21 September 2008 Equity Research Mobily is the brand name of the Saudi operations of Etihad Etisalat of the UAE. It is the second mobile phone operator in the Kingdom. Mobily offers a suite of wireless communication products and services and is developing a national fiber optic network. We believe that at its current share price Mobily is undervalued. Investment positives: • The influence of its largest shareholder, successful region telecoms operator, Etihad Etisalat. • Synergies in sales and services and potentially lucrative new revenue streams from recent and ongoing acquisitions. • A solid Kingdom-wide distribution network via franchises, corporate outlets and dealers. • Sophisticated marketing, which has allowed Mobily to build a strong brand name after only three years of operations. • The successful targeting of diverse groups within the Saudi market. • Operating in a sector of the telecoms industry that has strong growth prospects. Investment negatives: • Competition from a third mobile operator, Zain, which recently started operations, will challenge financial performance. • Dominant in the prepaid market, which tends to be more unstable than the postpaid market. • The balance sheet is highly leverage as a result of the a very high level of debt. • The company operates with tight liquidity and a heavy debt burden, typical for a company that requires a large amount of spending in the early phase of operations. 1 Investment summary 12-month target price SR78 Current price SR45 Sell Consider selling Hold Consider buying Buy SR82-73 SR88-83 >SR88 SR72-67 <SR67 Key ratios Price-earnings ratio (P/E) 14.03 Price-book ratio (P/B) 3.48 Return on equity (%) 23.7 Return on total assets (%) 7.5 Gross margin (%) 55.1 Operating margin (%) 22.7 Quick ratio 0.36 Market risk (beta) 1.02 Earnings yield (%) 7.12 Company risk (standard deviation) 0.32 Share price Share details Market cap (SR million) 22,200 Shares outstanding (million) 500 Free float (million) 299 Earnings per share (SR) 3.2 Dividends per share (SR) 0 Book value per share (SR) 12.87 52-week high (SR) 76.75 52-week low (SR) 38.2 Etihad Etisalat (Mobily): Well connected 30 35 40 45 50 55 60 65 70 75 80 06/01/2007 10/02/2007 17/03/2007 21/04/2007 26/05/2007 30/06/2007 04/08/2007 08/09/2007 21/10/2007 25/11/2007 05/01/2008 09/02/2008 15/03/2008 19/04/2008 24/05/2008 28/06/2008 02/08/2008 06/09/2008 BUY Target price*: SR78 Current price: SR45 Fair value: SR69 *12-month target

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

21 September 2008 Equity Research

Mobily is the brand name of the Saudi operations of Etihad Etisalat of the UAE. It is the second mobile phone operator in the Kingdom. Mobily offers a suite of wireless communication products and services and is developing a national fiber optic network. We believe that at its current share price Mobily is undervalued. Investment positives:

• The influence of its largest shareholder, successful region telecoms operator, Etihad Etisalat.

• Synergies in sales and services and potentially lucrative new revenue streams from recent and ongoing acquisitions.

• A solid Kingdom-wide distribution network via franchises, corporate outlets and dealers.

• Sophisticated marketing, which has allowed Mobily to build a strong brand name after only three years of operations.

• The successful targeting of diverse groups within the Saudi market.

• Operating in a sector of the telecoms industry that has strong growth prospects.

Investment negatives:

• Competition from a third mobile operator, Zain, which recently started operations, will challenge financial performance.

• Dominant in the prepaid market, which tends to be more unstable than the postpaid market.

• The balance sheet is highly leverage as a result of the a very high level of debt.

• The company operates with tight liquidity and a heavy debt burden, typical for a company that requires a large amount of spending in the early phase of operations.

1

Investment summary

12-month target price

SR78 Current price

SR45

Sell Consider selling

Hold Consider buying

Buy

SR82-73 SR88-83 >SR88 SR72-67 <SR67

Key ratios

Price-earnings ratio (P/E) 14.03

Price-book ratio (P/B) 3.48

Return on equity (%) 23.7

Return on total assets (%) 7.5

Gross margin (%) 55.1

Operating margin (%) 22.7

Quick ratio 0.36

Market risk (beta) 1.02

Earnings yield (%) 7.12

Company risk (standard deviation) 0.32

Share price

Share details

Market cap (SR million) 22,200 Shares outstanding (million) 500 Free float (million) 299 Earnings per share (SR) 3.2

Dividends per share (SR) 0 Book value per share (SR) 12.87

52-week high (SR) 76.75 52-week low (SR) 38.2

Etihad Etisalat (Mobily): Well connected

30

35

40

45

50

55

60

65

70

75

80

06/01/2007

10/02/2007

17/03/2007

21/04/2007

26/05/2007

30/06/2007

04/08/2007

08/09/2007

21/10/2007

25/11/2007

05/01/2008

09/02/2008

15/03/2008

19/04/2008

24/05/2008

28/06/2008

02/08/2008

06/09/2008

BUY Target price*: SR78 Current price: SR45 Fair value: SR69 *12-month target

Over the last decade the Saudi telecommunications sector has been transformed from a state monopoly into an open, competitive industry. Liberalization began in 1998, when the responsibility for providing telecom services was shifted from the Ministry of Post, Telegraphs, and Telephones to a new company, Saudi Telecommunications Company (STC). This was done to modernize and improve efficiency in a sector that had struggled to meet the demands of its customers. To expedite development of the necessary infrastructure, Lucent Technologies won a $4 billion contract to set up a fixed line network throughout Saudi Arabia and a $700 million contract to develop a mobile phone network. In 2001 the government passed the Telecom Act, which provided the foundations for the legal structure of the industry and led to the establishment of an independent regulator, the Communication and Information Technology Commission (CITC). STC’s monopoly on mobile services was broken in 2004, when Etihad Etisalat of the UAE won the license to become the Kingdom’s second mobile operator. Etihad Etisalat adopted the name Mobily for its Saudi operations and offered a 20 percent stake on the Saudi stock market to become the second listed Saudi telecoms company after STC, which floated a 20 percent stake the previous year. Accession to the World Trade Organization in 2005 formalized the government’s commitment to liberalize the entire telecoms sector and this occurred when STC’s monopoly on fixed lines was ended in 2007. New fixed line licenses were awarded to consortia headed by Bahrain Telecommunications, Hong Kong’s PCCW and Verizon of the US. The new fixed line operators are expected to start operations early next year. Last year the auction for a third mobile license was won by Zain of Kuwait. Zain was listed on the stock market in March 2008 and formally commenced operations on August 26 this year. Strong competition has stimulated the introduction of the latest technology, greatly improved the range of services available and pushed prices lower. Telecoms timeline

2

21 September 2008

Industry analysis

Zain begins operations

Third mobile license issued

and national frequency plan

established

Fixed line licences issued

to: Optical Communications

(Verizon of USA),

Mutakamilah (PCCW of

Hong Kong), and

Atheeb (Batelco of Bahrain).

