Evaluer. Simplifying Human Resource Documentation www.evaluer.co.in Employee Provident Fund Miscellaneous Provisions Act, 1961 Practical Compliance Reference Handbook In this handbook we will address the following: What the Employee Provident Fund Act, Employee Pension Scheme and Employee Deposit Linked Insurance mean. Meaning of wages for the purpose of provident fund deductions. Checklist and dos and Don’ts for an employer. Evaluer on Employment Law

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

Employee Provident FundMiscellaneous ProvisionsAct, 1961 Practical Compliance

Reference

Handbook

In this handbook we willaddress the following:

What the Employee ProvidentFund Act, Employee PensionScheme and Employee DepositLinked Insurance mean.

Meaning of wages for thepurpose of provident funddeductions.

Checklist and dos and Don’ts foran employer.

Evaluer on

Employment Law

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

1. INTRODUCTION TO THE EMPLOYEES PROVIDENT FUND AND MISCELLANEOUS PROVISIONS

ACT, 1952 (“EPF Act” or the “Act”).

1.1 The EPF Act has been enacted to provide for the institution of provident funds, pension

funds and deposit link insurance funds for employees in factories and other establishments.

The principal duty is laid upon the employer to put the Provident Fund Scheme into

operation and to make contribution of both the employees and employer’s share to the fund

then and there and deduct the employees share from their wages / salary. Under the EPF

Act, the Central Government has framed schemes to be called the Employee Provident Fund

Scheme (the “EPF Scheme”), Employee Pension Scheme (the “Pension Scheme”) and

Employee Deposit Link Insurance Scheme (“EDLIS” or the “EDLI Scheme”), for institution of

provident fund, pension fund and life insurance benefits to employees in factories and other

establishments. The EPF Act is applicable to every establishment or factory in which at least

20 (Twenty) or more persons have been employed. The EPF Act also provides that once an

establishment is liable to be covered under the Act, the said establishment shall continue to

be governed by the EPF Act, notwithstanding that the number of persons employed therein

at any time falls below 20 (Twenty).

1.2 COVERAGE OF AN EMPLOYEE

As per provisions contained in Para 26A of the Employee Provident Funds Scheme, 1952 (the

“Provident Fund Scheme” or the “Scheme”) once an employee becomes a member of the

provident fund, he continues to remain a member even if his salary exceed the upper limit

for coverage under the Scheme, until he withdraws the provident fund accumulation in full

and final settlement from the fund. In case a member of the provident fund leaves service of

an establishment and joins another establishment covered by the Scheme, even then he

continues to remain a member of the Scheme and the provident fund accumulation, in his

account, is transferred.

1.2.1 CONTRIBUTION AMOUNT TOWARDS EPF:

As per the EPF Act, an establishment is liable to contribute at the rate of 12 % (percentage

twelve) of basic component of employee’s salary to the Provident Fund. However,

contribution by the establishment is bifurcated into (i) contribution to Provident Fund, and

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

(ii) contribution to Pension Scheme. From an establishment’s share of contribution, a sum

equal to 8.33 % (percentage eight decimal three three) of basic wages up to Rs 15,000

(fifteen thousand only) is contributed towards Pension Scheme.

1.2.2 ADMINISTRATIVE CHARGES

In addition to the 12 % (percentage twelve) percent mentioned above, an establishment has

to pay an additional 1.10 % (percentage one decimal one zero) of salary of the employee as

administration charges. The concerned establishment is also required to pay a contribution

of 0.5 % (percentage zero decimal five) and administrative charges of .01% (percentage zero

decimal zero one) towards Employee Deposit Link Insurance Fund, up to a maximum limit of

Rs 15,000 (fifteen thousand only).

1.2.3 NOMINATION TO PREVAIL OVER WILL

A disposition of fund by Will is implied yet when nomination has been made nomination will

prevail over the Will.1

1.2.4 SUCCESSION CERTIFICATE NOT REQUIRED FOR PAYMENT TO NOMINEE

Succession certificate is not required for payment of amount to nominee of deceased.2

1.3 DEFINITION OF WAGES FOR CALCULATION OF EPF

EPF contribution is calculated on the basis of basic wages, dearness allowance (including

cash value of any food concession) and retaining allowance (if any) actually drawn during the

whole month whether paid on daily, weekly, fortnightly or monthly basis. The EPF Act

defines basic wages as, “All emoluments which are earned by an employee while on duty or

on leave or on holidays with wages in either case in accordance with the terms of the

contract of employment, but does not include:

i. the value in cash for any food concession;

ii. any dearness allowance (which means all cash payment by whatever name called paid to an

employee on account of a rise in the cost of living);

iii. house rent allowance;

1 Hardev Kaur vs. Jodh Singh Chowdhry, AIR 1969 P&H 44 (DB).2 Imambhai Gulamhusen Shaikh vs. Regional Provident Fund Commissioner, 1992 (45) FLR 166: 1982 (2) LLN 103: 1982 LabIC 1036 (Guj.) DB.

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

iv. overtime allowance;

v. bonus;

vi. commission;

vii. any other similar allowance payable to the employee in respect of his employment or of

work done in such employment; and

viii. any presents made by the employer.

1.3.1 FOLLOWING ITEMS ARE INCLUDED IN BASIC WAGES

i. Retaining allowance: the term retaining allowance means an allowance payable to an

employee during any period in which the establishment is not working, for retaining his / her

services.

ii. Allowance or reward for good work: this could be good work which is performed by an

employee during the course of employment which could be during the normal factory hours

or during over time hours.

iii. Production bonus: the portion of payment which is made by a company for production above

the ‘norm’ would constitute production bonus and will be included for the purpose of

provident fund contribution.

iv. Special allowance as per contract: special allowance paid for special services rendered by an

employee, which are emoluments earned by the employee in accordance with the terms of

the contract between the company and employee is also covered under the definition of

wages for provident fund contribution. Additionally, various special allowances paid by a

company to their employees under different heads, such as conveyance, educational

allowance, food concessions, medical, special holidays, night shift incentives, city

compensatory allowances all amount to wages within the meaning of the term wages for the

purpose of deduction towards provident fund. In Reynolds Pens India Private Limited Vs

Regional Provident Fund Commissioner3 the Madras High Court has held that various

allowances under different heads such as conveyance, educational allowances, food

concession, medical allowance, special holidays, night shift incentive, city compensatory

allowances are amounting to wages within the meaning of the term ‘basic wages’ as per

3 Management of Reynolds Pens India Private Limited vs. The Regional Provident Commissioner – II, 2011 LLR 876: 2011 (2)CLR 1033: 2011 (4) LLN 171: 2011 (131) FLR 690 (Mad)

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

section 2 (b) of the EPF Act for the purpose of deductions towards the provident fund

contributions.

v. Interim advance lump sum and settlement benefit: interim advance payment of lump sum

and amount paid towards settlement benefit form part of basic wages.

vi. Arrears of revised pay: when an award gives revised pay scales, the employee become

entitled to the revised emoluments and where the said revision is with retrospective effect,

the arrears paid to the employee, as a consequence, are emoluments earned by them while

on duty. Therefore the revised wage-structure, as a result of an award under the EPF Act has

to be taken as part of wages in the context of provident fund contributions.

vii. Encashment of leave: leave encashment must be included in basic wages for the purpose of

calculation contribution of provident fund.4

viii. Maternity benefit: payment made to a women employee during maternity benefit period

attracts contribution payment liability.

1.3.2 FOLLOWING ITEMS ARE EXCLUDED IN BASIC WAGES:

i. Personal allowance pay over and above the basic wages and dearness allowance for skill,

efficiency or past good record.

ii. Payment made in addition to normal rate of pay for working on a holiday or a festival

holiday.

iii. Area allowance given to employees living in a particular area to meet high cost of living in

that area.

iv. Disbursement benefits and injury compensation provided under the Employee State

Insurance Act, 1948 and Workmen’s Compensation Act, 1923.

v. Canteen subsidy paid to workers in lieu of canteen facilities which cannot be provided for

want of space etc.

vi. Commission on advertisement secured on newspapers.

vii. Payment made on account of un-availed leave at the time of discharge.

viii. Shift allowance paid to employees who work on shift duty on odd shifts.

ix. Shoes-allowance, entertainment allowance, fuel allowance, ex-gratia payment, typist’s

allowance, stenograph’s allowance, canvassing allowance, first-aid allowance, compensatory

4 Hindustan Lever Employees Union vs. Regional Provident Fund Commissioner, 1995 LLR 279

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

allowance, wages paid for holidays, tiffin allowance, cash handling allowance paid to cashier,

machine allowance, washing allowance, and / or subsistence allowance / wages.

