Economic Adviser's Wing Finance Division, Ministry of Finance Government of the People's Republic of Bangladesh June 2003 BANGLADESH ECONOMIC REVIEW 2003

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Economic Adviser's Wing Finance Division, Ministry of Finance

Government of the People's Republic of Bangladesh June 2003

BANGLADESH ECONOMIC REVIEW

2003

PREFACE Bangladesh Economic Review 2003 is published as a regular annual publication of the Government. The Review reflecting the state of Bangladesh economy and its current trend, is placed before the Jatiya Sangsad (Parliament) during its Budget Session every year. 2. The present Government had to undertake the responsibility of steering a fragile and unstable economy caused by gross economic mismanagement of the past regime. The macroeconomic situation of the country was further aggravated due to the negative impact of 9/11 coupled with the then global economic recession. Against these stark realities, the new Government faced the formidable challenges of managing the economy with courage and sagacity. During the last one and a half year, the Government achieved commenable progress in implementing wide-ranging reforms and a set of emergency recovery programmes aimed at restoring macroeconomic stability. This resulted in restoration of macroeconomic stability at a satisfactory level. In the Bangladesh Development Forum meeting held in Dhaka, the representatives of development partners put on record their highest appreciation of the impressive achievements made by the Government. 3. Poverty is an endemic problem in a developing country like Bangladesh. Although there has been sustained progress in achieving growth and poverty reduction, which can be attributed to the wide ranging reforms introduced and implemented in the early nineties, the depth and dimension of poverty is still a continuing challenge. Against these imperatives, the Government has finalised the draft of a three-year 'National Strategy for Economic Growth, Poverty Reduction and Social Development' through extensive consultation with the concerned stakeholders. In the light of this strategy, a 'Three-year Rolling Investment Programme' is being formulated. 4. The data presented in the Review facilitate analysis of the fundamentals of the overall economy. The Review has made assessments of vital issues of macro economy and also shed light on important sectors of the economy. In tandem with this, other important priority sectors like human resource development, poverty reduction and private sector development have been reviewed as well. To provide a wider understanding of the progress made by Bangladesh, comparisons with regional and international economic situations on selected areas have been presented. 5. We appreciate the cooperation extended by the Ministries/Divisions/Agencies in preparation of this Review by providing latest valuable data and information. We shall feel our endeavors amply rewarded if the information presented in the Review serve the purpose of enthusiastic readers, researchers, academics, students and stakeholder organisations. I thank the officers and staff of the Economic Adviser's Wing who worked relentlessly in preparation of this document. (M. Saifur Rahman) Minister for Finance & Planning

INTRODUCTION ''Bangladesh Economic Review'' is published as a vital document with basic information of the macroeconomic situation of the country covering current and previous fiscal years. This document, presented before the Parliament as background information of the Budget, reflects the status of socio-economic progress of the country. The prime objective of the document, however, is to present and review data/statistics that facilitate analysis of the macroeconomic trends of the country. In the English version of the Review, most of the data/statistics have been updated up to June 2003 based on their availabity. These have been duly reflected in the text where relevant. 2. Bangladesh Economic Review 2003 contains fourteen chapters. Chapter One presents a brief review of the macroeconomic situation of the country and the development strategies pursued by the Government. An assessment of the country's macroeconomic fundamentals like Gross Domestic Product, Savings and Investments, Price, Wage and Employment, Fiscal Policy and Fiscal Management, Monetary Policy and Monetary Management and External Sector is incorporated in Chapters Two to Six. In the Sector-specific chapters (chapters Seven to Twelve) developments in major sectors of the economy like agriculture, industry, power and energy, transport and communication and human resource development have been discussed. Chapters Thirteen and Fourteen pertains to the analysis on the Thrust Sectors and present a brief account of the initiatives of the government towards poverty reduction and private sector development respectively. Coloured charts, graphs, statistical tables and boxes, where relevant, have been used for further enrichment of the analysis. 3. The overall responsibility of preparing this document rests with the Economic Adviser's Wing of the Finance Division. I would like to thank the officers and staff of the Wing who performed their duties with deep devotion in publishing this document. I congratulate the relevant Ministries/Divisions/Agencies, which extended cooperation in preparation of this document by providing useful information. 4. The Review has been prepared amidst a range of constraints that may have caused some errors and omissions. To make this document more up-to-date and qualitatively rich, valuable suggestions from the inquisitive readers/researchers as well as the concerned Ministries/Divisions/Agencies will be gratefully acknowledged. (Zakir Ahmed Khan) Secretary Finance Division

