Energy Taxation in Europe, Japan and The United States

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Energy Taxation inEurope, Japan andThe United States

Summary of the energy taxation survey of electricity,fuels, district heat and transport in the EU and EFTAcountries, Japan and the United States released byFinnish Energy Industries in November 2010.

ENERGY TAXATION IN EUROPE,JAPAN AND THE UNITED STATES

TO THE READER

Almost all industrialised countries impose taxes onenergy. Transport fuels have carried a relativelyhigh fiscal tax for a long time. In Finland, the slumpof the early 1990s led to quickly increasing energytaxation, the primary goal of which was to makeup for the deficit in government finances. At thesame time, the other Nordic countries also raisedtheir energy taxes, but in most of the countriesenergy taxes were still at a low level at the time orenergy was not taxed at all, with the exception oftransport fuels.

The European Union made an attempt to standardiseenergy taxation practices as early as the beginningof the 1990s. However, it was only after manystages and the ratification of the financially muchmore heavyweight Emissions Trading Directive thatthe Energy Taxation Directive was approved in 2003.It lays down the structure of energy taxation andrelatively low minimum tax rates for fuels andpower.

The European Commission is currently updatingthe Energy Taxation Directive. According toinformation trickled from the Commission, the aimis to change the current taxation, based on energycontent, to become mainly based on carbonemissions. The taxation would steer particularlysectors outside emissions trading, and their minimumtax rates would be substantially raised. It is evidentthat the Commission will present its draft during2011.

The practices and levels of energy taxation varyconsiderably between countries. Therefore, it isessential to consider whether or not the nationaleconomies of high-taxation countries can sustainfurther increases in energy taxes in the increasinglytight global markets. On the other hand, regressiveenergy taxes substantially cut consumer demandfrom the other sectors of consumption. Thus, theyplace a particular burden on northern nationaleconomies, where energy consumption is relativelyhigh due to the cold climate and long distances.Naturally, energy is a tempting target for the taxman,as everyone needs it.

Comparative information on energy taxes is requiredboth by decision-makers and civil servants draftingthe taxation. Knowledge of energy taxation andestimates on its development are also necessaryfor businesses when making decisions on energyinvestments. Despite the increasing importance ofenergy taxation, only scant information on it isavailable.

This publication is a summary of the comparativeenergy tax survey published by Finnish EnergyIndustries in November 2010. The survey wascarried out to provide a basis for decision-makingconcerning energy taxation in central governmentand in industry, both in Finland and further afield.The main sources of the study were the EuropeanCommission, Eurostat, Euroheat & Power, Eurelectric,material published in the countries under scrutiny,as well as questionnaires on energy taxation sentto various parties in the relevant countries.

TAXATION OF ENERGY ANDTRANSPORT IN 30 COUNTRIES

The countries included in the survey are the EUmember countries (excl. Luxembourg and Cyprus)plus Iceland, Norway, Switzerland, Japan and theUnited States. In addition to Finland, taxation ondistrict heating was studied in Sweden, Norway,Denmark, Iceland, Poland, Austria, Italy, Franceand Germany.

The survey focuses on the taxation of electricityconsumption and generation, taxation of fuels inbusinesses and households, taxation of districtheating production and consumption, and taxationof transport. With regard to transport, the surveycovers the taxation of transport fuels and motorvehicle taxation based on environmental values, aswell as tax subsidies and monetary incentivesapplied to the purchase and use of electric vehicles.

The main focus of the survey is on excise taxation,but value added taxation and other tax-like chargesare also touched upon. Tax deductions andexemptions have been taken into consideration tothe extent that it has been possible on the basis ofthe material obtained.

Various exceptions and reliefs are often particularlydifficult to ascertain. Furthermore, the energy taxlegislation is extremely complex in some countries,with numerous tax levels. For this reason, we havebeen forced, to some degree, to use average ortypical tax levels of a consumer group under scrutiny.Some countries also apply tax-like charges, suchas feed-in tariffs, which have mostly been excludedfrom the comparison. However, they have beenmentioned in the actual report, if possible, but inthis brief summary only inasmuch as they are ofsignificant importance, as is the case in Germanelectricity taxation.

In Finland, the tax on fuels and electricity morethan doubled from the start of 2011. At the sametime, taxation of fuels was modified so that itconsists of energy content and carbon dioxidecomponents. Combined heat and power generation(CHP) fuels are subject to a 50 per cent reductionoff the carbon dioxide component. For Finland, thetax levels for both 2010 and 2011 are examined.

