Equity Instruments And Portfolio Construction Prof. Ian Giddy New York University New York University/ING Barings

Equity Instruments And Portfolio Construction Prof. Ian Giddy New York University New York University/ING Barings.

Dec 21, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Equity InstrumentsAnd

Portfolio Construction

Prof. Ian GiddyNew York University

New York University/ING Barings

Copyright ©1998 Ian H. Giddy Equity instruments 2

Equity Instruments

Equity in financing Rights Warrants Convertibles

Copyright ©1998 Ian H. Giddy Equity instruments 3

Equity

What it is How it’s issued

Copyright ©1998 Ian H. Giddy Equity instruments 4

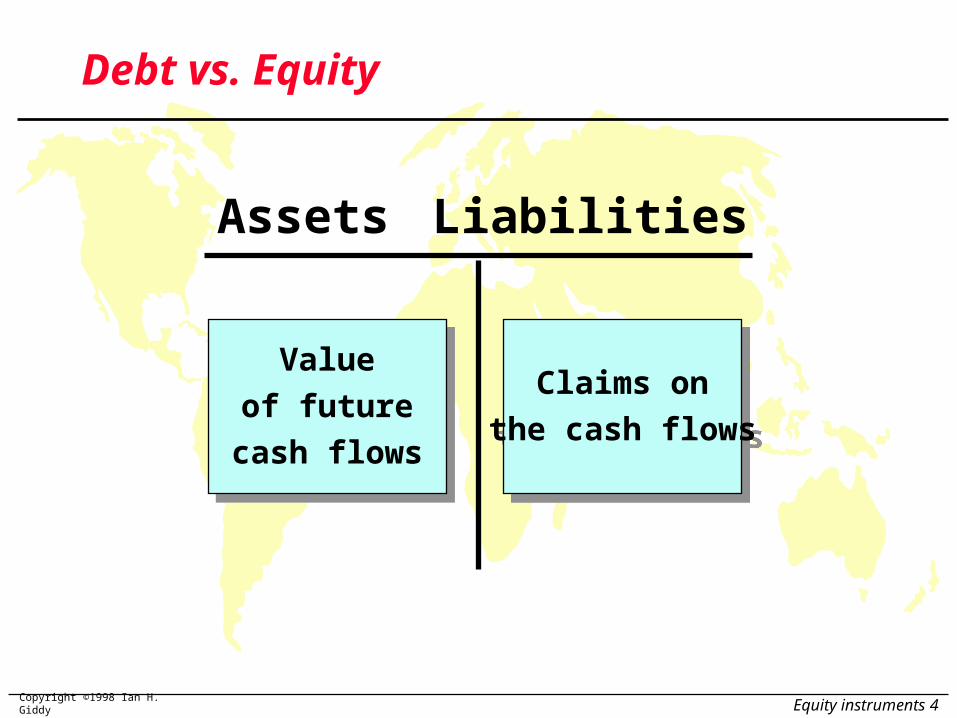

Debt vs. Equity

Value

of future

cash flows

Value

of future

cash flows

Claims on

the cash flows

Claims on

the cash flows

Assets Liabilities

Copyright ©1998 Ian H. Giddy Equity instruments 5

Debt vs Equity

Value

of future

cash flows

Value

of future

cash flows

Contractual int. & principal

No upside

Senior claims

Control via restrictions

Contractual int. & principal

No upside

Senior claims

Control via restrictions

Assets Liabilities

Debt

Residual payments

Upside and downside

Residual claims

Voting control rights

Residual payments

Upside and downside

Residual claims

Voting control rights

Equity

Copyright ©1998 Ian H. Giddy Equity instruments 6

Methods of Issuing New Securities

Method Type Definition

Public Offerings Negotiated Cash Offer Firm Commitment Company negotiates agreement

Cash Offer with investment banker to underwrite and distribute the new stocks.

Best Efforts Cash Offer Investment bankers sell as much as possible at the agreed-upon price. No guarantee as to how much cash will be raised.

Privileged Subscription Direct Rights Offer Company offers new stock directly to existing stockholders.

Standby Rights Offer Similar to direct rights offer, but net proceeds are guaranteed by the underwriters.

Copyright ©1998 Ian H. Giddy Equity instruments 7

Methods of Issuing New Securities (concluded)

Method Type Definition

Public Offerings Nontraditional Cash Offer Shelf Cash Offer Qualifying companies can

authorize all shares they expect to sell over a two year period and

sell them when needed.

Competitive Firm Company can elect to award Cash offer underwriting contract through a

public auction instead of negotiation.

Private Offerings Private Direct Placement Securities are sold directly to

purchaser, who, at least until very recently, generally could not resell securities for at least two years.

Copyright ©1998 Ian H. Giddy Equity instruments 8

Equity Issuance: A Red Herring

Subject to Completion, Dated December 19, 1989

25,000,000 Shares

The Reader’s Digest Association, Inc.Class A Nonvoting Common Stock

(par value $0.01 per share)

Of the 25,000,000 shares of Class A Nonvoting Common Stock offered, 21,000,000 are being offered hereby in the United Sates and 4,000,000 are being offered in a concurrent international offering outside the United States. The initial public offering price and the aggregate underwriting discount per share will be identical for both Offerings. The closing of the U.S. Offering is a condition to the closing of the International Offering, but the closing of the International Offering is not a condition to the closing of the U.S. Offering. See “Underwriting”.

All of the shares of Class A Nonvoting Common Stock offered are being sold by the Selling Stockholders. See “Selling Stockholders”. The Company will not receive any of the proceeds from the sale of shares by the Selling Stockholders. (continued)

Copyright ©1998 Ian H. Giddy Equity instruments 9

A Red Herring (continued)

Prior to the Offerings, there has been no public market for shares of Class A Nonvoting Common Stock. It is currently anticipated that the initial public offering price will be in the range of $18 to $22 per share. For the factors to be considered in determining the public offering price, see “Underwriting”.