CONTENTS

Preface

Introduction

List of Tables

List of Graphs

List of Boxes

List of Statistical Appendices

Socio-Economic Indicators of Bangladesh

Macro Chapters

Chapter 1. Macroeconomic Review and Development Strategies 1-18

Chapter 2. GDP, Saving and Investment 19-25

Chapter 3. Prices, Wages and Employment 26-32

Chapter 4. Fiscal Policy and Fiscal Management 33-39

Chapter 5. Monetary Policy and Monetary Management 40-48

Chapter 6. Foreign Trade, Exchange Rate Management and External

Sector

49-60

Sectoral Chapters

Chapter 7. Agriculture 61-73

Chapter 8. Industry 74-86

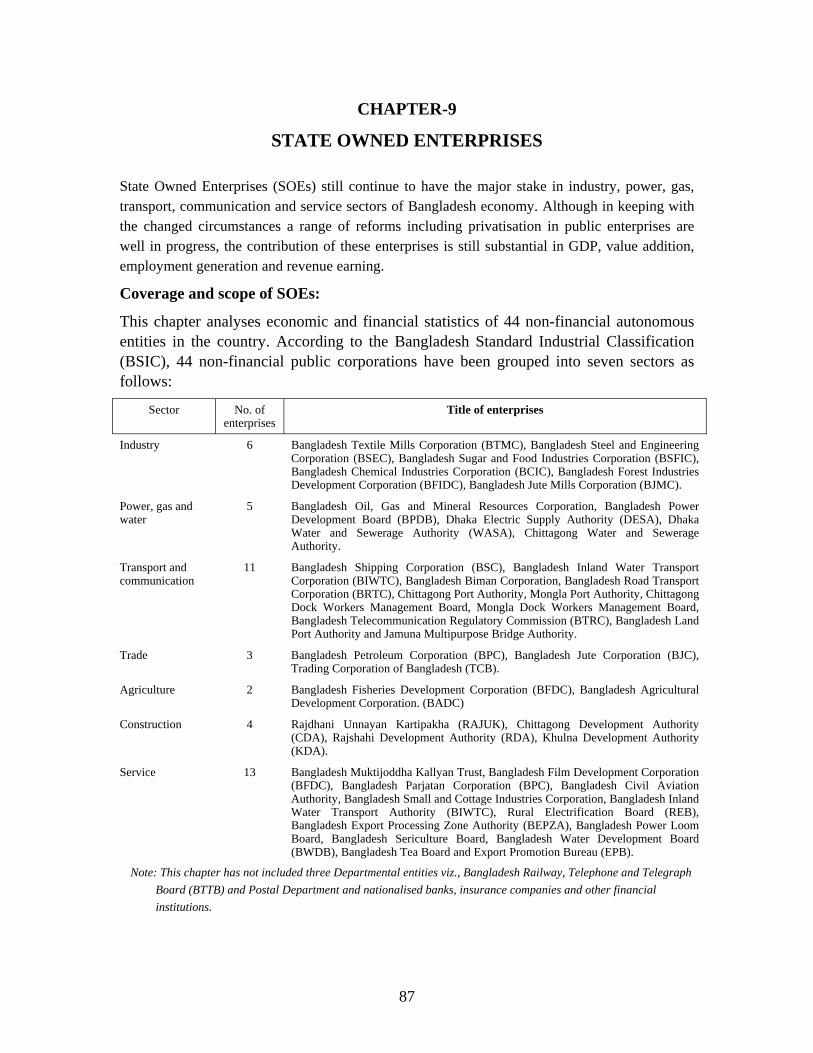

Chapter 9. State Owned Enterprises 87-89

Chapter 10. Power and Energy 90-107