In many countries, the taxation of electricity consumptionvaries, depending on the business sector and volume ofconsumption. There are differences in the taxation ofelectricity between industrial and service companies insix countries, namely Austria, Norway, Sweden, Germany,Finland and Denmark. The highest business power taxlevels with no relief for energy-intensive industries are inItaly, Germany and the Netherlands. The taxation of powerconsumed by service companies, on the other hand, isby far the tightest in Denmark and Sweden.

The EU minimum levels in industrial power taxation areapplied by seven countries, and in service company powertaxation by four countries. In Great Britain, Portugal,Switzerland and the United States, companies are notsubject to power consumption tax at all.

In seven countries included in the study, electricityproduced by renewable energy sources was exemptedfrom electricity tax.

Energy-intensive industry is granted relief from powertaxation in the Netherlands, Belgium, Italy, Austria,Lithuania, Norway, Sweden and Denmark, as well as inFinland.

Electricity consumption taxes for households are by farthe highest in Denmark. The EU minimum tax level forelectricity is applied by five member countries. In ninecountries, seven of them EU member states, there is noelectricity tax at all for households.

As a rule, power generation fuels are not taxed in the EUcountries. This is due to the EU Energy Taxation Directive,which stipulates that the member states must exemptfrom taxation energy products and electricity used forpower generation. However, the member states may settaxes on these products for environmental reasons. Ofthe EU countries, Italy, Lithuania and the Czech Republicmake use of this option for certain fuels. Of countriesoutside the EU included, Japan and Norway impose taxeson fuels used for power generation, although in Norwayalmost all electricity is produced by hydropower and thetax on fuels has no impact on power generation.

In Sweden and Denmark all power generation fuels aresubject to sulphur and nitrogen taxes, which thereforealso apply to renewable fuels. Nuclear fuel is not taxedin any European country. In Japan, nuclear fuel is subjectto tax at 13%.

In addition to Finland, only in Sweden, Norway and Spainare power plants taxed differently from general propertytax rates. The property tax separately levied on powerplants is the highest in Finland, if the municipal authoritydecides to apply the maximum permitted property tax(2.85%).

Other taxes and tax-like charges levied on power companiesin the countries under study may be divided into taxationof emissions (e.g. carbon dioxide, sulphur, nitrogen andair pollutants), regional taxes and charges levied by localauthorities, taxation of certain methods of powergeneration, and other taxes and charges.

Sulphur and nitrogen taxes or tax-like charges are appliedat least in Sweden, Denmark, Norway, Spain, Italy, Latvia,Hungary and Estonia. Carbon dioxide taxes on powergeneration fuels are only applied in some autonomousregions in Spain. In several countries, power companiespay local authorities at municipal and provincial levelvarious charges, e.g. for operating permits, use ofwaterways and land areas, and transformers.

Nuclear power in particular is subject to taxes and chargesdiffering from those imposed on other power production.They include taxes levied on nuclear waste and dismantlingof power plants, as well as e.g. taxes based on the thermaloutput of the nuclear reactor and the area of the buildingsconstructed within the restricted power plant area. InFinland, the financial resources for nuclear wastemanagement are collected by the government into theNational Nuclear Waste Fund.

TAXATION OF ELECTRICITY

Ital

y

Ger

man

y

Net

her

lands

Fran

ce

Fin

lan

d 2

01

1

Bel

giu

m

Pola

nd

Est

onia

Japan

Slo

venia

Fin

lan

d 2

01

0

Gre

ece

Den

mar

k

Slo

vaki

a

Cze

ch R

epublic

Bulg

aria

Latv

ia

Mal

ta

Hungar

y

Norw

ay

Sw

eden

Lith

uan

ia

Spai

n

EU

min

imum

Irel

and

Aust

ria

Rom

ania UK

Port

ugal

Sw

itze

rlan

d

US

1,6

1,4

1,2

1

0,8

0,6

0,4

0,2

0

ELECTRICITY TAXES FOR INDUSTRY, C/KWH

The diagram compares industrial companies typically consuming less than 10,000 MWh/year. In Germany, 2.21 c/kWh in additional various tax-like charges and network costs are levied. Several countries have various types of energy tax rebate procedures for industry: these are not

included in the diagram.

