Federal Democratic Republic of Ethiopia ETHIOPIA NATIONAL PULSES STRATEGY 2019-2024

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Federal DemocraticRepublic of Ethiopia

ETHIOPIA

NATIONAL PULSES STRATEGY2019-2024

This National Pulses Strategy was facilitated by Supporting Indian Trade and Investment for Africa, a South–South trade and investment initiative that aims to improve the com-petitiveness of select value chains through providing partnerships from institutions and businesses from India. Supporting Indian Trade and Investment for Africa is funded by the United Kingdom of Great Britain and Northern Ireland Department for International Development and implemented by the International Trade Centre (ITC). ITC is the joint agency of the World Trade Organization and the United Nations.

The Strategy was designed based on the process, methodology and technical as-sistance of ITC within the framework of its Trade Development Strategy programme. ITC-facilitated trade development strategies and roadmaps are oriented to the trade objectives of a country or region and can be tailored to high-level economic goals, specific development targets or particular sectors, allowing policymakers to choose their preferred level of engagement.

Technical support was provided by Charles Roberge and Abhilash Puljal. Genzeb Akele Zewdie managed the design process at the country level, under the overall project man-agement of Carolin Averbeck and general supervision of Govind Venuprasad.

In-country guidance and coordination of the Strategy design process was led by Assefa Yohannes, Manager, EPOSEPEA; Abdulsemed Abdo, Crop Development Director, MoANR; ZegeyeTekilu, Manager Agribusiness, ATA; Mulugeta Mohammed, Crop Marketing Director, MoT. The views expressed herein do not reflect the official opinion of ITC. Mention of firms, products and product brands does not imply the endorsement of ITC. This document has not been formally edited by ITC.

The International Trade Centre ( ITC )

Street address : ITC, 54-56, rue de Montbrillant, 1202 Geneva, SwitzerlandPostal address : ITC Palais des Nations 1211 Geneva, SwitzerlandTelephone : + 41- 22 730 0111Postal address : ITC, Palais des Nations, 1211 Geneva, SwitzerlandEmail : [email protected] : http :// www.intracen.org

Layout: Jesús Alés – www.sputnix.es

Federal DemocraticRepublic of Ethiopia

ETHIOPIA

NATIONAL PULSES STRATEGYVALUE CHAIN ROADMAP FOR PRODUCTION

AND TRADE OF PULSES FROM ETHIOPIA

2019-2024

Photo: (CC BY-SA 2.0) pixabay, by Natalie Gi from Pixabay.

II ETHIOPIA NATIONAL PULSES STRATEGY 2019-2024

IIIETHIOPIA NATIONAL PULSES STRATEGY 2019-2024

MESSAGE FROM MR. SANI REDI, MINISTER OF STATE FOR AGRICULTURE

Pulses are strategically important to Ethiopia as they are the second most important group of crops, after cere-als, and together they provide food and income to more than 10 million households. The overall acreage of pro-duction is over 1.5 million hectares and overall output is almost 3 million tons. Pulses are the third most important group of commodities export, after coffee and sesame, thereby contributing significantly to the country’s foreign currency requirements. Ethiopia ranks among the top ten countries in the world for pulses exports with an estimat-ed value of USD 248 million and volume of 338,974 tons in 2016. Ethiopia’s export trend in pulses has reached an average annual growth rate ( CAGR ) of 16% between 2011 and 2015. The Indian market is a major destina-tion of Ethiopian pulses which accounts for a total of about USD 35 million in exports ( Ministry of Trade Annual Report, 2016 ).

Despite Ethiopia’s growing exports of pulses in recent years, the country still remains a small player in the global market representing only 3% of world pulses exports in 2016. The potential of the sector is yet to be fully utilized as a result of various challenges along the entire value chain.

The National Pulses Sector Strategy responds to these constraints by providing Ethiopia with a detailed Plan of Action ( PoA ) that will facilitate growth in the sector within the next 5-year period. Through the steps outlined in the PoA, pulses stakeholders in Ethiopia will improve their ca-pability to offer competitive products. The Strategy also supports the implementation of Ethiopia’sGrowth and TransformationPlan II ( GTP II ) that has identified Agro-processing and respective value chains as priority sectors for further development given the country’s comparative advantage.

The Ministry of Agriculture ( MoA ) takes particular pleasure in welcoming the SITA Pulses Sector Strategy Roadmap and its detailed Plan of Action with the aim of boosting Ethiopian Pulse export to the regional and international market.

The National Pulses Strategy has exceeded our expecta-tions, not only in the successful mobilization of all sector stakeholders, but also in facilitating extensive and fruitful discussions between public and private sector stakehold-ers. Representatives from public and private sector as well as research institutions attended three successive consul-tations, allowing for a realistic evaluation of the challenges and opportunities of the sector and extensive debates to define the best way forward. This inclusive approach en-sured that all stakeholders were committed to the process and left with a clear understanding of each actor’s role.

A market led strategic orientation, prioritized by the pulses sector stakeholders and embedded into a detailed imple-mentation plan, provides a clear road map that can be leveraged to address constraints to trade, maximize value addition and support regional integration. This strategy is articulated around three strategic objectives:

1. Improve sector productivity and quality through en-hanced public and private support in research, input distribution, production, processing and export

2. Improve export competitiveness by strengthening backward production and planning by responding to market opportunities.

3. Strengthen the capacity of sector stakeholders to im-prove value addition.

In order to maintain the momentum sparked by the con-sultations, the Ministry is in the process of establishing a national pulse sector public-private partnership platform, which will support the implementation of the operational objectives defined in this Plan of Action.

We acknowledge the support of the International Trade Centre ( ITC ), Supporting Indian Trade and Investment for Africa ( SITA ) project and the Government of the United Kingdom through DFID for their support in developing this National Pulse Strategy; their initiative will benefit the Ministry as well as actors along the entire value chain in the successful promotion of the sector.

IV ETHIOPIA NATIONAL PULSES STRATEGY 2019-2024

MESSAGE FROM MR. HAILE BERHE, PRESIDENT OF THE ETHIOPIAN PULSES, OILSEEDS AND SPICES PROCESSORS-EXPORTERS ASSOCIATION (EPOSPEA)

The Ethiopian Pulses, Oilseeds and Spices Processors-Exporters Association ( EPOSPEA ) was established with the objective of building the capacity of its members to make them competitive in the global market. In this context, EPOSPEA is pleased to have partnered with International Trade Centre ( ITC ), Supporting Indian Trade and Investment for Africa ( SITA ) project, since its im-plementation in 2015, towards achievement of this objective.

This Value Chain Roadmap, aimed at strengthening the Ethiopian Pulses Sector, is prepared after extensive consultations – on the opportunities and constraints in relation to production, productivity, quality control, processing, packing, marketing and market access – with members of EPOSPEA and other stakeholders at the national level.

I wish to thank ITC, SITA and the Government of the United Kingdom through DFID, as well as all other stakeholders involved in the formulation of this stra-tegic document. As we embark on the implementation of the Value Chain Roadmap, EPOSPEA will endeavor to work closely with all relevant stake-holders not only for the benefit of its members, but also for the overall Pulses Sector.

VETHIOPIA NATIONAL PULSES STRATEGY 2019-2024

ACKNOWLEDGEMENTS

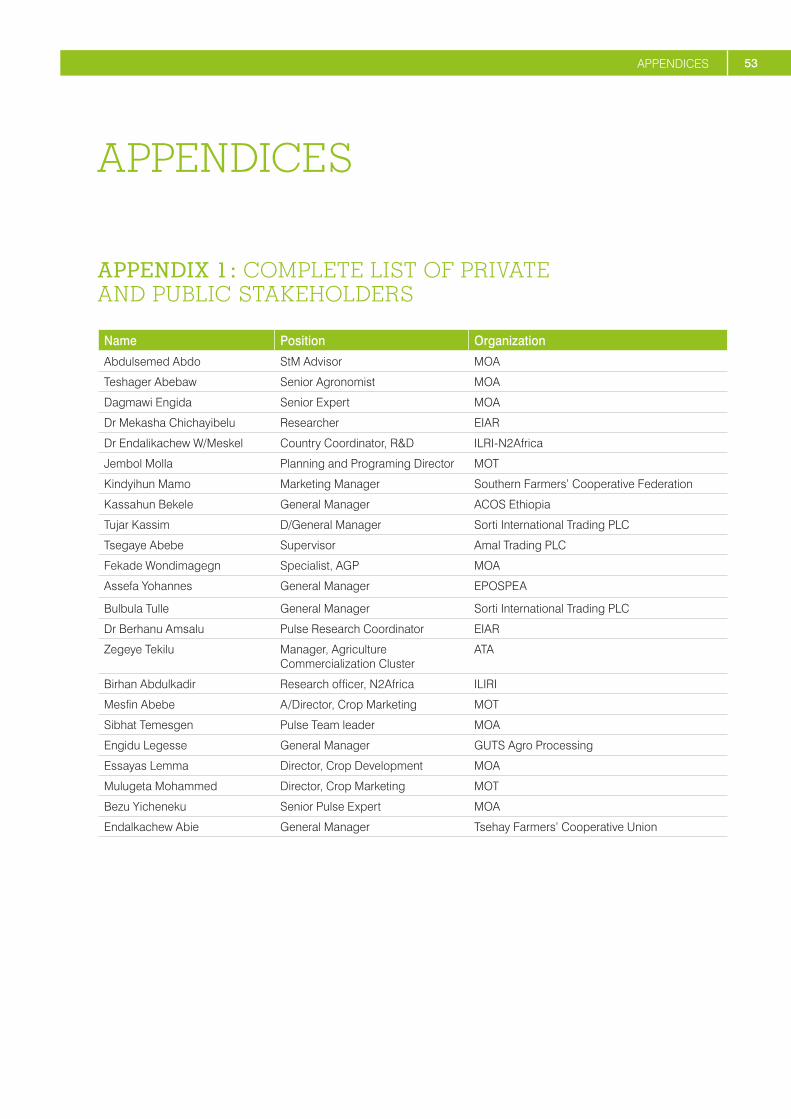

The National Pulses Strategy (the Strategy) was developed under the aegis of the Ministry of Agriculture and Natural Resources and the Ministry of Trade, Government of Ethiopia.The document benefited particularly from inputs and guidance provided by the members of this sector that steered the formulation of the Strategy, namely:

Name Organization Position

Dagmawi Engida Senior Expert MOA

Kassahun Bekele General Manager ACOS Ethiopia

Tsegaye Abebe Supervisor Amal Trading PLC

Dr Berhanu Amsalu Pulse Research Coordinator EIAR

Zegeye Tekilu Manager, Agriculture Commercialization Cluster

ATA

Sibhat Temesgen Pulse Team leader MOA

Engidu Legesse General Manager GUTS Agro Processing

Bezu Yicheneku Senior Pulse Expert MOA

Endalkachew Abie General Manager Tsehay Farmers’ Cooperative Union

The full list of public and private stakeholders who contributed their precious time to the design of this Strategy are detailed in appendix 1.

VI ETHIOPIA NATIONAL PULSES STRATEGY 2019-2024

EXECUTIVE SUMMARY 1

THE IMPORTANCE OF PULSES 5

GLOBAL TRENDS IN PULSES 8

PRODUCTION TRENDS OF PULSES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

TRADE TRENDS OF PULSES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

MAJOR IMPORTERS OF PULSES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

MAJOR EXPORTERS OF PULSES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

ETHIOPIA’S PULSES SECTOR 14

PRIORITY PULSES IN ETHIOPIA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

PULSE PRODUCTION IN ETHIOPIA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

PULSE TRADE IN ETHIOPIA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

VALUE CHAIN OF THE PULSES SECTOR IN ETHIOPIA . . . . . . . . . . . . . . . . . . . . . . . . . 22

VALUE CHAIN DIAGNOSTICS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

FOCUSING ON THE MOST PRESSING ISSUES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

ON THE PATH TO SUCCESS 31

THE VISION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

THE STRATEGIC OBJECTIVES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

THE FUTURE VALUE CHAIN OF THE SECTOR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

THE FUTURE VALUE CHAIN . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

THE FUTURE VALUE CHAIN ROADMAP . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

OPPORTUNITIES FOR THE ETHIOPIAN PULSES INDUSTRY 35

MARKET PERSPECTIVE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

VALUE OPTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

INSTITUTIONAL ADJUSTMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

REGULATORY AMENDMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

CONTENTS

VIIETHIOPIA NATIONAL PULSES STRATEGY 2019-2024

INVESTMENT REQUIREMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

MOVING TO ACTION – IMPLEMENTATION FRAMEWORK . . . . . . . . . . . . . . . . . . . . . . 42

MANAGING STRATEGY IMPLEMENTATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

PLAN OF ACTION FOR 2019-2023 45

APPENDICES 53

APPENDIX 1 : COMPLETE LIST OF PRIVATE AND PUBLIC STAKEHOLDERS . . . . . . 53

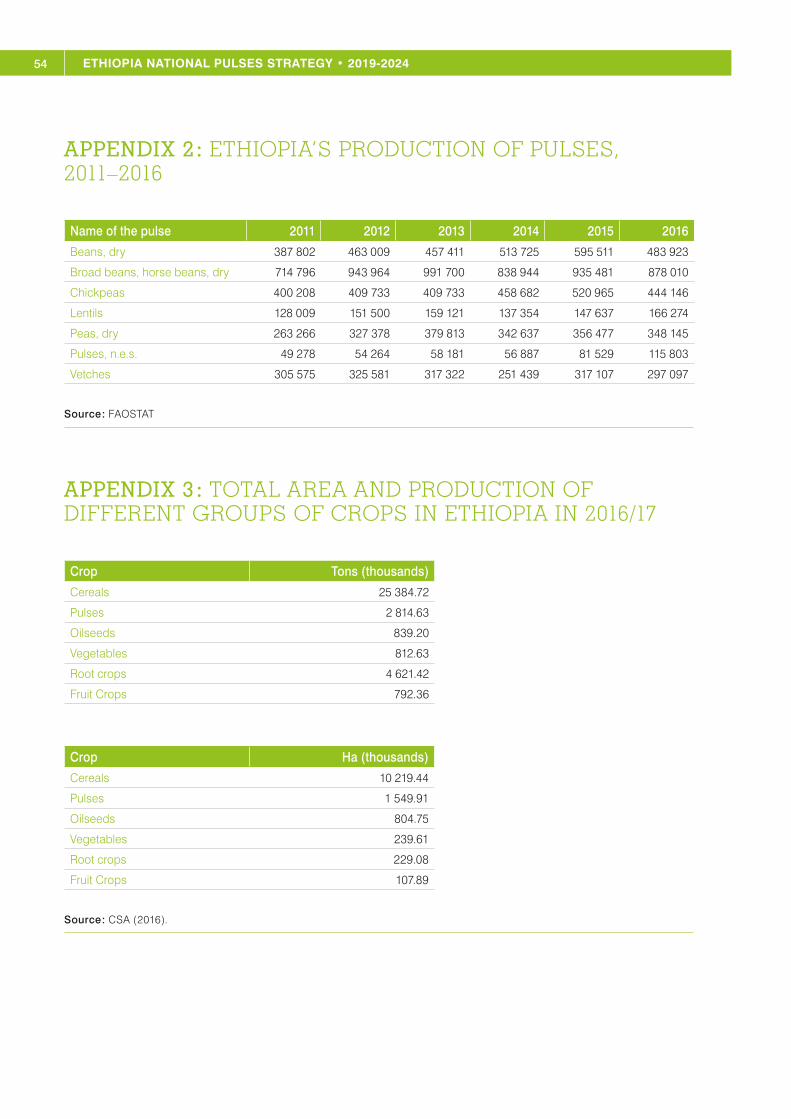

APPENDIX 2 : ETHIOPIA’S PRODUCTION OF PULSES, 2011–2016 . . . . . . . . . . . . . . . 54

APPENDIX 3 : TOTAL AREA AND PRODUCTION OF DIFFERENT GROUPS OF CROPS IN ETHIOPIA IN 2016/17 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

