RESILIENT EnerCom Oil & Services Conference February 17, 2010

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

RESILIENT

EnerCom Oil & Services Conference

February 17, 2010

2

Forward-Looking Statements

Statements made by representatives of LINN Energy, LLC during the course of this presentation that

are not historical facts are forward-looking statements. These statements are based on certain

assumptions and expectations made by the Company which reflect management’s experience,

estimates and perception of historical trends, current conditions, anticipated future developments and

other factors believed to be appropriate. Such statements are subject to a number of assumptions,

risks and uncertainties, many of which are beyond the control of the Company, which may cause

actual results to differ materially from those implied or anticipated in the forward-looking statements.

These include risks relating to financial performance and results, our indebtedness under our credit

facility, availability of sufficient cash flow to pay distributions and execute our business plan, prices

and demand for gas, oil and natural gas liquids, our ability to replace reserves and efficiently develop

our current reserves, our ability to make acquisitions on economically acceptable terms, and other

important factors that could cause actual results to differ materially from those anticipated or implied

in the forward-looking statements. See “Risk Factors” in the Company’s 2008 Annual Report on Form

10-K, 2009 Quarterly Report on Form 10-Q for the period ended September 30, 2009, and any other

public filings and press releases. LINN Energy undertakes no obligation to publicly update any

forward-looking statements, whether as a result of new information or future events. This

presentation has been prepared as of February 9, 2010.

LINN Energy’s mission is to acquire, develop

and maximize cash flow from a growing portfolio of

long-life oil and natural gas assets.

4

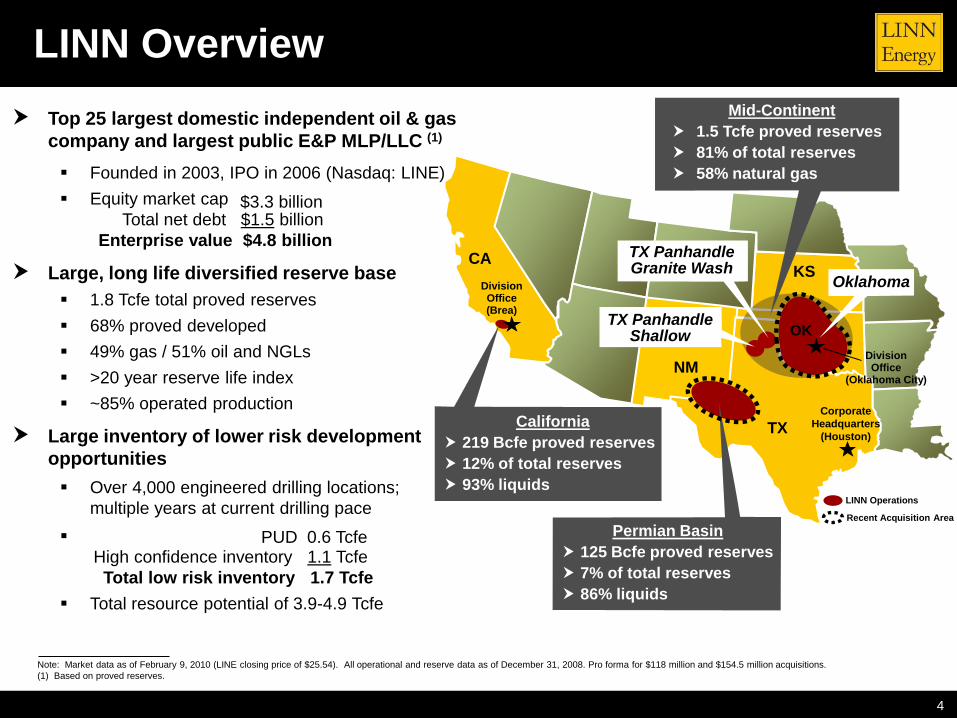

Top 25 largest domestic independent oil & gas

company and largest public E&P MLP/LLC (1)

Founded in 2003, IPO in 2006 (Nasdaq: LINE)

