PLEASE SEE ANALYST CERTIFICATION(S) AND IMPORTANT DISCLOSURES ON THE LAST PAGE.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PLEASE SEE ANALYST CERTIFICATION(S) AND IMPORTANT DISCLOSURES ON THE LAST PAGE.

Cover

“Without a measureless and perpetual uncertainty, thedrama of human life would be destroyed”Winston Churchill

“Reform is China’s second revolution”Deng Xiaoping

“Investing should be more like watching paint dry orwatching grass grow. If you want excitement, take $800and go to Las Vegas”Paul Samuelson

“All progress is based upon a universal innate desire on thepart of every living organism to live beyond its income”Samuel Butler

“I am not worried about the deficit. It is big enough to takecare of itself”Ronald Reagan

“Things do not happen. Things are made to happen”John F. Kennedy

“How much easier it is to be critical than to be correct”Benjamin Disraeli

Published by Barclays21 February 2013ISBN 978-0-9570088-1-6£100

Inside front cover

Barclays | Equity Gilt Study

21 February 2013 1

EQUITY GILT STUDY 2013

58th Edition The Equity Gilt Study has been published continuously since 1956, providing data, analysis and commentary on long-term asset returns in the UK and US. This publication provides a uniquely long and consistent database: the UK data go back to 1899, while the US data – provided by the Centre for Research in Security Prices at the University of Chicago – begin in 1925. We have also used the Equity Gilt Study as an opportunity to analyze medium- to long-term market trends.

Chapter 1 revisits the analysis of investment returns that appeared in last year's edition to account for the huge (roughly 20%) rally in global equities that has occurred since then. This performance can be attributed at least in part to the reduction in negative tail risks left over from the last crisis. With lower volatility having already been priced in, equity returns over the next five years are also expected to be lower – in the 3-4% range – than we had been anticipating previously and well below historic norms. Even so, returns on equities are likely to easily beat those on cash and bonds, both of which we expect to be negative in inflation-adjusted terms. The continuation of extraordinarily easy monetary policy should keep nominal returns on cash negligible, and the eventual normalization of monetary policy is expected to render returns on bonds even lower than cash.

Chapter 2 revisits last year’s theme that the prices of safe haven assets have been elevated because of the structural decrease in their supply. This time, we look at the structural demand for these assets, and find that it is likely to remain strong, reflecting banks' adjustments to new regulations and the behavior of investors in countries with ageing populations. As a result, the so-called “Great Rotation” out of bonds into equities is not likely to be as dramatic as many people think, and bond yields should remain low relative to historic norms.

Chapter 3 asks whether China can sustain economic growth and avoid the “middle income trap” that occurs when a developing country reaches middle income but is thwarted by rising wages and falling cost competitiveness on the one hand, and a lack of skills and innovation on the other. We argue that it can: the Chinese economy is in the middle of a major and broad-based structural transformation that will lead the country to slower but more sustainable growth. While the path is not without significant risks, our base case is that China will reach high-income status over the next decade or so.

Chapter 4 focuses on the risks associated with the extraordinary loose monetary policies of the major central banks since the onset of the financial crisis. Beyond the risk of high inflation, asset price bubbles and stagnant productivity resulting from the propping up of “zombie” companies could also emerge if extreme monetary accommodation is maintained for too long. The authorities will have to act deftly to ensure these risks from QE are contained.

Chapter 5 considers the portfolio implications of the new bond regime discussed in Chapters 1 and 2, taking as a starting point the assumption that the strong bond returns of the past 30 years are probably behind us.

We sincerely hope that you find the data and the essays interesting and enlightening, as well as useful inputs to your investment decisions.

Larry Kantor Head of Research, Barclays

Website: Equity Gilt Study on www.barclays.com E-mail: [email protected]

Barclays | Equity Gilt Study

21 February 2013 2

CONTENTS

Chapter 1 Low risk, low return 4 Although we cannot be sure that another financial crisis is not lurking around the corner, we think the ‘tail risks’ associated with the last crisis are probably behind us. When thinking about medium-term valuations and formulating expectations of investment returns, we think investors should, for now, work with a low-volatility base case, analogous to the 2003-07 ‘inter-crisis’ period of low volatility. In the next five years, we think the investment environment will be driven by two transitions. The eventual normalization of monetary conditions and China’s transition from economic ‘miracle’ to normal development could put downward pressure on equity returns. With valuations supported by a lower-risk environment and interest rates still at rock bottom, investors should expect lower returns. Over the next five years, we expect cash to provide inflation-adjusted returns of about -1.5% pa, ‘safe haven’ government bonds about -2%, and equities 3-4%. The implied equity risk premium remains in a historically normal 500-600bp range. Equities remain the most promising option for investors seeking positive, inflation-adjusted returns, and the main market risk seems to be that a migration to equities causes valuations to outrun fundamentals. But we are not there yet.

Chapter 2 Demand for safe havens to remain robust 16 Following on from the Equity Gilt Study 2012, in which we argued that conventional measures of the equity risk premium appeared elevated mainly because the structural decrease in the supply of risk-free assets had resulted in unusually low risk-free bond yields, we turn to the role of demand for safe-haven assets. We examine three sources of demand for such assets: official-sector demand via the investment of international reserve portfolios; institutional demand in a post-crisis era of tighter bank regulation; and private demand, particularly from an aging population across the developed world. We look for US institutional demand and the rotation of boomer investors into bonds to make up for some of the relative decline in demand from official sources, including our expectation of diminishing reserve accumulation in China. We conclude that structural demand for safe havens is likely to remain high and, when combined with the structural scarcity of such assets, is likely to keep interest rates on safe assets low by comparison with historical norms and conventional measures of the equity risk premium elevated.

Chapter 3 Can China avoid the middle-income trap? 35 Can China continue to grow while avoiding the ‘middle-income trap’ that occurs when a developing country fails to upgrade to high income status as a result of a lack of competitiveness and innovation? We believe that China should be able to reach high-income status over the next decade or so by narrowing its technological gap with advanced economies. Long-awaited structural improvements, including a narrowing of the current account surplus, a growing contribution of consumption to GDP and declining inequality, are already under way, but may be underappreciated by investors. In our view, political reform will be necessary to sustain economic growth in China, but we do not think current political institutions have exhausted the country’s growth potential yet. Science and technology have taken off much earlier in China relative to the experience of other emerging Asia economies. Although China’s economy faces many risks, we believe that it is unlikely to collapse, even though it may continue to look different from western advanced economies.

Barclays | Equity Gilt Study

21 February 2013 3

Chapter 4 QE carries risks beyond inflation 54 To a large extent, QE is a symptom rather than a cause of the economy’s underlying woes. Although it need not lead to high inflation, the latter may result from an increased tolerance of inflation in the face of stagnant real economic growth. The US and the UK appear most vulnerable to these pressures. Extraordinarily low yields on government bonds might push investors into riskier assets, but widespread uncertainty and strong savings intentions have so far prevented bubbles from arising. However, it remains to be seen whether the new macroprudential policy frameworks will be effective enough to stop damaging distortions from developing. Accommodative monetary policy and excessive forbearance by banks enable the survival of relatively weak companies that would otherwise be forced out of business, resulting in impaired productivity growth. We see the risk of structural degeneration as higher in Europe than in the US.

Chapter 5 Scenarios for a shifting bond landscape 67 Financial markets appear to be at a transitional point. Following on from the “Great Moderation” and the “Great Recession”, there now seems to be a debate over the next “Great” theme. The strong bond returns of the past 30 years are likely over. Against this backdrop, we analyse various financial scenarios and examine the implications for different investors.

