Efficient Securities Markets Institutional Development Initiative Global Capital Markets Development Department Securities Markets Group

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Efficient Securities Markets Institutional Development Initiative

Global Capital Markets Development Department

Securities Markets Group

2

• Introduction

•Bond Markets in East Africa

•ESMID

Agenda

3

• Africa’s housing & infrastructure financing needs are enormous

- US$93 billion or 15% of GDP

• Bulk of infrastructure undertaken by public sector using foreign currency loans

– Funding inadequate to meet all requirements

– Currency risk passed on to consumers

• Private Sector can contribute in bridging the financing gap

• Capital Markets can raise long-term local currency financing for infrastructure and housing

– Kenya Government raised US$240 million through bond market for infrastructure

– Kenya Electricity Generating Company - KenGen raised US$330 million in 10-yr bond for power generation projects

Introduction

4

Benefits of Well Functioning Local Currency Bond Markets

Better risk management for borrowers:• Lower interest rates • Reduced foreign currency risks• Reduced refinancing risks • Longer tenors

Improved yields for institutional investors

Improved ability to deal with financial crises

Financial sector diversification

Accelerated private sector development

Expanded housing and infrastructure financeThis generates growth and reduces poverty

5

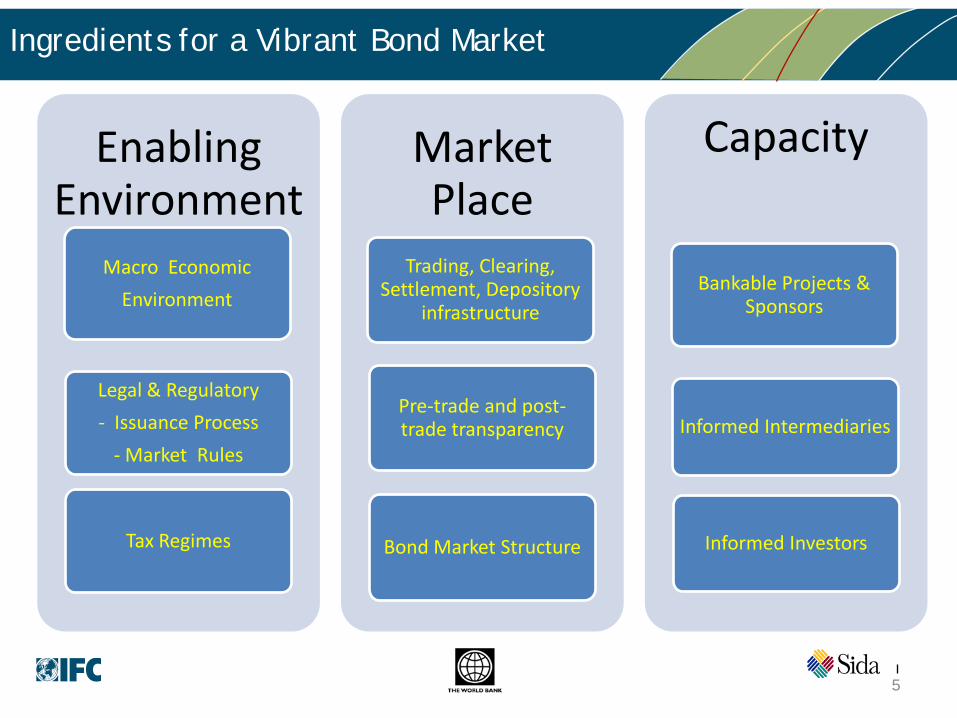

Ingredients for a Vibrant Bond Market

