Equity Valuation Dividend Discount Method with constant earnings growth rate 1

Equity Valuation Dividend Discount Method with constant earnings growth rate 1.

Jan 03, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Equity Valuation Dividend Discount Method with constant earnings growth rate

1

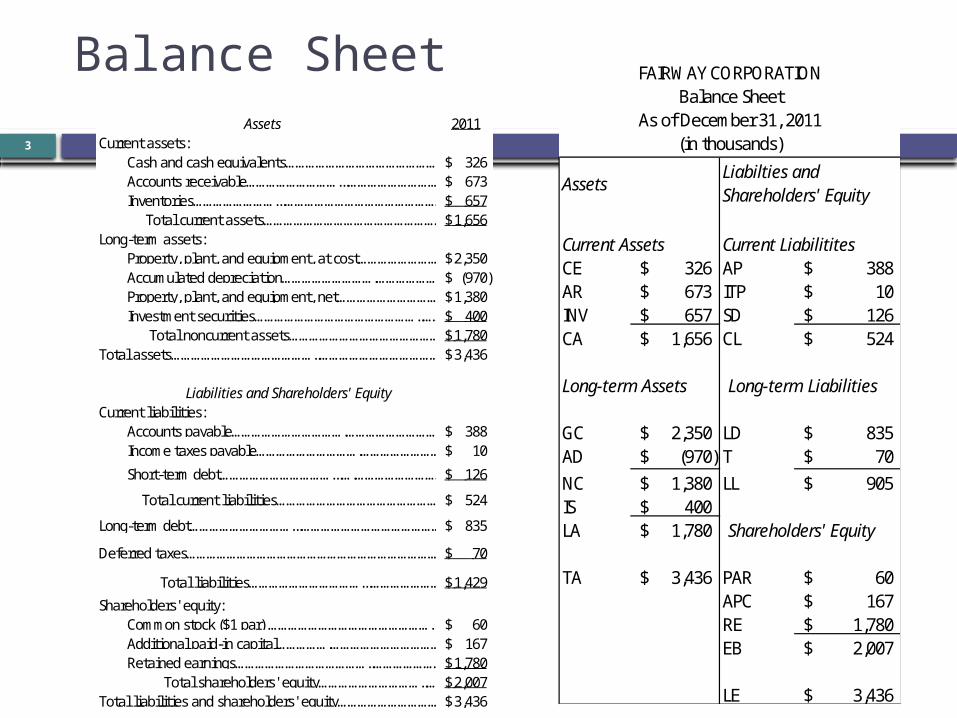

Balance Sheet2

Assets 2010 2011 ChangeCurrent assets:

Cash and cash equivalents…………………………………………….230$ 326$ 96$ Accounts receivable………………………...………………………………….586$ 673$ 87$ Inventories……………………...…………………………………………………..610$ 657$ 47$ Total current assets………………………………………………….1,426$ 1,656$ 230$

Long-term assets:Property, plant, and equipment, at cost…………………………………….2,000$ 2,350$ 350$ Accumulated depreciation……………………….………………………………..(1,000)$ (970)$ 30$ Property, plant, and equipment, net………………………………………………1,000$ 1,380$ 380$ Investment securities…………………………………………..…………………..450$ 400$ (50)$ Total noncurrent assets……………………………………………1,450$ 1,780$ 330$

Total assets……………………………………..………………………………………………..2,876$ 3,436$ 560$

Liabilities and Shareholders' EquityCurrent liabilities:

Accounts payable…………………………….…………………………………….332$ 388$ 56$ Income taxes payable………………………….…………………………………….9$ 10$ 1$

Short-term debt……………………………...….…………………………………….147$ 126$ (21)$

Total current liabilities………………………………………………..488$ 524$ 36$

Long-term debt…………………………...…………………………………………………….500$ 835$ 335$

Deferred taxes………………………………………………………………………..65$ 70$ 5$

Total liabilities……………………………...……………………………..1,053$ 1,429$ 376$

Shareholders' equity:Common stock ($1 par) …………………………………………...…………….50$ 60$ 10$ Additional paid-in capital…………….…………………………………….133$ 167$ 34$ Retained earnings…………………………………..………………………………1,640$ 1,780$ 140$ Total shareholders' equity…………………………..………………..1,823$ 2,007$ 184$