Application will be made to list the shares of Class A Nonvoting Common Stock on the New York Stock Exchange.

These securities have not been approved or disapproved by the securities and exchange commission nor has the commission passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal

offense.

(continued)

Copyright ©1998 Ian H. Giddy Equity instruments 10

A Red Herring (continued)

Initial Public Underwriting Proceeds to SellingOffering Price Discount (1) Stockholders (2)

Per Share............ $ $ $Total (3)............... $ $ $

(1) The Company and the Selling Stockholders have agreed to indemnify the Underwriters against certain liabilities, including liabilities under the Securities Act of 1933.

(2) Before deducting expenses, estimated to be $ , of which $ will be payable by the Company and $ will be payable by

the Selling Stockholders.

(3) The Selling Stockholders have granted the U.S. Underwriters an option for 30 days to purchase up to an additional 3,150,000 shares at the initial public offering price per share, less the underwriting discount, solely to cover over-allotments. Additionally, the Selling Stockholders have granted an over-allotment option with respect to an additional 600,000 shares as part of the International Offering. If such options are exercised in full, the total initial public offering price, underwriting discount and proceeds to Selling Stockholders will be $ and $ , respectively.

See “Underwriting”. (continued)

Copyright ©1998 Ian H. Giddy Equity instruments 11

A Red Herring (concluded)

The shares offered hereby are offered severally by the U.S. Underwriters, as specified herein, subject to receipt and acceptance by them and subject to their right to reject any order in whole or in part. It is expected that the certificates for the Shares will be ready for delivery at the offices of Goldman, Sachs & Co., New York, New York on or about , 1990.

Goldman, Sachs & Co. Lazard Freres & Co.The date of this Prospectus is ,1990.

Information contained herein is subject to completion or amendment. A registration statement relating to these securities has been filed with the Securities and Exchange Commission. These securities may not be sold nor may offers to buy be accepted prior to the time the registration statement becomes effective. This prospectus shall not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of these securities in any State in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such State.

`

Copyright ©1998 Ian H. Giddy Equity instruments 12

Tombstone Ad of an Equity Offering

58,750 Shares

Consolidated Rail CorporationCommon Stock(par value $1.00 per share)

__________

Price $28 Per Share

__________The shares are being sold by the United States Government pursuant to the Conrail Privatization

Act. The Company will not receive any proceeds from the sale of the shares.

Upon request a copy of the Prospectus describing these securities and the business of the Company may be obtained within any State from any Underwriter who may legally distribute it within such State. The securities are offered only by means of the Prospectus, and this announcement is neither an offer to sell nor a solicitation of any offer to buy.

52,000,000 SharesThe portion of the offering is being offered in the United States and Canada by the undersigned.

(continued)

Copyright ©1998 Ian H. Giddy Equity instruments 13

Tombstone Ad (continued)

Goldman, Sachs & Co. The First Boston Corporation

Merrill Lynch Capital Markets Morgan Stanley & Co.

Salomon Brothers, Inc. Shearson Lehman Brothers, Inc.

Alex Brown & Sons Dillon, Read &Co. Inc. Donaldson, Lufkin & Jenrette Drexel Burnham Lambert Hambrecht & Quist E.F. Hutton & Co. Inc.Incorporated Securities Corporation Incorporated Incorporated

Kidder, Peabody & Co. Lazard Freres & Co. Montgomery Securities Prudential-Bache Capital Funding Rbertson, Colman & StephensIncorporated

L.F. Rothschild, Unterberg, Towbin, Inc. Smith Barney, Harris Upham & Co. Wertheim Schroeder & Co. Dean Witter Reynolds Inc. Incorporated Incorporated

William Blair & Company J.C. Bradford & Co. Dain Bosworth A.G. Edwards & Sons, Inc. McDonald & Company Oppenheimer & Co., Inc. Incorporated Incorporated Incorporated

Piper, Jaffray & Hopwood Prescott, Ball & Turben, Inc. Thomson McKinnon Securities Inc. Wheat, First Securities, Inc. Incorporated

Advest, Inc. American Securities Corporation Arnhold and S.Bleichroeder, Inc. Robert W. Baird & Co. Bateman, Eichler, Hill Richard's Incorporated Incorporated

Sangfroid C. Bernstein & Co Inc Blunt Ellis & Loewl Boettcher & Co Inc Burns Fry and Timmins Inc Butcher & Singer Inc Cowen & Company Incorporated

Dominion Securities Corporation Eberstadt Fleming Inc Eppler, Guerin & Turner Inc First of Michigan Corp. First Southwest Company

Furman Selz Mager Dietz & Birney Gruntal & Co Inc Howard, Well, Laboulsse, Friedrichs Interstate Securities Corporation Incorporated Incorporated

Janney Montgomery Scott Inc Johnson, Lane Smith & Co Inc. Johnston, Lemon & Co. Josephthal & Co. Ladenburg, Thalmann & Co Inc. Incorporated Incorporated

Cyrus J. Lawrence Legg Mason Wood Walker Morgan Keegan & company Inc Moseley Securities Corporation Needham & Company Inc. Incorporated Incorporated

Neuberger & Berman The Ohio Company Rauscher Pierce Refanes Inc The Robinson-Humphrey Co Inc Rothschild Inc Stephens Inc

Stifel, Nicolaus & Company Sutro & Co. Tucker, Anthony & R. L. Day, Inc. Underwood, Neuhaus & Co. Wood Grudy Corp. Incorporated Incorporated Incorporated

(continued)

Copyright ©1998 Ian H. Giddy Equity instruments 14

This special bracket of minority-owned and controlled firms assisted the Co-LeadManagers in the United States Offering pursuant to the Conrail Privatization Act:

AIBC Investment Services Corporation Daniels & Bell, Inc. Dolsey Securities, Inc.

WR Lazard Securities Pryor, Govan Counts & Co. Inc. Muriel Siebbert & Co., Inc.