1.4 IMPORTANT CLARIFICATIONS FOR EPF CALCULATIONS

1.4.1 DEFINITION OF AN EXCLUDED EMPLOYEE

An excluded employee is i) an employee who has been a member of the provident fund had

withdrawn the full amount of accumulation in the fund on retirement from service after

attaining the age of 55 (fifty five) years; or (ii) an employee whose pay exceeds Rs 15,000

(fifteen thousand); or (iii) an apprentice whose appointment is governed by the standing

orders of the establishment; or (iv) an ex-member of the provident fund having received full

and final payment in respect of his membership after attaining the age of 55 (fifty five) years

and is re-employed.

1.4.2 CAN AN EMPLOYEE CONTRIBUTE OVER AND ABOVE THE MANDATORY 12 % AS

VOLUNTARY CONTRIBUTION?

Yes, an employee can contribute over and above the mandatory contribution of 12 %,

subject to a total contribution of not more than 100 % percent of basic wages / salary.

However a company or establishment is not obligated to contribute towards such voluntary

contribution done by an employee. Further, the said voluntary contribution will be treated

as normal contribution and cannot be withdrawn as and when the employee wishes to. The

voluntary contribution will be at a fixed percentage of basic and will remain the same

throughout the year. The concerned employee can give the mandate for deduction of

voluntary PF at the start of financial year.

1.4.3 WHAT IS THE SALARY LIMIT TOWARDS EPF CONTRIBUTION?

Employees drawing salary at the time of joining below Rs 15,000 (fifteen thousand) per

month are governed by the provisions of the EPF Act. However, once an employee becomes

a member of the provident fund, he continues to remain a member even if his salary

exceeds Rs 15,000 (fifteen thousand), until his death or till he withdraws the provident fund

accumulation.

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

Note: If the pay of the member exceeds Rs 15,000 the contribution payable by an

establishment shall be limited to the amount payable on Rs 15,000 only.

1.4.4 WHAT WILL BE THE TREATMENT FOR EPF CALCULATION WHEN AN EMPLOYEE’S SALARY

CROSSES THE WAGE CEILING OF RS 15,000 ?

If the salary of an employee exceeds the wage ceiling of Rs 15,000 per month, then he will

be entitled to remain covered up to Rs 15,000 per month.

1.4.5 TRANSFER OF PROVIDENT FUND ACCUMULATIONS

Provident Fund accumulations can be transferred to the new employer provident fund

account by filling up Form 13 with the new employer. In other words, where a member of

the Fund ceases to be employed in one region and secures employment in another region in

an establishment to which the Scheme applies, he may apply to the Commissioner in Form

13 within whose jurisdiction he was previously employed, in such form as the commissioner

may specify, for transfer of balance of the provident fund in his existing account to his

account in the other region.

1.4.6 COULD A COMPANY SPLIT MINIMUM WAGES IN ORDER TO MINIMIZE PROVIDENT FUND

CONTRIBUTION?

Yes. Although there is no Apex Court ruling to this effect, the Punjab & Haryana High Court in

Assistant Provident Fund Commissioner, Gurgaon Vs M/s G4S Security Services (India) Private

Limited has held that provident fund contributions are not necessarily to be paid on the

minimum wages which are fixed under the Minimum Wages Act, 1948 since the ‘basic

wages’ as defined under the EPF Act and ‘wages’ as defined under the Minimum Wages Act,

1948 are different. Therefore a company can split the minimum wages into allowances like

house rent and conveyance and washing allowance, etc which would not attract provident

fund contribution.

1.4.7 COULD THE EMPLOYEE WITHDRAW A PART OF HIS PF ACCUMULATIONS DURING

EMPLOYMENT?

An employee can utilize his provident fund accumulation partially for specific occasions, such

as:

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

i. Medical treatment: advance from the fund for illness viz. hospitalization for more than a

month, major surgical operation or suffering from tuberculosis, leprosy, paralysis, cancer,

heart ailment, etc. For self or family (spouse, children, and dependent parents). The

maximum amount that can be drawn shall not exceed the member’s basic wages (and

dearness allowance) for six months or his own share of contribution with interest in the fund

till date, whichever is less. The member should have shown proof of hospitalization for one

month or more with leave certificate for that period from the company. He must also prove

that he is not a member of the Employee State Insurance Corporation. Additionally, a

physically handicapped employee can withdraw up to six months basic salary and dearness

allowance, or his share of provident fund contribution with interest or the cost of

equipment. He will have to submit a medical certificate to prove the same.

ii. Marriage or education of self, children, sister or brother: an employee should have

completed a minimum of seven years of membership of the Fund. The maximum amount he

can draw is 50 % (percentage fifty) of his contribution. Withdrawal is permitted for his own

marriage, the marriage of his or her daughter, son, sister or brother or for the post-

matriculation education of his or her son or daughter. Proof to be submitted will be fee

payable to the educational institute or the wedding invite as the case may be. Not more than

3 (three) advances shall be permissible under this head.

iii. Damage to movable or immovable property of member due to natural calamity: a member

whose property (movable or immovable) has been damaged due to a natural calamity such

as earthquake, floods or riots can withdraw up to Rs 5,000 (five thousand only) or 50 %

(percentage fifty) of his total contribution including interest thereon whichever is less to

meet the unforeseen expenditure. The concerned member will have to will have to apply

within 4 (four) months of the calamity. Proof to be submitted will be a certificate of damage

from the requisite authority and a calamity declaration by the state government. The EPF Act

does not provide for any minimum service condition for the member in such a scenario.

iv. Employee physically handicapped: an employee, who is physically handicapped, may be

allowed, for purchasing equipment required to minimize his hardship. The withdrawal

amount shall not exceed the employee’s basic wages and dearness allowance for 6 (six)

months or his own share of contribution with interest thereon or the cost of the equipment,

whichever is less. No second advance shall be allowed under this category within a period of

3 (three) years from the date of last payment.

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

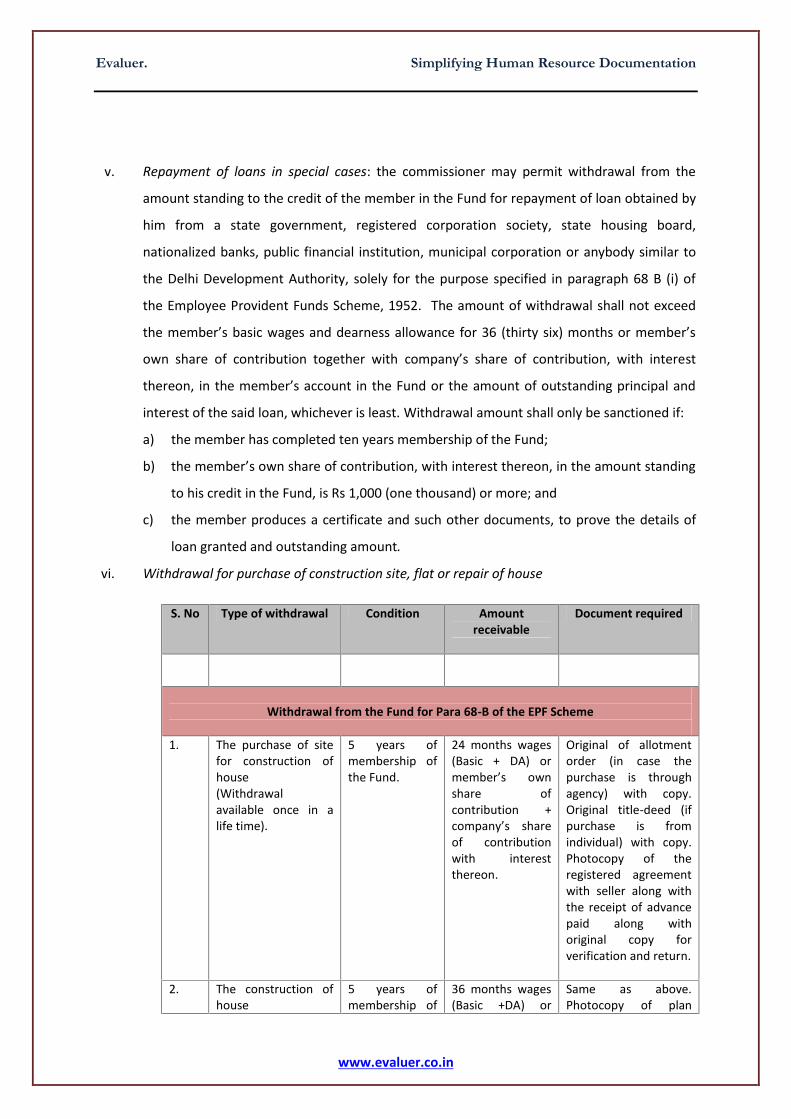

v. Repayment of loans in special cases: the commissioner may permit withdrawal from the