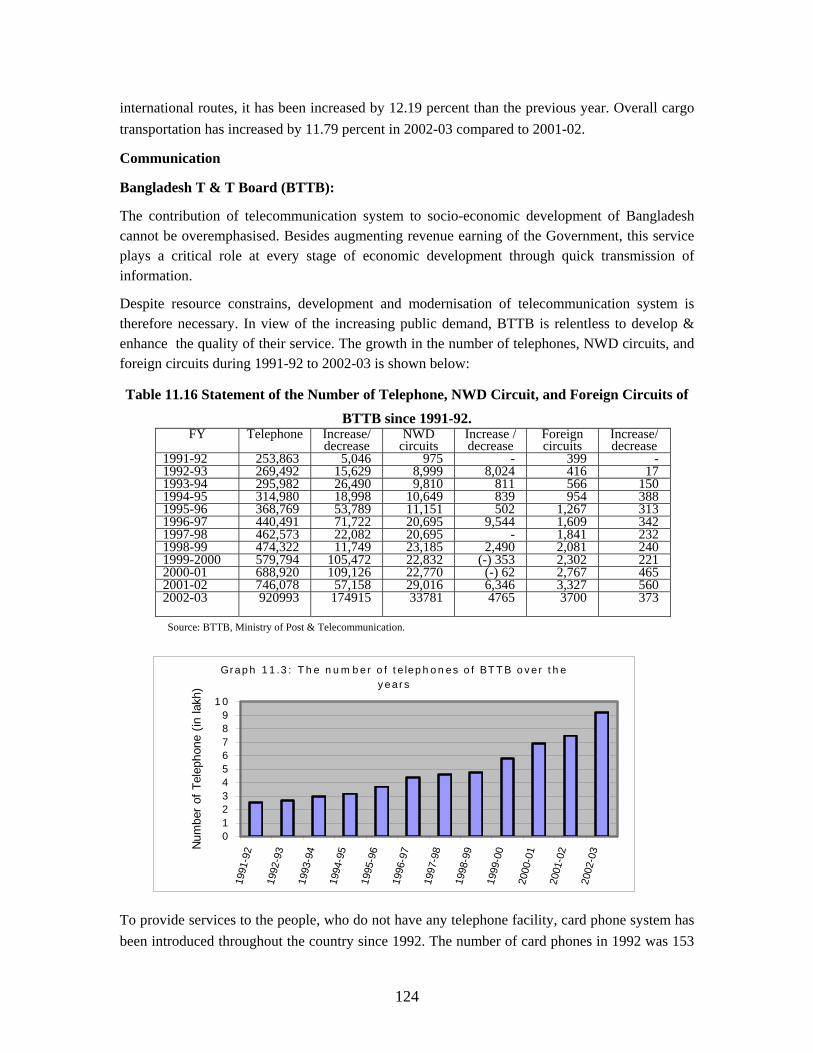

Chapter 11. Transport and Communication 108-128

Chapter 12. Human Resources Development

129-144

Thrust Area Chapters

Chapter 13. Poverty Alleviation 145-175

Chapter 14. Private Sector Development 176-190

vii

LIST OF TABLES Table Title Page

2.1 Per Capita GDP, GNI, NNI and National Savings and Investment (At

Market Prices)

19

2.2 Gross Domestic Product (GDP) at Current Prices 20

2.3 Sectoral Growth Rate of GDP at Constant Prices (Base: 1995-96) 21

2.4 Sectoral Share of GDP (%) at Constant Prices (1995-96) 22

2.5 Trends of Sectoral Contribution at Current Market Prices of Some Asian

Countries During the Last Two Decades.