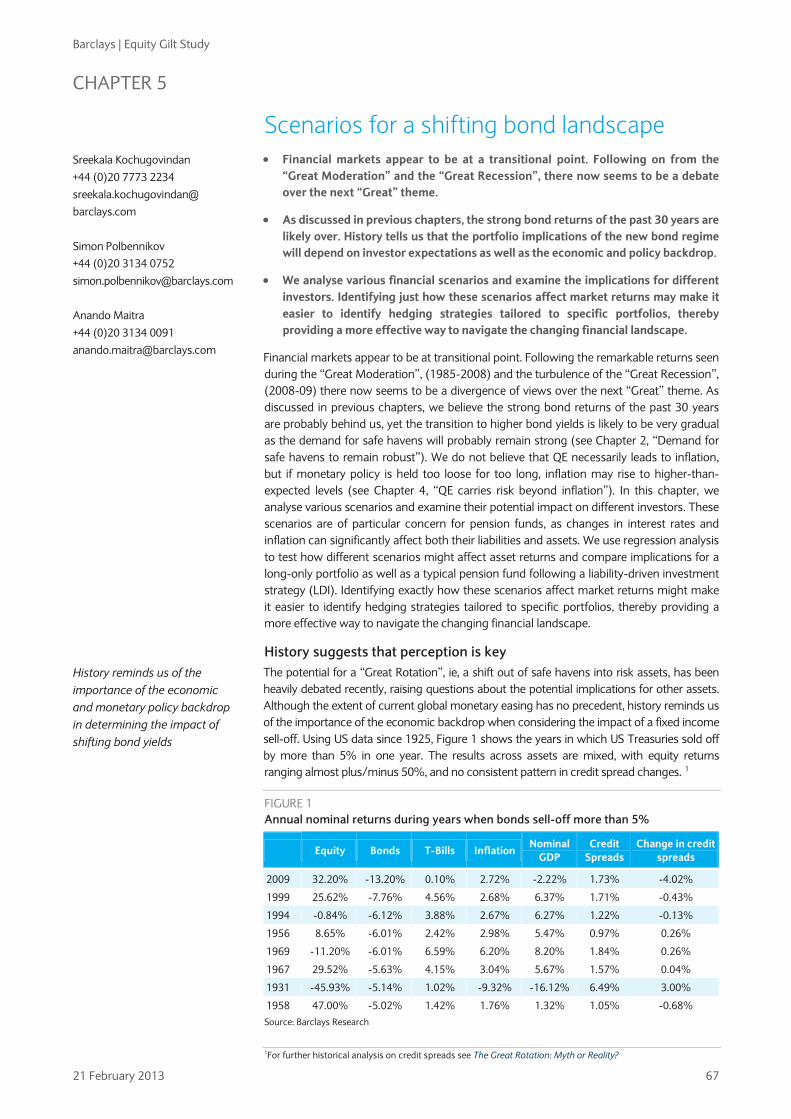

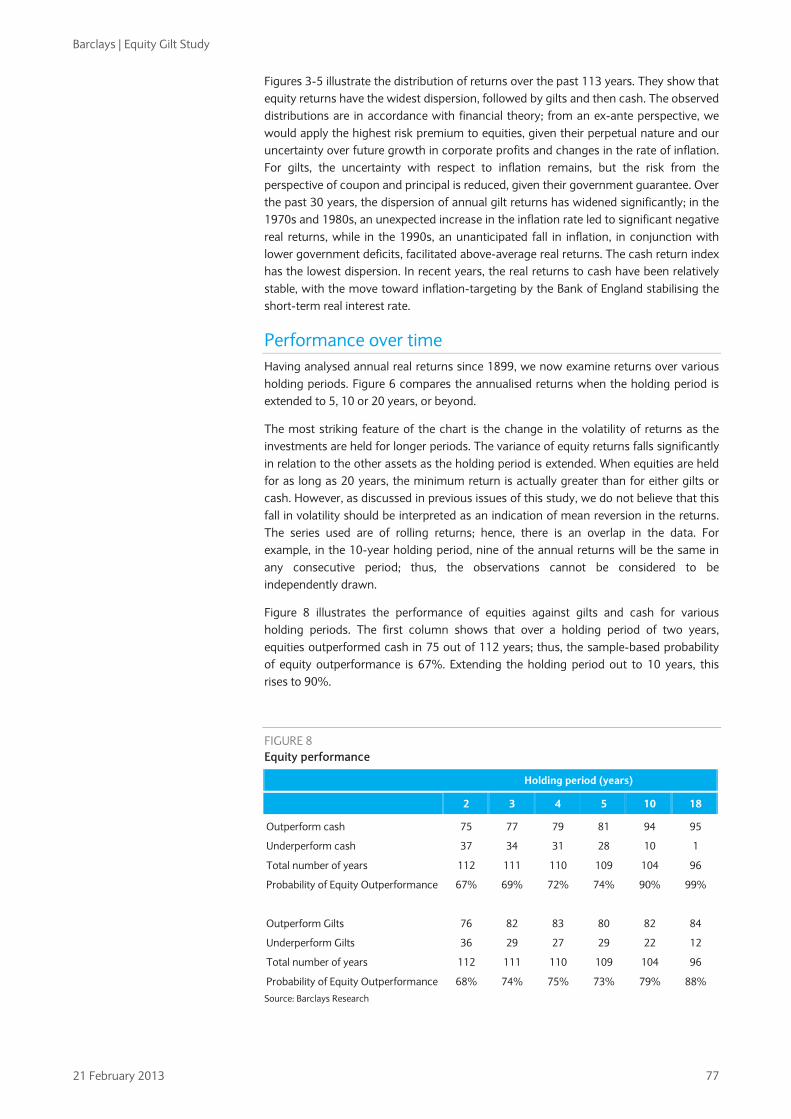

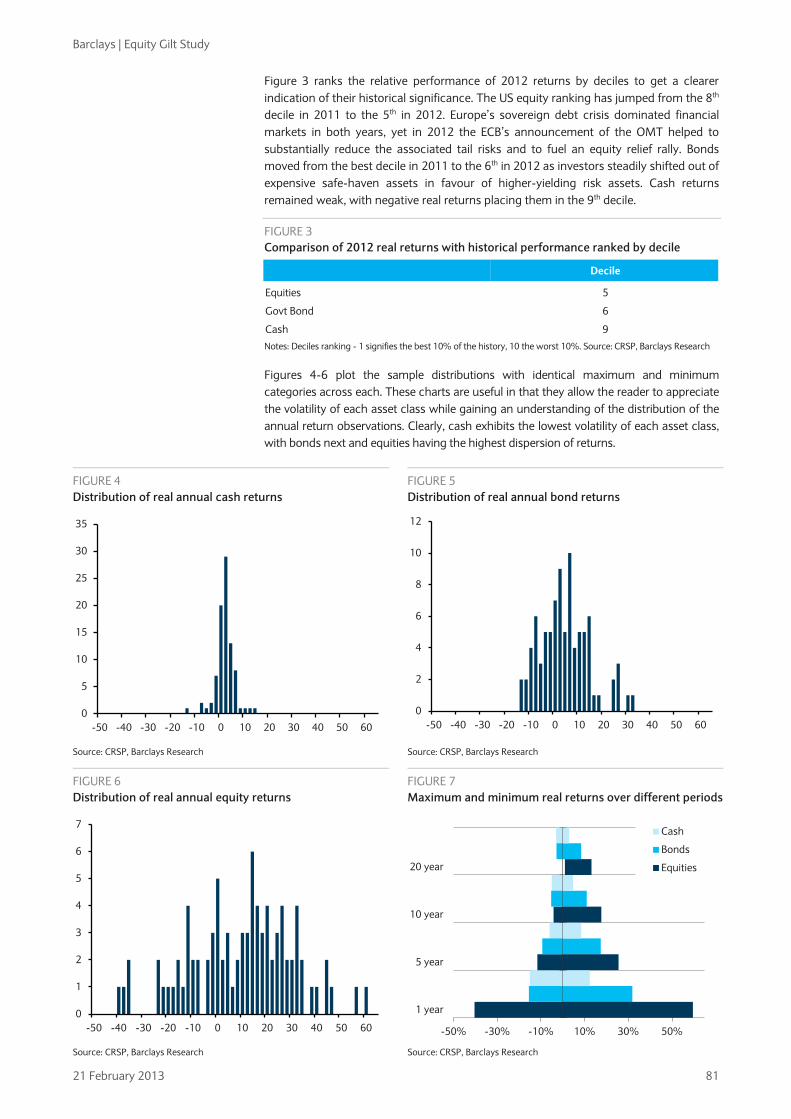

Chapter 6 UK asset returns since 1899 75 We analyse returns on equities, gilts and cash from end-1899 to end-2012. Equity markets performed well in 2012, rallying by 13.4%, despite turbulent market conditions. Nominal and inflation-linked gilt yields were much weaker relative to 2011. Gilts, along with Bunds and Treasuries, had benefited from the flight-to-quality flows during 2011 and the first half of 2012. However, the introduction of the OMT helped to reduce the tail risks associated with Europe and encouraged investors to move out of safe havens into riskier assets. Corporate bonds benefited from this trend last year and generated a 12% real return, compared with just 1.6% in 2011.

Chapter 7 US asset returns since 1925 80 Equities were the best-performing assets of 2012, producing a 14.1% real total return, despite following a turbulent path similar to that of UK and European markets. Treasury returns were weaker in 2012, just 2%, compared with 22.5% in 2011. TIPS outperformed Treasuries by 8% as inflation expectations rose. Breakevens widened against the backdrop of dovish monetary policy and improved market liquidity. Corporate bonds also performed well as investors moved out of safe havens, increasing their risk exposure.

Chapter 8 Barclays indices 84 We have calculated three indices: changes in the capital value of each asset class; changes to income from these investments; and a combined measure of the overall return, on the assumption that all income is reinvested.

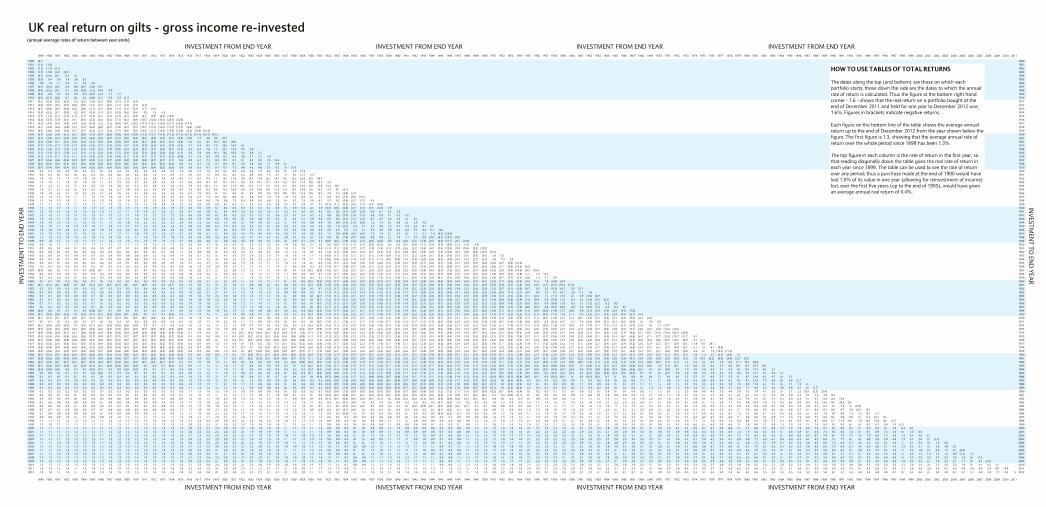

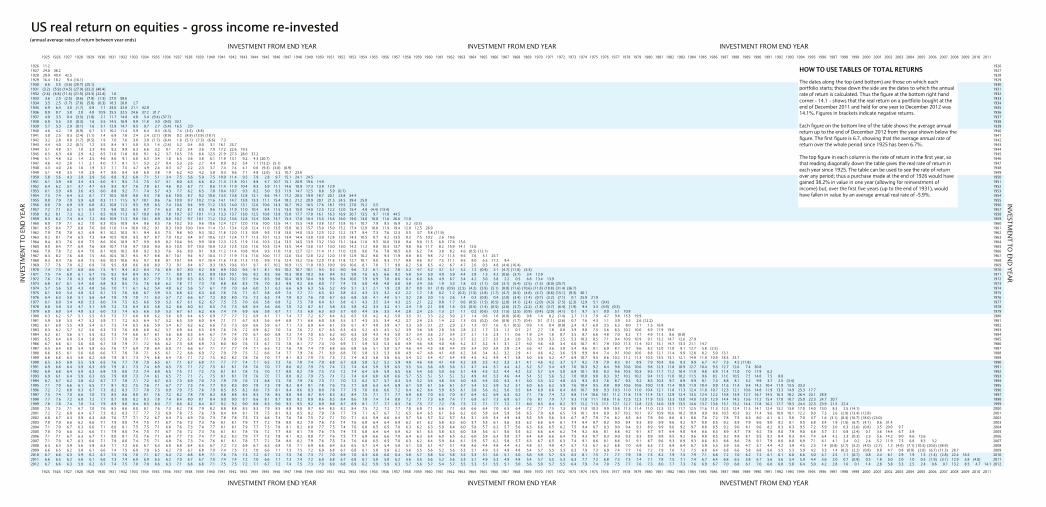

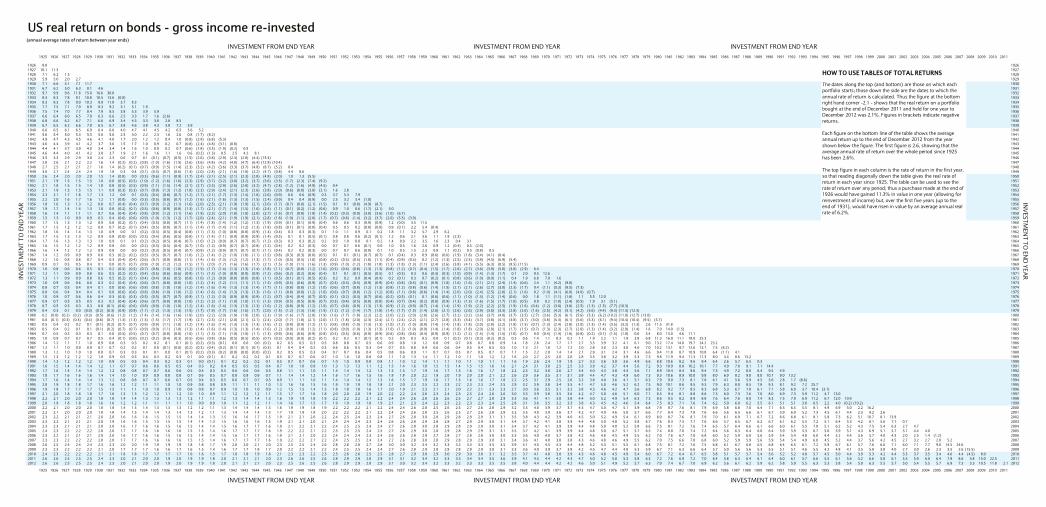

Chapter 9 Total investment returns 107 We present a series of tables showing the performance of equity and fixed-interest investments over any period of years since December 1899.

Barclays | Equity Gilt Study

21 February 2013 4

CHAPTER 1

Low risk, low return • Although we cannot be sure that another financial crisis is not lurking around the

corner, we think the ‘tail risks’ associated with the last crisis are probably behind us. When thinking about medium-term valuations and formulating expectations of investment returns, we think investors should, for now, work with a low-volatility base case, analogous to the 2003-07 ‘inter-crisis’ period of low volatility.

