EFFECTS OF DOMESTIC DEBT ON ECONOMIC GROWTH OF NIGERIA (1990 – 2010) Obiwuru, Timothy Chidi, University of Lagos, Nigeria Okwu, Andy Titus, Babcock University, Nigeria Ekezie Johnbosco Okeahialam, Postgraduate Student, Warwick University, U. K. ABSTRACT Persistent increases in stock of domestic debt in Nigeria have raised concerns about effects of such debt stock on growth of the economy. This study employed econometric methodology to examine the phenomenon of domestic debt in relation to growth of the Nigerian economy for the period 1990-2010. The objective was to establish the effect of the phenomenal debt stock increases on economic growth in Nigeria during the study period. The major tool of analysis was multiple regression model premised on theorised functional relationship between economic growth and domestic debt stock. Gross domestic product (GDP) entered the model as response variable and proxy for economic growth, domestic debt stock (DDS), expenditure on debt servicing (EDS) and domestic credit to the economy (DCE) were considered as the causal variables, with interest rate (INT) as the moderating variable. Data used for analysis were obtained from Statistical Bulletin of the Central Bank of Nigeria. Diagnostic tests were conducted to ascertain Stationarity, Co-integrating and Stability features of the data series. Facilitated with Econometric Views version7 (EViews7) statistical software, the LS estimation techniques were employed to obtain estimates of model parameters. The estimated model was subjected to evaluation. The results revealed that while those domestic debt components exerted significant positive effects on economic growth, interest rate exerted insignificant negative effect. On the aggregate, the variables jointly exerted significant effect, and highly explained variations in economic growth during the study period. Consequently, the study concluded that domestic debt enhanced growth during the period, and, thus, recommended that growth-oriented strategies should be top priority in domestic debt and its dynamics. Key words: Domestic debt, Economic growth, Analysis JEL Classification: C22, C51, H63, O47 1. INTRODUCTION The need to finance rising government expenditure, accommodate budget deficits, and implement monetary policies has been identified to be responsible for the rapid increase in the stock of Nigeria’s domestic debt. The history of domestic government debt goes back to 1958 when financial reforms introduced by the colonial government marked the beginning of the existing market for government borrowing in Nigeria. One major outcome of these reforms is the creation of the Central Bank of Nigeria (CBN) and the creation of Marketable Public Securities to finance fiscal deficit. According to paragraph 35 of the Central Bank of Nigeria (CBN) Ordinance

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

EFFECTS OF DOMESTIC DEBT ON ECONOMIC GROWTH OF NIGERIA (1990 – 2010)

Obiwuru, Timothy Chidi, University of Lagos, Nigeria

Okwu, Andy Titus, Babcock University, Nigeria

Ekezie Johnbosco Okeahialam, Postgraduate Student, Warwick University, U. K.

ABSTRACT

Persistent increases in stock of domestic debt in Nigeria have raised concerns about effects of such debtstock on growth of the economy. This study employed econometric methodology to examine thephenomenon of domestic debt in relation to growth of the Nigerian economy for the period 1990-2010.The objective was to establish the effect of the phenomenal debt stock increases on economic growth inNigeria during the study period. The major tool of analysis was multiple regression model premised ontheorised functional relationship between economic growth and domestic debt stock. Gross domesticproduct (GDP) entered the model as response variable and proxy for economic growth, domestic debtstock (DDS), expenditure on debt servicing (EDS) and domestic credit to the economy (DCE) wereconsidered as the causal variables, with interest rate (INT) as the moderating variable. Data used foranalysis were obtained from Statistical Bulletin of the Central Bank of Nigeria. Diagnostic tests wereconducted to ascertain Stationarity, Co-integrating and Stability features of the data series. Facilitatedwith Econometric Views version7 (EViews7) statistical software, the LS estimation techniques wereemployed to obtain estimates of model parameters. The estimated model was subjected to evaluation.The results revealed that while those domestic debt components exerted significant positive effects oneconomic growth, interest rate exerted insignificant negative effect. On the aggregate, the variablesjointly exerted significant effect, and highly explained variations in economic growth during the studyperiod. Consequently, the study concluded that domestic debt enhanced growth during the period, and,thus, recommended that growth-oriented strategies should be top priority in domestic debt and itsdynamics. Key words: Domestic debt, Economic growth, AnalysisJEL Classification: C22, C51, H63, O47

1. INTRODUCTION

The need to finance rising government expenditure, accommodate budgetdeficits, and implement monetary policies has been identified to beresponsible for the rapid increase in the stock of Nigeria’s domestic debt.The history of domestic government debt goes back to 1958 when financialreforms introduced by the colonial government marked the beginning of theexisting market for government borrowing in Nigeria. One major outcome ofthese reforms is the creation of the Central Bank of Nigeria (CBN) and thecreation of Marketable Public Securities to finance fiscal deficit.According to paragraph 35 of the Central Bank of Nigeria (CBN) Ordinance

1958, the bank shall be entrusted with the issue and management of FederalGovernment Loans publicly issued in Nigeria upon such terms and conditionsas may be agreed between the Federal Government and the Bank (CBN, 1999).Since the early 1960s, the ratio of domestic debt to gross domestic product(GDP) has been on the increase. Nigeria has not been alone in experiencingescalating levels of government domestic indebtedness, but in comparison toother countries in sub-Saharan Africa, Nigeria’s domestic debt-GDP ratio isclearly on the high side (Asogwa, 2005).

Fiscal and monetary policies are the two broad frameworks the governmentemploys to generate revenue for its expenditures as well as regulation ofthe economy. Fiscal policy is implemented through taxation while revenue-oriented monetary policy is implemented through issuing of domestic debtinstruments which are denominated in local currency. The NigerianGovernment uses domestic debt to part-finance its expenditure. Inprinciple, though limited to their abilities to issue such, the state andlocal governments can also issue debt instruments. The stock of governmentdebt is measured relative to national output in terms of nominal domesticdebt structure as a percentage of total debt which has grown tremendouslyfrom N0.23 billion at inception to N1.86 billion as at 1980. The level ofexternal debt became larger than that of domestic debt for the first timein 1986, at the inception of the Structural Adjustment Program (SAP). Eversince, the stock of external debt has consistently been larger thandomestic debt (Adesina, 2002). Domestic debt in poor countries has beenjustified on the ground that it facilitates development of deep and liquidinternal financial markets, protects countries from unfavourable externalshocks, and mitigates foreign exchange risk (Del and Piero, 2003; Aizenman,Pinto and Radziwill, 2004; Kumhof, 2005).

Theoretically, governments incur domestic debts to finance budget deficits,implement monetary policy and develop financial instruments to deepen thefinancial markets (Alison, 2003). Corroborating this, Soludo (2003)explains that countries borrow for two broad macroeconomic reasons: tofinance higher investment, higher consumption (education and health) and tofinance transitory balance of payments deficits (to lower nominal interestrates abroad, lack of domestic long-term credit, or to overcome hard budgetconstraints). This implies that economies incur debts to boost economicgrowth and reduce poverty. However, Soludo (2003) notes that once aninitial stock of debt grows to a certain level, servicing it becomes aburden and countries find themselves on the wrong side of the debt-laffercurve, with debt crowding out investment and growth. This seems to be thesituation in Nigeria today because real investment, which would accordinglyresult to high-speed growth with positive effects on poverty, seems to beon the downward slope.

Economic growth is a sustained increase in a country’s Gross DomesticProduct (GDP) over a considerable period of time. As a measure of economic

growth, like other macroeconomic indicators, it is expressible in nominaland real terms. For real terms, nominal GDP is adjusted for the effects ofinflation to provide a meaningful measure of growth over time. Theorysuggests that reasonable levels of borrowing by a developing country arelikely to enhance economic growth. Enhancing economic growth by at least 5%growth rate is likely to reduce poverty level. Thus, to encourage growth,countries at early stages of development, like Nigeria, borrow to augmentwhat they have because of dominance of small capital stock; hence they arelikely to have investment opportunities with rates of return higher thanthat of their counterparts in developed economies. This becomes effectiveas long as borrowed funds and some internally ploughed back funds areproperly utilized for productive investment and do not suffer frommacroeconomic instability, policies that distort economic incentives, orsizable adverse shocks. Growth, therefore, is likely to increase and allowfor timely debt repayments. When this cycle is maintained for a period oftime growth will affect per capita income positively which is aprerequisite for poverty reduction. These predictions are known to holdeven in theories based on the more realistic assumption that countries maynot be able to borrow freely because of the risk of debt denial (Pattillo,2002).

Although the debt overhang models do not analyze the effects of debt ongrowth explicitly, the implication still remains that large debt stockslower growth by partly reducing investment with a resultant negative effecton poverty. But the incentive effects associated with debt stocks tend toreduce the benefits expected from policy reforms that would enhanceefficiency and growth, such as trade liberalization and fiscal adjustment.When this happens the government will be less willing to incur currentcosts if it perceives that the future benefits, in terms of higher outputwill accrue partly to foreign lenders (Iyoha, 1999). In support of thisconcept, Stiglitz (2000) explained that government borrowing can crowd outinvestment, which will reduce future output and wages. However, the worksof Pattillo (2002), Pattillo, Poirson and Ricci (2004) were unable to findevidence of a significant crowding out effect, while Chowdhury (2004),Clements, Bhattacharya and Nguyen (2003) found that both debt burden anddebt service obligations have reduced investment and economic performance.When output and wages are affected, welfare of the citizens will be madevulnerable.

For the past two decades, Nigeria has borrowed large amounts, often athighly concessional interest rates with the hope to accelerate developmentthrough higher investment, faster economic growth and poverty reduction.But, on the contrary, economic growth and poverty situations are staggeringat the back door amidst excess debt, although the former was the initialintention. It is therefore obvious that Nigeria indebtedness has gonebeyond reasonable limits needed to achieve desired goals and engender debt-free or less debt burden that will enhance economic growth with a resultant

improvement in poverty level (Sanusi, 2003). For the understanding that,unlike domestic debt, external debt is more difficult to service and repay,focus has largely been on external debt thereby neglecting domestic debtentirely or mentioning it briefly. But this is true only when the domesticdebt stock is moderate and not when it is large and growing.

Consequently, this paper investigates the causality between domestic debtand economic growth in an attempt to establish the effects of domestic debtburden on economic growth in Nigeria by answering these questions: 1. Whathas been the effect of domestic debt stock on growth of the Nigerianeconomy? 2. How has government spending on domestic debt servicing affectedgrowth of the economy? 3. What has been the effect of domestic credit tothe economy on economic growth? 4. How has interest rate affected growthof the economy? 5. What has been the joint effect of domestic debt stockand its components on growth of the Nigerian economy? Following thisinstruction is Section Two in which related literature is reviewed. Sectionthree discusses the methodology used for analysis. In section four,analysis of data and discussions are carried out while Section fiveconcludes the paper and proffers recommendations.

