1 Engineering A Venture Capital Market: The Case of China Dr. Lin Lin ∗ Assistant Professor Faculty of Law National University of Singapore Email address: [email protected] Office Tel: (65) 6516 3576 Office Fax: (65) 6779 0979 Office Address: Faculty of Law, National University of Singapore, Federal Building #02-09, 469G Bukit Timah Road, Singapore 259776 Abstract Replicating the American experience in the creation of a venture capital market brings up the “simultaneity problem” as coined by Professor Ronald Gilson – three central inputs must be simultaneously available: (1) entrepreneurs, (2) providers of capital with the appetite for high-risk, high-return investments, and (3) specialized financial intermediaries which serve as the nexus of a set of sophisticated contracts. China now ranks second in the world, after only the U.S., in terms of venture capital investments received annually. This article examines how China has addressed the simultaneity problem in creating one of the fastest developing and largest engineered venture capital markets in the world within three decades. Based on quantitative, qualitative and hand-collected data and extensive interviews, this article finds that the Chinese government has helped solve the simultaneity problem with a degree of success and that this has been done mainly through laws and government policies, including: (1) providing public capital through various government programs and increasing private capital through the easing of ∗ Assistant Professor, Faculty of Law, National University of Singapore (NUS). This article was selected as one of ten invited papers for the 8th Stanford International Junior Faculty Forum 2015. Helpful comments on earlier drafts of this article were received from Prof. Yu Zhongxing, Prof. Anupam Chander, Prof. Nora Freeman Engstrom, Prof. Tan Yock Lin, Prof. Hans Tjio, Prof. Dan Puchniak, Prof. Umakanth Varottil, Prof. Wee Meng Seng, Prof. Qiao Shitong, Mr. Zhong Xing, Ms. Hu Ying, Mr. Florian Gamper, and participants of the 8th Stanford International Junior Faculty Forum 2015, the 12th Annual Asian Law Institute (ASLI) Conference 2015, the 15 th International Symposium of Commercial Law 2015, the Center for Banking and Financial Law Working-papers Series, the Finnish Chinese Law Center Guest Lecture, the National Taiwan University Law School Guest Lecture and the East Asia Institute of NUS Public Lecture. I also thank interviewees from China and Singapore, who generously shared their knowledge and insights with me. Interviews were conducted on an anonymous background basis. This research was generously supported by the Center for Banking & Finance Law and the Center of Law and Business at the Faculty of Law, National University of Singapore. All errors remain my own. Email: [email protected]

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Engineering A Venture Capital Market: The Case of China

Dr. Lin Lin∗

Assistant Professor Faculty of Law

National University of Singapore

Email address: [email protected] Office Tel: (65) 6516 3576 Office Fax: (65) 6779 0979

Office Address: Faculty of Law, National University of Singapore, Federal Building #02-09, 469G Bukit Timah Road, Singapore 259776

Abstract Replicating the American experience in the creation of a venture capital market brings up the “simultaneity problem” as coined by Professor Ronald Gilson – three central inputs must be simultaneously available: (1) entrepreneurs, (2) providers of capital with the appetite for high-risk, high-return investments, and (3) specialized financial intermediaries which serve as the nexus of a set of sophisticated contracts. China now ranks second in the world, after only the U.S., in terms of venture capital investments received annually. This article examines how China has addressed the simultaneity problem in creating one of the fastest developing and largest engineered venture capital markets in the world within three decades. Based on quantitative, qualitative and hand-collected data and extensive interviews, this article finds that the Chinese government has helped solve the simultaneity problem with a degree of success and that this has been done mainly through laws and government policies, including: (1) providing public capital through various government programs and increasing private capital through the easing of

∗ Assistant Professor, Faculty of Law, National University of Singapore (NUS). This article was selected as one of ten invited papers for the 8th Stanford International Junior Faculty Forum 2015. Helpful comments on earlier drafts of this article were received from Prof. Yu Zhongxing, Prof. Anupam Chander, Prof. Nora Freeman Engstrom, Prof. Tan Yock Lin, Prof. Hans Tjio, Prof. Dan Puchniak, Prof. Umakanth Varottil, Prof. Wee Meng Seng, Prof. Qiao Shitong, Mr. Zhong Xing, Ms. Hu Ying, Mr. Florian Gamper, and participants of the 8th Stanford International Junior Faculty Forum 2015, the 12th Annual Asian Law Institute (ASLI) Conference 2015, the 15th International Symposium of Commercial Law 2015, the Center for Banking and Financial Law Working-papers Series, the Finnish Chinese Law Center Guest Lecture, the National Taiwan University Law School Guest Lecture and the East Asia Institute of NUS Public Lecture. I also thank interviewees from China and Singapore, who generously shared their knowledge and insights with me. Interviews were conducted on an anonymous background basis. This research was generously supported by the Center for Banking & Finance Law and the Center of Law and Business at the Faculty of Law, National University of Singapore. All errors remain my own. Email: [email protected]

2

regulatory barriers towards institutional investors; (2) enhancing the availability of financial intermediaries through introducing a new and popular business vehicle – the limited partnership – for venture capital fund raising; and (3) encouraging entrepreneurship and facilitating the setting up and doing of business through revising the country’s tax, corporate and securities laws. This finding reinforces Gilson’s theory by proving that a government can help solve the simultaneity problem of engineering a venture capital market. Concurrently, this article seeks to show that although China’s venture capital market is established and led by the government, a key reason for its relative success is the central government’s efforts at adopting a more market-oriented approach towards capital allocation. The Chinese central government has sought to facilitate the availability of the three essential factors and to provide the necessary legislative and institutional infrastructure while ensuring that it does not exert direct control over the venture capital market. This approach is reflected in: (1) the changing role of the central government – from a direct financial intermediary that decides how exactly capital is to be allocated to a mere facilitator and provider of capital; (2) the evolving regulatory regime governing venture capital; (3) the increased role of private capital; (4) the predominance of private limited partnership-type venture capital funds; and (5) the increased number of private venture capital firms, startups and entrepreneurs. Nonetheless, to realize the industry’s full potential, there is still room for improvement in various social, legal, and economic areas.

3

Table of Contents I. Introduction ......................................................................................................................... 4 II. The Venture Capital Market with Chinese Characteristics ................................................. 8

A. The Concept of “Venture Capital” in the Chinese Context ............................................ 8 B. The Need for Venture Capital in China .......................................................................... 9

1. Satisfying Demand for Capital .................................................................................. 10 2. Re-charting Economic Development ........................................................................ 11

C. The Evolution of China’s Venture Capital Market and the Evolving Role of the Government .......................................................................................................................... 11

1. Emerging Phase (1985-1990) ................................................................................... 11 2. Experimentation Phase (1991-2000) ......................................................................... 12 3. Decline and Subsequent Growth (2001-2005) .......................................................... 12 4. Deepening Structural Reforms (2006- 2013) ............................................................ 13 5. Towards a More Market-Oriented System (2014-present) ....................................... 14

III. Engineering Problems in China ......................................................................................... 16 A. Capital ........................................................................................................................... 16

1. Public Capital ............................................................................................................ 16 2. Private Capital ........................................................................................................... 24

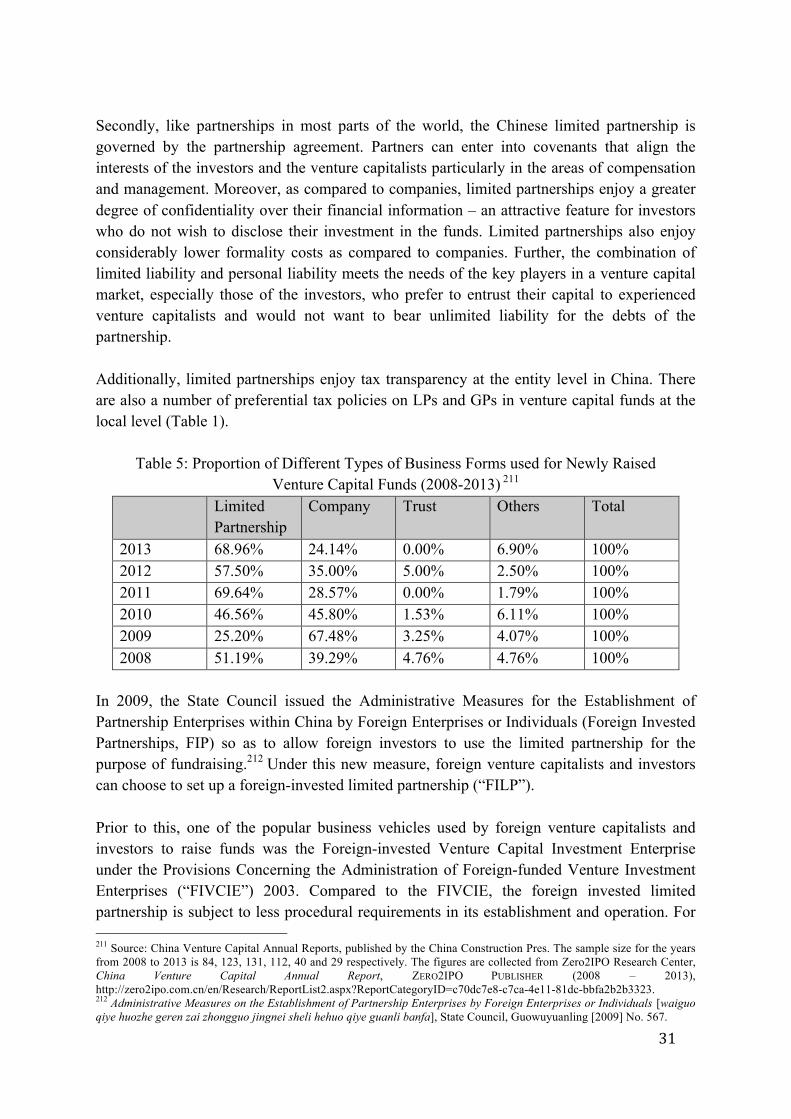

B. Financial Intermediaries ............................................................................................... 28 1. Adoption of the Limited Partnership: A Venture Capital Oriented Business Vehicle 30 2. Special Features of the Chinese Limited Partnership ............................................... 32 3. Concluding Remarks ................................................................................................. 36

C. Entrepreneurs ................................................................................................................ 37 1. Strengthening Entrepreneurship by Policies and Tax Reliefs ................................... 37 2. Entrepreneur-friendly Company Law Reforms ........................................................ 38 3. Concluding Remarks ................................................................................................. 40

IV. The Role of Law and Government .................................................................................... 40 V. Conclusion ......................................................................................................................... 44

4

I. Introduction Venture capital, which is the provision of financial capital to early-stage, high-potential, and high-growth entrepreneurial enterprises and technology companies, has been widely recognized as a powerful engine for a nation’s innovation, job creation, knowledge economy, and macroeconomic growth.1 There is a sizable body of research literature emphasizing the significant role of the venture capital market in commercializing cutting-edge science and linking finance and innovation.2 Empirical findings also confirm that equity financing in the form of venture capital, instead of debt financing, is predominant in high-tech industries.3 In light of the potential benefits of venture capital, the engineering of a venture capital market is of interest to the governments of many countries. According to Gilson, a leading scholar in the field of venture capital research, three key factors must be simultaneously present for a venture capital market to thrive: (1) providers of capital with the appetite for high-risk, high-return investments; (2) specialized financial intermediaries which properly incentivize all participants in the venture capital market; and (3) entrepreneurs.4 The key challenge for governments seeking to engineer a venture capital market is in ensuring the simultaneous availability of these factors – a venture capital market will not succeed if any factor is absent (the ‘simultaneity problem’). Of course, the engineering of a venture capital market is highly specific to the context of each country. Law and finance literature has discussed many other factors that contribute to the flourishing of a national venture capital market.5 These include real economic growth,6 sound macroeconomic policies, political stability, a conducive legal environment, strong investor protection,7 a large domestic market with investors willing to take risks with younger firms,8 liberal bankruptcy laws,9 tax incentives that accommodate the establishment of venture