Equity market cap

Total net debt $1.5 billion

Enterprise value $4.8 billion

Large, long life diversified reserve base

1.8 Tcfe total proved reserves

68% proved developed

49% gas / 51% oil and NGLs

>20 year reserve life index

~85% operated production

Large inventory of lower risk development

opportunities

Over 4,000 engineered drilling locations;

multiple years at current drilling pace

High confidence inventory 1.1 Tcfe

Total low risk inventory 1.7 Tcfe

Total resource potential of 3.9-4.9 Tcfe

$3.3 billion

PUD 0.6 Tcfe

LINN Overview

Note: Market data as of February 9, 2010 (LINE closing price of $25.54). All operational and reserve data as of December 31, 2008. Pro forma for $118 million and $154.5 million acquisitions.

(1) Based on proved reserves.

KS

Corporate

Headquarters

(Houston)

Division Office(Brea)

CA

TX

Division Office

(Oklahoma City)

California

219 Bcfe proved reserves

12% of total reserves

93% liquids

Permian Basin

125 Bcfe proved reserves

7% of total reserves

86% liquids

OK

TX PanhandleGranite Wash

TX PanhandleShallow

Mid-Continent

1.5 Tcfe proved reserves

81% of total reserves

58% natural gas

NM

LINN Operations

Recent Acquisition Area

Oklahoma

5

Mature U.S. oil and natural gas basins provide significant opportunity for

future growth and consolidation

LINN’s strategy is to :

Acquire mature oil and natural gas properties with the appropriate attributes

Asset Attributes

• Stable, long-life production

• High percentage of PDP

• Shallow decline

• Long reserve life index

• Low-risk, low-cost repeatable drilling

Efficiently operate and develop acquired properties

Reduce commodity price and interest rate risk through hedging

Return cash flow through the form of a distribution payment to unitholders

LINN’s Strategy

6

Attractive Acquisition Margins

(1) Represents weighted average blended five year forward oil and gas strip prices as of the closing date of acquisitions completed during the year. Source: Bloomberg.

Despite rising acquisition costs, acquisition margins remain strong

$4.65 $4.82

$6.42

$9.98

$7.92

$14.34 $13.92

$14.44

$0.83 $0.68

$2.10 $1.61

$2.41 $1.58 $1.63 $2.13

$4.32

$8.37 $5.51

$12.76 $12.29 $12.31

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

2003 2004 2005 2006 2007 2008 2009 2010

NYMEX Five Year Forward Strip ($ per Mcfe) (1)

LINN Weighted Average Acquisition Cost ($ per Mcfe)

$3.82 $4.14

7

Mid-Continent: Greater Stiles Ranch AreaTexas Panhandle Granite Wash Horizontal Well Activity

LINN spuds first horizontal well

0 4,000'

Scale

DYCO

STILES RANCH

Hemphill County

Newfield – McCoy 27-10H

IP: 12.0 MMcf/d

Newfield – Thomas 5-5H

IP: 20.0 MMcf/d

Newfield – Britt D 4-3H

IP: 21.0 MMcf/d

Newfield – McCoy 27-7H

IP: 25.0 MMcf/d

FRYE

RANCH

Devon – Zybach Truman 16-7H

IP: 14.9 MMcf/d

Devon – Holmes 17-5H

IP: 6.6 MMcf/dForest – Zybach 507H

IP: 17.0 MMcf/d

Newfield – Williams 33-7H

IP: 21.0 MMcf/d

Wheeler CountyDevon –Truman Zybach 16-10HIP: 8.3 MMcf/d

Samson – Zybach 313H

IP: 10.0 MMcf/d

Devon – Holmes 17-4H

IP: 11.8 MMcf/d

Tom Puryear 5-28H(Non-operated)

