(Empirically) Understanding Financial Regulation Amit Seru

(Empirically) Understanding Financial Regulation Amit Seru.

Dec 22, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

(Empirically) Understanding Financial Regulation

Amit Seru

Financial Regulation?

• Start with the view that regulation sometimes useful– Fragility, under-representation hypothesis…

• In my view the area with least empirical work– Compared to say empirical papers on capital structure

• Yet, after financial crisis, an area where inputs of economists needed the most

• Dodd Frank (US)• Ring Fencing (Everywhere)• Bank super-regulator (ECB)• Bank capital• …

What are the “facts” on financial regulation?

• To be fair, lots of debate on regulation, but we have been working with limited facts

• Broadly, classify work into two categories:– “Rules”

• Forces that shape rules and induce persistence• Design and effectiveness

– “Implementation”• Regulator incentives• Tools in implementing regulation

• Today, the more ignored facet -- “implementation”

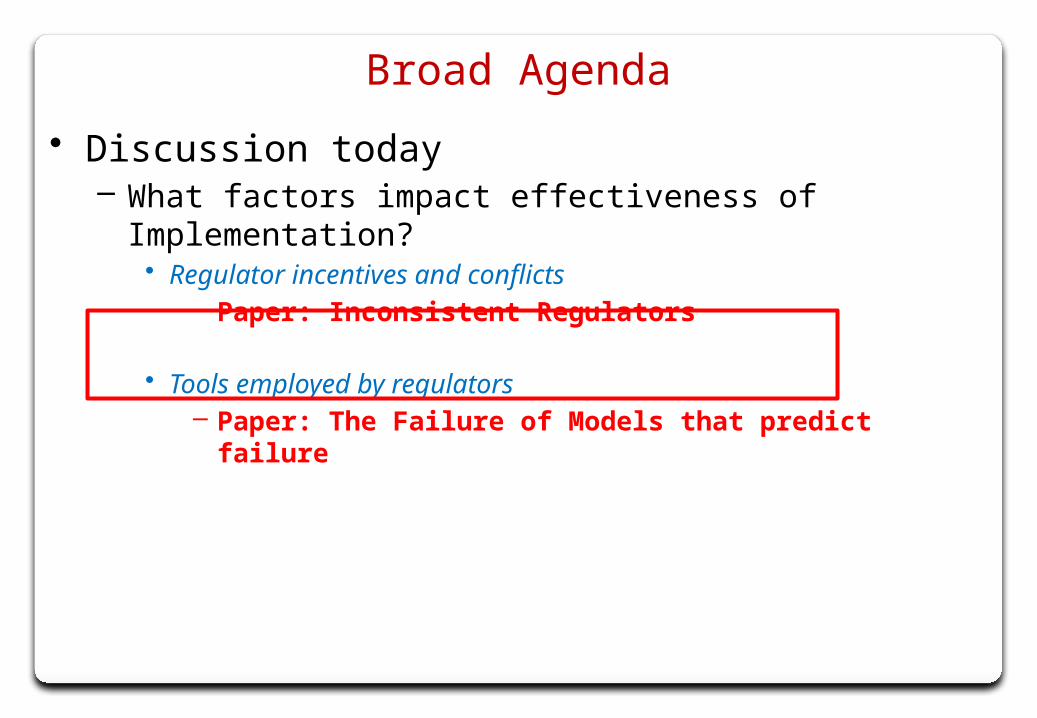

• Discussion today– What factors impact effectiveness of Implementation?

• Regulator incentives and conflicts– Paper: Inconsistent Regulators

• Tools employed by regulators– Paper: The Failure of Models that predict failure

Broad Agenda

Inconsistent Regulators: Evidence from Banking

The views expressed are those of the authors and are not necessarily those of the Federal Reserve Bank of New York or the Federal Reserve System

Amit Seru

Chicago and NBER

Francesco Trebbi

UBC, CIFAR, and NBER

Sumit Agarwal

NUS

David Lucca

New York Fed

• Fixing US banking regulatory structure at center of post-crisis debate− Dodd–Frank Wall Street Reform and Consumer Protection

Act passed to address potential failures− Most impetus on activities to regulate

• The “null”: once rules in place, all regulators the same

Motivation

• But effectiveness of regulation depends also on agents who implement it− Regulators have different incentives and institutional

design (“will of the regulator” is different)• Some paid through Fees, some paid through insurance premium…

Motivation

• But effectiveness of regulation depends also on agents who implement it− Regulators have different incentives and institutional

design (“will of the regulator” is different)− …and have overlapping jurisdictions…

