ESCAP/OHRLLS/ECE/Government of Lao PDR Final Regional Review of the Almaty Programme of Action Almaty Programme of Action 5‐7 March 2013, Vientiane, Lao PDR ENHANCING THE SHARE OF LLDCs IN GLOBAL TRADE FLOWS AND TRADE FACILITATION GLOBAL TRADE FLOWS AND TRADE FACILITATION (Priority 3 of APoA) Dr Mia Mikic Chief, Trade Policy and Analysis Section Trade and Investment Division

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ESCAP/OHRLLS/ECE/Government of Lao PDR Final Regional Review of the Almaty Programme of ActionAlmaty Programme of Action5‐7 March 2013, Vientiane, Lao PDR

ENHANCING THE SHARE OF LLDCs IN GLOBAL TRADE FLOWS AND TRADE FACILITATIONGLOBAL TRADE FLOWS AND TRADE FACILITATION

(Priority 3 of APoA)

Dr Mia MikicChief, Trade Policy and Analysis SectionTrade and Investment Division

Important messages

• The WTO accession need to be kept high on the agenda for the LLDCs still not members of the WTOthe LLDCs still not members of the WTO

• Continuing efforts should be put towards regional integration and intraregional trade including through APTAand intraregional trade, including through APTA

• Aid for Trade (AfT) initiative could be more effectively used in design of adequate policies and measuresdesign of adequate policies and measures

• The LLDCs should be actively involved in implementing the ESCAP resolution 68/3 on enabling paperless trade/ g p p

• The LLDCs are encouraged to fully utilize the tools to enhance trade facilitation and improve trade policy developed by international organizations (e.g., some tools developed by UNNExT, ESCAP)

2

Presentation structure

d d d l1. Recent trends and developments in trade of Asian LLDCs

2. Progress made in Priority 3 of APoA

3. ESCAP’s contribution

4. Key recommendations

3

RECENT TRENDS AND DEVELOPMENTS IN C S O S

TRADE OF ASIAN LLDCS

4

Partial export recovery for LLDCs

• Persistent trade surplus of

p y

• Persistent trade surplus of Asian LLDCs was driven by exports of naturalexports of natural resources

• Exports were seriously hit by the 2008 global economic crisis

• Only partial export• Only partial export recovery in 2010 (no data for 2011 for larger LLDCs)for 2011 for larger LLDCs)

5

Stark difference in export

• Exports are highly

and import structure• Imports are• Exports are highly

concentrated• Imports are

diversified

6

Exports’ recovery hindered by export direction

• LLDCs’ exports mainlyLLDCs exports mainly flow to ROW– Exports to– Exports to developing AP were about 30% (2010)about 30% (2010)

• Intraregional imports i t twere important

– Almost 60% of imports came from the region

7

Trade in services structureTrade in services ‐ structure

8

PROGRESS MADE IN PRIORITY 3 OF APOAOG SS O 3 O O

9

Progress on specific actionsProgress on specific actions

1) WTO i1) WTO accession

2) Market access2) Market access

3) Trade facilitation)

