Ethical Issues in Tax Practice and Procedure Thursday, June 25, 2015 12:20 P.M. – 1:50 P.M.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Ethical Issues in Tax Practice and Procedure

Thursday, June 25, 201512:20 P.M. – 1:50 P.M.

Presenters

Brian KatusianSeltzer Caplan McMahon Vitek750 B Street, Suite 2100San Diego, CA 92101Tel. 619.685.3186Email: [email protected]

Elizabeth Van CliefHughes & Pizzuto401 B Street, Suite 2400San Diego, CA 92101Tel. 619.239.1211Email: [email protected]

Ethical Rules

• In tax controversies and litigation, an attorney is subject to at least the following rules:– ABA Model Rules of Professional Conduct– California Rules of Professional Conduct– Treasury Department’s Circular 230– Tax Court Rules of Practice and Procedure

California Rules of Professional Conduct

• The California Rules of Professional Conduct are intended to regulate professional conduct of members of the State Bar through discipline.

• They have been adopted by the Board of Trustees and approved by the California Supreme Court pursuant to statute to protect the public and to promote respect and confidence in the legal profession.

• The rules and any related standards adopted by the Board are binding on all members of the State Bar.

California Compendium of Professional Responsibility

• The State Bar Office of Professional Competence publishes and sells a three-volume ethics reference manual, the California Compendium of Professional Responsibility, which contains:

• Ethics opinions published by The State Bar of California, the Bar Association of San Francisco, the Los Angeles County Bar Association, the Orange County Bar Association and the San Diego County Bar Association

• The Publication 250 Book (California Rules of Professional Conduct, State Bar Act, Selected Statutes and Rules of Court and more...)

• California Code of Judicial Conduct and a comprehensive subject matter research index.

Client Trust Accounting Handbook

• The trust accounting handbook is a practical guide created to assist attorneys comply with recordkeeping standards for client trust accounts that went into effect Jan. 1, 1993. The handbook includes:– a copy of the standards and statutes relating to an

attorney's trust accounting requirements,– a step-by-step description of how to maintain a client

trust account; and– sample forms.

• The handbook is currently only available online.

Ethics Hotline

• The Ethics Hotline, a confidential research service for attorneys only, helps lawyers identify and analyze their professional responsibilities.

• All calls to the Ethics Hotline generally are confidential.

• Telephone number: 800-238-4427

Hotliner News

• The Ethics Hotliner is an online resource providing the latest information on California legal ethics.

Ethics Opinions

• Ethics opinions issued by The State Bar of California Committee on Professional Responsibility and Conduct.

• The advisory opinions regarding the ethical propriety of hypothetical attorney conduct, although not binding, are often cited in the decisions of the Supreme Court, the State Bar Court Review Department and the Court of Appeal.

Circular 230

• Treasury Department Circular 230 sets forth the rules and ethical standards for persons representing clients in matters before the Internal Revenue Service, including examinations (audits) and administrative appeals.

• Attorney must promptly submit records or information to the IRS unless privileged.

• Example – During an IRS audit, attorney cannot delay case by unreasonably withholding documentation requested in IDR.

• Maintain a privilege log if withhold documentation such as emails.

§10.20 Information to be furnished

§10.20 Information to be furnished.• Must promptly notify

IRS if taxpayer lacks possession or control of documents.

• Identify of person who may have possession.

• Reasonable inquiry• Example – IRS serves

IDR on taxpayer, and taxpayer claims he lacks possession or control over requested information.

§10.20 Information to be furnished

• Cannot interfere with IRS effort to obtain records unless privileged.

• Example – Practitioner contacts a third-party witness and instructs witness to not talk to IRS. Practitioner has conflict of interest in representing both witness and taxpayer during IRS audit.

§10.21 Knowledge of client’s omission

• An attorney must advise the client of any noncompliance, error or omission.

• The attorney also must advise the client of the consequences (i.e., civil penalties and criminal offenses).