Newfield – Britt Ranch 14-13H

IP: 8.0 MMcf/d

Samson – Zybach 213H

IP: 5.9 MMcf/dNewfield – McCoy 27-8H

IP: 21.0 MMcf/d

Forest – Blasdale 204-1H

IP: 10.4 MMcf/d, 1,300 Bopd +

2,000 Bbls/d NGL’s

Chesapeake – Reed T 8H

IP: 5.6 MMcf/d

Forest Wells IP: 15.1 MMcf/d, 1,200 Bopd + 2,400 Bbls/d NGL’s

IP: 16.0 MMcf/d, 1,300 Bopd + 2,200 Bbls/d NGL’s

Industry Producing Wells

Industry Wells with IP’s

Industry Wells Permitted

1.0 – 3.1 MMcf/d

3.1 – 5.3 MMcf/d

LINN Acreage

Greater Stiles Ranch Area

~27,000 Gross Acres

~13,500 Net AcresLINN Peak Production from

Vertical Wells

Current Drilling Location

Waiting on Completion

8

Low risk asset base (1)

1.8 Tcfe of proved reserves

>20 year reserve life

68% proved developed

Financial flexibility

Extended maturity of credit facility to August 2012

($1.64 billion committed borrowing base)

2Q 2009, $250 million senior notes offering and $103 million public equity offering

4Q 2009, $189 million public equity offering

Borrowing capacity, including available cash, of ~$595 million at October 31, 2009

High levels of hedging

~100% of current production hedged through 2011

~100% of Mid-Continent basis hedged through 2011

~100% of floating interest rate expense hedged through 2013

Financial Strength

(1) Reserve data as of December 31, 2008. Pro forma for $118 million and $154.5 million acquisitions.

9

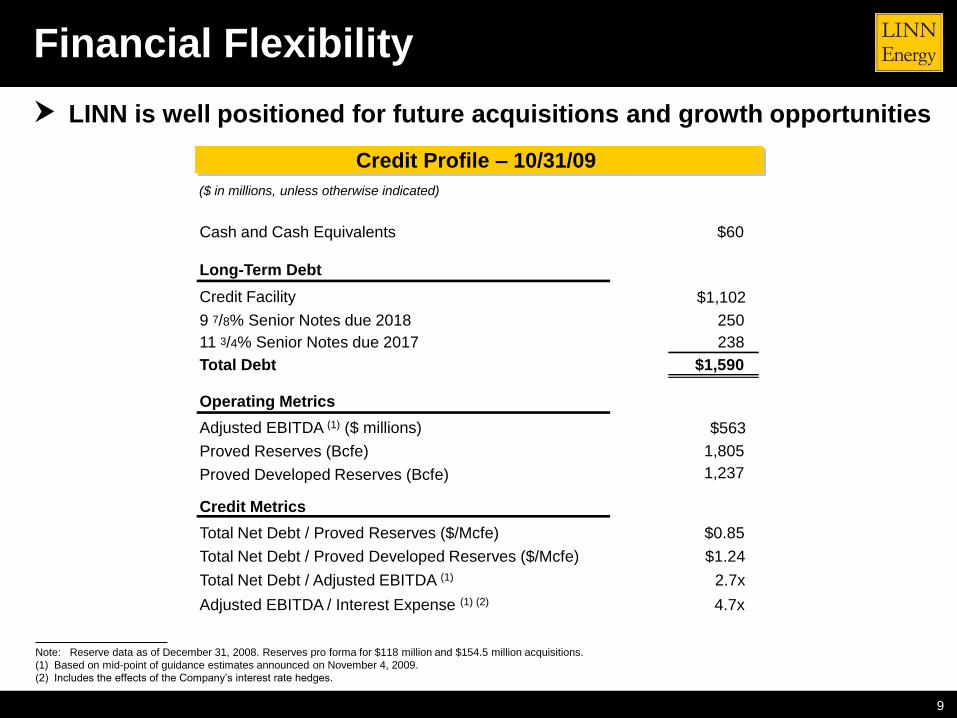

Note: Reserve data as of December 31, 2008. Reserves pro forma for $118 million and $154.5 million acquisitions.

(1) Based on mid-point of guidance estimates announced on November 4, 2009.

(2) Includes the effects of the Company’s interest rate hedges.

