CHAPTER ONE 1. Introduction 1.1 Background of the Study Modern organization originated in England during industrial age in the 1770's. Industrial age is known for the invention of machines, specifically for cotton milling and manufacturing cloths. All organizations need inputs of goods and services from external supplies or providers and it need resources for their survival. In organization concept, the basic types of resources are material resources, financial resources, human resources and information resources. Therefore managing the material resources of an organization is one of the important areas. (Tesfaye Debela, 2000) The scarcity of materials, which was felt during World War I in USA to a very large extent and it, has become difficult for production managers to supply the War goods. This has created it necessary to organize the Materials Management department for managing large inventories in stores and to analyze the problems arising to control and economize inventory cost problems and shortage elimination. The materials management was included as an important function of the management. With the development of principles of scientific management by F.W. Taylor in 20th century, the economic use of materials in all the organizations was critically felt to reduce the cost of production. The concept of materials management was widely spread during World War II. The conceptual foundation that gave rise to the

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CHAPTER ONE

1. Introduction 1.1 Background of the Study

Modern organization originated in England during industrial age

in the 1770's. Industrial age is known for the invention of

machines, specifically for cotton milling and manufacturing

cloths. All organizations need inputs of goods and services

from external supplies or providers and it need resources for

their survival. In organization concept, the basic types of

resources are material resources, financial resources, human

resources and information resources. Therefore managing the

material resources of an organization is one of the important

areas. (Tesfaye Debela, 2000)

The scarcity of materials, which was felt during World War I in

USA to a very large extent and it, has become difficult for

production managers to supply the War goods. This has created it

necessary to organize the Materials Management department for

managing large inventories in stores and to analyze the problems

arising to control and economize inventory cost problems and

shortage elimination. The materials management was included as

an important function of the management. With the development of

principles of scientific management by F.W. Taylor in 20th

century, the economic use of materials in all the organizations

was critically felt to reduce the cost of production. The

concept of materials management was widely spread during World

War II. The conceptual foundation that gave rise to the

management boom during and after the World War II, also gave

birth to an entirely new approach and idea in the management

field of what we understand largely today as materials

management. Although the concept is of recent origin and had its

root in the USA, it has now spread fairly widely all over the

world. (Datta,2009). Material management is a scientific

technique, concerned with Planning, Organizing &Control of flow

of materials, from their initial purchase to destination. It is

concerned with planning, organizing and controlling the flow of

materials from their initial purchase through internal

operations to the service point through distribution.

In Ethiopia the first government organization was established at

the time of the reign of minilik II at the beginning of the 20th

century. Public purchasing in Ethiopia was started recently

with the introduction of modern government administration. The

first form of rule and regulation of public purchasing emerged

during the reign of Haileselass I and recently the federal

government purchasing regulation No.1, 1991E.C and inventory

administration directive No.6/1991 helps to carry out materials

management of the public sectors.(Tesfaye Debela,2000)

Generally, materials in the form of raw materials, semi finished

goods, equipments, and supplies are of greater significance for

the success of organizational objectives and goals. So, properly

established materials management unit has very great

contribution to an organization through many ways: on time

delivery of required items with fair price, maximum inventory

controlling, adequate store management and other related

functions.

1.2 Description /Profile/of the study Area

Hintalo- Wejerat woreda is found in Tigray regional state about

760 km far from Addis Ababa to the North. It is located in the

southern-east part of Tigray. Adigudem is the head town of the

woreda. Before the establishment of federal democratic republic

of Ethiopian constitution the woreda was separated in three

woredas namely Hintalo, Adigudem and Wejerat while now it

consists them calling as Hintalo-Wojerat woreda.

The woreda is bounded with Enderta woreda in the North, Samre-

Seharti in the west, Emba Alaje south, Raya Azebo and Afar

region in the East. The total area of the woreda is about 91,

209 hectares and the average altitude of the woreda is about

14000-2500 meters. According to the 2007 census, the total

population of the woreda is 152,219 of which 95% are engaged in

farming. Both crop and livestock productions are the basic

economic activity of the people. The major production activity

in the study area is rain fed agriculture. The main crops are

cereals such as Barely, Wheat, Teff, Maize, Sorghum and pulses

like Bean, Vetch, chickpea, and lentils etc.

The woreda has 22 Tabias out of which 21 are rural Tabias

/peasant associations/ while one Tabia is town/ Urban-

administered by municipality. There are small towns govern

within the rural areas viz, Dongolat, Hintalo, Mai-nebri, Debub,

Hiwane and Adikeyh. Almost, all populations are Tigrigna

language speaker. Recently in the woreda there are about 22

public sectors having 1200 permanent employees to provide the

desired social, political and economical services to the

community. Among which Hintalo- Wejerat woreda finance office is

my research studies focus on. It has four major business

processes

1.3 Statement of the problem

Materials Management is the integrated functioning of purchasing

and allied activities so as to achieve the maximum coordination

and optimum expenditure in the area of materials.(Nair,1990)

From different activities of materials management, purchasing is

one among them. Purchasing plays a key role for the attainment

of organizational objectives by providing right quality of

inputs for users at the right time and cost. At woreda level

Purchasing is under taken by the finance office for the whole

public sectors of the woreda twice a year by collecting and

organizing their purchase requisition and through bidding.

However a number of problems are observed and complains are

heard from user sectors. that is ,about services provision

complains, about purchasing process(the purchased material

qualities, exaggerated price, delivery time)complains, about

material handling and issuing by store section, fixed asset

administration and others. All the above problems which are

raised from the public sectors taken the attention of the

researcher to assess how material management is practiced in

Hintalo Wejerat woreda finance office and to find the fact

through scientific research and to suggest appropriate remedial.

1.3.1 Research Questions

Therefore, this study attempts to answer the following basic

research questions,

How the concepts of materials management look like in the

finance office?

How the purchasing activities, inventory handling and

material classification are under taken?

What are procedures used in receiving, issuing, stock

taking and verification of material?

What and how documents are kept?

How does work integration of purchasing and store section

with other sectors of the woreda?

1.4 Objective of the Study

1.4.1 General Objective

The objective of this study is to assess the practice of

material management in the organization under consideration to

suggest on how to curb the problem.

1.4.2 Specific Objectives

According to general objective seen on the above, the specific

objectives of this study are as follows:

To assess how material management unit is organizing.

To identify how the purchasing activities inventory

handling and material classification are under taken.

To examine the procedures used in receiving, issuing, stock

taking and verification material.

To examine what and how documents are kept.

To evaluate the work integration of purchasing and store

section with other sectors.

1.5 Significance of the Study

This study was required for in partial fulfillment of the

requirements for obtaining the degree of Bachelors of Arts in

Development Management through assessing the practice of

material management in Hitalo wejerat woreda finance office and

it suggested possible solution to the finance office all sectors

of the woreda how to solve the problem observed and could serve

as a base for auditors, finance officers, researcher and others

for further investigation.

1.6 Scope /Delimitation of the Study

The study was conducted about how material management practice

in Hitalo wejerat woreda finance office: especially in

purchasing and property administration business unit, how did

the unit practice centralize purchasing activities for the 22

sectors of the woreda and their way of store management,

inventory control. Data was collected from user sectors,

purchasers, store keeper and auditors. The scope was restricted

on 2003 E.C--2005 E.C performance.

1.7 Limitations of the Study

Even though different efforts have been made, the researcher

faced some challenges while doing this study. The limitations

that faced the researcher were financial and time constraints.

These constraints solved by the researcher through wisely

utilizing the available scarce resources. Knowledge and

experience limitation of the researcher also another

constraints, this is solved through reading different related

research and books.

1.8 Organization of the Paper

The study paper is organized in five major issues in sequential

order. In chapter one the introduction of the study is raised.

What prominent scholars and researchers said about the study

under consideration critically is presented in chapter two under

the review of literature part. In chapter three Research Design

and Methodology is presented. In chapter four data collected is

analyzed, presented and interpreted. Finally, in chapter five

the conclusion and recommendation is presented.

1.9. Operationalization of Key Terms

Specification: means a document describing the quality, type and

standard with which the required goods, services, works or

consultancy services should comply.

Stock: means items that are purchased or produced or donated and

are not immediately consumed, which is temporally kept in a

storehouse until needed for use.

Requisition form: forms that are uses during purchase or

material requisition.

Materials: the substance or substances of which a thing is made

or composed.

Management: the process of dealing with or controlling things

or people. It is the art of getting things done through and with

people in formally organized groups.

CHAPTER TWO

2. Review of Related Literature

2.1 Introduction

In most of the organizations a lot of budget allocated to the

material resources. A material resource is one of fundamental

resources of organization. So, greater attention is required

towards the management of operations associated with materials.

The importance of materials management lies in the fact that it

facilitates operation and efficient use of materials and at the

time reduces cost.

In accordance with the statement of the problem in part one;

this part will deal with the overview of related literature.

2.2 An overview of Materials Management

2.2.1 Definition of material management

Different scholars have defined material management in several

ways we will see some of the definitions below:

Materials Management is the integrated functioning of purchasing

and allied activities so as to achieve the maximum coordination

and optimum expenditure in the area of materials (Nair, 1990)

Material Management is concerned with the management of material

flow into, through and out of system. It is decision making with

respect to design, procurement, storage, issue, packing and

handling and accounting of materials to get most out of every

amount invested in materials (Singh, 2008)

Material Management define as the function responsible for the

coordination of planning, sourcing, purchasing ,moving, storing

and controlling materials in an optimum manner so as to provide

a pre-decided services to the customer at a minimum cost

(Gopalakrishnan p. and sundaresan m.1977).

Generally, we can understand defining material management is

very broad concept and it may vary the type of organization and

organization

2.2.2 Function of Materials Management

Materials management is that activity of management which

primarily concern with the efficient flow of materials, to,

through and out of an organization for optimum use of materials.

The function therefore:

Materials forecasting, budgeting, planning and programming.

Scheduling, purchasing and procurement

Receiving and receiving inspection as to quality and quantity

Inventory control , storage and warehousing

Materials handling, movement control and traffic

Dispatch, shipping and disposals including wastes, scarps and

surplus materials.(Datta, 2009)

2.2.3 Objectives of Materials Management

The objectives of materials management can be categorized in to

Primary objective s and Secondary objectives.

The Primary objectives of materials management are efficient

materials planning, Buying or Purchasing, Procuring and

receiving, Storing and inventory control, Supply and

distribution of materials, Quality assurance, Good supplier and

customer relationship, improved departmental efficiency.

There can be several secondary objectives of materials

management. Some of them are Efficient production scheduling, To

take make or buy decisions, Prepare specifications and

standardization of materials, To assist in product design and

development, Forecasting demand and quantity of materials

requirements, Quality control of materials purchased, Material

handling, Use of value analysis and value engineering,

Developing skills of workers in materials management, Smooth

flow of materials in and out of the organization.

To fulfill all these objectives, it is necessary to establish

harmony and good co-ordination between all the employees of

material management department and with the other departments of

the organization.

(www.newagepublishers.com/samplechapter/001386.pdf ).

2.3 Major Activities of Materials Management

2.3.1 Purchasing

All organizations require supplies of materials and services

from outside sources. Therefore, purchasing and procurement are

common functions in almost all organizations. Purchasing implies

the act of exchange of goods and services for money, whereas

procurement is a generic terms with a wider connotation for the

total responsibility of acquiring goods and services. (Datta,

2009)

According to different scholars purchasing has several

definitions some of the definitions as follow:

Purchasing refers to a function in business whereby the

enterprise obtains the inputs for what it produces, as well as

other goods and services it requires. Purchasing is one of the

basic functions common to all types of business enterprise.

These functions are basic, because no business can operate

without, them (Dobler 1984)

Purchasing is the responsibility of buying the kinds and

quantities of materials authorized by the requisitions issued by

production scheduling, inventory control, engineering,

maintenance and other department of function requiring materials

(Leenders, 1989).

Generally “Purchasing” refers to the process of ordering and

receiving goods and services. It is a subset of the wider

procurement process. Purchasing refers to the process involved

in ordering goods such as request, approval, creation of a

purchase order record (a Purchase Order) and the receipting of

goods.

2.3.1.1. Fundamental Objectives of Purchasing

Fundamental objectives of purchasing is enumerated as follows

:( Datta, 2009)

To maintain continuity of supply

In doing so, minimum investment in stores and materials

inventory must be ensured, consistent with safety and economy.

Duplication of purchases, wastes, obsolescence and costly

delays must be avoided.

Proper quality standards based on suitability criteria must be

maintained.

Materials must be procured at lowest possible cost, consistent

with quality and service requirements.

