T r e n d s o f Y o u r B u s i n e s s E x c l u s i v e l y d i s t r i b u t e d b y India, Q4 2010 Electric Power Generation, Transmission and Distribution Please address all comments and enquiries to: [email protected] ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF. Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

T r e n d s o f Y o u r B u s i n e s s

E x c l u s i v e l y d i s t r i b u t e d b y

India, Q4 2010

Electric Power Generation, Transmission and Distribution

Please address all comments and enquiries to: [email protected]

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-2-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

! This report has been compiled to the best of the authors’ knowledge, using information originating from verifiedsources. The authors of the report take no responsibility for the consequences of any decisions and actions taken as aresult of the use of this report. This report refers to the Indian economy.

Contents Page1. Macroeconomic Scenario - 4

2. Analysis of Investment Attractiveness - 5

- Attractiveness Indicators - 5

- Driving Forces of Attractiveness - 5

- Risk-Profitability Maps - 7

3. Analysis of Revenue - 9

- Long-term Trend. Business Cycle. Correlation - 9

- Seasonality in Revenues. Seasonal Adjusted Revenues - 10

4. Concentration in the Sector - 11

5. Analysis of Financial Ratios - 12

- Distributions of Financials in the sector - 12

- General Indicators - 13

- Profitability Ratios - 18

- Liquidity Ratios - 21

- Financial Cycles - 22

- Financial Leverage Ratios - 23

- Production Factors - 25

- Investment Outlays - 27

- Costs - 29

- Structure of Fixed Assets - 33

- Structure of Current Assets - 34

- Structure of Current Liabilities - 35

- Main Leverages - 36

- DuPont’s Pyramid - 37

6. Companies from the Sector - 38

- Top Players - market shares - 38

- Top Players from the Sector - 39

- Listed Companies from the Sector - 40

- Mergers and Acquisitions - 41

7. Key Concepts - 42

- Definitions of Indices - 42

- Definitions of Selected Concepts - 44

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-3-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Analysed sector:

Class Electric Power Generation, Transmission and Distribution

The following sub-classes are included in the class:

Hydroelectric Power Generation Electric Power Transmission, Control, and Distribution Nuclear Electric Power Generation Fossil Fuel Electric Power Generation Other Electric Power Generation

Only the sub-classes marked by an arrow are covered by EconTrends reports.

EconTrends for India is the unique tool for analyzing various Indian industries. It contains description ofmacroeconomic environment, analysis of investment attractiveness, detailed analysis of revenue as well as in-depthanalysis of a wide scope of financial ratios. The report covers not the full sector but only its major part, since it is buildon the bottom-up aggregated financial data on listed companies from the Accord Fintech database reporting onquarterly basis. Quarterly financial data from Income Statement are adjusted to assert their consistency with yearlyaudited figures.

Profitability of a given industry is evaluated on the basis of average forecasted dynamics of EBITDA in two followingquarters. Every industry has a granted profitability mark that ranges from 1 up to 5, which reflects its profitabilityversus other industries. Higher mark indicates higher profitability. Risk of an industry in turn is measured by thestandard deviation of forecasted Profitability Index. Every industry has also an assigned risk mark that ranges from 1up to 5, which reflects its risk versus other industries. Higher mark means here lower risk. Each industry is at the endcharacterized by the following two parameters – its profitability and risk. They are used for evaluation of the short term investment attractiveness, that reflects preferences of investors seeking to maximize their rates of return and tominimize the risk they face.

The final Short-Term Investment Attractiveness Ranking of an analyzed industry explains its relative attractivenesscomparing to other sectors. The lower a position within the ranking the higher is attractiveness of an industry. Changesin this position replicate either changes in profitability or in risk. Additionally like in the case of profitability and riskmeasurement the final attractiveness is graded from 1 to 5, where the highest grade means the highest attractiveness.Lower grade means worse “investment-weather conditions”, so either lower profitability or higher risk. The Short-TermInvestment Attractiveness Ranking is presented according to the structure of the North American IndustryClassification System (NAICS). However the used system of industry classification is not fully compatible with theNational Classification of Activities in India due to Indian statistics - specific factors.

The Short-Term Investment Attractiveness Ranking developed for India under the EconTrends ® methodology is basedon the so called Profitability Index, that shows forecasted dynamics of EBITDA. It serves as a proxy for dynamics ofdirty cash flows in enterprises from a given industry. Fundamental components of the Profitability Index like net salesand EBITDA margin, are forecasted using econometric models. The behavior over time of all these categories isillustrated using appropriate pictograms in the “Map of Forces”.

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-4-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

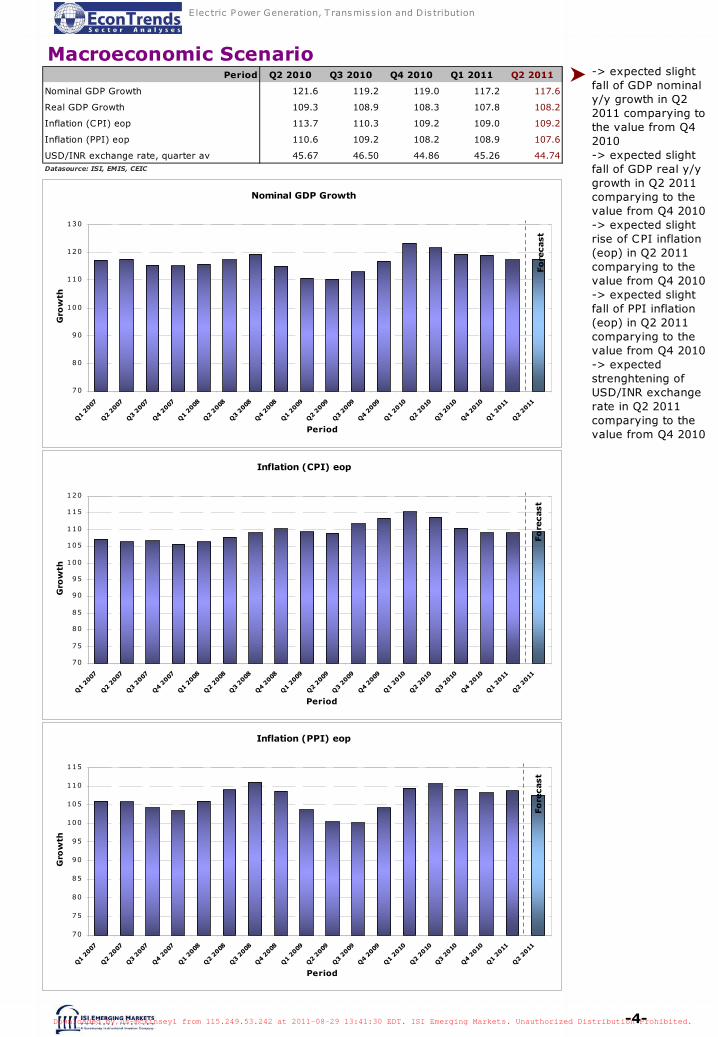

-> expected slight fall of GDP nominal y/y growth in Q2 2011 comparying to the value from Q4 2010-> expected slight fall of GDP real y/y growth in Q2 2011 comparying to the value from Q4 2010-> expected slight rise of CPI inflation (eop) in Q2 2011 comparying to the value from Q4 2010-> expected slight fall of PPI inflation (eop) in Q2 2011 comparying to the value from Q4 2010-> expected strenghtening of USD/INR exchange rate in Q2 2011 comparying to the value from Q4 2010

Macroeconomic Scenario

Nominal GDP Growth

70

80

90

100

110

120

130

Q1 2

007

Q2 2

007

Q3 2

007

Q4 2

007

Q1 2

008

Q2 2

008

Q3 2

008

Q4 2

008

Q1 2

009

Q2 2

009

Q3 2

009

Q4 2

009

Q1 2

010

Q2 2

010

Q3 2

010

Q4 2

010

Q1 2

011

Q2 2

011

Period

Gro

wth

Fo

recast

Period Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011

Nominal GDP Growth 121.6 119.2 119.0 117.2 117.6

Real GDP Growth 109.3 108.9 108.3 107.8 108.2

Inflation (CPI) eop 113.7 110.3 109.2 109.0 109.2

Inflation (PPI) eop 110.6 109.2 108.2 108.9 107.6

USD/INR exchange rate, quarter av 45.67 46.50 44.86 45.26 44.74Datasource: ISI, EMIS, CEIC

Inflation (CPI) eop

70

75

80

85

90

95

100

105

110

115

120

Q1 2

007

Q2 2

007

Q3 2

007

Q4 2

007

Q1 2

008

Q2 2

008

Q3 2

008

Q4 2

008

Q1 2

009

Q2 2

009

Q3 2

009

Q4 2

009

Q1 2

010

Q2 2

010

Q3 2

010

Q4 2

010

Q1 2

011

Q2 2

011

Period

Gro

wth

Fo

recast

Inflation (PPI) eop

70

75

80

85

90

95

100

105

110

115

Q1 2

007

Q2 2

007

Q3 2

007

Q4 2

007

Q1 2

008

Q2 2

008

Q3 2

008

Q4 2

008

Q1 2

009

Q2 2

009

Q3 2

009

Q4 2

009

Q1 2

010

Q2 2

010

Q3 2

010

Q4 2

010

Q1 2

011

Q2 2

011

Period

Gro

wth

Fo

recast

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-5-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

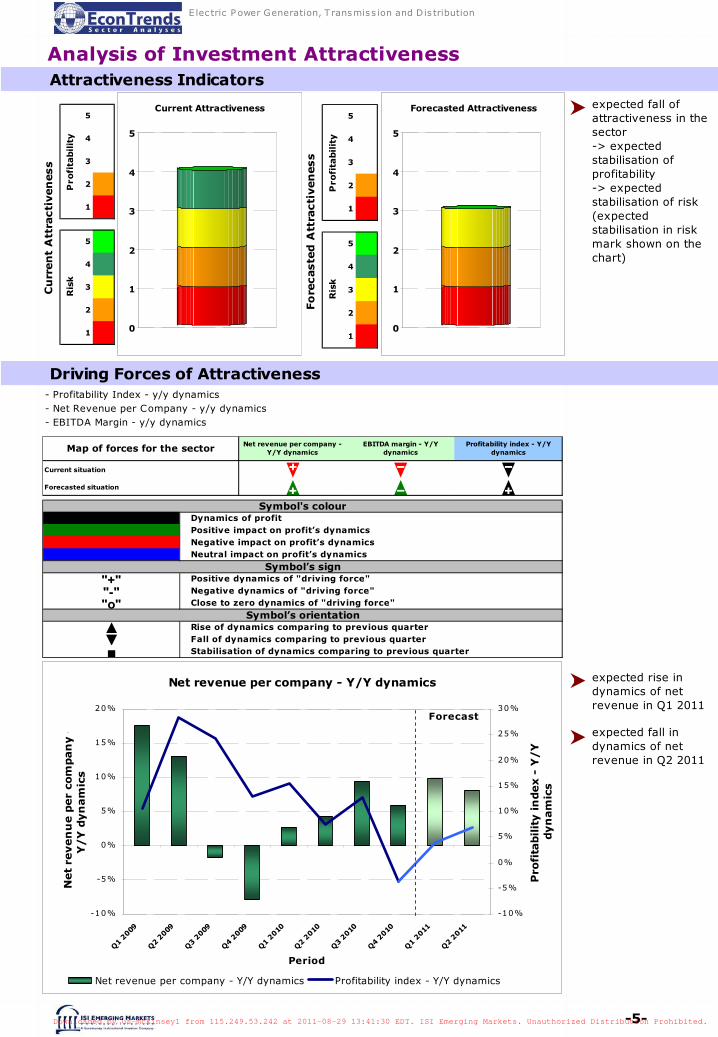

expected fall of attractiveness in the sector-> expected stabilisation of profitability-> expected stabilisation of risk (expected stabilisation in risk mark shown on the chart)

5 0

4 0

3 0

2 1

1 1

5 1

4 1

3 1

2 1

1 1

Cu

rren

t A

ttra

cti

ven

ess

Pro

fita

bilit

yR

isk

0

1

2

3

4

5

Current Attractiveness5 0

4 0

3 0

2 1

1 1

5 1

4 1

3 1

2 1

1 1

Fo

recaste

d A

ttra

cti

ven

ess

Pro

fita

bilit

yR

isk

0

1

2

3

4

5

Forecasted Attractiveness

Driving Forces of Attractiveness - Profitability Index - y/y dynamics- Net Revenue per Company - y/y dynamics - EBITDA Margin - y/y dynamics

Current situation b a aForecasted situation e d e

Map of forces for the sector Net revenue per company - Y/Y dynamics

EBITDA margin - Y/Y dynamics

Profitability index - Y/Y dynamics

"+""-""o"

▲▼■

Symbol's colour Dynamics of profit Positive impact on profit’s dynamics Negative impact on profit’s dynamics Neutral impact on profit’s dynamics

Symbol’s sign

Fall of dynamics comparing to previous quarter Stabilisation of dynamics comparing to previous quarter

Symbol’s orientation Rise of dynamics comparing to previous quarter

Positive dynamics of "driving force" Negative dynamics of "driving force" Close to zero dynamics of "driving force"

expected rise in dynamics of net revenue in Q1 2011

expected fall in dynamics of net revenue in Q2 2011

Analysis of Investment Attractiveness Attractiveness Indicators

Net revenue per company - Y/Y dynamics

-10%

-5%

0%

5%

10%

15%

20%

Q1 2

009

Q2 2

009

Q3 2

009

Q4 2

009

Q1 2

010

Q2 2

010

Q3 2

010

Q4 2

010

Q1 2

011

Q2 2

011

Period

Net

reven

ue p

er

com

pan

y -

Y/Y

dyn

am

ics

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Pro

fita

bilit

y in

dex -

Y/Y

dyn

am

ics

Net revenue per company - Y/Y dynamics Profitability index - Y/Y dynamics

Forecast

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-6-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

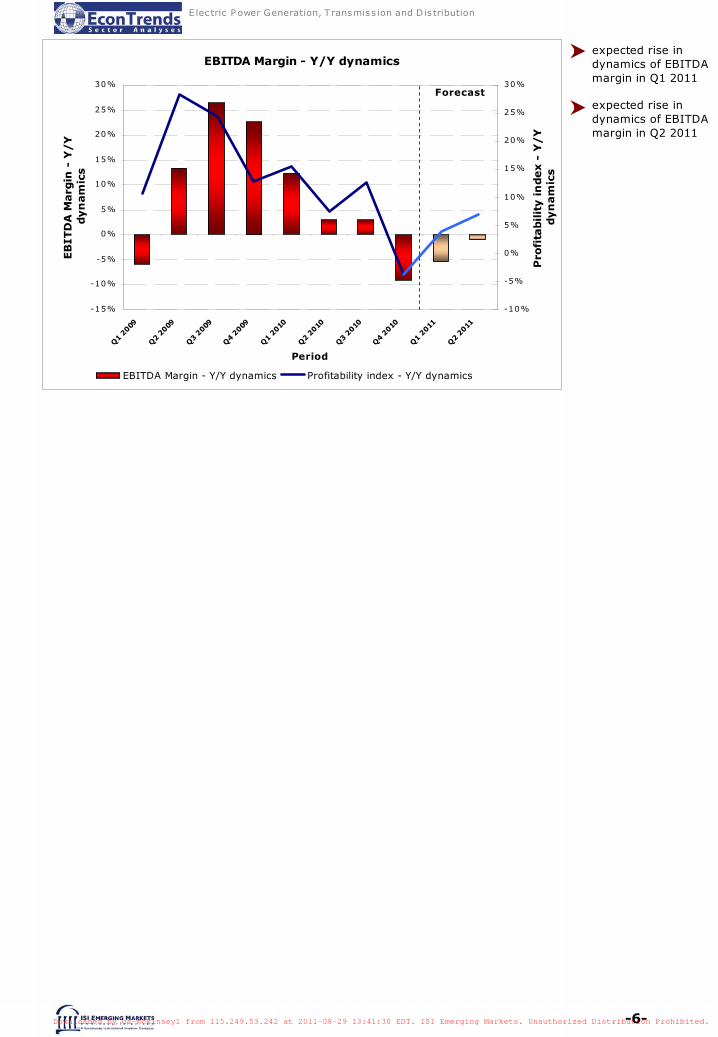

expected rise in dynamics of EBITDA margin in Q1 2011

expected rise in dynamics of EBITDA margin in Q2 2011

EBITDA Margin - Y/Y dynamics

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Q1 2

009

Q2 2

009

Q3 2

009

Q4 2

009

Q1 2

010

Q2 2

010

Q3 2

010

Q4 2

010

Q1 2

011

Q2 2

011

Period

EB

ITD

A M

arg

in -

Y/Y

dyn

am

ics

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Pro

fita

bilit

y in

dex -

Y/Y

dyn

am

ics

EBITDA Margin - Y/Y dynamics Profitability index - Y/Y dynamics

Forecast

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-7-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Risk-Profitability Maps

Risk - Profitability Map (current situation)

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

0.0 0.2 0.4 0.6 0.8 1.0 1.2

Risk

Pro

fita

bil

ity

All sectorsMost efficient sectorssub-classes belonging to selected groupSelected sector (C lass): Electric Power Generation, Transmission and DistributionInvestors' utility function

