Electronic Commerce Business Impacts Project EBIP OECD Crystal Sector Portugal 2001 Confidential

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Electronic Commerce Business Impacts Project

EBIP

OECD

Crystal Sector

Portugal

2001

Confidential

Taux de chômage standardisØs de l�OCDEParis, 5 juillet 2002

OCDE Taux de chômage standardisés-En pourcentage de la population active civile

mai jun jul aou sep oct nov dØc jan fØv mar avr mai

OCDE-Total 6.2 6.3 6.4 6.5 6.5 6.7 6.8 6.8 6.7 6.7 6.7 6.8 6.9

EU15 7.3 7.4 7.4 7.4 7.4 7.4 7.4 7.4 7.5 7.5 7.5 7.5 7.6

Zone euro 8.0 8.0 8.0 8.0 8.0 8.1 8.1 8.1 8.2 8.2 8.2 8.3 8.3

Sept grands 5.7 5.8 5.8 6.0 6.0 6.2 6.4 6.5 6.4 6.3 6.4 6.5 6.5

Canada 7.0 7.1 7.1 7.3 7.2 7.4 7.6 8.0 7.9 7.9 7.7 7.6 7.7

Allemagne 7.7 7.7 7.7 7.7 7.8 7.9 7.9 7.9 8.0 8.0 8.0 8.0 8.1

France 8.6 8.6 8.6 8.6 8.6 8.7 8.8 8.8 8.9 9.0 9.0 9.1 9.2

Italie 9.5 9.5 9.5 9.4 9.3 9.3 9.2 9.1 9.1 9.0 9.0 9.0

Japon 4.9 4.9 5.0 5.0 5.3 5.4 5.4 5.5 5.3 5.3 5.2 5.2 5.4

Royaume-Uni 5.0 5.0 5.0 5.0 5.1 5.1 5.1 5.1 5.0 5.1 5.1

Etats-Unis 4.4 4.6 4.6 4.9 5.0 5.4 5.6 5.8 5.6 5.5 5.7 6.0 5.8

2001 2002

OCDE Taux de chômage standardisés - Variation du taux sur 12 mois

mai jun jul aou sep oct nov dØc jan fØv mar avr mai

OCDE-Total -0.1 0.1 0.2 0.3 0.4 0.6 0.7 0.7 0.5 0.6 0.5 0.6 0.7

EU15 -0.6 -0.4 -0.4 -0.3 -0.2 -0.2 -0.1 -0.1 0.1 0.1 0.1 0.2 0.3

Zone euro -0.5 -0.5 -0.4 -0.4 -0.3 -0.1 0.0 0.0 0.1 0.2 0.2 0.3 0.3

Sept grands 0.0 0.2 0.1 0.3 0.4 0.7 0.8 0.9 0.8 0.7 0.8 0.8 0.8

Canada 0.3 0.4 0.3 0.2 0.3 0.4 0.7 1.2 1.0 1.0 0.7 0.6 0.7

Allemagne -0.1 0.0 0.0 0.0 0.2 0.3 0.3 0.3 0.4 0.4 0.3 0.3 0.4

France -0.8 -0.7 -0.6 -0.5 -0.4 -0.2 0.0 0.1 0.3 0.4 0.4 0.6 0.6

Italie -1.0 -1.0 -0.9 -0.9 -0.8 -0.7 -0.7 -0.8 -0.7 -0.7 -0.6 -0.5

Japon 0.3 0.2 0.3 0.4 0.6 0.7 0.6 0.7 0.5 0.6 0.5 0.4 0.5

Royaume-Uni -0.3 -0.2 -0.2 -0.2 -0.2 -0.1 0.0 0.1 -0.1 0.1 0.2

Etats-Unis 0.3 0.6 0.5 0.8 1.0 1.5 1.6 1.8 1.4 1.3 1.4 1.5 1.4

La zone OCDE comprend 26 pays.Les totaux incluent des estimations du SecrØtariat lorsque les donnØes ne sont pas disponibles.

EBIP Confidential ___________________________________________________________________

Introduction and background

The OECD definition for electronic transaction, approved by the Information,

Computer and Communication Policy Committee in September 1997, is that “an

electronic transaction is the sale or purchase of goods or services, whether between

businesses, households, individuals, governments or other public or private

organisations, conducted over computer-mediated networks. The goods and services

are ordered over those networks, but the payment and the ultimate delivery of the

good or service may be conducted on or off-line”.

The aim of this paper is to analyse e-business in the Portuguese Crystal Sector and

to discuss possible future trends. It is based on work conducted by Cap Gemini Ernst

& Young in September/October 2001, under the supervision of the Portuguese

Communications Institute (ICP), according to OECD methodologies.

E-business in Portugal

In 2000, the penetration rate of Internet in Portugal was 21,1%1.

According to a sample survey based on individuals done by ICP and the Observatory

for Science and Technology (OCT), 8,1%2 of the families in the sample had access to

the Internet at home in 1999. Those were eventually the ones with more interest in

doing electronic commerce.

1 ICP Statistics - The penetration rate is calculated on the basis of the total number of customers of

any type of access, whether paid or free-of-charge, divided by total population. Is based on

information supplied by the ISPs, and may include situations in which a user make use of more than

one ISP.

2 ICP/OCT – Survey on the use of ICT technologies by individuals – 1999. The survey adopted OECD

methodology and was done with a sample of 5998 individuals.

Portugal – Crystal Sector 2

EBIP Confidential ___________________________________________________________________

Regarding electronic commerce, 1,3%3 of the individuals surveyed had already done

online shopping in 1999 and 4,4%4 planned to do it in a year’s time. In 2000, 2,5%5 of

the Portuguese population did online shopping (B2C).

According to surveys done by ICP and IDC6, the main points against Internet and

B2C use by the Portuguese population seem to be costs, education of the population,

information and trust and security. The points for the use of Internet and B2C seem

to be educational/professional reasons/use, access/variety of products and ease.

There are several estimations to Internet penetration in enterprises that differ mainly

in sample construction. For instance, a sample survey on telecommunications use by

enterprises conducted by ICP and OCT7 uses businesses of every size but excludes

some sectors such as Financial Activities and Public Administration. A study

conducted by IDC8 does not include businesses with less than 10 workers but

includes businesses of Financial Activities and Public Administration.

According to ICP and OCT sample survey, 24,1%9 of the businesses had Internet

access in 2000.

3 ICP/OCT – Survey on the use of ICT technologies by individuals – 1999

4 ICP/OCT – Survey on the use of ICT technologies by individuals – 1999

5 IDC – Internet & E-Comm; Enterprises’ Strategy & Use Intentions in Portugal; July 2000

6 ICP/OCT – Survey on the use of ICT technologies by individuals – 1999; IDC – Internet & E-Comm;

Enterprises’ Strategy & Use Intentions in Portugal; July 2000

7 ICP/OCT – Survey on the use of ICT technologies by businesses – 2000. The survey adopted OECD

methodology and was done with a sample of 4922 enterprises.

8 IDC – Internet & E-Comm; Enterprises’ Strategy & Use Intentions in Portugal; July 2000

9 ICP/OCT – Survey on the use of ICT technologies by businesses – 2000.

Portugal – Crystal Sector 3

EBIP Confidential ___________________________________________________________________

According to other sources, 62,7% of Portuguese enterprises already had a website

in 2000 and 30,3% planned to have it until the end of that year10. The reasons stated

for not implementing a website are lack of perceived benefits, costs and high risk.

Regarding electronic commerce done by firms, the implementation of B2C

transactions in the enterprise’s website in 2000 was 14,1%11 (7,6% already done and

6,5% until the end of the year). The implementation of B2B was 8,1%12 (3,8% already

done and 4,3% until the end of the year). The main reasons stated to implement

electronic commerce were improve of consumer service and increase of revenues

and market share.

On the technological side, equipment and communications costs are considered to

be high and there are difficulties in systems and applications integration.

According to some industry and consultancy sources, regulation for the Internet and

e-business is still dispersed and has some omissions. It is also argued that there is a

lack of diffusion and promotion of the e-business and a reduced effectiveness of the

incentives and other kinds support to e-business projects.

At the market level, it is considered that there is a lack of contents, services and

support transaction systems. There are also few users because of transactional

habits, and people are not willing to take risks.

The promotion of e-business should be a joint action of decision-makers,

technological enablers and sector enterprises. Incentives and initiatives that try to

change the mentality of the consumer, install broadband communications and

provide for its liability and security are assumed to be necessary actions for the

development of e-business.