2.3.1.2. Purchasing Principles

The success of any organization activity is largely dependent

on the procurement of materials of right quality, in the right

quantities, from the right source, at right time and at right

price – popularly known as five ‘R’s of the art of efficient

purchasing . In the right quality ;In the right quantities;

In the right time; At the right price; From the right

source/supplier.

Right quality: The materials are the basic input and the

quality of the output. It should be noted that best quality is

not always the right quality. The right quality is determined by

the cost of the material and the technical characteristics as

suited to the specific requirements. The right quality should be

defined clearly and should be described in terms of

specifications. Material specification tells the supplier

exactly what the purchaser wants to buy. The right quality can

be measured by:- Durability, composition, performance, physical

tests, chemical analysis, grade.

Right quantity: The right quantity of the materials is

determined on the basis of economic ordering quantity (E.O.Q).

It is advantageous to purchase the materials on the basis of EOQ

lots. The EOQ describes the size of the order at which the

ordering costs and the inventory carrying cost will be the

minimum. The ordering cost consists of the cost of paper

processing such as paper, typing, postage, filing, cost of

personnel; the costs incidental to order placing such as follow

up, receiving, inspection etc. Thus ordering cost and carrying

costs are mutually exclusive. Therefore, the right quantity

means not less or more than the requirement.

Right time: The materials should be purchased at right time so

that it may not result in either excess investment in the stocks

or may result into stock outs. Efforts must be made to replenish

the materials at a point where they are reaching at the

reordering level. The purchase action is initiated at a time

when the material reaches to its pr-decided reordering level.

The reordering level is decided on the basis of the rate of

consumption and the lead time. It should be decided on the basis

of the probability of maximum periodic consumption and maximum

lead time. As stock holding is directly related with the lead

time, efforts should be directed towards the reduction of the

lead time so that carrying costs can be reduced to the minimum.

Right price: The investments in inventories are determined by

the prices charged for them. All attempts should be made to

procure the materials at right price because a slightest

reduction in the price results in substantial absolute monetary

gain. It should be noted that the low bidder is not always the

best bidder. The right price can be availed through searching

for the proper sources of supply and comparing all such sources

on some scientific basis.

Right source: The right source is a key consideration in

purchasing as all other ‘R’s. The suppliers are not only

supplying the required materials but they also supply the

information. The selection of right source involves the

considerations such as search for the more and more sources,

selection of the appropriate source through some scientific

analysis, negotiating with the selected supplier and post

purchase rating of the supplier.

Purchasing is both a science and an art. It is a science because

there are certain basic principles of purchasing. The

application of these principles, when put into practice, makes

the art of purchasing an interesting job. Every purchaser

should, therefore, acquaint himself with these basic principles

and apply them to his job. (Datta, 2009)

2.3.1.3. General procedure of purchasing

Procedures used in completing a total transaction normally vary

among different types of purchases and in different

organizations. However, purchasing procedures refers to the way

in which a purchase transaction is carried through from its

inception to its conclusion. A purchasing proceeding usually

begins with an investigation of new suppliers can be made for

renegotiating contracts with existing suppliers.

The general cycle of activities in purchasing most operating

materials and suppliers is fairly standardized. The following

steps constitute the typical purchasing procedures.

1. Organizing of purchase requisition.

The purchasing cycle begins with the recognition of needs for

materials from the users that can be units, individuals, or

stores. The need for a purchase typically originates in one of a

firm operating departments or in its inventory control section.

It is a stimulus for purchaser to initiate purchasing. The

essential information which requisition should contain includes

a description of the material; quantity, date required;

estimated unit cost; the date; an authorized signature. There

are two important forms for requisition.

Material requisition form: is usually filled by the using

department and presented to the store. Then, the store section

issues the material to using department.

Purchases requisition form: is a form filled by the store or

the user department to request purchases of items.

2. Verification of purchase requisition and budget.

The purchasing department verifies whether the requisition is

appropriately filled or not.

3. Evaluation and selection of the supplier.

As soon as the need has been established and precisely describe,

the buyer begins an investigation of the market to identify

potential source of supply. In the case of routine items for

which supplier relationship have already been developed, little

additional investing may be required to select a good source on

the other hand the purchase of high-value or new item may

require lengthy investigation of potential suppliers to make a

decision about the most desirable supplier.

4. Preparation of purchase order.

Once a supplier has been selected the purchasing department

prepares and issues a serially numbered purchase order. In most

cases the cases the purchase order becomes a legal contract

document. For this and other reasons the buyer in preparing and

wording the order should take great care.

5. Follow up

Also called expediting, purchasing bears full responsibility for

and order until the material is received and accepted. When

there is a reasonable chance that the supplier may not stay on

schedule important orders with critical delivery date should

receive active follow-up attention. There may be a need to speed

up (expedite) or even delay (De-expedite) delivery if the buyers

timing requirements under go unexpected changes.

6. Receiving and Inspection

The supplier ships materials with the packing slip, which

itemizes and describes the contents of the shipments. The

receiving clerk uses this packing slip in conjunction with

his/her copy of the purchase order to verify that the correct

material has been received.

7. Payment

The typical procedure involved is a simultaneous of the purchase

order, the receiving report and the invoice. By checking the

receiving report against the purchase order, the purchaser

determines whether the quantity and type of material ordered was

in fact received. Then by comparing the invoice with the

purchase order and received.

8. Evaluating the purchasing performance

Purchasers need to evaluate whether the materials purchase from

the supplier have satisfied the need of the users. This

evaluation will help whether to consider the supplier next time.

The specific procedures employed by each should be designed to

meet the unique needs of that firm. Properly designed procedures

should accomplish four objectives according to Dobler. These

are:-

i. Fulfill each task satisfactorily with minimum of time, effort

and proper work.

ii. Effectively communicates and coordinate the efforts of one

work group with another.

iii. Minimize overlapping effort and group conflicts.

iv. Permit effective management by exception (Dobler, 1996).

2.3.1.4. Methods of Procurement

Depending on the nature of the required goods, the quantity &

value involved and the period of supply, the Purchase Committee

must select after deliberation one of the following modes of

procurement for items:

(1) Open tender - by advertising in the press.

(2) Limited tender - by sending written enquiries to known,

reputed suppliers.

(3) Single tender - by sending written enquiries to a Single

supplier if, (a) In case of emergency, the required goods are

necessarily to be purchased from a particular source (b) It is

in the knowledge of the indenter that the stores/equipment

required is manufactured only by that supplier and none else

The following methods shall be used in public procurement

in Ethiopia:-

Open Bidding, Request for Proposals, Restricted Tendering,

Request for Quotation, Two stage Tendering, and Direct

Procurement.(Proclamation No. 649/2009, art 33)

Conditions for use of Restricted Tendering: Public bodies may

use restricted tendering as a method of procurement only where

the following conditions are satisfied:

It is a ascertained that the required object of procurement

is available only with limited

suppliers;

Where a repeated advertisement of the invitation to bid

fails to attract bidders in respect of procurement subject

to the directive to be issued by the Minister. (art. 49).

Conditions for use of Direct Procurement: Public bodies may use

direct procurement only where the following conditions are

satisfied: (a) when in absence of competitions for technical

reasons the goods, works consultancy or other required services

can be supplied or provided only by one candidate;(b) for

additional deliveries of goods by the original supplier which

are intended either as parts of replacement for existing

supplies, services or installations or as the extension of

existing supplies, services or installation where a change of

supplies would compel the public body to procure equipment or

services not meeting requirements of interchangeability with

already existing equipment or services;(c) within limits defined

in the procurement directive, when additional works, which have

been not included in the initial contract have, through

unforeseeable circumstances, become necessary since the

separation of the additional works from the initial contract

would be difficult for technical or economic reasons; (art 51)

(Proclamation No. 649/2009)

Conditions for use of Request for Proposal: Public bodies may

engage in procurement by means of request for proposals when

it seeks to obtain consultancy services or contracts for which

the component of consultancy services represents more than 50%

of the amount of the contract. (art 53)

Conditions for use of Request for Quotations: Public bodies

may engage in procurement by means of request for quotations for

the purchase of readily available goods or for procurement of

works or services for which there is an established market, so

long as the estimated value of the contract does not exceed an

amount stated in the procurement directive to be issued by the

Minister. (art 55)

Conditions for use of Two-Stage Bidding: Public bodies may

engage in procurement by means of two-stage bidding: when it is

not feasible for the public body to formulate detailed

specifications for the goods or works and in the case of

services, to identify their characteristics and, in order to

obtain the most satisfactory solution to its procurement needs;

When the public body seeks to enter into a contract for the

purpose of research, experiment, study or development, except

where the contract includes the production of goods in

quantities sufficient to establish their commercial viability or

to recover research and development costs; (art 57)

(Proclamation No. 649/2009)

2.3.1.5. Purchasing Organization Structure

Centralized purchasing: - when a business organizes its

purchasing function centrally only one purchasing department is

established. This is located centrally and is responsible for

making purchases for the whole organization. Centralization of

purchasing enables economies to be taken advantage of and fewer

orders being made.

Decentralized purchasing: - when a business separates the

purchasing function in to a number of separately organized

divisions, each division is autonomous and is responsible for

purchases made within its sphere of operations. (Dewan, 1996).

2.3.1.6. Purchasing Research

Purchasing research is systematic investigation to locate better

or alternative source of supply, to improve the quality and the

price, to value analyses various items, standardize

specifications and sizes, reduces varieties, find substitutes

for items in short supply, etc. It involves collecting and

docketing various information, such as names of suppliers, their

production capacity, annual output, grades and qualities

available, trend of price, etc.(Nair 1990)

2.3.2 Store Management

The stores in most organizations is an area in which all kinds

of materials needed for production, distribution, maintenance,

packaging, etc. are stored, received and issued. The stores

function is, therefore, basically concerned with holding stocks.

However, stores management covers a great deal more than just

these aspects, and includes the following activities: holding ,

controlling and issuing stocks; control of all storehouse, stock

yards and outside storage; materials handling functions;

quality control activities; etc.(carter Ray et.al,2005)

According to stock management manual (MoFED ,2010), The Stock

management involves the following functions and activities:

1. Identifying stock: - this function involves classification

and coding of stock. A code is a system of symbols or numbers or

a combination of symbols and numbers used for representing data

for purposes of communication or for storage or for processing

information.

According to (Saxena J.p., 2003) codification defined as it is

used to describe an item in short, this avoiding the necessity

of a long statement every time the need to describe the item

arises. Codes are very useful for the following reasons:

Every one finds a similar meaning in identifying an item

with the help of a code.

A code eliminates the possibility of duplication in names.

Items with different features but for same purpose can be

differentiated easily.

A code helps avoid long descriptions in Purchase

Requisitions.

Entries in bin cards, stick control cards, and account

records are made easily with codes.

The methods of codification are: Numerical code, Mnemonic code

(using alphabets), consonant code (abbreviation) and Alpha-

numeric code.(Saxena J.p. ,2003)

Classification means systematic arrangement in groups or

categories of stocks according to end use. The important

principles of stock classification are the like should be

associated with the like; simplicity and ease of understanding of

the stocks should be given paramount consideration.(MoFED ,2010)

2. Receiving: - actives performed in this function include

receiving of fixed assets, and stocks from all sources and

conducting inspection. Stocks and fixed assets may be received

in storehouses from outside suppliers, donors and from user

departments within the organization. Stocks must be properly

looked after when they arrive. The problem of quantity shortage,

damaged materials, incorrect items shipped, is detected during

receiving.

The main forms which shall be used in receiving an item are:

Receipt for articles or property (Model 19) and Damage/Shortage

Report (DSR)

3. Issue: - handing over stocks and fixed assets to users

departments and outsiders are the activities under this function.

Service given by storehouse to users department becomes effective

at the point where the store keeper issue stocks. Issue can be

divided into issue to user departments/units and issue to outside

branch stores and consumers. Stock represents money, in order to

avoid misappropriation or waste procedure should be laid. From

scheduling point of view, issues are made: (MoFED ,2010)

A. On imp-rest basis: - this is issuing stock, at the end of

given period, say a week or a month. The user concerned prepares

a list of materials consumed during that given period of time

and presents stores requisitions. This type of issue is

appropriate for stationery supplies.

B. Replacement issue: - for certain items like vehicle tires and

tools, users are required to present used article to the

storekeeper before a new one can be issued.

C. for non stock items like fixed assets, goods are issued and

delivered upon receipt by the storekeeper. The main forms that

shall be used are: Stores Requisition (Model 20), Issues for

articles or property (Model 22) and Gate Pass (GP)

The procedure for stock issue for users departments

involves the following three:

1. Approval of Requisitions: Before stocks can be issued there

must be proper authorization. Store keepers should keep full

details of the names, title and specimen signature of all

persons delegated to approve issue notes in a separate file. For

some materials, it might be necessary to restrict issuance to

certain levels of management, e.g., use of drugs, chemicals or

explosives must be restricted to authorized individuals.