23

2.6 Saving as Percentage of Gross Domestic Product (GDP) 24

2.7 Investment as Percentage of Gross Domestic Product (GDP) 25

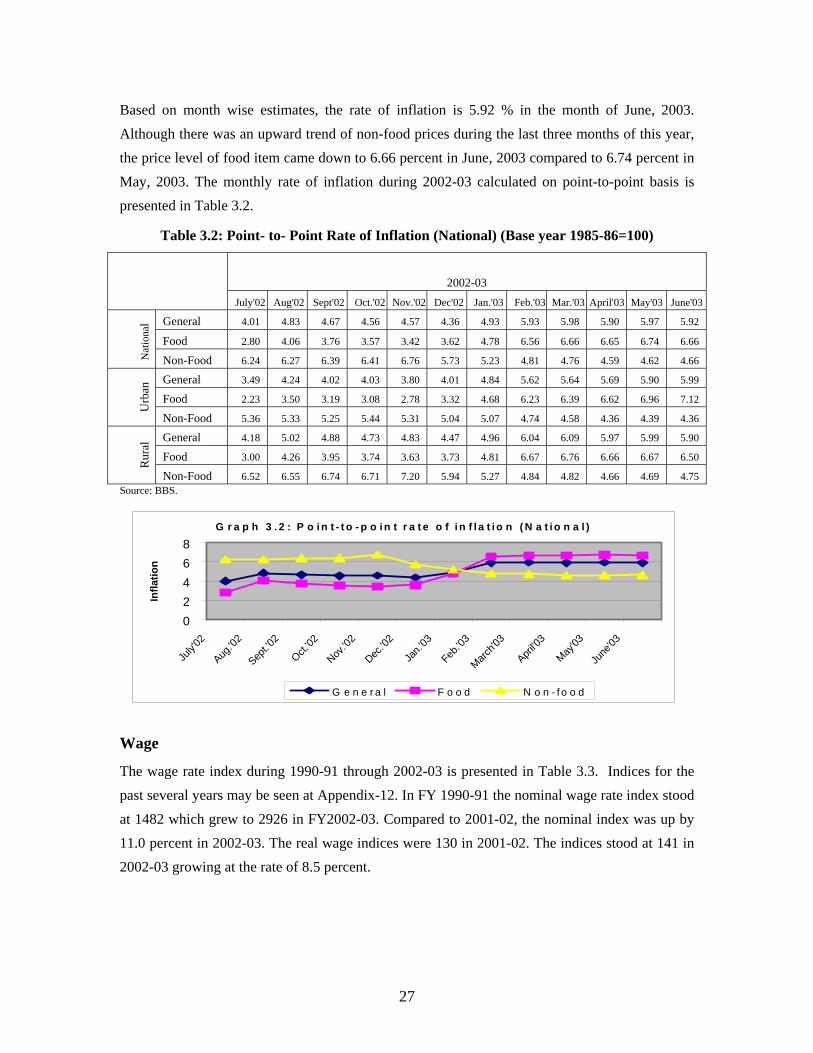

3.1 Consumer Price Index and Inflation (Base year 1985-86=100) 26

