www.angelbroking.com Market Outlook August 13, 2012 Dealer’s Diary Indian markets are expected to open negative, tracing negative opening trades in the SGX Nifty and the major Asian indices. The US markets moved modestly lower in early trading on Friday due to disappointing Chinese trade data for July which showed China’s trade surplus narrowed during the month as growth rates for both exports and imports fell below estimates, thus leading to renewed concerns about the outlook for the global economy. A report released by China's General Administration of Customs showed that Chinese exports grew by just 1% yoy in July 2012, decelerating from the 11.3% growth reported for June 2012, while imports rose at a slower rate in July 2012, up 4.7% compared to the 6.3% increase in June 2012. Also, the US Labor Department recently released a report showed an unexpected decrease of 0.6% in import prices in the month of July 2012 after tumbling by 2.4% in June 2012. The major European markets have also moved to the downside on Friday on the back of weak Chinese trade data. Meanwhile, Indian shares ended a choppy session on Friday with the rupee trading weak, tracking the ailing euro, and global cues remaining lackluster in the wake of dismal Chinese trade data. Markets Today The trend deciding level for the day is 17,540 / 5,315 levels. If NIFTY trades above this level during the first half-an-hour of trade then we may witness a further rally up to 17,608 – 17,659 / 5,336 – 5,351 levels. However, if NIFTY trades below 17,540 / 5,315 levels for the first half-an-hour of trade then it may correct up to 17,489 – 17,421 / 5,300 – 5,279 levels. Indices S2 S1 PIVOT R1 R2 SENSEX 17,421 17,489 17,540 17,608 17,659 NIFTY 5,279 5,300 5,315 5,336 5,351 News Analysis Bosch to temporarily suspend manufacturing operations at its plants Supreme Court denies PNGRB to enquire into IGL’s books of accounts Work on Dholera special investment region to start within a year Electrosteel Castings’ associate, Electrosteel Steels reports 1QFY2013 results 1QFY2013 Result Reviews- ONGC, SBI, Sun Pharma, Glaxo Pharma, RCom, Bharat Forge, Ashoka Buildcon, Godawari Power, CCCL, Madhucon Projects, Hitachi Home. 1QFY2013 Result Previews- Coal India, Tata Steel, Bosch, NMDC, India Cem. Refer detailed news analysis on the following page Net Inflows (August 9, 2012) ` cr Purch Sales Net MTD YTD FII 2,231 1,914 317 3,867 57,147 MFs 551 801 (250) (513) (8,592) FII Derivatives (August 10, 2012) ` cr Purch Sales Net Open Interest Index Futures 1,059 1,080 (21) 15,745 Stock Futures 1,381 2,006 (625) 24,645 Gainers / Losers Gainers Losers Company Price (`) chg (%) Company Price (`) chg (%) Amtek Auto 96 11.5 JPINFRATEC 50 (7.2) Jain Irrigation 84 5.0 SBI 1,888 (4.3) Tech Mahindra 800 5.0 Power Finance 183 (4.2) Indraprastha Gas 252 4.9 Ranbaxy Lab 483 (3.7) Shree Cement 3,199 3.6 GMR Infra 22 (3.4) Domestic Indices Chg (%) (Pts) (Close) BSE Sensex (0.0) (3.1) 17,558 Nifty (0.1) (2.6) 5,320 MID CAP 0.0 1.5 6,100 SMALL CAP (0.3) (18.9) 6,550 BSE HC (0.2) (15.9) 7,292 BSE PSU (0.8) (60.0) 7,084 BANKEX (0.9) (102.1) 11,889 AUTO (1.2) (115.9) 9,367 METAL 0.1 9.2 10,521 OIL & GAS 0.3 22.2 8,310 BSE IT 1.3 73.0 5,542 Global Indices Chg (%) (Pts) (Close) Dow Jones 0.3 42.8 13,208 NASDAQ 0.1 2.2 3,021 FTSE (0.1) (4.4) 5,847 Nikkei (1.0) (87.2) 8,891 Hang Seng (0.7) (133.4) 20,136 Straits Times 0.1 2.0 3,054 Shanghai Com (0.2) (5.3) 2,169 Indian ADRs Chg (%) (Pts) (Close) INFY 0.5 0.2 $41.8 WIT 1.0 0.1 $8.2 IBN (0.1) (0.1) $34.9 HDB 0.7 0.3 $35.6 Advances / Declines BSE NSE Advances 1,182 580 Declines 1,577 898 Unchanged 129 88 Volumes (` cr) BSE 2,192 NSE 10,499

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Market Outlook August 13, 2012

www.angelbroking.com

Market Outlook August 13, 2012

Dealer’s Diary Indian markets are expected to open negative, tracing negative opening trades in the SGX Nifty and the major Asian indices. The US markets moved modestly lower in early trading on Friday due to disappointing Chinese trade data for July which showed China’s trade surplus narrowed during the month as growth rates for both exports and imports fell below estimates, thus leading to renewed concerns about the outlook for the global economy. A report released by China's General Administration of Customs showed that Chinese exports grew by just 1% yoy in July 2012, decelerating from the 11.3% growth reported for June 2012, while imports rose at a slower rate in July 2012, up 4.7% compared to the 6.3% increase in June 2012. Also, the US Labor Department recently released a report showed an unexpected decrease of 0.6% in import prices in the month of July 2012 after tumbling by 2.4% in June 2012. The major European markets have also moved to the downside on Friday on the back of weak Chinese trade data.

Meanwhile, Indian shares ended a choppy session on Friday with the rupee trading weak, tracking the ailing euro, and global cues remaining lackluster in the wake of dismal Chinese trade data.

Markets Today The trend deciding level for the day is 17,540 / 5,315 levels. If NIFTY trades above this level during the first half-an-hour of trade then we may witness a further rally up to 17,608 – 17,659 / 5,336 – 5,351 levels. However, if NIFTY trades below 17,540 / 5,315 levels for the first half-an-hour of trade then it may correct up to 17,489 – 17,421 / 5,300 – 5,279 levels.

Indices S2 S1 PIVOT R1 R2

SENSEX 17,421 17,489 17,540 17,608 17,659

NIFTY 5,279 5,300 5,315 5,336 5,351

News Analysis Bosch to temporarily suspend manufacturing operations at its plants Supreme Court denies PNGRB to enquire into IGL’s books of accounts Work on Dholera special investment region to start within a year Electrosteel Castings’ associate, Electrosteel Steels reports 1QFY2013 results 1QFY2013 Result Reviews- ONGC, SBI, Sun Pharma, Glaxo Pharma, RCom,

Bharat Forge, Ashoka Buildcon, Godawari Power, CCCL, Madhucon Projects, Hitachi Home.

1QFY2013 Result Previews- Coal India, Tata Steel, Bosch, NMDC, India Cem. Refer detailed news analysis on the following page

Net Inflows (August 9, 2012) ` cr Purch Sales Net MTD YTD

FII 2,231 1,914 317 3,867 57,147

MFs 551 801 (250) (513) (8,592)

FII Derivatives (August 10, 2012) ` cr Purch Sales Net Open Interest

Index Futures 1,059 1,080 (21) 15,745

Stock Futures 1,381 2,006 (625) 24,645

Gainers / Losers Gainers Losers

Company Price (`) chg (%) Company Price (`) chg (%)

Amtek Auto 96 11.5 JPINFRATEC 50 (7.2)

Jain Irrigation 84 5.0 SBI 1,888 (4.3)

Tech Mahindra 800 5.0 Power Finance 183 (4.2)

Indraprastha Gas 252 4.9 Ranbaxy Lab 483 (3.7)

Shree Cement 3,199 3.6 GMR Infra 22 (3.4)

Domestic Indices Chg (%) (Pts) (Close)

BSE Sensex (0.0) (3.1) 17,558

Nifty (0.1) (2.6) 5,320

MID CAP 0.0 1.5 6,100

SMALL CAP (0.3) (18.9) 6,550

BSE HC (0.2) (15.9) 7,292

BSE PSU (0.8) (60.0) 7,084

BANKEX (0.9) (102.1) 11,889

AUTO (1.2) (115.9) 9,367

METAL 0.1 9.2 10,521

OIL & GAS 0.3 22.2 8,310

BSE IT 1.3 73.0 5,542

Global Indices Chg (%) (Pts) (Close)

Dow Jones 0.3 42.8 13,208

NASDAQ 0.1 2.2 3,021

FTSE (0.1) (4.4) 5,847

Nikkei (1.0) (87.2) 8,891

Hang Seng (0.7) (133.4) 20,136

Straits Times 0.1 2.0 3,054

Shanghai Com (0.2) (5.3) 2,169

Indian ADRs Chg (%) (Pts) (Close)

INFY 0.5 0.2 $41.8

WIT 1.0 0.1 $8.2

IBN (0.1) (0.1) $34.9

HDB 0.7 0.3 $35.6

Advances / Declines BSE NSE

Advances 1,182 580

Declines 1,577 898

Unchanged 129 88

Volumes (` cr)

BSE 2,192

NSE 10,499

www.angelbroking.com

Market Outlook August 13, 2012

Bosch to temporarily suspend manufacturing operations at its plants Bosch (BOS) has announced to temporarily suspend manufacturing at its plants (partial/full) during August 2012 in order to avoid unnecessary buildup of inventory and align the production as per the market demand. The domestic automobile industry which is the primary driver of company’s revenue, have witnessed a slowdown in demand recently due to sluggish economic growth, increasing fuel prices and weak consumer sentiments.