10 IDC – Internet & E-Comm; Enterprises’ Strategy & Use Intentions in Portugal; July 2000

11 IDC – Internet & E-Comm; Enterprises’ Strategy & Use Intentions in Portugal; July 2000

12 IDC – Internet & E-Comm; Enterprises’ Strategy & Use Intentions in Portugal; July 2000

Portugal – Crystal Sector 4

EBIP Confidential ___________________________________________________________________

Value chain analysis

Market structure indicators

Glass industries in Portugal include domestic glass (where crystal is included), flat

glass and packaging glass (bottles). Crystal producing enterprises represent 8% of

the total of glass industry. In 1999, the crystal represented 12% of total business

volume in the glass sector (95 million Euros).

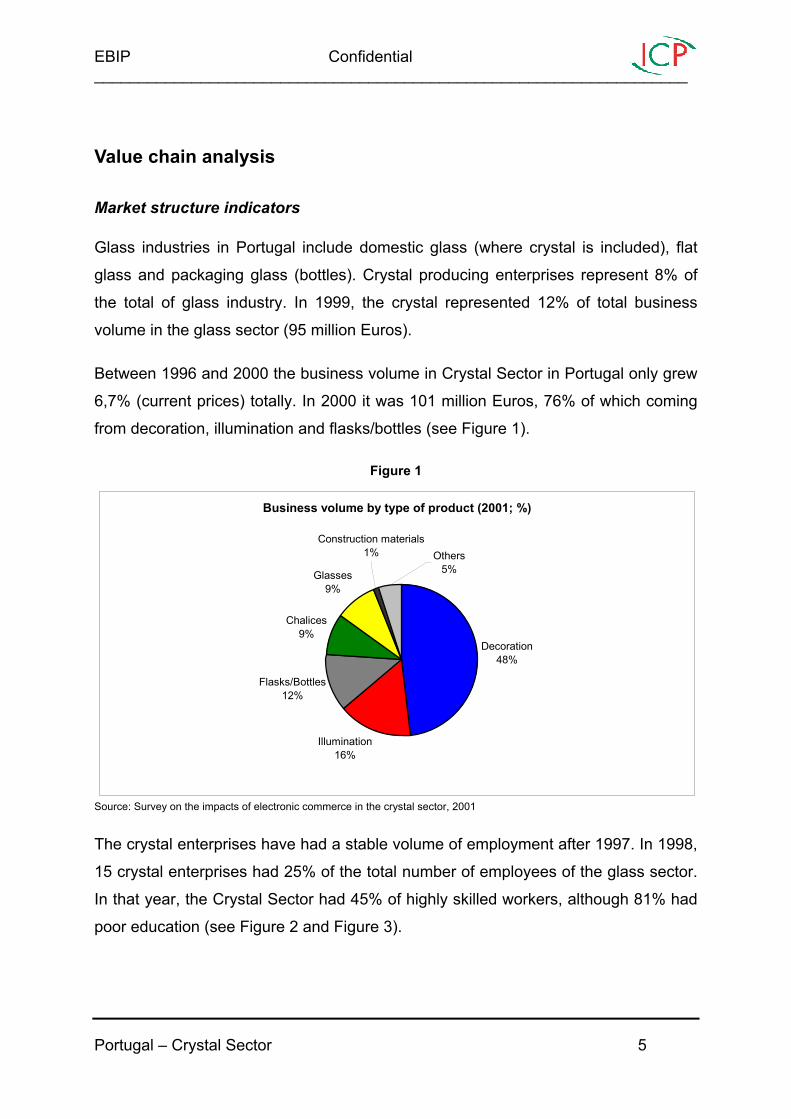

Between 1996 and 2000 the business volume in Crystal Sector in Portugal only grew

6,7% (current prices) totally. In 2000 it was 101 million Euros, 76% of which coming

from decoration, illumination and flasks/bottles (see Figure 1).

Figure 1

Business volume by type of product (2001; %)

Decoration48%

Illumination16%

Flasks/Bottles12%

Chalices9%

Glasses9%

Others5%

Construction materials1%

Source: Survey on the impacts of electronic commerce in the crystal sector, 2001

The crystal enterprises have had a stable volume of employment after 1997. In 1998,

15 crystal enterprises had 25% of the total number of employees of the glass sector.

In that year, the Crystal Sector had 45% of highly skilled workers, although 81% had

poor education (see Figure 2 and Figure 3).

Portugal – Crystal Sector 5

EBIP Confidential ___________________________________________________________________

Figure 2

Human resources qualifications in the crystal subsector(1998; %)

Assistants and apprentices

8,54%

Highly qualified workers45,44%

Medium and high cadres4,82%

Semi and non qualified workers35,46%

Unknown level0,63%

Foremans5,11%

Source: CONVIR, VitroCristal and Banco de Portugal

Figure 3

Habilitation level in the crystal subsector (1998; %)

Highschool15%

Unknown level1%

Licence degree/Graduation

3%

Lower than highschool

81%

Source: CONVIR, VitroCristal and Banco de Portugal

Crystal enterprises have a relatively high degree of internationalisation, larger than

the glass industry as a whole. Atlantis, the larger crystal producer, has international

investments and distribution networks. The enterprise exports to 30 different

countries, has 21 stores in Portugal, one in Barcelona and over 3000 points of sale

around the world.

Portugal – Crystal Sector 6

EBIP Confidential ___________________________________________________________________

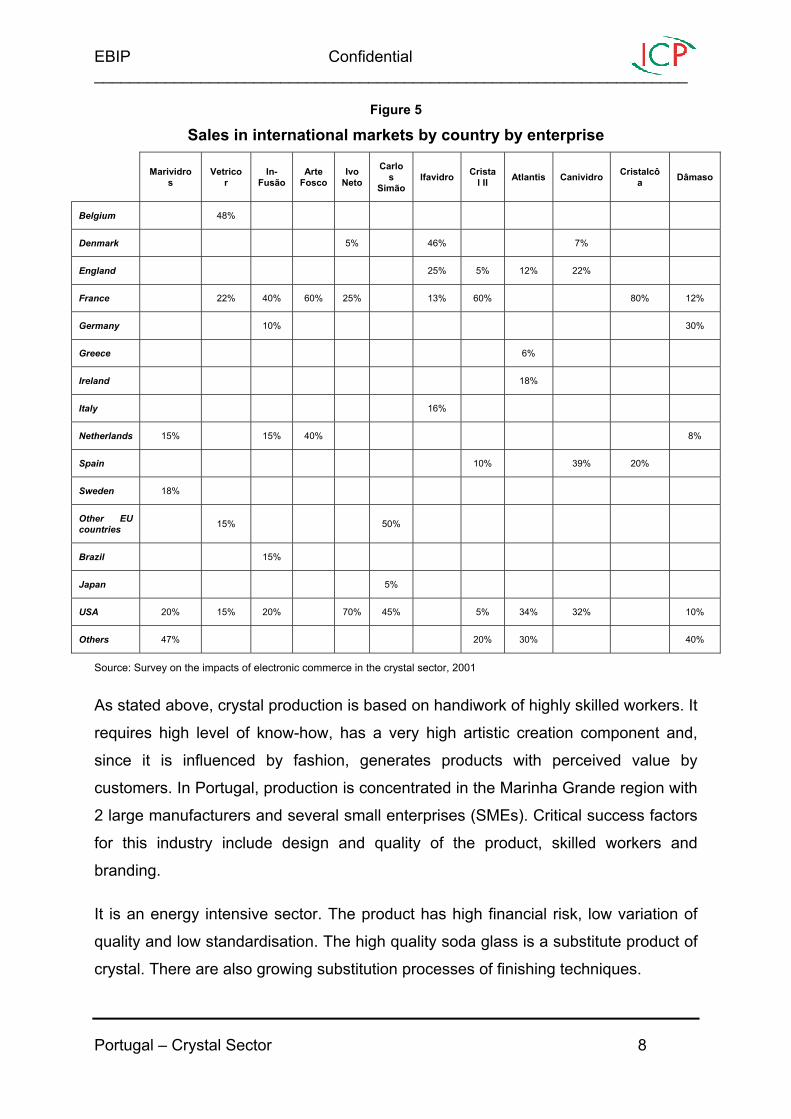

In 1999, exports of the sector were 52% of the total sales (see Figure 4 for evolution

of internal and external market sales). 47% of these exports went to France and the

United States (see Figure 5).

