Economics 615 Managing Regulation Compliance: Notes David L. Kelly Department of Economics University of Miami Box 248126 Coral Gables, FL 33134 [email protected] Current Version: Spring 2020

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Economics 615Managing Regulation Compliance:

Notes

David L. Kelly

Department of EconomicsUniversity of Miami

Box 248126Coral Gables, FL 33134

Current Version: Spring 2020

INTRODUCTION

I Managing Regulation Compliance

A What is this course about?

This course will look at regulation from the point of view of economic incentives and

within the lens of the firm’s sustainability initiatives.

1 Legal Framework

Many people think of regulation in a legal framework: students learn the legal require-

ments, constitutional issues, and the legislative process.

• The firm must maintain a minimum wage of $15 per hour.

• Under the Corporate Average Fuel Economy (CAFE) standards, the average fuel econ-

omy for all light trucks with footprint (wheelbase times track width) less than 41 square

feet sold by a manufacturer in the year must be at least 38.15 miles per gallon.

• Is carbon covered under the Clean Air Act?

2 Economic Framework

While the law says what must be done, how it is done is up to the firm. The “how” is the

economic framework and is the subject of most of this class. How the firm complies with

regulation is a strategic decision, as each regulation creates a set of economic

incentives that the firm responds to.

Definition 1 Managing Regulation Compliance: how regulation changes incentives at

the firm and how the firm responds.

Definition 2 Economics is the study of the allocation of scarce resources.

Economics is the study of the allocation of scarce resources. In this class, we study how

the firm allocates scarce resources in order to comply with regulation. Examples:

• The minimum wage raises the cost of hiring low skill workers. Should the firm reduce

the size of the low skill workforce (perhaps through automation) and/or pay existing

workers higher wages? Should the firm reduce health care benefits and use that money

to increase wages?

1

• Fuel economy improves by lowering weight. However, consumers prefer heavier vehicles.

Should the firm raise prices of heavier vehicles to deter purchase of low MPG cars?

Should the firm change the size of the wheel base to make the standard easier to attain?

Should the firm innovate? Should the firm merge with another firm that has a better

average?

Thinking about regulation in this way has an additional benefit: students will learn

how to design regulation that minimizes bad incentives and unintended conse-

quences and what regulation levels maximize the welfare of society. In the above

example, making the wheel base larger to get a lower MPG standard is a bad incentive. Car

companies incur costs to change the wheel base, consumers pay some of the higher costs but

do not get a better car, and fuel economy does not improve.

3 Sustainability Perspective

Regulation often increases the incentives for firms to be sustainable.

Definition 3 Sustainability: Meeting the needs of the present without compromising fu-

ture generations ability to meet their needs.

Definition 4 Sustainable Business: Voluntary actions taken by firms which create so-

cial/environmental benefits while at the same time benefiting the firm.

Since sustainability is voluntary and regulation is mandatory, the two might appear to be

unrelated. However, regulation not just a mandate, but is also a set of incentives which

affects voluntary decisions by the firm. Examples:

• Minimum wage: a firm focused on sustainability might pay higher than the minimum

wage. This (1) gets the firm a higher quality worker, and (2) makes the firm more

attractive to consumers and socially responsible investors, who value a company that

treats workers well. Now suppose the minimum wage rises.

– Since other firms must raise their wage, the firm has an incentive to raise it’s wage

as well, to maintain a reputation that it is doing more than the minimum.

– The cost of becoming sustainable rises, given the higher wage.

– Suppose the firm sustainability program focused on providing health insurance

to all workers. The higher minimum wage creates an incentive to reduce health

insurance contributions, to keep total compensation down.

2

• CAFE Standards:

– A company which exceeds the minimum fuel economy standard earns credits

which it can sell to firms that fail to exceed the minimum. This is a benefit to

being sustainable.

– Car sales are unpredictable. If gas prices are low, for example, the firm might

accidentally sell too many gas guzzlers and have to pay a penalty. Exceeding the

minimum reduces the likelihood of such an accident.

II How to Make Regulation Decisions

Now that we understand that regulation compliance is a decision, not just a legal require-

ment. How should the firm make regulation compliance decisions? The firm must

add up all of the costs and benefits of compliance and over-compliance. Thinking carefully

about these costs and benefits will also help us understand the costs and benefits of firm

sustainability strategies.

A Standard Economic Cost Trade-off

A general principle from economics is that the the additional cost of compliance in-

creases with the level of compliance. There is often “low hanging fruit” such that the

firm can achieve a low level of compliance fairly cheaply. Higher levels of compliance require

more expensive options.

• Minimum Wage:

– A few low skill workers could be replaced via automation or self service at rela-

tively low cost. For example, moving from full service to self service gas stations

reduces labor costs, but incurs a cost in that cars move though lines more slowly.

Workers in more complex jobs are more expensive to replace, requiring more so-

phisticated automation (e.g. artificial intelligence).

– In an accounting sense, the cost raising the wage of low skill workers by $1 is

$1. However, this dollar has to be obtained from some other alternative use in

the firm. At first, it is easy to find small amount of money which are not being

used efficiently at the firm. But as the wage rises, the firm must obtain more

dollars from valuable alternative uses, for example, investing in a new product or

3

market or investing in energy saving equipment. The costs in terms of forgone

investments increase with the wage level.

• CAFE Standards: The cost of achieving an average level of fuel economy increases

with the level of fuel economy.

– Small improvements in fuel economy can be obtained by, for example, using

smaller tires.

– Higher levels of fuel economy require more expensive additions, such as turbo

chargers and hybrid engines with regenerative brakes.

Definition 5 Accounting Cost Costs that appear on an accounting statement.

Definition 6 Opportunity Cost Accounting costs plus the value of using inputs in their

next best alternative.

Opportunity costs are higher than accounting costs. In the minimum wage example,

the accounting cost of increasing the wage by $1 is $1, since this is the cost that will appear

on the accounting statement. Suppose, however, that the $1 could be invested in insulation

which improves energy efficiency, ultimately reducing costs by $1.50. The opportunity cost

is $1.50: $1 of wage costs plus $0.50 of lost profits because the energy efficiency investment

was not made. If not otherwise specified, all costs in this class are opportunity

costs.

B Marginal Costs

Clearly opportunity costs matter for the regulation compliance decision. In addition, the

compliance decision uses marginal costs: the cost of one additional unit of compli-

ance (e.g. a higher wage or lower carbon emissions).

The idea behind marginal costs is to consider each unit of regulation compliance sepa-

rately. Should the firm increase its average miles per gallon from 26 to 27 MPG? Suppose to

get from 10-14 MPG required only smaller tires at minimal expense. This is not a relevant

cost because we are using smaller tires regardless of whether or not the firm achieves 26 or

27 MPG. What matters is only the additional cost of getting from 26 to 27 mpg. We will

see that marginal costs are in fact easy to calculate in practice.

4

C Sustainability Costs and Benefits

The point of sustainable business is to look beyond the simple cost of compliance de-

scribed above. In this course we will consider several additional benefits that regulation

over-compliance provides.

1. Achieving a higher compliance level results in direct marginal costs associated with

forgone opportunities, diverted labor, investment in new equipment, etc.

2. Achieving a higher compliance level creates marginal benefits by making

the firm more attractive to sustainability minded consumers.

• Greater product demand.

• Product differentiation.

• Market entry. Incumbent firms often find it difficult to compete with new entrants

that are focused on sustainability. Large incumbents must change hundreds of

products as consumers require the whole company to be sustainable, not just one

product. New entrants typically enter with a much smaller number of products

and can design supply chains and machines with sustainability in mind.

3. Achieving a higher compliance level generates marginal benefits in terms of

lowering the firm’s cost of capital by making the company more attractive

to socially responsible investors. The firm can use investment vehicles such as

green bonds, green private equity, and socially responsible mutual funds.

4. Achieving a higher compliance standard incurs marginal benefits in terms

of regulation incentives.

• Tradeable Permit Regulation. By over-complying, the firm saves the cost of pur-

chasing a permit required to pollute or emit carbon.

• Taxes. Carbon taxes and gasoline taxes have no fixed standard. Instead, the firm

earns tax savings for each unit of carbon emissions or gasoline reduced.

5. Achieving a higher compliance standard generates marginal benefits in

terms of lower risk.

• Over-complying reduces the risk of accidents, which hurts the firm’s reputation.

5

• Over-complying reduces the risk of accidental under-compliance. For example,

if the firm tries to achieve a MPG standard of 28 MPG, it reduces the risk of

missing the compliance standard of 26 MPG, which might occur if gas prices are

low and the firm sells too many SUVs.

6. Achieving a higher compliance standard incurs marginal benefits of inno-

vation and long term focus. Higher compliance levels eventually requires more

innovation.

• Innovations build off each other and sometimes spill over into areas other than

regulation compliance. One might invent a turbo-charger to save energy, but find

it conveys additional benefits in terms of faster acceleration.

• Sustainability minded firms keep a long term focus, anticipating trends that lead

to additional opportunities.

To compute the optimal compliance level, we will have to numerically consider

all of these benefits and costs.

III Welfare

The purpose of regulation is to improve the welfare of society. It is unlikely that all reg-

ulations result in the same welfare improvements. Which generates more carbon emissions

reductions per dollar of compliance costs, renewable fuel standards or CAFE standards?

A Importance Well-Designed Regulation

Even if one cares only about social goals and the environment and not compliance costs,

it still makes sense to support regulations which increase welfare at low compliance costs.

Unnecessarily costly regulation:

1. Generates political resistance, resulting in regulations which are not passed, or are

passed with loopholes, or which are held up in court due to lawsuits.

2. Results in more cheating and non-compliance. Regulated entities which are

saddled with unnecessary compliance costs have a strong incentive to cheat. Often the

alternative is going out of business.

6

3. Results in more decisions made solely to (legally) evade regulations. Firms

have a number of options for complying with regulations that achieve the standard

without actually achieving the regulation goals. With the CAFE standards, we saw

that auto manufacturers could comply with the regulation by changing the wheelbase,

rather than actually improving fuel economy. The costlier the regulation, the more

likely firms are to do actions like this which evade the spirit of the regulation.

B Market Failures

Many people ask why regulation is justified at all. Perhaps the market economy can maximize

welfare without regulation. Indeed the market seems very good at producing some goods.

No one talks about a shortage of Iphones. Yet, there are few if any subsidies for Iphone

production or minimum Iphone standards.

It turns out that two incredibly important theorems known as the welfare theorems (think

of E = mc2 but far more useful), discovered in the 1960s by Nobel Prize winners Kenneth

Arrow and Gerard Debreu establish precise conditions under which the decentralized market

maximizes welfare. We will study these theorems, mainly from the contraposi-

tive: when these conditions are violated (a market failure), as they often are,

regulation can improve welfare.

We will also see cases of government failure: the government sometimes fails to

impose regulation that maximizes welfare, even when a market failure exists.

Is there are solution when both markets and governments fail to maximize welfare? We

will learn that in fact consumers and investors, by creating incentives for firms, can improve

welfare in these situations. From this, we can see sustainable business through a new lens. If

markets or government worked, there would be no need for socially responsible

investing or sustainable consumers. But the recent paralysis of government, in

fact explains much of the new focus on sustainability. It is an alternative way to

improve welfare when governments fail to act.

C Welfare Criteria

When markets fail, government regulation can improve welfare. How can we determine which

types of regulation we should use? We will have 2 criteria:

1. Efficiency: the regulation should achieve social/environmental goals at the least pos-

sible cost. A corollary to efficiency is designing regulation that does not create perverse

7

incentives. When regulation creates an incentive to evade the regulation, no one wins.

Firms pay a cost to evade regulation, and society fails to get the benefits that the

regulation was designed to achieve.

2. Equity: the compliance costs should not be distributed in a way such that low income

households pay most of the cost.

D Balancing Stakeholders and the Business Roundtable Statement

Sometimes people present reductio ad absurdum arguments against sustainable business to

me. If the purpose of the firm is to improve the environment, why does the firm produce

any goods at all? If the purpose of the firm is to maintain a sustainable workforce, why not

reduce profits to zero and pay all business income as wages?