Plant location Partial/full Dates of shutdown

Bangalore Partial 11, 13, 14, 25, 27

Nashik Partial 17 to 31

Jaipur Full 16, 17, 18, 27, 28, 29

The company has been suspending operations at its plants in a phased manner to align production in-line with the market demand since June 2012. It had earlier announced temporary shutdown at its Jaipur plant (from June 28 to June 30, 2012 and July 25 to August 4, 2012), Bangalore plant (from June 29 to June 30, 2012, from July 13 to July 14, 2012 and July 27 to July 30, 2012) and Nashik plant (July 30 to July 31, 2012). At the CMP of `8,865, the stock is trading at 19.3x CY2013E earnings, which is in-line with its historical average of 20x. Thus, we recommend Neutral rating on the stock. Supreme Court denies PNGRB to enquire into IGL’s books of accounts The Supreme Court (SC) has declined to permit the Petroleum and Natural Gas Regulatory Board (PNGRB) to proceed with its inquiry against Indraprastha Gas Ltd (IGL) and some other companies over determining network tariff and compression charges. However, the SC has sought IGL’s reply on the same before passing the final order. During June 2012, the Delhi High Court had ruled that the PNGRB did not have the power to fix any component of network tariff or compression charges for any entity having its own distribution network. We maintain our Neutral view on the stock. Work on Dholera special investment region to start within a year According to news reports, work on Dholera Special Investment Region will start within a year. The central government has approved `3,000cr to create basic infrastructure for the project. The planned project will be coming up 90Kms from Ahmedabad within the Delhi Mumbai Industrial Corridor (DMIC). The investment sectors identified for the project include Heavy engineering, Automobiles and ancillaries, electronics, Pharmaceuticals & biotechnology, agro and food processing and IT/ITES. Mahindra lifespaces had signed a MOU with the government of Gujarat. The MOU is for the development of 3,000acres of integrated business city along the lines of the existing Mahindra World City (MWC). We maintain BUY rating on MLIFE with a Target price of `396.

www.angelbroking.com

Market Outlook August 13, 2012

Electrosteel Castings’ associate, Electrosteel Steels reports 1QFY2013 results Electrosteel Steels (ESL), an associate of Electrosteel Castings (ECL) reported an operating loss during 1QFY2013 as most of its integrated steel plants are yet to commission operations. ESL’s top-line stood at `12cr compared to `2cr in 1QFY2012 as it commenced partial operations at its plant (pig iron and DI pipes) during the quarter. However, it reported an operating loss of `10cr during the quarter. Depreciation and interest expenses stood at `14cr and `23cr respectively. Hence, it reported a loss at the PAT level of `46cr. We await results of ECL (expected to report results on August 14, 2012). Until then, we maintain our Buy rating on ECL with a target price of `22. Result Reviews

ONGC (CMP: `279/ TP: `321/ Upside: 15%) ONGC reported better-than-expected 1QFY2013 standalone results due to lower-than-expected subsidy burden. The company’s top line increased by 23.9% yoy to `20,084cr (slightly above our expectation of `19,478cr. The company shared a subsidy burden was `12,346cr in 1QFY2013 vs. `12,046cr of subsidy shared in 1QFY2012 and `14,170cr in 4QFY2012. ONGC’s crude oil net realization declined by 4.4% yoy to US$46.6/bbl. Oil production increased by 3.2% yoy to 6.54mn tonnes during 1QFY2013. EBITDA margin expanded by 230bp yoy to 57.7% and EBITDA increased by 24.0% yoy to `11,130cr. Reported net profit increased by 48.4% yoy to `6,077cr above our estimate of `5,382cr. The company has notified 10 discoveries during FY2013 including one major discovery (D1) off the west coast. D1’s Initial Oil in-place (IOIP) is expected to be 140mtoe. Currently D1 block is producing 12,500bopd. The company expects the production to reach 60,000bopd by January 2014. We maintain our Buy rating on the stock with a target price of `321. Y/E Sales OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

March (` cr) (%) (` cr) (`) (%) (x) (x) (x) (x)

FY2013E 156,331 37.7 26,796 31.3 18.7 8.9 1.6 3.5 1.2

FY2014E 159,043 36.3 27,892 32.6 17.3 8.6 1.4 3.3 1.1

State Bank of India (CMP: `1,888/ TP: `2,270/ Upside: 20%) During 1QFY2013, SBI reported standalone net profit of `3,752cr as against `1,584cr in 1QFY2012, which was in line with our estimates. The operating income growth was however lower than our expectations which was negated by lower than estimated provisioning expenses (investment write-back of `521cr). We recommend a Buy rating on the stock.

Slippages surge up significantly: During 1QFY2013, the bank’s advances grew by 18.9% yoy, while deposits were up by 16.1% yoy. Domestic saving deposits growth was moderate at 13.4% yoy which coupled with 2.9% yoy decline in volatile

www.angelbroking.com

Market Outlook August 13, 2012

domestic current account deposits lead to domestic CASA deposits growing at a modest pace of 10.1% yoy. The domestic NIMs for the bank were lower by 42bp qoq on account of interest rate reversals, lower lending rates (SME and agri rates lowered by 50-350bp eff. June 01, 2012), lower demand (seasonality effect) for short term working capital loans (substituted into lower yielding CPs) and higher cost of deposits during the quarter (up 29bp qoq to 6.2%). The performance on the fee income front was muted with other income excluding treasury declining by 2.6% yoy. The growth in CEB income was flat yoy, while dividend income was lower at `18cr compared to `228cr in 1QFY2012 (interim dividend from subsidiaries not taken this year). Forex income however remained strong, growing by 38.0% yoy during 1QFY2013. On the asset-quality front, the bank’s annualized slippage ratio for the quarter surged sharply to 5.0%, significantly higher than 2.3% witnessed in 4QFY2012. Almost 62.1% slippages were witnessed in the Corporate and SME segments. Amongst the corporate and SME segments slippages, major industries witnessing sequentially higher slippages were trading (`848cr vs. `56cr in 1QFY2012 and `396cr for entire FY2012) and infrastructure (`787cr in 1QFY2013 and `554cr in 4QFY2012) and engineering (`636cr vs. 112cr in 4QFY2012).

Outlook and valuation: At the CMP, the stock is trading at 1.2x FY2014E ABV (adjusting for value of subsidiaries 1.0x FY2014E ABV) vis-à-vis its historic range of 1.3–2.3x and median of 1.6x. Also, considering the bank’s dominant position and reach, high fee income and superior earnings quality, we recommend a Buy on the stock with a target price of `2,270. Y/E Op. Inc NIM PAT EPS ABV ROA ROE P/E P/ABV

March (` cr) (%) (` cr) (`) (%) (x) (x) (x) (x)

FY2013E 64,470 3.5 15,056 224.4 1,332.0 1.0 17.6 8.4 1.4

FY2014E 75,940 3.5 17,361 258.7 1,574.6 1.0 17.8 7.3 1.2

Sun Pharma (CMP: `676/ TP: -/ Upside: - %) For 1QFY2013, Sun Pharma reported net sales of `2,658cr, up 62.5% yoy, mainly driven by exports. The company’s OPM expanded to 45.8% in 1QFY2013 from 33.5% in 1QFY2012. Also, the gross margin came in line at 81.1% from 75.1% in 1QFY2012. Net profit during the quarter reported 58.8% yoy growth to `796cr, higher than expectations, mainly on back of the higher sales growth and expansion in OPM. However, on account of rich valuation recommend a Neutral on the stock. Y/E Sales OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

March (` cr) (%) (` cr) (`) (%) (x) (x) (x) (x)

FY2013E 9,272 38.6 2,347 22.7 17.9 29.8 4.8 15.6 6.0

FY2014E 11,080 38.0 2,333 22.6 15.6 29.9 4.2 12.6 4.8

www.angelbroking.com

Market Outlook August 13, 2012

Glaxo Pharma (CMP: `2,105/ TP: - / Upside: - % ) For 2QCY2012, Glaxo Pharma reported net sales of `636cr, up 13.3% yoy, mainly driven by domestic formulations. The company’s OPM is expected to 31.0% in 2QCY2012 from 33.2% in 1QCY2012. Net profit during the quarter reported 7.3% yoy growth to `163cr. However, on account of rich valuation recommend a Neutral on the stock.

Y/E Sales OPM PAT EPS RoE P/E P/BV EV/EBITDA EV/Sales

March (` cr) (%) (` cr) (`) (%) (x) (x) (x) (x)

CY2012E 2,651 31.7 644 76.0 30.8 27.7 5.9 18.7 5.9

CY2013E 2,993 31.2 698 82.4 29.0 25.5 5.1 16.4 5.1

Reliance Communication (CMP: `55 / TP: - / Upside: -)

Reliance Communication reported decent set of results for 1QFY2013. The company’s top-line remained flat qoq at `5,319. Average revenue per user declined by 2.0% qoq to `0.43/min, inline with expectations. EBITDA margin grew by 30bp qoq to 31.0%. PAT came in at `162cr, aided by tax write backs. We maintain our Neutral view on the stock.

