TANULMÁNYOK AZ INFORMÁCIÓ- ÉS TUDÁSFOLYAMATOKRÓL 11.; 2006/2; 213-242. O. 213 Electronic banking in Lithuania and Hungary - a co-operative research Dalia Kriksciuniene PhD– Ferenc Kiss PhD Vilnius University Kaunas Faculty of Humanities Department of informatics Muitinės Str. 8 LT-3000 Kaunas Lithuania Tel. (+37037) 42-25-66 e-mail: [email protected] Budapesti Műszaki és Gazdaságtudományi Egyetem Gazdaság- és Társadalomtudományi Kar Információ- és Tudásmenedzsment Tanszék 1111 Budapest, Sztoczek u. 2. St. ép. I. em. 117. Telefon: (36 1) 463-1832, Fax: (36 1) 463-4035 e-mail: [email protected] Abstract This article is going to summarize the results of a research investigating electronic channels applied in the finance sector, which have been achieved in the first step of the joint researches of BME ITM and Vilnius University. In addition to the general description of the financial and banking system of the two countries, this article deals with the areas of internet banking and mobile banking, as well as with the market of paying cards, furthermore presents the most important data, the characteristic properties, expectations and problems of these areas, from the aspect of the situation in Lithuania and Hungary. Keywords: internet-banking, mobil-banking, financial services, electronic channels 1. Introduction The Information and Knowledge Management Department of the Budapest Technical University started a comparative research together with the Kaunas Faculty of the Lithuanian Vilnius University in 2005. Lithuania is a Baltic state where the transformation of the economic system lags behind that in Hungary by 5 to 8 years or in certain areas by 10

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

TANULMÁNYOK AZ INFORMÁCIÓ- ÉS TUDÁSFOLYAMATOKRÓL 11.; 2006/2; 213-242. O.

213

Electronic banking in Lithuania and Hungary - a co-operative

research

Dalia Kriksciuniene PhD– Ferenc Kiss PhD

Vilnius University Kaunas Faculty of Humanities

Department of informatics

Muitinės Str. 8

LT-3000 Kaunas

Lithuania

Tel. (+37037) 42-25-66 e-mail: [email protected]

Budapesti Műszaki és Gazdaságtudományi Egyetem Gazdaság- és Társadalomtudományi Kar

Információ- és Tudásmenedzsment Tanszék

1111 Budapest, Sztoczek u. 2. St. ép. I. em. 117. Telefon: (36 1) 463-1832, Fax: (36 1) 463-4035

e-mail: [email protected]

Abstract

This article is going to summarize the results of a research investigating

electronic channels applied in the finance sector, which have been achieved in the

first step of the joint researches of BME ITM and Vilnius University. In addition to the general description of the financial and banking system of the two

countries, this article deals with the areas of internet banking and mobile banking,

as well as with the market of paying cards, furthermore presents the most important data, the characteristic properties, expectations and problems of these

areas, from the aspect of the situation in Lithuania and Hungary.

Keywords: internet-banking, mobil-banking, financial services, electronic

channels

1. Introduction

The Information and Knowledge Management Department of the Budapest Technical

University started a comparative research together with the Kaunas Faculty of the

Lithuanian Vilnius University in 2005. Lithuania is a Baltic state where the transformation

of the economic system lags behind that in Hungary by 5 to 8 years or in certain areas by 10

DALIA KRIKSCIUNIENE PHD– FERENC KISS PHD

214

years, meanwhile she is in a surprisingly similar phase as regards services and technological

support provided in the field of finances.

In the first segment of this work, the two universities have conducted a joint research in the

area of electronic channels, whereas they used the same questionnaire for understanding the

market. Results of this research are to be found hereunder.

2. Level of development of the banking system

Several specific properties of the domestic services and service providers can be explained

by the fact that during the period from 1949 to 1988 the domestic financial system as well

as the financial information technology proceeded on a development path definitely

different from that seen in Western Europe. Financial sector operating in a competitive

multi-actor market environment has been created through the reform of the single-level

bank system and later the transformation of the socio-economic system. An era

characterised by a monopole bank and a monopole insurance firm and complete absence of

securities trading was followed by the transformation of domestic service providers and a

large number of foreign entrants arriving at the domestic market with the most modern

technology then available, however, several years had to pass until the domestic

infrastructure enabled the spread of certain services (bank cards, ATM, POS, Home/Office

Banking, etc.) that have already proved themselves abroad.

In view of the characteristic features of the local market, almost all of the banks created

their expensive branch office networks covering at least a county centre or rather several

large cities. The only exceptions are the specialised, so-called niche-banks. Their common

characteristics are that their target clientele is not the retail sector and/or their products are

distributed exclusively through agents.

The system of financial services in Lithuania is on the level of development seen in

Hungary between 1992 and 96. Given the fact that the population of this country of three

million is, just like in Hungary, concentrated, i.e. the population of the capital city is

relatively large, 20% of the population lives in the capital, banking services take the same

shape. Head offices of the banks are concentrated in the capital cities, there are much less

branches in the country but networks are keep enlarging. Currently in the bank sector

foreign financial institutes are starting up just carefully, there were some acquisitions,

mainly of minority shareholdings, and there are some specimen branches of foreign banks

in the capital city and some large cities, but these are mostly just pioneering or are dedicated

to servicing the regular partners of their mother company on the Lithuanian market.

ELECTRONIC BANKING IN LITHUANIA AND HUNGARY - A CO-OPERATIVE RESEARCH

215

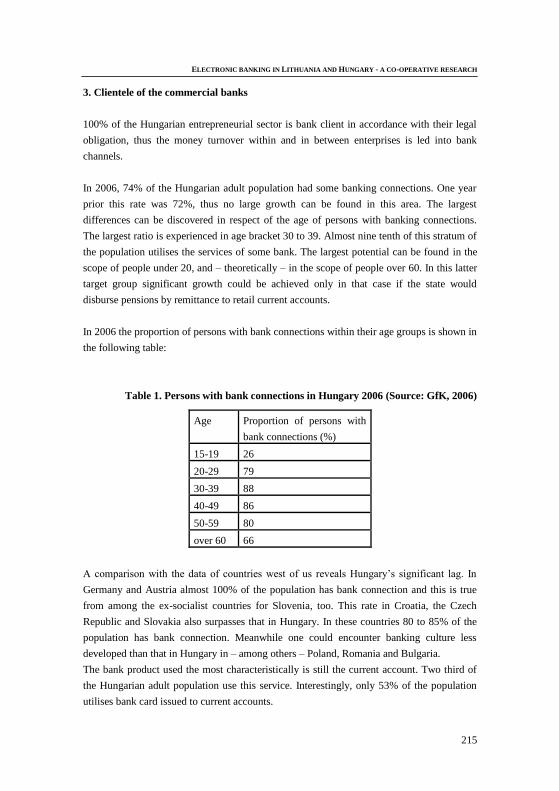

3. Clientele of the commercial banks

100% of the Hungarian entrepreneurial sector is bank client in accordance with their legal

obligation, thus the money turnover within and in between enterprises is led into bank

channels.

In 2006, 74% of the Hungarian adult population had some banking connections. One year

prior this rate was 72%, thus no large growth can be found in this area. The largest

differences can be discovered in respect of the age of persons with banking connections.

The largest ratio is experienced in age bracket 30 to 39. Almost nine tenth of this stratum of

the population utilises the services of some bank. The largest potential can be found in the

scope of people under 20, and – theoretically – in the scope of people over 60. In this latter

target group significant growth could be achieved only in that case if the state would

disburse pensions by remittance to retail current accounts.