1,3

5

1,2

3

1,0

8

0,7

6

0,7

03

0,5

02

0,5

01

0,4

47

0,3

5

0,3

05

0,2

63

0,2

5

0,1

34

0,1

32

0,1

14

0,1

0,1

0,0

562

0,0

53

0,0

5

0,1

0,1

0,0

5

0,0

5

0,0

5

0,0

5

0,0

521

0 0 0 0

Den

mar

k

Sw

eden

Ger

man

y

Fin

lan

d 2

01

1

Norw

ay

Ital

y

Net

her

lands

Fin

lan

d 2

01

0

Fran

ce

Bel

giu

m

Pola

nd

Est

onia

Japan

Slo

venia

Gre

ece

Slo

vaki

a

Cze

ch R

epublic

Bulg

aria

Latv

ia

Mal

ta

Hungar

y

Lith

uan

ia

Spai

n

EU

min

imum

Irel

and

Rom

ania

Aust

ria

UK

Port

ugal

Sw

itze

rlan

d

US

12

10

8

6

4

2

0

ELECTRICITY TAXES FOR SERVICE COMPANIES, C/KWH

Den

mar

k

Sw

eden

Ital

y

Ger

man

y

Fin

lan

d 2

01

1

Net

her

lands

Aust

ria

Norw

ay

Fran

ce

Fin

lan

d 2

01

0

Pola

nd

Gre

ece

Est

onia

Japan

Slo

venia

Bel

giu

m

Cze

ch R

epublic

Bulg

aria

Spai

n

Rom

ania

Mal

ta

EU

min

imum US

UK

Sw

itze

rlan

d

Slo

vaki

a

Port

ugal

Lith

uan

ia

Latv

ia

Irel

and

Hungar

y

12

10

8

6

4

2

0

ELECTRICITY CONSUMPTION TAXES FOR HOUSEHOLDS, C/KWH

In Germany, 3.97 c/kWh in various additional tax-like charges and network costs are levied.

For the Netherlands, the typical tax rate quoted by Eurostat of 1.6 c/kWh is applied, which is equivalent to annual electricity consumption of3,430 kWh. In Germany, 3.97 c/kWh in various additional tax-like charges and network costs are levied.

Norw

ay

Sw

eden

Fin

lan

d 2

01

1

Fin

lan

d 2

00

9

Den

mar

k

Irel

and

Aust

ria

Ger

man

y

Cyp

rus

Luxe

mbourg

Net

her

lands

Spai

n

UK

Fran

ce

Mal

ta

Slo

venia

Port

ugal

Cze

ch R

epublic

Slo

vaki

a

Hungar

y

Gre

ece

Cro

atia

Est

onia

Pola

nd

Bulg

aria

Latv

ia

Lith

uan

ia

Turk

ey

Rom

ania

1 400

1 200

1 000

800

600

400

200

0

DOMESTIC ELECTRICITY COSTS PER YEAR, EUROS/PERSON

Domestic electricity usage varies considerably in different countries due to seasonal differences in particular, as well as the composition of energyuse. The combined burden of electricity price and taxes should therefore be compared also as an annual total cost to households, when assessing

e.g. the effect of taxation on purchasing power or inflatory development.

VAT

Energy Tax

Electricity

9,6

8

2,9

7

2,0

5

1,7

1,3

5

1,3

5

1,0

8

0,8

8

0,7

6

0,5

02

0,5

01

0,4

47

0,3

5

0,3

05

0,2

5

0,1

32

0,1

14

0,0

5

0,1

0,1

0,0

5

0,0

5

0,0

5

0,0

5

0 0 0 00,1

0,1

0,0

15

9,6

8

2,9

7

2,3

4

2,0

5

1,7

0

1,6

0

1,5

0

1,3

5

1,2

1

0,8

83

0,5

01

0,5

00

0,4

47

0,3

50

0,3

05

0,1

9

0,1

14

0,1 0,1

0,1

0,1

0,1

0 0 0 00 0 0 00

1242

713

615

566

456

415

393

391

389

375

337

292

282

272

254

241

216

188

183

89

205

204

89

80

771

24176

74

55

In the study, the fuel tax levels of Norway, Sweden andDenmark vary between companies, depending on whetheror not they belong to the EU emissions trading scheme.With regard to excise duties on heavy fuel oil, natural gasand coal, the study includes excise duties in the EU andNorway that are levied on companies within EU emissionstrading. The excise duties on light fuel oil are included inrelation to households and companies outside emissionstrading.

From the beginning of 2011, Finland imposes the highesttax on heavy fuel oil in business use. The taxes are thenext highest in Great Britain and Norway. Of the otherNordic countries, Sweden levies a significantly lower taxon heavy fuel oil than Finland in 2011, and Denmark nonewhatsoever. In Denmark, natural gas, oil and coal productsused in light and heavy industrial processes are completelyexempted from energy tax and, within EU emissionstrading, also from carbon dioxide tax. Ten EU memberstates impose taxes on heavy fuel oil according to the EUminimum rate.

Light fuel oil is subject to the heaviest tax in business usein Greece, Italy and Malta.