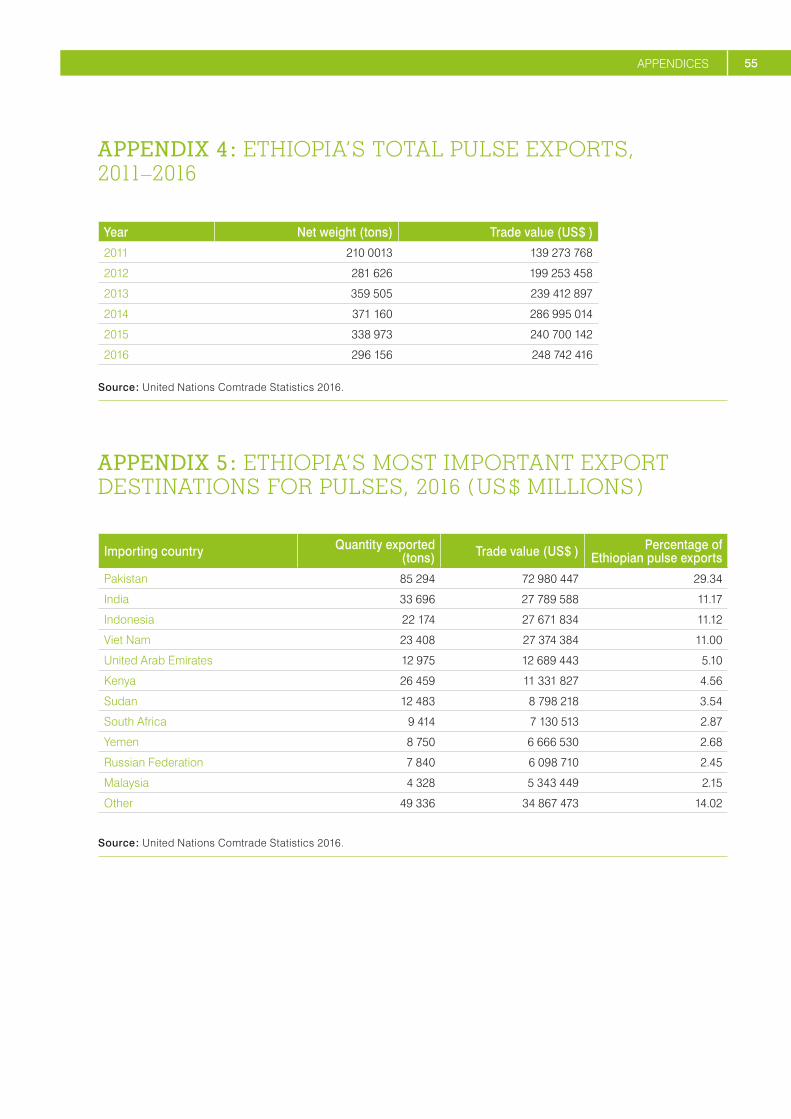

APPENDIX 4 : ETHIOPIA’S TOTAL PULSE EXPORTS, 2011–2016 . . . . . . . . . . . . . . . . . 55

APPENDIX 5 : ETHIOPIA’S MOST IMPORTANT EXPORT DESTINATIONS FOR PULSES, 2016 ( US $ MILLIONS ) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

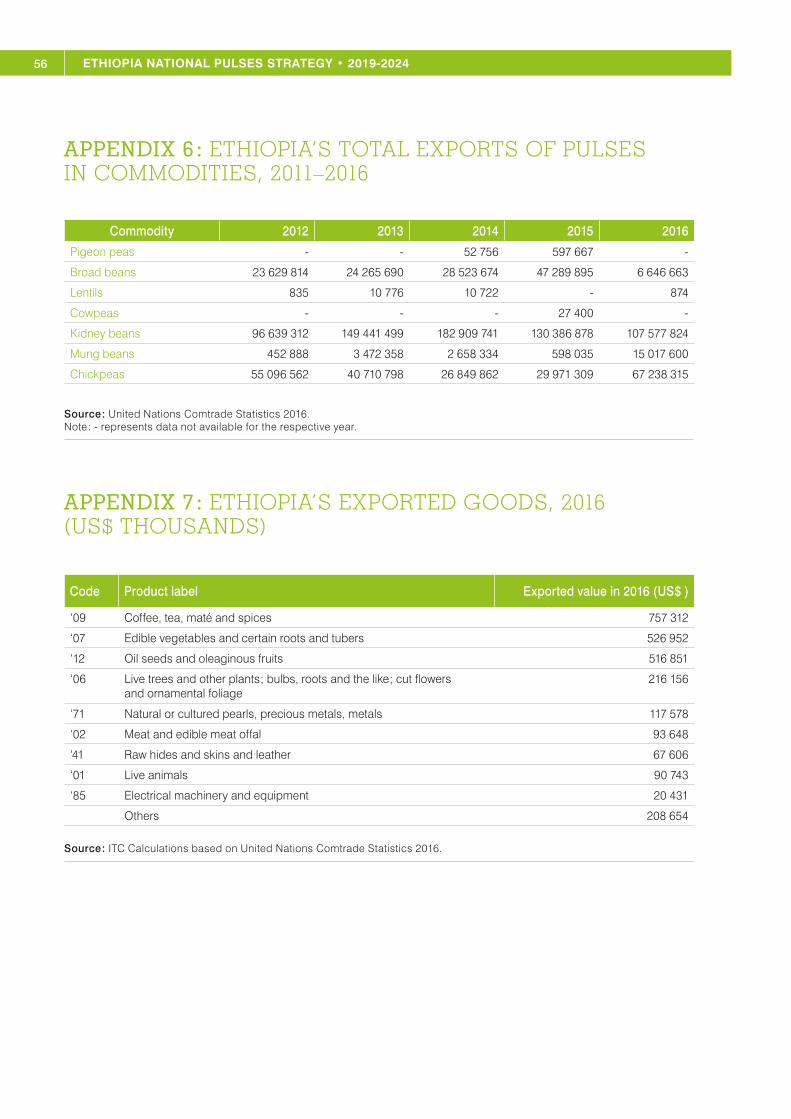

APPENDIX 6 : ETHIOPIA’S TOTAL EXPORTS OF PULSES IN COMMODITIES, 2011–2016 ( US $ THOUSANDS ) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

APPENDIX 7 : ETHIOPIA’S EXPORTED GOODS, 2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

APPENDIX 8 : SHARE OF PULSE CROPS IN GLOBAL EXPORTS IN 2016 . . . . . . . . . 57

APPENDIX 9 : EXPORTS OF PULSES BY REGION OR REGIONAL GROUP, 2007–2016 ( US $ THOUSANDS ) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

APPENDIX 10 : GLOBAL PULSE PRODUCTION BY VARIETY, 2016 . . . . . . . . . . . . . . . . 58

APPENDIX 11 : MAJOR PULSE PRODUCERS GLOBALLY, 2016 . . . . . . . . . . . . . . . . . . . 58

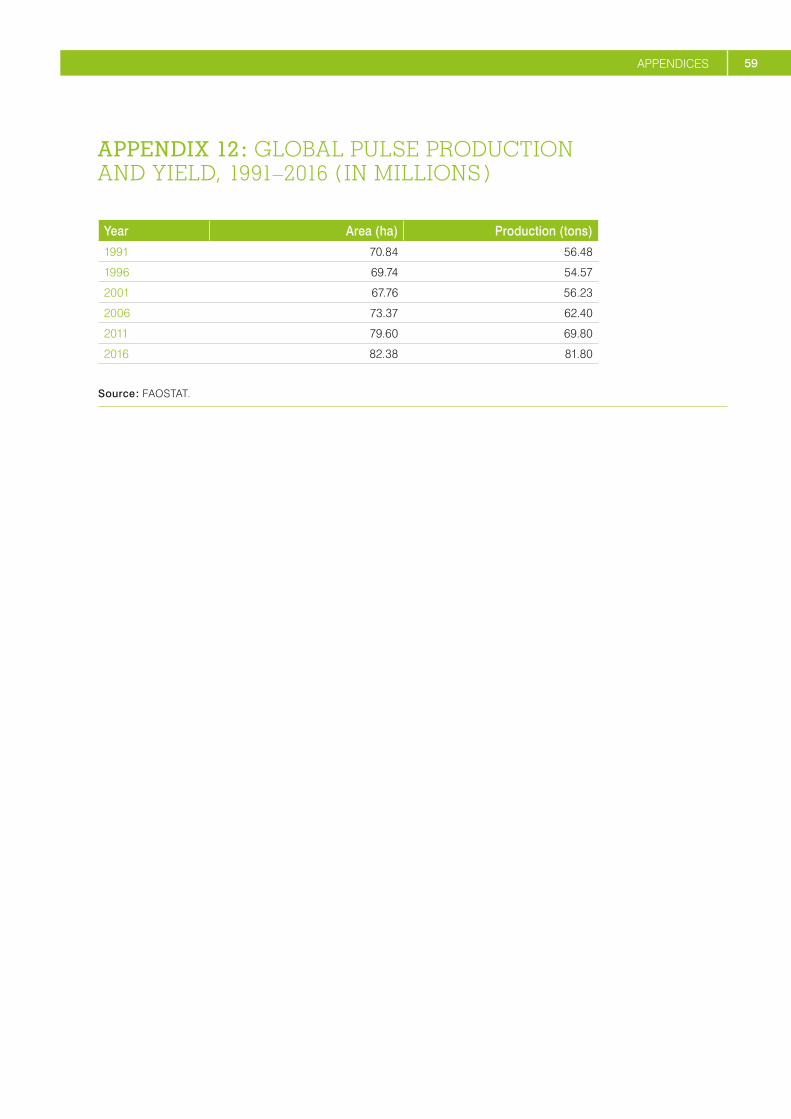

APPENDIX 12 : GLOBAL PULSE PRODUCTION AND YIELD, 1991–2016 ( IN MILLIONS ) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

REFERENCES 60

VIII ETHIOPIA NATIONAL PULSES STRATEGY 2019-2024

LIST OF FIGURES

Figure 1 : Profitability of growing cereals and pulses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Figure 2 : Average nitrogen fixation capacity of pulse species . . . . . . . . . . . . . . . . . . . . . 7

Figure 3 : Global pulses production and yield 1991–2016 ( millions of tons ) . . . . . . . . . 8

Figure 4 : Major global pulse producers, 2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Figure 5 : Global pulse production by variety, 2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Figure 6 : Share of pulse crops in global export in 2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

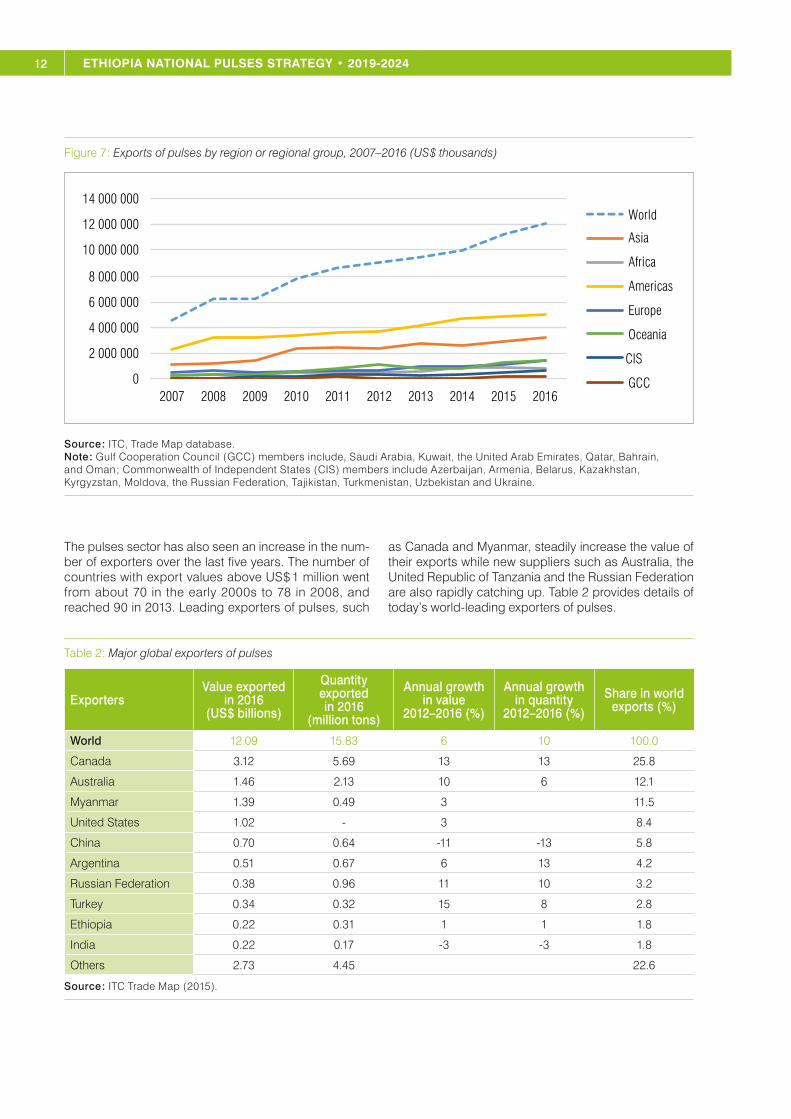

Figure 7 : Exports of pulses by region or regional group, 2007–2016 ( US $ thousands ) . 12