2. Processing of Requisitions: As stocks are needed they should

be requisitioned by the users department using Model 20. The aim

of raising a Stores Requisition is to authorize issue of stocks.

The stores requisition is prepared by users department in

single. This form should be forwarded to Property Administration

Officer (PAO) for approval.

Stocks of any type should only be issued to persons who produce

properly raised Stores Requisitions. Following the receipt of

the store requisition, the storekeeper prepares the issue sheet

and pick and handover the stock requested.

The store keeper prepares model 22 in 3 copies to be distributed

as follows.

1. The original shall be attached to the Stores Requisition and

sent to the stock clerk for posting the issue in stock

records

2. The duplicate copy shall be sent to the department/unit that

requisitioned for the stocks

3. The triplicate copy shall be retained in the pad by the

storekeeper for reference.(Ibid)

FIFO method: - First in first out method (FIFO) is in most

common use. It assumes that materials are issued from the oldest

stock and their unit costs also represent the oldest costs on

the stock ledger. Under this method goods consumed are those

which have been in stock on hand for the longest period and

those remaining represent the latest purchases. This method is

fairly simple and compatible with many organizational

operations. (Datta,2009) .In Ethiopia, according to regulation

number 6,1991 the store man should issue using FIFO method

(art.18,sub art 3) (Tesfaye Debela 2000).

4 .Stock record and accounting: - the major activities under this

function are keeping and updating and reporting the record for

the movement of stock. Control of stocks cannot be performed in

an efficient manner without some means of capturing and storing

information. Adequate and timely record-keeping is required for

proper stock-control. Records maintained keep track of the

movement of stocks into and out of the storage areas and the

balance of stocks remaining in the store. Careful handling and

proper use of property cannot be enforced without some

documentation. (MoFED, 2010)

The two most widely used stock documents are bin cards and stock

record cards.

1. Stock Bin card:-the purpose of maintaining a Stock Bin Card

on the shelf/rack is to show at glance the quantity available.

Bin cards are maintained by the storekeepers with the physical

stock itself by attaching bin cards or racks, using a separate

card for each item of stock.

2. Stock Record Cards: - as opposed to bin card, stock record

cards are kept together in one place under the custody of the

stock clerk. The purpose of maintaining Stock Records Cards is

to have record of the cost price and value of stock received,

issued and remaining balance in the storage. One card should be

prepared for each item in the stock. The stock card should be

arranged and maintained based on the stock classification and

coding.

5. Stock taking and stock control: - this function involves the

periodic physical count of stock and fixed assets in

storehouses, and ensuring materials and supplies are available

when needed.

Stock control is the activity of determining the range and

quantities of materials which should be stocked. It involves

techniques of maintaining stock items at levels which give

satisfactory service level while minimizing stock holding costs.

The major objective of any stock control system is to assure

that materials are on hand when they are needed. Specifically

the objectives are:

To determine when to replenish, by what quantities to

replenish and to fix minimum and maximum levels for each

stock item.

To identify damaged/obsolete stock items

Stock taking is the complete process of physically counting,

measuring or weighing the entire range of items in the stores

and recording the results in a systematic manner. The purposes

served by stock taking are as follows:

To verify the accuracy of stock records

To support the value of stock shown in the stores

documents by physical verification

To disclose the possibility of fraud, theft or loss

To reveal any weaknesses in the system for the custody and

control of stock. (Ibid)

Types of Stocktaking Operation

Periodic stocktaking:-it is performed at regular intervals,

usually at the end of each financial year or in some cases at

quarterly intervals. It is the most common method of checking

and counting the stock.

Continuous stocktaking:- in this system a selection or section

of items are checked every week. Throughout a twelve-month

period every item in stock would, therefore, be physically

counted and checked, without having to close the store.

Spot-checking: Spot-checks are designed to verify the stock

held, without a prior warning which could provide time for stock

to be replaced illegally. The system also act as a deterrent

against those who may contemplate theft, knowing that a sudden

check could herald an investigation.(carter Ray et.al ,2005)

6. Storage: - the proper keeping and preservation of stock and

fixed assets while it is in store houses and stock yards.

(MoFED, 2010)

2.3.3 Obsolete, Surplus and Scrap Management

Scrap materials:-these are rejects from the production process,

which cannot be used anymore and are to be thrown away.

Similarly, old, broken parts, rejects, cuts pieces of iron

sheets, angle iron, gaskets, insulation ,materials etc., are

generate during maintenance and repair works. Scrap materials,

if not disposed of, occupy valuable space. Disposal of scrap

material is a continuous process in a stores Division. (Saxena

J.p., 2003)

Surplus materials:- surplus materials are materials in the

store, which are more than what the user department requires due

to excessive purchasing.(Ibid)

Obsolete item are these materials and equipment which are not

damaged and have economic worth out no longer useful for the

operation of the many reasons.(Gopalakrishnan p. and sundaresan

m,1977).

According GOFAMM in Ethiopia, there are four commonly known

reasons to start the fixed assets disposal process. These are

when the asset is Unserviceable, obsolete, surplus and

abandoned.

Unserviceable – because of many factors including normal usage

of the assets, old age or accident, the cost of repairing the

asset might become much more expensive than the use the public

body can drive out of it. In such cases it becomes a rational

decision to dispose the asset instead of incurring additional

repair cost.

Obsolete - Obsolescence could happen due to several factors. An

asset could be rendered obsolete due to technological change. It

may not fit with other assets in use. The output of the asset

might not be accepted by the end user. Similarly, using the

asset might not be economical in terms of cost and time. Hence,

the asset needs to be disposed.

Surplus - Even if the asset is in a good condition, and is not

obsolete, the public body might not use it currently and in the

near future for some reason. Other public bodies might need such

assets. In such cases it is generally economical to dispose the

asset rather than keeping it and making it obsolete or

unserviceable.

Abandoned assets - These are assets held under police or other

legal institutes's custody, or assets the owners of which are

not known or are unable to satisfy some legal requirements to

become the final owner of the assets. This includes assets kept

by customs and police.( MoFED, 2007)

2.3.3.1 Methods of Disposing Unwanted Materials

According to regulation of administration of property, there are

three way of disposing public goods (art 25).These are transfer

to other sister organization, selling to public through auction

and throwing away the item as a junk.(Tesfaye Debela 2000)

CHAPTER THREE

3. Research Design and Methodology

3.1 Research Design

3.1.1 Type of the Study

In order to achieve the objectives of this paper, the researcher

employed descriptive research design. Descriptive research is

thus a type of research that is primarily concerned with

describing the nature or conditions and degree in detail of the

present situation. The emphasis is on description rather than on

judging or interpretation. So, in the view of the researcher it

could be more appropriate to analyze qualitative information.

Since the major purpose of descriptive research is description

of the state of affairs as it exists at present; according to

most writers. Descriptive research method is suitable to reflect

the actual performance of the office in relation to material

management.

3.1.2. The Target Population /Sampling Frame and

Sample Size

The population of the study was 1200 employees and they were

homogeneous. According to Gay L. (2006), said if the population

is homogeneous the researcher can use 10 percent of sample size

from the total population. Based on this, the sample size was

120 employees but because of the budget constraint the

researcher took 88 employees as a sample size. Such as all the

22 heads’ of public sectors and all heads’ of business process

units of the 22 public sectors of the woreda that is 36

employees and 22 experts through questionnaire, and 3

purchasers,3 store keepers, 2 internal auditors by interviews.

3.1.3. Sampling Technique

Non-probability purposive sampling technique was employed for

the respondents from all the heads' of public sectors, all

heads' of business process units of the public sectors of the

woreda , purchasers, store keepers and internal auditors and

also the researcher was taken one expert from each sector by

simple random sampling . The rationale for using these

techniques is the fact that the purpose of the study is to

assess the practice of material management in the organization

and to obtain accurate data, so, it is highly related with

respondents that mentioned above and they are helpful or

essential for the research studies. To meet this purpose and

given the previously mentioned limitations of the study it will

better to employ non- probability purposive sampling techniques

and simple random sampling.

3.2 Sources of Data and Method of Data Collection

The data for this study was collected from both primary and

secondary sources. Primary data was gathered from the selected

sample respondents through questionnaire as well as interview

were employed with purchasers, store keepers and internal

auditors. The second hand information from different reference

documents, library, was the source of secondary data.

The data to be collected from the main respondents through

questionnaires which is consisted of both open as well as closed

ended types of questions and by interviews/structured

interview/and the researcher himself collected data through

direct observation. The medium of communication/language/ with

the target population and other sample respondents is to be in

Tigrigna, thus, these calls for translating the questioners in

to Tigrigna. In addition the questioners are going to dispatch

to respondents and then to be gathered ordinarily by the

researcher himself.

3.3 Method of Data Analysis

Both qualitative and quantitative descriptions were used for

analysis. The data gathered from primary and secondary sources

of information was organized, summarized and analyzed by using

quantitative (table of frequency distribution, simple

percentage, ratio and other relevant statistical methods).

Information collected through interviews, opened questionnaire

and direct observations was analyzed qualitatively.

CHAPTER FOUR

4. Data Presentation, Analysis and Interpretation

4.1 Introduction

To gather data both primary and secondary sources of information

were used. The primary sources include data gathered by

distributing questionnaire to all the heads’ of public sectors

and all heads’ of business process units of the public sectors

of the woreda and one expert from each sector , and interview

conducted with the purchasers, store keepers and internal

auditors. Further personal observation of the purchasing

procedure was done. This chapter deals with discussion and

analysis of the data gathered from selected population through

questionnaire and interviews and from secondary data sources.

The result of the questionnaire, interviews and secondary data

information and the researcher direct observation presented and

discussed as follows in this chapter:

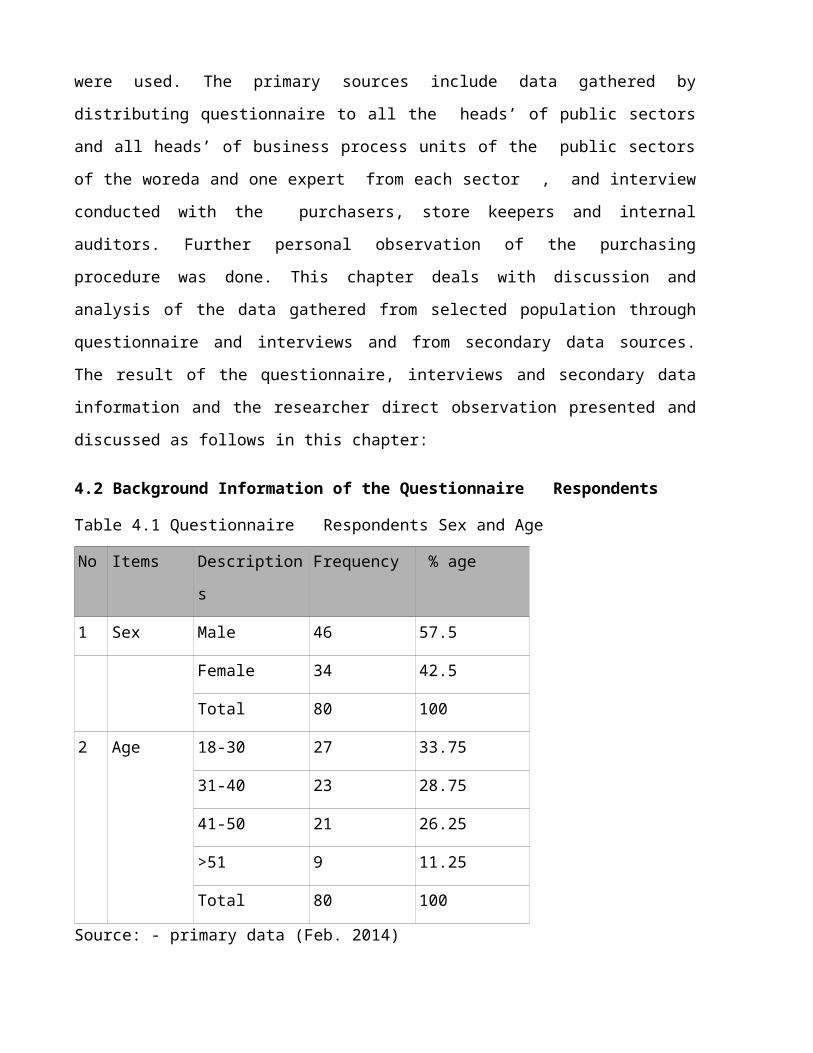

4.2 Background Information of the Questionnaire Respondents

Table 4.1 Questionnaire Respondents Sex and Age

No Items Description

s

Frequency % age

1 Sex Male 46 57.5

Female 34 42.5

Total 80 100

2 Age 18-30 27 33.75

31-40 23 28.75

41-50 21 26.25

>51 9 11.25

Total 80 100

Source: - primary data (Feb. 2014)

According to the above table 4.1, the sex structure of the total

questioner respondents 46 (57.5%) are male and the remaining 34

(42.5%) are female. As per the above table shows the age

satisfaction of the respondents from 18-30 years 27(33.75%), 31-

40 year 23(28.75%),41-50 year 21(26.25%), >51 year 9(11.25%).