The recent Business Roundtable statement illustrates the confusion. The Business Roundtable

statement says the purpose of the firm is to serve five stakeholders: customers, employees,

suppliers, communities, and shareholders. Notice that shareholders are conspicuously listed

last. The statement was criticized on one hand for being toothless and on the other hand

for not clearly stating which stakeholders have a priority (a recipe for lawsuits). How can

the firm satisfy five stakeholders? What weight should we attach to each stakeholder, when

their interests conflict (wages versus stockholder income)?

Although the statement is confusing, sustainable business principles, provide much

clearer guidance.

• Socially responsible investors push companies to have a sustainable workforce. But so-

cially responsible investors also value profits and dividends. They will push companies

to maintain a balance.

• Consumers want products produced by responsible companies, but also value products

that are reasonably priced. They will pay more for a responsible product, but not

tremendously more. In turn, this guides the firm to strike a balance between the

interests of consumers and other stakeholders, such as communities.

IV Stylized Facts

Here we can look at a few stylized facts, both with respect to regulation and the ultimate

goals of society that regulation addresses.

8

A Environment

The US has made many tremendous strides in terms of improving environmental quality

since the 1970s. Much of these achievements resulted from regulations such as the Clean Air

Act. This is not to say the game is over. A surprising conclusion from the recent literature

is that even modest levels of pollution can cause serious adverse health effects. Further,

regulation has been less successful in certain geographic regions and certain pollutants.

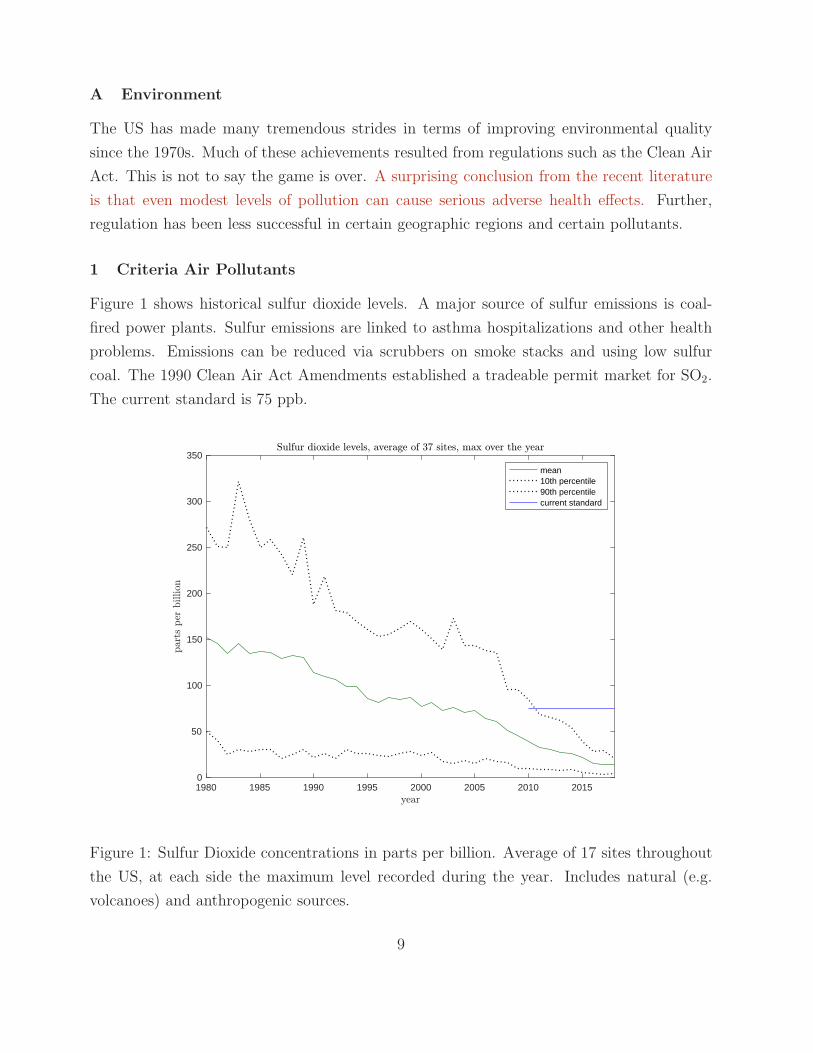

1 Criteria Air Pollutants

Figure 1 shows historical sulfur dioxide levels. A major source of sulfur emissions is coal-

fired power plants. Sulfur emissions are linked to asthma hospitalizations and other health

problems. Emissions can be reduced via scrubbers on smoke stacks and using low sulfur

coal. The 1990 Clean Air Act Amendments established a tradeable permit market for SO2.

The current standard is 75 ppb.

1980 1985 1990 1995 2000 2005 2010 20150

50

100

150

200

250

300

350

mean10th percentile90th percentilecurrent standard

Figure 1: Sulfur Dioxide concentrations in parts per billion. Average of 17 sites throughout

the US, at each side the maximum level recorded during the year. Includes natural (e.g.

volcanoes) and anthropogenic sources.

9

Figure 1 indicates that SO2 levels have fallen considerably. Only nine counties are cur-

rently “out of attainment” (exceed the minimum).

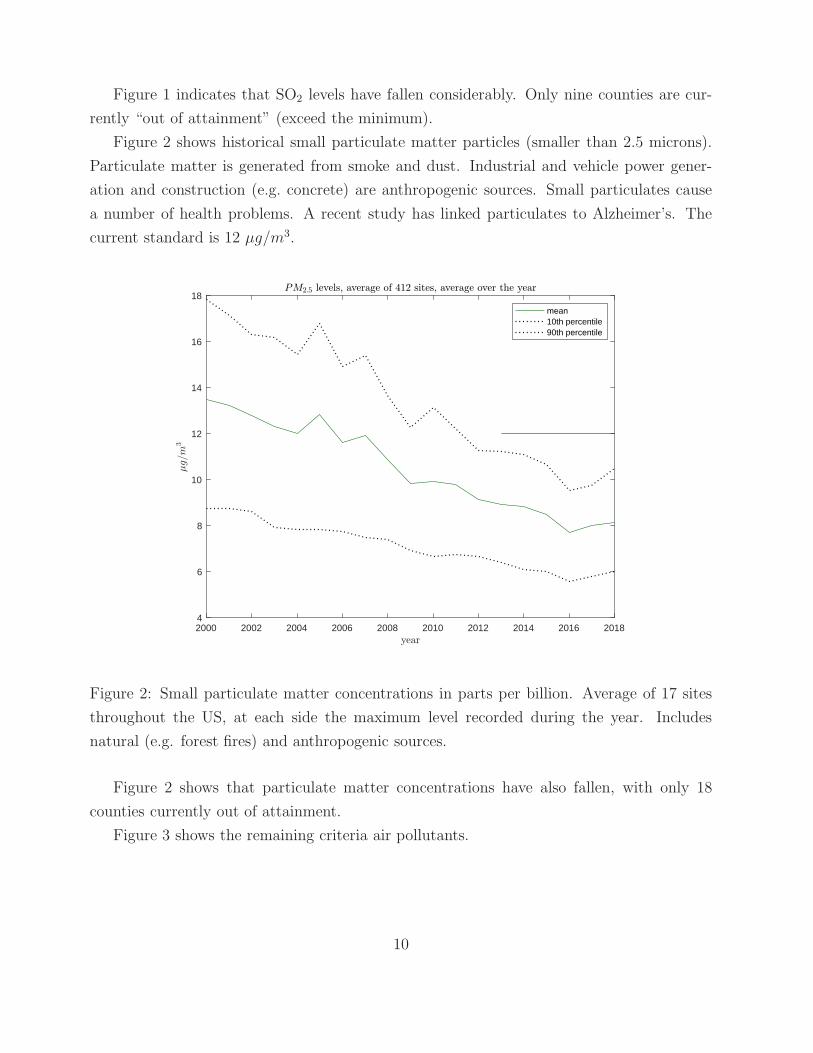

Figure 2 shows historical small particulate matter particles (smaller than 2.5 microns).

Particulate matter is generated from smoke and dust. Industrial and vehicle power gener-

ation and construction (e.g. concrete) are anthropogenic sources. Small particulates cause

a number of health problems. A recent study has linked particulates to Alzheimer’s. The

current standard is 12 µg/m3.

2000 2002 2004 2006 2008 2010 2012 2014 2016 20184

6

8

10

12

14

16

18

mean10th percentile90th percentile

Figure 2: Small particulate matter concentrations in parts per billion. Average of 17 sites

throughout the US, at each side the maximum level recorded during the year. Includes

natural (e.g. forest fires) and anthropogenic sources.

Figure 2 shows that particulate matter concentrations have also fallen, with only 18

counties currently out of attainment.

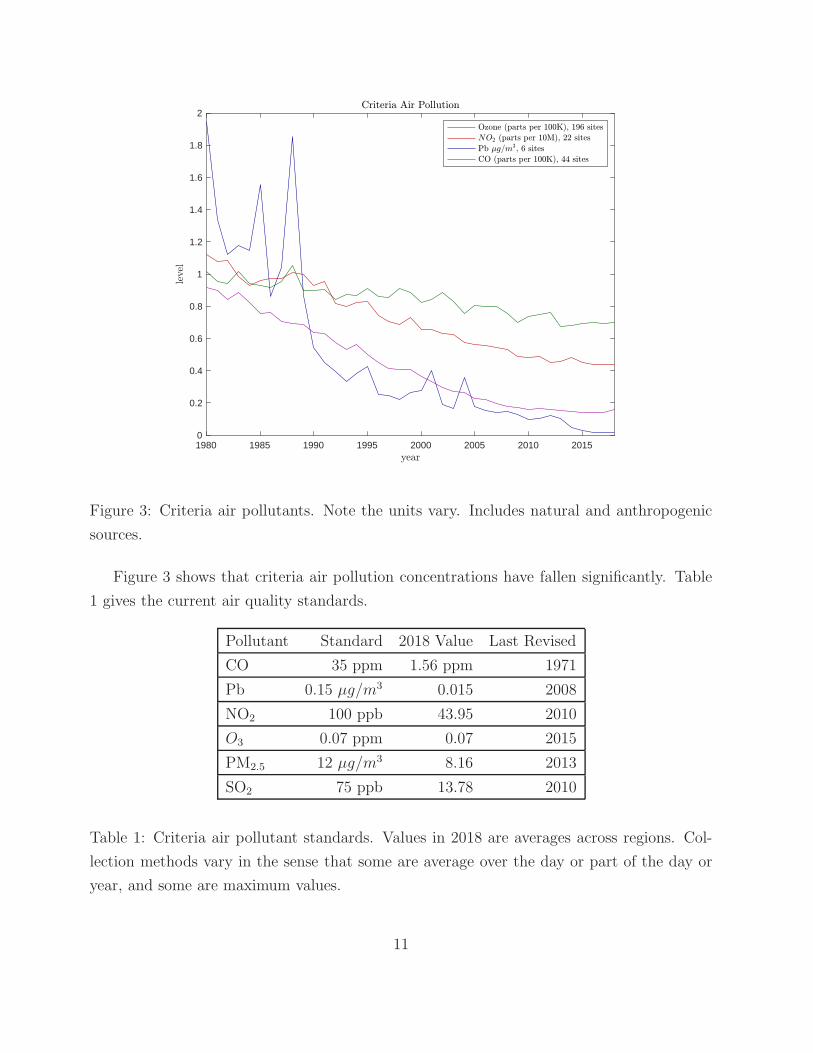

Figure 3 shows the remaining criteria air pollutants.

10

1980 1985 1990 1995 2000 2005 2010 20150

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

Figure 3: Criteria air pollutants. Note the units vary. Includes natural and anthropogenic

sources.

Figure 3 shows that criteria air pollution concentrations have fallen significantly. Table

1 gives the current air quality standards.

Pollutant Standard 2018 Value Last Revised

CO 35 ppm 1.56 ppm 1971

Pb 0.15 µg/m3 0.015 2008

NO2 100 ppb 43.95 2010

O3 0.07 ppm 0.07 2015

PM2.5 12 µg/m3 8.16 2013

SO2 75 ppb 13.78 2010

Table 1: Criteria air pollutant standards. Values in 2018 are averages across regions. Col-

lection methods vary in the sense that some are average over the day or part of the day or

year, and some are maximum values.

11

Table 1 shows that the average region is well below the standard for all pollutants except

ozone. However, a few counties exceed the minimum.