Figure 8 : Prioritized pulses and the criteria used . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Figure 9 : Production of pulses ( tons ) and relative share of specific crops in Ethiopia, 2011–2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Figure 10 : Distribution of pulse-growing areas in Ethiopia. . . . . . . . . . . . . . . . . . . . . . . . . 16

Figure 11 : Total area and production of different groups of crops in Ethiopia in 2016/17 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Figure 12 : Coverage of extension service and input use in pulses production, as compared with cereals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Figure 13 : Ethiopian exported goods in 2016 ( US $ millions ) . . . . . . . . . . . . . . . . . . . . . . . 19

Figure 14 : Ethiopia’s total pulses export in US $ million and tons, 2011–2016 . . . . . . . 19

Figure 15 : Proportion of pulses exported from Ethiopia, 2016 . . . . . . . . . . . . . . . . . . . . . . 20

Figure 16 : Largest destinations for Ethiopia’s pulse exports, 2016 ( US $ ) . . . . . . . . . . . 20

Figure 17 : Ethiopia’s most important export destinations in US $ million for pulses, 2016 21

Figure 18 : Ethiopia’s total exports of pulses in commodities, 2011–2016 ( US $ thousands ) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Figure 19 : Existing pulses value chain in Ethiopia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Figure 20 : Strategic objectives for the Ethiopian pulses sector . . . . . . . . . . . . . . . . . . . . 32

Figure 21 : The future value chain of the pulses sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

Figure 22 : Strategic objectives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

Figure 23 : Institutional framework for Ethiopian pulses sector development . . . . . . . . 43

IXETHIOPIA NATIONAL PULSES STRATEGY 2019-2024

TABLES

Table 1 : Major global importers of pulses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Table 2 : Major global exporters of pulses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Table 3 : Pulse production in Ethiopia by region, 2016 ( tons ) . . . . . . . . . . . . . . . . . . . . . . . 15

Table 4 : Ethiopian export earnings from pulses, 2012–2016 ( US $ thousands ) . . . . . . 22

Table 5 : Value chain segments needing FDI and likely sources . . . . . . . . . . . . . . . . . . . 41

BOXES

Box 1 : Overview of pulses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Box 2 : Import quotas on pulses in India . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Box 3 : Ethiopia’s product and market opportunities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

Box 4 : Support institutions in Ethiopia for the pulses sector . . . . . . . . . . . . . . . . . . . . . . . 38

Photo: (CC BY-SA 2.0)

XIETHIOPIA NATIONAL PULSES STRATEGY 2019-2024

ACRONYMS

ATA Ethiopian Agricultural Transformation Agency

BoA Bureau of Agriculture

CIS Commonwealth of Independent States

CSA Central Statistical Agency of Ethiopia

ECCSA Ethiopian Chamber of Commerce and Sectoral Associations

ECX Ethiopian Commodity Exchange

EIAR Ethiopian Institute of Agricultural Research

EIC Ethiopian Investment Commission

ENAO Ethiopian National Accreditation Office

EPOSPEA Ethiopian Pulses, Oilseeds and Spices Processors and Exporters’ Association

FAO Food and Agriculture Organization of the United Nations

FCA Federal Cooperative Agency

FDI Foreign direct investment

GAP Good Agricultural Practices

GCC Gulf Cooperation Council

GMP Good Management Practices

HS Harmonized System

ICT Information and communications technology

ITC International Trade Centre

MoANR Ministry of Agriculture and Natural Resources

MoFA Ministry of Foreign Affairs

MoFEC Ministry of Finance and Economic Cooperation

MoT Ministry of Trade

PoA Plan of Action

RARI Regional Agricultural Research Institute

SMEs Small and medium-sized enterprises

TVET Technical and vocational education and training

Photo: (CC BY-SA 2.0) Links, Green Lentils.

1EXECUTIVE SUMMARY

EXECUTIVE SUMMARY

The pulses sector in Ethiopia has the potential to be a key accelerator of agricultural development and growth. It plays a valuable role not only in boosting export earn-ings but also in enhancing the rural economy and social development. Pulses are pro-poor crops with a unique combination of benefits including rich nutritional value, high income-generation potential and the ability to con-vert atmospheric nitrogen into a usable form to improve soil fertility.

Pulses are strategically important to Ethiopia, as they are the third agricultural export commodity after coffee and oilseeds, and play a vital role in the country’s economy. In this Strategy, the following pulses are focused upon, listed under their appropriate Harmonized System ( HS ) codes from the World Customs Organization.

HS chapter HS 6-digit product code

HS 0713 : Dried leguminous vegetables, shelled, whether or not skinned or split

HS 071320 : Chickpeas ( garbanzos ), dried shelled, including seed

HS 071331 : Beans ( Vigna Mungo ( L. ), Hepper etc. ), dried shelled

HS 071310 : Peas, dried shelled, including seed

HS 071332 : Beans, small red ( adzuki ), dried shelled, including seed

HS 071333 : Kidney beans & white pea beans, dried shelled, including seed

HS 071334 : Bambara beans, dried, shelled

HS 071335 : Cowpeas, dried, shelled

HS 071339 : Beans Nesoi, dried shelled, including seed

HS 071340 : Lentils, dried shelled, including seed

HS 071350 : Broad beans & horse beans, dried shelled, including seed

HS 071360 : Pigeon peas, dried, shelled

HS 071390 : Leguminous vegetables, dried shelled, including seed

Photo: (CC BY-SA 2.0) DFID - UK Department for International Development

2 ETHIOPIA NATIONAL PULSES STRATEGY • 2019-2024

Globally, the volume of pulse production has increased gradually over the last 25 years, from 56.48 million tons in 1991 to 81.80 million tons in 2016. The largest markets for food pulses are in India, Bangladesh, Pakistan and Sri Lanka, while the largest market for animal feed pulses is the European Union. Five subsectors of pulses ( peas, kidney beans, chickpeas, lentils and gram beans ) ac-count for four-fifths of the market share of all traded pulses.

In Ethiopia, broad beans account for the greatest portion of production ( 32.12 % ), followed by dry beans ( 17.7 % ), chickpeas ( 16.25 % ), dry peas/field peas ( 12.74 % ), vetch-es/grass peas ( 10.87 % ) and lentils ( 6.8 % ). Most pulse production is concentrated in Amhara and Oromia re-gions, which together account for 87 % of the produc-tion of broad beans, 95 % of chickpeas, 77 % of common beans, 78 % of field peas and 93 % of lentils.

Despite being Ethiopia’s third commodity export, there has been low investment in pulse research compared with that for cereals, both by the Government and donors. Similarly, pulse initiatives have been given less priority. From a world market point of view, Ethiopia’s pulse ex-ports represent 3 % of world pulse exports.

According to 2016 data ( the most recent available ), the most important export destinations for pulses are Pakistan, India, Indonesia and Viet Nam. Pulses ac-counted for 6.93 % of export earnings in Ethiopia, and contributed more than US $ 248 million to the country’s hard currency reserves in 2016. In the last five years, the growth in exports in value has been 16 % annually, with broad beans representing the bulk of this growth. At present, pulses account for 13 % of the cropped land in Ethiopia. In terms of area, pulses are second in area cov-erage and production in Ethiopia after cereals, with over 1.5 million hectares and 2.67 million tons of production.

For the pulses sector to continue to add value and inten-sify market development, public and private industry rep-resentatives identified the following as the most pressing issues that should be addressed rapidly :

• Limited use of quality inputs ;• Extension services are not effective ;• Low farm productivity ;• Limited knowledge of value addition practices ;• Technology for mechanization for value addition is either

out of date or unknown ;• Poor sourcing practices ;• Postharvest losses and quality degradation during

storage and processing ;• Promotion to attract foreign direct investment ( FDI ) to the

sector is limited ;• Implementation of standards and codes of conduct at

production and processing levels ;• Limited links between the public and private sectors ;

• Poor dissemination of trade information, and limited promotion and inadequate brand promotion of pulses in destination markets ;

• Limited use of contract farming methods between producers, processors and exporters ;

• Limited postharvest storage infrastructure, leading to high postharvest losses ;

• Low technology and mechanization adoption ;• Limited branding and trade promotion capacities ;• Infrastructure for quality management is insufficient ;• Expensive and unreliable transportation network.

MARKET ORIENTATION

Based on global trends in the growing pulses sector, Ethiopia should set the following priorities, with short-, medium- and long-term goals. Short-term is defined as immediately to one year, medium-term as one to three years, and long-term is beyond three years.

Short-term goals :

� Continue concentrating on South Asia for trade and investments.

� Promote cooperation with overseas pulse organiza-tions to learn best practices and develop partnerships.

� Introduce a ‘national business code of conduct’ for pulse exporters.

Medium-term goals :

� Move towards value added products. � Incentivize investments.

Long-term goals :

� Establish a traceability and certification system for pulse products. This will enable organic farming.

THE WAY FORWARD

The pulses sector has significant potential to make so-cioeconomic contributions to Ethiopia through export-led growth. To realize this potential, competitive constraints and structural deficiencies must be addressed, and iden-tified opportunities should be leveraged. The following is a delineation of the proposed vision and strategic approach in this direction.

All stakeholders of the pulses sector value chain in Ethiopia agreed on the following vision statement.

3EXECUTIVE SUMMARY

‘Be a globally competitive exporter of high-quality pulses

through adoption of innovative technologies that support Ethiopian development and increase smallholders’ income.

’Strategic objectives

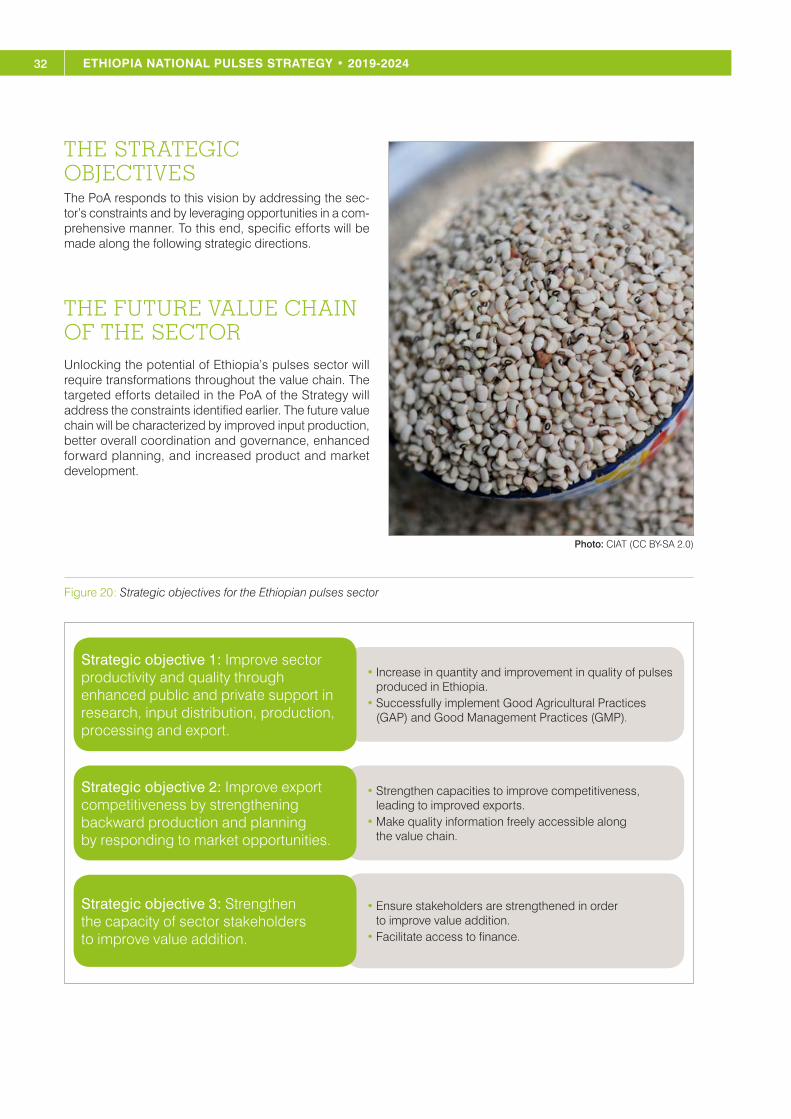

The Plan of Action ( PoA ) will respond to this vision by addressing the sector’s constraints and leveraging op-portunities in a comprehensive manner. To this end, spe-cific efforts will be made to meet the following strategic objectives.

Coordinating activities, monitoring progress, increasing institutional capacities and mobilizing resources for im-plementation will be critical to successful achievement

of these targets. Industry representatives recommended that a ‘national pulses network’ be rapidly established, operationalized and empowered. This advisory commit-tee is to be responsible for overall coordination, provision of policy guidance and monitoring industry development against the strategic objectives. An effectively organized and supported committee can plan industry development strategically. High-level support from the Government, in collaboration with strong championship by the private sector, will be the real drivers to transform Ethiopia into a global pulses destination.

• Increase in quantity and improvement in quality of pulses produced in Ethiopia.

• Successfully implement Good Agricultural Practices (GAP) and Good Management Practices (GMP).

Strategic objective 1: Improve sector productivity and quality through enhanced public and private support in research, input distribution, production, processing and export.

• Strengthen capacities to improve competitiveness, leading to improved exports.

• Make quality information freely accessible along the value chain.

Strategic objective 2: Improve export competitiveness by strengthening backward production and planning by responding to market opportunities.

• Ensure stakeholders are strengthened in order to improve value addition.

• Facilitate access to finance.

Strategic objective 3: Strengthen the capacity of sector stakeholders to improve value addition.

Photo: (CC BY-SA 2.0) Swathi Sridharan, Market in Addis Ababa.

5THE IMPORTANCE OF PULSES

THE IMPORTANCE OF PULSES

The Ministry of Agriculture and Natural Resources ( MoANR ) has mandated the Ethiopian Agricultural Transformation Agency ( ATA ) to develop a harmonized “National Pulses Strategy.” To achieve this task, national public and private stakeholders collaborated to identify systemic bottlenecks along the pulses value chain and propose long-term strategic interventions to strengthen

the sector. These interventions are intended to guide the trade development of the pulses sector in a coordinated way, with the objective of bringing about holistic transfor-mation across the value chain. This Strategy will be im-plemented under a 5-year time frame, from 2019 to 2024, and will be updated and refined by national stakeholders as sector development evolves.