6,750,000 SharesThis portion of the offering is being offered outside the United States and Canada by the undersigned

Goldman Sachs International Corp. First Boston International Limited

Merrill Lynch Capital Markets Morgan Stanley International

Salomon Brothers International Limited Shearson Lehman Brothers International

Algemene Bank Nederland N.V. Banque Bruxelles Lambert S.A. Banque Nationale de Paris Cazenove & Co. The Nikko Securities Co. (Europe) Ltd.

Nomura International N.M.. Rothschild & Sons J. Henry Schroder Wagg & Co. Societe Generale S. G. Warburg Securities Limited Limited Limited

ABC International Ltd. Banque Paribas Capital Markets Limited Calsse Nationale de Credit Agricole Compagnie de Banque et d’investissements, CBI

Credit Lyonnais Daiwa Europe IMI Capital Markets (UK) Ltd. Joh. Berenberg, Gossier & Co. Leu Securities Limited Limited

Morgan Greenfell & Co. Peterbroeck, van Campenhout & Cie SCS Swiss Volksbank Vereins-und Westbank Aldengrundschaft

J. Vontobel & Co. Ltd. M. M. Warburg-Brinckmann, Wirtz & Co. Westdeutsche Landesbank Yamaichi International (Europe) Limited

March 27, 1967

A Tombstone Ad (concluded)

Copyright ©1998 Ian H. Giddy Equity instruments 15

Rights Offerings

Rights offering Share rights Offering terms Subscription price Number of rights to purchase

a share Value of a right

Copyright ©1998 Ian H. Giddy Equity instruments 16

Ex Rights Stock Prices

Rights On Ex Rights

Announcement

date date dateEx-rights Record

September 30 October 13 October 15

Rights-on price $20.00

Ex-rights price $16.67

$3.33 =Value of a right

Copyright ©1998 Ian H. Giddy Equity instruments 17

The Value of a Right

The value of a right equals the difference in the price of the issuer’s outstanding shares before and after the rights offering, and is determined by three factors:

- the total amount of money to be raised,

- the subscription price of the new shares, and

- the number of existing shares.

The number of new shares to be issued equals

(Funds to be raised)/Subscription price

Copyright ©1998 Ian H. Giddy Equity instruments 18

The Value of a Right (concluded)

The number of rights needed to buy one share equals

(Number of old shares)/(Number of new shares)

After the offering, the new value of the firm is

Pre-offering firm value + funds raised,

and the new share price must be

(New firm value)/(Total number of shares outstanding).

The value of the right must equal

Old share price - new share price.

Copyright ©1998 Ian H. Giddy Equity instruments 19

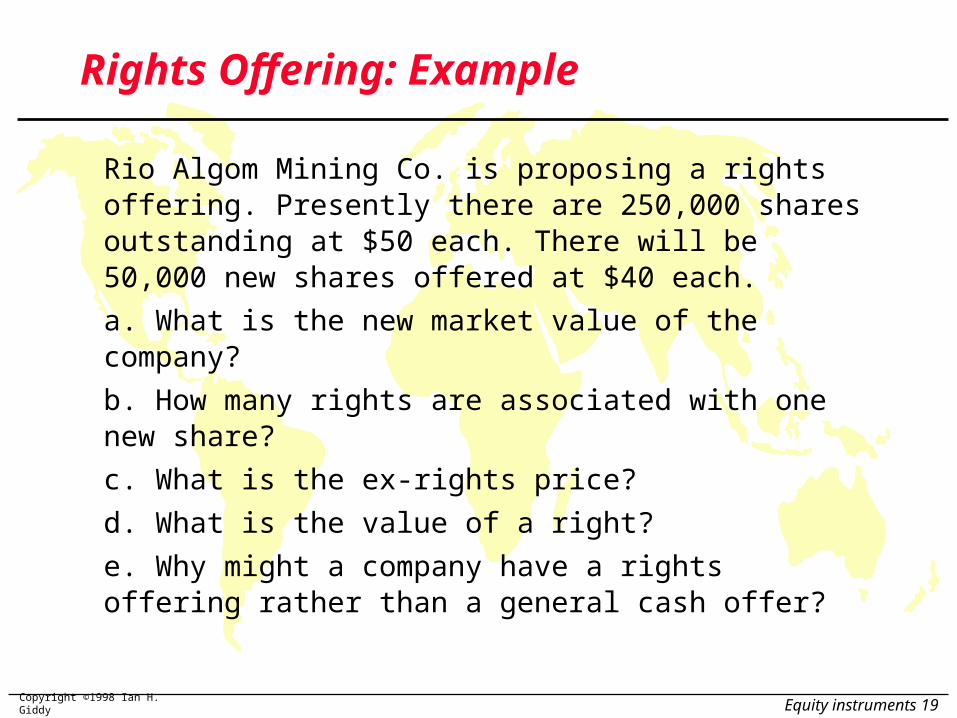

Rights Offering: Example

Rio Algom Mining Co. is proposing a rights offering. Presently there are 250,000 shares outstanding at $50 each. There will be 50,000 new shares offered at $40 each.

a. What is the new market value of the company?

b. How many rights are associated with one new share?

c. What is the ex-rights price?

d. What is the value of a right?

e. Why might a company have a rights offering rather than a general cash offer?

Copyright ©1998 Ian H. Giddy Equity instruments 20

Rights Offering: Example (cont.)

a. New value = (250,000 $50) + (50,000 $40)$14.5 million

b. There will be (250,000/ _______ ) = ____ rights associated with each new share.

c. The ex-rights price is $14.5 million/300,000 = $48.33.

d. The value of one right equals $____48.33 = $1.67.

Copyright ©1998 Ian H. Giddy Equity instruments 21

What is the Effect of an Equity Offering on Shareholder Value?

Dilution - loss in existing shareholders’ value

Dilution of proportionate ownership Dilution of market value Dilution of book value and earnings

per share (EPS) Under what circumstances does

market value dilution occur?