• Example – Taxpayer submits false document to IRS

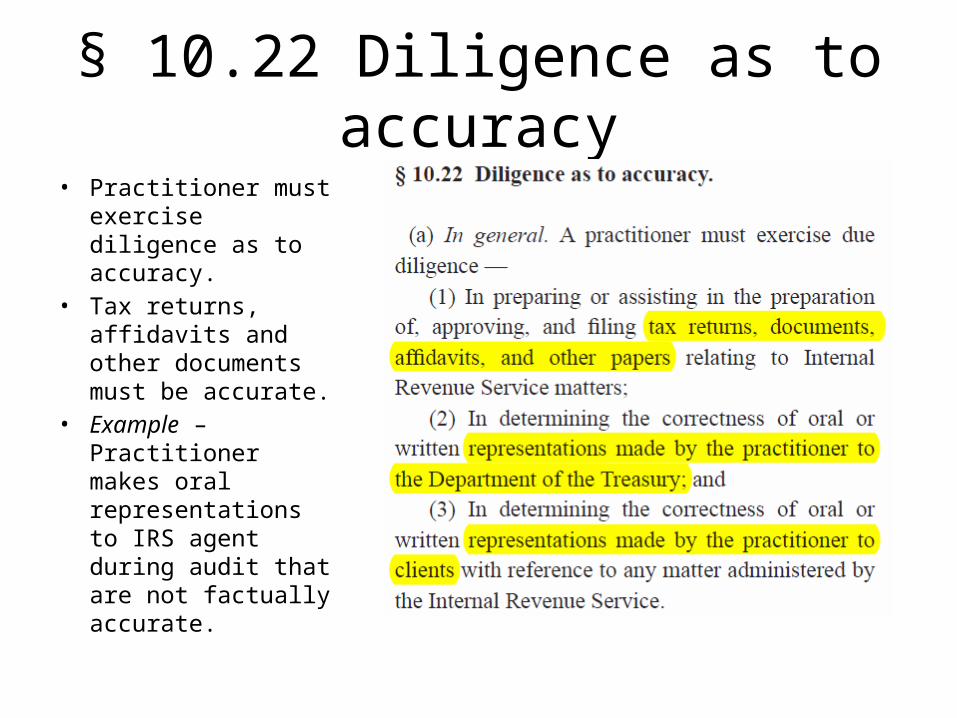

§ 10.22 Diligence as to accuracy• Practitioner must

exercise diligence as to accuracy.

• Tax returns, affidavits and other documents must be accurate.

• Example – Practitioner makes oral representations to IRS agent during audit that are not factually accurate.

§ 10.27 Fees

• Issue monthly statements to clients

• Statements should detail work performed, hours worked, and hourly rates

• Flat fee?

§ 10.27(b) Contingent Fees

• When may a practitioner charge a contingent fee for services?

• Practitioner may not charge a contingent fee for services rendered in connection with any matter before the IRS except under specified circumstances.

§ 10.28 Return of client’s records.• Promptly return all

records• Fee dispute

generally not relieve practitioner of his responsibility

§10.28 Return of client’s records.• Records of the client do

not include documents prepared by practitioner or agents if practitioner is withholding document pending client’s payment of fee

• Example – Written appraisal report prepared by expert witness in estate tax audit.

§10.29 Conflict of interest.

• Representation of one client will be directly adverse to another client.

• Significant risk that representation will be materially limited

• Reasonably believes provide competent and diligent representation

• Client waives conflict and gives informed consent in writing

• 36 months

§10.29 Conflict of interest

Cal Rules of Professional Conduct 3-310 Avoiding the Representation of Adverse Interests

• Husband and wife in Tax Court case

• Individual in IRS audit and witness who receives IRS summons

• Employer and employee

• Partnership and partners

• LLC and members• Corporation and

shareholders

(C) A member shall not, without the informed written consent of each client:

(1) Accept representation of more than one client in a matter in which the interests of the clients potentially conflict; or

(2) Accept or continue representation of more than one client in a matter in which the interests of the clients actually conflict; or

(3) Represent a client in a matter and at the same time in a separate matter accept as a client a person or entity whose interest in the first matter is adverse to the client in the first matter.