Box 1 : Overview of pulses

The Food and Agriculture Organization of the United Nations ( FAO ) has identified pulses as a subgroup of legumes, crop plant members of the Leguminosae family that produce edible dry mature seeds which are used for human and animal consumption. Only legumes harvested for dry grain are classified as pulses. For example, grain legumes used mainly for oil production, such as soybean and peanuts, are not considered pulses. Likewise, legumes used for sowing purposes ( such as clovers and alfalfa ) or as vegetables ( like green beans and green peas ) are not considered pulses. Pulses include dry beans, dry peas, dry broad beans, chickpeas, lentils, cow peas, pigeon peas, lupins and vetches.

From an agricultural point of view, multiple cropping systems that include pulses enhance soil fertility, improve yields and contribute to a more sustainable food system. Importantly, pulses have a very low water footprint compared with other protein sources and can be grown in very poor soils where other crops cannot be cultivated. Crop residues of pulses, and legumes in general, can also be used as animal fodder, thus increasing the quality of the animal diet.

From a health perspective, pulses are very high in protein and fibre, are low in fat and are a vital source of proteins and amino acids for humans. They also contain significant amounts of other essential nutrients like calcium, iron and lysine. Pulses can help lower blood cholesterol and attenuate blood glucose, which is a key factor in fighting diabetes and cardiovascular disease. In a study published by the International Journal of Multidisciplinary in 2016, doctors found that a dietary pulse intake significantly reduces low-density lipoprotein cholesterol levels, another study conducted in 2015 demonstrated that increased consumption of pulses decreases the risk of colorectal cancer.1 In fact, pulses are a large part of many countries’ traditional diets and are the main protein source for lower-income people worldwide. Pulses are a key ingredient in the average Ethiopian diet and an important source of protein.

Pulses can play an important role in climate change adaptation, since they have a broad genetic diversity from which climate-resilient varieties can be selected and/or bred. They play a diverse role in the farming systems of many developing countries, including as a food crop ( consumed as grain, green pods and leaves ) ; a cash crop ( which would be a higher source of income ) ; a fodder crop ( contributing to the productivity of the livestock system ) ; importantly, as a rotation crop, intercropped with cereals and roots/tubers ( reduces soil pathogens and provides nitrogen ) ; and finally they can grow in harsh environments such as in drought-prone areas where there are few options ( food security ).

6 ETHIOPIA NATIONAL PULSES STRATEGY • 2019-2024

In Ethiopia, pulses have the potential to increase incomes for smallholders. Pulses are generally more profitable than cereals, giving smallholders an economic incentive to in-crease pulse production ( see figure 1 ). Broad bean gives up to 77 % higher profit than wheat and up to six times more profit than barley. Similarly, chickpea gives up to 20 % higher profit compared with teff, four times higher compared with barley, and comparable returns to wheat.1 There is also significant untapped potential for pulses in domestic and international markets. Demand for most pulse imports is expected to increase in many destina-tion markets, particularly in Asia, where domestic pro-duction is expected to fall short of demand. Ethiopia has the potential to capitalize on the competitive advantage of geographic proximity to major export markets relative to other pulses exporters, and move towards supplying premium-quality grains and processed products to high-value markets.

1. Government of Ethiopia ( 2015 ). National Pulses Value Chain Development Strategy of Ethiopia ( Working Document 2016-2020 ). Addis Ababa. Available from https ://www.agriknowledge.org/downloads/nc580m674.

Pulses improve soil fertility and enhance ecosystem re-silience : When associated with the right strain of rhizo-bium bacteria ( biofertilizer ), pulses can fix up to 200kg of atmospheric nitrogen per hectare, equivalent to 0.4 tons of urea fertilizer. Further, the root system of pulses can go as deep as 2 metres and break the different layers of the soil, thus improving the structure of the soil and water infiltration, and nutrient recycling. Growing pulses and cereals alternately on the same land reduces the spread of diseases, insect pests and weeds.

Pulses are a source of high-quality animal feed : Globally, up to 25 % of pulses are used as feedstuff, particularly for pigs and poultry. Three main areas of current use globally are pet food, aquaculture, and traditional livestock diets, including for poultry, swine and cattle. In Ethiopia, pulse residues play an important role in the nutrition of livestock, supplying up to 12 tons/ha of residues with crude protein content of 8–14 %.2

2. Keftasa, Daniel ( 1988 ). Role of Crop Residues as Livestock Feed in Ethiopian Highlands. In African Forage Plant Genetic Resources, Evaluation of Forage Germplasm and Extensive Livestock Production Systems : Proceedings of the Third Workshop held at the International Conference Center Arusha, Tanzania, 27–30 April, 1987, B.H. Dwozela, ed. Addis Ababa : Pasture Network for Eastern and Southern Africa.

Figure 1 : Profitability of growing cereals and pulses

Source : FAO ( 2014 ).

7THE IMPORTANCE OF PULSES

Figure 2 : Average nitrogen fixation capacity of pulse species

Source : Zapata, F. and others ( 1987 ).

The importance of pulses, as outlined above, makes them ideal crops for simultaneously achieving three de-velopmental goals – reducing poverty, improving human health and nutrition, and enhancing ecosystem resil-ience. Because of their versatility and nutritional value, the global market for pulses is large and rapidly increas-ing. Indeed, the FAO and its Member States declared 2016 the ‘International Year of Pulses.’

With over 2 million hectares under cultivation and 3.2 mil-lion tons in annual production, and cultivated by over 9 million rural households ( Central Statistical Agency of Ethiopia ( CSA ), 2016 ), pulses are pro-poor crops that have high potential for improving the livelihoods of the rural poor in Ethiopia. To lead the transformation of the agricultural sector, pulses have been selected as one of the priority value chains in Ethiopia’s second five-year Growth and Transformation Plan target ( to double the 2014 yield by 2020 ).

Photo: pixabay, Image by Vijaya narasimha from Pixabay. Photo: pixabay, Image by alexdante from Pixabay.

8 ETHIOPIA NATIONAL PULSES STRATEGY • 2019-2024

GLOBAL TRENDS IN PULSES

Pulses represent a global industry worth over US $ 100 billion at the retail level, underpinned by 81 million tons of production which is exported to over 55 countries.

Rising income levels, along with population growth and an increase in middle-income classes in developing coun-tries, have increased demand for foodstuffs, including pulses. Some econometric studies estimate the range of demand elasticities for pulses to be between 1.5 and 2.3 This indicates that an annual increase in per capita in-come of around 6 % would lead to an increased demand of more than 10 % for pulses.4 The growth of middle-in-come classes in non-traditional markets such as those in Africa and Asia, and the rise of a supermarket culture in developing countries have led to increased demand for processed foods, which also drives increased demand for pulses, especially pigeon peas, chickpeas and dry peas.

3. Knight, R., ed. ( 2000 ). Linking Research and Market Opportunities for Pulses in the 21st Century : Proceedings of the Third International Food Legumes Research Conference. Springer Publishing.4. Alagh, Y.K. ( 2011 ). Future of Indian Agriculture. Indian Economic Journal, vol. 59, No. 1, April–June, pp. 40–55.

Change in dietary patterns is another key driver of in-creased demand for pulses. With greater awareness of coeliac disease and gluten sensitivity, demand is rising for pulses such as yellow peas, lentils and chickpeas, which are some of the best available gluten-free options. Pulses have now gained acceptance as the ‘new and improved’ centre of healthy eating.

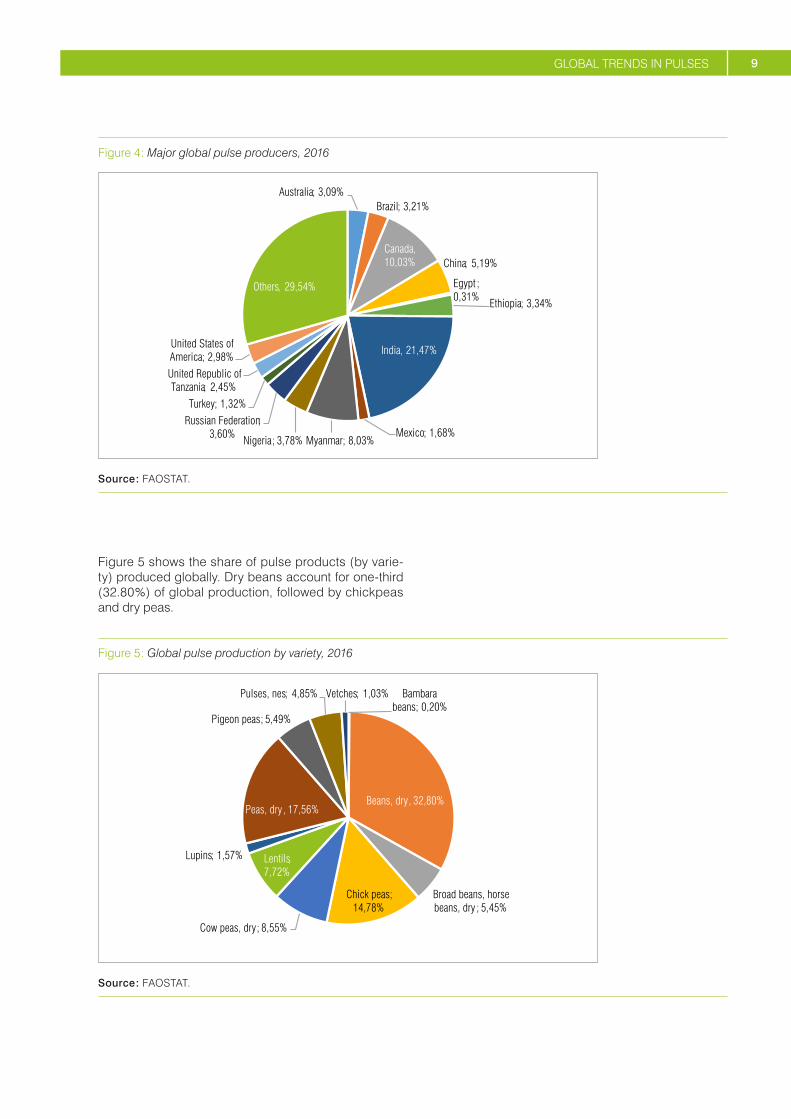

PRODUCTION TRENDS OF PULSESThe global volume of pulses production has increased gradually in the last 25 years, from 56.48 million tons in 1991 to 81.80 million tons in 2016. The world produc-tion of pulses is dominated by a few countries which in-clude India ( 21.47 % ), Canada ( 10.03 % ), China ( 5.19 % ), Myanmar ( 8.03 % ) and Nigeria ( 3.78 % ), which together account for more than half of the world’s output. African-origin pulses have gained significant importance in re-cent years.

Figure 3 : Global pulses production and yield 1991–2016 ( millions of tons )

56,48 54,57 56,2362,4

69,8

81,8

0

10

20

30

40

50

60

70

80

90

1991 1996 2001 2006 2011 2016

Production (tons) Area (ha)

Source : FAOSTAT.

9GLOBAL TRENDS IN PULSES

Figure 4 : Major global pulse producers, 2016

Australia; 3,09%Brazil; 3,21%

Canada, 10,03% China; 5,19%

Egypt ; 0,31%

Ethiopia; 3,34%

India, 21,47%

Mexico; 1,68%Myanmar; 8,03%Nigeria; 3,78%

Russian Federation; 3,60%

Turkey; 1,32%

United Republic of Tanzania; 2,45%

United States of America; 2,98%

Others, 29,54%

Source : FAOSTAT.

Figure 5 shows the share of pulse products ( by varie-ty ) produced globally. Dry beans account for one-third ( 32.80 % ) of global production, followed by chickpeas and dry peas.

Figure 5 : Global pulse production by variety, 2016

Bambara beans; 0,20%

Beans, dry, 32,80%

Broad beans, horse beans, dry ; 5,45%

Chick peas; 14,78%

Cow peas, dry; 8,55%

Lentils, 7,72%

Lupins; 1,57%

Peas, dry , 17,56%

Pigeon peas; 5,49%

Pulses, nes; 4,85% Vetches; 1,03%

Source : FAOSTAT.

10 ETHIOPIA NATIONAL PULSES STRATEGY • 2019-2024

TRADE TRENDS OF PULSESThe global trade in pulses accounts for 7.88 % of global production, with 92.12 % of production consumed local-ly.5 Still, the global trade in pulses is not a residual mar-ket, as several countries produce pulses for export, while many others rely on the world market to meet domestic demand. Since 1961, global trade in pulses has expanded by an average of 5.5 % per annum, reaching a volume of 17.2 million tons in 2016.6

Global consumption of pulses can be categorized into two major markets. One concerns the demand driven by human consumption, and the second by the alternate use of pulses for animal feed. Traditionally, low-quality, cheap pulses have been consumed as animal feed. In addition, there is some minor use of pulses in non-food sectors, including seeding and wastage. It can be safely assumed that there is limited variation in stocks from year to year, and that the non-food uses of pulses are a small percentage of total production. As a result, global con-sumption is more or less equal to global production. The largest markets for food pulses are in India, Bangladesh,

5. Calculations based on United Nations Comtrade and FAOSTAT ( 2016 ). The production quantity figures available from FAOSTAT are Bambara beans, beans ( dry ), broad beans, chickpeas, cowpeas, lentils and pulses n.e.s.6. FAOSTAT estimate ( 2016 ).

Pakistan and Sri Lanka, while the largest market for animal feed pulses is the European Union.7

Five subsectors of pulses ( peas, kidney beans, chick-peas, lentils and gram beans ) account for four-fifths of the market share of all traded pulses. Figure 6 shows the main prod ucts which are imported within the pulses sector. The most exported products are dried peas, which account for almost a quarter of global pulse imports ( with India being the high est importer at 41.9 % in terms of value ).

7. FAO ( 2002 ). Agricultural Commodities : Profiles and Relevant WTO Negotiating Issues. Available from www.fao.org/docrep/006/y4343e/y4343e02.htm.

Figure 6 : Share of pulse crops in global export in 2016

Dried peas22,77%

Dried chickpeas14,85%

Dried beans12,15%

Dried red 'adzuki' beans1,11%

Dried kidney beans14,39%Dried bambara beans

0,03%

Dried cow peas0,21%

Dried beans3,08%

Dried lentils22,89%

Dried broad beans and horse beans/ faba

beans3,70%

Dried pigeon peas2,18%

Dried leguminous vegetables

2,64%

Source : ITC calculations based on United Nations Comtrade statistics.