2. Theoretical Framework and Literature Review

Theoretically, crowding process arises once the government borrows heavilyfrom within the domestic economy. Such borrowing induces fund shortagesthat are further prompted by increased demand for investible funds whichdrives interest rates up, leading to reduction in private borrowing and,hence, limiting private investment. Though there are different types ofcrowding out effects, fiscal and financial crowding outs are relevant tothis paper. Fiscal crowding out is usually explained within the frameworkof Keynesian analysis. It occurs when increased government expenditure frombudget deficit raises aggregate demand, for constant money supply, theinterest rates rise. The stimulative effect of government deficit willcrowd out, in greater or lesser degree, a certain amount of privateinvestment. The Keynesians and the monetarists differ on the effects ofbudget deficit on the crowding effect. The main difference is thatKeynesians focus more on the short-run effect while the monetarists focuson the long-run effect. On the other hand, financial crowding out occurswhen the government increases its expenditure and finances it by sellingnew bonds in the money market. As such, the prices of securities fall andinterest rates rise. In response, the private sector postpones or curtailssome schemes because obtaining funds become costlier. Consequently, thegovernment expenditure crowds out private investment spending. Totalfinancial crowding out occurs when the bond-financed government expenditureequals the same amount of displaced private investment.

There are studies on the effects of domestic debt on economic growth. Blavy(2006) found that “threshold level of debt” is 21% of GDP, below that

level, debt is positively associated with productivity, but the coefficientfor the “above threshold debt” becomes negative and significant. The totaleffect of high debt on economic growth is significantly negative. He foundthat doubling of public debt would reduce productivity cum economic growthby about 1.5%. However, Abbas (2005) found a significant positive growth-payoff to debt, even at the very high levels of 93% of GDP. His analysispresented quite a complex picture of the relationship between domestic debtand growth. On the one hand, the results seemed to affirm conventionalwisdom that the decision to switch the source of budgetary finance fromexternal to domestic debt would be fraught with difficulties; on the other,the study obtained quite robust results on the growth-payoff of domesticdebt issuance in more developed financial systems. However, the overallrelationship remained negative. Abbas (2007) extended his previous work andfound the evidence that above a ratio of 35% of bank deposits, domesticdebt undermines economic growth. Gbosi (1998) was of the opinion thatborrowing by government from the domestic economy became the main source offinancing government expenditure due to the collapse of oil prices in theinternational market. He further explained that despite the various effortsmade by the government to rationalize public expenditure, much success hasnot been achieved in reducing the spending and this has continually raisedthe stock of domestic debt.

In another study, Waheed (2006) concluded that there is primary deficit soit has to be filled out by domestic debt, and that the only way to stop theprocess of debt accumulation is to reduce the primary deficit by continuedfiscal adjustment. This adjustment should not be achieved on the cost ofcut in development expenditure; rather there is need for serious efforts toincrease domestic tax revenue. Asogwa (2005) employed a more comprehensivetechnique to investigate the effects of domestic debt on economic growth.He concluded that domestic debt in Nigeria has continued to suffer a formof confidence crisis as market participants have consistently shown greaterunwillingness to hold longer maturities. In a cross-sectional study ofdomestic debt markets, Christensen (2004) employed a new data set on 27Sub-Sahara African countries for 20-year period, 1980–2000, and found thedomestic debt markets to be generally small, highly short term, often hainga narrow investors base, and that domestic debt servicing presentssignificant burdens to the budget, despite much smaller size of domesticdebt relative to foreign indebtedness. Further, the use of domestic debtwas found to have significant crowd-out effect on private investment.

Ajayi (1989) traces the origin of Nigeria’s debt problems to domesticlapses, the collapse of the international oil price in 1981 and thepersistent shocks from the international oil market. As a result of thedebt problem, credit facilities gradually dried up, which led to a numberof projects getting stalled. He advocated sustainable economic growth as apanacea to the debt burden. Sanusi (1988) noted that faulty domesticpolicies, which range from project financing mismatch and inappropriate

monetary and fiscal policies, were responsible for domestic borrowingproblem. For instance, the expansionary policies led to stupendousmacroeconomic fallout, which encouraged import but discouraged exportproduction. Oshadami (2006) concluded that domestic debt burden hasnegative effects on proper conduct of monetary policy, inflation and growthof the economy.

Cunningham (1993) found that debt burden has a negative effect on economicgrowth through the impact on the productivity of labour and capital. James(2006) found public debt to have no significant effect on the growth of theNigeria economy, noting that the fund borrowed were not channelled intoproductive ventures, but diverted into private purse. He emphasized thatfor the gains of the debt forgiveness to be realized, the war againstcorruption should be fought to the highest level. Obviously, the analysisaggregated external and domestic components of public debt; but the currentstudy considers domestic debt. Fosu (1996) argued that GDP growth isnegatively influenced via a diminishing marginal productivity of capital,and that, on the average, a high debt country faces about one percentagereduction in GDP growth rate annually. Queientin (1984) stated thatindebtedness amounts to a problem, if a country could not afford to repayits debt. The key is the cost of debt servicing which includes therepayment of principal and interest due on the loan. He justified borrowingas arising from increased government expenditure on development programmeswithout generally an additional income to finance it. Seetanah, Radachi andDurbarry (2007) and Hameed, Ashraf and Chaudhary (2008) also investigatedthe link between public debt and economic growth using Vector ErrorCorrection model and production function for the time series, respectively.They established that debt servicing burden has a negative effect onproductivity of labour and capital which ultimately negatively affectseconomic growth. Guidotti and Kamar (1991) studied the case of 15 emergingeconomies and found that domestic debt-GDP ratio went from 10% in 1981 to16% in 1988 and remained more or less constant over the period, and thatthese important differences in the process have led to accumulation ofdomestic and external debt in these countries. However the increase indomestic debt was mainly due to new borrowing and that of external debt wasdue to accumulation of arrears. This suggests that if emerging marketcountries had not been shut down from the international capital market,they would have probably accumulated more external and less domestic debt.

It is obvious from these studies that there has not been a consensus on theeffects of domestic debt on economic growth.

2.1 Overview of Domestic Debt in Nigeria

Domestic debt instruments play a vital role in any economy in the world,including capitalist, socialist and mixed economies. They provide economicagents with alternative options to banking for allocating their savings

accordingly. It is a key part of the collateral used by the government inthe financial markets and, thus, it has an important role in monetarypolicy implementation. The composition of Nigeria domestic debt shows thattreasury bills constitute the main component of government debt. Itaccounted for 77.4% of total domestic debt in 1960, declined to 51% by 1970but rose to 62% 2003. The decline in the percentage share of treasury billsin the mid-1970s happened as revenue from the oil sector improvedsubstantially (Okunrounmu, 1992). The growth in the level of Treasury billalso reflected the practice of rollover of matured securities andcontinuous recourse to conversion of ways and means advances outstanding atthe end of the year to treasury bills as a way of funding the fiscaldeficits. Treasury certificates, which were first issued in 1968,constituted one of the largest securities between 1983 and 1988. Treasurycertificates surpassed treasury bills issued to further deepen the domesticmoney market by increasing short term investment options available. In1995, the Federal Government of Nigeria reduced the debt serviceobligations on domestic government debt; consequently, treasury certificatewas abolished in 1996. In 1989, the monetary authorities introduced theauction bid system for flotation of treasury bonds as another instrument inthe portfolio of domestic debt. The objective was to minimize the serviceobligation on domestic debt arising from the liberalization policies. Thus,in 1989, N20 million worth of treasury bills representing 58.6% of treasurybills outstanding were converted to Treasury bond.

Development stocks were apparently the first government instruments to beissued. Development stocks were floated largely to provide developmentfinance either directly to meet the needs of the Federal Government or asloan lent to the state governments. The development stocks were firstregistered debt stocks in 1956. The stock outstanding increased in 1960,1987 and 1988. The stock is traded in the secondary market of the NigeriaStock Exchange (Alison, 2003).

In 1990, total domestic debt was N28, 440.2 million, but rose to N36,790.6million in 1991, an increase of N8,350.4 million. In 1994, domestic debtincreased to N84,093.1 million from N47,031.1 million in 1992, showing anincrease of N37,062.0 million. The increase in Government domestic debtbetween 1993 and 1994 exceeded the increase between 1990 and 1991 by N28,711.6 million. The increase was necessitated by the need for the Governmentto finance budget deficit. In 2000, domestic debt stock outstanding roseenormously to N343,674.1 million. The increase was almost five folds fromN84,093.1 million in 1994. By 2004 Government domestic debt had grown toN898,253.9 million showing an increase of N554,579.8 million. The highgrowth rate of domestic debt continued in 2005, N1,016,994.0 million,N1,166,000.7 million in 2006, N1,329,692.7 million in 2007, andN1,370,325.2 million in 2008. As at 30th September 2011, the stock ofdomestic debt in Nigeria stood at N5.31 trillion, representing about 17.52%of GDP. In absolute terms, Nigeria’s domestic debt has grown rapidly over