Conflicts of Interest

• Para Technologies Trust v. Commissioner, T.C. Memo 1992-575 (Tax Court granted Commissioner’s motion to compel the withdrawal of taxpayers’ attorney where attorney had conflict of interest; Tax Court cited ABA Model Rule 1.7(b) and 24(f)).

• Eriks v. Denver, 824 P.2d 1207, 1211-1212 (Wash. 1992) (citing Model Rules Rule 1.7 comment (1984) and holding that as a matter of law there was a conflict of interest between promoters of and investors in a tax shelter).

• Devore v. Commissioner, 963 F.2d 280 (9th Cir. 1992) (case remanded to Tax Court for evidentiary hearing to determine if Devore prejudiced by former counsel’s conflict of interest).

Engagement letter

• Scope of engagement• Client’s responsibilities• Legal fees, billing statements and advance

deposits• Handling of client files• Discharge and withdrawal • Joint representation

Tax Court Rule 33• Rule 33 applies to any

pleadings that you file in Tax Court.

• Example – Petitions, motions, etc.

• Fed. R. Civ. Proc. 11 applies in federal district court. It deals with signing of pleadings, motions, and other papers; representation to the court; and sanctions.

Client Pays You Cash or Cashier’s Check

• IRS Form 8300• Business receives more than $10,000 in “cash” in a single

transaction or related series of transactions.– “Cash” does not include personal checks. Includes U.S. and foreign

currency, coins, money order, cashier’s check, bank draft, traveler’s check.

• Can a lawyer refuse to disclose the identity of the client on Form 8300 based upon the attorney-client privilege? See U.S. v. Blackman, 72 F.3d 1418 (9th Cir. 1995).– Probably not. Only if disclosure would be “tantamount to [the

revelation of] a confidential privileged communication.” – Identity of client would have to be “inextricably intertwined with

confidential communications.”

Client uses proceeds from crimesto pay fees

• If the client uses proceeds from certain crimes to pay his lawyer, the fees may be subject to forfeiture by the government. See 21 U.S.C. § 853.

• Be cautious in ensuring that funds used to pay fees come from a legitimate source.

• By law, the IRS is prohibited from disclosing “confidential tax return information.” Internal Revenue Code § 6103. IRS agents will not talk to or correspond with an attorney without a valid Power of Attorney on file.

• Use Form 2848 Power of Attorney and Declaration of Representative. A separate form is required for each spouse, even if a joint tax return was filed. (Be aware that spouses may have a conflict of interest!)

• Link to Form 2848 on IRS website:

http://www.irs.gov/pub/irs-pdf/f2848.pdf • Fax the completed form to the central POA unit at (801) 620-4249 (for

California Taxpayers – or see 2848 Instructions for taxpayers residing elsewhere) as well as to the particular agent handling the matter.

Client Must Designate Representative by Written Authorization (IRS Power of Attorney Form)

Formal Opinion No. 2010-179 (Confidentiality and Technology)

Formal Opinion No. 2011-180 (Gifts from Clients)

Formal Opinion No. 2012-183 (Duty of Confidentiality and Seeking Legal Advice)

Formal Opinion No. 2012-184 (Virtual Law Office)

Formal Opinion No. 2012-185 (State Bar Complaints Threats)

Formal Opinion No. 2012-186 (Social Networking)

Formal Opinion No. 2013-187 (Third Party Payor)

Formal Opinion No. 2013-188 (Confidential Information and Unsolicited

E-Mail Correspondence)

Formal Opinion No. 2013-189 (Deceitful Conduct)

Formal Opinion No. 2014-190(Dissolving and Moving to New Firm)

Formal Opinion No. 2014-191(In Rem Bankruptcy Proceedings)

Formal Opinion No. 2015-192(Disclosure of Confidences at Motions for Withdrawal)

Related Documents