Dr. Ravi Shekhar Vishal Page 1 Employee Provident Fund Act Employee Provident Fund (EPF) is one of the main platforms of savings in India for nearly all people working in Government, Public or Private sector Organizations. This article is about what is Employee Provident Fund (EPF), Employee Pension Scheme (EPS), Employees Deposit Linked Insurance Scheme (EDLIS), how the contributions are calculated based on basic salary and dearness allowance, what are the EPF interest rate, how much would one save in EPF, how would one know about the amount accumulated in PF. What is Employee Provident Fund? A provident fund is created with a purpose of providing financial security and stability to elderly people. Generally one contributes in these funds when one starts as employee, the contributions are made on a regular basis (monthly in most cases). It’s purpose is to help employees save a fraction of their salary every month, to be used in an event that the employee is temporarily or no longer fit to work or at retirement. The investments made by a number of people / employees are pooled together and invested by a trust. Employee Provident Fund (EPF) is implemented by the Employees Provident Fund Organisation (EPFO) of India. An establishment with 20 or more workers working in any one of the 180+ industries ( given here ) should register with EPFO. Typically 12% of the Basic, DA, and cash value of food allowances has to be contributed to the EPF account. EPFO is a statutory body of the Indian Government under Labour and Employment Ministry. It is one of the largest social security organisations in the world in terms of members and volume of financial transactions undertaken. EPF, EPS, EDLIS The Constitution of India under “Directive Principles of State Policy” provides that the State shall within the limits of its economic capacity make effective provision for securing the right to work, to education and to public assistance in cases of unemployment, old-age, sickness & disablement and undeserved want. The EPF & MP Act, 1952 was enacted by Parliament and came into force with effect from 4th March,1952. A series of legislative interventions were made in this direction, including the Employees’ Provident Funds & Miscellaneous Provisions Act, 1952. Presently, the following

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Dr. Ravi Shekhar Vishal Page 1

Employee Provident Fund Act

Employee Provident Fund (EPF) is one of the main platforms of savings in India for nearly all

people working in Government, Public or Private sector Organizations. This article is about what

is Employee Provident Fund (EPF), Employee Pension Scheme (EPS), Employees Deposit

Linked Insurance Scheme (EDLIS), how the contributions are calculated based on basic salary

and dearness allowance, what are the EPF interest rate, how much would one save in EPF, how

would one know about the amount accumulated in PF.

What is Employee Provident Fund?

A provident fund is created with a purpose of providing financial security and stability to elderly

people. Generally one contributes in these funds when one starts as employee, the contributions

are made on a regular basis (monthly in most cases). It’s purpose is to help employees save a

fraction of their salary every month, to be used in an event that the employee is temporarily or no

longer fit to work or at retirement. The investments made by a number of people / employees are

pooled together and invested by a trust.

Employee Provident Fund (EPF) is implemented by the Employees Provident Fund

Organisation (EPFO) of India. An establishment with 20 or more workers working in any one of

the 180+ industries ( given here) should register with EPFO. Typically 12% of the Basic, DA,

and cash value of food allowances has to be contributed to the EPF account. EPFO is a statutory

body of the Indian Government under Labour and Employment Ministry. It is one of the largest

social security organisations in the world in terms of members and volume of financial

transactions undertaken.

EPF, EPS, EDLIS

The Constitution of India under “Directive Principles of State Policy” provides that the State

shall within the limits of its economic capacity make effective provision for securing the right to

work, to education and to public assistance in cases of unemployment, old-age, sickness &

disablement and undeserved want.

The EPF & MP Act, 1952 was enacted by Parliament and came into force with effect from 4th

March,1952. A series of legislative interventions were made in this direction, including the

Employees’ Provident Funds & Miscellaneous Provisions Act, 1952. Presently, the following

Dr. Ravi Shekhar Vishal Page 2

three schemes are in operation under the Acts:( Click on the link if interested in reading the acts

which are in pdf format)

1. Employees’ Provident Fund Scheme, (EPS)1952

2. Employees’ Deposit Linked Insurance Scheme,(EDILS) 1976

3. Employees’ Pension Scheme, 1995 (replacing the Employees’ Family Pension Scheme,

1971)(EPS)

Employees’ Pension Scheme (EPS) of 1995 offers pension on disablement, widow pension,

and pension for nominees. EPS program replaced the Family Pension Scheme (FPS). It is

financed by

diverting 8.33 percent of employer’s monthly contribution from the EPF(restricted to 8.33% of

6500 or Rs 541) and government’s contribution of 1.17 percent of the worker’s monthly wages.

The purpose of the scheme is to provide for

1) Superannuation Pension: Member who has rendered eligible service of 20 years and retires

on attaining the age of 58 years.

2) Retiring Pension: member who has rendered eligible service of 20 years and retires or

otherwise ceases to be in employment before attaining the age of 58 years.

3) Permanent Total Disablement Pension

4) Short service Pension: Member has to render eligible service of 10 years and more but less

than 20 years.

Employees Deposit Linked Insurance Scheme (EDLIS)

Under the EDLI scheme life insurance cover is provided to the PF members. The cost of the

scheme is borne by the employer but as the amount of life coverage under this statutory scheme

is very low (a maximum amount of Rs. 60,000), usually employers opt out of the EDLI scheme

by going for group insurance scheme which usually provides higher coverage to employees

without any increase in cost to the employer.

EPF, EPS and EDLIS are calculated on Basic salary, Dearness allowances(DA), cash value of

food concession and retaining allowances if any. Most of the organizations follow Basic+ DA

Method.