1 Ronald J. Gilson, Engineering a Venture Capital Market: Lessons from the American Experience, 55 STAN. L. REV. 1067, 1068 (2003). See generally on the importance of venture capital, Marco Da Rin et al., The Law and Finance of Venture Capital Financing in Europe: Findings from the RICAFE Research Project, 7(2) EBOR 525 (2006); Brigitte Haar, Impressions of the First RICAFE Conference: Risk Capital and the Financing of European Innovative Firms, 5(1) EUROPEAN BUSINESS ORGANIZATION LAW REVIEW 201 (2004). 2 Gilson, supra note 1, at 1068. 3 John Freear & William E. Wetzel, Who Bankrolls High-Tech Entrepreneurs?, 5(2) JOURNAL OF BUSINESS VENTURING 77 (1990); Robert E. Carpenter & Bruce C. Petersen, Capital Market Imperfections, High-tech Investment, and New Equity Financing, 112(477) THE ECONOMIC JOURNAL F54 (2002); cited in John Armour & Douglas Cumming, The Legislative Road to Silicon Valley, 58 OXFORD ECONOMIC PAPERS 598 (2006). 4 Gilson, supra note 1, at 1076-1078, 1093. 5 Armour & Cumming, supra note 3. 6 Armour & Cumming, supra note 3, at subsection 5.2. 7 Id., at 597. (Armour and Cumming’s empirical findings show that the ‘investor friendliness’ of a country’s legal and fiscal environment is a significant determinant of the supply of venture capital investment to entrepreneurial firms). 8 JOSH LERNER, BOULEVARD OF BROKEN DREAMS: WHY PUBLIC EFFORTS TO BOOST ENTREPRENEURSHIP AND VENTURE CAPITAL HAVE FAILED--AND WHAT TO DO ABOUT IT (2009), at 181-182. 9 Id., (arguing that a more liberal personal bankruptcy law stimulates demand for venture capital finance). However, as there is no personal bankruptcy law in China, this article will not address this issue in the context of China.

5

capital funds,10 an investor-friendly environment,11 a strong stock market12, and a culture of entrepreneurship.13 Efforts at engineering a venture capital market have been made by governments in many countries. A body of literature notes that government intervention has profoundly shaped the venture capital industries of countries such as Israel,14 Chile,15 Taiwan16 and Singapore.17 However, Lerner18 argues that government programs have generally not been very successful. Gilson asserts that the “U.S. venture capital market developed organically, largely without government assistance and certainly without government design.”19 He attributes the success of the U.S. venture capital market to private ordering.20 The “idiosyncratic” history of the U.S. venture capital market had encouraged the simultaneous emergence of a body of entrepreneurs, investors, and the right vehicles which served as the “nexus of a set of sophisticated contracts”.21 China offers a fascinating case study of how a national venture capital market can be engineered – its venture capital market is one of the fastest developing and largest engineered venture capital markets in the world.22 Before 1985, venture capital did not exist in China.23 After three decades of development, China now receives the second greatest amount of venture capital investment in the world, ranking only after the U.S.24 In 2015, 597 new venture capital funds were set up in China, raising more than USD 30 billion of fresh capital

10 Christian Keuschnigg & Soren Bo Nielsen, Startups, Venture Capitalists, and the Capital Gains Tax, 88(5) JOURNAL OF PUBLIC ECONOMICS 1011 (2004); Christian Keuschnigg & Soren Bo Nielsen, Tax Policy, Venture Capital, and Entrepreneurship, 87(1) JOURNAL OF PUBLIC ECONOMICS 175 (2003). Armour & Cumming, supra note 3, at section 4. 11 EUROPEAN VENTURE CAPITAL ASSOCIATION, BENCHMARKING EUROPEAN TAX AND LEGAL ENVIRONMENTS, EVCA, ZAVENTUM (2006); Cited in Armour & Cumming, supra note 3, at 600. 12 Bernard S. Black & Ronald J. Gilson, Does Venture Capital Require an Active Stock Market?, 11(4) JOURNAL OF APPLIED CORPORATE FINANCE 36 (1999); Edward B. Rock, Greenhorns, Yankees and Cosmopolitans: Venture Capital, IPOs, Foreign Firms, and US Markets, 2(2) THEORETICAL INQUIRIES IN LAW 711 (2001); Paul Gompers & Josh Lerner, The Venture Capital Revolution, 15(2) JOURNAL OF ECONOMIC PERSPECTIVES 145 (2001). Colin Mayer, Koen Schoors & Yishay Yafeh, Sources of Funds and Investment Activities of Venture Capital Funds: Evidence from Germany, Israel, Japan and the UK, 11(3) JOURNAL OF CORPORATE FINANCE 586 (2005). The author addresses the correlation between the stock market and the venture capital market in a separate article titled Venture Capital and the Structure of Stock Market: Lessons from China, ASIAN JOURNAL OF COMPARATIVE LAW (forthcoming). 13 Marc-Oliver Fiedler & Thomas Hellmann, Against All Odds: The Late but Rapid Development of the German Venture Capital Industry, 4(4) THE JOURNAL OF PRIVATE EQUITY 31, 37 (2001) (noting the importance of culture in general venture capital market). 14 Id. See also Gilson, supra note 1, at 1068; LERNER, supra note 8, at 42. 15 Gilson, supra note 1, at 1068; LERNER, supra note 8, at 42. 16 Christopher John Gulinello, Engineering a Venture Capital Market and the Effects of Government Control on Private Ordering: Lessons from the Taiwan Experience, 37(4) GEORGE. WASH. INT. LAW. REV 845 (2005). 17 LERNER, supra note 8, at 42. 18 LERNER, supra note 8, at 192. 19 See Gilson, supra note 1, at 1070. 20 Id., at 1069, 1093. 21 Id., at 1069, 1093. 22 Anette Jönsson, Venture Capital Continues to Flow into Chinese Startups, THE WALL STREET JOURNAL (Apr 28, 2015), http://www.wsj.com/articles/venture-capital-continues-to-flow-into-chinese-startups-1430244889; Venture Capital Soars and Investor Expectations Follow, NIKKEI ASIAN REVIEW (Feb 18, 2016), http://asia.nikkei.com/Politics-Economy/Economy/Venture-capital-soars-and-investor-expectations-follow; Lucida Shen, China is the Biggest Venture Capital Firm in the World, FORTUNE (Mar 9, 2016), http://fortune.com/2016/03/09/investors-venture-capital-china/. 23 The first venture capital firm was established in 1985. 24 See Back to Reality: Global Venture Capital Trends 2015, ERNST & YOUNG (2016) at 3, 10-12, http://www.ey.com/Publication/vwLUAssets/ey-global-venture-capital-trends-2015/$FILE/ey-global-venture-capital-trends-2015.pdf.

6

for investment. This represented a 57.89% increase from the previous year.25 Additionally, there was a total of 3445 venture capital investment deals in 2015, an increase of 79.9% from the previous year in terms of number. 26 In terms of volume, venture capital investments in China totaled USD 48.9 billion, surpassing that of the whole of Europe.27 Of the top five venture capital deals worldwide in 2015, three were made in China.28 Venture capital exits were at a healthy level, with the amount raised from exits via IPO and M&A reaching USD 8.2 billion and USD 11.5 billion respectively in 2015.29 As of end-2014, venture capital investments contributed directly and indirectly to 9.3% of China’s GDP.30 Indeed, these figures underline the significance of the Chinese venture capital market and its influence on China’s economy. The exponential growth of the venture capital market in China over the past decade seems to be without historical precedent. While India’s venture capital market is also developing rapidly, the value of venture capital investments added up to a comparatively smaller amount of USD 8.0 billion in 2015.31 In the UK, venture capital investments peaked in 2007 and have been relatively stagnant since,32 totaling USD 4.8 billion in 2015.33 The value of venture capital investments in Germany and France amounted to USD 2.9 billion and USD 1.9 billion respectively in 2015.34 This stands in stark contrast to China’s venture capital market, which has been maintaining a rapid growth rate since 2002, with fund raising, investments and exits reaching a record high in 2015, as illustrated above. Notably, China’s venture capital market did not emerge by virtue of private ordering, but was instead consciously and strategically designed by the state from the outset. Specifically, the government aimed to develop the nation’s venture capital market to encourage innovation and technology, and to stimulate structural reforms of the economy.35 Nonetheless, the development of the venture capital market was not without its difficulties. China’s legal system has long been regarded as problematic,36 and private ordering in China has also been criticized as less functional because of weak investor protection, 37 ineffective judicial

25 Zero2IPO Research Center, Venture Capital Annual Report 2015, ZERO2IPO PUBLISHER (2016). 26 See Id.; summary of 2015 Annual reports available at: http://research.pedaily.cn/201601/20160112392433.shtml 27 Ernst & Young, supra note 24. 28 Id., at 10. 29 Id., at 10. 30 Jiang Hua, China Venture Capital Forum Held in Shenzhen, CHINA ECONOMIC NEWS NETWORK (Jul 10, 2015), http://www.cet.com.cn/fgjj/yzlt/1585202.shtml. 31 Ernst & Young, supra note 24, at 2-3. See also Venture Capital in India, PREQIN (2015), http://www.preqin.com/docs/reports/Preqin-Venture-Capital-India-September-2015.pdf. 32 Annual value of venture capital investments on the UK market from 2007 to 2015, STATISTA (2016), http://www.statista.com/statistics/438743/venture-capital-investments-value-united-kingdom-uk/. 33 Ernst & Young, supra note 24. 34 Id., at 9. 35 Infra text accompanying notes 61-102. 36 See generally Jiangyu Wang, China: Legal reform in an emerging socialist market economy, in LAW AND LEGAL INSTITUTIONS OF ASIA: TRADITIONS, ADAPTATIONS AND INNOVATIONS (E. Ann Black & Gary F. Bell eds., 2011), ch 1; Donald Clarke, Peter Murrell, & Susan Whiting, The Role of Law in China’s Economic Development, in CHINA'S GREAT ECONOMIC TRANSFORMATION (Loren Brandt & Thomas G. Rawski eds., 2008). 37 See generally Nicholas C. Howson & Vikramaditya S. Khanna, The Development of Modern Corporate Governance in China and India, in CHINA, INDIA AND THE INTERNATIONAL ECONOMIC ORDER (M. Sornarajah and Jiangyu Wang eds., 2010) (on investor protection).