Enabling Environment

Macro Economic

Environment

Legal & Regulatory

- Issuance Process

- Market Rules

Tax Regimes

Market Place

Trading, Clearing, Settlement, Depository

infrastructure

Pre-trade and post-trade transparency

Bond Market Structure

Capacity

Bankable Projects & Sponsors

Informed Intermediaries

Informed Investors

Bond Markets in East Africa

7

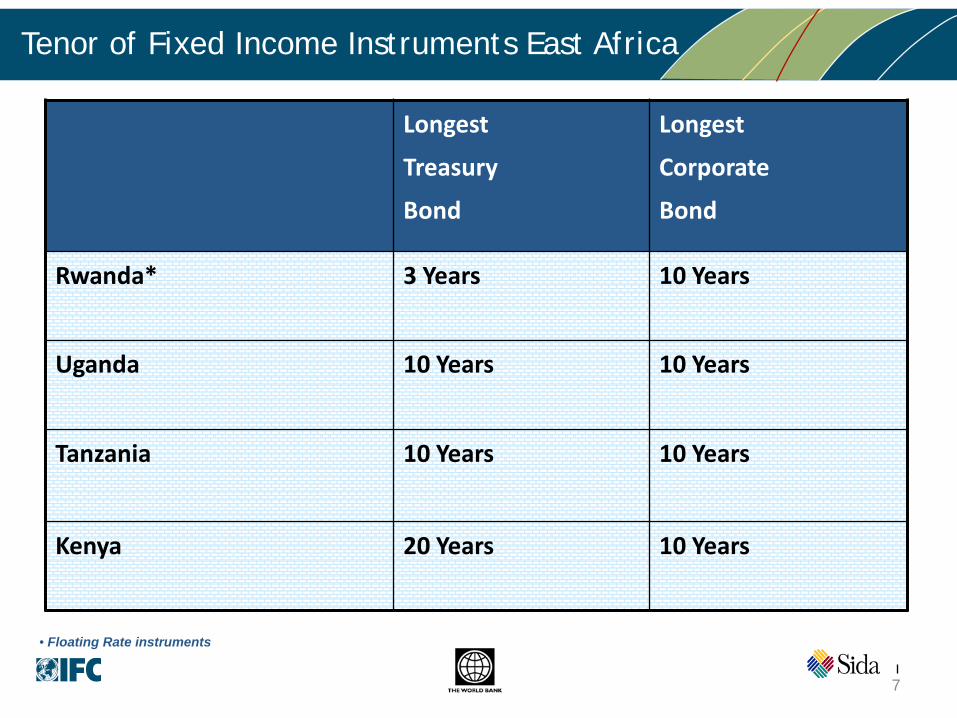

Tenor of Fixed Income Instruments East Africa

Longest

Treasury

Bond

Longest

Corporate

Bond

Rwanda* 3 Years 10 Years

Uganda 10 Years 10 Years

Tanzania 10 Years 10 Years

Kenya 20 Years 10 Years

• Floating Rate instruments

8

Treasury Yield Curves Uganda, Tanzania & Kenya as at 30 June 2010

Kenya

Uganda Tanzania

-

2.0000

4.0000

6.0000

8.0000

10.0000

12.0000

14.0000

O/N T/N 1W 1M 2M 3M 6M 9M 1Y 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y 10Y 11Y 12Y 13Y 14Y 15Y 16Y 17Y 18Y 19Y 20Y 21Y 22Y 23Y 24Y 25Y

Source: Standard Chartered Bank Kenya

Tenors have extended and yields have recently declined

9

East Africa Cumulative New Corporate Bond Issues (US$M)

-

100.0

200.0

300.0

400.0

500.0

600.0

700.0

2004 2005 2006 2007 2008 2009

Kenya

Uganda

Tanzania

Global Credit Crisis

Kenya has had record issuance of US$500 million in 2009, over 90% infrastructure

related KenGen (US$330

million) and Safaricom(US$100 million)

“The results clearly show that we can raise most of the funds needed to realise the goals of Vision 2030 through our own capital markets,” Kenya’s Prime Minister Mr Raila Odinga on the issue of KenGen bond.