Retaining allowances means an allowance payable for the time being to an employee of any

factory or other establishment during any period in which the establishment is not working, for

retaining his services.

Table below gives the rates of contribution of EPF, EPS, EDLI, Admin charges in India.

Dr. Ravi Shekhar Vishal Page 3

Scheme Name Employee contribution Employer contribution

Employee provident fund 12% 3.67%

Employees’ Pension scheme 0 8.33%

Employees Deposit linked insurance 0 0.5%

EPF Administrative charges 0 1.1%

EDLIS Administrative charges 0 0.01%

In industries like beedi, jute, guar gum factories, coir industry (other than spinning sector) the

Employee contribution is 10% while employer’s contribution is 1.67%.

Employees drawing basic salary upto Rs 6500/- have to compulsory contribute to the Provident

fund and employees drawing above Rs 6501/- have an option to become member of the

Provident Fund. It is beneficial for employees who draw salary above Rs 6501/- to become

member of Provident Fund as it is deducted from the salary before it is deposited on bank or

given hence compulsorily saving happens. Employee’s contribution is matched by

Employer’s contribution(till 12%) so extra money and it is helpful for tax purpose too. The

employer contribution is exempt from tax and employee’s contribution is taxable but

eligible for deduction under section 80C of Income tax Act.

Calculation of Employees Provident Fund Contributions

Basic salary of Rs 3500

Let us calculate the contribution of an employee who is getting a basic salary of Rs 3500.

Contribution Towards Calculation Amount

EPF Employees share 3500 x 12% 420

EPS Employer share 3500 x 8.33% 292

EPF employer share 3500 x 3.67% 128

EDLI charges 3500 x 0.5% 18

EPF Admin charges 3500 x 1.1% 39

EDLI Admin charges 3500 x 0.01% 0.35 ( round up to Rs 1/-)

Basic salary above Rs 6500

In such cases companies uses different method for calculation as per their pay roll

policy. Consider an employee getting a basic salary of 7500/- We can calculate it in different

ways but EPS is calculated only up to 6500/- that means the maximum amount is fixed to Rs

541.00. The three methods mentioned below are based on the above example.

Dr. Ravi Shekhar Vishal Page 4

Method-1

If company consider total basic salary above the limit fixed 6500.00 for PF

calculation. Employer has decided to contribute on total basic salary which is 12 % on 7500.00

equal to 900.00. EPS Share is fixed to 541. Balance (900-541) goes to EPF account 359.00. You

may be thinking that, what about 3.67%?, Here you don’t need to care about it.

Contribution Towards Calculation Amount

EPF Employees share 7500 x 12% 900

EPS Employer share 6500 x 8.33% 541

EPF employer share 7500 x 12% (-) 541 359

EDLI charges 7500 x 0.5% 38

EPF Admin charges 7500 x 1.1% 83

EDLI Admin charges 7500 x 0.01% 0.75 ( Round up to Rs 1/-)

Method -2

Some companies follows the below method in which employee share is calculated on 7500/- and

employer share is calculated on up limit Rs 6500/-

Contribution Towards Calculation Amount

EPF Employees share 7500 x 12% 900

EPS Employer share 6500 x 8.33% 541

EPF employer share 6500 x 3.67% 239

EDLI charges 6500 x 0.5% 33

EPF Admin charges 6500 x 1.1% 72

EDLI Admin charges 6500 x 0.01% 0.65 ( Round up to Rs 1/-)

Method-3

Some companies calculate both employer and employee shares on 6500/- in spite of higher basic

salary than 6500.00

Contribution Towards Calculation Amount

EPF Employees share 6500 x 12% 780

EPS Employer share 6500 x 8.33% 541

EPF employer share 6500 x 3.67% 239

EDLI charges 6500 x 0.5% 33

EPF Admin charges 6500 x 1.1% 72

EDLI Admin charges 6500 x 0.01% 0.65 ( Round up to Rs 1/-)

Dr. Ravi Shekhar Vishal Page 5

EPF scheme allows partial withdrawals for the purpose of marriage/illness/higher

education/house construction etc.

SOME COMMON QUESTIONS:

Q. What is the interest on the PF accumulations?

A : Compound interest as declared by Central Govt. is paid on the amount standing to the credit

of an employee as on 1st April every year.

Q. What is the EPF Interest Rate?

The EPF interest rate of India is decided by the central government with the consultation of

Central Board of trustees. In the past several decades, the interest rate has ranged from 8-12 % of

the balances maintained in the fund. The EPF interest rate notification is available on the official

website of EPF India on an annual basis. The same is communicated through major dailies in all