Y/E Sales OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

March (` cr) (%) (` cr) (`) (%) (x) (x) (x) (x)

FY2013E 22,125 31.9 925 4.5 2.5 12.2 0.3 6.1 2.0

FY2014E 23,734 32.0 1,207 5.8 3.1 9.3 0.3 5.1 1.6

Bharat Forge (CMP: `312/ TP: `358 / Upside: 15%) Bharat Forge (BHFC) reported lower-than-expected results for 1QFY2013 led by weak demand in the domestic automotive market and sharp increase in interest cost. Standalone revenue posted a 9.2% yoy (down 4.2% qoq) growth to `936cr led by 14.1% yoy (7% qoq) increase in net average realization on the back of rupee depreciation and superior product-mix. Total volume in tonnage terms declined 3.2% yoy (10.4% qoq) to 51, 288MT due to a 12% yoy decline in domestic medium and heavy commercial vehicle volumes (MHCV). Led by weakness in the domestic MHCV sales, domestic revenues declined 5.6% yoy (15.2% qoq). However, export revenues recorded a robust growth of 30.7% yoy (8.9% qoq) on the back of strong demand in commercial vehicle (CV) market in US, continued traction in non-auto segment in US and Europe and due to rupee depreciation. Non-auto segment revenues grew by 16.4% yoy drive by strong momentum across sectors. On the operating front, margins improved 84bp yoy (down 57bp qoq) to 25.1% which was in-line with our estimates owing to better product-mix and decline in raw-material expenses. Hence operating profit grew 13% yoy (down 6.3% qoq) to `235cr. Net profit however registered 8% yoy growth to `105cr, 12.4% below our

www.angelbroking.com

Market Outlook August 13, 2012

estimates, on account of 75.6% yoy (59% qoq) jump in interest expense. Other income on the other hand grew 72.7% yoy (93% qoq) which partially negated the impact of higher finance cost. At `312, the stock is trading at 10.6x FY2014E earnings. We maintain Buy on the stock with a revised target price of `358. Y/E Sales OPM PAT EPS RoE P/E P/BV EV/EBITDA EV/Sales

March (` cr) (%) (` cr) (`) (%) (x) (x) (x) (x)

FY2013E 7,004 16.2 483 20.8 20.3 13.1 2.5 6.3 1.0

FY2014E 7,985 16.4 595 25.6 21.2 10.6 2.1 5.1 0.8

Ashoka Buildcon (CMP: `255 / TP: `273 / Upside: 7%) For 1QFY2013, Ashoka Buildcon Ltd (ABL) reported a good set of numbers, broadly in line with our estimates. ABL’s top line witnessed a healthy growth of 19.8% to `466cr marginally higher than our estimate of `453cr. On the EBITDAM front, ABL’s margins came at 22.0%, a dip of 210bp yoy and in line with our estimate of 22.1%. At the earnings front as well, ABL reported decent growth of 27.4% to `41cr. As per media reports ABL is in advanced talks with Macquarie SBI Infrastructure Fund to sell 35% stake in its road subsidiary for `800cr. The deal if goes through would value the subsidiary at `2,300cr. This deal would be a big positive for ABL as funding for its road BOT projects has been a major overhang on the stock. Further owing to the sharp spike in share its price we recommend Accumulate on the stock with target price of `273. Y/E Sales OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

March (` cr) (%) (` cr) (`) (%) (x) (x) (x) (x)

FY2013E 2,023 22.4 141 26.7 12.9 12.9 1.2 9.3 2.1

FY2014E 2,303 22.4 165 31.3 13.3 13.3 1.0 10.4 2.3

Godawari Power and Ispat (CMP: `124/ TP: -/ Upside: -) Godawari Power and Ispat (GPIL) reported its 1QFY2013 results. Net sales increased by 22.7% to `602cr. On the operating front, although EBITDA increased by 44.4% yoy to `11cr, EBITDA margin contracted 449bp yoy to 18.2% on account of higher prices of key inputs. The other income fell by 29.8% yoy to `3cr. The net profit increased by 55.3% yoy to `47cr in line with increase in EBITDA. We keep our rating and target price under review. Y/E Sales OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

March (` cr) (%) (` cr) (`) (%) (x) (x) (x) (x)

FY2013E 2,085 16.8 117 36.9 14.3 3.4 0.4 2.9 0.5

FY2014E 2,139 18.2 146 45.9 15.2 2.7 0.4 2.3 0.4

www.angelbroking.com

Market Outlook August 13, 2012

CCCL (CMP: `17 / TP: - / Upside: - %) CCCL posted a dismal set of numbers once again for the quarter. A lower-than-expected performance at both the revenue and the EBITDAM front along with a high interest cost led to a higher-than-expected loss for the quarter. The top-line of the company declined by 4.8% yoy to `482cr against our estimate of `534cr. However, the major disappointment came on the margin front, as the company posted abysmal EBITDA margin of 2.7% a drop of 270bp yoy and 680bp qoq, against our expectations of it coming at 4.2%. Further, on the bottom-line front the company posted loss of `16cr vs a profit of `1cr in 1QFY2012 and against our expectations of `6cr loss mainly on account of poor performance at revenue and EBITDAM level and high interest cost (`26cr, a jump of 43.1% yoy). CCCL had an order inflow of `335cr during the quarter, taking its outstanding order book to `4,821cr. The company has disappointed on the earnings front and posted erratic margins since the last few quarters. Hence, we maintain our Neutral view on the stock. Y/E Sales OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

March (` cr) (%) (` cr) (`) (%) (x) (x) (x) (x)

FY2013E 2,489 7.0 44 2.4 6.9 7.1 0.5 5.2 0.4

FY2014E 2,755 7.8 67 3.6 9.8 4.6 0.4 4.3 0.3

Madhucon Projects (CMP: `37/ TP: `56 / Upside: 53%) For 1QFY2013, Madhucon Projects (MPL) reported mixed set of numbers with revenue coming below our expectations however higher EBITDAM resulted in better-than-expected earnings performance. On the top line front, MPL posted disappointing performance with yoy increase of 2.1% to `336cr, way below our expectations of `425cr. EBITDAM came in at 14.0%, flat on yoy basis but posted a jump of 220bp on qoq basis against our expectations of 11.9%. Interest cost stood at `24cr a jump of 15.1% on yoy basis but a decline of 11.3% on a sequential basis. On the earnings front, the company posted a decline of 11.9% on yoy basis at `7cr higher than our expectations of `5cr despite a higher tax rate (39.5%) on the back of higher EBITDAM and lower-than-expected interest cost. We maintain Buy on the stock with target price of `56. Y/E Sales OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

March (` cr) (%) (` cr) (`) (%) (x) (x) (x) (x)

FY2013E 2,206 10.7 34 4.6 8.6 7.9 0.4 6.6 0.7

FY2014E 2,502 10.7 35 4.7 8.3 7.8 0.4 6.4 0.7

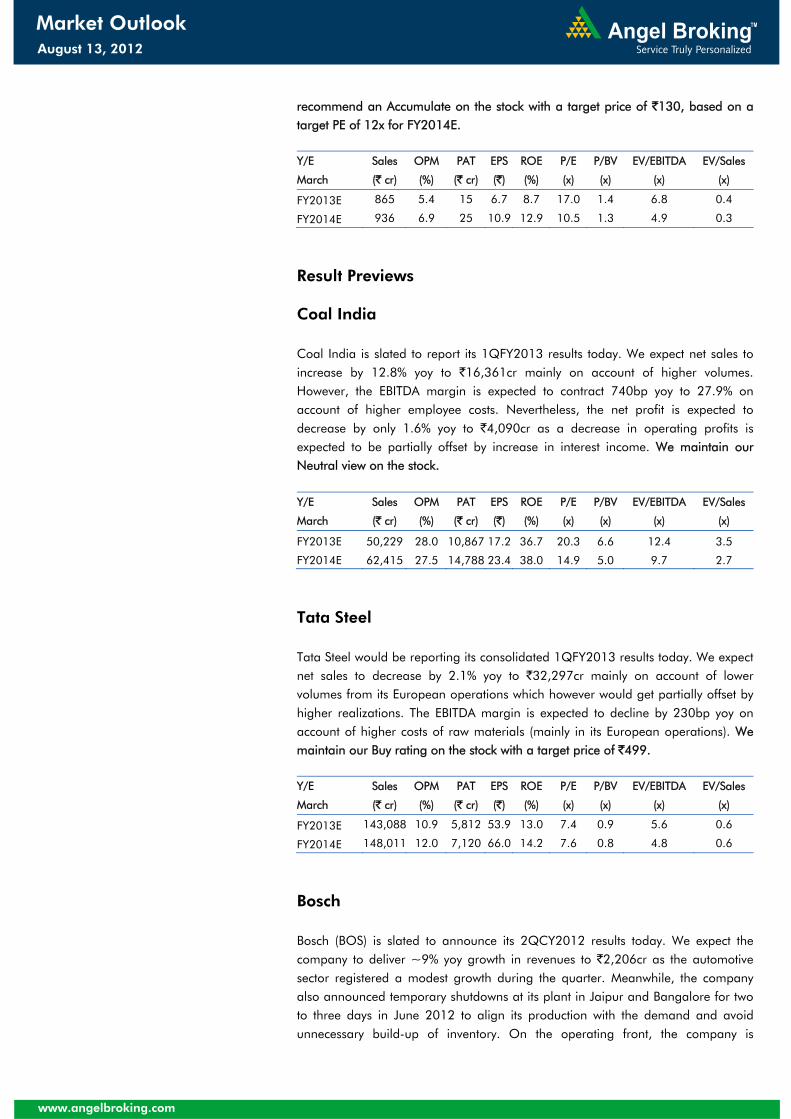

Hitachi Home (CMP – `114, TP: `130, Upside: 14.3%) For 4QFY2012, Hitachi reported a better than expected topline of `376cr, 14.6% higher yoy from `328cr in 1QFY2012. The company disappointed on the EBITDA margin front which came in at 6.8% in 1QFY2013, contraction of 108bp yoy from 7.9% in 1QFY2012 on account of higher other expenses. Net profit grew marginally by 3.8% yoy from `13.1cr in 1QFY2012 to `13.6cr in 1QFY2013. We

www.angelbroking.com

Market Outlook August 13, 2012

recommend an Accumulate on the stock with a target price of `130, based on a target PE of 12x for FY2014E. Y/E Sales OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

March (` cr) (%) (` cr) (`) (%) (x) (x) (x) (x)

FY2013E 865 5.4 15 6.7 8.7 17.0 1.4 6.8 0.4

FY2014E 936 6.9 25 10.9 12.9 10.5 1.3 4.9 0.3

Result Previews Coal India Coal India is slated to report its 1QFY2013 results today. We expect net sales to increase by 12.8% yoy to `16,361cr mainly on account of higher volumes. However, the EBITDA margin is expected to contract 740bp yoy to 27.9% on account of higher employee costs. Nevertheless, the net profit is expected to decrease by only 1.6% yoy to `4,090cr as a decrease in operating profits is expected to be partially offset by increase in interest income. We maintain our Neutral view on the stock. Y/E Sales OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

March (` cr) (%) (` cr) (`) (%) (x) (x) (x) (x)

