Estate Planning Estate Planning Presentation Presentation www.probatewilllawyersaustralia.com www.probatewilllawyersaustralia.com “ “ Before and After…” Before and After…” Alex Tees, Tel 02 9281 3230/0409813622 Alex Tees, Tel 02 9281 3230/0409813622 Solicitor, Estate Planning Adviser Solicitor, Estate Planning Adviser Email Email [email protected] SKYPE “alextees” SKYPE “alextees”

Estate Planning Presentation probatewilllawyersaustralia

Jan 22, 2016

Estate Planning Presentation www.probatewilllawyersaustralia.com. “Before and After…” Alex Tees, Tel 02 9281 3230/0409813622 Solicitor, Estate Planning Adviser Email [email protected] SKYPE “ alextees ”. Important disclaimer. - PowerPoint PPT Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Estate Planning Estate Planning PresentationPresentation

www.probatewilllawyersaustralia.comwww.probatewilllawyersaustralia.com

““Before and After…”Before and After…”Alex Tees, Tel 02 9281 3230/0409813622Alex Tees, Tel 02 9281 3230/0409813622

Solicitor, Estate Planning AdviserSolicitor, Estate Planning AdviserEmail Email [email protected] SKYPE “alextees” SKYPE “alextees”

Important disclaimerImportant disclaimer

• No person should rely on any part of the contents of this No person should rely on any part of the contents of this presentation without first obtaining advice from a qualified presentation without first obtaining advice from a qualified professional person. This presentation is given on the terms professional person. This presentation is given on the terms and understanding that the author is not responsible for the and understanding that the author is not responsible for the results of any actions taken on the basis of information in results of any actions taken on the basis of information in this presentation, nor for any error in or omission from this this presentation, nor for any error in or omission from this presentation. The author hereby expressly disclaims all and presentation. The author hereby expressly disclaims all and any liability and responsibility to any person, whether a any liability and responsibility to any person, whether a purchaser, recipient or reader of this presentation or not, in purchaser, recipient or reader of this presentation or not, in respect of anything, and of the consequences of anything, respect of anything, and of the consequences of anything, done or omitted to be done by any such person in reliance, done or omitted to be done by any such person in reliance, whether wholly or partially, upon the whole or any part of whether wholly or partially, upon the whole or any part of the contents of this presentation.the contents of this presentation.

““MODERN SUCCESSION MODERN SUCCESSION & ESTATE PLANNING “ & ESTATE PLANNING “

• Due to increasing complexity in family relationships Due to increasing complexity in family relationships and business/investment structuring, along with and business/investment structuring, along with complicated tax and legal regimes - modern estate complicated tax and legal regimes - modern estate planning, done properly, must encompass issues planning, done properly, must encompass issues such as such as ::– Efficient intergenerational transfer of wealth with harmonyEfficient intergenerational transfer of wealth with harmony– Asset protection (Asset protection (Keeping out “Predators/Creditors” Keeping out “Predators/Creditors”

& Keeping the Wealth in the Family & Keeping the Wealth in the Family ))– Tax (at both State and Federal level)Tax (at both State and Federal level)– Superannuation (Formation + Review of Deeds)Superannuation (Formation + Review of Deeds)– Trusts (Formation + Review of Deeds)Trusts (Formation + Review of Deeds)– Investments/insurance structuringInvestments/insurance structuring– Resolution of disputes and other issues through the use of Resolution of disputes and other issues through the use of

an “Independent Referree” – Dispute Resolutionan “Independent Referree” – Dispute Resolution

WHAT Lawyers should DO in WHAT Lawyers should DO in co-operation with Accountants co-operation with Accountants and Financial Plannersand Financial PlannersProvision of Provision of strategiesstrategies and and adviceadvice in in

collaboration with other professionalscollaboration with other professionals ( Accountants/Financial Planners) to deliver the ( Accountants/Financial Planners) to deliver the optimum outcome(s) for client (s):optimum outcome(s) for client (s): Modern Estate Planning Strategies Modern Estate Planning Strategies