Figure 4

Partition of sales between internal and external market

44%60% 61% 52% 59%

56%40% 39% 48% 41%

0%

20%

40%

60%

80%

100%

1996 1997 1998 1999 2000

Exports Internal market

Source: CONVIR, VitroCristal and Banco de Portugal

Portugal – Crystal Sector 7

EBIP Confidential ___________________________________________________________________

Figure 5

Sales in international markets by country by enterprise

Marividros

Vetricor

In-Fusão

Arte Fosco

Ivo Neto

Carlos

Simão Ifavidro Crista

l II Atlantis Canividro Cristalcôa Dâmaso

Belgium 48%

Denmark 5% 46% 7%

England 25% 5% 12% 22%

France 22% 40% 60% 25% 13% 60% 80% 12%

Germany 10% 30%

Greece 6%

Ireland 18%

Italy 16%

Netherlands 15% 15% 40% 8%

Spain 10% 39% 20%

Sweden 18%

Other EU countries 15% 50%

Brazil 15%

Japan 5%

USA 20% 15% 20% 70% 45% 5% 34% 32% 10%

Others 47% 20% 30% 40%

Source: Survey on the impacts of electronic commerce in the crystal sector, 2001

As stated above, crystal production is based on handiwork of highly skilled workers. It

requires high level of know-how, has a very high artistic creation component and,

since it is influenced by fashion, generates products with perceived value by

customers. In Portugal, production is concentrated in the Marinha Grande region with

2 large manufacturers and several small enterprises (SMEs). Critical success factors

for this industry include design and quality of the product, skilled workers and

branding.

It is an energy intensive sector. The product has high financial risk, low variation of

quality and low standardisation. The high quality soda glass is a substitute product of

crystal. There are also growing substitution processes of finishing techniques.

Portugal – Crystal Sector 8

EBIP Confidential ___________________________________________________________________

Technological changes, mainly in design, are a source of competitive advantages.

However, the time for the competitor to follow the leader is very short.

At the moment, 87% of crystal-producing enterprises are subcontracted. Design and

product development are imposed by customers (wholesalers and other distributors).

For that reason, suppliers, agents and distributors are likely to have stronger

bargaining power than small and medium sized crystal producers. Concerning raw

materials, however, the bargaining power of crystal producers and raw material

suppliers is probably similar.

Crystal is not a first need good and the purchase is dependent on the family’s

available income. Motives for buying are emotional and aesthetical except for some

utility objects. The frequency of buying these items is not high.

Figure 6

Partition of sales between domestic production and imports

51% 56% 59% 60%

49% 44% 41% 40%

0%

20%

40%

60%

80%

100%

1996 1997 1998 1999 2000

Imports Domestic production

not available

Source: CONVIR, VitroCristal and Banco de Portugal

There is a high level of concentration in domestic production. In 2000, two

enterprises of the Crystal Sector were responsible for 85% of the business volume

and 75% of the total number of employees of the analysed enterprises.

In the region of Marinha Grande, competition is very concentrated because there are

several SMEs that sell on that region. Nonetheless, since those SMEs sell their

products to wholesalers, at national level, only major companies sell to the final

Portugal – Crystal Sector 9

EBIP Confidential ___________________________________________________________________

consumer. International competition is strong since imports represent 60% of the

sector sales (see Figure 6 above).

Since high quality soda glass is a substitute product of crystal, producers of this kind

of glass are also competitors to the crystal-producing enterprises.

Regarding international competition, China and Taiwan have low costs strategies and

high levels of production. Nevertheless, the design is very limited and manufacturers

are dependent from the distributors.

East European countries produce automatic crystal and other. The design is

considered good, as well as the quality of products and the prices seem to be

competitive.

As exports are a large percentage of sales (see Figure 4 above), it can be suggested

that domestic firms operate in Portugal and abroad in a strongly competitive

environment.

Organisations in the value chain

The value chain can be seen as a series of activities from planning to retail. Each of

these activities has several identifiable success critical factors as well as different

participants and interested parties (see Figure 7 for value chain).

Portugal – Crystal Sector 10

EBIP Confidential ___________________________________________________________________

Figure 7

Activity description

Success critical factors

Planning/Strategic Marketing

Design and product

developmentProduction Transformation Marketing Wholesale

distribution Retail

• Development of positioning and representative brand image

• New products development

• Internationalisation strategy

• Supply of material and consumables needed for the subsequentfases (raw materials, energy, packaging, moulds, etc.)

• Production from glass mass, crystal and glass parts

• Manual work with or without moulds

• Manual activity with high artistic component

• Transformation done by cutting, tarnishing, painting, others

• Activity seldom performed by enterprises

• Absence of product identity, price, distribution or communication politics

• High negocialpower with manufacturers and transformers

• Activity of distributors is focused to the concept “home” where glass and crystal are present

• High number of small retailers (Ex.: Decoration stores) and big warehouses in Portugal and department stores abroad

• Impose the model and design

• Listen to the market• Keep up with the

tendencies • Perceived image by

the client

• Production articulation with supplying and orderings

• Quality and design of the work

• Energy consumption efficiency

• Production capacity flexibility

• Variety of finishing

• Production capacity flexibility

• Promotion of the product and brand image

• Market niches exploitation

• Parts flexibility related to demand needs

• Available references variety

• Enterprise credibility

• Strong distribution system

• High purchase volume

• Direct contact with market tendencies and client needs

Supplier chain

• New products creation and development

• High artistic component

• Some collaboration between clients, manufacturers and designers

• Innovation and quality image

• Keep up with the tendencies

• Keep up with the market

Final Market

• Convir/IAPMEI• AIC/VitroCristal• Manufacturers• Transformers• Suppliers*• Distributors*

• Suppliers• AIC/VitroCristal*• Manufacturers*

• Manufacturers• Suppliers*• Distributors*

• Transformers• Suppliers*• Distributors*

• AIC/VitroCristal• Leiria and Fátima

Tourism• Manufacturers• Transformers• Distributors*

• Distributors• AIC/VitroCristal*• Manufacturers*• Transformers*

• Distributors• AIC/VitroCristal*• Leiria and Fátima

Tourism*• Manufacturers*• Transformers*

• AIC/VitroCristal• Manufacturers• Transformers• Distributors• Leiria and Fátima

Tourism*

Participants

* Potential participants

Value chain of the Crystal SectorValue chain of the Crystal Sector

Those participants can be aggregated in three groups: individual firms, business

associations and institutions.

1. Individual firms

At the firm level, the value chain aggregates the suppliers, the glass crystal

enterprises and the distributors.

The suppliers provide the necessary materials to produce glass and crystal.

The glass enterprises are divided in producers (25%), transformers (25%) and

producers-transformers (50%). The producers make glass and manual crystal

goods. The transformers make finishing in glass and crystal goods using

tarnishing, painting, cutting and other methods. The producers-transformers make

both things.

Portugal – Crystal Sector 11

EBIP Confidential ___________________________________________________________________

The distributors are the intermediaries between the producers and transformers

and the retailers.

2. Business associations

VitroCristal and AIC (Crystal Industry Association) business associations that

support the development of the Crystal Sector, form and inform enterprises,

promote a brand image and quality of the product and promote the Glass Route.

The Glass Route is a tourist itinerary in the Marinha Grande geographical region

where one can visit, monuments, countryside, costal areas and local glass

production enterprises. The objective is to know more about the art of working

glass and crystal from glassmakers to glass transformers. It also includes a visit

to the glass museum in Marinha Grande.

3. Institutions

The project CONVIR is an Integrated Consolidation Project of Marinha Grande

Glass Region launched by VitroCristal. It aims to promote the glass production

enterprises, create commercial infrastructures and promote cultural and artistic

valorisation, entrepreneurial cooperation and human resources qualification.

IAPMEI is a national Support Institute to the SMEs that can also be important in

subsidising the development of the sector, support the integrated consolidation of

the glass sector in Marinha Grande and develop projects and studies to support

the crystal.

The Leiria and Fátima Tourism promote the tourism and the traditional products of

the region, make the occupation of hotels in the region efficient and promote the

Glass Route.

Analysing all available data, each value chain step suggests several implications to

electronic commerce (B2B and B2C).

Portugal – Crystal Sector 12

EBIP Confidential ___________________________________________________________________

− Planning and Strategic Marketing

Most of the enterprises do not intervene on the planning and strategic marketing

step of the value chain.

The two main enterprises of the sector make strategic marketing by defining and

positioning the brand on the market, internationalising, development of new

exclusive products and defining the way of entry and presence in international

markets.

VitroCristal/AIC promote a joint image of product quality, train and inform the

enterprises in this sector and launched a representative brand (MGlass) jointly

developed by designers and several enterprises of the sector.

The lacking of strategic marketing can represent an initial handicap to a fast

implementation of electronic commerce models.

− Design and product development

There is a general sense for the need of developing product lines, paralleled with

the culture of developing products with the clients in subcontract regimes. The

products must be publicised to the customer in catalogues.

The brand MGlass is a good example of intervention on the design and product

development step of the value chain.

E-business would promote a major use of electronic tools to increase the

cooperation between several participants in the development of a product

(suppliers, industries and clients).

− Supplier chain

Crystal production enterprises conduct their business with a small and fixed

number of suppliers (see Figure 8 and Figure 9).