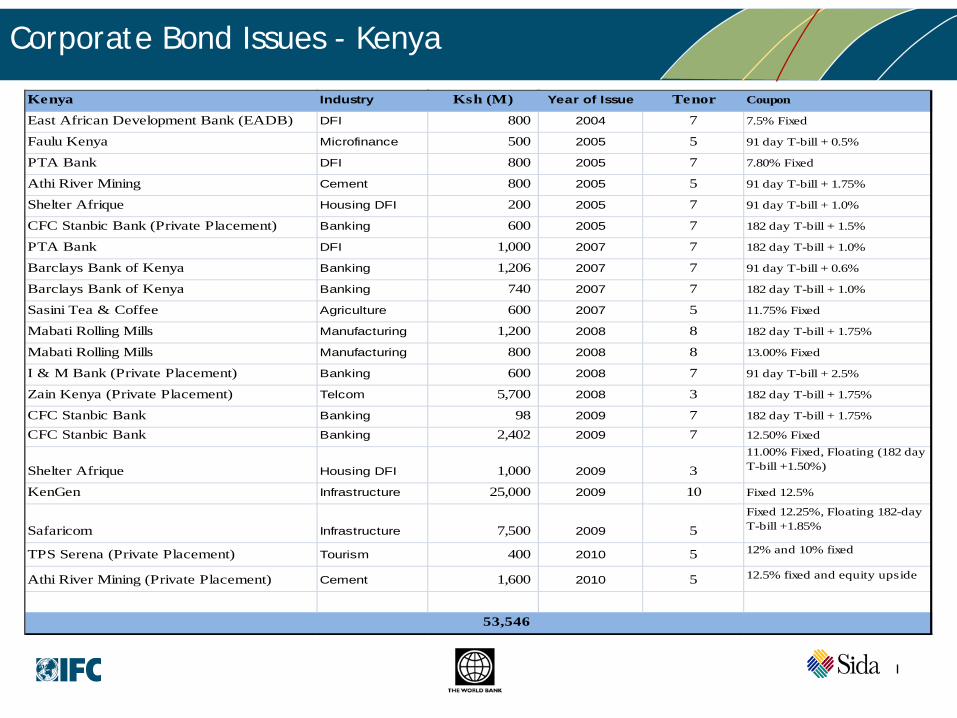

Corporate Bond Issues - Kenya

Kenya Industry Ksh (M) Year of Issue Tenor Coupon

East African Development Bank (EADB) DFI 800 2004 7 7.5% Fixed

Faulu Kenya Microfinance 500 2005 5 91 day T-bill + 0.5%

PTA Bank DFI 800 2005 7 7.80% Fixed

Athi River Mining Cement 800 2005 5 91 day T-bill + 1.75%

Shelter Afrique Housing DFI 200 2005 7 91 day T-bill + 1.0%

CFC Stanbic Bank (Private Placement) Banking 600 2005 7 182 day T-bill + 1.5%

PTA Bank DFI 1,000 2007 7 182 day T-bill + 1.0%

Barclays Bank of Kenya Banking 1,206 2007 7 91 day T-bill + 0.6%

Barclays Bank of Kenya Banking 740 2007 7 182 day T-bill + 1.0%

Sasini Tea & Coffee Agriculture 600 2007 5 11.75% Fixed

Mabati Rolling Mills Manufacturing 1,200 2008 8 182 day T-bill + 1.75%

Mabati Rolling Mills Manufacturing 800 2008 8 13.00% Fixed

I & M Bank (Private Placement) Banking 600 2008 7 91 day T-bill + 2.5%

Zain Kenya (Private Placement) Telcom 5,700 2008 3 182 day T-bill + 1.75%

CFC Stanbic Bank Banking 98 2009 7 182 day T-bill + 1.75%

CFC Stanbic Bank Banking 2,402 2009 7 12.50% Fixed

Shelter Afrique Housing DFI 1,000 2009 311.00% Fixed, Floating (182 day T-bill +1.50%)

KenGen Infrastructure 25,000 2009 10 Fixed 12.5%

Safaricom Infrastructure 7,500 2009 5Fixed 12.25%, Floating 182-day T-bill +1.85%

TPS Serena (Private Placement) Tourism 400 2010 5 12% and 10% fixed

Athi River Mining (Private Placement) Cement 1,600 2010 5 12.5% fixed and equity upside