Risk - Profitability Map (current situation)Zoom

0.00

0.02

0.04

0.06

0.08

0.10

0.12

0.00 0.02 0.04 0.06 0.08 0.10 0.12 0.14

Risk

Pro

fita

bil

ity

All sectorsMost efficient sectorssub-classes belonging to selected groupSelected sector (Class): Electric Power Generation, Transmission and DistributionInvestors' utility function

risk - profitability map (current situation)

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-8-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

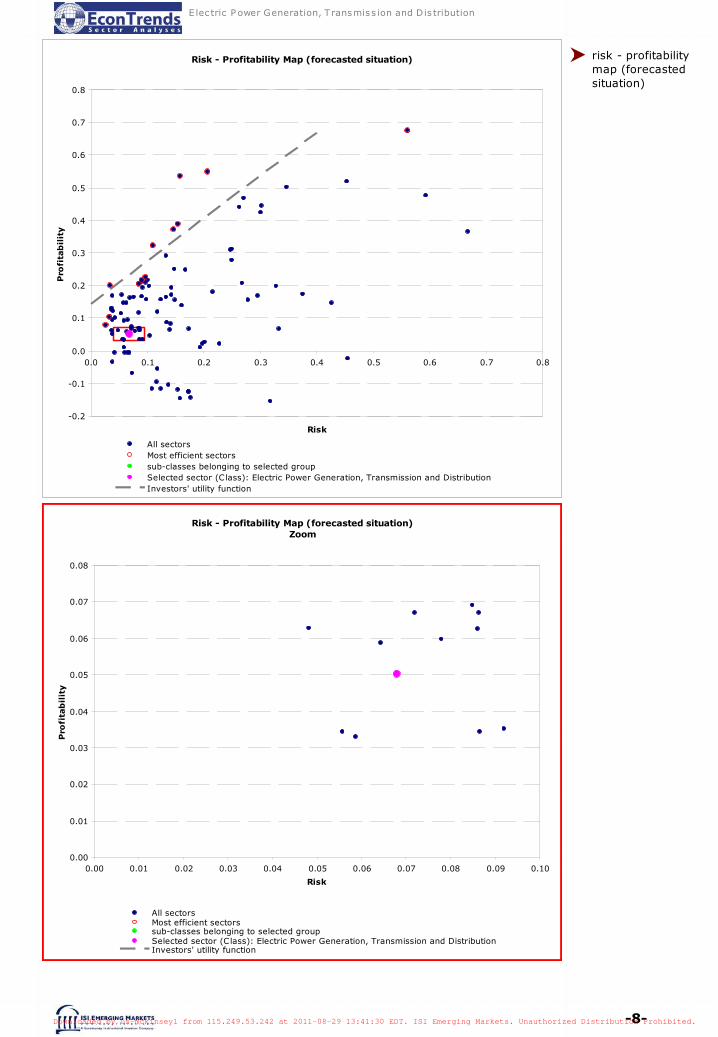

risk - profitability map (forecasted situation)

Risk - Profitability Map (forecasted situation)

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8

Risk

Pro

fita

bil

ity

All sectorsMost efficient sectorssub-classes belonging to selected groupSelected sector (C lass): Electric Power Generation, Transmission and DistributionInvestors' utility function

Risk - Profitability Map (forecasted situation)Zoom

0.00

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

0.00 0.01 0.02 0.03 0.04 0.05 0.06 0.07 0.08 0.09 0.10

Risk

Pro

fita

bil

ity

All sectorsMost efficient sectorssub-classes belonging to selected groupSelected sector (Class): Electric Power Generation, Transmission and DistributionInvestors' utility function

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-9-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

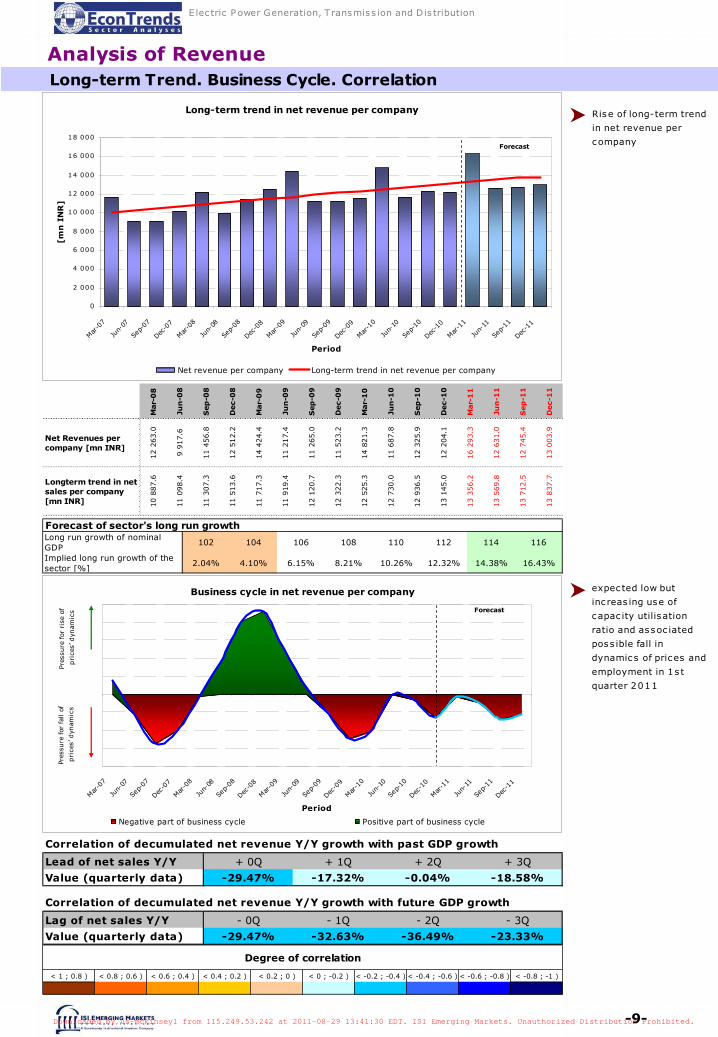

Analysis of Revenue Long-term Trend. Business Cycle. Correlation

Long-term trend in net revenue per company

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

Mar

-07

Jun-

07

Sep-

07

Dec-0

7

Mar-0

8

Jun-

08

Sep-08

Dec-0

8

Mar

-09

Jun-

09

Sep-

09

Dec-0

9

Mar

-10

Jun-

10

Sep-

10

Dec-1

0

Mar

-11

Jun-

11

Sep-

11

Dec-1

1

Period

[mn

IN

R]

Net revenue per company Long-term trend in net revenue per company

ForecastM

ar-

08

Jun

-08

Sep

-08

Dec-0

8

Mar-

09

Jun

-09

Sep

-09

Dec-0

9

Mar-

10

Jun

-10

Sep

-10

Dec-1

0

Mar-

11

Jun

-11

Sep

-11

Dec-1

1

Net Revenues per company [mn INR]

12 2

63.0

9 9

17.6

11 4

56.8

12 5

12.2

14 4

24.4

11 2

17.4

11 2

65.0

11 5

23.2

14 8

21.3

11 6

87.8

12 3

25.9

12 2

04.1

16 2

93.3

12 6

31.0

12 7

45.4

13 0

03.9

Longterm trend in net sales per company [mn INR] 1

0 8

87.6

11 0

98.4

11 3

07.3

11 5

13.6

11 7

17.3

11 9

19.4

12 1

20.7

12 3

22.3

12 5

25.3

12 7

30.0

12 9

36.5

13 1

45.0

13 3

56.2

13 5

69.8

13 7

12.5

13 8

37.7

Long run growth of nominal GDP

102 104 106 108 110 112 114 116

Implied long run growth of the sector [%]

2.04% 4.10% 6.15% 8.21% 10.26% 12.32% 14.38% 16.43%

Forecast of sector's long run growth

Rise of long-term trend

in net revenue per

company

expec ted low but

inc reas ing use of

capac ity utilisation

ratio and assoc iated

poss ible fall in

dynamics of prices and

employment in 1s t

quarter 2011

Business cycle in net revenue per company

Mar

-07

Jun-

07

Sep-07

Dec-0

7

Mar

-08

Jun-

08

Sep-

08

Dec-0

8

Mar

-09

Jun-

09

Sep-

09

Dec-0

9

Mar-1

0

Jun-

10

Sep-10

Dec-1

0

Mar

-11

Jun-

11

Sep-

11

Dec-1

1

Period

Negative part of business cycle Positive part of business cycle

Pres

sure

for

ris

e of

pri

ces’

dyn

amic

s

Pres

sure

for

fal

l of

pri

ces’

dyn

amic

s

Forecast

Lead of net sales Y/Y + 0Q + 1Q + 2Q + 3Q

Value (quarterly data) -29.47% -17.32% -0.04% -18.58%

Lag of net sales Y/Y - 0Q - 1Q - 2Q - 3Q

Value (quarterly data) -29.47% -32.63% -36.49% -23.33%

Correlation of decumulated net revenue Y/Y growth with past GDP growth

Correlation of decumulated net revenue Y/Y growth with future GDP growth

< 1 ; 0.8 ) < 0.8 ; 0.6 ) < 0.6 ; 0.4 ) < 0.4 ; 0.2 ) < 0.2 ; 0 ) < 0 ; -0.2 ) < -0.2 ; -0.4 ) < -0.4 ; -0.6 ) < -0.6 ; -0.8 ) < -0.8 ; -1 )

Degree of correlation

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-10-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

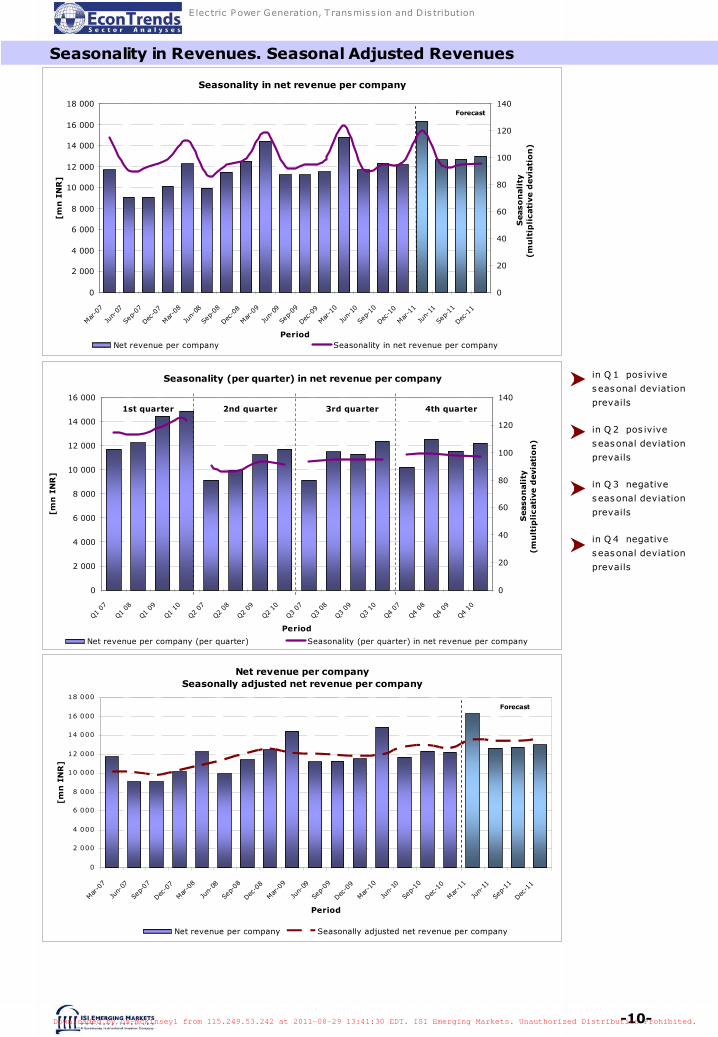

Seasonality in Revenues. Seasonal Adjusted Revenues

in Q 1 pos ivive

seasonal deviation

prevails

in Q 2 pos ivive

seasonal deviation

prevails

in Q 3 negative

seasonal deviation

prevails

in Q 4 negative

seasonal deviation

prevails

Seasonality in net revenue per company

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

Mar

-07

Jun-

07

Sep-

07

Dec-0

7

Mar-0

8

Jun-

08

Sep-

08

Dec-0

8

Mar

-09

Jun-

09

Sep-09

Dec-0

9

Mar-1

0

Jun-

10

Sep-

10

Dec-1

0

Mar

-11

Jun-

11

Sep-11

Dec-1

1

Period

[mn

IN

R]

0

20

40

60

80

100

120

140

Seaso

nali

ty(m

ult

ipli

cati

ve d

evia

tio

n)

Net revenue per company Seasonality in net revenue per company

Forecast

Seasonality (per quarter) in net revenue per company

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

Q1 07

Q1 08

Q1 09

Q1 10

Q2 07

Q2 08

Q2 09

Q2 10

Q3 07

Q3 08

Q3 09

Q3 10

Q4 07

Q4 08

Q4 09

Q4 10

Period

[mn

IN

R]

0

20

40

60

80

100

120

140

Seaso

nali

ty(m

ult

ipli

cati

ve d

evia

tio

n)

Net revenue per company (per quarter) Seasonality (per quarter) in net revenue per company

1st quarter 2nd quarter 3rd quarter 4th quarter

Net revenue per company Seasonally adjusted net revenue per company

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

Mar

-07

Jun-

07

Sep-

07

Dec-0

7

Mar

-08

Jun-

08

Sep-08

Dec-0

8

Mar

-09

Jun-

09

Sep-

09

Dec-0

9

Mar

-10

Jun-

10

Sep-

10

Dec-1

0

Mar

-11

Jun-

11

Sep-11

Dec-1

1

Period

[mn

IN

R]

Net revenue per company Seasonally adjusted net revenue per company

Forecast

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-11-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

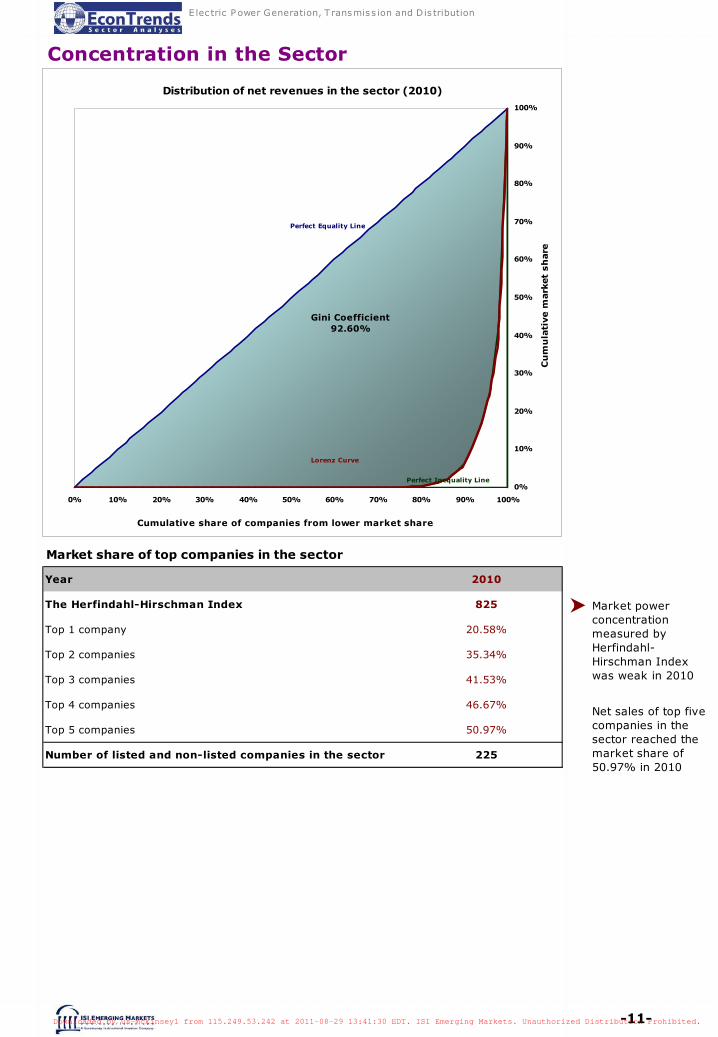

Market power concentration measured by Herfindahl-Hirschman Index was weak in 2010

Net sales of top five companies in the sector reached the market share of 50.97% in 2010

Market share of top companies in the sector

Year 2010

The Herfindahl-Hirschman Index 825

Top 1 company 20.58%

Top 2 companies 35.34%

Top 3 companies 41.53%

Top 4 companies 46.67%

Top 5 companies 50.97%

Number of listed and non-listed companies in the sector 225

Concentration in the Sector

Distribution of net revenues in the sector (2010)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Cumulative share of companies from lower market share

Cu

mu

lati

ve m

ark

et

sh

are

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Gini Coefficient92.60%

Lorenz Curve

Perfect Inequality Line

Perfect Equality Line

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-12-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Source: ISI , EM IS, C EIC