• In the next five years, we think the investment environment will be driven by two transitions. The eventual normalization of monetary conditions and China’s transition from economic ‘miracle’ to normal development could put downward pressure on equity returns.

• With valuations supported by a lower-risk environment and interest rates still at rock bottom, investors should expect lower returns. Over the next five years, we expect cash to provide inflation-adjusted returns of about -1.5% pa, ‘safe haven’ government bonds about -2%, and equities 3-4%. We see no reason to believe that high-grade credit will outperform.

• The implied equity risk premium remains in a historically normal 500-600bp range. Equities remain the most promising option for investors seeking positive, inflation-adjusted returns, and the main market risk seems to be that a migration to equities causes valuations to outrun fundamentals. But we are not there yet.

Diminished ‘tail risks’: A double-edged sword The collapse in asset-market volatility is a double-edged sword. On the one hand, it signals a genuine reduction in the tail risks of a globally destabilizing economic/financial event. This is a great relief for investors who have had to endure the anxiety created by such risks for several years. On the other hand, investors are ultimately paid to take risk, and without the wall of worry, what kind of rewards can they expect risky assets to yield? In this chapter, we offer some thoughts on the returns that may be on offer in the main asset classes, in the more tranquil financial environment that investors are likely to face in the immediate future. We extend previous work (including, in particular, “The equity risk premium: Cheap equity or expensive bonds?” Equity Gilt Study 2012) in the following ways.

Michael Gavin +1 212 412 5915 [email protected]

Piero Ghezzi +44 (0)20 3134 2190

FIGURE 1 A less volatile world

FIGURE 2 Equity returns tend to be low when interest rates are low

0

10

20

30

40

50

60

70

80

90

100

Dec-01 Dec-03 Dec-05 Dec-07 Dec-09 Dec-11

VIX V2X

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

-4.0 -3.0 -2.0 -1.0 0.0 1.0 2.0

Average real interest rate (% pa)

Long-term real equity return (% pa)

Source: Bloomberg Source: Elroy Dimson, Paul Marsh, and Mike Staunton, “Equity Premia around

the World”, manuscript, London School of Business, Oct 2011.

Barclays | Equity Gilt Study

21 February 2013 5

• We update our assessment of the outlook for investment returns to account for the substantial rally in global equities and the (more modest and more recent) selloff in ‘safe haven’ bond markets that market participants have enjoyed since early 2012. The roughly 18% rally in global equity prices that has occurred since the early days of 2012 amounts to a few years of the ‘steady-state’ equity appreciation that we deemed plausible in our assessment last year. It would be surprising if a forward-looking assessment of investment returns were untouched by a rally of this magnitude.

• We focus on a more concrete five-year investment horizon, rather than the less well defined ‘long run’ focus that we adopted last year.

• Finally, we embed in our thinking the assumption that the next five years are likely to be an ‘inter-crisis’ interlude, analogous in some ways to the 2003-07 period of low volatility between the collapse of the global equity bubble and the (even) more damaging collapse of the subsequent housing and credit bubble. Of course, five years is a long time and we cannot pretend to know that the coming half-decade will be untouched by economic or financial crisis. The spirit of our assumption is that a new crisis is far enough off that, for the next couple of years, investors will be able to make decisions mainly on the basis of considerations other than whether one ‘tail risk’ or another may be about to materialize.

Even if the next five years will be tranquil, they will be far from uneventful. We highlight two transitions that that we expect to be powerful drivers of asset markets over the next five years or so. The first is a likely normalization of monetary conditions, which should be reasonably far along, although most likely not complete, five years from now. The second is China’s transition to a new and qualitatively different development trajectory. This transition has been under way for some time, but has mainly been discussed within a Chinese national context (see Chapter 3, “Can China avoid the middle-income trap?” in this publication). We think that the integration of emerging market workers (including, most notably, Chinese workers) into the global labor force has been an extraordinarily powerful driver of employment, earnings, and asset prices around the world. It stands to reason that the transformation of the Chinese development trajectory could have equally powerful effects.

Can bonds earn more than cash? The 30-year bull market in what we now consider ‘safe haven’ government bonds probably reached a high-water mark in 2012, and investors in those bond markets are unlikely to continue to enjoy the combination of equity-like returns and bond-market volatility that they enjoyed during the boom. We agree with this consensus view, but also believe that the bull market in bonds is much more likely to end in a drawn-out whimper than in a 1994-style bond-market ‘bang’. There is nothing in the existing market context comparable to the leverage that contributed to the turmoil in 1994. Monetary authorities in the systemically important currencies are likely to keep the monetary floodgates open for many months to come and would likely use all the considerable means at their disposal to fend off any bond market selloff large enough to threaten the still-lacklustre economic recovery. Moreover, the global shortage of safe assets is unlikely to be materially narrowed in the coming decade, which does not mean that yields will never rise from current levels, but does mean that a persistent bid is likely to keep ‘safe haven’ bond prices elevated relative to historical norms (see “The equity risk premium: Cheap equities or expensive bonds?”, Equity Gilt Study 2012, and “Demand for safe havens to remain robust”, Chapter 2 in this publication).

Cash is likely to remain a value destroyer, in real terms If we want an estimate of the equity risk premium, we need a more quantitative assessment of the return on cash and bonds over our five-year investment horizon. The logical starting point is the yield curve. In the US, UK and euro area, government bond markets are pointing to a gradual normalization of monetary conditions over the coming years (Figure 3), but in all cases the normalization is expected to be incomplete

The 30-year bull market in ‘safe haven’ government bonds probably reached a high-water mark in 2012

Government bond markets point to a gradual normalization of monetary conditions over the coming years

Barclays | Equity Gilt Study

21 February 2013 6

by the end of our five-year investment horizon. In the US, for example, the 5y forward 1y interest rate (the yield curve’s interest-rate ‘forecast’ for 2018) is less than 2.5%, and the inflation-protected (TIPs) forward curve remains negative through 2018.

Figure 4 puts these forward rates into a US historical perspective and Figure 5 provides similar computations for GBP, EUR, and JPY interest rates. For our present purpose (which does not include a detailed analysis of relative value among these markets), the USD, GBP and EUR curves tell essentially the same story as in the US. Japan, where forward interest rates remain low for years to come and where the bond market outlook mainly reflects questions surrounding the recent turn toward more stimulative fiscal and monetary policies, is a case apart.

These forward rates are (by definition) the sum of the expected future rate and the term risk premium that the market attaches to owning bond duration rather than holding cash. For reasons discussed below, we believe that the term premium is low for short-duration bonds and that the expected return on cash over our five-year investment horizon is close to the average of the forward rates. The latter is (by construction) equivalent to the return on a 5y bond, which is on the order of 0.5-1% in the US, UK and euro area. After adjusting for expected inflation, a plausible value for the expected return on cash is thus something like -1.5%, though arguably lower in the UK and higher in the euro area.

FIGURE 3 The US yield curve implies a very gradual normalization…

FIGURE 4 …but real rates are projected to stay negative for 5 more yrs

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

2013 2015 2017 2019 2021

UST forward 1y interest rates

-10

-5

0

5

10

15

20

Apr-53 Apr-63 Apr-73 Apr-83 Apr-93 Apr-03 Apr-13

Nominal Real rate Note: Forward curve as of 2/15/2013. Source: Bloomberg, Barclays Research

Note: 1y US Treasury rates. Forecasts are from the UST nominal and TIPs curves. Source: Haver Analytics, Bloomberg, Barclays Research

FIGURE 5 Forward interest rates in the main reserve currencies

US UK Germany Japan

1y rates

Spot 0.15% 0.31% 0.06% 0.07%

1y forward 0.39% 0.32% 0.32% -0.02%

2y forward 0.70% 0.44% 0.44% 0.10%

3y forward 1.31% 1.28% 1.01% 0.23%

4y forward 1.76% 2.52% 1.47% 0.34%

5y forward 2.38% 2.54% 1.56% 0.67%

5y rates

spot 0.86% 0.97% 0.66% 0.14%

5y forward 3.16% 3.43% 2.66% 1.37%

10y forward 3.77% 3.96% 2.97% 2.25%

Source: Bloomberg, Barclays Research

Barclays | Equity Gilt Study

21 February 2013 7

Bond duration unlikely to provide an escape from low rates Except in the extremely unlikely event of a default, a 10y government bond will yield exactly 2.00%, 2.19%, and 1.65% if issued (in their own currency) by the US, UK and German government, respectively, and if the bond is held a full 10 years to maturity. But the hold-to-maturity thought experiment implicit in these yield-to-maturity calculations is not useful for most investors. More relevant is the return on bond duration over a given investment horizon. For the sake of concreteness, we ask what return to expect from maintaining exposure to bond duration for the coming five years equivalent to the duration embedded in the current 10y bond.

When interest rates are trending (lower in the past 30 years and likely higher in the next five), the holding period return is unlikely to match the yield to maturity. Even over long periods, this is no footnote. From 1982 to 2012, for example, continued exposure to the current 10y US Treasury bond would have yielded an investor 8.5% pa, more than 200bp above the average yield to maturity (6.4%) for those 10 years. This excess return was largely a windfall created by a decline in market interest rates beyond the wildest dreams of a typical bond investor circa 1982. Looking ahead, the problem is an anticipated increase in market rates.

Conceptually, the expected return on bonds can be expressed as the expected return on cash, plus the term risk premium that investors require as payment to own duration, which comes with mark-to-market volatility, rather than cash, which does not. This does not get us as far as we would like, because there is no consensus on the size or the term risk premium or even on whether it is positive or negative. Academic research has used a wide variety of economically-based and non-structural models to compute estimates of the yield curve, but there remains room for disagreement.

One prominent model of the term risk premium shows a strong decline since the early 1990s and a negative premium in the past couple of years (Figure 6). These estimates are based upon a purely statistical approach that does not embed specific financial-economic assumptions. But the decline of the estimated term risk premium coincides with a strong decline in the correlation between market returns on government bonds and equity risk, which turned negative around the year 2000, a ‘safe haven’ correlation that has been particularly prominent in the past couple of years (Figure 7). Figure 8 compares the ‘safe haven’ properties of safe EUR, GBP and JPY-denominated government bonds to those of the US. German and UK government bonds display strong ‘safe haven’ properties, although not as strong as US Treasuries. Japanese government bonds display a smaller ‘safe haven’ correlation. Figure 8 also shows that longer-duration bonds have had stronger ‘safe haven’ properties than shorter duration bonds.

In 1982-2012, continued exposure to the current 10y US Treasury bond would have yielded an investor 8.5% pa, more than 200bp higher than the average yield to maturity (6.4%) for those 10 years

FIGURE 6 Kim-Wright model of the US term risk premium

FIGURE 7 US Treasury beta to S&P 500

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jul-90 Jul-94 Jul-98 Jul-02 Jul-06 Jul-10

10-year UST term risk premium (Kim-Wright)

-0.5-0.4-0.3-0.2-0.10.00.10.20.30.40.50.6

Jan-91 Jan-94 Jan-97 Jan-00 Jan-03 Jan-06 Jan-09 Jan-12

5-yr 10-yr Source: Board of Governors of the Federal Reserve System Note: Rolling beta of UST return to the S&P 500, using 36 months of data.