Copyright ©1998 Ian H. Giddy Equity instruments 22

Debt vs Equity

Value

of future

cash flows

Value

of future

cash flows

Contractual int. & principal

No upside

Senior claims

Control via restrictions

Contractual int. & principal

No upside

Senior claims

Control via restrictions

Assets Liabilities

Debt

Residual payments

Upside and downside

Residual claims

Voting control rights

Residual payments

Upside and downside

Residual claims

Voting control rights

Equity

What if...

Claims

are inadequate?

Returns

are inadequate?

Copyright ©1998 Ian H. Giddy Equity instruments 23

When Debt and Equity are Not Enough

Value

of future

cash flows

Value

of future

cash flows

Contractual int. & principal

No upside

Senior claims

Control via restrictions

Contractual int. & principal

No upside

Senior claims

Control via restrictions

Assets Liabilities

Debt

Residual payments

Upside and downside

Residual claims

Voting control rights

Residual payments

Upside and downside

Residual claims

Voting control rights

Equity

Alternatives

Collateralized Asset-securitized Project financing

Preferred Warrants Convertible

Copyright ©1998 Ian H. Giddy Equity instruments 24

Equity-Linked Bonds

Bonds with warrants Convertible Bonds Index-linked Bonds

These are all example of hybrid bonds and should be priced by decomposition

Copyright ©1998 Ian H. Giddy Equity instruments 25

Stock-Purchase Warrants

Warrants are usually detachable and trade on the securities exchanges

Warrants are often added to a large debt issue as “sweeteners” to enhance the marketability of the issue

Exercise price Warrants usually have a limited life of about 10

years or less Warrants differ from rights and convertibles

Copyright ©1998 Ian H. Giddy Equity instruments 26

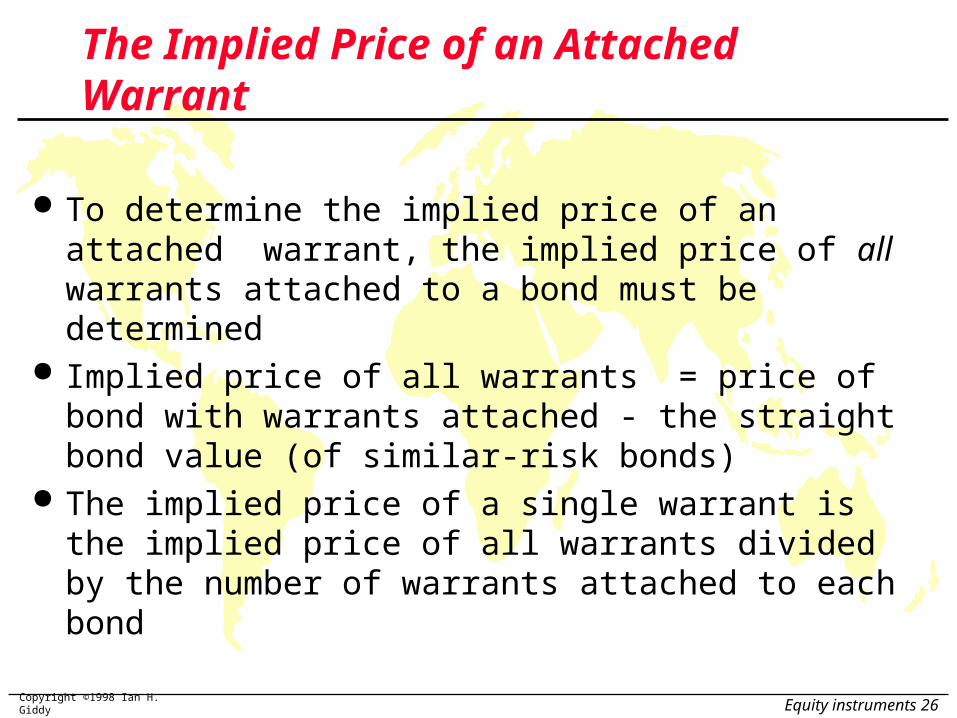

The Implied Price of an Attached Warrant

To determine the implied price of an attached warrant, the implied price of all warrants attached to a bond must be determined

Implied price of all warrants = price of bond with warrants attached - the straight bond value (of similar-risk bonds)

The implied price of a single warrant is the implied price of all warrants divided by the number of warrants attached to each bond

Copyright ©1998 Ian H. Giddy Equity instruments 27

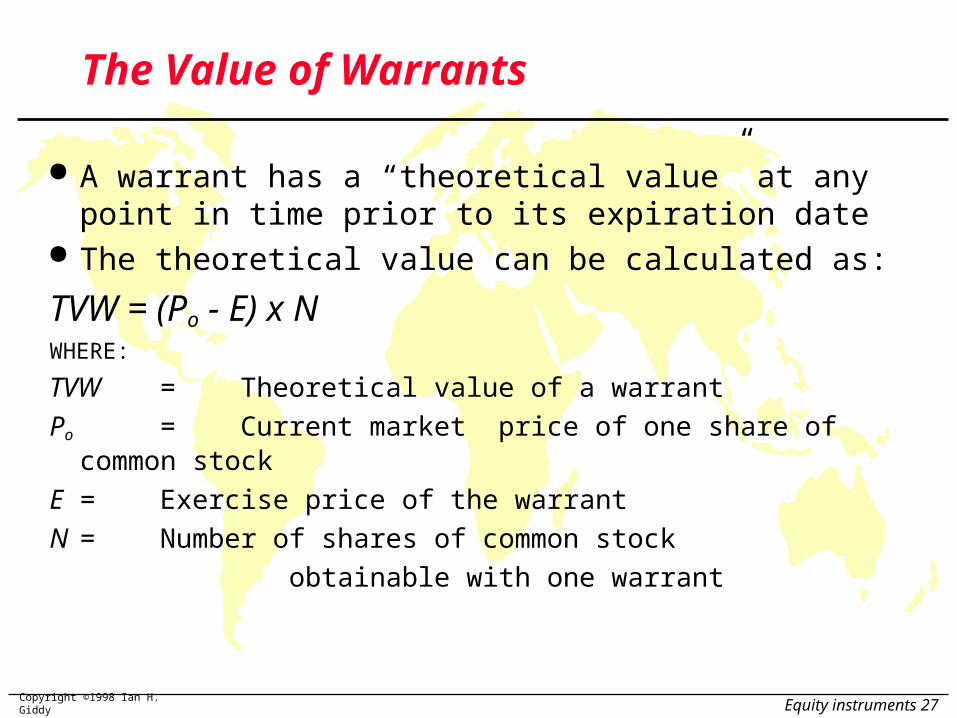

The Value of Warrants

A warrant has a “theoretical value” at any point in time prior to its expiration date

