Economic Update Mark Rider, Head of Investment Strategy

Economic Update Mark Rider, Head of Investment Strategy.

Dec 29, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Economic UpdateMark Rider, Head of Investment Strategy

2

Global growth: better and worse

The Transition Twins: China and Australia

Equities: home, away or just stay away?

What it all means for your clients

Three themes and their implications

3

Global Growth - better as at long run trend …

Source: Thomson Reuters Datastream, ANZ Global Wealth

4

… and unemployment has fallen a long way

Source: Thomson Reuters Datastream, ANZ Global Wealth

5

But worse as lower trend growth means lower returns

Source: Bloomberg, ANZ Global Wealth

6

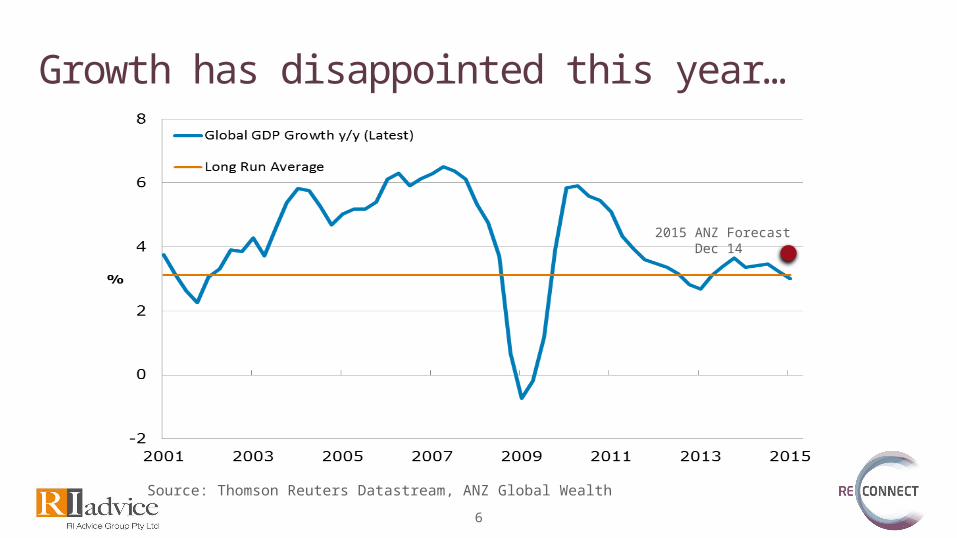

Growth has disappointed this year…

2015 ANZ Forecast Dec 14

Source: Thomson Reuters Datastream, ANZ Global Wealth

7

Weaker potential growth lower interest rates

DM avoids home grown deflation end to negative rates

Weak EM imparts a deflationary shock lower rates, commodities, resources stock and AUD

Bottom line: Interest rates to remain low

Implications

8

China – slowdown you move to fast

Source: Bloomberg, ANZ Global Wealth

9

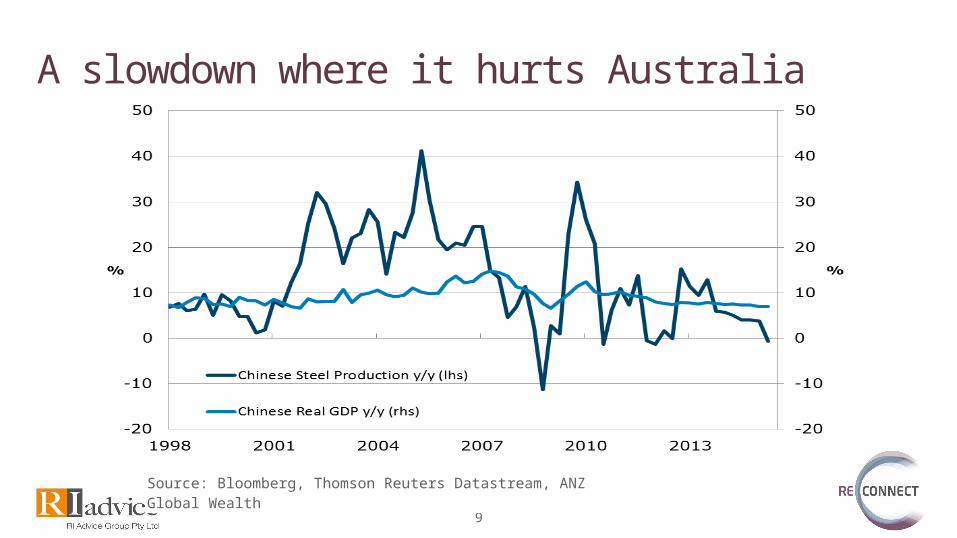

A slowdown where it hurts Australia

Source: Bloomberg, Thomson Reuters Datastream, ANZ Global Wealth

10

It’s not all bad news, just different

Source: China National Bureau of Statistics, ANZ Global Wealth

11

The economy may be slower than GDP suggests

Source: China National Bureau of Statistics, ANZ Global Wealth

12

Where will it end?

Source: Thomson Reuters Datastream, ANZ Global Wealth

13

Where will it end?

Source: Thomson Reuters Datastream, ANZ Global Wealth

?