Source: Barclays research

The decline of the estimated term risk premium coincides with a strong decline in the correlation between market returns on government bonds and equity risk

Barclays | Equity Gilt Study

21 February 2013 8

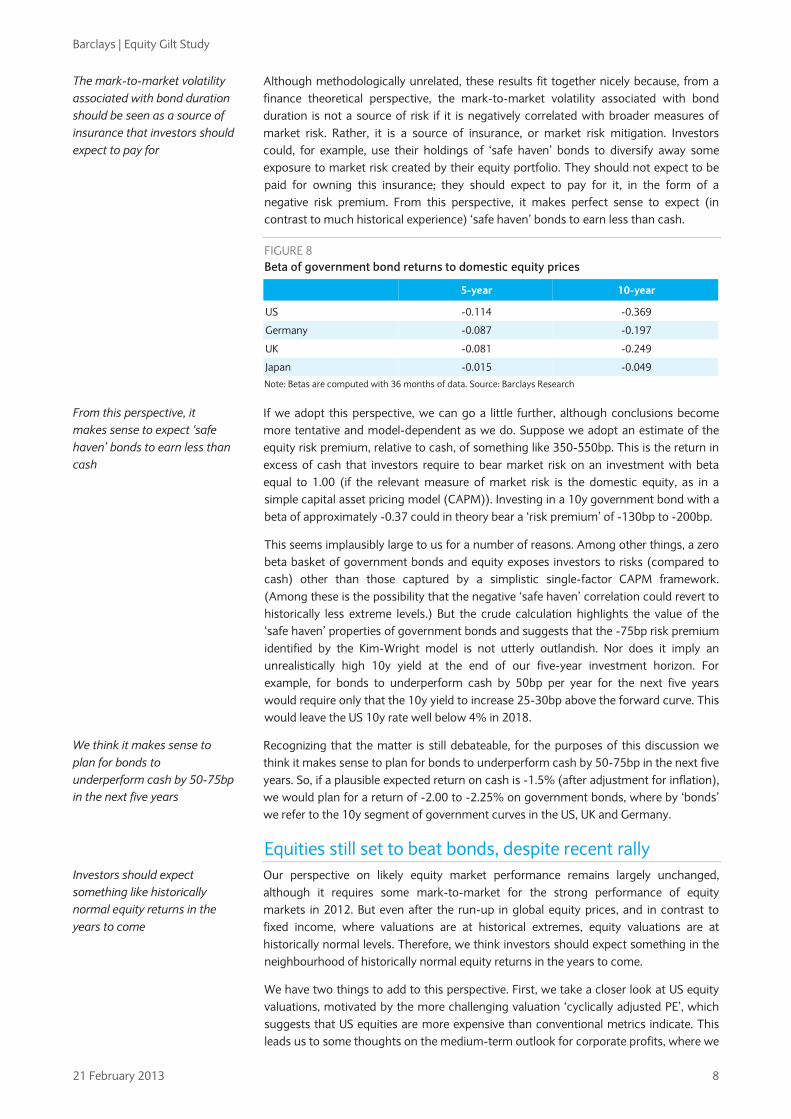

Although methodologically unrelated, these results fit together nicely because, from a finance theoretical perspective, the mark-to-market volatility associated with bond duration is not a source of risk if it is negatively correlated with broader measures of market risk. Rather, it is a source of insurance, or market risk mitigation. Investors could, for example, use their holdings of ‘safe haven’ bonds to diversify away some exposure to market risk created by their equity portfolio. They should not expect to be paid for owning this insurance; they should expect to pay for it, in the form of a negative risk premium. From this perspective, it makes perfect sense to expect (in contrast to much historical experience) ‘safe haven’ bonds to earn less than cash.

FIGURE 8 Beta of government bond returns to domestic equity prices

5-year 10-year

US -0.114 -0.369

Germany -0.087 -0.197

UK -0.081 -0.249

Japan -0.015 -0.049

Note: Betas are computed with 36 months of data. Source: Barclays Research

If we adopt this perspective, we can go a little further, although conclusions become more tentative and model-dependent as we do. Suppose we adopt an estimate of the equity risk premium, relative to cash, of something like 350-550bp. This is the return in excess of cash that investors require to bear market risk on an investment with beta equal to 1.00 (if the relevant measure of market risk is the domestic equity, as in a simple capital asset pricing model (CAPM)). Investing in a 10y government bond with a beta of approximately -0.37 could in theory bear a ‘risk premium’ of -130bp to -200bp.

This seems implausibly large to us for a number of reasons. Among other things, a zero beta basket of government bonds and equity exposes investors to risks (compared to cash) other than those captured by a simplistic single-factor CAPM framework. (Among these is the possibility that the negative ‘safe haven’ correlation could revert to historically less extreme levels.) But the crude calculation highlights the value of the ‘safe haven’ properties of government bonds and suggests that the -75bp risk premium identified by the Kim-Wright model is not utterly outlandish. Nor does it imply an unrealistically high 10y yield at the end of our five-year investment horizon. For example, for bonds to underperform cash by 50bp per year for the next five years would require only that the 10y yield to increase 25-30bp above the forward curve. This would leave the US 10y rate well below 4% in 2018.

Recognizing that the matter is still debateable, for the purposes of this discussion we think it makes sense to plan for bonds to underperform cash by 50-75bp in the next five years. So, if a plausible expected return on cash is -1.5% (after adjustment for inflation), we would plan for a return of -2.00 to -2.25% on government bonds, where by ‘bonds’ we refer to the 10y segment of government curves in the US, UK and Germany.

Equities still set to beat bonds, despite recent rally Our perspective on likely equity market performance remains largely unchanged, although it requires some mark-to-market for the strong performance of equity markets in 2012. But even after the run-up in global equity prices, and in contrast to fixed income, where valuations are at historical extremes, equity valuations are at historically normal levels. Therefore, we think investors should expect something in the neighbourhood of historically normal equity returns in the years to come.

We have two things to add to this perspective. First, we take a closer look at US equity valuations, motivated by the more challenging valuation ‘cyclically adjusted PE’, which suggests that US equities are more expensive than conventional metrics indicate. This leads us to some thoughts on the medium-term outlook for corporate profits, where we

The mark-to-market volatility associated with bond duration should be seen as a source of insurance that investors should expect to pay for

From this perspective, it makes sense to expect ‘safe haven’ bonds to earn less than cash

We think it makes sense to plan for bonds to underperform cash by 50-75bp in the next five years

Investors should expect something like historically normal equity returns in the years to come

Barclays | Equity Gilt Study

21 February 2013 9

see some downside risks from the exchange rate (in the US) and the prospective evolution of the Chinese growth model from one based upon super-abundant labor and inexpensive production inputs of all kinds, to a more balanced model.

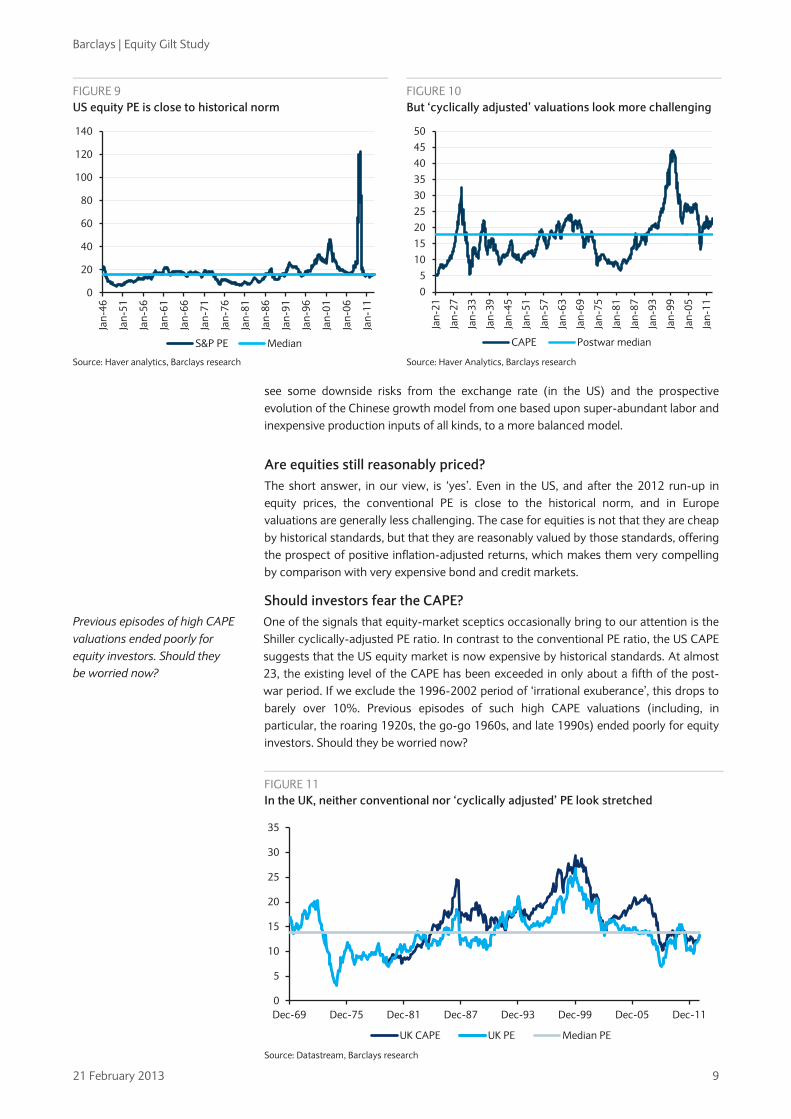

Are equities still reasonably priced? The short answer, in our view, is ‘yes’. Even in the US, and after the 2012 run-up in equity prices, the conventional PE is close to the historical norm, and in Europe valuations are generally less challenging. The case for equities is not that they are cheap by historical standards, but that they are reasonably valued by those standards, offering the prospect of positive inflation-adjusted returns, which makes them very compelling by comparison with very expensive bond and credit markets.

Should investors fear the CAPE? One of the signals that equity-market sceptics occasionally bring to our attention is the Shiller cyclically-adjusted PE ratio. In contrast to the conventional PE ratio, the US CAPE suggests that the US equity market is now expensive by historical standards. At almost 23, the existing level of the CAPE has been exceeded in only about a fifth of the post-war period. If we exclude the 1996-2002 period of ‘irrational exuberance’, this drops to barely over 10%. Previous episodes of such high CAPE valuations (including, in particular, the roaring 1920s, the go-go 1960s, and late 1990s) ended poorly for equity investors. Should they be worried now?

FIGURE 9 US equity PE is close to historical norm

FIGURE 10 But ‘cyclically adjusted’ valuations look more challenging

0

20

40

60

80

100

120

140

Jan-

46

Jan-

51

Jan-

56

Jan-

61

Jan-

66

Jan-

71

Jan-

76

Jan-

81

Jan-

86

Jan-

91

Jan-

96

Jan-

01

Jan-

06

Jan-

11

S&P PE Median

05

101520253035404550

Jan-

21

Jan-

27

Jan-

33

Jan-

39

Jan-

45

Jan-

51

Jan-

57

Jan-

63

Jan-

69

Jan-

75

Jan-

81

Jan-

87

Jan-

93

Jan-

99

Jan-

05

Jan-

11

CAPE Postwar median Source: Haver analytics, Barclays research Source: Haver Analytics, Barclays research

FIGURE 11 In the UK, neither conventional nor ‘cyclically adjusted’ PE look stretched

0

5

10

15

20

25

30

35

Dec-69 Dec-75 Dec-81 Dec-87 Dec-93 Dec-99 Dec-05 Dec-11

UK CAPE UK PE Median PE

Source: Datastream, Barclays research

Previous episodes of high CAPE valuations ended poorly for equity investors. Should they be worried now?

