Sustainable Investment SI Suisse 25 October 2006 ESN SI Methodology Guide Our original perspective • Environment – Social – Governance (ESG) initial risk exposure analysis in order to assess the value sharing process and its impact on value creation process (see p.16 and following) • Business model assessment with regards to sustainable development (SD) trends stated as a set of environmental and social trends (p.21) • Use of cutting edge business and academic literature (Steven Levitt, Jeffrey Sachs, C.K. Prahalad among others) in order to structure our analysis and to provide tools to assess social and environmental trends. • Examples of original items used in Environmental-Social-Governance ESG to focus on financial impacts (see glossary) Our product range • Online tool of companies corporate social responsibility ranking or involvement • Thematic research on deepening the analysis of one of the sustainable development trends or a major emerging or changing regulation • Sector research on the overview of environmental or social impacts on sales, assets or margins • Systematic company’s research with an integrated template on extra financial issues • In depth analysis of one company in order to assess the impact of one of the ESG dimension on value creation process or the impact of one or more trend of sustainable development on the company’s business model

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Sustainable Investment

SI Suisse 25 October 2006

ESN SI Methodology Guide

Our original perspective

• Environment – Social – Governance (ESG) initial risk exposure analysis in order to assess the

value sharing process and its impact on value creation process (see p.16 and following)

• Business model assessment with regards to sustainable development (SD) trends stated as a

set of environmental and social trends (p.21)

• Use of cutting edge business and academic literature (Steven Levitt, Jeffrey Sachs, C.K.

Prahalad among others) in order to structure our analysis and to provide tools to assess social

and environmental trends.

• Examples of original items used in Environmental-Social-Governance ESG to focus on financial

impacts (see glossary)

Our product range

• Online tool of companies corporate social responsibility ranking or involvement

• Thematic research on deepening the analysis of one of the sustainable development trends or a

major emerging or changing regulation

• Sector research on the overview of environmental or social impacts on sales, assets or margins

• Systematic company’s research with an integrated template on extra financial issues

• In depth analysis of one company in order to assess the impact of one of the ESG dimension on

value creation process or the impact of one or more trend of sustainable development on the

company’s business model

Sustainable Investment

Page 2

Table

ESN SI Methodology Guide .......................... ............................................. 1

Our original perspective

Our product range

Executive summary ................................. ................................................... 3

Why does ESN SI methodology target mainstream ..... ......................... 4

Overview of the market

Towards an ESN SI methodology

Theoretical foundations of SI ..................... ............................................... 8

Methodologies, mythologies, missed-ologies ?

Two ambiguous concepts: stakeholder and reputation risk

Why ESN SI methodology is different ............... ................................... 12

Benefits of ESN’s organizational structure

The four failures of existing methodologies… and our answers

How we want to work: ESN SI methodology ........... ............................ 15

Presentation of the ESN online tool on CSR ratings and initiatives by companies

Core dimensions of ESN’s SI approach: ESG analysis and SD

ESN SI template ................................... ..................................................... 17

Page 1: Fact s and figures

Page 2: Sustainable Development-Analysis

Scope of assessment and financial impacts ......... .............................. 25

Sector and company assessment

Financial impacts of sustainable development

Glossary .......................................... ........................................................... 28

Appendix: Comparison of CSR rating agencies methodo logies .... 31

ESN SI Methodology Guide

Page 3

Executive summary

The Sustainable Investment market is evolving quickly but it shifts further and further from its

morally grounded principles to a more sophisticated and integrated analysis. This shift

generates many distinctions and differentiations among the management syles and needs of

the different SRI funds.

ESN identified four cornerstones to set up a breakthrough in the Sustainable Investment

methodologies:

• separate clearly moral and financial implications of SI issues

• move the focus from transparency towards operational or long term economic

performance

• the integration into financial analysis will be done through clear and measurable

variables

• develop a top-down approach identifying impacts on the P&L or the balance sheet

Based on these methodology pillars, ESN introduce will introduce a diversified product range,

among other:

• an ESN online tool to identify companies rankings in the different sustainable

investment indexes and involvement in environmental and social initiatives

• a template systematically integrated in companies’ surveys enabling an assessment

of risk exposure of the company to environment-social-governance issues and an

analysis of the business model vis vis environmental and social trends

• Thematic research on deepening the analysis of one of the sustainable

development trends or a major emerging or changing regulation

Financial impacts of environmental, social and governance issues are described and the

different types of impacts are displayed with real examples.

The survey is concluded by a glossary of the items used in the template.

ESN SI Methodology Guide

Page 4

Why does ESN SI methodology target mainstream

Ethical funds strive to achieve two different targets: financial performance and improvement of

environmental social or ethical performance. The aim is to push companies to react to

economic (profit making) incentives, but also to social (taking into account such or such social

pressure) or ethical incentives (stop or start of a specific activity or practice).

The concept of Sustainable Investing, commonly abbreviated to SI, comprises investment

strategies in which investors do not base their asset selection decisions on financial criteria

alone anymore. In particular, they also take corporate governance, social and environmental

criteria into account. Below a short overview is provided of the historical development of

Sustainable Investing and the current size of the European SI market.

Overview of the market

• Historical development

Notwithstanding all the attention that has been drawn to Sustainable Investing during the last

few years, it is by no means a new phenomenon. At the end of the nineteenth century, certain

groups in the United States, primarily religious bodies, had already decided to let the world

know they were not prepared to invest in what they considered harmful businesses. Examples

are companies that produced or sold alcohol and tobacco or companies that made use of

child labour. In later years, other issues such as nuclear energy, gambling, manufacturing of

weapons and pollution were added.

The wave of interest in SI nowadays is largely a result of the various recently uncovered

corporate scandals of large corporations such as Enron or Parmalat. As a consequence,

many investors do not only care about a company’s financial performance anymore, but also

attach great value to its social responsibility.

The early, religion-based SI strategies mainly excluded potential companies (or sometimes

complete sectors) to invest in on the basis of a list with ‘wrong’ activities, but the

contemporary investor prefers to include companies that have adopted leading sustainable

policies and practices in his or her investment portfolio. This is called positive screening.

These investors are looking for companies that perform at the top of their industries on

sustainability issues such as environment protection, human rights and corporate

governance.

But not only investors are striving for more sustainable business practices. On a global level

the United Nations Global Compact, a voluntary initiative between companies and the United

Nations, encourages multinational corporations to initiate and especially share ideas and

actions to establish sustainable globalization. In this way socially responsible practices can be

spread around the world. Companies participating in the Global Compact must adopt ten core

values in the fields of human rights, labour standards, the environment and anti-corruption.

Examples are respecting the protection of international human rights, the elimination of

discrimination within the company, and encouraging the development of more

environmentally friendly technologies.

ESN SI Methodology Guide

Page 5

Furthermore, the United Nations Principles for Responsible Investment cover issues like

incorporating non-financial criteria into the investment decision and were signed this year by

thirty-nine institutional investors and thirty-six large investment companies.

• Definitions of core and broad SI

In practice, two broadly recognized approaches have evolved over the last years: core and

broad SI. The main difference between core and broad SI concerns the SI strategies that the

two measurements include. Core SI only comprises investors who use so-called ethical

exclusions and/or positive screening. Broad SI also includes investors who implement simple

exclusions, which means excluding single given sectors, and investors who enter into

dialogue on issues of concern with the companies they invest in. This is called engagement.

Furthermore, the explicit inclusion by asset managers of non-financial risks into the

conventional financial analysis, called integration, is included. The figure below clarifies this

distinction.