Portugal – Crystal Sector 13

EBIP Confidential ___________________________________________________________________

Figure 8

Average of players in the transactional cycle

Consultation Selection Negotiatio

n Suppliers

Raw materials 4 2 2 1

Energy 2 2 2 2

General services 3 3 3 1

Moulds 2 1 1 2

Packaging 3 2 1 1

Production consumables 4 2 2 2

Other consumables 0,3 0,3 0,3 1

Others 2 0,3 0,3 2

Source: Survey on the impacts of electronic commerce in the crystal sector, 2001

Figure 9

Market dynamics (suppliers entry and exit from the market)

Suppliers that seldom leave the market

77%

Suppliers that sometimes leave the

market15%

Suppliers that frequently leave the

market8%

Source: Survey on the impacts of electronic commerce in the crystal sector, 2001

In principle, this might allow for an ease of partnerships for e-business due to the

simple negotiation process with existing suppliers. Nevertheless, there is some

resistance shown to the adoption of e-business models, apparently as a result of

the reduced market dynamics and the stability of current relationships.

EBIP Confidential ___________________________________________________________________

Figure 11

Internationalisation of portuguese distribution enterprises(2000; %)

Distribution enterprises with [51%-75%] of international clients

36%

Distribution enterprises with [0%-25%] of

international clients43%

Distribution enterprises with [76%-100%] of international clients

14%

Distribution enterprises with [26%-50%] of international clients

7%

Source: Survey on the impacts of electronic commerce in the crystal sector, 2001

Potentially there are enough clients to allow for development of a B2B model and

the existing internationalisation and moderate market dynamics will not be

obstacles to the adoption of such model.

− Final market

The utility products have a high adaptation potential to the electronic sales

channel.

United States and France have the highest international sales concentration (see

Figure 5 on page 8). This is an advantage for e-business penetration because the

American markets have a tradition of buying from distant suppliers and also have

a high Internet penetration rate.

Dynamics and Trends

There is a slow adoption of electronic transaction technologies in crystal production

enterprises. “E-mail” and the “www” are the most common, adopted by 56% and 38%

of enterprises respectively (see Figure 12). Most of those who have adopted these

Portugal – Crystal Sector 16

EBIP Confidential ___________________________________________________________________

technologies do not have them integrated with internal information systems (see

Figure 13). Information collection and use are the main motivation to adopt electronic

transactions technologies with suppliers and clients.

Figure 12

From the 16 enterprises interviewed:

Transactional technologies

Have already adopted the technology

Plan to adopt the technology

EDI 0 0

Web EDI 1 0

Videotext 0 0

E-mail 9 2

WWW 6 6

Electronic technologies

Extranet 1 0

Fax 16 0 Non electronic technologies Telephone 16 0

Source: Survey on the impacts of electronic commerce in the crystal sector, 2001

Portugal – Crystal Sector 17

EBIP Confidential ___________________________________________________________________

Figure 13

Types of suppliers with whom transactional technologies have been adopted

Types of clients with whom transactional

technologies have been adopted

Production consumables 100% Wholesalers 83%

Other consumables 67% Store chains 67%

Raw materials 67% Specialised retailers 50%

Packaging 33% Department stores 50%

Moulds 33% Decoration chains 33%

Generic services 33% Large distribution channels 17%

Energy 33% Own distribution channels 17%

Source: Survey on the impacts of electronic commerce in the crystal sector, 2001

Transformation enterprises 17%

A possible way of illustrating the enterprise’s electronic commerce integration level is

the one shown in Figure 14.

Figure 14

EE -- b u s i n e s s m o d e l s a d o p t i o nb u s i n e s s m o d e l s a d o p t i o n

E n t e r p r is e in t e g r a t e d inin t e r c o n e c t e d

e n t e r p r is e s n e t w o r k s

E n t e r p r is e in t e g r a t e d inE n t e r p r is e in t e g r a t e d inin t e r c o n e c t e din t e r c o n e c t e d

e n t e r p r is e s n e t w o r k se n t e r p r is e s n e t w o r k s

E le c t r o n ic b u s in e s s a n d p r o c e s s e s

E le c t r o n ic b u s in e s s E le c t r o n ic b u s in e s s a n d p r o c e s s e sa n d p r o c e s s e s

E le c t r o n ic C o m m e r c eE le c t r o n ic E le c t r o n ic C o m m e r c eC o m m e r c e

In s t it u t io n a l

L e v e l o f C o m p le x ity

Pote

ntia

l Gai

n

I

I I

I I I

IV

A t la n tis

I vi m a

C r is a l

D â m a s o

I f a vid r o

I n - f u s ã o

V ic r im a g

Source: Survey on the impacts of electronic commerce in the crystal sector, 2001

Portugal – Crystal Sector 18

EBIP Confidential ___________________________________________________________________

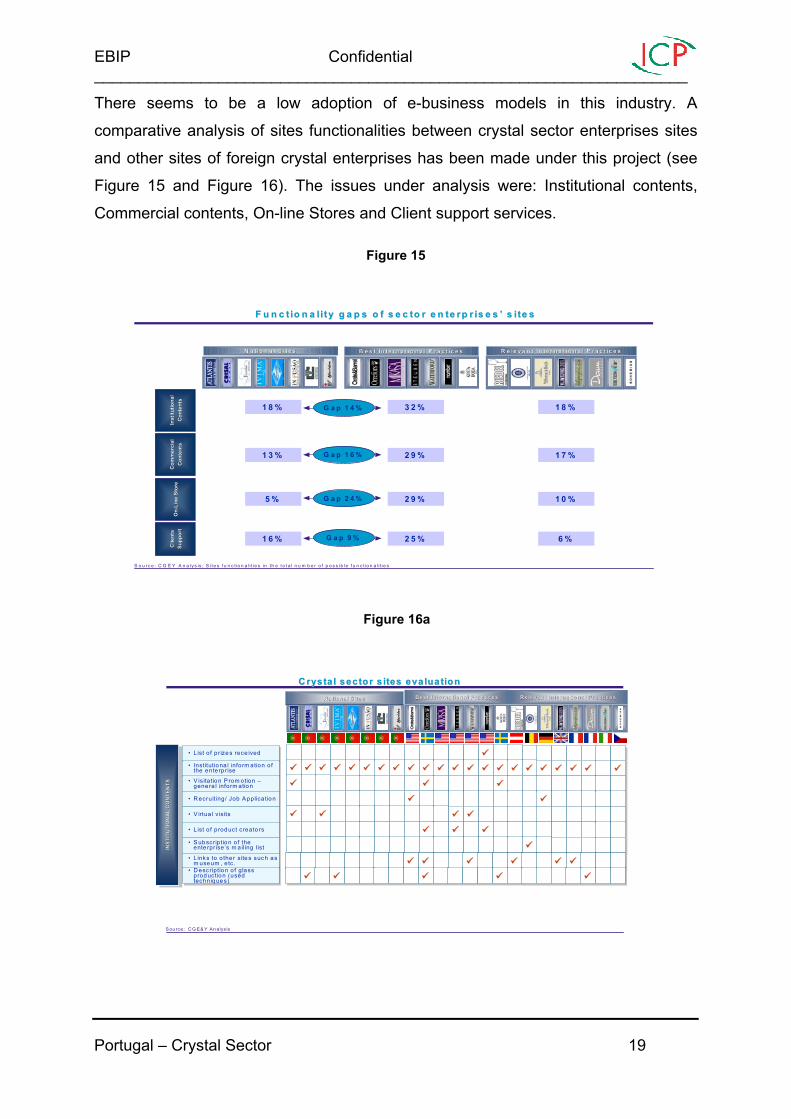

There seems to be a low adoption of e-business models in this industry. A

comparative analysis of sites functionalities between crystal sector enterprises sites

and other sites of foreign crystal enterprises has been made under this project (see

Figure 15 and Figure 16). The issues under analysis were: Institutional contents,

Commercial contents, On-line Stores and Client support services.