Natural gas is most highly taxed in business use by Malta,Switzerland and Austria in 2010. Ten countries impose noexcise duties at all on natural gas used by businesses.

Finland levies the highest tax on coal in 2011. In 2010,the highest taxes on coal were imposed by Switzerland,Norway and Finland.

Light fuel oil in domestic use is most highly taxed inGreece, Italy and Sweden. In the United States and GreatBritain, value added tax is the only tax levied on light fueloil in domestic use. The combined tax burden of exciseduty and value added tax is the heaviest in Sweden,Greece and Denmark.

The highest excise duties on domestic use of natural gasare in Denmark, Sweden and the Netherlands. The samecountries impose the highest taxes on natural gas alsowhen value added tax is included.

In addition to the Nordic countries, of the countriesincluded in the study also Spain, Ireland, Latvia, Slovenia,Switzerland and Estonia levy a carbon dioxide-based taxon heating and transport fuels.

It transpires that the carbon dioxide taxation in Swedenis clearly the highest of the countries included, EUR110/carbon dioxide tonne. The carbon dioxide tax ratesof the other countries vary between EUR 2–50/tCO2, theEstonian tax being the lowest and that levied by Finlandin 2011 the second highest after Sweden. Sweden’s highcarbon dioxide tax is explained by the structure of Swedishenergy taxation, where the carbon dioxide tax is anelement considerably greater than fiscal energy tax.However, the carbon dioxide tax relief to industry grantedby Sweden brings the tax levels for Swedish industry onaverage to that of the other countries, and from the startof 2011, also below the tax levels in Finland. Exemptionsor relief on carbon dioxide taxes are granted to companieswithin EU emissions trading in Sweden, Norway, Denmarkand Latvia.

TAXATION OF FUELS

TAXES ON HEAVY FUEL OIL FOR BUSINESSES, EUROS/TONNE

Fin

lan

d 2

01

1

UK

Norw

ay

Fin

lan

d 2

01

0

Irel

and

Aust

ria

Slo

venia

Sw

eden

Net

her

lands

Ital

y

Slo

vaki

a

Bulg

aria

Ger

man

y

Gre

ece

Cze

ch R

epublic

Japan

Fran

ce

Pola

nd

Hungar

y

Latv

ia

Port

ugal

Lith

uan

ia

Rom

ania

Mal

ta

Est

onia

Bel

giu

m

Spai

n

EU

min

imum

Den

mar

k

Sw

itze

rlan

d

US

200

180

160

140

120

100

80

60

40

20

0

Companies within EU emissions trading.

188

132

123

67

62,7

60

55

49,2

33,7

31,4

26,6

25,6

25

19

19

18,7

18,5

16

15,6

15,5

15,3

15,1

15,1

15 15 15

15 15

0 0 0

TAXES ON LIGHT FUEL OIL FOR HOUSEHOLDS, EUROS/1,000 L

Sw

eden

Gre

ece

Den

mar

k

Ital

y

Hungar

y

Rom

ania

Net

her

lands

Norw

ay

Fin

lan

d 2

01

1

Port

ugal

Slo

venia

Est

onia

Fin

lan

d 2

01

0

Aust

ria

Mal

ta

Spai

n

Latv

ia

Irel

and

Pola

nd

Fran

ce

Ger

man

y

Slo

vaki

a

Bulg

aria

Cze

ch R

epublic

Lith

uan

ia

Bel

giu

m

EU

min

imum

Sw

itze

rlan

d

US

UK

Japan

700

600

500

400

300

200

100

0

TAXES ON COAL FOR BUSINESSES, EUROS/TONNE

Fin

lan

d 2

01

1

Sw

itze

rlan

d

Norw

ay

Fin

lan

d 2

01

0

Aust

ria

Sw

eden

Slo

venia

Net

her

lands

Slo

vaki

a

Bel

giu

m

Fran

ce

Latv

ia

Hungar

y

Cze

ch R

epublic

Ger

man

y

Bulg

aria

Est

onia

Mal

ta

Gre

ece

Japan

Ital

y

Irel

and

Port

ugal

Lith

uan

ia

EU

min

imum

Rom

ania

Spai

n

Den

mar

k

US

Pola

nd

UK

160

140

120

100

80

60

40

20

0

Companies within EU emissions trading.

128,1

73,0

62,5

50,0

50,5

41,7

32,5

13,2

10,6

9,8

4

8,5

7

8,4

7

8,4

3

8,4

1

8,1

2

7,5

5

7,3

8

7,3

8

7,3

8

6,5

3

4,6

0

4,1

8

4,1

6

3,7

7

3,6

9

0,5

4

0,5

4

TAXES ON NATURAL GAS FOR BUSINESSES, EUROS/MWH

Companies within EU emissions trading.