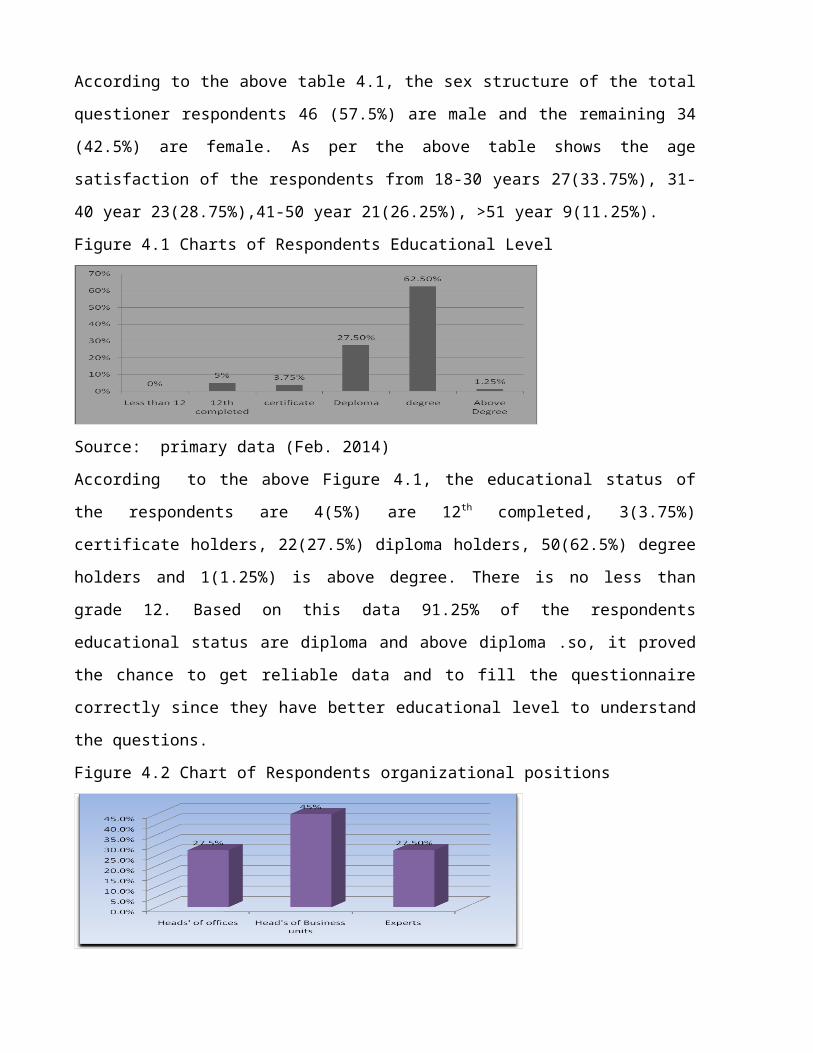

Figure 4.1 Charts of Respondents Educational Level

Source: primary data (Feb. 2014)

According to the above Figure 4.1, the educational status of

the respondents are 4(5%) are 12th completed, 3(3.75%)

certificate holders, 22(27.5%) diploma holders, 50(62.5%) degree

holders and 1(1.25%) is above degree. There is no less than

grade 12. Based on this data 91.25% of the respondents

educational status are diploma and above diploma .so, it proved

the chance to get reliable data and to fill the questionnaire

correctly since they have better educational level to understand

the questions.

Figure 4.2 Chart of Respondents organizational positions

Source: - primary data (Feb. 2014)

As the above Figure 4.2 shows us that respondents job positions

in their respective organization looks like from the total

respondents 22(27.5%) are heads' of the public sector

organization, 36(45%) are heads' of a business process unit and

22(27.5% are experts of the organization.

4.3 Purchasing Management Practice

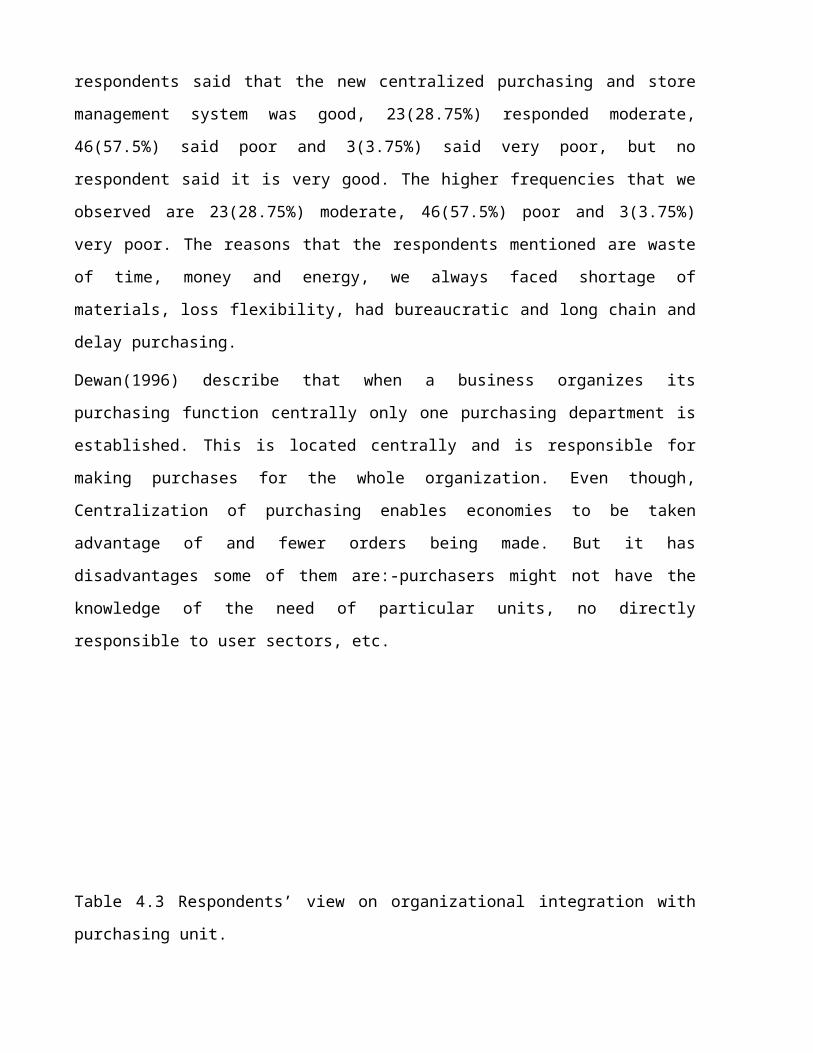

Table 4.2 Respondents’ view on centralized purchasing system

No Items Descripti

ons

Frequenc

y

% age

1 How did you rate the new

centralized purchasing and

store management system?

Very

good

0 0

good 8 10

moderat

e

23 28.75

poor 46 57.5

very

poor

3 3.75

Total 80 100

Source:- primary data (Feb. 2014)

As shown in the above table 4.2, only 8 (10%) of the

respondents said that the new centralized purchasing and store

management system was good, 23(28.75%) responded moderate,

46(57.5%) said poor and 3(3.75%) said very poor, but no

respondent said it is very good. The higher frequencies that we

observed are 23(28.75%) moderate, 46(57.5%) poor and 3(3.75%)

very poor. The reasons that the respondents mentioned are waste

of time, money and energy, we always faced shortage of

materials, loss flexibility, had bureaucratic and long chain and

delay purchasing.

Dewan(1996) describe that when a business organizes its

purchasing function centrally only one purchasing department is

established. This is located centrally and is responsible for

making purchases for the whole organization. Even though,

Centralization of purchasing enables economies to be taken

advantage of and fewer orders being made. But it has

disadvantages some of them are:-purchasers might not have the

knowledge of the need of particular units, no directly

responsible to user sectors, etc.

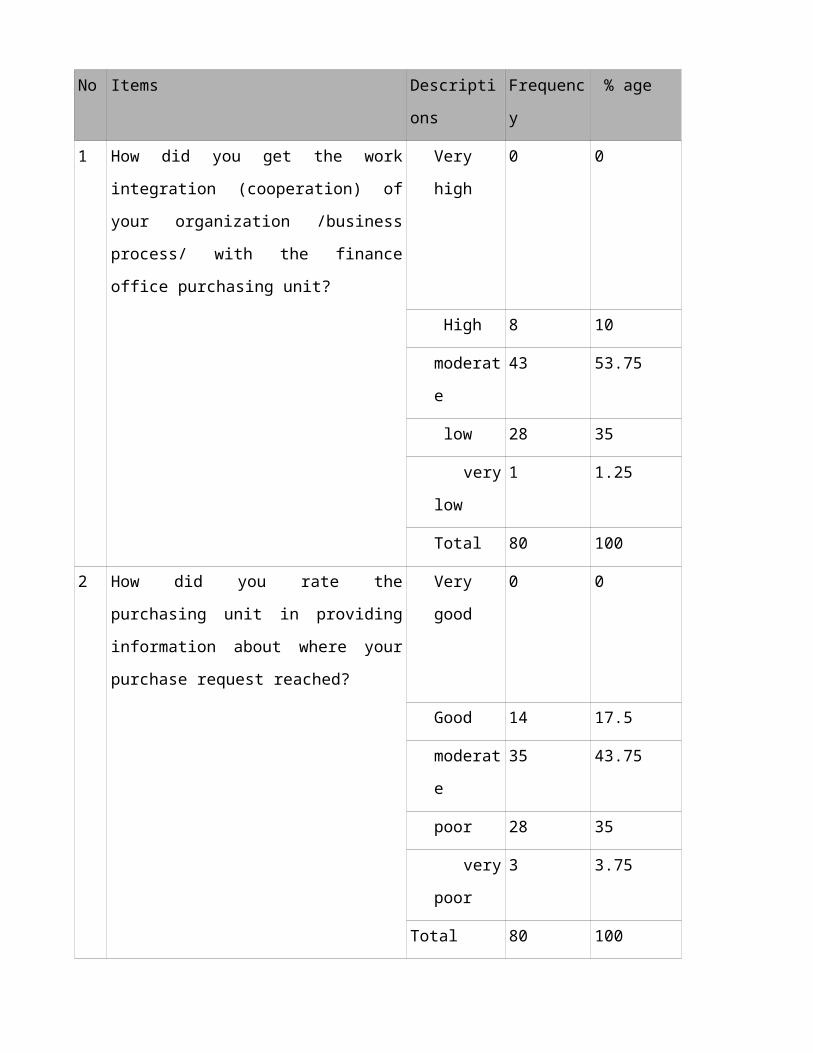

Table 4.3 Respondents’ view on organizational integration with

purchasing unit.

No Items Descripti

ons

Frequenc

y

% age

1 How did you get the work

integration (cooperation) of

your organization /business

process/ with the finance

office purchasing unit?

Very

high

0 0

High 8 10

moderat

e

43 53.75

low 28 35

very

low

1 1.25

Total 80 100

2 How did you rate the

purchasing unit in providing

information about where your

purchase request reached?