In 2006 the proportion of persons with bank connections within their age groups is shown in

the following table:

Table 1. Persons with bank connections in Hungary 2006 (Source: GfK, 2006)

Age Proportion of persons with

bank connections (%)

15-19 26

20-29 79

30-39 88

40-49 86

50-59 80

over 60 66

A comparison with the data of countries west of us reveals Hungary’s significant lag. In

Germany and Austria almost 100% of the population has bank connection and this is true

from among the ex-socialist countries for Slovenia, too. This rate in Croatia, the Czech

Republic and Slovakia also surpasses that in Hungary. In these countries 80 to 85% of the

population has bank connection. Meanwhile one could encounter banking culture less

developed than that in Hungary in – among others – Poland, Romania and Bulgaria.

The bank product used the most characteristically is still the current account. Two third of

the Hungarian adult population use this service. Interestingly, only 53% of the population

utilises bank card issued to current accounts.

DALIA KRIKSCIUNIENE PHD– FERENC KISS PHD

216

Whilst according to an international comparison we are not ranked favourably as regards the

utilisation of bank products, an investigation in the field of credit shows a different

situation. 22% of the adult population utilises some kind of bank credit and thus we come

ahead of countries like Austria, the Czech Republic and Slovakia and are just slightly

lagging behind the German experiences.

Divided Lithuanian people, who are interested in e-banking services, by how long do they

use this services, see (Picture 5), that, most part of e-banking consumers‘ use it about three

years.

8%

15%19%

24%

34%

0%

10%

20%

30%

40%

1-6

mo

nth

7-1

2 m

on

th

1-2

year

2-3

year

mo

re than

3 y

ear

Figure 1. Duration of usage e-banking services in Lithuania

Source: created by authors according to Lithuanian commercial banks questioning results.

Interesting fact, that despite all e-banking system disadvantages and lack of information

about using e-banking, almost 98 % consumers of e-banking systems state that and in future

they will use e-banking services. However even 61 % of respondents suppose that exist a

lack of information about usage of e-banking services. Particularly this lack exist for older

people.

ELECTRONIC BANKING IN LITHUANIA AND HUNGARY - A CO-OPERATIVE RESEARCH

217

4. Electronic financial services

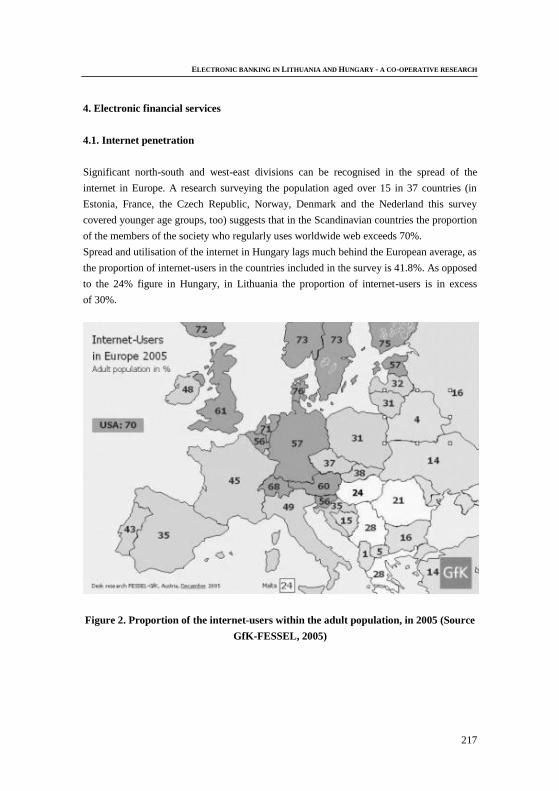

4.1. Internet penetration

Significant north-south and west-east divisions can be recognised in the spread of the

internet in Europe. A research surveying the population aged over 15 in 37 countries (in

Estonia, France, the Czech Republic, Norway, Denmark and the Nederland this survey

covered younger age groups, too) suggests that in the Scandinavian countries the proportion

of the members of the society who regularly uses worldwide web exceeds 70%.

Spread and utilisation of the internet in Hungary lags much behind the European average, as

the proportion of internet-users in the countries included in the survey is 41.8%. As opposed

to the 24% figure in Hungary, in Lithuania the proportion of internet-users is in excess

of 30%.

Figure 2. Proportion of the internet-users within the adult population, in 2005 (Source

GfK-FESSEL, 2005)

DALIA KRIKSCIUNIENE PHD– FERENC KISS PHD

218

4.2. Internet banking

Consequently, since the branch office network covers all major settlements, a certain (quite

large) group of the customers does not need to use remote applications because they can

arrange their businesses personally.

Internet-aided banking services have been launched at the beginning of the 90’s, at that time

in the form of terminal and other peripheral-bound home-banking systems, whilst “classic”,

browser-based internet aided financial services as we know them now, appeared on the

Hungarian market first in 1997.

In Lithuania internet-banking started in around 2000 when, making good use of the west-

European instances ahead of them, certain stages of the technology and therefore some

classic traps or obsolete or almost obsolete technologies that have been widely used for

example in Hungary could be leapt over.

Instead of the initial home-banking applications used in Hungary, Lithuania started with

internet-based solutions, thus the modem-aided, dial-up, thick client period has been leapt

over; also, in the field of Office Banking the application of leading-edge technologies was

more characteristic.

In Hungary, due to the shortcomings of the infrastructure and a characteristic disbelief

concerning novelties, the initial utilisation of electronic channels was very law, but the

graph hereunder properly illustrates the trend of continuous growth: by 2006 20% of the

retail clients, i.e. more than 800 thousand persons had internet-aided connection with their

banks.

ELECTRONIC BANKING IN LITHUANIA AND HUNGARY - A CO-OPERATIVE RESEARCH

219

The number and proportion of retail clients with internet-banking contracts

at the Hungarian commercial banks

0

100000

200000

300000

400000

500000

600000

700000

800000

90000031.1

2.2

000

31.0

3.2

001

30.0

6.2

001

30.0

9.2

001

31.1

2.2

001

31.0

3.2

002

30.0

6.2

002

30.0

9.2

002

31.1

2.2

002

31.0

3.2

003

30.0

6.2

003

30.0

9.2

003

31.1

2.2

003

31.0

3.2

004

30.0

6.2

004

30.0

9.2

004

31.1

2.2

004

31.0

3.2

005

30.0

6.2

005

31.1

2.2

005

30.0

6.2

006

0%

4%

8%

12%

16%

20%

24%

28%

32%

36%

Number of clients Proportion of cliens

Figure 3. Retail internet-banking users in Hungary 2000-2005. (Source: GKI, 2005)

Source: GKI – Report on the internet-economy (Focusing on the financial sector) 2005

Enterprises have been much more dynamic in understanding the advantages and the

necessity of electronic applications, in 2006 approximately 120 thousand firms arranged

their bank deals via internet, which represents 95 to 98% of the entire corporate bank

turnover. The customer rate at 20% that should be compared with this enormous figure can

be explained with the structure of the Hungarian corporate sector, because the vast majority

of the Hungarian firms are micro-enterprises that do not generate significant money

turnover meanwhile represent more than 80% of the count.

DALIA KRIKSCIUNIENE PHD– FERENC KISS PHD

220

The number and proportion of corporate clients with internet-banking

contracts at the Hungarian commercial banks

0

20000

40000

60000

80000

100000

12000031.1

2.2

000

31.0

3.2

001

30.0

6.2

001

30.0

9.2

001

31.1

2.2

001

31.0

3.2

002

30.0

6.2

002

30.0

9.2

002

31.1

2.2

002

31.0

3.2

003

30.0

6.2

003

30.0

9.2

003

31.1

2.2

003

31.0

3.2

004

30.0

6.2

004

30.0

9.2

004

31.1

2.2

004

31.0

3.2

005

30.0

6.2

005

31.1

2.2

005

30.0

6.2

006

0%

5%

10%

15%

20%

25%

30%

Number of clients Proportion of clients

Figure 4. Corporate internet-banking users in Hungary 2000-2005. (Source: GKI,

2005)

In Lithuania the count of the customers increased much more dynamically, the spread of

mobile channels was decisive there, mobile penetration and mobile service delivery grew

very dynamically and this is now coupled with some kinds of mobile internet

communication that from many aspects is much more popular than the communication via

internet; the internet access in Lithuania is significantly less widely spread.