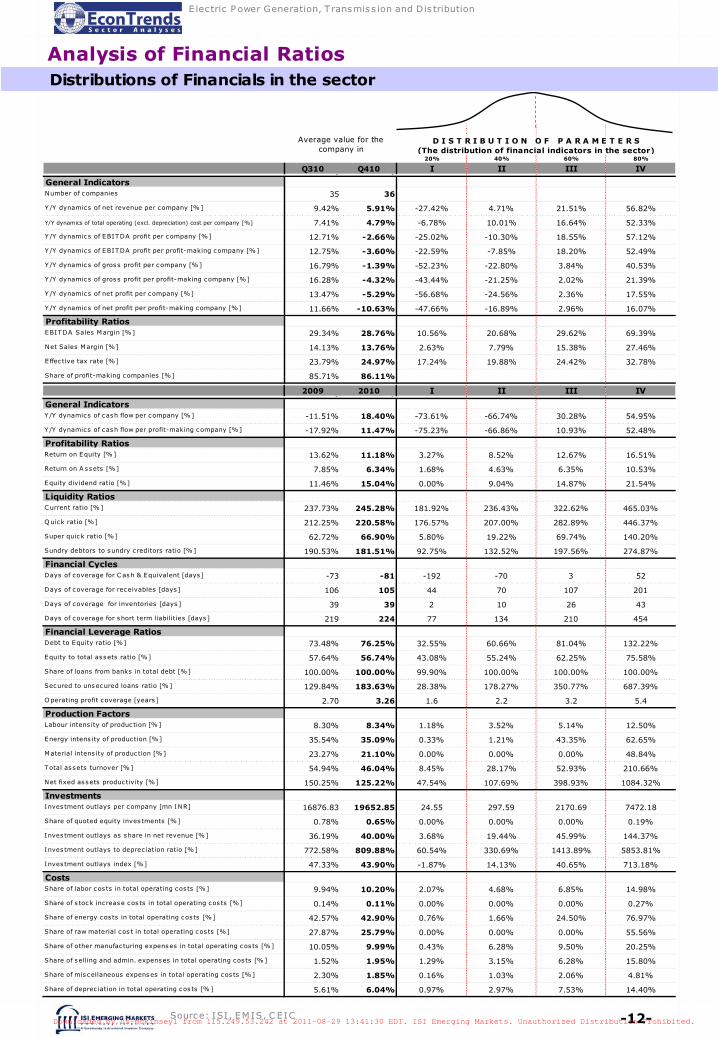

Analysis of Financial Ratios Distributions of Financials in the sector

20% 40% 60% 80%

Q310 Q410 I II III IV0 0General IndicatorsNumber of companies 35 36

Y /Y dynamics of net revenue per company [%] 9.42% 5.91% -27.42% 4.71% 21.51% 56.82%

Y/Y dynamics of total operating (excl. depreciation) cost per company [%] 7.41% 4.79% -6.78% 10.01% 16.64% 52.33%

Y/Y dynamics of EBITDA profit per company [%] 12.71% -2.66% -25.02% -10.30% 18.55% 57.12%

Y/Y dynamics of EBITDA profit per profit-making company [%] 12.75% -3.60% -22.59% -7.85% 18.20% 52.49%

Y/Y dynamics of gross profit per company [%] 16.79% -1.39% -52.23% -22.80% 3.84% 40.53%

Y/Y dynamics of gross profit per profit-making company [%] 16.28% -4.32% -43.44% -21.25% 2.02% 21.39%

Y/Y dynamics of net profit per company [%] 13.47% -5.29% -56.68% -24.56% 2.36% 17.55%

Y/Y dynamics of net profit per profit-making company [%] 11.66% -10.63% -47.66% -16.89% 2.96% 16.07%

Profitability RatiosEBITDA Sales Margin [%] 29.34% 28.76% 10.56% 20.68% 29.62% 69.39%

Net Sales Margin [%] 14.13% 13.76% 2.63% 7.79% 15.38% 27.46%

Effec tive tax rate [%] 23.79% 24.97% 17.24% 19.88% 24.42% 32.78%

Share of profit-making companies [%] 85.71% 86.11%

D I S T R I B U T I O N O F P A R A M E T E R S(The distribution of financial indicators in the sector)

Average value for the company in

2009 2010 I II III IV0 0General IndicatorsY /Y dynamics of cash flow per company [%] -11.51% 18.40% -73.61% -66.74% 30.28% 54.95%

Y/Y dynamics of cash flow per profit-making company [%] -17.92% 11.47% -75.23% -66.86% 10.93% 52.48%

Profitability RatiosReturn on Equity [%] 13.62% 11.18% 3.27% 8.52% 12.67% 16.51%

Return on A ssets [%] 7.85% 6.34% 1.68% 4.63% 6.35% 10.53%

Equity dividend ratio [%] 11.46% 15.04% 0.00% 9.04% 14.87% 21.54%

Liquidity RatiosC urrent ratio [%] 237.73% 245.28% 181.92% 236.43% 322.62% 465.03%

Q uick ratio [%] 212.25% 220.58% 176.57% 207.00% 282.89% 446.37%

Super quick ratio [%] 62.72% 66.90% 5.80% 19.22% 69.74% 140.20%

Sundry debtors to sundry c reditors ratio [%] 190.53% 181.51% 92.75% 132.52% 197.56% 274.87%

Financial CyclesDays of coverage for C ash & Equivalent [days] -73 -81 -192 -70 3 52

Days of coverage for receivables [days] 106 105 44 70 107 201

Days of coverage for inventories [days ] 39 39 2 10 26 43

Days of coverage for short term liabilities [days] 219 224 77 134 210 454

Financial Leverage RatiosDebt to Equity ratio [%] 73.48% 76.25% 32.55% 60.66% 81.04% 132.22%

Equity to total assets ratio [%] 57.64% 56.74% 43.08% 55.24% 62.25% 75.58%

Share of loans from banks in total debt [%] 100.00% 100.00% 99.90% 100.00% 100.00% 100.00%

Secured to unsecured loans ratio [%] 129.84% 183.63% 28.38% 178.27% 350.77% 687.39%

O perating profit coverage [years] 2.70 3.26 1.6 2.2 3.2 5.4

Production FactorsLabour intens ity of produc tion [%] 8.30% 8.34% 1.18% 3.52% 5.14% 12.50%

Energy intens ity of production [%] 35.54% 35.09% 0.33% 1.21% 43.35% 62.65%

Material intens ity of produc tion [%] 23.27% 21.10% 0.00% 0.00% 0.00% 48.84%

Total as sets turnover [%] 54.94% 46.04% 8.45% 28.17% 52.93% 210.66%

Net fixed assets produc tivity [%] 150.25% 125.22% 47.54% 107.69% 398.93% 1084.32%

InvestmentsInves tment outlays per company [mn INR] 16876.83 19652.85 24.55 297.59 2170.69 7472.18

Share of quoted equity inves tments [%] 0.78% 0.65% 0.00% 0.00% 0.00% 0.19%

Investment outlays as share in net revenue [%] 36.19% 40.00% 3.68% 19.44% 45.99% 144.37%

Investment outlays to deprec iation ratio [%] 772.58% 809.88% 60.54% 330.69% 1413.89% 5853.81%

Investment outlays index [%] 47.33% 43.90% -1.87% 14.13% 40.65% 713.18%

CostsShare of labor cos ts in total operating cos ts [%] 9.94% 10.20% 2.07% 4.68% 6.85% 14.98%

Share of s tock inc rease cos ts in total operating cos ts [%] 0.14% 0.11% 0.00% 0.00% 0.00% 0.27%

Share of energy cos ts in total operating cos ts [%] 42.57% 42.90% 0.76% 1.66% 24.50% 76.97%

Share of raw material cos t in total operating cos ts [%] 27.87% 25.79% 0.00% 0.00% 0.00% 55.56%

Share of other manufac turing expenses in total operating cos ts [%] 10.05% 9.99% 0.43% 6.28% 9.50% 20.25%

Share of selling and admin. expenses in total operating cos ts [%] 1.52% 1.95% 1.29% 3.15% 6.28% 15.80%

Share of mis cellaneous expenses in total operating cos ts [%] 2.30% 1.85% 0.16% 1.03% 2.06% 4.81%

Share of deprec iation in total operating cos ts [%] 5.61% 6.04% 0.97% 2.97% 7.53% 14.40%

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-13-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Source: ISI , EM IS, C EIC

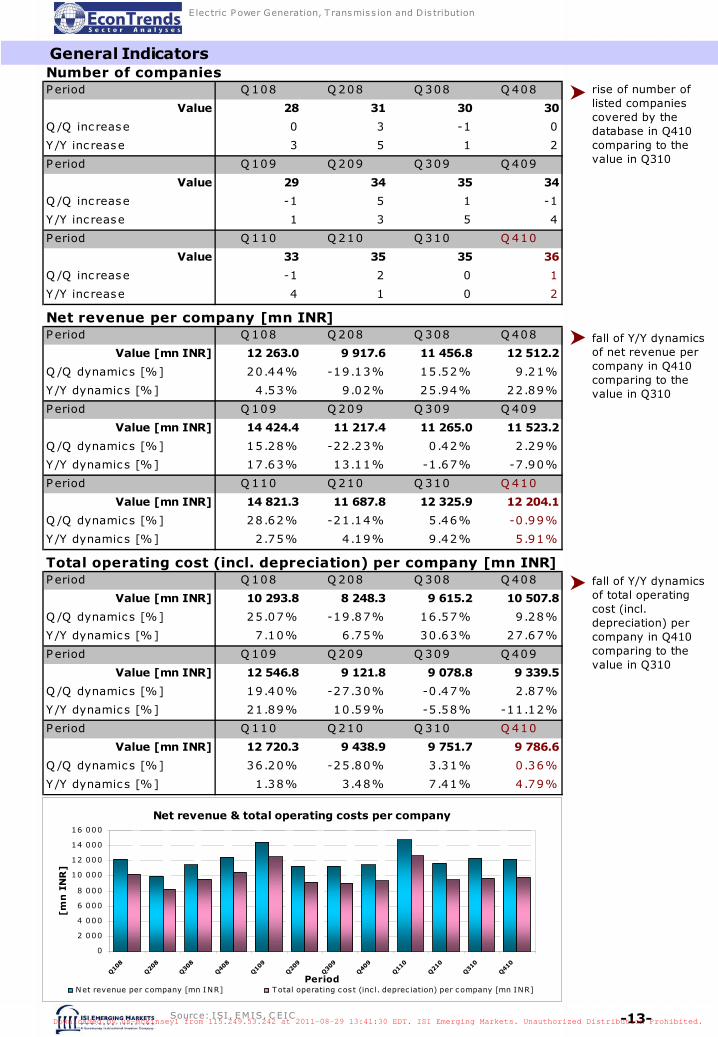

Number of companiesPeriod Q 108 Q 208 Q 308 Q 408

Value 28 31 30 30

Q /Q inc rease 0 3 -1 0

Y/Y inc rease 3 5 1 2

Period Q 109 Q 209 Q 309 Q 409

Value 29 34 35 34

Q /Q inc rease -1 5 1 -1

Y /Y inc rease 1 3 5 4

Period Q 110 Q 210 Q 310 Q 410

Value 33 35 35 36

Q /Q inc rease -1 2 0 1

Y/Y inc rease 4 1 0 2

Net revenue per company [mn INR]Period Q 108 Q 208 Q 308 Q 408

Value [mn INR] 12 263.0 9 917.6 11 456.8 12 512.2

Q /Q dynamics [%] 20.44% -19.13% 15.52% 9.21%

Y/Y dynamics [%] 4.53% 9.02% 25.94% 22.89%

Period Q 109 Q 209 Q 309 Q 409

Value [mn INR] 14 424.4 11 217.4 11 265.0 11 523.2

Q /Q dynamics [%] 15.28% -22.23% 0.42% 2.29%

Y/Y dynamics [%] 17.63% 13.11% -1.67% -7.90%

Period Q 110 Q 210 Q 310 Q 410

Value [mn INR] 14 821.3 11 687.8 12 325.9 12 204.1

Q /Q dynamics [%] 28.62% -21.14% 5.46% -0.99%

Y/Y dynamics [%] 2.75% 4.19% 9.42% 5.91%

Period Q 108 Q 208 Q 308 Q 408

Value [mn INR] 10 293.8 8 248.3 9 615.2 10 507.8

Q /Q dynamics [%] 25.07% -19.87% 16.57% 9.28%

Y/Y dynamics [%] 7.10% 6.75% 30.63% 27.67%

Period Q 109 Q 209 Q 309 Q 409

Value [mn INR] 12 546.8 9 121.8 9 078.8 9 339.5

Q /Q dynamics [%] 19.40% -27.30% -0.47% 2.87%

Y/Y dynamics [%] 21.89% 10.59% -5.58% -11.12%

Period Q 110 Q 210 Q 310 Q 410

Value [mn INR] 12 720.3 9 438.9 9 751.7 9 786.6

Q /Q dynamics [%] 36.20% -25.80% 3.31% 0.36%

Y/Y dynamics [%] 1.38% 3.48% 7.41% 4.79%

Total operating cost (incl. depreciation) per company [mn INR]

Net revenue & total operating costs per company

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

Q10

8

Q20

8

Q30

8

Q40

8

Q10

9

Q20

9

Q30

9

Q40

9

Q11

0

Q21

0

Q31

0

Q41

0

Period

[mn

IN

R]

Net revenue per company [mn INR] Total operating cos t (inc l. deprec iation) per company [mn INR]

General Indicators

rise of number of listed companies covered by the database in Q410 comparing to the value in Q310

fall of Y/Y dynamics of net revenue per company in Q410 comparing to the value in Q310

fall of Y/Y dynamics of total operating cost (incl. depreciation) per company in Q410 comparing to the value in Q310

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-14-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Source: ISI , EM IS, C EIC

EBITDA profit per company [mn INR]Period Q 108 Q 208 Q 308 Q 408

Value [mn INR] 3 158.1 2 606.7 2 933.9 3 281.1

Q /Q dynamics [%] 2.27% -17.46% 12.55% 11.83%

Y/Y dynamics [%] -3 .79% 9.93% 2.95% 6.25%

Period Q 109 Q 209 Q 309 Q 409

Value [mn INR] 3 642.4 3 127.9 3 350.9 3 647.4

Q /Q dynamics [%] 11.01% -14.13% 7.13% 8.85%

Y/Y dynamics [%] 15.33% 19.99% 14.21% 11.16%

Period Q 110 Q 210 Q 310 Q 410

Value [mn INR] 3 994.1 3 357.9 3 776.8 3 550.3

Q /Q dynamics [%] 9.51% -15.93% 12.48% -6.00%

Y/Y dynamics [%] 9.66% 7.35% 12.71% -2.66%

EBITDA profit per company [mn INR]

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Period

[mn

IN

R]

-5%

0%

5%

10%

15%

20%

25%

Y/Y

dynam

ics

of

EB

ITD

A

pro

fit

per

com

pany (

all

com

panie

s) [

%]

EBITDA profit per company [mn INR] Y /Y dynamics of EBITDA profit per company (all companies) [%]

P eriod Q 108 Q 208 Q 308 Q 408

Value [mn INR] 3 689.7 2 886.0 3 143.6 3 786.8

Q /Q dynamics [%] 15.22% -21.78% 8.93% 20.46%

Y/Y dynamics [%] 7.91% 17.03% 10.31% 18.25%

Period Q 109 Q 209 Q 309 Q 409

Value [mn INR] 4 086.4 3 702.3 3 909.5 4 277.2

Q /Q dynamics [%] 7.91% -9.40% 5.60% 9.40%

Y/Y dynamics [%] 10.75% 28.28% 24.36% 12.95%

Period Q 110 Q 210 Q 310 Q 410

Value [mn INR] 4 718.7 3 976.3 4 408.1 4 123.3

Q /Q dynamics [%] 10.32% -15.73% 10.86% -6.46%

Y/Y dynamics [%] 15.47% 7.40% 12.75% -3.60%

EBITDA profit per profit-making company [mn INR]

EBITDA profit per profit-making company [mn INR]

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

5 000

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Period

[mn

IN

R]

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Y/Y

dynam

ics

of

EB

ITD

A

pro

fit

per

com

pany (

pro

fit-

makin

g c

om

panie

s) [

%]

EBITDA profit per profit-making company [mn INR]Y /Y dynamics of EBITDA profit per company (profit-making companies ) [%]

fall of Y/Y dynamics of EBITDA profit per company in Q410 comparing to the value in Q310

fall of Y/Y dynamics of EBITDA profit per profit-making company in Q410 comparing to the value in Q310

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-15-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Source: ISI , EM IS, C EIC