amount standing to the credit of the member in the Fund for repayment of loan obtained by

him from a state government, registered corporation society, state housing board,

nationalized banks, public financial institution, municipal corporation or anybody similar to

the Delhi Development Authority, solely for the purpose specified in paragraph 68 B (i) of

the Employee Provident Funds Scheme, 1952. The amount of withdrawal shall not exceed

the member’s basic wages and dearness allowance for 36 (thirty six) months or member’s

own share of contribution together with company’s share of contribution, with interest

thereon, in the member’s account in the Fund or the amount of outstanding principal and

interest of the said loan, whichever is least. Withdrawal amount shall only be sanctioned if:

a) the member has completed ten years membership of the Fund;

b) the member’s own share of contribution, with interest thereon, in the amount standing

to his credit in the Fund, is Rs 1,000 (one thousand) or more; and

c) the member produces a certificate and such other documents, to prove the details of

loan granted and outstanding amount.

vi. Withdrawal for purchase of construction site, flat or repair of house

S. No Type of withdrawal Condition Amountreceivable

Document required

Withdrawal from the Fund for Para 68-B of the EPF Scheme

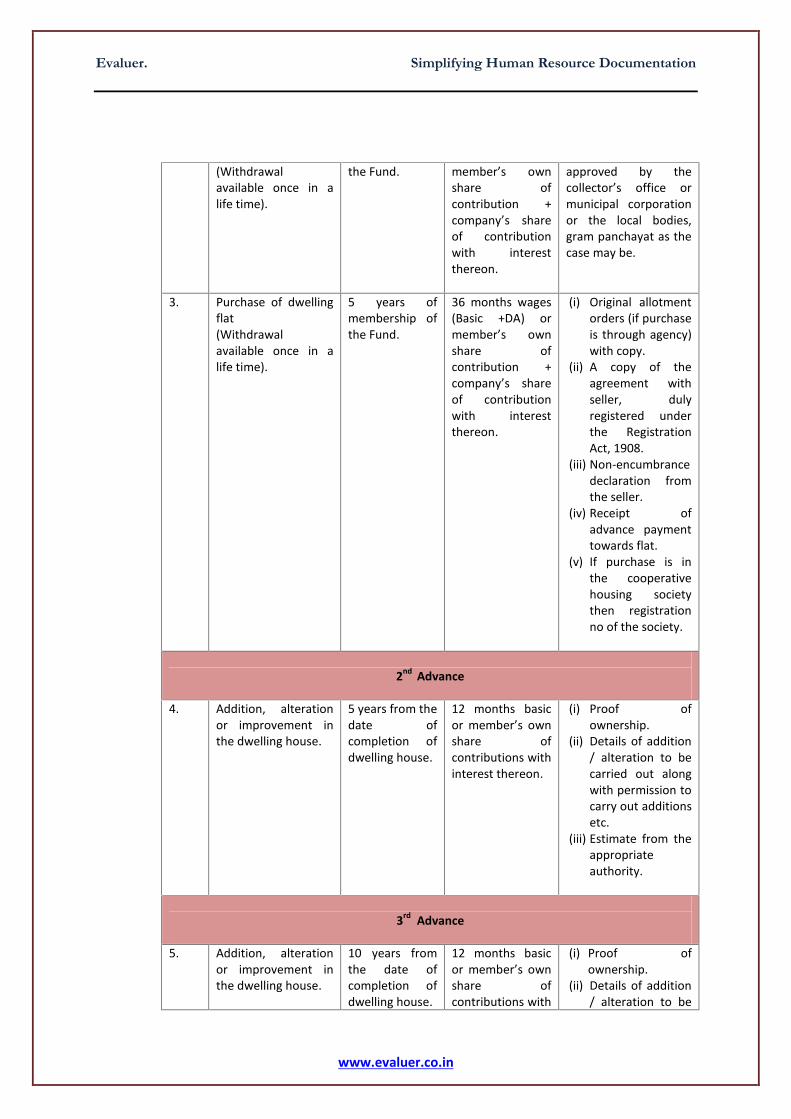

1. The purchase of sitefor construction ofhouse(Withdrawalavailable once in alife time).

5 years ofmembership ofthe Fund.

24 months wages(Basic + DA) ormember’s ownshare ofcontribution +company’s shareof contributionwith interestthereon.

Original of allotmentorder (in case thepurchase is throughagency) with copy.Original title-deed (ifpurchase is fromindividual) with copy.Photocopy of theregistered agreementwith seller along withthe receipt of advancepaid along withoriginal copy forverification and return.

2. The construction ofhouse

5 years ofmembership of

36 months wages(Basic +DA) or

Same as above.Photocopy of plan

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

(Withdrawalavailable once in alife time).

the Fund. member’s ownshare ofcontribution +company’s shareof contributionwith interestthereon.

approved by thecollector’s office ormunicipal corporationor the local bodies,gram panchayat as thecase may be.

3. Purchase of dwellingflat(Withdrawalavailable once in alife time).

5 years ofmembership ofthe Fund.

36 months wages(Basic +DA) ormember’s ownshare ofcontribution +company’s shareof contributionwith interestthereon.

(i) Original allotmentorders (if purchaseis through agency)with copy.

(ii) A copy of theagreement withseller, dulyregistered underthe RegistrationAct, 1908.

(iii) Non-encumbrancedeclaration fromthe seller.

(iv) Receipt ofadvance paymenttowards flat.

(v) If purchase is inthe cooperativehousing societythen registrationno of the society.

2nd Advance

4. Addition, alterationor improvement inthe dwelling house.

5 years from thedate ofcompletion ofdwelling house.

12 months basicor member’s ownshare ofcontributions withinterest thereon.

(i) Proof ofownership.

(ii) Details of addition/ alteration to becarried out alongwith permission tocarry out additionsetc.

(iii) Estimate from theappropriateauthority.

3rd Advance

5. Addition, alterationor improvement inthe dwelling house.

10 years fromthe date ofcompletion ofdwelling house.

12 months basicor member’s ownshare ofcontributions with

(i) Proof ofownership.

(ii) Details of addition/ alteration to be

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

interest thereon. carried out alongwith permission tocarry out additionsetc.

(iii) Estimate from theappropriateauthority.

vii. Option for withdrawal for investment in Pension Beema Yojana

The employee should be more than 55 (fifty five) years of age. Amount receivable is 90%

(percentage ninety) of both contributions. Payment to be made to Life Insurance

Corporation directly.

1.4.8 CIRCUMSTANCES IN WHICH ACCUMULATIONS ARE PAID TO THE MEMBER BY WAY OF

FINAL SETTLEMENT

Accumulation in the provident fund account of a member become payable for final

settlement under following circumstances:

i. on retirement from service after attaining the age of 58 (fifty eight) years;

ii. on retirement as a result of total and permanent disablement rendering incapable for work;

iii. immediately before migration from India for permanent settlement abroad or for taking

employment abroad;

iv. termination of service upon mass or individual retrenchment;

v. termination of service under voluntary retirement scheme; and

vi. termination of job and remaining unemployed for over 2 (two) months or leaving the job

from a covered establishment and joining the establishment not covered by the EPF Act.

1.4.9 COVERAGE OF EMPLOYEES ENGAGED BY A CONTRACTOR

The term ‘employee’ used in section 2 (f) of the EPF Act includes any person employed by or

through a contractor. Thus contract labourer will get advantages of the EPF Scheme framed

under the EPF Act, including appropriate EPF contributions. The prescribed contributions

have to be made in respect of the contract labour in the same manner and at the same rates

as applicable to the employees directly employed by the company. It is the duty of

contractor to pay the contributions in respect of its employees. The principal employer is

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

responsible for overseeing that the contractor does not violate any provisions of the EPF Act

as applicable to a contractor.