FY2013E 50,229 28.0 10,867 17.2 36.7 20.3 6.6 12.4 3.5

FY2014E 62,415 27.5 14,788 23.4 38.0 14.9 5.0 9.7 2.7

Tata Steel Tata Steel would be reporting its consolidated 1QFY2013 results today. We expect net sales to decrease by 2.1% yoy to `32,297cr mainly on account of lower volumes from its European operations which however would get partially offset by higher realizations. The EBITDA margin is expected to decline by 230bp yoy on account of higher costs of raw materials (mainly in its European operations). We maintain our Buy rating on the stock with a target price of `499. Y/E Sales OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

March (` cr) (%) (` cr) (`) (%) (x) (x) (x) (x)

FY2013E 143,088 10.9 5,812 53.9 13.0 7.4 0.9 5.6 0.6

FY2014E 148,011 12.0 7,120 66.0 14.2 7.6 0.8 4.8 0.6

Bosch Bosch (BOS) is slated to announce its 2QCY2012 results today. We expect the company to deliver ~9% yoy growth in revenues to `2,206cr as the automotive sector registered a modest growth during the quarter. Meanwhile, the company also announced temporary shutdowns at its plant in Jaipur and Bangalore for two to three days in June 2012 to align its production with the demand and avoid unnecessary build-up of inventory. On the operating front, the company is

www.angelbroking.com

Market Outlook August 13, 2012

expected to post a 170bp yoy expansion in operating margin to 20% led by decline in raw-material expenses. The net profit is expected to register a 13% yoy growth to `316cr. At `8,865 the stock is trading at 19.3x CY2013E earnings, which is in-line with its historical average of 20x. Currently we have a Neutral rating on the stock.

Y/E Sales OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

Dec. (` cr) (%) (` cr) (`) (%) (x) (x) (x) (x)

CY2012E 9,106 19.3 1,288 410.2 22.1 21.6 4.8 14.0 2.6

CY2013E 10,255 19.3 1,445 460.3 20.4 19.3 3.9 12.0 2.2

NMDC NMDC is slated to announce its 1QFY2013 results today. We expect the company’s top-line to decrease by 2.7% yoy to `2,706cr on account of decrease in sales volumes. On the operating front, the EBITDA margin is expected to decrease by 490bp yoy to 76.1%. The bottom-line is expected to decrease by 3.7% yoy to `1,735cr. We maintain our Neutral view on the stock.

Y/E Sales OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

March (` cr) (%) (` cr) (`) (%) (x) (x) (x) (x)

FY2013E 11,959 78.2 7,553 19.1 27.1 9.5 2.3 5.0 3.9

FY2014E 13,062 78.6 8,287 20.9 24.4 8.9 1.9 4.3 3.4

India Cements India cements is expected to announce its 1QFY2013 results today. We expect the company to post an 8.6% yoy growth in its topline to `1,152cr, aided largely by better realization. OPM is expected to increase by 322bp yoy to 26%. Bottomline is expected to grow by 6.2% yoy to `108cr. We maintain a neutral view on the stock.

Y/E Sales OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/tone*

Dec. (` cr) (%) (` cr) (`) (%) (x) (x) (x) (US $)

CY2012E 4,364 18.8 283 9.2 8.0 9.3 0.7 5.5 52

CY2013E 4,791 19.1 349 11.4 9.5 7.5 0.7 4.9 Note: * computed on TTM basis

www.angelbroking.com

Market Outlook August 13, 2012

Quarterly Bloomberg Brokers Consensus Estimate Coal India - Consolidated (13/08/2012) Particulars (` cr) 1QFY13E 1QFY12 y-o-y (%) 4QFY12 q-o-q (%)

Net sales 16,680 14,499 15 19,419 (14)

EBITDA 4,763 4,824 (1) 4,210 13

EBITDA margin (%) 28.6 33.3 21.7

Net profit 4,210 4,144 2 4,013 5

NMDC Ltd - (13/08/2012) Particulars (` cr) 1QFY13E 1QFY12 y-o-y (%) 4QFY12 q-o-q (%)

Net sales 2,805 2,783 1 2,594 8

EBITDA 2,334 1,801 30 1,925 21

EBITDA margin (%) 83.2 64.7 74.2

Net profit 1,765 1,801 (2) 1,642 7

Suzlon Energy Ltd - Consolidated (13/08/2012) Particulars (` cr) 1QFY13E 1QFY12 y-o-y (%) 4QFY12 q-o-q (%)

Net sales 4,792 4,126 16 6,695 (28)

EBITDA 377 237 59 404 (7)

EBITDA margin (%) 7.9 5.7 6.0

Net profit (129) 63 (305) (299) (57)

Tata Steel Ltd - Consolidated (13/08/2012) Particulars (` cr) 1QFY13E 1QFY12 y-o-y (%) 4QFY12 q-o-q (%)

Net sales 32,552 32,840 (1) 33,860 (4)

EBITDA 3,243 4,423 (27) 3,179 2

EBITDA margin (%) 10.0 13.5 9.4

Net profit 689 5,322 (87) 403 71

Essar Oil Ltd - (14/08/2012) Particulars (` cr) 1QFY13E 1QFY12 y-o-y (%) 4QFY12 q-o-q (%)

Net sales 19,268 14,946 29 17,514 10

EBITDA 354 928 (62) 285 24

EBITDA margin (%) 1.8 6.2 1.6

Net profit (790) 469 (268) (515) 53

HDIL - Consolidated (14/08/2012) Particulars (` cr) 1QFY13E 1QFY12 y-o-y (%) 4QFY12 q-o-q (%)

Net sales 505 502 1 167 202

EBITDA 263 256 3 51 416

EBITDA margin (%) 52.1 51.0 30.5

Net profit 151 209 (28) 97 56

www.angelbroking.com

Market Outlook August 13, 2012

Hindalco Industries Ltd - (14/08/2012) Particulars (` cr) 1QFY13E 1QFY12 y-o-y (%) 4QFY12 q-o-q (%)

Net sales 6,870 5,979 15 7,563 (9)

EBITDA 749 867 (14) 865 (13)

EBITDA margin (%) 10.9 14.5 11.4

Net profit 507 644 (21) 640 (21)

Reliance Infrastructure Ltd - (14/08/2012) Particulars (` cr) 1QFY13E 1QFY12 y-o-y (%) 4QFY12 q-o-q (%)

Net sales 4,462 3,371 32 5,674 (21)

EBITDA 483 696 (31) 617 (22)

EBITDA margin (%) 10.8 20.6 10.9

Net profit 334 430 (22) 658 (49)

Reliance Power - Consolidated (14/08/2012) Particulars (` cr) 1QFY13E 1QFY12 y-o-y (%) 4QFY12 q-o-q (%)

Net sales 1,005 542 85 533 89

EBITDA 364 185 97 179 103

EBITDA margin (%) 36.2 34.1 33.6

Net profit 224 196 14 231 (3)

Unitech Ltd - Consolidated (14/08/2012) Particulars (` cr) 1QFY13E 1QFY12 y-o-y (%) 4QFY12 q-o-q (%)

Net sales 638 596 7 716 (11)

EBITDA 124 120 4 389 (68)

EBITDA margin (%) 19.4 20.1 54.3

Net profit 85 102 (17) 3 2647

IDFC Ltd - Consolidated (14/08/2012) Particulars (` cr) 1QFY13E 1QFY12 y-o-y (%) 4QFY12 q-o-q (%)

Net profit 371 314 18 332 12

Economic and Political News

Foreign Telcos can bid alone in 2G Auctions Centre tells power forum to fall in line on open access PFC considers `17,000cr transition loans to discoms

Corporate News

Maruti’s Manesar plant may become operational next week Sun Pharma to spin off local formulation business Tata may produce high performance engines in India, UK

Source: Economic Times, Business Standard, Business Line, Financial Express, Mint

Date Company

August 13, 2012 Coal India, NMDC, Tata Steel, Bosch India, GSK Pharma, Suzlon Energy, India Cements, PTC India

August 14, 2012Hindalco, Reliance Power, IDFC, Nalco, Essar Oil, Reliance Infra., Unitech, HDIL, Monnet Ispat, Amara Raja Batteries, Orchid Chemicals, Simplex Infra, Electrosteel Castings, Finolex Cables, Cravatex, S. Kumars Nationwide

Source: Bloomberg, Angel Research

Result Calendar

Global economic events release calendar

Date Country Event Description Unit Period Bloomberg Data

Last Reported Estimated

August 14, 2012 UK CPI (YoY) % Change Jul 2.40 2.30

IndiaMonthly Wholesale Prices YoY%

% Change Jul 7.25 7.20

US Producer Price Index (mom) % Change Jul 0.10 0.20

Euro Zone Euro-Zone GDP s.a. (QoQ) % Change 2Q A -- (0.20)

Germany GDP nsa (YoY) % Change 2Q P 1.70 0.90

August 15, 2012 UK Jobless claims change % Change Jul 6.10 6.00

US Industrial Production % Jul 0.43 0.50

US Consumer price index (mom) % Change Jul -- 0.20

August 16, 2012 US Initial Jobless claims Thousands Aug 11 361.00 365.00

US Housing Starts Thousands Jul 760.00 758.00

US Building permits Thousands Jul 760.00 766.00

Euro Zone Euro-Zone CPI (YoY) % Jul 2.40 2.40

August 22, 2012 US Existing home sales Millions Jul 4.37 4.52

August 23, 2012 Germany PMI Services Value Aug A 50.30 --

Germany PMI Manufacturing Value Aug A 43.00 --

Euro ZoneEuro-Zone Consumer Confidence

Value Aug A (21.50) --

US New home sales Thousands Jul 350.00 360.00

August 24, 2012 UK GDP (YoY) % Change 2Q P (0.80) --

August 28, 2012 US Consumer ConfidenceS.A./

1985=100Aug 65.90 --

August 29, 2012 US GDP Qoq (Annualised) % Change 2Q S 1.50 --

August 30, 2012 Germany Unemployment change (000's) Thousands Aug 7.00 --

August 31, 2012 India Qtrly GDP YoY% % Change 2Q 5.30 --

September 01, 2012 China PMI Manufacturing Value Aug 50.10 --

September 03, 2012 India Imports YoY% % Change Jul (13.46) --

India Exports YoY% % Change Jul (5.45) --

UK PMI Manufacturing Value Aug 45.40 --

Source: Bloomberg, Angel Research

www.angelbroking.com

August 13, 2012

Market Outlook

Market Strategy August 13, 2012

www.angelbroking.com

Macro watch

Exhibit 1: Quarterly GDP trends

5.9

7.5

9.8

7.4

9.4

8.5

7.6 8.2

9.2

8.0

6.7 6.1

5.3

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

4QFY

09

1QFY

10

2QFY

10

3QFY

10

4QFY

10

1QFY

11

2QFY

11

3QFY

11

4QFY

11

1QFY

12

2QFY

12

3QFY

12

4QFY

12

(%)