14

As China’s nominal growth collapses…

Source: Thomson Reuters Datastream, ANZ Global Wealth

15

As China’s nominal growth collapses…

Source: Thomson Reuters Datastream, ANZ Global Wealth

16

A capex cliff looms

Source: Australian Bureau of Statistics, ANZ Global Wealth

17

Housing is the only source of growth

-3.0% -0.5% +0.5%

Source: Australian Bureau of Statistics, ANZ Global Wealth

18

AUD remains under pressure

Source: Bloomberg, Thomson Reuters Datastream, ANZ Global Wealth

19

China not growing how it used to lower commodity prices

Australian capex cliff sub trend growth and lower rates

A$ under pressure

Implications

20

Equities – home, away or just stay away?

Source: Bloomberg, ANZ Global Wealth

21

It’s all to do with earnings

Source: Bloomberg, ANZ Global Wealth

22

Current versus “mid cycle” earnings

Source: Bloomberg, ANZ Global Wealth

23

Equities – reasonable value

Source: Thomson Reuters Datastream, ANZ Global Wealth

24

Home or away?

3.8

3.9

4.0

4.1

4.2

4.3

4.4

4.5

4.6

4.7

4.8

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1970 1974 1978 1982 1986 1990 1994 1998 2002 2006 2010 2014

Australia's Terms of Trade and Equity Performance

Relative Performance (LHS) Terms of Trade (RHS)

Source: Thomson Reuters Datastream, ANZ Global Wealth

25

Equities – no longer cheap, but not really expensive

Earnings growth likely issue for Australia and EM

Falling terms of trade favours DM over Australia

Implications

26

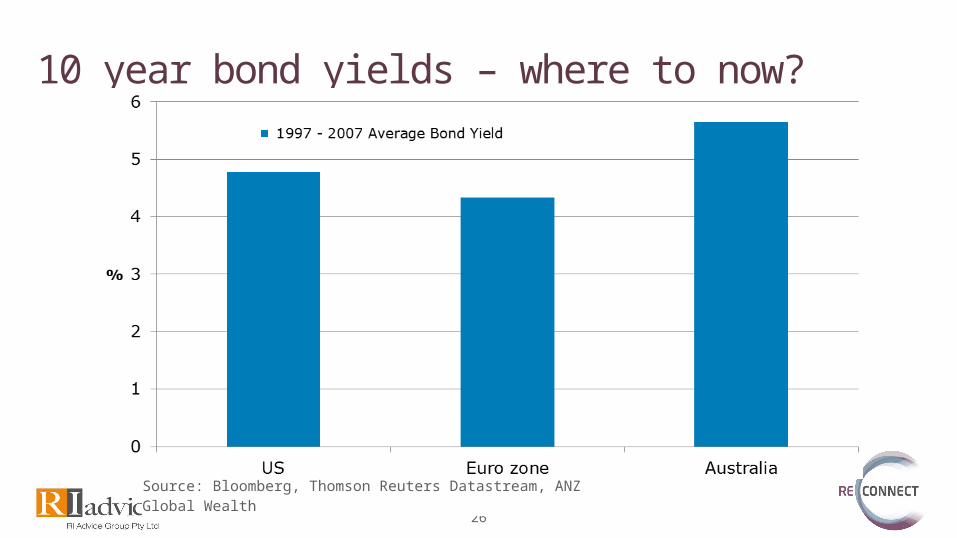

10 year bond yields – where to now?

Source: Bloomberg, Thomson Reuters Datastream, ANZ Global Wealth

27

10 year bond yields – where to now?

Source: Bloomberg, Thomson Reuters Datastream, ANZ Global Wealth

28

10 year bond yields – where to now?

Source: Bloomberg, Thomson Reuters Datastream, ANZ Global Wealth

29

10 year bond yields – where to now?

Source: Bloomberg, Thomson Reuters Datastream, ANZ Global Wealth

30

Lower expected returns in prospect

Source: Mercer, Bloomberg, ANZ Global Wealth

31

Forces continue for low interest rates but now poor returns

Equity valuations okay, but earnings growth the issue

Prospective returns have moderated

Tactically cautious

Conclusions

32

This information is issued by the Australia and New Zealand Banking Group Limited (ABN 11 005 357 522, AFSL 234 527). The information is current as at 20 August 2015 and will be subject to change.

The information is of a general nature and has been prepared without taking account of your or your clients personal needs, financial circumstances or objectives. It is intended for informational purposes only.

Whilst every effort has been taken to ensure the information used is accurate and reliable, no warranty is given as to the accuracy of the information and no liability is accepted for your reliance on the information.

The views expressed are those of the presenters based on their interpretation of current market conditions and data.

Statements made during the presentation do not and are not intended to represent financial advice or a recommendation to hold, acquire or dispose of any investment.

Before acting on this information you should consider whether the information is appropriate having regard to your or your clients personal needs, financial circumstances or objectives. Investors should always read the Product Disclosure Statement for the relevant product and seek financial advice before making an investment decision.

Before making any investment decision you need to consider whether there are any adverse consequences for you or your clients, including exit fees, other loss of benefits or increase in investment risks. Past performance is not indicative of future performance.

Any investment is subject to investment risk, including possible repayment delays and loss of income and principal invested. Before making any investment decision you need to consider whether there are any adverse consequences for you or your clients, including exit fees, other loss of benefits or increase in investment risks.

ANZ's colour blue is a trademark of ANZ.

Disclaimer

Related Documents