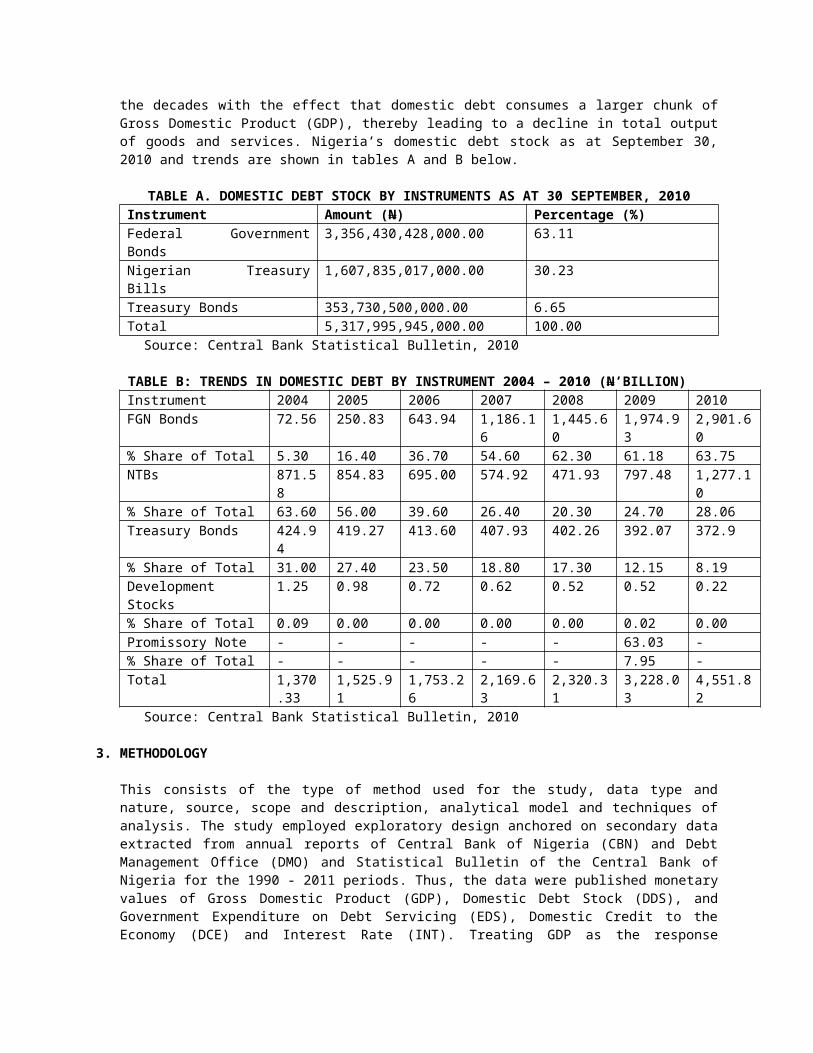

the decades with the effect that domestic debt consumes a larger chunk ofGross Domestic Product (GDP), thereby leading to a decline in total outputof goods and services. Nigeria’s domestic debt stock as at September 30,2010 and trends are shown in tables A and B below.

TABLE A. DOMESTIC DEBT STOCK BY INSTRUMENTS AS AT 30 SEPTEMBER, 2010Instrument Amount (N) Percentage (%)Federal GovernmentBonds

3,356,430,428,000.00 63.11

Nigerian TreasuryBills

1,607,835,017,000.00 30.23

Treasury Bonds 353,730,500,000.00 6.65Total 5,317,995,945,000.00 100.00

Source: Central Bank Statistical Bulletin, 2010

TABLE B: TRENDS IN DOMESTIC DEBT BY INSTRUMENT 2004 – 2010 (N’BILLION)Instrument 2004 2005 2006 2007 2008 2009 2010FGN Bonds 72.56 250.83 643.94 1,186.1

61,445.60

1,974.93

2,901.60

% Share of Total 5.30 16.40 36.70 54.60 62.30 61.18 63.75NTBs 871.5

8854.83 695.00 574.92 471.93 797.48 1,277.1

0% Share of Total 63.60 56.00 39.60 26.40 20.30 24.70 28.06Treasury Bonds 424.9

4419.27 413.60 407.93 402.26 392.07 372.9

% Share of Total 31.00 27.40 23.50 18.80 17.30 12.15 8.19DevelopmentStocks

1.25 0.98 0.72 0.62 0.52 0.52 0.22

% Share of Total 0.09 0.00 0.00 0.00 0.00 0.02 0.00Promissory Note - - - - - 63.03 -% Share of Total - - - - - 7.95 -Total 1,370

.331,525.91

1,753.26

2,169.63

2,320.31

3,228.03

4,551.82

Source: Central Bank Statistical Bulletin, 2010

3. METHODOLOGY

This consists of the type of method used for the study, data type andnature, source, scope and description, analytical model and techniques ofanalysis. The study employed exploratory design anchored on secondary dataextracted from annual reports of Central Bank of Nigeria (CBN) and DebtManagement Office (DMO) and Statistical Bulletin of the Central Bank ofNigeria for the 1990 - 2011 periods. Thus, the data were published monetaryvalues of Gross Domestic Product (GDP), Domestic Debt Stock (DDS), andGovernment Expenditure on Debt Servicing (EDS), Domestic Credit to theEconomy (DCE) and Interest Rate (INT). Treating GDP as the response

variable and proxy for economic growth; DDS and EDS as the causal variablesand proxies for domestic debt; INT and DCE as moderating variables andproxies for domestic capital and its cost respectively, a multipleregression model was specified to show the perceived functionalrelationship between economic growth and domestic debt.

3.1 Model Specification

Nigeria’s domestic debt and its allied characterization are categorizedinto the debt stock and servicing expenditure. Given that the intendedpurpose of domestic debt is to stimulate economic and other activities todrive the growth and development processes of the economy, proceeds fromgovernment debt contracts find their way to the intermediary financialinstitutions and private sector businesses to stimulate investment,employment and ultimately accelerate economic growth via increases in theoutput of goods and services. Thus, through the intermediary financialinstitutions, the domestic debt stock enters the credit channel to theeconomy at some cost (interest rate) in the process. From this perspective,DDS, EDS, DCE and INT are considered appropriate as determinants of GDP.Consequently, the relationship between economic growth and domestic debtstock is functionally expressed as:

GDP = f(DDS, EDS, DCE, INT) while the underlying regression model of therelationship is:

GDP = λ0 + λ1DDS + λ2EDS + λ3DCE + λ4INT + µwhere λ0 is the intercept or GDP of the economy without domestic debt ,

λi (i = 1, 2, 3, 4) are the model coefficients. Each captures the effectof associated proxy variable on economic growth (GDP), u is stochasticvariable included in the model to accommodate effect of other factors thatcan cause GDP to change but which are not explicitly included in theregression model.

A priori expectation is positive for DDS, EDS and DCE, but negative forINT. That is, since domestic debt stock, government spending on debtservices and domestic credit to the economy are sources of financingproductive investment, but interest rate discourages real investment, itis expected that while rising domestic debt stock, spending on domesticdebt servicing and credit to the economy enhance economic growth throughincreased GDP, rising interest rate retard growth via decline in GDP. Theassumptions here are that the government borrows from the investingprivate sector, keeps the borrowed funds with private sector financialintermediaries and disburses the funds through them. Thus, while DDSinitially reduces private sector investment, it enhances governmentinvestment and other expenditures. As the government services debts andundertakes other expenditures, investible funds accrue to the privatesector and investment is expanded. As part of their relevance, theintermediary financial institutions channel part of the debt stock intheir custody and other financial resources as credit to the economy.

Given that the recipients are the investing private sector, investment isfurther expanded. All these lead accelerate economic growth and increaseGDP. On the other hand, rising interest rate reduces investment throughhigher cost of capital or investment and, thus, hinders economic growth.Hence, λ1, λ2, λ3 > 0; λ4 < 0.

The functional relationship and associated regression model are specifiedto test the following hypotheses and, thus, answer the research questions:

H01: Domestic debt stock has no significant effect on economic growth.H02: Economic growth is not significantly affected by domestic debt

servicing.H03: Domestic credit to the economy has no significant relevance to

economic growth. H04: Interest rate bears no significant relevance to economic growth.H05: Domestic debt components have no significant joint effect on

economic growth.

Facilitated with the statistical software, Econometric Views version 7(EViews7) and using data on variables, the intercept and coefficients ofthe regression model were estimated via the least squares (LS) techniques,and subsequently evaluated for statistical significance, explanatorystrength and autocorrelation. While statistical significance of thecoefficients or effects of the respective causal variables was evaluatedusing the t-statistic, significance of their joint effect is determinedwith the F-statistic. Further, the coefficient of determination (R-squared) was used to test the strength of the variables in explainingvariations in GDP during the study period. With the Durbin-Watsonstatistic, autocorrelation was tested for the regression equation.

4. DATA, DIAGNOSTICS, REGRESSION RESULTS AND DISCUSSION

Data on which analysis was anchored are as presented in Table C below.