Photo: (CC BY-SA 2.0) by PDPics from Pixabay.

11GLOBAL TRENDS IN PULSES

MAJOR IMPORTERS OF PULSESIndia has been by far the largest importer of pulses over the past decade and accounts for about 31.5 % of world imports. Specifically, India’s imports increased from US $ 1.459 billion in 2008 to US $ 4.017 billion in 2016. The high demand for pulses in India is mostly due to its vegetarian population, the increase of purchasing pow-er across its poorest population and unfavourable local weather conditions.8

8. Reddy, A. Amarender, Bantilan, M.C.S. and Mohan, Geetha ( 2013 ) Pulses Production Scenario : Policy and Technological Options ( Policy Brief No. 26 ). Patancheru, Andhra Pradesh, India : International Crops Research Institute for the Semi-Arid Tropics,..Available from http ://oar.icrisat.org/6812/1/26_Policy_BriefIndia %20_2013.pdf.

Another country that has shown an impressive rise of de-mand for pulses during the past five years is China. Its share has risen from a 2 % average for 2008–2009 to a 6 % average for 2012–2013.9 In fact, due to its growing use of dry pea protein to enrich vermicelli noodles and the coun-try’s slow expansion of pulse production, China is likely to change from being a net exporter to a net importer of pulses. It may also overtake India as the number one im-porter of yellow peas in the near future.

9. Ibid.

Table 1 : Major global importers of pulses

Importers

Value imported in 2016

( US $ billions )

Quantity imported in 2016

( million tons )

Annual growth in value

2012–2016 ( % )

Annual growth in quantity

2012–2016 ( % )

Share in world imports ( % )

World 12.74 16.78 6 8 100.0

India 4.02 6.18 17 14 31.5

Pakistan 0.70 0.89 18 15 5.5

Bangladesh 0.48 0.85 13 11 3.8

United Arab Emirates 0.43 0.48 16 10 3.4

China 0.42 1.07 -10 7 3.3

United States of America 0.39 - -4 3.1

Egypt 0.38 0.43 -2 1 3.0

Turkey 0.38 0.47 16 15 3.0

Brazil 0.33 0.41 -8 -4 2.6

Italy 0.26 0.31 -1 3 2.0

Others 4.94 5.68 38.8

Source : ITC calculations based on United Nations Comtrade statistics.

MAJOR EXPORTERS OF PULSESIn the past three decades, there has been impressive growth in the global exports of pulses. The compound an-nual growth rate between 2007 and 2016 was 10.1 %.10 By 2016, pulse exports reached a record high of US $ 12.091 billion.

10. Calculations based on United Nations Comtrade data for 2007–2016. Photo: (CC BY 2.0) pixabay, “seeds dried” by Rachel Tayse

12 ETHIOPIA NATIONAL PULSES STRATEGY • 2019-2024

Figure 7 : Exports of pulses by region or regional group, 2007–2016 ( US $ thousands )

0

2 000 000

4 000 000

6 000 000

8 000 000

10 000 000

12 000 000

14 000 000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

World

Asia

Africa

Americas

Europe

Oceania

CIS

GCC

Source : ITC, Trade Map database. Note : Gulf Cooperation Council ( GCC ) members include, Saudi Arabia, Kuwait, the United Arab Emirates, Qatar, Bahrain, and Oman ; Commonwealth of Independent States ( CIS ) members include Azerbaijan, Armenia, Belarus, Kazakhstan, Kyrgyzstan, Moldova, the Russian Federation, Tajikistan, Turkmenistan, Uzbekistan and Ukraine.

The pulses sector has also seen an increase in the num-ber of exporters over the last five years. The number of countries with export values above US $ 1 million went from about 70 in the early 2000s to 78 in 2008, and reached 90 in 2013. Leading exporters of pulses, such

as Canada and Myanmar, steadily increase the value of their exports while new suppliers such as Australia, the United Republic of Tanzania and the Russian Federation are also rapidly catching up. Table 2 provides details of today’s world-leading exporters of pulses.

Table 2 : Major global exporters of pulses

ExportersValue exported

in 2016 ( US $ billions )

Quantity exported in 2016

( million tons )

Annual growth in value

2012–2016 ( % )

Annual growth in quantity

2012–2016 ( % )

Share in world exports ( % )

World 12.09 15.83 6 10 100.0

Canada 3.12 5.69 13 13 25.8

Australia 1.46 2.13 10 6 12.1

Myanmar 1.39 0.49 3 11.5

United States 1.02 - 3 8.4

China 0.70 0.64 -11 -13 5.8

Argentina 0.51 0.67 6 13 4.2

Russian Federation 0.38 0.96 11 10 3.2

Turkey 0.34 0.32 15 8 2.8

Ethiopia 0.22 0.31 1 1 1.8

India 0.22 0.17 -3 -3 1.8

Others 2.73 4.45 22.6

Source : ITC Trade Map ( 2015 ).

13GLOBAL TRENDS IN PULSES

Box 2 : Import quotas on pulses in India

The Indian government has tightened norms for the import of pulses to ensure that its domestic prices do not fall below the minimum support price. The prices of most pulses have been below the minimum support price levels, leading to farmer unrest in the main pulse-growing areas.

Processors and traders have demanded that the government stop even restricted imports by the end of March 2019. India has imposed a quota of 5 million tons on annual imports of pulses which, if not terminated, will add to the already mounting stocks in the country. Domestic prices of most pulses such as pigeon pea, green gram and Bengal gram are below the minimum support price.

In August 2017, the Government restricted imports of pigeon peas, green gram and black gram. The free import of these varieties has been restricted by imposing a quota of 2 million tons on pigeon peas and 3 million tons on green gram and black gram taken together, except if imported by millers. In May 2018, the Government imposed an import cap on split and milled dal as well. Exporting pulses, which was not allowed for more than a decade, was also freed up in 2017. However, domestic prices have improved very little. Then the government fixed the quantity for imports to millers at 150,000 tons each of black gram and green gram along with 200,000 tons of pigeon peas, including split and other forms. According to government estimates, India imported 4.7 million tons of pulses between April 2017 and November 2017, which is 71 % of what the country imported during the 2016/17 fiscal year and 80.8 % of what it imported in the 2015/16 fiscal year.

For more information on import quotas in India please see : Madhvi Sally ( 2018 ). Government tightens norms for import of pulses, Economic Times, 14 May. Available from: https ://economictimes.indiatimes.com/markets/commodities/news/government-tightens-norms-for-import-of-pulses/articleshow/64155924.cms.

Photo: (CC BY-SA 2.0) Swathi Sridharan, Securing incomes for women in Ethiopia.

14 ETHIOPIA NATIONAL PULSES STRATEGY • 2019-2024

ETHIOPIA’S PULSES SECTOR

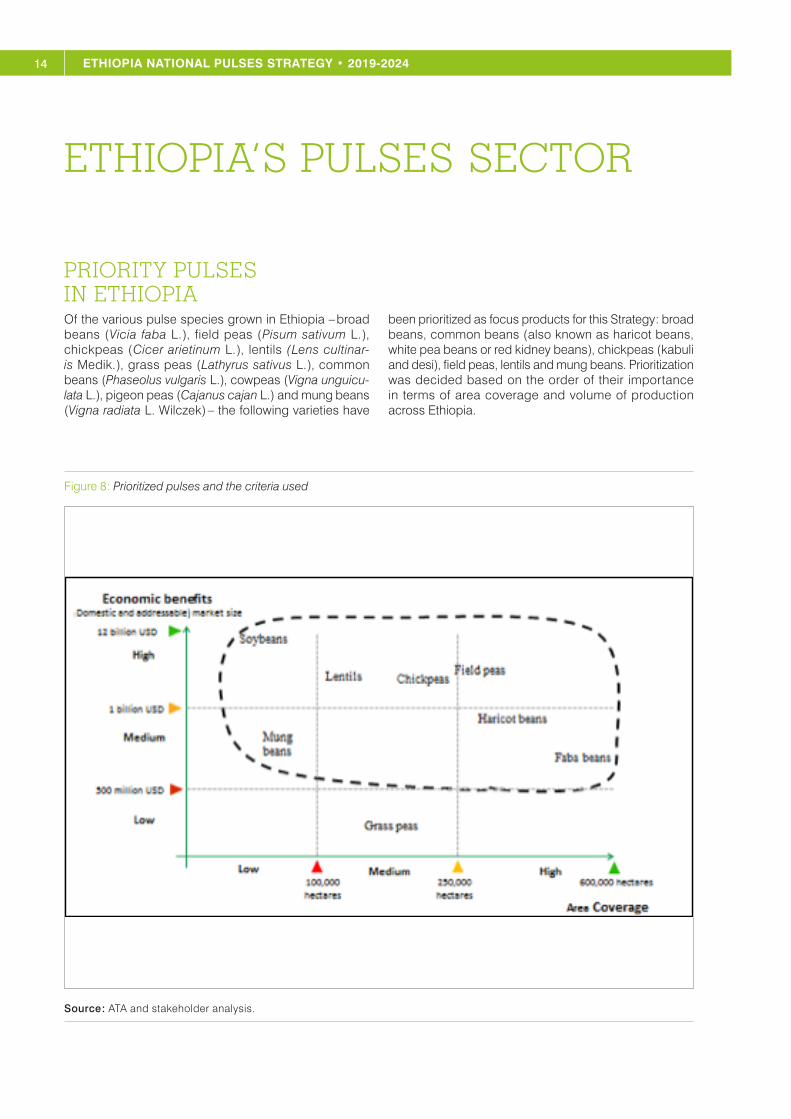

PRIORITY PULSES IN ETHIOPIAOf the various pulse species grown in Ethiopia – broad beans ( Vicia faba L. ), field peas ( Pisum sativum L. ), chickpeas ( Cicer arietinum L. ), lentils ( Lens cultinar-is Medik. ), grass peas ( Lathyrus sativus L. ), common beans ( Phaseolus vulgaris L. ), cowpeas ( Vigna unguicu-lata L. ), pigeon peas ( Cajanus cajan L. ) and mung beans ( Vigna radiata L. Wilczek ) – the following varieties have

been prioritized as focus products for this Strategy : broad beans, common beans ( also known as haricot beans, white pea beans or red kidney beans ), chickpeas ( kabuli and desi ), field peas, lentils and mung beans. Prioritization was decided based on the order of their importance in terms of area coverage and volume of production across Ethiopia.

Figure 8 : Prioritized pulses and the criteria used

Source : ATA and stakeholder analysis.

15ETHIOPIA’S PULSES SECTOR

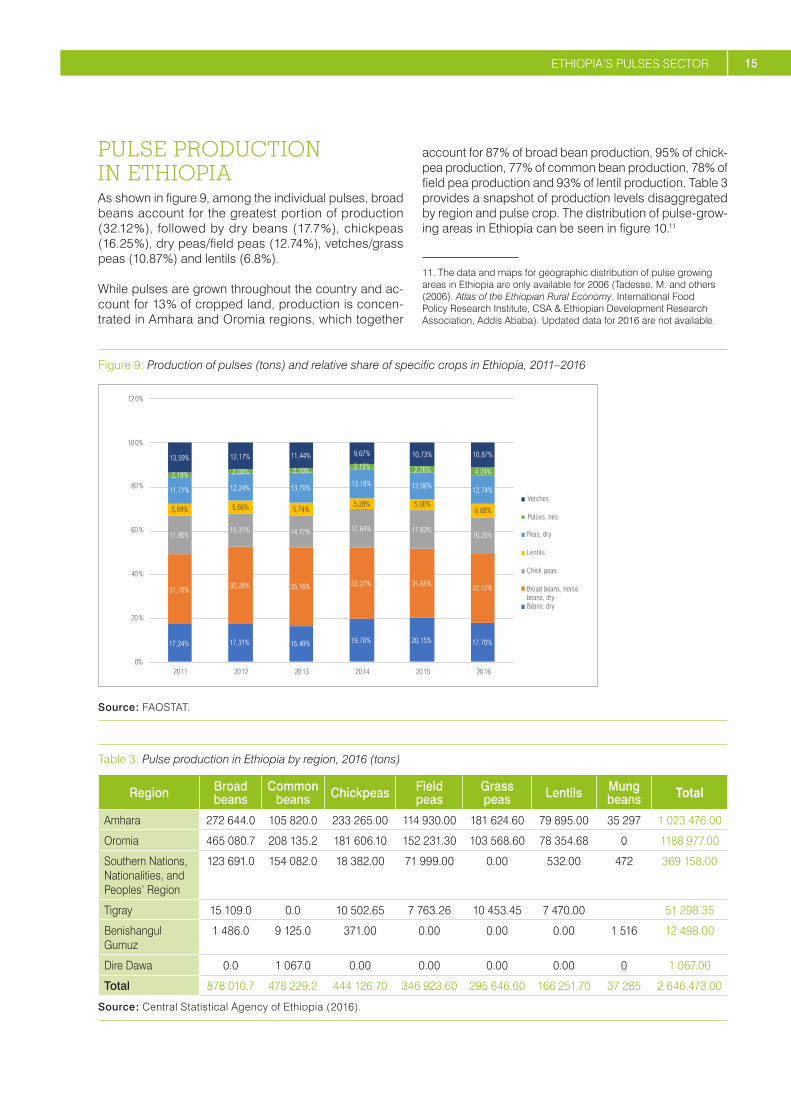

PULSE PRODUCTION IN ETHIOPIAAs shown in figure 9, among the individual pulses, broad beans account for the greatest portion of production ( 32.12 % ), followed by dry beans ( 17.7 % ), chickpeas ( 16.25 % ), dry peas/field peas ( 12.74 % ), vetches/grass peas ( 10.87 % ) and lentils ( 6.8 % ).

