Asiamoney’s 2013 Best Domestic Equity House Economics flash 24 August 2015 Disclosure: Bahana Securities does and seeks to do business with companies covered in its research reports. Investors should consider this report as only a single factor in making their investment decision. Please see the important disclaimer information on the back of this report 2014 Finance Asia's Best Equity House Alpha Southeast Asia 2014 Best Research Call FMCG Sector Asiamoney's 2013 Best Domestic Equity House 2015 Institutional Investors Highest Ranked Local Research House 2015 Global Banking & Finance Review Best Research House Indonesia economic outlook Fakhrul Fulvian Adi Saputra E-mail: [email protected] Email: [email protected] Phone: +6221 2505081 ext. 3602 Phone: +6221 2505081 ext. 3693 Tough times ahead Moderate domestic demand and investment to continue: Private consumption growth of below 5% y-y in 2Q15 and declining imports in July (- 28% y-y) affirm our view of continued weak domestic demand and investment and leads us to make changes to our macro indicators (exhibit 2). The tight monetary policy of the past two years should continue to result in economic moderation through 1Q16. Region-wise, we expect the commodity economy outside of Java to persist with lower growth amid soft commodity prices. At this point, room for a BI rate cut to spur growth still appears limited, as the Indonesia-US real interest rate gap remains small (exhibit 10). Historically, a recovery has often followed a negative output gap by 3-4 quarters (exhibit 5). 2016 state budget draft seems overly optimistic: Last week, the government announced its 2016 state budget plan, which included IDR1,848tn of government revenue (+5% y-y). The target looks high, as assuming a IDR250tn shortfall in 2015, we estimate that tax revenue would have to jump 26.4% y-y in 2016 to achieve the target (exhibit 15). A higher regional transfer portion is an interesting part of the new budget, leading to greater unpredictability in terms of execution risk. Global slowdown, a blessing and a curse: The IMF already cut its 2015 GDP growth forecast for emerging economies to 4.2% from 4.6% in 2014 on lower commodity prices (exhibit 6) and tightening global financial conditions. For Indonesia, lower oil prices are already having a positive net effect on the external trade balance, as the CAD-to-GDP ratio was only 2.1% in 2Q15 (2014: 3.1%). We estimate that every 10% drop in the oil price would increase the monthly trade balance by USD78m. That said, even though the 2Q15 trade balance was a net positive, continued steep export drops (2Q15: -19.2% y-y) and an ongoing lower Indonesian shares in global markets are restraining the country’s ability to generate foreign reserves to finance external debt. Stable inflation the key to avoid a vicious circle: Indonesia currently is the only country with above 5% y-y inflation among its peers (exhibit 20), caused by several fuel-price hikes since 2013. In terms of purchasing power parity (PPP), this is why the IDR has depreciated the most among these countries. Technically, without another supply shock, we believe inflation should be below 5.0% at end-2015, but we see possible upside from the recent El Nino weather pattern and possible additional fuel-price hikes due in September/October. In our view, a managable inflation level is imperative to prevent a vicious circle of currency depreciation and high inflation. Fair and manageable moderation is expected this time: The recent IDR depreciation has raised concerns about foreign debt payments and the sufficiency of foreign reserves, which now cover just 6.9 months of imports. We remain cautious on this issue, although 2Q15 private external debt growth has slowed but to a still high level of 9.7% y-y (1Q15: 13.4%). However, BI's tightening policy, in place since 2013, has normalized the Exhibit 1. Macro assumptions 2014A 2015F 2016F 2017F Cur acc (% GDP) -3.0 -2.0 -2.3 -2.3 Fiscal bal (% GDP) -2.3 -2.2 -2.2 -2.3 GDP growth(% y-y) 5.0 4.7 5.1 5.2 Inflation (% y-y) 8.4 4.8 5.2 5.3 Oil price(USD/bbl) 57.3 55.0 57.0 63.0 Oil price(USD/bbl)* 99.5 58.0 55.0 60.0 IDR/1USD 12,385 14,000 14,500 14,000 BI rate (% p.a.) 7.75 7.50 7.00 6.50 FX reserve (USDbn) 111.9 105.0 110.0 112.0 Source: BI, BPS, Bahana estimate, *Average Brent oil price Exhibit 2. Forecast changes 2015F 2016F Old New Old New GDP growth (%) 4.86 4.72 5.29 5.10 CAD (% of GDP) 2.50 2.00 2.30 2.30 IDR/USD, Average 13,350 13,455 14,200 14,533 IDR/USD, End-year 13,700 14,000 14,000 14,500 Source: Bahana estimate Exhibit 3. GDP growth trend 6.1 6.8 6.2 6.5 6.5 6.3 6.0 5.9 6.1 6.2 5.9 5.9 5.6 5.6 5.5 5.6 5.1 5.0 5.0 5.0 5.0 4.7 4.7 4.0 4.5 5.0 5.5 6.0 6.5 7.0 4Q09 2Q10 4Q10 2Q11 4Q11 2Q12 4Q12 2Q13 4Q13 2Q14 4Q14 2Q15 (%) Source: Bank Indonesia Exhibit 4. Interest rate and inflation 7.50 7.50 7.50 7.00 7.25 3.99 4.83 8.36 6.38 7.15 7.88 6.90 6.09 6.09 0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0 9.0 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15F Jan-16F Apr-16F Jul-16F Oct-16F (%) BI rate CPI y-y Source: Bank Indonesia, Bahana estimate Exhibit 5. Output gap 4.5 5.0 5.5 6.0 6.5 7.0 -0.8 -0.6 -0.4 -0.2 0.0 0.2 0.4 0.6 0.8 1Q07 4Q07 3Q08 2Q09 1Q10 4Q10 3Q11 2Q12 1Q13 4Q13 3Q14 2Q15 (%) (%) Output Gap (LHS) Annualized GDP Growth (RHS) 2009-2010 economic moderation period Source: Statistics Indonesia, Bahana Estimate

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Asiamoney’s

2013

Best Domestic

Equity House

Economics flash

24 August 2015

Disclosure: Bahana Securities does and seeks to do business with companies covered in its research reports. Investors should consider this report as only a single factor

in making their investment decision.

Please see the important disclaimer information on the back of this report

2014Finance Asia's

Best Equity House

Alpha Southeast Asia

2014 Best Research Call FMCG Sector

Asiamoney's2013

Best DomesticEquity House

2015Institutional

Investors Highest RankedLocal Research

House

2015Global

Banking & FinanceReview

Best ResearchHouse

Indonesia economic outlook

Fakhrul Fulvian Adi Saputra E-mail: [email protected] Email: [email protected]

Phone: +6221 2505081 ext. 3602 Phone: +6221 2505081 ext. 3693

Tough times ahead

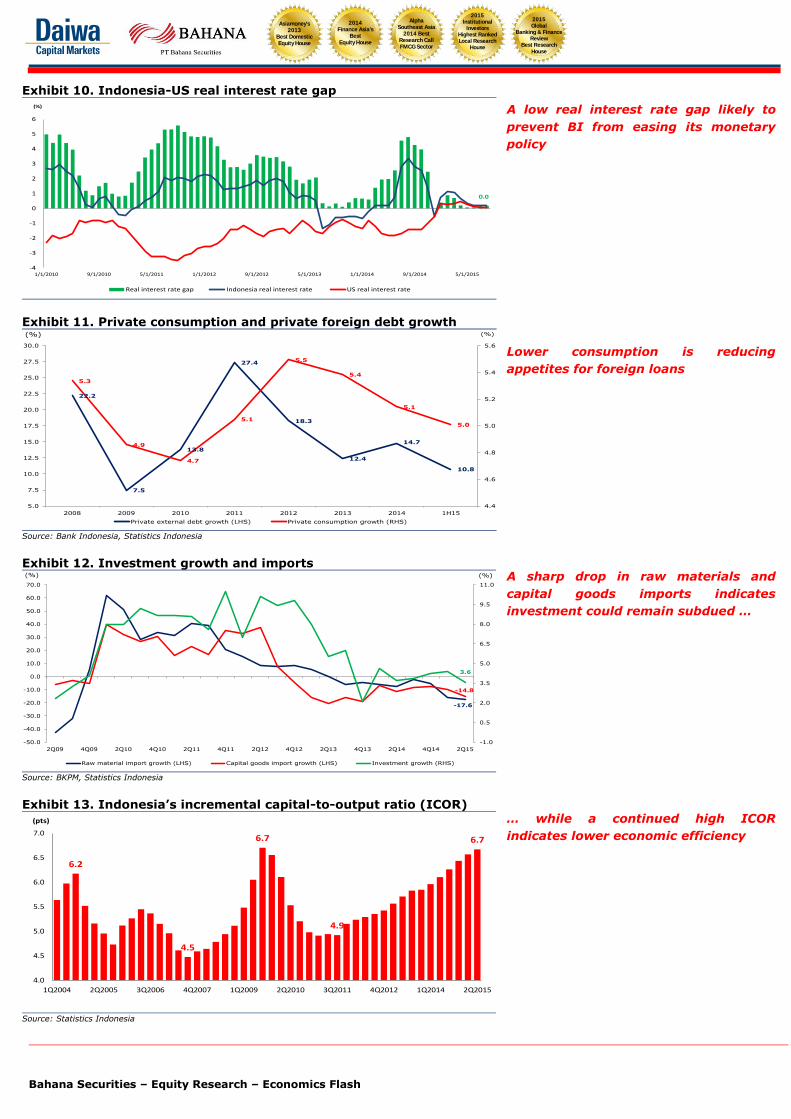

Moderate domestic demand and investment to continue: Private

consumption growth of below 5% y-y in 2Q15 and declining imports in July (-

28% y-y) affirm our view of continued weak domestic demand and

investment and leads us to make changes to our macro indicators (exhibit

2). The tight monetary policy of the past two years should continue to result

in economic moderation through 1Q16. Region-wise, we expect the

commodity economy outside of Java to persist with lower growth amid soft

commodity prices. At this point, room for a BI rate cut to spur growth still

appears limited, as the Indonesia-US real interest rate gap remains small

(exhibit 10). Historically, a recovery has often followed a negative output gap

by 3-4 quarters (exhibit 5).

