Effective Project Development For Renewable Energy Projects Tax Planning for Renewable Energy Projects November, 2008 Stephen J. Fyfe Partner, Borden Ladner Gervais LLP

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Effective ProjectDevelopment For Renewable Energy Projects

Tax Planning for Renewable Energy Projects

November, 2008

Stephen J. FyfePartner, Borden Ladner Gervais LLP

2

Overview

Principal tax benefits available to developers of renewable energy projectsUnderstanding Class 43.1 and 43.2 and the Specified Energy Property RulesLimitations on the use of tax benefitsMonetizing Tax BenefitsCross border inbound investment

3

Federal Tax Benefits

Federal Tax Incentives• Property included in Class 43.1 and/or 43.2

which are eligible for accelerated depreciation at a rate of 30%/50%

• Canadian Renewable and Conservation Expense (CRCE) which provides for a 100% write off of development type expenditures

4

Federal Tax Benefits

Class 43.1 describes renewable energy and energy conservation systems and property eligible for a 30% CCA deductionClass 43.2 incorporates the same definition but provides a 50% CCA deduction for property acquired after February 22, 2005 and before 2012Canadian renewable and conservation expenses or “CRCE” are development type expenses incurred in connection with a qualifying energy system—such expenses are specifically described in section 1219 ITR

5

Federal Tax Benefits

To qualify for accelerated depreciation, the property must be qualifying generation equipment and form part of an energy system described I n Class 43.1 to Schedule II of the ITRClass 43.1 Technical Guide describes the types of qualifying renewable and energy conservation systems; it includes schematics and technical discussions relating to qualifying systems, and analysis of outlays or expenditures which qualify for CRCE treatmentCRA takes the position that the Guide is conclusive with respect to engineering and scientific matters

6

Federal Tax Benefits

Class 43.1 and Class 43.2 of Schedule II to the Income Tax Regulations provides accelerated CCA (30/50% per year on a declining balance basis) for specified clean energy generation equipment The class incorporates by reference a detailed list of eligible equipment that generates energy in the form of electricity or heat, by:• using a renewable energy source (e.g. wind, solar,

small hydro);• using waste fuel (e.g. landfill gas, wood waste,

manure); or• making efficient use of fossil fuels (e.g. high efficiency

cogeneration systems, which produce electricity and heat simultaneously).

7

Federal Tax Benefits

The deductions are considered tax benefits because this Class 43.1/43.2 is an explicit exception to the general practice of setting CCA rates based on the useful life of assetThis incentive for investment is premised on the environmental benefits of low-emission or no-emission energy generation equipmentCCA Class 43.2 was introduced in 2005 and is currently available for assets acquired on or after February 23, 2005 and before 2020. Assets acquired before February 23, 2005 are included in Class 43.1 (30%)Eligibility criteria for these classes are generally the same except that cogeneration systems that use fossil fuels must meet a higher efficiency standard in the case of fossil fuel for Class 43.2 than for Class 43.1

8

Federal Tax Benefits

ELECTRICITY• High efficiency cogeneration equipment;• Wind turbines;• Small hydroelectric facilities up to 50 MW;• Fuel cells;• Photovoltaic equipment;• Wave and tidal power equipment;• Equipment that generates electricity using

geothermal energy;• Equipment that generates electricity using

certain waste sources.

Class 43.2 covers a variety of stationary clean energy generation equipment that is used to produce electricity or heat, or used to produce certain fuels from waste that are in turn used to produce electricity or heat. There is an ever expanding list of eligible systems, generally described below:

HEAT• Active solar equipment;• Wind turbines;• District heating equipment that

distributes heat from cogeneration;• Equipment that generates heat for

an industrial process using certain waste sources;

• Heat recovery equipment used in electricity generation and industrial processes.

9

Federal Tax Benefits

FUELS FROM WASTE• Equipment that recovers

landfill gas or digester gas;• Equipment used to convert

biomass into bio-oil;• Equipment used to produce

biogas through anaerobic digestion.

Class 43.2 covers a variety of stationary clean energy generation equipment that is used to produce electricity or heat, or used to produce certain fuels from waste that are in turn used to produce electricity or heat. There is an ever expanding list of eligible systems, generally described below:

10

Federal Tax

The property of a qualifying system must be acquired by the taxpayer for use for the purpose of earning income from a business or property in CanadaGenerally, only new generating type equipment and related property fit within Class 43.1 However, used equipment may be included in this class where:• It was previously described as either a Class 34 or

Class 43.1 asset in the hands of the transferor; and it has remained at the same project site until the acquisition by the purchaser

• It was acquired less than five years after it became available for use by the transferor

11

Federal Tax Benefits

Consideration has been given to the issue of whether the use of generating equipment for testing purposes may disqualify the equipment as “new”propertyNormally, property becomes eligible for CCA once it becomes capable of generating revenue for the owner; however, in the energy context, property often generates revenue during a testing phaseCRA has ruled that such “testing” revenue will not disqualify generation equipment from being considered new property