3.2 Point-to-Point Rate of Inflation (National) (Base year 1985-86=100) 27

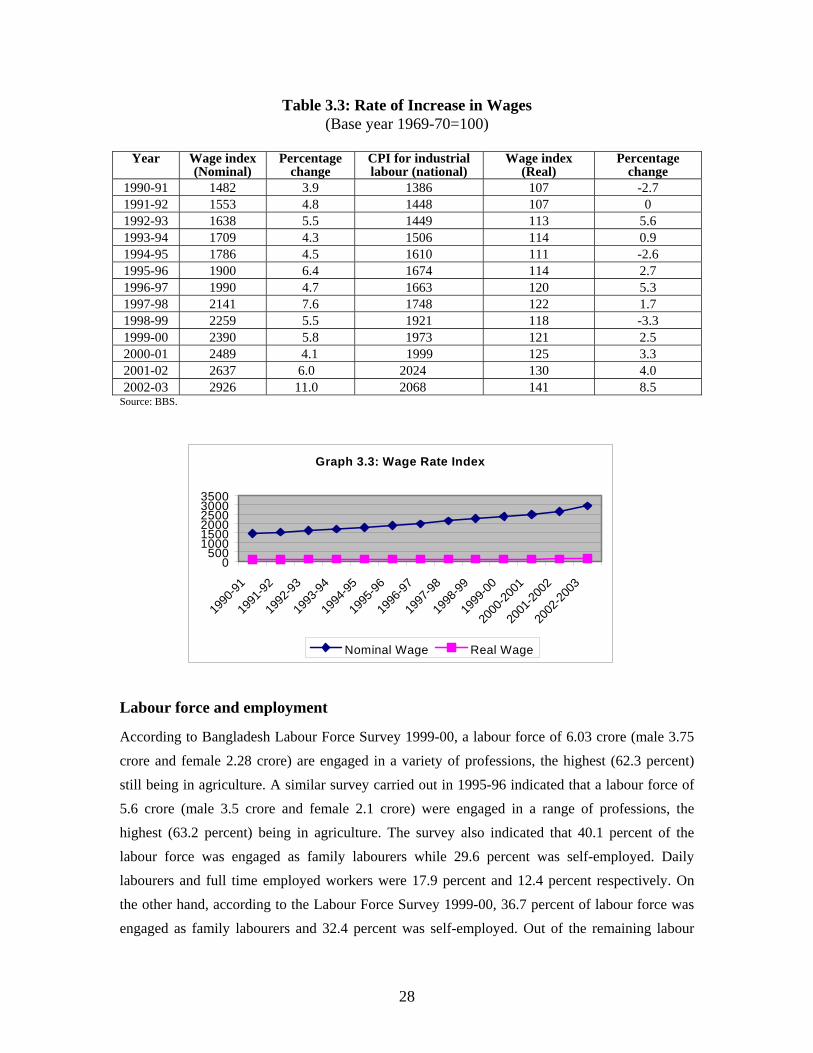

3.3 Rate of Increase in Wages (Base year 1969-70=100) 28

3.4 Share of Employed Labour Force by Sector 29