The number of customers highlights a difference: within a nation of approx. 3 million the

customer count is one million and two hundred thousand that means that more than half of

the population in active age has become internet banking customer, this technology thus

showed a very fast increase in Lithuania, the population have a fundamental affinity for the

use of electronic devices and the utilisation of such services.

Recently Lithuanian banks have started apace development of internet – banking systems.

The first bank which has started to offer internet services was AB Bankas “Snoras”.

Through the internet the client can get information about account debit, flow history of

money, as well as to get information about transactions, to assign the bank to make local,

international and constant transactions, to find out the information about exchange rate, to

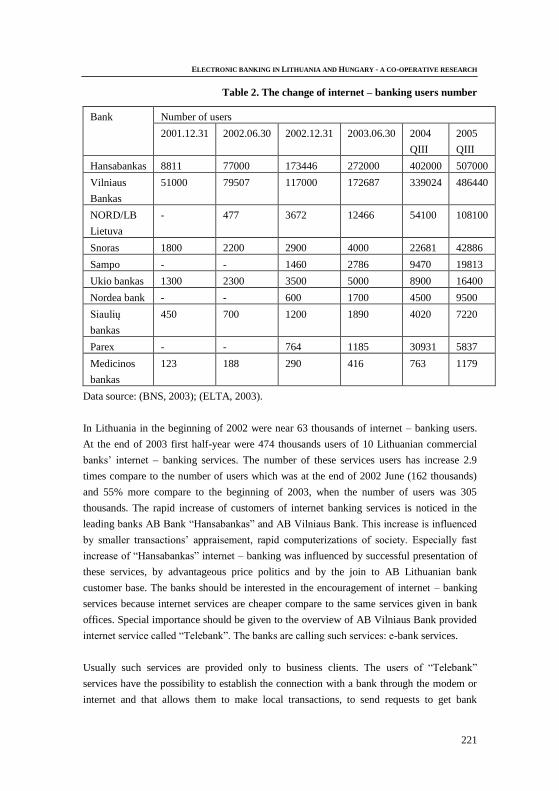

order payment cards. The number of users of such services is increasing rapidly. In the table

3 there is presented the data of internet – banking users’ number change starting from 31st

of December 2001 and finishing with 30th of June 2003.

ELECTRONIC BANKING IN LITHUANIA AND HUNGARY - A CO-OPERATIVE RESEARCH

221

Table 2. The change of internet – banking users number

Bank Number of users

2001.12.31 2002.06.30 2002.12.31 2003.06.30 2004

QIII

2005

QIII

Hansabankas 8811 77000 173446 272000 402000 507000

Vilniaus

Bankas

51000 79507 117000 172687 339024 486440

NORD/LB

Lietuva

- 477 3672 12466 54100 108100

Snoras 1800 2200 2900 4000 22681 42886

Sampo - - 1460 2786 9470 19813

Ukio bankas 1300 2300 3500 5000 8900 16400

Nordea bank - - 600 1700 4500 9500

Siaulių

bankas

450 700 1200 1890 4020 7220

Parex - - 764 1185 30931 5837

Medicinos

bankas

123 188 290 416 763 1179

Data source: (BNS, 2003); (ELTA, 2003).

In Lithuania in the beginning of 2002 were near 63 thousands of internet – banking users.

At the end of 2003 first half-year were 474 thousands users of 10 Lithuanian commercial

banks’ internet – banking services. The number of these services users has increase 2.9

times compare to the number of users which was at the end of 2002 June (162 thousands)

and 55% more compare to the beginning of 2003, when the number of users was 305

thousands. The rapid increase of customers of internet banking services is noticed in the

leading banks AB Bank “Hansabankas” and AB Vilniaus Bank. This increase is influenced

by smaller transactions’ appraisement, rapid computerizations of society. Especially fast

increase of “Hansabankas” internet – banking was influenced by successful presentation of

these services, by advantageous price politics and by the join to AB Lithuanian bank

customer base. The banks should be interested in the encouragement of internet – banking

services because internet services are cheaper compare to the same services given in bank

offices. Special importance should be given to the overview of AB Vilniaus Bank provided

internet service called “Telebank”. The banks are calling such services: e-bank services.

Usually such services are provided only to business clients. The users of “Telebank”

services have the possibility to establish the connection with a bank through the modem or

internet and that allows them to make local transactions, to send requests to get bank

DALIA KRIKSCIUNIENE PHD– FERENC KISS PHD

222

cheque, to buy or sell currency, to issue or to change bank guarantee, to issue or to change

accreditation, to issue voucher, to make transfers to the payment cards of employees, to get

information about the account, debit in the account, exchange rates etc. There are much

more people who have a contract of internet – banking usage then the number of people

who are really using it. Only around 40% of all banks’ customers who have bank card are

using internet – banking services (Sytas 2003). One person signs as a customer of several

banks, but is using the services only of one bank. Quite often even having the possibility to

use internet – banking services people do not use it. The banks try to motivate the clients to

use e – services (advertisement, lower prices of internet services etc.). However, the banks

do not the result they do expect to get. According to the data of information technology

products; and consultation company Metasite, the web pages of most Lithuanian banks to

not satisfy the needs of the customers (Sytas 2004). According to the opinion of company

employees, the bank put big investments into the design and technologies of the web page,

but they do not care if the web page satisfies the needs of the customers.

Starting from the beginning of year 2004 the number of internet – banking clients has

increased in 23%. In the first half year of 2005 were more than 784 thousands clients

internet – banking. Compare to the beginning of 2005 the number of clients has increased

23 %, and the growth in the last 12 months is around 65 %

4.3. Payment cards:

4.3.1. Hungary

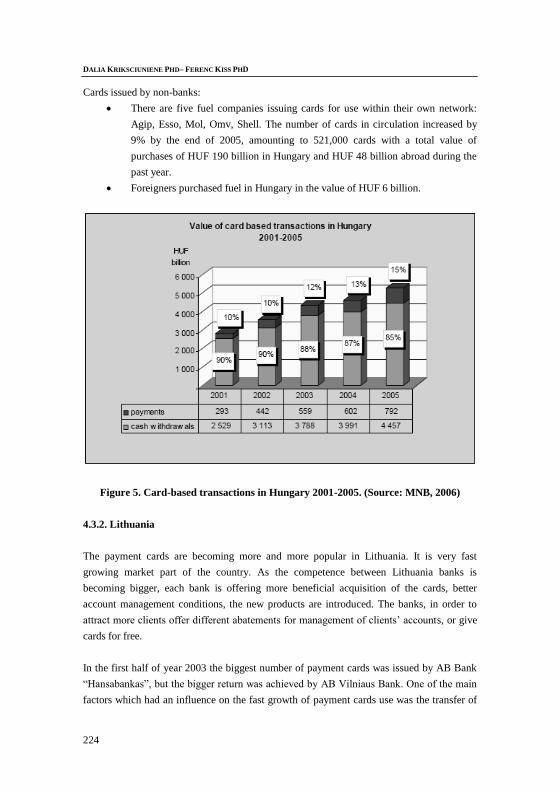

Changes in the number of bank issued payment cards in circulation:

The rate of increase in the number of cards in circulation during the year once

again shows a rising trend, approaching the level as it was five years ago (13 %

in 2005). At the end of 2005 there were 7.4 million bank issued cards in

circulation; bringing the total to close to eight million with the cards issued by

entities other than banks also included.

22 credit institutions and one financial enterprise issue cards. Twenty banks are

involved in issuing debit cards and six offer debit cards linked to a credit line.

Credit cards are offered by fourteen banks, whereas charge cards are offered by

four banks and one financial enterprise.