Motivation

• But effectiveness of regulation depends also on agents who implement it− Regulators have different incentives and institutional

design (“will of the regulator” is different)− …and have overlapping jurisdictions…

• Differences in regulator incentives may have benefits such as completing the “information” set

• …but can lead to systematic differences in how same rule is implemented => effectiveness ▼− Plenty of anecdotes: OTS /FDIC & Washington Mutual

Motivation

0

200

400

600

800

1000

1200

1400

1600

Spre

ad (b

p)

WaMu 5 year CDS Spread

FDIC asks OTS to downgrade

CAMELS to 3.OTS downgrades

CAMELS to 3FDIC asks OTS to downgrade to 4. OTS disagrees

Reid: “You [Bair] are not a super-

regulator”

FDIC downgrades to 4. OTS follows

“Jamie deal”If not, would have wiped $45

billion Deposit Insurance Fund

Reid: “Cannot believe audacity of this woman [Bair]”

OTS gives a CAMELS rating of 2

Draws fees of $30 mill/year (15%)

• This is an anecdote…is this behavior systematic?

• Within the context of US banking, we ask:− Do different regulators implement same rules differently?− What are the consequences of inconsistent oversight?

Motivation

• Heterogeneity of regulator actions and responsibilities makes comparisons difficult

• Heterogeneity of financial firms that are regulated, who can “select” a regulator

Empirical Challenges?

• Heterogeneity of regulator actions and responsibilities makes comparisons difficult− Narrow down focus: “on-site” prudential supervision− A clear metric: “CAMELS” rating…from 1 [safe] to 5 [failing]− Comparable: By law, ratings all regulators equivalent

• Heterogeneity of financial firms that are regulated, who can “select” a regulator− Exploit legally-determined policy that assigns federal and

state regulators to a bank at “exogenous” time intervals• Rotations pre-determined => Track differences in regulators’

behavior when dealing with same bank

What we do?

What we do?

Timing

Federal Regulator cycle

Federal=1

State Regulator cycle

Federal=0

... …

• CAMELS rating given when exam cycle starts− Typically 2-3 weeks onsite; total of more than 50 men/