1.4.10 WILL THE ARREARS OF WAGES, PAID TO AN EMPLOYEE BY VIRTUE OF AN AWARD,

ATTRACT PROVIDENT FUND CONTRIBUTIONS?

Yes. Contributions towards provident fund will be payable on arrears of wages given to

employees on the basis of an award. Additionally, if the establishment revises the existing

pay-scale of an employee with effect from back date then the revised wages will attract

provident fund contribution from the effective date payable.

1.4.11 WILL THE AMOUNT OF COMMISSIONS, AS PAID TO THE EMPLOYEES, ATTRACT THE

APPLICABILITY OF EPF ACT?

Wages, as defined under the EPF Act means all emoluments which are earned by an

employee while on duty or on leave or on holidays with wages in either case, in accordance

with the terms and conditions of employment. So the commission being paid as

remuneration to the employee shall attract the liability of coverage as also payment of

contribution in respect of them.

1.5 PENSION SCHEME

The second scheme to run under the EPS is the pension scheme. The pension scheme is

framed in order to provide for superannuation pension to the employee himself, and widow

/ widower or children of the employee. All employees covered under the EPF Act, who have

not completed the age of 58 (fifty eight) years become members of pension scheme.

1.5.1 CONTRIBUTION TO THE PENSION SCHEME

From and out of the contribution payable by an establishment towards EPF Scheme each

month, a part of the contribution representing 8.33 % (eight decimal three three) of basic

wages is contributed to Pension Scheme from Employer’s share of contribution. The

maximum contributory salary however shall be limited to Rs 15,000 only.

1.5.2 CALCULATION OF PENSIONABLE SALARY

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

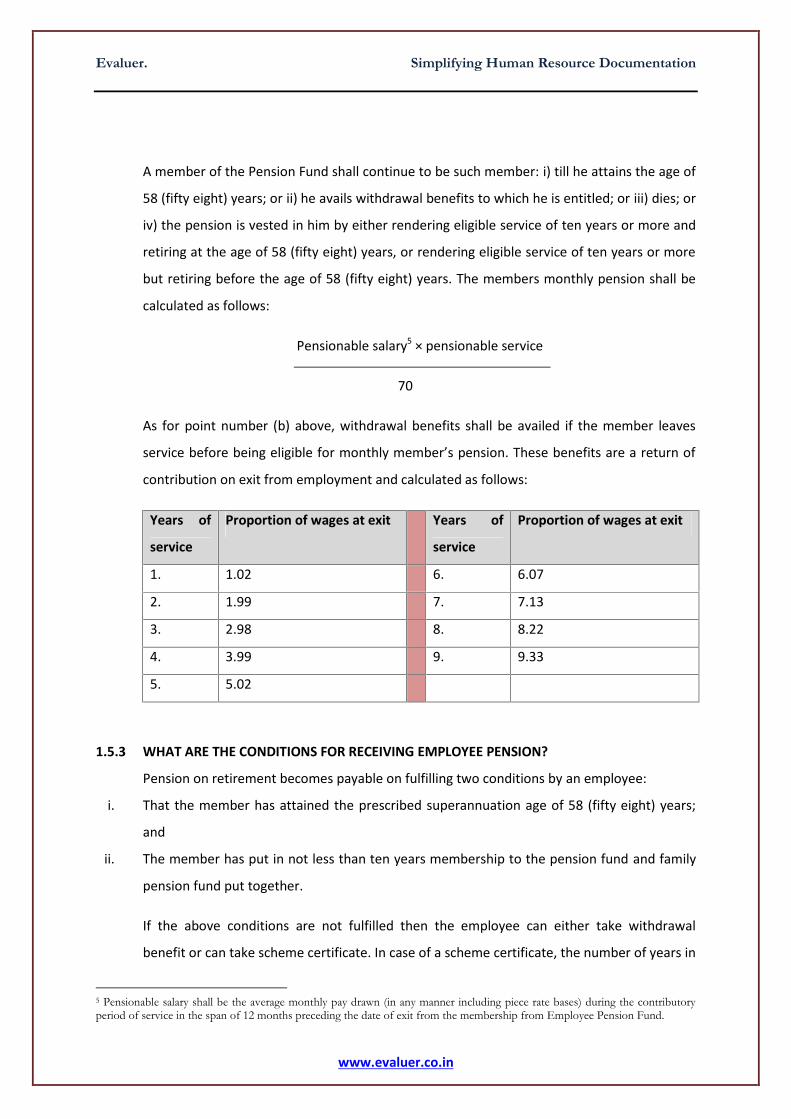

A member of the Pension Fund shall continue to be such member: i) till he attains the age of

58 (fifty eight) years; or ii) he avails withdrawal benefits to which he is entitled; or iii) dies; or

iv) the pension is vested in him by either rendering eligible service of ten years or more and

retiring at the age of 58 (fifty eight) years, or rendering eligible service of ten years or more

but retiring before the age of 58 (fifty eight) years. The members monthly pension shall be

calculated as follows:

Pensionable salary5 × pensionable service

70

As for point number (b) above, withdrawal benefits shall be availed if the member leaves

service before being eligible for monthly member’s pension. These benefits are a return of

contribution on exit from employment and calculated as follows:

Years of

service

Proportion of wages at exit Years of

service

Proportion of wages at exit

1. 1.02 6. 6.07

2. 1.99 7. 7.13

3. 2.98 8. 8.22

4. 3.99 9. 9.33

5. 5.02

1.5.3 WHAT ARE THE CONDITIONS FOR RECEIVING EMPLOYEE PENSION?

Pension on retirement becomes payable on fulfilling two conditions by an employee:

i. That the member has attained the prescribed superannuation age of 58 (fifty eight) years;

and

ii. The member has put in not less than ten years membership to the pension fund and family

pension fund put together.

If the above conditions are not fulfilled then the employee can either take withdrawal

benefit or can take scheme certificate. In case of a scheme certificate, the number of years in

5 Pensionable salary shall be the average monthly pay drawn (in any manner including piece rate bases) during the contributoryperiod of service in the span of 12 months preceding the date of exit from the membership from Employee Pension Fund.

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

past service can be added to any future service that he / she may put in, in any other

covered establishment. By virtue of being a holder of a scheme certificate, if the member

dies before the age of 58 (fifty eight) years, widow and children shall be entitled for pension.

1.5.4 PENSION – IF AN EMPLOYEE HAS WORKED FOR LESS THAN TEN YEARS

If an employee has completed less than ten years of service, he can avail of the pension as a

lump sum by opting for withdrawal benefits as explained above.

1.5.5 PENSION – WHEN EMPLOYEE CHANGES HIS JOB

When an employee changes his job and shifts his provident fund account, his pension does

not get transferred automatically. He needs to apply for a scheme certificate through Form

10C and route it through the new employer. The certificate has details of the previous

employer and years of pension contribution. The provident fund scheme is linked to an

individual but the employee pension scheme is a pool-based scheme and cannot be started

all over again. So when he changes a job, his earlier service is not considered and reduces

the pension sum.

1.5.6 BENEFITS PROVIDED BY PENSION SCHEME

i. Monthly member’s pension : Superannuation pension / retirement pension is

payable on attaining the age of 58 (fifty eight).

This is calculated as mentioned in the formula

above.

ii. Monthly disability pension : A member who is permanently and totally

disabled during employment shall be entitled to

pension subject to a minimum of Rs 250 (two

hundred fifty) per month notwithstanding the

fact that he / she has not rendered the

pensionable service entitling him to pension,

provided that he has made at least one month’s

contribution to the pension fund. The pension

under this shall be tenable for the life time of

the member.

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

iii. Monthly widow / widowerpension :

Pension from the date following the date of

death of the member whether in service or

after exit from employment or after retirement

/ commencement of monthly member pension.

In case there are two or more widows, family

pension shall be payable to the eldest surviving

widow. On her death it shall be payable to the

next surviving widow, if any. The term eldest

would mean seniority with reference to the

date of marriage.

iv. Monthly children pension : If there are any surviving children of the

deceased member, falling within the definition

of family, they shall be entitled to a monthly

children pension in addition to the monthly

widow / widower pension.

Monthly children pension for each child shall be

equal to 25 % (percentage twenty five) of the

amount admissible to the widow / widower of

the deceased member subject to a minimum

monthly children pension for each child of the

deceased member of Rs 250 (two hundred and

fifty).