Total liabilities and shareholders' equity………………………………….………..2,876$ 3,436$ 560$

FAIRWAY CORPORATIONBalance Sheet

As of December 31, 2010, and 2011(in thousands)

Balance Sheet

3

Assets 2011Current assets:

Cash and cash equivalents……………………………………………. 326$ Accounts receivable………………………...………………………………….673$ Inventories……………………...…………………………………………………..657$ Total current assets………………………………………………….1,656$

Long-term assets:Property, plant, and equipment, at cost…………………………………….2,350$ Accumulated depreciation……………………….………………………………..(970)$ Property, plant, and equipment, net………………………………………………1,380$ Investment securities…………………………………………..…………………..400$ Total noncurrent assets……………………………………………1,780$

Total assets……………………………………..………………………………………………..3,436$

Liabilities and Shareholders' EquityCurrent liabilities:

Accounts payable…………………………….…………………………………….388$ Income taxes payable………………………….…………………………………….10$

Short-term debt……………………………...….…………………………………….126$

Total current liabilities………………………………………………..524$

Long-term debt…………………………...…………………………………………………….835$

Deferred taxes……………………………………………………………………….. 70$

Total liabilities……………………………...……………………………..1,429$

Shareholders' equity:Common stock ($1 par) …………………………………………...…………….60$ Additional paid-in capital…………….…………………………………….167$ Retained earnings…………………………………..………………………………1,780$ Total shareholders' equity…………………………..………………..2,007$

Total liabilities and shareholders' equity………………………………….………..3,436$

Current Assets Current Liabilitites CE 326$ AP 388$ AR 673$ ITP 10$ INV 657$ SD 126$ CA 1,656$ CL 524$

Long-term Assets Long-term Liabilities

GC 2,350$ LD 835$ AD (970)$ T 70$ NC 1,380$ LL 905$ IS 400$ LA 1,780$ Shareholders' Equity

TA 3,436$ PAR 60$ APC 167$ RE 1,780$ EB 2,007$

LE 3,436$

Assets Liabilties and Shareholders' Equity

FAIRWAY CORPORATION Balance Sheet

As of December 31, 2011 (in thousands)