women workday − Report prepared/discussed within a quarter

CAMELS Upgrades/Downgrades

SMBs, FRB-STATE rotating

CAMELS upgrade CAMELS downgrade

Freq. Percent Freq. Percent

FRB 115 35.83 491 73.28

STATE 206 64.17 179 26.72

Total 321 100 670 100

Mean SD Mean SD

∆CAMELS -1 0 1.091 0.331

NMBs, FDIC-STATE rotating

CAMELS upgrade CAMELS downgrade

Freq. Percent Freq. Percent

FDIC 1262 47.14 3376 61.58

STATE 1415 52.86 2106 38.42

Total 2677 100 5482 100

Mean SD Mean SD

∆CAMELS -1 0 1.134 0.391

CAMELS Upgrades/Downgrades

Federal regulator twice

as likely to downgradethan State

SMBs, FRB-STATE rotating

CAMELS upgrade CAMELS downgrade

Freq. Percent Freq. Percent

FRB 115 35.83 491 73.28

STATE 206 64.17 179 26.72

Total 321 100 670 100

Mean SD Mean SD

∆CAMELS -1 0 1.091 0.331

NMBs, FDIC-STATE rotating

CAMELS upgrade CAMELS downgrade

Freq. Percent Freq. Percent

FDIC 1262 47.14 3376 61.58

STATE 1415 52.86 2106 38.42

Total 2677 100 5482 100

Mean SD Mean SD

∆CAMELS -1 0 1.134 0.391

CAMELS Upgrades/Downgrades

Counter-balanced by

upgradesby State

SMBs, FRB-STATE rotating

CAMELS upgrade CAMELS downgrade

Freq. Percent Freq. Percent

FRB 115 35.83 491 73.28

STATE 206 64.17 179 26.72

Total 321 100 670 100

Mean SD Mean SD

∆CAMELS -1 0 1.091 0.331

NMBs, FDIC-STATE rotating

CAMELS upgrade CAMELS downgrade

Freq. Percent Freq. Percent

FDIC 1262 47.14 3376 61.58

STATE 1415 52.86 2106 38.42

Total 2677 100 5482 100

Mean SD Mean SD

∆CAMELS -1 0 1.134 0.391

Putting it Together

0

.1

.2

.3

.4C

um

ula

tive

CA

ME

LS

1st

2nd

3rd

4th

5th

6th

7th

8th

Supervisor Rotations

Conditional on the 1st rotation with a Federal Agency Unconditional