( ( Before and after deathBefore and after death )) Testamentary Trusts ( Trusts created after death)Testamentary Trusts ( Trusts created after death) Family TrustsFamily Trusts Self-managed superannuation funds (SMSF)Self-managed superannuation funds (SMSF) Business succession planning.(Business succession planning.(a “will” for a a “will” for a

Business Business ))

Estate Planning - HOW a Lawyer Estate Planning - HOW a Lawyer should and can OPERATEshould and can OPERATE

Timeframes agreed with client and referrer at each stage to Timeframes agreed with client and referrer at each stage to ensure efficient completion and accountability ensure efficient completion and accountability

Fixed Fees or a fixed range of fees & the First meeting Fixed Fees or a fixed range of fees & the First meeting with client(s) is purely a scoping exercise & with client(s) is purely a scoping exercise & obligation free ( obligation free ( often in Accountants/Financial Planners ‘ office )often in Accountants/Financial Planners ‘ office )

CollaborationCollaboration/Reporting to Accountant/Fin’Planner at each /Reporting to Accountant/Fin’Planner at each stage stage = = Further FeeFurther Fee && protection opportunities..for you protection opportunities..for you

Systematic and efficient delivery ( x 3 Meetings)Systematic and efficient delivery ( x 3 Meetings) Technical and client-related queries welcomed from all Technical and client-related queries welcomed from all

Referrers/Client(s) Referrers/Client(s) Referral to other Specialist Tax ServicesReferral to other Specialist Tax Services

Why is it different ? - Why is it different ? - the way the way it is recommended to operate it is recommended to operate compared tocompared to OTHER LAW OTHER LAW FIRMS ?FIRMS ? High level technical expertise in superannuation , taxation , High level technical expertise in superannuation , taxation ,

and Trust law – Solicitor(s) should work with and have and Trust law – Solicitor(s) should work with and have access access to the resources of Accounting advisory firmsto the resources of Accounting advisory firms.(throughout the .(throughout the World)World)

Specialist Solicitors who understand and appreciate the Specialist Solicitors who understand and appreciate the Financial planning process, work togetherFinancial planning process, work together with Clients’ with Clients’ Financial Planners & Accountants.Financial Planners & Accountants.

Encourage First meetings/other meetings at Financial Encourage First meetings/other meetings at Financial Planners/Accountants’ office and/or clients home/office.Planners/Accountants’ office and/or clients home/office.

Fixed price contracts (or Fixed Range) (Fixed price contracts (or Fixed Range) (Approx 75% Tax Approx 75% Tax DeductionDeduction))

Comprehensive Estate Planning Portfolio / Folder.Comprehensive Estate Planning Portfolio / Folder. Delivery meetings can be Optional Family meetings to Delivery meetings can be Optional Family meetings to

include the children – builds bridges to next generationinclude the children – builds bridges to next generation

A Modern Will – Creative use of Trusts A Modern Will – Creative use of Trusts after Death…(as well as after Death…(as well as * Other * Other structures structures ))• Will Maker/Testator makes a Will to flexibly provide ;Will Maker/Testator makes a Will to flexibly provide ;• Optional Testamentary Trust or other *Structures Optional Testamentary Trust or other *Structures

created after Death created after Death (*Note Tax laws may change !?)(*Note Tax laws may change !?)• ““Beneficiaries” Persons receiving Money & Property , Beneficiaries” Persons receiving Money & Property ,

receive it via a Trust of which they or their receive it via a Trust of which they or their Nominated Person become TrusteeNominated Person become Trustee

• Provides Tax Efficiency and Assett ProtectionProvides Tax Efficiency and Assett Protection• * If the law changes Provision for Other Structures * If the law changes Provision for Other Structures

such as Partnerships, Joint Ventures and different such as Partnerships, Joint Ventures and different types of Companies/Corporations may be types of Companies/Corporations may be necessary…..necessary…..