Financial Flexibility

LINN is well positioned for future acquisitions and growth opportunities

Credit Profile – 10/31/09

($ in millions, unless otherwise indicated)

Cash and Cash Equivalents

Credit Facility

9 7/8% Senior Notes due 2018

Total Debt

Operating Metrics

Adjusted EBITDA (1) ($ millions)

Proved Reserves (Bcfe)

Proved Developed Reserves (Bcfe)

Credit Metrics

Total Net Debt / Proved Reserves ($/Mcfe)

Total Net Debt / Proved Developed Reserves ($/Mcfe)

Total Net Debt / Adjusted EBITDA (1)

Adjusted EBITDA / Interest Expense (1) (2)

Long-Term Debt

11 3/4% Senior Notes due 2017

$60

250

$1,590

$0.85

$1.24

2.7x

4.7x

$1,102

238

1,805

$563

1,237

10

$90.00 $90.00 $100.00 $100.00

$90.00 $90.00

$110.00 $75.00

0

1,000

2,000

3,000

4,000

5,000

2010 2011 2012 2013

Vo

lum

e (

MB

bls

)

50%48%

$99.68 $82.50

Puts provide upside on hedged volumes Puts and collars provide upside on

hedged volumes

Gas Positions Oil Positions

Current Hedge Position

$9.50

$8.90

$8.84

$8.11

0.0

8.0

16.0

24.0

32.0

40.0

48.0

56.0

64.0

2010 2011

Vo

lum

e (

Bc

f)

Swaps Puts (1)

31%

39%

$8.66

$9.25

Percent Puts (2)

Approximately 100% hedged through 2011 provides cash flow stability

(1) Includes puts which settle on the Panhandle Eastern Pipeline Index (PEPL) to hedge basis differential associated with gas production in the Mid-Continent.

(2) Calculated as percentage of hedged volume in the form of puts.

(3) As presented in the table above, the Company has outstanding fixed price oil swaps on 6,000 Bbls per day at a price of $100.00 per Bbl for the years ending December 31, 2012, and

December 31, 2013. The Company has derivative contracts that extend the swaps for each of the years ending December 31, 2014, December 31, 2015, and December 31, 2016, if

the counterparties determine that the strike prices are in-the-money on a designated date in each respective preceding year. The extension for each year is exercisable without

respect to the other years.

(4) Includes collars with floor / ceiling prices of $90.00 / $112.00 and $90.00 / $112.25 on 250 MBbls and 276 MBbls of oil for FY 2010-FY 2011, respectively.

Percent Puts (2)Swaps (3) Collars (4) Puts (2)

11

102%

108%

44%

40%

29%

58%

0%

20%

40%

60%

80%

100%

120%

FY 2010E FY 2011E

LINE Swaps

% P

rod

uc

tio

n H

ed

ge

d

Note: 2009E production held flat for FY 2010E-2011E. LINN’s 2009E production based on mid-point of 2009E guidance announced on November 4, 2009. Source: RBC Capital Markets.

E&P Peer Group includes: Berry Petroleum, Comstock Resources, Encore Acquisition, Mariner Energy, Petrohawk, Quicksilver Resources, SandRidge Energy, Swift Energy and

Whiting Petroleum.

(1) 2009E peer group production per Wall Street research. Hedge data based on publicly available data.

LINE PutsLINE Collars

LINN Production Hedged vs. Peers

Hedged much more than peers while still preserving upside potential

Median Production Hedged Q3 09 (1)

12

Attractive Value & Liquidity in MLP Sector

Note: Market data as of February 9, 2010. Source: Bloomberg.

Last 3 Months Trading Data

LINN Energy offers:

Significant trading liquidity compared to MLP/LLC sector (55+ total)

No IDRs (no general partner burden on cash flow)

E&P sector provides more acquisition opportunities

Largest E&P MLP/LLC (less competition for larger acquisitions)

Yield spread of approximately 225 bps to midstream average

Average Average Daily Volume

Top 5 Most Liquid MLP/LLCs Ticker Price Units Traded Value ($MM) No IDRs Yield

Kinder Morgan Energy Partners, LP KMP $60.12 776 $46,636 6.86%

Enterprise Products Partners, LP EPD $31.05 1,282 $39,791 7.22%

Energy Transfer Partners, LP ETP $44.40 844 $37,461 8.10%

Linn Energy, LLC LINE $26.21 1,099 $28,817 9.87%

Plains All American Pipeline, LP PAA $52.30 346 $18,110 7.07%

13

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

1/13/06 7/18/06 1/20/07 7/25/07 1/27/08 7/31/08 2/2/09 8/7/09 2/9/10

LINE Total Return LINE Price Appreciation S&P Mid-Cap E&P Index S&P 500 Index

LINN Historical Return

Note: Market data as of February 9, 2010 (LINE closing price of $25.54). Source: Bloomberg.