3G Services launched,

Internet restructring, E-

transaction Act, E-crimes

Act & Cert established

WTO membership and

Mobily launches service

E-transaction

Program"Yasser", EasyNet,

Home PC Initiative

Mobily receives license

Liberalization of data and

mobile services

ICT Ministry established, IT

added to CITC, liberalization

of VSAT

IPO of STC (20%)

Telecom bylaw

Telecom Act and CITC

formedLiberalization of ISP sector

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

The current position Fixed lines: Growth in the number of fixed lines in the Kingdom averaged 4 percent over the last six years and at the end of 2007 there were 4 million fixed telephone lines, 73 percent of which were in residences. This gives Saudi Arabia the second largest number of fixed lines in the Middle East, after Egypt. Total teledensity is around 16.3 percent (163 telephones lines for every 1,000 inhabitants). This is above the average for the Arab countries and the developing world, but at the low end of the GCC states. The introduction of competition in the fixed line sector should lift teledensity over the years to come. Mobile: The number of mobile subscribers in the Kingdom has surged from just 2.5 million in 2001 to 28.4 million at the end of 2007. Last year alone there were 8.7 million new subscribers. Mobile penetration stood at 116 percent at the end of last year, below the rates in most other GCC countries, but well above the average elsewhere in the region (note that data in the table below is for 2006). Research from CITC indicates that prepaid subscribers (where users purchase credit in advance) constitute the majority of subscribers (83 percent). Internet: At the end of 2007, there were 6.4 million internet users in the Kingdom, the largest number of users anywhere in the Arab world. Internet penetration was 26 percent. The number of internet users has grown by around 36 percent per year since 2001. Broadband subscribers surged from 24,000 in 2004 to over 623,000 at the end of 2007 and were up nearly ten-fold over the last two years. Growth in internet use, particularly via broadband, has been constrained by the lack of service providers. Liberalization of fixed line services should improve the availability of this technology. Regional telecoms indicators (2006)

Source: Jadwa, CITC

0

5

10

15

20

25

30

2001 2002 2003 2004 2005 2006 2007

(millions)

Post-paid Pre-paid

Fixed line penetration

Mobile phone subscribers

3

21 September 2008

Fixed

Teledensity

Fixed Lines

(Million)

Mobile

Penetration

Mobile Subscribers

(Million)

Internet

Penetration

Internet Users

(Million)

Algeria 8% 3.0 61% 21.0 10% 3.5

Bahrain 25% 0.2 115% 0.8 23% 0.2

Egypt 15% 11.0 28% 17.0 5% 3.8

Jordan 11% 0.6 80% 4.5 10% 0.7

KSA 18% 3.8 82% 19.6 20% 4.7

Kuwait 19% 0.5 100% 1.8 25% 0.8

Lebanon 18% 0.6 29% 1.0 14% 0.8

Oman 16% 0.4 70% 1.2 9% 0.2

Qatar 28% 0.3 100% 0.2 14% 0.1

Syria 19% 3.2 27% 3.5 10% 1.7

UAE 30% 1.5 126% 5.0 40% 1.7

Yemen 5% 1.0 12% 2.0 5% 0.9

Averages

Arab World 11% 35% 7% Developed countries 52% 82% 60% Developing countries 15% 30% 10%

World 20% 40% 16%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2001 2002 2003 2004 2005 2006 2007

(millions)

0

10

20

30

40

50

60

70

80

(percent)

Business lines Residential lines Households teledensity (RHS) Population teledensity (RHS)

0

1

2

3

4

5

6

7

2001 2002 2003 2004 2005 2006 2007

(million)

Internet users

Source: Jadwa, Mobily, STC, CITC

Source: Jadwa, Mobily, STC, CITC

Source: Jadwa, Mobily, STC, CITC

Growth drivers The following are the main drivers of growth in the telecoms sector: • Demographics: Saudi Arabia has a young and fast-growing

population. Around 32 percent are between the ages of 15 and 29, the age range that is a major target for all the telecom operators. The continued influx of expatriate workers (over 1 million new work visas were issued last year) will add to the demand for telecoms.

• Hardware costs: Technological innovation and competition within the retail sector is likely to continue to reduce the cost of mobile handsets and computers and drive further subscriber growth. The fall in the cost of computers is greatly increasing demand for internet connectivity and broadband services.

• Foreign competition: New foreign telecoms operators in the Kingdom will stimulate greater competition, lower prices and introduce new services and technologies, stimulating demand for telecoms.

• Government policy: The government is promoting greater use of the internet. Schools and colleges are being provided with internet access and a government program is in place that allows individuals to purchase computers at low prices. In addition, the economic cities under development are being fitted with the most up to date technology and Riyadh governorate plans to cover the whole city with wireless internet access.

• Availability of connectivity technology: Increased availability

of 3G technology (which provides wireless internet via several devices) gives access to the internet to customers where fixed lines (and therefore dial-up internet connections) are unavailable. It also allows the convenience of mobile access to the internet.

• Greater availability of Arabic language internet content: The

growing amount of Arabic language software and websites will increase the demand for internet access.

Revenues Telecom revenues have leapt from SR20 billion in 2001 to SR43 billion in 2007 as the number of subscribers has surged. The mobile business accounted for approximately 80 percent of telecom revenue in 2007, compared to 40 percent in 2001. The following factors explain why revenues from mobile services have outpaced those from fixed lines: • Convenience of immediate access and having a roaming

network across the region. • The inclusion of variety of attractive features such as cameras

and internet access. • Cheaper local and international call fees than from fixed lines. • Quicker and easier to set up than a fixed line. • Improved coverage and reliability of the mobile network owing to

more mobile phone masts.

4

21 September 2008

0

5

10

15

20

25

30

35

40

45

2001 2002 2003 2004 2005 2006 2007

(SR billion)

Fixed and data services Mobile services

Telecom revenues

Source: CITC

0 5 10 15 20 25 30

0 to 9

10 to 19

20 to 29

30 to 39

40 to 49

50 to 59

60 to 69

70 +

(age)

(percent of total)

Young population

Impact of the new operator The entry of Zain into the market will heighten competition. STC was slow to react to Mobily and lost 31 percent of its market share in Mobily’s first year of operations. Both existing operators are in a far better position to cope with competition this time around. In order to sustain subscribers and profitability, STC has made major investments in technology and improved its customer service program. Mobily has been marketing aggressively and building up its provision of sophisticated technology in preparation for Zain. Nonetheless, Zain is an experienced regional operator and we expect it capture up to 5 percent of the market share in its first year. Zain will put pressure on pricing, margins and customer retention. All the operators are likely to offer more competitive pricing plans that will hit average voice revenue per subscriber and additional features and services including high-speed data, imaging, entertainment and location-based services. We also expect a greater differentiation between the services offered to different types of customers.