Fin

lan

d 2

01

5

Fin

lan

d 2

01

3

Mal

ta

Fin

lan

d 2

01

1

Sw

itze

rlan

d

Aust

ria

Ger

man

y

Slo

venia

Spai

n

Net

her

lands

Sw

eden

Irel

and

Est

onia

Fin

lan

d 2

01

0

Ital

y

Slo

vaki

a

Cze

ch R

epublic

Fran

ce

Hungar

y

Japan

Rom

ania

EU

min

imum

Bel

giu

m

Norw

ay

Den

mar

k

US

UK

Port

ugal

Pola

nd

Lith

uan

ia

Latv

ia

Gre

ece

Bulg

aria

16

14

12

10

8

6

4

2

0

13,7

11,5

9,3

6

6,7

2

9,0

2

6,6

0

5,5

0

4,4

2

4,1

4

4,0

0

3,5

9

2,7

7

2,5

2

2,1

0

1,8

7

1,3

2

1,2

3

1,1

9

1,1

2

0,7

86

0,6

14

0,5

40

0,3

27

VAT

Excise Duties

626

620

617

568595

471

381

365

322

272

239

233

232

219

207

190

187

185

183

171

170

155

134

132

127

126

102

89

27

24

20

0 0 0 0 0 0 0 0 0 0

0 0 0 0

District heating fuels are subject to energy taxes incommon with other fuels (see Taxation of fuels).

In the district heat generation of the countries surveyed,heavy fuel oil and coal are the most highly taxed. Taxationof natural gas in district heat production would rise inFinland in 2013 to the highest level of all the countriesnow surveyed, if the tax levels of the other countriesremain unchanged.

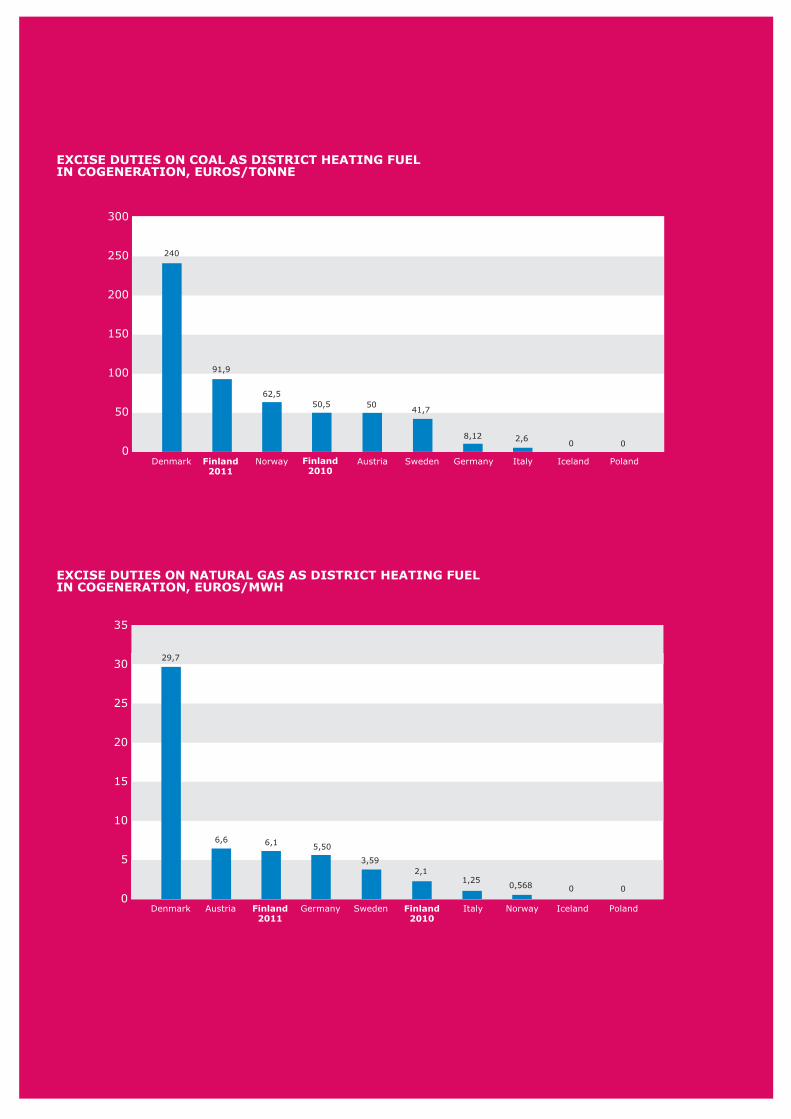

Taxation of fuels used for heat production in power anddistrict heat cogeneration is by far the highest in Denmark.The taxes levied on coal for heat production in cogenerationin 2011 in Finland are the second highest, and those onnatural gas and heavy fuel oil the third highest.