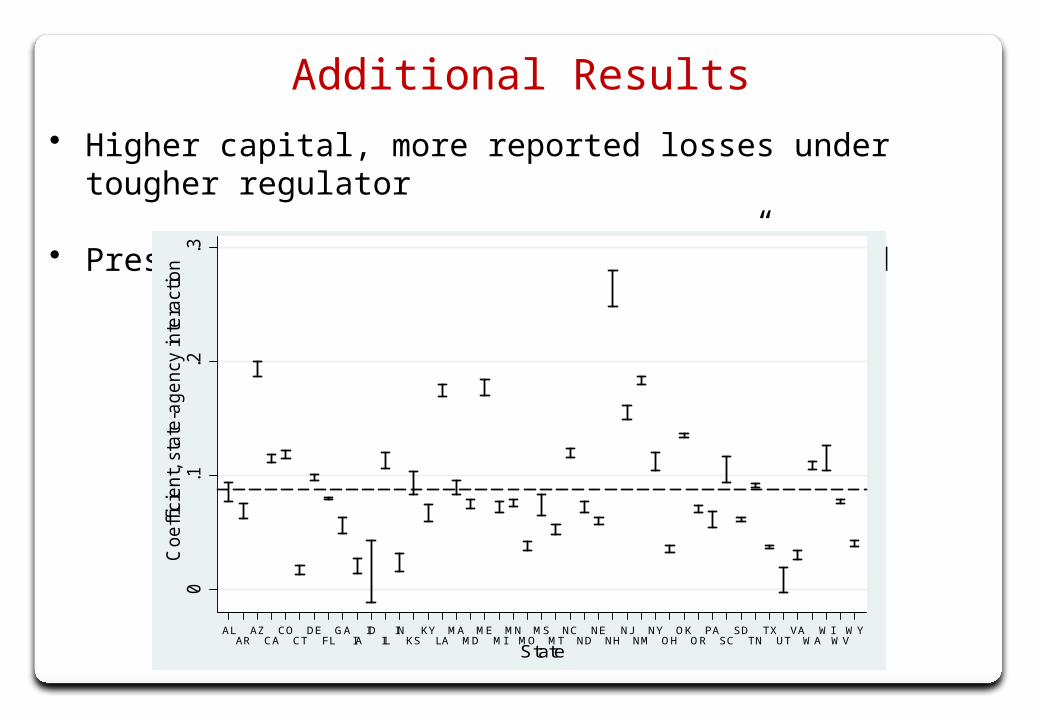

• Higher capital, more reported losses under tougher regulator

• Present across regions: “State-Fed” spread

Additional Results

• Higher capital, more reported losses under tougher regulator

• Present across regions: “State-Fed” spread

Additional Results

0.1

.2.3

Coe

ffic

ien

t, s

tate

-age

ncy

inte

ract

ion

ALAR

AZCA

COCT

DEFL

GAIA

IDIL

INKS

KYLA

MAMD

MEMI

MNMO

MSMT

NCND

NENH

NJNM

NYOH

OKOR

PASC

SDTN

TXUT

VAWA

WIWV

WY

State

SMBs and NMBs

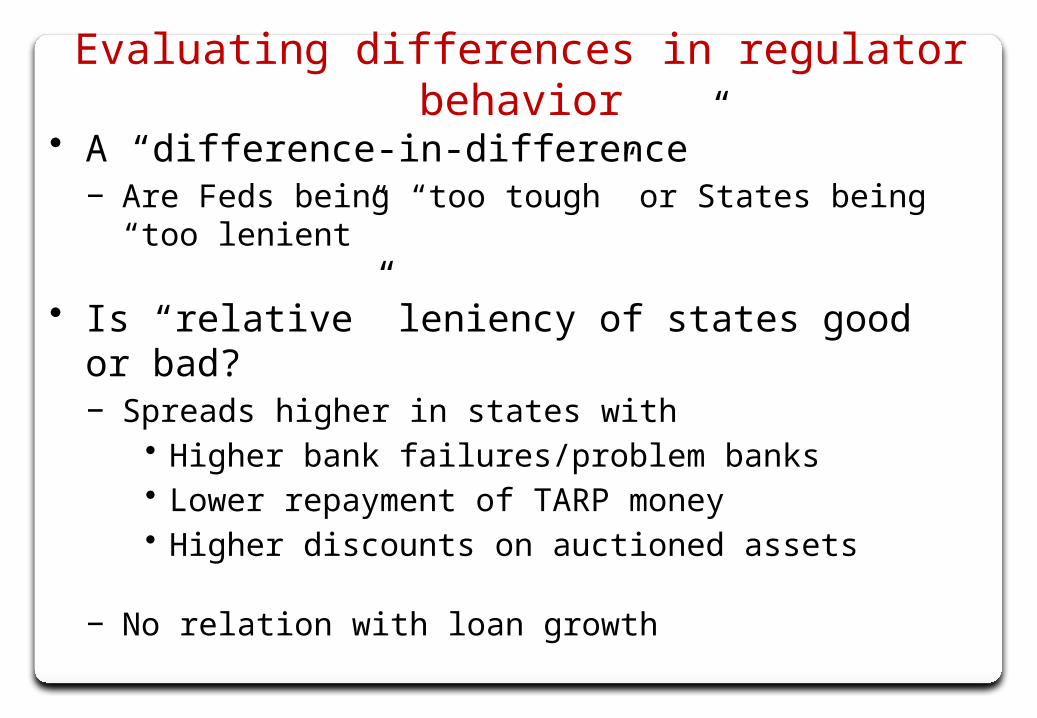

• A “difference-in-difference”− Are Feds being “too tough” or States being “too lenient”

• Is “relative” leniency of states good or bad?− Spreads higher in states with

• Higher bank failures/problem banks• Lower repayment of TARP money• Higher discounts on auctioned assets

− No relation with loan growth

Evaluating differences in regulator behavior

• Why these differences?− Local regulators protect local constituents

• Higher spread during “tougher” times

− Regulatory capture• Higher spread for banks who pay more fees• Limited support for “revolving door”

− Competence/Funding of resources: • Higher spread in states with lower “ability” of regulators• Higher spread in states with lower resources

Why differences between regulators?

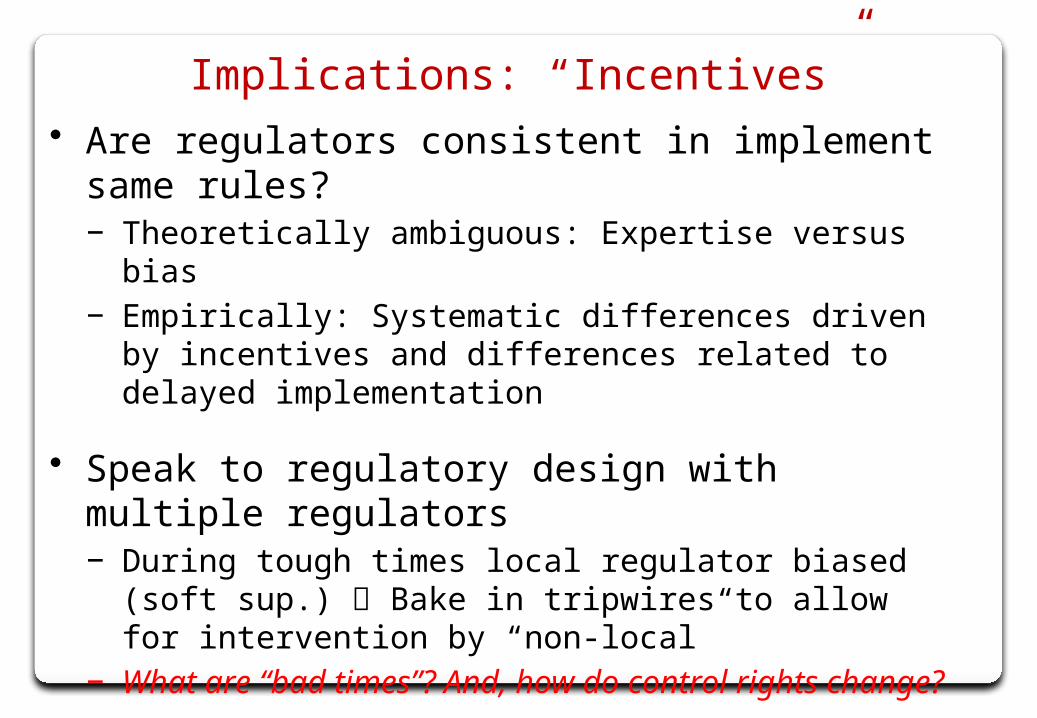

• Are regulators consistent in implement same rules? − Theoretically ambiguous: Expertise versus bias− Empirically: Systematic differences driven by incentives

and differences related to delayed implementation

• Speak to regulatory design with multiple regulators − During tough times local regulator biased (soft sup.)