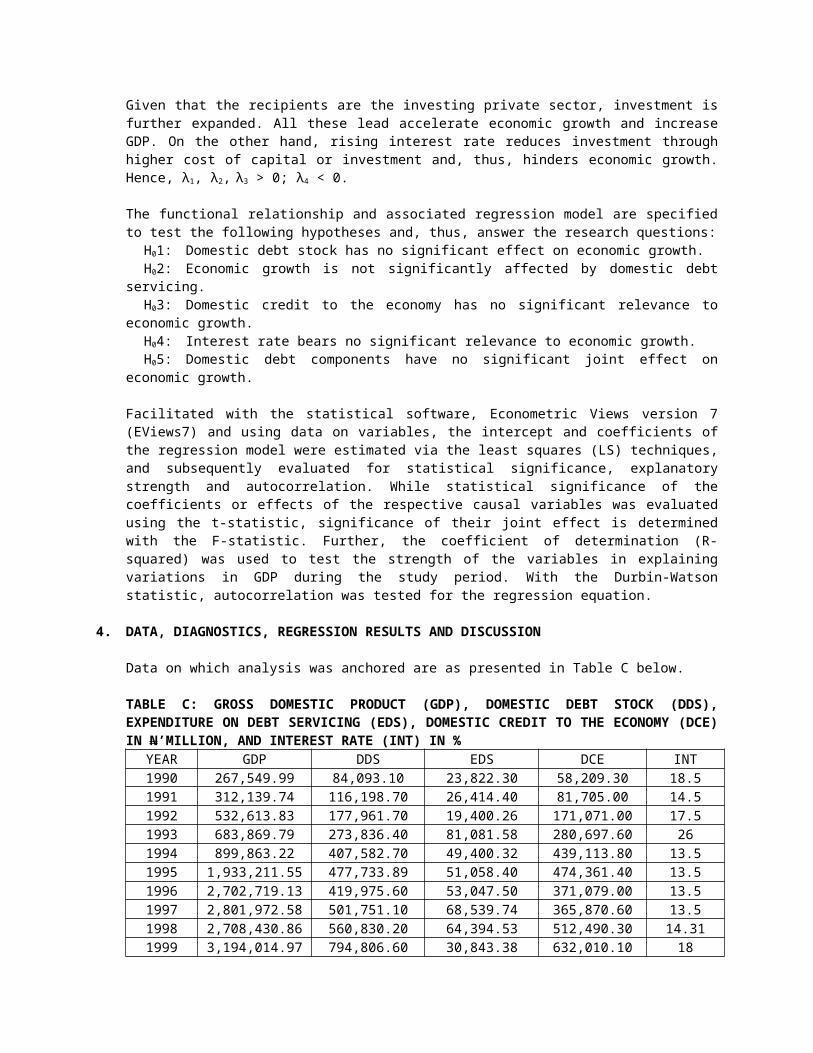

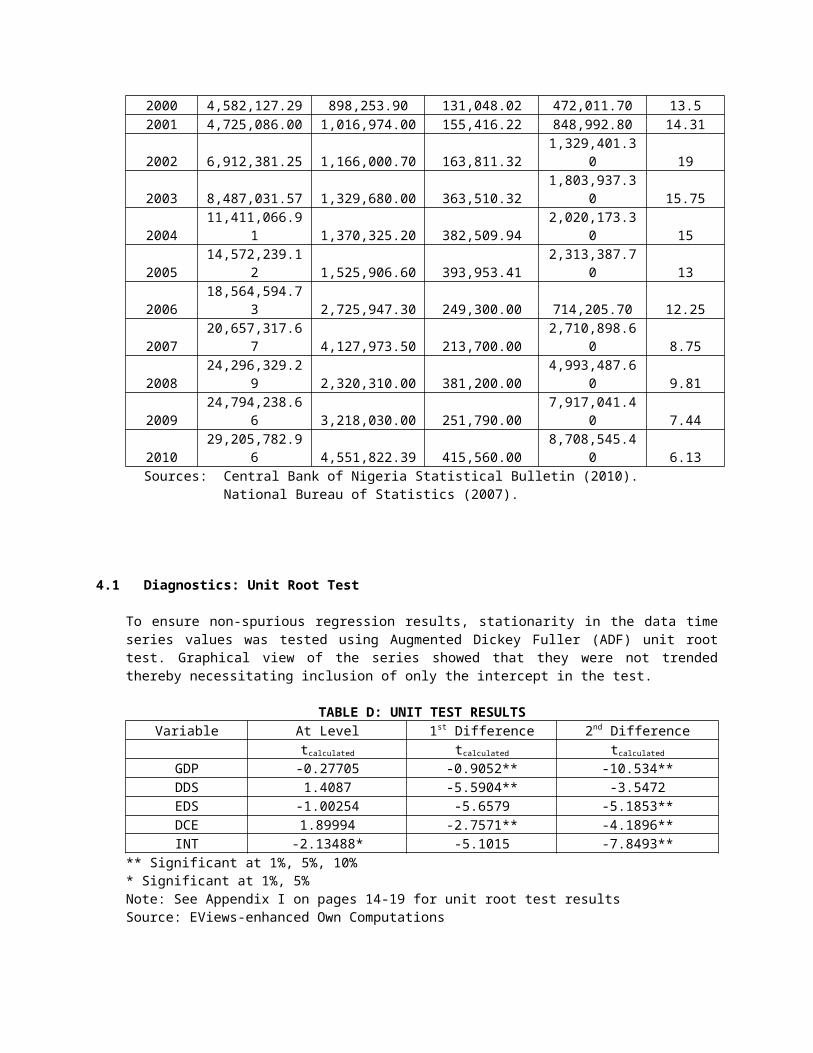

TABLE C: GROSS DOMESTIC PRODUCT (GDP), DOMESTIC DEBT STOCK (DDS),EXPENDITURE ON DEBT SERVICING (EDS), DOMESTIC CREDIT TO THE ECONOMY (DCE)IN N’MILLION, AND INTEREST RATE (INT) IN %

YEAR GDP DDS EDS DCE INT1990 267,549.99 84,093.10 23,822.30 58,209.30 18.51991 312,139.74 116,198.70 26,414.40 81,705.00 14.51992 532,613.83 177,961.70 19,400.26 171,071.00 17.51993 683,869.79 273,836.40 81,081.58 280,697.60 261994 899,863.22 407,582.70 49,400.32 439,113.80 13.51995 1,933,211.55 477,733.89 51,058.40 474,361.40 13.51996 2,702,719.13 419,975.60 53,047.50 371,079.00 13.51997 2,801,972.58 501,751.10 68,539.74 365,870.60 13.51998 2,708,430.86 560,830.20 64,394.53 512,490.30 14.311999 3,194,014.97 794,806.60 30,843.38 632,010.10 18

2000 4,582,127.29 898,253.90 131,048.02 472,011.70 13.52001 4,725,086.00 1,016,974.00 155,416.22 848,992.80 14.31

2002 6,912,381.25 1,166,000.70 163,811.321,329,401.3

0 19

2003 8,487,031.57 1,329,680.00 363,510.321,803,937.3

0 15.75

200411,411,066.9

1 1,370,325.20 382,509.942,020,173.3

0 15

200514,572,239.1

2 1,525,906.60 393,953.412,313,387.7

0 13

200618,564,594.7

3 2,725,947.30 249,300.00 714,205.70 12.25

200720,657,317.6

7 4,127,973.50 213,700.002,710,898.6

0 8.75

200824,296,329.2

9 2,320,310.00 381,200.004,993,487.6

0 9.81

200924,794,238.6

6 3,218,030.00 251,790.007,917,041.4

0 7.44

201029,205,782.9

6 4,551,822.39 415,560.008,708,545.4

0 6.13Sources: Central Bank of Nigeria Statistical Bulletin (2010).

National Bureau of Statistics (2007).