While pulses are grown throughout the country and ac-count for 13 % of cropped land, production is concen-trated in Amhara and Oromia regions, which together

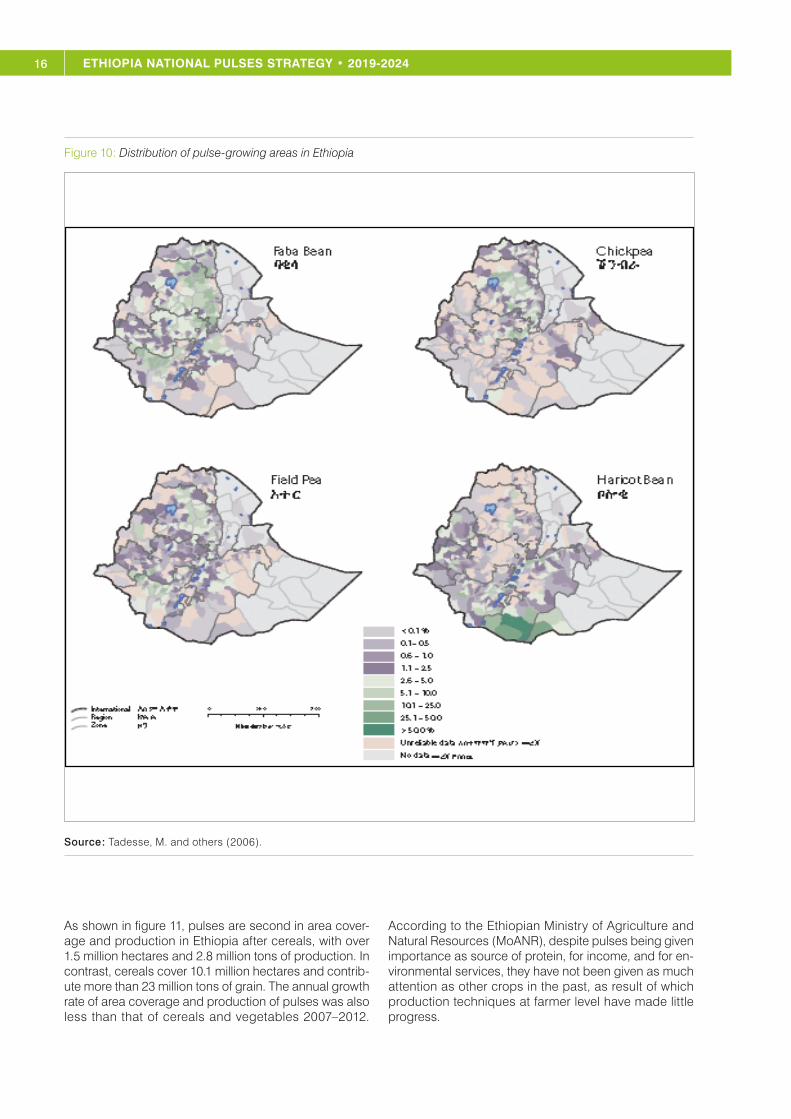

account for 87 % of broad bean production, 95 % of chick-pea production, 77 % of common bean production, 78 % of field pea production and 93 % of lentil production. Table 3 provides a snapshot of production levels disaggregated by region and pulse crop. The distribution of pulse-grow-ing areas in Ethiopia can be seen in figure 10.11

11. The data and maps for geographic distribution of pulse growing areas in Ethiopia are only available for 2006 ( Tadesse, M. and others ( 2006 ). Atlas of the Ethiopian Rural Economy. International Food Policy Research Institute, CSA & Ethiopian Development Research Association, Addis Ababa ). Updated data for 2016 are not available.

Figure 9 : Production of pulses ( tons ) and relative share of specific crops in Ethiopia, 2011–2016

17,24% 17,31% 16,49% 19,76% 20,15% 17,70%

31,78% 35,28% 35,76% 32,27% 31,66% 32,12%

17,80%15,31% 14,77% 17,64% 17,63%

16,25%

5,69% 5,66% 5,74%5,28% 5,00%

6,08%

11,71% 12,24% 13,70% 13,18% 12,06% 12,74%

2,19% 2,03% 2,10% 2,19% 2,76% 4,24%

13,59% 12,17% 11,44% 9,67% 10,73% 10,87%

0%

20%

40%

60%

80%

100%

120%

2011 2012 2013 2014 2015 2016

Vetches

Pulses, nes

Peas, dry

Lentils

Chick peas

Broad beans, horsebeans, dryBeans, dry

Source : FAOSTAT.

Table 3 : Pulse production in Ethiopia by region, 2016 ( tons )

Region Broad beans

Common beans Chickpeas Field

peasGrass peas Lentils Mung

beans Total

Amhara 272 644.0 105 820.0 233 265.00 114 930.00 181 624.60 79 895.00 35 297 1 023 476.00

Oromia 465 080.7 208 135.2 181 606.10 152 231.30 103 568.60 78 354.68 0 1188 977.00

Southern Nations, Nationalities, and Peoples’ Region

123 691.0 154 082.0 18 382.00 71 999.00 0.00 532.00 472 369 158.00

Tigray 15 109.0 0.0 10 502.65 7 763.26 10 453.45 7 470.00 51 298.35

Benishangul Gumuz

1 486.0 9 125.0 371.00 0.00 0.00 0.00 1 516 12 498.00

Dire Dawa 0.0 1 067.0 0.00 0.00 0.00 0.00 0 1 067.00

Total 878 010.7 478 229.2 444 126.70 346 923.60 295 646.60 166 251.70 37 285 2 646 473.00

Source : Central Statistical Agency of Ethiopia ( 2016 ).

16 ETHIOPIA NATIONAL PULSES STRATEGY • 2019-2024

Figure 10 : Distribution of pulse-growing areas in Ethiopia

Source : Tadesse, M. and others ( 2006 ).

As shown in figure 11, pulses are second in area cover-age and production in Ethiopia after cereals, with over 1.5 million hectares and 2.8 million tons of production. In contrast, cereals cover 10.1 million hectares and contrib-ute more than 23 million tons of grain. The annual growth rate of area coverage and production of pulses was also less than that of cereals and vegetables 2007–2012.

According to the Ethiopian Ministry of Agriculture and Natural Resources ( MoANR ), despite pulses being given importance as source of protein, for income, and for en-vironmental services, they have not been given as much attention as other crops in the past, as result of which production techniques at farmer level have made little progress.

17ETHIOPIA’S PULSES SECTOR

Figure 11 : Total area and production of different groups of crops in Ethiopia in 2016/17

25 3 85

2 8 158 39 8 13

4 6 217 92

Cereals Pulses Oilseeds Vegetables Root crops Fruit crops

Production ('000 tons)

10 219

1 550805 240 229 108

Cereals Pulses Oilseeds Vegetables Root crops Fruit crops

Area ('000 ha)

Source : CSA ( 2016 ).

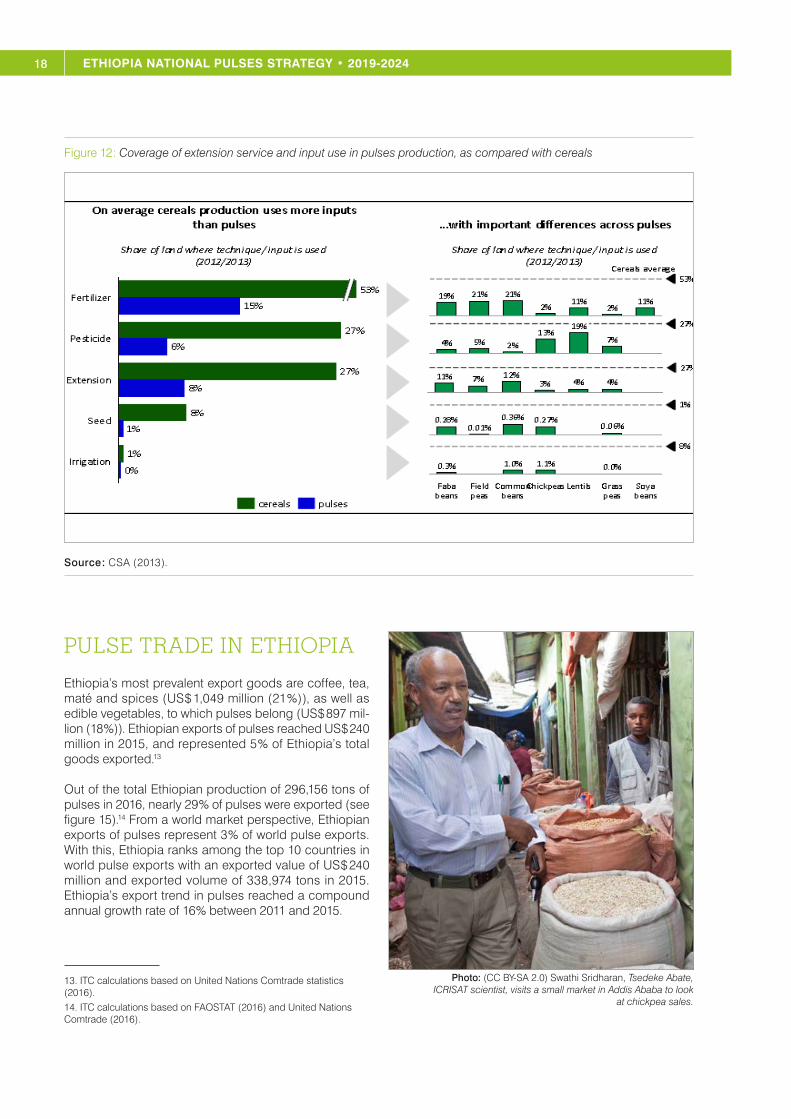

There has been low investment in pulses research com-pared with cereals, by both the Government and donors. Similarly, pulse initiatives have been given less priority. As shown in figure 12, extension service coverage has been far less on pulses : only 6 % compared with 27 % coverage for cereals, 25 % for vegetables and 15 % for root crops.12 Moreover, most farmers face great short-ages of high-yielding, disease-resistant varieties because of low access to improved seed ; currently, less than 1 % of pulse land is covered with improved seed annually, while for cereals the coverage is 8 %. Similarly, the use of chemical fertilizers and pesticides for pulses is negligible. Among the pulse crops, common beans and chickpeas have relatively better seed use than the other pulses, while broad beans, field peas and common beans enjoy higher fertilizer application than the other pulses.

12. The data for coverage of extension service and input use in pulses production as compared with cereals in Ethiopia is only available for 2012–2013 : updated data for 2016 is not available.

Photo: (CC BY-SA 2.0) ICRISAT

18 ETHIOPIA NATIONAL PULSES STRATEGY • 2019-2024

Figure 12 : Coverage of extension service and input use in pulses production, as compared with cereals

Source : CSA ( 2013 ).

PULSE TRADE IN ETHIOPIA

Ethiopia’s most prevalent export goods are coffee, tea, maté and spices ( US $ 1,049 million ( 21 % ) ), as well as edible vegetables, to which pulses belong ( US $ 897 mil-lion ( 18 % ) ). Ethiopian exports of pulses reached US $ 240 million in 2015, and represented 5 % of Ethiopia’s total goods exported.13

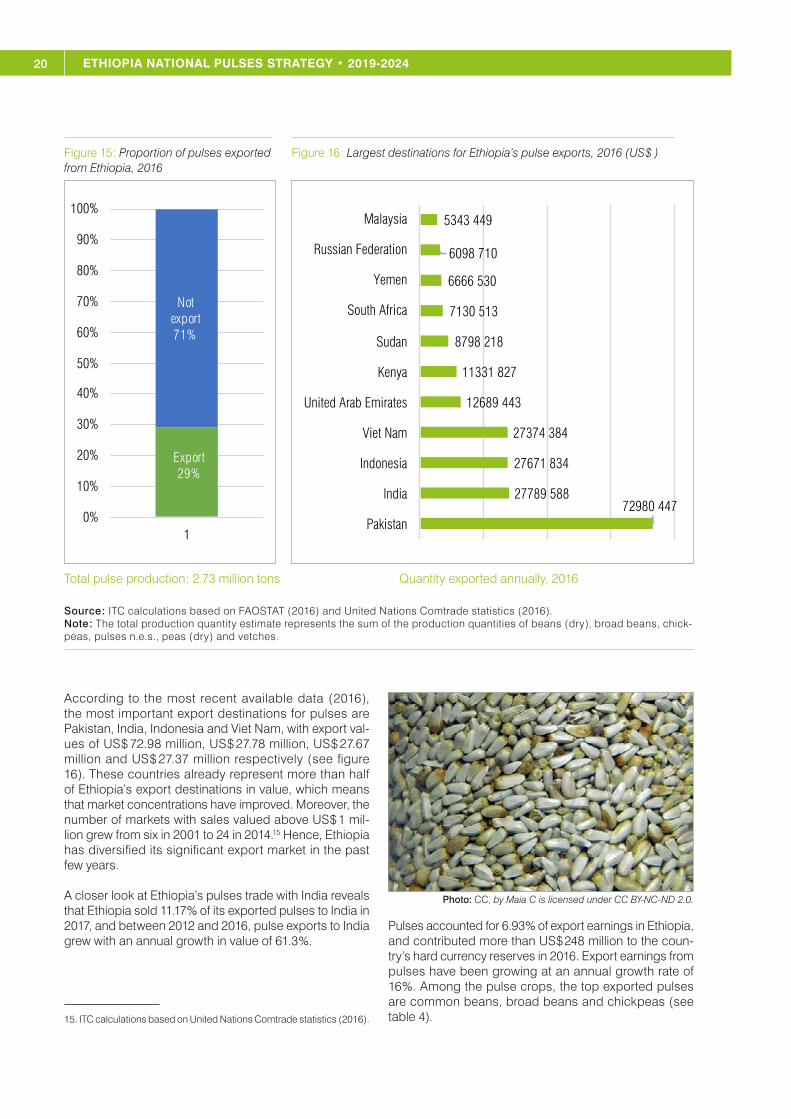

Out of the total Ethiopian production of 296,156 tons of pulses in 2016, nearly 29 % of pulses were exported ( see figure 15 ).14 From a world market perspective, Ethiopian exports of pulses represent 3 % of world pulse exports. With this, Ethiopia ranks among the top 10 countries in world pulse exports with an exported value of US $ 240 million and exported volume of 338,974 tons in 2015. Ethiopia’s export trend in pulses reached a compound annual growth rate of 16 % between 2011 and 2015.

13. ITC calculations based on United Nations Comtrade statistics ( 2016 ).14. ITC calculations based on FAOSTAT ( 2016 ) and United Nations Comtrade ( 2016 ).

Photo: (CC BY-SA 2.0) Swathi Sridharan, Tsedeke Abate, ICRISAT scientist, visits a small market in Addis Ababa to look

at chickpea sales.

