Education Funding Alternatives (including what to do with over-funded UGMAs/UTMAs) Carl Waldman, Esq. and Rich Linsday The Advisors Forum April 22, 2009 1

Education Funding Alternatives (including what to do with over-funded UGMAs/UTMAs) Carl Waldman, Esq. and Rich Linsday The Advisors Forum April 22, 2009.

Dec 17, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Education Funding Alternatives(including what to do with over-funded

UGMAs/UTMAs)

Carl Waldman, Esq. and Rich Linsday

The Advisors ForumApril 22, 2009

1

Increasing Demand

• Rising college costs• Clients have need of advisors knowledgeable in

educational savings techniques• Advisors have need of planning team members

knowledgeable in these techniques

2

QUALIFIED TUITION PROGRAMS (529 PLANS)

3

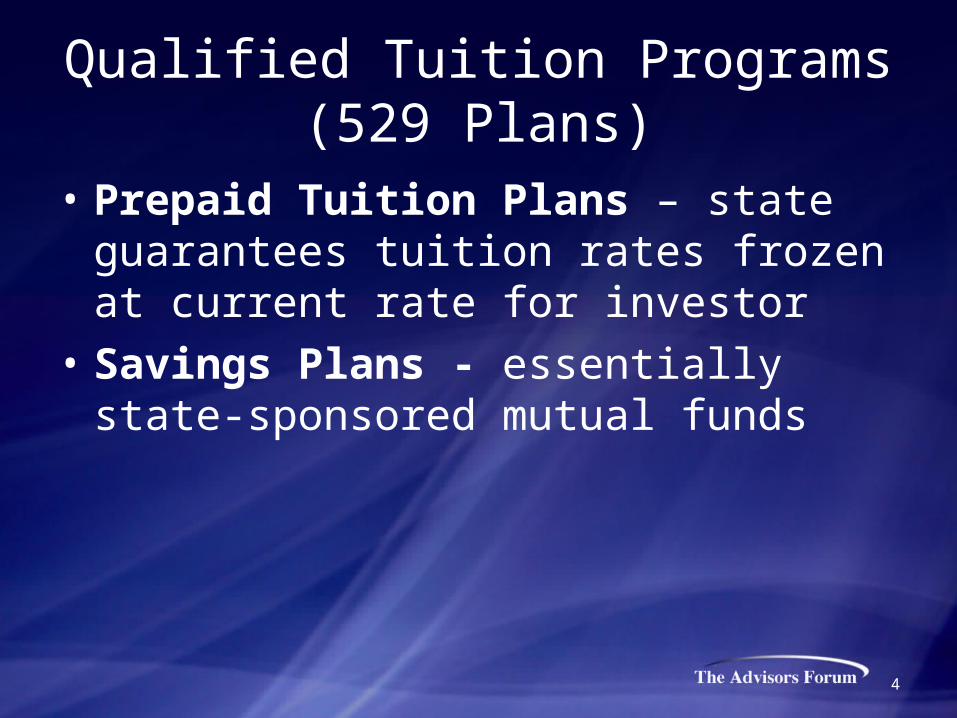

Qualified Tuition Programs (529 Plans)

• Prepaid Tuition Plans – state guarantees tuition rates frozen at current rate for investor