The theoretical value can be calculated as:

TVW = (Po - E) x NWHERE:

TVW = Theoretical value of a warrant

Po = Current market price of one share of common stock

E = Exercise price of the warrant

N = Number of shares of common stock

obtainable with one warrant

Copyright ©1998 Ian H. Giddy Equity instruments 28

Sony Warrants

Sony Electronics has outstanding warrants exercisable at Yen400/share that entitle holders to purchase three shares of common stock per warrant. If Sony’s common stock is currently selling for Y45/share, the TVW =

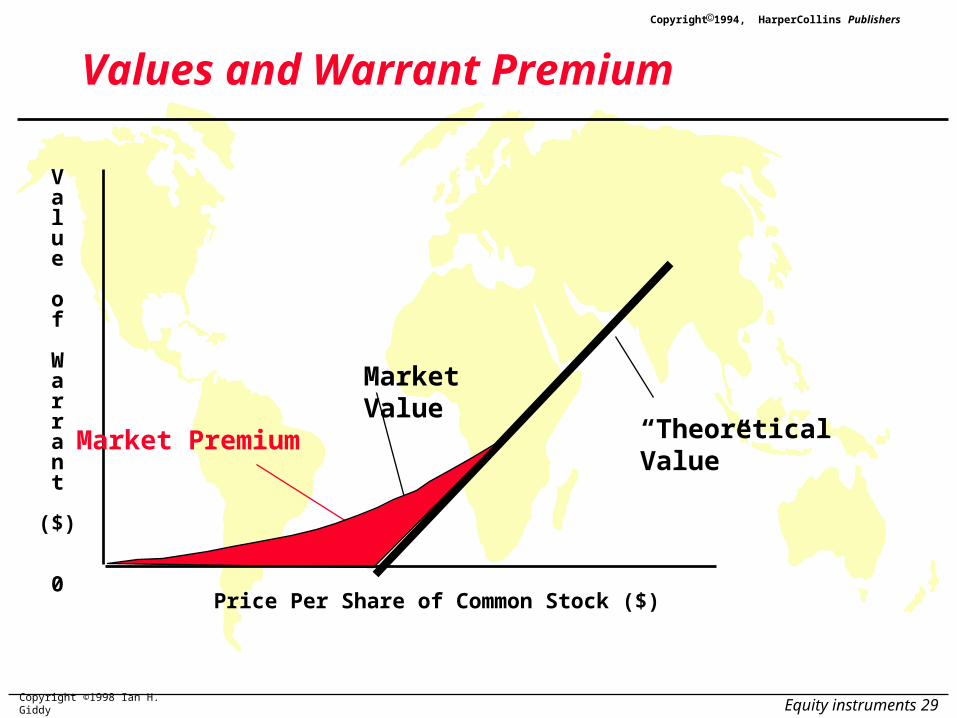

TVW = (Y45 - Y40) x 3 = Y15The market value of a warrant is generally greater than

its theoretical value; the difference, known as the warrant premium is due to investor expectations and opportunities for further gain before expiration.

Copyright ©1998 Ian H. Giddy Equity instruments 29

Values and Warrant Premium

“TheoreticalValue”

Market ValueMarket Premium

Value

of

Warrant

($)

0Price Per Share of Common Stock ($)

1994, HarperCollins PublishersCopyright

Copyright ©1998 Ian H. Giddy Equity instruments 30

Convertible Bonds

Bond may be converted into stock The Conversion Ratio is the number of

shares of common stock that can be received in exchange for each convertible security

The Conversion Price is the per share common stock price at which the exchange effectively takes place

Copyright ©1998 Ian H. Giddy Equity instruments 31

Convertibles

The Conversion Period is a limited time within which a security may be exchanged for common stock

The Conversion Value is the market value of the security based upon the conversion ratio times the current market price of the firm's common stock

Earnings effects: Firms must report Primary EPS, treating all contingent

securities that derive their value from their conversion privileges or common stock characteristics as common stock

Firms must report Fully Diluted EPS treating all contingent securities as common stock