LINN Total Return and Stock Price Appreciation (LINE IPO – 2/9/10)

21.62%

-9.20%

81.84%

18.49%

14

Note: Market data as of February 9, 2010 (LINE closing price of $25.54).

(1) The Q1 2006 distribution, adjusted for the partial period from the Company's closing of the IPO on January 19, 2006 through March 31, 2006, equates to $0.32 per unit.

Distribution History

Since IPO, LINN has generated a total return of approximately 82%

58% increase in quarterly distribution since IPO

Consistently paid the distribution for 16 quarters

Distribution History

$ 0.63

$9.08

$0.80

$1.23

$1.75

$2.27

$2.84

$3.41

$4.04

$4.67

$5.30

$5.93

$6.56

$7.19

$7.82

$8.45

$ 0.63

$ 0.43

$ 0.63

$ 0.40

$ 0.40

$ 0.52

$ 0.52

$ 0.57

$ 0.57

$ 0.63

$ 0.63

$ 0.63

$ 0.63

$ 0.63

$ 0.63

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

- Current Distribution - Cumulative Distribution

2006 2007 2008 2009

(1)

LINN Energy’s mission is to acquire, develop

and maximize cash flow from a growing portfolio of

long-life oil and natural gas assets.

Appendix

17

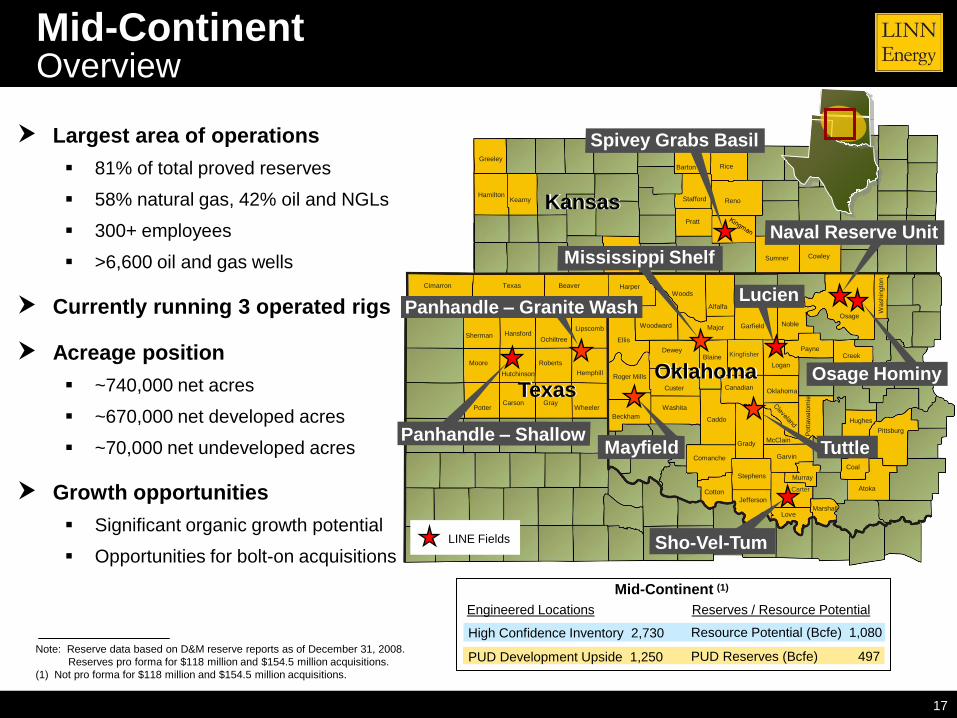

Mid-Continent Overview

Mid-Continent (1)