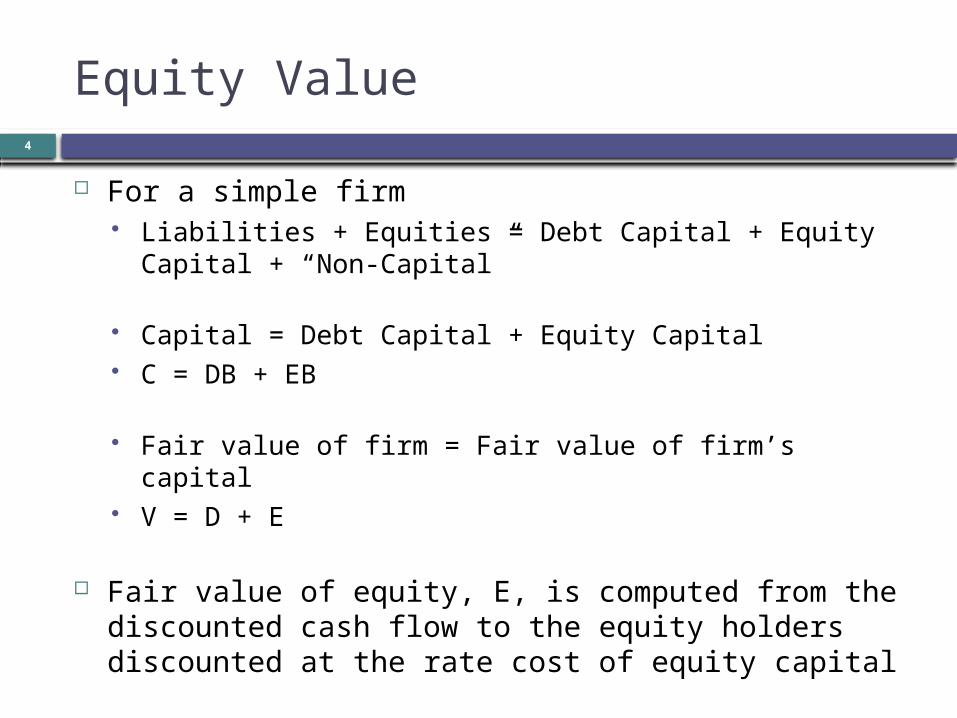

Equity Value

For a simple firm Liabilities + Equities = Debt Capital + Equity Capital + “Non-Capital”

Capital = Debt Capital + Equity Capital C = DB + EB

Fair value of firm = Fair value of firm’s capital V = D + E

Fair value of equity, E, is computed from the discounted cash flow to the equity holders discounted at the rate cost of equity capital