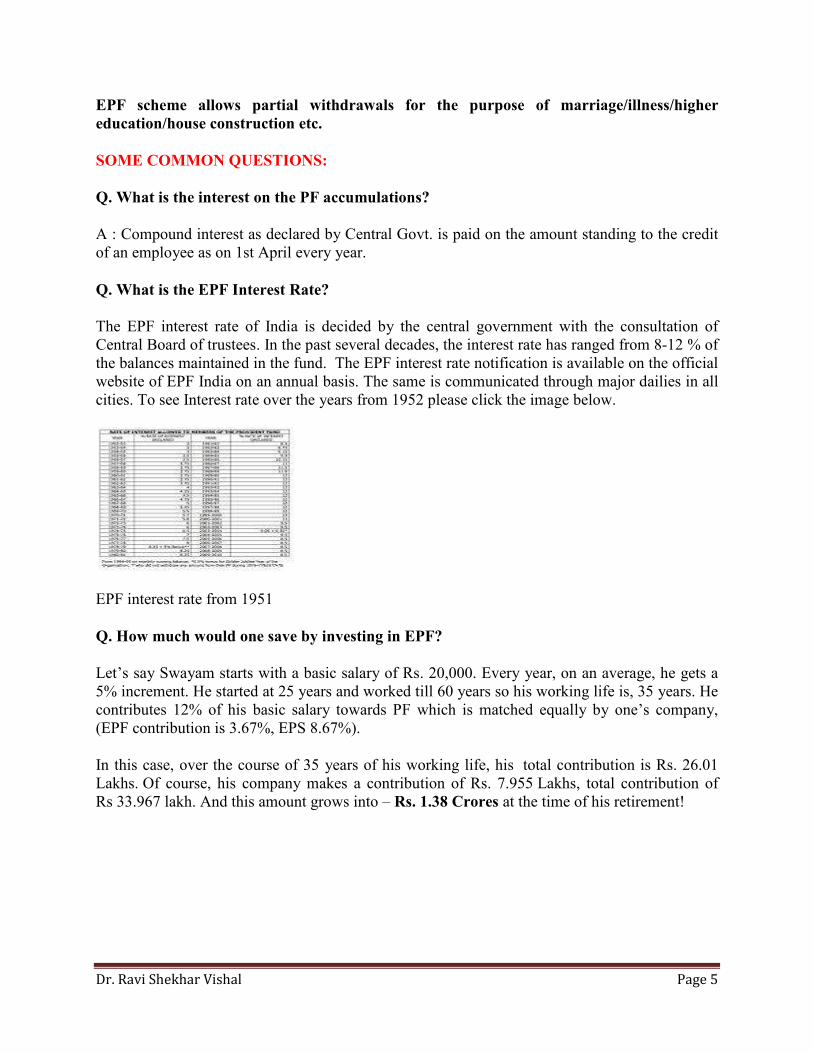

cities. To see Interest rate over the years from 1952 please click the image below.

EPF interest rate from 1951

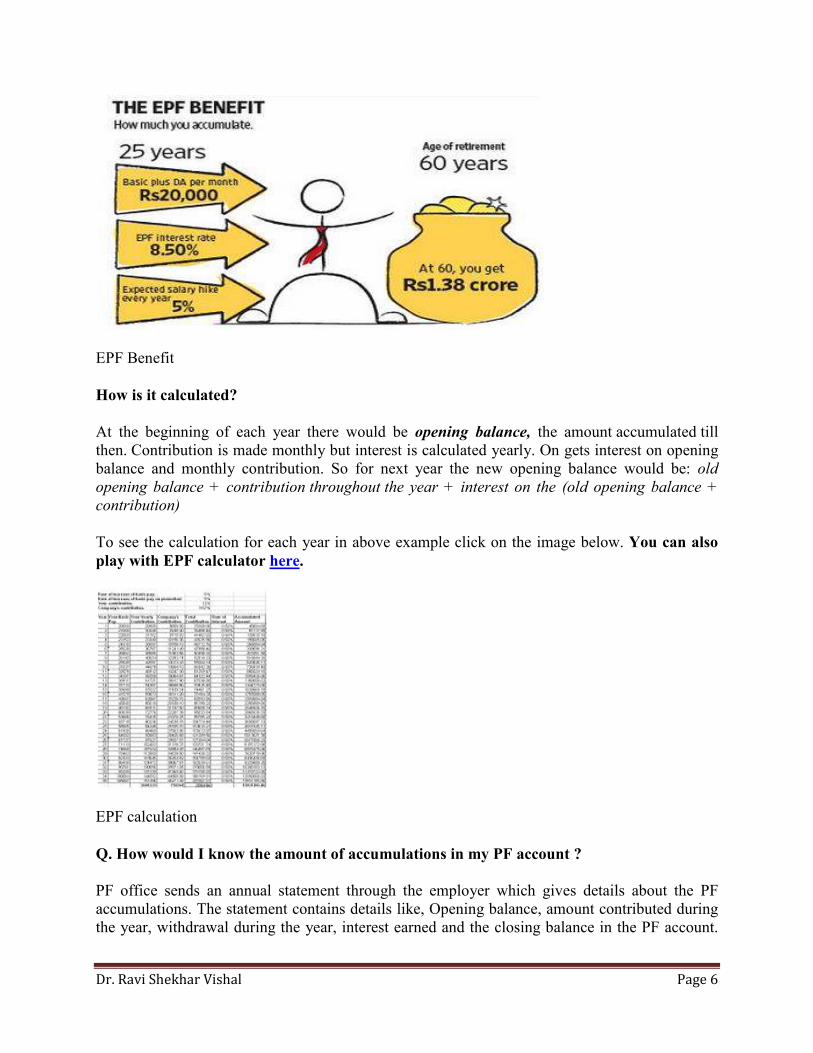

Q. How much would one save by investing in EPF?

Let’s say Swayam starts with a basic salary of Rs. 20,000. Every year, on an average, he gets a

5% increment. He started at 25 years and worked till 60 years so his working life is, 35 years. He

contributes 12% of his basic salary towards PF which is matched equally by one’s company,

(EPF contribution is 3.67%, EPS 8.67%).

In this case, over the course of 35 years of his working life, his total contribution is Rs. 26.01

Lakhs. Of course, his company makes a contribution of Rs. 7.955 Lakhs, total contribution of

Rs 33.967 lakh. And this amount grows into – Rs. 1.38 Crores at the time of his retirement!