Source: CSO, Angel Research

Exhibit 2: IIP trends

3.7 3.4 2.5

(5.0)

6.0

2.7

1.0

4.3

(2.8) (0.9)

2.5

(1.8)

(6.0)

(4.0)

(2.0)

-

2.0

4.0

6.0

8.0

Jul-1

1

Aug

-11

Sep-

11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

Feb-

12

Mar

-12

Apr

-12

May

-12

Jun-

12

(%)

Source: MOSPI, Angel Research

Exhibit 3: Monthly WPI inflation trends

9.4 9.8 10.0 9.9 9.5

7.76.9 7.4 7.7 7.5 7.6 7.3

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Jul-1

1

Aug

-11

Sep-

11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

Feb-

12

Mar

-12

Apr

-12

May

-12

Jun-

12

(%)

Source: MOSPI, Angel Research

Exhibit 4: Manufacturing and services PMI

48.0

50.0

52.0

54.0

56.0

58.0

60.0

Jun-

11

Jul-1

1

Aug

-11

Sep-

11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

Feb-

12

Mar

-12

Apr

-12

May

-12

Jun-

12

Mfg. PMI Services PMI

Source: Market, Angel Research; Note: Level above 50 indicates expansion

Exhibit 5: Exports and imports growth trends

(30.0)

(15.0)

0.0

15.0

30.0

45.0

60.0

75.0

Jul-1

1

Aug

-11

Sep-

11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

Feb-

12

Mar

-12

Apr

-12

May

-12

Jun-

12

Exports yoy growth Imports yoy growth(%)

Source: Bloomberg, Angel Research

Exhibit 6: Key policy rates

4.00

5.00

6.00

7.00

8.00

9.00

Aug

-11

Sep-

11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

Feb-

12

Mar

-12

Apr

-12

May

-12

Jun-

12

Jul-1

2

Aug

-12

Repo rate Reverse Repo rate CRR (%)

Source: RBI, Angel Research

Company Name Reco CMP Target Mkt Cap Sales ( ₹cr ) OPM(%) EPS (₹) PER(x) P/BV(x) RoE(%) EV/Sales(x)

( ₹ ) Price ( ₹) ( ₹ cr ) FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E

Agri / Agri Chemical

Rallis Neutral 124 - 2,412 1,466 1,686 14.8 14.8 7.0 8.1 17.7 15.3 3.8 3.2 22.6 22.5 1.7 1.5

United Phosphorus Buy 120 170 5,527 8,421 9,263 16.5 16.5 15.0 17.0 8.0 7.1 1.2 1.0 15.6 15.5 0.8 0.7

Auto & Auto Ancillary

Amara Raja Batteries Accumulate 319 345 2,724 2,715 3,041 15.3 15.3 29.2 32.8 10.9 9.7 2.5 2.0 26.0 23.3 1.0 0.8

Apollo Tyres Buy 86 99 4,325 13,412 15,041 11.0 11.0 11.5 14.2 7.5 6.1 1.3 1.1 18.7 19.4 0.5 0.4

Ashok Leyland Buy 23 30 6,106 14,920 16,850 9.0 9.3 2.2 2.8 10.5 8.4 1.9 1.7 13.3 15.6 0.5 0.4

Automotive Axle Buy 335 430 506 993 1,140 11.6 11.5 36.9 43.0 9.1 7.8 1.8 1.5 21.2 21.3 0.6 0.4

Bajaj Auto Neutral 1,680 - 48,609 21,285 23,927 18.2 18.3 108.5 121.3 15.5 13.9 6.4 5.2 46.1 41.3 1.9 1.6

Bharat Forge Buy 312 359 7,264 7,004 7,985 16.2 16.4 20.8 25.6 15.0 12.2 2.8 2.4 20.3 21.2 1.1 1.0

Bosch India Neutral 8,853 - 27,799 9,106 10,255 19.4 19.3 410.2 460.3 21.6 19.2 4.8 3.9 22.1 20.4 2.7 2.3

CEAT Buy 101 164 345 4,989 5,634 8.7 8.5 32.7 41.1 3.1 2.5 0.5 0.4 15.8 16.9 0.3 0.2

Exide Industries Accumulate 130 149 11,063 5,899 6,771 16.0 17.0 7.4 9.1 17.7 14.3 3.2 2.7 19.0 20.2 1.5 1.3

FAG Bearings Neutral 1,532 - 2,546 1,505 1,747 17.7 18.0 111.5 130.0 13.8 11.8 2.9 2.3 22.8 21.7 1.4 1.2

Hero Motocorp Buy 1,914 2,428 38,224 26,097 29,963 15.0 15.3 139.5 151.8 13.7 12.6 6.5 4.9 54.6 44.3 1.2 1.0

JK Tyre Buy 93 135 380 7,517 8,329 6.1 6.3 26.2 38.5 3.5 2.4 0.5 0.4 13.4 17.2 0.3 0.3

Mahindra and Mahindra Buy 739 879 45,352 36,536 41,650 11.6 11.5 49.3 54.9 15.0 13.5 3.1 2.6 22.1 21.1 1.0 0.8

Maruti Accumulate 1,164 1,227 33,615 42,887 49,079 5.5 6.6 66.8 87.6 17.4 13.3 2.0 1.8 12.1 14.1 0.6 0.5

Motherson Sumi Buy 172 216 6,725 23,342 26,366 7.8 8.2 13.3 18.0 12.9 9.5 3.1 2.4 26.2 28.4 0.5 0.4

Subros Buy 28 34 169 1,230 1,378 8.8 8.6 4.5 5.7 6.2 4.9 0.6 0.6 9.8 11.8 0.4 0.3

Tata Motors Buy 232 292 61,830 195,096 219,428 12.8 12.8 39.0 43.9 6.0 5.3 1.7 1.3 32.6 28.2 0.4 0.3

TVS Motor Accumulate 39 43 1,872 7,545 8,301 6.2 6.1 4.9 5.4 8.0 7.3 1.4 1.3 18.8 18.2 0.2 0.2

Capital Goods

ABB* Sell 772 498 16,355 8,760 10,023 5.5 7.5 12.4 20.7 62.1 37.2 6.0 5.3 10.1 15.2 1.8 1.6

BGR Energy Neutral 274 - 1,980 3,669 4,561 11.0 11.0 24.7 29.6 11.1 9.3 1.6 1.5 15.3 16.7 - 0.6

BHEL Neutral 229 - 56,001 47,801 43,757 19.4 19.8 25.7 23.9 8.9 9.6 1.9 1.6 22.7 18.3 1.1 0.9

Blue Star Neutral 187 - 1,685 3,047 3,328 5.4 6.9 9.6 16.2 19.5 11.5 3.8 3.1 20.7 29.7 0.6 0.5

Crompton Greaves Accumulate 116 128 7,441 12,691 14,096 7.0 8.5 6.5 9.1 17.8 12.7 1.9 1.7 11.1 14.2 0.6 0.5

Jyoti Structures Buy 38 67 313 2,622 2,801 10.6 11.0 10.9 13.4 3.5 2.8 0.5 0.4 13.7 14.9 0.3 0.3

KEC International Buy 57 69 1,458 6,858 7,431 7.5 8.3 9.0 11.5 6.3 4.9 1.1 1.0 26.9 27.2 0.3 0.3

LMW Accumulate 1,768 1,992 1,992 2,369 2,727 11.7 11.7 143.4 166.0 12.3 10.7 2.1 1.9 17.4 18.4 0.4 0.2

Thermax Neutral 500 - 5,961 5,514 5,559 8.9 9.6 26.9 28.4 18.6 17.6 3.2 2.9 18.4 17.1 1.0 1.0

www.angelbroking.com

August 13, 2012

Market Outlook

Stock Watch

Company Name Reco CMP Target Mkt Cap Sales ( ₹cr ) OPM(%) EPS (₹) PER(x) P/BV(x) RoE(%) EV/Sales(x)

( ₹ ) Price ( ₹) ( ₹ cr ) FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E

Cement

ACC Neutral 1,342 - 25,190 11,220 12,896 20.0 20.6 71.1 81.2 18.9 16.5 3.3 3.0 18.1 19.0 2.0 1.6

Ambuja Cements Neutral 194 - 29,890 10,205 11,659 24.6 24.2 10.8 12.0 17.9 16.1 3.7 3.4 19.7 19.8 2.5 2.1

India Cements Neutral 86 - 2,628 4,364 4,791 18.9 19.1 9.2 11.4 9.3 7.5 0.7 0.7 8.0 9.5 0.5 0.5

J K Lakshmi Cements Neutral 95 - 1,160 1,964 2,278 19.5 20.4 16.3 17.9 5.8 5.3 0.8 0.7 14.7 14.6 0.7 1.1

Madras Cements Neutral 171 - 4,075 3,608 3,928 27.4 26.9 15.6 18.1 11.0 9.5 1.7 1.5 16.8 16.9 1.8 1.5