12

Federal Tax Benefits

ACTIVE SOLAR SYSTEMSExtraction and concentration of solar energy by collecting it in a gaseous or liquid medium and transporting that medium to either a point of use, or a storage facilityTo qualify for Class 43.1, the solar heat energy must also be used directly in connection with an industrial processGenerally, there are two kinds of active solar heating systems Conventional active solar heating uses separate solar energy collector systems to collect the solar energy directly from the sunGround source heat pumps use the ground primarily to heat a liquid or gas used in an industrial process or in a greenhouse

13

Federal Tax Benefits

ACTIVE SOLAR SYSTEMSActive solar system assets that may qualify for Class 43.1 include the following: • solar energy collectors;• solar energy conversion equipment;• solar water heaters;• energy storage equipment;• control equipment and components designed to interface

with other heating equipment; and• for qualifying ground source heat pump systems, the heat

pump (and ancillary systems) and the underground piping system and the equipment described above.

14

Federal Tax Benefits

ACTIVE SOLAR SYSTEMSIneligible assets would include: • a building or parts of buildings; and• equipment used to distribute heated air or water

in a building.

15

Federal Tax Benefits

SMALL-SCALE HYDROELECTRIC INSTALLATIONA qualifying small-scale hydroelectric installation has a planned average generating capacity not exceeding 50 megawatts (MW)Additions to qualifying systems that increase design capacity are also eligible for Class 43.1, so long as the resulting average annual capacity of the system does not exceed 50 MW or 15 MW (if acquired before December 11, 2001)

16

Federal Tax Benefits

SMALL-SCALE HYDROELECTRIC INSTALLATIONThe types of small-scale hydroelectric assets that may qualify as Class 43.1 additions include the following: • electrical generator equipment and plant including the

related canal, dam dike, overflow spillway, and penstock;• fishways and fish bypasses;• a powerhouse, complete with generator and related

ancillary equipment;• control equipment, including devices for power

synchronization and phase voltage adjustment; and• transmission lines (and related equipment up to the

interface with the electrical distribution system).

17

Federal Tax Benefits

SMALL-SCALE HYDROELECTRIC INSTALLATIONAssets of a small-scale hydroelectric system ineligible for Class 43.1 would include: • electrical distribution equipment;• assets normally included in Class 10; and• Class 17 such as roads, sidewalks, and bridges.

18

Federal Tax Benefits

HEAT RECOVERY SYSTEMSHeat-recovery systems that recover thermal waste for re-use are eligible for Class 43.1, other than thermal waste arising from the production of electricity

19

Federal Tax Benefits

HEAT RECOVERY SYSTEMSEligible heat recovery systems include the following assets: • heat exchangers and other heat extraction devices;• the portion of the heat transfer system (including piping,

ducting and other equipment) between the point of heat extraction, and the interface with the end-use system, the first shut-off valve, or the boundary of ownership, whichever occurs first;

• waste heat boilers (“heat recovery steam generators”); and

• ancillary equipment such as pumps and valves, fans, thermal energy storage equipment (e.g., storage tanks that otherwise would not be required), and monitoring and control instrumentation, including control panels.

20

Federal Tax Benefits

WIND ENERGY CONVERSION SYSTEMSWind energy conversion systems are fixed devices that are used primarily to convert wind energy to electricity. Qualifying wind energy conversion systems include the following assets: • wind-driven turbine;• electrical generating and related equipment, including

control and power conditioning and battery storage equipment;

• support structures;• the powerhouse, together with related ancillary

equipment; and• the transmission equipment.

21

Federal Tax Benefits

WIND ENERGY CONVERSION SYSTEMSWind energy assets not eligible for Class 43.1 include: • electrical distribution equipment and facilities;• other back-up generating equipment (e.g., diesel

engine, main switch, or power bar); and• vehicle, telephone equipment, certain temporary

access roads, sidewalks and other assets normally included in Class 10 or 17.

22

Federal Tax Benefits

A photovoltaic electrical generation system is a fixed location device that is used primarily to convert solar energy to electricity. It may qualify for Class 43.1 so long as the peak capacity of the system is not less than 3 kilowatts (kW).Eligible assets of a qualifying photovoltaic system include: • the solar cells, modules;• related equipment, including control and power conditioning

and battery storage equipment;• support structures for the solar array; and• transmission equipment.

PHOTOVOLTAIC ELECTRICAL GENERATION SYSTEM

23

Federal Tax Benefits

Ineligible assets would include: • electrical distribution equipment and facilities;• other back-up generating equipment; and• vehicles, telephone equipment, certain temporary

access roads, sidewalks and other assets normally included in Class 10 or 17.

PHOTOVOLTAIC ELECTRICAL GENERATION SYSTEM

24

Federal Tax Benefits

These systems consist of above-ground equipment primarily used to generate electrical energy from geothermal energy. Assets eligible for Class 43.1 include the following: • pumps, heat exchangers, steam separators, above-

ground pipelines, and ancillary equipment used to collect the geothermal energy;

• electrical generating equipment and related equipment, including control and power conditioning equipment, and equipment designed to store electrical energy; and

• property otherwise included in Class 10 and 17.