The difference between core and broad SI

Source: Eurosif (2006)

• Size of the European SI market

Both the core and the broad SI market experienced substantial growth over the past two

years, even after correcting for the overall growth of the entire equity market. Compared to

the general investment market Sustainable Investing still represents much growth potential.

Although the development started somewhat later in Europe than in the United States, the

European market for SI is currently quite advanced. According to a recent study by the

European Social Investment Forum (Eurosif), an umbrella association that covers sustainable

investment issues at the European level, over EUR 1 trillion is invested in Europe taking

sustainability criteria into account. This is only the case when a broad measure of SI is

considered. The size of the core SI market is estimated to be EUR 105 billion. Moreover,

national differences with respect to the scale and scope of Sustainable Investing are large

(see the figure below).

Ethical exclusions

Positive screens, including best-in-class and pioneer screening

Simple exclusions, including norms-based screening

Engagement

Integration

Co

re S

I

Bro

ad S

I

ESN SI Methodology Guide

Page 6

Size of core and broad SI in several European countrie s (in billion Euros)

Source: Eurosif (2006)

The figure above shows the sizes of the core and broad SI markets in a number of European

countries. As becomes clear, The Netherlands is the leading market in core SI with assets

under management of EUR 41.5 billion. This is mainly due to the heavy presence of the

Dutch pension fund PGGM, who is one of the members of the Enhanced Analytics Initiative.

The United Kingdom has the second largest core SI market with assets under management

worth EUR 30.5 billion. Church and charity investors are still the most important players in this

market. Furthermore, the UK broad SI market is by far the largest of all European countries

considered, mainly because of the investments by occupational pension funds. Except for

Belgium, Sustainable Investing is still much less pronounced in the other European countries

under consideration, but as explained before the growth potential is substantial.

Possible reasons for the differences in size across countries are the different historical

backgrounds of the market and the varying degree of activism of early investors. For

example, Sustainable Investing can be traced back in the United Kingdom at least to the

1920’s.

Towards an ESN SI methodology

• The need for SI research

In response to the increased interest of investors in Sustainable Investing, currently more SI

research is being carried out than ever before. Many specialized SI research companies

emerged during the last decade and an increasing number of research departments of

traditional investment banks are employing one or more SI analysts nowadays. This latter

trend is partly the result of the demand from large institutional investors.

13

7

25

9.58.2

2.9

41.5

1.5

30.5

1.2

13.8

5.3

2.9

47.5

7.5

0

10

20

30

40

50

60

Austria Belgium France Germany Italy The

Netherlands

Spain Sw itzerland United Kingdom

Core SI Broad SI

149 781

ESN SI Methodology Guide

Page 7

To provide mainstream brokers with an incentive to write innovative research on social,

ethical and environmental issues, a group of leading European institutional investors initiated

the Enhanced Analytics Initiative (EAI). To show the urgent need they have for the integration

of sustainability issues into traditional investment research, the EAI allocates up to five

percent of its commission budgets to brokers publishing high quality SI research. All relevant

research reports are evaluated semi-annually by an independent consulting agency to decide

which brokers qualify for the commissions. Some examples of members of the EAI are ABP

Investments (The Netherlands), BNP Paribas Asset Management (France), PGGM (The

Netherlands), RCM (United Kingdom), which is part of Allianz Dresdner Asset Management,

and Universities Superannuation Scheme (United Kingdom).

So definitely there is a need among large institutional investors for research companies

analyzing and processing information that is frequently not taken into account by the

traditional financial analysis.

• ESN’s point of view: SI is also relevant for mainstream investors

The regional differences of each market certainly complicated the development of a common

ESN SI methodology that fits each member country’s SI market, but after many meetings and

discussions the ESN SI team finalized this methodology document, which shows in great

detail our approach to Sustainable Investing research. The coming sections will explain what

makes our methodology unique and, on a more practical level, how the ESN SI team wants to

work in the future.

In our opinion, information regarding the sustainable development policy of a company is

valuable for all investors, because this information is necessary, just as financial performance

data, to have a complete picture of how a company is doing and where its future risks and

opportunities lie. Many sustainability issues can potentially have large impacts at a company’s

operations. For example, companies using environmentally unfriendly production techniques

or neglecting the needs of their employees might be heavily criticized by environmentalists or

trade unions, which can dramatically reduce their reputation and the demand for their

products or services. As a second example, companies where employees have to work in

unpleasant circumstances might find that their employees lack motivation and productivity,

thereby increasing labour costs. Moreover, the impact of corporate scandals like the ones we

experienced the last few years (e.g. falsification of balance sheets as seen in case of Enron

and Parmalat) would probably have been much smaller if corporate governance issues had

been analyzed more thoroughly.

So the way in which a company manages the above and many other sustainability issues

should be a point of concern to every investor. It is very important to gather information on

which companies’ operations are most sustainable and where each company’s strengths and

weaknesses with respect to sustainability lie. Only in this way investors can identify both

potential sources of risk and opportunities related to corporate governance practices, social

and environmental issues, and anticipate on possible changes in a company’s (legal)

environment.

ESN SI Methodology Guide

Page 8

Theoretical foundations of SI

There is no way and no need to reinvent an absolute methodology satisfying all needs of

information of SI and mainstream investors. But there is a need to develop a methodology

analysing and processing informations which are not necessarily taken into account by

financial analysis to enrich and deepen it. The aim of such an analysis is to provide

recommendations on companies or sectors that will generate higher value in the long run.

Methodologies, mythologies, missed-ologies ?

Methodologies have been developed for 20 years on sustainable investment and non

financial data. This methodology cannot be ignored, but there is a growing concern about

these works. Are they missed-ologies, mythologies, methodologies?

• Missed-ologies

To begin with, two remarks about “missed-odologies”. SI despite the great research it has

generated has missed opportunities to be considered as a key methodology for financial

markets. Many opportunities have been missed by the SI community and its methodology.

Everybody mentions Enron as a problem, but it has not been pointed as deficient by SRI

investors. It could have. For instance this company had one of the most accomplished CSR

report with disclosure of its CO2 emissions. No SI analyst asked to its financial counterpart

how the company could generate sales with generating CO2. The same demonstration could

be done for Parmalat, Worldcom, Ahold, …

A second issue is the spreading of the potential SRI intuition. Alstom had been identified as

problematic due to its poor employees and customers‘ relationships in 2001 that is a year

before problems popped up. However, it was not considered in the financial community as so

catastrophic as it happened in 2003. By the way the mention of poor employees’ relationships

is not anecdotic as the first decision of Patrick Kron, as new Alstom CEO, was to change its

Human Resources Director.

• Mythologies

Mythologies refer to the belief underneath sustainable investment. Based on the sentence of

John Stuart Mill “One person with a belief is equal to a force of ninety-nine who have only

interest”, some SI investors strive to focus on companies “with belief”. Beyond the discussion

of its relevance, the implementation of it as an investment choice raises two questions:

• How to measure the belief? This raises the problem of the way to measure it?

Intention, implementation, results? This question shows that these methodologies

turn to be very interpretative.

• Which belief should be measured? This raises the problem of what should be

measured? Is it a belief in new activities, new technologies, new practices? These

questions do not only refer to marketing questions about investment style or

opportunities. It also refers to strong beliefs. There is some strong similarities

between the set of investment guidelines of US and UK “ethical funds”.