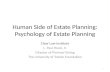

Example – Optional Trusts After DeathExample – Optional Trusts After Death

EXECUTOR

(May not be the same Person)

TRUSTEE (S)

TRUST TRUST TRUST

EXECUTOR EXECUTOR WILLWILL

The Efficient Will – *Possible use of Trusts The Efficient Will – *Possible use of Trusts after Death………..after Death………..

Optional Discretionary Testamentary

Trust

!

E

Trustee

Beneficiaries include: ( THOSE RECEIVING GIFTS ) Primary Beneficiary

–Surviving Spouse/Children

Family Members Related Entities

Trustee - Primary Beneficiary(Surviving Spouse/Children)

B

Case Study 1 – Wealthy Woman marries a Case Study 1 – Wealthy Woman marries a much less Wealthy Gentleman – Who Needs much less Wealthy Gentleman – Who Needs Protection ?Protection ?

Assets and Possible Family SituationAssets and Possible Family Situation

• ( Married or Unmarried)( Married or Unmarried)

• Possibly have one childPossibly have one child

• Woman owns a House/PropertyWoman owns a House/Property

• Woman a High income earner/ & Woman a High income earner/ & WealthyWealthy

• Perhaps the Husband will never have a Perhaps the Husband will never have a high income earning capacityhigh income earning capacity

Case Study 1 - Case Study 1 - ESTATE PLANNING ESTATE PLANNING - WISHES & Concerns - Whose ? !! - WISHES & Concerns - Whose ? !!

• Protect the child if both or One Spouse diesProtect the child if both or One Spouse dies

• Ensure Husband does not receive too much Ensure Husband does not receive too much “loot” from His Wealthy Wife if she dies first ? “loot” from His Wealthy Wife if she dies first ? ( & Protect the Child as well !)( & Protect the Child as well !)

• Ensure the Husband at least has a Roof over Ensure the Husband at least has a Roof over his head and adequate provision while he his head and adequate provision while he cares for the child if Wife dies before him…cares for the child if Wife dies before him…

• Ensure Equity & Sensitivity …………Ensure Equity & Sensitivity …………

Case Study 1 -Possible Case Study 1 -Possible StrategiesStrategies• A Separate Care for the Spouse Trust for the A Separate Care for the Spouse Trust for the

Husband with little wealthHusband with little wealth• A Separate Trust for the Husband with A Separate Trust for the Husband with

sufficient Money/Propertysufficient Money/Property• A Separate Trust for the child with another A Separate Trust for the child with another

relative of the Wife as Trustee (Husband relative of the Wife as Trustee (Husband given right to occupy Family Home for given right to occupy Family Home for life ,while Child receives all the Wifes’ life ,while Child receives all the Wifes’ Estate………)Estate………)

• Recommend and Ensure the Husband owns Recommend and Ensure the Husband owns Adequate & generous Life Insurance over the Adequate & generous Life Insurance over the Life of his Wife in case she dies first…….Life of his Wife in case she dies first…….

Case Study 2 – George & MarinaCase Study 2 – George & Marina

George 55, Marina 54 George 55, Marina 54 - both - both retiredretired

• Children ; Jessica 27 (De Facto), Children ; Jessica 27 (De Facto),

• Sarah , 22 (Married) Sarah , 22 (Married)

• Jack 21, (Has a Disability, numerous Jack 21, (Has a Disability, numerous Partners)Partners)

Case Study 2 – George & Case Study 2 – George & MarinaMarina• ASSETSASSETS

HomeHome Joint tenantsJoint tenants

Investment Investment

Property 1Property 1Joint tenantsJoint tenants

Managed Managed fundsfunds

SMSF (Self Managed Super’ SMSF (Self Managed Super’ Fund)Fund)

SharesShares SMSFSMSF

Direct Direct propertyproperty

SMSFSMSF

Case Study 2 – George & Case Study 2 – George & MarinaMarina

• ESTATE PLANNING - Wishes & ConcernsESTATE PLANNING - Wishes & Concerns

George to Marina and vice versa in the first instanceGeorge to Marina and vice versa in the first instance