Very

good

0 0

Good 14 17.5

moderat

e

35 43.75

poor 28 35

very

poor

3 3.75

Total 80 100

Source:- primary data (Feb. 2014)

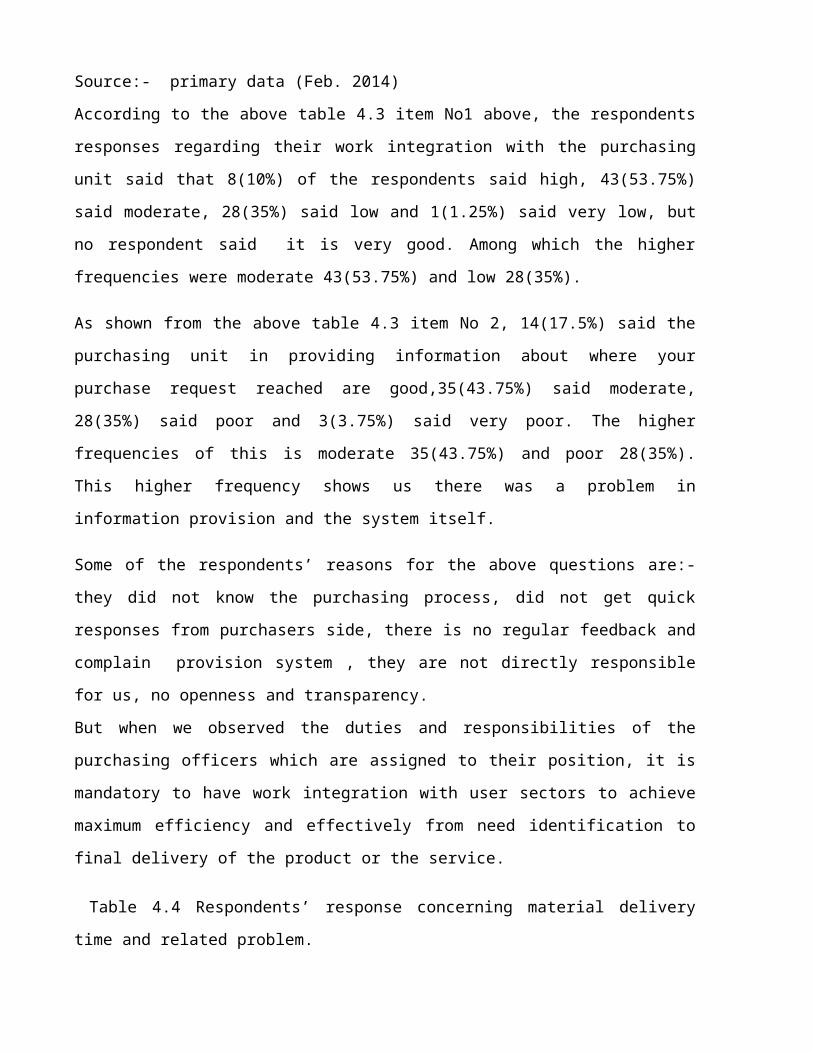

According to the above table 4.3 item No1 above, the respondents

responses regarding their work integration with the purchasing

unit said that 8(10%) of the respondents said high, 43(53.75%)

said moderate, 28(35%) said low and 1(1.25%) said very low, but

no respondent said it is very good. Among which the higher

frequencies were moderate 43(53.75%) and low 28(35%).

As shown from the above table 4.3 item No 2, 14(17.5%) said the

purchasing unit in providing information about where your

purchase request reached are good,35(43.75%) said moderate,

28(35%) said poor and 3(3.75%) said very poor. The higher

frequencies of this is moderate 35(43.75%) and poor 28(35%).

This higher frequency shows us there was a problem in

information provision and the system itself.

Some of the respondents’ reasons for the above questions are:-

they did not know the purchasing process, did not get quick

responses from purchasers side, there is no regular feedback and

complain provision system , they are not directly responsible

for us, no openness and transparency.

But when we observed the duties and responsibilities of the

purchasing officers which are assigned to their position, it is

mandatory to have work integration with user sectors to achieve

maximum efficiency and effectively from need identification to

final delivery of the product or the service.

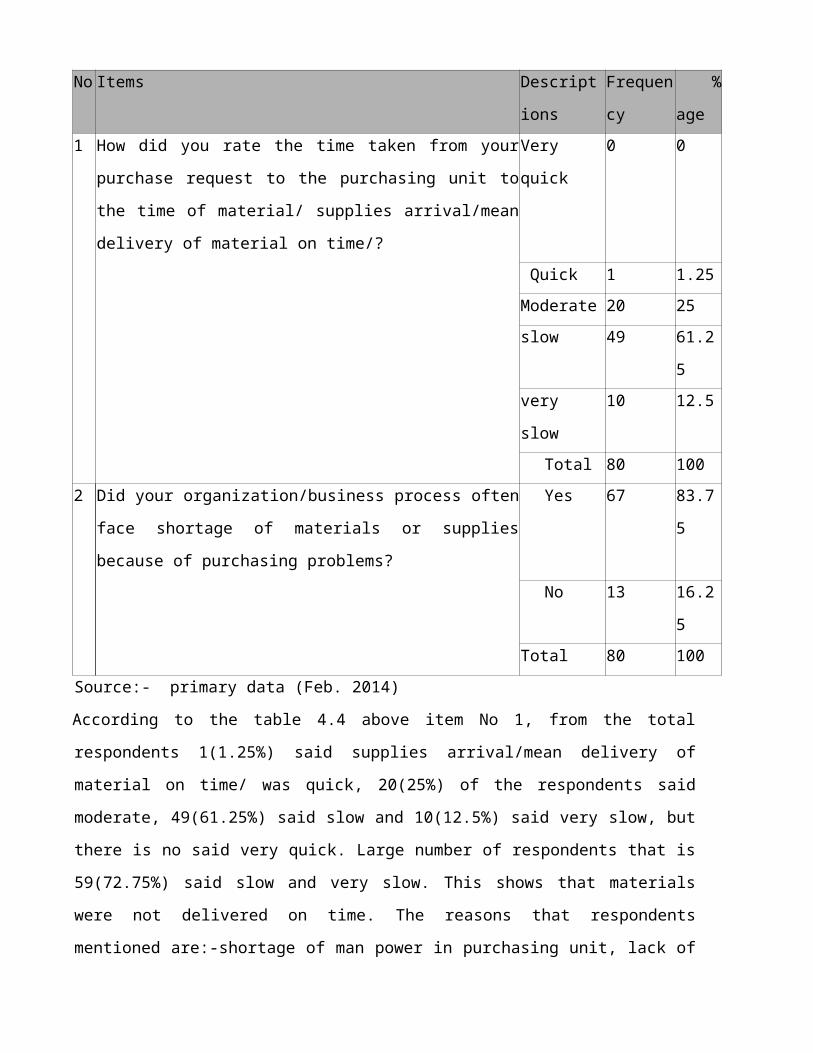

Table 4.4 Respondents’ response concerning material delivery

time and related problem.

No Items Descript

ions

Frequen

cy

%

age1 How did you rate the time taken from your

purchase request to the purchasing unit to

the time of material/ supplies arrival/mean

delivery of material on time/?

Very

quick

0 0

Quick 1 1.25Moderate 20 25slow 49 61.2

5very

slow

10 12.5

Total 80 1002 Did your organization/business process often

face shortage of materials or supplies

because of purchasing problems?

Yes 67 83.7

5

No 13 16.2

5Total 80 100

Source:- primary data (Feb. 2014)

According to the table 4.4 above item No 1, from the total

respondents 1(1.25%) said supplies arrival/mean delivery of

material on time/ was quick, 20(25%) of the respondents said

moderate, 49(61.25%) said slow and 10(12.5%) said very slow, but

there is no said very quick. Large number of respondents that is

59(72.75%) said slow and very slow. This shows that materials

were not delivered on time. The reasons that respondents

mentioned are:-shortage of man power in purchasing unit, lack of

skill and experience of purchasers to meet the purchasing

requirements, the purchasing process is very long, until to

organize all sectors material requirement ...

In addition as shown in the above table 4.4 item No 2, 67(83.75%)

of the respondents said that their organization and/or business

unit often face shortage of materials because of purchasing

problems. But the remaining 13(16.25%) said they didn't face

shortage of materials because of purchasing problem. Large

number of respondents that is 67(83.75%) who said often face

shortage of materials their reason that of purchasing problem as

per the required time.

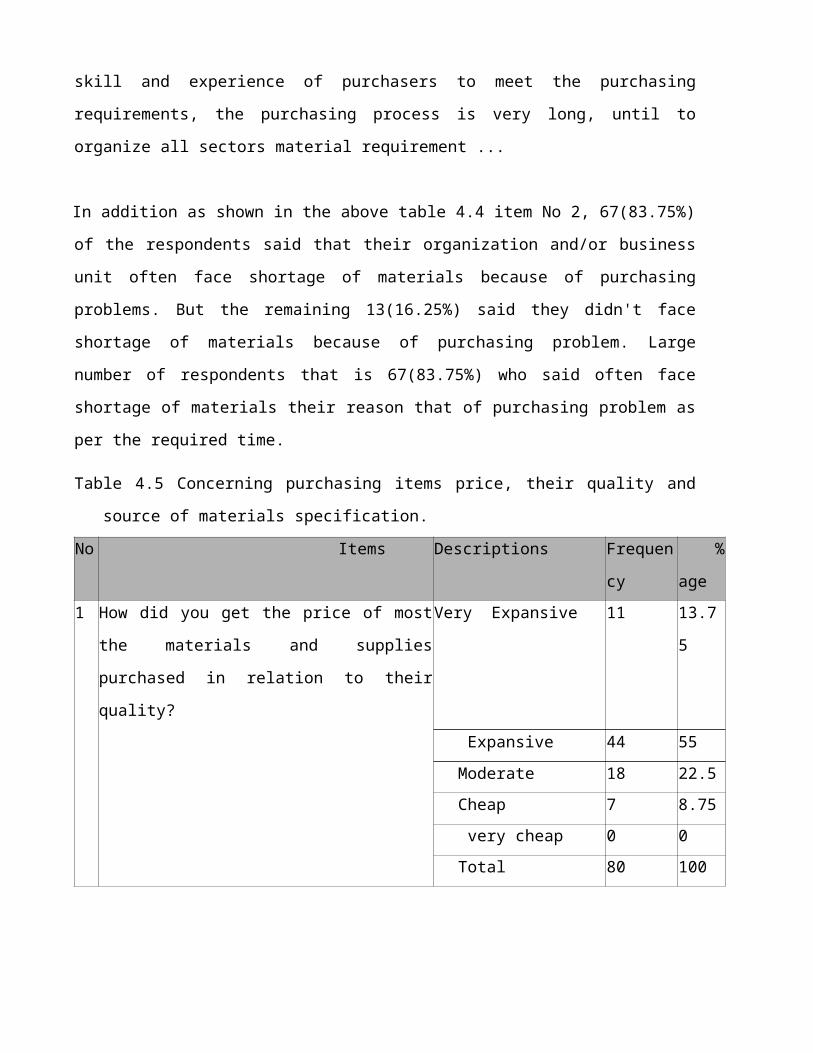

Table 4.5 Concerning purchasing items price, their quality and

source of materials specification.

No Items Descriptions Frequen

cy

%

age1 How did you get the price of most

the materials and supplies

purchased in relation to their

quality?

Very Expansive 11 13.7

5

Expansive 44 55Moderate 18 22.5Cheap 7 8.75 very cheap 0 0Total 80 100

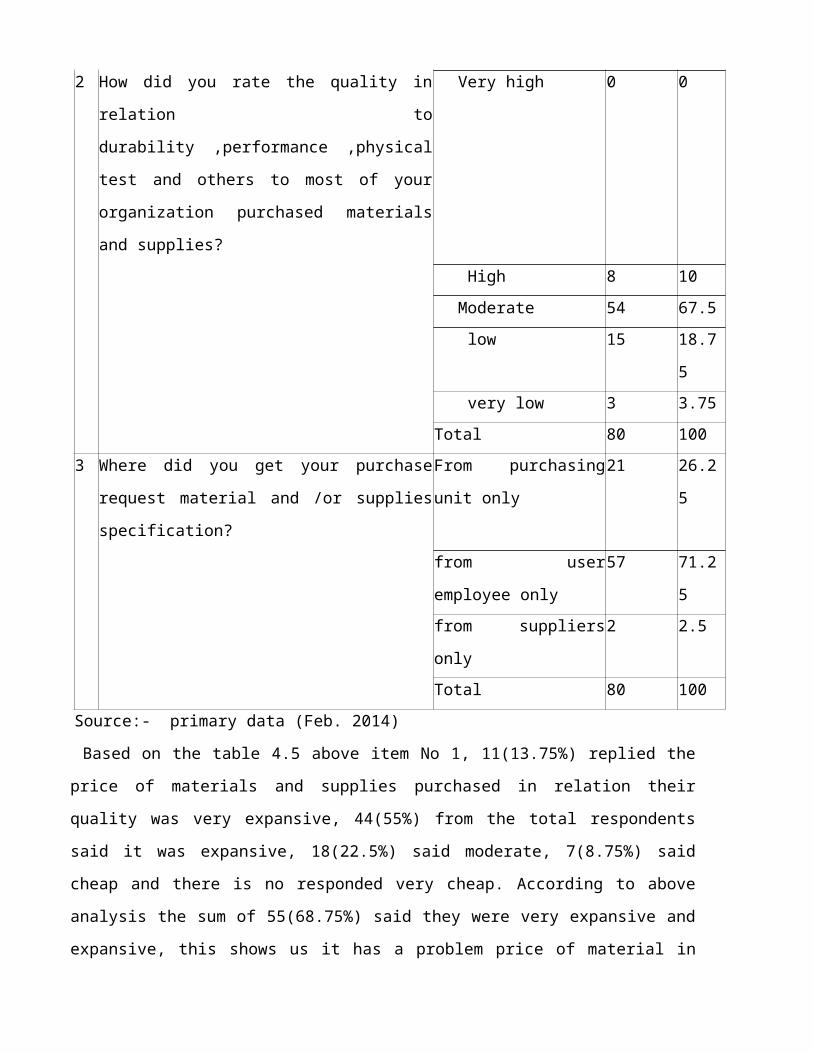

2 How did you rate the quality in

relation to

durability ,performance ,physical

test and others to most of your

organization purchased materials

and supplies?