Mobily is a joint stock company with an authorized and paid up capital of SR5 billion. It has announced that it will increase its capital by 40 percent to SR7 billion through a rights issue. There are currently 500 million shares outstanding. Mobily is the brand name of the Saudi operations of Etihad Etisalat of the UAE. It is the second operator of mobile phone services in Saudi Arabia.

A consortium led by Etihad Etisalat of the UAE won the second mobile phone license in Saudi Arabia in August 2004 with a bid of SR12.2 billion. It also acquired a 3G license for another SR753.8 million in December 2004. In order to operate in the Kingdom, Etihad Etisalat was required to have at least five Saudi investment partners and float 20 percent of its capital on the stock market. The initial public offer was oversubscribed by 51 times and the company was listed on the stock market in October 2004.

Etihad Etisalat adopted the brand name Mobily and started operating in the Kingdom in 2005. The management of Mobily entered into a service agreement with Etihad Etisalat which requires Mobily to pay an annual management fee of SR37.5 million ($10 million). Etihad Etisalat provides consulting services in areas such as the provision of customer services, management of capital investment and senior management services.

Mobily now offers a suite of wireless communication products and services that are designed to meet the needs of its targeted customer groups: individuals, businesses and government. Aggressive advertising, competitive pricing and product innovation have enabled Mobily to build up its subscriber base to 11.1 million at the end of 2007 (around 47 percent of the total market). Mobily dominates the market for prepaid mobile calls. Mobily distributes through owned and operated flagships, franchise-based fully branded outlets and co-branded outlets. In addition, it has 939 preferred dealers and over 4,000 dealers/sellers throughout the Kingdom.

5

21 September 2008

The company

Ownership structure

Technology

Mobily’s technological platform is of a high standard. At the end of 2007 Mobily had 4,843 base stations covering the majority of the Kingdom, 993 of which were enabled to provide 3G services. (A base station is a radio transmitter that is the hub of a wireless network and a bridge that connects between a wired and wireless network.) The buildup of Mobily’s 3G network has allowed it to offer internet services where dial up connections are unavailable. This technology has made a major contribution to Mobily’s operations and will be the main revenue driver in the coming years.

A key technological development for Mobily is the SR1 billion Saudi National Fiber Network. This 12,500 km network will cover all the major cities in the Kingdom and the project involves the installation of several of wireless base stations to establish high-capacity data centers and the laying of fiber rings in Riyadh, Jeddah, Khobar and Dammam. It should be completed by the end of 2008 and once operational it will allow Mobily to transmit data and phone services for both landline and mobiles at ultra high speed. This wireless offering will compete with STC, which is currently the only operator in the Kingdom that provides users with internet connectivity via DSL (Digital Subscriber Line, a technology that allows digital data to pass through telephone lines or networks). It should be heavily used as the Kingdom steps up usage of wireless internet access.

Products and services At the end of 2007 Mobily was offering 44 services, ranging from entertainment to connectivity, targeted at specific segments of the Saudi market including youth, women and business. It was the first operator to specifically target the corporate sector, forming Mobily Business which is separate from the company’s mass market consumer offerings. Mobily Business introduced the BlackBerry to the Kingdom and as a result more than 20 banks and corporate institutions are registered Mobily Business customers. Mobily has also introduced high-speed mobile internet offers, which include unlimited download packages and discounts to customers who use various internet connectivity technologies (GPRS and HSDPA). Mobily has done a solid job of creating loyalty to programs to retain subscribers. It runs a reward program called Neqaty, under which all Mobily subscribers are automatically awarded points in line with their spending. Subscribers can redeem their points for text messages, internet usage or products at partner retailers. Loyalty programs are

6

21 September 2008

2004 2008

Etisalat UAE-based telecoms service provider 35% 26.25%

GOSI State-owned private sector pension fund manager 15% 11.25%

Saudi Investors Abdul Aziz Alsaghyir Investment Co. 7% 5.63%

Abdullah & Said M. O. Binzager Co. 4% 3.38%

Al Jomaih Holding Co. 6% 4.5%

Riyadh Cables Group Of Companies 6% 4.5%

Rana Investment 6% 4.5%

Listed on the stock market 20% 40%

an important way of maintaining customers tempted by the launched of Zain.

Acquisitions

Mobily has acquired two Saudi information technology companies. The first, Bayanat Al-Oula for Network Services, is a data service provider that offers data and online services. Prior to the acquisition in September 2007, Bayanat was granted a license from CITC to construct and operate a new national optical, data, and wireless network. In addition, Bayanat is currently constructing and running an international gateway through which connectivity to the internet and other internet service providers will be established. This acquisition allows Mobily to diversify its services by entering into the WIMAX (Worldwide Interoperability for Microwave Access) market and provide data communication services to its customers. (WIMAX is a technology that provides high-speed wireless data transmission.)

In July 2008, Mobily was approved by the CITC to acquire Zajil, the Kingdom’s first internet service provider (ISP), for SR80 million. Zajil has been providing data and network communication services since 1989 and has a strong client base including some government ministries and leading corporations. It has partnered with local and international players such as Cisco and IBM.

In order to provide DSL lines, Zajil and other internet service providers are currently completely dependent on STC, which is the Kingdom’s only DSL provider. When Bayanat’s network is complete, use of Zajil as an ISP will be a useful source of revenues to Mobily. As the new network is likely to result in lower internet browsing fees, it may attract other ISPs from the STC network and further boost Mobily’s revenues.

In order to save costs and enhance its customer service, Mobily InfoTech was established in Bangalore, India in March 2008. This will provide IT solutions and consulting services to the parent company in areas such as billing, customer relationship management and service provision. The company so far has more than 100 employees and it is planning to further expand by the end of the year.

Brand recognition Mobily has invested heavily to establish a strong brand name in the Kingdom. It uses television, newspapers and billboards and sponsors a leading football club in order to target both the 15-30 year old age range and the business market. It has targeted these two sectors in particular, as they are the heaviest spenders on mobile technology. Capturing and locking in these customers will provide a solid basis for further revenue generation. The company’s marketing and advertising costs went up by 28 percent last year to SR466 million. We view the hefty advertising spending to be necessary, since the company has been in operation only three years and is now facing new competition.

Management We met with Mobily’s management in preparing this report. They

7

21 September 2008

consist of a strong set of professionals combining industry specialists with broader experience. The management team has so far delivered on its business plan and has been aggressive in introducing technology, products and services in the Kingdom. Intensified competition following the introduction of Zain will test the management’s ability to continue to innovate to retain mobile subscribers.