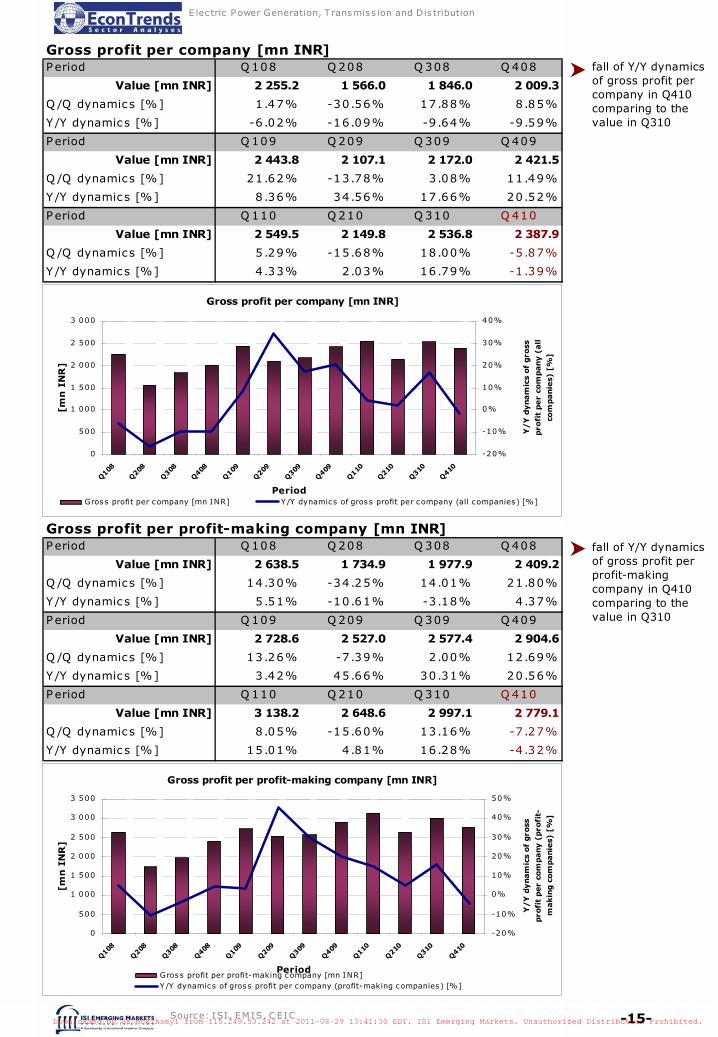

Gross profit per company [mn INR]Period Q 108 Q 208 Q 308 Q 408

Value [mn INR] 2 255.2 1 566.0 1 846.0 2 009.3

Q /Q dynamics [%] 1.47% -30.56% 17.88% 8.85%

Y/Y dynamics [%] -6 .02% -16.09% -9.64% -9.59%

Period Q 109 Q 209 Q 309 Q 409

Value [mn INR] 2 443.8 2 107.1 2 172.0 2 421.5

Q /Q dynamics [%] 21.62% -13.78% 3.08% 11.49%

Y/Y dynamics [%] 8.36% 34.56% 17.66% 20.52%

Period Q 110 Q 210 Q 310 Q 410

Value [mn INR] 2 549.5 2 149.8 2 536.8 2 387.9

Q /Q dynamics [%] 5.29% -15.68% 18.00% -5.87%

Y/Y dynamics [%] 4.33% 2.03% 16.79% -1.39%

Gross profit per profit-making company [mn INR]Period Q 108 Q 208 Q 308 Q 408

Value [mn INR] 2 638.5 1 734.9 1 977.9 2 409.2

Q /Q dynamics [%] 14.30% -34.25% 14.01% 21.80%

Y/Y dynamics [%] 5.51% -10.61% -3.18% 4.37%

Period Q 109 Q 209 Q 309 Q 409

Value [mn INR] 2 728.6 2 527.0 2 577.4 2 904.6

Q /Q dynamics [%] 13.26% -7.39% 2.00% 12.69%

Y/Y dynamics [%] 3.42% 45.66% 30.31% 20.56%

Period Q 110 Q 210 Q 310 Q 410

Value [mn INR] 3 138.2 2 648.6 2 997.1 2 779.1

Q /Q dynamics [%] 8.05% -15.60% 13.16% -7.27%

Y/Y dynamics [%] 15.01% 4.81% 16.28% -4.32%

Gross profit per company [mn INR]

0

500

1 000

1 500

2 000

2 500

3 000

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Period

[mn

IN

R]

-20%

-10%

0%

10%

20%

30%

40%

Y/Y

dynam

ics

of

gro

ss

pro

fit

per

com

pany (

all

com

panie

s) [

%]

Gross profit per company [mn INR] Y /Y dynamics of gross profit per company (all companies ) [%]

Gross profit per profit-making company [mn INR]

0

500

1 000

1 500

2 000

2 500

3 000

3 500

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Period

[mn

IN

R]

-20%

-10%

0%

10%

20%

30%

40%

50%

Y/Y

dynam

ics

of

gro

ss

pro

fit

per

com

pany (

pro

fit-

makin

g c

om

panie

s) [

%]

Gross profit per profit-making company [mn INR]Y /Y dynamics of gross profit per company (profit-making companies) [%]

fall of Y/Y dynamics of gross profit per company in Q410 comparing to the value in Q310

fall of Y/Y dynamics of gross profit per profit-making company in Q410 comparing to the value in Q310

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-16-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Source: ISI , EM IS, C EIC

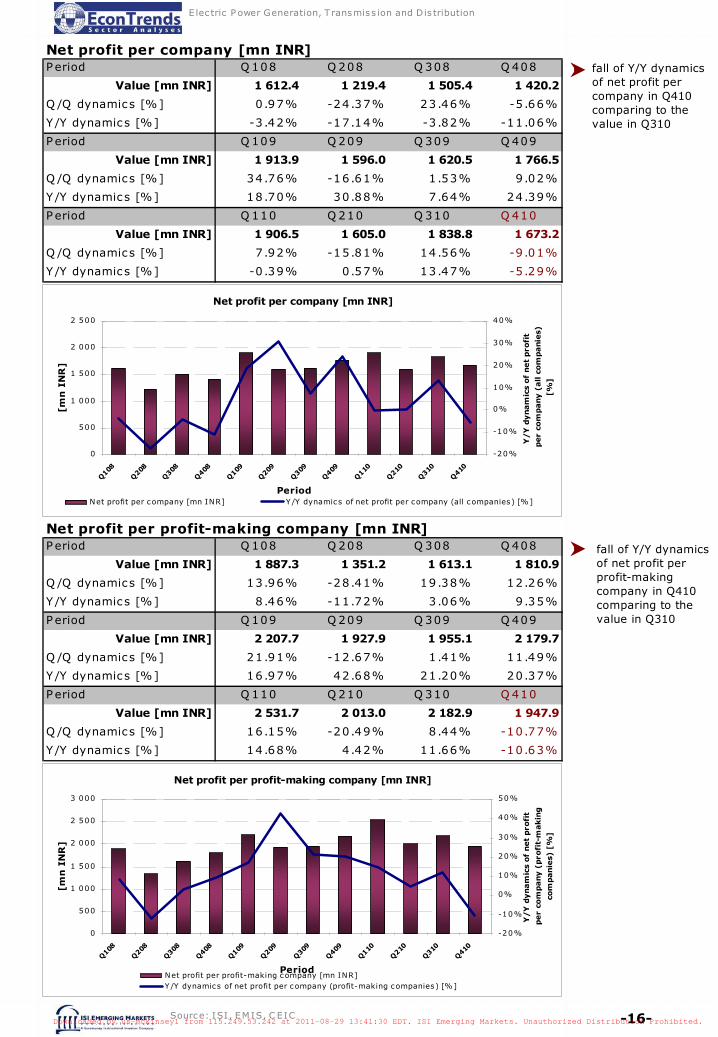

Net profit per company [mn INR]Period Q 108 Q 208 Q 308 Q 408

Value [mn INR] 1 612.4 1 219.4 1 505.4 1 420.2

Q /Q dynamics [%] 0.97% -24.37% 23.46% -5.66%

Y/Y dynamics [%] -3 .42% -17.14% -3.82% -11.06%

Period Q 109 Q 209 Q 309 Q 409

Value [mn INR] 1 913.9 1 596.0 1 620.5 1 766.5

Q /Q dynamics [%] 34.76% -16.61% 1.53% 9.02%

Y/Y dynamics [%] 18.70% 30.88% 7.64% 24.39%

Period Q 110 Q 210 Q 310 Q 410

Value [mn INR] 1 906.5 1 605.0 1 838.8 1 673.2

Q /Q dynamics [%] 7.92% -15.81% 14.56% -9.01%

Y/Y dynamics [%] -0 .39% 0.57% 13.47% -5.29%

Net profit per company [mn INR]

0

500

1 000

1 500

2 000

2 500

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Period

[mn

IN

R]

-20%

-10%

0%

10%

20%

30%

40%

Y/Y

dynam

ics

of

net

pro

fit

per

com

pany (

all c

om

panie

s)

[%]

Net profit per company [mn INR] Y /Y dynamics of net profit per company (all companies) [%]

Net profit per profit-making company [mn INR]Period Q 108 Q 208 Q 308 Q 408

Value [mn INR] 1 887.3 1 351.2 1 613.1 1 810.9

Q /Q dynamics [%] 13.96% -28.41% 19.38% 12.26%

Y/Y dynamics [%] 8.46% -11.72% 3.06% 9.35%

Period Q 109 Q 209 Q 309 Q 409

Value [mn INR] 2 207.7 1 927.9 1 955.1 2 179.7

Q /Q dynamics [%] 21.91% -12.67% 1.41% 11.49%

Y/Y dynamics [%] 16.97% 42.68% 21.20% 20.37%

Period Q 110 Q 210 Q 310 Q 410

Value [mn INR] 2 531.7 2 013.0 2 182.9 1 947.9

Q /Q dynamics [%] 16.15% -20.49% 8.44% -10.77%

Y/Y dynamics [%] 14.68% 4.42% 11.66% -10.63%

Net profit per profit-making company [mn INR]

0

500

1 000

1 500

2 000

2 500

3 000

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Period

[mn

IN

R]

-20%

-10%

0%

10%

20%

30%

40%

50%

Y/Y

dynam

ics

of

net

pro

fit

per

com

pany (

pro

fit-

makin

g

com

panie

s) [

%]

Net profit per profit-making company [mn INR]Y /Y dynamics of net profit per company (profit-making companies) [%]

fall of Y/Y dynamics of net profit per company in Q410 comparing to the value in Q310

fall of Y/Y dynamics of net profit per profit-making company in Q410 comparing to the value in Q310

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-17-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Source: ISI , EM IS, C EIC

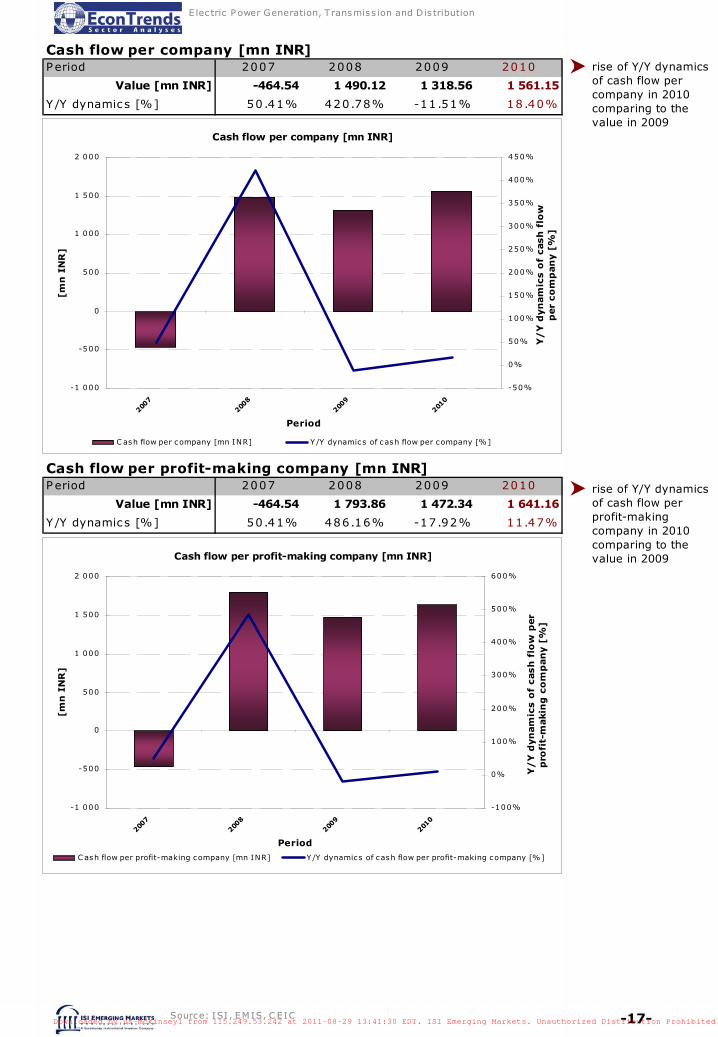

Cash flow per company [mn INR]

-1 000

-500

0

500

1 000

1 500

2 000

2007

2008

2009

2010

Period

[mn

IN

R]

-50%

0%

50%

100%

150%

200%

250%

300%

350%

400%

450%

Y/

Y d

yn

am

ics o

f cash

flo

w

per

co

mp

an

y [

%]

C ash flow per company [mn INR] Y /Y dynamics of cash flow per company [%]

rise of Y/Y dynamics of cash flow per company in 2010 comparing to the value in 2009

Cash flow per company [mn INR]Period 2007 2008 2009 2010

Value [mn INR] -464.54 1 490.12 1 318.56 1 561.15

Y/Y dynamics [%] 50.41% 420.78% -11.51% 18.40%

Cash flow per profit-making company [mn INR]

-1 000

-500

0

500

1 000

1 500

2 000

2007

2008

2009

2010

Period

[mn

IN

R]

-100%

0%

100%

200%

300%

400%

500%

600%

Y/

Y d

yn

am

ics o

f cash

flo

w p

er

pro

fit-

makin

g c

om

pan

y [

%]

C ash flow per profit-making company [mn INR] Y /Y dynamics of cash flow per profit-making company [%]

rise of Y/Y dynamics of cash flow per profit-making company in 2010 comparing to the value in 2009

Cash flow per profit-making company [mn INR]Period 2007 2008 2009 2010

Value [mn INR] -464.54 1 793.86 1 472.34 1 641.16

Y/Y dynamics [%] 50.41% 486.16% -17.92% 11.47%

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-18-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Source: ISI , EM IS, C EIC

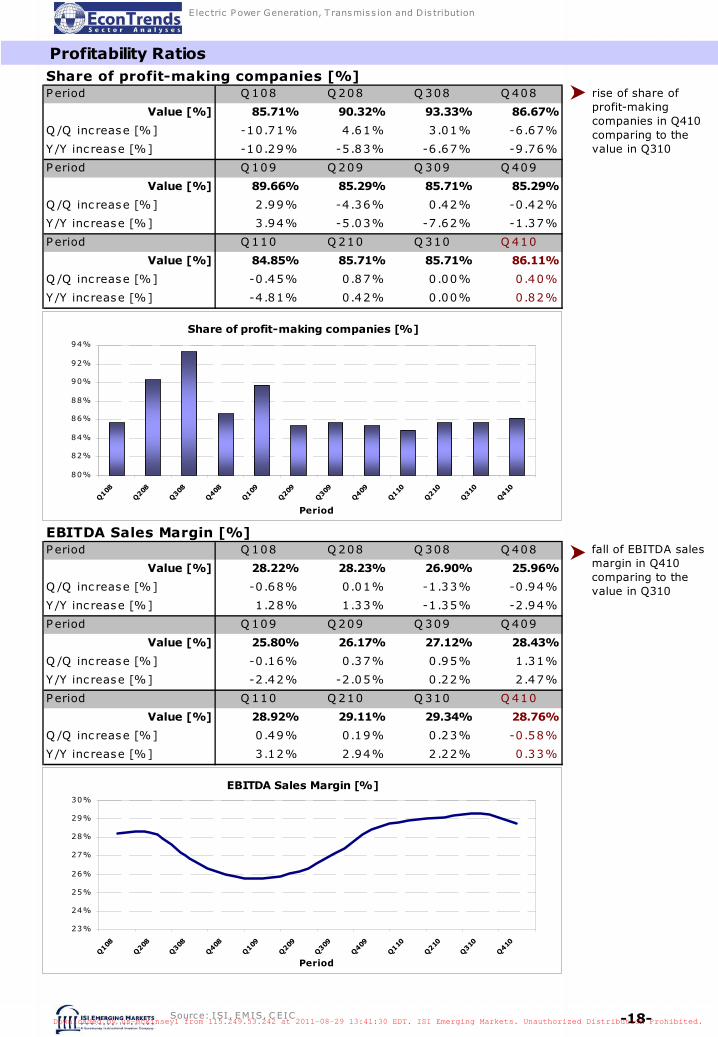

Profitability Ratios Share of profit-making companies [%]Period Q 108 Q 208 Q 308 Q 408

Value [%] 85.71% 90.32% 93.33% 86.67%

Q /Q inc rease [%] -10 .71% 4.61% 3.01% -6.67%

Y/Y inc rease [%] -10 .29% -5.83% -6.67% -9.76%

Period Q 109 Q 209 Q 309 Q 409

Value [%] 89.66% 85.29% 85.71% 85.29%

Q /Q inc rease [%] 2.99% -4.36% 0.42% -0.42%

Y/Y inc rease [%] 3.94% -5.03% -7.62% -1.37%

Period Q 110 Q 210 Q 310 Q 410

Value [%] 84.85% 85.71% 85.71% 86.11%

Q /Q inc rease [%] -0 .45% 0.87% 0.00% 0.40%

Y/Y inc rease [%] -4 .81% 0.42% 0.00% 0.82%

Share of profit-making companies [%]

80%

82%

84%

86%

88%

90%

92%

94%

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Period

EBITDA Sales Margin [%]Period Q 108 Q 208 Q 308 Q 408

Value [%] 28.22% 28.23% 26.90% 25.96%

Q /Q inc rease [%] -0 .68% 0.01% -1.33% -0.94%

Y/Y inc rease [%] 1.28% 1.33% -1.35% -2.94%

Period Q 109 Q 209 Q 309 Q 409

Value [%] 25.80% 26.17% 27.12% 28.43%

Q /Q inc rease [%] -0 .16% 0.37% 0.95% 1.31%

Y/Y inc rease [%] -2 .42% -2.05% 0.22% 2.47%

Period Q 110 Q 210 Q 310 Q 410

Value [%] 28.92% 29.11% 29.34% 28.76%

Q /Q inc rease [%] 0.49% 0.19% 0.23% -0.58%

Y/Y inc rease [%] 3.12% 2.94% 2.22% 0.33%

EBITDA Sales Margin [%]