GEOTHERMAL ELECTRICAL GENERATION SYSTEMS

25

Federal Tax Benefits

Ineligible geothermal system assets include: • buildings and structures or portions thereof, with the

exception of working platforms that primarily serve the eligible equipment;

• below-ground wells and pipelines;• electrical transmission and distribution equipment;• equipment designed to store electrical energy (batteries);• other back-up generating equipment (such as a diesel

engine, main switch or power bar); and• vehicles, telephone equipment, access roads, sidewalks

and other assets normally included in Class 10 or 17.

GEOTHERMAL ELECTRICAL GENERATION SYSTEMS

26

Federal Tax Benefits

These systems are, in general, used to produce thermal energy for an industrial process, primarily from the combustion of wood waste, municipal waste, landfill gas, or digester gasAssets eligible for Class 43.1 include:• above ground equipment used to collect landfill

gas or digestion gas, to remove non-combustibles and contaminants

SPECIFIED-WASTE FUEL COLLECTION SYSTEMS

27

Federal Tax Benefits

Specified-waste fuel heat production system assets used for purpose of generating heat energy from the consumption of wood waste municipal waste, landfill gas, digestion gas, or bio-oil if heat is used directly in an industrial process or a greenhouse that are eligible for Class 43.1 include: • components of the heat generating system (including controls and

instrumentation), water treatment, and conditioning equipment, and air-handling systems;

• components of the fuel-handling system whose primary purpose is to increase the heat value of the combustible portion of the fuel by grinding, shredding, compacting or drying;

• working platforms, including catwalks, access ladders, and walkways, that are an integral part of the heat-production system (platforms that serve the surrounding structure are ineligible);

• tanks, heat exchangers and other ancillary equipment used to collect, remove contaminants or dilutants, or store the gas.

SPECIFIED-WASTE FUEL HEAT PRODUCTION SYSTEMS

28

Federal Tax Benefits

CRCE are development expenses incurred in respect of an energy project where at least 50% of the capital cost of the assets to be used in that property are described in Class 43.1 or 43.2CRCE is fully deductible when incurred and can be carried forward indefinitelyAlternatively, CRCE may be renounced to shareholders through the flow-through share agreement mechanism; discussed below

29

Federal Tax Benefits

CRCE is prescribed by section 1219 ITR, and includes both specific examples, and specific exclusions; the specific inclusions are: • pre-feasibility and feasibility studies for suitable sites and

potential markets;• costs necessary to determine the extent and location of the

energy resource, including access to the site, temporary roads, and their maintenance costs;

• negotiation and site approval costs dealing with various regulatory authorities for environmental compliance, building codes, local by-laws, etc.;

• site preparation costs that are not directly related to the installation of equipment;

• service connection costs incurred in order to transmit power from the project to the purchaser of the electricity; and

• the cost of acquiring and installing a test wind turbine.

30

Federal Tax Benefits

Regulation 1219 specifically excludes from the definition of CRCE:• Soft costs, such as project management and

administration fees, legal fees, insurance, interest and financing fees, amounts payable to non-residents

• Some of these non-qualifying expenses may be deducted under other provisions of the ITA

• Costs currently capitalized as Class 43.1 expenditures or any other CCA class, including all costs directly associated with their acquisition and installation other than Test Wind Turbine

31

Federal Tax Benefits

Interaction between general provisions of Tax Act and specific energy tax provisions create ambiguitiesConstruction period costs, and related soft costs, must be capitalized and add to cost of depreciable property; subsection 18(3.1)This construction rule applies for all purposes of the Tax ActHowever, CRCE often includes development type expenses associated with construction activity

32

Federal Tax Benefits

CRA takes position that “building” for purpose of the scope of 18(3.1) is the same as the definition used in the capital cost allowance provisionsTurbines, generators, steam condensers, cooling systems, feedwater pumps, wastewater collection systems, drain, pipelines, transformers, although often forming part of building are specifically described in Schedule IIEligible capital property is another example; expenditures of a capital nature made in respect of business ventures that are abandoned are generally treated as ECE

33

Federal Tax Benefits

However the CRA has provided more beneficial treatment for some CRCEIn connection with an abandoned wind project:“however, the fact that the development of a renewable energy project is subsequently abandoned due to...unforeseen factors…will not necessarily preclude such project development costs from being included in CRCE. In such circumstances, it will be necessary to establish that such developmental activities were in respect of a project…for which it was reasonable to expect that at least 50% of the capital cost of the depreciable property to be used in the project would be the capital cost of property described in Class 43.1”

34

Provincial Tax Benefits

Ontario• Class 43.2 now includes

biogas production equipment and additional applications of ground-source heat pump and waste-to-energy systems