Tax incentives on the production of district heating throughcogeneration exist in Finland, Sweden, Germany andDenmark. In the countries studied, no other taxes werelevied on district heat production.

Iceland is the only country where district heatingconsumption was subject to a special consumption tax.This is a two per cent resource tax levied on the retailprice. In Iceland, Norway, Italy and France, a reducedrate of value added tax is applied to district heating.

In two countries, electricity produced in heat and powercogeneration is exempted from electricity tax.

TAXATION OF DISTRICTHEATING

100

90

80

70

60

50

40

30

20

10

0

SHARES OF DISTRICT HEATING ON HEATING MARKETS IN 2007, %

Iceland Sweden Denmark Finland Poland Austria Germany France Norway Italy

94

55

50 4947

18

13

5 4,82,5

Euroheat & Power, ecoheat4.eu.

35

30

25

20

15

10

5

0

EXCISE DUTIES ON NATURAL GAS AS DISTRICT HEATING FUELIN COGENERATION, EUROS/MWH

IcelandSwedenDenmark Finland2011

Austria Germany PolandNorwayItalyFinland2010

300

250

200

150

100

50

0

EXCISE DUTIES ON COAL AS DISTRICT HEATING FUELIN COGENERATION, EUROS/TONNE

IcelandSwedenDenmark Finland2011

Austria Germany PolandNorway ItalyFinland2010

240

91,9

62,550,5 50

41,7

8,12 2,60 0

29,7

6,6 6,1 5,50

3,592,1

1,250,568 0 0

Of the countries included in the study, diesel is the mosthighly taxed in Great Britain, Norway and Switzerland, ifthe excise duty and value added tax are added together.The lowest taxes by a long way are levied in the UnitedStates.

The highest taxes on petrol, with excise duty and valueadded tax combined are in Norway, the Netherlands,Greece and Great Britain. In Finland, the total taxationon petrol is the fifth highest after the above countries.

The study also looks at environment-based motor vehicletaxation. In eleven countries, the registration charge ofa new vehicle is based on carbon emissions. The registrationcharge may also be based on engine size, or on price andfuel consumption, as is the case in Austria. Vehicles withthe lowest emissions are completely exempt from theregistration charge in the Netherlands and Spain. Bulgaria,Great Britain, Luxembourg, Sweden, Germany, Slovakia,the Czech Republic and Estonia do not levy a registrationcharge at all.

In eight countries, the annual vehicle tax is based oncarbon emissions. In some countries, such as Denmark,the vehicle tax is based on fuel consumption. Vehicleswith the lowest emissions are completely exempt fromthe annual vehicle tax in Great Britain, Sweden andGermany.

In Spain, Luxembourg, Portugal and France, peoplepurchasing a new low-emission car receive an incentivepayment if they scrap an old or high-mileage car at thesame time. The payment varies between EUR 500 andEUR 2,500. An old car is defined as one more than 10years old in all the above countries.

The purchase and use of electric vehicles is subsidised inmany countries through taxation. In seven countries,electric cars are entitled to relief or full exemption fromregistration charges. Similarly, exemption from the annualvehicle tax is granted in seven of the countries includedin the survey.

In Spain, Great Britain, Cyprus and France, direct monetarysubsidies are available for the purchase of electric vehiclesor new low-emission cars. The sum varies betweenEUR 700 and EUR 6,000.

Other benefits granted to purchasers of electric vehiclesinclude the right to deduct 30% of the vehicle purchaseprice in income taxation in Belgium, the right to drive onbus lanes, free parking in public car parks, exemptionfrom road tolls and car ferry charges in Norway, and areduced tax rate on electric vehicles for businesses inSweden.