19ETHIOPIA’S PULSES SECTOR

Figure 13 : Ethiopian exported goods in 2016 ( US $ millions )

Coffee, tea, maté and spices29%

Edible vegetables and certain roots and tubers

20%

Oil seeds and oleaginous fruits

20%

Live trees and other plants; bulbs, roots and the like; cut flowers and

ornamental foliage8%

Meat and edible

meat offal4%

Raw hides and skins and leather

3%

Live animals3%

Electrical machinery and equipment

1%

Others8%

Natural or cultured pearls, precious metals,

metals4%

Figure 14 : Ethiopia’s total pulses export in US $ million and tons, 2011–2016

139.27

199.25

239.41

286.99

240.7248.74

0

50 000

100 000

150 000

200 000

250 000

300 000

350 000

400 000

0

50

100

150

200

250

300

350

2011 2012 2013 2014 2015 2016

tons

USD

mill

ion

Trade value (US$) Net weight (kg)

Source : ITC calculations based on United Nations Comtrade statistics ( 2016 ).

20 ETHIOPIA NATIONAL PULSES STRATEGY • 2019-2024

Figure 15 : Proportion of pulses exported from Ethiopia, 2016

Figure 16 : Largest destinations for Ethiopia’s pulse exports, 2016 ( US $ )

72980 44727789 588

27671 834

27374 384

12689 443

11331 827

8798 218

7130 513

6666 530

6098 710

5343 449

Pakistan

India

Indonesia

Viet Nam

United Arab Emirates

Kenya

Sudan

South Africa

Yemen

Russian Federation

Malaysia

Not export 71%

Export 29%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1

Total pulse production : 2.73 million tons Quantity exported annually, 2016

Source : ITC calculations based on FAOSTAT ( 2016 ) and United Nations Comtrade statistics ( 2016 ). Note : The total production quantity estimate represents the sum of the production quantities of beans ( dry ), broad beans, chick-peas, pulses n.e.s., peas ( dry ) and vetches.

According to the most recent available data ( 2016 ), the most important export destinations for pulses are Pakistan, India, Indonesia and Viet Nam, with export val-ues of US $ 72.98 million, US $ 27.78 million, US $ 27.67 million and US $ 27.37 million respectively ( see figure 16 ). These countries already represent more than half of Ethiopia’s export destinations in value, which means that market concentrations have improved. Moreover, the number of markets with sales valued above US $ 1 mil-lion grew from six in 2001 to 24 in 2014.15 Hence, Ethiopia has diversified its significant export market in the past few years.

A closer look at Ethiopia’s pulses trade with India reveals that Ethiopia sold 11.17 % of its exported pulses to India in 2017, and between 2012 and 2016, pulse exports to India grew with an annual growth in value of 61.3 %.

15. ITC calculations based on United Nations Comtrade statistics ( 2016 ).

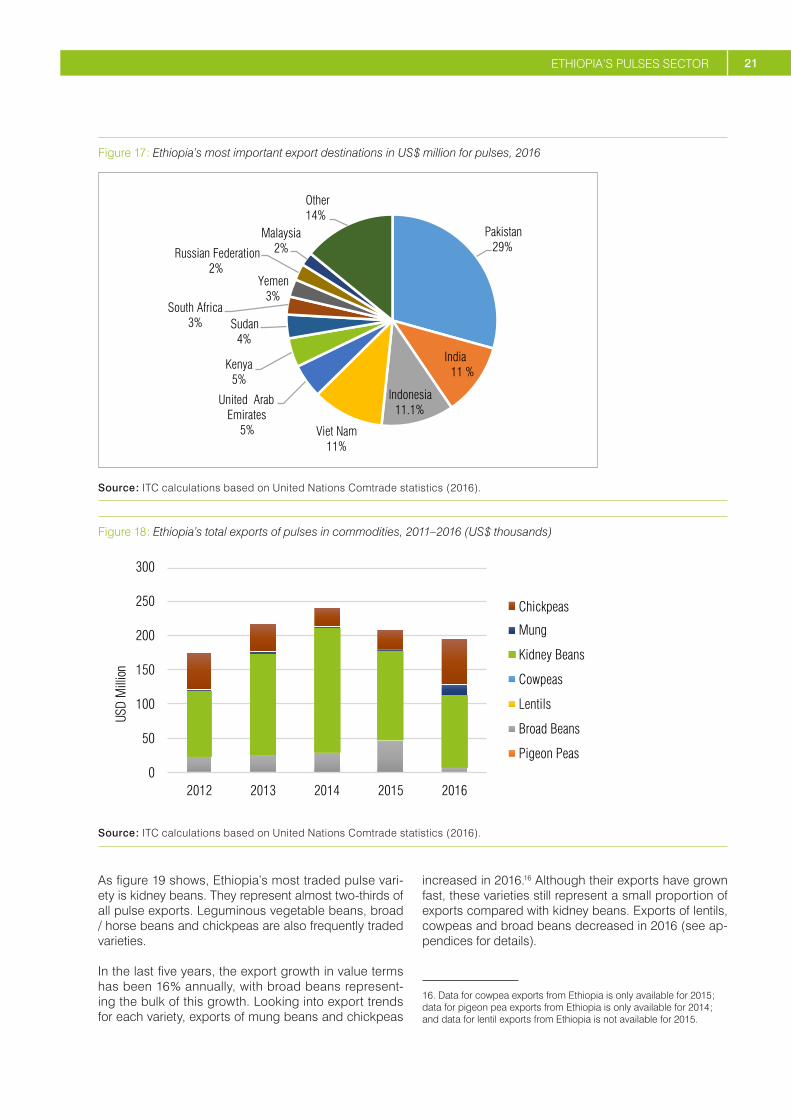

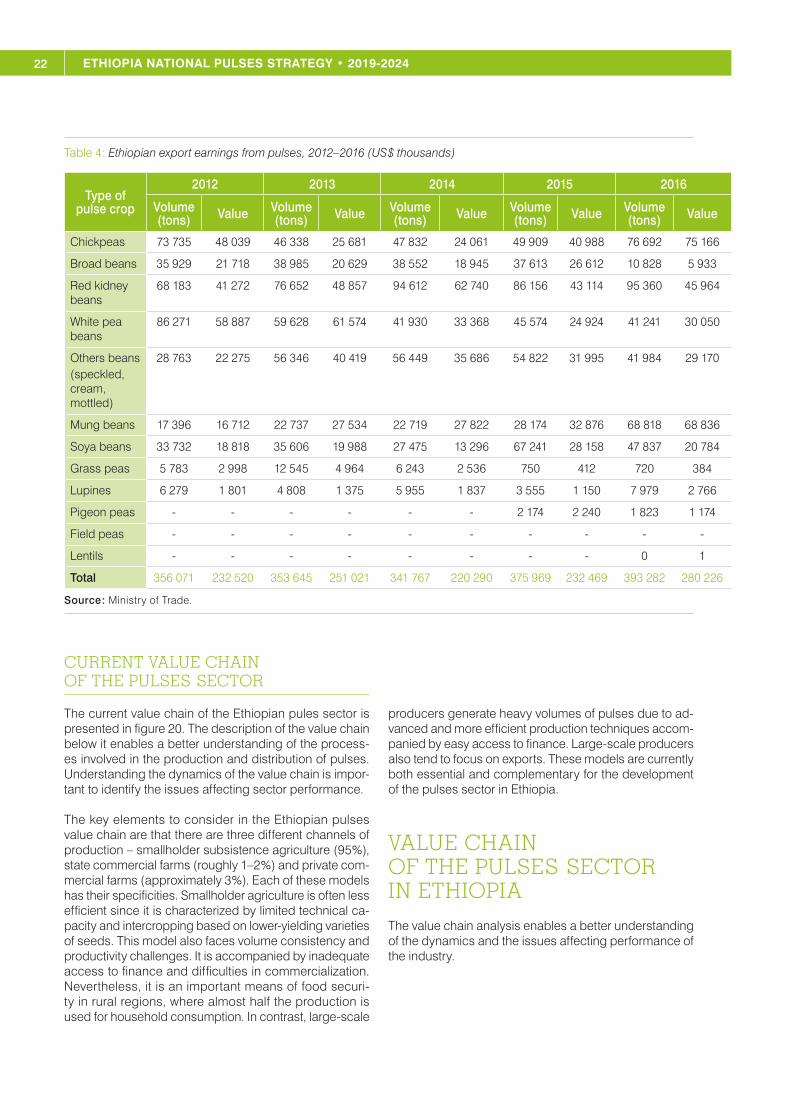

Pulses accounted for 6.93 % of export earnings in Ethiopia, and contributed more than US $ 248 million to the coun-try’s hard currency reserves in 2016. Export earnings from pulses have been growing at an annual growth rate of 16 %. Among the pulse crops, the top exported pulses are common beans, broad beans and chickpeas ( see table 4 ).

Photo: CC, by Maia C is licensed under CC BY-NC-ND 2.0.

21ETHIOPIA’S PULSES SECTOR

Figure 17 : Ethiopia’s most important export destinations in US $ million for pulses, 2016

Pakistan 29%

India 11 %

Indonesia 11.1%

Viet Nam11%

United Arab Emirates

5%

Kenya5%

Sudan4%

South Africa3%

Yemen3%

Russian Federation2%

Malaysia2%

Other14%

Source : ITC calculations based on United Nations Comtrade statistics ( 2016 ).

Figure 18 : Ethiopia’s total exports of pulses in commodities, 2011–2016 ( US $ thousands )

0

50

100

150

200

250

300

2012 2013 2014 2015 2016

USD

Mill

ion

Chickpeas

Mung

Kidney Beans

Cowpeas

Lentils

Broad Beans

Pigeon Peas

Source : ITC calculations based on United Nations Comtrade statistics ( 2016 ).

As figure 19 shows, Ethiopia’s most traded pulse vari-ety is kidney beans. They represent almost two-thirds of all pulse exports. Leguminous vegetable beans, broad / horse beans and chickpeas are also frequently traded varieties.

In the last five years, the export growth in value terms has been 16 % annually, with broad beans represent-ing the bulk of this growth. Looking into export trends for each variety, exports of mung beans and chickpeas

increased in 2016.16 Although their exports have grown fast, these varieties still represent a small proportion of exports compared with kidney beans. Exports of lentils, cowpeas and broad beans decreased in 2016 ( see ap-pendices for details ).

16. Data for cowpea exports from Ethiopia is only available for 2015 ; data for pigeon pea exports from Ethiopia is only available for 2014 ; and data for lentil exports from Ethiopia is not available for 2015.

22 ETHIOPIA NATIONAL PULSES STRATEGY • 2019-2024

Table 4 : Ethiopian export earnings from pulses, 2012–2016 ( US $ thousands )

Type of pulse crop

2012 2013 2014 2015 2016

Volume ( tons ) Value Volume

( tons ) Value Volume ( tons ) Value Volume

( tons ) Value Volume ( tons ) Value

Chickpeas 73 735 48 039 46 338 25 681 47 832 24 061 49 909 40 988 76 692 75 166

Broad beans 35 929 21 718 38 985 20 629 38 552 18 945 37 613 26 612 10 828 5 933

Red kidney beans

68 183 41 272 76 652 48 857 94 612 62 740 86 156 43 114 95 360 45 964

White pea beans

86 271 58 887 59 628 61 574 41 930 33 368 45 574 24 924 41 241 30 050

Others beans( speckled, cream, mottled )

28 763 22 275 56 346 40 419 56 449 35 686 54 822 31 995 41 984 29 170

Mung beans 17 396 16 712 22 737 27 534 22 719 27 822 28 174 32 876 68 818 68 836

Soya beans 33 732 18 818 35 606 19 988 27 475 13 296 67 241 28 158 47 837 20 784

Grass peas 5 783 2 998 12 545 4 964 6 243 2 536 750 412 720 384

Lupines 6 279 1 801 4 808 1 375 5 955 1 837 3 555 1 150 7 979 2 766

Pigeon peas - - - - - - 2 174 2 240 1 823 1 174

Field peas - - - - - - - - - -

Lentils - - - - - - - - 0 1

Total 356 071 232 520 353 645 251 021 341 767 220 290 375 969 232 469 393 282 280 226

Source : Ministry of Trade.