Monthly pension to the child shall be payable

until he attains the age of 25 (twenty five)

years.

Monthly pension shall be admissible to the

maximum of two children at a time and will run

from the oldest to the youngest child in that

order.

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

In the event of death or remarriage of the

widow / widower after sanctioning of widow /

widower pension the children shall be entitled

in lieu of the monthly children pension from the

date following the date of death / remarriage of

the widow / widower.

v. Orphan pension : Orphan children up to the age of 25 (twenty

five) years are entitled for monthly orphan

pension equal to 75 % (percentage seventy five)

of the amount of widow pension, subject to a

minimum of Rs 750 (seven hundred and fifty)

per child. The orphan pension shall be

admissible to a maximum of two orphans and

shall run from the oldest to the youngest.

vi. Nominee pension : In case of unmarried members, a person

nominated by the member will get pension

equal to widow pension.

1.5.7 WHAT IS FAMILY UNDER PENSION SCHEME?

Under Employees’ Pension Scheme, a family means: i) wife in case of male member of the

Employees’ Pension Fund; ii) husband in case of a female member of the Employees’ Pension

Fund; and iii) minor sons and unmarried daughters (also includes legally adopted children) of

a member of the Employees’ Pension Fund.

1.6 EMPLOYEE DEPOSIT LINKED INSURANCE SCHEME

The third scheme to operate under the EPF Act is the Employee Deposit Linked Insurance

Scheme (the “EDILS”). The purpose of this scheme is to provide for life assurance benefits to

the employees of an establishment to which the EPF Act applies. According to the EDLI

Scheme, an establishment is required to contribute 0.5 % (percentage zero decimal five)

percent of the employee’s monthly basic pay, capped at Rs 15,000, as premium. This

contribution is deposited in a Deposit-Linked Insurance Fund established under the EPF Act.

The employees are not required to make any contribution.

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

1.6.1 ASSURANCE BENEFITS

Assurance benefit means a payment linked to the average balance in the provident fund

account of an employee, payable to a person belonging to his family or otherwise entitled to

it in the event of death of the employee. On the death of the employee while in service, the

nominee or any other person entitled to receive the provident fund benefits will, in addition

to the provident fund, receive the assurance benefit under the employees deposit linked

insurance scheme.

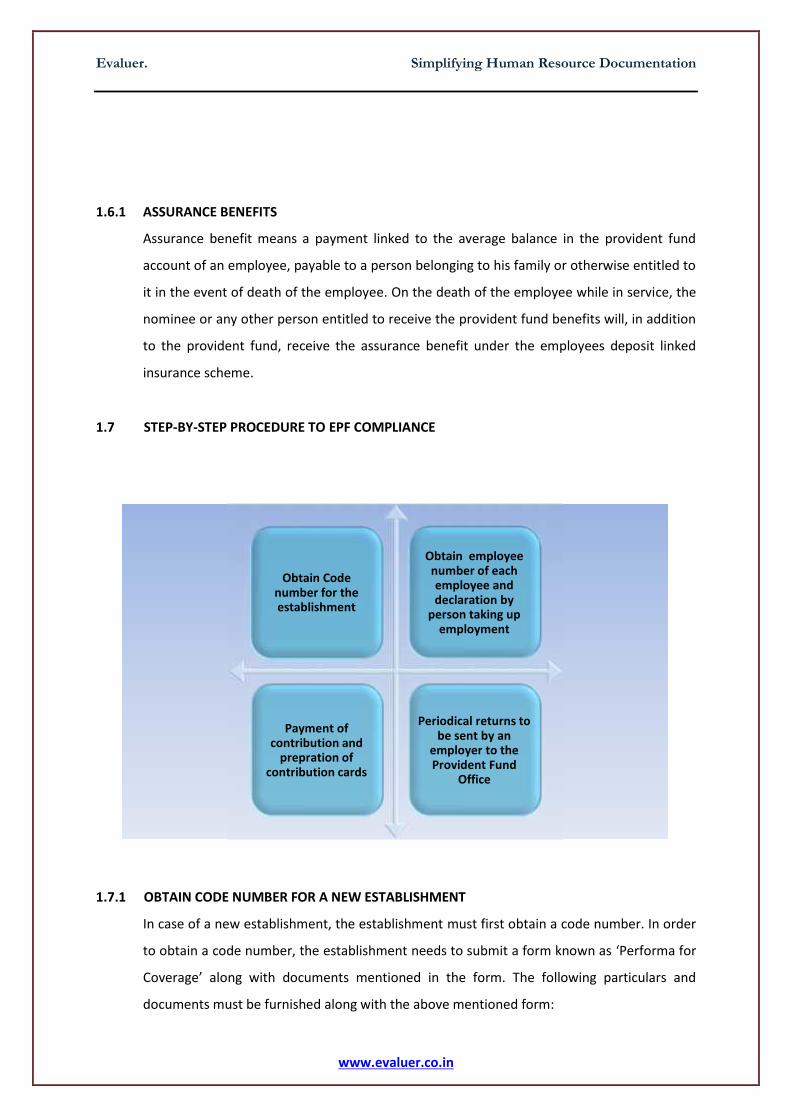

1.7 STEP-BY-STEP PROCEDURE TO EPF COMPLIANCE

1.7.1 OBTAIN CODE NUMBER FOR A NEW ESTABLISHMENT

In case of a new establishment, the establishment must first obtain a code number. In order

to obtain a code number, the establishment needs to submit a form known as ‘Performa for

Coverage’ along with documents mentioned in the form. The following particulars and

documents must be furnished along with the above mentioned form:

Obtain Codenumber for theestablishment

Obtain employeenumber of eachemployee anddeclaration by

person taking upemployment

Payment ofcontribution and

prepration ofcontribution cards

Periodical returns tobe sent by an

employer to theProvident Fund

Office

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

i. Particulars of the establishment (to be submitted along with documents mentioned below).

a. name of establishment / factory and address;

b. details of head office and branches with address;

c. details of code number, if any allotted to the head office;

d. date of incorporation of the company, along with documentary proof of

incorporation;

e. employment strength at present; and month-wise employment strength from the

date of set up may be furnished in separate statement;

f. nature of business activity / manufacturing activity;

g. details of legal set-up of the establishment (i.e. whether it is a private / public limited

company, partnership, society or proprietary concern;

h. ownership particulars: name, addresses and designation of managing director,

directors, partners, secretary etc;

i. wages / salary disbursed for the month;

j. details of bankers, including bank branches, bank account numbers;

k. income tax permanent account number;

l. details of bank drafts amounting to the provident fund contribution and

administrative charges paid in respect of the employees.

ii. Essential document to be submitted (submit applicable documents)

a. a copy of memorandum of association and articles of association and the certificate of

incorporation issued by the registrar of companies, in case of public and private

limited companies;

b. a copy of partnership deed in case of a partnership;

c. a copy of registration certificate issued by the registrar if co-operative societies;

d. a copy of registration certificate issued by the registrar in the case of societies

registered under Societies Registration Act, 1860 along with a copy of the object and

rules of the society;

e. partition deed creating HUF;

f. any agreement or other legal documents in case of association of persons as defined

in income tax act.

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

iii. Documents that can be submitted as proof of date if set-up (any one of these document has

to be submitted)

a. first sales invoice;

b. any proof regarding date of trial production;

c. incorporating certificate issued by the registrar of companies together with the report

of the managing director at the shareholders in the annual report;

d. commencement of business certificate issued by the registrar of companies;

e. license / permission issued by the municipal authorities;

f. license issued by the health authorities;

g. first assessment order issued by the sales tax authorities;

h. first assessment order issued by the income tax authorities;

i. certificate issued by the small scale industries authorities registering the

establishment;

j. reports / returns to central excise authorities;

k. sanction / connection of power like H.T connection, L.T connection.

1.7.2 OBTAIN ACCOUNT NUMBER OF EACH EMPLOYEE

Following steps must be followed in order to obtain account number for each employee

qualified to become a member of the fund:

i. Check whether the new employee is a member of the Fund or not. If yes, ask for the account

number and / or the name and particulars of the last employer. If not, he shall be required to

furnish particulars regarding himself and his nominee required for the Deceleration Form in

Form 2.

ii. Along with the above, send to the commissioner a return of the employees qualifying to

become members of the Fund for the first time during the preceding month in Form 5.

iii. On receipt of the above information, the commissioner shall promptly allot an account

number to each employee qualifying to become a member.