Dr. Ravi Shekhar Vishal Page 6

EPF Benefit

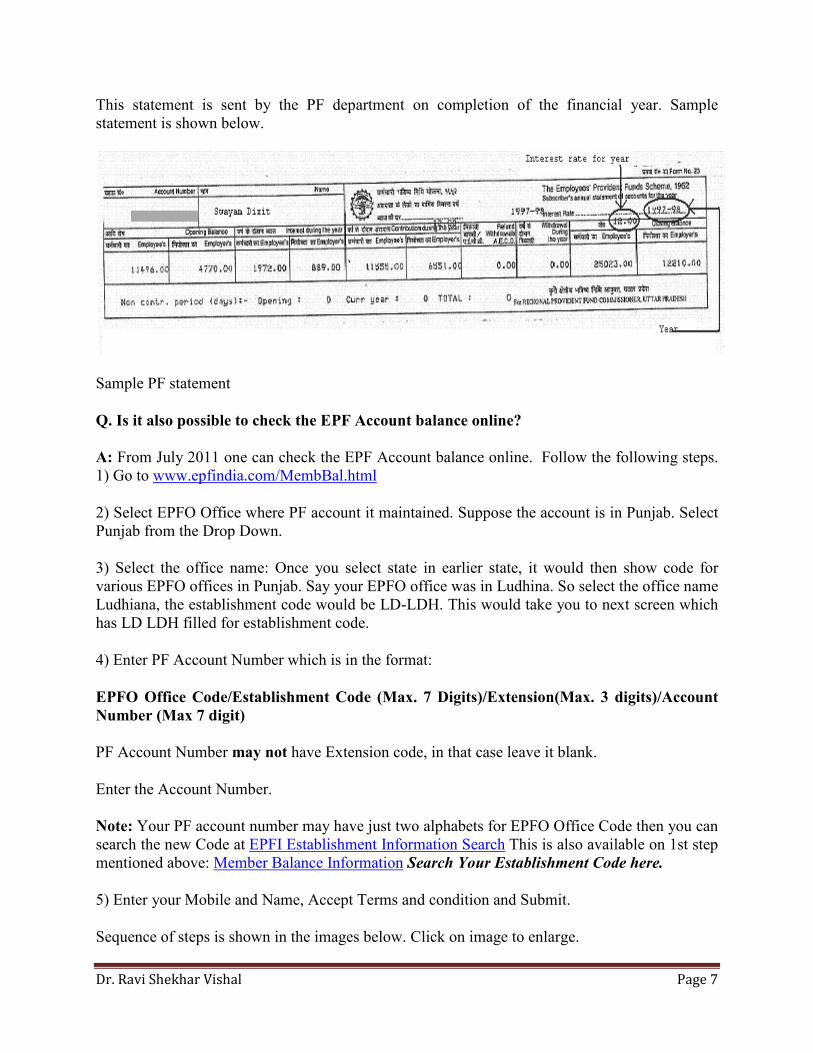

How is it calculated?

At the beginning of each year there would be opening balance, the amount accumulated till

then. Contribution is made monthly but interest is calculated yearly. On gets interest on opening

balance and monthly contribution. So for next year the new opening balance would be: old

opening balance + contribution throughout the year + interest on the (old opening balance +

contribution)

To see the calculation for each year in above example click on the image below. You can also

play with EPF calculator here.

EPF calculation

Q. How would I know the amount of accumulations in my PF account ?

PF office sends an annual statement through the employer which gives details about the PF

accumulations. The statement contains details like, Opening balance, amount contributed during

the year, withdrawal during the year, interest earned and the closing balance in the PF account.