ESN SI Methodology Guide

Page 9

SI was theoretically based on the assessment of Corporate Social Responsibility. As

explained in the Appendix, this measurement is extremely complex for the reasons given

earlier.

• Methodologies

After the discussions of mythologies, we would like to insist on the need to focus on the “DO“

part of the word “methodology. The methodology should not be purely theoretic. It should

rather be used as a framework for frequent production ready to be integrated in financial

analysis. It should be reactive and easy to modify in order to enable reactive studies and

possibility to change.

The “DO” part of the methodology should enable to frame the analysis according to the

different incentive it relies upon (economic, social or ethical) Therefore our scheme should

enable us to split the different incentives, and moreover to treat any issue with potential

economic impact. The aim of the framework is to provide a flexible frame to analyse any

company or any sector, and further on any event.

Two ambiguous concepts: stakeholder and reputation risk

For a deep comparative analysis of CSR rating methodologies, please refer to the appendix.

Apart from the CSR rating agencies, a lot of consultants and advisers have been giving the

opinion on corporate social responsibility and its potential impact on financial performance.

This literature is based on two concepts: stakeholder and reputation risk.

To make it short, every stakeholder that may consider to be impacted by the company should

have a word to say as this may impact the company in the short or in the long run.

This idea looks generous but clearly lacks of consistency. These two concepts mix moral and

economic issues and lack of economic relevance.

A first overview of the use of the concept is provided by the following table (next page), where

all potential grievances or demand by stakeholders are listed per sector. This looks interesting

for a company or for student, but this overview raised two questions. Do these challenges

have any financial impact? Are all these issues really important, beside external

communication?

As stated earlier, these issues might not be irrelevant but they are not necessarily the most

important ones. Therefore ESN SI team will stick to more pragmatic methodology.

Stakeholder theory is the philosophical stone of SI analysis. This concept of stakeholder is

taken as such by methodologies without measuring clearly what it encompasses. It might also

referred in a milder way as external pressures, social pressures, and it implies that the

stakeholder is taken into account as such by the investor and by the companies it invests in.

It has been strongly criticised in its early days by Milton Friedman on ideological grounds.

More recently it has been criticized by authors on methodological grounds. As stated by

Antonacopoulou & Meric1, the stakeholder theory was first a instrumental discourse for crisis

management before turning into a management philosophy. However as these authors point

1 Antonacopoulou & Meric, 2006

ESN SI Methodology Guide

Page 10

out, the stakeholder theory is reductive (as it reduces the issue to stakeholders enabled to

build contracts with companies), normative (as stakeholders’ demands are considered

simultaneously with their own legitimacy and integrable in the corporate strategy).

The second useful definition is the definition of risk provided by Peter Sandman2. He defines it

as a twofold concept, including hazard (itself combining probability and impact) and outrage

(that could be described by other authors as “perceived risk”).

Risk = Hazard + Outrage

Sandman insists that they are different targets and tasks to reduce each of them. In other

words, reducing the danger does not necessarily reduce the hazard and vice versa.

Stockholder’s demands refer to outrage, instead of danger. A company may not address both

issues simultaneously. For example, BP has disclosed heavy investment plans in bio fuels but

has severely neglected its investment in refineries until its accidents in US refineries in 2005

and in Alaska in summer 2006.

Collective layoffs in France are another good example of the distortion of analysis introduced

by stakeholder and outrage. First in 2005, collective layoffs represented merely 30% of total

layoffs. 25% of layoffs end up in legal proceedings (usually won by employees). Therefore the

outrage focus is on termination fee and financial reserves whereas the risk question is more

on the employability and the personal development of employees.

2 In Levitt: Freakonomics, 2005

ESN SI Methodology Guide

Page 11

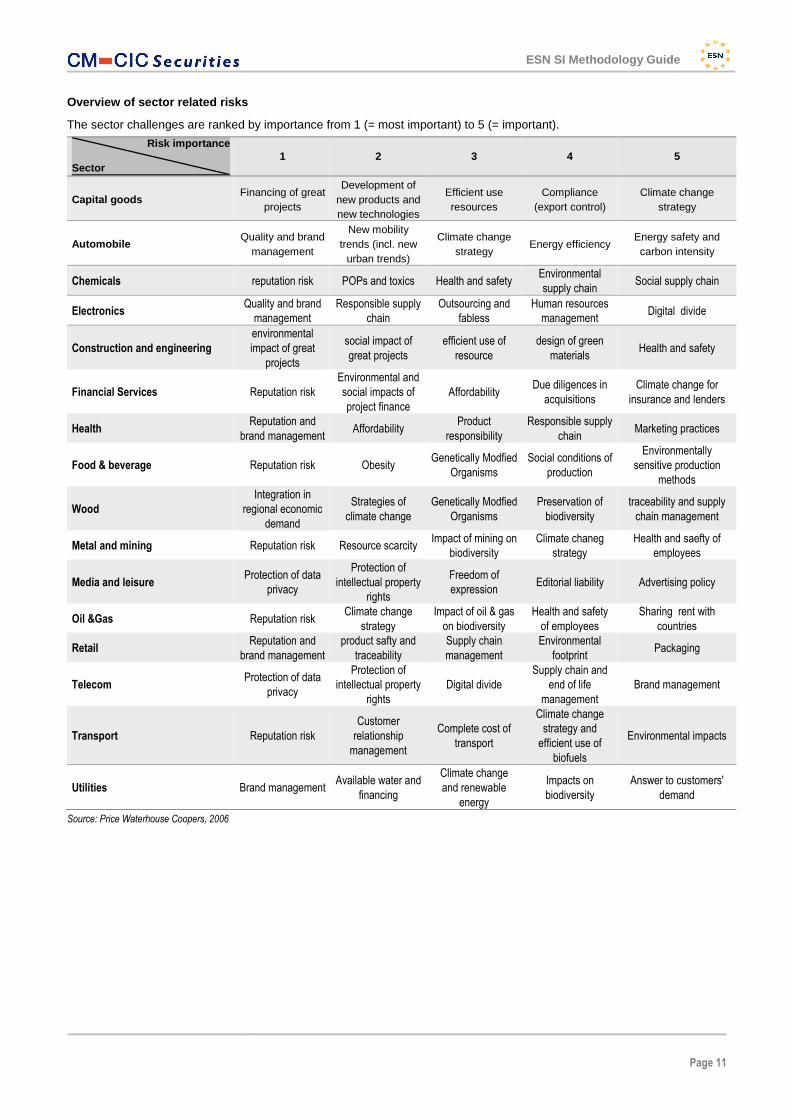

Overview of sector related risks

The sector challenges are ranked by importance from 1 (= most important) to 5 (= important).