53,546

11

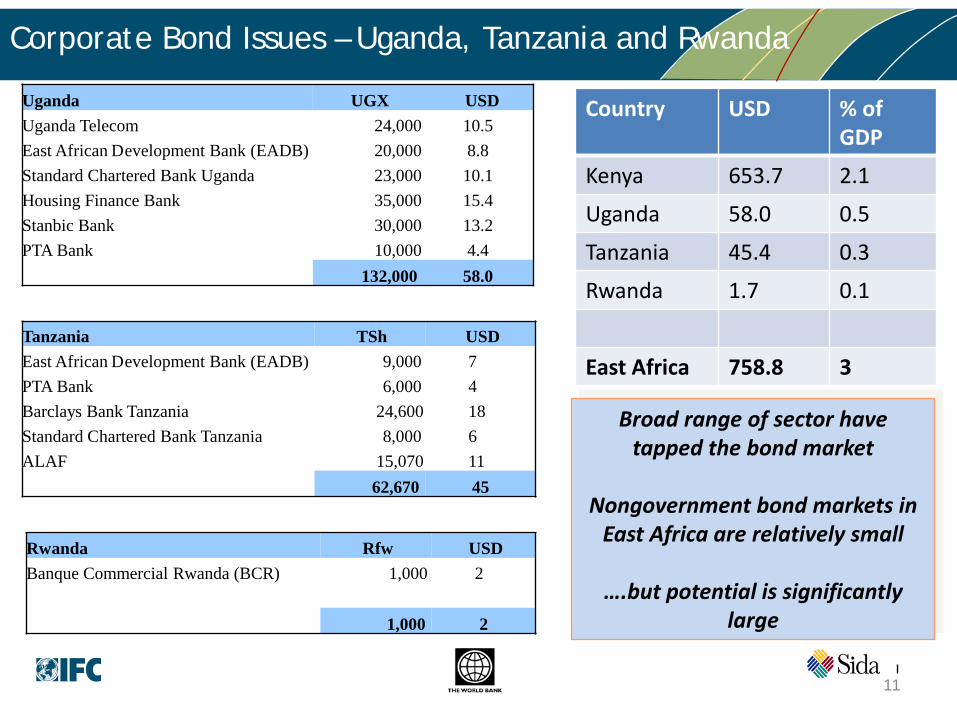

Corporate Bond Issues – Uganda, Tanzania and Rwanda

Uganda UGX USDUganda Telecom 24,000 10.5East African Development Bank (EADB) 20,000 8.8Standard Chartered Bank Uganda 23,000 10.1Housing Finance Bank 35,000 15.4Stanbic Bank 30,000 13.2PTA Bank 10,000 4.4

132,000 58.0

Tanzania TSh USD East African Development Bank (EADB) 9,000 7 PTA Bank 6,000 4 Barclays Bank Tanzania 24,600 18 Standard Chartered Bank Tanzania 8,000 6 ALAF 15,070 11

62,670 45

Rwanda Rfw USD Banque Commercial Rwanda (BCR) 1,000 2

1,000 2

Country USD % of GDP

Kenya 653.7 2.1

Uganda 58.0 0.5

Tanzania 45.4 0.3

Rwanda 1.7 0.1

East Africa 758.8 3

Broad range of sector have tapped the bond market

Nongovernment bond markets in East Africa are relatively small

….but potential is significantly large

12

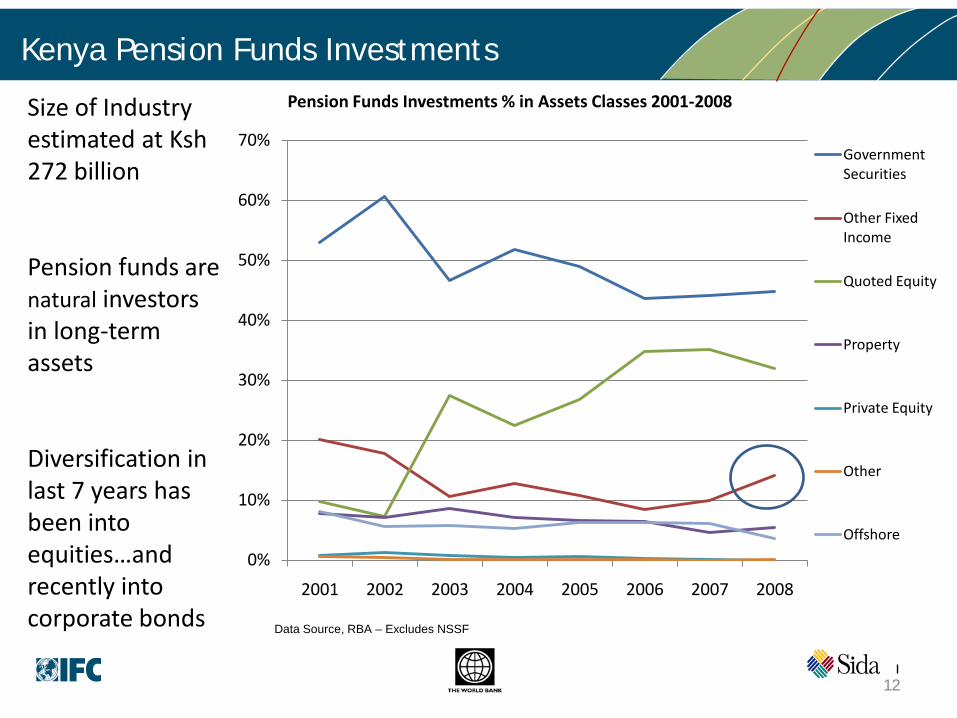

Kenya Pension Funds Investments

Size of Industry estimated at Ksh272 billion

Pension funds are natural investors in long-term assets

Diversification in last 7 years has been into equities…and recently into corporate bonds Data Source, RBA – Excludes NSSF