Figure 15

Inst

itutio

nal

Inst

itutio

nal

Con

tent

sC

onte

nts

Com

mer

cial

C

omm

erci

al

Con

tent

sC

onte

nts

On

On --

Line

Sto

reLi

ne S

tore

Clie

nts

Clie

nts

Supp

ort

Supp

ort

B e s t In te r n a ti o n a l P r a c tic e sB e s t In te r n a t io n a l P r a c t ic e s R e le v a n t In te r n a t io n a l P r a c tic e sR e le v a n t In te r n a t io n a l P r a c t ic e s

F u n c t io n a l i t y g a p s o f s e c to r e n te r p r is e s ’ s i te sF u n c t io n a l i t y g a p s o f s e c to r e n te r p r is e s ’ s i te s

S o u r c e : C G E Y A n a ly s is ; S it e s f u n c t io n a lit ie s in th e t o t a l n u m b e r o f p o s s ib le f u n c t io n a lit ie s

1 8 % 3 2 % 1 8 %

1 3 % 2 9 % 1 7 %

5 % 2 9 % 1 0 %

1 6 % 2 5 % 6 %

N a tio n a l S ite s N a tio n a l S ite s

G a p 1 4 %

G a p 1 6 %

G a p 2 4 %

G a p 9 %

Figure 16a

B est Interna tio na l P ra ctice sB est Interna tio na l Pra ctice s R ele va nt Interna tio na l P ra ctice sR ele va nt Interna tio na l P ra ctice s

INST

ITUT

ION

AL C

ON

TENT

SIN

STIT

UTI

ONA

L CO

NTE

NTS

INST

ITUT

ION

AL C

ON

TEN

TS

• L ist of prize s rece ived• L ist o f prize s rece ived

• Institutiona l inform atio n of the e nte rprise

• Inst itutio na l inform ation o f the ente rprise

• V is ita tio n P rom otio n –gene ra l inform ation

• V is itat io n P rom otion –genera l inform atio n

• R ecru iting/ Job A pplicatio n• R ecruiting/ Job Applicat io n

• V irtua l v is its• V irtua l v is its

• L ist of product creato rs• L ist o f prod uct creato rs

• S ub scrip tion of the ente rprise’s m a iling list

• S ub scrip tio n o f the ente rprise’s m a iling list

• L inks to o the r s ite s suc h a s m use um , etc.

• L inks to o the r s ite s such as m useum , e tc.

• D esc rip tion of g la ss productio n (used techniques)

• D esc riptio n o f glass prod uctio n (used techniq ue s)

S ource: C G E& Y An alys is

N a tiona l S ite sN a tiona l S ite s

C rysta l sector s ites evaluationC rysta l sector s ites eva luation

Portugal – Crystal Sector 19

EBIP Confidential ___________________________________________________________________

Figure 16b

CO

MM

ERC

IAL

CO

NTEN

TSC

OM

MER

CIA

L C

ONT

ENTS

CO

MM

ERC

IAL

CO

NTEN

TS

• Product information (High level)

• Product information (High level)

• Products catalogue (detailed)• Products catalogue (detailed)

• Search of products• Search of products

• Photos of collection pieces, new pieces, etc.

• Photos of collection pieces, new pieces, etc.

• Books list• Books list

• Distributors list• Distributors list

• Addresses and stores (contacts and maps)

• Addresses and stores (contacts and maps)

• Advertising campaigns• Advertising campaigns

• Calendar of exhibitions/fairs/wine tasting

• Calendar of exhibitions/fairs/wine tasting

• List with gift suggestions• List with gift suggestions

• Forms for pieces sales• Forms for pieces sales

• Request for catalogues, brochures

• Request for catalogues, brochures

• Customised gifts• Customised gifts

• Product commercialisation (Ex.: furniture)

• Product commercialisation (Ex.: furniture)

Source: CGE&Y Analysis

Melhores práticas InternacionaisMelhores práticas Internacionais Relevant International PracticesRelevant International PracticesBest International PracticesBest International PracticesNational SitesNational Sites

Crystal sector sites evaluation (cont.)Crystal sector sites evaluation (cont.)

Figure 16c

Source: CGE&Y Analysis

CO

MM

ERC

IAL

CO

NTEN

TS (c

ont.)

CO

MM

ERC

IAL

CO

MM

ERC

IAL

CO

NTEN

TS (c

ont.)

CO

NTEN

TS (c

ont.)

ON

-LIN

E ST

OR

EO

NO

N -- L

INE

STO

RE

LIN

E ST

OR

E

• Wedding gifts lists, etc.• Wedding gifts lists, etc.

• Information on delivery services

• Information on delivery services

• Creation of an account (become a member)

• Creation of an account (become a member)

• Promotion of bridal events• Promotion of bridal events

• On-line shopping• On-line shopping

• Orderings visualisation• Orderings visualisation

• Shipping of purchase offers coupons

• Shipping of purchase offers coupons

• Enterprise’s credit card• Enterprise’s credit card

• On-line shopping using instructions

• On-line shopping using instructions

• FAQ’s• FAQ’s

• Track of ordered products• Track of ordered products

• Comments/Suggestions• Comments/Suggestions

• Newsletter• Newsletter

CLI

ENTS

SU

PPO

RT

CLI

ENTS

SU

PPO

RT

CLI

ENTS

SU

PPO

RT

Melhores práticas InternacionaisMelhores práticas Internacionais Relevant International PracticesRelevant International PracticesBest International PracticesBest International PracticesNational SitesNational Sites

Crystal sector sites evaluation (cont.)Crystal sector sites evaluation (cont.)

Portugal – Crystal Sector 20

EBIP Confidential ___________________________________________________________________

According to this analysis, it may be suggested that sites of Portuguese crystal

production enterprises may have several gaps concerning commercial content,

transactional capabilities and quality of the site itself (see Figure 15 and Figure 16).

The usability variables of the sites of crystal producing enterprises were also

analysed (see Figure 17). The usability variables considered were Information

Architecture, Design, Brand Impact, Marketing, Functionality and Content.

Figure 17 Inf

ormati

on

Infor

mation

Archit

ectur

e

Archit

ectur

e

Design

Design

Brand I

mpact

Brand I

mpact

Marketi

ng

Marketi

ng

Functi

onality

Functi

onality

2 2 2 2 2

2 3 2 2 2

2 3 2 2 2

3 2 2 3 2

1 1 1 1 1

2 2 2 2 2

3 2 2 2 2

2 2 2 2 2

Source: CGE&Y Analysis

Content

Content

2

2

2

2

1

2

2

2

Key:1 – Low quality2 – Low differentiation and attractive to users3 – Attractive with differentiated value proposal to users

Key:1 – Low quality2 – Low differentiation and attractive to users3 – Attractive with differentiated value proposal to users

Crystal sector sites evaluation Crystal sector sites evaluation –– Usability variablesUsability variables

From Figure 17 above it can be suggested that there is room for improvement in

national crystal sector sites.

Enterprises say that in order to adopt e-business they have to adapt business

processes, educate their employees, secure their systems and add quality and

functionality to the Website.

The suppliers and distributors that could push the e-business adoption are inactive,

probably because the way processes are traditionally done is good and they do not

Portugal – Crystal Sector 21

EBIP Confidential ___________________________________________________________________

see a need for change. On the other hand, since the crystal product is not very easy

to sell on a model B2C there are no reasons to innovate and the inactivity remains.

The main impacts and benefits from the “e” stated by the interviewed enterprises are

the growth of sales and efficiency in relations with partners. Other indicated impacts

were publicity (indicated by 94%), ordering processes (69% of the enterprises),

market expansion (94%), product differentiation (94%) and expansion (94%).

Crystal enterprises do not have many expectations regarding process innovation. As

for the value chain they expect to enlarge the number of clients and use a new

distribution channel. Only two enterprises were able to identify real impacts on

transaction support and relational and product innovation.

Crossing the two dimensions (transactional and trade), the main expected impacts

are relational innovation, transaction preparation and production support (see Figure

18).

Figure 18

Synthesis matrix of impacts expectations on Synthesis matrix of impacts expectations on transactional level versus organizational leveltransactional level versus organizational level

Diversification

Differentiation

Customisation

Anticipation

Studies

Logistics

Production chain

Coordination

Expansion

Segmentation

Trust

Loyalty

Expe

cted

impa

cts

on th

e bu

sine

ssPr

oduc

t In

nova

tion

Rela

tiona

l In

nova

tion

T ransaction preparation Transaction com pletion Production support

Expected im pacts on transaction process

Proc

ess

Inno

vatio

n

Source: Questionnaire on the Impact of Electronic Commerce in the Crystal Sector, 2001

Advertising Catalogues Inform ation Services Negotiation Ordering Billing and

Payment Finance DeliveryCapture of

Transaction Inform ation

Inform ation M anagem ent

M arket Analysis

M arket Development

9

9

1

6

1

6

2

3

1

4

2

4

2

1

2

1

3

4

3

4 4

4

1

1

3

5

1

2

1

4

7

13

5050 2222 4343

5959

2424

3232

Portugal – Crystal Sector 22

EBIP Confidential ___________________________________________________________________