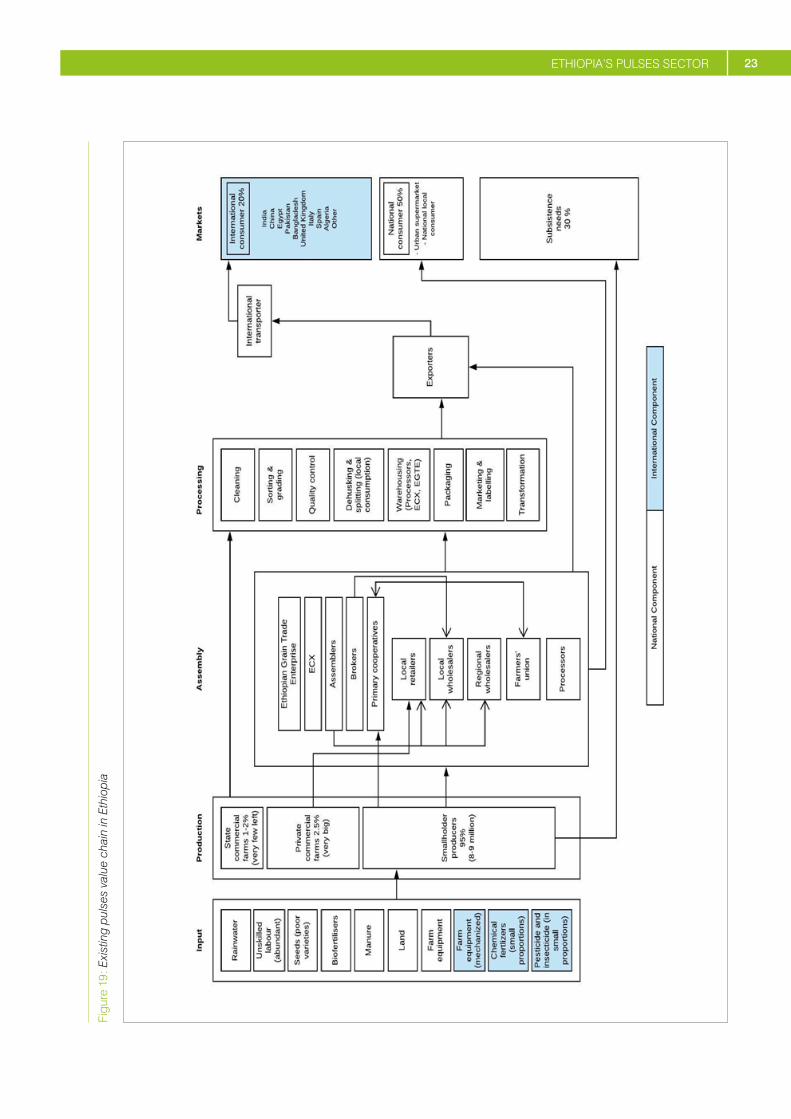

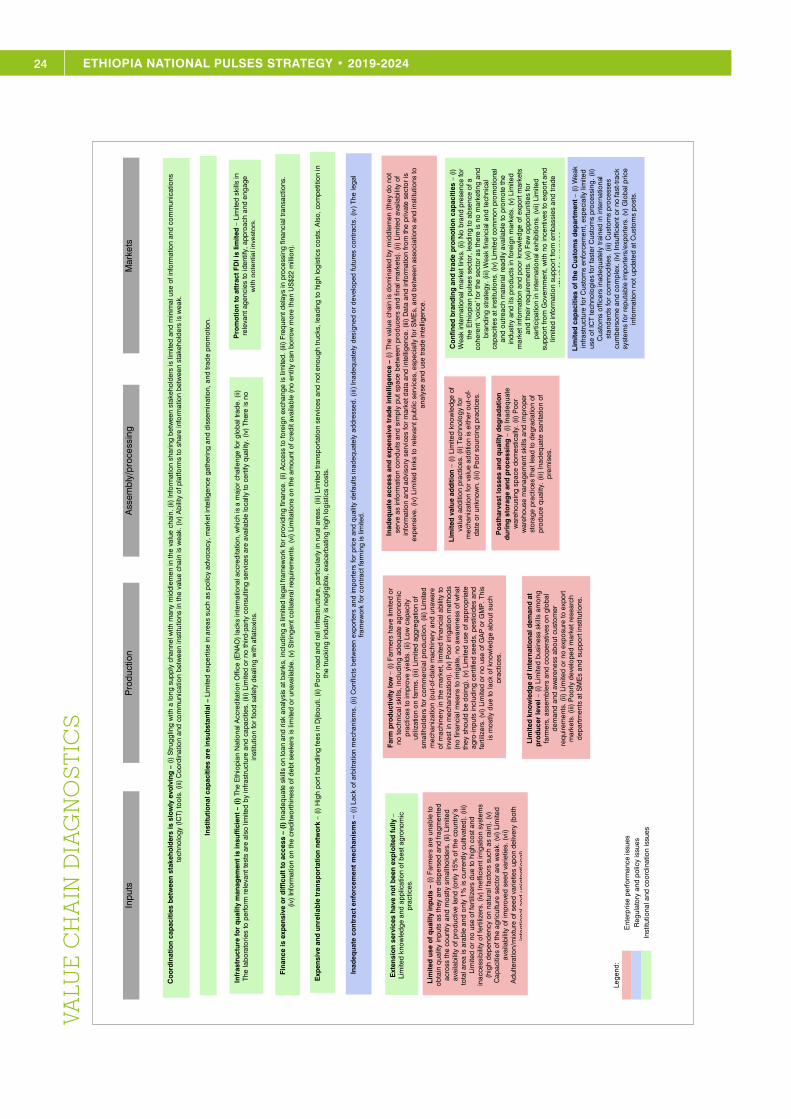

CURRENT VALUE CHAIN OF THE PULSES SECTOR

The current value chain of the Ethiopian pules sector is presented in figure 20. The description of the value chain below it enables a better understanding of the process-es involved in the production and distribution of pulses. Understanding the dynamics of the value chain is impor-tant to identify the issues affecting sector performance.

The key elements to consider in the Ethiopian pulses value chain are that there are three different channels of production – smallholder subsistence agriculture ( 95 % ), state commercial farms ( roughly 1–2 % ) and private com-mercial farms ( approximately 3 % ). Each of these models has their specificities. Smallholder agriculture is often less efficient since it is characterized by limited technical ca-pacity and intercropping based on lower-yielding varieties of seeds. This model also faces volume consistency and productivity challenges. It is accompanied by inadequate access to finance and difficulties in commercialization. Nevertheless, it is an important means of food securi-ty in rural regions, where almost half the production is used for household consumption. In contrast, large-scale

producers generate heavy volumes of pulses due to ad-vanced and more efficient production techniques accom-panied by easy access to finance. Large-scale producers also tend to focus on exports. These models are currently both essential and complementary for the development of the pulses sector in Ethiopia.

VALUE CHAIN OF THE PULSES SECTOR IN ETHIOPIA

The value chain analysis enables a better understanding of the dynamics and the issues affecting performance of the industry.

23ETHIOPIA’S PULSES SECTOR

Figu

re 1

9 : E

xist

ing

puls

es v

alue

cha

in in

Eth

iopi

a

24 ETHIOPIA NATIONAL PULSES STRATEGY • 2019-2024VA

LUE

CH

AIN

DIA

GN

OS

TIC

S

Inp

uts

P

rod

uctio

n

A

ssem

bly

/pro

cess

ing

Mar

kets

Leg

end

:

E

nter

pris

e p

erfo

rman

ce is

sues

Reg

ulat

ory

and

pol

icy

issu

es

In

stitu

tiona

l and

co

ord

inat

ion

issu

es

Far

m p

rod

uct

ivit

y lo

w –

(i)

Far

mer

s ha

ve li

mite

d o

r no

tech

nica

l ski

lls, i

nclu

din

g a

deq

uate

ag

rono

mic

p

ract

ices

to im

pro

ve y

ield

s. (

ii) L

ow

cap

acity

ut

iliza

tion

on

farm

s. (

iii)

Lim

ited

ag

gre

gat

ion

of

smal

lho

lder

s fo

r co

mm

erci

al p

rod

uctio

n. (

iii)

Lim

ited

m

echa

niza

tion

(out

-of-d

ate

mac

hine

ry a

nd u

naw

are

of m

achi

nery

in th

e m

arke

t, lim

ited

fina

ncia

l abi

lity

to

inve

st in

mec

hani

zatio

n). (

iv)

Poo

r irr

igat

ion

met

hod

s (n

o fi

nanc

ial m

eans

to ir

rigat

e, n

o a

war

enes

s o

f wha

t th

ey s

houl

d b

e d

oing

). (

v) L

imite

d u

se o

f ap

pro

pria

te

agro

-inp

uts

incl

udin

g c

ertif

ied

seed

s, p

estic

ides

and

fe

rtili

zers

. (vi

) Li

mite

d o

r no

use

of G

AP

or

GM

P. T

his

is m

ost

ly d

ue to

lack

of k

now

led

ge

abo

ut s

uch

pra

ctic

es.

Lim

ited

use

of

qu

alit

y in

pu

ts –

(i)

Far

mer

s ar

e un

able

to

ob

tain

qua

lity

inp

uts

as th

ey a

re d

isp

erse

d a

nd fr

agm

ente

d

acro

ss th

e co

untr

y an

d m

ost

ly s

mal

lho

lder

s. (

ii) L

imite

d

avai

labi

lity

of p

rod

uctiv

e la

nd (

onl

y 15

% o

f the

co

untr

y’s

tota

l are

a is

ara

ble

and

onl

y 1%

is c

urre

ntly

cul

tivat

ed).

(iii

) Li

mite

d o

r no

use

of f

ertil

izer

s d

ue to

hig

h co

st a

nd

inac

cess

ibili

ty o

f fer

tiliz

ers.

(iv

) In

effic

ient

irrig

atio

n sy

stem

s (h

igh

dep

end

ency

on

natu

ral f

acto

rs s

uch

as r

ain)

. (v)

C

apac

ities

of t

he a

gric

ultu

re s

ecto

r ar

e w

eak.

(vi

) Li

mite

d

avai

labi

lity

of im

pro

ved

see

d v

arie

ties.

(vi

i) A

dul

tera

tion/

mix

ture

of s

eed

varie

ties

upo

n de

liver

y (b

oth

in

tent

iona

l and

uni

nten

tiona

l).

Ext

ensi

on

ser

vice

s h

ave

no

t b

een

exp

loit

ed f

ully

–

Lim

ited

kno

wle

dg

e an

d a

ppl

icat

ion

of b

est a

gro

nom

ic

pra

ctic

es.

Lim

ited

kn

ow

led

ge

of

inte

rnat

ion

al d

eman

d a

t p

rod

uce

r le

vel –

(i)

Lim

ited

bus

ines

s sk

ills

amo

ng

farm

ers,

ass

emb

lers

and

co

ope

rativ

es o

n g

lob

al

dem

and

and

aw

aren

ess

abo

ut c

usto

mer

re

qui

rem

ents

. (ii)

Lim

ited

or

no e

xpo

sure

to e

xpo

rt

mar

kets

. (iii

) P

oorly

dev

elo

ped

mar

ket r

esea

rch

dep

artm

ents

at S

ME

s an

d s

upp

ort

inst

itutio

ns.

Lim

ited

val

ue

add

itio

n –

(i)

Lim

ited

kno

wle

dge

of

valu

e ad

diti

on

pra

ctic

es. (

ii) T

echn

olo

gy

for

mec

hani

zatio

n fo

r va

lue

add

itio

n is

eith

er o

ut-o

f-d

ate

or

unkn

ow

n. (

iii)

Po

or

sour

cing

pra

ctic

es.

Inad

equ

ate

acce

ss a

nd

exp

ensi

ve t

rad

e in

telli

gen

ce –

(i)

The

valu

e ch

ain

is d

om

inat

ed b

y m

idd

lem

en (

they

do

no

t se

rve

as in

form

atio

n co

ndui

ts a

nd s

imp

ly p

ut s

pac

e b

etw

een

pro

duc

ers

and

fina

l mar

kets

). (

ii) L

imite

d a

vaila

bilit

y of

in

form

atio

n an

d a

dvi

sory

ser

vice

s fo

r m

arke

t dat

a an

d in

telli

gen

ce. (

iii)

Dat

a an

d in

form

atio

n fr

om

the

priv

ate

sect

or

is

exp

ensi

ve. (

iv)

Lim

ited

link

s to

rel

evan

t pub

lic s

ervi

ces,

esp

ecia

lly fo

r S

ME

s, a

nd b

etw

een

asso

ciat

ions

and

inst

itutio

ns to

an

alys

e an

d u

se tr

ade

inte

llige

nce.

Po

sth

arve

st lo

sses

an

d q

ual

ity

deg

rad

atio

n

du

rin

g s

tora

ge

and

pro

cess

ing

– (

i) In

adeq

uate

w

areh

ous

ing

sp

ace

dom

estic

ally

. (ii)

Poo

r w

areh

ous

e m

anag

emen

t ski

lls a

nd im

pro

per

sto

rag

e p

ract

ices

that

lead

to d

egra

dat

ion

of

pro

duc

e q

ualit

y. (

iii)

Inad

equa

te s

anita

tion

of

pre

mis

es.

Infr

astr

uct

ure

fo

r q

ual

ity

man

agem

ent

is in

suff

icie

nt

– (i

) Th

e E

thio

pian

Nat

iona

l Acc

red

itatio

n O

ffice

(E

NA

O)

lack

s in

tern

atio

nal a

ccre

dita

tion,

whi

ch is

a m

ajo

r ch

alle

nge

for

glo

bal

trad

e. (

ii)

The

lab

ora

torie

s to

per

form

rel

evan

t tes

ts a

re a

lso

limite

d b

y in

fras

truc

ture

and

cap

aciti

es. (

iii)

Lim

ited

or

no th

ird-p

arty

co

nsul

ting

ser

vice

s ar

e av

aila

ble

loca

lly to

cer

tify

qua

lity.

(iv

) Th

ere

is n

o

inst

itutio

n fo

r fo

od

saf

ety

dea

ling

with

afla

toxi

ns.

Inad

equa

te c

ontr

act e

nfor

cem

ent m

echa

nism

s –

(i) L

ack

of a

rbitr

atio

n m

echa

nism

s. (i

i) Co

nflic

ts b

etw

een

expo

rters

and

impo

rters

for p

rice

and

qual

ity d

efau

lts in

adeq

uate

ly a

ddre

ssed

. (iii

) Ina

dequ

atel

y de

sign

ed o

r dev

elop

ed fu

ture

s co

ntra

cts.

(iv)

The

lega

l fra

mew

ork

for c

ontra

ct fa

rmin

g is

lim

ited.

Co

ord

inat

ion

cap

acit

ies

bet

wee

n s

take

ho

lder

s is

slo

wly

evo

lvin

g –

(i)

Str

ugg

ling

with

a lo

ng s

upp

ly c

hann

el w

ith m

any

mid

dlem

en in

the

valu

e ch

ain.

(ii)

Info

rmat

ion

shar

ing

bet

wee

n st

akeh

old

ers

is li

mite

d a

nd m

inim

al u

se o

f inf

orm

atio

n an

d c

om

mun

icat

ions

te

chno

logy

(IC

T) to

ols

. (iii

) C

oord

inat

ion

and

co

mm

unic

atio

n b

etw

een

inst

itutio

ns in

the

valu

e ch

ain

is w

eak.

(iv

) A

bili

ty o

f pla

tform

s to

sha

re in

form

atio

n b

etw

een

stak

eho

lder

s is

wea

k.

Lim

ited

cap

acit

ies

of

the

Cu

sto

ms

dep

artm

ent

– (i)

Wea

k in

fras

truc

ture

for

Cus

tom

s en

forc

emen

t, es

pec

ially

lim

ited

us

e o

f IC

T te

chno

log

ies

for

fast

er C

usto

ms

pro

cess

ing

. (ii)

C

usto

ms

offi

cers

inad

equa

tely

trai

ned

in in

tern

atio

nal

stan

dar

ds

for

com

mo

diti

es. (

iii)

Cus

tom

s p

roce

sses

cu

mb

erso

me

and

co

mp

lex.

(iv

) In

suffi

cien

t or

no fa

st-t

rack

sy

stem

s fo

r re

put

able

imp

ort

ers/

expo

rter

s. (

v) G

lob

al p

rice

info

rmat

ion

not u

pda

ted

at C

usto

ms

po

sts.

Co

nfi

ned

bra

nd

ing

an

d t

rad

e p

rom

oti

on

cap

acit

ies

– (i)

W

eak

inte

rnat

iona

l mar

ket l

inks

. (ii)

No

bra

nd p

rese

nce

for

the

Eth

iopi

an p

ulse

s se

cto

r, le

adin

g to

ab

senc

e o

f a

cohe

rent

‘vo

ice’

for

the

sect

or a

s th

ere

is n

o m

arke

ting

and

b

rand

ing

str

ateg

y. (i

ii) W

eak

finan

cial

and

tech

nica

l ca

pac

ities

at i

nstit

utio

ns. (

iv)

Lim

ited