Very high 0 0

High 8 10Moderate 54 67.5 low 15 18.7

5 very low 3 3.75

Total 80 1003 Where did you get your purchase

request material and /or supplies

specification?

From purchasing

unit only

21 26.2

5

from user

employee only

57 71.2

5from suppliers

only

2 2.5

Total 80 100Source:- primary data (Feb. 2014)

Based on the table 4.5 above item No 1, 11(13.75%) replied the

price of materials and supplies purchased in relation their

quality was very expansive, 44(55%) from the total respondents

said it was expansive, 18(22.5%) said moderate, 7(8.75%) said

cheap and there is no responded very cheap. According to above

analysis the sum of 55(68.75%) said they were very expansive and

expansive, this shows us it has a problem price of material in

relation to their quality.

As observed in table 4.5 above item No 2 , only 8(10%) of the

total respondents said the quality in relation to

durability ,performance and physical test purchased materials

and supplies they were high, 54(67.5%) responded it was moderate,

15(18.75%) said it was low and 3(3.75%) said very low. The higher

frequencies that are sum of 72(90%) said they were moderate, low

and very low. All this shows purchased materials have a problem

regarding to their durability, performance and physical test

(strength, color, size, shape and other related variable).

The above table 4.5 item No 3, 21(26.25%) responded that they

found their purchase request specification from purchasing unit

only, 57(71.25%) said from user employee only and 2(2.5%) said

from suppliers only. This indicates there was no clear source

for specifications. Response to the interview question,

regarding about way of decide the specification of purchasing

materials and supplies, the purchasing units said that the

specification (types, size, color etc) that sent by requesting

organization (each sector). But some time they requested us to

show them specification of purchasing goods. This is the main

problem for the delay of purchase process.

The purchasing processes and methods that the purchaser used was

according to the regional purchasing public properties regulation

125/2003, the methods that they used were different according to

their budget. If the purchase requested amount become less than

60 thousand birr the manual allow to make through Performa, 60-

100 thousand birr through open tender excluded VAT registered,

above 100 thousand birr through media open tender included

VAT registered and less than 5 thousand birr, when there was

urgent need come they directly purchased. But mostly the

purchaser unit used limited tenders. The purchases purchasing

documents which were helped to facilitates purchasing were:-

purchase requisition form, Performa invoice, bid analysis sheet.

Purchase steps which was practice by the purchasing unit were:-

Approved budget for each sectors by council of the woreda,

collect purchase requesting from different sectors, organize them

based on type, finance center, check budget of the organization,

etc.

According to purchasing unit interview, they didn't make

assessment about customers satisfaction and dissatisfaction

(complain) but before receiving it will be checked by technical

expert the materials' quality, then the purchasing would be

undertaken. Regarding to the schedule that they follow, they said

that we have had a schedule which was two in a year purchasing

time frame, such as September and February, but usually we didn’t

follow the schedule according to its time frame because of the

following problem:- all sectors request didn’t come as required,

absence of man power in purchase unit, etc.

Purchasing research is systematic investigation to locate better

or alternative source of supply, to improve the quality and the

price, to value analyses various items, standardize

specifications and sizes, reduces varieties, find substitutes

for items in short supply, etc. It involves collecting and

docketing various information, such as names of suppliers, their

production capacity, annual output, grades and qualities

available, trend of price, etc.(Nair 1990)

The success of any organization activity is largely dependent on

the procurement of materials of right quality, in the right

quantities, from the right source, at right time and at right

price. The right quality is determined by the cost of the

material and the technical characteristics as suited to the

specific requirements. The right quality should be defined

clearly and should be described in terms of specifications. The

quality specifications are controlled before the materials are

issued for the organizational processes. The right quality can

be measured by: Durability, composition, performance, physical

tests, chemical analysis, grade.(Datta,2009)

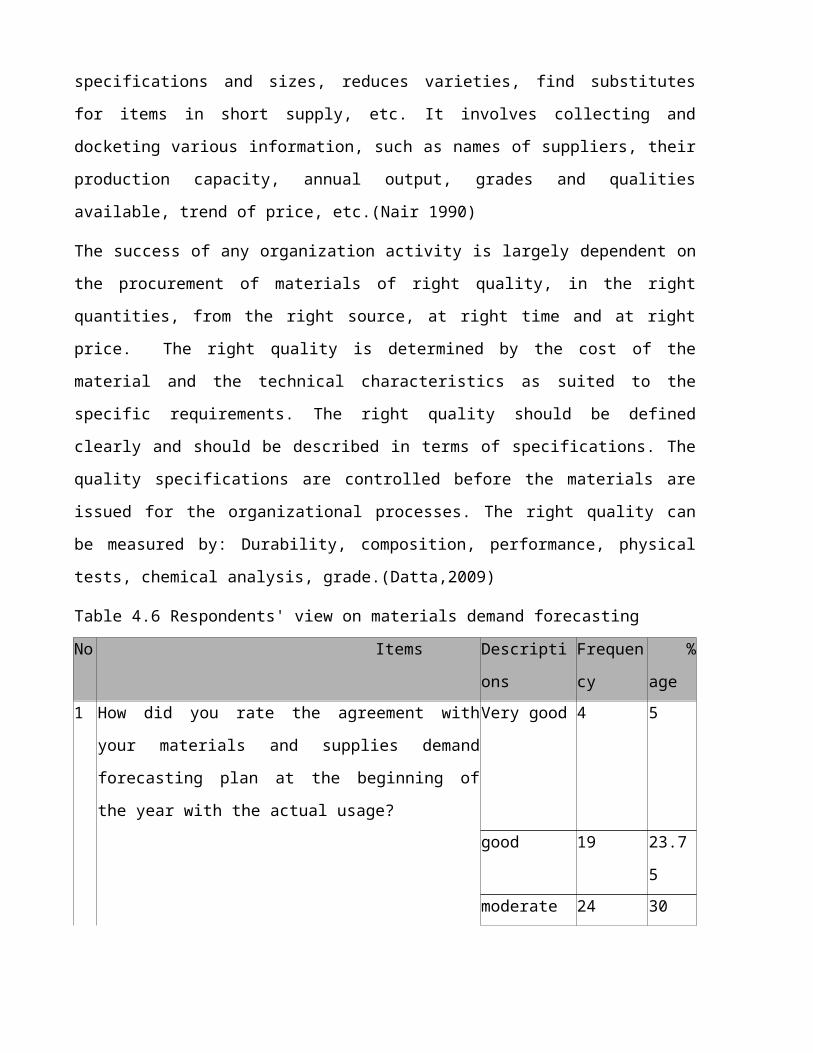

Table 4.6 Respondents' view on materials demand forecasting

No Items Descripti

ons

Frequen

cy

%

age1 How did you rate the agreement with

your materials and supplies demand

forecasting plan at the beginning of

the year with the actual usage?

Very good 4 5

good 19 23.7

5moderate 24 30

poor 29 36.2

5very poor 4 5Total 80 100

Source:- primary data (Feb. 2014)

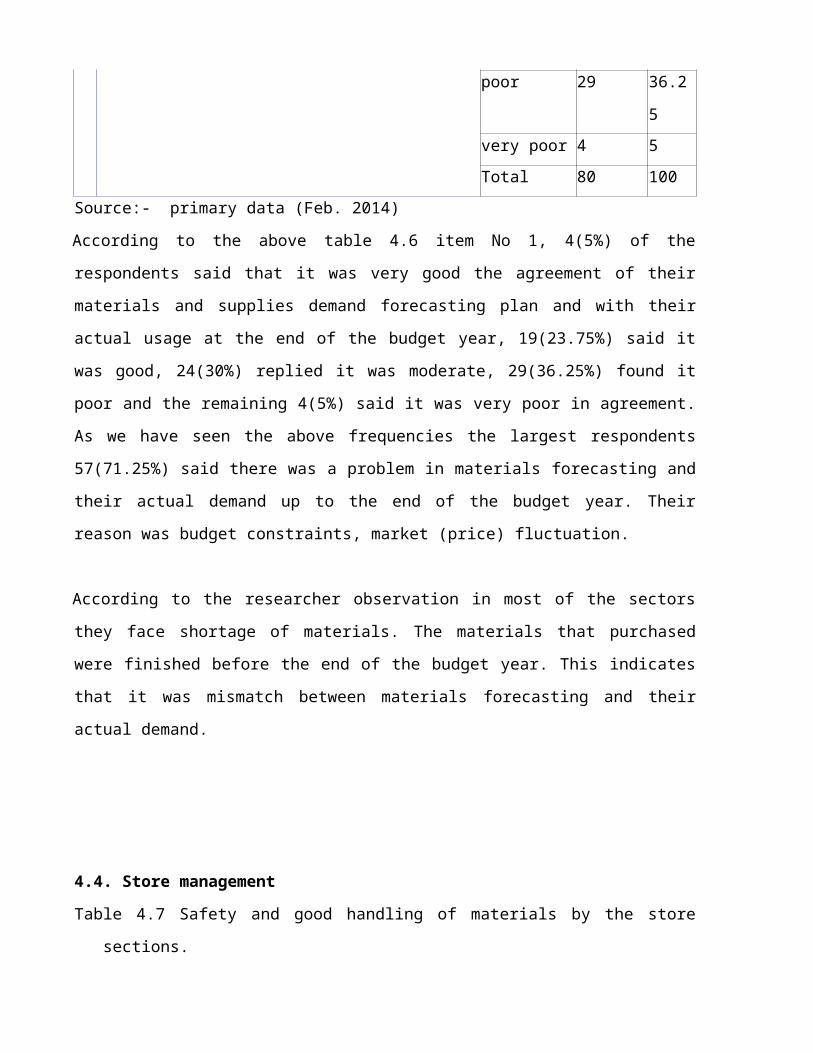

According to the above table 4.6 item No 1, 4(5%) of the

respondents said that it was very good the agreement of their

materials and supplies demand forecasting plan and with their

actual usage at the end of the budget year, 19(23.75%) said it

was good, 24(30%) replied it was moderate, 29(36.25%) found it

poor and the remaining 4(5%) said it was very poor in agreement.

As we have seen the above frequencies the largest respondents

57(71.25%) said there was a problem in materials forecasting and

their actual demand up to the end of the budget year. Their

reason was budget constraints, market (price) fluctuation.

According to the researcher observation in most of the sectors

they face shortage of materials. The materials that purchased

were finished before the end of the budget year. This indicates

that it was mismatch between materials forecasting and their

actual demand.