Barclays | Equity Gilt Study

21 February 2013 10

We think the answer is ‘no’, but not because signals delivered by the CAPE ought to be discounted as a matter of principle. Corporate earnings are heavily influenced by cyclical and other transitory factors, and some form of adjustment for spikes and temporary wiggles in earnings is valuable in principle, and in practice. Under some circumstances, the Shiller CAPE does a good job of this. But as most readers are aware, the ‘cyclical adjustment’ in the CAPE does not attempt to identify ‘cyclical’ influences and remove them from the earnings data, it merely smoothes (inflation-adjusted) earnings by taking a 10-year average. This makes sense for short-lived spikes such as the 2008 earnings downdraft, but it introduces a misleading lag in the response to more long-lived shifts in the level or growth rate of corporate earnings.

In the event of a long-lived upward shift in earnings, the CAPE will eventually normalize, but as a result of the gradual (specifically, 10-year) response of ‘cyclically adjusted’ earnings rather than a correction in equity prices. Even under reasonably cautious assumptions about future corporate earnings, this looks like the more probable scenario for the US. But before we get there, we should acknowledge that this discussion applies primarily to the US, and not more generally. In Europe, for example, earnings are (unsurprisingly) depressed relative to ‘cyclically adjusted’ earnings.

In the US, on the other hand, earnings are now very high relative to ‘cyclically adjusted’ earnings, as measured by the usual 10-year average. The question is whether this gap reflects mainly transitory factors, or a more enduring upward shift in earnings that the 10-year average has been slow to reflect.

To answer this question, it helps to consider some concrete scenarios. Suppose that the CAPE eventually normalizes at its historical average of just under 18, and we define ‘eventually’ as 10 years from now. This assumption, along with various assumptions about the trajectory of future earnings, determines the future equity price (inflation-adjusted, along with all the other numbers in these scenarios).

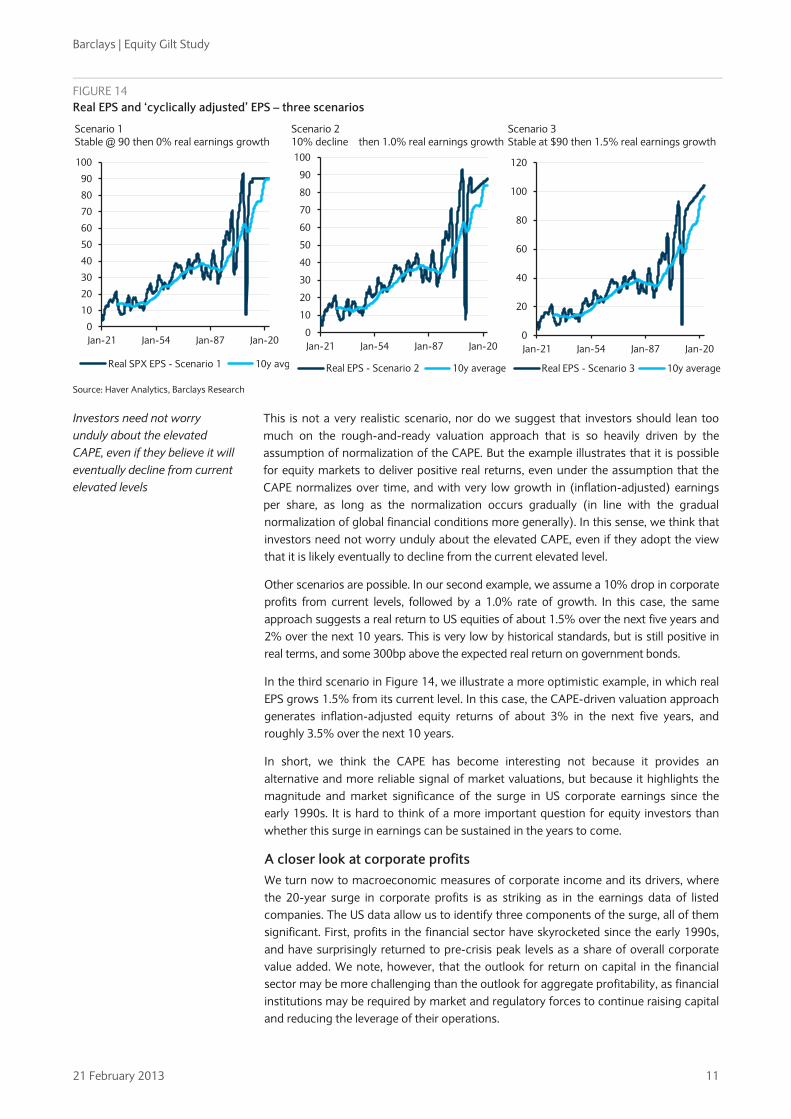

We consider three scenarios, which are more in the nature of plausible base cases, not risk cases that might arise (for example) in the event of a major recession. In the first, we assume that the EPS reaches $90 at end-2012 and remains constant at that level (again, in inflation-adjusted terms) for the next 10 years. As the first chart in Figure 14 illustrates, ‘cyclically adjusted’ EPS would gradually rise to $90, as a mechanical result of the 10-year averaging process. Under the assumption that the CAPE falls to its historical median of 17.8, real equity prices would end the 10-year period about 5% above their current level (1520), for a total inflation-adjusted return of about 2.5% pa, assuming a dividend yield of roughly 2%.

We think the answer is ‘no’

In the US, earnings are now very high relative to ‘cyclically adjusted’ earnings

FIGURE 12 UK real EPS is close to 10y average

FIGURE 13 US EPS is much higher than 10y average

0

100

200

300

400

500

600

Dec

-69

Jul-

72

Feb-

75

Sep-

77

Apr

-80

Nov

-82

Jun-

85

Jan-

88

Aug

-90

Mar

-93

Oct

-95

May

-98

Dec

-00

Jul-

03

Feb-

06

Sep-

08

Apr

-11

UK Real EPS 10y average

0102030405060708090

100

Jan-

21Ju

n-26

Nov

-31

Apr

-37

Sep-

42Fe

b-48

Jul-

53D

ec-5

8M

ay-6

4O

ct-6

9M

ar-7

5A

ug-8

0Ja

n-86

Jun-

91N

ov-9

6A

pr-0

2Se

p-07

Real SPX EPS 10y average Source: Datastream Source: Haver Analytics, Barclays research

Barclays | Equity Gilt Study

21 February 2013 11

FIGURE 14 Real EPS and ‘cyclically adjusted’ EPS – three scenarios

Scenario 1 Stable @ 90 then 0% real earnings growth

0

10

20

30

40

50

60

70

80

90

100

Jan-21 Jan-54 Jan-87 Jan-20

Real SPX EPS - Scenario 1 10y avg

Scenario 2 10% decline then 1.0% real earnings growth

0

10

20

30

40

50

60

70

80

90

100

Jan-21 Jan-54 Jan-87 Jan-20

Real EPS - Scenario 2 10y average

Scenario 3 Stable at $90 then 1.5% real earnings growth

0

20

40

60

80

100

120

Jan-21 Jan-54 Jan-87 Jan-20

Real EPS - Scenario 3 10y average

Source: Haver Analytics, Barclays Research

This is not a very realistic scenario, nor do we suggest that investors should lean too much on the rough-and-ready valuation approach that is so heavily driven by the assumption of normalization of the CAPE. But the example illustrates that it is possible for equity markets to deliver positive real returns, even under the assumption that the CAPE normalizes over time, and with very low growth in (inflation-adjusted) earnings per share, as long as the normalization occurs gradually (in line with the gradual normalization of global financial conditions more generally). In this sense, we think that investors need not worry unduly about the elevated CAPE, even if they adopt the view that it is likely eventually to decline from the current elevated level.

Other scenarios are possible. In our second example, we assume a 10% drop in corporate profits from current levels, followed by a 1.0% rate of growth. In this case, the same approach suggests a real return to US equities of about 1.5% over the next five years and 2% over the next 10 years. This is very low by historical standards, but is still positive in real terms, and some 300bp above the expected real return on government bonds.

In the third scenario in Figure 14, we illustrate a more optimistic example, in which real EPS grows 1.5% from its current level. In this case, the CAPE-driven valuation approach generates inflation-adjusted equity returns of about 3% in the next five years, and roughly 3.5% over the next 10 years.

In short, we think the CAPE has become interesting not because it provides an alternative and more reliable signal of market valuations, but because it highlights the magnitude and market significance of the surge in US corporate earnings since the early 1990s. It is hard to think of a more important question for equity investors than whether this surge in earnings can be sustained in the years to come.

A closer look at corporate profits We turn now to macroeconomic measures of corporate income and its drivers, where the 20-year surge in corporate profits is as striking as in the earnings data of listed companies. The US data allow us to identify three components of the surge, all of them significant. First, profits in the financial sector have skyrocketed since the early 1990s, and have surprisingly returned to pre-crisis peak levels as a share of overall corporate value added. We note, however, that the outlook for return on capital in the financial sector may be more challenging than the outlook for aggregate profitability, as financial institutions may be required by market and regulatory forces to continue raising capital and reducing the leverage of their operations.

Investors need not worry unduly about the elevated CAPE, even if they believe it will eventually decline from current elevated levels

Barclays | Equity Gilt Study

21 February 2013 12

The second component is profits generated by international operations, which skyrocketed from roughly 2.5% of corporate value added before the early 1990s, to roughly 5.5% now. The third component is profit generated by domestic operations of nonfinancial corporations. This remains the largest component of profits, and also the biggest contributor of the three to the growth in aggregate profits between the early 1990s and now.

FIGURE 15 US corporate profits as a share of value added by the corporate sector

0%

5%

10%

15%

20%

25%

30%

Q1 48 Q1 55 Q1 62 Q1 69 Q1 76 Q1 83 Q1 90 Q1 97 Q1 04 Q1 11

Domestic non-financial sector Financial sector Rest of world Source: Haver Analytics

In preparation for this chapter, we searched for academic research on the topic, expecting that a sea change of this magnitude would be the object of study by academic economists. We were disappointed to find little since the mid-1990s. Nevertheless, some stylized facts are easy to draw out of the data. In a statistical explanation of nonfinancial domestic profits as a share of corporate value added, we identified three powerful drivers:

• The first is the business cycle, represented by the rate of capacity utilization. This exerts a powerful influence, but is volatile and is not a major factor in the 20-year trend rise in corporate profitability.

• The second is the real exchange rate where, consistent with a number of academic studies from the early 1990s, we found that a weaker currency is associated with a higher rate of profits in the US. The estimated effect is powerful; all else equal, a 10% real exchange rate depreciation is estimated to increase the rate of profit by nearly a percentage point (from about 10% in the early 1990s). But the real exchange rate was almost exactly as weak in the early 1990s as it is now, so this factor explains little of the rise in the past 20 years.