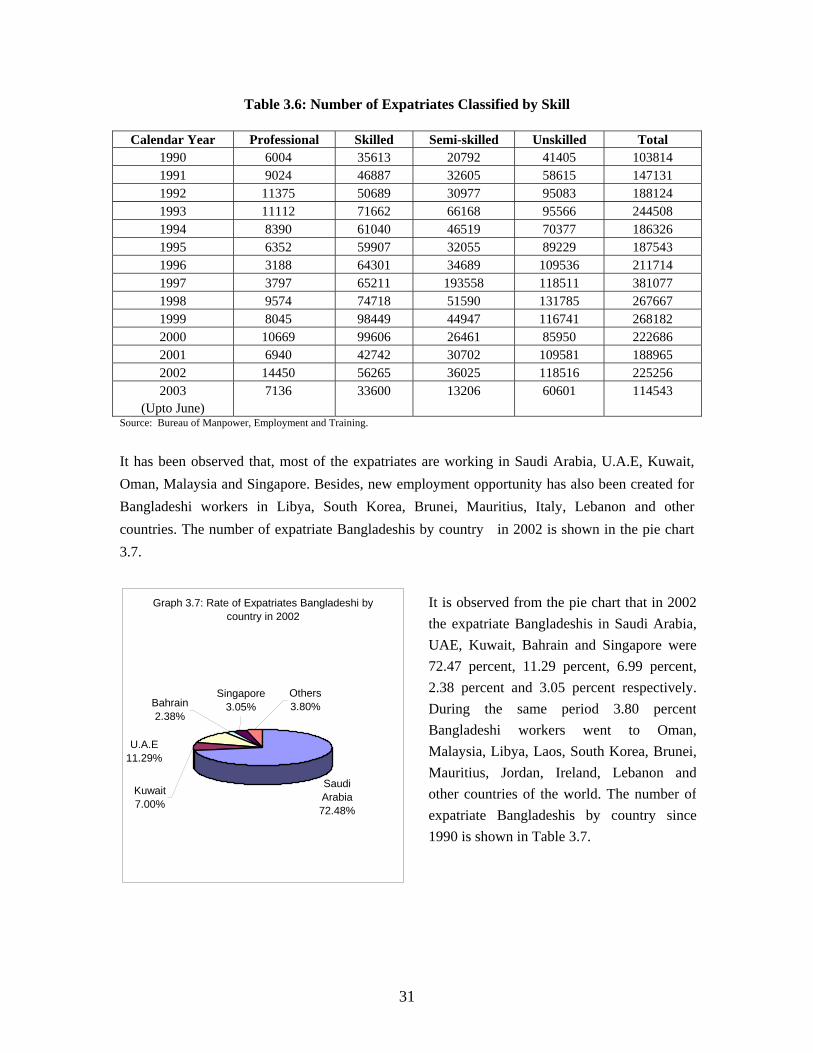

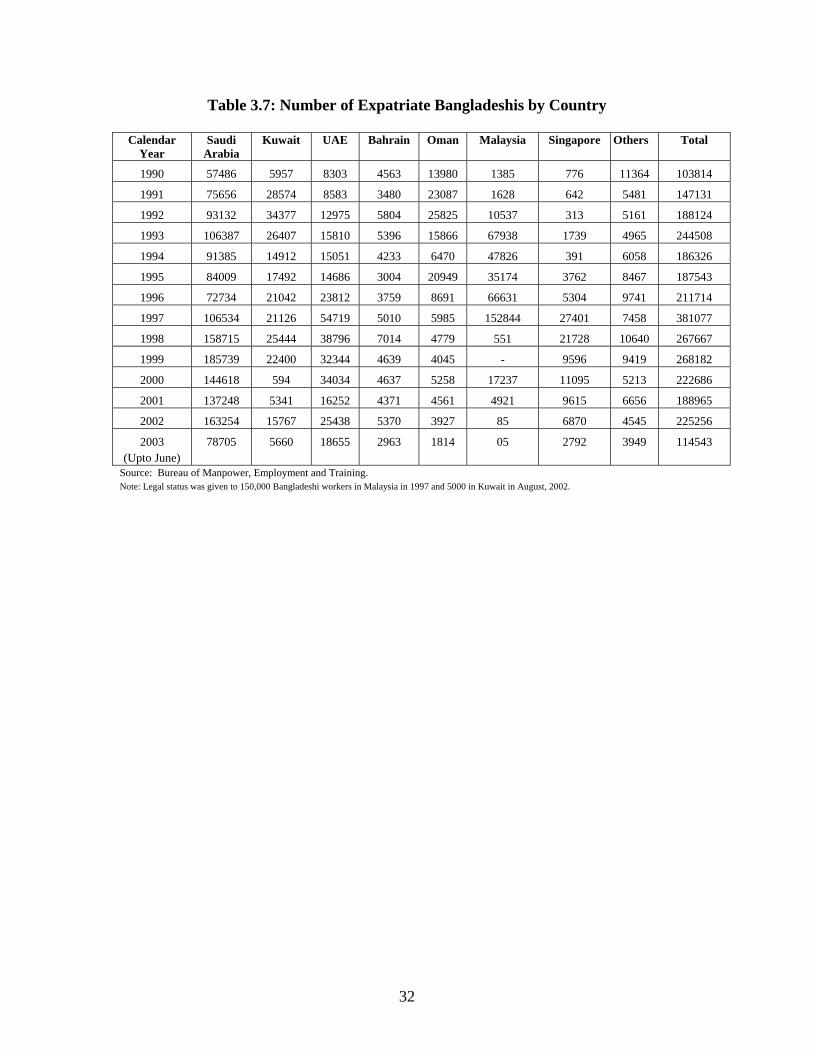

3.5 Number of Expatriate Bangladeshis and their Remittances 30

3.6 Number of Expatriates Classified by Skill 31