Shree Cements Neutral 3,165 - 11,026 5,519 6,293 24.5 23.7 156.6 225.3 20.2 14.1 5.0 4.3 22.3 26.0 1.7 1.3

UltraTech Cement Neutral 1,673 - 45,854 20,167 22,752 21.7 23.0 90.8 107.8 18.4 15.5 18.4 15.5 - - 1.9 1.7

Construction

Ashoka Buildcon Accumulate 255 273 1,343 2,014 2,293 22.4 22.4 22.6 26.7 11.3 9.6 1.2 1.1 11.4 11.9 2.5 2.8

Consolidated Co Neutral 17 - 309 2,489 2,755 7.0 7.8 3.0 4.0 5.6 4.2 0.5 0.4 8.7 10.8 0.3 0.3

Hind. Const. Neutral 17 - 1,046 4,239 4,522 9.9 11.2 (2.3) (1.0) (7.6) (17.9) 1.0 1.1 (11.4) (5.6) 1.2 1.2

IRB Infra Buy 119 166 3,955 3,964 4,582 42.3 40.2 15.5 16.9 7.7 7.0 1.2 1.0 16.6 15.8 2.6 2.4

ITNL Buy 164 232 3,193 6,840 7,767 26.4 26.1 24.4 28.4 6.7 5.8 1.0 0.9 16.0 16.2 2.6 2.8

IVRCL Infra Buy 44 61 1,186 5,510 6,722 8.8 9.0 2.5 4.6 17.5 9.7 0.6 0.6 3.4 5.8 0.7 0.6

Jaiprakash Asso. Buy 75 91 15,970 15,259 17,502 25.7 24.7 4.2 5.0 17.7 15.0 1.5 1.4 8.5 9.3 2.4 2.1

Larsen & Toubro Accumulate 1,424 1,553 87,244 60,474 69,091 12.1 11.5 79.7 85.4 17.9 16.7 3.0 2.6 16.3 15.1 1.6 1.4

Madhucon Proj Buy 36 56 266 2,206 2,502 10.7 10.7 4.6 4.7 7.8 7.7 0.4 0.4 5.2 5.0 0.7 0.7

Nagarjuna Const. Accumulate 40 45 1,031 5,804 6,513 8.0 8.6 3.0 3.5 13.2 11.5 0.4 0.4 3.2 3.6 0.6 0.7

Patel Engg. Neutral 81 - 566 3,609 3,836 13.1 13.1 14.0 14.6 5.8 5.6 0.4 0.3 6.3 6.1 1.0 1.1

Punj Lloyd Neutral 50 - 1,660 11,892 13,116 8.9 8.9 1.7 3.1 29.5 16.2 0.6 0.5 1.9 3.4 0.6 0.5

Sadbhav Engg. Buy 132 182 1,979 2,789 3,147 10.6 10.7 8.4 10.4 15.6 12.6 2.1 1.8 15.0 15.6 0.9 0.8

Simplex Infra Buy 205 265 1,014 6,732 7,837 8.1 8.4 23.5 29.4 8.7 7.0 0.8 0.7 9.6 11.0 0.5 0.4

Financials

Allahabad Bank Neutral 127 - 6,340 7,233 8,579 3.1 3.3 40.5 40.9 3.1 3.1 0.6 0.5 19.4 17.0 - -

Andhra Bank Neutral 96 - 5,383 4,959 5,787 3.1 3.1 22.7 24.5 4.2 3.9 0.7 0.6 16.0 15.3 - -

Axis Bank Buy 1,071 1,373 44,362 15,961 19,583 3.1 3.2 117.3 143.1 9.1 7.5 1.7 1.4 20.1 20.8 - -

Bank of Baroda Buy 628 829 24,571 15,830 19,300 2.6 2.7 118.9 147.1 5.3 4.3 0.8 0.7 16.7 18.0 - -

Bank of India Buy 272 323 15,604 13,159 15,851 2.4 2.5 61.1 71.1 4.5 3.8 0.8 0.7 16.6 17.0 - -

Bank of Maharashtra Neutral 46 - 2,689 3,471 3,889 3.1 3.1 9.0 11.5 5.1 4.0 0.7 0.6 13.7 15.5 - -

Canara Bank Buy 349 421 15,481 11,334 13,629 2.2 2.3 75.4 85.1 4.6 4.1 0.7 0.6 15.2 15.3 - -

Central Bank Neutral 70 - 5,142 7,181 8,365 2.5 2.7 16.3 21.8 4.3 3.2 0.7 0.7 12.7 15.1 - -

www.angelbroking.com

August 13, 2012

Market Outlook

Stock Watch

Company Name Reco CMP Target Mkt Cap Sales ( ₹cr ) OPM(%) EPS (₹) PER(x) P/BV(x) RoE(%) EV/Sales(x)

( ₹ ) Price ( ₹) ( ₹ cr ) FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E

Financials

Corporation Bank Accumulate 389 436 5,756 5,067 5,998 2.1 2.3 105.6 111.0 3.7 3.5 0.6 0.6 17.6 16.3 - -

Dena Bank Buy 88 107 3,091 3,177 3,595 2.8 2.8 25.2 25.4 3.5 3.5 0.6 0.5 18.9 16.4 - -

Federal Bank Accumulate 423 459 7,237 2,697 3,171 3.4 3.4 47.9 58.0 8.9 7.3 1.1 1.0 13.6 14.7 - -

HDFC Neutral 690 - 103,813 7,340 8,805 3.5 3.5 31.5 37.8 21.9 18.2 4.4 3.9 34.8 32.2 - -

HDFC Bank Neutral 602 - 141,940 21,936 27,454 4.4 4.4 28.7 36.0 21.0 16.7 4.0 3.4 20.7 22.0 - -

ICICI Bank Buy 955 1,169 109,730 22,356 27,157 2.9 3.0 68.7 82.0 13.9 11.6 1.7 1.5 14.2 15.5 - -

IDBI Bank Buy 84 101 10,758 7,952 9,876 1.9 2.2 18.5 23.6 4.6 3.6 0.6 0.5 12.8 14.7 - -

Indian Bank Accumulate 172 190 7,375 6,294 7,191 3.4 3.4 40.6 44.9 4.2 3.8 0.7 0.6 18.1 17.4 - -

IOB Accumulate 71 80 5,687 7,473 8,732 2.5 2.5 16.7 22.6 4.3 3.2 0.5 0.5 11.8 14.4 - -

J & K Bank Accumulate 924 1,026 4,477 2,625 2,921 3.6 3.5 194.4 191.9 4.8 4.8 0.9 0.8 21.2 18.0 - -

LIC Housing Finance Accumulate 248 279 12,516 1,867 2,338 2.4 2.4 21.1 28.5 11.8 8.7 1.9 1.7 17.5 20.4 - -

Oriental Bank Buy 226 278 6,601 6,518 7,458 2.8 2.9 61.3 65.1 3.7 3.5 0.6 0.5 15.2 14.3 - -

Punjab Natl.Bank Buy 724 950 24,543 20,116 23,625 3.3 3.4 152.8 173.9 4.7 4.2 0.9 0.7 18.2 18.0 - -

South Ind.Bank Buy 23 27 2,593 1,514 1,717 2.8 2.7 4.0 4.2 5.7 5.4 1.1 1.0 20.5 18.5 - -

St Bk of India Buy 1,888 2,270 126,690 64,470 75,940 3.5 3.5 224.4 258.7 8.4 7.3 1.4 1.2 17.6 17.8 - -

Syndicate Bank Buy 94 119 5,661 6,840 7,996 2.9 3.0 25.7 29.2 3.7 3.2 0.6 0.5 17.9 17.8 - -

UCO Bank Neutral 68 - 4,497 5,488 6,338 2.4 2.5 17.3 17.7 3.9 3.8 0.8 0.7 17.0 15.3 - -

Union Bank Buy 164 230 9,012 10,299 12,227 2.9 3.0 42.1 49.3 3.9 3.3 0.7 0.6 16.7 17.1 - -

United Bank Buy 53 79 1,928 3,634 4,194 2.8 2.9 18.2 23.0 2.9 2.3 0.4 0.4 15.0 16.7 - -

Vijaya Bank Neutral 53 - 2,604 2,579 3,028 2.1 2.3 8.8 11.6 6.0 4.6 0.7 0.6 11.1 13.3 - -

Yes Bank Buy 357 453 12,683 3,255 4,228 2.8 3.0 34.2 42.7 10.5 8.4 2.2 1.8 23.3 23.8 - -

FMCG

Asian Paints Neutral 3,719 - 35,670 11,198 13,184 16.3 16.3 121.0 144.8 30.7 25.7 10.3 8.1 37.4 35.3 3.1 2.6

Britannia Buy 453 633 5,417 5,835 6,824 6.3 6.7 20.7 27.5 21.9 16.5 8.5 6.4 42.7 44.3 0.9 0.8

Colgate Neutral 1,179 - 16,039 3,018 3,429 20.9 22.3 34.6 41.0 34.1 28.8 31.4 23.8 99.5 94.1 5.2 4.5

Dabur India Neutral 120 - 20,905 6,124 7,030 17.0 16.8 4.5 5.2 26.8 23.2 11.1 8.8 43.2 41.5 3.4 2.9

GlaxoSmith Con* Neutral 2,816 - 11,843 3,124 3,663 17.1 17.6 104.5 123.8 27.0 22.8 8.4 6.7 34.4 32.8 3.4 2.9

Godrej Consumer Neutral 620 - 21,095 5,973 7,000 18.4 18.6 22.8 27.2 27.2 22.8 7.5 6.0 31.3 38.4 3.7 3.1

HUL Neutral 498 - 107,592 25,350 28,974 13.9 13.9 14.3 16.5 34.9 30.2 20.8 16.0 70.9 59.8 4.0 3.5