• Government promoting investments in new renewable energy sources, conservation and demand management, and new or refurbished nuclear generating capacity, as well as investments in Ontario's transmission infrastructure (2008 Budget)

Quebec• Direct government support

for energy research and development

• Reimbursable tax credit to certain wind generated electricity producers (geographical conditions)

• Accelerated CCA rates for ground-source heat pump systems and systems for converting waste into energy

35

Provincial Tax Benefits

Alberta• Provincial Government

matches the federal CCA treatment on Class 43.1 assets (s.6.1 Alberta Corporate Tax Act)

British Columbia• Exemption from new

Carbon Tax (2008) for renewable energy such as biodiesel, ethanol and biomass

36

Limitations on the Use of Tax Benefits

Tax Act has a number of general limitations related to loss trading and use of tax benefits by persons unrelated to the business that generated losses or tax benefits;In the energy sector, there are three principal limitations• The Specified Energy Property Rules, which limit CCA

deductions to income from energy project• “at-risk rules” which limit losses from a limited partnership

interest to the cost basis of that partnership interest• “tax shelter rules” which can both deny deduction of losses,

and reduce cost amount of property by related “limited recourse financing”

Specified energy property rules are the most intrusive limitation in the renewable energy area. Where they apply, you generally don’t worry about at-risk rules or tax shelter rules

37

Limitations on the Use of Tax Benefits

The SEP rules restricts CCA deduction for cost of specified energy property to the amount of income generated by such property unless:• The owner of the property is a principal business

corporation, or a partnership of principal business corporations

• The property is to be used by the owner primarily for the purpose of gaining income from a business e.g. Farming, paper mill, steel manufacturing, carried on in Canada (other than the business of selling energy produced by the property)

• Property leased by the owner in the ordinary course of carrying on business in Canada, and the owner and lessee meet certain conditions related to the business, e.g. “A Qualified Leasing Company”

38

Limitations on the Use of Tax Benefits

SEP Rules have their own definition of principal business corporationThe principal business carried on “throughout the year” was one of:• Manufacturing or processing• Mining• The sale, distribution or production of

electricity, natural gas, oil, steam, heat or any other form of energy or potential energy

39

Limitation on Use of Tax Benefits

SEP Rules

Trust

Fund

GPGP

ProjectLP 1

ProjectLP 2

ProjectLP 3

InvestcoInvestco

Taxable Income Start UpTaxable Income

40

Limitations on use of Tax Benefits

At-Risks Rules• Applicable to all limited partners and “specified

members” of a partnership• Such persons can claim “limited partnership loss” which

is their “at-risk amount” less certain deductions• At-risk amount is adjusted cost base less:

• Current year losses• The amount of any benefits intended to reduce the

risk of the investments to revenue guarantees, reimbursements, arrangements, put options and other collateral guarantees intended to reduce true economic exposure

41

Limitations on use of Tax Benefits

Tax Shelter Rules• Consequences of tax shelter investment:

• Failure to obtain tax shelter identification number will result in penalties and denial of deduction

• Current deductions and cost of property acquired by partnership or other tax shelter identity are reduced by related “limited recourse financing”

42

What is a Tax Shelter• Statements representation that deductions or losses are

available to any investor• Those statements originate with promoter or its agents• Such losses or deductions exceed cost of property over

a four year periodWhere to look for Representations• Offering documents• Marketing materials• Copies of tax opinions issued to other investors• Private conversations• In your own mind?

Limitations on use of Tax Benefits

43

Monetizing Tax Benefits

Flow-through shares are the last officially sanctioned “tax shelter”Such shares are issued by a principal-business corporation—in this context, a corporation that has or expects to have more than half of its property included in Class 43.1 or [43.2] A principal business corporation can renounce its CRCE deduction in favour of its shareholders pursuant to a flow-through share agreement• Shareholders receive a tax deduction that may otherwise

be delayed or unused by the Corporation• Corporation positions itself to be more attractive to

investors resulting in more equity investment

44

Monetizing Tax Benefits

In order to qualify as a FTS, a share must meet the following requirements:• Issued pursuant to an agreement in writing• Issued by a principal business corporation• Corporation must incur expense equal to

consideration received for FTS• Expenses can be incurred in subsequent taxation

year and carried back – look-back ruleWhat happens when a PBC renounces CRCE it does not actually incur?