High Confidence Inventory 2,730

PUD Development Upside 1,250

Resource Potential (Bcfe) 1,080

PUD Reserves (Bcfe) 497

Reserves / Resource PotentialEngineered Locations

Largest area of operations

81% of total proved reserves

58% natural gas, 42% oil and NGLs

300+ employees

>6,600 oil and gas wells

Currently running 3 operated rigs

Acreage position

~740,000 net acres

~670,000 net developed acres

~70,000 net undeveloped acres

Growth opportunities

Significant organic growth potential

Opportunities for bolt-on acquisitions

Texas

Kansas

Oklahoma

Panhandle – Granite Wash

Mayfield TuttlePanhandle – Shallow

Osage Hominy

Sho-Vel-TumLINE Fields

Naval Reserve Unit

Barton

Clark Cowley

Greeley

Kearny

Pratt

Reno

Rice

Stafford

Sumner

Hamilton

Alfalfa

BeaverCimarron

Ellis

Garfield

Harper

MajorNoble

Osage

Texas

Woods

Woodward

Washin

gto

n

Carson Gray

Hansford

HemphillHutchinson

Lipscomb

Moore

Ochiltree

Potter

Roberts

Sherman

Wheeler

Beckham

Blaine

Caddo

CanadianCuster

Dewey

Logan

Roger Mills

Washita

Atoka

Coal

Comanche

Cotton

Creek

Garvin

Grady

Hughes

Jefferson

Love

McClain

Marshall

Murray

Payne

Pittsburg

Stephens

Pott

aw

ato

mie

Kingfisher

Carter

Oklahoma

Mississippi Shelf

Spivey Grabs Basil

Lucien

Note: Reserve data based on D&M reserve reports as of December 31, 2008.

Reserves pro forma for $118 million and $154.5 million acquisitions.

(1) Not pro forma for $118 million and $154.5 million acquisitions.

18

Mid-Continent: Acreage Comparison

(1) Estimated based on public data.

(2) Estimated based on available industry producing and permitting data.

Hemphill County

Wheeler County

Roberts County

Gray County

Greater Stiles Ranch Area

0 4 miles

Scale

0 4 miles

Scale

Frye

Ranch

Stiles Ranch

LINN Energy

Forest Oil (est) (1)

Newfield Exploration (est) (2)

Buffalo WallowTwo Step

Seventh StepMendota Ranch

Lard Ranch

Dyco

Twin Channel

LINN Granite Wash Acreage

~ 70,000 Gross Acres

~ 38,000 Net Acres

89% Held By Production

Industry leading position in the Granite Wash trend

19

TX

NM

Levelland

Iatan / Snyder

Spraberry

King Mountain

Gomez

Goldsmith

Carlsbad

GrayburgShafter Lake

Ozona

Owen Mesa / Pearl / Teas

Livingston Ridge

Eddy

Lea

Hockley

Garza

Dawson

Andrews

Howard

MidlandEctor

Winkler

Upton

Schieicher

Pecos

CraneWard

Crockett

LINE Fields

Permian Basin Overview

Long-life, low-risk reserves

21 MMBoe proved reserves

86% liquids (~68% proved developed)