ITC Neutral 268 - 209,730 29,513 33,885 35.4 35.8 9.3 10.8 28.9 24.8 9.5 8.0 35.6 35.0 6.8 5.9

www.angelbroking.com

August 13, 2012

Market Outlook

Stock Watch

Company Name Reco CMP Target Mkt Cap Sales ( ₹cr ) OPM(%) EPS (₹) PER(x) P/BV(x) RoE(%) EV/Sales(x)

( ₹ ) Price ( ₹) ( ₹ cr ) FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E

FMCG

Marico Neutral 191 - 12,278 4,667 5,427 12.8 12.9 6.6 8.1 28.7 23.4 7.7 6.0 30.0 28.8 2.7 2.2

Nestle* Neutral 4,407 - 42,486 8,610 10,174 20.9 21.2 114.8 139.8 38.4 31.5 23.2 16.1 71.2 60.3 5.0 4.1

Tata Global Neutral 133 - 8,215 7,207 7,927 9.7 10.0 6.6 7.9 20.0 16.9 2.0 2.0 8.6 9.5 1.0 0.9

IT

HCL Tech Accumulate 537 585 37,209 24,400 27,049 18.6 17.5 41.1 45.0 13.1 11.9 2.9 2.5 22.7 21.1 1.5 1.3

Hexaware Accumulate 116 133 3,438 1,947 2,161 22.0 21.4 11.4 12.1 10.2 9.6 2.6 2.2 26.4 24.0 1.5 1.3

Infosys Accumulate 2,313 2,530 132,828 39,151 41,743 31.6 31.9 161.9 174.5 14.3 13.3 3.4 2.9 23.8 22.1 2.8 2.5

Infotech Enterprises Accumulate 175 187 1,951 1,889 2,065 18.0 17.5 18.0 19.7 9.7 8.9 1.4 1.2 14.5 13.7 0.7 0.6

KPIT Cummins Reduce 134 124 2,387 2,149 2,331 15.6 14.8 10.7 11.2 12.5 11.9 2.6 2.1 20.6 17.8 1.1 0.9

Mahindra Satyam Accumulate 92 97 10,862 7,574 8,062 19.6 18.4 9.5 9.7 9.8 9.6 1.6 1.3 16.1 14.1 1.0 0.9

Mindtree Accumulate 629 708 2,565 2,341 2,513 18.6 17.1 66.5 70.8 9.5 8.9 2.1 1.7 22.3 19.3 0.9 0.8

Mphasis Neutral 392 - 8,243 5,704 6,009 18.6 17.7 36.0 37.1 10.9 10.6 1.5 1.3 14.0 12.6 1.0 0.8

NIIT Accumulate 36 40 588 1,162 1,304 14.8 15.1 7.1 8.8 5.0 4.1 0.8 0.7 16.7 18.4 0.3 0.2

Persistent Neutral 379 - 1,516 1,193 1,278 25.6 24.3 42.6 44.3 8.9 8.6 1.5 1.3 17.2 15.5 0.9 0.8

TCS Neutral 1,278 - 250,094 61,046 67,507 29.3 29.1 67.3 72.4 19.0 17.6 6.1 5.0 31.9 28.3 3.9 3.5

Tech Mahindra Reduce 800 726 10,202 6,282 6,477 17.5 16.5 82.9 85.0 9.7 9.4 2.1 1.7 21.6 18.4 1.6 1.4

Wipro Buy 349 420 85,983 43,492 48,332 19.4 19.3 25.1 28.0 13.9 12.5 2.6 2.2 18.6 18.0 1.7 1.4

Media

D B Corp Buy 190 236 3,475 1,597 1,785 22.9 24.2 11.1 13.9 17.0 13.6 3.2 2.8 20.2 22.1 2.1 1.8

HT Media Buy 90 113 2,109 2,111 2,263 15.2 15.2 7.3 8.1 12.3 11.0 1.3 1.2 11.2 11.2 0.5 0.4

Jagran Prakashan Buy 91 112 2,886 1,506 1,687 22.5 23.2 6.2 7.0 14.7 13.0 3.5 3.2 25.0 25.7 2.1 1.9

PVR Neutral 186 - 481 625 732 17.4 17.1 13.3 15.6 13.9 11.9 1.5 1.3 13.2 13.8 1.2 1.0

Sun TV Network Neutral 311 - 12,256 1,981 2,239 77.0 76.7 18.6 21.3 16.8 14.6 4.2 3.7 27.1 27.5 5.7 4.8

Metals & Mining

Bhushan Steel Neutral 470 - 9,984 11,979 14,584 31.6 31.0 49.2 61.4 9.6 7.7 1.3 1.1 14.1 15.2 2.8 2.4

Coal India Neutral 349 - 220,188 68,841 74,509 25.3 25.3 24.1 26.1 14.5 13.4 4.0 3.3 30.4 26.8 2.3 2.0

Electrosteel Castings Buy 19 22 657 1,984 2,074 11.2 12.6 2.0 2.7 9.3 7.0 0.4 0.1 4.2 5.5 0.5 0.5

Hind. Zinc Accumulate 125 142 52,669 12,446 13,538 56.1 56.6 15.2 16.5 8.2 7.6 1.6 1.4 21.7 19.8 2.4 1.7

Hindalco Neutral 123 - 23,511 83,212 91,057 9.0 9.9 13.7 18.1 9.0 6.8 0.7 0.6 7.9 9.6 0.5 0.5

JSW Steel Neutral 730 - 16,280 38,740 41,459 17.3 17.0 79.9 89.4 9.1 8.2 0.9 0.8 10.4 10.6 0.9 0.8

MOIL Neutral 264 - 4,439 918 993 50.7 50.9 24.5 26.1 10.8 10.1 1.6 1.5 16.0 15.5 2.5 2.2

Monnet Ispat Buy 312 447 2,006 3,115 3,748 22.1 25.1 59.1 66.8 5.3 4.7 0.7 0.6 15.6 15.3 1.4 1.0

www.angelbroking.com

August 13, 2012

Market Outlook

Stock Watch

Company Name Reco CMP Target Mkt Cap Sales ( ₹cr ) OPM(%) EPS (₹) PER(x) P/BV(x) RoE(%) EV/Sales(x)

( ₹ ) Price ( ₹) ( ₹ cr ) FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E

Metals & Mining

Nalco Neutral 53 - 13,724 8,474 9,024 12.6 16.2 2.6 3.6 20.8 14.9 1.1 1.1 5.6 7.5 1.2 1.1

NMDC Neutral 181 - 71,801 11,959 13,062 78.2 78.6 19.1 20.9 9.5 8.7 2.3 1.9 27.1 24.4 3.9 3.4

SAIL Neutral 85 - 35,068 47,252 60,351 14.2 14.8 9.6 11.7 8.9 7.2 0.8 0.7 9.4 10.6 1.2 1.0

Sesa Goa Neutral 191 - 16,595 7,704 8,034 33.6 34.6 42.0 43.1 4.6 4.4 0.9 0.8 22.3 19.2 0.4 -

Sterlite Inds Neutral 111 - 37,303 41,680 45,382 24.2 23.2 16.3 16.9 6.8 6.6 0.7 0.7 11.3 10.7 0.5 0.4

Tata Steel Buy 400 499 38,887 143,088 148,011 10.9 12.1 53.9 66.0 7.4 6.1 0.9 0.8 12.2 13.4 0.6 0.6

Sarda Buy 128 148 459 1,251 1,321 22.7 23.4 33.0 37.1 3.9 3.5 0.6 0.5 15.1 14.8 0.7 0.7

Prakash Industries Buy 60 73 810 2,694 2,906 14.6 16.6 17.9 22.6 3.4 2.7 0.4 0.3 11.4 12.8 0.5 0.4

Oil & Gas

Cairn India Buy 324 380 61,845 16,605 17,258 75.4 71.7 57.0 54.9 5.7 5.9 1.0 0.9 20.2 16.3 2.7 2.1

GAIL Neutral 368 - 46,629 50,176 55,815 15.5 15.8 35.4 36.5 10.4 10.1 1.8 1.6 18.9 17.0 0.1 -

ONGC Accumulate 279 321 238,955 156,331 159,043 37.7 36.3 31.3 32.6 8.9 8.6 1.6 1.4 18.7 17.3 1.2 1.1

Reliance Industries Neutral 782 - 256,086 362,700 380,031 7.9 8.0 61.5 64.3 12.7 12.2 1.3 1.2 10.3 9.9 0.7 0.6

Gujarat Gas Neutral 303 - 3,885 2,472 3,267 16.1 11.5 21.2 19.2 14.3 15.8 4.9 4.2 33.4 28.7 1.5 1.1

Indraprastha Gas Neutral 252 - 3,526 3,040 3,135 24.3 26.7 24.8 27.9 10.2 9.0 2.4 2.0 25.5 23.6 1.2 1.0

Petronet LNG Buy 151 176 11,321 22,696 29,145 8.1 6.6 14.1 14.2 10.7 10.6 3.2 2.6 34.1 26.9 0.6 0.4Gujarat State Petronet Ltd. Neutral 72 - 4,040 1,041 939 91.8 91.9 8.5 7.4 8.5 9.7 1.4 1.3 18.1 14.0 4.8 5.3

Pharmaceuticals

Alembic Pharma Buy 59 91 1,104 1,624 1,855 14.2 15.6 6.6 9.1 8.9 6.4 2.2 1.7 27.5 29.2 0.9 0.8

Aurobindo Pharma Buy 103 156 3,003 5,243 5,767 14.6 14.6 11.8 12.6 8.7 8.2 0.9 0.4 11.4 10.9 0.7 0.6

Aventis* Neutral 2,207 - 5,083 1,482 1,682 15.5 15.5 95.0 104.0 23.2 21.2 4.1 3.2 18.6 17.0 3.2 2.8

Cadila Healthcare Accumulate 874 953 17,894 6,196 7,443 18.5 19.5 37.6 47.7 23.2 18.3 5.2 4.2 26.8 27.5 2.9 2.3