Assume that the cash flow to equity holders is only dividends

4

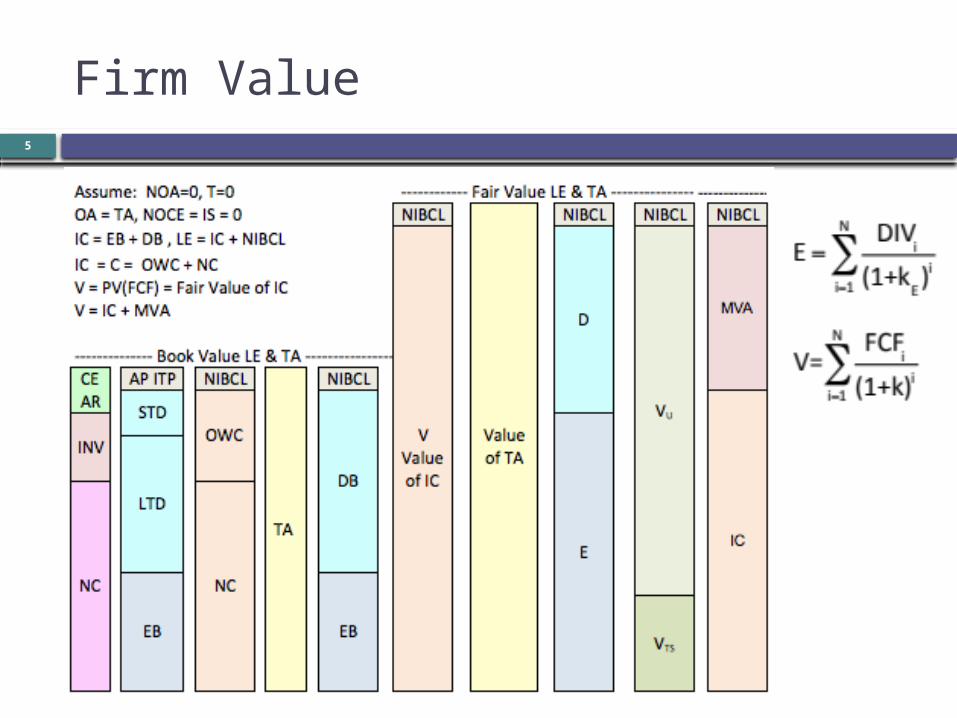

Firm Value5

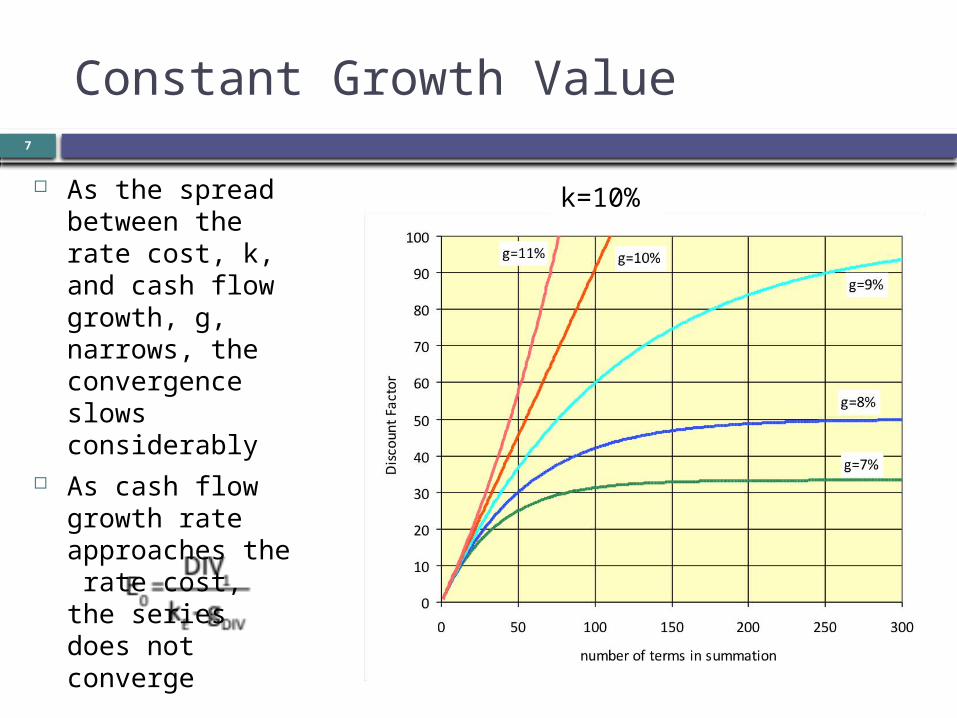

Constant Growth Rate Equity Value

The value of an financial entity is the present value of future cash flows discounted at the rate cost of the cash flows

Now assume that the dividend is growing at a constant rate, gDIV

Write as a infinite sum as follow

6

N

1ii

E

i0 )k(1

DIVE

1i

iE

1iDIV

10 )k(1)g(1

DIVE

)k(1)g(1

...)k(1)g(1

)k(1)g(1

k11

DIVEE

1DIV

3E

2DIV

2E

DIV

E10

)g1(DIVDIV DIV1i-i

Constant Growth Value

As the spread between the rate cost, k, and cash flow growth, g, narrows, the convergence slows considerably

As cash flow growth rate approaches the rate cost, the series does not converge

7

k=10%

Equity Value Management

Explore the relationships between Earnings growth Dividend payouts Cost of equity (rate) Fair value of equity

Based on the Dividend Discount Method with dividends growing at a constant rate) Gordon Growth Formula