Copyright ©1998 Ian H. Giddy Equity instruments 32

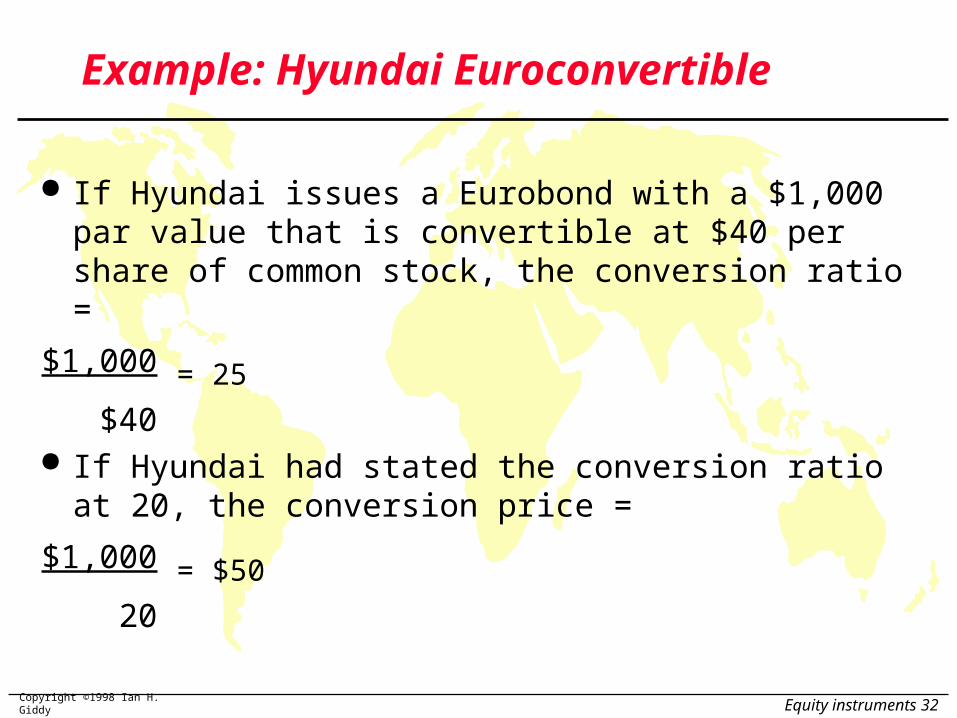

Example: Hyundai Euroconvertible

If Hyundai issues a Eurobond with a $1,000 par value that is convertible at $40 per share of common stock, the conversion ratio =

$1,000 = 25

$40 If Hyundai had stated the conversion ratio at 20, the

conversion price =

$1,000 = $50

20

Copyright ©1998 Ian H. Giddy Equity instruments 33

Financing With Convertibles

Motives for using convertibles include: It is a deferred sale of common stock that decreases the

dilution of both ownership and earnings They can be used as a “sweetener” for financing They can be sold at a lower interest rate than nonconvertibles They have far fewer restrictive covenants than

nonconvertibles It provides a temporarily cheap source of funds (assuming

bonds) for financing projects Most convertibles have a call feature that enables the issuer to

force conversion when the price of the common stock rises above the conversion price

Copyright ©1998 Ian H. Giddy Equity instruments 34

Determining the Value of a Convertible Bond

There are three values associated with a convertible bond:Straight Bond Value is the price at which the bond

would sell in the market without the conversion featureThe Conversion Value is the product of the current

market price of stock times the conversion ratio of the bond

The Market Value is the straight or conversion value plus a market premium based upon future (expected) stock price movements that will enhance the value of the conversion feature

Copyright ©1998 Ian H. Giddy Equity instruments 35

Siam Cement

Siam Cement sold a $1,000 par value, 20-year convertible bond with a 12% coupon. A straight bond would have been sold with a 14% coupon. The conversion ratio is 20

Straight Bond Value$120 x (PVIFA14%,20) + $1,000 x (PVIF14%,20) =$120 x (6.623) + $1,000 x (.073) = $867.76

Conversion Value at various market prices of stock

Stock Price Conversion Value $30 $ 600 40 800 50 (Conversion Price) 1,000 (Par Value) 60 1,200

70 1,400 80 1,600

The straight bond value is the minimum price at which the convertible bond would be traded

Copyright ©1998 Ian H. Giddy Equity instruments 36

Values and Market Premium

StraightBond Value

Market Premium

Value

of

Convertible

Bond

($) 0

Price Per Share of Common Stock

Conversion Value

Copyright ©1998 Ian H. Giddy Equity instruments 37

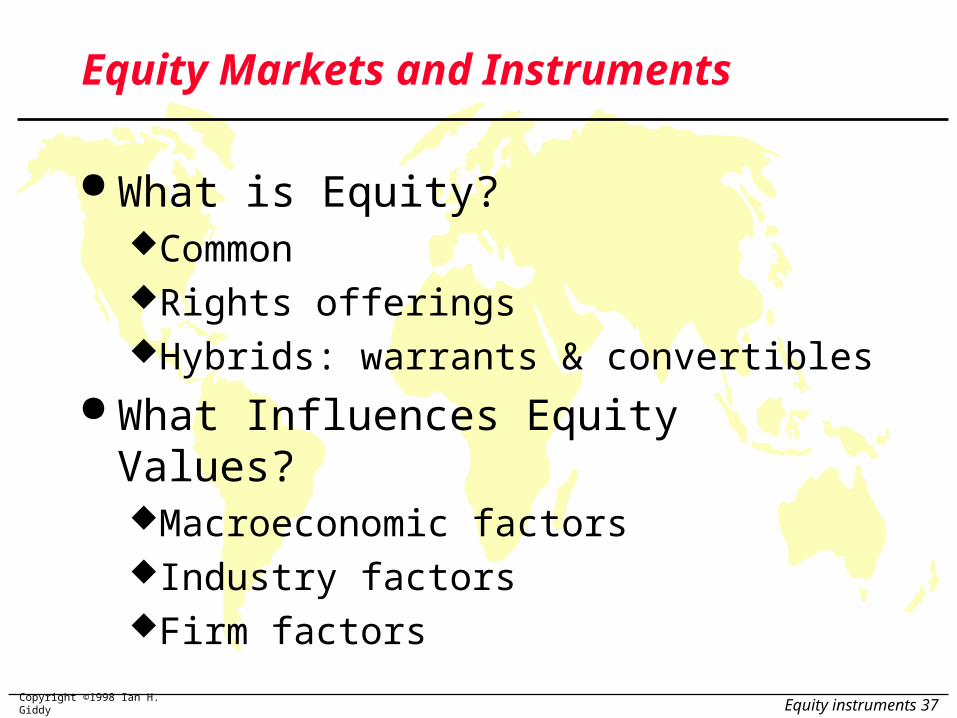

Equity Markets and Instruments

What is Equity?CommonRights offeringsHybrids: warrants & convertibles

What Influences Equity Values?Macroeconomic factorsIndustry factorsFirm factors

Copyright ©1998 Ian H. Giddy Equity instruments 38

Fundamental Analysis Approach to Fundamental Analysis

Domestic and global economic analysisIndustry analysisCompany analysis

Why use the top-down approach?