Risk importanc e

Sector

1 2 3 4 5

Capital goods Financing of great

projects

Development of new products and new technologies

Efficient use resources

Compliance (export control)

Climate change strategy

Automobile Quality and brand

management

New mobility trends (incl. new

urban trends)

Climate change strategy

Energy efficiency Energy safety and carbon intensity

Chemicals reputation risk POPs and toxics Health and safety Environmental

supply chain Social supply chain

Electronics Quality and brand

management

Responsible supply

chain

Outsourcing and

fabless

Human resources

management Digital divide

Construction and engineering

environmental

impact of great

projects

social impact of

great projects

efficient use of

resource

design of green

materials Health and safety

Financial Services Reputation risk

Environmental and

social impacts of

project finance

Affordability Due diligences in

acquisitions

Climate change for

insurance and lenders

Health Reputation and

brand management Affordability

Product

responsibility

Responsible supply

chain Marketing practices

Food & beverage Reputation risk Obesity Genetically Modfied

Organisms

Social conditions of

production

Environmentally

sensitive production

methods

Wood

Integration in

regional economic

demand

Strategies of

climate change

Genetically Modfied

Organisms

Preservation of

biodiversity

traceability and supply

chain management

Metal and mining Reputation risk Resource scarcity Impact of mining on

biodiversity

Climate chaneg

strategy

Health and saefty of

employees

Media and leisure Protection of data

privacy

Protection of

intellectual property

rights

Freedom of

expression Editorial liability Advertising policy

Oil &Gas Reputation risk Climate change

strategy

Impact of oil & gas

on biodiversity

Health and safety

of employees

Sharing rent with

countries

Retail Reputation and

brand management

product safty and

traceability

Supply chain

management

Environmental

footprint Packaging

Telecom Protection of data

privacy

Protection of

intellectual property

rights

Digital divide

Supply chain and

end of life

management

Brand management

Transport Reputation risk

Customer

relationship

management

Complete cost of

transport

Climate change

strategy and

efficient use of

biofuels

Environmental impacts

Utilities Brand management Available water and

financing

Climate change

and renewable

energy

Impacts on

biodiversity

Answer to customers'

demand

Source: Price Waterhouse Coopers, 2006

ESN SI Methodology Guide

Page 12

Why ESN SI methodology is different

Benefits of ESN’s organizational structure

Driven by the demand from (institutional) investors and the growing sustainability awareness

among society in general and corporations in particular, ESN (the European Securities

Network) now presents its SI methodology. ESN is a strategic partnership in the equity

brokerage activities of ten leading banks & securities houses. So ESN is very well capable to

evaluate SI issues in a multi-domestic context. Each partner intends to provide in-depth

research on current national sustainability matters so that this information can help as many

investors as possible in making their investment decisions. In this way investors can optimally

take advantage again of the multi-domestic character of ESN. In order to write research on SI

subjects, ESN created a SI team consisting of analysts fully or partly allocated to that subject.

The four failures of existing methodologies… and ou r answers

Based on the overview of existing methodologies (for further details, see Appendix) we can

clearly identify the four mistakes done so far and provide our own answer.

The four failures and our answers

Source: ESN SI Team

• Failure 1: Mixing different targets

The first failure of CSR rating agencies is to mix the different targets focused by the SRI

funds. As discussed in the first part, these funds have a financial target and a moral or social

aim.

A recent book, “Freakonomics” written by Steven Levitt, is of high interest to understand the

lack of grip of CSR rating methodologies. Every human being answers to different incentives.

The problem is to be fully aware of the different types of incentives we rely upon, and not to

mix them up. For instance, replacing moral incentives by economic incentives is not always

relevant. Steven Levitt provides the example of this kindergarten where parents came late to

pick up their children. The kindergarten then decided to fix a 3£ fine per delay. The parents

were then relieved from their moral obligation to pick up their children. Delays multiplied, and

when the fine was raised to higher levels, the delays’ rate stayed high. Giving a (always too

#

1• Mixing different targets (Economic, Environmental, Social)

2• Transparency is in focus

3• Assume that CSR's impact as a whole is easy to measure

4• Accounting for all potential stakeholder grievances

Source: ESN SI Team

• Analyse targets' characteristics• Focus on targets driven by economic incentives and analyse their financial impacts

• Focus on operational and long-term performance to account for potential economic impacts• Exclusive application of clear and measurable variables

• Clearly identify potential financial impacts of the extra-financial dimensions

AnswerFailure

ESN SI Methodology Guide

Page 13

low) price to something that does not have one might disable to achieve the target and might

as well pervert the system.

At corporate level, one might raise inspiring questions based on this example, developed in

the ESN survey “Looking at quotas under every angle”. So far the price is much too low to be

economically incentive for European companies. There is a need either to increase the price

(for example by restricting the amount of allowances) or to reintroduce moral or social

incentives (such as stringent regulations) to simply make it work. Although we are keen to the

market we are aware that market can not solve all issues.

Our answer: In a broader picture, every research on SI issues should answer first the

question whether the target is moral or economic. Then the survey should focus (or at least

include one part) on economic incentive, and its subsequent financial impacts.

• Failure 2: Transparency is in focus

The second failure of CSR rating agencies is to focus on transparency. This has induced a

bias in the selection of companies. The majority of SI funds or SI indexes are based on a

reduced set of large caps. This has an impact on its performance. Beyond transparency,

there are many other issues that could be targeted:

- Operational performance: some processes or managerial procedures may improve the

way a company operates its plants; for instance, a quality certification may reduce the

defaults or delays in a production or delivery process.

- long term performance: the exact assessment of land remediation issues in a company

may lead to the estimation of financial reserves; for example, in 2004, Rio Tinto had to set up

a provision of 250m £ in order to remediate land pollutions in Indonesia and its further

consequences.

Our answer: The set of information provided by our research should focus on operational

performance and long term performance that contain more potential financial impacts than the

search of transparency itself.

• Failure 3: Assume that CSR’s impact as a whole is easy to measure

The third failure is to rely on a belief that CSR performance as a whole has an impact on

financial performance as a whole. This assumption implies that CSR can be measured in an

integrated and standardised way.

A seminal paper written by Margolis and Walsh has demonstrated that these links were not

that simple. They suggest to be more modest and to first deepen research on linkages with

clearly defined variables such as sales, margin, assets or possibly stock price, for financial

performance and staff turnover, environmental management systems, or independence of the

Board for extra financial issues.

Our answer: The integration into financial analysis will be done through clear and

measurable variables, and will not use the easy to manipulate concept of WACC to integrate

extra-financials into financials.

ESN SI Methodology Guide

Page 14

• Failure 4: Accounting for all potential stakeholder grievances

The fourth failure is to rely on stakeholder issue and to try to collect all potential grievances.

This bottom up approach has two drawbacks. First it lacks of structure and hierarchy and

second it is quickly overloaded by local particularities of the different markets and countries.

For local companies, there are local stakeholders. How can we identify global stakeholders?

Our answer: Our methodology is based on a top down approach that clearly identifies from

the P&L or from the balance sheets the potential impacts of the different extra-financial

dimensions.

ESN SI Methodology Guide

Page 15

How we want to work: ESN SI methodology

Based on the methodology pillars explained in second part we will describe how we structure

our corporate SI analysis. In the preliminary section we will explain the online information

service we will deliver on all European companies.

Moreover, we describe our SI template that will be included in all reports published by ESN.

The template enlightens how extra financial issues will be assessed and structured into 2

separate parts: one on facts and figures, displaying the risk exposure to environmental, social

and governance issues, and the second on sustainable development trends,.

The second section explains how sector and corporate issues are connected, and how to

process SI information into financial analysis.

Presentation of the ESN online tool on CSR ratings and initiatives by

companies

As stated in the previous paragraph, as a broker, the only way to assess companies is to

assess them according to financial estimates, although we may integrate different items in the

assessment. We will not try to rank companies according to morality.

Regarding moral and social initiatives of the companies, we provide an information on

corporate disclosure and involvement. Our on line “responsibility spreadsheet” displays for

every company of the Stoxx 600, its inclusion in the major European sustainability indexes

(ASPI, DJSI Europe, FTSE4Good Europe) and its involvement in the major responsibility

initiatives (to begin with, Global Compact and Principles of Responsible Investment).