1.7.3 PREPARATION AND RENEWAL OF CONTRIBUTION CARDS

The concerned establishment shall prepare a contribution card in form or form 3A as may be

appropriate, in respect of every employee in his employment who is entitled and required to

become a member of a fund including those who produce an account number and in respect

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

of whom no fresh deceleration is required. Contribution cards shall consist of information

like amount recovered every month from the wages of an employee as well as the

contribution made by the employer in respect of each such employee. The contribution

cards shall be current for 1 (one) year except, in respect of first contribution period which

may be less or more than 1 (one) year.

1.7.4 RETURNS, FORMS, RECORDS TO BE MAINTAINED AND SUBMITTED TO AUTHORITIES

1.7.5 FOR AN UN-EXEMPTED ESTABLISHMENT

S.NO.

COMPLIANCE REQUIREMENTS SOURCEVERIFICATION

DUE DATE

Total number of employees _________Total number of apprentices _________Total number of employees drawing wages of Rs. 15,000and below ___________

ONE TIME RETURN ON COVERAGEPARTICULARS OF OWNERSHIP

1. Return of ownership: the establishment shall furnish tothe regional commissioner in Form 5A, particulars of allbranches, departments, directors, partners, manager ofthe establishment or any other person who is in ultimatecontrol over the affairs of factory or establishment.

For record of the provident fund office.

[Para 36 (a) of EPF Scheme and Para 21 of PensionScheme]

Form 5A Once in thebeginning andthereafter whenthere is change ofownership.

In duplicate,within 15 Days ofcoverage.

2. Return of employees: The establishment shall send tothe regional commissioner, within 15 days of coverage ofthe establishment a consolidated return, of employeesentitled to become members of the Fund showing thebasic wages, retaining allowance etc paid to each suchemployee.

If there is no employee who is required or entitled tobecome a member of the Fund, the establishment shallsend “NIL” return.

[Para 36 (1) of EPF Scheme and Para 20 of the PensionScheme]

Form 9(Revised)

.

Within 15(Fifteen) days ofcoverage ofestablishment.

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

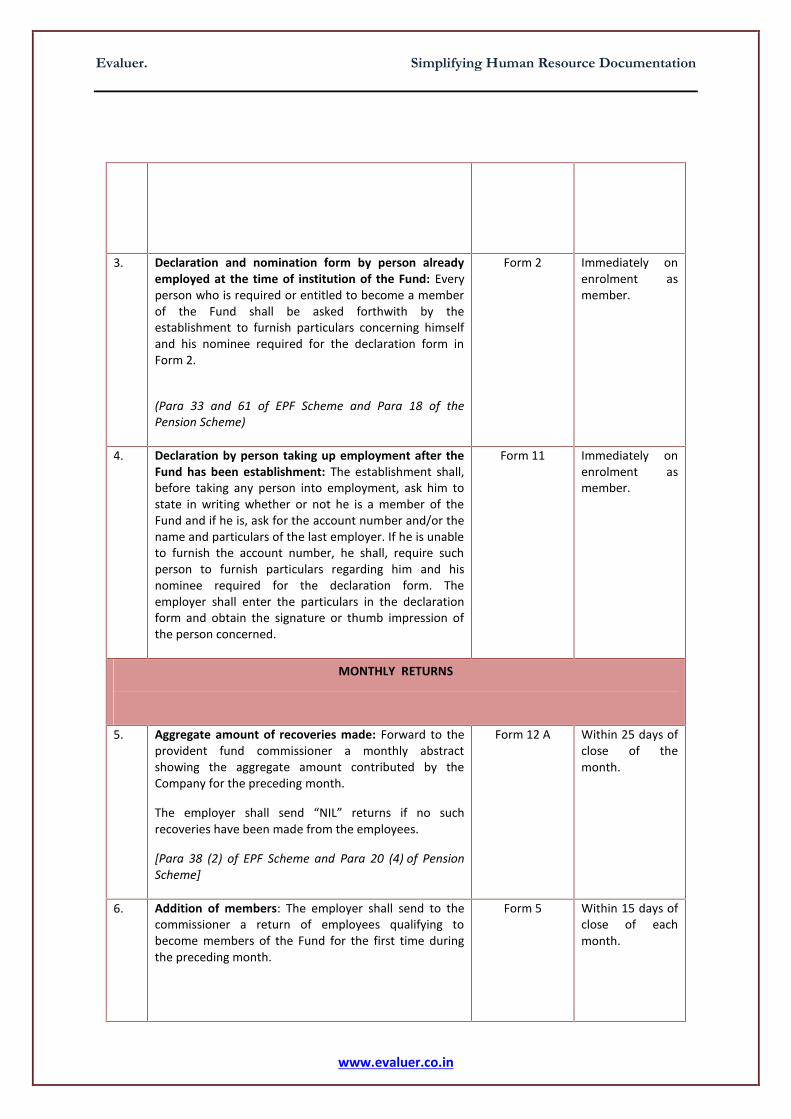

3. Declaration and nomination form by person alreadyemployed at the time of institution of the Fund: Everyperson who is required or entitled to become a memberof the Fund shall be asked forthwith by theestablishment to furnish particulars concerning himselfand his nominee required for the declaration form inForm 2.

(Para 33 and 61 of EPF Scheme and Para 18 of thePension Scheme)

Form 2 Immediately onenrolment asmember.

4. Declaration by person taking up employment after theFund has been establishment: The establishment shall,before taking any person into employment, ask him tostate in writing whether or not he is a member of theFund and if he is, ask for the account number and/or thename and particulars of the last employer. If he is unableto furnish the account number, he shall, require suchperson to furnish particulars regarding him and hisnominee required for the declaration form. Theemployer shall enter the particulars in the declarationform and obtain the signature or thumb impression ofthe person concerned.

Form 11 Immediately onenrolment asmember.

MONTHLY RETURNS

5. Aggregate amount of recoveries made: Forward to theprovident fund commissioner a monthly abstractshowing the aggregate amount contributed by theCompany for the preceding month.

The employer shall send “NIL” returns if no suchrecoveries have been made from the employees.

[Para 38 (2) of EPF Scheme and Para 20 (4) of PensionScheme]

Form 12 A Within 25 days ofclose of themonth.

6. Addition of members: The employer shall send to thecommissioner a return of employees qualifying tobecome members of the Fund for the first time duringthe preceding month.

Form 5 Within 15 days ofclose of eachmonth.

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

7.

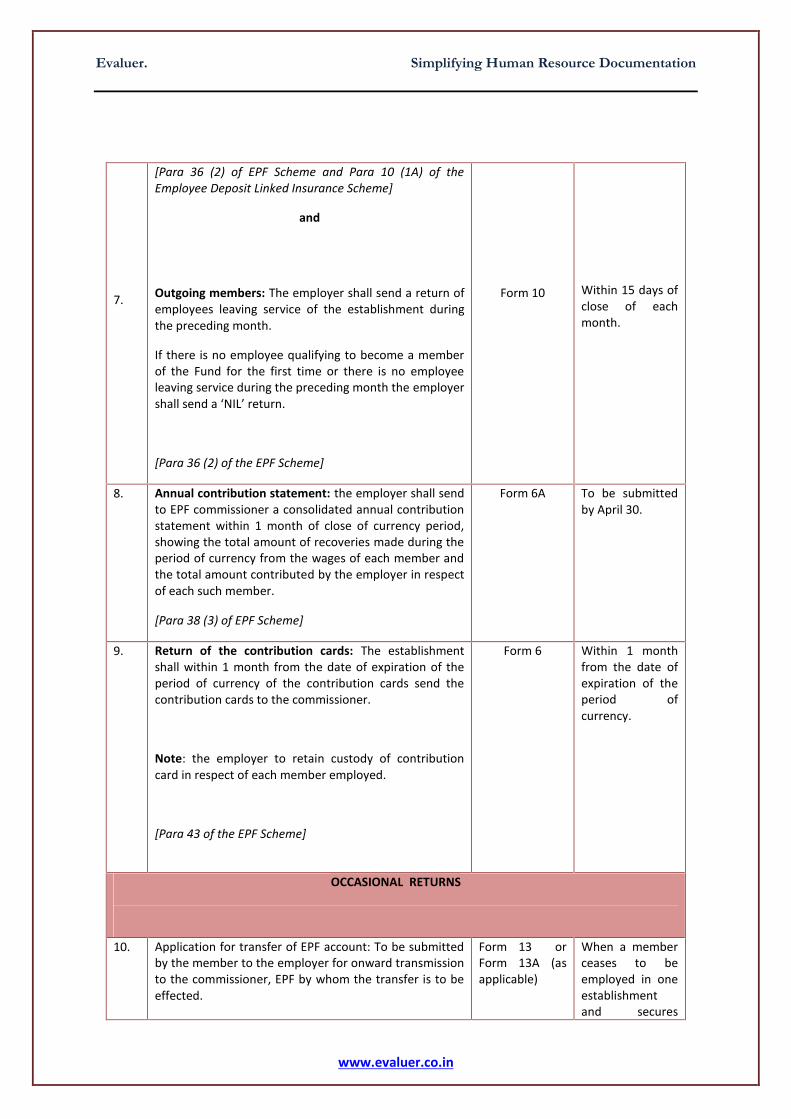

[Para 36 (2) of EPF Scheme and Para 10 (1A) of theEmployee Deposit Linked Insurance Scheme]

and

Outgoing members: The employer shall send a return ofemployees leaving service of the establishment duringthe preceding month.