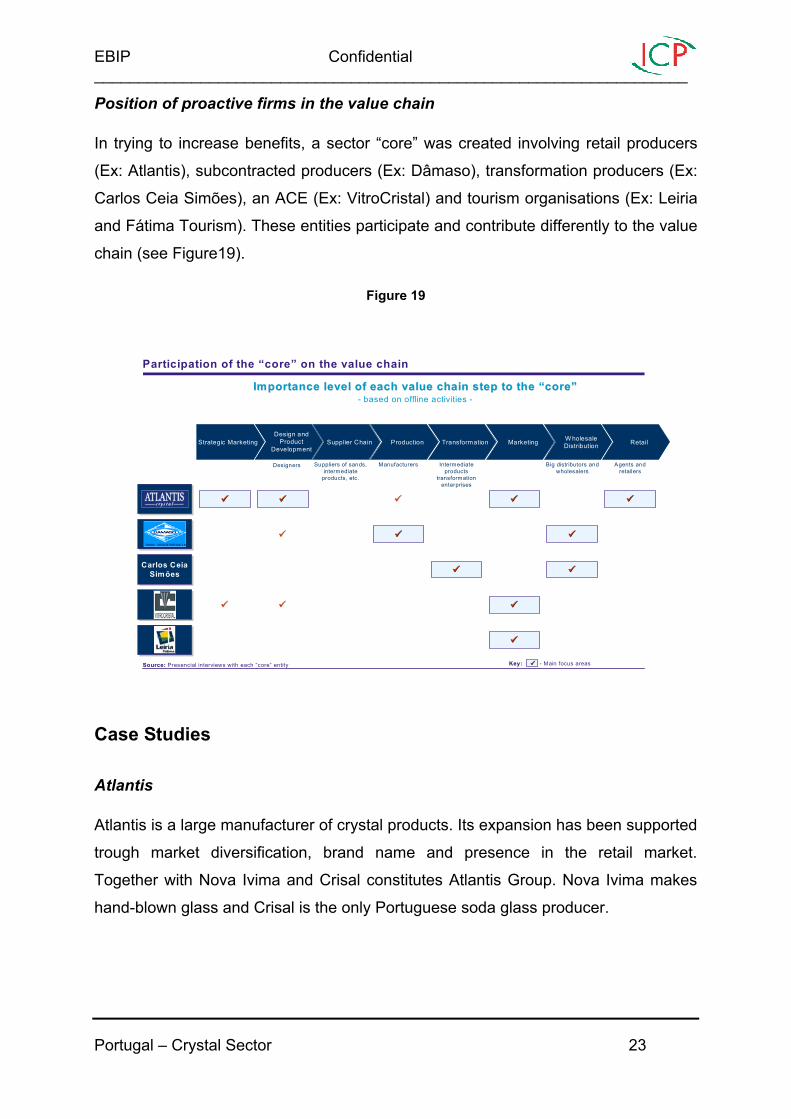

Position of proactive firms in the value chain

In trying to increase benefits, a sector “core” was created involving retail producers

(Ex: Atlantis), subcontracted producers (Ex: Dâmaso), transformation producers (Ex:

Carlos Ceia Simões), an ACE (Ex: VitroCristal) and tourism organisations (Ex: Leiria

and Fátima Tourism). These entities participate and contribute differently to the value

chain (see Figure19).

Figure 19

Participation of the “core” on the value chain

Importance level of each value chain step to the “core” Importance level of each value chain step to the “core” - based on offline activities -

Carlos Ceia Simões

Carlos Ceia Simões

Source:Source: Presencial interviews with each “core” entity

Suppliers of sands, intermediate

products, etc.

Designers Manufacturers Intermediate products

transformation enterprises

Big distributors and wholesalers

Agents and retailers

Key:Key: - Main focus areas

Supplier ChainStrategic MarketingDesign and

Product Development

Production Transformation Marketing W holesale Distribution Retail

Case Studies

Atlantis

Atlantis is a large manufacturer of crystal products. Its expansion has been supported

trough market diversification, brand name and presence in the retail market.

Together with Nova Ivima and Crisal constitutes Atlantis Group. Nova Ivima makes

hand-blown glass and Crisal is the only Portuguese soda glass producer.

Portugal – Crystal Sector 23

EBIP Confidential ___________________________________________________________________

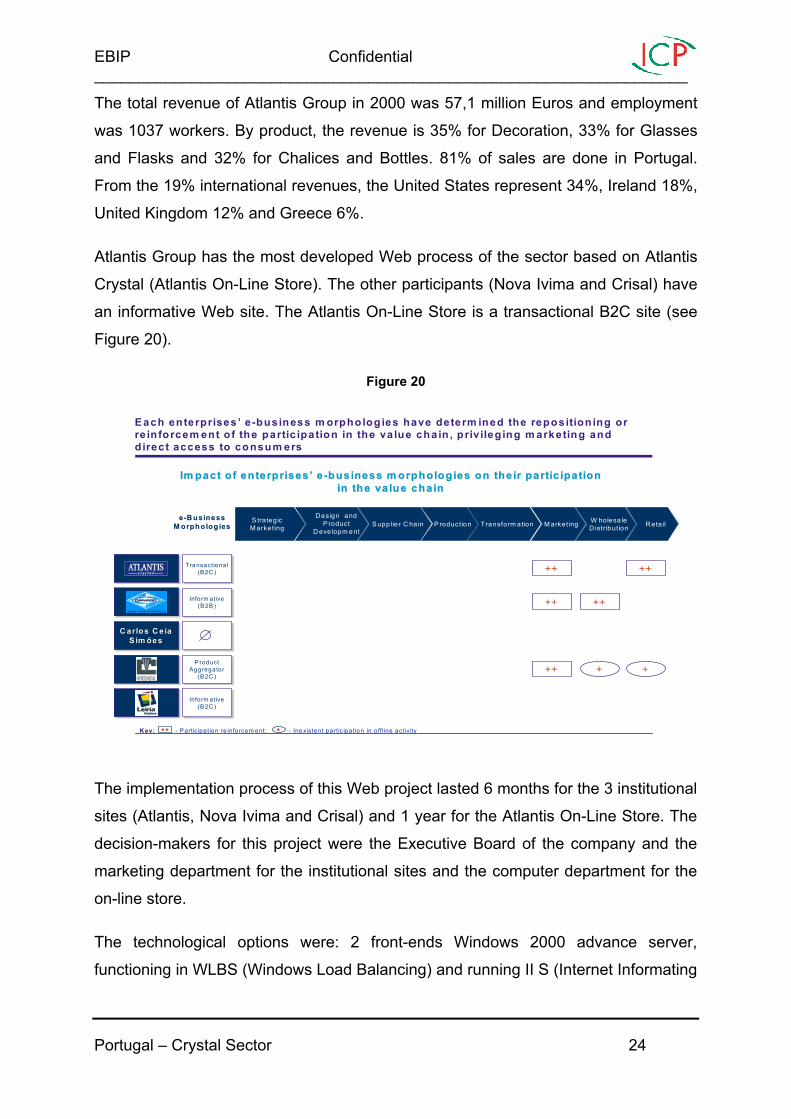

The total revenue of Atlantis Group in 2000 was 57,1 million Euros and employment

was 1037 workers. By product, the revenue is 35% for Decoration, 33% for Glasses

and Flasks and 32% for Chalices and Bottles. 81% of sales are done in Portugal.

From the 19% international revenues, the United States represent 34%, Ireland 18%,

United Kingdom 12% and Greece 6%.

Atlantis Group has the most developed Web process of the sector based on Atlantis

Crystal (Atlantis On-Line Store). The other participants (Nova Ivima and Crisal) have

an informative Web site. The Atlantis On-Line Store is a transactional B2C site (see

Figure 20).

Figure 20

E ach enterprises ’ e -business m orpholog ies have determ ined the reposition ing or re in forcem ent of the partic ipation in the va lue chain , privileg ing m arketing and d irect access to consum ers

Im pact of enterprises ’ eIm pact of enterprises ’ e --business m orphologies on the ir partic ipation business m orphologies on the ir partic ipation in the va lue chainin the va lue chain

C arlos C eia S im ões

C arlosC arlos C eia C e ia S im õesS im ões

S upp lier C ha inS trategic M arketing

D esig n a nd P roduct

D eve lopm entP roduction Transform ation M arketing W holesa le

D istr ibution R eta il

++++

++++

++++

++

++++

++++

++

K ey:K ey: - Partic ipatio n re inforcem ent; - Ine xiste nt partic ipatio n in o ff line activ ity++++ ++

ee--B usiness B usiness M orpho log iesM orphologies

Tra nsactio na l (B2C )

Tra nsactio na l (B2C )

P roduct Aggregator

(B2C )

P roduct Aggregator

(B2C )

Inform ative (B2C )

Inform ative (B2C )

Inform ative (B2B)

Inform ative (B2B)

The implementation process of this Web project lasted 6 months for the 3 institutional

sites (Atlantis, Nova Ivima and Crisal) and 1 year for the Atlantis On-Line Store. The

decision-makers for this project were the Executive Board of the company and the

marketing department for the institutional sites and the computer department for the

on-line store.