Bake in tripwires to allow for intervention by “non-local”− What are “bad times”? And, how do control rights change?

Implications: “Incentives”

• Discussion today– What factors impact effectiveness of Implementation?

• Regulator incentives and conflicts– Paper: Inconsistent Regulators

• Tools employed by regulators– Paper: The Failure of Models that predict failure

Broad Agenda

The Failure of Models that Predict Failure

Uday Rajan

Michigan

Amit Seru

Chicago and NBER

Vikrant Vig

LBS

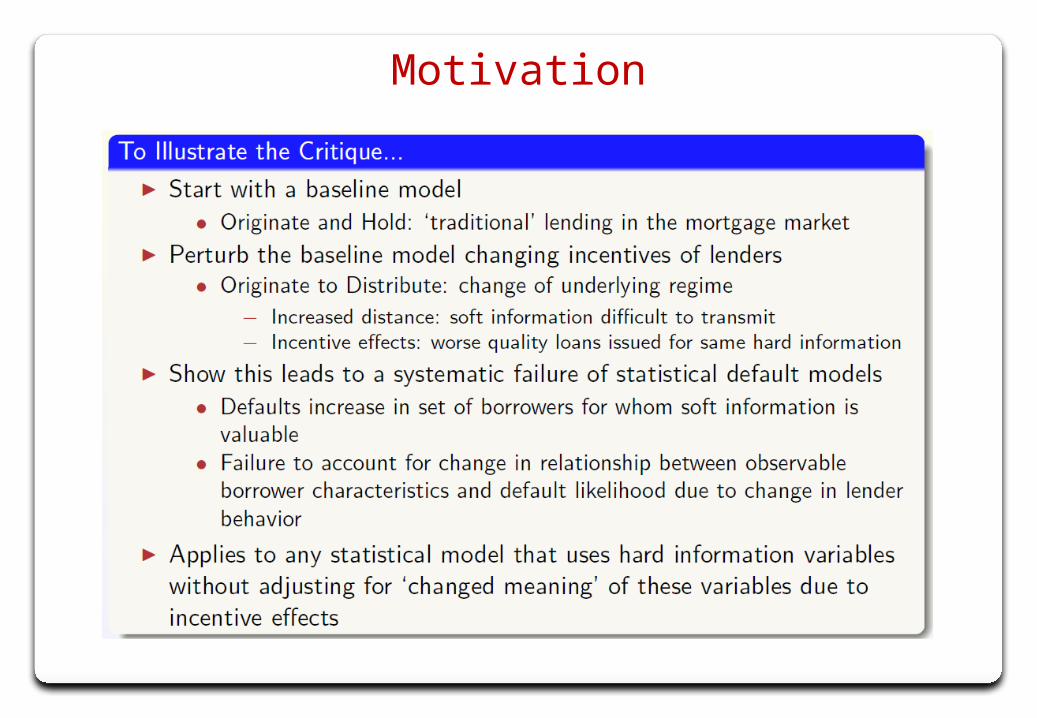

Motivation

Motivation

Motivation

Motivation

Motivation

Increased Reliance on Hard Information

Low Regime

High Regime

Increased Reliance on Hard Information

A “Model” used by S&P and Regulators

Baseline “Model”

Actual versus Predicted Defaults

Under-prediction by the “Model” is Systematic

Implications: “Models”

Conclusion

• Limited empirical work on banking regulation

– “Rules”• Forces that shape rules and induce persistence• Design and effectiveness

– “Implementation”• Regulator incentives• Tools in implementing regulation

• Talked about the more ignored implementation– Both papers really about understanding “incentives”