The ratio of debit cards among all cards is 86% (down from 92% in the previous

year), of which 5% features a debit card linked to a credit line. The number of

credit cards has doubled in a year, their share increased from 8% to 14%,

whereas the percentage of charge cards remain below one per cent.

ELECTRONIC BANKING IN LITHUANIA AND HUNGARY - A CO-OPERATIVE RESEARCH

223

The share of co-branded and affinity cards have increased by 29%, reaching one

million by the end of last year. Eleven banks offer these products in co-operation

with retailers and non-profit organisations.

At the end of 2005 18% of the cards were issued with EMV chips (up from 5%

of the previous year).

ATM and EFTPOS networks

The number of ATMs increased at a steady rate in the past five years; there were

3,531 terminals at the end of 2005. The 9,988 POS terminals installed in bank

branches and post offices also facilitate the electronic cash withdrawal; 2% of

these are enabled to read EMV chips.

The number of retail outlets accepting Visa and MasterCard shows a growth of

only 1% in the past year, there are 19,854 shops accepting Visa, and 19,941

accepting MasterCard. The number of retail outlets accepting Amex cards has

dropped by 28%, to 8,092 due to a change of the acquirer. Diners cards are

accepted in 4,012 shops and JCB is accepted in 8,893 shops.

There are 29,538 electronic POS terminals installed at retail acceptance points,

where practically all transactions are authorised which contributes to the higher

safety of card use. Twenty-two per cent (22%) of the devices are able to read

EMV chips.

Turnover realised with bank issued payment cards:

Acquiring turnover:

In the past year, 209 million transactions were conducted with domestic and

foreign issued cards, in the value of HUF 5,249 billion. The transaction number

rose by 8%, the value increased by 10%, in comparison to the previous year.

The share of cash withdrawal transactions continued to fall; of every one

hundred transactions 55 transactions were cash withdrawals (as oppose to 58 in

the previous year), with 51 ATM and 4 POS transactions. In respect of purchase

transactions, of every one hundred transactions, there were 41 payments through

POS terminals at retail outlets, with 4 mobile phone loading at ATMs.

Issuing turnover

In the past year, Hungarian card holders used their cards on 203 million

occasions inside and outside of the country, in the value of HUF 5,220 billion.

The number rose by 11%, the value grew by 9%.

DALIA KRIKSCIUNIENE PHD– FERENC KISS PHD

224

Cards issued by non-banks:

There are five fuel companies issuing cards for use within their own network:

Agip, Esso, Mol, Omv, Shell. The number of cards in circulation increased by

9% by the end of 2005, amounting to 521,000 cards with a total value of

purchases of HUF 190 billion in Hungary and HUF 48 billion abroad during the

past year.

Foreigners purchased fuel in Hungary in the value of HUF 6 billion.

Figure 5. Card-based transactions in Hungary 2001-2005. (Source: MNB, 2006)

4.3.2. Lithuania

The payment cards are becoming more and more popular in Lithuania. It is very fast

growing market part of the country. As the competence between Lithuania banks is

becoming bigger, each bank is offering more beneficial acquisition of the cards, better

account management conditions, the new products are introduced. The banks, in order to

attract more clients offer different abatements for management of clients’ accounts, or give

cards for free.

In the first half of year 2003 the biggest number of payment cards was issued by AB Bank

“Hansabankas”, but the bigger return was achieved by AB Vilniaus Bank. One of the main

factors which had an influence on the fast growth of payment cards use was the transfer of

ELECTRONIC BANKING IN LITHUANIA AND HUNGARY - A CO-OPERATIVE RESEARCH

225

salaries and the increase of services’ package. Besides, the payment card use fee is not big.

The net of cash machines is expanding and there are more places where is possible to pay

using payment cards. In April 2003 AB Vilniaus Bank and AB Bank “NORD/LB Lietuva”

have signed the contract for joint cash machines net use. Based on this contract the clients

of these banks have the same rights while taking cash from the cash machines of both

banks.

In Lithuania very popular magnetic payment cards have been started to change into

microprocessor cards, which are widely used in the world. The microprocessor cards are

more save and secure, using them it is possible to make more transfers. The number of

payment cards is increasing. The number of it should be still increasing at least for two

more years, until all the potential clients will obtain it. Latter the market should stabilize and

increase in not so fast.

The market of payment cards has increased 2.9% in the 1st quarter of year 2005. According

to the data on the 1st of April all the country commercial banks had issued 2.785 millions of

different payments cards, and their turnover reached 4.03 milliards Lt – 26.3% more than

last year. Compare to the 1st of April 2004, the number of payment cards of all the banks

has increased 14.8%. In Lithuania at the beginning of April were 1.018 cash machines and

near 20.700 places where it is possible to pay with payment card.

The bankers are still predicting the growth, which will not be so fast. The growth is

influenced by the expansion of country payment cards market, competence, more favorable

cards purchase and new products.

4.4. Mobil-banking

In Hungary the most frequented functions within mobile banking are the transaction

confirmation and the communication of the single-use, time framed login password

necessary for the use of internet banking; basically these two operations cover the majority

of the transactions. There are some information services and in the fields of parking or

motorway toll sticker purchase, payment via radiophone has just been started, but for the

time being these represent just a marginal part. Harsh separation from mobile service

providers emerges among other reasons because the SIM-card is the property of the mobile

service providers, and the banks, on the basis of the regulation and the market approach

applied by different market actors, are afraid to enable their clientele to execute open

transactions on the networks of the mobile service providers, as they are fearful of the

DALIA KRIKSCIUNIENE PHD– FERENC KISS PHD

226

violation of the confidentiality of data, or that a mobile service provider could easily grab

their client portfolio.

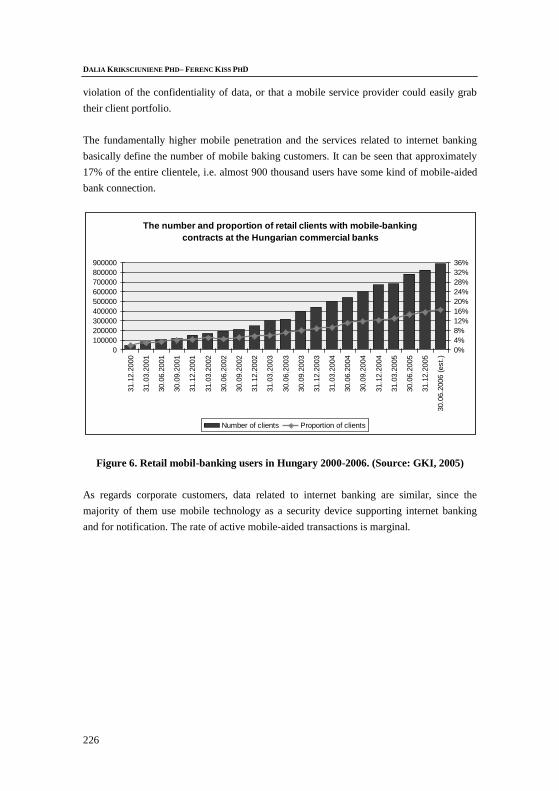

The fundamentally higher mobile penetration and the services related to internet banking

basically define the number of mobile baking customers. It can be seen that approximately

17% of the entire clientele, i.e. almost 900 thousand users have some kind of mobile-aided

bank connection.

The number and proportion of retail clients with mobile-banking

contracts at the Hungarian commercial banks

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

31.1

2.2

000

31.0

3.2

001

30.0

6.2

001

30.0

9.2

001

31.1

2.2

001

31.0

3.2

002

30.0

6.2

002

30.0

9.2

002

31.1

2.2

002

31.0

3.2

003

30.0

6.2

003

30.0

9.2

003

31.1

2.2

003

31.0

3.2

004

30.0

6.2

004

30.0

9.2

004

31.1

2.2

004

31.0

3.2

005

30.0

6.2

005

31.1

2.2

005

30.0

6.2

006 (

est.