Then equally to childrenThen equally to children

Specific protection required for Jack due to disabilitySpecific protection required for Jack due to disability

Wealth to be Wealth to be retained in the familyretained in the family

Derive some tax efficiencyDerive some tax efficiency

Case Study 2 – George & Case Study 2 – George & MarinaMarina

• Possible STRATEGIESPossible STRATEGIES

““Estate Estate Assets”Assets”

Testamentary Trusts & Testamentary Trusts & *other optional Structure *other optional Structure (s)(s)

Family HomeFamily Home Sever tenancySever tenancy

Investment Investment Property 1Property 1

Sever tenancySever tenancy

SMSF (Super SMSF (Super Fund)Fund)

BDBN (Binding Death BDBN (Binding Death Benefit Nomination)Benefit Nomination)

Case Study 2 – George & Case Study 2 – George & MarinaMarina

•STRATEGIE(S) - WILLSSTRATEGIE(S) - WILLS

ConcernConcern StrategyStrategyProtection of family Protection of family wealth from spousal wealth from spousal and other claimsand other claims

Testamentary Trusts (TTs) & Testamentary Trusts (TTs) & other Structures with crisis other Structures with crisis provisions (removal of provisions (removal of Trustees, Directors, Trustees, Directors, “Controllers” etc)“Controllers” etc)

Protection for JackProtection for Jack

- Control - Control

- Conflicts of - Conflicts of interestinterest

Protective TrustProtective Trust

- ‘Family’ control- ‘Family’ control

- Testamentary Protector- Testamentary Protector

Understanding of Understanding of “non-estate assets” “non-estate assets” and planning requiredand planning required

Sever joint tenancy (Family Sever joint tenancy (Family Home)Home)

Cascading Binding Death Cascading Binding Death Benefit Nominations (Super’)Benefit Nominations (Super’)

STRATEGIES – SMSF- Super’FundsSTRATEGIES – SMSF- Super’Funds

Concerns & StrategyConcerns & Strategy

Maximise superannuation benefits during lifetime, Maximise superannuation benefits during lifetime, potential inability of survivor to recontribute to superpotential inability of survivor to recontribute to super

- Use “Reversionary” pensions- Use “Reversionary” pensions Optimising tax with protectionOptimising tax with protection(*BDBN = Binding Death Benefit Nomination) - Cascading (*BDBN = Binding Death Benefit Nomination) - Cascading

*BDBNs*BDBNs - first, reversionary- first, reversionary - then, *LPR- then, *LPR(* Legal Personal Representative )(* Legal Personal Representative ) Ongoing control of SMSF -Corporate Trustee appropriate ? Ongoing control of SMSF -Corporate Trustee appropriate ?

Other Possible Strategies – Some “Non Other Possible Strategies – Some “Non Estate Property” – Family Trusts Estate Property” – Family Trusts /Super’/Super’ Concerns & StrategyConcerns & Strategy1) Transition of control of Family Trust -Trust Deed 1) Transition of control of Family Trust -Trust Deed

Review Review - Deed of Future Dealing / Alter Trust Deed - Deed of Future Dealing / Alter Trust Deed ( to take in succession)( to take in succession)

2) “The Business” Release of value in the business 2) “The Business” Release of value in the business – – how to pass on to familyhow to pass on to family- Business Succession Agreement – “A Will for a - Business Succession Agreement – “A Will for a

Business”Business”

3) Superannuation3) Superannuation Nominate LPR as beneficiary,Nominate LPR as beneficiary, Insurance(s)Insurance(s) Nominate LPR as beneficiaryNominate LPR as beneficiary

Case Study 3 – Simpler CaseCase Study 3 – Simpler Case

•FAMILY SITUATIONFAMILY SITUATION• Jack, 53 & Jill 49 - both still workingJack, 53 & Jill 49 - both still working

• 4 children 4 children :: Mark 23 … Mark 23 … single (Jacks child first marriage)single (Jacks child first marriage)

Steve 21 … Steve 21 … single, (Jacks child first marriage)single, (Jacks child first marriage)

