

Targets for 2023 Vision

Unemployment rate down to 5%

Employment rate up to 55%

Non-farm informal employment down to 15%

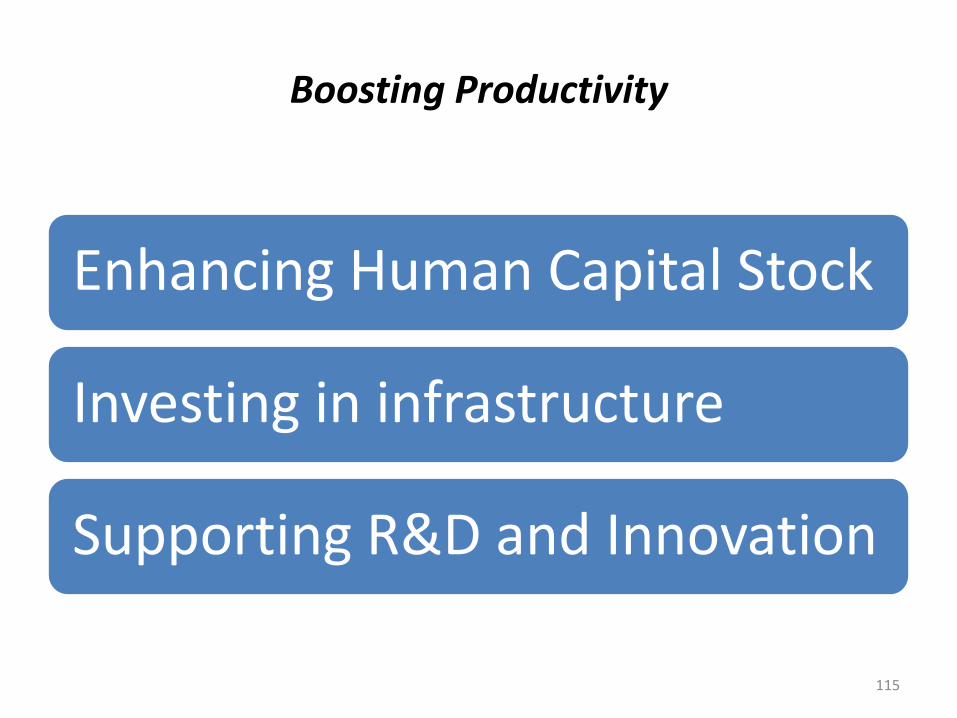

Boosting Productivity

Enhancing Human Capital Stock

Investing in infrastructure

Supporting R&D and Innovation

115

Higher Labor Productivity in Large Companies

116

( La

bo

r P

rod

uct

ivit

y o

f La

rges

t to

Sm

alle

st E

nte

rpri

ses,

% ,2

01

0)

Source: TURKSTAT, OECD, Enterpreneurship at a Glance 2013

4,2

1

1

2

2

3

3

4

4

5TU

RK

EY

Po

lan

d

Hu

nga

ry

Po

rtu

gal

Ital

y

Spai

n

Slo

vak

Rep

.

Slo

ven

ia

Be

lgiu

m

Swit

zerl

and

Au

stra

lia

Au

stri

a

Esto

nia

Swed

en

Fin

lan

d

Fran

ce

Ger

man

y

UK

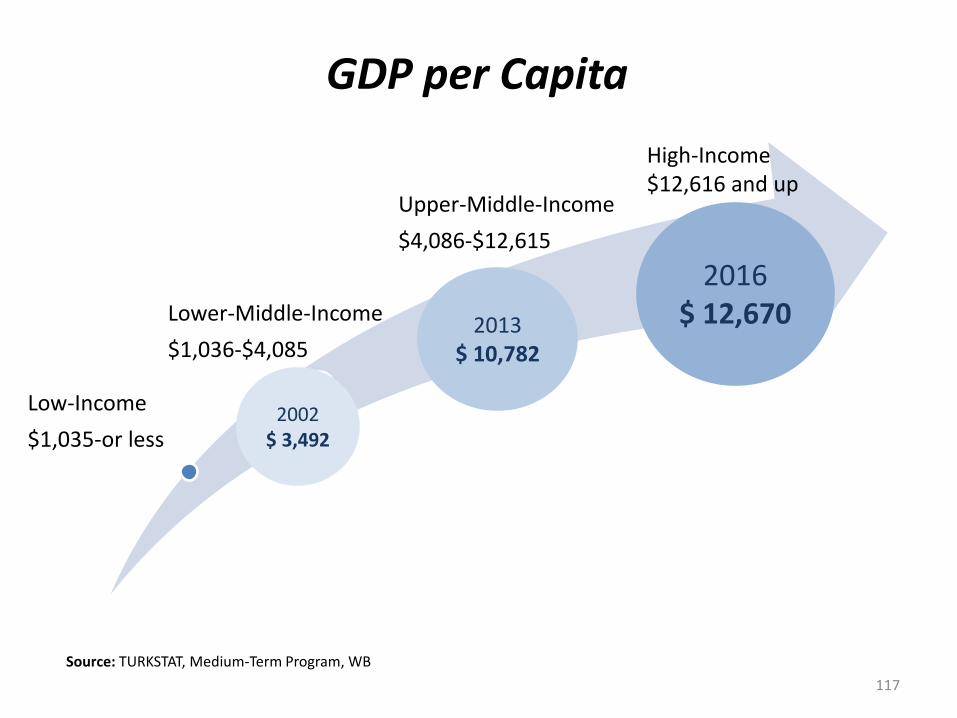

GDP per Capita

Low-Income

$1,035-or less

Lower-Middle-Income

$1,036-$4,085

Upper-Middle-Income

$4,086-$12,615

117

High-Income $12,616 and up

2002 $ 3,492

2013 $ 10,782

2016 $ 12,670

Source: TURKSTAT, Medium-Term Program, WB

GDP

Source: TURKSTAT, Medium-Term Program,PwC

2002

2050

2002 $ 230 billion

2050 $ 5 trillion

2013 $ 820 billion

2023 $ 2 trillion

118

Thank You…

119

Related Documents