• Savings Plans - essentially state-sponsored mutual funds

4

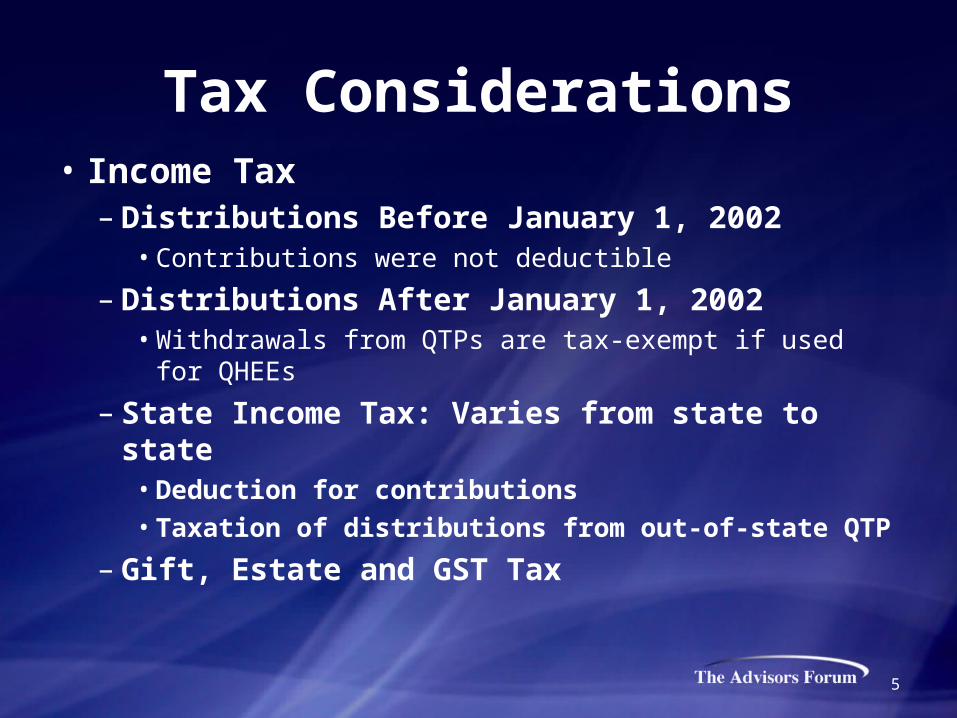

Tax Considerations• Income Tax– Distributions Before January 1, 2002

• Contributions were not deductible

– Distributions After January 1, 2002• Withdrawals from QTPs are tax-exempt if used for QHEEs

– State Income Tax: Varies from state to state• Deduction for contributions• Taxation of distributions from out-of-state QTP

– Gift, Estate and GST Tax

5

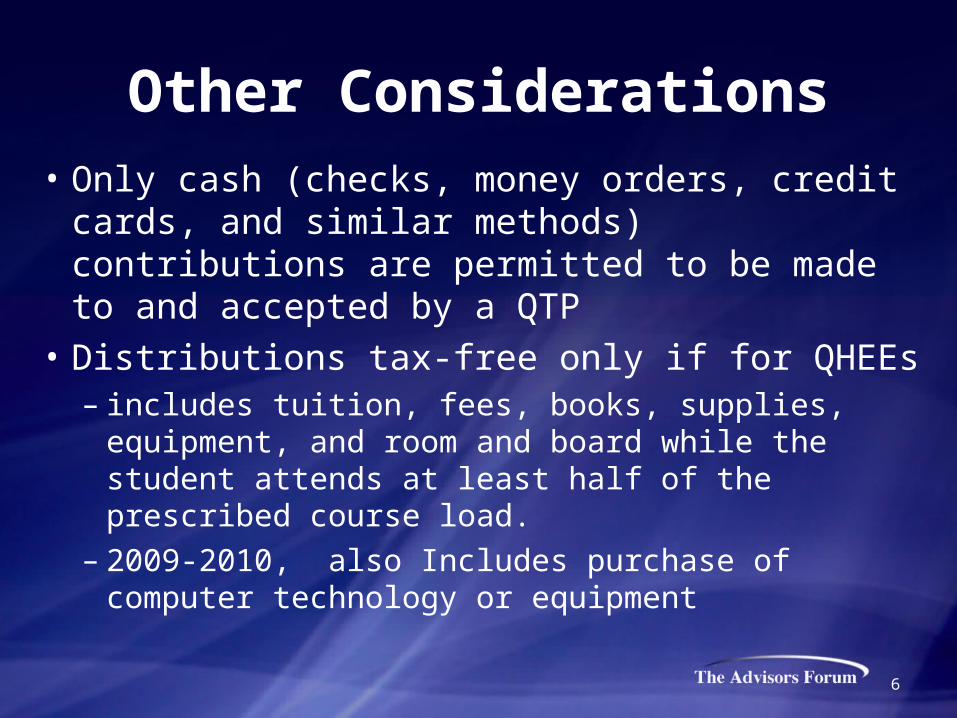

Other Considerations• Only cash (checks, money orders, credit cards,

and similar methods) contributions are permitted to be made to and accepted by a QTP

• Distributions tax-free only if for QHEEs– includes tuition, fees, books, supplies, equipment,

and room and board while the student attends at least half of the prescribed course load.

– 2009-2010, also Includes purchase of computer technology or equipment

6

Other Considerations• $1500 Reimbursement for student living at

home• Tax-free rollovers if within 60 days of distrib. (for

PSAs)• Costs – Issue where the state offers an identical plan with

lower cost structure?