Dr. Ravi Shekhar Vishal Page 7

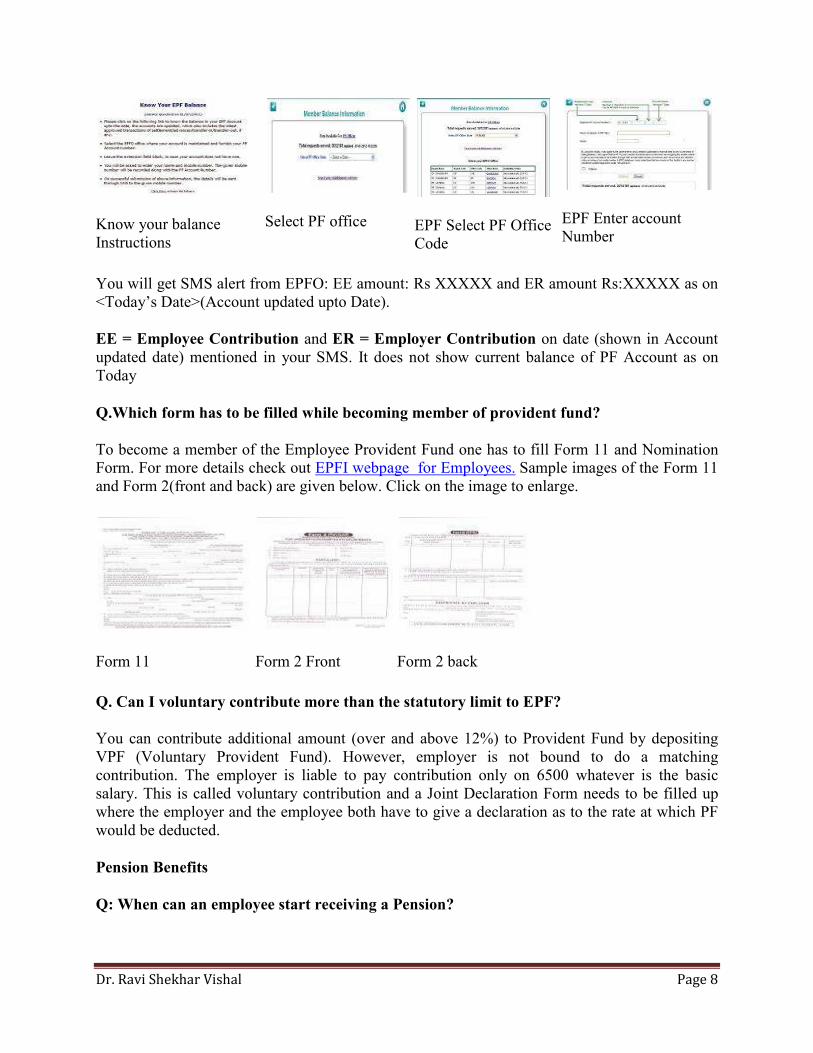

This statement is sent by the PF department on completion of the financial year. Sample

statement is shown below.

Sample PF statement

Q. Is it also possible to check the EPF Account balance online?

A: From July 2011 one can check the EPF Account balance online. Follow the following steps.

1) Go to www.epfindia.com/MembBal.html

2) Select EPFO Office where PF account it maintained. Suppose the account is in Punjab. Select

Punjab from the Drop Down.

3) Select the office name: Once you select state in earlier state, it would then show code for

various EPFO offices in Punjab. Say your EPFO office was in Ludhina. So select the office name

Ludhiana, the establishment code would be LD-LDH. This would take you to next screen which

has LD LDH filled for establishment code.

4) Enter PF Account Number which is in the format:

EPFO Office Code/Establishment Code (Max. 7 Digits)/Extension(Max. 3 digits)/Account

Number (Max 7 digit)

PF Account Number may not have Extension code, in that case leave it blank.

Enter the Account Number.

Note: Your PF account number may have just two alphabets for EPFO Office Code then you can

search the new Code at EPFI Establishment Information Search This is also available on 1st step

mentioned above: Member Balance Information Search Your Establishment Code here.

5) Enter your Mobile and Name, Accept Terms and condition and Submit.

Sequence of steps is shown in the images below. Click on image to enlarge.

Dr. Ravi Shekhar Vishal Page 8

Know your balance

Instructions

Select PF office

EPF Select PF Office

Code

EPF Enter account

Number

You will get SMS alert from EPFO: EE amount: Rs XXXXX and ER amount Rs:XXXXX as on

<Today’s Date>(Account updated upto Date).

EE = Employee Contribution and ER = Employer Contribution on date (shown in Account

updated date) mentioned in your SMS. It does not show current balance of PF Account as on

Today

Q.Which form has to be filled while becoming member of provident fund?

To become a member of the Employee Provident Fund one has to fill Form 11 and Nomination

Form. For more details check out EPFI webpage for Employees. Sample images of the Form 11

and Form 2(front and back) are given below. Click on the image to enlarge.

Form 11

Form 2 Front

Form 2 back

Q. Can I voluntary contribute more than the statutory limit to EPF?

You can contribute additional amount (over and above 12%) to Provident Fund by depositing

VPF (Voluntary Provident Fund). However, employer is not bound to do a matching

contribution. The employer is liable to pay contribution only on 6500 whatever is the basic

salary. This is called voluntary contribution and a Joint Declaration Form needs to be filled up

where the employer and the employee both have to give a declaration as to the rate at which PF

would be deducted.

Pension Benefits

Q: When can an employee start receiving a Pension?

Dr. Ravi Shekhar Vishal Page 9

A: A employee can start receiving the pension under EPS only after rendering a minimum

service of 10 years and attaining the age of 58/50 years. However, no pension is payable before

the age of 50 years and early pension after 50 years but before the age of 58 years is subject to

discounting factor @ 4% (w.e.f. 26.09.2008) for every year falling short of 58 years. In case of

death / disablement, the above restriction doesn’t apply.

Q: How long the pension is available?

A: Lifelong pension is available to the member and upon his death members of the family are

entitled for the pension.

Q: What is the formula for calculating the monthly pension?

A: Under Employees’ Pension Scheme, the monthly retiring pension is decided on the basis of

‘Pensionable Service’ and ‘Pensionable Salary’ and is worked out as follows

Monthly pension=( Pensionable salary*Pensionable service)/70

Pensionable Salary is arrived at by considering the average contributing salary immediately

preceding 12 months from the date of exit from the scheme, normally this would be limited to Rs

6,500 p.m. unless certain enhanced contributions are made by the employer with

permission. Pensionable Service is the service in years rendered by the member for which

contributions have been received maximum cannot exceed 35 years

Q: What is the maximum amount of Pension available under EPS? A: Based on a maximum employment period of 35 years, and maximum contribution of Rs 6500,

the maximum amount of pension as per the Pension formula would be = 6500 * 35)/70 = Rs

3,250 per month or Rs. 39,000(3250 * 12) per year.

Q. Is the Monthly Pension paid under EPS just?

The amount of pension is meager. If one would have invested Rs 541 in a recurring deposit at the

rate of 8% for 35 years one would get 12,49,263 as maturity amount. If this maturity amount is

put in buying the Pension plan say LIC’s Jeevan Akshay VI and put the above amount Rs

12,49,263 in the premium calculator of LIC with option as Annuity payable for life, one would

get monthly pension of Rs 10,150 which is much more than Rs 3250.