)

0%

4%

8%

12%

16%

20%

24%

28%

32%

36%

Number of clients Proportion of clients

Figure 6. Retail mobil-banking users in Hungary 2000-2006. (Source: GKI, 2005)

As regards corporate customers, data related to internet banking are similar, since the

majority of them use mobile technology as a security device supporting internet banking

and for notification. The rate of active mobile-aided transactions is marginal.

ELECTRONIC BANKING IN LITHUANIA AND HUNGARY - A CO-OPERATIVE RESEARCH

227

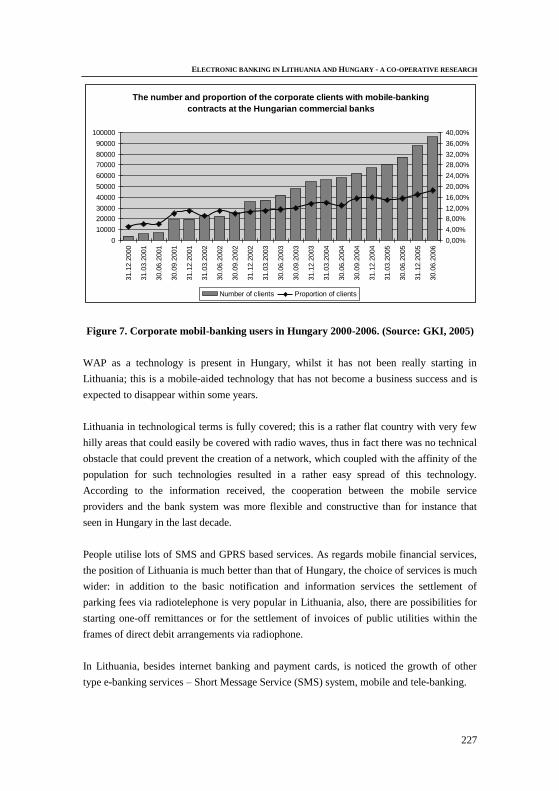

The number and proportion of the corporate clients with mobile-banking

contracts at the Hungarian commercial banks

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

10000031.1

2.2

000

31.0

3.2

001

30.0

6.2

001

30.0

9.2

001

31.1

2.2

001

31.0

3.2

002

30.0

6.2

002

30.0

9.2

002

31.1

2.2

002

31.0

3.2

003

30.0

6.2

003

30.0

9.2

003

31.1

2.2

003

31.0

3.2

004

30.0

6.2

004

30.0

9.2

004

31.1

2.2

004

31.0

3.2

005

30.0

6.2

005

31.1

2.2

005

30.0

6.2

006

0,00%

4,00%

8,00%

12,00%

16,00%

20,00%

24,00%

28,00%

32,00%

36,00%

40,00%

Number of clients Proportion of clients

Figure 7. Corporate mobil-banking users in Hungary 2000-2006. (Source: GKI, 2005)

WAP as a technology is present in Hungary, whilst it has not been really starting in

Lithuania; this is a mobile-aided technology that has not become a business success and is

expected to disappear within some years.

Lithuania in technological terms is fully covered; this is a rather flat country with very few

hilly areas that could easily be covered with radio waves, thus in fact there was no technical

obstacle that could prevent the creation of a network, which coupled with the affinity of the

population for such technologies resulted in a rather easy spread of this technology.

According to the information received, the cooperation between the mobile service

providers and the bank system was more flexible and constructive than for instance that

seen in Hungary in the last decade.

People utilise lots of SMS and GPRS based services. As regards mobile financial services,

the position of Lithuania is much better than that of Hungary, the choice of services is much

wider: in addition to the basic notification and information services the settlement of

parking fees via radiotelephone is very popular in Lithuania, also, there are possibilities for

starting one-off remittances or for the settlement of invoices of public utilities within the

frames of direct debit arrangements via radiophone.

In Lithuania, besides internet banking and payment cards, is noticed the growth of other

type e-banking services – Short Message Service (SMS) system, mobile and tele-banking.

DALIA KRIKSCIUNIENE PHD– FERENC KISS PHD

228

Short Message Service (SMS) system.

In Lithuania at a current time is possible to manage financial affairs through the mobile

phone from any place where is the connection. The clients of the banks can get information

about their account using mobile technologies. Lithuania commercial banks have started to

offer the first mobile banking services in the year 2000. In April 2000 AB Bank “Snoras”

presented the service, which allowed users to get information about card debit, last made

transactions and exchange rate by sending SMS. This service should become even more

popular as the number of mobile phones users is increasing.

Mobile banking.

AB Bank “Snoras” was the first who have offered BRPP service, which allows getting

information about account debit and exchange rates. The implementation of BRPP is very

expensive, but such service lets to keep and attract new clients. Later on, the other Lithuania

commercial banks as well have started to offer the mobile banking services. The benefit of

theses services banks are counting indirectly – they evaluate the time which the client would

spend while calling to the bank or coming to bank office. From year 2002 the clients of

Nordea Bank Finland Plc (Lithuania) can make bank transfers using General Packer Radio

Services (GPRS) technology. In this case the data is send through GSM connection net. The

clients have possibility to check their account and deposit, make local and international

transactions, and send questions to the bank. Having one number and one password is

possible to use Internet and mobile banking services. Some banks a careful with mobile

banking services (Andružytė 2002a). There is an opinion that it is enough to afford services

through SMS, as this service is available in all mobile phones, while BRPP and GPRS – not

in all mobile phones and that could reduce the number of mobile banking users.

In Lithuania is possible pay the bills, transfer money from one account to another, to get

information about account debit, to get general bank information about currency purchase

prices, payment cards, bank accounts, loans and to get many other services through the

phone. Such and similar services are offered by several Lithuania commercial banks, such

as Vilniaus Bank, Nord/LB Bank and “Hansabankas”.

Always is very important to ensure the security, and it is why all the Lithuania commercial

banks which offer tele-banking services have their own systems, which ensure privacy. For

example, in Vilniaus Bank, the client who signs the contract gets identification card, where

is shown clients’ ID number and collection of codes. In the contract is written the temporal

password. The ID and password are used in order to recognize the client, and the collection

of codes is used to sign and to confirm the transfers. In this way is possible to manage the

accounts. The bank will make the transfer only to those recipients, which will be included

while signing the contract.

ELECTRONIC BANKING IN LITHUANIA AND HUNGARY - A CO-OPERATIVE RESEARCH

229

Even not having special contracts the banks usually give general information through the

phone. The only requirement is to use tone dialing phones.

There is a possibility to manage the finance using mobile phone from any connection zone.

This service is offered to the users of Omnitel by Vilniaus Bank, and Nord/LB Lietuva is

working with Omnitel, Bite GSM and TELE2 mobile services companies.

VB Mobilinija – is the best way for the user to get information about the situation in the

account. After becoming the user of VB Mobilinija is possible to check the debit of the

account, to get notice about changes in the account seven days per week in any place where

the mobile connection is. In order to become the user of VB Mobilinija the user has to sign

the contract of e-services support.

In the beginning of year 2003 the VB Mobilinija was used by 4.5 thousands of users, and

the fixed phone connection system VB Linija was used by 44 thousands users.

Now using NORD/LB service SMS LINIJA the users can get information about the bank

and payment card account directly to the mobile phone. SMS LINIJA service can be used

not only in Lithuania, but in foreign countries as well. There can be two kinds of

information:

The answers to the queries. The client is sending the query to the bank, and bank is sending

the answer;

Robotic reports. The information will be sent automatically in some periods or after some

changes in the account are made. It is possible each day to get information about currency

purchase prices. It is possible to get reports when there are made any changes in the

account. There is a possibility to set the threshold which will define when the notice about

the changes in the account should be sent. In order to get robotic report it is necessary to

activate this service. After if you want there is possibility to cancel this service or activate it

again.