7

enforcement of laws, and the lack of judicial independence.38 Despite these problems, China’s national venture capital market was established, with a high growth rate, within three decades. China’s fascinating experience seems to challenge the orthodox view that top-down efforts by governments are likely to be unsuccessful in promoting venture capital. The pivotal question is: if empirical studies show that government programs have not been very successful on average and across countries, how has China managed to create the second largest venture capital market despite having premature legal infrastructure? This article seeks to fill the gap in literature39 by examining, based on quantitative, qualitative and hand-collected data and extensive interviews, how China has addressed the simultaneity problem with a degree of success.40 The focus of this article is on the role of the government in laying down the legal and institutional infrastructure for the venture capital market through the enactment of laws. This article does not focus on venture capital contracting in detail as it is a separate and complicated issue which will be addressed in another of the author’s articles.41 The main findings of this article would provide guidance for constructing a rough template for government efforts at engineering venture capital markets around the world through law reform. This article should be of particular interest to policymakers and legislators in jurisdictions such as Australia,42 Taiwan43 and Singapore44 who have explicitly sought to develop a national venture capital market. The remaining parts of this article are structured as follows. Part II provides fresh insights 38 See generally JIANFU CHEN, LEGAL INSTITUTIONS IN CHINESE LAW: CONTEXT AND TRANSFORMATION (2008), ch 4. 39 Although there exists literature discussing the legal infrastructure and contractual designs that are used to address the agency problem within the venture capital cycle, theoretical studies on the key legal and institutional determinants of a viable venture capital industry, and sophisticated comparative studies between the two largest venture capital markets (i.e., U.S. and China) are limited. In particular, the special characteristics of Chinese venture capital market, and the peculiar legal problems which the Chinese market faces remain largely unexplored. See generally Ronald J. Gilson, The Legal Infrastructure of High Technology Industrial Districts: Silicon Valley, Route 128, and Covenants not to Compete, 74 N. Y. U. L. REV. 575 (1999); Ronald J. Gilson & David M. Schizer, Understanding Venture Capital Structure: A Tax Explanation for Convertible Preferred Stock, 116 H. L. REV. 874 (2003); Ronald J. Gilson, Engineering Venture Capital Markets: Lessons from the American Experience, 55 STAN. L. REV. 1067 (2003); Ronald J. Gilson & Bernard S. Black, Does Venture Capital Require an Active Stock Market?, 11 JOURNAL OF APPLIED CORPORATE FINANCE 37 (1999); Ronald J. Gilson & Bernard S. Black, Venture Capital and the Structure of Capital Markets: Banks Versus Stock Markets, 47 JOURNAL OF FINANCIAL ECONOMICS 243 (1998). 40 The empirical study consists of three parts. The first part is a study on a sample of fifty venture capital limited partnership agreements. These agreemnts are obtained from leading Chinese law firms and venture capital firms, i.e. Gaorong Capital, Chengwei Capital, Beijing Fangda Law Firm, Beijing Global Law Firm, Beijing Jincheng Tongda Law Firm, Chongqing Zhonghao Law Firm, Shanghai Yuantai Law Firm and Shenzhen Huashang Law Firm. The second part is the interviews with practitioners. This consists primarily of venture capitalists, counsel, and investors from twenty venture capital funds. The interviewees come from the six cities that are the major places of venture capital investments in China, i.e. Beijing, Shanghai, Tianjin, Shenzhen, Chongqing, and Guangzhou. The last part comprises the study of a wide range of official data and reports published by the leading service providers in China’s venture capital industry, i.e. the Annual Report of the Venture Capital Market in China published by the Zero2IPO Research Center, the China Venture Capital Yearbook published by China Venture Capital Research Institution, and the annual reports on venture capital published by the VentureChina.cn. 41 Lin Lin, Venture Capital Contracting in China: A Law and Economic Analysis, NUS CBFL WORKING PAPER (2016). 42 The Treasury and the Department of Industry, Innovation, Science, Research and Tertiary Education, Australian Government, Review of Venture Capital and Entrepreneurial Skills, THE AUSTRALIAN PRIVATE EQUITY & VENTURE CAPITAL ASSOCIATION LTD (2012), https://www.avcal.com.au/documents/item/516 at para. 4.4, p. 13 (“Australia’s venture capital sector is an important component of Australia’s innovation system”); at para. 4.18, p. 17 (“In terms of venture capital support, the Australian Government provides a range of equity- and tax-based venture capital programs”). Examples of governmental supports include the Innovation Investment Fund (equity-based) (see para. 4.19, p. 17) and the Early Stage Venture Capital Limited Partnerships program (tax-based) (see para. 4.23, p. 18). 43 See Gulinello, supra note 16. 44 See LERNER, supra note 8.

8

into the evolution, special characteristics and legal framework of China’s venture capital market. Part III specifically examines the Chinese experience in tackling the simultaneity problem as coined by Gilson. It also identifies the salient issues within each factor and makes suggestions for future reforms. Part IV returns to the theoretical basis of this article and systematically explores the role of law and government in engineering a venture capital market. Part V concludes.

II. The Venture Capital Market with Chinese Characteristics

A. The Concept of “Venture Capital” in the Chinese Context The concept of venture capital was first debated in China in 1985 in the central government’s “Decision to Reform the Science and Technology System”.45 Prior to that, and before the launch of the open-door policy and economic reform (gaige kaifang) in 1978, the legacy of the planned economy was such that all decisions regarding production and investment were embodied in a government-formulated plan. Consequently, there were no private enterprises in China, let alone startups or venture capital. Today the understanding of “venture capital” in China amongst professionals is consistent with international practice, in the sense that venture capital is a subset of private equity,46 and consists of an equity investment in high-growth, high-risk, and often high-technology firms that need capital to finance product development or growth. Although venture capital and private equity share similar legal structures, incentive schemes and investors, venture capital tends to focus on early-stage high-risk companies that are technologically intensive, whereas private equity invests in virtually every industry, especially later-stage companies.47 Also, venture capital does not include restructuring or leveraged buyout financing whereas it is common for private equity firms to acquire majority control of an existing or mature firm from its current owners.48 Nonetheless, due to the short history of the Chinese venture capital market, the understanding of venture capital amongst ordinary investors is limited and the term “venture capital” is commonly confused with “private equity”.49 The number of venture capital firms which strictly invest in the venture capital sector but not the private equity sector is much smaller than reported.50 Many existing Chinese venture capital firms arose from the capital market boom and have limited experience in the venture capital industry,51 and most venture capitalists were investment bankers prior to entering the industry and hence do not possess 45 The Decision to Reform the Science and Technology Systems, CPC CENTRAL COMMITTEE (Mar 13, 1985), http://cpc.people.com.cn/BIG5/64162/134902/8092254.html. 46 My interviews with lawyers, legal counsel and venture capitalists indicate that their understanding on venture capital is consistent with the international definition of venture capital (on file with author). 47 Id. 48 See Gilson, supra note 1; see also James A. Brander, Qianqian Du & Thomas Hellmann, The Effects of Government-Sponsored Venture Capital: International Evidence, 19(2) REVIEW OF FINANCE 571 (2014), available at http://strategy.sauder.ubc.ca/hellmann/pdfs/BranderDuHellmannRoF2014.pdf. 49 My interviews with lawyers, legal counsel and venture capitalists indicate that ordinary investors do not have clear idea on the difference between private equity and venture capital (on file with author). 50 Interview with Mr. A (anonymity requested), Vice President, Shanghai X Capital Co, Nov 2015 (on file with author). 51 Id.

9

sufficient venture capital expertise or market track records.52 Therefore, when selecting portfolio companies to invest in, Chinese investors tend to focus more on business models, firm size and cash flows instead of the company’s growth potential. Naturally, these investors are unwilling to commit too much capital to high-risk, early-stage startups.53 Instead, they are inclined towards making short-term investments in later stage portfolio companies in traditional industries to achieve quicker returns.54 Further, unlike a typical venture capital cycle in the U.S., which usually lasts for seven to ten years, a recent survey has shown that the average cycle in China is merely 32 months (two to three years).55 In recent times, the boundary between venture capital and private equity has become increasingly blurred. Many venture capital firms which used to invest in early-stage startups, having had to cope simultaneously with fund-raising difficulties after the 2008 global financial crisis as well as investors’ expectations for higher returns, have become more inclined to invest in later-stage and lower-risk enterprises, especially pre-IPO companies, to gain quick returns.56 Meanwhile, recent government efforts in building up a multi-layered capital market framework, coupled with the rapid development of the mobile internet industry, have prompted traditional private equity firms to shift their investment preferences from later-stage and pre-IPO companies to early-stage companies. 57 Significantly, the catchphrase used to reflect the industry trend in China has changed from “quanmin PE” (which translates to “everyone invests in the private equity industry”) in 2010 to the current “quanmin VC” (which translates to “everyone is keen on venture capital investment”).58

B. The Need for Venture Capital in China The importance of a national venture capital market is widely accepted by governments around the world.59 The venture capital market provides “a unique link between finance and innovation, providing start-up and early-stage firms organizational forms particularly well-suited to innovation with capital market access that is tailored to the special task of financing these high-risk, high-return activities.”60 Developing a national venture capital market is high on the agenda of the Chinese government for two major reasons: firstly, to satisfy the demand

52 Lin Lin, The Private Equity Limited Partnership in China: A Critical Evaluation of Active Limited Partners, 13(1) JOURNAL OF CORPORATE LAW STUDIES 185, 200 (2013). 53 Id. 54 Id., at 187 and 192. 55 Zhong Zhimin, 287 VC/PE backed Companies Are Applying for Listing, CHINA SECURITIES JOURNAL (Zhongguozhengquanbao) (Jun 20, 2012). The survey was conducted using data as of June 14, 2012. Statistics show that the investment cycles of two venture capital firms were less than 20 months, and only 5 firms had cycles above 40 months. 17 firms had investment cycles between 20-40 months. 56 See Zhou Ming, PE and VC Investment Strategies Are Converging [PE yu VC Touzi Shuangshuang Houyi], CHINA SECURITIES JOURNAL (Zhongguozhengquanbao) (Mar 17, 2008). 57 See The Booming of the New Third Board [Xin sanban chixu huobao de PE / VC daju jinru juejin], CHINA SECURITIES JOURNAL (Zhongguozhengquanbao) (Jan 17, 2015). 58 Yu Tian Er, The Movement from Mass PE to Mass VC is the Product of the Times [Changjiang guohong touzi hehuo ren lichunyi: Quanmin PE dao quanmin VC shi shidai chanwu], GRAND YANGTZE CAPITAL, Dec 3, 2014, http://www.grandyangtze.com/article/article?parent_id=3&id=39. 59 See LERNER, supra note 8, at 63-64. 60 Gilson, supra note 1, at 1068.

10

for capital from startups and small and medium size (“SME”) firms, and secondly, to re-chart the economic development of the nation.61

1. Satisfying Demand for Capital The growth of startups and SME firms has long been constrained by a substantial capital gap in China, as China’s stock markets are unable to serve as viable financing channels for SMEs. Apart from dealing with the prohibitively high costs and long waiting times (caused by the current approval system) involved in an IPO, startups and SMEs, by virtue of their youth or size, also face difficulties in meeting the stringent listing requirements set by the two Main Boards.62 Moreover, unlike state-owned enterprises (“SOEs”), which are able to receive low-interest loans from state-owned banks (in part due to administrative influence), private companies face enormous difficulties in securing bank loans.63 Such problems with securing debt financing are exacerbated for startups, which typically have insufficient collateral to offer as security.

Meanwhile, the number of businesses has been increasing, particularly after a streamlining process in 2014, spearheaded by the enactment of the revised Company Law of the People’s Republic of China (PRC).64 From January to September 2015, 3.16 million new companies were registered, a 19.3% rise from the same period the previous year.65 In Beijing’s Zhongguancun district, the so-called “Chinese Silicon Valley”, an average of 7 new companies were registered every minute from March 2014 to May 2015. 66 This inadvertently contributed to a high demand for venture capital as an important means of startup financing. Such demand is appositely complemented by the venture capitalists’ appetite for high-risk, high-return investments and their ability to provide access to industrial connections and managerial skills.