23%

24%

25%

26%

27%

28%

29%

30%

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Period

rise of share of profit-making companies in Q410 comparing to the value in Q310

fall of EBITDA sales margin in Q410 comparing to the value in Q310

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-19-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Source: ISI , EM IS, C EIC

Net Sales Margin [%]Period Q 108 Q 208 Q 308 Q 408

Value [%] 15.37% 14.46% 13.54% 12.48%

Q /Q inc rease [%] -0 .35% -0.91% -0.92% -1.07%

Y/Y inc rease [%] 0.63% -0.62% -2.34% -3.24%

Period Q 109 Q 209 Q 309 Q 409

Value [%] 12.54% 12.97% 13.26% 14.24%

Q /Q inc rease [%] 0.07% 0.43% 0.28% 0.99%

Y/Y inc rease [%] -2 .83% -1.49% -0.29% 1.77%

Period Q 110 Q 210 Q 310 Q 410

Value [%] 14.11% 13.99% 14.13% 13.76%

Q /Q inc rease [%] -0 .13% -0.12% 0.14% -0.37%

Y/Y inc rease [%] 1.57% 1.02% 0.88% -0.48%

Net Sales Margin [%]

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Period

Effective tax rate [%]Period Q 108 Q 208 Q 308 Q 408

Value [%] 25.66% 25.96% 24.85% 23.95%

Q /Q inc rease [%] -0 .51% 0.30% -1.11% -0.90%

Y/Y inc rease [%] 3.44% 2.38% 0.59% -2.22%

Period Q 109 Q 209 Q 309 Q 409

Value [%] 21.10% 21.60% 22.85% 22.98%

Q /Q inc rease [%] -2 .85% 0.50% 1.25% 0.12%

Y/Y inc rease [%] -4 .56% -4.36% -2.00% -0.97%

Period Q 110 Q 210 Q 310 Q 410

Value [%] 22.90% 22.98% 23.79% 24.97%

Q /Q inc rease [%] -0 .08% 0.08% 0.82% 1.18%

Y/Y inc rease [%] 1.80% 1.37% 0.94% 1.99%

Effective tax rate [%]

0%

5%

10%

15%

20%

25%

30%

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Period

rise of effective tax rate in Q410 comparing to the value in Q310

fall of net sales margin in Q410 comparing to the value in Q310

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-20-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Source: ISI , EM IS, C EIC

Return on Assets [%]Period 2007 2008 2009 2010

Value [%] 13.16% 8.27% 7.85% 6.34%

Y/Y inc rease [%] 0.63% -4.89% -0.42% -1.51%

Equity dividend ratio [%]Period 2007 2008 2009 2010

Value [%] 11.75% 11.75% 11.46% 15.04%

Y/Y inc rease [%] 1.56% 0.00% -0.29% 3.59%

fall of return on assets in 2010 comparing to the value in 2009

rise of equity dividend ratio in 2010 comparing to the value in 2009

Return on Assets [%]

0%

2%

4%

6%

8%

10%

12%

14%

2007

2008

2009

2010

Period

Equity dividend ratio [%]

0%

2%

4%

6%

8%

10%

12%

14%

16%

2007

2008

2009

2010

Period

Return on Equity [%]Period 2007 2008 2009 2010

Value [%] 17.40% 12.99% 13.62% 11.18%

Y/Y inc rease [%] -0 .48% -4.41% 0.62% -2.44%

fall of return on equity in 2010 comparing to the value in 2009

Return on Equity [%]

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

2007

2008

2009

2010

Period

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-21-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Source: ISI , EM IS, C EIC

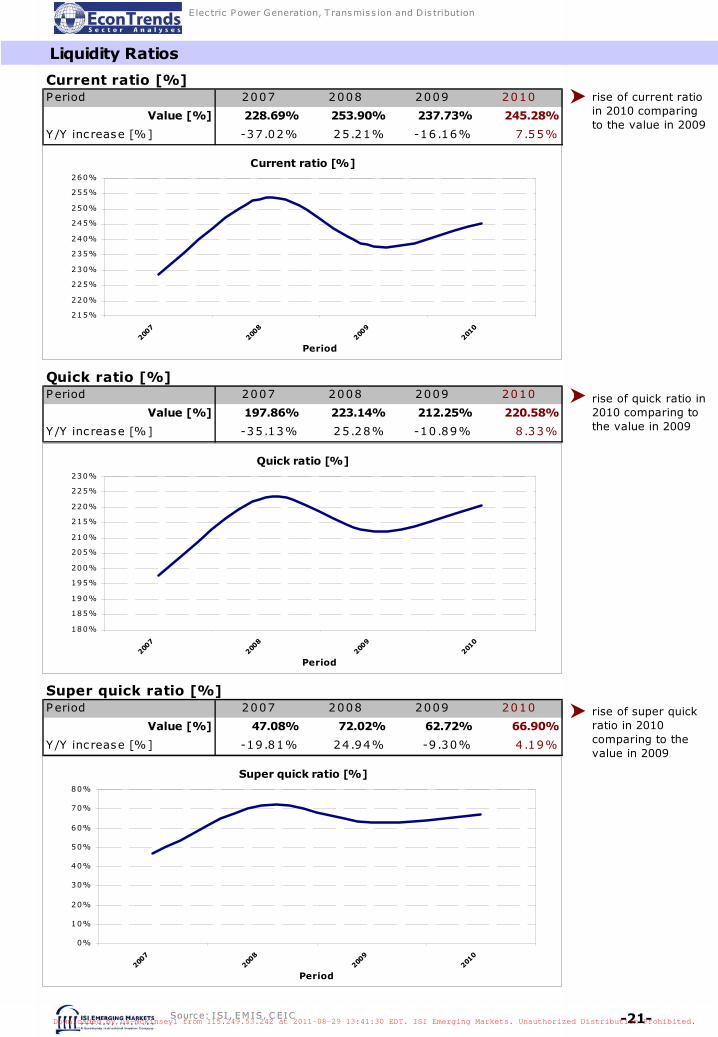

Liquidity Ratios

Current ratio [%]Period 2007 2008 2009 2010

Value [%] 228.69% 253.90% 237.73% 245.28%

Y/Y inc rease [%] -37 .02% 25.21% -16.16% 7.55%

Current ratio [%]

215%

220%

225%

230%

235%

240%

245%

250%

255%

260%

2007

2008

2009

2010

Period

Quick ratio [%]Period 2007 2008 2009 2010

Value [%] 197.86% 223.14% 212.25% 220.58%

Y/Y inc rease [%] -35 .13% 25.28% -10.89% 8.33%

Quick ratio [%]

180%

185%

190%

195%

200%

205%

210%

215%

220%

225%

230%

2007

2008

2009

2010

Period

Super quick ratio [%]Period 2007 2008 2009 2010

Value [%] 47.08% 72.02% 62.72% 66.90%

Y/Y inc rease [%] -19 .81% 24.94% -9.30% 4.19%

Super quick ratio [%]

0%

10%

20%

30%

40%

50%

60%

70%

80%

2007

2008

2009

2010

Period

rise of current ratio in 2010 comparing to the value in 2009

rise of quick ratio in 2010 comparing to the value in 2009

rise of super quick ratio in 2010 comparing to the value in 2009

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-22-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Source: ISI , EM IS, C EIC

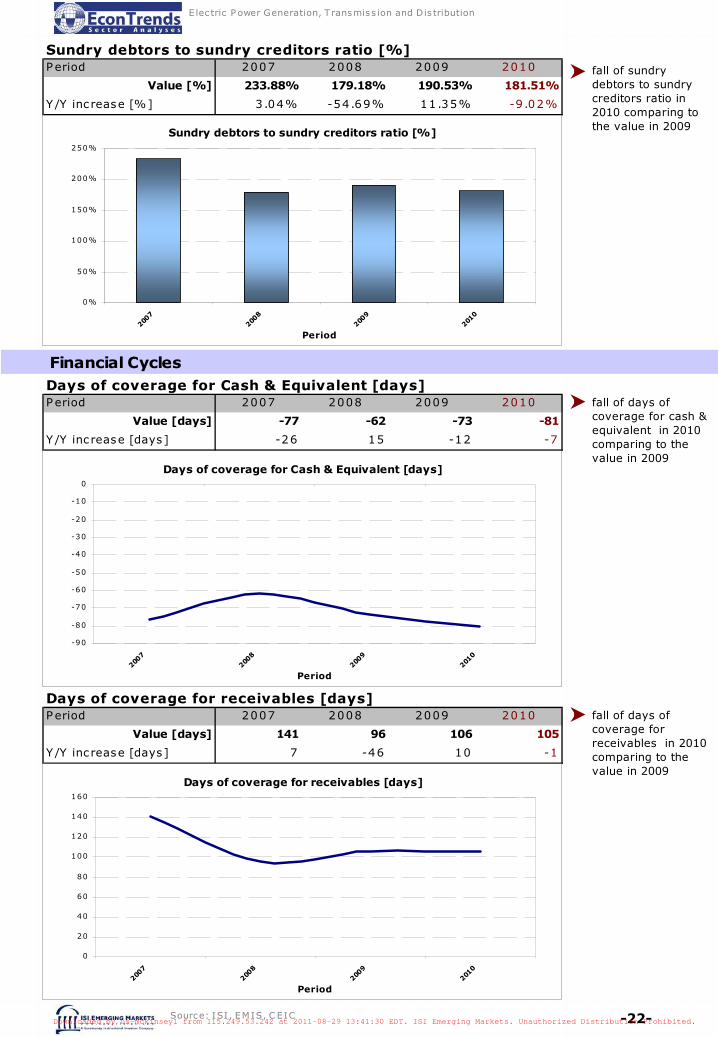

Sundry debtors to sundry creditors ratio [%]Period 2007 2008 2009 2010

Value [%] 233.88% 179.18% 190.53% 181.51%

Y/Y inc rease [%] 3.04% -54.69% 11.35% -9.02%

Sundry debtors to sundry creditors ratio [%]

0%

50%

100%

150%

200%

250%

2007

2008

2009

2010

Period

Financial Cycles

fall of sundry debtors to sundry creditors ratio in 2010 comparing to the value in 2009

Days of coverage for Cash & Equivalent [days]Period 2007 2008 2009 2010

Value [days] -77 -62 -73 -81

Y/Y inc rease [days] -26 15 -12 -7

Days of coverage for Cash & Equivalent [days]

-90

-80

-70

-60

-50

-40

-30

-20

-10

0

2007

2008

2009

2010

Period

Days of coverage for receivables [days]Period 2007 2008 2009 2010

Value [days] 141 96 106 105

Y/Y inc rease [days] 7 -46 10 -1

Days of coverage for receivables [days]

0

20

40

60

80

100

120

140

160

2007

2008

2009

2010

Period

fall of days of coverage for cash & equivalent in 2010 comparing to the value in 2009

fall of days of coverage for receivables in 2010 comparing to the value in 2009

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-23-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Source: ISI , EM IS, C EIC

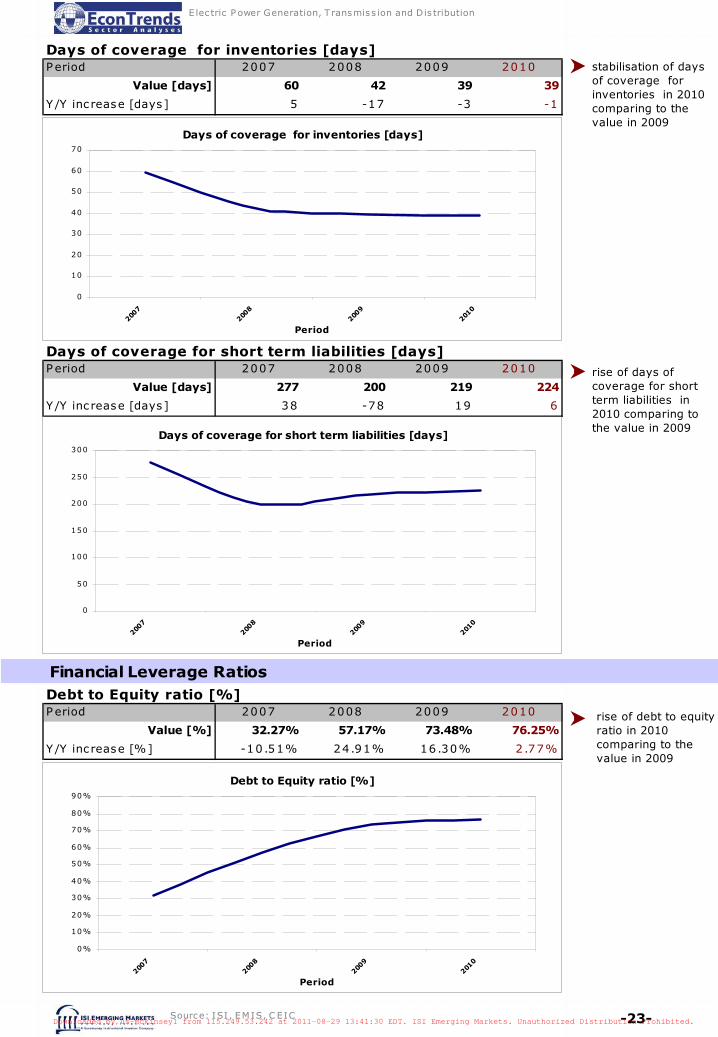

Days of coverage for inventories [days]Period 2007 2008 2009 2010

Value [days] 60 42 39 39

Y/Y inc rease [days] 5 -17 -3 -1

Days of coverage for inventories [days]

0

10

20

30

40

50

60

70

2007

2008

2009

2010

Period

Days of coverage for short term liabilities [days]Period 2007 2008 2009 2010

Value [days] 277 200 219 224

Y/Y inc rease [days] 38 -78 19 6

Days of coverage for short term liabilities [days]

0

50

100

150

200

250

300

2007

2008

2009

2010

Period

stabilisation of days of coverage for inventories in 2010 comparing to the value in 2009

rise of days of coverage for short term liabilities in 2010 comparing to the value in 2009

Financial Leverage Ratios

rise of debt to equity ratio in 2010 comparing to the value in 2009

Debt to Equity ratio [%]Period 2007 2008 2009 2010

Value [%] 32.27% 57.17% 73.48% 76.25%

Y/Y inc rease [%] -10 .51% 24.91% 16.30% 2.77%

Debt to Equity ratio [%]

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2007

2008

2009

2010

Period

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-24-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Source: ISI , EM IS, C EIC

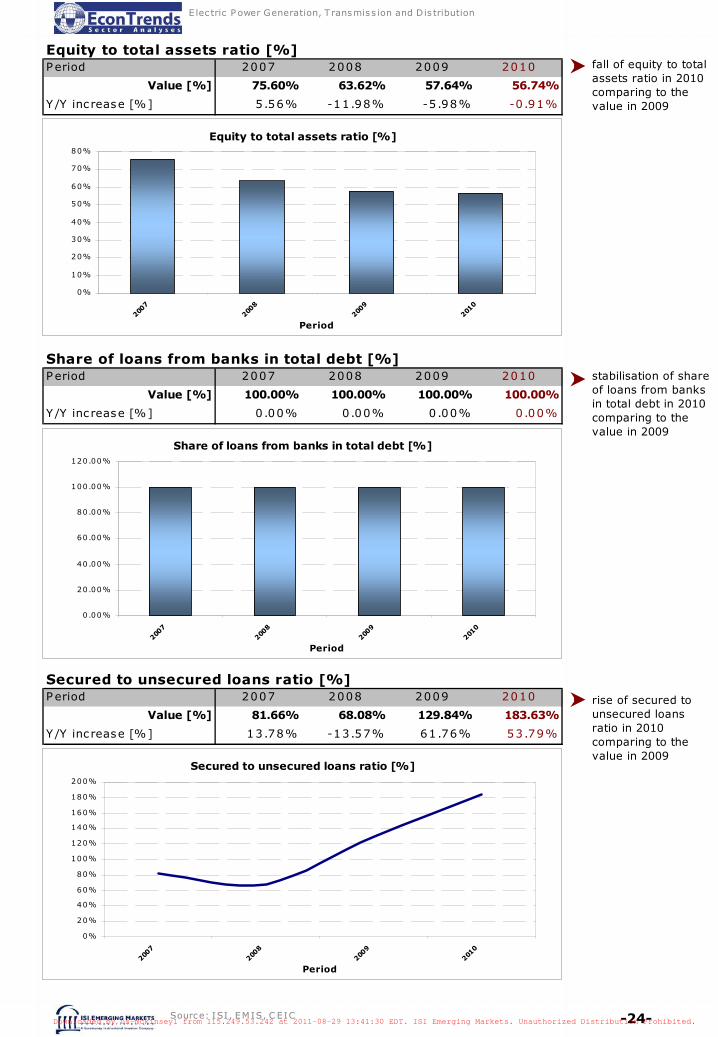

Equity to total assets ratio [%]Period 2007 2008 2009 2010

Value [%] 75.60% 63.62% 57.64% 56.74%

Y/Y inc rease [%] 5.56% -11.98% -5.98% -0.91%

Share of loans from banks in total debt [%]Period 2007 2008 2009 2010

Value [%] 100.00% 100.00% 100.00% 100.00%

Y/Y inc rease [%] 0.00% 0.00% 0.00% 0.00%

Secured to unsecured loans ratio [%]Period 2007 2008 2009 2010

Value [%] 81.66% 68.08% 129.84% 183.63%

Y/Y inc rease [%] 13.78% -13.57% 61.76% 53.79%

Equity to total assets ratio [%]