45

Monetizing Tax Benefits

The usual entry structure for third party investors, is to consolidate their capital in a limited partnership which subscribes for FTS of a general partner company which makes CRCE eligible expendituresNormally, only wind energy transactions work for this strategy, because capital cost of test wind turbines are included in CRCE; described belowCan be completed by prospectus offering or private placement to accredited investors

46

Monetizing Tax Benefits

Test Wind Turbines described in subsection 1219(3) ITR as follows:• Purpose of installation is testing• Cap on test turbines equal to 20% of project

capacity• No common connection to grid• 1500M from closest turbine

47

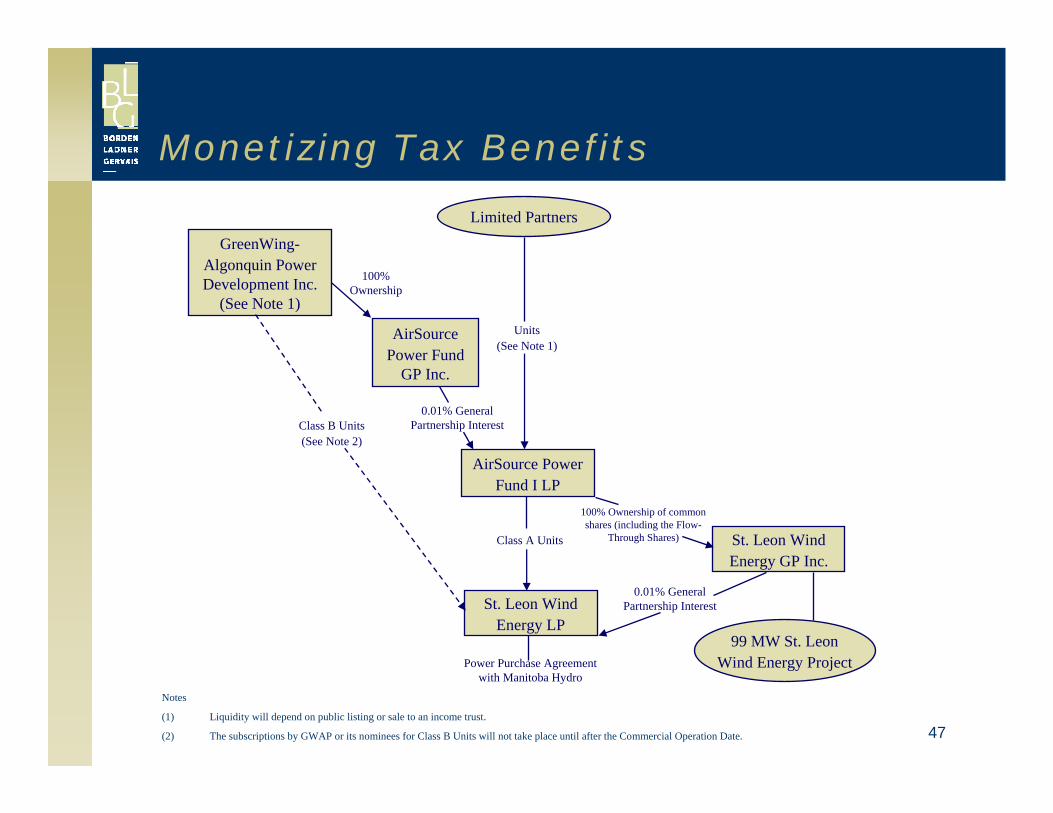

Monetizing Tax Benefits

Limited Partners

AirSource PowerFund I LP

St. Leon WindEnergy LP

St. Leon WindEnergy GP Inc.

GreenWing-Algonquin PowerDevelopment Inc.

(See Note 1)

AirSourcePower Fund

GP Inc.

99 MW St. LeonWind Energy ProjectPower Purchase Agreement

with Manitoba Hydro

Units(See Note 1)

Class B Units(See Note 2)

Class A Units

100% Ownership

0.01% General Partnership Interest

100% Ownership of common shares (including the Flow-

Through Shares)

0.01% General Partnership Interest

Notes

(1) Liquidity will depend on public listing or sale to an income trust.

(2) The subscriptions by GWAP or its nominees for Class B Units will not take place until after the Commercial Operation Date.

48

Monetizing Tax Benefits

What are the possible exit strategies for this investment?Contribute Class A units to a mutual fund corporation?Listing of the units of the limited partnership?Strategic purchaser? Power income funds?