In this article we covered about EPF, EPS, the calculation etc. In the next article we shall cover

about how to withdraw or transfer from EPF, EPS. Difference between EPF and PPF? If you find

something missing or incorrect please let us know, we shall correct is As Soon As Possible

(ASAP). Hope you found this article helpful. What are you thoughts on EPF? Does it make sense

to contribute to EPF?

Dr. Ravi Shekhar Vishal Page 10

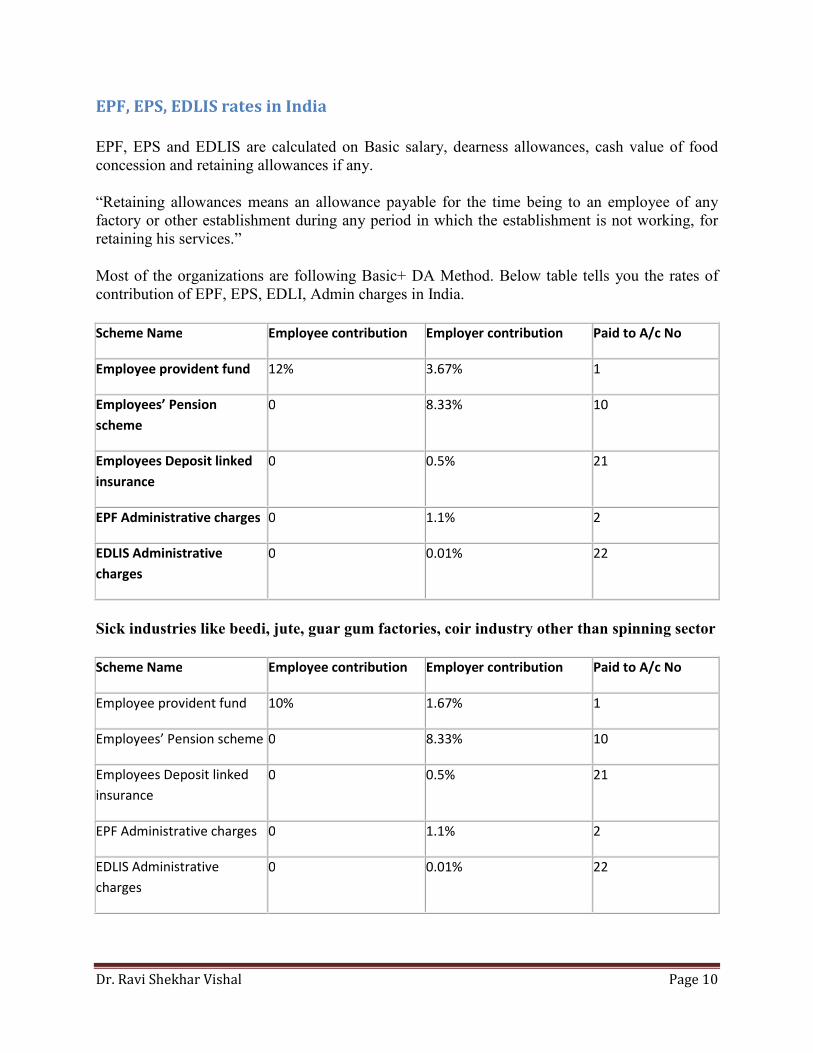

EPF, EPS, EDLIS rates in India

EPF, EPS and EDLIS are calculated on Basic salary, dearness allowances, cash value of food

concession and retaining allowances if any.

“Retaining allowances means an allowance payable for the time being to an employee of any

factory or other establishment during any period in which the establishment is not working, for

retaining his services.”

Most of the organizations are following Basic+ DA Method. Below table tells you the rates of

contribution of EPF, EPS, EDLI, Admin charges in India.

Scheme Name Employee contribution Employer contribution Paid to A/c No

Employee provident fund 12% 3.67% 1

Employees’ Pension

scheme

0 8.33% 10

Employees Deposit linked

insurance

0 0.5% 21

EPF Administrative charges 0 1.1% 2

EDLIS Administrative

charges

0 0.01% 22

Sick industries like beedi, jute, guar gum factories, coir industry other than spinning sector

Scheme Name Employee contribution Employer contribution Paid to A/c No

Employee provident fund 10% 1.67% 1

Employees’ Pension scheme 0 8.33% 10

Employees Deposit linked

insurance

0 0.5% 21

EPF Administrative charges 0 1.1% 2

EDLIS Administrative

charges

0 0.01% 22

Dr. Ravi Shekhar Vishal Page 11

Inspection charges payable by employer

Inspection charges must be paid by the employer in the following Cases.

1. Some establishment are exempted from EDLI contribution as they are providing the same

nature of benefit without any contributions from employee, such establishments are liable to

pay 0.005% on Basic salary

2. The establishments exempted under the scheme should pay 0.18% of Basic salary towards

inspection charges.