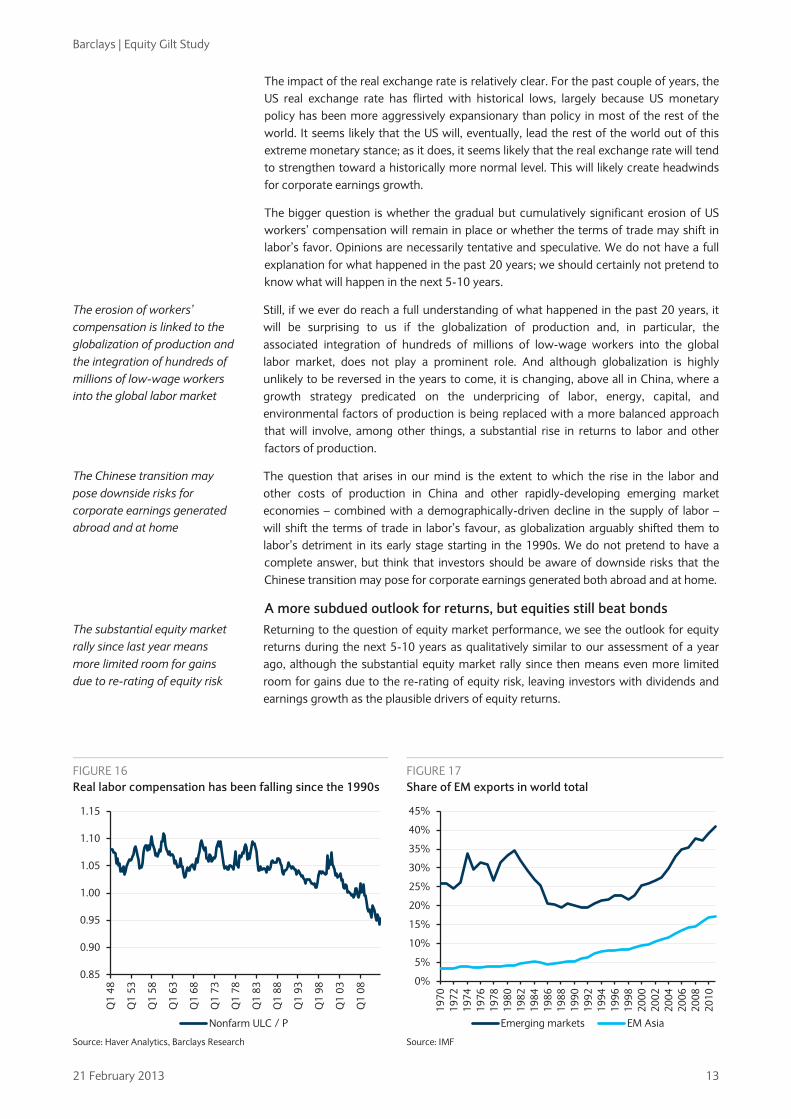

• The third is the cost of labor, as measured by the ratio of unit labor costs to the price of private-sector output. This measure of labor compensation fluctuated in a narrow range until the early 1990s, then began to fall steadily, registering a cumulative fall of nearly 10% (Figure 16), which implies that labor compensation fell far short of the cumulative growth in productivity during the 20 years. Our statistical analysis suggests that the decline in this measure of labor compensation fully explains the rise in the rate of nonfinancial corporate profit from the early 1990s to the present.

At one level, it is unsurprising that the 20-year surge in corporate profits has been associated with a gap between growth in productivity and labor compensation. Still, other explanations are conceivable, and it concentrates the mind to see the expected association borne out in the data. The relevant question for us is what this might suggest about the outlook for profitability in the years to come.

The 20-year surge in corporate profits has been associated with a gap between growth in productivity and labor compensation

Barclays | Equity Gilt Study

21 February 2013 13

The impact of the real exchange rate is relatively clear. For the past couple of years, the US real exchange rate has flirted with historical lows, largely because US monetary policy has been more aggressively expansionary than policy in most of the rest of the world. It seems likely that the US will, eventually, lead the rest of the world out of this extreme monetary stance; as it does, it seems likely that the real exchange rate will tend to strengthen toward a historically more normal level. This will likely create headwinds for corporate earnings growth.

The bigger question is whether the gradual but cumulatively significant erosion of US workers’ compensation will remain in place or whether the terms of trade may shift in labor’s favor. Opinions are necessarily tentative and speculative. We do not have a full explanation for what happened in the past 20 years; we should certainly not pretend to know what will happen in the next 5-10 years.

Still, if we ever do reach a full understanding of what happened in the past 20 years, it will be surprising to us if the globalization of production and, in particular, the associated integration of hundreds of millions of low-wage workers into the global labor market, does not play a prominent role. And although globalization is highly unlikely to be reversed in the years to come, it is changing, above all in China, where a growth strategy predicated on the underpricing of labor, energy, capital, and environmental factors of production is being replaced with a more balanced approach that will involve, among other things, a substantial rise in returns to labor and other factors of production.

The question that arises in our mind is the extent to which the rise in the labor and other costs of production in China and other rapidly-developing emerging market economies – combined with a demographically-driven decline in the supply of labor – will shift the terms of trade in labor’s favour, as globalization arguably shifted them to labor’s detriment in its early stage starting in the 1990s. We do not pretend to have a complete answer, but think that investors should be aware of downside risks that the Chinese transition may pose for corporate earnings generated both abroad and at home.

A more subdued outlook for returns, but equities still beat bonds Returning to the question of equity market performance, we see the outlook for equity returns during the next 5-10 years as qualitatively similar to our assessment of a year ago, although the substantial equity market rally since then means even more limited room for gains due to the re-rating of equity risk, leaving investors with dividends and earnings growth as the plausible drivers of equity returns.

FIGURE 16 Real labor compensation has been falling since the 1990s

FIGURE 17 Share of EM exports in world total

0.85

0.90

0.95

1.00

1.05

1.10

1.15

Q1

48

Q1

53

Q1

58

Q1

63

Q1

68

Q1

73

Q1

78

Q1

83

Q1

88

Q1

93

Q1

98

Q1

03

Q1

08

Nonfarm ULC / P

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

Emerging markets EM Asia Source: Haver Analytics, Barclays Research Source: IMF

The erosion of workers’ compensation is linked to the globalization of production and the integration of hundreds of millions of low-wage workers into the global labor market

The Chinese transition may pose downside risks for corporate earnings generated abroad and at home

The substantial equity market rally since last year means more limited room for gains due to re-rating of equity risk

Barclays | Equity Gilt Study

21 February 2013 14

In the US, where the ‘cyclical’ rebound in earnings seems largely complete, and secular drivers of earnings seem marked by at least as much downside risk as upside potential, we think it would be optimistic to assume more than 1.5-2.0% growth in real EPS for the next half decade of so, consistent with an expected real return of something like 3.5-4.0%. This is low by historical standards, but the implied risk premium vs government bonds of 550-600bp is at the high end of historical experience. In Europe, where a cyclical rebound in earnings is more plausible, valuations are less challenging, and dividend payouts higher, equities are likely to offer expected returns 100-150bp higher than in the US in the next half decade or so.

Credit can earn more than bonds, but not much As heavily influenced as credit markets are by developments in both government bond and equity markets, we require a benchmark against which to evaluate over- or underperformance compared with those markets. We adopt an empirical approach based on the idea that returns on corporate credit can be expressed as the sum of the return on government bonds, a beta to the equity market, and what is left unexplained. In our empirical formulation, the government bond markets are both intermediate and long-duration bonds, and we allow the data to determine the appropriate weight (which turns out to be about 75% to intermediate bonds and 25% to long bonds).

Using monthly data from 1973, roughly 75% of the variation in returns on US investment-grade corporate credit can be explained by statistical correlations with government bonds and equity markets. The remaining 25%, though not the largest part of the asset class’s total return, is nevertheless interesting. Figure 18 shows the cumulative ‘outperformance’, as measured by the idiosyncratic component of this statistical decomposition, since the early 1970s.

Simplistic though the approach may be, it highlights the relative performance of credit during key episodes of recent financial history. The underperformance of credit during the 1996-2002 equity-market bubble stands out clearly, and the underperformance of credit during the 2008-09 collapse is even more striking. The results also highlight the rapid recovery of credit from the recent collapse, and the substantial cumulative outperformance by credit since the immediate pre-crisis years. The strong performance of high-grade credit is also evident in valuations. Credit spreads are still above their pre-crisis lows, but they are below historically normal levels, and we think it would be optimistic to project a substantial decline in spreads during the coming five years. If spreads remain constant (at, for example, just under 140bp for corporate bonds in the Barclays US Aggregate index), then credit will outperform ‘safe haven’ bonds, but not by enough to avoid negative inflation-adjusted returns during the next five years.

Equities are likely to offer expected returns that are higher in Europe than in the US

FIGURE 18 Cumulative outperformance of investment-grade corporate credit in the US

-0.30

-0.25

-0.20

-0.15

-0.10

-0.05

0.00

0.05

0.10

Jan-73 Jan-77 Jan-81 Jan-85 Jan-89 Jan-93 Jan-97 Jan-01 Jan-05 Jan-09 Jan-13

Cumulative outperformance of high-grade credit Source: Barclays Research

Barclays | Equity Gilt Study

21 February 2013 15

Conclusion As the economic and financial tails risks that loomed so large in the aftermath of the 2008-09 financial collapse recede, investors confront a more tranquil environment, but one in which valuations are far more challenging, and prospective investment returns correspondingly diminished. In the next half-decade, investors also face the probable need to navigate an eventual sea change in the global financial environment, as the extraordinarily expansionary monetary stances of central banks around the world give way to a gradual normalization of financial conditions. Precisely how this will play out will depend upon valuations, positioning, and economic developments in the months and years to come. But the present reality of extraordinarily loose monetary policy suggests to us that real returns on cash will remain low during the next five years, when we think investors should be prepared to lose about 1.5% after adjustment for inflation in the US, with returns a little lower in the UK and higher in the euro area.

The pending normalization of financial conditions, although likely to be delayed and gradual, is likely to result in particularly low returns in ‘safe haven’ bond markets. We think that investors should be prepared to lose 50-75bp more on long-term ‘safe haven’ bonds than the 1.5% pa that they are likely to lose in cash (after adjustment for inflation). These low returns on government bonds are an artefact of the five-year time horizon that is our focus. After that period, market yields will likely have risen to levels that offer investors modestly positive returns on their ‘safe haven’ bond investments.

With credit spreads above their historical lows, but somewhat lower than historical normal levels, we think it would be overly optimistic for investors to expect a further decline in spreads during the next half decade. It seems reasonable to assume that investors will collect the credit spread, roughly 135bp for investment grade corporates, which would be enough to mitigate but not to eliminate the probable loss of real value created by the exposure to interest-rate duration associated with (unhedged) exposure to credit markets.

Our estimate of expected returns to equity is lower than published in last year’s Equity Gilt Study. This reflects, in part, our present focus on a five-year investment horizon, during which we expect the yield structure of global asset markets to be depressed by the extremely expansionary monetary policy likely to prevail, even if the gradual normalization of financial conditions begins during that period, as we expect. The lower estimate of prospective equity returns also reflects the 18% rise in global equity prices since the beginning of 2012, which brought forward capital gains that might otherwise have contributed to returns in coming years.

Despite our reduced estimate of the return on equities, the estimated equity risk premium remains in the 500-600bp range, broadly consistent with historical experience. Although absolute returns are likely to be lower than long historical experience, equities have become the only real option for investors seeking positive inflation-adjusted returns. Especially if the low-volatility environment persists, as now seems to be the relevant base case, the risk (not so unpleasant to contemplate) now seems to be that the search for return will push investors more forcefully into equities, causing yet more challenging valuations and eventually undermining the investment case for equities. But we do not think that we are there yet; in the absence of an economic or financial shock to our reasonably benign case, we think that for equity investors, things are likely to get better before they get worse.

Investors should be prepared to lose 50-75bp more on long-term ‘safe haven’ bonds than the 1.5% pa that they are likely to lose in cash

For equity investors, things are likely to get better before they get worse

Barclays | Equity Gilt Study

21 February 2013 16

CHAPTER 2

Demand for safe havens to remain robust • Following on from the Equity Gilt Study 2012, in which we argued that

conventional measures of the equity risk premium appeared elevated mainly because the structural decrease in the supply of risk-free assets had resulted in unusually low risk-free bond yields, we turn to the role of demand for safe-haven assets.

• We examine three sources of demand for such assets: official-sector demand via the investment of international reserve portfolios; institutional demand in a post-crisis era of tighter bank regulation; and private demand, particularly from an aging population across the developed world.