Reserve life of over 20 years

7% of total reserves

Acreage position

~33,000 net acres

~33,000 net developed acres

Growth opportunities

>250 proved low-risk infill drilling and

optimization opportunities

Opportunities for bolt-on acquisitions

20

Brea Canyon Area

Tonner Area

LINN Acreage

Oil Wells

Brea-Olinda Field

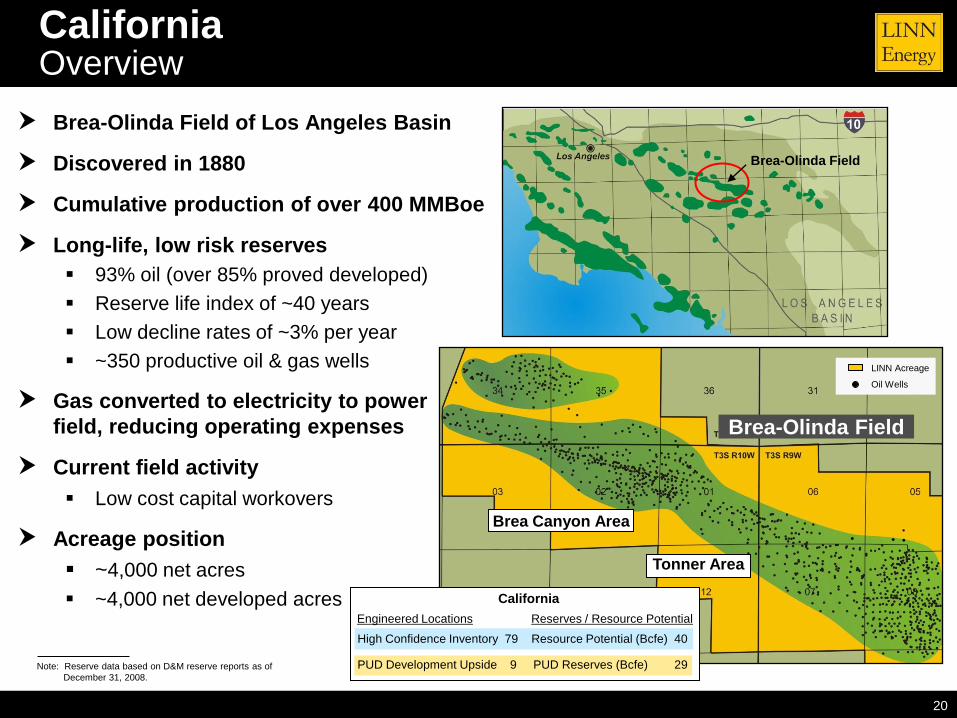

CaliforniaOverview

Brea-Olinda Field of Los Angeles Basin

Discovered in 1880

Cumulative production of over 400 MMBoe

Long-life, low risk reserves

93% oil (over 85% proved developed)

Reserve life index of ~40 years

Low decline rates of ~3% per year

~350 productive oil & gas wells

Gas converted to electricity to power

field, reducing operating expenses

Current field activity

Low cost capital workovers

Acreage position

~4,000 net acres

~4,000 net developed acres

Brea-Olinda Field

Note: Reserve data based on D&M reserve reports as of

December 31, 2008.

California

High Confidence Inventory 79 Resource Potential (Bcfe) 40

PUD Development Upside 9 PUD Reserves (Bcfe) 29

Reserves / Resource PotentialEngineered Locations

21

Low Risk Inventory For The Future

Includes 4,068 drilling locations and 2.6-3.6 Tcfe of capital inventory

High

Confidence

Inventory

1.1 Tcfe

PUD Development

Upside

0.53 Tcfe

Proved Developed

1.13 Tcfe

Prospective

Oklahoma 745 209

TX Panhandle – Shallow 333 143

TX Panhandle – Granite Wash 172 145

California 9 29

TX Panhandle – Granite Wash 757 570

Oklahoma 1,050 360

TX Panhandle – Shallow 923 150

California 79 40

Engineered Locations

Resource

Potential (Bcfe) Total Wells

Engineered Locations Reserves (Bcfe)

PDP / PDNP

PUD

2,809

Down spacing opportunities

Mississippi Shelf

TX Panhandle – Granite Wash (Horizontal)

TX Panhandle – Shallow

Unrisked Resource Potential (Tcfe)

Total Wells

1,259

1-2 Tcfe

2.8 Tcfe

3.8-4.8 Tcfe

1.7 Tcfe

1.1 Tcfe

Cumulative

Total

Note: Not pro forma for $118 million and $154.5 million acquisitions.

.

22

The Company defines adjusted EBITDA as income (loss) from continuing operations plus the following adjustments: Net operating cash flow from acquisitions and divestitures, effective date through closing date;

Interest expense;

Depreciation, depletion and amortization;

Impairment of goodwill and long-lived assets;

Write-off of deferred financing fees and other;

(Gain) loss on sale of assets, net;

Unrealized (gain) loss on commodity derivatives;

Unrealized (gain) loss on interest rate derivatives;

Realized (gain) loss on interest rate derivatives;

Realized (gain) loss on canceled derivatives;

Unit-based compensation expenses;

Exploration costs;

IPO cash bonuses; and

Income tax (benefit) expense.

