EFFECT OF THE LOSS OF PLANT PROTECTION PRODUCTS RICHARD KING October 2014

EFFECT OF THE LOSS OF PLANT PROTECTION PRODUCTS RICHARD KING October 2014.

Dec 26, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

EFFECT OF THE LOSS OF PLANT PROTECTION

PRODUCTS

RICHARD KING

October 2014

POLICY ENVIRONMENT• EU Authorisation process (Reg. EC 1107/2009)

- risk to hazard-based criteria

- changing Guidance

• Water Framework Directive and related legislation- Drinking Water Directive

- Groundwater Directive

• Conditions of Approval for Neonicotinoids (485/2013)

• UK-specific implementation and guidelines- including ‘extension of authorisation for minor use’ (EAMU)

LOSSES OF ACTIVES

Details – pages 17-18

Likelihood of Loss/Restrictions:

Low

Medium

High

Around 250 UK approved active substances

10

Insecticides

Fungicides

12

Herbicides16

Molluscicides2

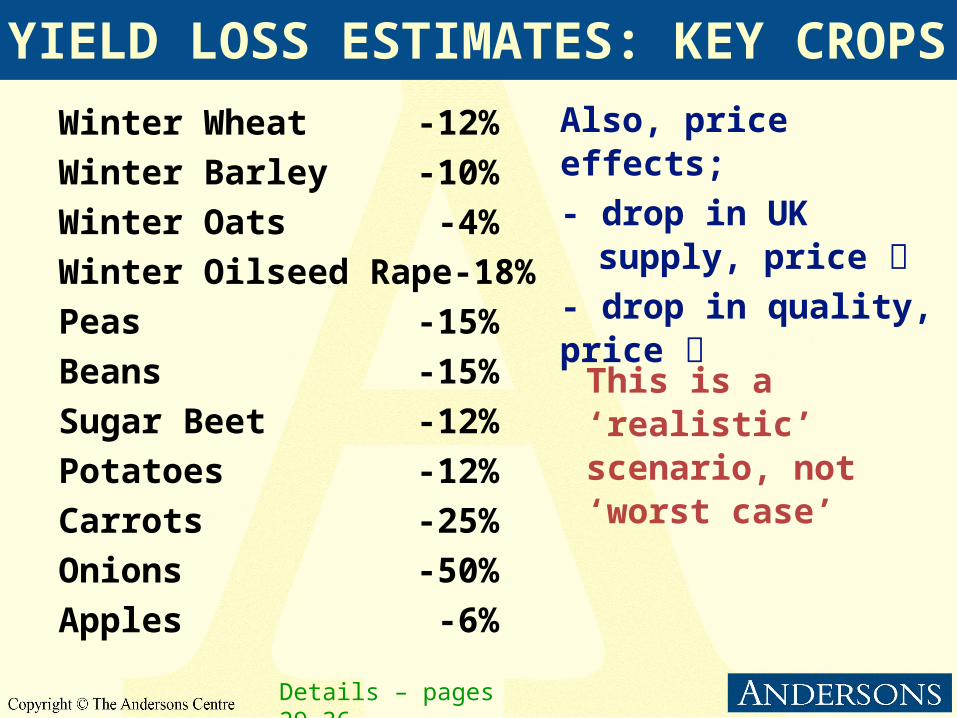

YIELD LOSS ESTIMATES: KEY CROPS

Winter Wheat -12%

Winter Barley -10%

Winter Oats -4%

Winter Oilseed Rape -18%

Peas -15%

Beans -15%

Sugar Beet -12%

Potatoes -12%

Carrots -25%

Onions -50%

Apples -6%

Details – pages 29-36

Also, price effects;

- drop in UK supply, price

- drop in quality, price

This is a ‘realistic’ scenario, not ‘worst case’

FINANCIAL EFFECTS - AGRICULTURE£m Base Post-Loss

Cereals 2,886 2,454

Other Combinables 914 641

Roots (Potato & Sugar Beet) 976 751

Vegetables 1,227 737

Fruit 586 392

Other Agricultural Output 16,146 16,251

Total Output 22,734 21,225

Intermediate Consumption 14,689 14,830

Gross Value Added (GVA) 8,045 6,395

Other Costs (less subsidy) 3,261 3,350

Total Income from Farming 4,784 3,045

-20%

-36%Details – page 46

CROPPING CHANGES• Area of main winter combinable crops drop

- increase in spring cropping (including maize and ‘alternatives’)

- fallow and temporary grass area rises

• Areas of roots and veg decline by 5 to 50%- 100% for vining peas

• Apples area down 30%

• Why?- certain pests in certain locations simply cannot be controlled

- lower (marketable) yields make production uneconomic in marginal situations

- competition from lower cost imports

Details – page 47

WIDER EFFECTS• Agri-food sector makes up 7% of the economy and 13% of

employment

• Food and drink manufacturers have GVA of £24.1bn- reduction in raw material availability (and/or higher costs) will

result in ‘off-shoring’ over medium term

- loss of GVA of up to £2.5bn and 35,000 to 40,000 jobs

• Agricultural supply industry also affected by lower output- GVA loss of £0.28bn and 3,500-4,000 jobs

• Higher food prices

• Ongoing effect on research and development- uncertain and costly regulatory environment – risk v reward

- focus moving to GM and emerging markets

Details – pages 49→

WIDER STILL• Moral dimension of constraining food production

- 842m people globally without enough to eat

- Europe has favourable soils and climate

• Alternatives to ‘traditional’ PPP have a role- Precision Farming, Integrated Pest Management, Bio-pesticides,

new technologies and even Organic

- but as part of a rounded approach including PPP

• Current direction of policy in the area of PPP is likely to lead to considerable economic and social loss with the gains at best uncertain or minimal.

CONTACT INFORMATION

Richard King

Partner – The Andersons Centre

Andersons Research Team

Melton Mowbray

01664 503208

Related Documents