2016 state budget draft seems overly optimistic: Last week, the

government announced its 2016 state budget plan, which included

IDR1,848tn of government revenue (+5% y-y). The target looks high, as

assuming a IDR250tn shortfall in 2015, we estimate that tax revenue would

have to jump 26.4% y-y in 2016 to achieve the target (exhibit 15). A higher

regional transfer portion is an interesting part of the new budget, leading to

greater unpredictability in terms of execution risk.

Global slowdown, a blessing and a curse: The IMF already cut its 2015

GDP growth forecast for emerging economies to 4.2% from 4.6% in 2014 on

lower commodity prices (exhibit 6) and tightening global financial conditions.

For Indonesia, lower oil prices are already having a positive net effect on the

external trade balance, as the CAD-to-GDP ratio was only 2.1% in 2Q15

(2014: 3.1%). We estimate that every 10% drop in the oil price would

increase the monthly trade balance by USD78m. That said, even though the

2Q15 trade balance was a net positive, continued steep export drops (2Q15:

-19.2% y-y) and an ongoing lower Indonesian shares in global markets are

restraining the country’s ability to generate foreign reserves to finance

external debt.

Stable inflation the key to avoid a vicious circle: Indonesia currently is

the only country with above 5% y-y inflation among its peers (exhibit 20),

caused by several fuel-price hikes since 2013. In terms of purchasing power

parity (PPP), this is why the IDR has depreciated the most among these

countries. Technically, without another supply shock, we believe inflation

should be below 5.0% at end-2015, but we see possible upside from the

recent El Nino weather pattern and possible additional fuel-price hikes due in

September/October. In our view, a managable inflation level is imperative to

prevent a vicious circle of currency depreciation and high inflation.

Fair and manageable moderation is expected this time: The recent IDR

depreciation has raised concerns about foreign debt payments and the

sufficiency of foreign reserves, which now cover just 6.9 months of imports.

We remain cautious on this issue, although 2Q15 private external debt

growth has slowed but to a still high level of 9.7% y-y (1Q15: 13.4%).

However, BI's tightening policy, in place since 2013, has normalized the

Exhibit 1. Macro assumptions

2014A 2015F 2016F 2017F

Cur acc (% GDP) -3.0 -2.0 -2.3 -2.3

Fiscal bal (% GDP) -2.3 -2.2 -2.2 -2.3

GDP growth(% y-y) 5.0 4.7 5.1 5.2

Inflation (% y-y) 8.4 4.8 5.2 5.3

Oil price(USD/bbl) 57.3 55.0 57.0 63.0

Oil price(USD/bbl)* 99.5 58.0 55.0 60.0

IDR/1USD 12,385 14,000 14,500 14,000

BI rate (% p.a.) 7.75 7.50 7.00 6.50

FX reserve (USDbn) 111.9 105.0 110.0 112.0 Source: BI, BPS, Bahana estimate, *Average Brent oil price

Exhibit 2. Forecast changes

2015F 2016F

Old New Old New

GDP growth (%) 4.86 4.72 5.29 5.10

CAD (% of GDP) 2.50 2.00 2.30 2.30

IDR/USD, Average 13,350 13,455 14,200 14,533

IDR/USD, End-year 13,700 14,000 14,000 14,500 Source: Bahana estimate

Exhibit 3. GDP growth trend

6.1

6.8

6.2

6.5 6.5

6.3

6.05.9

6.16.2

5.95.9

5.6 5.65.5

5.6

5.1

5.05.0

5.0 5.0

4.74.7

4.0

4.5

5.0

5.5

6.0

6.5

7.0

4Q09 2Q10 4Q10 2Q11 4Q11 2Q12 4Q12 2Q13 4Q13 2Q14 4Q14 2Q15

(%)

Source: Bank Indonesia

Exhibit 4. Interest rate and inflation

7.50 7.50 7.50

7.007.25

3.99

4.83

8.36

6.387.15

7.88

6.90

6.09

6.09

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15F Jan-16F Apr-16F Jul-16F Oct-16F

(%)

BI rate CPI y-y

Source: Bank Indonesia, Bahana estimate

Exhibit 5. Output gap

4.5

5.0

5.5

6.0

6.5

7.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1Q07 4Q07 3Q08 2Q09 1Q10 4Q10 3Q11 2Q12 1Q13 4Q13 3Q14 2Q15

(%)(%)

Output Gap (LHS) Annualized GDP Growth (RHS)

2009-2010 economic moderation period

Source: Statistics Indonesia, Bahana Estimate

Bahana Securities – Equity Research – Economics Flash

2014Finance Asia's

Best Equity House

Alpha Southeast Asia

2014 Best Research Call FMCG Sector

Asiamoney's2013

Best DomesticEquity House

2015Institutional

Investors Highest RankedLocal Research

House

2015Global

Banking & FinanceReview

Best ResearchHouse

external balance. Moreover, current country debt levels are still far from

1998 recessions levels.

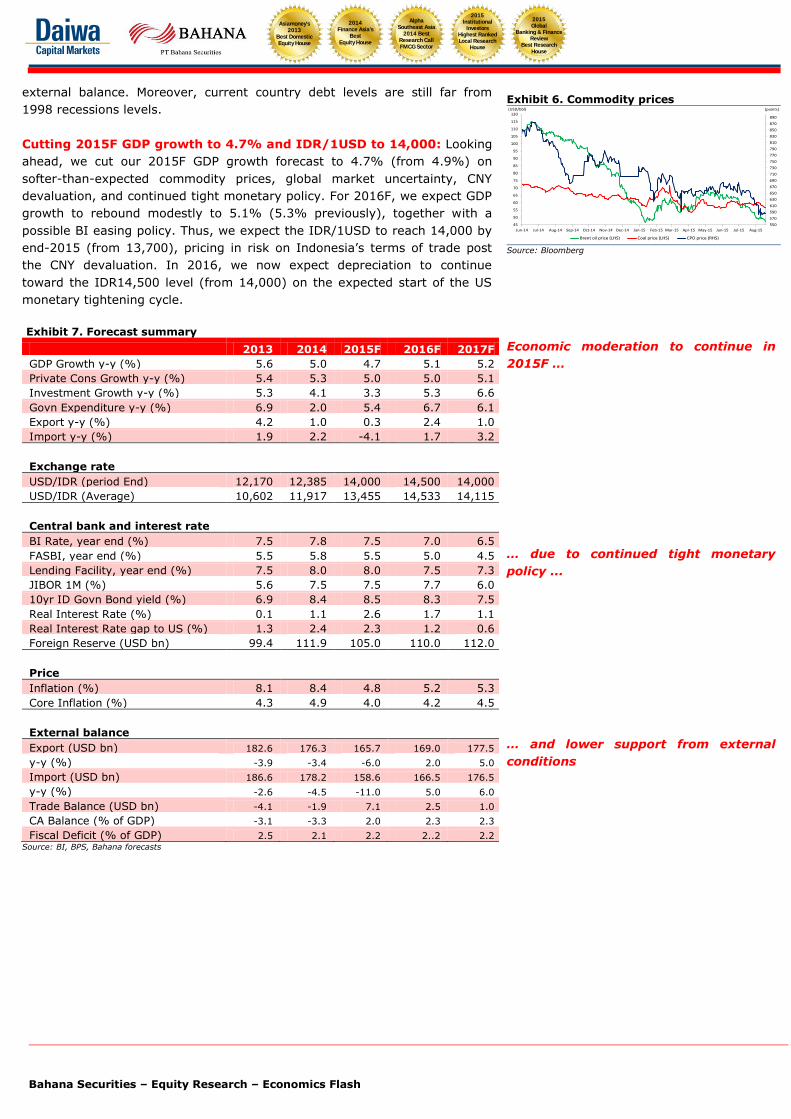

Cutting 2015F GDP growth to 4.7% and IDR/1USD to 14,000: Looking

ahead, we cut our 2015F GDP growth forecast to 4.7% (from 4.9%) on

softer-than-expected commodity prices, global market uncertainty, CNY

devaluation, and continued tight monetary policy. For 2016F, we expect GDP

growth to rebound modestly to 5.1% (5.3% previously), together with a

possible BI easing policy. Thus, we expect the IDR/1USD to reach 14,000 by

end-2015 (from 13,700), pricing in risk on Indonesia’s terms of trade post

the CNY devaluation. In 2016, we now expect depreciation to continue

toward the IDR14,500 level (from 14,000) on the expected start of the US

monetary tightening cycle.