The technological options were: 2 front-ends Windows 2000 advance server,

functioning in WLBS (Windows Load Balancing) and running II S (Internet Informating

Portugal – Crystal Sector 24

EBIP Confidential ___________________________________________________________________

5) with 3 site servers. The database runs in 2 back-ends, in Windows 2000, running

SQL 2000 in cluster. The on-line store has broadband. The investments already done

until now in Communications, Development and Maintenance were 3000 thousand

escudos (14,96 thousand Euros) for institutional sites and 18000 thousand escudos

(89,78 thousand Euros) for on-line store.

A Baan System does the application systems integration in the back office

compatible with the electronic platform and Netgest, a front-end invoice program that

had a licence cost of 200 thousand escudos (1 thousand Euros).

Dâmaso

Dâmaso is a producer of glass and construction material focused on production “by

order” and is strongly dependent from distributors and agents. Currently Dâmaso is

betting on design and product innovation.

Total revenue in 2000 was 11 million Euros and employment was 324 workers. By

product, the revenue is 85% for Decoration and 15% for Construction Material. 15%

of sales are done in Portugal. From the 85% international sales, Germany represent

30%, France 12%, United States 10% and the Netherlands 8%.

Initially, Dâmaso only wanted to be present on the Internet but now other alternatives

are under development. It has an informative B2B site, where information to business

clients is provided (see Figure 20 above).

The implementation process of the website lasted 3 months, after a one-month

decision process. This implementation was needed due to the representativeness

and importance of the company.

This project was totally financed by PEDIP II and CPD. PEDIP II was an Incentives

Program to the Portuguese Industry that aimed to support strategic development of

science and technology institutions, R&D projects from industry, entrepreneurship

and academia-industry partnerships. CPD is a Portuguese Design Centre whose

Portugal – Crystal Sector 25

EBIP Confidential ___________________________________________________________________

mission is to act as an intermediary between the business and corporate world and

the design services it requires, to assist design professionals in finding career

openings and to bring the world of design to a wider, more active audience.

The application systems integration is done on a UNIX platform with totally integrated

MUI software with several supporting modules to the needs of the company. The

implementation process lasted 1 year. The initial investment was 6000 thousand

escudos (29,93 thousand Euros).

Carlos Ceia Simões

Carlos Ceia Simões is a transformer focused on acquiring intermediate products and

adding value to them trough design. Produces “by order” and is also dependent from

distributors. Its main activity transformation but occasionally does glass production.

The total revenue in 2000 was 1462,8 million Euros and 29 workers were employed.

By product, the revenue is 30% for Chalices, 30% for Glasses, 10% for Flasks and

Bottles and 30% for others. 5% of sales are done in Portugal. From the 95%

international sales, the European Union represents 50%, United States 45% and

Japan 5%.

Carlos Ceia Simões is currently finishing the process of installing an Intranet with

external electronic mail but is already interested in the development of a website.

The implementation process of the Intranet is due immediately. The decision process

lasted 3 days and the reasons for implementing this solution were the needs of the

company and the reduced cost.

The technological option was Netpower from Telepac. Initial investment was 5000

escudos (24,94 Euros) and maintenance costs 3000 escudos (14,96 Euros) per

month. The project began in July 2000 and is still running.

Portugal – Crystal Sector 26

EBIP Confidential ___________________________________________________________________

The integration of application systems is done by a platform with PHC 4.0 computer

support, compatible with a Web platform. This platform enables the management of

buys, billing, stock management, treasury, accounting and wages.

The integration of technological systems is foreseen to January 2002 and this

implementation process will last 1 year.

This solution is going to be implemented because it is an open solution with

changeable parameters and there are good financial conditions to do it. The

investment already done is 7000 thousand escudos (34,92 thousand Euros).

VitroCristal

VitroCristal is an ACE (Businesses Complementary Group) that aims to promote and

develop the sector, supporting enterprises in marketing, obtaining funding and

promoting sector projects (Ex: Internationalisation).

Its mission is to implement in Portugal and internationally the glass brand of Marinha

Grande. Its objectives are to promote an international brand that represents the

quality of glass products from Marinha Grande and to form and inform, particularly in

what concerns innovation and competition, the sector enterprises.

Currently, they are developing a strategic action plan in order to consolidate the glass

industrial cluster of Marinha Grande in the next two years, in all production phases,

including design, decoration/finishing and industrial workmanship. Still, they are trying

to consolidate a brand of the sector (MGlass).

Their projects are to explore the MGlass brand in international markets, promote

internal and external initiatives of cultural and tourist valorisation of the Glass Region,

develop the quality image of the MGlass brand and improve the enterprises

technologically and environmentally.

The enterprise has a product aggregation B2C site that aims to promote the

industry’s products and the MGlass brand in particular (see Figure 20 above).

Portugal – Crystal Sector 27

EBIP Confidential ___________________________________________________________________

Leiria and Fátima Tourism

The Leiria and Fátima Tourism promotes the Glass Region and creates some

prestige for the region brands by associating them with the tradition and quality of

manual crystal.

Its mission is to push national and international tourism trough an integrated offer

based on attractive factors of the region, promoting adequate physical and

organisational structures and communication actions in an integrated and coherent

manner. The objectives are positioning tourism has one of the major incentives to the

economic development of the region, increase the notoriety of the tourist offer, seek

traditional products of the region and promote the Glass Route jointly with

VitroCristal/ACE.

Currently is increasing the occupation rate of hotels in the region and providing

tourists the adequate information.

The future projects are to turn the hotel reservation process more efficient by

centralising an electronic support (Internet) and increase the satisfaction level of

tourists by providing adequate information to different market targets.

It has an informative B2C site on the offers of the tourism region, including crystal

products (see Figure 20 above).

Exploratory Scenarios

On the section “Position of proactive firms in the value chain” it was mentioned the

creation of a sector “core” with retail producers, subcontracted producers,

transformation producers, an ACE and tourism.

This “core” should promote the modernisation of industry actors upstream and

downstream, develop a joint plan to facilitate the access to incentives, integrate

Portugal – Crystal Sector 28

EBIP Confidential ___________________________________________________________________

actors who will be the role models to small enterprises and/or enterprises with less

developed organisational cultures, congregate efforts to promote the Glass Region

and maximise the efficiency and synergy in the industry trough e-business models.

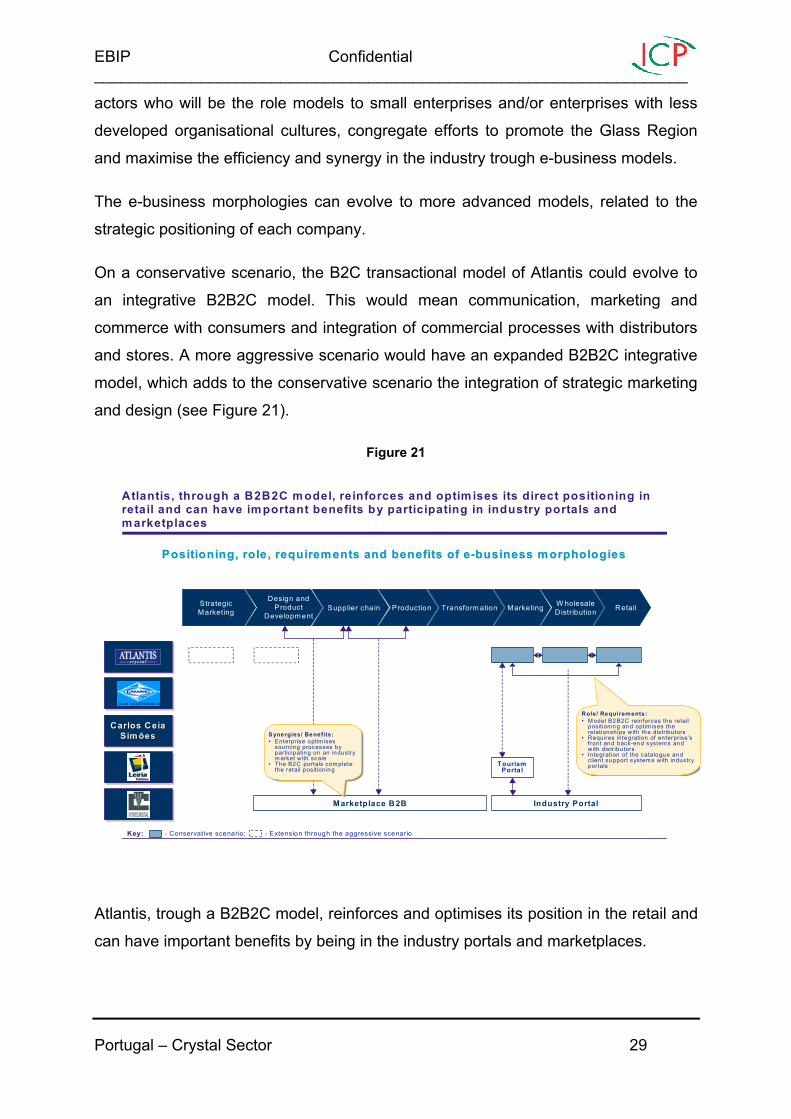

The e-business morphologies can evolve to more advanced models, related to the

strategic positioning of each company.