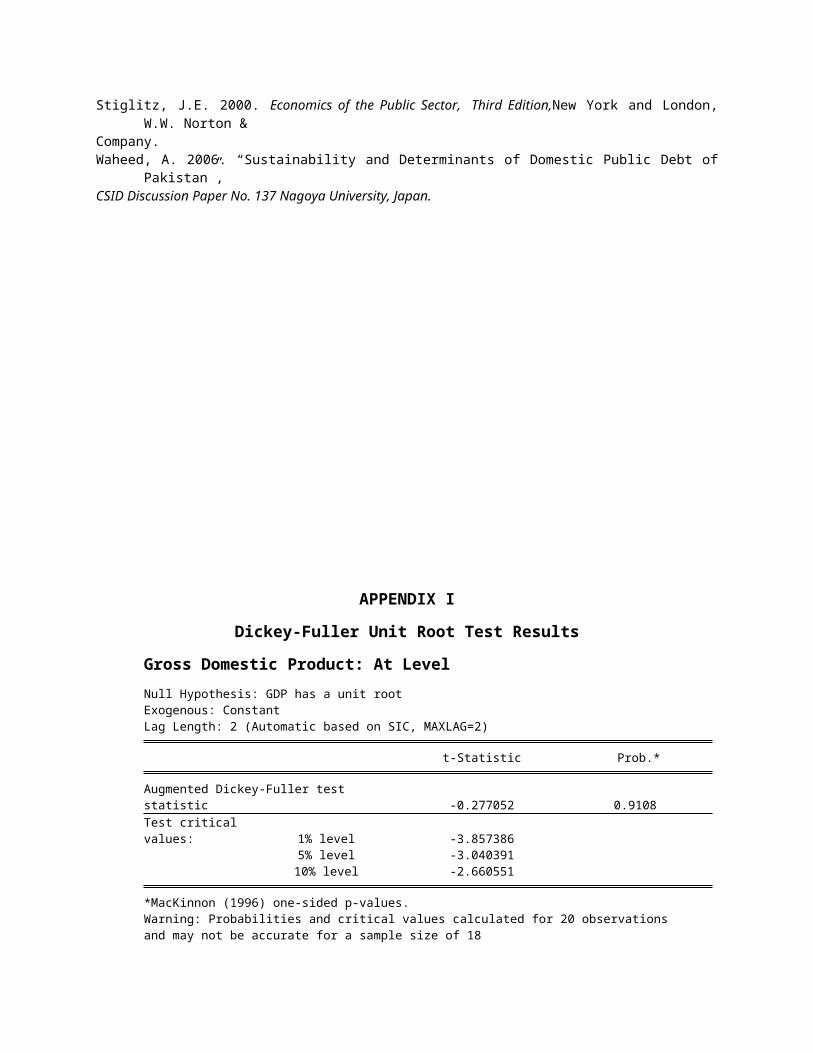

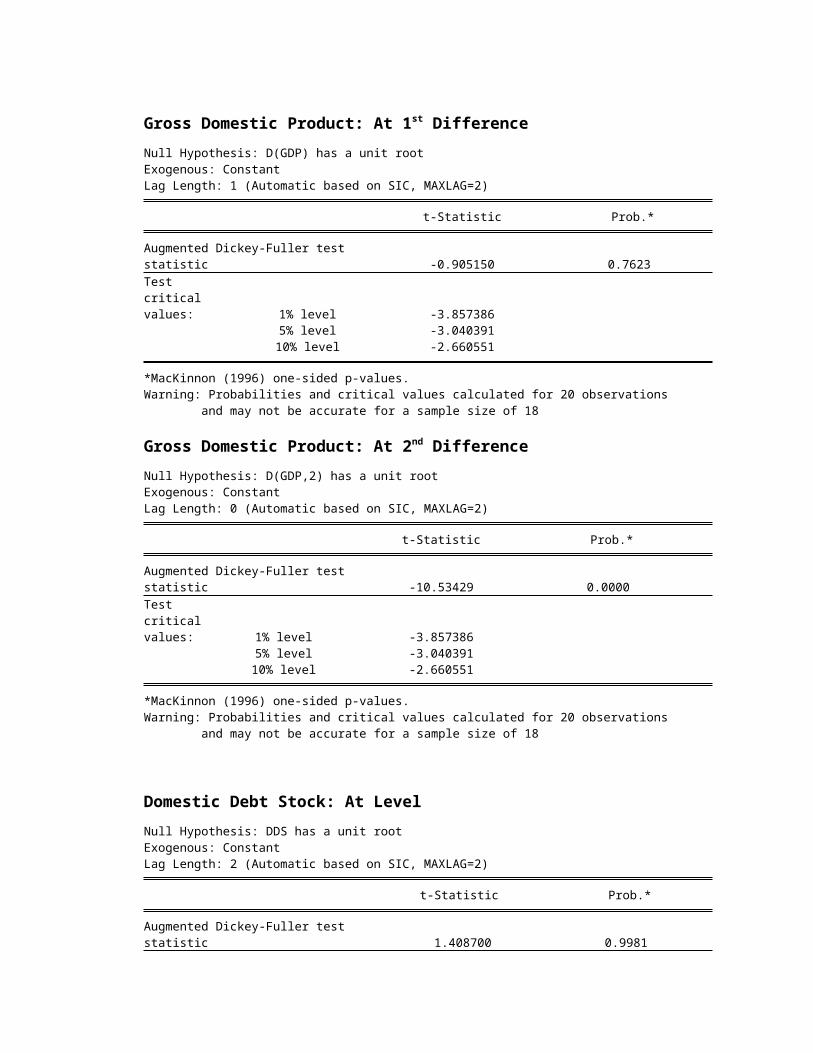

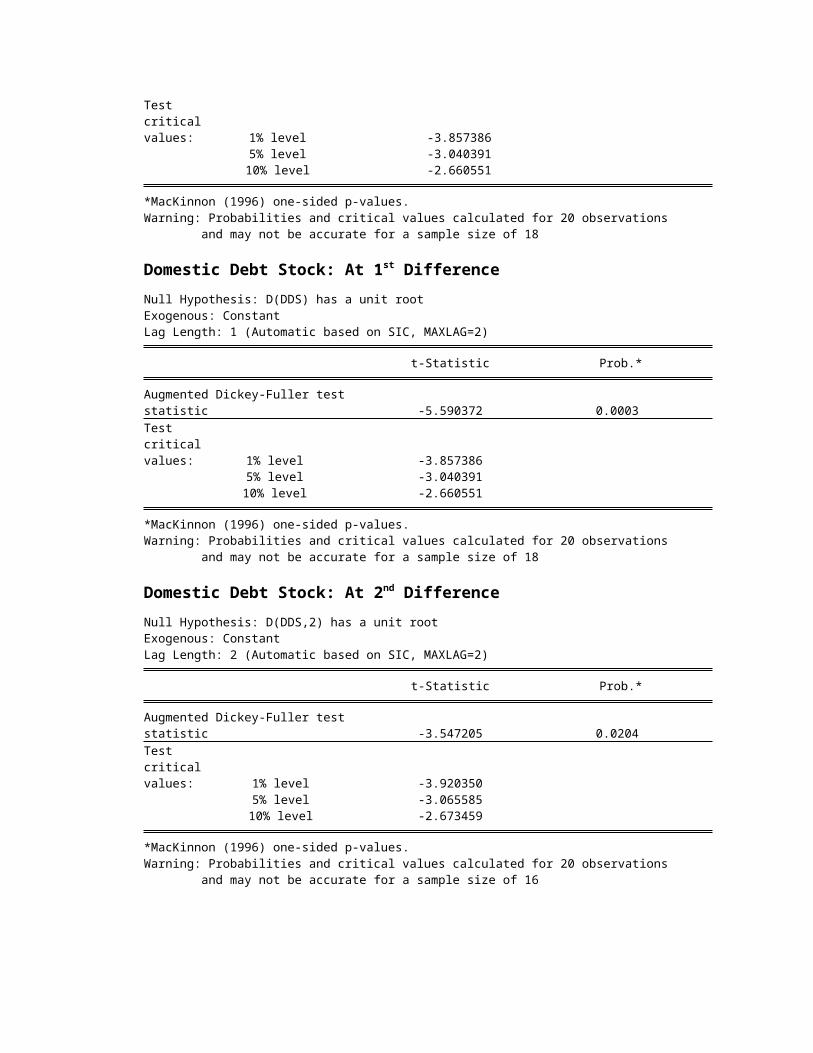

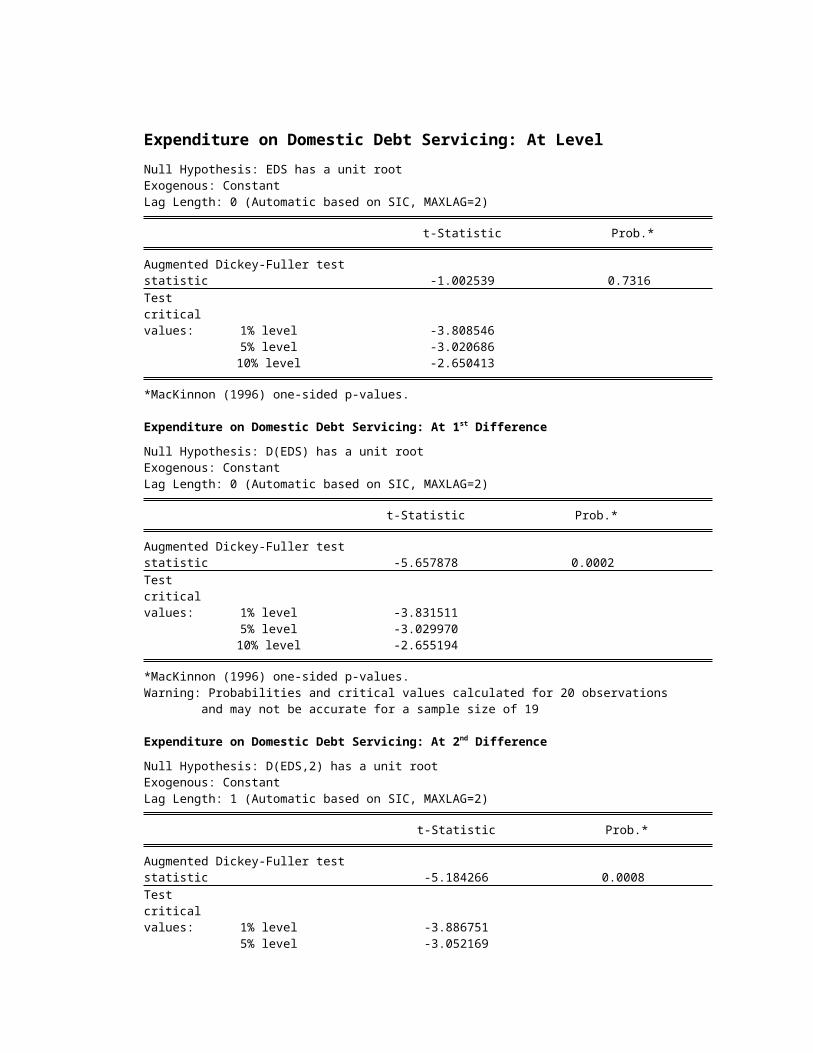

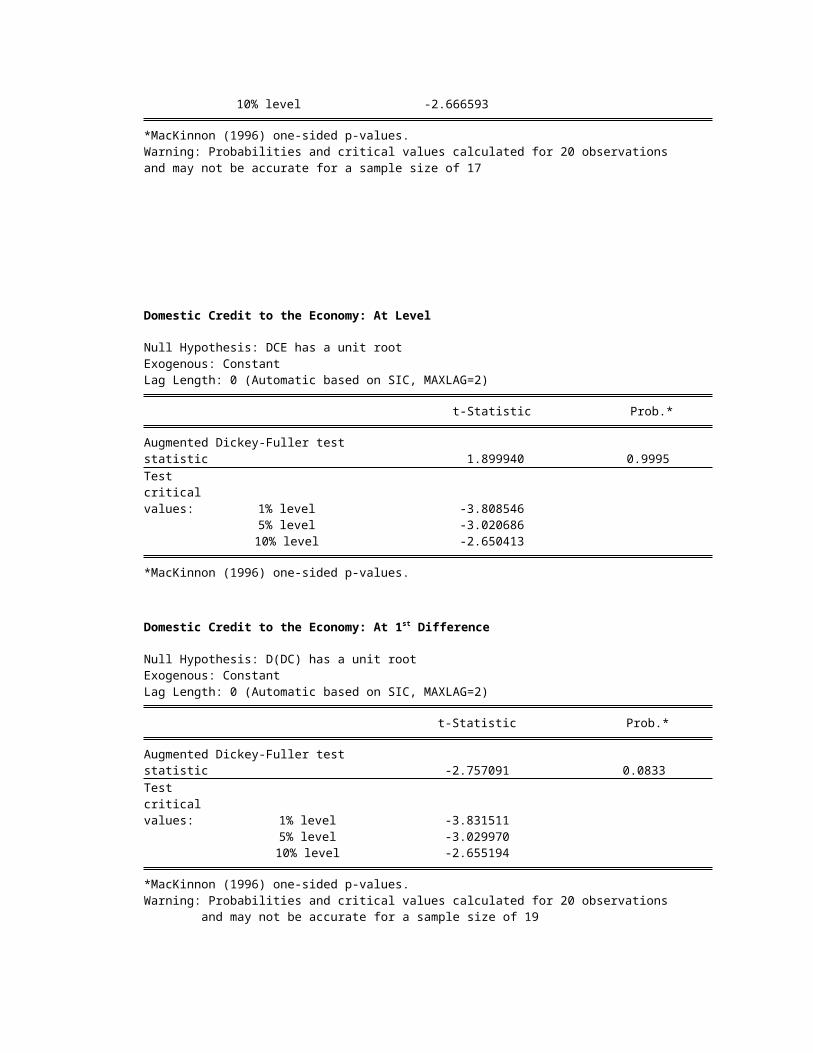

4.1 Diagnostics: Unit Root Test

To ensure non-spurious regression results, stationarity in the data timeseries values was tested using Augmented Dickey Fuller (ADF) unit roottest. Graphical view of the series showed that they were not trendedthereby necessitating inclusion of only the intercept in the test.

TABLE D: UNIT TEST RESULTSVariable At Level 1st Difference 2nd Difference

tcalculated tcalculated tcalculated

GDP -0.27705 -0.9052** -10.534**DDS 1.4087 -5.5904** -3.5472EDS -1.00254 -5.6579 -5.1853**DCE 1.89994 -2.7571** -4.1896**INT -2.13488* -5.1015 -7.8493**

** Significant at 1%, 5%, 10%* Significant at 1%, 5% Note: See Appendix I on pages 14-19 for unit root test resultsSource: EViews-enhanced Own Computations

Results of the unit root test shows that the time series of GDP, EDS, DCEand INT were stationary at 2nd differencing, DDS was stationary only at 1st

differencing, and INT was stationary only at level. This establishes that,though with varying stationarity levels, the series were stationary and,thus, provide basis to reject the null hypothesis that unit root ornonstationarity exists.