Further, Chinese innovation and IT infrastructure have been greatly improved after the launch of various state programs promoting science and technology, such as the 985 Program and the Torch Program launched in late 1980s (see Appendix 2 on “entrepreneurship”). As of March 2015, there were more than 1,600 technology incubators supporting more than 80,000 startups.67 In 2015, China saw 1,102,000 invention patent applications, which was 18.7% more than the previous year, with 359,000 of them being authorised.68 The importance of venture capital is further exemplified by the fact that many of today’s Chinese internet giants 61 Developing science and technology was one of the “Four Modernizations” set forth by Premier Zhou Enlai in 1963, and enacted by Deng Xiaoping from 1978, to modernize the four fields of “agriculture, industry, national defense, and science and technology”. 62 Lin Lin, Venture Capital and the Structure of Stock Markets: Lessons from China, NUS CBFL WORKING PAPER, ASIAN JOURNAL OF COMPARATIVE LAW (forthcoming) at 17. 63 See Lan Yuping, Venture Capital can Effectively Solve the Problem of Capital Financing of Small and Medium Enterprises [Fengxian Touzi ke Youxiao Jiejue Zhongxiao Qiye Rongzi Nan], INTERNATIONAL FINANCING (Guoji Rongzi) (Sep 8, 2010). 64 The Company Law of the People’s Republic of China, National People’s Congress [2005] Presidential Decree No. 42. 65 China’s New Companies Surge 19.3% in Q1-Q3, CHINA DAILY ASIA (Oct 15, 2015), http://www.chinadailyasia.com/business/2015-10/15/content_15329850.html. 66 Zhang Lulu, China’s Startup Boom: 7 New Firms Every Minute, CHINA.ORG.CN (Jun 9, 2015), http://www.china.org.cn/business/2015-06/09/content_35775291.htm. 67 See Science and Technology Minister Wan Gang answers reporters' questions [keji buzhang wangang da jizhewen], CHINA.ORG.CN (May 30, 2015), http://www.china.com.cn/zhibo/zhuanti/2015lianghui/2015-03/11/content_34996059.htm. 68China Received over 1 Million Invention Patent Applications in 2015, STATE INTELLECTUAL PROPERTY OFFICE OF THE PRC (Jan 20, 2016), http://english.sipo.gov.cn/news/official/201601/t20160120_1231391.html.

11

that have assumed macroeconomic significance and influence, such as Sina,69 Sohu70 and Alibaba71, were former recipients of venture capital backing in their early days.

2. Re-charting Economic Development China’s Gross Domestic Product (“GDP”) growth rate fell from 10.4% in 2010 to 7.3% in 2014,72 with traditional economic sectors such as manufacturing and real estate sectors showing signs of weakening.73 Also, with a population of 1.3 billion and a labor force of 900 million, China faces strong pressure to address an increasingly significant unemployment issue.74 It is thus imperative for the government to foster the development of high-technology industries and a knowledge-based economy to enhance competitiveness and promote sustainable growth.

In short, China’s need for sustainable economic development has resulted in a greater emphasis on innovation and IT infrastructure, a huge increase in eager investors with excess capital,75 a new generation of entrepreneurs76 and an increased number of small businesses. This mix of factors has translated into a strong demand for high-risk, high return venture capital.

C. The Evolution of China’s Venture Capital Market and the Evolving Role of the Government

1. Emerging Phase (1985-1990) Venture capital has had a much shorter history in China than in the U.S.77 The Chinese government has only sought to replicate America’s success in developing an effective venture capital market since the 1980s,78 with the concept of venture capital being first officially introduced in China in 1985.79 The industry only began to emerge in the same year when the first venture capital firm, the China New Technology Venture Capital Company

69 Sina is one of the largest Chinese online media companies for Chinese communities. 70 Sohu is one of the largest Chinese Internet companies. 71 Alibaba is a Chinese e-commerce company that provides consumer-to-consumer, business-to-consumer and business-to-business sales services via web portals. 72 GDP Growth (Annual %), WORLD BANK (Feb 11, 2016), http://data.worldbank.org/indicator/NY.GDP.MKTP.CD/countries/CN?display=graph. World Bank figures for China’s GDP in 2015 were not available at the time of this article. 73 Mark Magnier, As Growth Slows, China Highlights Transition From Manufacturing to Service, THE WALL STREET JOURNAL (Jan 19, 2016), http://www.wsj.com/articles/as-growth-slows-china-highlights-transition-from-manufacturing-to-service-1453221751; Michael Lelyveld, China Growth Slows Despite Stimulus Spur, RADIO FREE ASIA (May 2, 2016), http://www.rfa.org/english/commentaries/energy_watch/china-growth-slows-despite-stimulus-spur-05022016102142.html. 74 Views of the State Council on Policy Measures relating to Mass Public Entrepreneurship [Guowuyuan guanyu dali tuijin dazhong chuangye chuangxin. Ruogan zhengce cuoshi de yijian], STATE COUNCIL NEWS RELEASE (Jun 16, 2015), http://www.gov.cn/zhengce/content/2015-06/16/content_9855.htm. 75 See infra text accompanying note 169. 76 See infra text accompanying notes 286 - 287. 77 See LERNER, supra note 8, at 8. The U.S. has over 70 years of experience in venture capital since the 1940s. 78 After the open door and economic reform, Chinese policy makers have made consistent efforts to study the experience of Silicon Valley in developing the venture capital industry. In the 1980s, a large number of scholars were sent to the U.S. to pursue higher degrees. Some of them, including the “Godfather” of venture capital in China – Mr. Cheng Siwei, brought back the idea of venture capital and started to promote it. See A Historical and Modern Look at the Chinese Venture Capital Market, XINHUAWANG (May 13, 2008). See Cheng Siwei, Developing Venture Capital, Revitalizing China, 3(2) CHINA VENTURE CAPITAL (Jun, 2004), at 1. 79 Supra text accompanying note 45.

12

(zhongguo xinjishu chuangye touzi gongsi) was set up as a government-initiated project.80 Prior to that, there were no venture capital firms, let alone a market for venture capital in China. To facilitate technology and innovation, the Ministry of Science and Technology launched the influential Torch Program in 1988, which kick-started a nation-wide focus on high-tech development and innovation. However, venture capital developed slowly in this period due to the lack of a stock market and unfamiliarity with the new concept.81 Thereafter, a number of government-backed companies were set up to provide financing to high-tech startups.82

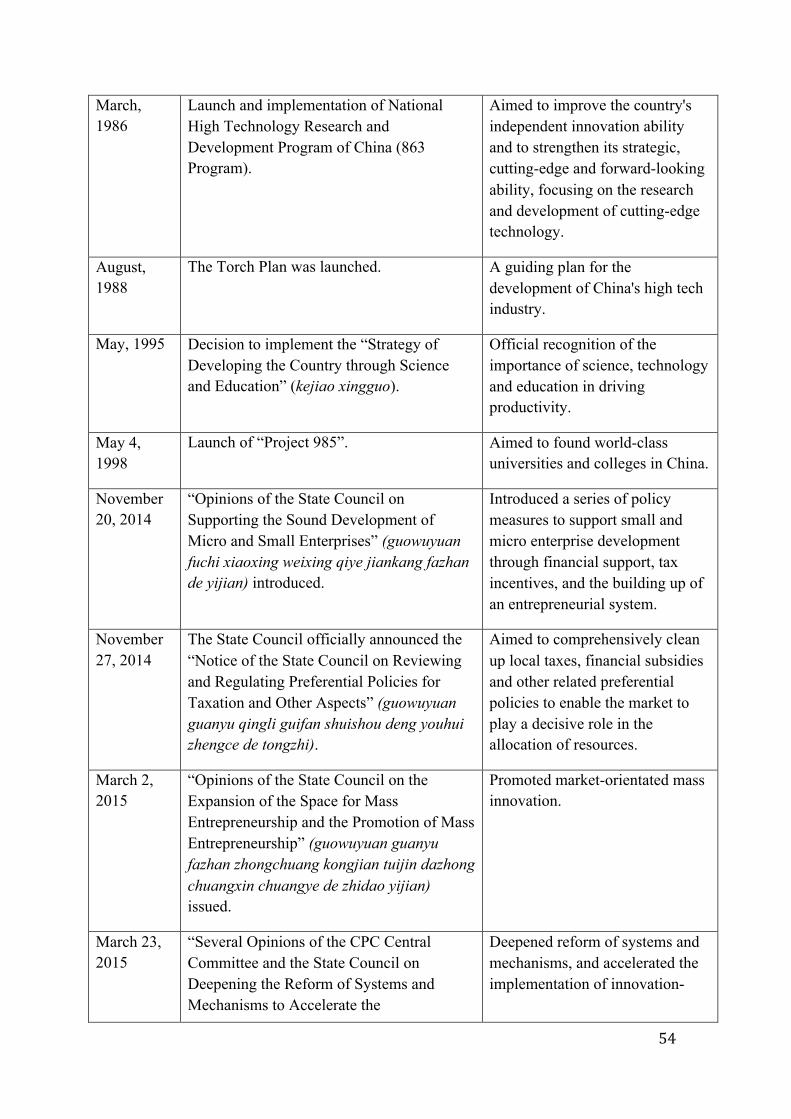

2. Experimentation Phase (1991-2000) The year 1998 marked a turning point, when Mr. Cheng Siwei,83 the then vice chairman of the National People’s Congress Standing Committee presented a groundbreaking “No.1 Proposal” urging the development of a venture capital market in China.84 After the proposal, a series of policies were issued, including the Strategy of Invigorating China through Science and Education (kejiao xingguo) and the Law on Promoting the Transformation of Scientific and Technological Achievements 1996 (see Appendix 2 on “entrepreneurship”). 85 Meanwhile, a number of government funds were set up to provide capital to high-tech startups.86 Foreign venture capital firms like IDG Capital Partners and Walden International also started to enter the Chinese market. Significantly, the establishment of the Shanghai Stock Exchange and the Shenzhen Stock Exchange in 1990 offered new exit channels for venture capital investments. Before that, venture capital-backed firms were unable to exit via IPOs. Nonetheless, government-backed venture capital firms still dominated the industry during this period, 87 and the role of private venture capital firms was very limited due to the limited choices of business vehicles available at that time.88

3. Decline and Subsequent Growth (2001-2005)89 Venture capital investment declined substantially in China after the burst of the “dot-com bubble” in 2001 and the global economic slowdown in 2002. Thereafter, in order to provide a business-friendly regulatory environment and a feasible legal framework to venture capital

80 See ZHU SHAOPING & GE YI, THE AMENDMENT OF THE PARTNERSHIP ENTERPRISE LAW OF PEOPLE’S REPUBLIC OF CHINA, 4 (2004). See also Lu Haitian, Tan Yi & Chen Gongmeng, Venture Capital and the Law in China, 37 HKLJ 229 (2007). 81 Id. 82 Cheng Siwei, Preface, in CHENG SIWEI ON VENTURE CAPITAL (2008). 83 Mr. Cheng Siwei is known as the “Godfather” of venture capital in China. He began to promote the concept of venture capital when he returned from his MBA studies from the University of California, Los Angeles, in 1984. He presented this proposal to the first meeting of the 9th Chinese People’s Political Consultative Conference. 84 Cheng Siwei, The History and Status Quo of China’s Venture Capital, in CHENG SIWEI ON VENTURE CAPITAL (2008). 85 In 1999, the Ministry of Science and Technology, the State Development Planning Commission, the State Economic and Trade Commission, the People’s Bank of China, the Ministry of Finance, the State Administration of Taxation and the China Securities Regulatory Commission jointly issued the Opinions on Establishing a Venture Investment Mechanism. 86 Such as the Technical Innovation Fund for Small and Medium Sized Enterprises 1999. See The Glorious Growth of the Private Equity Investment Industry over 10 years [Simu Guquan Touziye Shinian Huali Feiyue, 2014 Nian Kaiqi Zhongguo Guquan Touzi Shidai], PEDATA.CN (Apr 24, 2015), http://www.pedata.cn/main_do/news_detail/214294. 87 Beijing Zhongguancun Technology Venture Capital Company was the first private venture capital firm in China. In 1992, the first foreign VC (IDG Capital), entered into China. In 1995, the Administrative Measures on Foreign-Established Industry Investment Funds [Sheli jingwai zhongguo chanye touzi jijin guanli banfa], State Council, People’s Bank of China, was promulgated. The 1st Sino Foreign Joint Venture in the venture capital sector – Kezhao High Tech Co. Foreign PE invested in Sohu, Sina, 163, etc. and eventually got them listed on NASDAQ. See Steve Blank, The Rise of Chinese Venture Capital (Part 3 of 5) (Apr 12, 2013), http://steveblank.com/2013/04/12/the-rise-of-chinese-venture-capital/. 88 Limited Partnership was not available in this period. 89 Refer to Figure 2 below for a timeline of key developments since 2002.

