All rights reserved. Enterprise Products Partners L.P. Enterprise Products Partners L.P. Platts NGLs Conference September 23, 2013 Lynn Bourdon Group SVP www.enterpriseproducts.com

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

All rights reserved. Enterprise Products Partners L.P.

Enterprise Products Partners L.P.Platts NGLs Conference

September 23, 2013

Lynn BourdonGroup SVPwww.enterpriseproducts.com

All rights reserved. Enterprise Products Partners L.P. 2

Forward–Looking Statements

This presentation contains forward-looking statements based on the beliefs of the company,as well as assumptions made by, and information currently available to our managementteam. When used in this presentation, words such as “anticipate,” “project,” “expect,” “plan,”“seek,” “goal,” “estimate,” “forecast,” “intend,” “could,” “should,” “will,” “believe,” “may,”“potential” and similar expressions and statements regarding our plans and objectives forfuture operations, are intended to identify forward-looking statements.Although management believes that the expectations reflected in such forward-lookingstatements are reasonable, it can give no assurance that such expectations will prove to becorrect. You should not put undue reliance on any forward-looking statements, which speakonly as of their dates. Forward-looking statements are subject to risks and uncertainties thatmay cause actual results to differ materially from those expected, including insufficient cashfrom operations, adverse market conditions, governmental regulations, the possibility that taxor other costs or difficulties related thereto will be greater than expected, the impact ofcompetition and other risk factors discussed in our latest filings with the Securities andExchange Commission.All forward-looking statements attributable to Enterprise or any person acting on our behalfare expressly qualified in their entirety by the cautionary statements contained herein, in suchfilings and in our future periodic reports filed with the Securities and Exchange Commission.Except as required by law, we do not intend to update or revise our forward-lookingstatements, whether as a result of new information, future events or otherwise.

All rights reserved. Enterprise Products Partners L.P. 3

Topics

Shale Fundamentals

NGL Supply Potential

U.S. LPG Export Update

Ethane Fundamentals and A New Market?

On Purpose Polymer Production

Questions

All rights reserved. Enterprise Products Partners L.P. 4

Key Investment Considerations

One of the largest U.S. publicly traded energy partnerships with an enterprise value of more than $70 billion 64th on Fortune 500

Integrated midstream energy system serving producers and consumers of natural gas, natural gas liquids (NGLs), crude oil, petrochemicals and refined productsDiversified sources of cash flowVisibility to growth with approximately $8.0 billion of capital projects currently under constructionInvestor-friendly structure and history of successful execution

• No General Partner incentive distribution rights (IDRs) – lower cost of capital

• Top credit rated MLP – Baa1 / BBB+ • Raised distribution in each of the last 36 consecutive quarters• 7.1% distribution growth for 2Q13 vs. 2Q12• Significant insider ownership with management and affiliates

owning ≈38% of EPD units outstanding

All rights reserved. Enterprise Products Partners L.P. 5

EPD Portfolio of Integrated Assets

50,000 miles of natural gas, NGL, crude oil, refined products and petrochemical pipelines200 MMBbls of NGL, refined products and crude oil, and 14 Bcf of natural gas storage capacity24 natural gas processing plants

22 NGL & Propylene fractionators6 offshore hub platformsNGL import / export terminals (including LPG)Butane isomerization complex; octane enhancement facility; high-purity isobutylene facility

Major Asset Overview

All rights reserved. Enterprise Products Partners L.P. 6

0 500250Miles

Source: EPD Fundamentals; USGS Production 2008

Crude OilGas

Gas

EPD Pipelines

Existing North American Production

Shale Plays

Oil

Liquids (NGL & Products)

Existing Wells and Shale PlaysShales: Source Rock of Conventional Oil and Gas

Marcellus – 100 years

Utica – 80 years

Bakken / Williston – 35 years

Eagle Ford – 45 years

Mississippian – 40 years

Barnett – 30 yearsHaynesville / Bossier – 80 years

POTENTIAL YEARS OF DRILLING

All rights reserved. Enterprise Products Partners L.P. 7

Crude Oil and Natural Gas Prices Shale Brings a New Normal

Source: NYMEX

Historical Forecast

All rights reserved. Enterprise Products Partners L.P. 8

Plentiful Supply Available Below $5

Potential gas additions 2012 to 2025 (Bcfd)

Gas Price Required for 20% Before Income Tax (BFIT) ReturnsIncludes NGL Upgrade (if any)