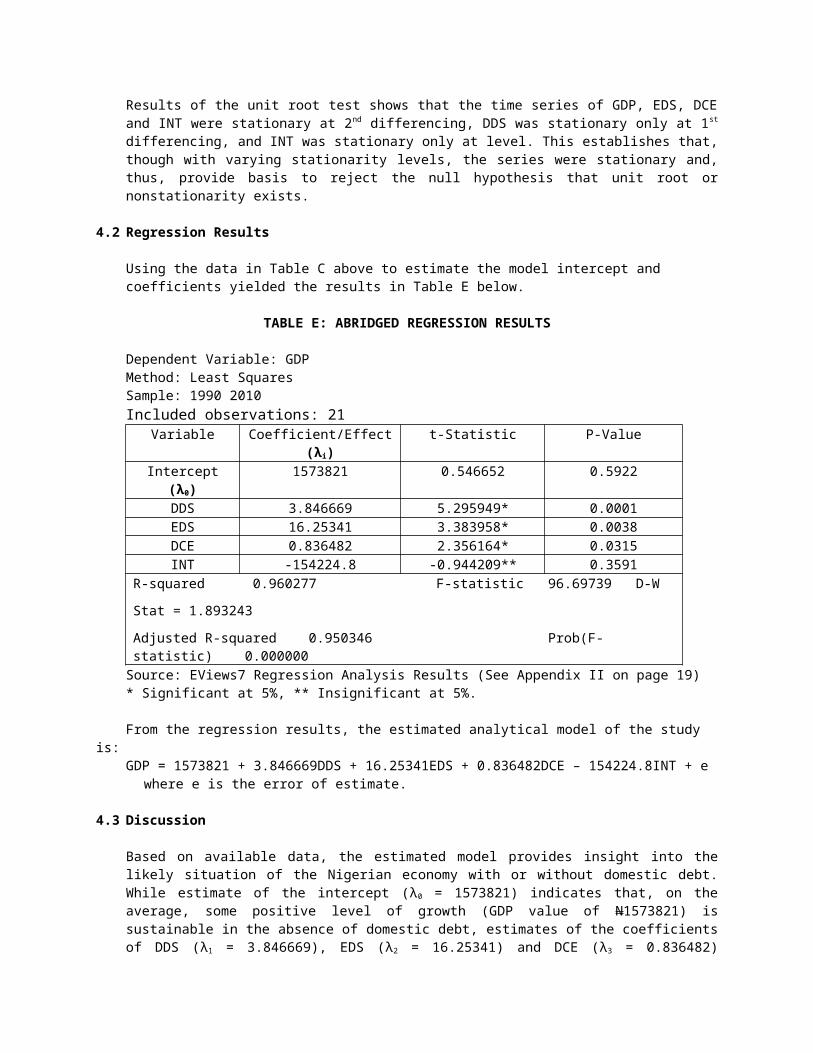

4.2 Regression Results

Using the data in Table C above to estimate the model intercept and coefficients yielded the results in Table E below.

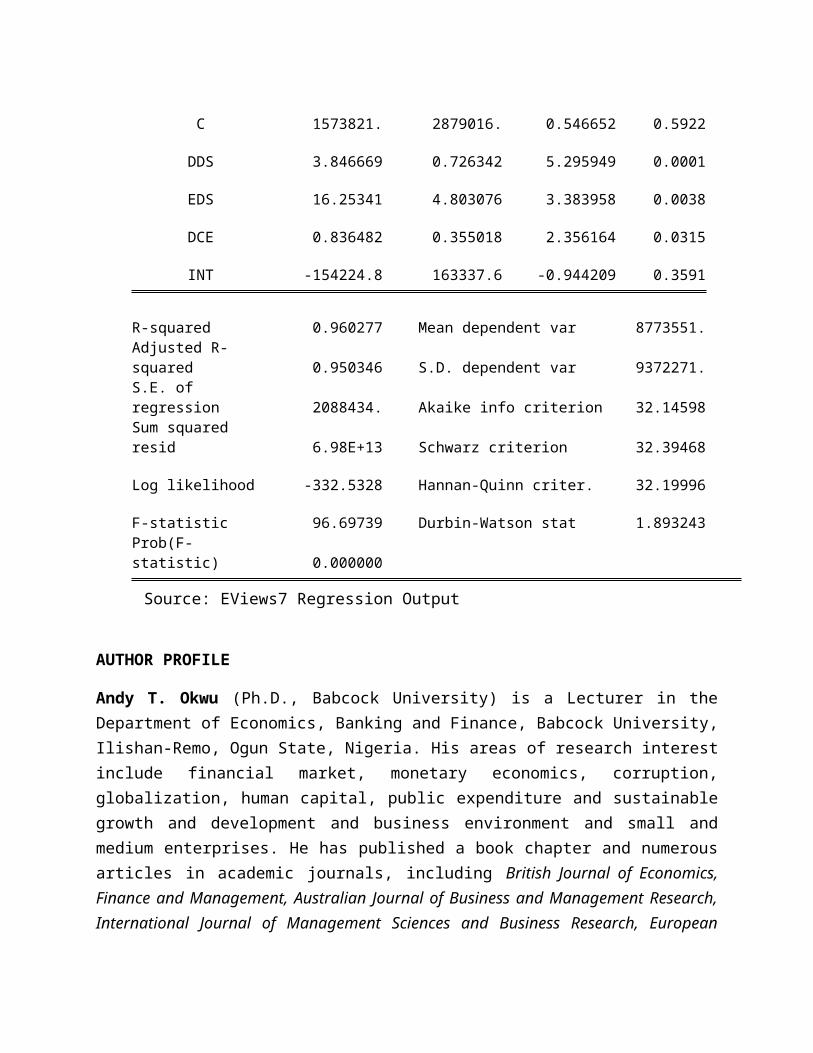

TABLE E: ABRIDGED REGRESSION RESULTS

Dependent Variable: GDPMethod: Least SquaresSample: 1990 2010Included observations: 21

Variable Coefficient/Effect(λi)

t-Statistic P-Value

Intercept(λ0)

1573821 0.546652 0.5922

DDS 3.846669 5.295949* 0.0001EDS 16.25341 3.383958* 0.0038DCE 0.836482 2.356164* 0.0315INT -154224.8 -0.944209** 0.3591

R-squared 0.960277 F-statistic 96.69739 D-W

Stat = 1.893243

Adjusted R-squared 0.950346 Prob(F-statistic) 0.000000Source: EViews7 Regression Analysis Results (See Appendix II on page 19)* Significant at 5%, ** Insignificant at 5%.

From the regression results, the estimated analytical model of the study is:

GDP = 1573821 + 3.846669DDS + 16.25341EDS + 0.836482DCE – 154224.8INT + e where e is the error of estimate.

4.3 Discussion

Based on available data, the estimated model provides insight into thelikely situation of the Nigerian economy with or without domestic debt.While estimate of the intercept (λ0 = 1573821) indicates that, on theaverage, some positive level of growth (GDP value of N1573821) issustainable in the absence of domestic debt, estimates of the coefficientsof DDS (λ1 = 3.846669), EDS (λ2 = 16.25341) and DCE (λ3 = 0.836482)

indicate that increases in each of domestic debt stock, expenditure ondomestic debt servicing and domestic credit to the economy enhanceeconomic growth, and vice versa. These are consistent with the pre-estimation expectation in this study. Specifically, N1 million increase inDDS, EDS and DCE induce respective increases of about N3.8 million, N16.3million and N0.84 in GDP, and vice versa. The estimate of coefficient ofINT (λ4 = - 154224.8) indicates that rising interest rate discouragesinvestment and reduces growth through decline in GDP. This is in line withexpectation, and it suggests that 1% increase in interest rate tends toreduce GDP by about N154224.8 million. Thus, the estimates show that whileDDS, EDS and DCE have positive effects on GDP, INT has negative effect. Interms of magnitude, EDS has greater positive effect than each of DDS andDCE. This suggests that investors channel debt servicing proceeds tofurther investments than the entire domestic borrowers invest fundsborrowed from the intermediaries. Worthy of note from the results is thatthe negative effect of INT on GDP outweighs the combined positive effectsof DDS, EDS and DCE thereby suggesting that interest rate is a morestrategic variable of investment and production output than domestic debtstock and its other components.

Further, the positive effects of DDS, EDS and DCE are significant at the5% level of significance as evidenced by the respective p-values (0.0001,0.0038 and 0.0315) associated with the t-statistics (5.295949, 3.383958and 2.356164) of the relevant coefficients (3.846669, 16.25341 and0.836482), but the negative effect of INT is not significant at 5% levelas proved by the p-value of 0.3591 associated with the t-statistic (-0.944209) of its coefficient (-154224.8). Thus, though interest rate seemsa more strategic variable, each of debt stock, debt services and credit tothe economy bears more relevance in growth process of the Nigerianeconomy. However, the p-value of 0.000000 associated with the F-statistic(96.69739) for aggregate effect provides empirical evidence that thesedomestic debt components jointly exert statistically significant positiveeffect on growth of the Nigerian economy during the study period. This isconsistent with the finding by Abbas (2005), but not with the studies byHammed et al (2008), Seetanah et al. (2007), James (2006), Fosu (1996) andCunningham (1993) which reported significant negative effects. However,while hypotheses H01, H02, H03 and H05 are not accepted, H04 is notrejected. By these, the research questions are addressed and studyobjective achieved.

Appropriateness of these domestic debt components in the model is furthersubstantiated by the R-squared (0.960277 or 96%) and its adjusted value(0.950346 or 95%) with negligible difference of 0.009931 or 1%. This isclearly reflected in their strength to explain about 95% variations in GDPfor the study period. The remaining 5% are due to the stochastic variableor estimation error in the model.

Since the Durbin-Watson statistic computed from the data sets is greaterthan upper critical value of Durbin-Watson statistic (1.893243 > 0.927),there is no evidence of autocorrelation.

5. POLICY IMPLICATION, CONCLUSION And RECOMMENDATIONS

The constraint on the analytical model is that the domestic debtcomponents determine

the growth proxy, GDP. This implies that national income or GDP changes inresponse to changes in domestic debt. Technically, it means that onlygrowth-oriented domestic debts are incurred. When growth dictatesdomestic debt dynamics, then every available debt component may beemployed because of their dependency on growth. The government may causedomestic debt depend on growth by making domestic debt to be influenced byvariables other than the growth that necessitate it. Relevance of thispolicy situates primarily within the context of domestic debt stock,expenditure on domestic debt servicing and domestic credit to the economybecause they exert positive effects on growth.

Human behaviour is erratic. Therefore, the effects of domestic debt stockand its components in this model, which are consistent with expectations,may be rendered spurious in practice by human actions. This isparticularly true because domestic debt is raised and allocated by humanbeings. Therefore, debt management units should be subjected to thesurveillance of the Economic and Financial Crimes Commission (EFCC). Thiswill ensure effective allocation of debt proceeds and accelerate economicgrowth.

Since the estimated coefficients of the analytical model have the expectedsigns, the study concludes that domestic debt stock, expenditure ondomestic debt servicing and domestic credit to the economy enhance growthof the economy, interest rate retards it. On the aggregate, these domesticdebt components have significant effect on growth. Therefore, they arerelevant determinants of economic growth in Nigeria. Consequently, thisstudy recommends that enhanced economic growth-oriented strategies shouldbe the top priority in domestic debt and its management dynamics. Forinstance, since domestic debt stock, debt servicing expenditures of thegovernment and domestic credit to the economy were found to exertsignificant positive effects on economic growth, but interest rate wasfound to retard growth, more funds should be generated through domesticdebt part of which should be used to provide conducive investment climatefor private sector participation, and the remaining channeled to realsector private investment through domestic credit to the economy.Essentially, this study advocates increases in the volume of short- andlong-term domestic debt instruments as well as more debt servingexpenditure and domestic credit to the economy at reduced interest rate.Thus, domestic debt should continued to be used as stimulant of economic

growth by switching the source of budgetary finance from external todomestic debt as a conventional wisdom. This will mitigate adverseexternal shocks in the case of dwindling revenue caused by decline inworld oil prices. .