EPF Ceiling Limit

EPF ceiling limit is fixed to 6500/-.The employer is liable to pay contribution only on 6500/-

Whatever is the basic salary

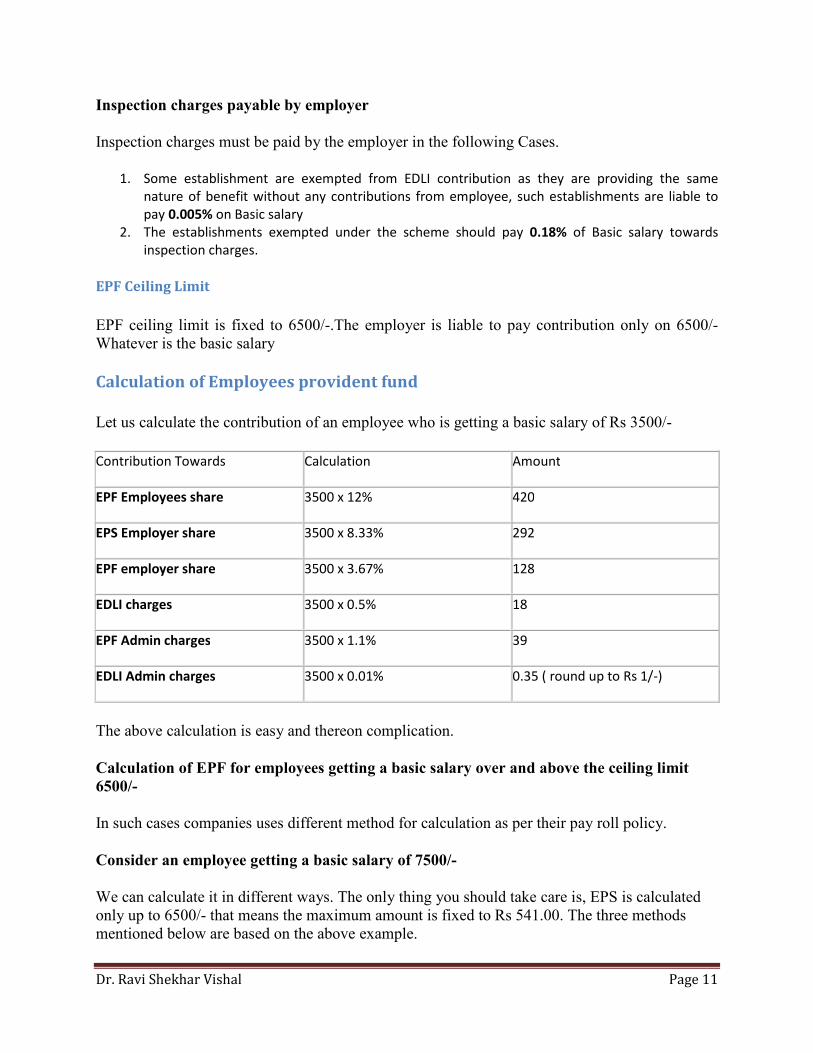

Calculation of Employees provident fund

Let us calculate the contribution of an employee who is getting a basic salary of Rs 3500/-

Contribution Towards Calculation Amount

EPF Employees share 3500 x 12% 420

EPS Employer share 3500 x 8.33% 292

EPF employer share 3500 x 3.67% 128

EDLI charges 3500 x 0.5% 18

EPF Admin charges 3500 x 1.1% 39

EDLI Admin charges 3500 x 0.01% 0.35 ( round up to Rs 1/-)

The above calculation is easy and thereon complication.

Calculation of EPF for employees getting a basic salary over and above the ceiling limit

6500/-

In such cases companies uses different method for calculation as per their pay roll policy.

Consider an employee getting a basic salary of 7500/-

We can calculate it in different ways. The only thing you should take care is, EPS is calculated

only up to 6500/- that means the maximum amount is fixed to Rs 541.00. The three methods

mentioned below are based on the above example.

Dr. Ravi Shekhar Vishal Page 12

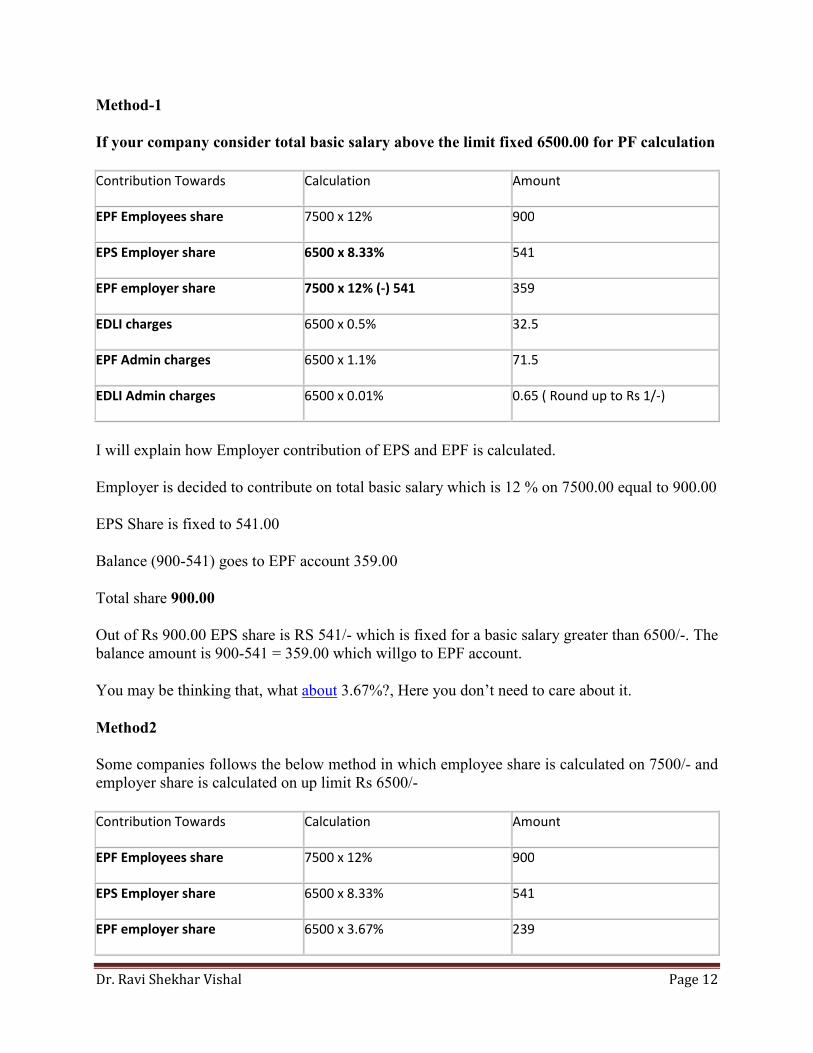

Method-1

If your company consider total basic salary above the limit fixed 6500.00 for PF calculation