7

COVERDELL EDUCATION SAVINGS ACCOUNTS (ESAS)

8

Tax Considerations

• Funds to be used for qualified education expenses

• Contributions constitute a completed gift• Funds are includible in the beneficiary’s estate

9

Other Considerations

• Cash-only contributions• Beneficiary’s parent or legal guardian controls

the account until the beneficiary attains the age of majority

• Change of beneficiary varies by plan

10

11

UTMA / UGMA ACCOUNTS

Tax Considerations

• Age of beneficiary• Income used to support or maintain the minor• Transfer to a minor under UGMA or UTMA• Death of custodian

12

Other Considerations

• Gifts to UGMA or UTMA• Beneficiary reaching age of majority• Types of assets

13

Over Funded UTMA/UGMA Accounts

• Donor/Custodian wishes to retain custodianship as long as possible: Options?

• Demand Right when the beneficiary reaches majority

• Conversion to a 529 Plan or Other Assets– FLP or FLLC interest?

14

15

2503(C) MINOR’S TRUSTS

Tax Considerations

• Gift tax annual exclusion• Contributions of up to $13,000 not subject to

gift tax

16

Other Considerations

• Continuing a minor’s trust after the beneficiary reaches majority

• Beneficiary must have a reasonable period of time after attaining 21 to withdraw all of the trust principal and undistributed income

• The trust should grant the minor a testamentary general power of appointment to avoid inclusion in parent trust maker’s estate, if beneficiary were to die

17

18

DEMAND TRUSTS

Tax Considerations

• Immediately notify custodian of transfers to the trust

• $13,000 per year (in 2009) allowed free of gift and GST tax

• Assets removed from trust maker’s estate• Beneficiary of a demand right trust is the trust’s

owner• For a grantor trust, the trust maker is the trust’s

owner19

Other Considerations

• Notices of gifts to trust• Control over beneficiary’s use of property

during lifetime and disposition upon death

20

21

U.S. SAVINGS BONDS (SERIES EE)

Tax Considerations

• Interest earnings exempt from state and local income taxes

• Bonds issued in 1990 or later are exempt from federal income tax

• Bonds held after the maturity date earn interest semiannually

• Owner must report income at maturity

22

Other Considerations

• Bonds may be redeemed after 6 months• Bonds are nontranferrable and payable only

to owner

23

24

LIFE INSURANCE

Tax Considerations• Withdrawals from a cash value life insurance

policy (other than a MEC) are not subject to income tax until the cumulative withdrawals exceed the cost basis

• Policy loans from cash value life insurance policies may be used to avoid current income tax on cash distributions in excess of cost basis

• If the policy continues until death, the income-tax-free death benefit will repay any policy loans

25

Other Considerations

• Premature death of policy holder• Universal life and variable universal life

policies are best suited for cash value distributions

26

27

DIRECT PAYMENTS TO AN EDUCATIONAL INSTITUTION

Considerations

• Contribute directly to educational institution• Not subject to gift, estate, or GST tax• Donor should make contributions to the

school while the child is presently enrolled• Make agreement with institution to pay future

tuition increases• Should be non-refundable

28

29

HEETS (Health & Education Exclusion Trusts)

Tax Considerations

• Relatively new concept• Trust designed to take advantage of gift and

GSTT exclusions for direct payments to education institutions and medical providers

• Properly drafted, trust will not be subject to GSTT tax – ever

30

Other Considerations

• Should be established in a state that permits dynasty trusts

• Requires a charitable beneficiary that has a significant interest that is not separate from the non-charitable beneficiaries’ interests– E.g., Give trustee discretionary distribution rights

of principal and income to the charity – With a minimum “floor” distribution

31

32

CREDITS AND DEDUCTIONS

Hope Scholarship/American Opportunity Credit

• Tax credit for up to four years of post-secondary education expenses

• Increase income level limits• Hope Scholarship Credit back in 2011

33

Lifetime Learning Credit

• Credit for 20% of up to $10,000 in combined tuition and mandatory fees

• Cannot claim Hope Credit and Lifetime Learning Credit in same tax year

34

Tuition and Fees

• Deduction for $4,000 of the college tuition and related expenses

• Cannot be claimed if Hope or Lifetime Learning Credits are claimed in same tax year

• Expires at end of 2009

35

Deduction for Student Loan Interest

• Deduction for up to $2500 of student loan interest for college expenses

36

Tax-free Scholarships

• Most scholarships and grants are tax-free if the recipient does not have to provide services in exchange for the award

37

Student Aid

• Free Application for Federal Student Aid (FAFSA) http://www.fafsa.ed.gov/

• College Parents of America (www.collegeparents.org)

38

39

THANK YOU

Related Documents