1. Achieving the national standard is apparently more difficult in some regions versus

others. Does it make sense to have a uniform national standard?

2. Other forces must be at work besides national regulation. What are the incentives to

reduce air pollution that are not regulation based?

The answers will be important from the point of view of a firm considering how much to

emit.

2 Greenhouse Gases

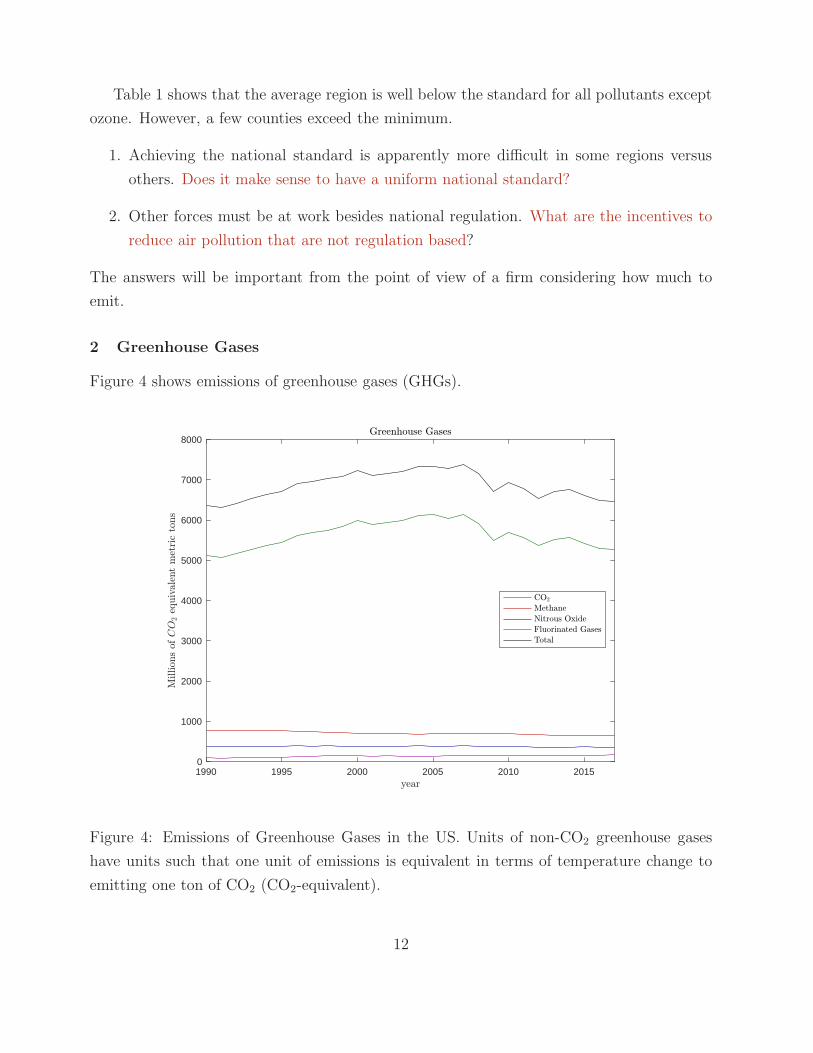

Figure 4 shows emissions of greenhouse gases (GHGs).

1990 1995 2000 2005 2010 20150

1000

2000

3000

4000

5000

6000

7000

8000

Figure 4: Emissions of Greenhouse Gases in the US. Units of non-CO2 greenhouse gases

have units such that one unit of emissions is equivalent in terms of temperature change to

emitting one ton of CO2 (CO2-equivalent).

12

Emissions of GHGs correlate with economic production. The peak in GHG emissions

in 2007 is due to the recession which began in 2008. Nonetheless, the economy has fully

recovered from the recession and total emissions are still falling (slowly!). GHG emissions

in 2017 are roughly the same as emissions in 1992-1993. Carbon Dioxide accounts for the

biggest part of the drop, but most other greenhouse gases have been falling as well.

We do not have a single Federal GHG regulation, such as the European Cap and Trade

System (ETS). But that should not be confused with saying no regulations exist on GHGs.

A host of Federal and State regulations exist, from taxes on gasoline, CAFE standards, state

renewable fuel standards, light bulb standards, and thousands of other regulations exist

which in part reduce GHGs.

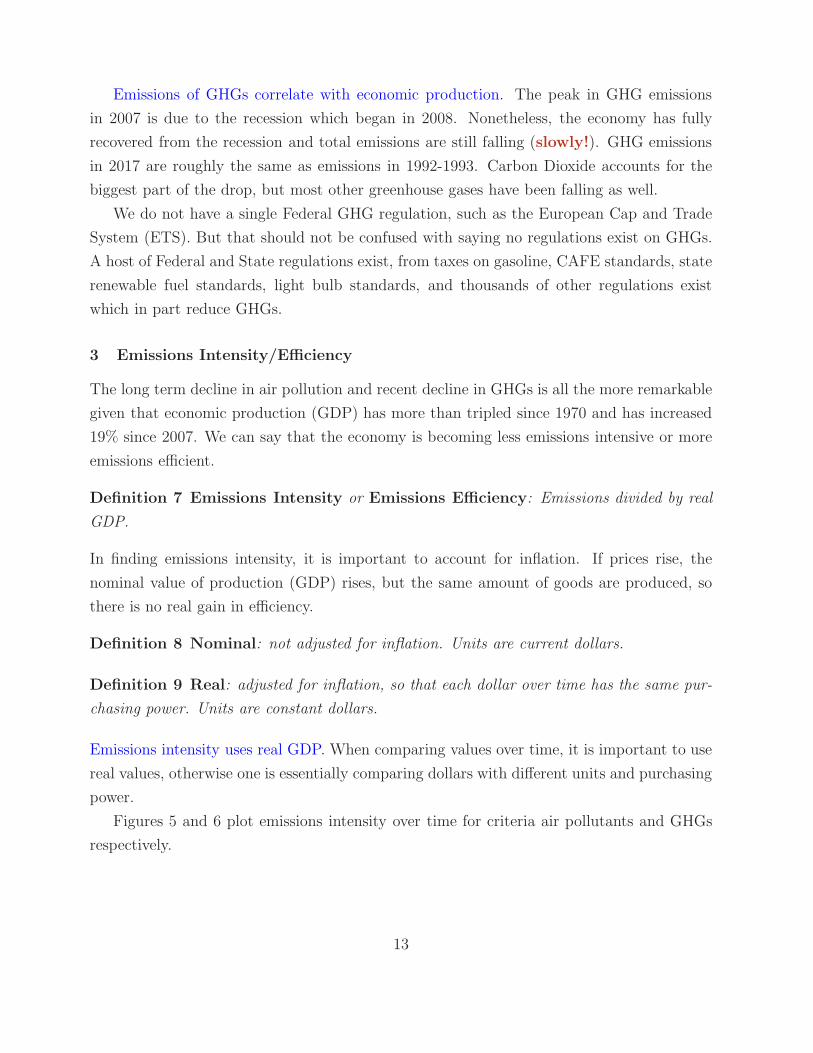

3 Emissions Intensity/Efficiency

The long term decline in air pollution and recent decline in GHGs is all the more remarkable

given that economic production (GDP) has more than tripled since 1970 and has increased

19% since 2007. We can say that the economy is becoming less emissions intensive or more

emissions efficient.

Definition 7 Emissions Intensity or Emissions Efficiency: Emissions divided by real

GDP.

In finding emissions intensity, it is important to account for inflation. If prices rise, the

nominal value of production (GDP) rises, but the same amount of goods are produced, so

there is no real gain in efficiency.

Definition 8 Nominal: not adjusted for inflation. Units are current dollars.

Definition 9 Real: adjusted for inflation, so that each dollar over time has the same pur-

chasing power. Units are constant dollars.

Emissions intensity uses real GDP. When comparing values over time, it is important to use

real values, otherwise one is essentially comparing dollars with different units and purchasing

power.

Figures 5 and 6 plot emissions intensity over time for criteria air pollutants and GHGs

respectively.

13

1980 1985 1990 1995 2000 2005 2010 20150

0.5

1

1.5

2

2.5

Figure 5: Emissions Intensity of Criteria Air Pollutants.

1990 1995 2000 2005 2010 20150

1

2

3

4

5

6

7

Figure 6: Emissions Intensity of GHGs.

14

Figures 5 and 6 show very large declines in emissions intensity over time in the US.

Some regulations actually focus on emissions intensity rather than total emis-

sions. CAFE standards are a kind of intensity regulation, focusing on the efficiency of the

car rather than the amount of gasoline consumed. We will study intensity regulations and

see welfare differences versus regulations on total emissions.

Emissions intensity can also be used to assess industries. For example, the fashion indus-

try accounts for 2% of world GDP but 8% of world carbon emissions. The fashion industry

is therefore not very emissions efficient, emitting a lot of carbon to produce goods that are

relatively low value.

B Social Regulations

A number of regulations exist which are designed reduce income inequality, promote devel-

opment, and to provide health, education, or other social benefits. Consider the minimum

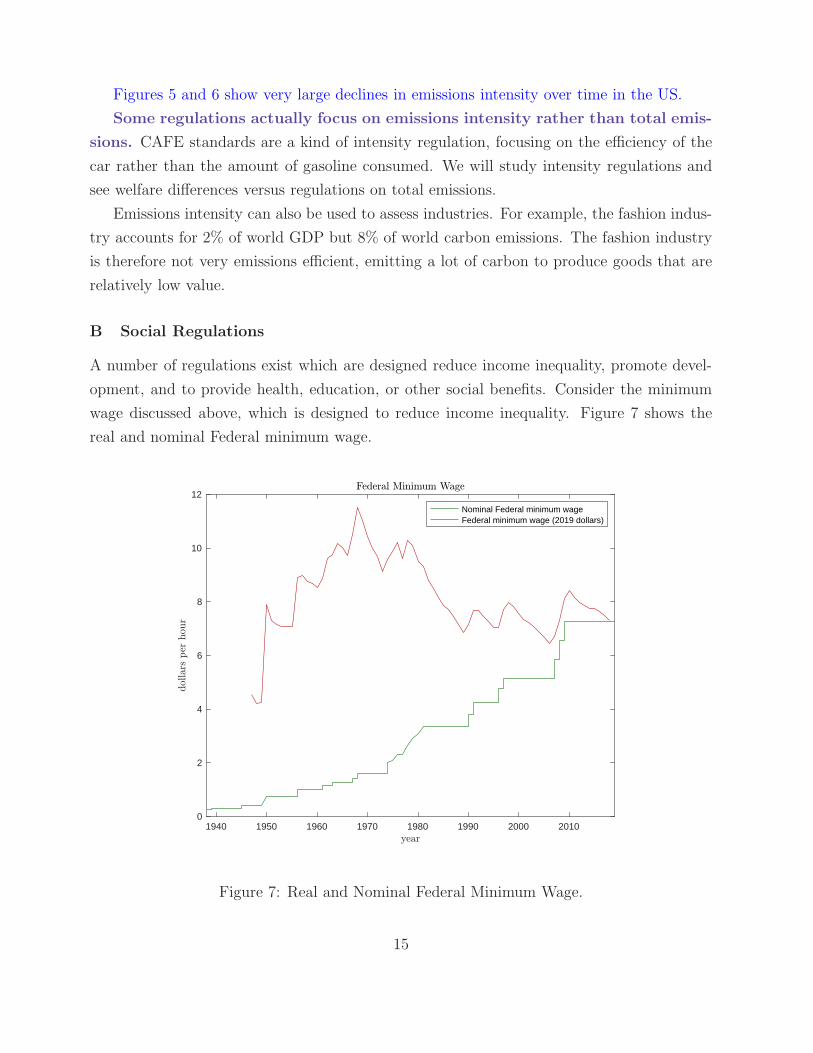

wage discussed above, which is designed to reduce income inequality. Figure 7 shows the

real and nominal Federal minimum wage.

1940 1950 1960 1970 1980 1990 2000 20100

2

4

6

8

10

12

Nominal Federal minimum wageFederal minimum wage (2019 dollars)

Figure 7: Real and Nominal Federal Minimum Wage.

15

The nominal Federal Minimum Wage has not changed since 2009. Nonetheless, the real

minimum wage falls over time as inflation reduces the purchasing power of the nominal

Federal minimum. The real minimum wage been roughly constant since 1990. In turn,

many states and municipalities have set their own higher minimum wages.