• More needs to be done to extend our understanding

BACK UP: REGULATORS

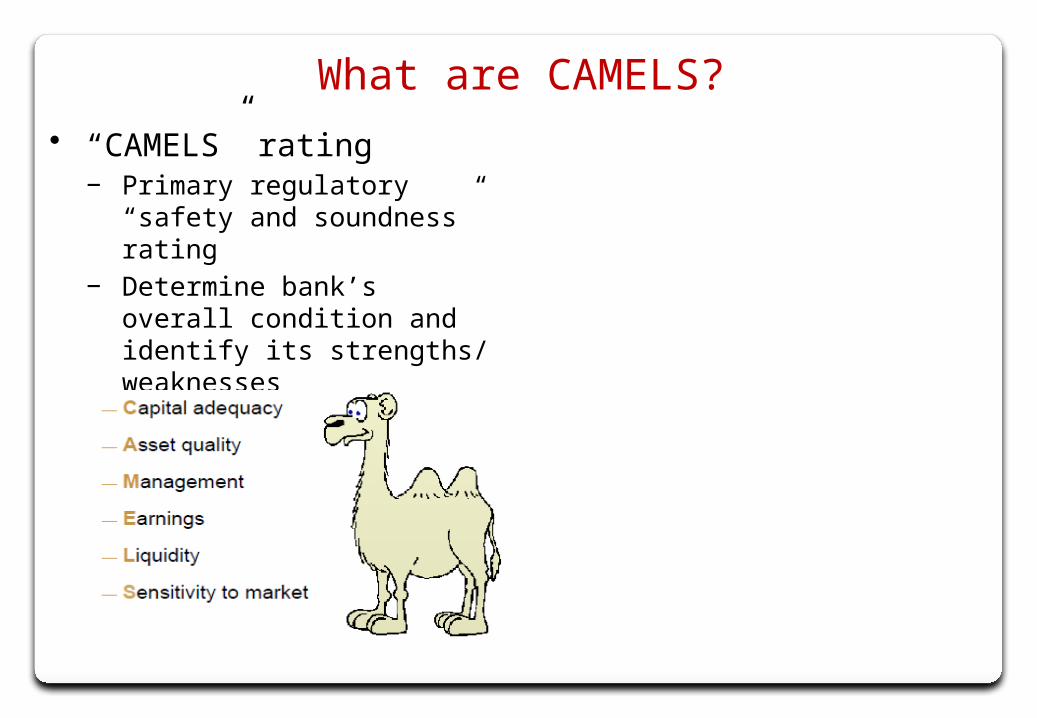

What are CAMELS?

• “CAMELS” rating− Primary regulatory “safety and

soundness” rating− Determine bank’s overall

condition and identify its strengths/ weaknesses

What are CAMELS?

• CAMELS key in regulation− Licensing, M&A, branching− Insurance premium− Restructuring decisions− Govt. funding (e.g., TARP)

• Each exam followed with regulator action to improve/maintain ratings− Less severe: MOUs− More severe : Formal actions

(cease & desist/ suspension)− Confidential to regulators and

bank

• “CAMELS” rating− Primary regulatory “safety and

soundness” rating− Determine bank’s overall

condition and identify its strengths/ weaknesses

• Legally-determined rotation policy circumvents bank self-selection− Riegle Act of 1994: federal agencies required to use state

reports as substitute in alternate 12-month cycles (18-month for small banks) to reduce regulatory duplication• Rotation between State Regulator and FRB for SMBs• Rotation between State Regulator and FDIC for NMBs

− ~80% US commercial Banks covered (38% by assets)

What we do

Riegle Act of 1994

• The aim of these rules:− “[to] Foster coordination in order to reduce the dual

regulatory burden on state chartered banks, by substituting a federal examination with a state examination”.

− Before 1994 both Fed and State visited every period.

• Was not a deliberate “optimal mix” of more-less lenient regulators: “Good cop/Bad cop”− No such channel discussed in the legislative debate− Federal regulators don’t know of extra information

conceded by the bank to State regulators that is shared with them

• Prudential supervisory assessments and lead agency information from National Examination Database of the Federal Reserve System

• All commercial bank-specific variables including total assets, Tier1 capital, leverage, delinquency, nonperforming loans ratios, return on assets from Call Reports

• State supervisory budget and resource allocation data from Profile of State Bank Supervisor by the Conference of State Bank Supervisors

• Sample Period: 1996:Q1 to 2011:Q1; about 6500 banks and 55000 exams

Data

• Regulatory design (Stigler, 1971 and Peltzman, 1976)− Regulatory wedges and capture: Stigler (1971) and Peltzman (1976) to

Djankov, LaPorta, Lopez-de-Silanes, Shleifer (2002)− Theory of regulatory design in presence of informational asymmetries:

Laffont and Tirole (1993); Dewatripont and Tirole (1994); Boot and Thakor (1993); Hellman, Murdock and Stiglitz (2000)

• Banking regulation: Jayaratne and Strahan (1996); Berger and Hannan (1998); Kroszner and Strahan, (1999)

• Regulatory arbitrage in banking: Rosen (2003); Rosen (2005); Kane (2000); Calomiris (2006); Rezende (2011).