4.4. Store management

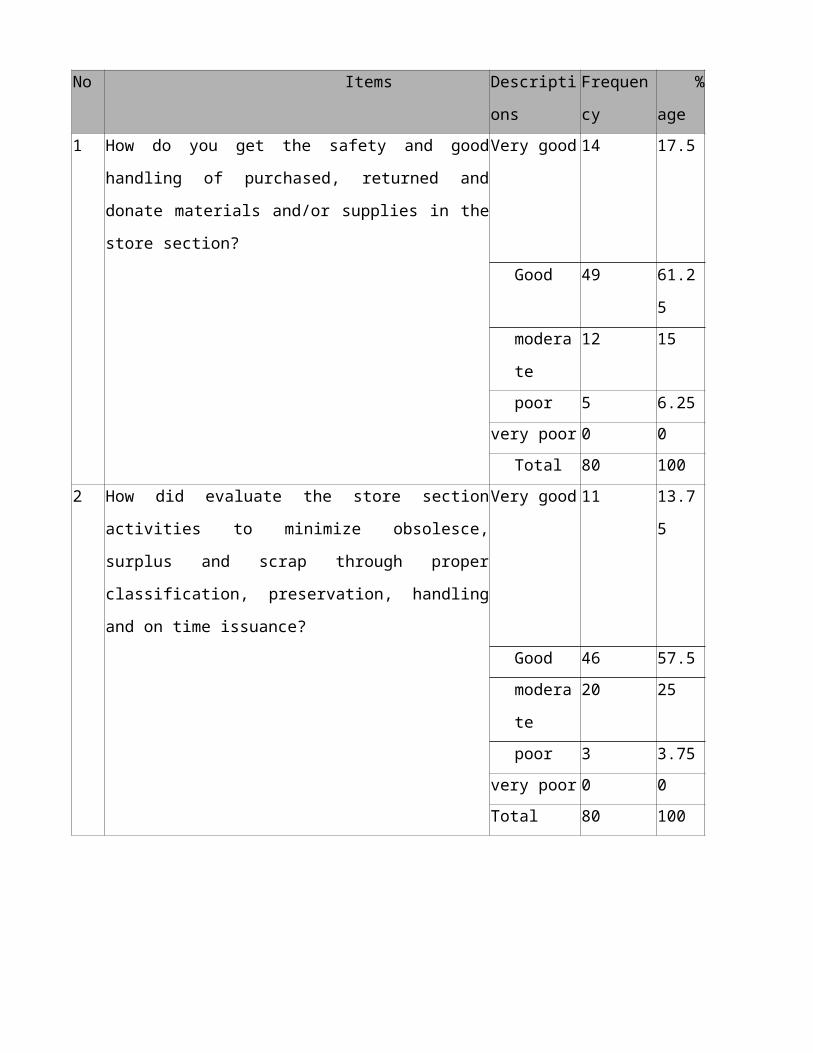

Table 4.7 Safety and good handling of materials by the store

sections.

No Items Descripti

ons

Frequen

cy

%

age1 How do you get the safety and good

handling of purchased, returned and

donate materials and/or supplies in the

store section?

Very good 14 17.5

Good 49 61.2

5modera

te

12 15

poor 5 6.25very poor 0 0

Total 80 1002 How did evaluate the store section

activities to minimize obsolesce,

surplus and scrap through proper

classification, preservation, handling

and on time issuance?

Very good 11 13.7

5

Good 46 57.5modera

te

20 25

poor 3 3.75very poor 0 0Total 80 100

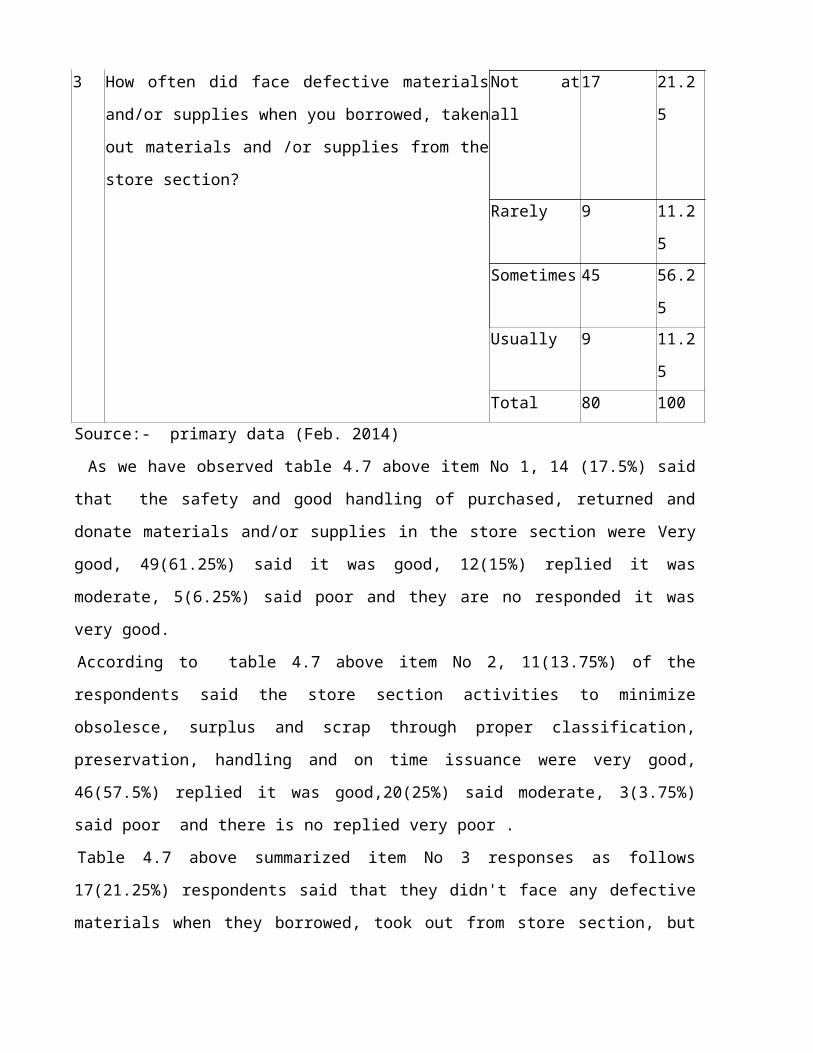

3 How often did face defective materials

and/or supplies when you borrowed, taken

out materials and /or supplies from the

store section?

Not at

all

17 21.2

5

Rarely 9 11.2

5Sometimes 45 56.2

5Usually 9 11.2

5Total 80 100

Source:- primary data (Feb. 2014)

As we have observed table 4.7 above item No 1, 14 (17.5%) said

that the safety and good handling of purchased, returned and

donate materials and/or supplies in the store section were Very

good, 49(61.25%) said it was good, 12(15%) replied it was

moderate, 5(6.25%) said poor and they are no responded it was

very good.

According to table 4.7 above item No 2, 11(13.75%) of the

respondents said the store section activities to minimize

obsolesce, surplus and scrap through proper classification,

preservation, handling and on time issuance were very good,

46(57.5%) replied it was good,20(25%) said moderate, 3(3.75%)

said poor and there is no replied very poor .

Table 4.7 above summarized item No 3 responses as follows

17(21.25%) respondents said that they didn't face any defective

materials when they borrowed, took out from store section, but

others 9(11.25%) said they rarely face defective materials or

supplies, 45(56.25%) replied they sometimes face it and

9(11.25%) said they usually face defective items in the store

section. A sum of 64(78.75%) respondents face any defective

materials when they borrowed, took out from store sections.

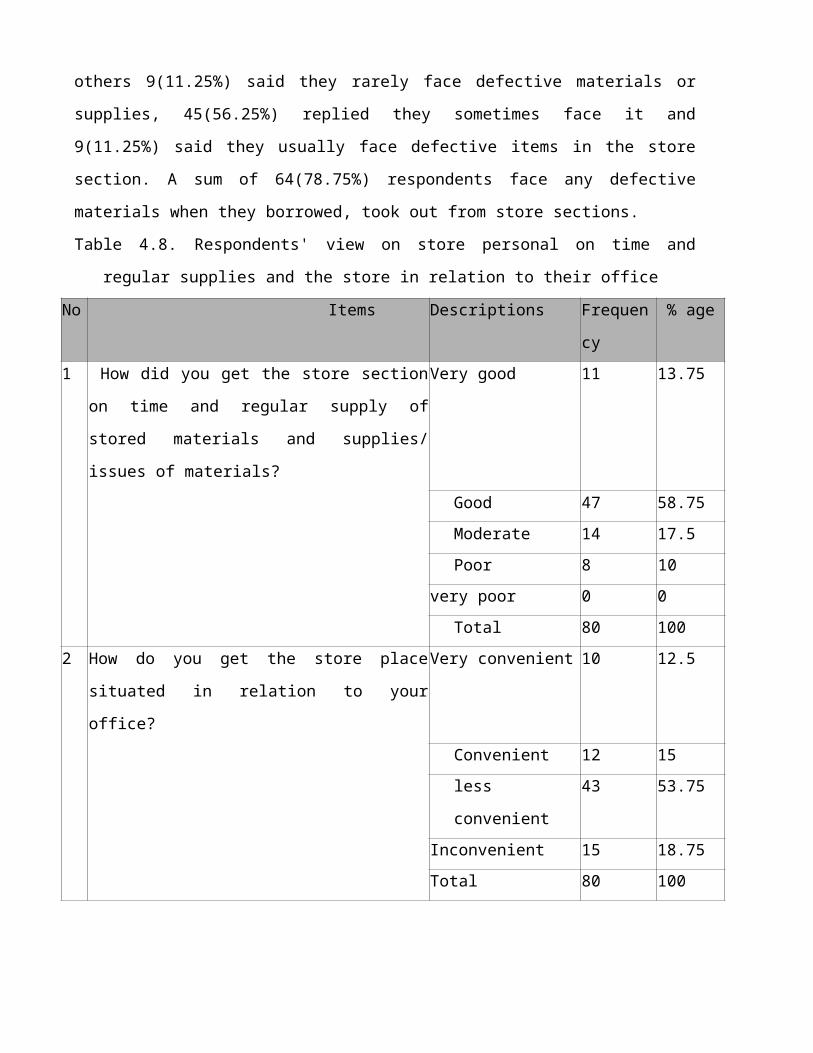

Table 4.8. Respondents' view on store personal on time and

regular supplies and the store in relation to their office

No Items Descriptions Frequen

cy

% age

1 How did you get the store section

on time and regular supply of

stored materials and supplies/

issues of materials?

Very good 11 13.75

Good 47 58.75Moderate 14 17.5Poor 8 10

very poor 0 0Total 80 100

2 How do you get the store place

situated in relation to your

office?

Very convenient 10 12.5

Convenient 12 15less

convenient

43 53.75

Inconvenient 15 18.75Total 80 100

3 Do you get a record kept about the

details of item available in the

store up to date?

Yes 61 76.25

No 19 23.75Total 80 100

Source:- primary data (Feb. 2014)

Table 4.8 above shows that for item No 1 from the total

respondents 11(13.75%) found that the store section on time and

regular supply of stored materials and supplies were very good,

47(58.75%) said it was good, 14(17.5%) said moderate, 8(10%) said

that it was poor but there is no respond it was very poor.

Based on the above table 4.8 item No 2, 10(12.5%) of the total

respondents that the store place situated in relation to your

office has been Very convenient, 12(15%) responded Convenient,

43(53.75%) said it was less convenient and the remaining

15(18.75%) said it was Inconvenient. From the total respondents

who said less convenient and Inconvenient have been a total of

58(72.25%) respondents and their reasons were their store has

been found too far from the office location create a problem to

get items very quickly and other said there is no store in some

office.

According to the store management response and the researcher

observation in response to interview question “How do you see the

location and the size of the store(s) that you work?” the stores

that have in the woreda was not centralized for each sector as

purchase. The materials that have been purchased by the central,

it distributed immediately for each sectors. As the researcher

observed, without some sectors that which has huge materials/

Agriculture office, finance office, education office …../. In the

most sectors didn’t have storehouse and store keeper. Materials

in those sectors were stored in the office and receiving and

issuing materials by one expert as additional work. So, those

materials vulnerable for theft and fraud.

According to table 4.8 above item No 3, 61(76.25%) said that they

got a record kept about the details of item available in the

store up to date. The remaining 19(23.75%) of the respondents did

not find that.

According to the store personals in response to the interview

question and researcher observation :- types of store control

forms that they used and How to keep them, store control systems

and procedures that they followed in receiving, maintaining and

issuing materials and supplies. They said that, in relation to

the types of inventory control forms that have been used were:

They used receiving note model 19 for receiving purchasing and

donated items. Receiving has been done when purchasers or any

donor brought the items with the necessary receipt voucher of the

supplier which describe type, quantity and value of each items,

then recording the receipt information in three copies and

checking with the item received and proven one copy to the one

carried in the item. They used issuance model 22, if requesting

form /model 20/ was filled by owner sector with name of employee,

described item type, quantity and signed by respected official

and then by filling all the information found in model 20 to the

model 22 with three copies and issued the item with one copy. In

addition to control stock/consumable materials and fixed assets,

they use STOCK CARD which contains cost and BIN CARD to control

stock materials. Both receiving and issuing model have been

prepared by each sector. But, there was not a practice of record

keeping through model 70A-to record all items daily transaction

and model 70B- to record and follow up all non-consumable items.