0%

10%

20%

30%

40%

50%

60%

70%

2001 2002 2003 2004 2005 2006 2007 2008

Pension Funds Investments % in Assets Classes 2001-2008

Government Securities

Other Fixed Income

Quoted Equity

Property

Private Equity

Other

Offshore

13

Challenges to Bond Market Development – East Africa

Lack of Capacity

• Regulators• Market participants•Project Preparation

gap

Inadequate Market Infrastructure

• Trading, clearing, settlement, and depository

• Transparency -information collection and dissemination

• Rating agencies

Weak Regulatory Environment

• Issuance process

• Tax regimes

• Investment requirements

• Market rules

• Licensing framework

Small and Fragmented Markets

• Lack of critical mass of issuers and investors

• Inability to take advantage of economies of scale

14

Lessons/Issues - – East Africa

• Approval process is still long (average 6 months)

• Merit based process applied

• Not much differentiation with equity issues

• No recognition of sophisticated institutional investor base

• There is a growing institutional investor base – seeking avenues to diversify and enhance returns

ESMID

16

ESMID Africa

ESMID:

• Efficient

• Securities

• Markets

• Institutional

• Development

A partnership between:

• Swedish International Development Cooperation

Agency (Sida)

• International Finance Corporation (IFC)

• World Bank

Foster development of well functioning securities markets to:

• Broaden availability of local-currency investment instruments

• Enable private sector development

• Improve financing for housing & infrastructure

• Create jobs and improve livelihoods

INITIAL FUNDING

USD 5.5 million from Sida

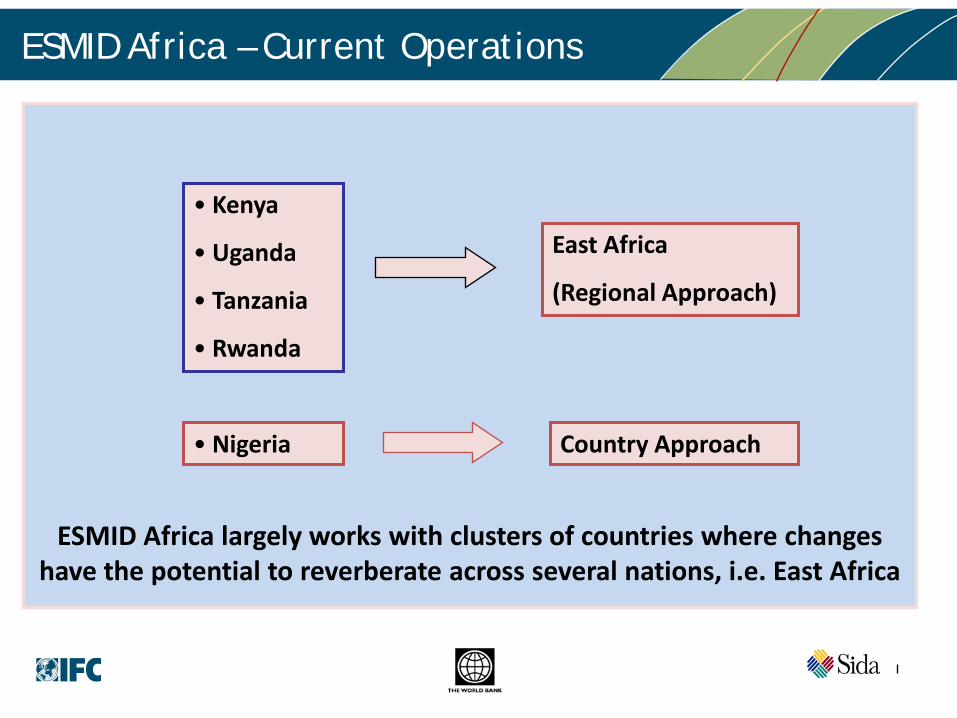

ESMID Africa – Current Operations

ESMID Africa largely works with clusters of countries where changeshave the potential to reverberate across several nations, i.e. East Africa

• Kenya

• Uganda

• Tanzania

• Rwanda

• Nigeria

East Africa

(Regional Approach)