Exhibit 7. Forecast summary

2013 2014 2015F 2016F 2017F

GDP Growth y-y (%) 5.6 5.0 4.7 5.1 5.2

Private Cons Growth y-y (%) 5.4 5.3 5.0 5.0 5.1

Investment Growth y-y (%) 5.3 4.1 3.3 5.3 6.6

Govn Expenditure y-y (%) 6.9 2.0 5.4 6.7 6.1

Export y-y (%) 4.2 1.0 0.3 2.4 1.0

Import y-y (%) 1.9 2.2 -4.1 1.7 3.2

Exchange rate

USD/IDR (period End) 12,170 12,385 14,000 14,500 14,000

USD/IDR (Average) 10,602 11,917 13,455 14,533 14,115

Central bank and interest rate

BI Rate, year end (%) 7.5 7.8 7.5 7.0 6.5

FASBI, year end (%) 5.5 5.8 5.5 5.0 4.5

Lending Facility, year end (%) 7.5 8.0 8.0 7.5 7.3

JIBOR 1M (%) 5.6 7.5 7.5 7.7 6.0

10yr ID Govn Bond yield (%) 6.9 8.4 8.5 8.3 7.5

Real Interest Rate (%) 0.1 1.1 2.6 1.7 1.1

Real Interest Rate gap to US (%) 1.3 2.4 2.3 1.2 0.6

Foreign Reserve (USD bn) 99.4 111.9 105.0 110.0 112.0

Price

Inflation (%) 8.1 8.4 4.8 5.2 5.3

Core Inflation (%) 4.3 4.9 4.0 4.2 4.5

External balance

Export (USD bn) 182.6 176.3 165.7 169.0 177.5

y-y (%) -3.9 -3.4 -6.0 2.0 5.0

Import (USD bn) 186.6 178.2 158.6 166.5 176.5

y-y (%) -2.6 -4.5 -11.0 5.0 6.0

Trade Balance (USD bn) -4.1 -1.9 7.1 2.5 1.0

CA Balance (% of GDP) -3.1 -3.3 2.0 2.3 2.3

Fiscal Deficit (% of GDP) 2.5 2.1 2.2 2..2 2.2 Source: BI, BPS, Bahana forecasts

Exhibit 6. Commodity prices

550

570

590

610

630

650

670

690

710

730

750

770

790

810

830

850

870

890

45

50

55

60

65

70

75

80

85

90

95

100

105

110

115

120

Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15

(points)(USD/bbl)

Brent oil price (LHS) Coal price (LHS) CPO price (RHS)

Source: Bloomberg

Economic moderation to continue in

2015F …

… due to continued tight monetary

policy ...

… and lower support from external

conditions

Bahana Securities – Equity Research – Economics Flash

2014Finance Asia's

Best Equity House

Alpha Southeast Asia

2014 Best Research Call FMCG Sector

Asiamoney's2013

Best DomesticEquity House

2015Institutional

Investors Highest RankedLocal Research

House

2015Global

Banking & FinanceReview

Best ResearchHouse

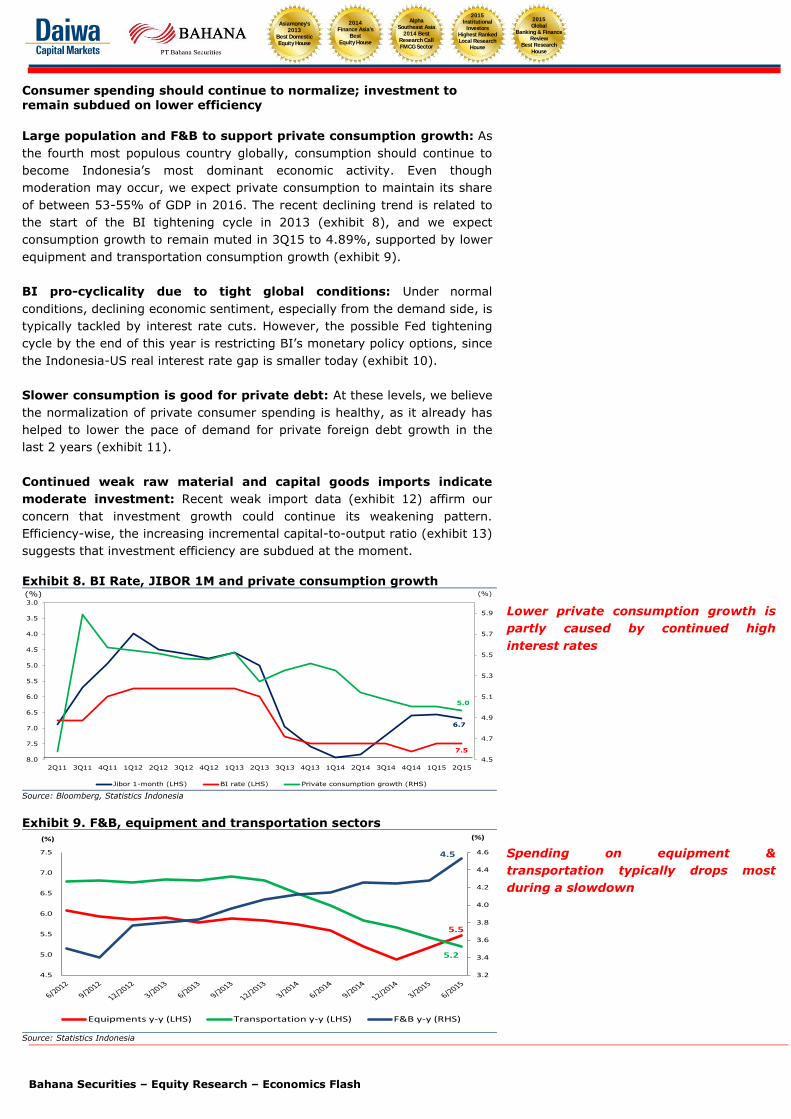

Consumer spending should continue to normalize; investment to

remain subdued on lower efficiency

Large population and F&B to support private consumption growth: As

the fourth most populous country globally, consumption should continue to

become Indonesia’s most dominant economic activity. Even though

moderation may occur, we expect private consumption to maintain its share

of between 53-55% of GDP in 2016. The recent declining trend is related to

the start of the BI tightening cycle in 2013 (exhibit 8), and we expect

consumption growth to remain muted in 3Q15 to 4.89%, supported by lower

equipment and transportation consumption growth (exhibit 9).

BI pro-cyclicality due to tight global conditions: Under normal

conditions, declining economic sentiment, especially from the demand side, is

typically tackled by interest rate cuts. However, the possible Fed tightening

cycle by the end of this year is restricting BI’s monetary policy options, since

the Indonesia-US real interest rate gap is smaller today (exhibit 10).

Slower consumption is good for private debt: At these levels, we believe

the normalization of private consumer spending is healthy, as it already has

helped to lower the pace of demand for private foreign debt growth in the

last 2 years (exhibit 11).

Continued weak raw material and capital goods imports indicate

moderate investment: Recent weak import data (exhibit 12) affirm our

concern that investment growth could continue its weakening pattern.

Efficiency-wise, the increasing incremental capital-to-output ratio (exhibit 13)

suggests that investment efficiency are subdued at the moment.

Exhibit 8. BI Rate, JIBOR 1M and private consumption growth

6.7

7.5

5.0

4.5

4.7

4.9

5.1

5.3

5.5

5.7

5.9

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

(%)(%)

Jibor 1-month (LHS) BI rate (LHS) Private consumption growth (RHS) Source: Bloomberg, Statistics Indonesia

Exhibit 9. F&B, equipment and transportation sectors

5.5

5.2

4.5

3.2

3.4

3.6

3.8

4.0

4.2

4.4

4.6

4.5

5.0

5.5

6.0

6.5

7.0

7.5

(%)(%)

Equipments y-y (LHS) Transportation y-y (LHS) F&B y-y (RHS)

Source: Statistics Indonesia

Lower private consumption growth is

partly caused by continued high

interest rates

Spending on equipment &

transportation typically drops most

during a slowdown

Bahana Securities – Equity Research – Economics Flash

2014Finance Asia's

Best Equity House

Alpha Southeast Asia

2014 Best Research Call FMCG Sector

Asiamoney's2013

Best DomesticEquity House

2015Institutional

Investors Highest RankedLocal Research

House

2015Global

Banking & FinanceReview

Best ResearchHouse

Exhibit 10. Indonesia-US real interest rate gap

0.0

-4

-3

-2

-1

0

1

2

3

4

5

6

1/1/2010 9/1/2010 5/1/2011 1/1/2012 9/1/2012 5/1/2013 1/1/2014 9/1/2014 5/1/2015

(%)