Adjusted EBITDA is a significant non-GAAP performance metric used by Company management to indicate (prior to the establishment of any reserves by its Board of Directors) the cash distributions the Company expects to pay unitholders. Specifically, this financial measure indicates to investors whether or not the Company is generating cash flow at a level that can sustain or support an increase in its quarterly distribution rates. Adjusted EBITDA is also a quantitative metric used throughout the investment community with respect to publicly-traded partnerships and limited liability companies.

Historical Financial StatementsReconciliation of Non-GAAP Measures

23

The following presents a reconciliation of income (loss) from continuing operations

to adjusted EBITDA:

Historical Financial StatementsAdjusted EBITDA

($ in thousands) Year Ended December 31,

2008 2007 2006

Income (loss) from continuing operations $825,657 $(356,194) $69,811

Plus:

Net operating cash flow from acquisitions and

divestitures, effective date through closing date 3,436 67,417 712

Interest expense, cash 81,704 35,974 5,155

Interest expense, noncash 12,813 3,000 754

Depreciation, depletion and amortization 194,093 69,081 4,352

Impairment of goodwill and long-lived assets 50,505 --- ---

Write-off of deferred financing fees and other 6,728 3,460 3,342

(Gain) loss on sale of assets, net (98,763) 1,767 28

Unrealized (gain) loss on commodity derivatives (734,732) 388,733 (77,494)

Reclassification of derivative settlements --- (5,946) (5,654)

Unrealized (gain) loss on interest rate derivatives 50,638 29,548 (82)

Realized (gain) loss on interest rate derivatives 16,036 (1,467) (282)

Realized loss on canceled derivatives 81,358 --- ---

Unit-based compensation expenses 14,699 13,518 21,612

Exploration costs 7,603 4,053 286

IPO cash bonuses --- --- 2,039

Income tax (benefit) expense 2,712 4,788 (1,973)

Adjusted EBITDA from continuing operations $514,487 $257,732 $22,606

Adjusted EBITDA from discontinued operations $14,087 $42,681 $48,103

24

Reserve Replacement / F&D CalculationsReconciliation of Non-GAAP Measures

Year Ended

Costs incurred (in thousands): December 31 , 2008

Property acquisition costs:

Proved 595,795$

Unproved 4,111

Development costs 332,557

Costs incurred 932,463$

Less:

Asset retirement obligation costs (680)

Discontinued operations (32,207)

Costs expended - continuing operations 899,576$ A

Less:

Property acquisition costs - continuing operations (584,630)

Oil and gas capital 314,946$ B

Reserve data - continuing operations (MMcfe):

Purchase of minerals in place 368,136

Extensions, discoveries and other additions 228,083

Annual additions, excluding price-related revisions 596,219 C

Less:

Purchase of minerals in place (368,136)

Annual additions, excluding price-related revisions and acquisitions 228,083 D

Annual production 77,548 E

Calculations

Reserve replacement cost 1.51$ A / C

Reserve replacement ratio 769% C / E

Finding and development cost from the drill bit 1.38$ B / D

Drill bit reserve replacement ratio 294% D / E

25

Cautionary Note to U.S. Investors — The United States Securities and Exchange Commission (―SEC‖) permits oil and gas companies, in their filings with the SEC, to disclose only proved reserves that a company has demonstrated by actual production or conclusi ve formation tests to be economically and legally producible under existing economic and operating conditions. Any reserve estimate s provided in this presentation that are not specifically designated as being estimates of proved reserves may include not o nly proved reserves, but also other categories of reserves that the SEC's guidelines strictly prohibit the Company from including in filings with the SEC. Investors are urged to consider closely the disclosure in the Company’s Annual Report filed on Form 10-K for fiscal year ended December 31, 2008, available from the Company at 600 Travis, Suite 5100, Houston, Texas 77002 (Attn: Investor Relations). You can also obtain this report from the SEC by calling 1 -800-SEC-0330 or from the SEC's website at www.sec.gov.

Related Documents