Country Approach

18

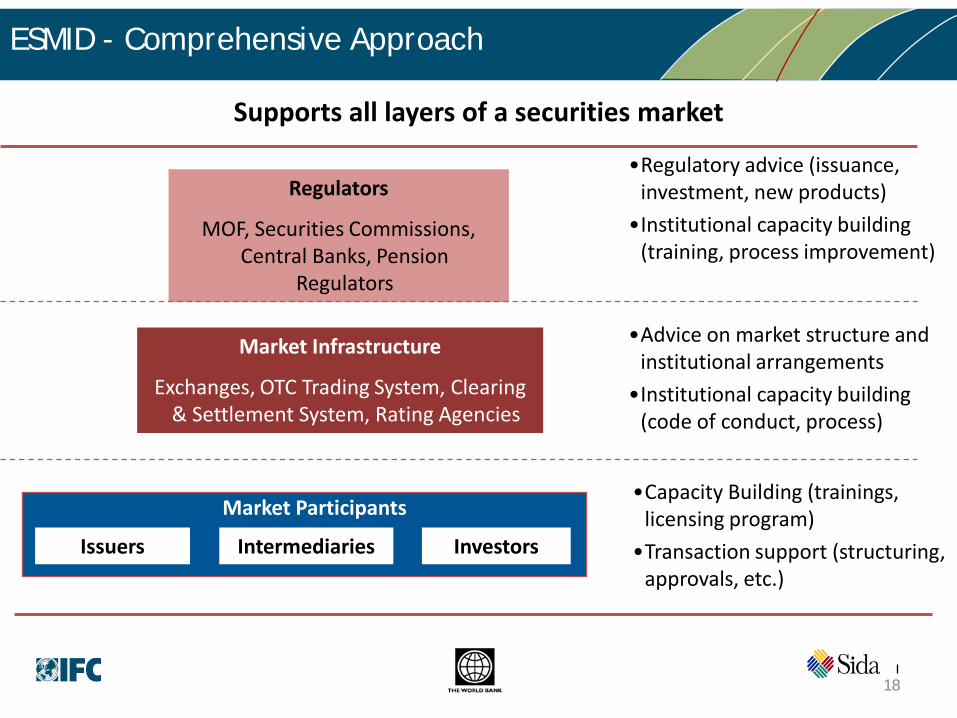

ESMID - Comprehensive Approach

Regulators

MOF, Securities Commissions, Central Banks, Pension

Regulators

Market Infrastructure

Exchanges, OTC Trading System, Clearing & Settlement System, Rating Agencies

Issuers Intermediaries Investors

Market Participants

•Regulatory advice (issuance, investment, new products)

•Institutional capacity building (training, process improvement)

•Advice on market structure and institutional arrangements

•Institutional capacity building (code of conduct, process)

•Capacity Building (trainings, licensing program)

•Transaction support (structuring, approvals, etc.)