• Implementation of rules by auditors, standards in accounting literature: Gunther-Moore (2002)

Related Literature

• Regulatory outcome variable of interest Yit (e.g. the composite CAMELS rating).

• Linearly determined by a vector of characteristics of the bank i at quarter t, Bit, and by the identity of the supervisor Sit at quarter t.

• According to the following equation:

Yit = α +βBit +σSit +θi +λt +ϵit ,

including bank-specific fixed effects θ and quarter fixed effects λ.

Empirical Strategy

• Rewriting in terms of within-bank and within-quarter deviations:

y = βb + σs + ϵ (1)

• Let b=[b1, b2]’ where b2 is omitted/unobservable. Then can modify (1) to:

y = β1b1+ β2b2 + σs + ϵ (2)

• If regulatory setting is endogenous:

s = δb + η (3)

Empirical Strategy

cov(s, β2b2 + ϵ) ≠ 0

• The predetermined policy rule (Riegle Act) allows to replace:

s = δb + η (3)

with the predetermined policy p:

s = p + n,

where the following orthogonality condition holds:

p b2 | i SMB or i NMB.⊥ ∈ ∈

− Conditional on the bank being an SMB or NMB subject to rotation p, we can consistently estimate effect of supervisor on y

Empirical Strategy

Rotation Spells

Supervisor Identity on CAMELS

(1) (2) (3) (4) (5) (6) (7)Combined CAMELS

Capital rating Asset rating

Management rating

Earnings rating

Liquidity rating

Sensitivity rating

Within-bank mean 1.680 1.490 1.510 1.768 1.900 1.578 1.721

Within-bank SD 0.295 0.290 0.396 0.331 0.435 0.300 0.288

Lead agency = FRB 0.096*** 0.038*** 0.077*** 0.135*** 0.099*** 0.061*** 0.096***

[0.011] [0.012] [0.020] [0.012] [0.014] [0.009] [0.018]

Cluster State State State State State State State

Fixed effects Quarter Quarter Quarter Quarter Quarter Quarter Quarter

Bank ID Bank ID Bank ID Bank ID Bank ID Bank ID Bank ID

Observations 38110 38107 38110 38108 38108 38108 32479

Adjusted R-squared 0.551 0.528 0.449 0.493 0.580 0.529 0.473

# of banks 1042 1042 1042 1042 1042 1042 976

# of clusters 41 41 41 41 41 41 41

Supervisor Identity on CAMELS

(1) (2) (3) (4) (5) (6) (7)Combined CAMELS

Capital rating Asset rating

Management rating

Earnings rating

Liquidity rating

Sensitivity rating

Within-bank mean 1.680 1.490 1.510 1.768 1.900 1.578 1.721

Within-bank SD 0.295 0.290 0.396 0.331 0.435 0.300 0.288

Lead agency = FRB 0.096*** 0.038*** 0.077*** 0.135*** 0.099*** 0.061*** 0.096***

[0.011] [0.012] [0.020] [0.012] [0.014] [0.009] [0.018]

Cluster State State State State State State State

Fixed effects Quarter Quarter Quarter Quarter Quarter Quarter Quarter

Bank ID Bank ID Bank ID Bank ID Bank ID Bank ID Bank ID

Observations 38110 38107 38110 38108 38108 38108 32479

Adjusted R-squared 0.551 0.528 0.449 0.493 0.580 0.529 0.473

# of banks 1042 1042 1042 1042 1042 1042 976

# of clusters 41 41 41 41 41 41 41

Supervisor identity on CAMELS

(1) (2) (3) (4) (5) (6) (7)Combined CAMELS

Capital rating

Asset rating

Management rating

Earnings rating

Liquidity rating

Sensitivity rating

Within-bank mean 1.686 1.508 1.587 1.784 1.862 1.547 1.640

Within-bank SD 0.389 0.363 0.500 0.426 0.490 0.347 0.319

Lead agency = FDIC 0.072*** 0.059*** 0.072*** 0.088*** 0.063*** 0.037*** 0.051***

[0.007] [0.010] [0.012] [0.009] [0.011] [0.008] [0.007]

Cluster State State State State State State State

Fixed effects Quarter Quarter Quarter Quarter Quarter Quarter Quarter

Bank ID Bank ID Bank ID Bank ID Bank ID Bank ID Bank ID

Observations 240576 240572 240572 240572 240572 240572 211836

Adjusted R-squared 0.496 0.489 0.427 0.466 0.485 0.505 0.474

# of banks 5329 5329 5329 5329 5329 5329 5310

# of clusters 48 48 48 48 48 48 48

Evaluating differences in regulator behavior

(1) (2) (3) (4) (5)