Real interest rate gap Indonesia real interest rate US real interest rate

Exhibit 11. Private consumption and private foreign debt growth

22.2

7.5

13.8

27.4

18.3

12.4

14.7

10.8

5.3

4.9

4.7

5.1

5.5

5.4

5.1

5.0

4.4

4.6

4.8

5.0

5.2

5.4

5.6

5.0

7.5

10.0

12.5

15.0

17.5

20.0

22.5

25.0

27.5

30.0

2008 2009 2010 2011 2012 2013 2014 1H15

(%)(%)

Private external debt growth (LHS) Private consumption growth (RHS)

Source: Bank Indonesia, Statistics Indonesia

Exhibit 12. Investment growth and imports

-17.6

-14.8

3.6

-1.0

0.5

2.0

3.5

5.0

6.5

8.0

9.5

11.0

-50.0

-40.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

2Q09 4Q09 2Q10 4Q10 2Q11 4Q11 2Q12 4Q12 2Q13 4Q13 2Q14 4Q14 2Q15

(%)(%)

Raw material import growth (LHS) Capital goods import growth (LHS) Investment growth (RHS)

Source: BKPM, Statistics Indonesia

Exhibit 13. Indonesia’s incremental capital-to-output ratio (ICOR)

6.2

4.5

6.7

4.9

6.7

4.0

4.5

5.0

5.5

6.0

6.5

7.0

1Q2004 2Q2005 3Q2006 4Q2007 1Q2009 2Q2010 3Q2011 4Q2012 1Q2014 2Q2015

(pts)

Source: Statistics Indonesia

A low real interest rate gap likely to

prevent BI from easing its monetary

policy

Lower consumption is reducing

appetites for foreign loans

A sharp drop in raw materials and

capital goods imports indicates

investment could remain subdued …

… while a continued high ICOR

indicates lower economic efficiency

Bahana Securities – Equity Research – Economics Flash

2014Finance Asia's

Best Equity House

Alpha Southeast Asia

2014 Best Research Call FMCG Sector

Asiamoney's2013

Best DomesticEquity House

2015Institutional

Investors Highest RankedLocal Research

House

2015Global

Banking & FinanceReview

Best ResearchHouse

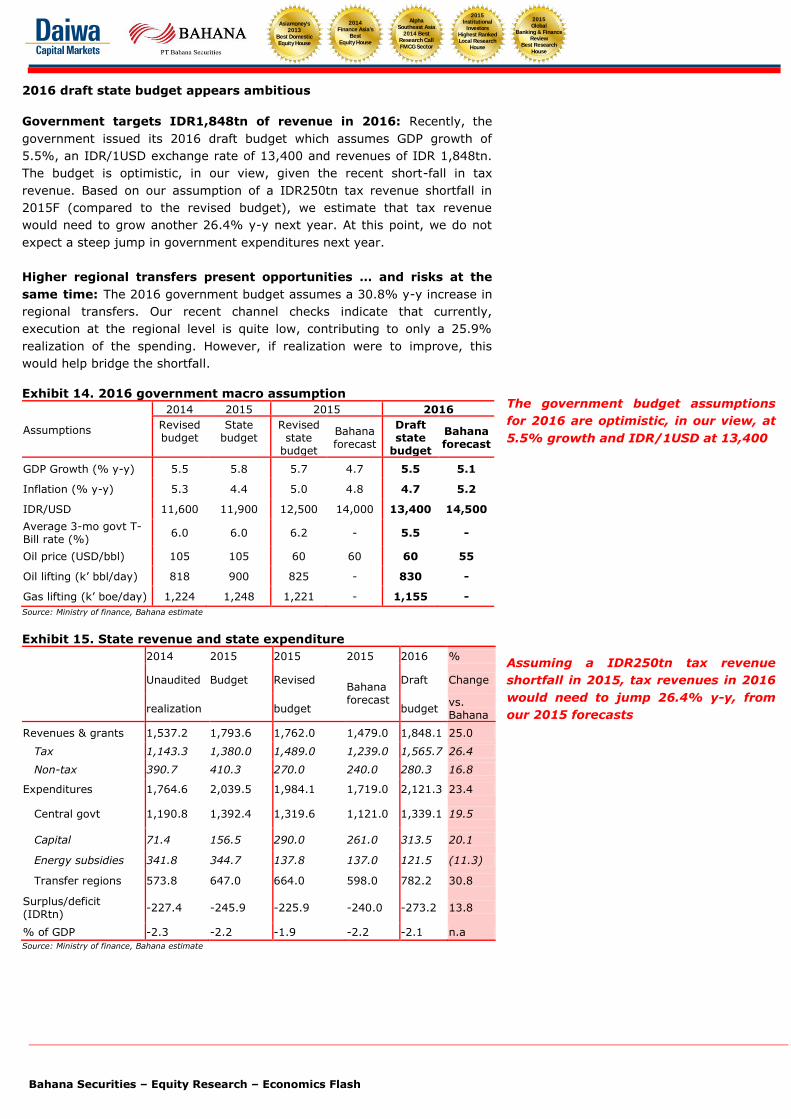

2016 draft state budget appears ambitious

Government targets IDR1,848tn of revenue in 2016: Recently, the

government issued its 2016 draft budget which assumes GDP growth of

5.5%, an IDR/1USD exchange rate of 13,400 and revenues of IDR 1,848tn.

The budget is optimistic, in our view, given the recent short-fall in tax

revenue. Based on our assumption of a IDR250tn tax revenue shortfall in

2015F (compared to the revised budget), we estimate that tax revenue

would need to grow another 26.4% y-y next year. At this point, we do not

expect a steep jump in government expenditures next year.

Higher regional transfers present opportunities … and risks at the

same time: The 2016 government budget assumes a 30.8% y-y increase in

regional transfers. Our recent channel checks indicate that currently,

execution at the regional level is quite low, contributing to only a 25.9%

realization of the spending. However, if realization were to improve, this

would help bridge the shortfall.

Exhibit 14. 2016 government macro assumption

Assumptions

2014 2015 2015 2016

Revised budget

State budget

Revised state

budget

Bahana forecast

Draft state

budget

Bahana forecast

GDP Growth (% y-y) 5.5 5.8 5.7 4.7 5.5 5.1

Inflation (% y-y) 5.3 4.4 5.0 4.8 4.7 5.2

IDR/USD 11,600 11,900 12,500 14,000 13,400 14,500

Average 3-mo govt T-Bill rate (%)

6.0 6.0 6.2 - 5.5 -

Oil price (USD/bbl) 105 105 60 60 60 55

Oil lifting (k’ bbl/day) 818 900 825 - 830 -

Gas lifting (k’ boe/day) 1,224 1,248 1,221 - 1,155 -

Source: Ministry of finance, Bahana estimate

Exhibit 15. State revenue and state expenditure

2014 2015 2015 2015 2016 %

Unaudited Budget Revised Bahana forecast

Draft Change

realization budget budget vs. Bahana

Revenues & grants 1,537.2 1,793.6 1,762.0 1,479.0 1,848.1 25.0

Tax 1,143.3 1,380.0 1,489.0 1,239.0 1,565.7 26.4

Non-tax 390.7 410.3 270.0 240.0 280.3 16.8

Expenditures 1,764.6 2,039.5 1,984.1 1,719.0 2,121.3 23.4

Central govt 1,190.8 1,392.4 1,319.6 1,121.0 1,339.1 19.5

Capital 71.4 156.5 290.0 261.0 313.5 20.1

Energy subsidies 341.8 344.7 137.8 137.0 121.5 (11.3)

Transfer regions 573.8 647.0 664.0 598.0 782.2 30.8

Surplus/deficit (IDRtn)

-227.4 -245.9 -225.9 -240.0 -273.2 13.8

% of GDP -2.3 -2.2 -1.9 -2.2 -2.1 n.a Source: Ministry of finance, Bahana estimate