Supports all layers of a securities market

19

ESMID East Africa Components

Legal & Regulatory Assistance

Primary issuance framework for non-government bonds

Asset Backed Securities

Bond Market Structure

Strengthening the Market Place

Market Infrastructure

Pre-trade and post-trade transparency

Bond Market Structure

Capacity

Building

Certification & Licensing framework

Securities Training Modules

Regional Training Provider

Regionalization

Regulatory Framework

Market Infrastructure

Issuers & Investors

Transactions Support

20

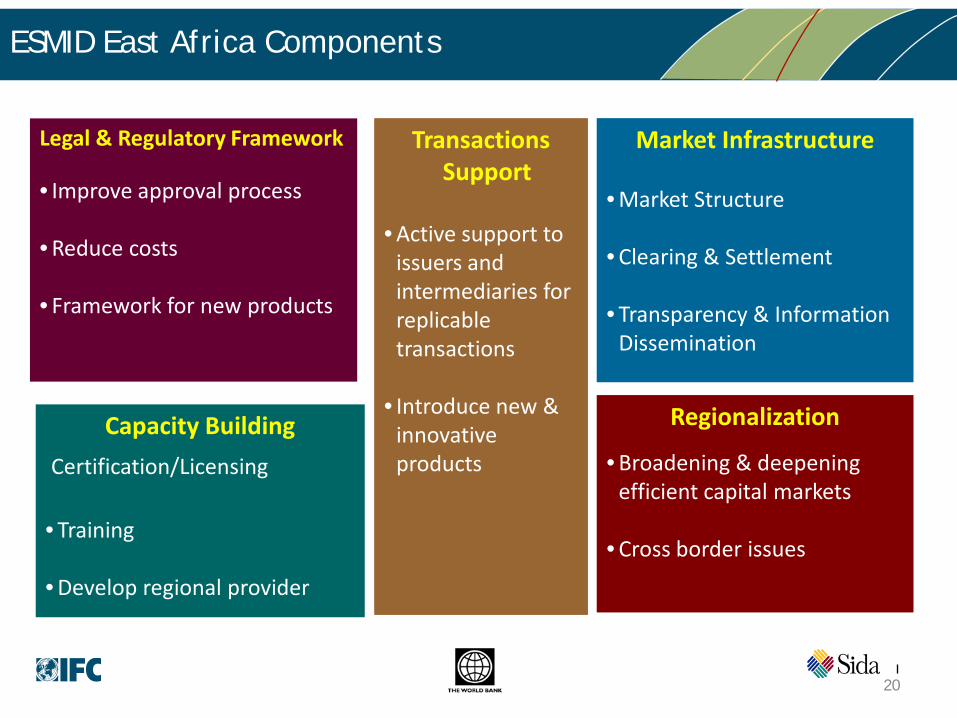

ESMID East Africa Components

Legal & Regulatory Framework

• Improve approval process

• Reduce costs

• Framework for new products

Capacity Building

Certification/Licensing

• Training

• Develop regional provider

Market Infrastructure

• Market Structure

• Clearing & Settlement

• Transparency & Information Dissemination

Regionalization

• Broadening & deepening efficient capital markets

• Cross border issues

Transactions Support

• Active support to issuers and intermediaries for replicable transactions

• Introduce new & innovative products

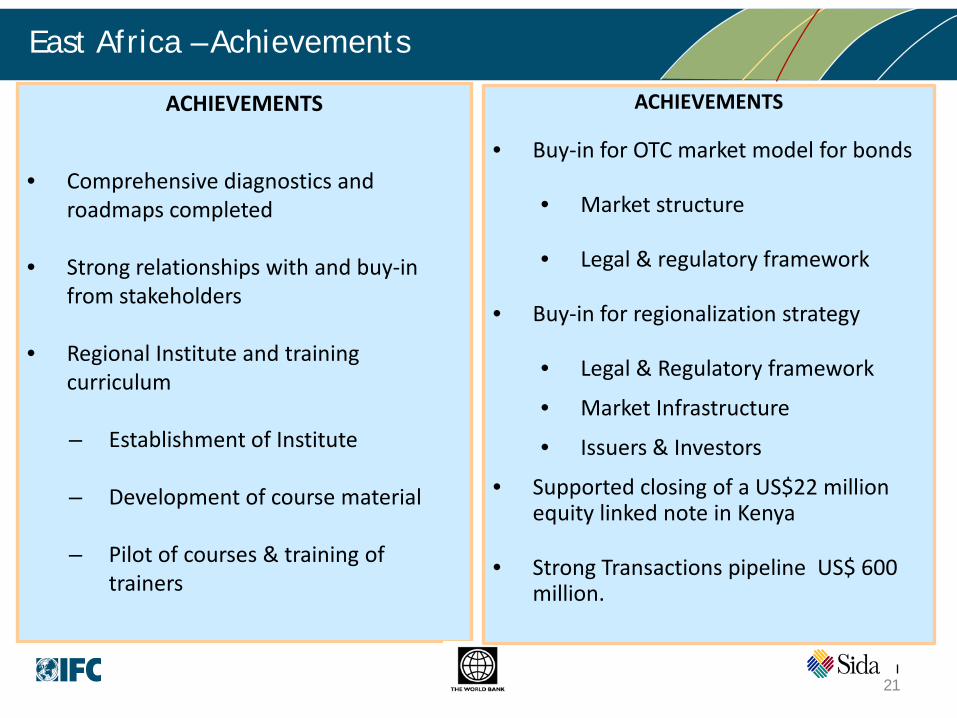

East Africa – Achievements

ACHIEVEMENTS

• Comprehensive diagnostics and roadmaps completed

• Strong relationships with and buy-in from stakeholders

• Regional Institute and training curriculum

– Establishment of Institute

– Development of course material

– Pilot of courses & training of trainers

21

ACHIEVEMENTS

• Buy-in for OTC market model for bonds

• Market structure

• Legal & regulatory framework

• Buy-in for regionalization strategy

• Legal & Regulatory framework

• Market Infrastructure

• Issuers & Investors

• Supported closing of a US$22 million equity linked note in Kenya

• Strong Transactions pipeline US$ 600 million.