Separately from all other tele-banking services should be discussed Vilniaus Bank tele-

banking service VB Telebank. The banks such services are calling e-banking services.

These services are offered only for business clients. In order to supports such service the

modem connections should be established. The banker installs the program and teaches the

client to work with it.

“VB Telebankas” offered by Vilniaus Bank lets to manage accounts, to get information

from the bank and to make transactions sitting in the work place. All the information from

DALIA KRIKSCIUNIENE PHD– FERENC KISS PHD

230

the client computer reaches Vilniaus Bank system through the modem connection in a short

time, and the quality of the services depends on technical characteristics of clients’

computer, connection line and “VB Telebank” performance.

From year 1997 such tele-banking services are offered by Nord/LB Lietuva. In general, it

seems that tele-banking has a big development potentiality in Lithuania. It gives the comfort

to the client, possibility to use bank services at any time. Especially high potentiality has

mobile banking.

4.5. Electronic services

4.5.1. Hungary

In 2006 in Hungary about 20 financial institutes provided some kind of electronic banking

services. The choice of products is quite large; in addition to the full scope of banking

services the banks’ electronic portfolio includes investment and insurance services, too. The

following graph illustrates the most popular internet banking services and the relevant

expectations.

ELECTRONIC BANKING IN LITHUANIA AND HUNGARY - A CO-OPERATIVE RESEARCH

231

Expected changes in the composition of instructions related to retail accounts during the next 12

months, based on the banks’ opinion

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Remittances

Transaction checking

Retrieval of account information

Filling up mobile balance

Sales/purchase of investment units

Time deposits

Sales/purchase of government

securities

Credit application

Direct debit

Sales/purchase of shares

Figure 8. Expected changes in the composition of instructions related to retail accounts

during the next 12 months, based on the banks’ opinion [-100 significant decrease;

+100 significant increase]; Q4 2005 (Source: GKI, 2005)

4.5.2. Lithuania

4.5.2.1. Commercial banks Internet-banking services of Lithuania

In Lithuania the choice of services is significantly smaller. Customers can retrieve some

basic information from internet banks, and initiate one-off remittance or remittances in the

frames of direct debit arrangements, more complex services are for the time being scarce,

meanwhile refilling mobile accounts via internet bank is very popular, which in Hungary is

rather arranged via ATM’s.

Recently Lithuanian commercial banks especially speedy implement internet-banking

systems in case to become more modern and attractive and to introduce all their services in

computer of individual consumer or organization. Currently more then half banks of

Lithuania are implemented clients service systems by the Internet.

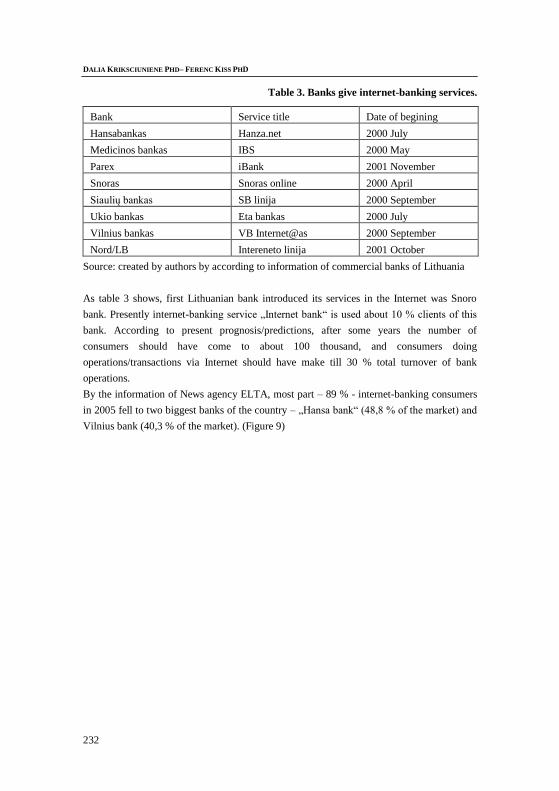

Further is showed some banks, which are give internet-banking services, internet systems

titles and beginning dates of lend this services for consumers (table 3).

DALIA KRIKSCIUNIENE PHD– FERENC KISS PHD

232

Table 3. Banks give internet-banking services.

Bank Service title Date of begining

Hansabankas Hanza.net 2000 July

Medicinos bankas IBS 2000 May

Parex iBank 2001 November

Snoras Snoras online 2000 April

Siaulių bankas SB linija 2000 September

Ukio bankas Eta bankas 2000 July

Vilnius bankas VB Internet@as 2000 September

Nord/LB Intereneto linija 2001 October

Source: created by authors by according to information of commercial banks of Lithuania

As table 3 shows, first Lithuanian bank introduced its services in the Internet was Snoro

bank. Presently internet-banking service „Internet bank“ is used about 10 % clients of this

bank. According to present prognosis/predictions, after some years the number of

consumers should have come to about 100 thousand, and consumers doing

operations/transactions via Internet should have make till 30 % total turnover of bank

operations.

By the information of News agency ELTA, most part – 89 % - internet-banking consumers

in 2005 fell to two biggest banks of the country – „Hansa bank“ (48,8 % of the market) and

Vilnius bank (40,3 % of the market). (Figure 9)

ELECTRONIC BANKING IN LITHUANIA AND HUNGARY - A CO-OPERATIVE RESEARCH

233

48,8

40,3

5,7

2

1

0,9

0,4

0,4

0,1

0 10 20 30 40 50

Hansa Bankas

Vilniaus Bankas

Nord/LB

Snoro Bankas

Ūkio bankas

Sampo bankas

Šiaulių bankas

Parex Bankas

Medicinos Bankas

Figure 9. Internet-banking market share by banks in percents, 2005, first half-year

(Source: ELTA)

Hansa bank internet – banking service „Hanza.net“ number of consumers‘ from the

begining of 2005 grow from 11 % till 383 thousand, Vilnius bank service „VB Internetas“ –

from 29 % till 315,654 thousand. Per year „hanza.net“ number of consumers‘ grow 41 %,

„VB nternetas” – 83 %.

First half-year of 2005 most fast grow third by size bank „NORD/LB Lietuva“ Internet line

clients‘ number – it multiplied 99 % and was 44,4 thousand (5,7 % of market). Comparing

with the end of June of 2004, number of internet-banking clients’ is grew 2,5 times.

Fourth by size commercial bank „Snoras“ had 16 thousand (2 % of market) internet-banking

clients in the end of June and comparing with the middle of 2004 – three time.

For Ukio bank accrue 1 % of clients – in the end of June there were 7,529 thousand. The

growth in 2005 amount 16 % comparing with the middle of 2004 – 51 %.

DALIA KRIKSCIUNIENE PHD– FERENC KISS PHD

234

First half-year of 2005 „Sampo“ bank internet-banking number of clients is grew 52 % to

7,185 thousand (0,9 % of market; comapring with June of 2003 it make more than 1,5 time).

Siaulių bank had 3,361 thousand internet-banking clinets‘ (0,4 % of market; the growth in

2005 – 29 %, over the last twelve month – 78 %).

For Parex bank accrue 3 thousand internet-banking clients‘ (0,4 % of market; number of

clients’ in 2005 is grew 77 %, over the last twelve month – 1,5 times).

The smallest commercial Medicinos bank in the end of June had 713 internet-banking

clients (0,1 % of market).

Banks, lending internet-banking services, can be divided in two main parts: (1) services for

the individual consumers; (2) services for the enterprises (business clients).

Individual consumers, without juridical person status currently can do few operations via

Internet, review information. Every card holder can foot the bill via Internet. Via Internet it

is possible pay for utilities, do transfers to other accounts, signing triangular agreement

between bank and services supplier it is possible to do debit transfers. For example, every

month bank automatically deduct mobile operators‘ tax, pay other monthly tax.