49

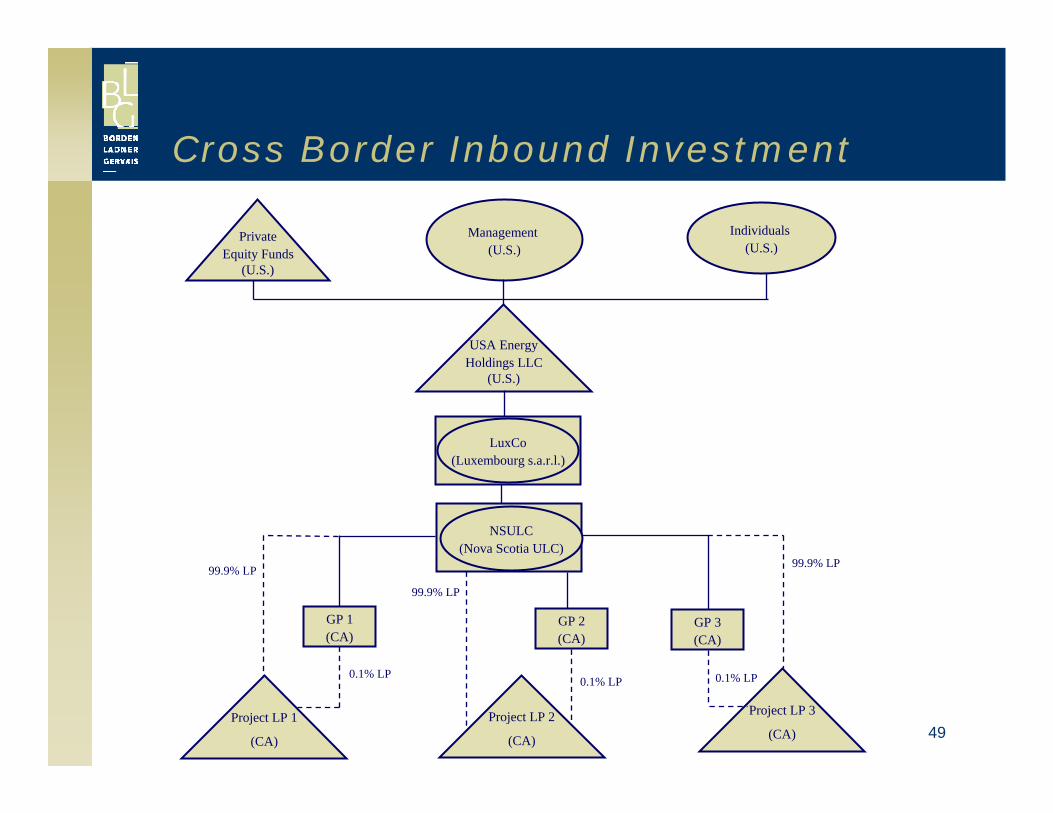

Cross Border Inbound Investment

PrivateEquity Funds

(U.S.)

Management (U.S.)

Individuals (U.S.)

USA EnergyHoldings LLC

(U.S.)

Project LP 1

(CA)

Project LP 2

(CA)

Project LP 3

(CA)

LuxCo(Luxembourg s.a.r.l.)

NSULC(Nova Scotia ULC)

GP 1(CA)

GP 2(CA)

GP 3(CA)

99.9% LP

99.9% LP

99.9% LP

0.1% LP0.1% LP0.1% LP

50

Cross Border Inbound Investment

Ordinary Income: effective tax rate of 35.87%$100 ordinary income in CanadaCanadian corporate tax will be imposed at NSULC level at a rate of 32.5%1

Remaining $67.50, when distributed to LuxCo 2, will be subject to withholding tax at treaty rate of 5%, and thus LuxCo will receive $64.13Each investor in USA Energy Holdings LLC will report its proportionate share of such $100 of ordinary income, subject to US federal income tax at a rate of 35%, irrespective of timing of actual distributionSum of Canadian corporate and withholding taxes already imposed ($35.88) should be fully creditable against, although it will exceed, the Investors’ corresponding US federal income tax liability of $35.00Therefore, for each $100 of ordinary income, the Investors will receive after-tax income of $64.13

1 This summary is based upon US federal tax rates and Canadian tax rates at January 1, 2008.2 This summary does not address any Luxembourg tax considerations, and assumes that both direct income taxes and withholdingtaxes imposed by Luxembourg will be de minimis. Further, this summary does not address potential arguments by the CanadaRevenue Agency of treaty shopping or abuse.