10

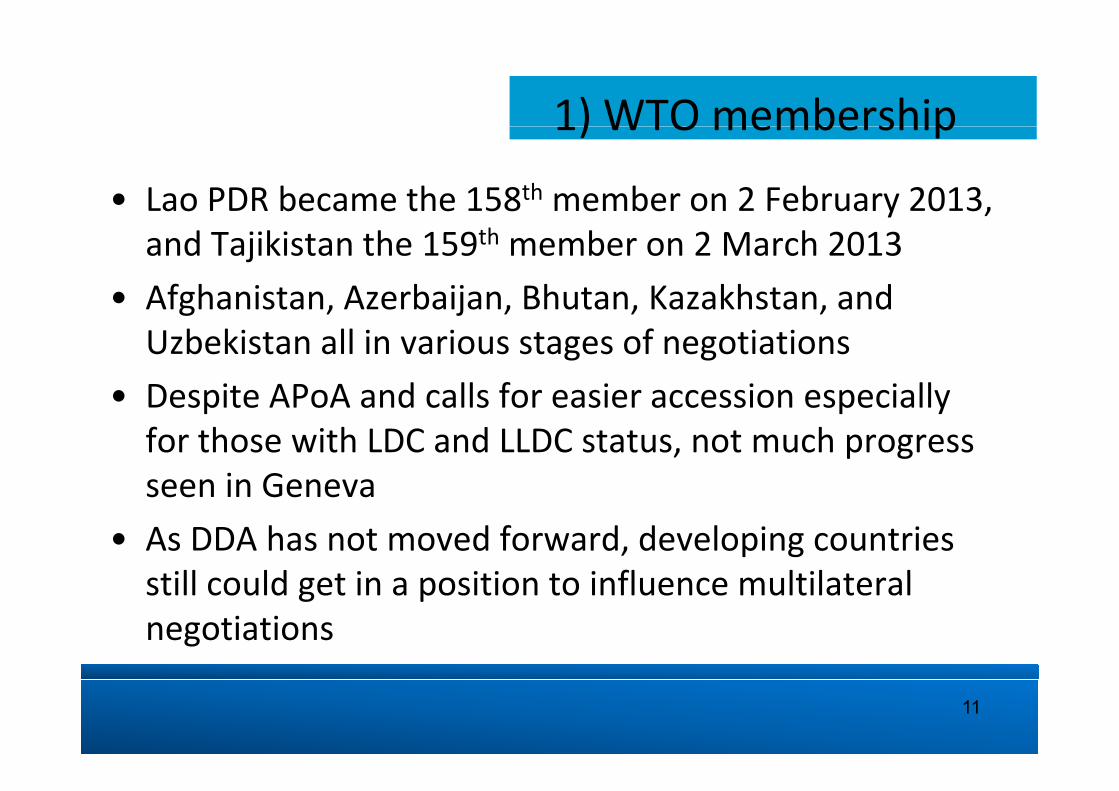

1) WTO membership1) WTO membership

• Lao PDR became the 158th member on 2 February 2013, y ,and Tajikistan the 159th member on 2 March 2013

• Afghanistan, Azerbaijan, Bhutan, Kazakhstan, andAfghanistan, Azerbaijan, Bhutan, Kazakhstan, and Uzbekistan all in various stages of negotiations

• Despite APoA and calls for easier accession especially• Despite APoA and calls for easier accession especially for those with LDC and LLDC status, not much progress seen in Genevaseen in Geneva

• As DDA has not moved forward, developing countries till ld t i iti t i fl ltil t lstill could get in a position to influence multilateral negotiations

11

2) Market access: MLT system2) Market access: MLT system

Proportion of e portsProportion of exports of all products (except arms) into developed country p ymarkets under zero duty

12

Market access: preferential trade agreementsp gEconomy Agreement in force Trade coverage in percent, average

2008‐2010

Export Import

Afghanistan 4 81.00 51.24

Armenia* 9 27 20 32 03Armenia* 9 27.20 32.03

Azerbaijan 10 8.63 45.89

Bhutan 3 94.90 77.24

Kazakhstan 11 19.64 44.09

Kyrgyzstan* 11 46.98 56.78

Lao PDR* 10 72.90 89.45

Mongolia* 0 0 0.00

Nepal* 3 57 48 56 46Nepal* 3 57.48 56.46

Tajikistan* 9 42.72 45.42

Turkmenistan 7 15.37 40.08

Uzbekistan 10 54.25 46.87Note:* denotes WTO members

13

Better market access, but supply side ‐ export diversification is too weak

9000

7000

8000

9000

5000

6000

7000

rt P

rodu

cts

3000

4000

5000

. of 8

-Dig

it Ex

por

1000

2000

3000

No.

0

1000

China

India

Thail

and

ng, C

hina

Malays

iand

ones

iaSing

apor

ehil

ippine

sViet

nam

Pakist

anSri L

anka

nglad

esh

Nepal

Cambo

diaMon

golia

Lao P

DRgh

anist

anw G

uinea Fiji

Maldive

sall

Islan

dsVan

uatu

Kiribati

Bhutan

Samoa

Tong

aon

Islan

dsMicr

ones

iaPala

u

THon

g Kon

g M Ind SinPhi V P SrBan

g

Ca M LaAfgh

Papua

New M

Marsh

all V

Solomon Mic

CountrySource: ARTNeT Policy Brief 19, 2009

14

3) Progress in trade facilitation (time to export)

80

90

10020062012

60

70

30

40

50

0

10

20

0

15

LLDCs trade costs up to 7 times higher p gthan other developing countries

Comprehensive trade costs (CTC) between selected economies and the USA

*Source: ESCAP Trade Cost Database (Ver.2, 2011)Note: NT‐CTC: CTC excluding tariff costs