The government budget assumptions

for 2016 are optimistic, in our view, at

5.5% growth and IDR/1USD at 13,400

Assuming a IDR250tn tax revenue

shortfall in 2015, tax revenues in 2016

would need to jump 26.4% y-y, from

our 2015 forecasts

Bahana Securities – Equity Research – Economics Flash

2014Finance Asia's

Best Equity House

Alpha Southeast Asia

2014 Best Research Call FMCG Sector

Asiamoney's2013

Best DomesticEquity House

2015Institutional

Investors Highest RankedLocal Research

House

2015Global

Banking & FinanceReview

Best ResearchHouse

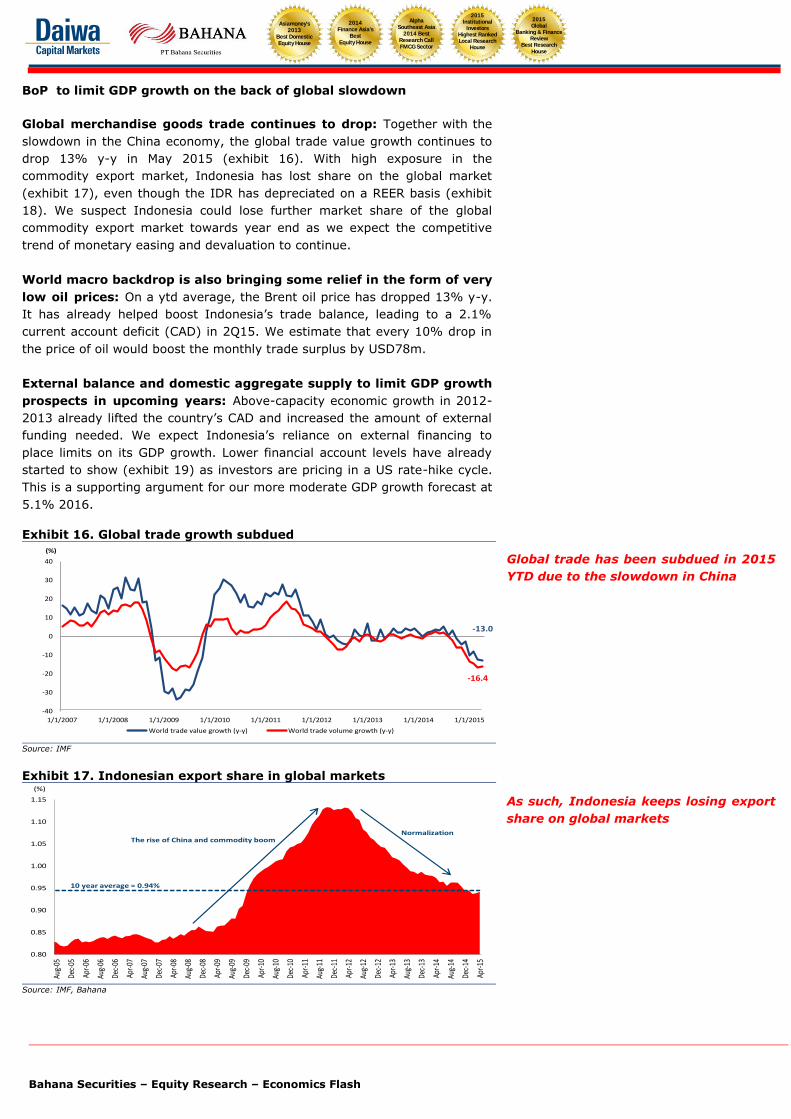

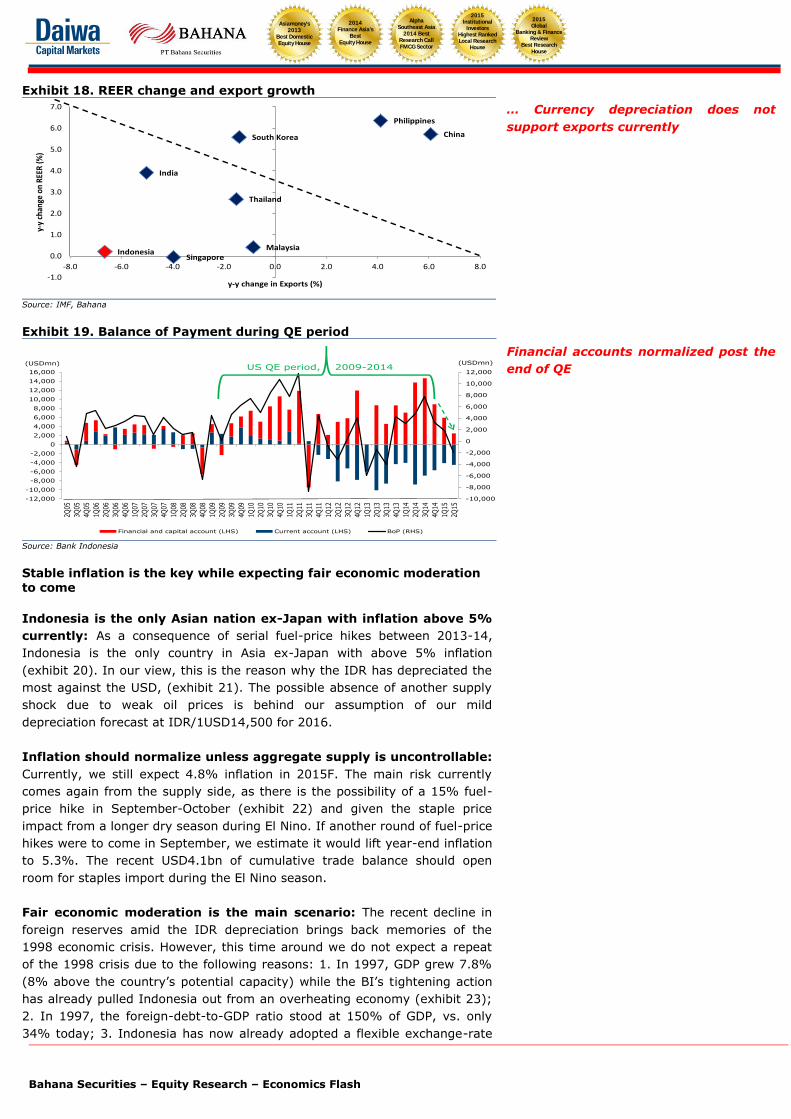

BoP to limit GDP growth on the back of global slowdown

Global merchandise goods trade continues to drop: Together with the

slowdown in the China economy, the global trade value growth continues to

drop 13% y-y in May 2015 (exhibit 16). With high exposure in the

commodity export market, Indonesia has lost share on the global market

(exhibit 17), even though the IDR has depreciated on a REER basis (exhibit

18). We suspect Indonesia could lose further market share of the global

commodity export market towards year end as we expect the competitive

trend of monetary easing and devaluation to continue.

World macro backdrop is also bringing some relief in the form of very

low oil prices: On a ytd average, the Brent oil price has dropped 13% y-y.

It has already helped boost Indonesia’s trade balance, leading to a 2.1%

current account deficit (CAD) in 2Q15. We estimate that every 10% drop in

the price of oil would boost the monthly trade surplus by USD78m.

External balance and domestic aggregate supply to limit GDP growth

prospects in upcoming years: Above-capacity economic growth in 2012-

2013 already lifted the country’s CAD and increased the amount of external

funding needed. We expect Indonesia’s reliance on external financing to

place limits on its GDP growth. Lower financial account levels have already

started to show (exhibit 19) as investors are pricing in a US rate-hike cycle.

This is a supporting argument for our more moderate GDP growth forecast at

5.1% 2016.

Exhibit 16. Global trade growth subdued

-13.0

-16.4

-40

-30

-20

-10

0

10

20

30

40

1/1/2007 1/1/2008 1/1/2009 1/1/2010 1/1/2011 1/1/2012 1/1/2013 1/1/2014 1/1/2015

(%)

World trade value growth (y-y) World trade volume growth (y-y)

Source: IMF Exhibit 17. Indonesian export share in global markets

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

Aug-

05

Dec-

05

Apr-0

6

Aug-

06

Dec-

06

Apr-0

7

Aug-

07

Dec-

07

Apr-0

8

Aug-

08

Dec-

08

Apr-0

9

Aug-

09

Dec-

09

Apr-1

0

Aug-

10

Dec-

10

Apr-1

1

Aug-

11

Dec-

11

Apr-1

2

Aug-

12

Dec-

12

Apr-1

3

Aug-

13

Dec-

13

Apr-1

4

Aug-

14

Dec-

14

Apr-1

5

(%)

10 year average = 0.94%

The rise of China and commodity boom Normalization

Source: IMF, Bahana

Global trade has been subdued in 2015

YTD due to the slowdown in China

As such, Indonesia keeps losing export

share on global markets

Bahana Securities – Equity Research – Economics Flash

2014Finance Asia's

Best Equity House

Alpha Southeast Asia

2014 Best Research Call FMCG Sector

Asiamoney's2013

Best DomesticEquity House

2015Institutional

Investors Highest RankedLocal Research

House

2015Global

Banking & FinanceReview

Best ResearchHouse

Exhibit 18. REER change and export growth

IndonesiaMalaysia

China

Thailand

Singapore

Philippines

India

South Korea

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

-8.0 -6.0 -4.0 -2.0 0.0 2.0 4.0 6.0 8.0

y-y

chan

ge o

n R

EER

(%)

y-y change in Exports (%)

Source: IMF, Bahana

Exhibit 19. Balance of Payment during QE period

-10,000

-8,000

-6,000

-4,000

-2,000

0

2,000

4,000

6,000

8,000

10,000

12,000

-12,000

-10,000

-8,000

-6,000

-4,000

-2,000

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2Q05

3Q05

4Q05

1Q06

2Q06

3Q06

4Q06

1Q07

2Q07

3Q07

4Q07

1Q08

2Q08

3Q08

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

(USDmn)(USDmn)

Financial and capital account (LHS) Current account (LHS) BoP (RHS)