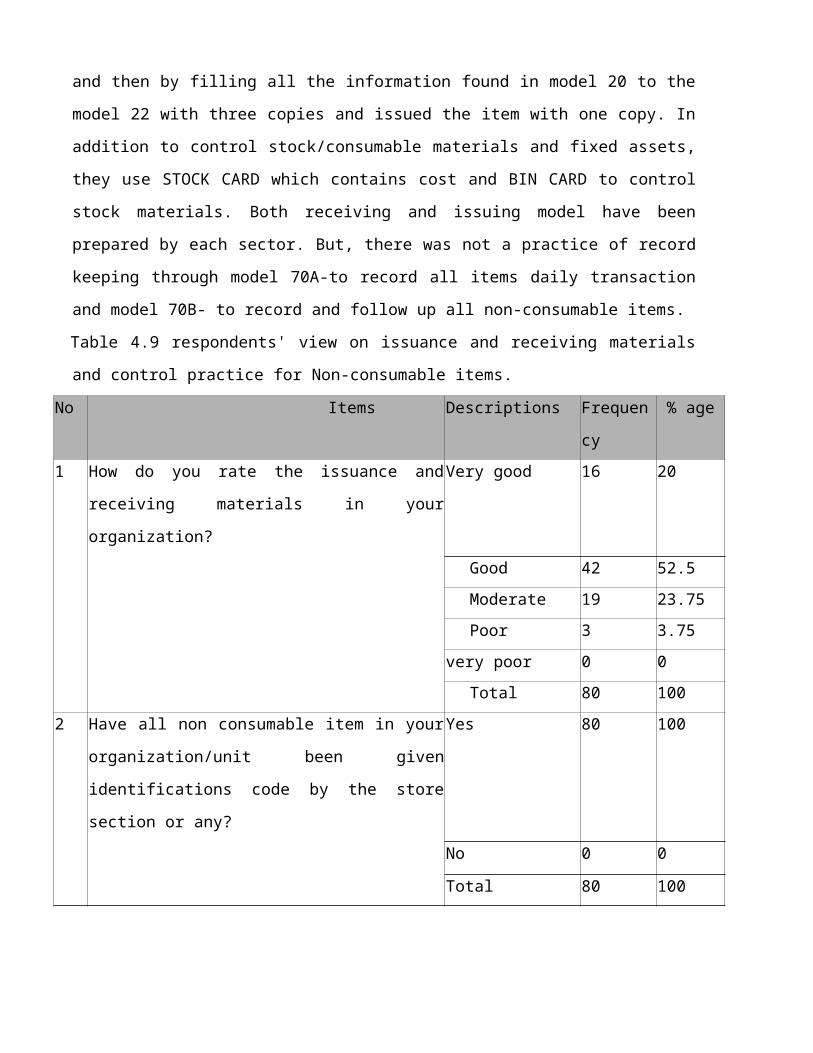

Table 4.9 respondents' view on issuance and receiving materials

and control practice for Non-consumable items.

No Items Descriptions Frequen

cy

% age

1 How do you rate the issuance and

receiving materials in your

organization?

Very good 16 20

Good 42 52.5Moderate 19 23.75Poor 3 3.75

very poor 0 0Total 80 100

2 Have all non consumable item in your

organization/unit been given

identifications code by the store

section or any?

Yes 80 100

No 0 0

Total 80 100

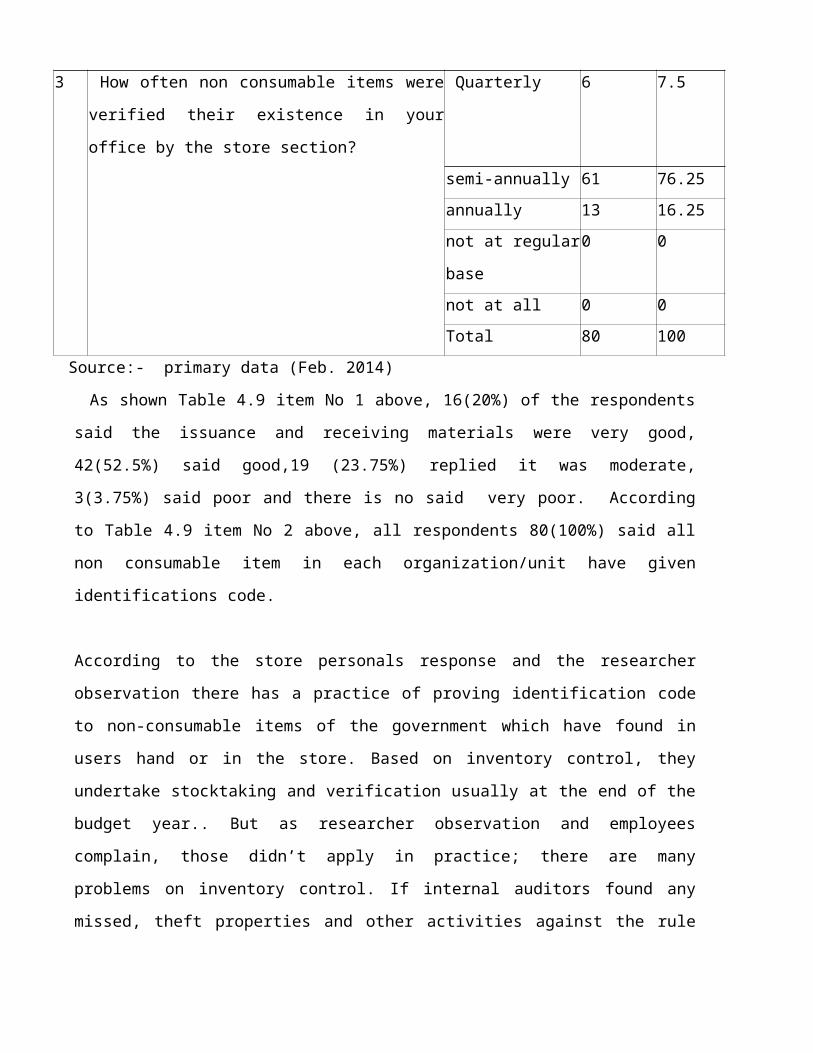

3 How often non consumable items were

verified their existence in your

office by the store section?

Quarterly 6 7.5

semi-annually 61 76.25annually 13 16.25not at regular

base

0 0

not at all 0 0Total 80 100

Source:- primary data (Feb. 2014)

As shown Table 4.9 item No 1 above, 16(20%) of the respondents

said the issuance and receiving materials were very good,

42(52.5%) said good,19 (23.75%) replied it was moderate,

3(3.75%) said poor and there is no said very poor. According

to Table 4.9 item No 2 above, all respondents 80(100%) said all

non consumable item in each organization/unit have given

identifications code.

According to the store personals response and the researcher

observation there has a practice of proving identification code

to non-consumable items of the government which have found in

users hand or in the store. Based on inventory control, they

undertake stocktaking and verification usually at the end of the

budget year.. But as researcher observation and employees

complain, those didn’t apply in practice; there are many

problems on inventory control. If internal auditors found any

missed, theft properties and other activities against the rule

and regulation of public property administration they wrote a

report to the head of the office to make appropriate decision

and follow the implementation of the decision.

The interview question about cross checking each and every

purchasing activity as per the rule and regulation, they said

that mostly we have been focused on after purchase was

undertaken. But their assigned duties show to check before and

after every purchase; this shows no practice of pr-checking of

the purchasing activities.

The above table 4.9 also vividly shows that for the item No 3

about frequencies of non consumable items(fixed assets)

verification their existence,6(7,5%) said that it was undertaken

in a Quarterly base, 61(76.25%) said in semi-annually base and

13(16.25%)said in annually base. This tells as there is no

regular time to verification non consumable items (fixed assets)

their existence in each sector. For the interview question, “How

often do you verify the existence of non consumable items in the

user departments and stores?” the store personals said that we

have been verify the existence of non consumable items in the

user departments and stores in special case /when in any sector

has a theft rumor/ but there was not undertaken in regular base

or at fixed time schedule.

Stock taking is the complete process of physically counting,

measuring or weighing the entire range of items in the stores

and recording the results in a systematic manner. The purposes

stock taking are to verify the accuracy of stock records, to

support the value of stock shown in the stores documents by

physical verification, to disclose the possibility of fraud,

theft or loss and to reveal any weaknesses in the system for the

custody and control of stock. Therefore, public sectors should

be verified(stoke taking) public properties at least once a

year.(MoFED ,2010)

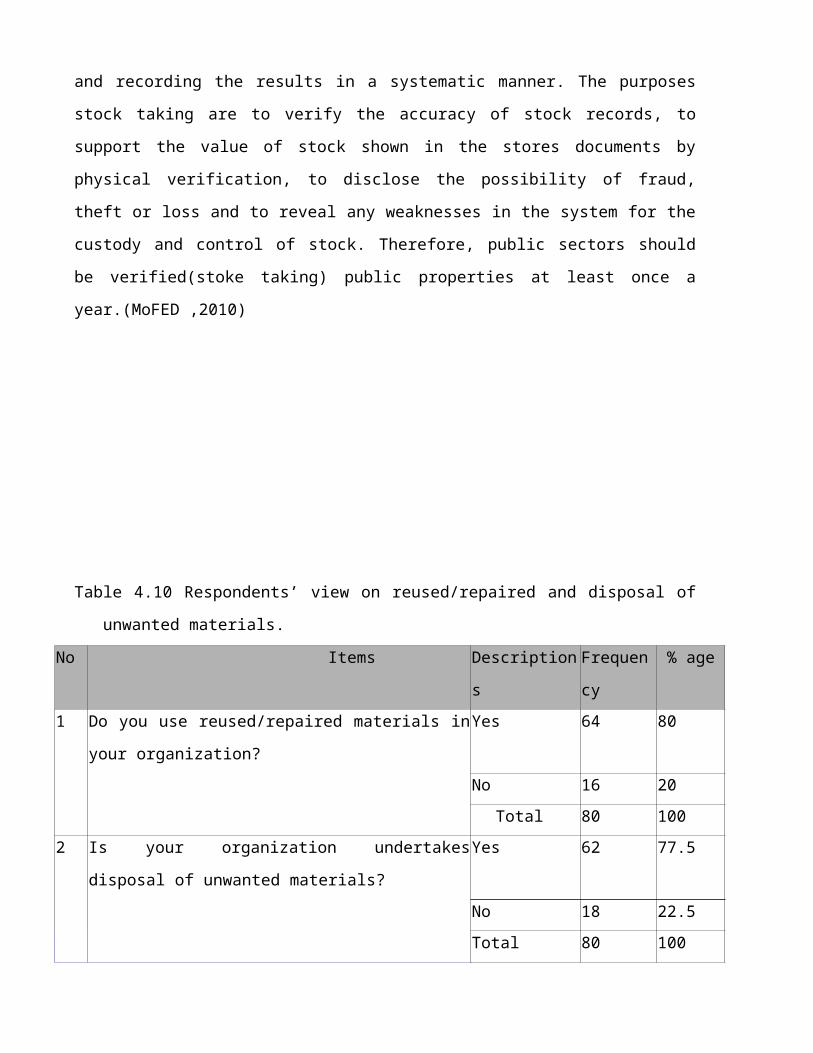

Table 4.10 Respondents’ view on reused/repaired and disposal of

unwanted materials.

No Items Description

s

Frequen

cy

% age

1 Do you use reused/repaired materials in

your organization?

Yes 64 80

No 16 20Total 80 100

2 Is your organization undertakes

disposal of unwanted materials?

Yes 62 77.5

No 18 22.5Total 80 100

Source:- primary data (Feb. 2014)

According to the above table 4.10 item No 1, 64(80%) of the

respondents said they were used the repaired materials in their

organization and the remaining 16(20%) said they didn't repaired

materials.

Based on the above table 4.10 item No 2, 62(77.5%) said that

they were undertakes disposal of unwanted materials in their

organizations and the remaining 18(22.5%) respondents said they

didn't undertakes disposal of unwanted materials in their

organizations. According to internal auditors' response to the

interview question, about undertaking disposal unwanted

materials. They said that, each sectors if they want to dispose

unwanted materials they send the list of materials that

disposing to finance office. Then the disposal committees have

checked the unwanted materials and dispose through the three way

of disposing public goods such as transfer to other sister

organization, selling to public through auction and throwing

away the item as a junk. Mostly they were used selling to public

through auction.

According GOFAMM in Ethiopia, there are four commonly known

reasons to start the fixed assets disposal process. These are

when the asset is Unserviceable, obsolete, surplus and

abandoned. Hence, according to regulation of administration of

property, there are three way of disposing public goods (art

25).These are transfer to other sister organization, selling to

public through auction and throwing away the item as a junk.

(Tesfaye Debela 2000)

CHAPTER FIVE

5. Summary of Major Findings, Conclusions and

Recommendations

5.1 Summary of Major Findings

Centralized purchasing is commonly practiced within the

woreda. As the document and purchasers response shows that 22

sector have been organized in a centralized way which reduces

the work effort duplication. Purchasing activities have been