Source: World Bank, LPI 2012, No data on Turkmenistan 16

Capacity to trade still underdevelopedp y p

N l

Logistics Performance Index (LPI) Score

Tajikistan

Mongolia

Nepal

Kyrgyz Republic

Afghanistan

j

Lao PDR

Azerbaijan

Uzbekistan

Armenia

Bhutan

Lao PDR

Si

Hong Kong, China

Kazakhstan

Source: World Bank, LPI 2012, No data for Turkmenistan0 1 2 3 4 5

Singapore

17

Trade‐related servicesCountries Enabling Trade Index (ETI) Getting Credit

Availability and quality of Global ranking Global ranking transport service

(score, 1‐7) (out of 132) (out of 185)

Afghanistan ‐ ‐ 154Afghanistan 154

Armenia 3.77 62 40

Azerbaijan 3.86 53 53

Bhutan ‐ ‐ 129

Kazakhstan 3.84 57 83

K t 2 99 110 12Kyrgyzstan 2.99 110 12

Lao PDR ‐ ‐ 167

Mongolia 2.96 112 53g

Nepal 2.72 124 70

Tajikistan 3.35 90 180

18Turkmenistan ‐ ‐ ‐

Uzbekistan ‐ ‐ 154 18

ESCAP’s contributionSC s co t but o

19

ESCAP TA to LLDCs in trade and trade facilitation

Gaps of ESCAP

National Level

Gaps of LLDCs Support areas mechanisms

P li ki1) Lack of

h d Policy‐makingProgramme implementationStakeholder coordination

human and financial resources

2) L k f Subregional LevelNetworkingKnowledge‐sharing

2) Lack of technical and institutional

it

Regional level

Transit cooperation

Net orking

capacity 3) Lack of

political and li Networking

Knowledge‐sharingRegional integration

policy support

20

ESCAP TA for PTA negotiations, trade and investment reforms and business development

• Preparation of the negotiation mandate– Audit of domestic regulation– Setting consultative and coordinating processes

• Inputs for formulation of negotiation strategies and• Inputs for formulation of negotiation strategies and positionsImpact assessment• Impact assessment

• Capacity building for all aspects of negotiations

21

UN Network of Experts for Paperless Trade in Asia and the Pacific (UNNExT)

Partnership

22

Asia‐Pacific Trade Agreement (APTA)

MAIN FEATURESMAIN FEATURES• The only REGION‐WIDE trading

agreement• Significant market potential

SAFTA AFTASAFTA AFTA• Significant market potential OPEN to all developing countries

• BRIDGE to other RTAs• It WORKS simple and

APTA

AFTA

APTA

AFTA

• It WORKS ‐ simple and operational rules of origin allow utilization of preferences

• Margin of preferences locked to

ECOTA PICTAECOTA PICTA

• Margin of preferences locked to MFN so NO deterioration of preferences

• Ever EVOLVING

Extending into new areas of integration:

Trade facilitationdTrade in services

Investment Non‐tariff barriers

23

Some key recommendations to further t d d t d f ilit ti

• The WTO accession need to be kept high on the agenda for the ill b f h

trade and trade facilitation

LLDCs still not members of the WTO• Continuing efforts should be put towards regional integration

and intraregional tradeand intraregional trade • Aid for Trade (AfT) initiative could be more effectively used in

design of adequate policies and measuresdesign of adequate policies and measures• The LLDCs should be actively involved in implementing the

ESCAP resolution 68/3 on enabling paperless tradeESCAP resolution 68/3 on enabling paperless trade• The LLDCs are encouraged to fully utilize the tools to enhance

trade facilitation and improve trade policy developed by p p y p yinternational organizations (e.g., some tools developed by UNNExT, ESCAP)

24

In summary

• Potential for integration of LLDCs into expanded South –h d d i h ld b d i b li i dSouth trade and investment should be driven by policies and

action tos pport incl si e and s stainable de elopment especiall– support inclusive and sustainable development especiallyfor agriculture and services

– improve transfer of technology– improve transfer of technology– reduce trade costsenhancemarket access– enhancemarket access

– utilize aid, especially Aid for Trade, effectivelyfacilitate movement of people between the countries and– facilitate movement of people between the countries andsubregions (tourism, education, temporary work, etc).

25

THANK YOU

Please visit for more details:www.unescap.org

www unescap org/tidwww.unescap.org/tid

www.unescap.org/unnext

www.artnetontrade.org

26

Related Documents