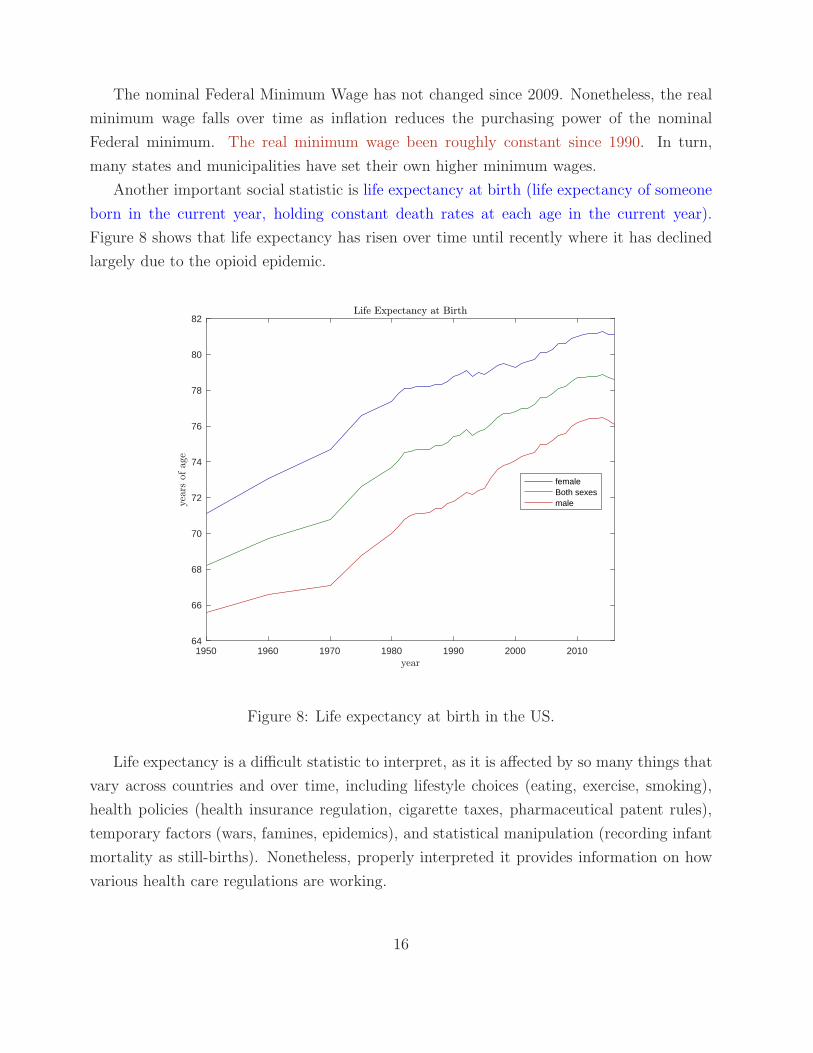

Another important social statistic is life expectancy at birth (life expectancy of someone

born in the current year, holding constant death rates at each age in the current year).

Figure 8 shows that life expectancy has risen over time until recently where it has declined

largely due to the opioid epidemic.

1950 1960 1970 1980 1990 2000 201064

66

68

70

72

74

76

78

80

82

femaleBoth sexesmale

Figure 8: Life expectancy at birth in the US.

Life expectancy is a difficult statistic to interpret, as it is affected by so many things that

vary across countries and over time, including lifestyle choices (eating, exercise, smoking),

health policies (health insurance regulation, cigarette taxes, pharmaceutical patent rules),

temporary factors (wars, famines, epidemics), and statistical manipulation (recording infant

mortality as still-births). Nonetheless, properly interpreted it provides information on how

various health care regulations are working.

16

V Regulation Facts

Regulations are difficult to measure. A regulation may have little effect (few make the

Federal minimum wage), or a very dramatic effect. Regulations also might impose large or

negligible costs. Costs and benefits might also be small, but significant on small groups of

people (e.g. agricultural price supports). These caveats aside, we can look at a few statistics.

The Federal government has several categories:

Definition 10 Economically Significant Rules: have an annual effect on the economy

of $100M or more or adversely affect in a material way the economy, a sector of the economy,

productivity, competition, jobs, the environment, public health or safety, or State, local, or

tribal governments or communities.

Definition 11 Significant Rules: create a serious inconsistency or otherwise interfere

with an action taken or planned by another agency; materially alter the budgetary impact of

entitlements, grans, user fees, or loan programs or the rights and obligations of the recipients

thereof; or raise novel legal or policy issues arising out of legal mandates, the President’s

priorities, or the principles set forth. Includes economically significant rules.

Definition 12 Major Rules: one that has resulted in or is likely to result in (1) an an-

nual effect on the economy of $100M or more; (2) a major increase in costs or prices for

consumers, individual industries, federal, state, or local government agencies, or geographic

regions; or (3) significant adverse effects on competition, employment, investment, produc-

tivity, or innovation, or on the ability of US-based enterprises to compete with foreign-based

enterprises in domestic and export markets.

These definitions are both vague and inclusive of many different ideas. Plenty of ambiguity

exists as to how to categorize each regulation.

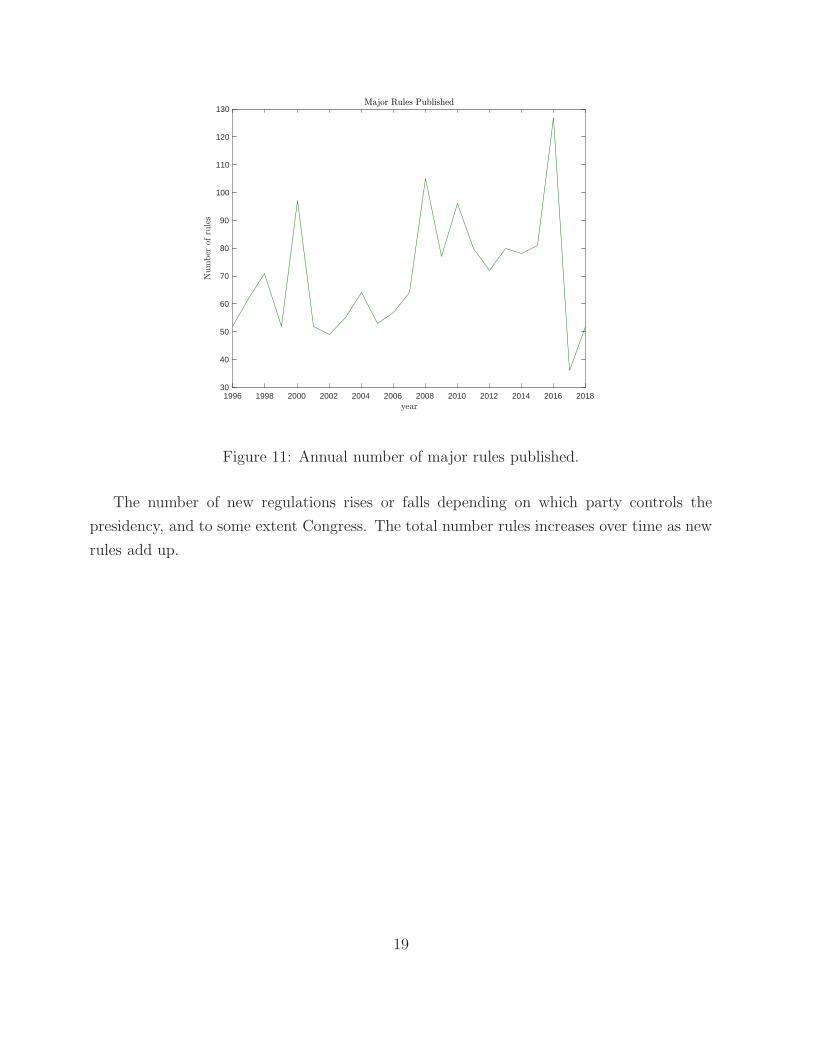

Figures 9-11 show the number of new Federal regulations, separated by economic cost.

17

1985 1990 1995 2000 2005 2010 20150

10

20

30

40

50

60

70

80

90

100

Figure 9: Annual number of economically significant rules published. Year starts and ends in

late January (presidential year). Source: George Washington University Regulatory Studies

Center.

1995 2000 2005 2010 201550

100

150

200

250

300

350

400

Figure 10: Annual number of significant rules published.

18

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 201830

40

50

60

70

80

90

100

110

120

130

Figure 11: Annual number of major rules published.

The number of new regulations rises or falls depending on which party controls the

presidency, and to some extent Congress. The total number rules increases over time as new

rules add up.

19

MARKETS AND MARKET FAILURES

I Markets and Market Failures

This section will build in part on Eco 613. You may want to review your notes from that

class.

Unregulated markets provide many goods and services quite efficiently. Few complain

about shortages of Iphones. But other valuable goods seem to be under-provided, for example

clean air, ecosystems, innovations, and income equality (people value societies where income

is relatively evenly distributed). If a valuable good is under-provided, a case exists for

government regulation.

The first step to determine what kinds of goods are under-provided (and even what

“under-provided” means) and how the unregulated market “decides” what/how much goods

to produce. Doing so is helpful because companies must decide what/how much goods to

produce, and this decision is affected both by regulation and by sustainability considera-

tions. Once we understand how the unregulated market produces, we can make the case for

regulation and see how different kinds of regulation affect firm production decisions. The

eventual goal is to design a type of regulation that provides an optimal amount of each good.

A Private Supply and Demand

Consider a firm supplying a good to an unregulated market. The firm must decide how many

goods to produce. We will also start by assuming the market is perfectly competitive.

Definition 13 Perfect Competition: firms have no ability to influence input or output

prices.

Examples:

• Commodity markets (for example, oil and agricultural products) are competitive. An

oil producer sells oil on the world market at the spot price of oil (currently about $60

per barrel). Suppose an oil firm in Texas charges $60.01. Then the company would

lose all customers, who would just buy from someone else at $60.

• Many Retail markets such as internet retail, Uber/Lyft, and gasoline stations are

competitive.

20

• The market for Iphones is not competitive. if Apple raises the price, some customers

will buy other phones, but many will pay the higher price.

Competitive markets are characterized by:

1. Non-differentiated products. The same product is produced by all companies.

2. A large number of producers exist.

3. Customers have full information about prices.

Sustainability note: Producing sustainable products helps companies differenti-

ate products, reducing competition.

B Private Marginal Cost

How many goods should a firm supply to a competitive market? It is useful to break down

the decision to produce each individually. Let Q denote the number of units produced and

TC (Q) the total cost of production (which depends on Q).

Definition 14 Marginal Costs: The cost of one additional unit of production.

The formula is:

MC =∆TC

∆Q(1)

Here ∆ means difference: ∆Q = Qnew −Qold.

Sometimes, people confuse marginal costs with average costs.

Definition 15 Average Costs: Total costs divided by production.

The formula is:

ATC =TC

Q(2)

For example, the marginal cost of an additional passenger on an airplane which is not full

is less than $5. When another passenger is added, the only costs that rise are the peanuts

and the fuel cost of the extra weight. In contrast, the average cost can be substantial: if the

flight costs $10,000 (not including the plane) and 200 passengers are on the flight, then the

average cost is $10K/200 = $50, which is much larger.