Framework of Analysis

Portfolio Diversificationand the

Capital Asset Pricing Model

Prof. Ian GiddyNew York University

New York University/ING Barings

Copyright ©1998 Ian H. Giddy Equity instruments 40

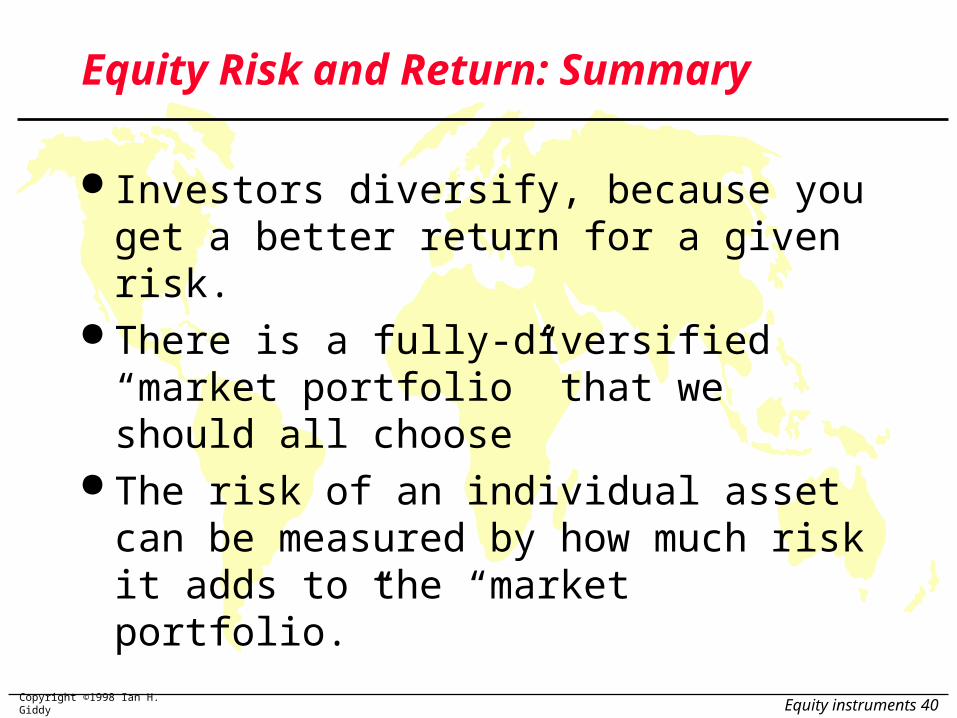

Equity Risk and Return: Summary

Investors diversify, because you get a better return for a given risk.

There is a fully-diversified “market portfolio” that we should all choose

The risk of an individual asset can be measured by how much risk it adds to the “market portfolio.”

Copyright ©1998 Ian H. Giddy Equity instruments 41

Capital Allocation Possibilities:Treasuries or an Equity Fund?

rf=7%

E(rP)

=17%

P=27%

10%

P

Expected Return

Risk

7%

THE EQUITY FUND

Copyright ©1998 Ian H. Giddy Equity instruments 42

We Can Buy Some T-bills and Some of the Risky Fund...

C.A.L.

SLOPE=0.37

E(R)

SD

17%

14%

18.9% 27%

ONE PORTFOLIO:

30% Bills, 70% Fund

E(R)=.3X7+.7X17=14%

SD=.7X27=18.9%

rf=7%

Copyright ©1998 Ian H. Giddy Equity instruments 43

...Or Buy Two Risky Assets

A

E(r)

B

Copyright ©1998 Ian H. Giddy Equity instruments 44

Diversification

Asset F Asset G Portfolio of Assets F and

GReturn

Time

Return

Time

Return

Time

kkk

Copyright ©1998 Ian H. Giddy Equity instruments 45

Portfolio Return...

To compute the return of a portfolio: use the weighted average of the returns of all assets in the portfolio, with the weight given each asset calculated as

(value of asset)/(value of portfolio).

The portfolio return E(Rp) is:

E(Rp) = (w1k1)+(w2k2)+ ... (wnkn) = wj kj

where wj = weight of asset j, kj = return on asset j

Copyright ©1998 Ian H. Giddy Equity instruments 46

...and Risk (Standard Deviation)

Portfolio return is the weighted average of all assets’ returns,

But portfolio standard deviation is normally less than the weighted average of all assets’ standard deviations!

The reason: asset returns are imperfectly correlated.

Copyright ©1998 Ian H. Giddy Equity instruments 48

Risk and Return of Stocks, Bonds and a Diversified Portfolio

Rate of Return

State Prob. Equity Bond Portfolio

Recession 1/3 -7% +17% +5%

Normal 1/3 +12% +7% +9.5%Boom 1/3 +28% -3% +12.5%

Expected Return 11% 7.0% 9.0%Variance 204.7% 66.7% 9.5%Standard Deviation 14.3% 8.2% 3.1%

Copyright ©1998 Ian H. Giddy Equity instruments 49

The Correlation Between Stock and Bond Returns Covariance

= 0.3333(-7-11)(17-7) + 0.3333(12-11)(7-7) +0.3333(28-11)(-3-7)

= -116.67 Correlation

= -116.66 / 14.3(8.2) = -0.99

p R E R R E Rss

n

s e e s b b1

, ,( ) ( )

cov ,e b

e b

Copyright ©1998 Ian H. Giddy Equity instruments 50

Portfolio Return and Standard DeviationGiven:

WS = 0.5 RS = 12% S = 25%

WB = 0.5 RB = 9% B = 12%

and S,B = 0.2

Rp = 0.5(12)+0.5(9) = 10.5%

P = [(0.5)2(25) 2+(0.5) 2(12) 2+2(0.5)(0.5)(25)(12)(0.2)]1/2

= (156.25+36+30)1/2

= (222.25) 1/2

= 14.91%

Copyright ©1998 Ian H. Giddy Equity instruments 51

The Minimum-Variance Frontier of Risky Assets

Efficient frontier

Individual assets

Global minimum-variance portfolio

E(r)