13

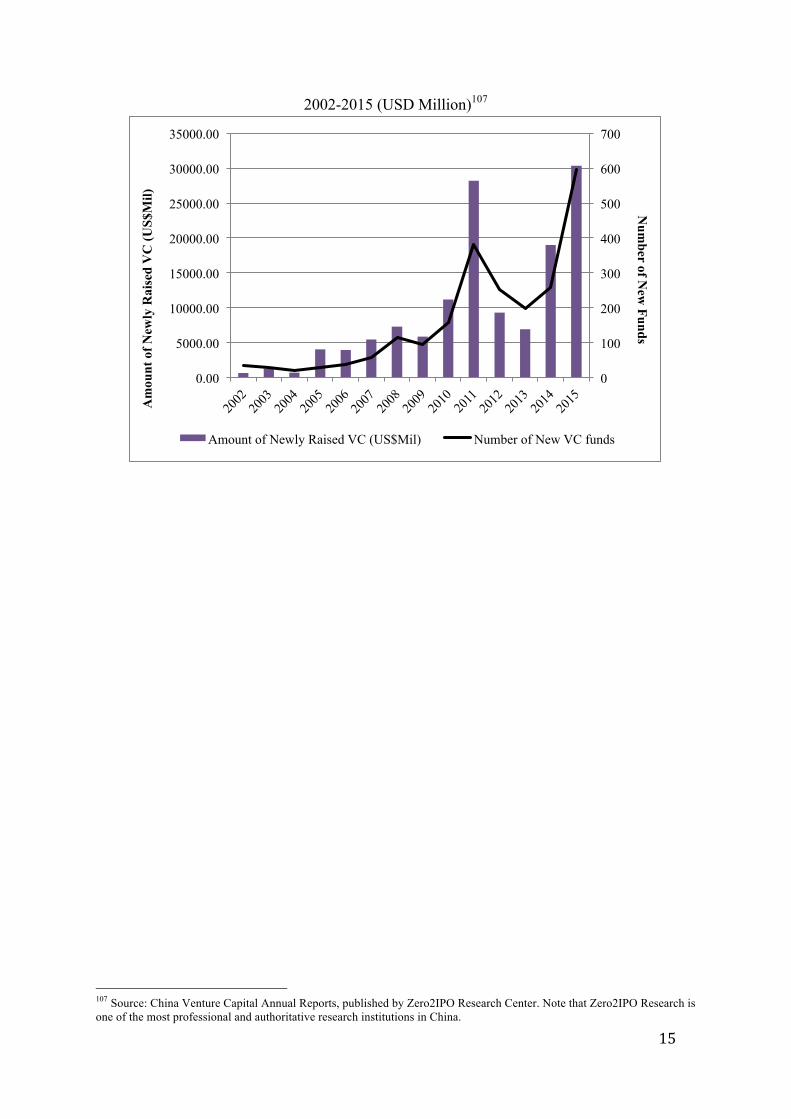

participants, clear guidance and regulations were issued on matters pertaining to the establishment, management, supervision, taxation and foreign investment 90 of venture capital.91 To facilitate the exit of venture capital-backed companies, the Small and Medium-sized Enterprise Board (“SME Board”)92 was launched in 2004. As a result of these policy incentives, venture capital funds raised more than USD 4 billion in 2005, exceeding the cumulative amounts raised in the past three years (Figure 1 and Figure 2).

4. Deepening Structural Reforms (2006- 2013) The adoption of the limited partnership in 2006 was essential to the Chinese venture capital market as it provided a new business vehicle for venture capitalists and investors to raise funds.93 The introduction of the limited partnership was part of the government’s strategy to develop scientific innovation as articulated in its 11th Five-Year Plan (2006-2010),94 which identified the promotion of venture capital investment as a critical element for achieving “independent innovation” and sustainable economic progress in China.95 Although the number and volume of funds raised dipped in 2009 due to the global financial crisis, both the number of newly established venture funds and the amounts raised increased two-fold in 2011 (Figure 1). The major contributors to this venture capital boom included the launch of a new NASDAQ-like secondary board – ChiNext, new measures allowing insurance funds to make equity investments,96 the launch of several Qualified Foreign Limited Partner (“QFLP”) schemes in Shanghai, Beijing, Tianjin and Chongqing which permitted foreign qualified institutional investors to make equity investments in Chinese markets, as well as the substantial increase in investments by the National Social Securities Fund (“NSSF”) in private equity (of more than RMB 6 billion).97

As such, although the suspension of the IPO process by the China Securities Regulatory Commission (“CSRC”) from November 2012 to January 2014 negatively affected fund-

90 The Regulations on the Administration of Foreign Invested Venture Capital Enterprises, Ministry of Foreign Trade and Economic Cooperation, Ministry of Science and Technology, State Administration for Industry and Commerce, State Administration of Taxation, State Administration of Foreign Exchange (2003) allowed foreigners intending to invest in the Chinese VC market to do so through setting up an FIVCIE which can take the form of an incorporated entity or a non-legal person entity. 91Interim Measures for Administration of Startup Investment Enterprises, National Development and Reform Commission, Ministry of Science and Technology, Ministry of Finance, Ministry of Commerce, People's Bank of China, State Administration of Taxation, State Administration for Industry and Commerce, China Banking Regulatory Commission, China Securities Regulatory Commission, and State Administration for Foreign Exchange [2005] Order No. 39. 92 In 2004, the Small and Medium-sized Enterprise Board was launched at Shenzhen, China. 93 Administrative Measures relating to the Establishment of Partnerships in China by Foreign Enterprises or Individuals, State Council [2009] Order No. 567. In 2001, the Interim Measure on the Establishment of Foreign-Invested Venture Capital Enterprises [guanyu sheli waishang touzi chuangye qiye de zhanxing guiding] (2001) was issued. In 2002, the Foreign Investment Industry Guidance Catalogue was issued to attract more foreign investment. In 2005, the State Administration of Foreign Exchange issued the Circular 75, which greatly improved the foreign equity investment environment in China. 94 See The Eleventh Five Year Plan, CENTRAL COMMITTEE OF THE CHINA COMMUNIST PARTY, passed on October 11, 2005 at the Fifth Meeting of the Sixteenth Central Committee of the China Communist Party. 95 See Reasons for revising Partnership Enterprise Law, NATIONAL PEOPLE’S CONGRESS NEWS RELEASE (May 2006). Before the introduction of LPs, the only major legal structures generally available for venture capital firms in PRC were the Limited Liability Company, Joint Stock Company and General Partnership, but all of them were unattractive because of their inherent features. 96 The Interim Measures for Equity Investment with Insurance Funds, China Insurance Regulatory Commission (2010), allowed insurance funds allowed to make equity investments. 97 See Appendix 2.

14

raising in both 2012 and 2013, the reforms discussed in the previous paragraph accelerated the reboot of the venture capital market in 2014. This was further assisted by the 2013 nation-wide expansion of the National Equities Exchange and Quotation (“NEEQ”) system (also known as the “New Third Board”), which has now become an important exit vehicle for venture capital-backed startup firms.98

5. Towards a More Market-Oriented System (2014-present) Since 2014, the Chinese central government seems to be moving towards a “Government Led + Market Operation” model in providing public funding,99 instead of directly participating in the allocation of capital. The State Council announced in 2015 that China would be setting up the RMB 40 billion (USD 6.5 billion) State Venture Capital Investment Guidance Fund (“SVCIGF”) (guojia xinxingchanye chuangyetouzi yindao jijin) to support startups in emerging industries, foster innovation, and upgrade the industry.100 Public tenders would be made to select qualified professional firms to manage the fund.101 Rather than setting up and directing the government-backed funds, the central government stated that it would instead be a limited participant by only providing funding.102 However, whether the new SVCIGF will be effective and whether local governments103 will follow the central government’s approach towards government funds remains an open question.104

In summary, although the Chinese venture capital market was dominated by state-owned venture capital firms and venture capital funds in the 1980s and 1990s, it has seen a rapid emergence of private firms and investors since 2006. As a result, private individual and families form the majority of investors in the venture capital and private equity market in terms of number.105 Further, the majority of leading venture capital firms in China today are private firms and foreign firms.106 Arguably, this has been achieved largely through the evolution of the central government’s role and approach to developing the venture capital market – from a direct participant in capital allocation (through establishing state-owned venture capital firms and funds) to a capital provider that intervenes less in the capital allocation process (focusing on the easing of regulatory barriers for the entry of foreign and private capital into the venture capital market).

Figure 1: New Venture Capital Commitments against New Venture Capital Funds

98 According to Zero2IPO statistics, in the year 2015 alone, 929 venture capital-backed companies were listed on the NEEQ, accounting for 51.2% of the total exit vehicles in 2015. See further information on the correlation between the stock market and the venture capital market in Lin, supra note 62. 99 Zero2IPO Research Center, Report of the China Government Guidance Fund 2015 [2015 Nian Zhongguo Zhengfu Yindao Jijin Fazhan Baogao Jianban], ZERO2IPO PUBLISHER (Feb 28, 2015). 100 Id. 101 Id. 102 See infra text accompanying notes 158- 165 on further discussion of the new direction of the SVCIGF. 103 In China, provincial and sub-provincial leaders on local level have a significant amount of autonomy. There are five practical (de facto) levels of local government: the provincial (province, autonomous region, municipality, and special administrative region), prefecture, county, township, and village. 104 See infra text accompanying notes 158- 165 on further discussion of the new direction of the SVCIGF. 105 See Table 2 & Table 3 in this article noting that government guidance funds only account for 2% of all investors on average. 106 See The Top 50 VC Firms of the Year 2015 (ranked by Zero2ipo), PEDAILY.CN (Dec 4, 2015), http://pe.pedaily.cn/201512/20151204391023.shtml.

15

2002-2015 (USD Million)107

107 Source: China Venture Capital Annual Reports, published by Zero2IPO Research Center. Note that Zero2IPO Research is one of the most professional and authoritative research institutions in China.