2 to 4Bcf/d

2 to 5Bcf/d

1 to 3Bcf/d

2 to 5Bcf/d

1 to 2Bcf/d

4 to 5Bcf/d

1 to 3Bcf/d

2 to 3Bcf/d

5 to 11Bcf/d

1 to 2Bcf/d

2 to 3Bcf/d

1 to 4Bcf/d

Source: EPD Fundamentals

Potential Gas Additions – 25 to 50 Bcf/d by 2025

All rights reserved. Enterprise Products Partners L.P. 9

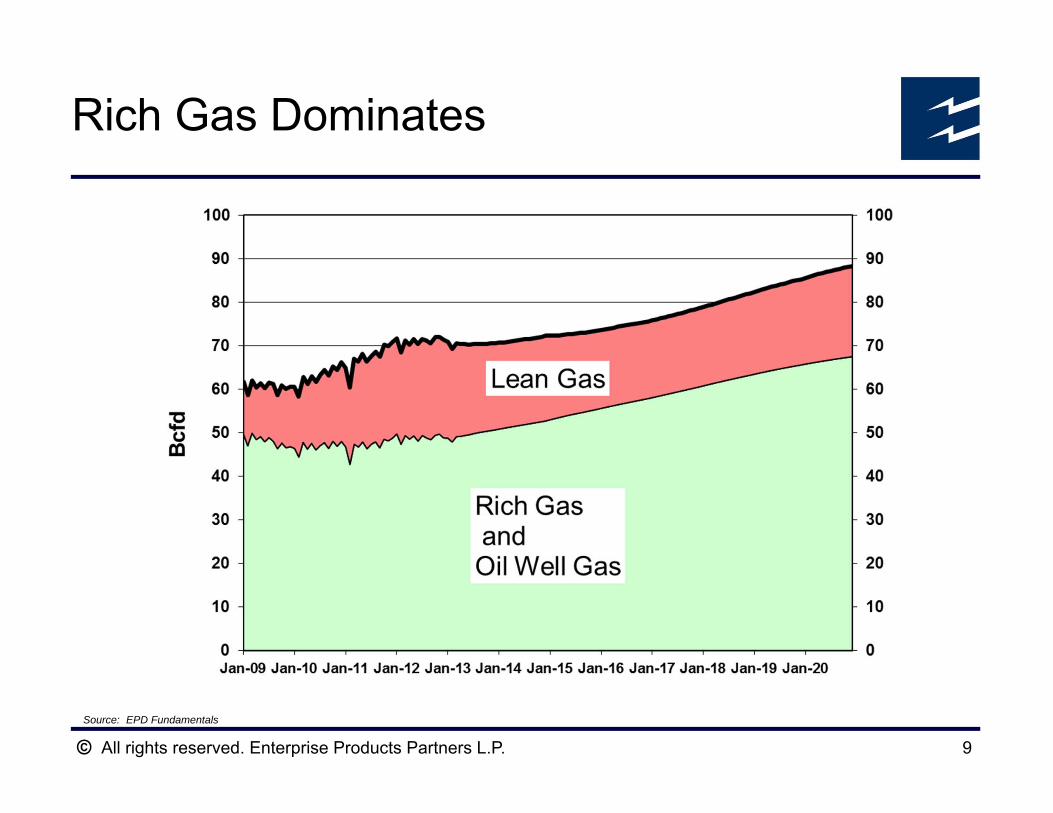

Rich Gas Dominates

Source: EPD Fundamentals

All rights reserved. Enterprise Products Partners L.P. 10

Producer NGL UpliftUsing 12 Month Strip

Source: EPD Fundamentals and NYMEX; as of September 2013

All rights reserved. Enterprise Products Partners L.P. 11

NG Demand Growth Next 5–7 YearsPower Generation, Industrial and Exports

GulfEG1.0

SEEG1.0

NEEG1.0MW

EG2.0

WestEG1.0

INDUST.2.0–4.0

Export6.0

RC0.7–1.5

Oil Sands(Demand)

1.0–1.5

Power Generation* 4.0–7.0

Industrial / Chems 2.0–4.0

NGVs 0.5–1.5

LNG Exports 4.0–6.0

R/C Conversion 0.5–1.5

Potential (Bcf/d) 11–20* Depends on emission and CO2 rulesSources: EIA and EPD Fundamentals

All rights reserved. Enterprise Products Partners L.P. 12

ROCKIES

PERMIAN

MID-CONTINENT

APPALACHIAN

GULF COAST

OTHER

131

902

694

975

8394966

Total Mbd 1425

2013-2015 Growth

2015-2020 Growth

April 2013 Actual

U.S. NGL Supply PotentialAssuming Sufficient Markets

MBbls/d

MBD

Source: EPD Fundamentals

All rights reserved. Enterprise Products Partners L.P. 13

NGLs – U.S. Demand Matrix

NGL Ethane PropaneNormal Butane Iso-Butane

Natural Gasoline

Percent of NGL BBL 40% 30% 8% 10% 12%

Petrochemicals

Heating, Crop Drying, Fuels

Motor Fuels

Export

Source: EPD Fundamentals

All rights reserved. Enterprise Products Partners L.P. 14

Export Opportunity Matrix

C1Boiling Point:

-258.7

C2BP: -127.5

C3BP: -44.0 C4

BP: 31.0

C5+BP: 97.0

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Dis

coun

t to

NW

E

Ease of Transport

Harder EasierLow

High

Arb

itrag

e Va

lue

Source: EPD Fundamentals

All rights reserved. Enterprise Products Partners L.P. 15

Propane and Butane Daily Balances

Exports will continue to be the balancing factor for LPGsSource: EPD Fundamentals

Demand Low CasePropane Butanes

Incremental Supply Potential 573 354 Less: PDH 60

Incremental Exports 375 50 Incremental Cracker / Refining Demand 100

Add: Cracker Conversion To Ethane 100

Excess Supply Potential MBbl/d 238 204

Demand High CasePropane Butanes

Incremental Supply Potential 573 354 Less: PDH 120

Incremental Exports 450 150 Incremental Cracker / Refining Demand 150

Add: Cracker Conversion To Ethane 100

Excess Supply Potential MBbl/d 103 54

(MBbls/d)

(MBbls/d)

All rights reserved. Enterprise Products Partners L.P. 16

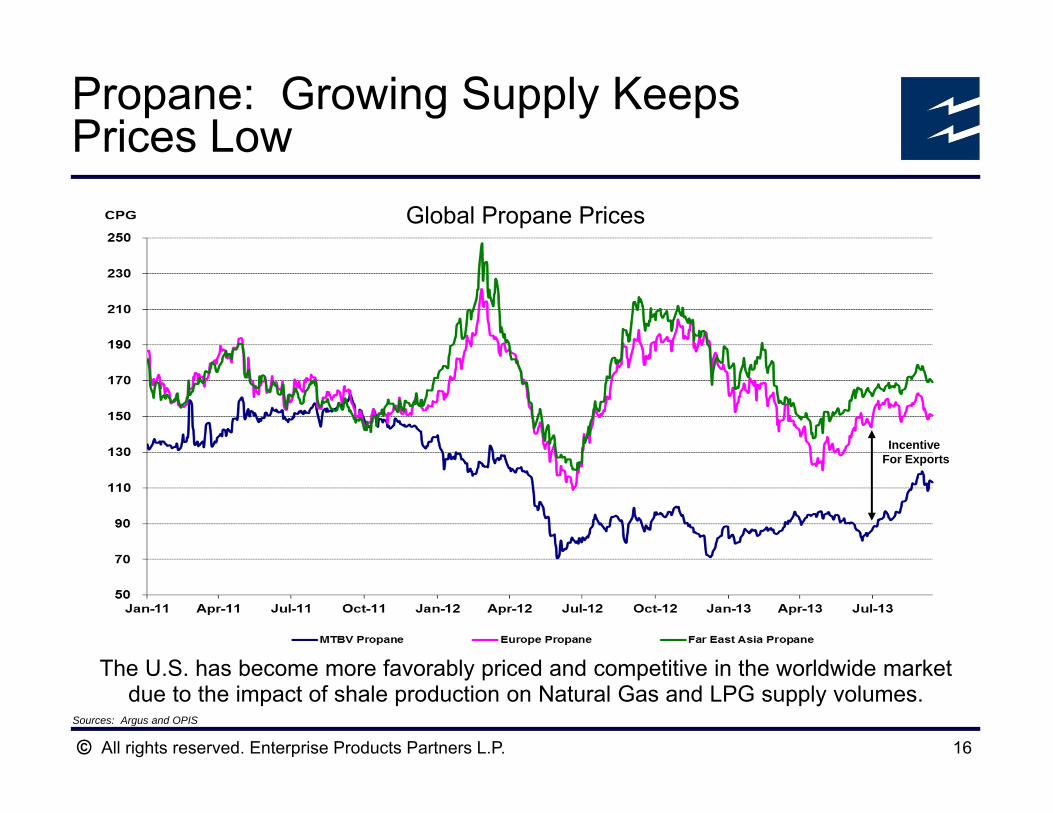

Propane: Growing Supply Keeps Prices Low

Sources: Argus and OPIS

The U.S. has become more favorably priced and competitive in the worldwide market due to the impact of shale production on Natural Gas and LPG supply volumes.