Copyright ©1998 Ian H. Giddy Equity instruments 52

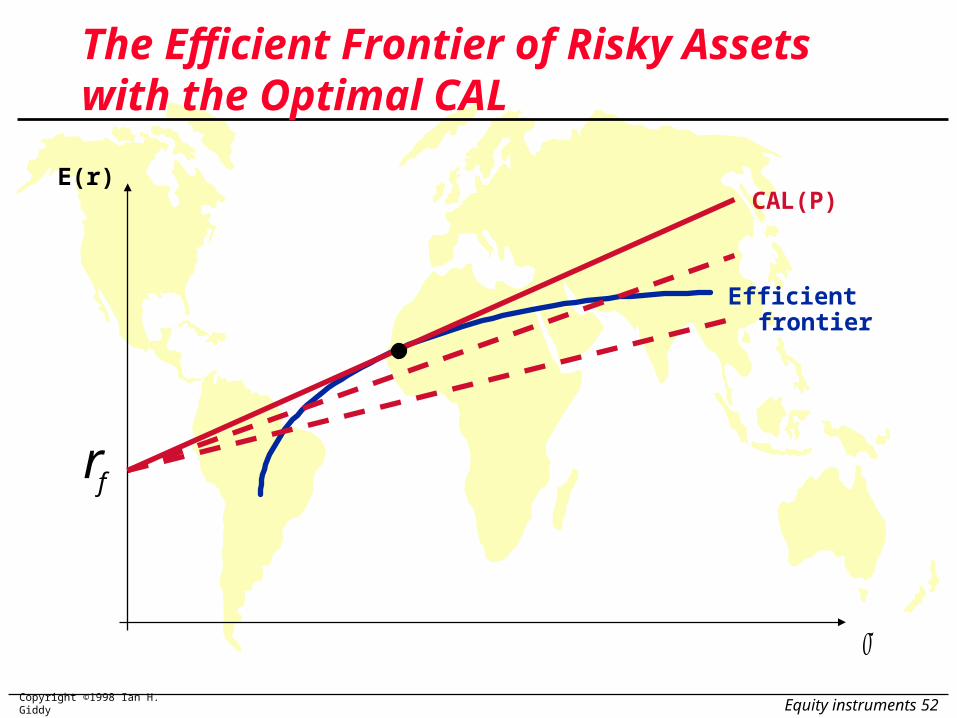

The Efficient Frontier of Risky Assets with the Optimal CAL

Efficient frontier

CAL(P)E(r)

rf

Copyright ©1998 Ian H. Giddy Equity instruments 53

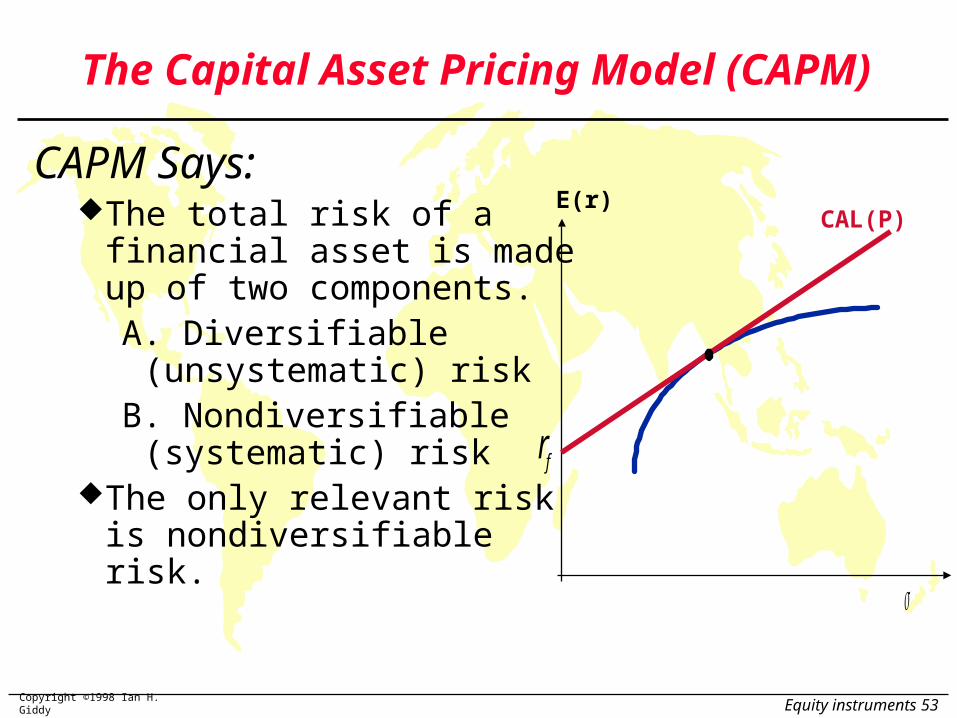

The Capital Asset Pricing Model (CAPM)

CAPM Says:The total risk of a financial

asset is made up of two components.A. Diversifiable

(unsystematic) riskB. Nondiversifiable

(systematic) risk The only relevant risk is

nondiversifiable risk.

CAL(P)E(r)

rf

Copyright ©1998 Ian H. Giddy Equity instruments 54

The Equation for the CAPM

Rj = RF + j (Rm - RF)where:Rj = Required return on asset j;

RF = Risk-free rate of return

j = Beta Coefficient for asset j;

Rm = Market return

The term [j(Rm - RF)] is called the risk premium and (Rm-RF) is called the market risk premium

Copyright ©1998 Ian H. Giddy Equity instruments 58

www.giddy.org

Ian Giddy

NYU Stern School of Business

Tel 212-998-0332; Fax 212-995-4233

http://www.giddy.org

Related Documents