• We look for US institutional demand and the rotation of boomer investors into bonds to make up for some of the relative decline in demand from official sources, including our expectation of diminishing reserve accumulation in China.

• We conclude that structural demand for safe havens is likely to remain high and, when combined with the structural scarcity of such assets, is likely to keep interest rates on safe assets low by comparison with historical norms and conventional measures of the equity risk premium elevated.

The abrupt and radical change in the valuation of high-quality, liquid government bonds, or ‘safe havens’, following the onset of the Great Recession is now entering its fifth calendar year. The rich valuation environment for safe havens has frequently been described as an artifact of the financial crisis: demand from private investors seeking insurance in stormy financial markets combined with asset purchases from systemically important central banks engaged in quantitative easing to produce rock-bottom interest rates across most developed government bond markets. There is little doubt that cyclical factors following the deepest global recession since the Great Depression have been important factors in the low interest rate environment.

In “The equity risk premium: Cheap equities or expensive bonds?”, 2012 Equity Gilt Study, 8 February 2012, we outlined our view that low interest rates on safe assets were driven by more than cyclical factors alone. In our view, the relative scarcity of high-quality, liquid government bonds was among the more convincing structural explanations for low interest rates on safe assets. We used the safe-asset shortage argument to buttress our view that conventional measures of the equity risk premium were elevated mainly because the valuation of safe assets had changed radically and abruptly, not because equity investors had become significantly more intolerant of holding equity risk.

We still agree with this but acknowledge that our analysis was based primarily on the supply of safe havens and did not examine fully their demand, which is the focus here. After all, the supply of safe havens will likely be held in equilibrium, but the obvious question is at what price (and yield). To understand this fully requires knowing more about the objectives of the myriad of investors who include such assets in their portfolio decisions. We examine three components of safe asset demand: official-sector demand via the investment of international reserve portfolios; institutional demand in a post-crisis era of tighter bank regulation; and private demand, particularly from an aging population across the developed world.

We find that structural demand for safe havens is likely to remain high and, when combined with the structural scarcity of such assets, to keep interest rates on safe assets low and conventional measures of the equity risk premium elevated. The rebalancing of the global economy following the crisis should slow the growth of international reserve portfolios, particularly in China, where we see the country in the

Michael Gapen

+1 212 526 8536 [email protected]

The rich valuation environment for safe havens has frequently been described as an artifact of the financial crisis

But low rates on safe assets are driven by more than cyclical factors: they result from the relative scarcity of high-quality, liquid government bonds

The supply of safe havens will likely be held in equilibrium, but the question is at what price (and yield)

A much tighter regulatory landscape and an aging population will result in lasting demand for safe assets

Barclays | Equity Gilt Study

21 February 2013 17

early stages of breaking away from its old growth model (see Chapter 3, “Can China avoid the middle-income trap?”) but we find that demand for safe havens from official sources will remain important and their investment mandates make them fairly price- insensitive. We expect official demand for such assets to be complemented by two important shifts in the coming years. First is a much tighter regulatory landscape, where we see Basel III recommendations for higher capital and stronger liquidity coverage ratios as generating a structural increase in demand for safe havens, particularly from US financial institutions. Second, the aging population in the developed world should provide lasting demand for dollar- and euro-denominated safe havens due to shortened investment horizons and the need to fund current consumption during retirement years. We highlight the US, where the aging of the baby boom generation means almost half of US households will have a head of household aged 55 or older by the end of the decade. This investor class controls nearly two-thirds of household net worth and total financial assets in the US, and their portfolio decisions will carry proportionately larger weight.1

The main conclusions of this chapter are in concert with our findings elsewhere in the Equity Gilt Study 2013. Conventional wisdom suggests the current low interest rate environment cannot last. Some proponents of this view believe the combination of rock-bottom yields and high equity risk premium will produce a herd effect, or “great rotation,” as investors abandon fixed income investments in favour of equities, decimating investor portfolios with high exposure to fixed income. Other proponents of this view cite bloated central bank balance sheets as leading to rising inflation and higher nominal yields.

We find ourselves in partial agreement. We agree that low yields on safe haven assets and wide equity risk premiums will ultimately reward those investors willing to move out the risk spectrum (see Chapter 1, “Low risk, low return”). However, our view that equities remain attractive for those with a medium-term or longer horizon is partly dependent on structural shifts in the supply and demand for safe havens that are likely to keep the existing risk-reward structure in place. We would have less conviction about the relative attractiveness of equities at current valuations if our views on safe havens were influenced by cyclical factors alone. In addition, we are inclined to discount the risks of inflation associated with quantitative easing and the unprecedented expansion of central bank balance sheets (see Chapter 4, “QE carries risks beyond inflation”). None of this is to say that yields cannot rise; they undoubtedly will to some degree, as markets and policy normalize and economies continue to heal and cleanse the imbalances of the previous decade. However, structural factors limiting safe haven supply and supporting demand suggest to us that low real and nominal yields on safe havens will be more the norm than the exception in the years ahead.

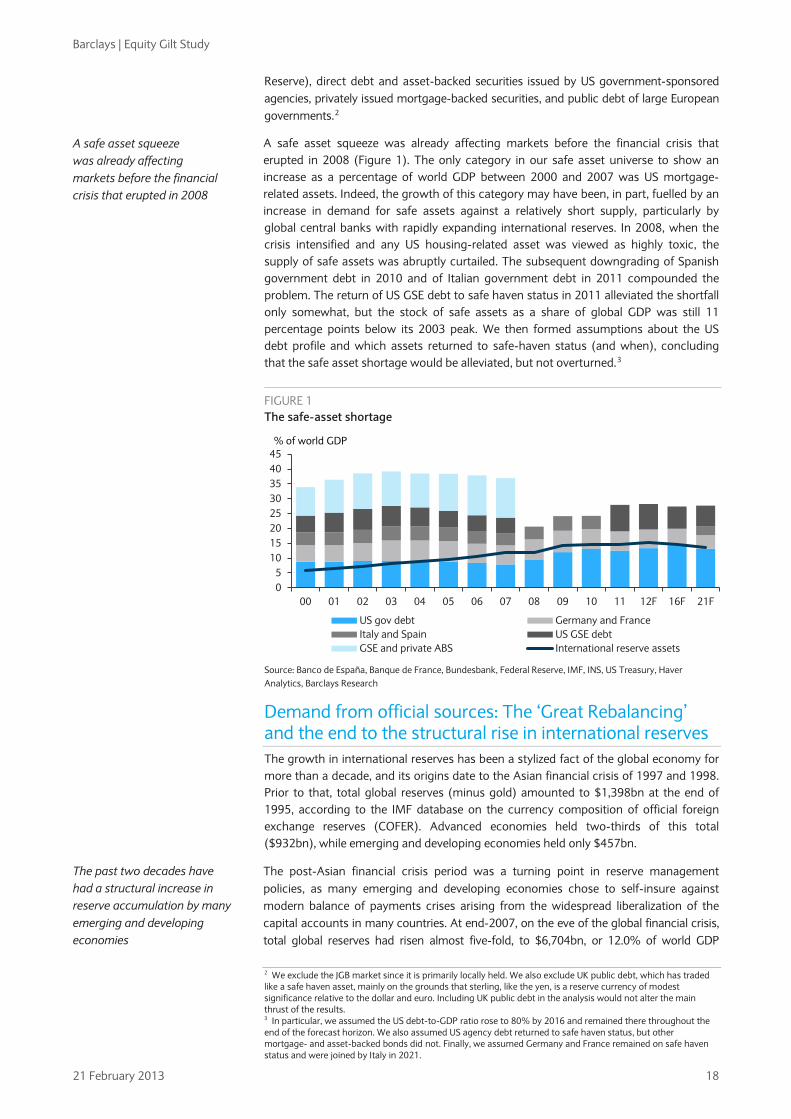

The supply of safe assets: Where are we? We begin with a brief review of our findings on the safe asset shortage. To illustrate our view that the relative scarcity of high-quality, liquid government bonds was among the more convincing structural explanations for low interest rates on safe assets, we defined the safe asset universe at the onset of the Great Recession and plotted the outstanding stock of these assets as a percentage of world GDP over time (see “The equity risk premium: Cheap equities or expensive bonds?”, Equity Gilt Study 2012, 8 February 2012). The precise definition of a safe asset can vary depending on context, but we assume that it is reasonable to expect such assets to deliver very low default risk, high liquidity, and low currency risk. In applying this screen, we viewed the safe asset universe as including US government debt (excluding that held by the Federal

1 Outside of official demand from international reserve portfolios, we focus our analysis on US institutions and households since outstanding US Treasuries and US GSE debt accounts for more than 75% of the safe haven universe at present (Figure 1). US institutions and households are likely to exhibit a high degree of “home bias” in their portfolio decisions since financial institutions are subject to regulatory requirements to hold a sufficient liquidity backstop against local currency deposits and US households nearing retirement have a US dollar-denominated consumption basket. We leave non-US institutional and private sector demand for safe havens for future work.

Our view on the relative attractiveness of equities is predicated on structural factors that will keep yields on safe assets low

Barclays | Equity Gilt Study

21 February 2013 18

Reserve), direct debt and asset-backed securities issued by US government-sponsored agencies, privately issued mortgage-backed securities, and public debt of large European governments.2

A safe asset squeeze was already affecting markets before the financial crisis that erupted in 2008 (Figure 1). The only category in our safe asset universe to show an increase as a percentage of world GDP between 2000 and 2007 was US mortgage-related assets. Indeed, the growth of this category may have been, in part, fuelled by an increase in demand for safe assets against a relatively short supply, particularly by global central banks with rapidly expanding international reserves. In 2008, when the crisis intensified and any US housing-related asset was viewed as highly toxic, the supply of safe assets was abruptly curtailed. The subsequent downgrading of Spanish government debt in 2010 and of Italian government debt in 2011 compounded the problem. The return of US GSE debt to safe haven status in 2011 alleviated the shortfall only somewhat, but the stock of safe assets as a share of global GDP was still 11 percentage points below its 2003 peak. We then formed assumptions about the US debt profile and which assets returned to safe-haven status (and when), concluding that the safe asset shortage would be alleviated, but not overturned.

3

FIGURE 1 The safe-asset shortage

05

1015202530354045

00 01 02 03 04 05 06 07 08 09 10 11 12F 16F 21F

US gov debt Germany and FranceItaly and Spain US GSE debtGSE and private ABS International reserve assets

% of world GDP

Source: Banco de España, Banque de France, Bundesbank, Federal Reserve, IMF, INS, US Treasury, Haver Analytics, Barclays Research

Demand from official sources: The ‘Great Rebalancing’ and the end to the structural rise in international reserves The growth in international reserves has been a stylized fact of the global economy for more than a decade, and its origins date to the Asian financial crisis of 1997 and 1998. Prior to that, total global reserves (minus gold) amounted to $1,398bn at the end of 1995, according to the IMF database on the currency composition of official foreign exchange reserves (COFER). Advanced economies held two-thirds of this total ($932bn), while emerging and developing economies held only $457bn.

The post-Asian financial crisis period was a turning point in reserve management policies, as many emerging and developing economies chose to self-insure against modern balance of payments crises arising from the widespread liberalization of the capital accounts in many countries. At end-2007, on the eve of the global financial crisis, total global reserves had risen almost five-fold, to $6,704bn, or 12.0% of world GDP

2 We exclude the JGB market since it is primarily locally held. We also exclude UK public debt, which has traded like a safe haven asset, mainly on the grounds that sterling, like the yen, is a reserve currency of modest significance relative to the dollar and euro. Including UK public debt in the analysis would not alter the main thrust of the results. 3 In particular, we assumed the US debt-to-GDP ratio rose to 80% by 2016 and remained there throughout the end of the forecast horizon. We also assumed US agency debt returned to safe haven status, but other mortgage- and asset-backed bonds did not. Finally, we assumed Germany and France remained on safe haven status and were joined by Italy in 2021.