TAXATION OF TRANSPORT

TAXES ON PETROL, EUROS/LITRE

Norw

ay

Net

her

lands

Gre

ece

UK

Fin

lan

d 2

01

2

Fin

lan

d 2

01

0

Ger

man

y

Bel

giu

m

Den

mar

k

Sw

eden

Fran

ce

Port

ugal

Ital

y

Irel

and

Cze

ch R

epublic

Sw

itze

rlan

d

Slo

vaki

a

Slo

venia

Hungar

y

Lith

uan

ia

Aust

ria

Mal

ta

Pola

nd

Est

onia

Spai

n

Rom

ania

Latv

ia

Japan

Bulg

aria

EU

min

imum US

1,2

1

0,8

0,6

0,4

0,2

0

TAXES ON DIESEL, EUROS/LITRE

UK

Norw

ay

Sw

itze

rlan

d

Sw

eden

Den

mar

k

Fin

lan

d 2

01

2

Irel

and

Ger

man

y

Gre

ece

Cze

ch R

epublic

Slo

venia

Ital

y

Fran

ce

Net

her

lands

Fin

lan

d 2

01

0

Est

onia

Hungar

y

Port

ugal

Bel

giu

m

Slo

vaki

a

Aust

ria

Latv

ia

Mal

ta

Pola

nd

Rom

ania

Spai

n

Bulg

aria

EU

min

imum

Lith

uan

ia

Japan US

1,2

1

0,8

0,6

0,4

0,2

0

VAT

Excise Duties

VAT

Excise Duties

0,9

1

0,7

9

0,7

5

0,7

1

0,6

8

0,6

8

0,6

6

0,6

6

0,6

5

0,6

5

0,6

4

0,6

2

0,6

1

0,6

0

0,5

8

0,5

7

0,5

7

0,5

5

0,5

2

0,5

1

0,5

5

0,5

0

0,4

9

0,4

70,5

1

0,5

2

0,4

6

0,4

5

0,3

3

0,0

8

0,5

7

0,9

9

0,9

5

0,9

5

0,9

1

0,9

0

0,9

0

0,8

7

0,8

6

0,8

5

0,8

4

0,8

2

0,8

2

0,7

9

0,7

7

0,7

3

0,7

3

0,7

1

0,6

4

0,6

3

0,6

00,6

6

0,6

0

0,5

5

0,5

50,6

2

0,6

3

0,5

5

0,5

2

0,4

9

0,0

7

0,7

0

CHARGES, TAXES AND SUBSIDIES ON A NEW MOTOR VEHICLE

ACEA - European Automobile Manufacturers’ Association. Dash (-) denotes the absence of the charge or subsidy.

Country

Austria

Belgium

BulgariaCyprus

Czech RepublicDenmark

EstoniaFinland

France

Germany

Great Britain

Greece

HungaryIreland

ItalyLatviaLithuaniaLuxembourg

Malta

The NetherlandsPolandPortugal

Romania

SlovakiaSloveniaSpain

Sweden

General VAT

20

21

2015

2025

2023

19.6

19

17.5(20 % in 2011)

23

2521

20212115

18

192221

24

192018

25

Registration charge

Based on price and fuel consumption. Benefitor environmental tax of max. 16 %.Based on engine capacity and age; inWallonia on CO2 emissions.

–Based on engine capacity and CO2emissions.–Based on price: 105% up to EUR 10,600,180% of remainder–Based on price and CO2 emissions. Tax %= 4.88 + (0.122 x CO2). Min. 12.2%, max.48.8%.Based on CO2 emissions; EUR 200(<156–160 g/km) – EUR 2,600(>over 245 g/km).

–

–

Based on engine capacity and emissions.5–50 %. Electric and hybrid vehicles exemptfrom registration charge.Based on emissions.Based on CO2 emissions: 14%(max. 120 g/km) – 36% (>225 g/km).

± EUR 300.Based on CO2 emissions.EUR 15.–

Based on price, CO2 emissions and vehiclelength.Based on price and CO2 emissions.Based on engine capacity: 3.1–18.6%.Based on engine capacity and CO2emissions.

Based on engine capacity and CO2emissions.–Based on price: 1–13%.Based on CO2 emissions; registration chargefrom 0 per cent (emissions <120 g/km) to14.75 per cent (>200 g/km).

–

Environmentbased taxation, taxsubsidies and direct financial subsidy–

Reductions on vehicle purchase price ofvehicles with emissions below 115 g/kmmax. EUR 4,540.–Annual motor vehicle tax based on enginecapacity and CO2 emissions.–Annual motor vehicle tax based on fuelconsumption of the vehicle.––

Buyer of new vehicle with max. emissionsof 125 g/km receives EUR 5,000 bonus.Buyer of new vehicle with max. emissionsof 155 g/km receives incentive payment ofEUR 500, if old car scrapped at the sametime. Environmental charge and annualenvironmental tax for highemission vehicles.Annual motor vehicle tax based on CO2emissions.Annual motor vehicle tax based on CO2emissions.–

–Annual motor vehicle tax based on CO2emissions: EUR 104 (max. 120 g/km) –EUR 2,100 (> 225 g/km).–––Annual motor vehicle tax based on CO2emissions. Buyer of new vehicle with max.emissions of 120 g/km receives incentivepayment of EUR 2,500 and of 120150 g/kmEUR 1,500, if old car scrapped at the sametime.Annual motor vehicle tax based on CO2emissions and age of vehicle.––Buyer of new vehicle with max. emissionsof 130 g/km receives incentive payment ofEUR 1,0001,250, if old car scrapped at thesame time.–

––Buyers of new vehicle with max. emissionsof 149 g/km receive incentive payment ofEUR 2,000, if old car scrapped at the sametime.Annual motor vehicle tax based on CO2emissions. Vehicles classified asenvironmentally friendly exempt from motorvehicle tax.