US QE period, 2009-2014

Source: Bank Indonesia

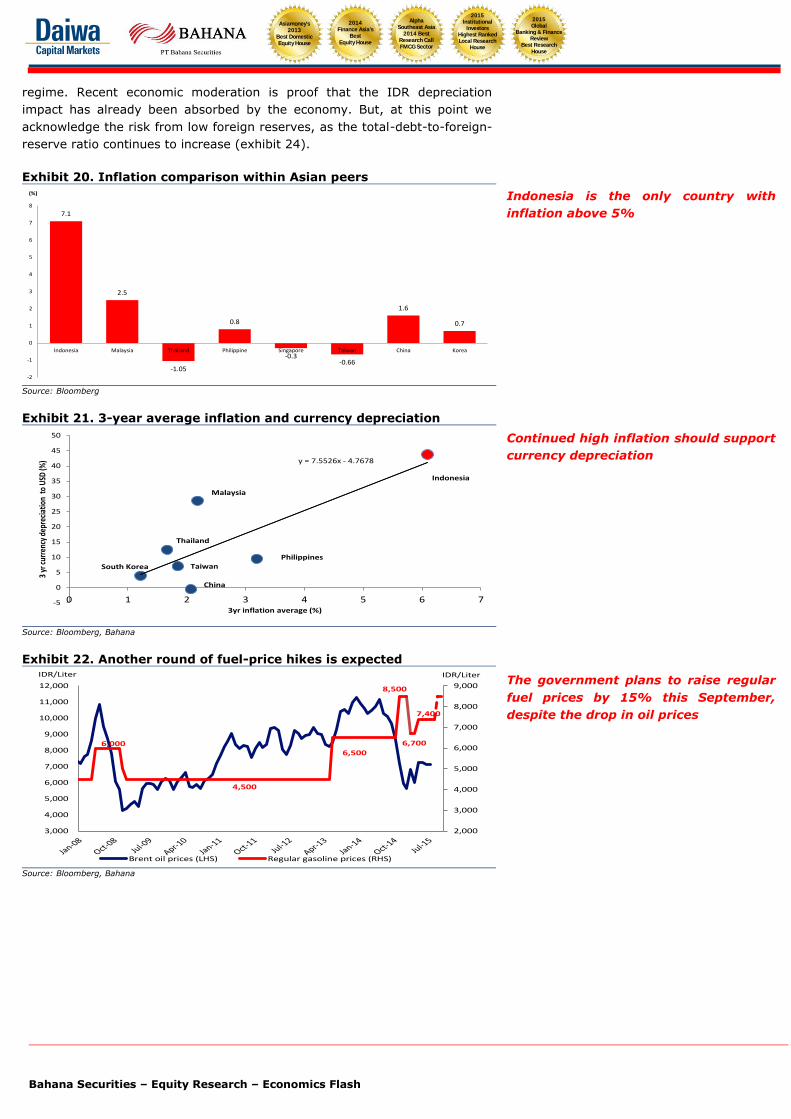

Stable inflation is the key while expecting fair economic moderation to come

Indonesia is the only Asian nation ex-Japan with inflation above 5%

currently: As a consequence of serial fuel-price hikes between 2013-14,

Indonesia is the only country in Asia ex-Japan with above 5% inflation

(exhibit 20). In our view, this is the reason why the IDR has depreciated the

most against the USD, (exhibit 21). The possible absence of another supply

shock due to weak oil prices is behind our assumption of our mild

depreciation forecast at IDR/1USD14,500 for 2016.

Inflation should normalize unless aggregate supply is uncontrollable:

Currently, we still expect 4.8% inflation in 2015F. The main risk currently

comes again from the supply side, as there is the possibility of a 15% fuel-

price hike in September-October (exhibit 22) and given the staple price

impact from a longer dry season during El Nino. If another round of fuel-price

hikes were to come in September, we estimate it would lift year-end inflation

to 5.3%. The recent USD4.1bn of cumulative trade balance should open

room for staples import during the El Nino season.

Fair economic moderation is the main scenario: The recent decline in

foreign reserves amid the IDR depreciation brings back memories of the

1998 economic crisis. However, this time around we do not expect a repeat

of the 1998 crisis due to the following reasons: 1. In 1997, GDP grew 7.8%

(8% above the country’s potential capacity) while the BI’s tightening action

has already pulled Indonesia out from an overheating economy (exhibit 23);

2. In 1997, the foreign-debt-to-GDP ratio stood at 150% of GDP, vs. only

34% today; 3. Indonesia has now already adopted a flexible exchange-rate

… Currency depreciation does not

support exports currently

Financial accounts normalized post the

end of QE

Bahana Securities – Equity Research – Economics Flash

2014Finance Asia's

Best Equity House

Alpha Southeast Asia

2014 Best Research Call FMCG Sector

Asiamoney's2013

Best DomesticEquity House

2015Institutional

Investors Highest RankedLocal Research

House

2015Global

Banking & FinanceReview

Best ResearchHouse

regime. Recent economic moderation is proof that the IDR depreciation

impact has already been absorbed by the economy. But, at this point we

acknowledge the risk from low foreign reserves, as the total-debt-to-foreign-

reserve ratio continues to increase (exhibit 24).

Exhibit 20. Inflation comparison within Asian peers

7.1

2.5

-1.05

0.8

-0.3-0.66

1.6

0.7

-2

-1

0

1

2

3

4

5

6

7

8

Indonesia Malaysia Thailand Philippine Singapore Taiwan China Korea

(%)

Source: Bloomberg

Exhibit 21. 3-year average inflation and currency depreciation

Indonesia

Malaysia

Thailand

PhilippinesTaiwan

China

South Korea

y = 7.5526x - 4.7678

-5

0

5

10

15

20

25

30

35

40

45

50

0 1 2 3 4 5 6 7

3 yr

cur

renc

y de

prec

iatio

n to

USD

(%)

3yr inflation average (%)

Source: Bloomberg, Bahana

Exhibit 22. Another round of fuel-price hikes is expected

6,000

4,500

6,500

8,500

6,700

7,400

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

IDR/LiterIDR/Liter

Brent oil prices (LHS) Regular gasoline prices (RHS)

Source: Bloomberg, Bahana

Indonesia is the only country with

inflation above 5%

Continued high inflation should support

currency depreciation

The government plans to raise regular

fuel prices by 15% this September,

despite the drop in oil prices

Bahana Securities – Equity Research – Economics Flash

2014Finance Asia's

Best Equity House

Alpha Southeast Asia

2014 Best Research Call FMCG Sector

Asiamoney's2013

Best DomesticEquity House

2015Institutional

Investors Highest RankedLocal Research

House

2015Global

Banking & FinanceReview

Best ResearchHouse

Exhibit 23. Business cycle comparison (1990-2015)

7.8

-13.6

5.0

6.4

4.5

6.4

4.8

-8

-6

-4

-2

0

2

4

6

8

10

-15

-10

-5

0

5

10

4Q1991 2Q1993 4Q1994 2Q1996 4Q1997 2Q1999 4Q2000 2Q2002 4Q2003 2Q2005 4Q2006 2Q2008 4Q2009 2Q2011 4Q2012 2Q2014

(%)(%)

Output Gap (RHS) Annualized GDP Growth (LHS)

Economic Overheating

Asian Crisis

SubprimeMortgage

GlobalSlowdown

Source: Statistics Indonesia, Bahana

Exhibit 24.Foreign-reserve-to-debt ratio

27.838.7

55.764.9

81.9

138.8

111.1

226.6

26.136.1

50.669.3

87.2 106.7

108.3

246.0

0

50

100

150

200

250

300

Turkey Indonesia Malaysia India Korea Philippine Thailand Taiwan

(%)

July 2014 July 2015

Source: Bloomberg

The economy is unlikely to overheat

like it did in 1998

Low foreign-reserve-to-debt ratio is a

downside factor

Fakhrul Fulvian

[email protected] 3602

Melvin Mikha Reminov

[email protected] Associate

ext 3621

Research: +62 21 250 5081

Harry [email protected]

Senior Associate DirectorHead of Research

Strategy, Consumer

ext 3600direct: +62 21 250 5735

Dealing Room: +62 21 527 0808 (Foreign Institutional)

Teguh Hartanto

[email protected] Director

Deputy Head of Research

Banks, Cement, Aviationext 3610

Leonardo Henry Gavaza, [email protected]

Senior Research ManagerAuto, Heavy equipment, Telco

ext 3608

Chandra Widjanarka

[email protected] Analyst

ext 1252

+62 21 250 5508 (Domestic Institutional)

Ashish Agrawal

[email protected] President

Institutional Equity Salesext 2550 / 2553

Reynard Poernawan

[email protected] Equity Sales

ext 2528

John M. [email protected]

Equity Salesext 2549

Yohanes Adhi Handoko

[email protected], Surabaya Branch

ext 7250

Suwardi Widjaja

[email protected] Sales

ext 2548

Amelia Husada

[email protected] President

Institutional Equity Salesext 2552

Michael W Setjoadi [email protected]