ReferencesAbbas, S. M. 2005. “Public Debt, Sustainability and Growth in Post-HIPC Sub-Saharan Africa: The Role of DD” Paper for GD Net’s 2004/05 project on Macroeconomic

Policy Challenges of Low Income Countries. Abbas, S. M. 2007. Public Domestic Debt and Growth in LICs, Doctoral Thesis Draft,

University of Oxford, Oxford.Adesina, A. S. 2002. An Econometric Study of Debt Overhang, Debt Reduction, Investment andEconomic Growth in Nigeria, National Centre for Economic Management andAdministration (NCEMA), Ibadan, Monograph Series No. 8Aizenman, J., Pinto, B.,and Radziwill, A. 2004. “Sources for FinancingDomestic Capital, Is Foreign Saving a Viable Option for Developing Countries?”NBER Working Paper No. 10624.Ajayi, E. A. 1989. “Nigerian Debt Management Experience, Central Bank ofNigeria Review, vol.13, No. 2.Alison, J. 2003. “Key Issues for Analyzing Domestic Debt Sustainability”, DebtRelief International Publication, ISBN: 1-903971-07-1.Asogwa, R. C. 2005. Domestic Government Debt Structure, Risk Characteristics and

Monetary Policy Conduct, The McGraw-Hill Companies, Inc., United States ofAmerica.Blavy, R. 2006, “Public Debt and Productivity: The Difficult Quest for Growthin Jamaica”, IMF Working Paper No. 06/235. Central Bank of Nigeria, 1999. Statistical Bulletin, vol. 10 No. 1, pp.102-103Central Bank of Nigeria, 2010. Statistical Bulletin, vol. 21 No. 6, pp. 67-71Chowdhury, A. R. 2004. “External Debt, Growth and the HIPC Initiative: Is the

Country Choice TooNarrow?” in Addison, Hansen and Tarp (Eds), Debt Relief for Poor Countries.Christensen, J. 2004. “Domestic Debt Market in Sub-Sahara Africa.” IMF WorkingPaper WP/0646.Clements, B., Bhattacharya, R., and Nguyen, T. Q. 2003. “External Debt, PublicInvestment, and Growth in Low-Income Countries” IMF Working Paper No. 03/249.Cunningham, R. T. 1993. “The Effects of Debt Burden on Economic Growth inHeavily IndebtedNations”, Journal of Economic Development, pp. 115-126.Debt Management Office, 2007. Yearly Analysis of Change in FGN Domestic Debt Portfolio, 2005-

EndMarch 2007, Debt Management Office, Abuja.****Del, V. C. and Piero, U. 2003, “The Development of Domestic Markets for

Government Bonds”, TheFuture of Capital Markets in Developing Countries.Fosu, A. K. 1996. “The Impact of External Debt on Economic Growth in Sub-

Sahara Africa”, Journal of

Economic Development, vol. 12, No. 1.Gbosi, A. N. 1998. “The impact of Nigeria’s Domestic Debt on Macroeconomic

Environment”, First Bankof Nigeria Review.Guidotti, P. E. and Kamar, M. S. 1991. “Domestic Public Debt of Externally

Indebted Countries”, IMFoccasional publication Sci. J., vol. 5, 54-57.Hameed, A. H. A. and Chaudhary,M. A. 2008. “External Debt and its Impact on

the Economy”, International Monetary Fund, August. Retrieved from: http://ideas.repec.org/a/ecm/emetrp/v55y1987i on 03/7/2013.

Iyoha, M. A. 1999. Macroeconomics for Developing World, Miyo Educational Publishers,Benin City.James, F. 2006. “The Effects of Public Debt on the Growth of Nigerian Economy.Unpublished B.Sc. Research Project, Department of Economics, Kogi State University,Anyigba.Kumhof, M., and Tanner, E. 2005, “Government Debt: A Key Role in FinancialIntermediation” IMF Working Paper No. 05/57.Okunrounnmu, T. O. 1992. “A Review of Development in Domestic Debt in Nigeria(1989-1991), CBN Research Department Occasional Paper No.4.Oshadami, O. L. 2006. “The Impact of Domestic Debt on Nigeria’s Economic

Growth”, Unpublished B.Sc.Research Project, Department of Economics, Kogi State University, Anyigba.Pattillo, C. 2002. “External Debt and Growth, Finance and Development”, A

Quarterly Magazine of theIMF, Vol. 39, No 2.Pattillo, C., Poirson, H. & Ricci, R. 2004. “What Are the Channels Through

Which External Debt AffectsGrowth?”, IMF Working Paper, No. 04/15.Queientin, R. 1984. “Nigeria and Debt Problems: Causes and Solution. A Paper

Presented at aConference Organized by the United Bank for Africa Plc, Lagos.Sanusi, J. O. 1988. “Genesis of Nigeria’s Debt Problems: Problems and

Prospects for DebtConversion”, A Lecture Delivered on Debt Conversion/Asset Trading Organized by

Continental Bank ofNigeria.Sanusi, J. O. 2003. “Nigeria Indebtedness, Desired Goals and Poverty Level”, A

paper presented at the7th Monetary Policy Forum organized by the Central Bank of Nigeria at the CBN

Conference Hall, Abuja.Seetanah, B., Padachi, K. and Durbarry, R. 2007. “External Debt and Economic

Growth: A Vector Error Correction Approach, International Journal of Business Research, vol. 7, No. 5.Soludo, C. C. 2003. Debt, Poverty and Inequality: The Debt Trap in Nigeria, Africa World

Press, NJ, pp.23-74.

Stiglitz, J.E. 2000. Economics of the Public Sector, Third Edition,New York and London,W.W. Norton &

Company.Waheed, A. 2006. “Sustainability and Determinants of Domestic Public Debt of

Pakistan”, CSID Discussion Paper No. 137 Nagoya University, Japan.

APPENDIX I

Dickey-Fuller Unit Root Test Results

Gross Domestic Product: At LevelNull Hypothesis: GDP has a unit rootExogenous: ConstantLag Length: 2 (Automatic based on SIC, MAXLAG=2)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -0.277052 0.9108Test critical values: 1% level -3.857386

5% level -3.04039110% level -2.660551

*MacKinnon (1996) one-sided p-values.Warning: Probabilities and critical values calculated for 20 observationsand may not be accurate for a sample size of 18

Gross Domestic Product: At 1st DifferenceNull Hypothesis: D(GDP) has a unit rootExogenous: ConstantLag Length: 1 (Automatic based on SIC, MAXLAG=2)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -0.905150 0.7623Test critical values: 1% level -3.857386

5% level -3.04039110% level -2.660551

*MacKinnon (1996) one-sided p-values.Warning: Probabilities and critical values calculated for 20 observations and may not be accurate for a sample size of 18

Gross Domestic Product: At 2nd DifferenceNull Hypothesis: D(GDP,2) has a unit rootExogenous: ConstantLag Length: 0 (Automatic based on SIC, MAXLAG=2)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -10.53429 0.0000Test critical values: 1% level -3.857386

5% level -3.04039110% level -2.660551

*MacKinnon (1996) one-sided p-values.Warning: Probabilities and critical values calculated for 20 observations and may not be accurate for a sample size of 18

Domestic Debt Stock: At LevelNull Hypothesis: DDS has a unit rootExogenous: ConstantLag Length: 2 (Automatic based on SIC, MAXLAG=2)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic 1.408700 0.9981

Test critical values: 1% level -3.857386

5% level -3.04039110% level -2.660551

*MacKinnon (1996) one-sided p-values.Warning: Probabilities and critical values calculated for 20 observations and may not be accurate for a sample size of 18

Domestic Debt Stock: At 1st DifferenceNull Hypothesis: D(DDS) has a unit rootExogenous: ConstantLag Length: 1 (Automatic based on SIC, MAXLAG=2)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -5.590372 0.0003Test critical values: 1% level -3.857386

5% level -3.04039110% level -2.660551

*MacKinnon (1996) one-sided p-values.Warning: Probabilities and critical values calculated for 20 observations and may not be accurate for a sample size of 18

Domestic Debt Stock: At 2nd DifferenceNull Hypothesis: D(DDS,2) has a unit rootExogenous: ConstantLag Length: 2 (Automatic based on SIC, MAXLAG=2)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -3.547205 0.0204Test critical values: 1% level -3.920350

5% level -3.06558510% level -2.673459

*MacKinnon (1996) one-sided p-values.Warning: Probabilities and critical values calculated for 20 observations and may not be accurate for a sample size of 16

Expenditure on Domestic Debt Servicing: At LevelNull Hypothesis: EDS has a unit rootExogenous: ConstantLag Length: 0 (Automatic based on SIC, MAXLAG=2)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -1.002539 0.7316Test critical values: 1% level -3.808546

5% level -3.02068610% level -2.650413

*MacKinnon (1996) one-sided p-values.

Expenditure on Domestic Debt Servicing: At 1st Difference

Null Hypothesis: D(EDS) has a unit rootExogenous: ConstantLag Length: 0 (Automatic based on SIC, MAXLAG=2)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -5.657878 0.0002Test critical values: 1% level -3.831511

5% level -3.02997010% level -2.655194

*MacKinnon (1996) one-sided p-values.Warning: Probabilities and critical values calculated for 20 observations and may not be accurate for a sample size of 19

Expenditure on Domestic Debt Servicing: At 2nd Difference

Null Hypothesis: D(EDS,2) has a unit rootExogenous: ConstantLag Length: 1 (Automatic based on SIC, MAXLAG=2)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -5.184266 0.0008Test critical values: 1% level -3.886751

5% level -3.052169

10% level -2.666593

*MacKinnon (1996) one-sided p-values.Warning: Probabilities and critical values calculated for 20 observationsand may not be accurate for a sample size of 17

Domestic Credit to the Economy: At Level

Null Hypothesis: DCE has a unit rootExogenous: ConstantLag Length: 0 (Automatic based on SIC, MAXLAG=2)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic 1.899940 0.9995Test critical values: 1% level -3.808546

5% level -3.02068610% level -2.650413

*MacKinnon (1996) one-sided p-values.