8

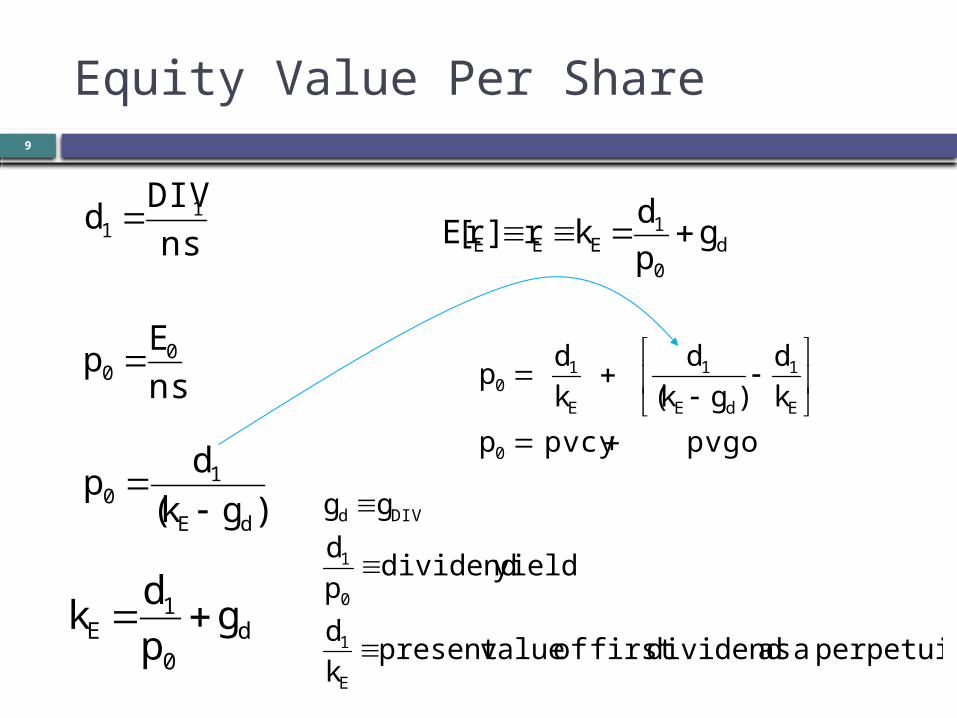

Equity Value Per Share

d0

1EEE g

pd

kr]r[E

d0

1E g

pd

k

)gk(d

pdE

10

pvgo pvcy p

kd

)gk(d

kd

p

0

E

1

dE

1

E

10

ns

Ep

ns

DIVd

00

11

9

perpetuity a as dividend firstof value presentkd

yield dividendpd

gg

E

1

0

1

DIVd

Share price v. Dividend Growth Rate

d1 = $0.50, kE = 10%

p0 = pvcy + pvgo

10

$-

$10

$20

$30

$40

$50

0% 1% 2% 3% 4% 5% 6% 7% 8% 9%

Shar

e pr

ice,

p0

dividend growth rate, gd

p0

pvgo

pvdy

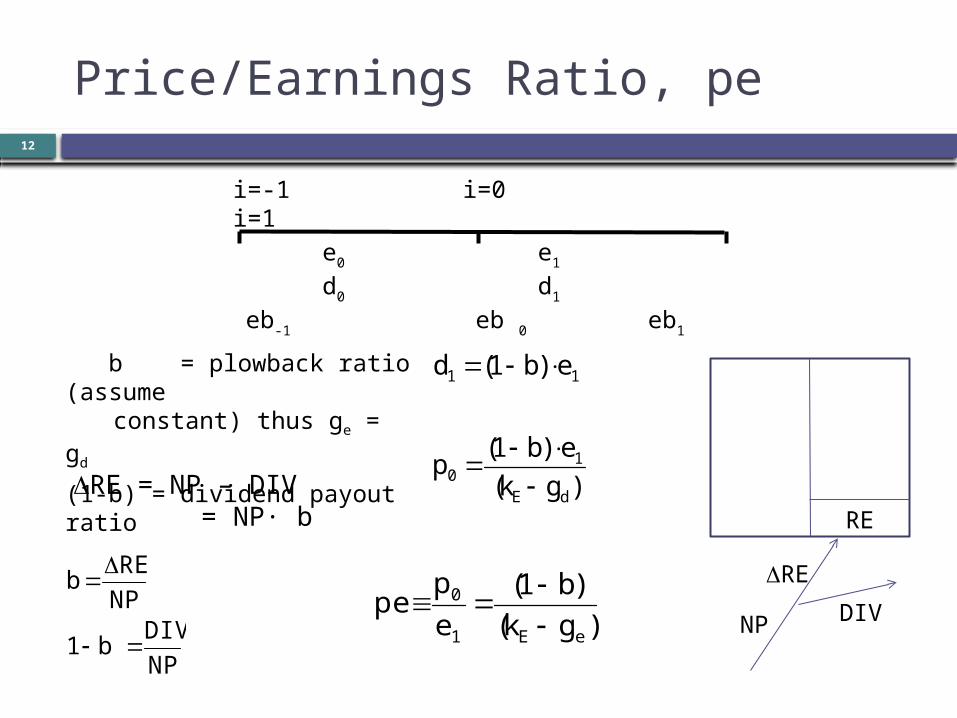

Price/Earnings Ratio: pe 11

D C = D EB + DDB

= DRE + D PAR + DAPC + DDB

D C = additional capitalDDB = additional debtD EB = additional equityDRE = additional retained earnings (=NP1 – DIV1)D PAR = additional common equity at parDAPC = additional paid in common equity

i=-1 Previous period i=0 Next period i=1

Price/Earnings Ratio, pe

i=-1 i=0 i=1

e0 e1

d0 d1

eb-1 eb 0 eb1

)gk(e)b1(

p

e)b1(d

dE

10

11

)gk()b1(

ep

peeE1

0

b = plowback ratio (assume constant) thus ge = gd

(1-b) = dividend payout ratio

12

NPDIV

b1

NPRE

b

D

DRE = NP – DIV = NP b∙ RE

NP

DRE

DIV

Price/Earnings Ratio: pe

In the case of no additional (external) investor financing DDB = 0, DAPC = D PAR = 0 D C = D EB = DRE