Federal Agency 0.092*** 0.093*** 0.091*** 0.092*** 0.090***[0.010] [0.010] [0.010] [0.010] [0.009]

Federal agency * Failure Rate 0.036*** 0.005[0.009] [0.010]

Federal agency * Problem Bank Rate 0.060*** 0.053***[0.008] [0.009]

Federal agency * TARP Repayment -0.020* -0.017**[0.011] [0.008]

Federal agency * Asset Sale Discount 0.013** 0.016**[0.006] [0.007]

Cluster State State State State StateFixed Effects Quarter Quarter Quarter Quarter Quarter

Bank ID Bank ID Bank ID Bank ID Bank ID

Observations 46344 46429 41972 45254 41103Adjusted R-squared 0.477 0.486 0.48 0.472 0.493# of clusters 49 51 41 46 39

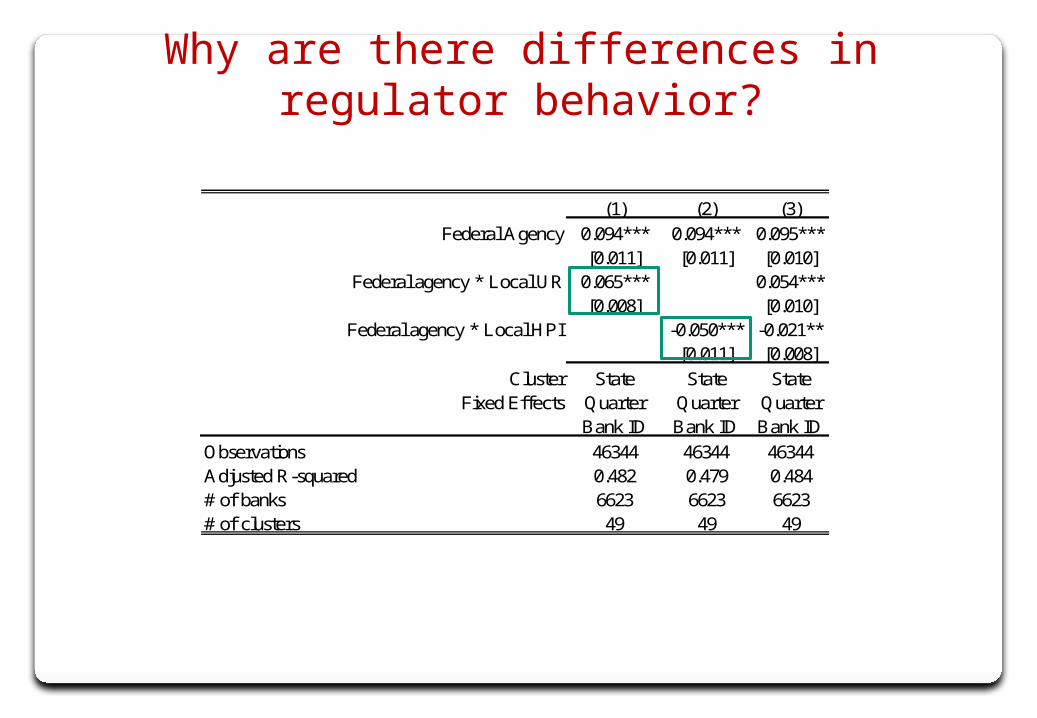

Why are there differences in regulator behavior?

(1) (2) (3)

Federal Agency 0.094*** 0.094*** 0.095***[0.011] [0.011] [0.010]

Federal agency * Local UR 0.065*** 0.054***[0.008] [0.010]

Federal agency * Local HPI -0.050*** -0.021**[0.011] [0.008]

Cluster State State StateFixed Effects Quarter Quarter Quarter

Bank ID Bank ID Bank ID

Observations 46344 46344 46344Adjusted R-squared 0.482 0.479 0.484# of banks 6623 6623 6623# of clusters 49 49 49

Two additional analysis

• Assess changes in supervisory standards for the same bank around the passage of the Act− Allows for comparison of a regime change from “tougher

regulator present all the time” to “tougher regulator present only half the time”

• Include all depository institutions and regulators (OCC, OTS, Fed, FDIC, State).− Allows comparison of results when we allow for movement

into and out of the state system

BACK UP: DEFAULT MODELS

Placebo Test

Cross-Sectional Evidence

“Perfect Foresight” Model does not correct fully

Related Documents