This spreadsheet will be updated monthly, including

• A range of CSR initiatives that will be increased upon opportunity.

• A set of information collected in a specific spreadsheet on alcohol sales, military

sales, gambling sales, tobacco sales, and nuclear production (for utilities)

Core dimensions of ESN’s SI approach: ESG analysis and SD

This SI analytical template will be included in every “company report” published by ESN. It is

made of Environmental Social Governance analysis, a Sustainable Development framework

and a comment on some exclusion activities.

Environmental – Social – Governance (and its acronym ESG) has been emerging in the

wording of SRI and extra financial as a reduction of SRI wide scope, influenced by a wide

range of stakeholders to the “material” impacts. In this ESG analysis we will assess the risk

exposure of company to this issue. In case one issue seems risky for the company it should

be pointed out in the comment, and logically should be integrated in the valuation step of the

company.

This template aims at identifying hidden items or hidden dynamics in the company before

focusing on financial analysis. This approach is inspired by the clinical economics framework

ESN SI Methodology Guide

Page 16

developed by Jeffrey Sachs, in its last book “The reduction of poverty”. Jeffrey explains that

before realising a traditional macroeconomic analysis of a country it is necessary to analyse

its geography, demography, transport infrastructure and … All these dimensions would be

summarised in a short template of things to know before proposing a standard scheme.

Similarly the aim is to build up a framework of clinical management, where the analyst could

pick up important information before building its valuation model and foreseeing the business

strategy of a company. This template enables an assessment of value sharing process of

the company and its potential consequences on the value creation process .

We see the ESG-criteria named above as the basis of our SI-research as we believe them to

be the decisive drivers for a greater economic benefit of a company if they are widely fulfilled.

Moreover, the three pillars have become more and more established, not only in the literature,

but also in day-to-day practice.

The strategic objectives behind the three dimensions ought therefore to be an important

element of corporate thinking and conduct and support the search for concrete solutions.

Implementation of our criteria can help, for instance, to secure reputational advantages over

competitors, and thus financial benefits, and can therefore be regarded as a strategy aimed at

competitiveness.

ESN believes that these three SI dimensions should not be viewed in isolation but need to be

considered together in a common context since the respective sub-disciplines interact with

each other. The following diagram summarizes these interrelationships:

Core dimensions of ESN’s SI Research

Source: ESN

For example, in July 2006, Faurecia has been involved in a controversy on bribery with some

German carmakers. Apart from any moral considerations, this controversy revealed the high

dependency of Faurecia on a few clients. Volkswagen, for example represented in 2005 22%

of Faurecia’s sales. The controversy had an unexpected consequence in corporate

governance when the CEO was pushed to resign because through the reporting systems he

knew about the bribery system although it had been implemented prior to his nomination as

CEO.

Source: ESN

ESNSI Approach

Ecologicalaspects

Social aspects

Corporate Governance

aspects

ESN SI Methodology Guide

Page 17

ESN SI template

As described above the ESN SI template is made up of a two-fold structure covering relevant

SI issues from the field of ESG analysis: 1) facts and figures and 2) sustainable development

trends. After having identified the three dimensions of analysis we took an in depth-look at the

potential issues to be analyzed. This analysis was conducted in cooperation with various

universities in different ESN partner countries: among others our scope of analysis is based

on specialists’ knowledge gathered at e.g. the University of Applied Sciences of Osnabrück,

the University of Mannheim (both Germany) and at University of Tilburg (Netherlands) and

therefore satisfies theoretical criteria as well as practical needs.

Page 1: Fact s and figures

The underlying thought was to identify such questions which are a) meaningful, b) obtainable

and c) apply on a cross-national level. In the following we provide an overview of when we

regard an issue to fulfill those criteria.

• Is the information meaningful?

In our view, an issue is meaningful if it helps to identify companies which do better in terms of

sustainable behavior than others. In other words: an issue which is fulfilled by a broad number

of companies has only a limited explanatory power, whereas such ESG-issues which are

complied with by only a handful of companies help to filter the “good ones”. Hence, the

meaningful criteria enable the reader to automatically get a feeling whether the company

under investigation can be classified as a sustainable leader, a follower or even a non-applier

of the corresponding sustainable management systems and policies.

• Is the information obtainable?

In order to make a comparison with other companies possible, regardless which sector these

belong to, we have paid close attention to the availability of data for the issues of analysis.

Thus, our selection is principally based on information which is a) obtainable in the annual

reports, b) on a company’s homepage or c) in the corresponding sustainability reports

published by a company which mostly comply with international standards such as the Global

Reporting Initiative. Thus, the data can be obtained by consulting publicly available

information helping to avoid a subjectivity bias which is likely to arise when contacting a

company directly.

• Does the information apply on a cross-national level?

As ESN is a strategic partnership in the equity brokerage of ten leading different banks and

securities in Europe our clear aim was to ensure that the issues of our sustainability analysis

can be applied on a cross-national level. Hence, we avoided to filter only those issues which

are of strong interest in just one member country. Thus, our selection represents issues which

do not only stand in the ESG focus in some of the partner countries, but in all of them.

However, we would like to point out that our ESG template consists of a twofold structure:

while the majority of issues to be analyzed is binding for all ESN partners, each member is

free to analyze a maximum of up to X issues in each of the three dimensions which are not

covered by the overall content of the template (for further details please refer to pages XXff.).

The ESG template is displayed below.

ESN SI Methodology Guide

Page 18

Governance Shareholders

Double voting right (Y/N)

Comment

Shareholder's agreement (Y/N)

Free Float (%)

Others shareholders holding more than 5% of capital (%)

State (%)

Administration

Combined CEO / Chairman (Y/N)

Comment Number of Directors (board)

Number independent Directors (disclosed)

Compensation

CEO compensation (excepted SO) (€)

Comment

Variable part in CEO compensation (%)

Executive Committee total compensation (excepted SO) (€)

In which, variable part (%)

Compensation of non executive (€)

Stocks options

Total in circulation

Comment

Stock options restricted to CEO (€)

Average weighted price (€)

SO dilution (31/12/2005) total (%)

Control Audit fees/ fees to auditor (%)

Comment Number of consolidated companies

Source: ESN

Environment and Social Reporting CSR Report (Y/N) Code of Conduct (Y/N)

Supplier’s screening system (Y/N) Global or Sector Initiative (eg. Global

Compact) (Y/N)

Source: ESN

Social Employees R&D

Number of employees R&D (% of sales)

Gender diversity (% woman) Cumulated R&D (% of fixed assets)

Average age of employees (years)

Wages (% of sales) Customers & Suppliers

Average remuneration per employee retreated from management compensation (€)

Sourcing (% sourcing/sales)

Sales to local/national governments (% )

Pension liabilities (€) Warranty cost (€)

Source: ESN

Environnement Major environmental impact (Production/Use/Recycling)

Env. Management System / certification (ISO14001/EMAS) (% )

Raw materials (% of sales) Water consumption (m3)

Energy consumption (kWh ; Tep …) Waste production (t)

Energy Cost (% of sales) CO2 Emissions (t)

Source: ESN

For every ESG dimension, the analysis describes how we evolved from traditional ESG

reporting questions towards ESG analysis.

ESN SI Methodology Guide

Page 19

• Governance

In the traditional corporate governance reporting, the issues would focus on these issues.

Governance reporting at a glance

Corporate

Governance

conduct

• Upholding the company's credibility and enhancing its image, thus building reputation capital,

• Improving management and supervisory board decision quality and control by liability being assumed for the

consequences of gross management errors,

• Greater transparency by applying international accounting standards, introducing segment reporting and holding

regular analyst meetings,

• Social legitimation of the company.