0

100

200

300

400

500

600

700

0.00

5000.00

10000.00

15000.00

20000.00

25000.00

30000.00

35000.00 N

umber of N

ew Funds

Am

ount

of N

ewly

Rai

sed

VC

(US$

Mil)

Amount of Newly Raised VC (US$Mil) Number of New VC funds

16

Figure 2: New Venture Capital Commitments over the Years and the Major Policies and

Legal Developments 2002-2015

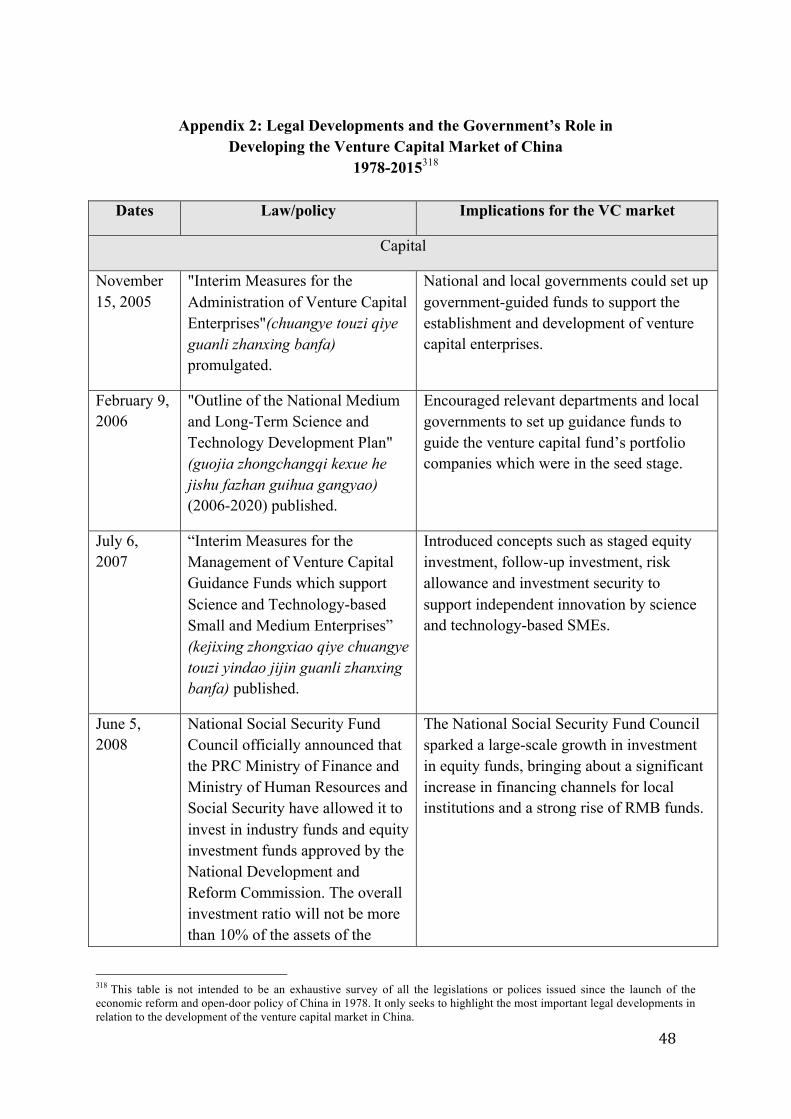

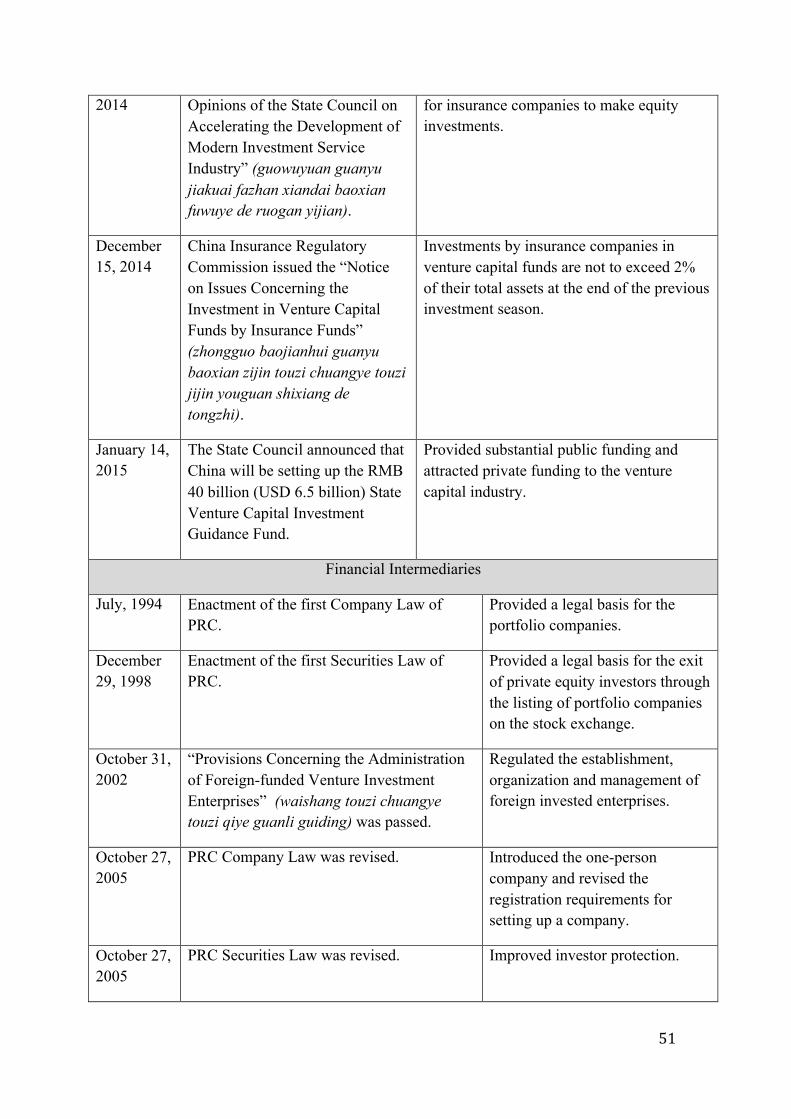

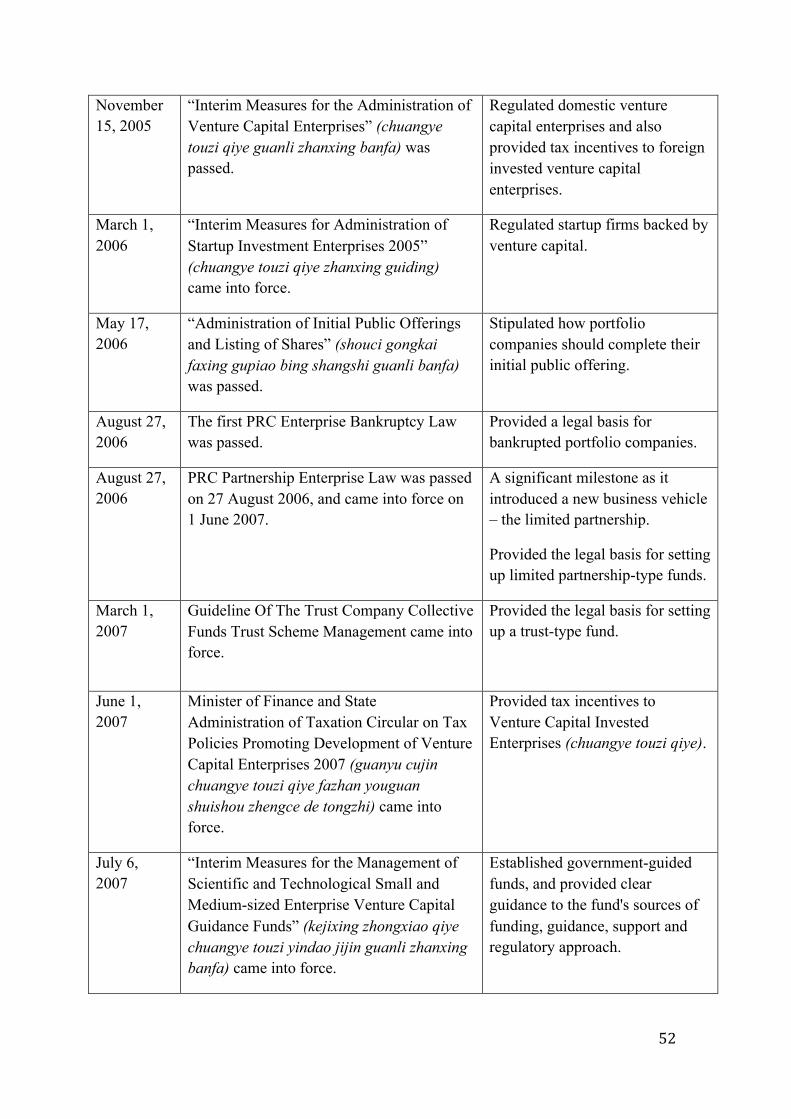

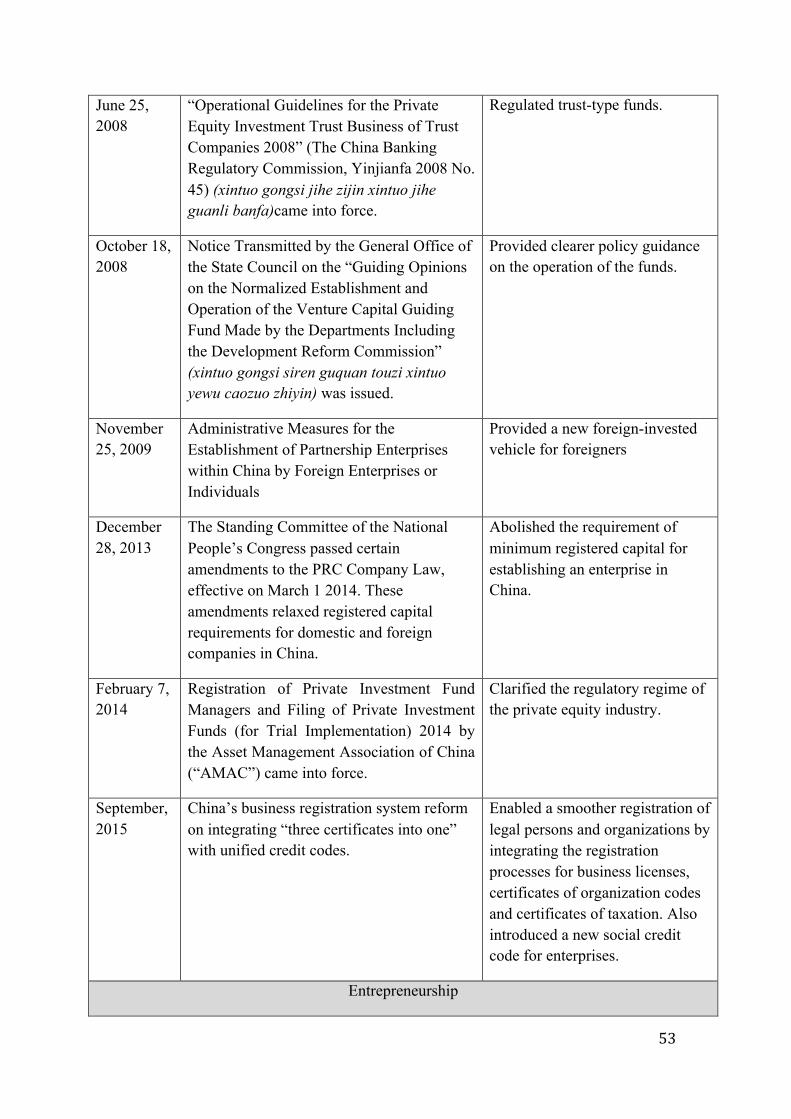

III. Engineering Problems in China This part will critically explore how the three-factor simultaneity problem has been gradually tackled in China, from a comparative and empirical perspective.108

A. Capital

1. Public Capital Funds for venture capital investment can be divided into two types depending on their source: government funding109 and private funding. Government funding has been recognized as one of the most important sources of funding for fueling entrepreneurship across countries, after bank credit.110 Many countries have promulgated various kinds of government programs to support entrepreneurial businesses, typically through setting up government-sponsored funds to make investments in startups. Notable examples include Israel’s Yozma Program,111 Germany’s Deutsche Wagnisfinanzierungsgesellschaft (“WFG”),112 New Zealand’s Venture

108 See also Appendix 1 for a brief overview of the legislative efforts at tackling the simultaneity problem in China. 109 In this article, government funding typically refers to capital provided by central and local governments from their budgets. 110 See The EY G20 Entrepreneurship Barometer 2013, ERNST & YOUNG (2013). See also Adapting and Evolving: Global Venture Capital Insights and Trends 2014, ERNST & YOUNG (2014) at 14, http://www.ey.com/Publication/vwLUAssets/Global_venture_capital_insights_and_trends_2014/$FILE/EY_Global_VC_insights_and_trends_report_2014.pdf. 111 Gilson, supra note 1, at 1097-1098. 112 See Gilson, supra note 1.