On a conservative scenario, the B2C transactional model of Atlantis could evolve to

an integrative B2B2C model. This would mean communication, marketing and

commerce with consumers and integration of commercial processes with distributors

and stores. A more aggressive scenario would have an expanded B2B2C integrative

model, which adds to the conservative scenario the integration of strategic marketing

and design (see Figure 21).

Figure 21

Key:Key: - Conservative scenario; - Extens ion through the aggressive scenario

Atlantis, through a B2B2C m odel, reinforces and optim ises its direct positioning in retail and can have im portant benefits by participating in industry portals and m arketplaces

Positioning, role, requirem ents and benefits of ePositioning, role, requirem ents and benefits of e --business m orphologiesbusiness m orphologies

Supplier cha inStrategic Marketing

Design and Product

Developm entProduction Transform ation Marketing W holesale

Distribution Retail

Carlos Ceia Sim ões

CarlosCarlos Ceia Ceia Sim õesSim ões

Marketplace B 2B

Tourism Porta l

Industry Portal

Synergies/ Benefits:• Enterprise optim ises

sourcing processes by participating on an industry m arket with scale

• The B2C portals com plete the retail positioning

Synergies/ Benefits:• Enterprise optim ises

sourcing processes by participating on an industry m arket with scale

• The B2C portals com plete the retail positioning

Role/ Requirements:• M odel B2B2C reinforces the retail

positioning and optim ises the relationships with the distributors

• Requires integration of enterprise’s front and back-en d system s and with distributors

• Integration of the catalogue and client support system s with industry portals

Role/ Requirements:• M odel B2B2C reinforces the retail

positioning an d optim ises the relationships with the distributors

• Requires integration of enterprise’s front and back-end system s and with distributors

• Integration of the catalogue and client support system s with industry portals

Atlantis, trough a B2B2C model, reinforces and optimises its position in the retail and

can have important benefits by being in the industry portals and marketplaces.

Portugal – Crystal Sector 29

EBIP Confidential ___________________________________________________________________

Dâmaso, which now has an informative B2B model, could evolve to an integrative

B2B model downstream, on a conservative scenario. This means integration of

commercial processes with distributors. On a more aggressive scenario, it might

evolve to an integrative B2B2C model, which are communication, marketing and

commerce with consumers and integration of commercial processes with distributors

(see Figure 22).

Figure 22

Dâmaso, by developing an integrative B2B model downstream optimises its relation with distributors and is able to support a market approximation strategy on the industry B2C portals and benefit from e-Procurement

Supplier ChainStrategic Marketing

Design and Product

DevelopmentProduction Transformation Marketing Wholesale

Distribution Retail

Carlos Ceia Simões

CarlosCarlos Ceia Ceia SimõesSimões

Marketplace B2B

Tourism Portal

Industry Portal

Synergies/ Benefits:• Enterprise optimises sourcing processes by

participating in an industry scale market • B2C portals complete the retail positioning • B2C portals allow greater brand visibility on the

market, support on direct approximation to consumers and support to the market distribution network

Synergies/ Benefits:• Enterprise optimises sourcing processes by

participating in an industry scale market • B2C portals complete the retail positioning • B2C portals allow greater brand visibility on the

market, support on direct approximation to consumers and support to the market distribution network

Role/ Requirements:

• Integrative B2B model downstream optimises the relationship with distributors, critical factor to the activity;

• Requires the creation of an electronic catalogue and the integration of enterprise’s front and back-end systems and with distributors

• Integration of the catalogue and customer support services with the industry portals

Role/ Requirements:

• Integrative B2B model downstream optimises the relationship with distributors, critical factor to the activity;

• Requires the creation of an electronic catalogue and the integration of enterprise’s front and back-end systems and with distributors

• Integration of the catalogue and customer support services with the industry portals

Positioning, role, requirements and benefits of ePositioning, role, requirements and benefits of e--business morphologiesbusiness morphologies

Key:Key: - Conservative Scenario; - Extension through the aggressive scenario

Dâmaso, by developing an integration B2B model downstream optimises its relation

with the distributors, being able to support an approximation strategy to the markets

using B2C portals from the industry and benefit from the e-Procurement.

The conservative evolution of Carlos Ceia Simões can be an integrative B2B model

upstream, which is the integration of procurement processes and supplying

upstream. The aggressive scenario would be an integrative B2B upstream and

Portugal – Crystal Sector 30

EBIP Confidential ___________________________________________________________________

downstream, integrating procurement processes and supplying upstream with

distributors downstream (see Figure 23).

Figure 23

Carlos Ceia Simões, through an integrative B2B model upstream optimises and reinforces the control over mould suppliers and designers, having benefits from the industry portals

Supplier ChainStrategic Marketing

Design and Product

DevelopmentProduction Transformation Marketing Wholesale

Distribution Retail

Carlos Ceia Simões

CarlosCarlos Ceia Ceia SimõesSimões

Marketplace B2B

Tourism Portal

Industry Portal

Synergies/ Benefits:• Enterprise optimises sourcing processes by

participating on an industry scale market • B2C portals complete the retail positioning • B2C portals allow greater brand/product

visibility in the market and distribution network support in accessing the market

Synergies/ Benefits:• Enterprise optimises sourcing processes by

participating on an industry scale market • B2C portals complete the retail positioning • B2C portals allow greater brand/product

visibility in the market and distribution network support in accessing the market

Role/ Requirements:

• Integrative B2B model upstream optimises the relationship with mould suppliers and designers critical to the enterprise’s transformation activity

• Requires the catalogues creation and systems integration with suppliers (Ex.: CAD drawings transference)

Role/ Requirements:

• Integrative B2B model upstream optimises the relationship with mould suppliers and designers critical to the enterprise’s transformation activity

• Requires the catalogues creation and systems integration with suppliers (Ex.: CAD drawings transference)

(external)

Positioning, role, requirements and benefits from ePositioning, role, requirements and benefits from e--business morphologiesbusiness morphologies

Key:Key: - Conservative scenario; - Extension through the aggressive scenario

Carlos Ceia Simões, trough a B2B integrated model upstream optimises and

reinforces the control over the mould suppliers and designers.

VitroCristal can evolve from product aggregator (non transactional B2C) to business

aggregator (e-procurement) and product aggregator (transactional B2C) (see Figure

24).

Leiria and Fátima Tourism have now an informative B2C model. It can develop an

integrative B2B2C model, which are communication, marketing and commerce with

consumers and integration of processes with distributors and retailers (see Figure

24).

Portugal – Crystal Sector 31

EBIP Confidential ___________________________________________________________________

Figure 24

VitroCristal and Leiria and Fátima Tourism are the ones that should create the e-procurement and B2C portals with the necessary size to obtain return

Supplier ChainStrategic Marketing

Design and Product

DevelopmentProduction Transformation Marketing Wholesale

Distribution Retail

Carlos Ceia Simões

CarlosCarlos Ceia Ceia SimõesSimões

Marketplace B2B

Tourism Portal

Industry Portal

Role/ Requirements:

• These portals would aggregate all industry’s enterprises, assuring the size of operations and the investment optimisation;

• Require the enterprises massive participation/adherence and the integration of their back-office systems with the portals’ e-business solutions

Role/ Requirements:

• These portals would aggregate all industry’s enterprises, assuring the size of operations and the investment optimisation;

• Require the enterprises massive participation/adherence and the integration of their back-office systems with the portals’ e-business solutions

Positioning, role, requirements and benefits from ePositioning, role, requirements and benefits from e--business morphologiesbusiness morphologies

Key:Key: - Conservative scenario; - Extension through the aggressive scenario

VitroCristal and the Leiria and Fátima Tourism are the ones that should create e-

Procurement and B2C portals with the necessary size to have return.

Conclusion

Gathering all, one can easily conclude that crystal producing enterprises in Portugal

still have a way to go in the implementation of e-business processes. B2B

relationships seem to be propitious in this sector. That is why mentalities of all value

chain intervenients must evolve to “e” and implement electronic transaction

technologies. A B2C model is less viable because of enterprises’ unawareness of the

market.

Portugal – Crystal Sector 32

EBIP Confidential ___________________________________________________________________

Enterprises should plan ahead and implement marketing strategies. E-business can

promote cooperation between several participants in the development of a product

(suppliers, industries and clients).

By now, there are not a large enough number of “e” companies to say that we have

an electronic market in this industry.

Portugal – Crystal Sector 33

Related Documents

![Tech Buisness[1]](https://static.cupdf.com/doc/110x72/554a06cbb4c9055b7a8b55e2/tech-buisness1.jpg)