Major internet services‘ offer can get business enterprises. Every bank lending number of

services‘ and lending ways differ and often depends from the individual agreement, by

evaluating bank lending services and enterprise requirements, i.e., for the company can

mismatch package of services.

Therefore the internet-banking rapidly develop in Lithuania. It conditions many factors. The

main internet-banking advantage against traditional business – flexibility and simplicity. It

saves time and money.

4.5.2.2. Lithuanian e-banking services’ estimation by clients opinion

Appreciate fact, that banks‘ ability to compete increasingly depends from its ability better

serve client, and at the same time more part clients‘ want work with banks via Internet, the

question is: Does country banks catch to prepare properly serve clients via Internet? Where

are in this area advantages, where – disadvantages? Who were become leaders, who – drag?

In case to answer these questions, we use by Lithuanian commercial banks subscribe

prepared bank clients‘ survey data.

ELECTRONIC BANKING IN LITHUANIA AND HUNGARY - A CO-OPERATIVE RESEARCH

235

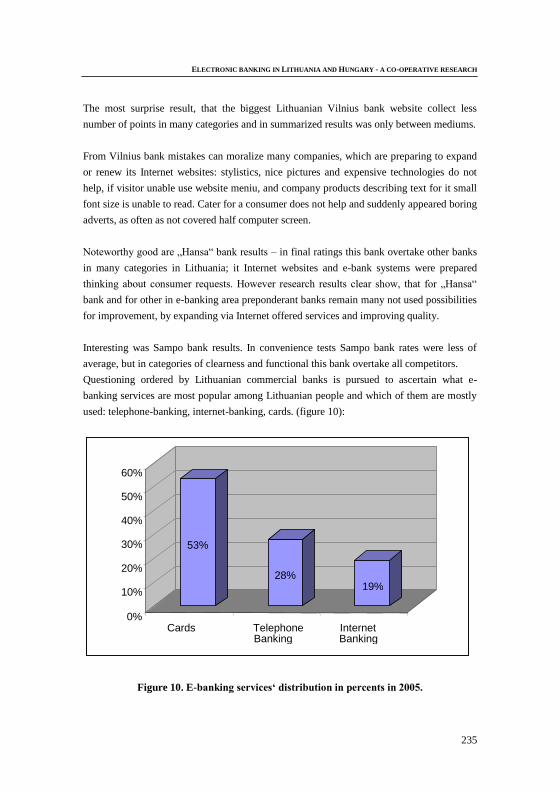

The most surprise result, that the biggest Lithuanian Vilnius bank website collect less

number of points in many categories and in summarized results was only between mediums.

From Vilnius bank mistakes can moralize many companies, which are preparing to expand

or renew its Internet websites: stylistics, nice pictures and expensive technologies do not

help, if visitor unable use website meniu, and company products describing text for it small

font size is unable to read. Cater for a consumer does not help and suddenly appeared boring

adverts, as often as not covered half computer screen.

Noteworthy good are „Hansa“ bank results – in final ratings this bank overtake other banks

in many categories in Lithuania; it Internet websites and e-bank systems were prepared

thinking about consumer requests. However research results clear show, that for „Hansa“

bank and for other in e-banking area preponderant banks remain many not used possibilities

for improvement, by expanding via Internet offered services and improving quality.

Interesting was Sampo bank results. In convenience tests Sampo bank rates were less of

average, but in categories of clearness and functional this bank overtake all competitors.

Questioning ordered by Lithuanian commercial banks is pursued to ascertain what e-

banking services are most popular among Lithuanian people and which of them are mostly

used: telephone-banking, internet-banking, cards. (figure 10):

Figure 10. E-banking services‘ distribution in percents in 2005.

53%

28% 19%

0%

10%

20%

30%

40%

50%

60%

Cards Telephone Banking

Internet Banking

DALIA KRIKSCIUNIENE PHD– FERENC KISS PHD

236

Source: created by authors according to Lithuanian commercial banks questioning results.

Picture 2 shows that currently mostly prevalent e-banking service is cards. Cards use 53 %

respondents.

Almost 48 % respondents use Vilnius bank e-banking services, 27 % - Hansa bank e-

banking services, 15 % - Nord/LB e-banking services. (figure 11)

Figure 11. Lithuanian commercial banks distribution by popularity in percents

Source: created by authors according to Lithuanian commercial banks questioning results

(2003-2004).

4.6. Users, motivations, problems

Facts hindering the use of internet-banking are two-sided: on the one hand there are

significant problems and deficiencies in the use of the internet itself. On the other hand,

pushing financial affairs towards the internet gives rise to fundamental questions of

confidence.

48%

27%

15% 10%

0%

10%

20%

30%

40%

50%

Vilniaus

bankas

Hansa bankas Nord/LB Other

ELECTRONIC BANKING IN LITHUANIA AND HUNGARY - A CO-OPERATIVE RESEARCH

237

The access to the internet may face many objective and subjective obstacles. An

investigation of the hindering factors might provide us with some information regarding the

difficulties households must face prior to joining the internet and in the course of its use.

In Hungary almost everybody marked the high price of the internet services as the hardest

obstacle. The lack of the computer is, of course, a large problem among households not yet

joining the internet. Among groups not yet joining the internet lack of motivation could

cause problems; roughly half of the household masters stated that they do not need internet

and almost 40% of them said that internet is not of interest for them. Lack of education

exercises a significant restrictive influence, too.

Factors hindering use of internet by the citizens in Hungary

0% 10% 20% 30% 40% 50% 60% 70% 80%

Physical challenge

Lack of understanding

Does not need internet

Is afraid of the damaging impacts of

the use of internet

Deems internet to be insecure

Does not know possibilities ensured by

internet

Is not interested in internet

Internet is expensive

His/her computer is not internet-

friendly

Does not have computer

Has internet

Does not have but intends to purchase internet

Does not have and does not want internet

Figure 12. Factors hindering use of internet by the citizens in Hungary (Source: ITTK)

Exaggeratedly quick changes coupled with the lack of organic evolution caused that in the

B2C sector no financial/electronic financial culture has developed that would have deep

roots. The bank system is sufficiently well developed to become a participant or even to

direct a swap for a better developed culture, the basic problems are appearing rather on the

demand side.

Basic circumstances are also disfavouring this area since the people are scarcely supplied

with ICT means specifically with internet, but an even more troublesome factor is digital

illiteracy (almost 60% of the Hungarian population could be deemed to be digitally

DALIA KRIKSCIUNIENE PHD– FERENC KISS PHD

238

illiterate; Karajánnisz-Tardos 2006), i.e. a problem created by the negative synergy among

supply of means, skills, command of languages, and some other deficiencies. Bad financial

position of a large part of the population makes a significant group within the potential users

to be reserved or even unconfident in respect of innovations related to money and money

management. Incomplete information and disbeliefs united with this seemingly reasonable

lack of confidence might result in total restraint from new finance technologies.

The only solution for the above problems could be an extended customer education. Given

the fact that the most important one out of key factors of usage is confidence, this should be

improved through furnishing the customer with realistic pictures on the basis of which they

could make informed and grounded decisions. In Hungary it is still missing. Customers

learn events from the press where only bad and negative cases deserve publication, thus the

press presents a unilaterally negative picture about the services. Meanwhile the campaigns

run by banks serve marketing targets and do not even give a try to deliver unbiased

information, thus the customer takes information from this source with scepticism. In

Lithuania the real risk and things deserving due considerations are explained already to

school children. There is a syllabus for secondary schools on financial culture, thus the

prospective customers in Lithuania start using services in possession of more knowledge

and what is even more, the information they receive stems from an independent source. This

is completely missing in Hungary. The use of electronic financial culture is not sufficiently

grounded.

In pursuance of better understanding of e-banking advantage for consumers in Lithuania, it

was asked bank employees‘ to describe those services advantages. By the opinion of Vilnius

bank employees‘, for doing every day operations internet-banking is easier and cheaper

way. Moreover, few advantage from it get and consumers using internet-banking, because

they can cheaper, easier and faster do main bank operations.