17

Investment Fund (“NZVIF”), 113 and Singapore’s Early Stage Venture Fund (“ESVF”) scheme.114 However, not all government programs have been successful.115 Many factors affect the effectiveness of government programs, including the duration of the programs,116 their size117 and flexibility,118 the presence of incentives for the financial intermediary to monitor portfolio companies,119 and the implementation process.120 Empirical evidence indicates that a well-designed government-sponsored fund which sufficiently incentivizes fund managers and employs appropriate monitoring mechanisms to ensure maximum returns would increase the overall level of venture capital investment and fundraising,121 and vice versa.122 This is illustrated by Chile and Israel’s venture capital programs, which emphasize the need for market forces as opposed to Germany’s heavy governmental involvement in capital allocation during the venture capital investment process.123

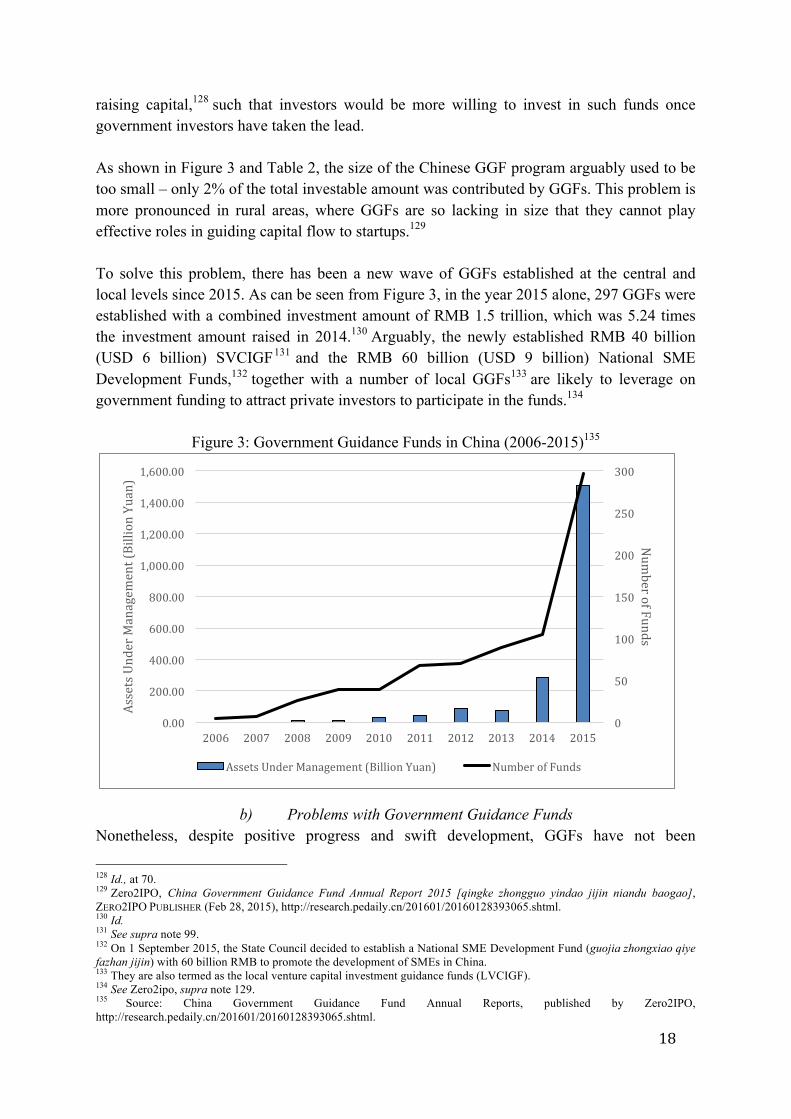

a) The Rise of Government Guidance Funds In China, venture capital funding has been provided to tech startups through various government-sponsored programs, particularly through Government Guidance Funds (“GGF”) (zhengfu yindao jijin),124 which are designed to increase the supply of venture capital to early-stage enterprises and implement national industrial policy by directing capital into government encouraged innovative industries.125 The sizing of the government program is important to venture capital financing. A public program that is too small would hardly have any impact on a large and diverse economy, while a program that is too large might crowd out or discourage private funding.126 Also, small firms typically face great difficulties in raising capital, due to the information asymmetry between the entrepreneurs and investors, resulting in reduced investor confidence.127 Government funds are thus advantageous as they have an “add-on effect” in

113 For a detailed analysis of the program, see Josh Lerner, David Moore, Stuart Shepherd, A Study of New Zealand Venture Capital and Private Equity Market and Implications for Public Policy, LECG LIMITED (2005). 114 Terence Lee, Singapore Government to Pump $48 Million into Six Venture Capital Funds, TECHINASIA (Apr 22, 2014). 115 See Gilson, supra note 1; LERNER, supra note 8. 116 LERNER, supra note 8, at 112-116 (arguing that encouraging entrepreneurship requires a long-term commitment on the part of public officials, and thus they should not have a short-term perspective or require quick returns under the government programs). 117 Id., at 117-123 (arguing that either too small or too large a government initiative can pose profound difficulties). 118 Id., at 124-127 (suggesting that government officials must appreciate the need for the flexibility in venture capital investment and rely more on market forces in selecting the sectors, locations, and portfolio companies). 119 See Gilson, supra note 1. 120 LERNER, supra note 8. 121 Armour & Cumming, supra note 3, at 601; Douglas J. Cumming & Jeffrey G. MacIntosh, Crowding Out Private Equity: Canadian Evidence, 21(5) JOURNAL OF BUSINESS VENTURING 569 (2006). 122 Id. 123 See Gilson, supra note 1, at 1094-1099. 124 The Industrial Investment Fund is a special type of government-backed fund whereby capital is raised from “specific institutional investors”, including the Social Security Fund, SOEs, commercial banks, insurance companies, securities companies, financial institutions and other institutional investors specified by the NDRC. 125 See 2008 Venture Capital Fund Specifications and Operational Guide. 126 LERNER, supra note 8, at 117-119. 127 LERNER, supra note 8, at 69.

18

raising capital,128 such that investors would be more willing to invest in such funds once government investors have taken the lead. As shown in Figure 3 and Table 2, the size of the Chinese GGF program arguably used to be too small – only 2% of the total investable amount was contributed by GGFs. This problem is more pronounced in rural areas, where GGFs are so lacking in size that they cannot play effective roles in guiding capital flow to startups.129 To solve this problem, there has been a new wave of GGFs established at the central and local levels since 2015. As can be seen from Figure 3, in the year 2015 alone, 297 GGFs were established with a combined investment amount of RMB 1.5 trillion, which was 5.24 times the investment amount raised in 2014.130 Arguably, the newly established RMB 40 billion (USD 6 billion) SVCIGF131 and the RMB 60 billion (USD 9 billion) National SME Development Funds,132 together with a number of local GGFs133 are likely to leverage on government funding to attract private investors to participate in the funds.134

Figure 3: Government Guidance Funds in China (2006-2015)135

b) Problems with Government Guidance Funds Nonetheless, despite positive progress and swift development, GGFs have not been

128 Id., at 70. 129 Zero2IPO, China Government Guidance Fund Annual Report 2015 [qingke zhongguo yindao jijin niandu baogao], ZERO2IPO PUBLISHER (Feb 28, 2015), http://research.pedaily.cn/201601/20160128393065.shtml. 130 Id. 131 See supra note 99. 132 On 1 September 2015, the State Council decided to establish a National SME Development Fund (guojia zhongxiao qiye fazhan jijin) with 60 billion RMB to promote the development of SMEs in China. 133 They are also termed as the local venture capital investment guidance funds (LVCIGF). 134 See Zero2ipo, supra note 129. 135 Source: China Government Guidance Fund Annual Reports, published by Zero2IPO, http://research.pedaily.cn/201601/20160128393065.shtml.

0

50

100

150

200

250

300

0.00

200.00

400.00

600.00

800.00

1,000.00

1,200.00

1,400.00

1,600.00

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Num

berofFundsAssetsUnderManagem

ent(BillionYuan)

AssetsUnderManagement(BillionYuan) NumberofFunds

19

unproblematic. First, government intervention in investment choice is prevalent within GGFs. Local governments often mandate the sectors, companies or locations which are to be funded through GGFs.136 In particular, it is common for a local government to require GGF-backed venture capital firms to invest in certain companies within the region, instead of similar companies elsewhere that may have higher growth potential and are in need of capital.137 This could lead to conflicts between the GGF and the venture capital firm, resulting in disincentives to the latter in finding promising projects and causing it to be less willing to receive funding from GGFs in future projects.

There are also problematic local regulations that unduly restrict the length of investments and size of the investee companies. For example, the Measures of Jiangsu Emerging Venture Capital Investment Guidance Fund specifies that the maximum length of the investment is five years,138 which is inconsistent with the international practice of between 7 to 10 years.139

Second, there exists a flawed governance structure and system for the selection of managers within local GGFs. For instance, under the Measures of the Shanghai Angel Investment Guidance Fund 2014 (“Shanghai AIGF Measures”), the manager of the Shanghai AIGF is not selected from the private sector, but is statutorily appointed. The manager currently appointed is a subsidiary of another government-backed fund – the Shanghai Technology Entrepreneurship Foundation for Graduates (“EFG”), who “shall exercise the rights as the investors of the Shanghai AIGF”.140 Two questions naturally follow: first, how would the EFG “exercise the rights as an investor” effectively since it does not provide capital contribution to the fund and does not own any equity interests in the fund? Second, how would the EFG monitor the fund effectively and fairly when the fund is being operated by its subsidiary? Also, unlike the ordinary venture capital limited partnership model where a professional venture capital firm serves as the general partner and is subject to various legal and contractual constraints (e.g. unlimited liability for the debts of the fund, fiduciary duties of the general partner and the limited partners’ derivative action mechanism), there is no effective mechanism to constrain the behavior of the Shanghai AIGF’s statutorily mandated fund manager.

136 For example, Article 6(5) of the Implementation Rules of the Shanghai Angel Investment Guidance Fund [Shanghaishi tianshi touzi yindao jijin guanli shishi xize], Shanghai Science and Technology Committee, Hukehe [2014] No. 49 states that the Shanghai Angel Investments Guidance Fund is to invest mainly in companies within Shanghai. 137 Article 8 of the Implementation Rules of the Shanghai Angel Investment Guidance Fund, supra note 136, states that investments by the Shanghai Angel Investments Guidance Fund into each portfolio company shall be between RMB 5 million – 30 million RMB and that this amount shall not exceed 50% of the total subscribed capital of the portfolio company. 138 Article 41 of the Measures of the Jiangsu Emerging Industry Venture Capital Investment Guidance Fund [Jiangsu sheng xinxing chanye chuangye touzi yindao jijin guanli banfa] states that the duration of investments made by the Jiangsu Emerging Industry Venture Capital Investment Guidance Fund shall not exceed 5 years unless approval is sought from the fund’s management committee 139 LERNER, supra note 8, 140Implementation Rules of the Shanghai Angel Investment Guidance Fund, supra note 136, Article 3.