The telecom sector in the Kingdom is suffering from a shortage of industry experienced professionals. Higher salaries will be an inevitable result of this and some delays to the roll-out of new services are possible. Mobily had more than 3,000 employees at the end of 2007, more than 80 percent of which are Saudis (its Saudization requirement is 30 percent).

Mobily’s revenues have grown in line with its subscriber base. Total revenues grew by 44 percent last year to SR8.4 billion owing to rising receipts from calls. Revenues fall under the following categories:

• Usage: Revenues from all outgoing calls and other chargeable events, such as text messaging and downloading. Usage accounted for 77 percent of Mobily’s revenues in 2007.

• Interconnect revenue: Revenue collected from other telecoms operators for the use of Mobily’s network. This accounted for around 17 percent of Mobily’s revenue in 2007.

• Rental fees: Line rental fees are charged on a monthly basis for post paid customers and accounted for 3.5 percent of the total revenues in 2007.

• Visitor roaming: Roaming revenue comes from when visitors use Mobily’s network while in the Kingdom and when Mobily customers use their phones outside the Kingdom. These accounted for 1.3 percent of revenues last year.

• Activation fee: A one-time fee paid by a new subscriber in order to activate a line. It made up 0.3 percent of Mobily’s revenues last year.

• Other: All other revenues make up of 1.6 percent of the total revenue in 2007.

While costs have risen owing to subscriber growth, they have done so at a lower rate than revenues. Interconnection costs accounted for almost half of Mobily’s costs last year, followed by transfers to the government, which more than doubled last year. Gross margin measures the percent of total sales revenue that Mobily keeps after incurring the direct expenses associated with producing services sold. Gross margins have improved in line with higher revenues. In 2007, Mobily’s gross margin was 55.1 percent. The net profit margin became positive in 2006 at 12.0 percent and rose to 16.6 percent last year. Profitability ratios have improved in line with the rapid growth in subscriber base. Profitability ratios because positive in 2006 and generally improved during 2007. Return on equity was 23.7 percent and return on invested capital reached 15 percent last year.

8

21 September 2008

Financial analysis

Activation fees

0%

Rental fees

3%

Usage

77%

Interconnect

revenue

17%

Visitor roaming

1%

Other

2%

Revenue breakdown

Profitability ratios (percent)

In 2007 Mobily secured a Sharia-compliant financing package of SR10.8 billion from local, regional and international financial institutions. For the largest component of this, Mobily used airtime minutes as the underlying commodity, selling these to financial institutions. They are then sold back to Mobily with a small premium and Mobily distributes the airtime minutes to its subscribers. This injection of cash was to repay a short term loan of SR7.1 billion and to finance future expansion. Mobily has also secured working capital and financial support Murabaha facilities. According to the management these have yet to be utilized.

Financing facility

Mobily will pay back the loan over six years on a semi annually basis. The repayment amount varies depending on interest rates and other terms. By structuring the loan this way it is a long-term liability, whereas the loan it repaid was a short-term liability. Mobily also received a short-term financing facility from local financial institutions of SR1.5 billion to finance the acquisition of Bayanat al-Oula. Converting the debt to long term has the effect of improving the liquidity ratios, though they remain very low because of the large borrowing and spending in the early phase of Mobily’s operations. The current ratio, which compares current assets to current liabilities, is increasing from a very low base, as is the quick ratio, which measures the amount of liquid assets available to offset current debt. Ratios under 1.0 are considered weak and should move to more healthy territory over the coming years. Liquidity ratios

Debt ratios have improved in the past three years as the company has ramped up operations. Leverage ratios

0

1

2

3

4

5

6

7

8

9

2005 2006 2007

(SR billion)

Operating revenue Cost of operations

Revenue and cost of operations

9

21 September 2008

SR million

Airtime financing facility 9,178.50

Working capital Murabaha facility 750.00

Financial support Murabaha facility 843.75

2005 2006 2007

Current ratio 0.11 0.18 0.52

Quick ratio 0.03 0.11 0.36

Net working capital (SR million) -9,602 -9,502 -2,916

2008H1

0.37

0.27

-5,865

2005 2006 2007

Long-term debt to total capital 0.29 0.26 0.57

Debt to equity ratio 3.12 2.9 2.36

Equity to total assets (%) 24 26 30

Equity to total capital (%) 71 74 43

2008 H1

0.46

1.14

27.9

46.8

2005 2006 2007

Net profit margin -70.3 12.0 16.6

Return on total assets -14.4 4.1 7.5

Return on equity -29.5 15.5 23.7

Return on invested capital -59.0 16.5 15.0

After three years of operation, Mobily’s assets have increased by 23 percent. Licenses accounted for 57 percent of total assets at the end of 2007, followed by property, plant and equipment which accounted for 28 percent of the total. Accounts receivable almost doubled last year and made up nearly half of the company’s current assets at the end of last year. As of first of half of 2008 current and quick ratio have declined and net working capital has gone further into negative territory. Liabilities are up by 13 percent since 2005, mainly because of additional borrowing for expansion and maintenance. Long-term loan is the largest liability, accounting for 57 percent of the total at the end of 2007, followed by short-term creditors, which accounted for 22 percent. Liabilities to short-term creditors more than doubled last year due to an increase in purchases from suppliers.

First half 2008 results

Results for the first half of 2008 were encouraging. Net income was up by 40 percent compared to the first half of 2007. Sales were driven by a substantial increase in subscribers, expanding by 24 percent, and supported the 22 percent increase in operating income. Sophisticated 3G products have contributed strongly to the revenue growth, though we believe that prepaid and post paid mobile business remain the main revenue drivers. Total assets increased by 30 percent, largely driven by the acquisition of Bayanat al-Oula. Current liabilities were up by 122 percent, caused by higher short term borrowing to finance the Bayanat acquisition and the airtime financing facility. Quarterly performance (SR ‘000)

We base our valuation of Mobily on a combination of the discounted cash flow (DCF) and relative valuation approaches. We have assigned 70 percent weight to the DCF and 30 percent to relative valuation.

DCF valuation calculations • Risk free rate: 4.11 percent. • Equity risk premium: 9.30 percent. • Beta: 1.02. • Terminal growth rate: 3 percent. Projected cash flows: We project that net income growth will average 22 percent per year based on Mobily maintaining its market share in the growing mobile market, an increase in broadband penetration and strong revenues from the new fiber optic network.