Marina 20 …Marina 20 … De Facto (Jills child 1De Facto (Jills child 1stst marriage ) marriage )

Helena , Age 3 (Jack & Jills child 2Helena , Age 3 (Jack & Jills child 2ndnd Marriage) Marriage)

Case Study 3 Jack & Jill - Case Study 3 Jack & Jill - AssetsAssets

Home - Joint tenantsHome - Joint tenants

Investment property – Joint TenantInvestment property – Joint Tenant

SMSF (Self Managed Super’ Fund)SMSF (Self Managed Super’ Fund)

SharesShares SMSFSMSF

Jack & Jill (not over the Hill) Jack & Jill (not over the Hill) (3)(3)• Possible ESTATE PLANNING Possible ESTATE PLANNING

WISHES & ConcernsWISHES & Concerns

Jack to Jill and vice versa in the first instanceJack to Jill and vice versa in the first instance

Then equally to childrenThen equally to children

Specific protection required for Helena due to young ageSpecific protection required for Helena due to young age

Keep wealth in Family ;Wealth to be Keep wealth in Family ;Wealth to be retained in the retained in the familyfamily

Derive some tax efficiencyDerive some tax efficiency

After Jack & Jill Die …. (3)After Jack & Jill Die …. (3)

Some Strategies :Some Strategies :

1.Estate Assets Optional Testamentary 1.Estate Assets Optional Testamentary TrustsTrusts

2.Home - 2.Home - Sever Joint tenancySever Joint tenancy

3.Investment Prop - Sever Joint tenancy3.Investment Prop - Sever Joint tenancy

4.SMSF (Super Fund) -4.SMSF (Super Fund) - BDBN BDBN

(Binding Death Benefit Nomination(s)(Binding Death Benefit Nomination(s)

General Wills StrategiesGeneral Wills Strategies

• STRATEGIES – WILLSSTRATEGIES – WILLS (cont) (cont)ConcernConcern StrategyStrategy

Tax efficiencyTax efficiency Trust structureTrust structure

- income splitting properties- income splitting properties

- 102AG concessions for - 102AG concessions for minorsminors

Executors discretionsExecutors discretions

Ability for Ability for younger younger beneficiaries to beneficiaries to ‘fritter-away’ ‘fritter-away’ wealthwealth

Qualifying Age – eg 25Qualifying Age – eg 25

““Young Mens Young Mens disease”(beware “young disease”(beware “young ladies disease” as well !)ladies disease” as well !)

Estate conflicts – Estate conflicts – Loans Loans

Equalisation provisionsEqualisation provisions

SummarySummary

No two No two strategiesstrategies are the same are the same

No two Testamentary Trusts are the sameNo two Testamentary Trusts are the same

Strategy must be consistent and coherent across estate Strategy must be consistent and coherent across estate and non-estate assetsand non-estate assets

MustMust be a collaborative approach –Advisers/Lawyers be a collaborative approach –Advisers/Lawyers

Don’t forget Enduring Powers of Attorney /GuardianshipDon’t forget Enduring Powers of Attorney /Guardianship

SpecialistSpecialist strategy and intellectual property – no ‘one size strategy and intellectual property – no ‘one size fits all’fits all’

Thank You ! – Reminder – Optimal Thank You ! – Reminder – Optimal ProcessProcess

Any Questions ? Tel Alex Tees,Any Questions ? Tel Alex Tees, 0409813622 / 02 9281 3230 0409813622 / 02 9281 3230 [email protected] www.legalexchange.com.auwww.legalexchange.com.auProcess ;Process ;

1)1) Get Facts Straight – List Assets/PropertyGet Facts Straight – List Assets/Property2)2) Compare Notes with Clients Accountant, Compare Notes with Clients Accountant,

Financial PlannerFinancial Planner3)3) Interview to Confirm instructionsInterview to Confirm instructions4)4) Explanation/Signing InterviewExplanation/Signing Interview5)5) Optional Optional Family Meeting ?Family Meeting ?

Related Documents