22

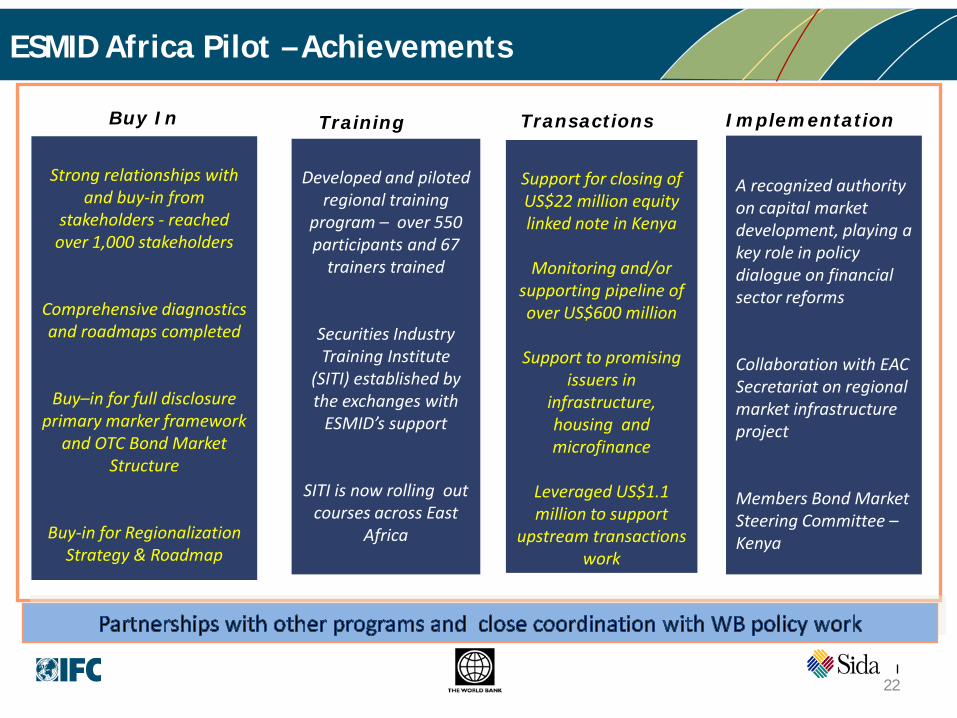

ESMID Africa Pilot – Achievements

Strong relationships with and buy-in from

stakeholders - reached over 1,000 stakeholders

Comprehensive diagnostics and roadmaps completed

Buy–in for full disclosure primary marker framework

and OTC Bond Market Structure

Buy-in for Regionalization Strategy & Roadmap

Developed and piloted regional training

program – over 550 participants and 67

trainers trained

Securities Industry Training Institute

(SITI) established by the exchanges with

ESMID’s support

SITI is now rolling out courses across East

Africa

A recognized authority on capital market development, playing a key role in policy dialogue on financial sector reforms

Collaboration with EAC Secretariat on regional market infrastructure project

Members Bond Market Steering Committee –Kenya

Support for closing of US$22 million equity linked note in Kenya

Monitoring and/or supporting pipeline of over US$600 million

Support to promising issuers in

infrastructure, housing and microfinance

Leveraged US$1.1 million to support

upstream transactions work

Buy In Training Transactions Implementation

23

“We at the NSE support this initiative. We know it will broaden the reach of our members in common competence and standards of dealings in the markets.” – James Wangunyu, Chairman, Nairobi Stock Exchange, Sep 2008

“The [ESMID] project comes at a time when Kenya and other African countries are grappling with the needs of their growing economies and the need to improve infrastructure.” – East African Standard, Sep 2007

“ESMID has been very instrumental in coming up with a framework that we can follow in the coming future…” --Pierre Celestin Rwabukumba, Capital Markets Advisory Council of Rwanda, Nov 2008

“ESMID has come in and provided a diagnostic on the situation on the ground…it is an independent and objective diagnostic. It is a collaborative process… they have come and brought all stakeholders on…” –Simon Rutega, CEO, Uganda Securities Exchange, Nov 2008

THANK YOU

24

THANK YOU

Related Documents