51

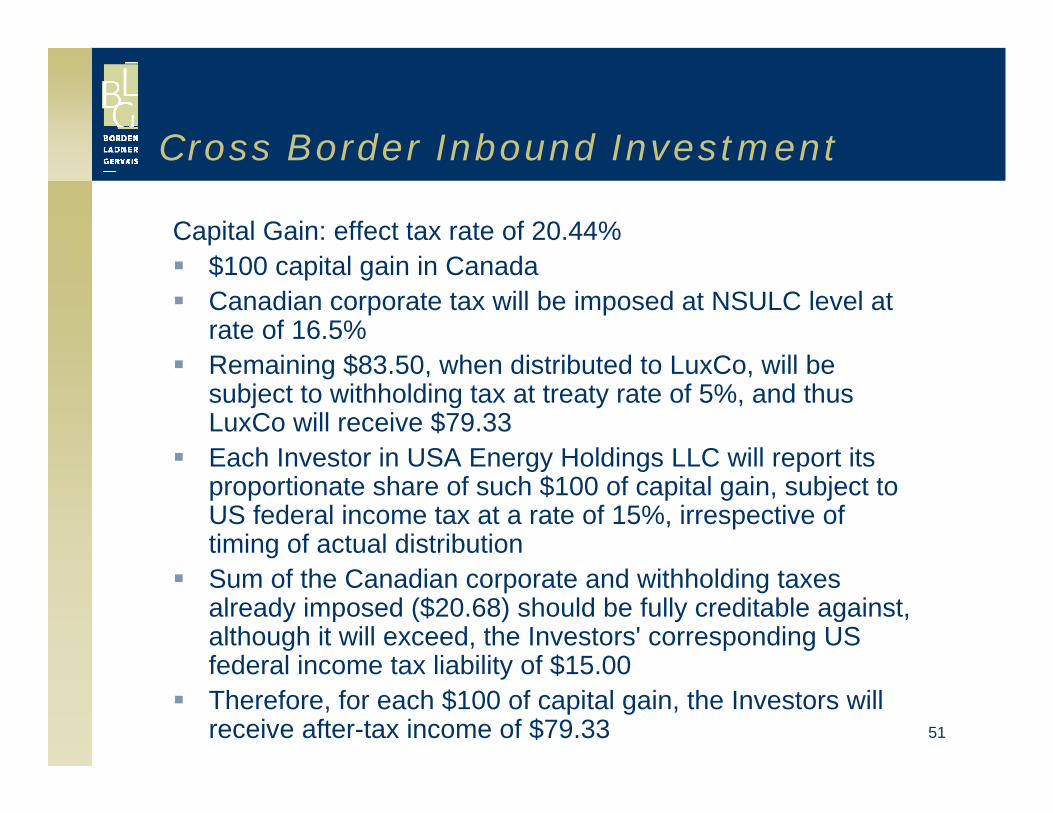

Capital Gain: effect tax rate of 20.44%$100 capital gain in CanadaCanadian corporate tax will be imposed at NSULC level at rate of 16.5%Remaining $83.50, when distributed to LuxCo, will be subject to withholding tax at treaty rate of 5%, and thus LuxCo will receive $79.33Each Investor in USA Energy Holdings LLC will report its proportionate share of such $100 of capital gain, subject to US federal income tax at a rate of 15%, irrespective of timing of actual distributionSum of the Canadian corporate and withholding taxes already imposed ($20.68) should be fully creditable against, although it will exceed, the Investors' corresponding US federal income tax liability of $15.00Therefore, for each $100 of capital gain, the Investors will receive after-tax income of $79.33

Cross Border Inbound Investment

52

Exemption from Canadian Tax$100 capital gain from the sale by LuxCo of interest in NSULCIf interests in NSULC meet certain conditions, capital gain is exempt from tax under treaty3

Investors should generally be subject only to US federal income tax on such gain. For an Investor wholly exempt from US federal income tax, the sale by LuxCo of interests in NSULC may eliminate the only taxes (i.e., Canadian corporate and withholding taxes) to which that Investor is subjectAs a result, structuring sales at the LuxCo level may reduce the effective tax rate of that Investor by 20.68%

3 Even if the interests in the NSULC are deemed to derive their value principally from real property situated in Canada, an exemptionFrom tax under the treaty is still available if the real property is found to be used in the business of the NSULC.

Cross Border Inbound Investment

53

USCo

Management (U.S.)

Individuals (U.S.)

PrivateEquity Funds

(U.S.)

USA EnergyHoldings LLC

(U.S.)

Project LP 1

(CA)

Project LP 2

(CA)

Project LP 3

(CA)

Canco

GP 1(CA)

GP 2(CA)

GP 3(CA)

99.9% LP

99.9% LP

99.9% LP

0.1% LP0.1% LP0.1% LP

Cross Border Inbound Investment

54

Ordinary Income: effective tax rate of 45.49%$100 ordinary income in CanadaCanadian corporate tax will be imposed at Canco level at rate of 33%Remaining $67.00, when distributed to USCo, will be subject to withholding tax at treaty rate of 5%, and thus USCo will receive $63.65USCo will report $100 of ordinary income, subject to US federal income tax at rate of 35%. Sum of Canadian corporate and withholding taxes already imposed ($36.35) should be fully creditable against, although it will exceed, USCo's US federal income tax liability of $35.00, and USCo will not be required to pay additional US federal income taxUpon USCo's distribution of remaining $63.65 to USA Energy Holdings LLC, each Investor in USA Energy Holdings LLC will be deemed to receive its proportionate share of $63.65 of qualified dividend income, subject to US federal income tax at a rate of 15%Therefore, for each $100 of ordinary income, the Investors will receive after-tax income of $54.10