Title

Title

10

21 September 2008

Valuation

Other Payable

4%

Short-term

ceditors

22%

Long term loan

57%

Current portion

of long term

loan

7%

Due to related

parties

1%

Accured

expenses

9%

Plant, property

and equipment,

net

28%

Cash

4%

Licenses

57%

Accounts

receivable, trade

7%

Short term

investments

4%

Asset composition (end-2007)

Liability composition (end-2007)

First Half Second Quarter

2007 2008 2007 2008

Service revenue 3,905,162 4,851,341 2,028,608 2,543,553

Gross profit 2,094,306 2,636,613 1,108,899 1,413,011

Net income 554,455 774,421 303,845 448,407

EPS (SR) 1.11 1.55 0.61 0.90

The total mobile penetration rate is expected to increase to 133 percent in 2012, from 116 percent in 2007. This is a much lower rate than over the past years, but given the high population growth, still equates to a healthy increase in absolute terms. As the wireless industry continues to mature, we judge that Mobily’s future growth will be increasingly dependent on its ability to provide a technology platform that allows existing customers to upgrade their services. This will require Mobily to expand network coverage, improve network quality and broaden its array of products and services, which will be reflected in high investment and marketing expenditure. We think Mobily will maintain around a 40 percent market share. Telecom projections

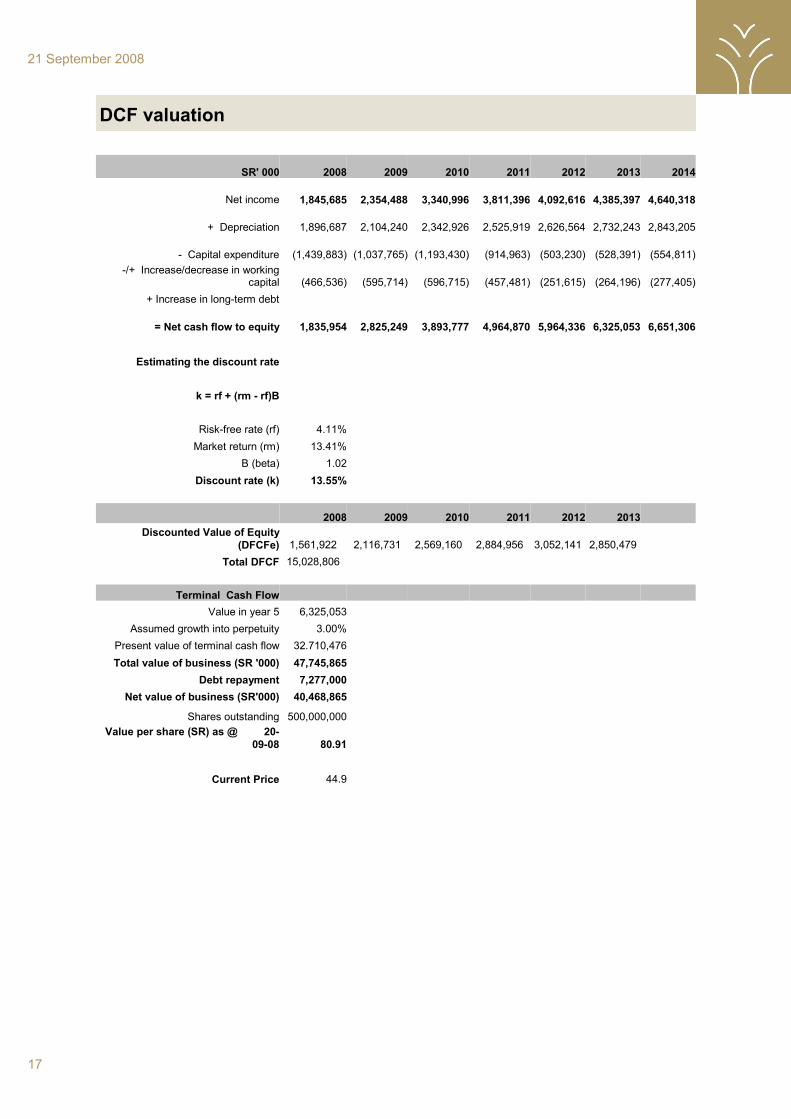

Broadband penetration is expected to more than double over the next five years to reach 23 percent by 2012. Broadband will be the primary driver of growth for Mobily and its greater penetration should result in significant revenues from the company’s fiber optic network. The commencement of operations by Zain will put pressure on pricing, margins and customer retention. Zain has initiated some high profile offers since it launched in August and we expect it to achieve a market share of 5 percent by the end of this year. Mobily has agreed to allow Zain to use its telecom infrastructure for its early years of operations, which will open another revenue stream. Mobily’s net income will also benefit from an agreement to outsource network operations that will reduce operating costs by around 20 percent from 2008. We assume that there are no further entrants to the mobile market over the next five years. We selected the net cash flow to equity (NCFe) approach as the appropriate measure of economic income to use in this valuation. Net cash flow represents the maximum amount of cash that could be distributed to shareholders without affecting the company’s normal operational cash requirements. We calculated net cash flow to equity by adding back depreciation and deducting capital expenditures, debt repayments and increases in working capital from net income. We believe that Mobily has sufficient funds to finance its operations and management has told us that they do not plan to assume any new debt. We calculated that the present value of the company’s NCFe for fiscal years 2008 through 2013 is approximately SR6.3 billion. Mobily will continue to generate cash flows beyond the discrete projection period and we have selected a long-term growth rate of 3 percent as appropriate for Mobily’s net cash flow. Combining the present value of the terminal cash flow with the present value of the discrete cash flow projections results in a total value of Mobily of SR40.5 billion. Based on the above, the DCF results in a fair market value of Mobily’s common stock on the valuation date of SR 80.9.