Cipla Accumulate 350 399 28,090 8,031 9,130 23.4 22.4 18.4 20.0 19.0 17.5 3.1 2.7 17.8 16.6 3.3 2.8

Dr Reddy's Neutral 1,646 - 27,937 10,696 11,662 20.7 21.0 83.7 92.9 19.7 17.7 4.1 3.4 22.4 21.0 2.7 2.5

Dishman Pharma Accumulate 86 92 697 1,280 1,536 17.8 17.8 9.2 11.3 9.4 7.7 0.7 0.7 7.7 8.5 1.2 1.0

GSK Pharma* Neutral 2,105 - 17,828 2,651 2,993 31.7 31.2 76.0 82.4 27.7 25.5 8.0 6.9 30.8 29.0 5.8 5.0

Indoco Remedies Buy 56 92 519 685 837 15.2 15.2 7.4 8.9 7.6 6.3 1.1 1.0 15.9 16.3 0.9 0.8

Ipca labs Buy 406 475 5,117 2,850 3,474 20.7 20.7 29.2 36.6 13.9 11.1 3.3 2.6 26.1 26.1 2.0 1.6

Lupin Accumulate 581 647 25,981 8,426 10,082 19.7 20.0 27.4 32.4 21.2 17.9 5.1 4.1 27.0 25.2 3.0 2.4

Orchid Chemicals Buy 107 178 756 2,117 2,434 17.7 17.7 16.7 22.2 6.4 4.8 0.6 0.5 9.5 11.5 1.0 0.8

Ranbaxy* Neutral 483 - 20,408 12,046 11,980 18.0 15.8 35.7 29.8 13.5 16.2 5.1 4.1 43.1 28.1 1.7 1.7

www.angelbroking.com

August 13, 2012

Market Outlook

Stock Watch

Company Name Reco CMP Target Mkt Cap Sales ( ₹cr ) OPM(%) EPS (₹) PER(x) P/BV(x) RoE(%) EV/Sales(x)

( ₹ ) Price ( ₹) ( ₹ cr ) FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E

Pharmaceuticals

Sun Pharma Neutral 676 - 69,856 9,272 11,080 38.6 38.0 22.7 22.6 29.8 29.9 5.0 4.4 17.9 15.6 6.1 4.9

Power

CESC Accumulate 300 342 3,748 5,218 5,644 24.2 23.8 44.6 47.6 6.7 6.3 0.7 0.6 11.0 10.6 1.0 1.1

GIPCL Accumulate 67 77 1,020 1,557 1,573 29.3 28.7 10.8 11.0 6.3 6.1 0.7 0.6 10.8 10.2 1.1 1.0

NTPC Reduce 172 158 141,698 74,111 85,789 23.2 23.6 12.4 14.0 13.9 12.2 1.7 1.6 13.0 13.5 2.6 2.4

Real Estate

Anant Raj Buy 48 78 1,409 657 875 52.0 56.1 8.4 12.7 5.7 3.8 0.4 0.3 6.3 8.9 3.4 2.6

DLF Neutral 210 - 35,709 9,878 12,033 44.7 46.1 9.6 13.4 22.0 15.7 1.4 1.3 6.4 8.7 6.1 5.0

HDIL Buy 81 115 3,394 2,441 3,344 55.1 48.2 22.7 26.6 3.6 3.0 0.3 0.3 8.8 9.4 3.2 2.4

MLIFE Accumulate 357 396 1,458 813 901 26.2 26.6 32.0 37.1 11.2 9.6 1.2 1.1 10.4 11.0 2.2 1.9

Telecom

Bharti Airtel Neutral 256 - 97,122 79,542 87,535 30.9 32.2 10.3 15.0 24.9 17.0 1.8 1.6 7.2 9.6 1.9 1.6

Idea Cellular Neutral 74 - 24,510 22,988 25,333 26.4 26.9 3.5 4.9 21.4 15.2 1.7 1.6 8.1 10.2 1.5 1.3

Rcom Neutral 55 - 11,270 22,125 23,734 31.9 32.0 4.5 5.9 12.2 9.3 0.3 0.3 2.5 3.1 2.0 1.6

zOthers

Abbott India Accumulate 1,536 1,628 3,263 1,662 1,899 11.4 12.5 69.8 90.4 22.0 17.0 5.0 4.1 24.9 26.6 1.8 1.5

Bajaj Electricals Buy 173 246 1,723 3,569 4,172 8.6 9.2 17.3 22.3 10.0 7.7 2.2 1.8 22.9 25.3 0.5 0.4

Cera Sanitaryware Buy 300 352 380 396 470 16.7 16.5 28.0 33.2 10.7 9.0 2.2 1.8 23.8 23.1 1.1 0.9

Cravatex Buy 623 785 161 302 364 5.7 6.0 49.0 71.0 12.7 8.8 3.8 2.7 29.8 30.7 0.6 0.5

CRISIL Neutral 885 - 6,208 982 1,136 34.3 34.3 34.3 40.0 25.8 22.1 11.7 9.3 50.9 46.9 5.9 4.9

Finolex Cables Buy 39 61 597 2,334 2,687 8.8 9.3 7.6 10.2 5.1 3.8 0.7 0.6 13.7 16.1 0.2 0.1

Force Motors Buy 437 591 570 2,214 2,765 4.5 5.4 39.5 73.9 11.1 5.9 0.5 0.5 4.4 7.6 0.1 0.1

Goodyear India Accumulate 335 370 773 1,543 1,646 8.1 9.2 32.3 39.4 10.4 8.5 2.1 1.8 21.7 22.4 0.3 0.2

Graphite India Buy 82 124 1,606 2,158 2,406 18.1 18.9 12.4 14.0 6.6 5.9 0.9 0.8 14.0 14.3 0.9 0.7

Greenply Industries Buy 188 309 454 1,925 2,235 10.6 10.9 29.6 44.1 6.4 4.3 1.0 0.8 16.8 21.0 0.5 0.4

HEG Accumulate 211 229 844 1,586 1,685 17.9 18.1 16.1 25.7 13.2 8.2 1.0 0.9 7.5 11.6 1.2 1.1

Hitachi Buy 113 160 259 857 968 6.9 8.4 10.2 16.0 11.1 7.0 1.4 1.2 12.9 17.8 0.4 0.3

Honeywell Automation Buy 2,463 2,842 2,177 1,847 2,162 4.3 7.3 61.0 120.0 40.4 20.5 3.2 2.8 9.3 16.3 1.1 0.9

INEOS ABS India Accumulate 673 744 1,183 1,056 1,081 8.1 10.6 33.8 46.5 19.9 14.5 2.8 2.3 14.7 17.5 1.1 1.0

ITD Cementation Neutral 230 - 265 1,451 1,669 12.3 12.4 32.4 41.5 7.1 5.5 0.6 0.6 9.4 10.9 0.6 0.6

Jyothy Laboratories Accumulate 134 145 2,167 1,248 1,468 9.8 10.4 5.9 7.2 22.7 18.8 3.3 3.0 15.0 16.6 2.1 1.7

MCX Buy 1,136 1,598 5,791 610 702 65.5 67.0 67.9 79.9 16.7 14.2 4.9 4.1 29.1 28.9 6.6 5.2

MRF Buy 10,650 12,884 4,517 11,804 12,727 10.4 10.5 1,289.9 1,431.3 8.3 7.4 1.6 1.3 21.3 19.4 0.5 0.5

www.angelbroking.com

August 13, 2012

Market Outlook

Stock Watch

Company Name Reco CMP Target Mkt Cap Sales ( ₹cr ) OPM(%) EPS (₹) PER(x) P/BV(x) RoE(%) EV/Sales(x)

( ₹ ) Price ( ₹) ( ₹ cr ) FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E

zOthers

Page Industries Neutral 3,070 - 3,424 887 1,108 18.3 18.6 95.0 120.9 32.3 25.4 16.9 13.7 57.4 59.5 3.9 3.1

Relaxo Footwears Buy 550 684 660 1,019 1,208 12.3 13.0 51.0 68.4 10.8 8.0 2.9 2.1 30.3 30.2 0.8 0.7

Sintex Industries Buy 60 79 1,632 4,751 5,189 16.3 16.6 13.6 15.8 4.4 3.8 0.6 0.5 12.9 13.2 0.7 0.6

Siyaram Silk Mills Buy 290 392 272 1,042 1,173 12.4 12.5 66.3 78.5 4.4 3.7 0.9 0.7 21.1 20.8 0.5 0.4

S. Kumars Nationwide Buy 24 45 718 7,279 8,290 21.0 21.0 15.0 17.6 1.6 1.4 0.2 0.2 13.7 13.9 0.7 0.6

SpiceJet Buy 34 40 1,669 5,647 6,513 3.5 6.5 1.9 4.9 17.7 7.0 41.7 6.0 - - 0.4 0.4

TAJ GVK Buy 70 108 439 300 319 35.8 36.2 7.9 9.1 8.9 7.7 1.2 1.1 13.9 14.4 1.8 1.5

Tata Sponge Iron Buy 336 424 518 787 837 16.2 17.5 58.5 66.9 5.8 5.0 0.8 0.7 14.9 15.1 0.3 0.2

TVS Srichakra Buy 307 427 235 1,476 1,660 7.1 8.3 32.5 61.0 9.4 5.0 1.5 1.2 16.7 26.8 0.4 0.4

United Spirits Neutral 825 - 10,784 10,289 11,421 13.5 14.3 31.0 42.9 26.6 19.2 2.1 1.9 8.1 10.3 1.7 1.6

Vesuvius India Accumulate 365 413 740 628 716 16.4 16.5 29.8 34.4 12.2 10.6 2.1 1.8 18.8 18.6 1.0 0.8

Source: Company, Angel Research; Note: *December year end; #September year end; &October year end; Price as on August 10, 2012

www.angelbroking.com

August 13, 2012

Market Outlook

Stock Watch

www.angelbroking.com

August 13, 2012

Market Outlook

Related Documents