A safe asset squeeze was already affecting markets before the financial crisis that erupted in 2008

The past two decades have had a structural increase in reserve accumulation by many emerging and developing economies

Barclays | Equity Gilt Study

21 February 2013 19

(Figure 2). Emerging and developing economies accounted for much of the rise, with reserves climbing from $475bn in 1995 to $4,272bn in 2007, for a 64% share of total global reserves (Figure 3). In just 12 years, emerging/developing economies had become the dominant holders of international reserves.

The precautionary motive The level of accumulated reserves in many countries was generally viewed as far exceeding the amount needed to protect against conditional access to capital markets and adjustment costs. Studies that estimated the optimal level of precautionary reserves conditioned reserve balances on the level of government expenditures, level of debt, cost of adjustment, size of international transactions, economic variability, and exchange rate regime (fixed versus floating), among other factors.4

Competitiveness, terms of trade, and export promotion

These concluded that precautionary demand for international reserves, while an important contributing factor, was insufficient to explain fully the structural shift in reserve demand that began in the late 1990s.

In the years following the Asian financial crisis, many of the affected economies were subject to substantial real exchange rate depreciations, which enhanced competitiveness and terms of trade and, ultimately, led to improved trade balances. For example, real effective exchange rates at the end of 2004 in many of the affected economies were substantially below their pre-crisis levels (Figure 4). The combination of exchange rate regimes, controls and taxes on capital inflows and exchange market interventions allowed trade surpluses to persist and prevented currency appreciation. The widespread adoption of these policies by Asian countries, particularly China, led some to frame the issue of reserve accumulation as a normal evolution of the international monetary system.5

4 For an analysis of the determinants of reserve accumulation in emerging and developing economies, see Michael Gapen and Michael Papaioannou, 2008, “Reserve accumulation: Macroeconomics and management issues,” in Y. Kurihari, S. Takaya, H. Harui, and H. Kamae, editors, Information Technology and Economic Development, IGI Global: Hershey, PA; Olivier Jeanne and Romain Ranciere, 2006, “The Optimal Level of international reserves for emerging market countries: Formulas and applications, IMF Working Paper 06/229; and J. Aizenman and N. Marion, 2002, “The high demand for international reserves in the Far East: What’s going on? NBER Working Paper No. 9266, Cambridge: NBER.

Proponents of this view argued that the emergence of a fixed exchange rate periphery in Asia re-established the US as the center of a new Bretton-Woods-style international monetary order. In this scenario, Asia’s economic growth would ultimately require financial liberalization and floating exchange rates. In the meantime, however, the system of undervalued exchange rates and capital controls led to official capital outflows and the accumulation of reserve asset claims on the US.

5 See Michael Dooley, David Folkerts-Landau, and Peter Garber, 2003, “An essay on the revived Breton Woods system, NBER Working Paper No. 9971, Cambridge: NBER.

FIGURE 2 The desire to self-insure prompted a sharp growth in the reserve portfolios of many emerging economies

FIGURE 3 The share of total reserves held by emerging and developing economies rose steadily

0

2

4

6

8

10

12

14

16

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11

Total international reserves

Emerging and developing economies

Advanced economies

% of world GDP

20

25

30

35

40

45

50

55

60

65

70

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11

Emerging and developing economies

Advanced economies

% Share of total foreign exchange holdings

Source: IMF Statistics Department COFER database and International Financial Statistics

Source: IMF Statistics Department COFER database and International Financial Statistics

Precautionary demand for international reserves is insufficient to explain the structural increase in reserve demand

Undervalued exchange rates and capital controls in Asian countries led to official capital outflows and the accumulation of reserve asset claims on the US

Barclays | Equity Gilt Study

21 February 2013 20

FIGURE 4 Real effective exchange rates: 1996-2012

50

60

70

80

90

100

110

120

130

96 98 00 02 04 06 08 10 12

USD EUR PHP MYR SGD THB

12/31/96 = 100

Real effective exchange rate

Source: Barclays Research

The Great Rebalancing The prolonged accumulation of reserves from persistent structural imbalances had a deleterious effect on global financial stability and was unwound in a disorderly manner. There had been a vigorous debate about how long the arrangement could persist, given the mutually reinforcing policies of the public sectors in Asia and the US, and the degree to which these policies were beyond the reach of the private sector and market forces. The answer came in 2008, when market forces overwhelmed the system. The substantial and immediate adjustment seems to have brought an end to the period of aggressive reserve accumulation by official sources. The current account surpluses of major Asian economies have fallen, while the large current account deficits of the US and other developed economies have narrowed (Figures 5 and 6). Real exchange rate misalignment has also been reduced (Figure 4). The rebalancing of the global economies has been substantial and was achieved in fairly short order, but not without significant economic disruption to global markets along the way.

In retrospect, the marked growth in seemingly safe asset-backed securities was largely an endogenous response to the fact that the bulk of the current account surpluses was held and managed by risk-averse public sector institutions. These surpluses, accumulated in the form of foreign exchange reserves to reduce risks of future balance of payments crises, needed somewhere to go. The burgeoning securitized market substituted for high-quality, liquid government securities, which were becoming increasingly scarce. Excluding

The crisis of 2008 brought an end to the period of aggressive reserve accumulation by official sources

FIGURE 5 The current account surpluses of major Asian economies have fallen…

FIGURE 6 …and current account deficits mean global imbalances have been reduced

0

2

4

6

8

10

12

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

China Japan

Current account balance, % of GDP

-12

-10

-8

-6

-4

-2

0

2

4

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

US UK Spain Italy

Current account balance, % of GDP

Note: 2012 data are Barclays’ forecast. Source: SAFE, BOJ, Barclays Research Source: BDE, BdIt, BEA, BoJ, Bundesbank, ECB, ONS, Haver Analytics

Barclays | Equity Gilt Study

21 February 2013 21

the asset-backed securities category from Figure 1, the remaining supply of safe assets shrunk from 27.6% of world GDP in 2003 to 20.6% in 2008. The sharp increase in US Treasury debt in response to the economic contraction and financial instability that followed has not been enough to offset the loss of the GSEs, the asset-backed mortgage market and, later, the sovereign debt of Italy and Spain.

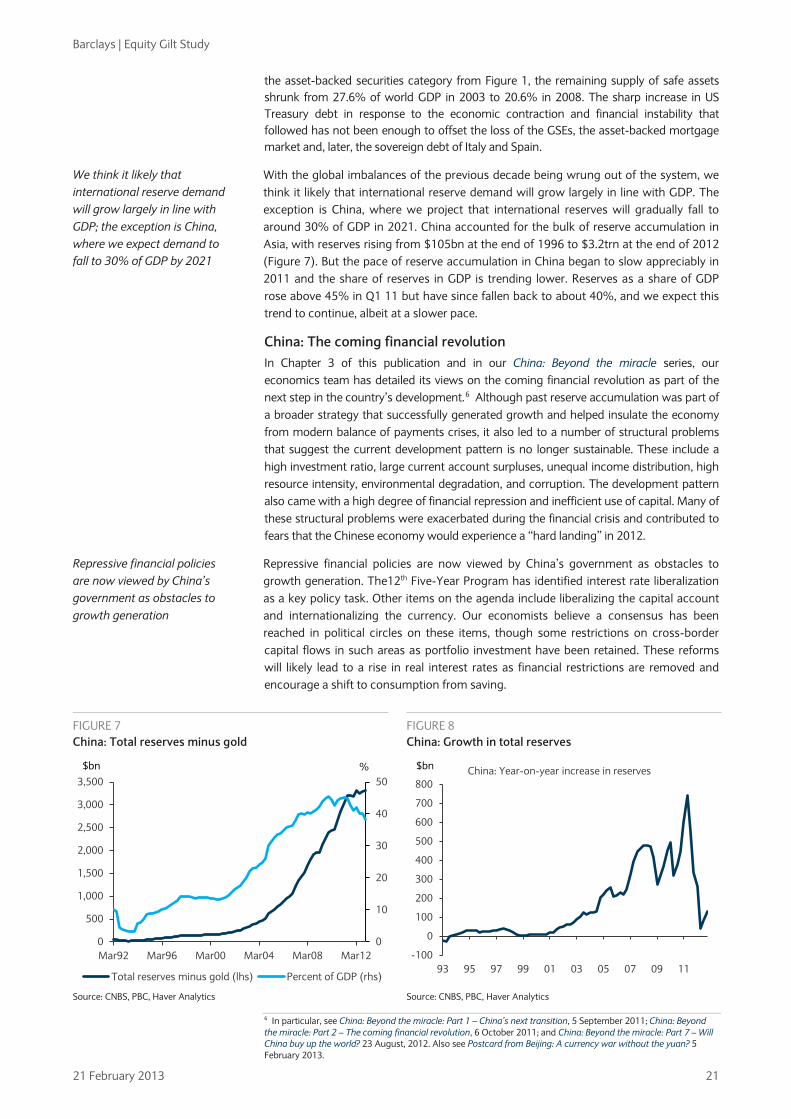

With the global imbalances of the previous decade being wrung out of the system, we think it likely that international reserve demand will grow largely in line with GDP. The exception is China, where we project that international reserves will gradually fall to around 30% of GDP in 2021. China accounted for the bulk of reserve accumulation in Asia, with reserves rising from $105bn at the end of 1996 to $3.2trn at the end of 2012 (Figure 7). But the pace of reserve accumulation in China began to slow appreciably in 2011 and the share of reserves in GDP is trending lower. Reserves as a share of GDP rose above 45% in Q1 11 but have since fallen back to about 40%, and we expect this trend to continue, albeit at a slower pace.

China: The coming financial revolution In Chapter 3 of this publication and in our China: Beyond the miracle series, our economics team has detailed its views on the coming financial revolution as part of the next step in the country’s development.6

Repressive financial policies are now viewed by China’s government as obstacles to growth generation. The12th Five-Year Program has identified interest rate liberalization as a key policy task. Other items on the agenda include liberalizing the capital account and internationalizing the currency. Our economists believe a consensus has been reached in political circles on these items, though some restrictions on cross-border capital flows in such areas as portfolio investment have been retained. These reforms will likely lead to a rise in real interest rates as financial restrictions are removed and encourage a shift to consumption from saving.

Although past reserve accumulation was part of a broader strategy that successfully generated growth and helped insulate the economy from modern balance of payments crises, it also led to a number of structural problems that suggest the current development pattern is no longer sustainable. These include a high investment ratio, large current account surpluses, unequal income distribution, high resource intensity, environmental degradation, and corruption. The development pattern also came with a high degree of financial repression and inefficient use of capital. Many of these structural problems were exacerbated during the financial crisis and contributed to fears that the Chinese economy would experience a “hard landing” in 2012.

6 In particular, see China: Beyond the miracle: Part 1 – China’s next transition, 5 September 2011; China: Beyond the miracle: Part 2 – The coming financial revolution, 6 October 2011; and China: Beyond the miracle: Part 7 – Will China buy up the world? 23 August, 2012. Also see Postcard from Beijing: A currency war without the yuan? 5 February 2013.

We think it likely that international reserve demand will grow largely in line with GDP; the exception is China, where we expect demand to fall to 30% of GDP by 2021

FIGURE 7 China: Total reserves minus gold

FIGURE 8 China: Growth in total reserves

0

10

20

30

40

50

0

500

1,000

1,500