21

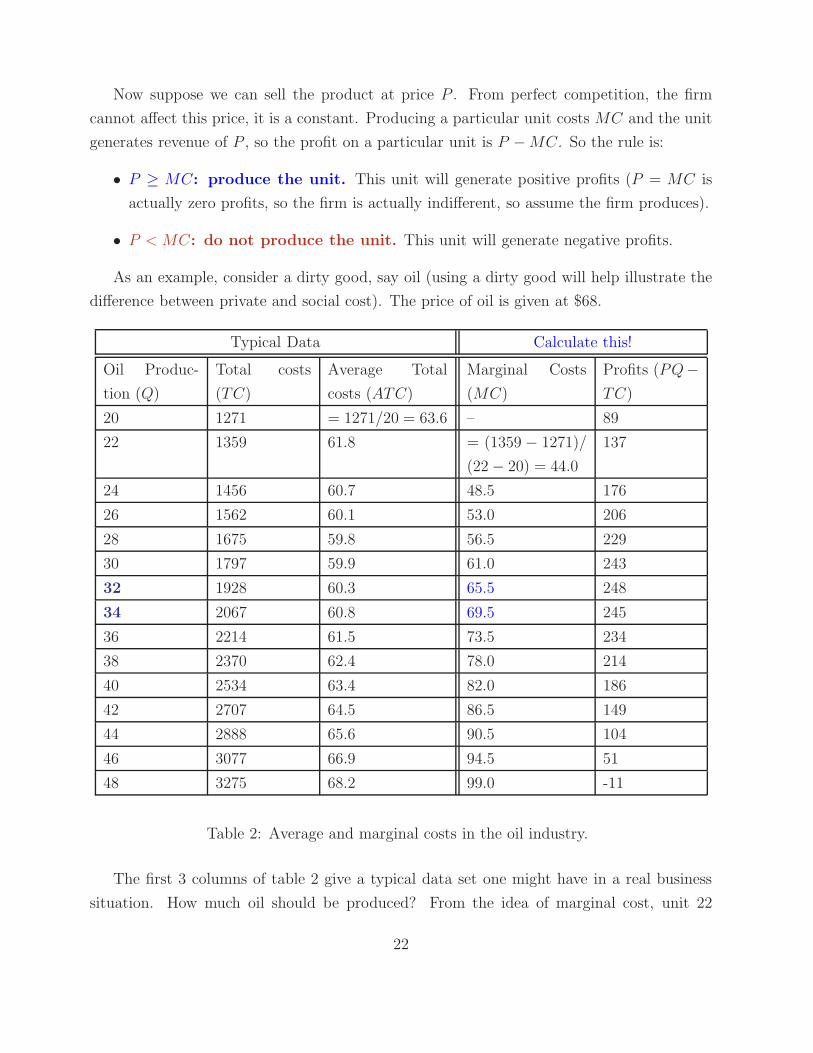

Now suppose we can sell the product at price P . From perfect competition, the firm

cannot affect this price, it is a constant. Producing a particular unit costs MC and the unit

generates revenue of P , so the profit on a particular unit is P −MC. So the rule is:

• P ≥ MC: produce the unit. This unit will generate positive profits (P = MC is

actually zero profits, so the firm is actually indifferent, so assume the firm produces).

• P < MC: do not produce the unit. This unit will generate negative profits.

As an example, consider a dirty good, say oil (using a dirty good will help illustrate the

difference between private and social cost). The price of oil is given at $68.

Typical Data Calculate this!

Oil Produc-

tion (Q)

Total costs

(TC)

Average Total

costs (ATC)

Marginal Costs

(MC)

Profits (PQ−

TC)

20 1271 = 1271/20 = 63.6 – 89

22 1359 61.8 = (1359 − 1271)/

(22− 20) = 44.0

137

24 1456 60.7 48.5 176

26 1562 60.1 53.0 206

28 1675 59.8 56.5 229

30 1797 59.9 61.0 243

32 1928 60.3 65.5 248

34 2067 60.8 69.5 245

36 2214 61.5 73.5 234

38 2370 62.4 78.0 214

40 2534 63.4 82.0 186

42 2707 64.5 86.5 149

44 2888 65.6 90.5 104

46 3077 66.9 94.5 51

48 3275 68.2 99.0 -11

Table 2: Average and marginal costs in the oil industry.

The first 3 columns of table 2 give a typical data set one might have in a real business

situation. How much oil should be produced? From the idea of marginal cost, unit 22

22

generates $68− $44 = $24 of profit and should be produced. Unit 38 generates $68− $78 =

−$10 of profit and should not be produced. Overall, between 32 and 34 units should be

produced, as this is where P = MC.

Notice that MC increases with the quantity produced. Many marginal costs are con-

stant. For the oil driller, costs such as shipping and taxes are constant costs per unit. Any

constant per unit cost is a marginal cost. But other marginal costs increase. With

oil, it becomes more difficult to extract larger volumes as less efficient wells must be brought

online. Saudi wells operate at a marginal cost of $10 per barrel, US fracking is about $37

per barrel (for the Permian Basin in Texas), and North Sea oil is about $39 per barrel. Once

Saudi wells are at maximum production, the marginal cost rises from $10 to $37 since the

more costly fracking wells are brought online.

From Table 2, we can also use marginal cost to determine how the supply of goods to the

market varies with the price. For example, at a price of $48.50, 24 units are supplied and

the marginal cost is $48.50, at a price of $53, 26 units are supplied and the marginal cost is

$53, etc.

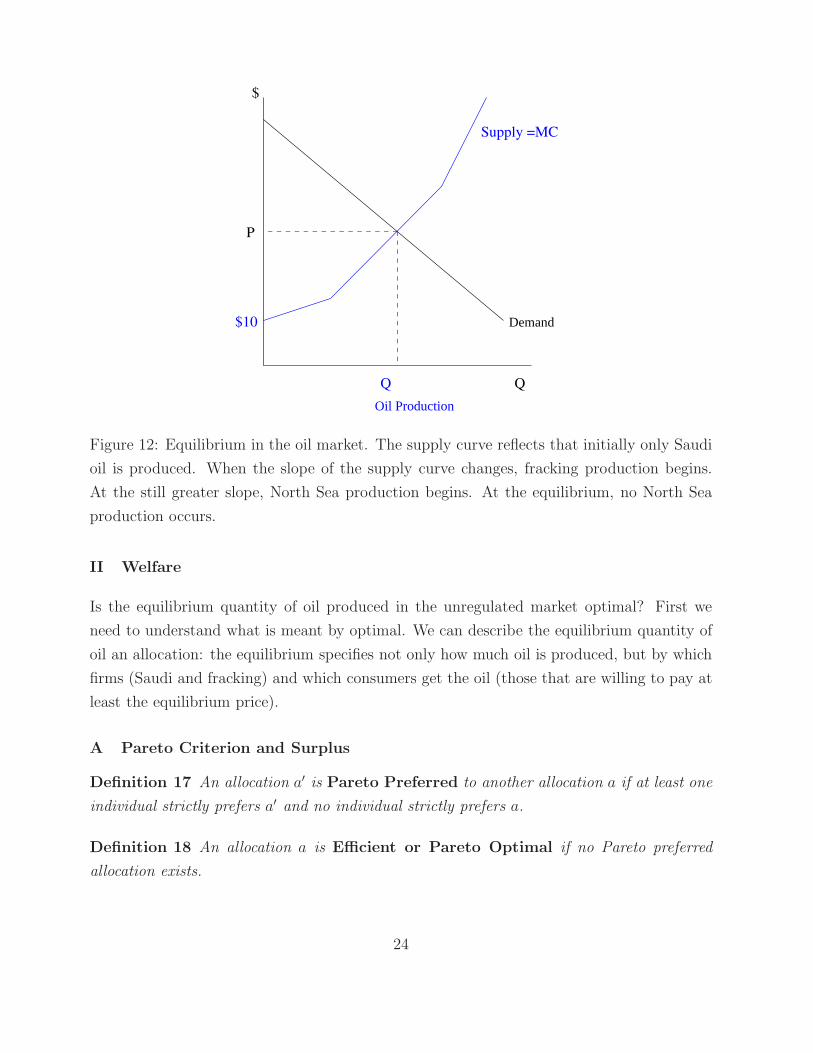

C Equilibrium

First, let us review what equilibrium means:

Definition 16 Equilibrium: A set of quantities and prices such that no one has an incen-

tive to change behavior.

Suppose demand was greater than supply at a price of $53. Consumers begin to bid up the

price in the world oil spot markets. Producers then have an incentive to increase production

and/or bring new wells online to satisfy that demand. As the price increases, some but not

all consumers drop out because oil is too expensive. The process stops when supply equals

demand. Conversely, when supply exceeds demand, an excess of oil is produced and sellers

begin to decrease prices on the world spot market. As the price falls, expensive producers

drop out, and additional buyers, motivated by the low prices, enter. Supply decreases and

demand increases until supply equals demand.

23

Demand

Oil Production

Supply =MC

Q

$

Q

$10

P

Figure 12: Equilibrium in the oil market. The supply curve reflects that initially only Saudi

oil is produced. When the slope of the supply curve changes, fracking production begins.

At the still greater slope, North Sea production begins. At the equilibrium, no North Sea

production occurs.

II Welfare

Is the equilibrium quantity of oil produced in the unregulated market optimal? First we

need to understand what is meant by optimal. We can describe the equilibrium quantity of

oil an allocation: the equilibrium specifies not only how much oil is produced, but by which

firms (Saudi and fracking) and which consumers get the oil (those that are willing to pay at

least the equilibrium price).

A Pareto Criterion and Surplus

Definition 17 An allocation a′ is Pareto Preferred to another allocation a if at least one

individual strictly prefers a′ and no individual strictly prefers a.

Definition 18 An allocation a is Efficient or Pareto Optimal if no Pareto preferred

allocation exists.

24

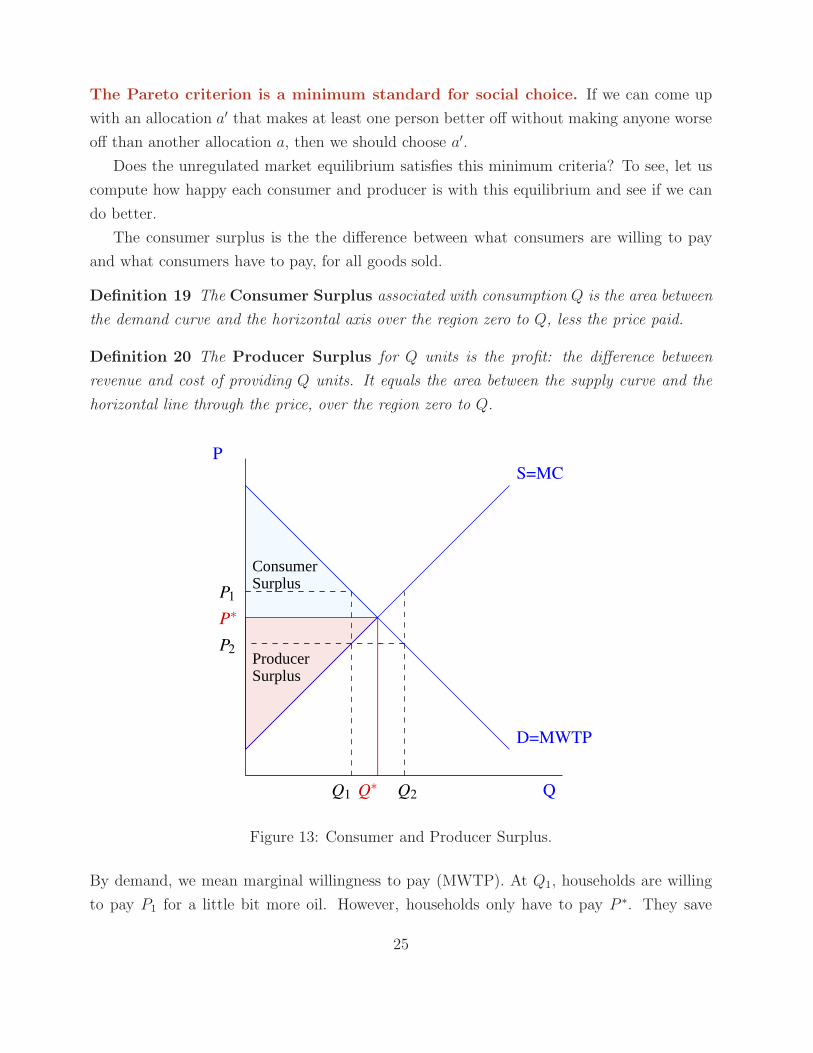

The Pareto criterion is a minimum standard for social choice. If we can come up

with an allocation a′ that makes at least one person better off without making anyone worse

off than another allocation a, then we should choose a′.

Does the unregulated market equilibrium satisfies this minimum criteria? To see, let us

compute how happy each consumer and producer is with this equilibrium and see if we can

do better.

The consumer surplus is the the difference between what consumers are willing to pay

and what consumers have to pay, for all goods sold.

Definition 19 The Consumer Surplus associated with consumption Q is the area between

the demand curve and the horizontal axis over the region zero to Q, less the price paid.