Domestic Credit to the Economy: At 1st Difference

Null Hypothesis: D(DC) has a unit rootExogenous: ConstantLag Length: 0 (Automatic based on SIC, MAXLAG=2)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -2.757091 0.0833Test critical values: 1% level -3.831511

5% level -3.02997010% level -2.655194

*MacKinnon (1996) one-sided p-values.Warning: Probabilities and critical values calculated for 20 observations and may not be accurate for a sample size of 19

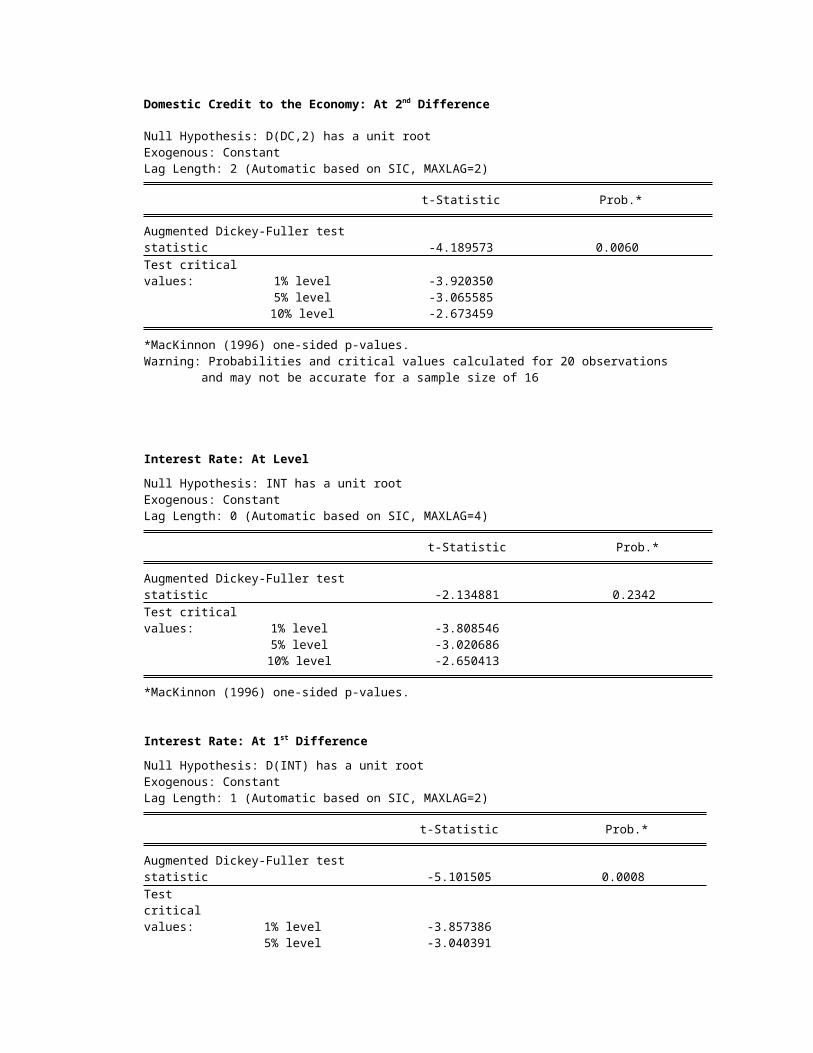

Domestic Credit to the Economy: At 2nd Difference

Null Hypothesis: D(DC,2) has a unit rootExogenous: ConstantLag Length: 2 (Automatic based on SIC, MAXLAG=2)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -4.189573 0.0060Test critical values: 1% level -3.920350

5% level -3.06558510% level -2.673459

*MacKinnon (1996) one-sided p-values.Warning: Probabilities and critical values calculated for 20 observations and may not be accurate for a sample size of 16

Interest Rate: At Level

Null Hypothesis: INT has a unit rootExogenous: ConstantLag Length: 0 (Automatic based on SIC, MAXLAG=4)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -2.134881 0.2342Test critical values: 1% level -3.808546

5% level -3.02068610% level -2.650413

*MacKinnon (1996) one-sided p-values.

Interest Rate: At 1st Difference

Null Hypothesis: D(INT) has a unit rootExogenous: ConstantLag Length: 1 (Automatic based on SIC, MAXLAG=2)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -5.101505 0.0008Test critical values: 1% level -3.857386

5% level -3.040391

10% level -2.660551

*MacKinnon (1996) one-sided p-values.Warning: Probabilities and critical values calculated for 20 observations and may not be accurate for a sample size of 18

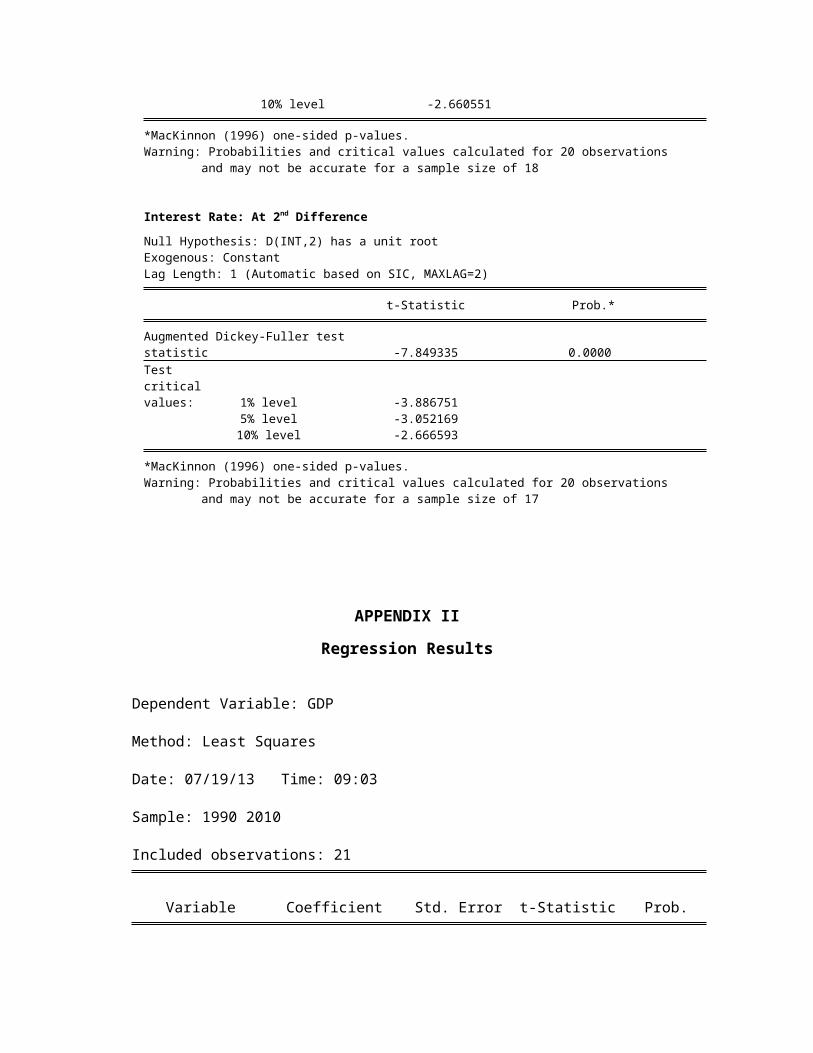

Interest Rate: At 2nd Difference

Null Hypothesis: D(INT,2) has a unit rootExogenous: ConstantLag Length: 1 (Automatic based on SIC, MAXLAG=2)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -7.849335 0.0000Test critical values: 1% level -3.886751

5% level -3.05216910% level -2.666593

*MacKinnon (1996) one-sided p-values.Warning: Probabilities and critical values calculated for 20 observations and may not be accurate for a sample size of 17

APPENDIX II

Regression Results

Dependent Variable: GDP

Method: Least Squares

Date: 07/19/13 Time: 09:03

Sample: 1990 2010

Included observations: 21

Variable Coefficient Std. Error t-Statistic Prob.

C 1573821. 2879016. 0.546652 0.5922

DDS 3.846669 0.726342 5.295949 0.0001

EDS 16.25341 4.803076 3.383958 0.0038

DCE 0.836482 0.355018 2.356164 0.0315

INT -154224.8 163337.6 -0.944209 0.3591

R-squared 0.960277 Mean dependent var 8773551.Adjusted R-squared 0.950346 S.D. dependent var 9372271.S.E. of regression 2088434. Akaike info criterion 32.14598Sum squared resid 6.98E+13 Schwarz criterion 32.39468

Log likelihood -332.5328 Hannan-Quinn criter. 32.19996

F-statistic 96.69739 Durbin-Watson stat 1.893243Prob(F-statistic) 0.000000

Source: EViews7 Regression Output

AUTHOR PROFILE

Andy T. Okwu (Ph.D., Babcock University) is a Lecturer in theDepartment of Economics, Banking and Finance, Babcock University,Ilishan-Remo, Ogun State, Nigeria. His areas of research interestinclude financial market, monetary economics, corruption,globalization, human capital, public expenditure and sustainablegrowth and development and business environment and small andmedium enterprises. He has published a book chapter and numerousarticles in academic journals, including British Journal of Economics,Finance and Management, Australian Journal of Business and Management Research,International Journal of Management Sciences and Business Research, European

Journal of Economics, Finance and Administration Sciences, European Scientific Journal,European Journal of Social Sciences, DLSU Business and Economics Review, PPCSSInternational Journal Series, ICAN Journal of Accounting & Finance, Babcock Journal ofManagement and Social Sciences, Babcock Journal of Economics, Banking and Finance,etc.

Timothy C. Obiwuru (Ph.D. in view, University of Lagos) is aLecturer in the Department of Actuarial Science, University ofLagos, Lagos State, Nigeria. His areas of research interestinclude financial market, government expenditure, inflation andexchange rates, social protection, risks, inflation and insuranceoperations, human capital, leadership and the environment ofbusiness. He has published two books in mathematics andstatistics and numerous articles in academic journals, includingInternational Journal on Tropical Focus, Journal of Risk and Insurance,Journal of Business Studies and Technology Development, African Journal of Humanitiesand Society, European Journal of Social Sciences, International Journal of ManagementSciences and Business Research, Australian Journal of Business and ManagementResearch, European Scientific Journal, International Bulletin of Business Administrationand ICAN Journal of Accounting and Finance, etc.

Johnbosco O. Ekezie (M.Sc. in view, Warwick University) holds aB.Sc. degree in Economics from Babcock University, Ogun State,Nigeria. He is about to complete his postgraduate studies inBusiness Analytics and Consulting at Warwick Business School,Warwick University, Coventry, United Kingdom. He has showntremendous interest in business research and consulting. Hisareas of interest include financial market and business dynamics,environment and consulting.

Related Documents