11

21 September 2008

2008 2009 2010 2011 2012

Fixed line penetration (%) 16.8 16.6 16.7 16.6 16.5

Mobile penetration (%) 117.2 125.6 127.4 129.3 131.7

Internet penetration (%) 32.6 43.3 56.6 66.9 82.0

Broadband penetration (%) 3.8 3.9 4.1 4.5 4.9

Computers (per 1,000 population) 232.0 251.0 268.0 288.0 308.0

Total IT spending (US$ m) 7,772 8,549 9,319 10,064 10,869

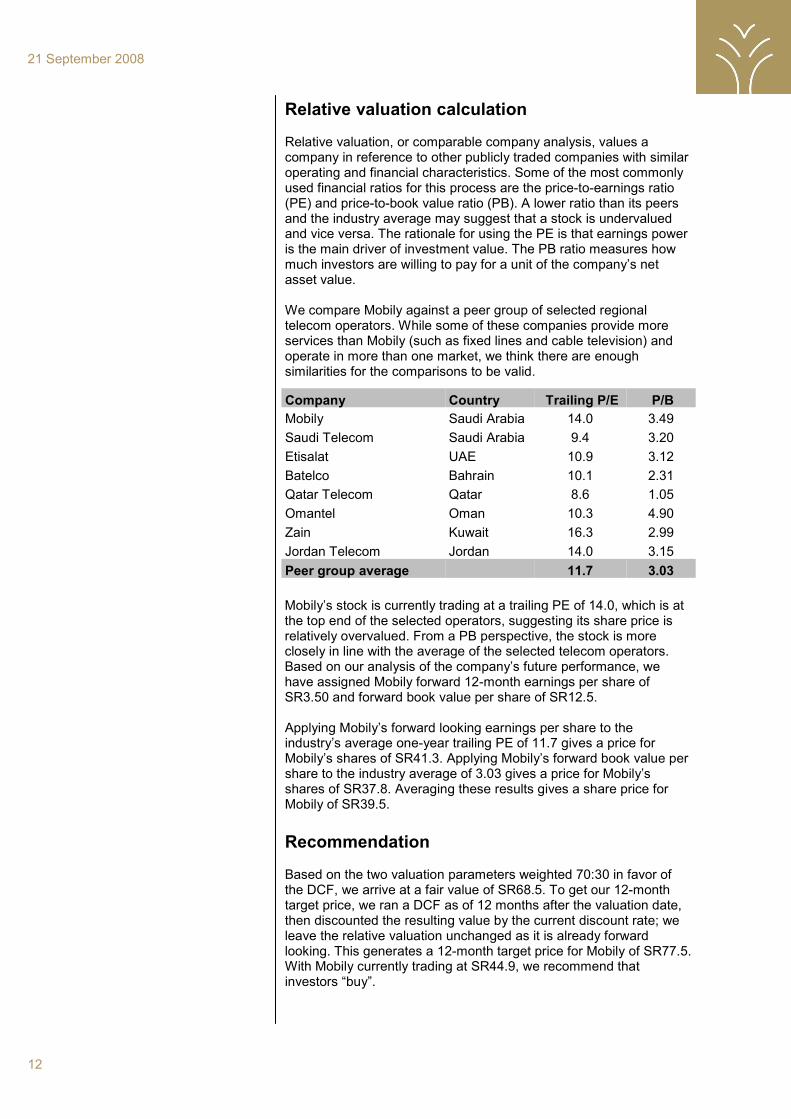

Relative valuation calculation Relative valuation, or comparable company analysis, values a company in reference to other publicly traded companies with similar operating and financial characteristics. Some of the most commonly used financial ratios for this process are the price-to-earnings ratio (PE) and price-to-book value ratio (PB). A lower ratio than its peers and the industry average may suggest that a stock is undervalued and vice versa. The rationale for using the PE is that earnings power is the main driver of investment value. The PB ratio measures how much investors are willing to pay for a unit of the company’s net asset value. We compare Mobily against a peer group of selected regional telecom operators. While some of these companies provide more services than Mobily (such as fixed lines and cable television) and operate in more than one market, we think there are enough similarities for the comparisons to be valid.

Mobily’s stock is currently trading at a trailing PE of 14.0, which is at the top end of the selected operators, suggesting its share price is relatively overvalued. From a PB perspective, the stock is more closely in line with the average of the selected telecom operators. Based on our analysis of the company’s future performance, we have assigned Mobily forward 12-month earnings per share of SR3.50 and forward book value per share of SR12.5. Applying Mobily’s forward looking earnings per share to the industry’s average one-year trailing PE of 11.7 gives a price for Mobily’s shares of SR41.3. Applying Mobily’s forward book value per share to the industry average of 3.03 gives a price for Mobily’s shares of SR37.8. Averaging these results gives a share price for Mobily of SR39.5.

Recommendation Based on the two valuation parameters weighted 70:30 in favor of the DCF, we arrive at a fair value of SR68.5. To get our 12-month target price, we ran a DCF as of 12 months after the valuation date, then discounted the resulting value by the current discount rate; we leave the relative valuation unchanged as it is already forward looking. This generates a 12-month target price for Mobily of SR77.5. With Mobily currently trading at SR44.9, we recommend that investors “buy”.

12

21 September 2008

Company Country Trailing P/E P/B

Mobily Saudi Arabia 14.0 3.49

Saudi Telecom Saudi Arabia 9.4 3.20

Etisalat UAE 10.9 3.12

Batelco Bahrain 10.1 2.31

Qatar Telecom Qatar 8.6 1.05

Omantel Oman 10.3 4.90

Zain Kuwait 16.3 2.99

Jordan Telecom Jordan 14.0 3.15

Peer group average 11.7 3.03

13

21 September 2008

Price per

share (SR) Weights Contribution

Valuation method

Free cash flow to equity (DCF) 80.9 70% 56.6

Relative valuation (PE/PB) 39.5 30% 11.9

Fair value price (SR) 68.5

12-month target price (SR) 76.2

14

21 September 2008

The bar on the front page of this report is Jadwa’s method of conveying our investment recommendation as clearly and concisely as possible. The bar is based on traffic lights, where green means “go” (buy), yellow is “slow” (hold), and red is “stop” (sell). Our 12-month target for the stock is the middle of the yellow area. This is the price that we expect the shares to trade at in 12 months time. This is different to fair value, which is our estimate of the fair value of the company’s share price as of the valuation date. We use five colors in our recommendation bar, with those on either side of the yellow area signifying that an investor should consider buying or selling the stock. The price range for each of these alternatives is within the colored section. These price ranges have been adjusted to take account of share price volatility (using the stock's variance-mean ratio). The more volatile the share price, the larger the price ranges.

The Jadwa recommendation bar

12-month target price

SR78 Current price

SR45

Sell Consider selling

Hold Consider buying

Buy

SR82-73 SR88-83 >SR88 SR72-67 <SR67

15

21 September 2008

Performance matrix

This table ranks Mobily’s performance against what we believe are the key success factors for the sector it operates in (telecoms). A green rating is positive, yellow neutral and red negative.

Factor Measures Mobily status Rating

Valuation Fair market value of the company. The stock is under valued.

Management How efficiently and effectively the company is run.

A strong management team that have established a solid track record.

Competitive position

The position of one business relative to others in the same industry.

Mobily has a healthy position with a variety of consumer groups, but will be challenged by Zain.

Brand recognition To promote the name of the business in the market and achieve recognition.

Mobily has invested heavily to successfully establish a strong brand name.

Product mix The degree of homogeneity between products, product lines, business lines and services.

Mobily target diverse clients within the Saudi market. Recent acquisitions will diversify revenue streams.

Technology The extent to which the company employs technology or needs to make additional investments to remain competitive.

Mobily's technology platform is of a high standard.