Research AnalystConsumer, Healthcare, Poultry

ext 3613

Nurul Farida

[email protected] Sales

ext 2543

Adrian Mahendra Putra

[email protected] AnalystIndustrial Estate

ext 3614

Hanna Marionda

[email protected] Trader

ext 2525

Adriana Kosasih

[email protected] Executive

ext 2541

Ari Santosa

[email protected] Trader

ext 2554

Adi Saputra

[email protected] & Fixed Income Associate

ext 3693

Robin Sutanto

[email protected] Analyst

Propertyext 3620

Agustinus Reza Kirana

[email protected] Analyst

Plantations, Shipping, Transportationext 3616

Research AnalystCement, Infratructure,Toll roads

ext 3605

Muhammad Wafi

[email protected] Analyst

ext 3609

+62 31 535 2788 (Surabaya Branch)

Arandi [email protected]

Research AnalystCoal, Metals, Oil & Gas

ext 3619

Head of Equity Sales & TradingInstitutional Equity Sales

ext 2545

Made Ayu Wijayati

[email protected] Executive

ext 3607

Sanni Satrio Dwi Utomo

[email protected] Associate

ext 3611

Andre Natala Susanto

[email protected] Associate

ext 3601

Bagus Adi Yoga Prawira

[email protected] AnalystConsumer, Media

ext 3604

Zefanya Halim

[email protected] Manager

ext 3612

Novianty Permata Sari

ext 3618

Head Office Surabaya Branch

Graha Niaga, 19th Floor Wisma BII, Ground Floor

Jl. Jend. Sudirman Kav. 58 Jl. Pemuda 60-70

Jakarta 12190 Surabaya 60271

Indonesia Indonesia

Tel. 62 21 250 5081 Tel. 62 31 535 2788

Fax. 62 21 522 6049 http://www.bahana.co.id Fax. 62 31 546 1157

Important Disclosures and Disclaimer This publication is prepared by PT.Bahana Securities and reviewed by Daiwa Securities Group Inc. and/or its affiliates, and distributed outside Indonesia by Daiwa Securities Group Inc. and/or its affiliates, except to the extent expressly provided herein. Certain copies of this publication may be distributed inside and outside of Indonesia by PT. Bahana Securities in accordance with relevant laws and regulations. This publication and the contents hereof are intended for information purposes only, and may be subject to change without further notice. Any use, disclosure, distribution, dissemination, copying, printing or reliance on this publication for any other purpose without our prior consent or approval is strictly prohibited. Any review does not constitute a full verification of the publication and merely provides a minimum check. Neither Daiwa Securities Group Inc. nor any of its respective parent, holding, subsidiaries or affiliates, nor any of its respective directors, officers, servants and employees, represent nor warrant the accuracy or completeness of the information contained herein or as to the existence of other facts which might be significant, and will not accept any responsibility or liability whatsoever for any use of or reliance upon this publication or any of the contents hereof. Neither this publication, nor any content hereof, constitute, or are to be construed as, an offer or solicitation of an offer to buy or sell any of the securities or investments mentioned herein in any country or jurisdiction nor, unless expressly provided, any recommendation or investment opinion or advice. Any view, recommendation, opinion or advice expressed in this publication constitutes the views of the analyst(s) named herein and does not necessarily reflect those of Daiwa Securities Group Inc. and/or its affiliates nor any of its respective directors, officers, servants and employees except where the publication states otherwise. This research report is not to be relied upon by any person in making any investment decision or otherwise advising with respect to, or dealing in, the securities mentioned, as it does not take into account the specific investment objectives, financial situation and particular needs of any person.

Neither Daiwa Securities Group Inc. nor any of its affiliates is licensed to undertake any business within the Republic of Indonesia. Any display of any trade name or logo of the Daiwa Securities Group Inc. on this publication shall not be deemed to be an undertaking of any business within the Republic of Indonesia.

Daiwa Securities Group Inc., its subsidiaries or affiliates, or its or their respective directors, officers and employees from time to time may have trades as principals, or have positions in, or have other interests in the securities of the company under research including market making activities, derivatives in respect of such securities or may have also performed investment banking and other services for the issuer of such securities. The following are additional disclosures.

Ownership of Securities

For “Ownership of Securities” information, please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action.

Investment Banking Relationship

For “Investment Banking Relationship”, please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action.

Japan

Daiwa Securities Co. Ltd. and Daiwa Securities Group Inc.

Daiwa Securities Co. Ltd. is a subsidiary of Daiwa Securities Group Inc.

Investment Banking Relationship

Within the preceding 12 months, The subsidiaries and/or affiliates of Daiwa Securities Group Inc. * has lead-managed public offerings and/or secondary offerings (excluding straight bonds) of the securities of the following companies: Modern Land (China) Co. Ltd (1107 HK); econtext Asia Ltd (1390 HK); Accordia Golf Trust (AGT SP); Hua Hong Semiconductor Ltd (1347 HK); GF Securities Co Ltd (1776 HK); Mirae Asset Life Insurance Co Ltd (085620 KS).

*Subsidiaries of Daiwa Securities Group Inc. for the purposes of this section shall mean any one or more of:

• Daiwa Capital Markets Hong Kong Limited (大和資本市場香港有限公司)

• Daiwa Capital Markets Singapore Limited

• Daiwa Capital Markets Australia Limited

• Daiwa Capital Markets India Private Limited

• Daiwa-Cathay Capital Markets Co., Ltd.

• Daiwa Securities Capital Markets Korea Co., Ltd

Disclosure of Interest of Bahana Securities

Investment Banking Relationship

Within the preceding 12 months, Bahana Securities has lead-managed public offerings and/or secondary offerings (excluding straight bonds) of the securities of the following companies: J Resources Asia Pasific Tbk PT (PSAB IJ); Waskita Karya Persero Tbk PT (WSKT IJ); Adhi Karya Persero Tbk PT (ADHI IJ); PP Properti Tbk PT (PPRO IJ); Merdeka Copper Gold Tbk PT (MDKA IJ)

Hong Kong

This research is distributed in Hong Kong by Daiwa Capital Markets Hong Kong Limited (大和資本市場香港有限公司) (“DHK”) which is regulated by the Hong Kong Securities and Futures Commission. Recipients of this research in Hong Kong may contact DHK in respect of any matter arising from or in connection with this research.

Relevant Relationship (DHK)

DHK may from time to time have an individual employed by or associated with it serves as an officer of any of the companies under its research coverage.

Singapore

This research is distributed in Singapore by Daiwa Capital Markets Singapore Limited and it may only be distributed in Singapore to accredited investors, expert investors and institutional investors as defined in the Financial Advisers Regulations and the Securities and Futures Act (Chapter 289), as amended from time to time. By virtue of distribution to these category of investors, Daiwa Capital Markets Singapore Limited and its representatives are not required to comply with Section 36 of the Financial Advisers Act (Chapter 110) (Section 36 relates to disclosure of Daiwa Capital Markets Singapore Limited’s interest and/or its representative’s interest in securities). Recipients of this research in Singapore may contact Daiwa Capital Markets Singapore Limited in respect of any matter arising from or in connection with the research.

Australia

This research is distributed in Australia by Daiwa Capital Markets Australia Limited and it may only be distributed in Australia to wholesale investors within the meaning of the Corporations Act. Recipients of this research in Australia may contact Daiwa Capital Markets Stockbroking Limited in respect of any matter arising from or in connection with the research.

India

This research is distributed in India to Institutional Clients only by Daiwa Capital Markets India Private Limited (Daiwa India) which is an intermediary registered with Securities & Exchange Board of India as a Stock Broker, Merchant Bank and Research Analyst. Daiwa India, its Research Analyst and their family members and its associates do not have any financial interest save as disclosed or other undisclosed material conflict of interest in the securities or derivatives of any companies under coverage. Daiwa India and its associates may have received compensation for any products other than Investment Banking (as disclosed) or brokerage services from the subject company in this report during the past 12 months. Unless otherwise stated in BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action, Daiwa India and its associates do not hold more than 1% of any companies covered in this research report.

There is no material disciplinary action against Daiwa India by any regulatory authority impacting equity research analysis activities as of the date of this report.

Taiwan

This research is distributed in Taiwan by Daiwa-Cathay Capital Markets Co., Ltd and it may only be distributed in Taiwan to institutional investors or specific investors who have signed recommendation contracts with Daiwa-Cathay Capital Markets Co., Ltd in accordance with the Operational Regulations Governing Securities Firms Recommending Trades in Securities to Customers. Recipients of this research in Taiwan may contact Daiwa-Cathay Capital Markets Co., Ltd in respect of any matter arising from or in connection with the research.

Philippines

This research is distributed in the Philippines by DBP-Daiwa Capital Markets Philippines, Inc. which is regulated by the Philippines Securities and Exchange

Commission and the Philippines Stock Exchange, Inc. Recipients of this research in the Philippines may contact DBP-Daiwa Capital Markets Philippines, Inc.

in respect of any matter arising from or in connection with the research. DBP-Daiwa Capital Markets Philippines, Inc. recommends that investors

independently assess, with a professional advisor, the specific financial risks as well as the legal, regulatory, tax, accounting, and other consequences of a proposed transaction. DBP-Daiwa Capital Markets Philippines, Inc. may have positions or may be materially interested in the securities in any of the markets

mentioned in the publication or may have performed other services for the issuers of such securities.