Definition 20 The Producer Surplus for Q units is the profit: the difference between

revenue and cost of providing Q units. It equals the area between the supply curve and the

horizontal line through the price, over the region zero to Q.

SurplusProducer

ConsumerSurplus

Q∗

P∗

Q1 Q2

S=MC

D=MWTP

Q

P

P1

P2

Figure 13: Consumer and Producer Surplus.

By demand, we mean marginal willingness to pay (MWTP). At Q1, households are willing

to pay P1 for a little bit more oil. However, households only have to pay P ∗. They save

25

P −P ∗ which can be used to purchase something else. Similarly, on unit Q1, producers make

P ∗ −Q1 profits. So we can say three things about the market equilibrium:

1. Production takes place at the lowest cost producers.

2. The production goes to the consumers who value that production the most (measured

by their willingness to pay).

3. There is no Pareto preferred allocation to Q∗.

Consider any allocation Q2 > Q. Some producers (stockholder or entrepreneurs) are

worse off, they must produce oil at negative profits. Consider any allocation Q1 < Q. A few

consumers are worse off, they lose the opportunity to purchase a good they value at more

than P ∗ for a price P ∗ (consumer surplus decreases). A few producers are also worse off,

they lose the opportunity to profitably supply goods to the market.

Thus, there is no way to improve on the market equilibrium without making someone

worse off, so the market equilibrium is Pareto Optimal. Total surplus is maximized.

B Welfare Theorems

The optimality result for a single good can be extended to the entire economy, under certain

conditions.

THEOREM 1 First Fundamental Theorem of Welfare Economics: The competitive

equilibrium of a market economy is Pareto Optimal/Efficient.

THEOREM 2 Second Fundamental Theorem of Welfare Economics: Any efficient

allocation can be achieved by a market economy provided resources are appropriately dis-

tributed before the market operates.

Assumptions of welfare theorems:

1. Complete Markets and Property Rights. A well-defined, transferable, and secure

property right exists for each good. A market exists to trade the rights to each good.

The benefits of each good accrues to the owner of the property right. This is equivalent

to saying no public good or externalities exist.

2. Atomistic Participants. Producers and consumers are small relative to the market

and thus cannot influence prices (no monopolies/oligopolies).

26

3. Complete Information. Consumers and producers have equal knowledge of current

and future prices.

4. No Transaction Costs. It must be costless to price and trade each good.

That the market equilibrium is Pareto Optimal is a beautiful theoretical result. However,

the assumptions make clear that Markets may fail: one or more assumptions of the welfare

theorems is not satisfied, and thus the market does not provide the optimal quantity of a

good.

People often misinterpret the welfare theorems. They do not say that the market should

not be regulated. Instead they state when markets fail, and when government intervention

can lead to Pareto preferred allocations. Examples:

• Clean air: a firm could produce clean air by emitting less pollution. However, no

market exists to sell clean air. The firm cannot prevent households from consuming

clean air without paying. We should therefore expect markets to provide less clean air

than is optimal.

• Water: water is highly regulated, but is there an externality or public good? Companies

can and do sell water, and consumers cannot consume water made by firms for free.

Producing water does not generate any external benefits that the firm cannot capture

through higher prices.

• Safe working conditions: safe working conditions are demanded by workers and sup-

plied by firms. But there is no market in which a worker could buy safer working

conditions (less obvious markets may exist: workers may demand a wage premium for

working in unsafe environments). Further, information on safety conditions might be

hard to come by for workers.

• Gender pay equality. Similarly, no obvious market exists, but firms which practice

gender pay equality may attract more productive workers. However, the information

problem exists in that it is unclear to workers how much firms value their labor.

Definition 21 Externality: Production or consumption activity which affects a third party

without compensation.

• Negative Externality: Production or consumption which reduces a third party’s util-

ity or profits without compensation.

27

• Positive Externality: Production or consumption which increases a third party’s

utility or profits without compensation.

The second welfare theorem is about distribution or equality. It says that by allocating

wealth unevenly, we can generate many different competitive equilibria which are Pareto

Efficient. Think carefully: an allocation where one person receives all goods is a Pareto

efficient allocation: no way exists to make one person better off without making the wealthy

person worse off. By giving one person all resources at the beginning, the resulting compet-

itive equilibrium will generate an allocation in which one person continues to have all the

resources. From this we conclude:

• Efficiency and Equity are different.

• The market produces efficient allocations (subject to the conditions above), but does

not ensure equity.

III Social Marginal Cost

A Output Markets

To find the optimal allocation when markets fail, we need to consider all marginal costs,

not just those paid by the firm. Consider oil. One barrel of oil results in the emission of

0.43 metric tons of CO2 per barrel of oil. Carbon emissions results in climate change which

imposes a number of costs:

1. Health costs. Climate change causes increased heat related mortality (e.g. heat

stroke), increases in disease (e.g. West Nile virus), illnesses resulting from poor air

quality (e.g. ozone rises, causing more asthma).

2. Productivity costs. Climate change decreases labor productivity (workers are sick

more often and are less productive working outdoors in the heat) and agricultural

productivity (some crops do less well in the heat).

3. Sea level rise costs. Especially coastal property damage.

4. See the 4th National Climate Assessment for a complete listing (22 total).

None of these are paid by the oil company. They are social costs not private costs.

28

Definition 22 Social costs: All production costs including those paid by someone other

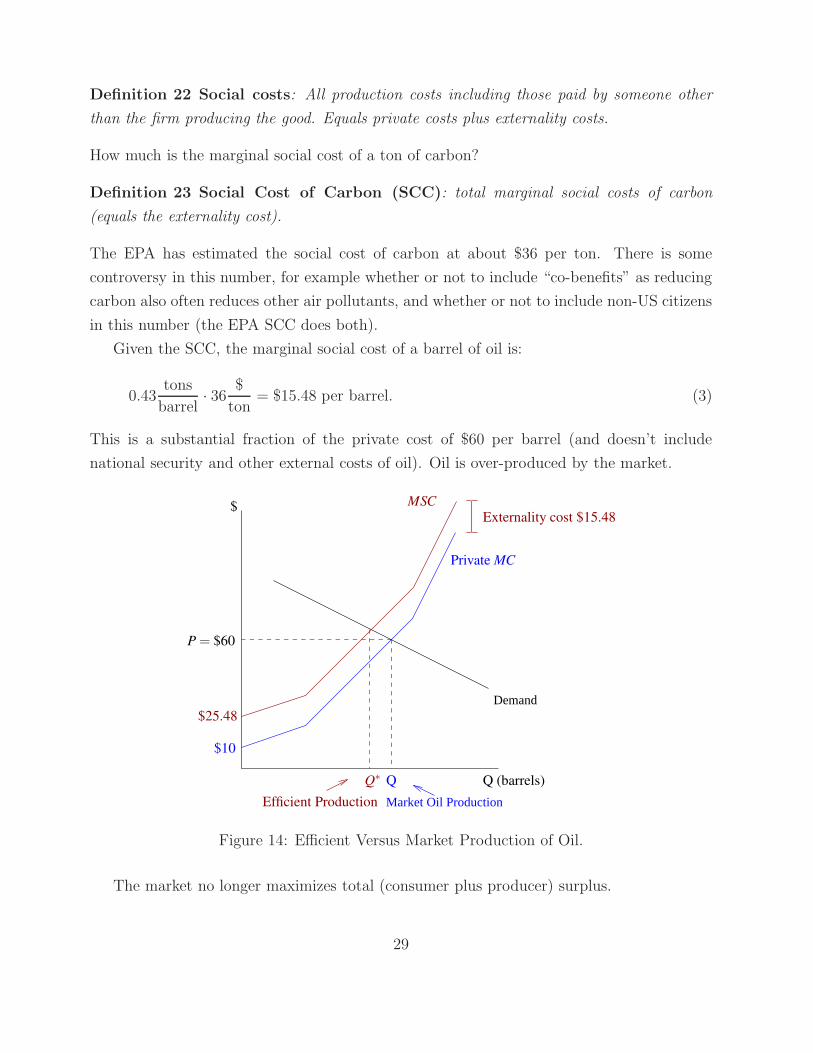

than the firm producing the good. Equals private costs plus externality costs.

How much is the marginal social cost of a ton of carbon?

Definition 23 Social Cost of Carbon (SCC): total marginal social costs of carbon

(equals the externality cost).

The EPA has estimated the social cost of carbon at about $36 per ton. There is some

controversy in this number, for example whether or not to include “co-benefits” as reducing

carbon also often reduces other air pollutants, and whether or not to include non-US citizens

in this number (the EPA SCC does both).

Given the SCC, the marginal social cost of a barrel of oil is:

0.43tons

barrel· 36

$

ton= $15.48 per barrel. (3)

This is a substantial fraction of the private cost of $60 per barrel (and doesn’t include

national security and other external costs of oil). Oil is over-produced by the market.

Demand

Market Oil Production

Q∗

Externality cost $15.48

Efficient Production

$25.48

Q (barrels)

Private MC

MSC

$10

Q

$

P = $60

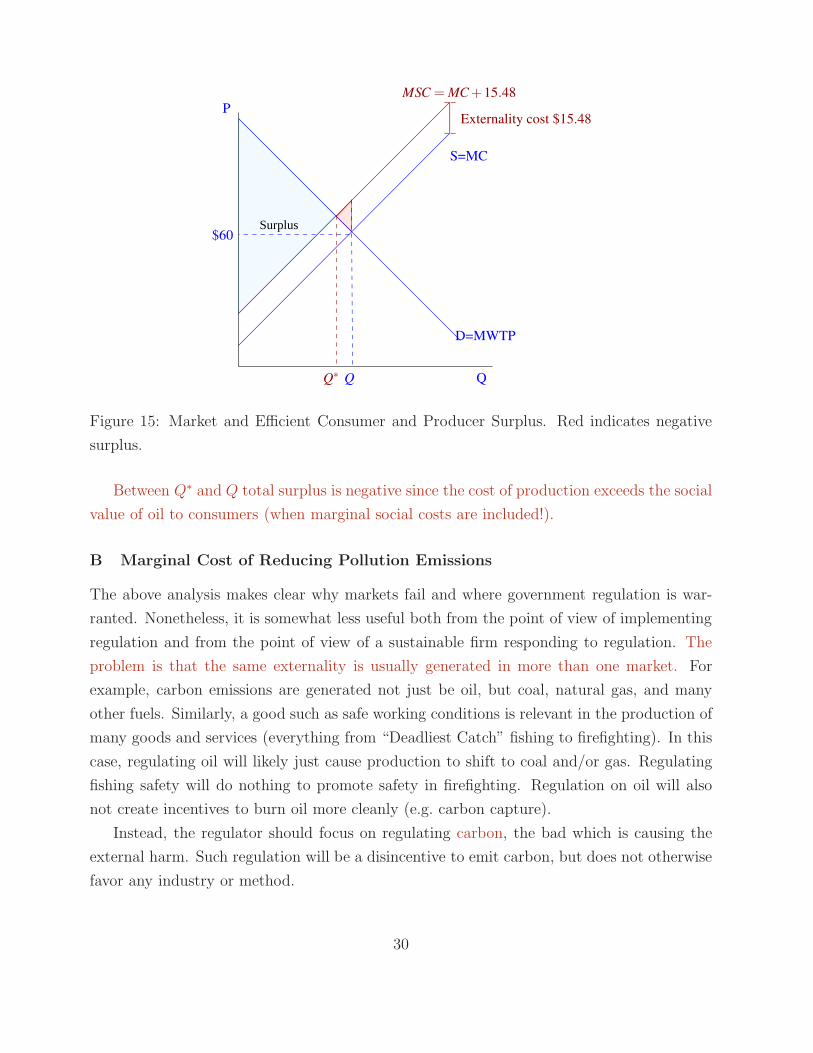

Figure 14: Efficient Versus Market Production of Oil.

The market no longer maximizes total (consumer plus producer) surplus.

29

Surplus$60

Q

S=MC

Externality cost $15.48

MSC = MC+15.48

Q∗

P

D=MWTP

Q

Figure 15: Market and Efficient Consumer and Producer Surplus. Red indicates negative

surplus.

Between Q∗ and Q total surplus is negative since the cost of production exceeds the social

value of oil to consumers (when marginal social costs are included!).