Contribution Towards Calculation Amount

EPF Employees share 7500 x 12% 900

EPS Employer share 6500 x 8.33% 541

EPF employer share 7500 x 12% (-) 541 359

EDLI charges 6500 x 0.5% 32.5

EPF Admin charges 6500 x 1.1% 71.5

EDLI Admin charges 6500 x 0.01% 0.65 ( Round up to Rs 1/-)

I will explain how Employer contribution of EPS and EPF is calculated.

Employer is decided to contribute on total basic salary which is 12 % on 7500.00 equal to 900.00

EPS Share is fixed to 541.00

Balance (900-541) goes to EPF account 359.00

Total share 900.00

Out of Rs 900.00 EPS share is RS 541/- which is fixed for a basic salary greater than 6500/-. The

balance amount is 900-541 = 359.00 which willgo to EPF account.

You may be thinking that, what about 3.67%?, Here you don’t need to care about it.

Method2

Some companies follows the below method in which employee share is calculated on 7500/- and

employer share is calculated on up limit Rs 6500/-

Contribution Towards Calculation Amount

EPF Employees share 7500 x 12% 900

EPS Employer share 6500 x 8.33% 541

EPF employer share 6500 x 3.67% 239

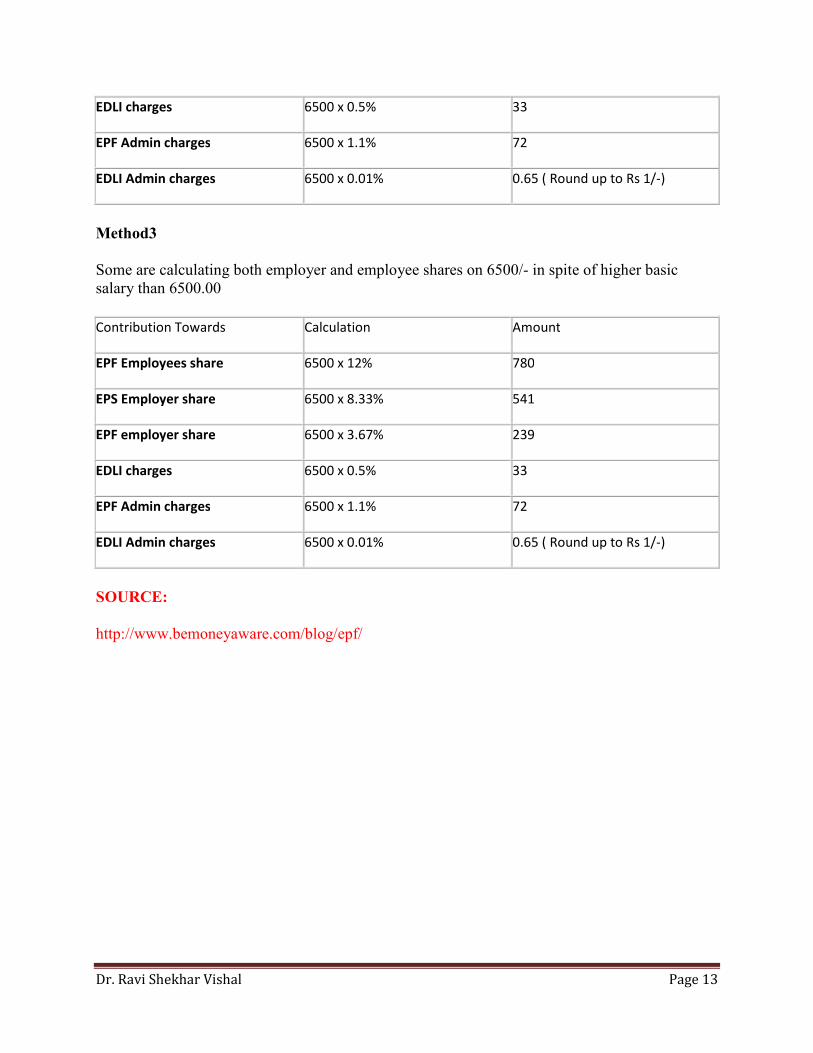

Dr. Ravi Shekhar Vishal Page 13

EDLI charges 6500 x 0.5% 33

EPF Admin charges 6500 x 1.1% 72

EDLI Admin charges 6500 x 0.01% 0.65 ( Round up to Rs 1/-)

Method3

Some are calculating both employer and employee shares on 6500/- in spite of higher basic

salary than 6500.00

Contribution Towards Calculation Amount

EPF Employees share 6500 x 12% 780

EPS Employer share 6500 x 8.33% 541

EPF employer share 6500 x 3.67% 239

EDLI charges 6500 x 0.5% 33

EPF Admin charges 6500 x 1.1% 72

EDLI Admin charges 6500 x 0.01% 0.65 ( Round up to Rs 1/-)

SOURCE:

http://www.bemoneyaware.com/blog/epf/

Related Documents