According to Snoras bank employees‘ opinion, e-banking advantages are, that e-banking

consumers save many time and can dispose of their saving at any day time.

Employees‘ of commercial banks of Lithuania stated some e-banking disadvantages.

According to them, one of the main disadvantages of e-banking development is e-signature

is unavailable yet. Therefore, initial documents are only papers with real signatures.

Banks, which decide to lend for their clients internet-banking services and expand it, has

more attention give for services advertisement and its lending for consumers. According to

Ukio bank, bank which wants have more internet-banking clients‘, ought give more assets

for the advertisement of services and potential consumers‘ motivation and teaching. With

ELECTRONIC BANKING IN LITHUANIA AND HUNGARY - A CO-OPERATIVE RESEARCH

239

this idea agree and Siaulių bank employees. According to them, for majority of banks

clients are lacking in information about e-banking services, therefore baks, in order to have

more those services consumers‘, have to appoint with advertisement.

Parex bank members mostly attention appoint to safety. If it is not enough attention is

appointed on clients data protection, it will be possible in breaks in bank information system

or clients‘ data bases. Then can be appropriated clients‘ accounts money or damaged data

bases. Bank employees could be dangerous, too. In selfish cases they can change clients

data for appropriation their money. Risk for safety can do virus appeared in information

system.

Clients of commercial banks of Lithuania and internet-banking emphasize those services

advantages, i.a., in 24 hours period via day it is possible:

access to the account and review useful information;

know or calculate currency rate;

pay for aids.

Positively internet-banking services appreciate accountants of companies, because with help

of internet-banking systems they can see all accounts balance, tranfers history,

accomplished commission history and information about it.

Often for important clients banks give exclusive conditions by automating their accountancy

systems, clients‘ data bases relating with payment commission.

So, internet-banking has few disadvantages, however by the viewpoint of consumers‘ and

bank members‘, internet-banking lending advantages are more important than

disadvantages.

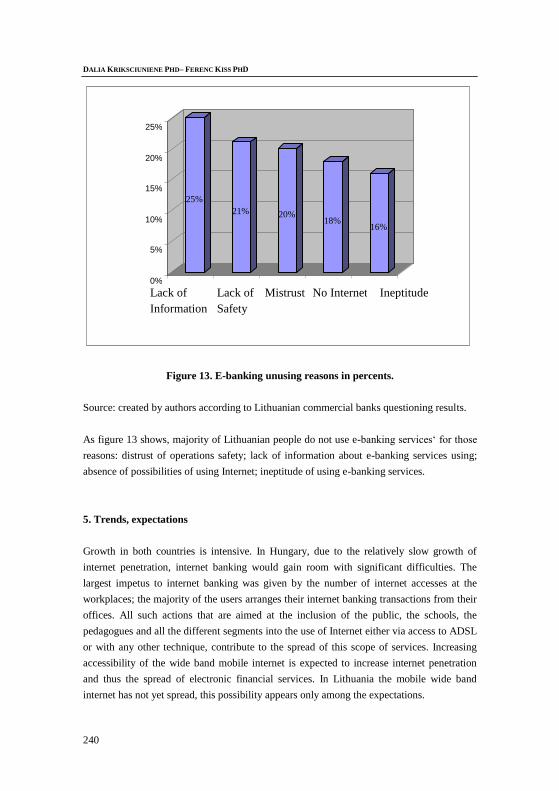

Figure 13 shows how are distributed reasons of e-banking not using which give respondents

who are not use e-banking services‘.

DALIA KRIKSCIUNIENE PHD– FERENC KISS PHD

240

Figure 13. E-banking unusing reasons in percents.

Source: created by authors according to Lithuanian commercial banks questioning results.

As figure 13 shows, majority of Lithuanian people do not use e-banking services‘ for those

reasons: distrust of operations safety; lack of information about e-banking services using;

absence of possibilities of using Internet; ineptitude of using e-banking services.

5. Trends, expectations

Growth in both countries is intensive. In Hungary, due to the relatively slow growth of

internet penetration, internet banking would gain room with significant difficulties. The

largest impetus to internet banking was given by the number of internet accesses at the

workplaces; the majority of the users arranges their internet banking transactions from their

offices. All such actions that are aimed at the inclusion of the public, the schools, the

pedagogues and all the different segments into the use of Internet either via access to ADSL

or with any other technique, contribute to the spread of this scope of services. Increasing

accessibility of the wide band mobile internet is expected to increase internet penetration

and thus the spread of electronic financial services. In Lithuania the mobile wide band

internet has not yet spread, this possibility appears only among the expectations.

25%

21% 20% 18%

16%

0%

5%

10%

15%

20%

25%

Lack of

Information

Mistrust Lack of

Safety

No Internet Ineptitude

ELECTRONIC BANKING IN LITHUANIA AND HUNGARY - A CO-OPERATIVE RESEARCH

241

In both countries the confidentiality problems are deemed as issues of key importance,

banks and mobile service providers equally struggle with that. The public reacts sensibly to

such problems and in general, the press picks such topics up. Thus the confidence should be

fostered in both countries, which could be achieved by spreading realistic information and

comprehensive knowledge in order that the customers could understand the real advantages

and disadvantages that accompany the use of this technology and thus they could make

grounded decisions.

DALIA KRIKSCIUNIENE PHD– FERENC KISS PHD

242

Bibliography

[1] Levišauskaitė K., Rakevičienė J. [interaktyvus]. 2004 [žiūrėta 6 m. vasario 17d.].

Prieiga per internetą <

http://www.lb.lt/lt/leidiniai/pinigu_studijos2004_2/levisauskaite.pdf>

[2] BNS 2003: Hansa-LTB kortelėmis pavijo Vilniaus banką. – Verslo žinios 15, 4.

[3] ELTA 2003: Internetinė bankininkystė artėja prie 0,5 klientų. – Verslo žinios 131,

7.

[4] Sytas A. 2003a: Mokamųjų kortelių rinka plėsis dar metus. – Verslo žinios 39, 4.

[5] Sytas A. 2003b: Skuba registruotis, neskuba naudotis. – Verslo žinios 31, 5.

[6] Sytas A. 2004: Internetiniams bankams trūksta dėmesio klientui. – Verslo žinios

23, 9.

[7] Andružytė R. 2002a: „Nordea“ vilioja mobiliąja bankininkyste. – Verslo žinios

216, 5.

[8] European Parliament 2001: Directive 2001/97/EC of the European Parliament and

of the Council of 4 December 2001 on Prevention of the Use of the Financial

System for the Purpose of Money Laundering.

[9] European Parliament 2000: Directive 2000/31/EC of the European Parliament and

of the Council of 8 June 2000 on Certain Legal Aspects of Informatikon Sodiety

Servines, in Particuliar Electronic Commerce, In the Internal Market.Irodalom 1

[10] MNB (The Hungarian National Bank): The payment card business in Hungary

2005,

http://english.mnb.hu/resource.aspx?resourceID=mnbfile&resourcename=fizkar_2

005_en

[11] GKI – Report on the internet-economy (Focusing on the financial sector) 2005.

http://www.gki.hu/index.php?cid=432&lang=hu

[12] GfK Hungária: 2006-ban nem nőtt számottevően a banki kapcsolattal rendelkezők

aránya (sajtóközlemény), Financial data services, 2006,

http://www.gfk.hu/sajtokoz/fr4.htm

[13] GfK - FESSEL: Minden harmadik európai rendelkezik internet-hozzáféréssel

(sajtóközlemény), http://www.gfk.hu/sajtokoz/fr5.htm

[14] ITTK: Kutatási Jelentés 2005, INFONIA Alapítvány - INFINIT Műhely, Budapest

2006, p. 6-30.

Related Documents