If there is no employee qualifying to become a memberof the Fund for the first time or there is no employeeleaving service during the preceding month the employershall send a ‘NIL’ return.

[Para 36 (2) of the EPF Scheme]

Form 10 Within 15 days ofclose of eachmonth.

8. Annual contribution statement: the employer shall sendto EPF commissioner a consolidated annual contributionstatement within 1 month of close of currency period,showing the total amount of recoveries made during theperiod of currency from the wages of each member andthe total amount contributed by the employer in respectof each such member.

[Para 38 (3) of EPF Scheme]

Form 6A To be submittedby April 30.

9. Return of the contribution cards: The establishmentshall within 1 month from the date of expiration of theperiod of currency of the contribution cards send thecontribution cards to the commissioner.

Note: the employer to retain custody of contributioncard in respect of each member employed.

[Para 43 of the EPF Scheme]

Form 6 Within 1 monthfrom the date ofexpiration of theperiod ofcurrency.

OCCASIONAL RETURNS

10. Application for transfer of EPF account: To be submittedby the member to the employer for onward transmissionto the commissioner, EPF by whom the transfer is to beeffected.

Form 13 orForm 13A (asapplicable)

When a memberceases to beemployed in oneestablishmentand secures

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

(Para 57 of EPF Scheme)

employment inanotherestablishment.

11. Application for financing a life insurance policy out of theprovident fund account.

(Para 62 EPF Scheme)

Form 14 At the discretionof the employee.

12. Application by an adult member of the Provident FundScheme for claiming provident fund dues.

[Para 72 (5) of the EPF Scheme]

Form 19 At the time whenmember of thefund leavesservice.

13. For claiming withdrawal benefits under the PensionScheme by a member.

Form 10 C As required bythe member.

14. Application for monthly pension. Form 10 D As and whenrequired.

15. Application for payment of assurance benefit ofdeceased employee to nominee.

(Para 23 of the Employee Deposit-Linked InsuranceScheme)

Form 5 (IF) As and whenrequired.

16. In the event of death of member, this form is to be usedby a nominee / family member to claim the member'sProvident Fund accumulation.

Form 20 As and whenrequired.

RECORD MAINTENANCE

18. The company shall maintain an inspection book, for anInspector to record his observation on visiting theestablishment.

[Para 36 (4) of EPF Scheme]

Inspection bookas specified bycommissioner

Inspection bookmaintained forobservations ofthe Inspector.

19. The establishment shall maintain such accounts inrelation to the amounts contributed to the Fund by himand by his employee as the Central Board may, fromtime to time, direct.

[Para 36 (5) of EPF Scheme]

As directed bythe CentralBoard.

CONTRIBUTION CHECK

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

20.

21

22.

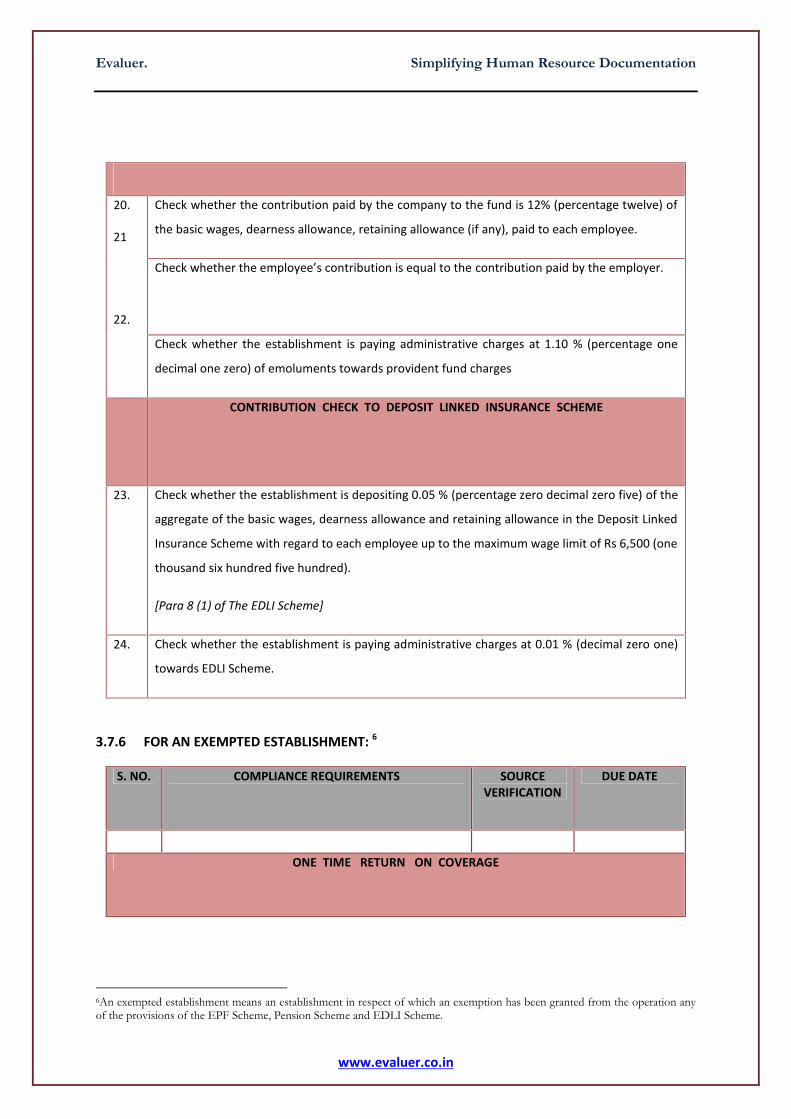

Check whether the contribution paid by the company to the fund is 12% (percentage twelve) of

the basic wages, dearness allowance, retaining allowance (if any), paid to each employee.

Check whether the employee’s contribution is equal to the contribution paid by the employer.

Check whether the establishment is paying administrative charges at 1.10 % (percentage one

decimal one zero) of emoluments towards provident fund charges

CONTRIBUTION CHECK TO DEPOSIT LINKED INSURANCE SCHEME

23. Check whether the establishment is depositing 0.05 % (percentage zero decimal zero five) of the

aggregate of the basic wages, dearness allowance and retaining allowance in the Deposit Linked

Insurance Scheme with regard to each employee up to the maximum wage limit of Rs 6,500 (one

thousand six hundred five hundred).

[Para 8 (1) of The EDLI Scheme]

24. Check whether the establishment is paying administrative charges at 0.01 % (decimal zero one)

towards EDLI Scheme.