B Marginal Cost of Reducing Pollution Emissions

The above analysis makes clear why markets fail and where government regulation is war-

ranted. Nonetheless, it is somewhat less useful both from the point of view of implementing

regulation and from the point of view of a sustainable firm responding to regulation. The

problem is that the same externality is usually generated in more than one market. For

example, carbon emissions are generated not just be oil, but coal, natural gas, and many

other fuels. Similarly, a good such as safe working conditions is relevant in the production of

many goods and services (everything from “Deadliest Catch” fishing to firefighting). In this

case, regulating oil will likely just cause production to shift to coal and/or gas. Regulating

fishing safety will do nothing to promote safety in firefighting. Regulation on oil will also

not create incentives to burn oil more cleanly (e.g. carbon capture).

Instead, the regulator should focus on regulating carbon, the bad which is causing the

external harm. Such regulation will be a disincentive to emit carbon, but does not otherwise

favor any industry or method.

30

• General Rule: regulation should on the cause of the externality, not goods which

indirectly affect the externality.

From the perspective of the sustainable firm, rarely is the goal to produce less to offset

externality costs. Instead, the goal is to keep production constant but still reduce the

negative externality (carbon). For example, Google does not try to limit searches to reduce

carbon emissions from electricity, but instead tries to increase electricity from renewable

sources.

The market inefficiency can be rephrased as an over-production of the particular bad

causing the negative externality, or the particular good causing the positive externality.

Firms incur marginal costs to reduce the bad/increase the good.

Definition 24 Marginal Cost of Reducing: the marginal cost of reducing a bad causing

an externality.

Definition 25 Marginal Cost of Increasing: the marginal cost of increasing a good

causing a positive externality.

Recall, the units of marginal cost are $ per unit of production ($/Q). Analogously, the

marginal cost of reducing/increasing has units of $ per unit of the bad or good.

For example, consider sulfur dioxide (SO2) emissions, which cause asthma. The formula

is:

MCR = −∆TC

∆SO2

=$

metric ton(4)

Since total costs rise when SO2 falls, the fraction is negative, so the negative sign

makes the marginal cost of reducing positive. Some ways to reduce emissions of SO2:

1. A coal fired power plant could switch from high sulfur (Appalachian Bituminous) to

low sulfur coal. High sulfur coal costs $2.40 per million BTU (mmBTU) and low sulfur

coal costs $4.56/mmBTU. This type of low sulfur coal has 0.53 lbs sulfur/mmBTU

and high sulfur coal has 1.74 lbs sulfur/mmBTU. The marginal cost is:

MCR = −4.56− 2.40

0.53− 1.74=

$1.79

lb Sulfur. (5)

2. An electricity consumer (e.g. Google) could switch from high sulfur coal powered elec-

tricity to renewables. The average price of solar, for example, is $16/mmBTU. Since

31

renewables emit no sulfur:

MCR = −2.40− 16

0− 1.74=

$7.82

lb Sulfur. (6)

3. A 2 hour worker safety training course taken by 10 workers each paid $20 per hour.

The cost is 2 · 10 · $20 = $400. We need a measure of the “good” that results. Suppose

we say that the risk of accidents falls from 3 per year to 1 per year. The marginal cost

of reducing is:

MCR = −$400− 0

1− 3= $200 per accident reduced. (7)

Sometimes, the marginal cost of reducing is actually small or zero, instead a fixed cost

exists. The calculation is then whether or not the benefits of reducing to the firm are enough

to cover the fixed cost.

• A paper mill could re-purpose sawdust and other byproducts into biofuels (“co-generation”).

Although co-generation requires up-front capital expenditures, the marginal cost of

reducing is actually negative: it is cheaper to use co-generation than conventional elec-

tricity to power paper mills. US paper mills now use 5% coal, 25% natural gas, and

70% biomass. Moving to 80% biomass and 20% natural gas would cut carbon emissions

intensity in half. This illustrates the difference between fixed costs and marginal costs.

Sometimes, the marginal cost of reducing/increasing is small and the issue is the up

front expense.

Calculating the MCR is important for the sustainability manager. It represents

the cost to the firm of being more sustainable.

C The Marginal Cost of Reducing from Switching Production Inputs

The above calculations were actually simplified, because the inputs, high sulfur coal, low

sulfur coal, and solar, are perfect substitutes in electricity production. That is, all units were

per mmBTU. Switching from 1 mmBTU of high sulfur coal to 1 mmBTU of low sulfur coal

does not matter from a production standpoint, because the exact same energy is provided.

Suppose, however, the sustainable and non-sustainable inputs are not perfect substitutes.

How can we calculate the marginal cost of reducing?

32

The answer is to use production inputs optimality condition derived in micro:

MRTS =MPx

MPy

=Px

Py

. (8)

Here x is the non-sustainable input to be replaced, y is the sustainable input to be increased,

MP is the marginal product, Px and Py are the input prices, and MRTS is the marginal

rate of technical substitution. For reference:

Definition 26 The Marginal Rate of Technical Substitution (MRTS) is the rate at

which one input is substituted for another while keeping production constant. It is the ratio

of the marginal products.

Definition 27 The Marginal Product is the additional output from an additional unit of

an input.

MPx =∆Q

∆x. (9)

Condition (8) says that if we have an extra dollar to spend on production inputs, we

should be indifferent between spending that dollar on x or y. If not, then we can reallocate

an existing dollar from the input that produces less to the input that produces more.

MPx

Px

=MPy

Py

. (10)

In the above equation units are production per dollar for each input.

Note: In 20 years of doing this, I have never found a case where a company

is using inputs optimally (the left and right hand side of equation 8 are not equal). The

good news is, if the company is using too much of an input which is not sustainable, the

marginal cost of reducing will be negative (profits increase by reducing the non-sustainable

input).

Deriving the marginal cost of reducing involves several steps:

1. Replace 1 unit of x with MRTS units of y. Production remains constant.

2. Calculate the change in cost: we have reduced x by 1 and so have saved Px dollars.

However, we have added MRTS units of y, and thus added MRTS · Py to costs. The

net change in costs is: ∆TC = MRTS · Py − Px.

3. Calculate the change in emissions from replacing 1 unit of x with MRTS units of y.

33

4. Divide the additional costs, by the change in emissions to get the marginal cost of

reducing.

1 Example 1: Google Replaces Coal with Solar

Consider again replacing high sulfur coal with solar energy. Here is the data:

• Cost of high sulfur coal: $59.29 per short ton.

• Productivity of coal: 24.73 mmBTU per short ton.

• Price of solar: $60 per mWh.

• Productivity of solar: 3.75 mmBTU per mWh.

• One short ton of coal emits 43.03 lbs of sulfur.

Next, we can derive the marginal cost of reducing:

1. The MRTS is the ratio of marginal products. We put the non-sustainable input on

top:

MRTS =MPc

MPs

=24.73

3.75= 6.59 mWh/short ton. (11)

One short ton of coal generates as much heat as 6.59 mWh of solar. So we replace 1

short ton of coal with 6.59 mWh of solar. Electricity production remains constant.

2. For the change in cost, we have:

∆TC = MRTS · Ps − Pc = 6.59 · $60− $59.29 = $336.11. (12)

By switching inputs, we have added $336.11 to our costs.

3. We have removed 1 short ton of sulfur, and so sulfur emissions fall by 43.02 lbs, since

solar emits no sulfur.

4. Compute the MCR:

MCR = −∆TC

∆S= −

$336.11

−43.02= $7.81 per pound sulfur. (13)

Notice that the answer is the same as we derived in equation (6), up to rounding error.

Usually the data in actual business situations is in this form, however.

34

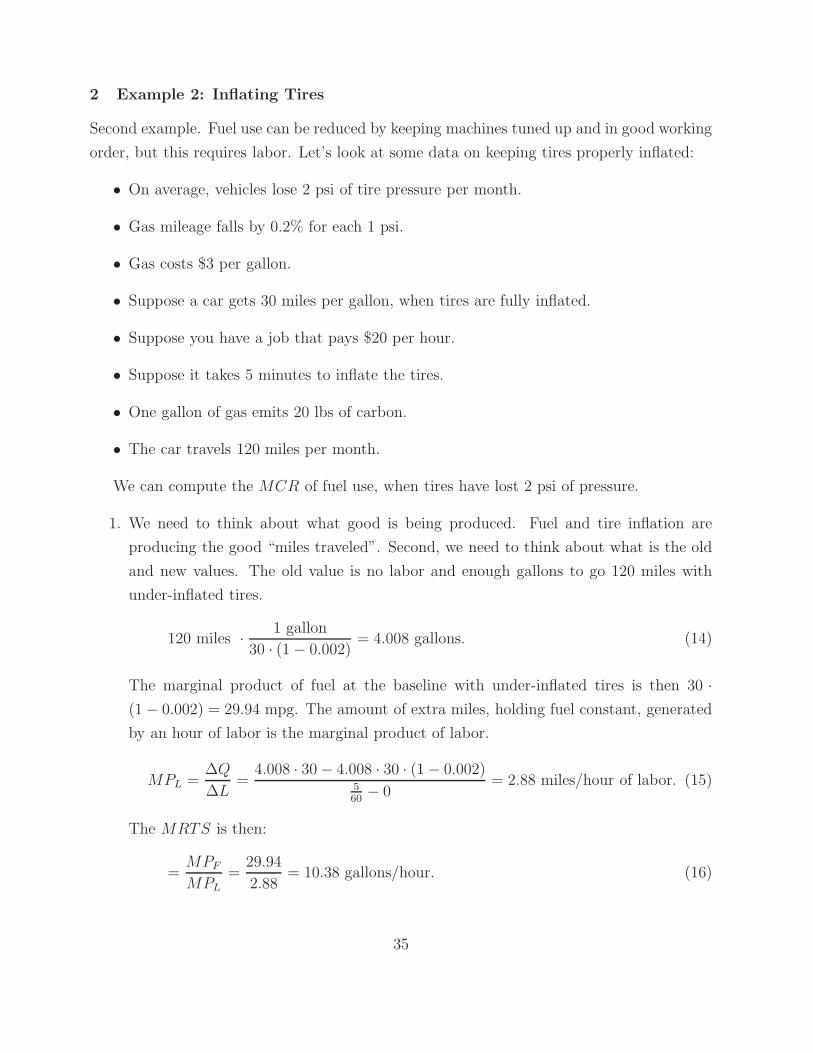

2 Example 2: Inflating Tires

Second example. Fuel use can be reduced by keeping machines tuned up and in good working

order, but this requires labor. Let’s look at some data on keeping tires properly inflated:

• On average, vehicles lose 2 psi of tire pressure per month.

• Gas mileage falls by 0.2% for each 1 psi.

• Gas costs $3 per gallon.

• Suppose a car gets 30 miles per gallon, when tires are fully inflated.

• Suppose you have a job that pays $20 per hour.

• Suppose it takes 5 minutes to inflate the tires.

• One gallon of gas emits 20 lbs of carbon.

• The car travels 120 miles per month.

We can compute the MCR of fuel use, when tires have lost 2 psi of pressure.

1. We need to think about what good is being produced. Fuel and tire inflation are

producing the good “miles traveled”. Second, we need to think about what is the old

and new values. The old value is no labor and enough gallons to go 120 miles with

under-inflated tires.

120 miles ·1 gallon

30 · (1− 0.002)= 4.008 gallons. (14)

The marginal product of fuel at the baseline with under-inflated tires is then 30 ·

(1− 0.002) = 29.94 mpg. The amount of extra miles, holding fuel constant, generated

by an hour of labor is the marginal product of labor.

MPL =∆Q

∆L=

4.008 · 30− 4.008 · 30 · (1− 0.002)5

60− 0

= 2.88 miles/hour of labor. (15)

The MRTS is then:

=MPF

MPL

=29.94

2.88= 10.38 gallons/hour. (16)

35

2. We consider replacing one gallon with an extra 10.38 hours of labor (think of a fleet

with many cars). The extra cost is:

∆TC = MRTS · PL − PF = 10.38 · $20− $3 = $204.57. (17)

3. Assume labor emits no carbon. One gallon of gas and thus 20 lbs of carbon is saved.

4. Compute:

MCR = −∆TC

∆C= −

$204.57

−20= $10.23 per pound carbon. (18)

This is an inexpensive way to reduce carbon (much less than $36 per ton), and that is with

only 120 miles traveled per month. The more miles that are traveled in a month, the more

productive is the labor.