For relevant securities and trading rules please visit SEC and PSE link at http://www.sec.gov.ph/irr/AmendedIRRfinalversion.pdf and

http://www.pse.com.ph/ respectively.

United Kingdom

This research report is produced by Daiwa Capital Markets Europe Limited and/or its affiliates and is distributed in the European Union, Iceland, Liechtenstein, Norway and Switzerland. Daiwa Capital Markets Europe Limited is authorised and regulated by The Financial Conduct Authority (“FCA”) and is a member of the London Stock Exchange, Eurex and NYSE Liffe.

This publication is intended for investors who are not Retail Clients in the United Kingdom within the meaning of the Rules of the FCA and should not therefore be distributed to such Retail Clients in the United Kingdom. Should you enter into investment business with Daiwa Capital Markets Europe’s affiliates outside the United Kingdom, we are obliged to advise that the protection afforded by the United Kingdom regulatory system may not apply; in particular, the benefits of the Financial Services Compensation Scheme may not be available.

Daiwa Capital Markets Europe Limited has in place organisational arrangements for the prevention and avoidance of conflicts of interest. Our conflict management policy is available at http://www.uk.daiwacm.com/about-us/corporate-governance-regulatory.

Germany

This document is distributed in Germany by Daiwa Capital Markets Europe Limited, Niederlassung Frankfurt which is regulated by BaFin (Bundesanstalt fuer Finanzdienstleistungsaufsicht) for the conduct of business in Germany.

Bahrain

This research material is distributed by Daiwa Capital Markets Europe Limited, Bahrain Branch, regulated by The Central Bank of Bahrain and holds Investment Business Firm – Category 2 license and having its official place of business at the Bahrain World Trade Centre, South Tower, 7th floor, P.O. Box 30069, Manama, Kingdom of Bahrain. Tel No. +973 17534452 Fax No. +973 535113

This material is provided as a reference for making investment decisions and is not intended to be a solicitation for investment. Investment decisions should be made at your own discretion and risk. Accordingly, no representation or warranty, express or implied, is made as to and no reliance should be placed on the fairness, accuracy, completeness or correctness of the information and opinions contained in this document, Content herein is based on information available at the time the research material was prepared and may be amended or otherwise changed in the future without notice. All information is intended for the private use of the person to whom it is provided without any liability whatsoever on the part of Daiwa Capital Markets Europe Limited, Bahrain Branch, any associated company or the employees thereof. If you are in doubt about the suitability of the product or the research material itself, please consult your own financial adviser. Daiwa Capital Markets Europe Limited, Bahrain Branch retains all rights related to the content of this material, which may not be redistributed or otherwise transmitted without prior consent.

United States

This report is distributed in the U.S. by Daiwa Capital Markets America Inc. (DCMA). It may not be accurate or complete and should not be relied upon

as such. It reflects the preparer’s views at the time of its preparation, but may not reflect events occurring after its preparation; nor does it reflect

PT.Bahana Securities’ or DCMA’s views at any time. Neither PT.Bahana Securities, DCMA nor the preparer has any obligation to update this report

or to continue to prepare research on this subject. This report is not an offer to sell or the solicitation of any offer to buy securities. Unless this report

says otherwise, any recommendation it makes is risky and appropriate only for sophisticated speculative investors able to incur significant losses.

Readers should consult their financial advisors to determine whether any such recommendation is consistent with their own investment objectives,

financial situation and needs. This report does not recommend to U.S. recipients the use of any of PT.Bahana Securities’ or DCMA’s non-U.S. affiliates to effect trades in any security and is not supplied with any understanding that U.S. recipients of this report will direct commission business to

such non-U.S. entities. Unless applicable law permits otherwise, non-U.S. customers wishing to effect a transaction in any securities referenced in this

material should contact a Daiwa entity in their local jurisdiction. Most countries throughout the world have their own laws regulating the types of

securities and other investment products which may be offered to their residents, as well as a process for doing so. As a result, the securities

discussed in this report may not be eligible for sales in some jurisdictions. Customers wishing to obtain further information about this report should

contact DCMA: Daiwa Capital Markets America Inc., Financial Square, 32 Old Slip, New York, New York 10005 (Tel no. 212-612-7000).

Ownership of Securities

For “Ownership of Securities” information please visit BlueMatrix disclosure Link at https://daiwa3.bluematrix.com/sellside/Disclosures.action .

Investment Banking Relationships

For “Investment Banking Relationships” please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action.

DCMA Market Making

For “DCMA Market Making” please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action.

Research Analyst Conflicts

For updates on “Research Analyst Conflicts” please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action. The

principal research analysts who prepared this report have no financial interest in securities of the issuers covered in the report, are not (nor are any members of their household) an officer, director or advisory board member of the issuer(s) covered in the report, and are not aware of any material

relevant conflict of interest involving the analyst or DCMA, and did not receive any compensation from the issuer during the past 12 months except as

noted: no exceptions.

Research Analyst Certification

For updates on “Research Analyst Certification” and “Rating System” please visit BlueMatrix disclosure link at

https://daiwa3.bluematrix.com/sellside/Disclosures.action. The views about any and all of the subject securities and issuers expressed in this

Research Report accurately reflect the personal views of the research analyst(s) primarily responsible for this report (or the views of the firm

producing the report if no individual analysts[s] is named on the report); and no part of the compensation of such analyst(s) (or no part of the

compensation of the firm if no individual analyst[s)] is named on the report) was, is, or will be directly or indirectly related to the specific recommendations or views contained in this Research Report.

For stocks and sectors in Indonesia covered by Bahana Securities, the following rating system is in effect:

Stock ratings are based on absolute upside or downside, which is the difference between the target price and the current market price. Unless otherwise specified, these ratings are set with a 12-month horizon. It is possible that future price volatility may cause a temporary mismatch between upside/downside for a stock based on the market price and the formal rating. "Buy": the price of the security is expected to increase by 10% or more. "Hold": the price of the security is expected to range from an increase of less than 10% to a decline of less than 5%. "Reduce": the price of the security is expected to decline by 5% or more.

Sector ratings are based on fundamentals for the sector as a whole. Hence, a sector may be rated “Overweight” even though its constituent stocks are all rated “Reduce”; and a sector may be rated “Underweight” even though its constituent stocks are all rated “Buy”. “Overweight”: positive fundamentals for the sector. “Neutral”: neither positive nor negative fundamentals for the sector. “Underweight”: negative fundamentals for the sector.

Ownership of Securities For “Ownership of Securities” information, please visit BlueMatrix disclosure Link at https://daiwa3.bluematrix.com/sellside/Disclosures.action .

Investment Banking Relationships For “Investment Banking Relationship”, please visit BlueMatrix disclosure Link at https://daiwa3.bluematrix.com/sellside/Disclosures.action . Relevant Relationships (Bahana Securities) Bahana Securities may from time to time have an individual employed by or associated with it serves as an officer of any of the companies under its research coverage.

Bahana Securities market making Bahana Securities may from time to time make a market in securities covered by this research.

Additional information may be available upon request.

Japan - additional notification items pursuant to Article 37 of the Financial Instruments and Exchange Law

(This Notification is only applicable where report is distributed by Daiwa Securities Co. Ltd.)

If you decide to enter into a business arrangement with us based on the information described in materials presented along with this document, we ask you to pay close attention to the following items.

In addition to the purchase price of a financial instrument, we will collect a trading commission* for each transaction as agreed beforehand with you. Since

commissions may be included in the purchase price or may not be charged for certain transactions, we recommend that you confirm the commission for

each transaction.

In some cases, we may also charge a maximum of ¥ 2 million (including tax) per year as a standing proxy fee for our deposit of your securities, if you are

a non-resident of Japan.

For derivative and margin transactions etc., we may require collateral or margin requirements in accordance with an agreement made beforehand with

you. Ordinarily in such cases, the amount of the transaction will be in excess of the required collateral or margin requirements.

There is a risk that you will incur losses on your transactions due to changes in the market price of financial instruments based on fluctuations in interest

rates, exchange rates, stock prices, real estate prices, commodity prices, and others. In addition, depending on the content of the transaction, the loss

could exceed the amount of the collateral or margin requirements. There may be a difference between bid price etc. and ask price etc. of OTC derivatives handled by us.

Before engaging in any trading, please thoroughly confirm accounting and tax treatments regarding your trading in financial instruments with such experts

as certified public accountants.

*The amount of the trading commission cannot be stated here in advance because it will be determined between our company and you based on current

market conditions and the content of each transaction etc.

When making an actual transaction, please be sure to carefully read the materials presented to you prior to the execution of agreement, and to take responsibility for your own decisions regarding the signing of the agreement with us.

Corporate Name: Daiwa Securities Co. Ltd.

Financial instruments firm: chief of Kanto Local Finance Bureau (Kin-sho) No.108

Memberships: Japan Securities Dealers Association, Financial Futures Association of Japan

Japan Securities Investment Advisers Association

Type II Financial Instruments Firms Association

Related Documents