Expansion potential Where the company is in its life

cycle and what future projects or plans does it have to maintain growth momentum.

The fiber optic network and integration of Zajil bolster Mobily's expansion potential in what is already a fast growing sector.

Quality of Service Customers' impressions about the services provided.

Mobily's subscribers are affected by dropped calls and coverage issues.

Disclosure & Transparency

How forthcoming and open the company is with regards to sharing and disclosing information.

Mobily is one of the most transparent companies in Saudi Arabia and has a strong investor relations department.

Profitability The end-result of a company's operations utilizing all resources at its disposal.

Profitability ratios have improved in line with the rapid growth in subscriber base.

Activity How efficient management is in using its assets.

Activity ratios are generally on an upward trend, though the average collection period has worsened.

Performance Efficient utilization of assets in generating sales.

Sales continued to grow as a percentage of both fixed assets and total assets.

Liquidity Company's ability to meet short-term and current obligations on time.

Measures of liquidity have improved significantly, but remain very low because of the large borrowing and spending in the early phase of operations.

Coverage Long term solvency and ability to deal with financial problems.

Coverage ratios are improving.

Leverage Capital adequacy and company's

ability to meet long-term obligations and take advantage of opportunities as they arise.

Mobily's balance sheet is highly leveraged.

16

21 September 2008

The discounted cash flow model

The DCF method estimates value on the basis of future cash flows over an investment horizon using empirical market data, macroeconomic and industry evidence and the underlying fundamental trends of the subject company. The DCF method then applies a present value discount rate, known as the required rate of return on investment, to project future cash flows, which results in an estimation of net present value of projected cash flows. The value of the company is estimated by projecting the cash flows that the company is expected to produce and discounting those cash flows back to the valuation date using a discount rate that reflects the related risk. An in-depth analysis of the company’s revenues, fixed and variable expenses and capital structure were conducted.

DCF valuation calculations Present value discount rate: We estimated the cost of Mobily’s equity capital (net of long-term debt) using the capital asset pricing model which incorporates a risk free rate, a long-term risk premium and a company’s stock beta.

• Risk free rate: The risk free rate is used as to measure the opportunity cost of investing. Since DCF analysis is based upon a long-term investment horizon, the appropriate risk-free rate is that of a long-term government security. We use the 10-year Saudi riyal bond issued by SAMA, which yielded 4.11 percent on the valuation date.

• Equity risk premium: We calculate the equity risk premium as the average of the arithmetic and geometric means of TASI historical returns, less the long-term rate of return on the 10-year SAMA bond. The arithmetic mean of the TASI over the period from 1980 to September 21 2008, was 15.99 percent. The geometric mean over the same period was 11.07 percent. The average of the two is 13.5 percent, which is the market return. Accordingly, the equity risk premium is 9.3 percent.

• Beta: Beta is a measure of the risk inherent in the company’s investment returns. The market (TASI) beta is always one. A stock beta that is higher than one, as in the case of Mobily (1.02) indicates that the stock tends to more volatile (up or down) than the TASI (by 3 percent in this case). Applying beta to the long-term equity risk premium gives a beta-adjusted long-term equity risk premium of 9.45 percent .

The capital asset pricing model resulted in a total estimated cost of equity capital of approximately 13.55 percent. This is arrived at by adding the beta-adjusted equity risk premium and the risk free rate.

17

21 September 2008

DCF valuation

SR' 000 2008 2009 2010 2011 2012 2013

Net income 1,845,685

2,354,488

3,340,996

3,811,396

4,092,616

4,385,397

+ Depreciation 1,896,687

2,104,240

2,342,926

2,525,919

2,626,564

2,732,243

- Capital expenditure (1,439,883)

(1,037,765)

(1,193,430)

(914,963)

(503,230)

(528,391)

-/+ Increase/decrease in working capital (466,536)

(595,714)

(596,715)

(457,481)

(251,615)

(264,196)

+ Increase in long-term debt

= Net cash flow to equity 1,835,954

2,825,249

3,893,777

4,964,870

5,964,336

6,325,053

Estimating the discount rate

k = rf + (rm - rf)B

Risk-free rate (rf) 4.11%

Market return (rm) 13.41%

B (beta) 1.02

Discount rate (k) 13.55%

2008 2009 2010 2011 2012 2013

Discounted Value of Equity

(DFCFe) 1,561,922 2,116,731 2,569,160 2,884,956 3,052,141 2,850,479

Total DFCF 15,028,806

Terminal Cash Flow

Value in year 5 6,325,053

Assumed growth into perpetuity 3.00%

Present value of terminal cash flow 32.710,476

Total value of business (SR '000) 47,745,865

Debt repayment 7,277,000

Net value of business (SR'000) 40,468,865

Shares outstanding 500,000,000

Value per share (SR) as @ 20-

09-08 80.91

Current Price 44.9

2014

4,640,318

2,843,205

(554,811)

(277,405)

6,651,306

18

21 September 2008

Balance sheet

Financial statements

As of December 31

2005 2006 2007

SR '000 SR '000 SR '000

ASSETS Current Assets: Cash and cash equivalents 185,172 547,523 703,198 Prepayments and other current assets 71,061 Short term investments 782,765 716,688 810,295 Accounts receivable, trade 166,822 739,228 1,459,733 Inventories 32,075 38,048 69,190 Total Current Assets 1,166,834 2,041,487 3,113,477 Investments in affiliated companies License Acquisition fees, net 12,313,626 11,800,160 11,286,694 Plant, property and equipment, net 2,757,207 3,847,532 5,478,552 Investments - - 1,836 Total Fixed Assets 15,070,833 15,647,692 16,767,082

TOTAL ASSETS 16,237,667 17,689,179 19,880,559

LIABILITIES & SHAREHOLDERS

EQUITY Current Liabilities: Accured Expenses 2,133,514 1,687,156 1,207,463 Creditors 876,118 1,516,376 3,076,067 Due to Related Parties 193,251 179,335 111,485 Other Payable - 320,294 623,687 Deferred Revenue 218,017 - - Borrowings 7,348,129 7,839,943 1,010,625 Total Current Liabilities 10,769,029 11,543,104 6,029,327

Founding Shareholders Loan 1,600,000 1,600,000 - Long-term debt - - 7,912,356 Employees End of Service Plan 2,650 13,096 26,349 Total Long-term Liabilities 1,602,650 1,613,096 7,938,705

Total Liabilities 12,371,679 13,156,200 13,968,032

SHAREHOLDERS' EQUITY Share capital 5,000,000 5,000,000 5,000,000 Accumulated Loss (1,039,915) (467,021) - Statutory reserve - - 137,955 Retained earnings - - 774,572 TOTAL SHAREHOLDERS' EQUITY 3,960,085 4,532,979 5,912,527