And a scalable firm with a constant plowback, b

)roebk()b1(

ep

peE

13

b = plowback ratio

reinvestment of earnings

(1-b) = dividend payout ratio

eb = equity book value per share

Long run assumption ge=geb

Price/Earnings Ratio: pe14

eb0 100$

ge 15%b 0.8e1 2.00$

Note: With this input, after ~40 years geb -> ge

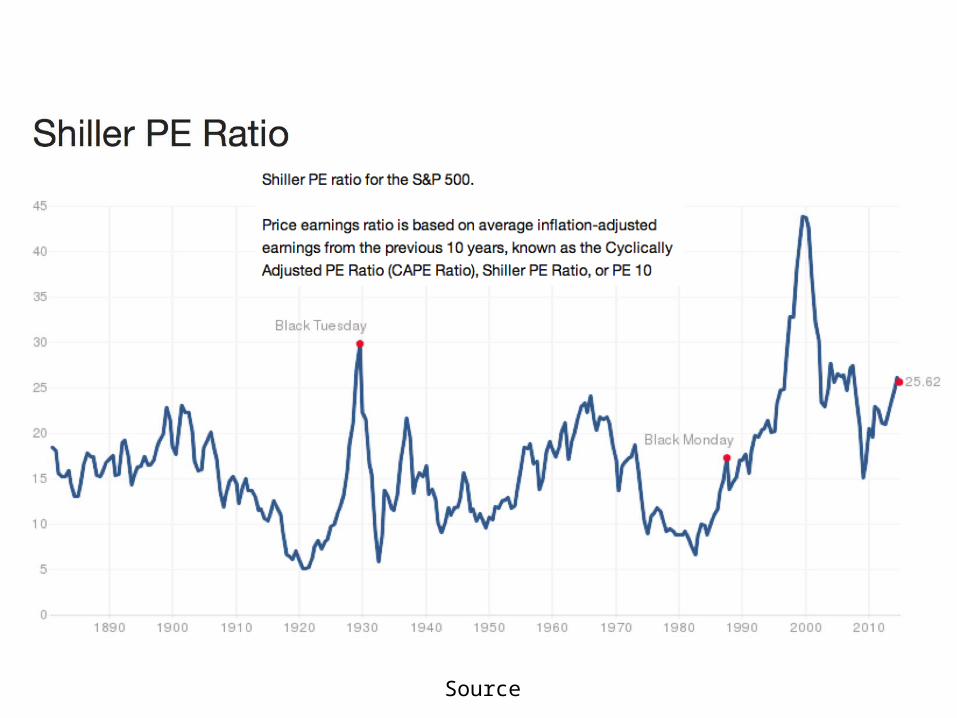

PEG Ratio

The peg is a price measure normalized for earnings (e1) and earnings growth rate (ge) 3 to 5 years estimated growth rate

Typical heuristic > 2 relatively high valuation = 1 pe ratio = earnings growth (converting ratio to percent) < 1 relatively low valuation

Morningstar Table

eEee gkg100)b1(

g100pe

peg

16

Valuation Ratios 17

Forward PE Ratio18

Critical Growth Rates

Internal growth rate, gint: the maximum growth rate that does not require additional external financing

Sustainable growth rate, gsus: the maximum growth rate that maintains the current capital structure, , with additional investor contributed debt

EBDB

19

NA-1 NA0 NA1

IC-1 IC0 IC1

i=-1 i=0 i=1

DIV0 = NP0 (1-b) DIV∙ 1= NP0 (1-b) (1+g)∙ ∙

DRE0 = NP0 b∙ DRE1=NP0 b (1+g)∙ ∙

Critical growth rate derivations for core business operationsSo use • NA not TA and• IC not C or LE• NAIC• roa is return on net book assets• roe is return on book equity