Source: ESN SI team

In recent years, Corporate Governance has received a great deal of attention on a global

scale. This has been sparked not least of all by a raft of company failures in Europe and all

over the world that were directly the result of mismanagement and shortcomings in the

supervision over management's conduct of the company's affairs. The most prominent cases

were Enron, Worldcom and Parmalat.

Reporting on Corporate Governance lacked of an appropriate extent and precision for quite a

long time. Hence, it was above all voluntary initiatives or standards set by a number of

countries such as the ‘OECD principles’ to pave the way for a legal framework addressing

Corporate Governance as an essential part of a company’s yearly reporting. In the meantime,

a corresponding code or even laws have been passed in nearly all major capital markets of

the world. Thus transparency regarding the Corporate Governance quality of companies from

different sectors and/or countries has increased by far over the past years.

Therefore, in ESN SI analysis, governance issues are broken down into four issues.

• First there is a need to understand the structure of shareholding (such as the

existence of different shareholders such as state, the existence of a shareholder’s

agreement or double voting rights).

• Second the composition of the Board enables to identify the potential conflict of

interest between different Board members. The problem may be the existence of

Board directors representing the potentially conflicting interests with the ones of the

company. If it is the case that a Board Director represents either a competitor (e.g.,

Nokian Renkaat and Bridgestone), or a predatory client (e.g., Aegis and Bolloré) or a

shareholder with diverging interests (e.g. Vivendi and Vivendi Environment in 2001)

or if Board Directors that may mainly contradict themselves block any strategic

decision (e.g., doubts on Alcatel Lucent).

• Third the remuneration issue is focused on three potential impacts: 1) abnormal

remuneration of Executive Directors: when remuneration is not related to corporate

performance or when related to inconsistent performance indexes. 2) Dilution of

stock value through the attribution of stock options.

• Fourth and last the control issue enables to check the potential difficulties of internal

control through the number of consolidated companies or the discrepancies of

external audit, e.g. in the case Enron.

ESN SI Methodology Guide

Page 20

Beyond these standard questions, corporate governance might be the most frequent issue in

the analysis. As stated in “Freakonomics”, white collar crime is expected to rise as the control

systems are much lower than the economic incentive to cheat (as previously mentioned

scandals – Enron, …- prove it).

• Social

In the traditional corporate governance reporting, the issues would focus on these issues

Social reporting at a glance

Social conduct

• Advantages in the recruitment market in attracting highly qualified personnel and building stronger loyalty of

existing human capital,

• Enhanced efficiency through improvements on the social front (e.g. employees concentrate better if their work-life

balance is more rounded, resulting in fewer defects in production and thus higher product quality),

• Increased productivity as a result of greater employee satisfaction,

• Lower rates of absenteeism through measures to promote health and to prevent accidents.

Source: ESN SI team

Any company which sees itself as a responsible corporate citizen should also report on its

social management and related activities. Here, the maxim “Do well and talk about it“ applies.

Reporting on the company’s commitment to its employees, the local community and global

development is information which is relevant both for investors and for critical stakeholders.

If this information is withheld from the public, this can lead to a critical perception on behalf of

the public, and especially of critical stakeholder groups, possibly seeing the company’s

activities in a wrong light. This, in turn, can have an adverse effect on sales.

Therefore, in ESN SI analysis, social issues cover three areas of interest:

• First there is a set of questions to assess in a gross idea of the amount, the age and

the gender of employees and its financial impact on the profit & loss sheet (wages)

as well as in the balance sheet (provisions for retirement expenses). Company’s

employees represent one of the most important assets. High employee satisfaction

and employee loyalty can have a positive effect on company’s earnings by

increasing productivity. Also, high employee satisfaction can reduce the probability

of attacks from stakeholders like trade unions and NGOs.

• Secondly, there is a set of question to understand the mount of the brand, the impact

of R&D (again in the P&L as in the balance sheet) and so on the existence of brand

in the intangibles. The social performance of suppliers which is the crucial point for

stakeholder attacks is illustrated because the sourcing of goods from suppliers

aggravates a company’s ability to guarantee social proper working conditions. These

improper working conditions can result in negative customer reactions and

decreasing revenues. Also, customer structure, e.g. a high dependence from state

orders may influence a company’s behavior and damage its reputation in case of

corruption.

• Third point is the investment for Research and Development, which affects a

company’s ability to realize profits in the long-run.

ESN SI Methodology Guide

Page 21

• Environment

In the traditional environment reporting, the issues would focus on these issues:

Environmental reporting at a glance

Environnemental

conduct

• Compliance with existing and anticipated requirements and laws, thus avoiding potential litigation costs,

• Positive effect on a company’s image,

• Lower production costs as a result of more energy- and resource-efficient production through the use of

environmentally friendly processes,

• Safeguarding intact surroundings (e.g. healthy environment) as a precondition for business activity,

• Competitive advantages over rivals through environmental commitment in markets where products and services

are becoming more and more similar.

Source: ESN SI team

Based on this reporting scheme, the risk of a company’s business activities having a negative

impact on the environment is far greater in producer/manufacturing industries than at banks

or software companies for instance. So it is understandable, owing to the lower stakeholder

expectations, for banks or software firms to report less about environmental performance at

their locations.

Indirect reputation risks for banks can be far greater which can result from financing projects

with a potentially harmful environmental impact. However, as the impact arising at the bank’s

own locations is less complex and extensive than for companies in producer/manufacturing

industries, the reporting will obviously be on a comparatively smaller scale. In the case of

services companies the stakeholder focus is less on the environmental impact at the

company’s own operations and more on the effects of its business decisions.

Therefore, in ESN SI analysis, environmental issues are broken down into two major

questions:

• The first question refers to the step of the life cycle of the product where the major

environmental impact happens. It refers to simple environmental classification:

production, use or recycling, ad enables a first assessment of the financial impact of

environmental issues.

• The second question refers to the basic environmental impacts of a company (water,

energy, waste) and its basic control. Depending on the business of the company

environmental issues realize differently, e.g. a manufacturer affects the environment

much more by its operations than a retail company. This fact can also be read from

environmental performance indicators, such as CO2-Emissions or water

consumption. The higher the environmental impact of a company’s operation is the

higher the need to invest in environmentally friendly production technologies will be

in the future. Also, stakeholder attacks against companies that pollute the

environment combined with increased consumer perception can decrease revenues.

An important part of a company’s responsibility towards a proper handling of environmental

issues is the implementation of an appropriate management system, whose systematic

conduct reduces the probability of lawsuits and negative reactions from customers which

could result in decreasing revenues.

ESN SI Methodology Guide

Page 22

Page 2: Sustainable Development-Analysis

The concept of sustainable development originates from the so called Brundtland report,

which was published under the title “Our Common Future” by the World Commission on

Environment and Development, also known as the Brundtland Commission in 1987.

According to the Brundtland report sustainable development is closely linked to three different

categories, namely the social, environmental and economic dimension.

The most recent text from the United Nations – the World Summit Outcome Document –

dates back to 2005 and refers to the "interdependent and mutually reinforcing pillars" of

sustainable development as economic development, social development, and environmental

protection.

There is a need to separate Sustainable Development from ESG analysis. Sustainable

Development is a set of long term trends and as such refer to intergenerational balance. As

demonstrated by Rawls, there is no possibility to achieve an intergenerational equilibrium by

contractual means only because there is a need of moral grounds and incentives. Therefore

we will consider sustainable development issues as long term issues based on moral

incentives with potential economic impacts (not necessarily in the long run).