20

Moreover, under the Shanghai AIGF Measures,141 a steering committee comprising the deputy mayor of Shanghai and other government bureaucrats is in charge of the policy-making and supervision of the Shanghai AIGF.142 Given the lack of expertise and experience of government officials in making venture capital investments, it is uncertain whether they would be able to ensure the efficient and effective use of the Shanghai AIGF’s assets in coordination with other key players. Further, the Shanghai AIGF Measures mandate the establishment of a separate investment committee comprising external experts and government representatives to review and vote for investment proposals. 143 These government officials may intervene directly in the decision-making process of the Shanghai AIGF, thus causing internal conflicts. Also, while the general partner of an ordinary venture capital fund is constrained by fiduciary duties and potential personal liability, government officials in the investment committee of the Shanghai AIGF are neither penalized nor rewarded for decisions made by the committee. Consequently, ensuring that these officials do not misuse resources of the GGF to obtain personal benefits remains a difficult task. Third, local governments or GGFs often guarantee investment losses suffered by venture capital firms, resulting in a lack of incentives on the part of the venture capital firm and the entrepreneurs. Examples include the GGFs of Beijing, 144 Jiangsu, 145 Guangzhou 146 and Shanghai.147 Under the Shanghai AIGF Measures, the Shanghai government will guarantee and compensate venture capital firms for up to 60% of their actual losses caused by investments in scientific and technological enterprises at seed stage or up to 30% if at start-up stage,148 as well as RMB 3 million of their actual losses for each investment project and RMB 6 million for annual investments by each investment firm.149 141 Id. Article 3 states that the steering committee is the highest management institution for the Shanghai Angel Investments Guidance Fund and is responsible for the policymaking and supervision of the fund. Public information reveals that the steering committee includes the deputy mayor of the Shanghai city as the leader and bureaucrats from the 12 departments of the Shanghai government. See Liang Jialin, The First Angel Investments Guidance Fund was set up in Shanghai, JINGJI GUANCHA BAO (Dec 24, 2014), http://www.eeo.com.cn/2014/1224/270637.shtml. 142 Id. 143 Article 12 of the Implementation Rules of the Shanghai Angel Investment Guidance Fund, supra note 136, states that the fund must set up an independent investment review committee to review investment proposals. The committee will comprise experts and representatives from relevant government agencies. 144 The Measures on the Zhongguancun Talent Attraction Investment Fund [zhonguancun guojia zizhu chuangxin shifanqu youxiurencai zhichi zijin guanli banfa] Zhongkeyuanfa [2013] No. 40 also stipulates subsidies for venture capital investments within Zhongguancun. 145The Measures on the Jiangsu Emerging Industrial Venture Capital Investments Guidance Fund [Jiangsusheng xinxing chanye chuangye touzi yindao jijin guanli banfa], Jiangsu Development and Reform Committee, Sufagaiguifa [2011] No. 8 states that angel investment firms would be compensated for up to 50% of the losses they incur from investments into seed or early-stage technology-based enterprises, provided that these losses were incurred within three years from the time the relevant investments were made, up to a limit of RMB 3 million. 146 The Trial Measures for the Technology Enterprises Incubator Venture Capital and Credit Risk Compensation Fund [guanyu keji qiye fuhuaqi chuangye touzi ji xindai fengxian buchang zijin shixing xize], Yuekeguicaizi [2015] No. 21 states that venture capital firms will be compensated for up to 50% of the losses they incur from investments made into early-stage enterprises in the Guangdong Province Technology Enterprises Incubator, up to a limit of RMB 2 million. 147 Shanghai Angel Investment Risk Compensation Interim Measures [shanghaishi tianshi touzi fengxian buchang guanli zhanxing banfa], Shanghai Science and Technology Committee, Shanghai Finance Bureau and Shanghai Finance Bureau and Shanghai Development and Reform Commission, Hukehe [2015] No. 27. 148 Id. Article 9. 149 Id. Article 10.

21

Such venture capital firms would unfortunately be less incentivized to perform effectively and work for the best interests of the funds under their management. Guarantee schemes which are funded by taxpayers’ money would also create public grievance towards the GGFs as the very nature of venture capital investments is high-risk. Guarantee schemes are also problematic because they are usually implemented by government officials who may not possess sufficient expertise in calculating the losses suffered, and who may prefer to compensate venture capital firms that are government-backed. For example, the Shanghai AIGF Measures state that a steering group comprising government officials is responsible for the implementation of the compensation scheme.150 Statistics show that many of the venture capital firms in Shanghai that received compensation for their investment losses were indeed government-backed firms.151 Fourth, GGFs often negotiate for a smaller compensation package for GGF-backed venture capital firms, resulting in lower incentives for the latter. Typically, the most popular distribution of the GP’s compensation is the so-called “2/20 Rule”. 152 The GP’s compensation comprises two parts: an annual management fee for its services comprising 2 to 2.5 % of the committed capital, and a carried interest of 20 to 25 % of the profits realized by the fund.153 This is however not always the case for GGF-backed venture capital firms. Local governments are often overly protective of the taxpayer’s money while negotiating profit allocation, resulting in the venture capital firm being paid less than a 20% carried interest,154 or in the GGFs being given priority in the distribution of profits over the venture capital firm.155 Meanwhile, numerous GGFs have not set up a comprehensive appraisal system to measure the performance of the GGF and the GGF’s manager,156 resulting in a lack of clear and detailed rules on the evaluation of the GGF.157

c) New Directions and Ways Forward for Regulating GGFs Cognizant of the problems within the local GGFs as discussed above, the Chinese central government has begun to move towards a market-oriented approach in the provision of

150 Id. Article 11. 151 Id. Article 8 specifies that applicants for compensation shall make a filing with the relevant registrar in charge of venture capital investments. Statistics show that out of more than 110 venture capital firms which had made filings for compensation as of January 2016, most were state-owned venture capital firms; see Why is the Government Subsidizing Venture Capital Investment Failures [fengxian touzi shibai, pingshenme zhengfu lai tieqian], INTOUCH TODAY (Jan 27, 2016), http://view.news.qq.com/original/intouchtoday/n3417.html. 152 Victor Fleischer, Two and Twenty: Taxing Partnership Profits in Private Equity Funds, 83 N.Y.U. L. REV. 1, 3 (2008). 153 Kate Litvak, Venture Capital Partnership Agreements: Understanding Compensation Arrangements, 76 UNIVERSITY OF CHICAGO LAW REVIEW 161 (2009). 154 Zero2IPO, supra note 129. 155 Four Problems Faced by Government Guidance Funds [qidi zhengfu yindao jijin: sida wenti lanlu], PEDAILY (May 12, 2016), http://pedaily.baijia.baidu.com/article/449928. 156 Article 24 of the Implementation Rules of the Shanghai Angel Investment Guidance Fund, supra note 136 states generally that the steering committee and its office are responsible for the supervision and evaluation of government guidance funds, but provides no specific evaluation criteria. 157 Article 30 of the Interim Measures of the Government Investment Fund [zhengfu touzi jijin zhanxing guanli banfa], Ministry of Finance, Caiyu [2015] No. 210. simply specifies that the GGF should set up an evaluation system for the fund, but provides no detailed rules on how the assessment should be made.

22

funding for venture capital.158 This involves attracting more private investors into the venture capital market (which will be discussed in the next section) and reducing government intervention in the operation of the GGFs, which is largely reflected in the newly established SVCIGF 2015159 and the Interim Measures of the Government Investment Fund 2015 which specify that the GGFs should operate based on market forces.160

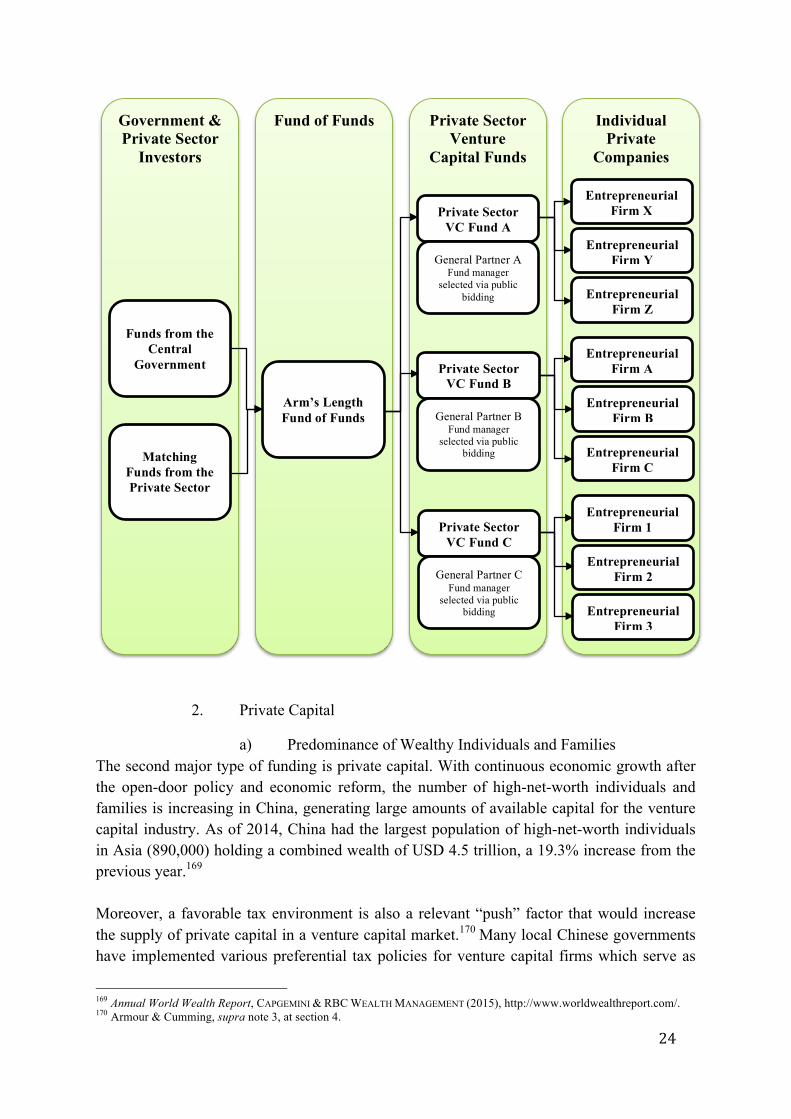

Several observations and suggestions may be made. First, according to Gilson, the ceding of control to market forces would mitigate operational inefficiencies arising from the incompetence and lack of professional experience on the part of government authorities. It also helps to tackle agency problems caused by the divergence of interests between governments and venture capital firms. The local government should avoid participation in the selection of portfolio companies and not seek to direct venture capital towards later-stage government-linked companies within their regions. Funding should be provided to early-stage startups that are in high demand of capital, instead of later-stage companies that allow the generation of quick returns. Also, as noted by Cumming and Johan, the impact of government-sponsored VC funds depends not only on the design of the program but also on the selection of the VC managers.161 Instead of appointing government-linked companies, governments should select experienced, professional and independent venture capital firms to manage the funds on a commercial basis.162 The SVCIGF is a positive step forward on both points (Diagram 1). Further, requiring matching funds to be raised from the private sector would help to reduce the dangers of uninformed decisions and political interference.163 The SVCIGF takes a step in the right direction – it will comprise RMB 40 billion of capital funding, with RMB 10-15 billion coming from the government and the remainder coming from other investors such as private enterprises and large institutional investors.164 Arguably, by allowing more than half of the funding to originate from the private sector, government interference is mitigated and the fund’s managers can make more informed commercial decisions on capital allocation. Second, the structure of the GGFs should be simplified to reduce bureaucracy and transaction costs, and to increase professionalism. A “fund of funds” (FOF) approach taken by the SVCIGF seems more desirable for GGFs (Diagram 1). Under the FOF model, the consolidated fund will make investments in a number of other funds and each of these funds will invest into a portfolio of companies. By doing so, the consolidated fund enjoys broader exposure to the industry and diversification of the risks associated with a single investment.

158 See Zero2IPO, supra note 129. 159 See Zero2IPO, supra note 129. 160 See e.g. Interim Measures of the Government Investment Fund [zhengfu touzi jijin zhanxing guanli banfa], supra note 157, Article 11. 161 Douglas Cumming & Sofia Johan, Pre-seed government venture capital funds, 7(1) J INT ENTREP 26 (2009). 162 The third key feature of the SVCIGF is that the government does not participate in fund management, and instead relies on incentivized financial intermediaries. Further, the SVCIGF will invite public tenders from professional fund managers for investment decisions. 163 LERNER, supra note 8, at 128-133. 164 400 yi guojia chuangtou jijin dingceng fangan sheji yi jiben wancheng [The Design of the 40 billion State Venture Capital Investment Fund has been completed], SINA FINANCE (Mar 30, 2015), http://finance.sina.com.cn/china/20150330/155021844627.shtml.

23