3.7.6 FOR AN EXEMPTED ESTABLISHMENT: 6

S. NO. COMPLIANCE REQUIREMENTS SOURCEVERIFICATION

DUE DATE

ONE TIME RETURN ON COVERAGE

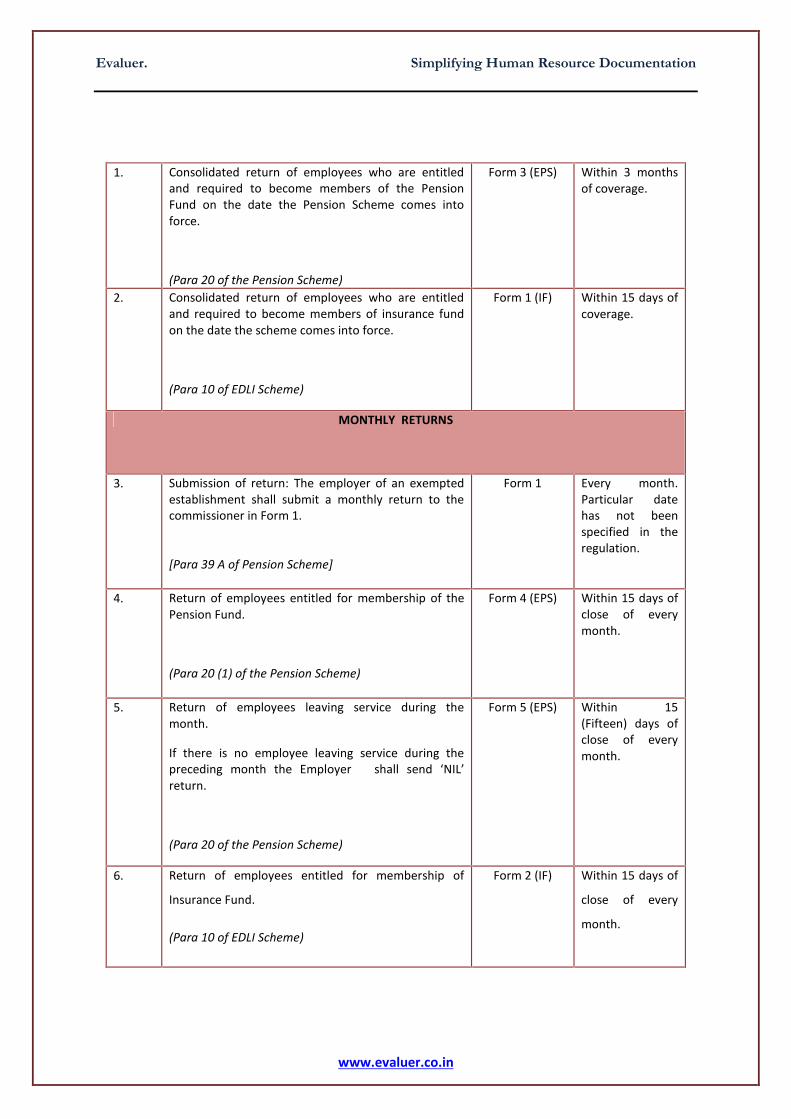

6An exempted establishment means an establishment in respect of which an exemption has been granted from the operation anyof the provisions of the EPF Scheme, Pension Scheme and EDLI Scheme.

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

1. Consolidated return of employees who are entitledand required to become members of the PensionFund on the date the Pension Scheme comes intoforce.

(Para 20 of the Pension Scheme)

Form 3 (EPS) Within 3 monthsof coverage.

2. Consolidated return of employees who are entitledand required to become members of insurance fundon the date the scheme comes into force.

(Para 10 of EDLI Scheme)

Form 1 (IF) Within 15 days ofcoverage.

MONTHLY RETURNS

3. Submission of return: The employer of an exemptedestablishment shall submit a monthly return to thecommissioner in Form 1.

[Para 39 A of Pension Scheme]

Form 1 Every month.Particular datehas not beenspecified in theregulation.

4. Return of employees entitled for membership of thePension Fund.

(Para 20 (1) of the Pension Scheme)

Form 4 (EPS) Within 15 days ofclose of everymonth.

5. Return of employees leaving service during themonth.

If there is no employee leaving service during thepreceding month the Employer shall send ‘NIL’return.

(Para 20 of the Pension Scheme)

Form 5 (EPS) Within 15(Fifteen) days ofclose of everymonth.

6. Return of employees entitled for membership of

Insurance Fund.

(Para 10 of EDLI Scheme)

Form 2 (IF) Within 15 days of

close of every

month.

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

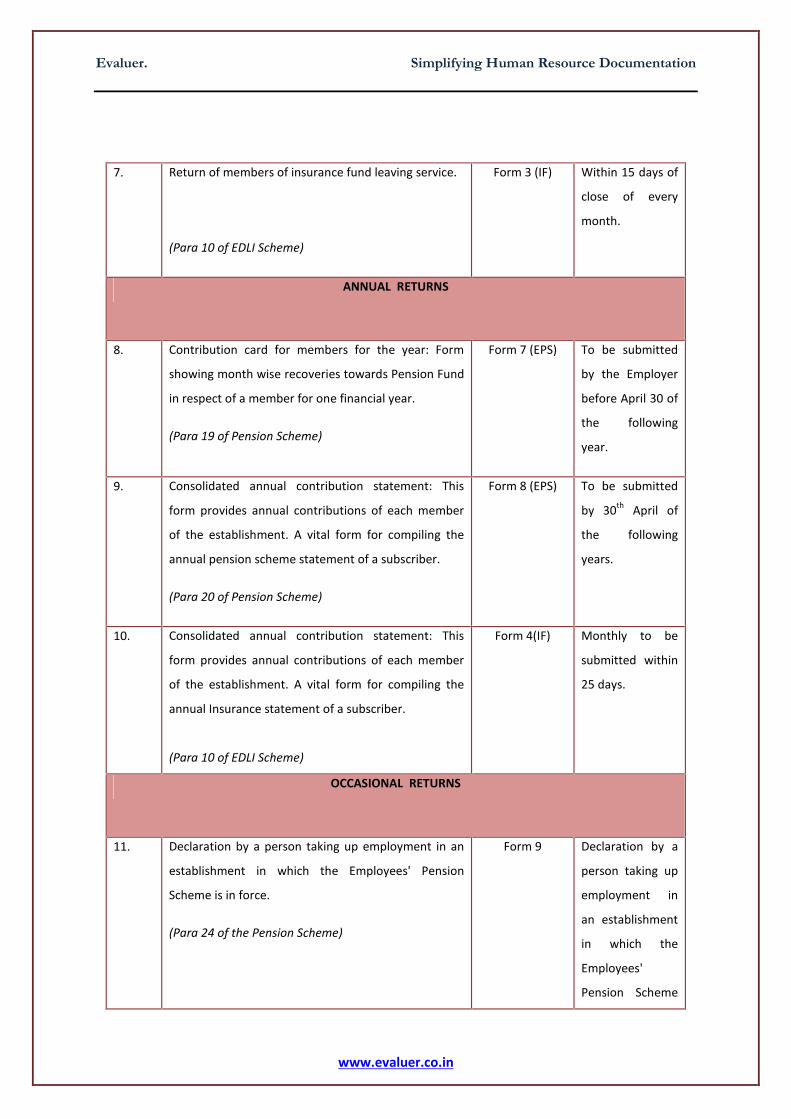

7. Return of members of insurance fund leaving service.

(Para 10 of EDLI Scheme)

Form 3 (IF) Within 15 days of

close of every

month.

ANNUAL RETURNS

8. Contribution card for members for the year: Form

showing month wise recoveries towards Pension Fund

in respect of a member for one financial year.

(Para 19 of Pension Scheme)

Form 7 (EPS) To be submitted

by the Employer

before April 30 of

the following

year.

9. Consolidated annual contribution statement: This

form provides annual contributions of each member

of the establishment. A vital form for compiling the

annual pension scheme statement of a subscriber.

(Para 20 of Pension Scheme)

Form 8 (EPS) To be submitted

by 30th April of

the following

years.

10. Consolidated annual contribution statement: This

form provides annual contributions of each member

of the establishment. A vital form for compiling the

annual Insurance statement of a subscriber.

(Para 10 of EDLI Scheme)

Form 4(IF) Monthly to be

submitted within

25 days.

OCCASIONAL RETURNS

11. Declaration by a person taking up employment in an

establishment in which the Employees' Pension

Scheme is in force.

(Para 24 of the Pension Scheme)

Form 9 Declaration by a

person taking up

employment in

an establishment

in which the

Employees'

Pension Scheme

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

is in force.

Evaluer. Simplifying Human Resource Documentation

www.evaluer.co.in

For further information please

Disclaimer:

This handbook is not an advertisement or any form of solicitation. This

handbook has been compiled for general information of the public and does

not constitute professional guidance or legal opinion. Readers should

obtain appropriate professional advice.

Simplifying Human Resource Documentation

Delhi | Bangalore | Chandigarh

Related Documents