IV Sustainability Considerations

The sustainability officer’s job is essentially to think broadly about the marginal cost of

reducing/increasing, recognizing hidden marginal costs that accrue from non-sustainable

production. For example, Google has a marginal energy cost per search. But too much

energy use makes Google less attractive to socially responsible investors. Google’s financing

cost (cost of capital) increases. The financing benefit of reducing offsets some of the marginal

cost of reducing.

Recall that we have six categories.

1. Direct costs: labor, machines, or raw materials (including energy) used to produce

the good. This is the cost of the sustainable inputs replacing the non-sustainable

inputs.

2. Cost of capital: savings (negative marginal cost) incurred because the firm becomes

more attractive to socially responsible investors.

3. Regulatory costs: savings imposed by regulation, including reduced taxes and fines.

4. Risk costs: savings corresponding to decreases in reputation risk and environmental

accidents caused by non-sustainable production.

36

5. Customer loss: savings in terms of additional customer demand from producing

products in a more sustainable way.

6. Innovation/long term focus.

The changes in marginal costs due to sustainability considerations are calculated in

an identical manner to the change in direct costs above. For example, suppose Google

is able to get a lower interest rate on a loan, by reducing sulfur dioxide emissions. Sup-

pose the present value of the interest savings is $200M, and to obtain the loan Google

had to sulfur emissions by 100 million pounds. The marginal savings is $200M/100M =

$2/lb.Thenetmarginalcostis : $7.81−$2 = $5.81 per lb sulfur. The goal is to reduce the

marginal cost to zero or even negative, so that the firm benefits from reducing.

V Public Goods

A Definitions

Definition 28 A good (bad) is Excludable if it is practical to selectively allow consumers

to consume (avoid consuming) the good.

1. Electricity is excludable: FPL allows only those consumers who pay for electricity to

use it.

2. A park is somewhat excludable: the city can pay for fences and a gate, and a booth

to charge those who enter. But people can still appreciate it from a distance.

3. Beaches are less excludable: Even for private beaches, it is difficult to prevent others

from using it, especially if they are simply checking out the view from the street.

4. Clean air is non-excludable: there is no way to charge for clean air.

Definition 29 A good (bad) is Rival if consumption of a unit of the good (bad) by one

person diminishes the amount of the good (bad) available to others to consume.

1. Electricity is Rival: the juice powering my computer cannot be used again to power

something else.

2. A park is somewhat rival: one person using the park does not mean others cannot use

it, until the park is filled to capacity.

37

3. Beaches are less rival: a beach can hold a large number of people before being filled to

capacity.

4. Clean air is non-rival: for all practical purposes, everyone can breathe the air at the

same time.

So rival and excludable should be viewed on a continuum. The degree of non-excludability

depends on the cost of exclusion. The degree of non-rivalry depends on the number of people

who can use the good before capacity is reached.

Definition 30 A Pure Public Good is non-rival and non-excludable

Non-rival goods violate assumption 1 of the welfare theorems: the benefits of the good do

not accrue solely to the owner. Excludable goods also violate assumption 1: the property

right is not secure. Public goods will be under-provided in a market economy, since people

besides the owner can use the good without paying for it. Therefore, the price does not

reflect what people are willing to pay.

B Optimal Provision of Public Goods

Supply of a public good is the same as supply of any other good. As in the previous section,

companies may want to provide public goods as part of their sustainability programs. Con-

sider a company which donates to help save endangered species. The benefits of biodiversity

are non-rival and non-excludable. The goal of the sustainability manager is to find

benefits to the firm for public goods provision, so that a business case can be

made.

Demand for a non-rival good is different. If Jack is willing to pay $2.50 for the beach

and April is willing to pay $3, then we should provide the beach as long as it costs less than

$5.50 to produce, because both Jack and April can consume the beach together.

If the beach were rival, we would need to provide two beaches. Thus if beaches are rival

we should provide one beach if the first beach costs less than $3, and a second beach if the

second costs less than $2.50.

With non-rival goods, we sum the price each consumer is willing to pay (we

sum the demand curves vertically).

• Jack: is willing to pay PJ = −0.75Q+ 4.

• April: is willing to pay PA = −1.5Q + 6.

38

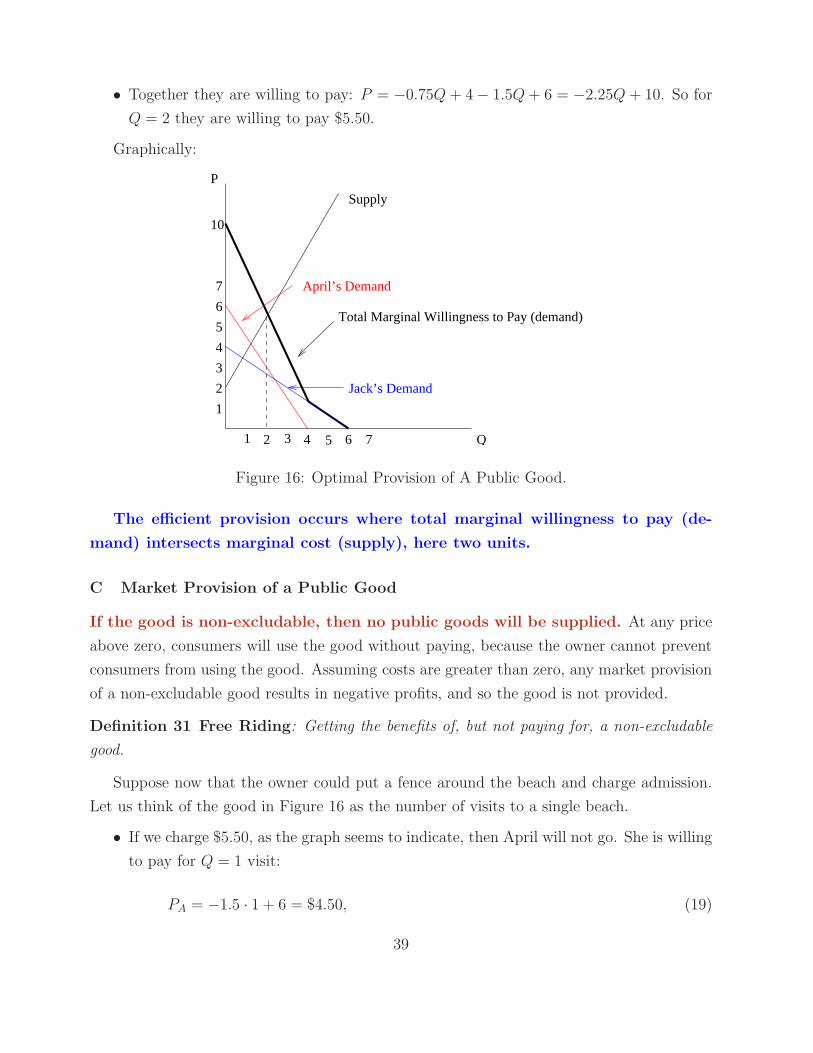

• Together they are willing to pay: P = −0.75Q + 4− 1.5Q+ 6 = −2.25Q + 10. So for

Q = 2 they are willing to pay $5.50.

Graphically:

P

Q

1

2

3

4

5

6

7

Total Marginal Willingness to Pay (demand)

Jack’s Demand

10

Supply

April’s Demand

21 3 4 5 6 7

Figure 16: Optimal Provision of A Public Good.

The efficient provision occurs where total marginal willingness to pay (de-

mand) intersects marginal cost (supply), here two units.

C Market Provision of a Public Good

If the good is non-excludable, then no public goods will be supplied. At any price

above zero, consumers will use the good without paying, because the owner cannot prevent

consumers from using the good. Assuming costs are greater than zero, any market provision

of a non-excludable good results in negative profits, and so the good is not provided.

Definition 31 Free Riding: Getting the benefits of, but not paying for, a non-excludable

good.

Suppose now that the owner could put a fence around the beach and charge admission.

Let us think of the good in Figure 16 as the number of visits to a single beach.

• If we charge $5.50, as the graph seems to indicate, then April will not go. She is willing

to pay for Q = 1 visit:

PA = −1.5 · 1 + 6 = $4.50, (19)

39

but the cost is $5.50.

• If If we charge $5.50, then Jack will not go. He is willing to pay for Q = 1 visit:

PJ = −0.75 · 1 + 4 = $3.25, (20)

but the cost is $5.50.

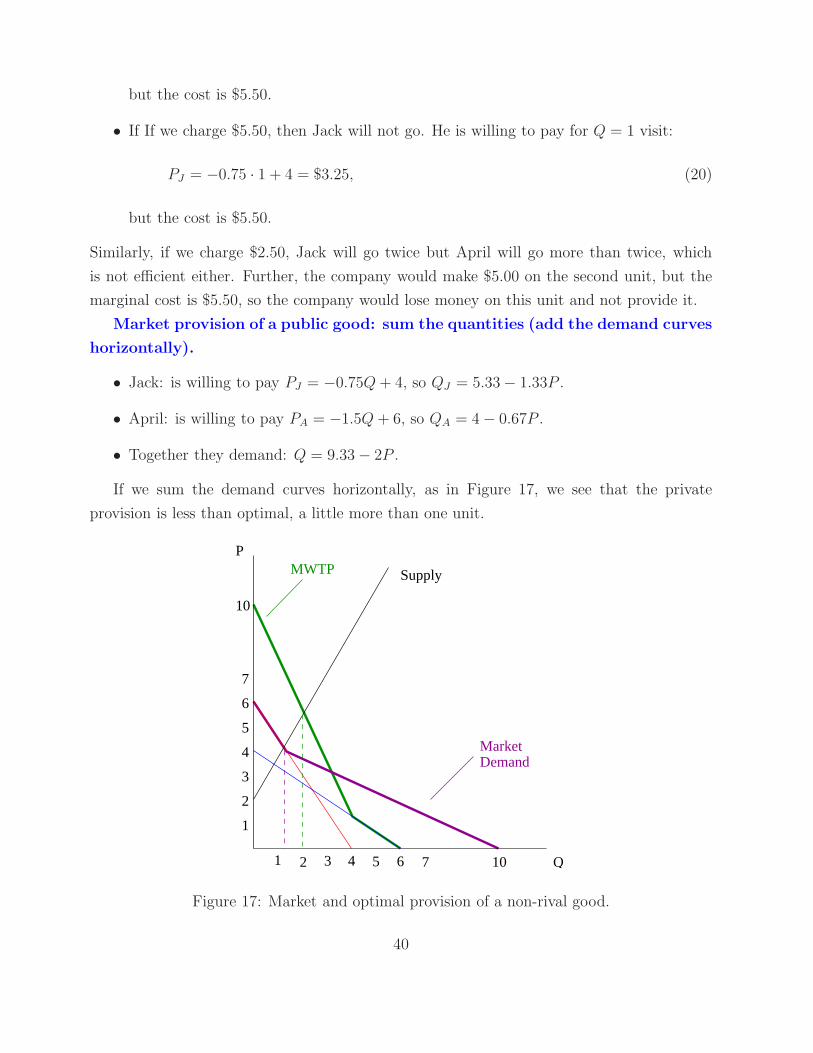

Similarly, if we charge $2.50, Jack will go twice but April will go more than twice, which

is not efficient either. Further, the company would make $5.00 on the second unit, but the

marginal cost is $5.50, so the company would lose money on this unit and not provide it.

Market provision of a public good: sum the quantities (add the demand curves

horizontally).

• Jack: is willing to pay PJ = −0.75Q+ 4, so QJ = 5.33− 1.33P .

• April: is willing to pay PA = −1.5Q + 6, so QA = 4− 0.67P .

• Together they demand: Q = 9.33− 2P .

If we sum the demand curves horizontally, as in Figure 17, we see that the private

provision is less than optimal, a little more than one unit.

10

P

Q

1

2

Market4

5

6

7

10

SupplyMWTP

4 6 752 31

3Demand

Figure 17: Market and optimal provision of a non-rival good.

40

The key is that the producer must charge the same price to both Jack and April. If Jack

and April pooled their money and offered a total of $5.50 for their second trips, the producer

would accept. But then Jack and April cannot easily bargain with each other. April may

claim she is not willing to pay $3, to try to get Jack to pay more, for example.

41

Related Documents