0%

10%

20%

30%

40%

50%

60%

70%

80%

2007

2008

2009

2010

Period

Share of loans from banks in total debt [%]

0 .00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

2007

2008

2009

2010

Period

Secured to unsecured loans ratio [%]

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

2007

2008

2009

2010

Period

fall of equity to total assets ratio in 2010 comparing to the value in 2009

stabilisation of share of loans from banks in total debt in 2010 comparing to the value in 2009

rise of secured to unsecured loans ratio in 2010 comparing to the value in 2009

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-25-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Source: ISI , EM IS, C EIC

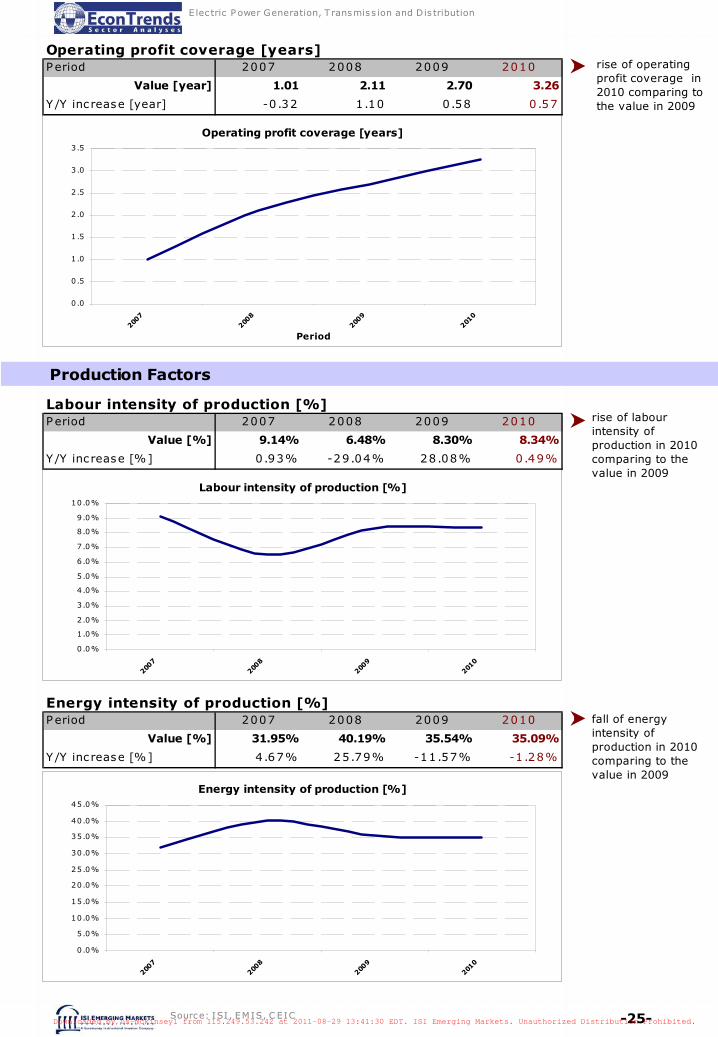

rise of operating profit coverage in 2010 comparing to the value in 2009

Operating profit coverage [years]

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2007

2008

2009

2010

Period

Operating profit coverage [years]Period 2007 2008 2009 2010

Value [year] 1.01 2.11 2.70 3.26

Y/Y inc rease [year] -0 .32 1.10 0.58 0.57

Production Factors

Labour intensity of production [%]

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

2007

2008

2009

2010

Energy intensity of production [%]

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

2007

2008

2009

2010

Labour intensity of production [%]Period 2007 2008 2009 2010

Value [%] 9.14% 6.48% 8.30% 8.34%

Y/Y inc rease [%] 0.93% -29.04% 28.08% 0.49%

Energy intensity of production [%]Period 2007 2008 2009 2010

Value [%] 31.95% 40.19% 35.54% 35.09%

Y/Y inc rease [%] 4.67% 25.79% -11.57% -1.28%

rise of labour intensity of production in 2010 comparing to the value in 2009

fall of energy intensity of production in 2010 comparing to the value in 2009

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-26-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Source: ISI , EM IS, C EIC

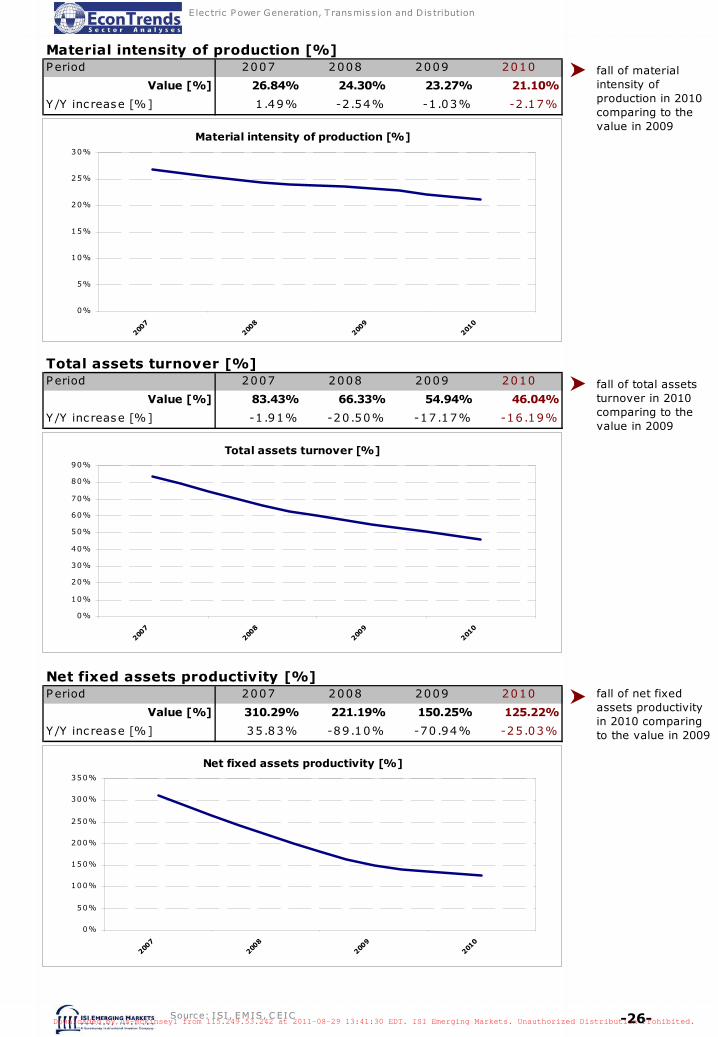

fall of material intensity of production in 2010 comparing to the value in 2009

fall of total assets turnover in 2010 comparing to the value in 2009

fall of net fixed assets productivity in 2010 comparing to the value in 2009

Material intensity of production [%]Period 2007 2008 2009 2010

Value [%] 26.84% 24.30% 23.27% 21.10%

Y/Y inc rease [%] 1.49% -2.54% -1.03% -2.17%

Material intensity of production [%]

0%

5%

10%

15%

20%

25%

30%

2007

2008

2009

2010

Total assets turnover [%]Period 2007 2008 2009 2010

Value [%] 83.43% 66.33% 54.94% 46.04%

Y/Y inc rease [%] -1 .91% -20.50% -17.17% -16.19%

Net fixed assets productivity [%]Period 2007 2008 2009 2010

Value [%] 310.29% 221.19% 150.25% 125.22%

Y/Y inc rease [%] 35.83% -89.10% -70.94% -25.03%

Total assets turnover [%]

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2007

2008

2009

2010

Net fixed assets productivity [%]

0%

50%

100%

150%

200%

250%

300%

350%

2007

2008

2009

2010

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-27-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Source: ISI , EM IS, C EIC

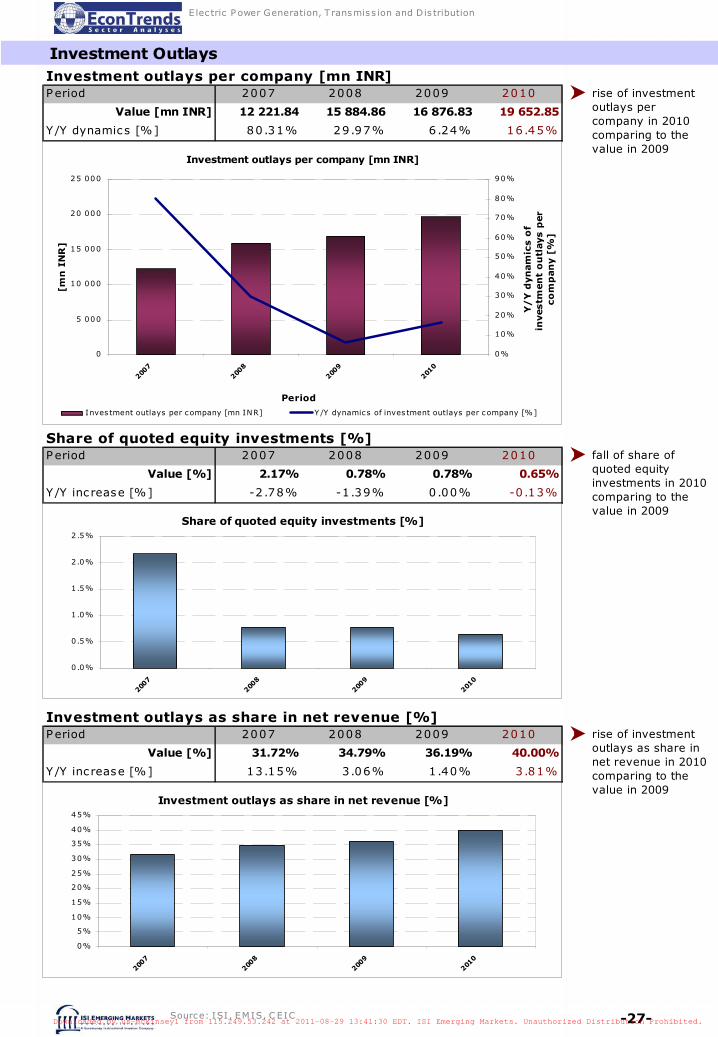

Investment OutlaysInvestment outlays per company [mn INR]Period 2007 2008 2009 2010

Value [mn INR] 12 221.84 15 884.86 16 876.83 19 652.85

Y/Y dynamics [%] 80.31% 29.97% 6.24% 16.45%

Share of quoted equity investments [%]Period 2007 2008 2009 2010

Value [%] 2.17% 0.78% 0.78% 0.65%

Y/Y inc rease [%] -2 .78% -1.39% 0.00% -0.13%

Investment outlays as share in net revenue [%]Period 2007 2008 2009 2010

Value [%] 31.72% 34.79% 36.19% 40.00%

Y/Y inc rease [%] 13.15% 3.06% 1.40% 3.81%

rise of investment outlays per company in 2010 comparing to the value in 2009

fall of share of quoted equity investments in 2010 comparing to the value in 2009

rise of investment outlays as share in net revenue in 2010 comparing to the value in 2009

Investment outlays per company [mn INR]

0

5 000

10 000

15 000

20 000

25 000

2007

2008

2009

2010

Period

[mn

IN

R]

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Y/

Y d

yn

am

ics o

f in

vestm

en

t o

utl

ays p

er

co

mp

an

y [

%]

Inves tment outlays per company [mn INR] Y /Y dynamics of inves tment outlays per company [%]

Share of quoted equity investments [%]

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

2007

2008

2009

2010

Investment outlays as share in net revenue [%]

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2007

2008

2009

2010

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-28-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Source: ISI , EM IS, C EIC

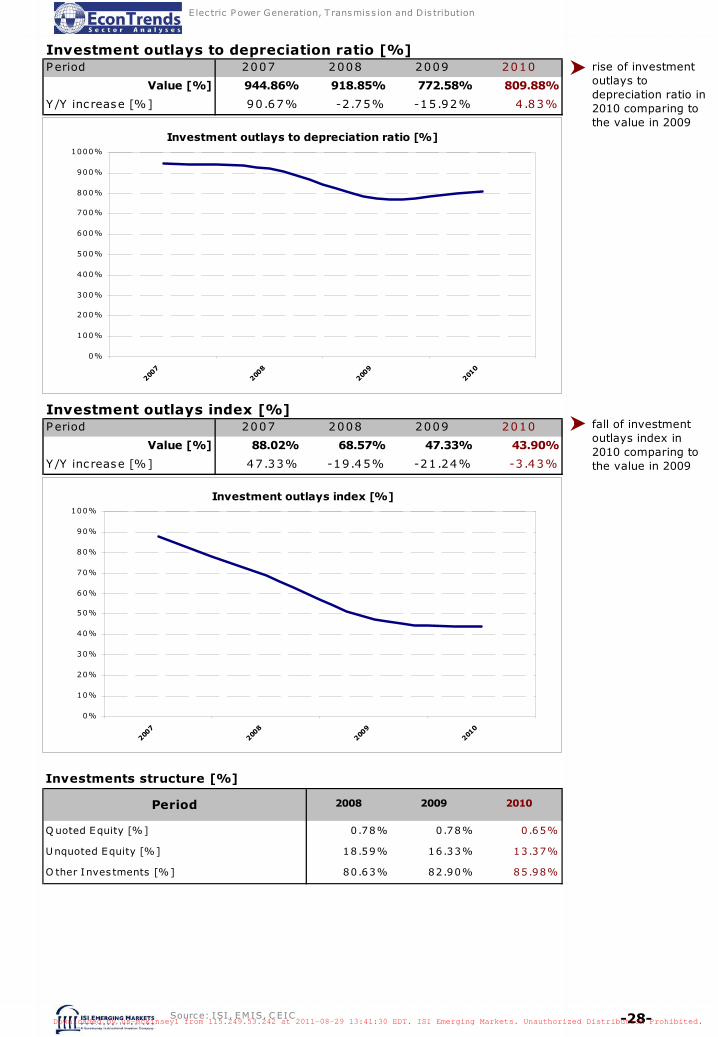

rise of investment outlays to depreciation ratio in 2010 comparing to the value in 2009

fall of investment outlays index in 2010 comparing to the value in 2009

Investment outlays to depreciation ratio [%]Period 2007 2008 2009 2010

Value [%] 944.86% 918.85% 772.58% 809.88%

Y/Y inc rease [%] 90.67% -2.75% -15.92% 4.83%

Investment outlays index [%]Period 2007 2008 2009 2010

Value [%] 88.02% 68.57% 47.33% 43.90%

Y/Y inc rease [%] 47.33% -19.45% -21.24% -3.43%

Investments structure [%]

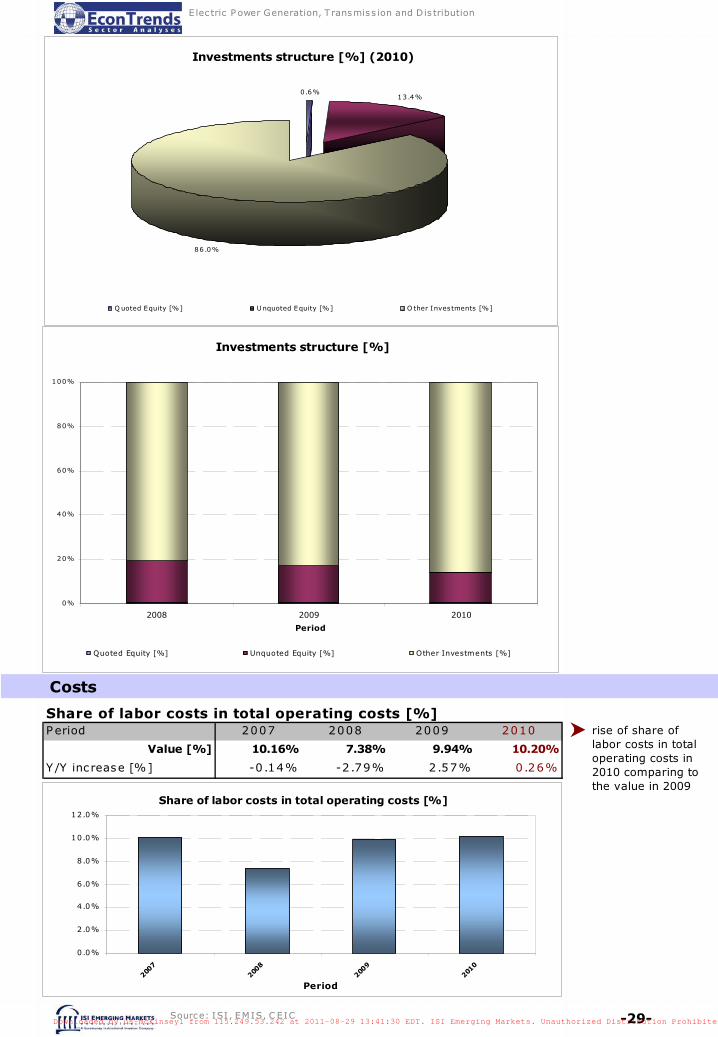

Q uoted Equity [%] 0.78% 0.78% 0.65%

Unquoted Equity [%] 18.59% 16.33% 13.37%

O ther Inves tments [%] 80.63% 82.90% 85.98%

Period 2008 2009 2010

Investment outlays to depreciation ratio [%]