SUBSIDIES ON THE PURCHASE AND USE OF AN ELECTRIC VEHICLE

ACEA - European Automobile Manufacturers’ Association.

Austria

Belgium

Cyprus

Czech Republic

Denmark

Finland

France

Germany

Great Britain

Greece

Ireland

Norway

Portugal

Spain

Sweden

Vehicles using alternative fuel receive additional bonus of max. EUR 500 at time of registration. Electric vehicles are exempt from registration charge and monthly motor vehicle tax.

Buyers of electric vehicles can deduct 30% of electric vehicle purchase price in taxation on income,max. EUR 9,000.

A subsidy of EUR 700 granted for purchasing an electric vehicle. A company or person is eligible forthe subsidy for a maximum of seven vehicles.

Electric and hybrid vehicles and other vehicles running on alternative fuels are exempt from roadtax. Road tax is only payable on vehicles used for commercial purposes.

Electric vehicles running purely on electricity are exempt from registration charge and pay the lowestpossible annual motor vehicle tax. However, rechargeable hybrid vehicles are not exempted fromthe registration charge.

Motive power tax of electric cars was reduced from the start of 2011 by an average of 77%, ofrechargeable diesel hybrid car by 27%, and of rechargeable petrol hybrid car by over 90%.

A subsidy is available for the purchase of a new vehicle with CO2 emissions not exceeding 125 g/km.The maximum subsidy is EUR 5,000 for vehicles with emissions not exceeding 60 g/km. The subsidysum must not be in excess of 20% of the vehicle purchase price inclusive of VAT. If the battery isleased, the battery cost is added to the purchase price applied to determine the subsidy. Hybridvehicles with emissions of 135 g/km or less receive a subsidy of EUR 2,000.

Electric vehicles are exempt from annual motor vehicle tax for five years, starting from the date offirst registration.

Electric vehicles exempt from annual motor vehicle tax. Electric vehicles exempt from companyvehicle tax for five years. Electric vans entitled to fiveyear exemption from charge (EUR 3,500)payable for the benefit derived from the van. From 2011, buyers of electric vehicles (incl. rechargeablehybrid cars) entitled to 25 per cent reduction off list price of the vehicle, with maximum reductionEUR 5,900.

Electric and hybrid vehicles exempt from registration charge.

Electric and hybrid vehicles receive max. EUR 2,500 deduction from registration charge.

At time of purchase, electric vehicles are exempt from both car tax and value added tax, and theypay a very low annual registration charge. An electric vehicle may be parked free of charge in carparks owned by public authorities. Owners of electric vehicles are exempt from road tolls and alsofares for cars on national car ferries. Electric vehicles also have a higher mileage allowance in thepublic sector.

Electric vehicles are fully exempted from registration charge, and hybrid vehicles receive a 50 percent reduction.

Buyers of electric vehicle receive max. 20% subsidy off vehicle sale price (max. EUR 6,000).

Five-year exemption from annual motor vehicle tax for hybrid vehicles (emissions max. 120 g/km)and electric vehicles consuming 37 kWh/100 km in electricity. The taxable value of electric and hybridvehicles is reduced by 40% in company vehicle taxation compared to corresponding petrol or dieselvehicles. Maximum reduction EUR 1,750 per annum.

The complete survey reportin Finnish is available at

www.energia.fi

or may be ordered in printedformat from Finnish EnergyIndustries. Please send anycomments on the survey [email protected].

Finnish Energy Industries

Fredrikinkatu 51-53 BP.O. Box 100FI-00101 HelsinkiTel. +358 (0)9 530 520Fax +358 (0)9 5305 2900

ET Brussels Office17, Rue de la Charité, 5th floorB-1210 Brussels, BelgiumTel. +358 (0)9 1728 5301Gsm +358 (0)40 569 6996Fax +32(0)2 223 0805

www.energia.fi

Ma

ino

sto

imis

to L

ain

e/S

uo

me

n G

raa

fise

t P

alv

elu

t 2

01

1

Related Documents