TOTAL LIABILITIES &

SHAREHOLDERS' EQUITY 16,331,764 17,689,179 19,880,559

19

21 September 2008

Income statement

Cash flow statement

As of December 31

2005 2006 2007

SR '000 SR '000 SR '000 Operating Revenue 1,661,737 5,840,815 8,440,432 Cost of operations (967,240) (2,680,466) (3,792,193) Gross operating income 694,497 3,160,349 4,648,239 Provisions (52,650) (124,174) (291,847) SG & A expenses (754,614) (1,035,671) (1,409,583) Depreciation & amortization (739,141) (844,979) (1,030,919) Total operating expenses (1,546,405) (2,004,824) (2,732,349) Operating income, net (851,908) 1,155,525 1,915,890 Financial Charges (347,641) (478,680) (555,391) Other Income 32,170 23,513 43,251 Income before Zakat (1,167,379) 700,358 1,403,750 Provision for Zakat

Provision for Tax (24,202) Net Income (1,167,379) 700,358 1,379,548 Shares outstanding (units) 5,000,000 5,000,000 5,000,000 Earnings per share (EPS) SR (0.23) 1.40 2.76

For fiscal year ending December 31

2005 2006 2007

SR '000 SR '000 SR '000

Net cash provided by (used in) operating activities 1,325,742 1,928,010 2,153,202

Net cash provided by (used in) investing activities (15,776,607) (1,819,310) (1,878,177)

Net cash provided by (used in) financing activities 13,948,129 253,651 (119,350)

Cash and cash equivalents at yearend 185,172 547,523 703,523

20

21 September 2008

Ratio analysis

Fiscal years ending December 31

2005 2006 2007

Liquidity

Current ratio 0.11 0.18 0.52 Quick ratio (Acid-Test) 0.03 0.11 0.36 Net working capital (SR million) (9,602) (9,502) (2,916)

Activity

Turnover:

Sales to net working capital (0.2) (0.6) (2.9) Inventory 60.3 76.45 70.72

Receivables 19.9 12.9 7.7 Average collection period (days) 18 28 48

Days to sell inventory 6 5 5

Performance (Asset utilization ratios)

Sales to fixed assets 0.6 1.5 1.5

Sales to total assets 0.10 0.33 0.43

Profitability (per share)

Gross margin (%) 41.8 54.1 55.1 Operating margin before depreciation (%) 41.8 54.1 55.1 Operating margin after depreciation (%) -51.3 19.8 22.7 Pretax profit margin (%) -70.3 12.0 16.6 Net profit margin (%) -70.3 12.0 16.6 Return on:

Total assets (%) -14.4 4.1 7.5 Equity (%) -29.5 15.5 23.7 Investment (%) -59.0 16.5 15.3 Average assets (%) -14.4 4.1 7.5 Average equity (%) -59.0 16.5 26.9 Invested capital (ROIC, %) -59.0 16.5 15.3

Leverage (Balance sheet)

Long-term debt to total capital 0.29 0.26 0.57 Debt to equity ratio 3.12 2.90 2.36 Equity to total assets (Equity ratio, %) 24 26 30

Equity to total capital(%) 71 74 43

21

21 September 2008

Summary of quarterly results

Balance sheet as on

30/09/2007 31/12/2007 31/03/2008 30/06/2008

Current assets 2,652,149 3,018,869 3,287,192 3,365,293

Inventory 40,626 69,190 71,035 85,635

Investments 0 1,836 1,836 0

Fixed assets 4,446,915 5,478,552 6,042,285 6,964,256

Other assets 11,415,062 11,286,694 11,158,328 12,650,538

Total assets 18,554,752 19,855,141 20,560,676 23,065,722

Current liabilities 4,719,863 6,003,909 6,625,677 9,316,131

Non-current liabilities 8,436,831 7,938,705 7,946,458 7,312,643

Other liabilities 0 0 0 0

Shareholder's equity 5,398,058 5,912,527 5,988,541 6,436,948

Total liabilities & shareholder equity 18,554,752 19,855,141 20,560,676 23,065,722

Statements of Income for the period ending

30/09/2007 31/12/2007 31/03/2008 30/06/2008

Sales 2,124,575 2,410,694 2,307,788 2,543,553

Sales cost 948,449 1,036,977 1,084,186 1,130,542

Total income 1,176,126 1,373,717 1,223,602 1,413,011

Other revenues 9,639 17,855 14,031 5,236

Total revenues 1,185,765 1,391,572 1,237,633 1,418,247

Admin and marketing expenses 461,503 434,456 112,073 199,277

Total expenses 875,141 860,912 909,448 967,354

Net income before zakat 310,624 530,660 328,185 450,893

Zakat 0 16,191 2,171 2,486

Net Income 310,624 514,469 326,014 448,407

Other expenses 149,385 144,741 504,980 448,363

Depreciation 264,253 281,715 292,395 319,714

Disclaimer of Liability

The information contained in this research (hereinafter refer to as “Research”) has been obtained from various sources whose data is believed to be reliable and accurate. Jadwa Investment does not claim and has no way of ascertaining that such information is precise or free of error. This Research shall not be reproduced, redistributed or passed directly or indirectly to any other person or published in whole or in part for any purpose without written consent of Jadwa Investment. The information, opinions, rankings or recommendations contained in this Research are submitted solely for informational purposes. This Research is not an advice to sell nor is it a solicitation to buy any securities, or to take into account any particular investment objectives, or financial positions or is intended to meet the particular needs of any investor who may receive this Research. Jadwa Investment or its directors, staff, or affiliates make no warranty, representation or undertaking whether expressed or implied, nor does it assume any legal liability, whether direct or indirect, or responsibility for the accuracy, completeness or usefulness of any information that is contained in this Research. It is not the intention of this Research to be used or deemed as an advice, option or for any action that may take place in the future. Investors should seek an independent opinion before taking any investment action. The investor should understand that the income of investments is subject to fluctuation and that the price or the value may change at any time. Any action relying on this Research in whole or in part is entirely the sole responsibility of the investor. Jadwa Investment or its directors, staff, or affiliates may have a financial interest in the security referred to herein. All rights connected with this Research are reserved to Jadwa Investment. This Research may be updated or changed at any time without prior written notice.

22

21 September 2008

For comments and queries please contact: Brad Bourland Chief Economist [email protected] Gasim Abdulkarim Equity Research Director [email protected] or the author: Salman Aga Equity Research Associate [email protected] Head office: Phone +966 1 279-1111 Fax +966 1 279-1571 P.O. Box 60677, Riyadh 11555 Kingdom of Saudi Arabia www.jadwa.com

Related Documents