0%

100%

200%

300%

400%

500%

600%

700%

800%

900%

1000%

2007

2008

2009

2010

Investment outlays index [%]

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007

2008

2009

2010

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-29-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Source: ISI , EM IS, C EIC

Investments structure [%]

0%

20%

40%

60%

80%

100%

2008 2009 2010

Period

Quoted Equity [%] Unquoted Equity [%] Other Investments [%]

Costs

Share of labor costs in total operating costs [%]Period 2007 2008 2009 2010

Value [%] 10.16% 7.38% 9.94% 10.20%

Y/Y inc rease [%] -0 .14% -2.79% 2.57% 0.26%

Share of labor costs in total operating costs [%]

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2007

2008

2009

2010

Period

rise of share of labor costs in total operating costs in 2010 comparing to the value in 2009

Investments structure [%] (2010)

0.6%13.4%

86.0%

Q uoted Equity [%] Unquoted Equity [%] O ther Investments [%]

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-30-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Source: ISI , EM IS, C EIC

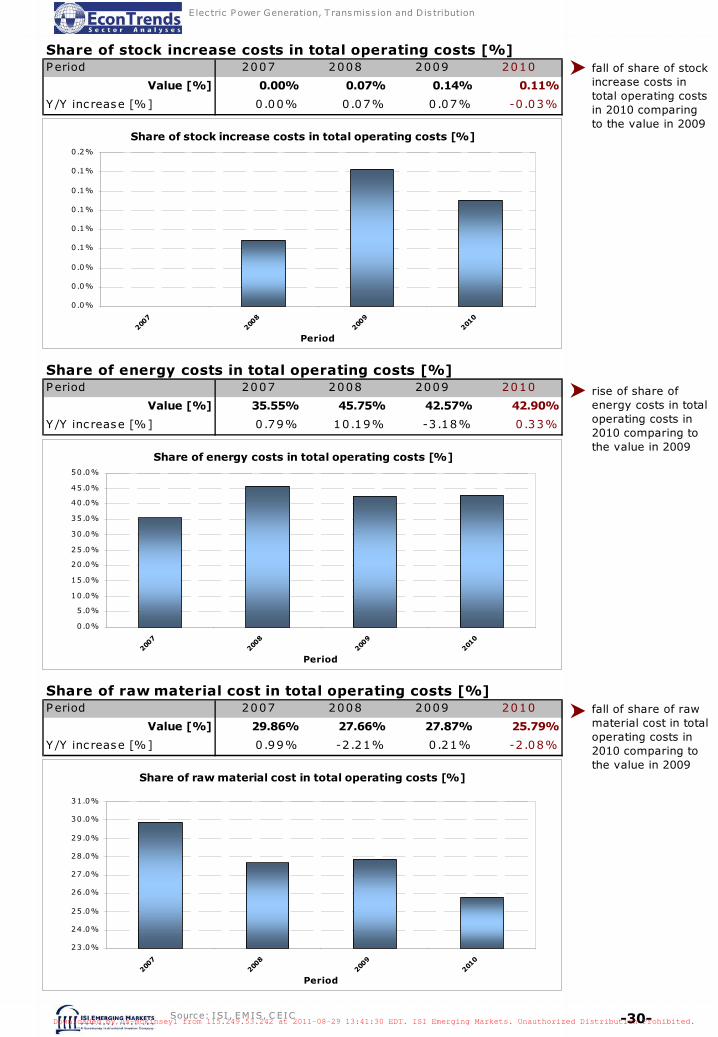

fall of share of stock increase costs in total operating costs in 2010 comparing to the value in 2009

rise of share of energy costs in total operating costs in 2010 comparing to the value in 2009

fall of share of raw material cost in total operating costs in 2010 comparing to the value in 2009

Period 2007 2008 2009 2010

Value [%] 0.00% 0.07% 0.14% 0.11%

Y/Y inc rease [%] 0.00% 0.07% 0.07% -0.03%

Share of stock increase costs in total operating costs [%]

Share of stock increase costs in total operating costs [%]

0.0%

0.0%

0.0%

0.1%

0.1%

0.1%

0.1%

0.1%

0.2%

2007

2008

2009

2010

Period

Period 2007 2008 2009 2010

Value [%] 35.55% 45.75% 42.57% 42.90%

Y/Y inc rease [%] 0.79% 10.19% -3.18% 0.33%

Share of energy costs in total operating costs [%]

Share of energy costs in total operating costs [%]

0 .0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

2007

2008

2009

2010

Period

Period 2007 2008 2009 2010

Value [%] 29.86% 27.66% 27.87% 25.79%

Y/Y inc rease [%] 0.99% -2.21% 0.21% -2.08%

Share of raw material cost in total operating costs [%]

Share of raw material cost in total operating costs [%]

23.0%

24.0%

25.0%

26.0%

27.0%

28.0%

29.0%

30.0%

31.0%

2007

2008

2009

2010

Period

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-31-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Source: ISI , EM IS, C EIC

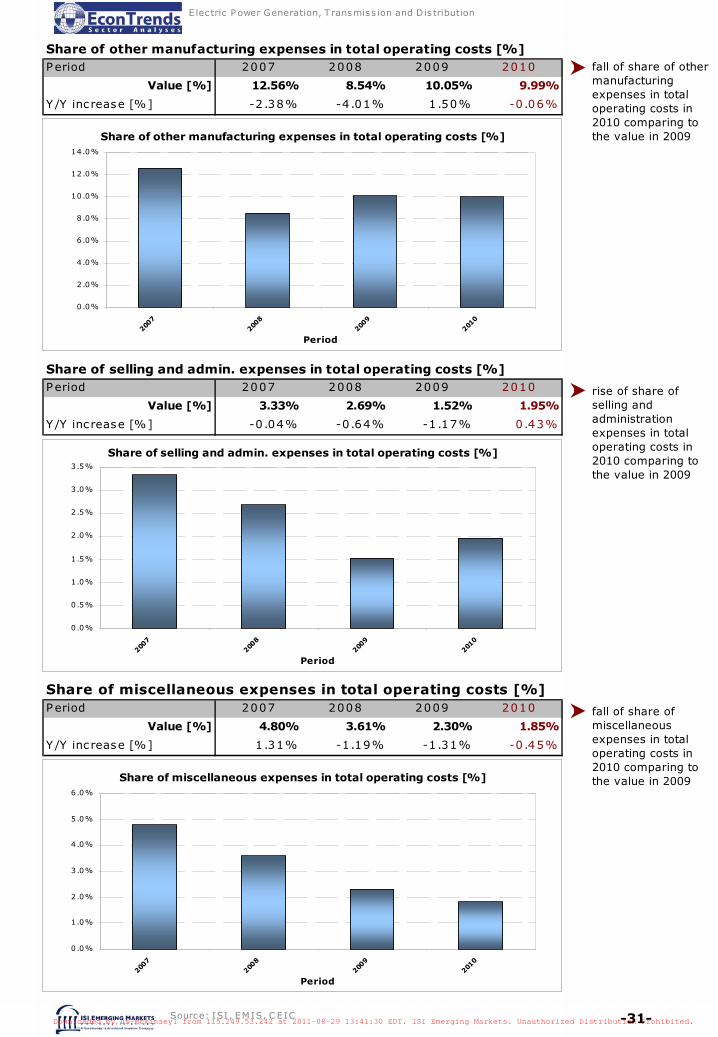

fall of share of other manufacturing expenses in total operating costs in 2010 comparing to the value in 2009

rise of share of selling and administration expenses in total operating costs in 2010 comparing to the value in 2009

fall of share of miscellaneous expenses in total operating costs in 2010 comparing to the value in 2009

Period 2007 2008 2009 2010

Value [%] 12.56% 8.54% 10.05% 9.99%

Y/Y inc rease [%] -2 .38% -4.01% 1.50% -0.06%

Share of other manufacturing expenses in total operating costs [%]

Period 2007 2008 2009 2010

Value [%] 3.33% 2.69% 1.52% 1.95%

Y/Y inc rease [%] -0 .04% -0.64% -1.17% 0.43%

Share of selling and admin. expenses in total operating costs [%]

Period 2007 2008 2009 2010

Value [%] 4.80% 3.61% 2.30% 1.85%

Y/Y inc rease [%] 1.31% -1.19% -1.31% -0.45%

Share of miscellaneous expenses in total operating costs [%]

Share of other manufacturing expenses in total operating costs [%]

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

2007

2008

2009

2010

Period

Share of selling and admin. expenses in total operating costs [%]

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2007

2008

2009

2010

Period

Share of miscellaneous expenses in total operating costs [%]

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2007

2008

2009

2010

Period

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-32-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Source: ISI , EM IS, C EIC

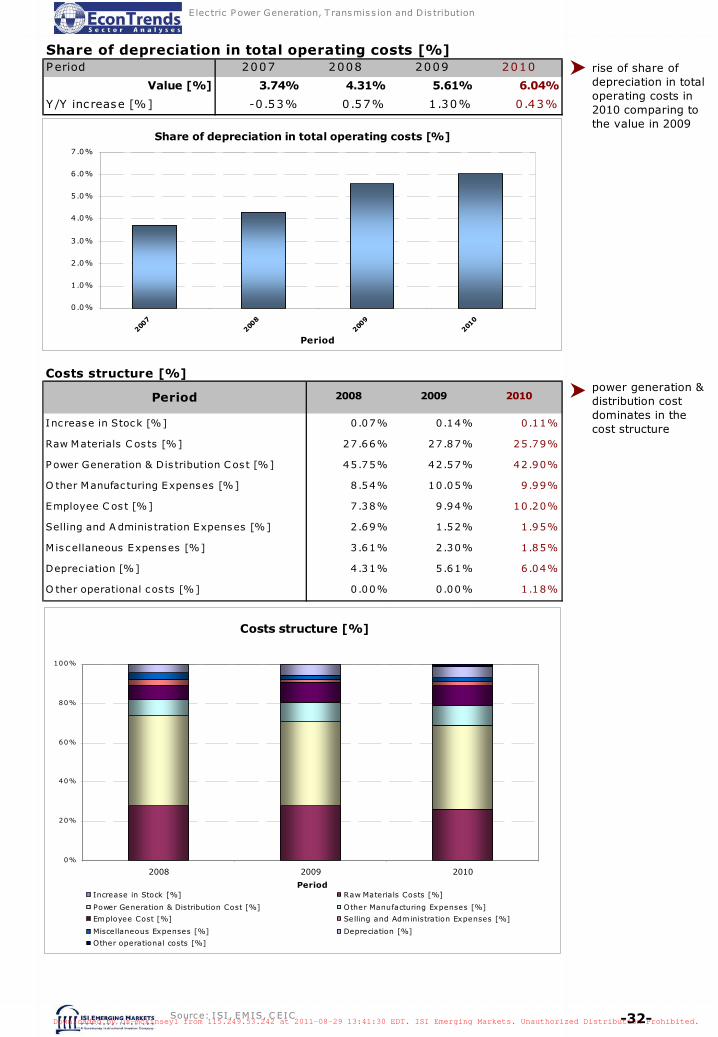

Share of depreciation in total operating costs [%]

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

2007

2008

2009

2010

Period

Period 2007 2008 2009 2010

Value [%] 3.74% 4.31% 5.61% 6.04%

Y/Y inc rease [%] -0 .53% 0.57% 1.30% 0.43%

Share of depreciation in total operating costs [%]rise of share of depreciation in total operating costs in 2010 comparing to the value in 2009

Costs structure [%]

Inc rease in Stock [%] 0.07% 0.14% 0.11%

Raw Materials C os ts [%] 27.66% 27.87% 25.79%

P ower Generation & Dis tribution C os t [%] 45.75% 42.57% 42.90%

O ther Manufac turing Expenses [%] 8.54% 10.05% 9.99%

Employee C os t [%] 7.38% 9.94% 10.20%

Selling and A dminis tration Expenses [%] 2.69% 1.52% 1.95%

Miscellaneous Expenses [%] 3.61% 2.30% 1.85%

Deprec iation [%] 4.31% 5.61% 6.04%

O ther operational cos ts [%] 0.00% 0.00% 1.18%

Period 2008 2009 2010

Costs structure [%]

0%

20%

40%

60%

80%

100%

2008 2009 2010

PeriodIncrease in Stock [%] Raw Materials Costs [%]

Power Generation & Distribution Cost [%] Other Manufacturing Expenses [%]

Employee Cost [%] Selling and Administration Expenses [%]

Miscellaneous Expenses [%] Depreciation [%]

Other operational costs [%]

power generation & distribution cost dominates in the cost structure

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-33-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

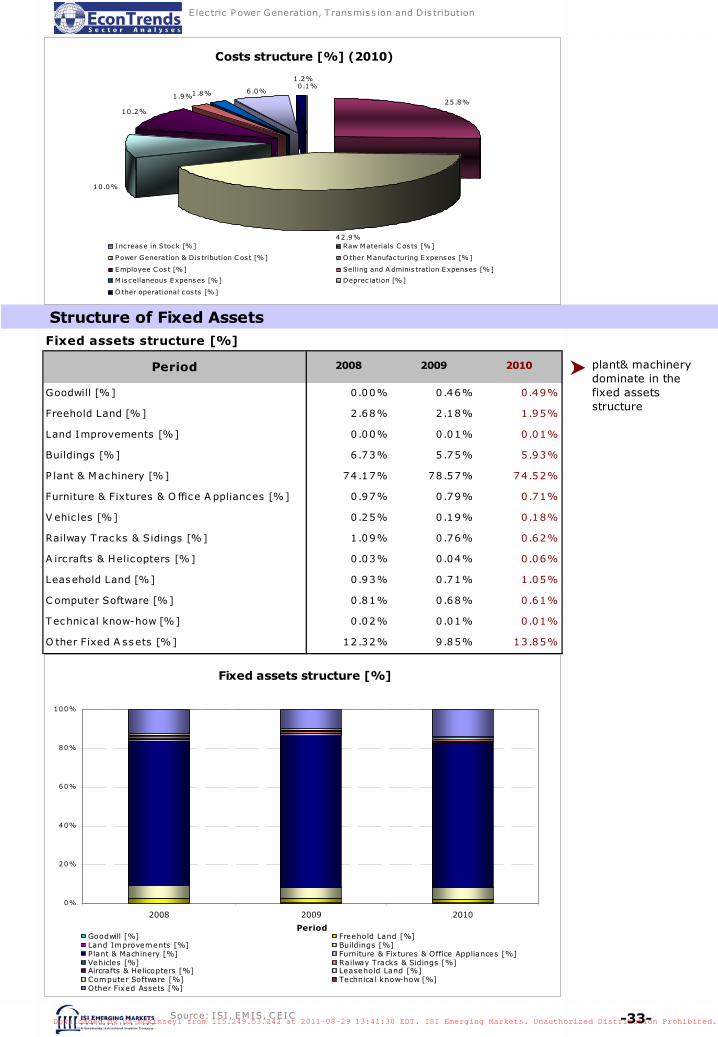

Structure of Fixed Assets

Costs structure [%] (2010)

0 .1%

25.8%

10.0%

10.2%

1.9%1.8%

1.2%

6.0%

42.9%Increase in Stock [%] Raw Materials C os ts [%]

Power Generation & Dis tribution C os t [%] O ther Manufac turing Expenses [%]

Employee C os t [%] Selling and A dminis tration Expenses [%]

M iscellaneous Expenses [%] Deprec iation [%]

O ther operational cos ts [%]

Fixed assets structure [%]

Goodwill [%] 0.00% 0.46% 0.49%

Freehold Land [%] 2.68% 2.18% 1.95%

Land Improvements [%] 0.00% 0.01% 0.01%

Buildings [%] 6.73% 5.75% 5.93%

P lant & Machinery [%] 74.17% 78.57% 74.52%

Furniture & Fixtures & O ffice A ppliances [%] 0.97% 0.79% 0.71%

V ehic les [%] 0.25% 0.19% 0.18%

Railway T racks & Sidings [%] 1.09% 0.76% 0.62%

A irc rafts & Helicopters [%] 0.03% 0.04% 0.06%

Leasehold Land [%] 0.93% 0.71% 1.05%

C omputer Software [%] 0.81% 0.68% 0.61%

Technical know-how [%] 0.02% 0.01% 0.01%

O ther Fixed A ssets [%] 12.32% 9.85% 13.85%

Period 2008 2009 2010

Fixed assets structure [%]

0%

20%

40%

60%

80%

100%

2008 2009 2010

PeriodGoodwill [%] Freehold Land [%]Land Improvements [%] Buildings [%]Plant & Machinery [%] Furniture & Fixtures & Office Appliances [%]Vehicles [%] Railway Tracks & Sidings [%]Aircrafts & Helicopters [%] Leasehold Land [%]Computer Software [%] Technical know-how [%]Other Fixed Assets [%]

plant& machinery dominate in the fixed assets structure

Source: ISI , EM IS, C EIC

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-34-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