Based on the work provided by various international institutions (among others, the United

Nations and the World Resources Institute) we will consider sustainable development as a set

of eight long term trends.

Set of sustainable development trends

1. AGEING POPULATION • Answering to the new needs of population

• Adapting its workforce to ageing employees

2. GLOBALISATION • Developing global supply chain and sales

• Managing global supply chain and the process acceleration

3. GLOBAL POLLUTIONS • Fighting climate change

• Fighting acid rain and other global pollution (ozone layer, oceans),

4. NEW POWERS IN THE SOCIETY • Defining a new relation with government and fighting corruption

• Answering to the rise of NGOs

5. REDUCTION OF POVERTY

• Seizing the opportunities of bottom of the pyramid

• Answering to specific needs of poor employees or poor

neighbouring populations (availability of basic services)

6. RESSOURCE DEPLETION & LOSS OF BIODIVERSITY • Increasing resources efficiency

• Protecting biodiversity

7. RISE OF PRIVACY & SEARCH OF IDENTITY • Protecting individual identity

• Respecting tribal rights to land and customs:

8. HEALTH • Occupational health in a long range perspective

• Global Health issues (AIDS, malaria)

Source: ESN SI Team

As stated by Al Gore in his conferences and movie “An unconvenient truth”, there is not “one

trend explaining everything”, but rather a set of potentially contradicting trends to which

companies should answer if they want to survive in ten to twenty years.

ESN SI Methodology Guide

Page 23

Therefore these trends are used as a set of questions to the business model of the company

in order to know whether it is relevant given the future trend. For instance it has proved

irrelevant for American carmakers to produce high gas guzzling cars as the climate change

trend has made these cars useless.

For each SD question, the analyst will define which kind of financial impact it could have on

the company (impact on sales, margin or assets). Trends that would be considered not

relevant would be left aside. 4 to 5 trends are expected to be activated per company.

In the following paragraphs, we provide a quick des cription of the trends.

The first trend, ageing population , addresses a key issue that encompasses all countries.

Except India and Africa, all countries have been undergoing an ageing of their population.

There are two potential impacts. The first one is related to the development of new products

an services for this ageing population. The second one is related to the adaptation of

production processes to ageing employees.

The second trend, globalisation, refers to the extension of supply chain and markets

globally. It raises two questions. First, is the company able to develop its supply chain and

sales globally beyond its continent? Second is the company able to manage its supply chain

without overstretching it (traceability and logistics chain issue) and taking advantage of

countries, not only by the wage level.

The third trend, global pollutions , addresses the major issues regarding pollutions globally.

First there is a need to identify climate change. It may have an impact on sales (car industry,

capital goods for any related innovation), cost (cement) or asses (utilities). Second there is a

need to address other global pollutions (acid rain, zone layer, ocean)

The fourth trend, new powers in society, refers to two main questions. First there is a need

to the company’s dependence on government and to think about the relationship (corruption,

lobbying). Second there is an issue with the rise of NGOs and their implication in the

relationship between company and government.

The fifth trend, poverty reduction, addresses two phenomena. The first is the emergence of

effective demand from low revenue population (India, South East Asia). These populations

represent 80% of the word population and, are not addressed by western companies yet,

except two or three examples (Unilever). The second one is the demand of employees (Wal-

Mart and health insurance expenses) or neighbouring local populations (Shell and other oil

companies in Nigeria) to get (relative) minimal services.

The sixth trend, resources efficiency and biodivers ity, refers to two partly addressed

issues. The first one is the resources efficiency. It has been improved by 20% to 50% in the

last 20 years but it has not been enough to avoid resources depletion as the growth and

globalisation implied a 80% improvement (factor 4 concept by the Wuppertal Institute in

Europe)

The seventh trend refers to the need of data privac y and protection of identity . Our

ways of life have turned more and more standardised and electronics development have risen

the fear of 1984 fiction by George Orwell turning reality. There is a need of diversity3, that

3 Without diversity and personal creativity, there is no need , no demand and no growth.

ESN SI Methodology Guide

Page 24

companies should protect and if possible develop. And that is for individual rights of the

computer user as well as for the native tribes in remote areas.

The last trend refers to the health issue . Two separate questions will be assessed. First

there is need to understand impact of global health issues on product (for pharmaceuticals)

as well on its impact on workforce (for companies settled in Asia or Africa). Second there is a

need to assess the long range diseases of clients (obesity) or occupational illnesses of

employees (asbestos). These issues will change dramatically their sectors.

Once the framework is explicit, we will explain how we integrate these in the valuation.

ESN SI Methodology Guide

Page 25

Scope of assessment and financial impacts

Adding the (ESG+SD) issues does not only give a more complete image of the past

performance of the company, but will also reflect future strengths and weaknesses.

Integrating sustainable development items into valuation could bring us to the question of

what could be the effect of sustainable development on sales, margins, assets and valuation.

Sector and company assessment

• Sector assessment

At sector level , the first step is the financial framing whose need was already mentioned in

the second part. The aim is the identification of major environmental and social im pacts

on financial performance (balance sheet or profit & loss sheet) and therefore the gross

assessment of potential impact on sales, margins an d assets .

However this sector overview is not the ultimate solution for companies’analysis. First only a

few sectors are homogeneous in the activities. In Industrial goods and services, it is difficult to

compare Schneider Electric and Randstad, or even in industrial services, Randstad and

Bunzl. Second, even in standardized sectors, the comparison is difficult. For example, in

chemicals, companies producing industrial gases are specific as they do not generate toxic

releases, and as Co2 issue may impact their sales growth (instead of the margin impact

borne by other chemicals). Third some companies have business areas in different sectors,

making difficult the assimilation to one sector. Therefore the sector level of analysis will

constitute a frame but not an aim as such as the ai m is to achieve integration in the

company’s valuation.

• Company assessment

The company analysis starts first with the ESG “facts and figures” that displays the risk

exposure of the company to the most important issues from Environmental, Social or

Governance dimensions. Second the business model is assessed regarding long range

questions.

Based on this broad picture, the analysis could focus on

• One of the ESG facts and deepen the analysis, on the gender diversity issue and analyse

the potential glass ceiling issue within the company or the lack of career management

and its consequence regarding staff turnover.

• One of the SD trends and assess the impact of the trends on costs, sales or assets of the

company.

The result of this focus could be displayed and reused in the following sections of the

company report:

- in the risk and strategic analysis

- in the valuation process.

ESN SI Methodology Guide

Page 26

Financial impacts of sustainable development

• Impact on sales

Investing in sustainable development items can have an impact on companies’ sales. On the

one hand the company can attract new customers and on the other hand they will avoid their

products to be boycotted by some organisations. We often see specific types of customers

like students impacts sales of specific products (Nike, …) when it appears companies’

operations harm the environment or the social environment. Furthermore we should be

looking for companies developing product that will solve future problems like desalination of

seawater, recycling, … Companies investing in these new technologies could add a new

product line and new sales line to the group’s turnover.

Three examples of impact on sales

Negative impact from

poor supply chain

management

• A supply chain management based on low cost of materials may generate disruption of raw materials

stocks and prevent production and therefore negatively impact on sales growth. Nissan has bitterly

experienced this situation in Japan in 2003 with work stop up to 3 weeks in its plan due to a lack of steel4.