Critical Growth Rates20

DNA = D IC = IC1 – IC0

= DDB + D EB

= DDB + DAPC + DPAR + DRE

DNA = g NA∙ 0

DNA = DRE DDB

= NP0 b (1+g) + ∙ ∙ DDB

NA-1 NA0 NA1

i=-1 i=0 i=1

DRE0 = NP0 b∙ DRE=NP0 b (1+g)∙ ∙

DNA = DRE + DDB

Internal Growth Rate, gint 21

bNP)g1(RE

0DB

DBRENAgNA

int

int

D

D

DDD

b·NP )g(1 NA g intint

b·NP b·NP) (NA g

b·NP b·NP g - NA g

int

intint

)roab1(roab

g

roab )roab - (1 g

NANP

roa

int

int

NA-1 NA0 NA1

i=-1 i=0 i=1

DRE0 = NP0 b∙ DRE1=NP0 b (1+g)∙ ∙

DNA1 = DRE1 + DDB1

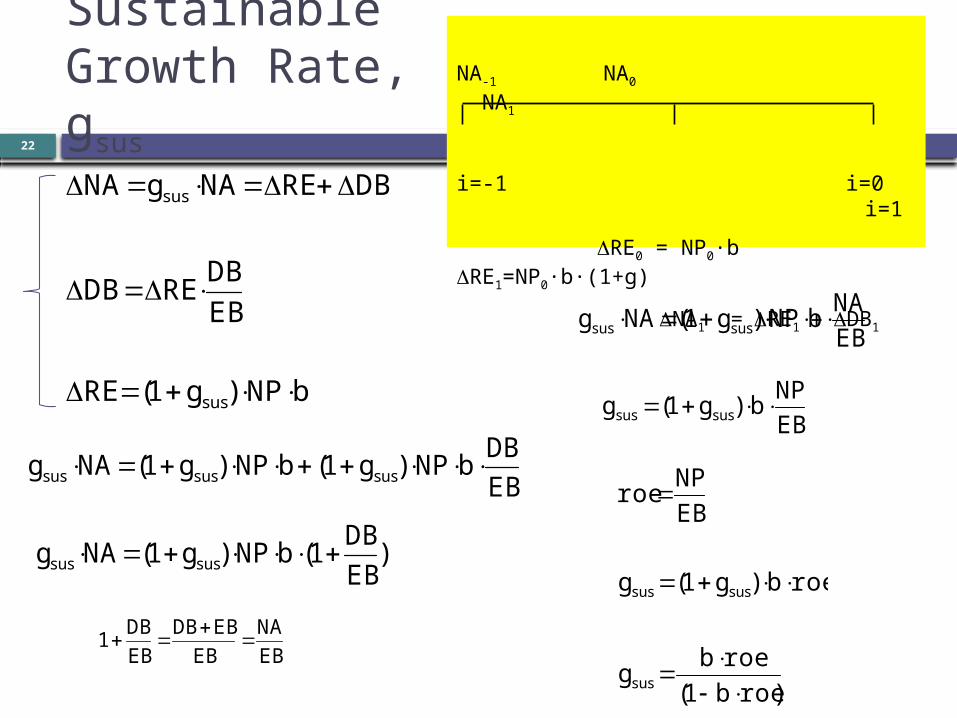

Sustainable Growth Rate, gsus

22

EBDB

bNP)g1(bNP)g1(NAg sussussus

)EBDB

1(bNP)g1(NAg sussus

EBNA

EBEBDB

EBDB

1

EBNA

bNP)g1(NAg sussus

EBNP

b)g1(g sussus

)roeb1(roeb

g

roeb)g1(g

EBNP

roe

sus

sussus

NA-1 NA0 NA1

i=-1 i=0 i=1

DRE0 = NP0 b∙ DRE1=NP0 b (1+g)∙ ∙

DNA1 = DRE1 + DDB1

bNP)g1(RE

EBDB

REDB

DBRENAgNA

sus

sus

D

DD

DDD

Related Documents