Cross Border Inbound Investment

55

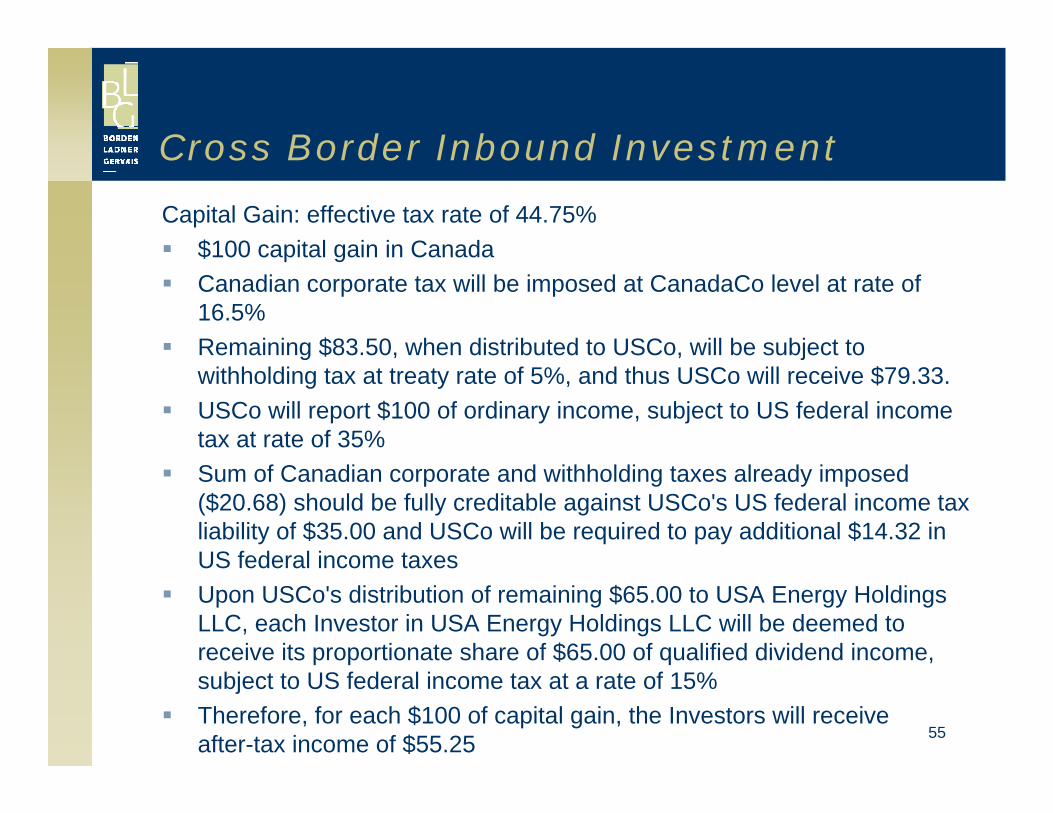

Capital Gain: effective tax rate of 44.75%$100 capital gain in CanadaCanadian corporate tax will be imposed at CanadaCo level at rate of 16.5%Remaining $83.50, when distributed to USCo, will be subject to withholding tax at treaty rate of 5%, and thus USCo will receive $79.33.USCo will report $100 of ordinary income, subject to US federal income tax at rate of 35%Sum of Canadian corporate and withholding taxes already imposed ($20.68) should be fully creditable against USCo's US federal income tax liability of $35.00 and USCo will be required to pay additional $14.32 in US federal income taxesUpon USCo's distribution of remaining $65.00 to USA Energy Holdings LLC, each Investor in USA Energy Holdings LLC will be deemed to receive its proportionate share of $65.00 of qualified dividend income, subject to US federal income tax at a rate of 15%Therefore, for each $100 of capital gain, the Investors will receive after-tax income of $55.25

Cross Border Inbound Investment

56

4 The treaty exemption applies to interests in the NSULC to the extent they do not derive their value principally from real property situated in Canada. If an exit strategy involves the sale by an NSULC of the underlying projects, that issue is no longer a consideration.

Cross Border Inbound Investment

Exemption from Canadian taxThere is no exemption analogous to the Canada-Luxembourg treaty with respect to this structure4

57

Existing Structure of US Investments:Currently Prevailing US Tax Rates

USCo

Management (U.S.)

Individuals (U.S.)

PrivateEquity Funds

(U.S.)

USA EnergyHoldings LLC

(U.S.)

Project LP

58

Existing Structure of US Investments:Currently Prevailing US Tax Rates

Ordinary Income: effective tax rate of 44.75%$100 ordinary income in USUSCo will report $100 of ordinary income, subject to US federal income tax rate of 35%Upon USCo’s distribution of remaining $65.00 to US Energy Holdings LLC, each Investor in US Energy Holdings LLC will be deemed to receive its proportionate share of $65.00 of qualified dividend income, subject to US federal income tax at a rate of 15%Therefore, for each $100 of ordinary income, the Investors will receive after-tax income of $55.25

59

Existing Structure of US Investments:Currently Prevailing US Tax Rates

Capital Gain: effective tax rate of 44.75%$100 capital gain in USUSCo will report $100 of capital gain, subject to US federal income tax at a rate of 35%Upon USCo’s distribution of remaining $65.00 to US Energy Holdings LLC, each Investor in US Energy Holdings LLC will be deemed to receive its proportionate share of $65.00 of qualified dividend income, subject to US federal income tax at a rate of 15%Therefore, for each $100 of capital gain, the Investors will receive after-tax income of $55.25

60

Contact Information

If you have specific areas of concern or require further details we would be pleased to elaborate on any of these

matters. Please Contact:

Stephen J. FyfePartner

Tel: (416) 367-6650Email: [email protected]

DM#3925813 v.4

Related Documents