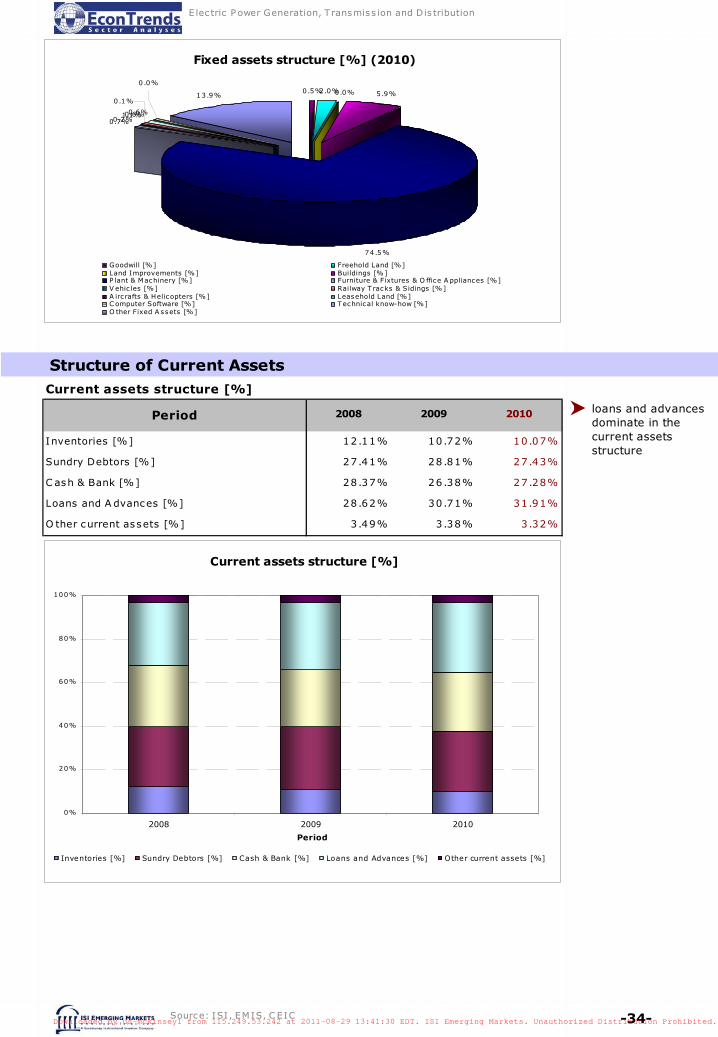

Fixed assets structure [%] (2010)

0.5%2.0% 5.9%

74.5%

0.7%0.2%1.1%0.6%

13.9%

0.0%0.0%

0.6%

0.1%

Goodwill [%] Freehold Land [%]Land Improvements [%] Buildings [%]P lant & Machinery [%] Furniture & Fixtures & O ffice A ppliances [%]V ehic les [%] Railway T racks & Sidings [%]A irc rafts & Helicopters [%] Leasehold Land [%]C omputer Software [%] Technical know-how [%]O ther Fixed A ssets [%]

Structure of Current AssetsCurrent assets structure [%]

Inventories [%] 12.11% 10.72% 10.07%

Sundry Debtors [%] 27.41% 28.81% 27.43%

C ash & Bank [%] 28.37% 26.38% 27.28%

Loans and A dvances [%] 28.62% 30.71% 31.91%

O ther current assets [%] 3.49% 3.38% 3.32%

Period 2008 2009 2010 loans and advances dominate in the current assets structure

Current assets structure [%]

0%

20%

40%

60%

80%

100%

2008 2009 2010

Period

Inventories [%] Sundry Debtors [%] Cash & Bank [%] Loans and Advances [%] Other current assets [%]

Source: ISI , EM IS, C EIC

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-35-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

Current assets structure [%] (2010)

10.1%

27.4%

31.9%

3.3%

27.3%

Inventories [%] Sundry Debtors [%] C ash & Bank [%] Loans and A dvances [%] O ther current assets [%]

Structure of Current Liabilities

Short-term liabilities structure [%]

Sundry C reditors [%] 26.71% 25.40% 25.80%

Unc laimed Dividend [%] 0.04% 0.05% 0.05%

Interes t A cc rued But Not Due [%] 0.80% 1.30% 1.44%

P rovis ions [%] 31.22% 29.35% 30.38%

O ther Short-term Liabilities [%] 41.24% 43.91% 42.33%

Period 2008 2009 2010 other short-term liabilities dominate in the short-term liabilities structure

Short-term liabilities structure [%]

0%

20%

40%

60%

80%

100%

2008 2009 2010

Period

Sundry Creditors [%] Unclaimed Dividend [%] Interest Accrued But Not Due [%]

Provisions [%] Other Short-term Liabilities [%]

Source: ISI , EM IS, C EIC

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-36-

E lec tric P ower Generation, T ransmiss ion and Dis tribution

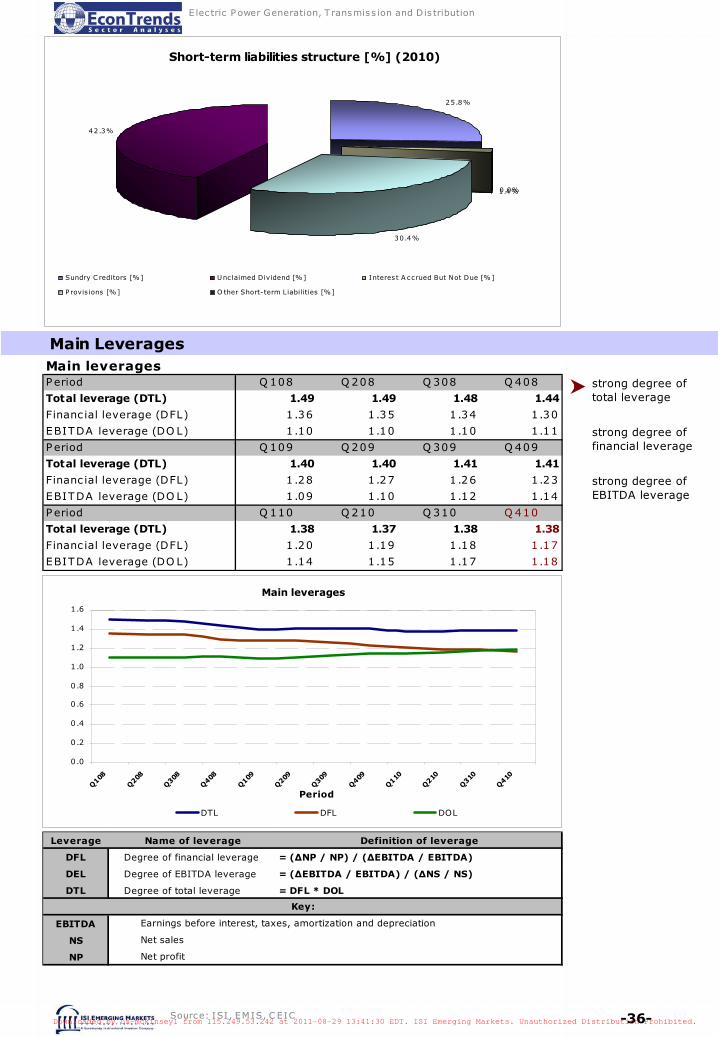

Short-term liabilities structure [%] (2010)

25.8%

0.0%

30.4%

42.3%

1.4%

Sundry C reditors [%] Unc laimed Dividend [%] Interes t A ccrued But Not Due [%]

P rovis ions [%] O ther Short-term Liabilities [%]

Source: ISI , EM IS, C EIC

Main LeveragesMain leveragesPeriod Q 108 Q 208 Q 308 Q 408

Total leverage (DTL) 1.49 1.49 1.48 1.44

Financ ial leverage (DFL) 1 .36 1.35 1 .34 1.30

EBITDA leverage (DO L) 1 .10 1.10 1 .10 1.11

Period Q 109 Q 209 Q 309 Q 409

Total leverage (DTL) 1.40 1.40 1.41 1.41

Financ ial leverage (DFL) 1 .28 1.27 1 .26 1.23

EBITDA leverage (DO L) 1 .09 1.10 1 .12 1.14

Period Q 110 Q 210 Q 310 Q 410

Total leverage (DTL) 1.38 1.37 1.38 1.38

Financ ial leverage (DFL) 1 .20 1.19 1 .18 1.17

EBITDA leverage (DO L) 1 .14 1.15 1 .17 1.18

Main leverages

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Period

DTL DFL DOL

Leverage Name of leverage Definition of leverage

DFL Degree of financial leverage = (ΔNP / NP) / (ΔEBITDA / EBITDA)

DEL Degree of EBITDA leverage = (ΔEBITDA / EBITDA) / (ΔNS / NS)

DTL Degree of total leverage = DFL * DOL

EBITDA

NS

NP Net profit

Key:

Earnings before interest, taxes, amortization and depreciation

Net sales

strong degree of total leverage

strong degree of financial leverage

strong degree of EBITDA leverage

ISIEmergingMarketsPDF us-mckinsey1 from 115.249.53.242 on 2011-08-29 13:41:30 EDT. DownloadPDF.

Downloaded by us-mckinsey1 from 115.249.53.242 at 2011-08-29 13:41:30 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

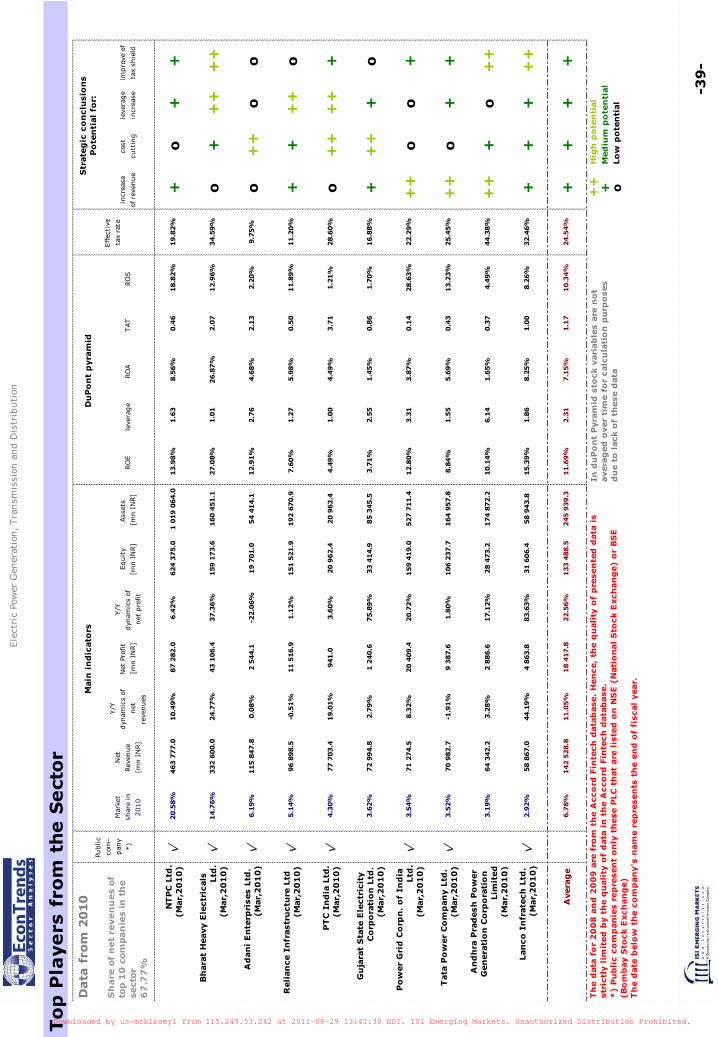

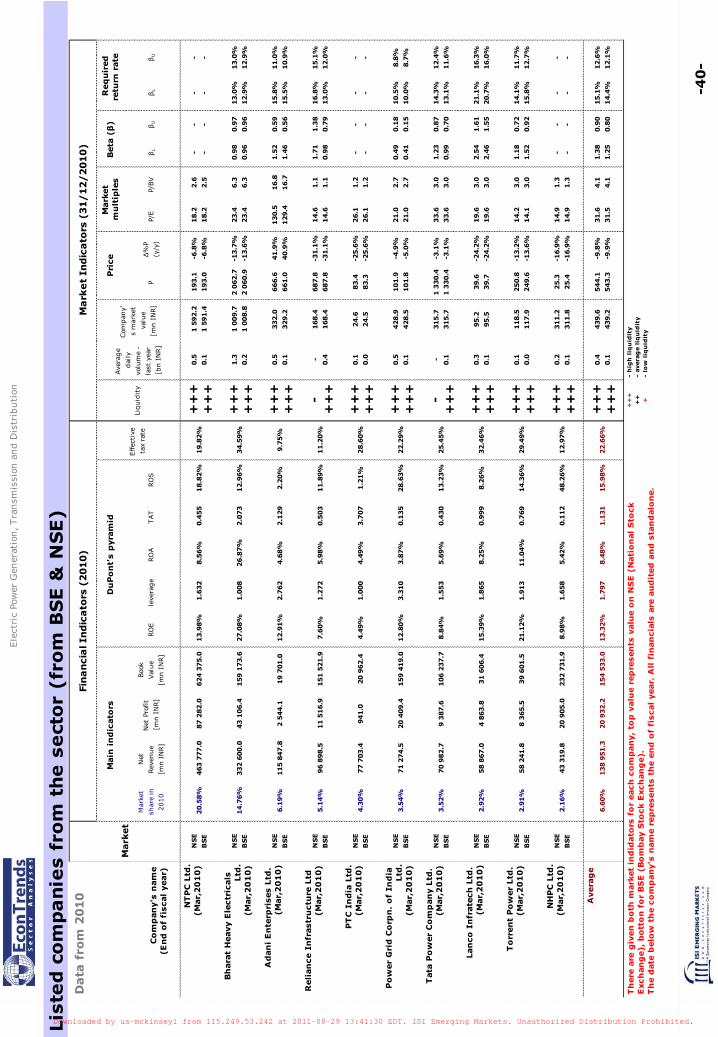

-37

-

Ele

ctri

c Po

wer

Gen

erat

ion, Tra

nsm

issi

on a

nd D

istr

ibuti

on

Du

Po

nt’

s P

yra

mid

Equit

y

per

com

apny

2010

60 5

52

2009

48 9

37

2008

43 8

01

2007

34 9

10

Levera

ge

2010

1.7

6

Ass

ets

per

com

pany

2010

106 7

21

2009

1.7

3

2009

84 8

93

2008

1.5

7

2008

68 8

43

RO

E

2010

11.2

%

2007

1.3

2

TA

T

2010

0.4

6

2007

46 1

74

2009

13.6

%

2009

0.5

5

2008

13.0

%

2008

0.6

6

2007

17.4

%

RO

A

2010

6.3

%

2007

0.8

3

Net

revenue

per

com

pany

2010

49 1

37

2009

7.8

%

2009

46 6

40

2008

8.3

%

2008

45 6

63

2007

13.2

%

RO

S

2010

13.8

%

2007

38 5

25

2009

14.3

%

2008

12.5

%

2007

15.8

%

Net

pro

fit

per

com

pany

2010

6 7

69

2009

6 6

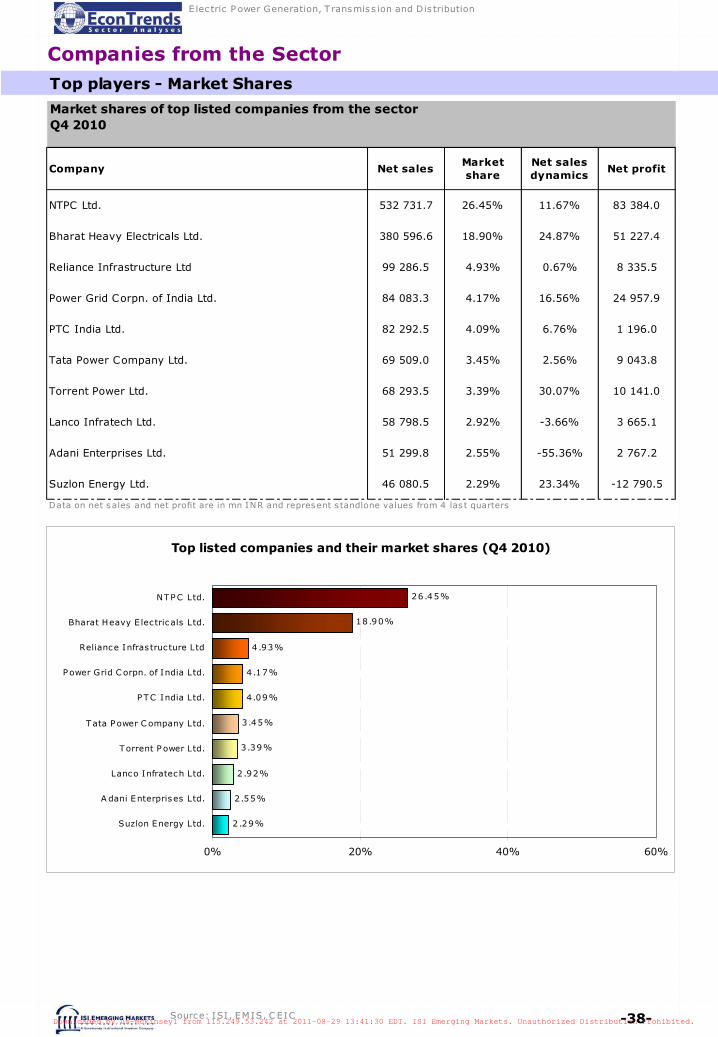

63