Incentive For Exports

Global Propane Prices

All rights reserved. Enterprise Products Partners L.P. 17

0

10

20

30

40

50

60

70

80

Qatar U.S.A. Saudi Arabia U.A.E. Norway Algeria Kuwait Venezuela Nigeria

Milli

on B

arre

ls

EPD Others

Led by Enterprise’s Loadings, the U.S. is Now the Top Propane Exporter…

Top Propane Exporters 2013 YTD

Source: Waterborne

20132012 2013201220132012

All rights reserved. Enterprise Products Partners L.P. 18

-

10

20

30

40

50

60

70

80

90

100

110

120

130

Qatar U.S.A. Saudi Arabia U.A.E. Norway Algeria Kuwait Venezuela Nigeria

Mill

ion

Bar

rels

Butane Propane

…However U.S. Butane Exports Have Lagged Behind, But Not For Long

Top LPG Exporters 2013 YTD

Source: Waterborne

20132012 20132012

All rights reserved. Enterprise Products Partners L.P. 19

EPD’s LPG Export SystemThe World Class Facility Continues to Grow

EPD has 655 MBPD of fractionation capacity that can produce LE propane

Pipeline interconnectivity provides access to additional supply

Multiple high rate propane wells that can deliver at 10,000 BPH each

Integrated pipeline system that is dedicated to the delivery of propane and butane to docks for export

Export capacity expansion is completePropane: 13,500 BPH

Butane: 12,000 BPH

EPD has the ability to load LPG vessels at multiple docks

EPD terminal has been in this business for 30 years and has unloaded / loaded over 397 MMBbls of LPG (over 3,000 Loads)

Evaluating further enhancements

All rights reserved. Enterprise Products Partners L.P. 20

The Importance of ExportsCritical in Maintaining NGL Production

20

40

60

80

100

120

140

Jan Feb Mar Apr May Jun Jul Aug Sept Oct Nov Dec

MMBPropane Inventory Forecast

(excludes Propylene)

Min 2000-11 2012 2012 Inventory if Exports excludedRange 2005–2011

Without exports, inventory overhang likely devastating to rig counts

Normal Range2012 Inventories

2012 Inventories without Exports!

Sources: EPD Fundamentals and EIA

All rights reserved. Enterprise Products Partners L.P. 21

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2013 2014 2015 2016 2017 2018 2019 2020

MB

PD

Supply Forcast Cracker Demand Non Waterborne Export Demand

Ethane Supply / Demand PictureLooking for a New Market

Available for Export

Source: EPD Fundamentals

All rights reserved. Enterprise Products Partners L.P. 22

0

10

20

30

40

50

60

70

U.S. (Ethane) U.S. (Naphtha) W. Europe(Naphtha)

Far East Asia(Naphtha)

Oct-2005 Current

U.S. Ethylene Crackers: Significant Global Cost Advantage

Using an average ethylene plant (≈1.5 billion lbs. per year), a 40 cent per lb. margin advantage is

≈$700MM per year incremental margin for a single plant!

Sources: IHS and EPD Fundamentals

U.S

. Cen

ts P

er P

ound

All rights reserved. Enterprise Products Partners L.P. 23

Ethane (MTBV)

Naphtha (NWE)

cpg 25 250

Ethylene Costs (Dollars per pound) $.08 $.48

Savings of $700 Million per YearTotal NWE Ethylene Capacity:

23.7 MM mt/year

Converting 1/3 of NWE operating capacity to ethane feed equals 415 MBPD of ethane demandSource: EPD Fundamentals

NWE is a Prime Opportunity for a New Ethane Outlet

All rights reserved. Enterprise Products Partners L.P. 24

Changing to an Ethane Feedstock Has a Dramatic Impact on Co-Product Supply

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Propylene Crude C4s Pyrolysis Gas

Poun

d Yi

eld

per P

ound

Eth

ylen

e

Naphtha Ethane

Converting a 1.5 Billion Lb/year naphtha cracker to ethane reduces propylene production by 740 Million Lbs/year and butane production by 390 Million Lbs/year

Source: IHS CMAI

All rights reserved. Enterprise Products Partners L.P. 25

On Purpose Propylene Production is Expected to Fill the Gap

Source: IHS CMAI

0

5

10

15

20

25

30

35

40

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Million Po

unds

Stm. Cracker Production FCC Splitters Imports Total Demand

PDH GapEconomic Recession

All rights reserved. Enterprise Products Partners L.P. 26

Summary

Shale resources are significant and long termEven with projected robust gas demand growth there is still 25 Bcf/d of gas supply “on the shelf” at low prices U.S. LPG exports will continue to serve as a viable balancing mechanism for U.S. supply and demandEurope and Asia appear to be new markets for U.S. Ethane Global naphtha crackers cannot ignore the U.S. ethane cost advantage

All rights reserved. Enterprise Products Partners L.P. 27

Thank you!

Questions?

Related Documents