Negative impacts from

human resources

management (or lack of

it).

• A traditional human resources policy may assess whether the company has the capacity of developing new

projects. For example, after its massive layoffs and resignations, Boeing in 2000-01 had not enough skilled

workforce to develop new aircrafts, military or civil. Its two major projects were actually rejected in 2001-02.

• In August 2006, a 20 days strike in the mine of Escondida has not impacted the cost structure of the mine

and its main owners (BHP Billiton and Rio Tinto) but it had a direct impact on sales of Rio Tinto as the

company had no copper stock to alleviate the shortage. There was a direct loss of sales of raw and

processed products.

Positive impacts on

sales and growth

• A new market whose potential would not be clearly identified yet is an opportunity to identify new sources

sales and growth for a company. For instance, the market of desalination may represent an increase of

sales for some European companies depending on their technological and strategic advantage to succeed

on this market5.

Source: ESN SI Team

• Impact on margins

The impact of socially related investments on margins is more difficult to measure. Investing

in training facilities and other social initiatives could weight on the short run performance as

the company’s costs would increase. Again in the long run the company could benefit from

lower employee turnover, absenteeism or would avoid strike costs. This would increase

productivity and reduce long term investments in new forces benefiting the margins.

Ecological initiatives as energy savings can be quantified. In the short run when the company

decides to invest in waste reduction or limitation of energy consumption costs will increase.

Indeed these investments will need additional capex having its impact on the company’s free

cash flow. However immediate cost reduction related to energy savings will be integrated into

4 GERPISA, 2005 5 ESN- CM CIC Securities : would you like a glass of seawater ? 8 September 2006

ESN SI Methodology Guide

Page 27

the cost of goods sold reducing the cost per product and supporting a possible increase of the

operational margin of the company.

Two examples of impacts on margins

Avian Flu

• A research on avian flu assessed the impacts of avian influenza on sales and margins of European

pharmaceuticals6. Impacts on sales might not be as important as it has been expected as medical organisations

strive to circumvent the disease. A strong discount has been bargained by government in order to make margins

flat for companies. A potential impact has been identified in the assets.

Carbon

• Another research has assessed the amount of CO over-allocation on the EU ETS market. It concludes that in

case carbon quota were not given (as subsidies) but paid by companies (as cost) it would impact the pre tax profit

of highly emitting companies (cement, utilities) up to 16%.

Source: ESN SI Team

• Impact on asstes and liabilities

Asset is an important impact as there exists a huge number of latent liabilities. Reducing

these latent liabilities add reliability to the company which in the longer run could lead to

additional business for the company.

Two examples may be provided

Impact of land remediation Impact of water scarcity

The analysis of land remediation management would enable to assess the need of

supplementary provisions for liabilities in order to clean up contaminated land. In

this area, the lack of rehabilitation strategy accepted by authorities can be

damaging. For instance, An extreme case is the closure of Kelian mine in Papua

New Guinea. Rio Tinto had to set up financial reserves up to 250 m€ in 2002.

The assessment of water scarcity risk on asset has proved interesting for 20

European companies (see footnote 6). Considering a set of countries suffering from

water scarcity known as “the thirst triangle”, a research has assessed the

percentage of assets that could be at risk given its location in the “thirst triangle”.

For 3 sectors (paper, steel, fertilizer) and 20 companies, it has been proved that 4

of them have a percentage of assets over 10% located in these “thrsity” countries.

Source: CM CIC Securities

6 ESN – Van Lanschot : Avian Influenza, 21 September 2006

ESN SI Methodology Guide

Page 28

Glossary

About corporate social responsibility and Sustainable Investment

Corporate Social Responsibility (CSR): set of policies implemented by companies in order

to take into account the consequences of its production, products and services over minority

shareholders, customers, suppliers, employees, environment, and the surrounding

communities.

Sustainable Investment (SI): Investment taking into account two targets: a financial one and

a non “short term” financial one (moral, social, or long term profitability)

Governance

Double voting rights: the question enables to check whether treats its shareholders equally.

Our preferred scheme is: one share = one vote.

Shareholders’ agreement: the question enables to check if some shareholders’ have an

agreement to share power and subsequent rights to buy their own shares.

Free float: it gives and indication on the liquidity of the title

Employees shareholders (%): percentage of capital held by employees (careful if there is

much of it it might be used as autocontrol)

State (%): percentage of capital held by the State

Combined CEO/Chairman (Y/N): this question checks whether the power is concentrated in

one person or broken down into 2 persons having each one a specific role

Number of Directors of the Board: this number should be high enough to collect different

advices and perspectives and small enough to enable decision (between 6 and 12)

Number of independent directors (disclosed): the number reflects the ability of the

company to integrate independent opinion in the decision process. The estimates of

independent directors according to the analyst may be added in the comments.

CEO compensation and its variable part: enables to make a first assessment of the

incentive efficiency of the compensation

Executive compensation and its variable part: enables to make a first assessment of the

incentive efficiency of the compensation

Non executive compensation: enables to assess potential conflict of intrest through

excessive remuneration of non executives.

Stock option in circulation: description of the amount of stock option

SO restricted to CEO: enables to assess the breakdown of SO and the part taken by the

CEO.

ESN SI Methodology Guide

Page 29

Stock Option weighted price : this item enables to assess the cost for the company of the

stock price, through the difference between this weighted price and the average stock price.

The second item (SO dilution ) assesses the loss for the shareholder.

Audit fees to auditor: this question enables to check the potential conflict of interest of

auditors to make sure the remuneration for audit higher than the one for advice.

Number of consolidated companies: it gives the amount of companies integrated in the

Group.

Environmental and social reporting

CSR (or SD) report or Code of Conduct: enables to check the level of environmental and

social communication disclosed by company.

Suppliers screening system: enables to check the first step of suppliers’ policy

Global or sector initiative: indicates the involvement of a company in sectoral or global

initiatives to improve social or environmental issues

Social

Number of employees: size of the company

Gender diversity: it provides an indication whether the company restricts its entry to women

(physically hard work, for instance) or whether it is rather feminine work (with a potential

problem if the management is mainly male)

Average age of employees: enables to check whether the company is subject to ageing

employees

Wages (% sales): assess the importance of labour in the cost structure

Average remuneration per employee retreated from ma nagement compensation : the

aim of this item is to assess the average cost per employee so that the contribution is better

identified, and could be compared to traditional productivity ratios.

Pension liabilities: it may impact severely on fixed assets.

R&D/ sales: it enables to check if differentiation and innovation is source of value creation by

the company

Cumulated R&D/ sales: it enables to check whether the value creation ay be embedded in

the assets

Sourcing (%sales): it describes the degree of vertical integration of a company and enables

to assess the financial impact of suppliers relationships

Sales to governments (% sales): it is a first overview of the degree of dependence to

government clients; dependence to other clients may be added in the comments

Warranty cost: it may impact severely on fixed assets

Environmental impact in the life cycle: the idea is to understand where exactly lies the

environmental impact of a product/service, during its production, its use or its recycling. The

ESN SI Methodology Guide

Page 30

subsequent financial impacts are fairly different. Use Impacts usually generate impacts on

sales, recycling a margin impact, production an impact on assets

Raw materials (% sales): this assesses the dependence of the company on one natural

resource

Energy consumption (kWh, Pet…): this data is a first approximation of the company’s

dependence on energy and its exposure to the climate change issue

Energy cost (% sales): tis item displays whether the energy impact is a long terme issue or

has already a financial relevance for the company