3.7 Number of Expatriate Bangladeshis by Country 32

4.1 Revenue Receipts 33

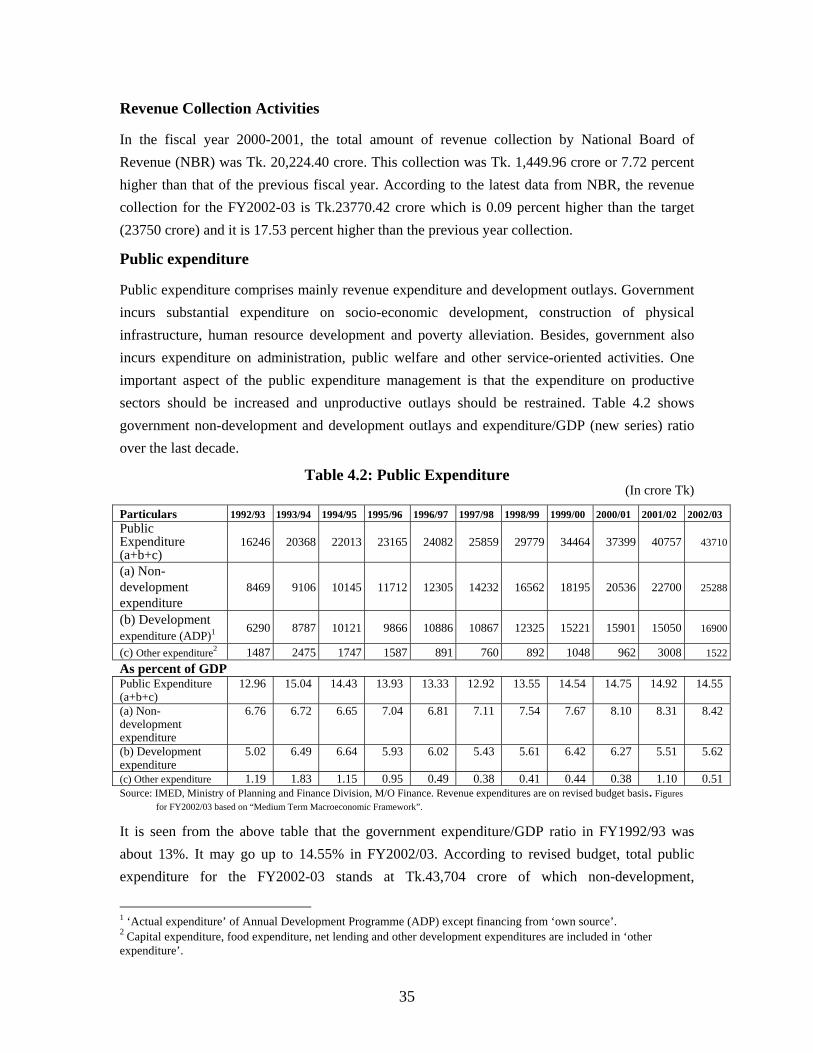

4.2 Public Expenditure 35

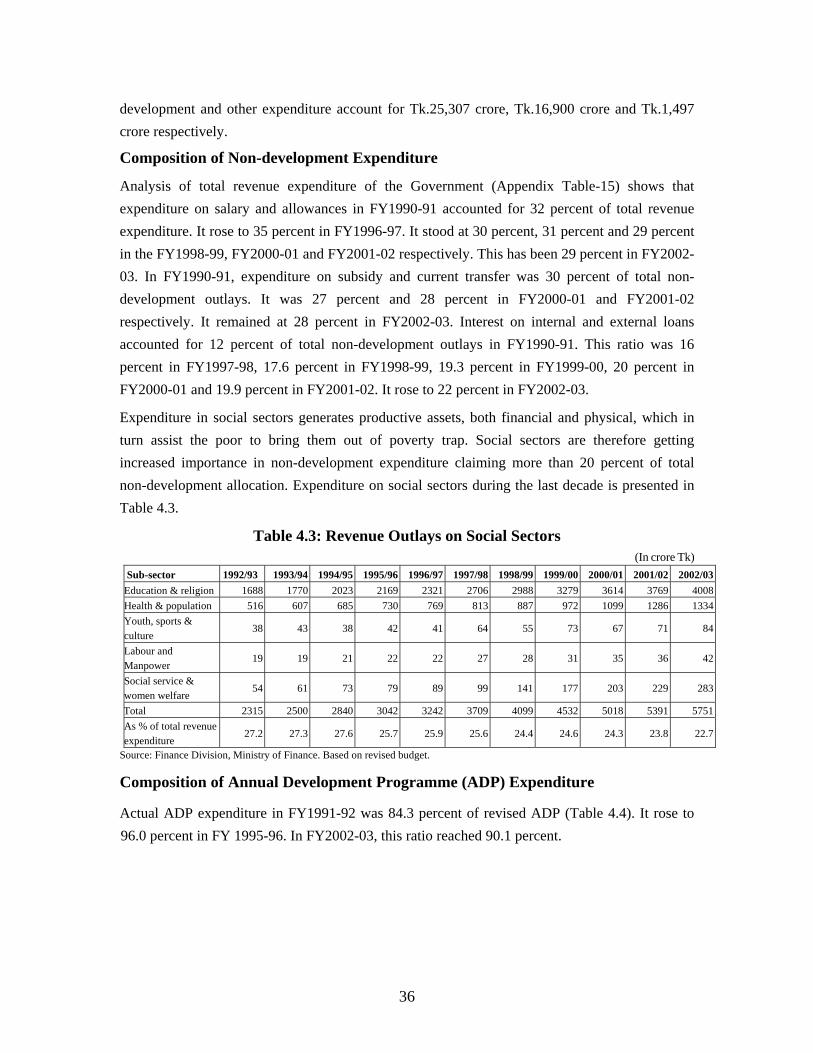

4.3 Revenue Outlays on Social Sectors 36

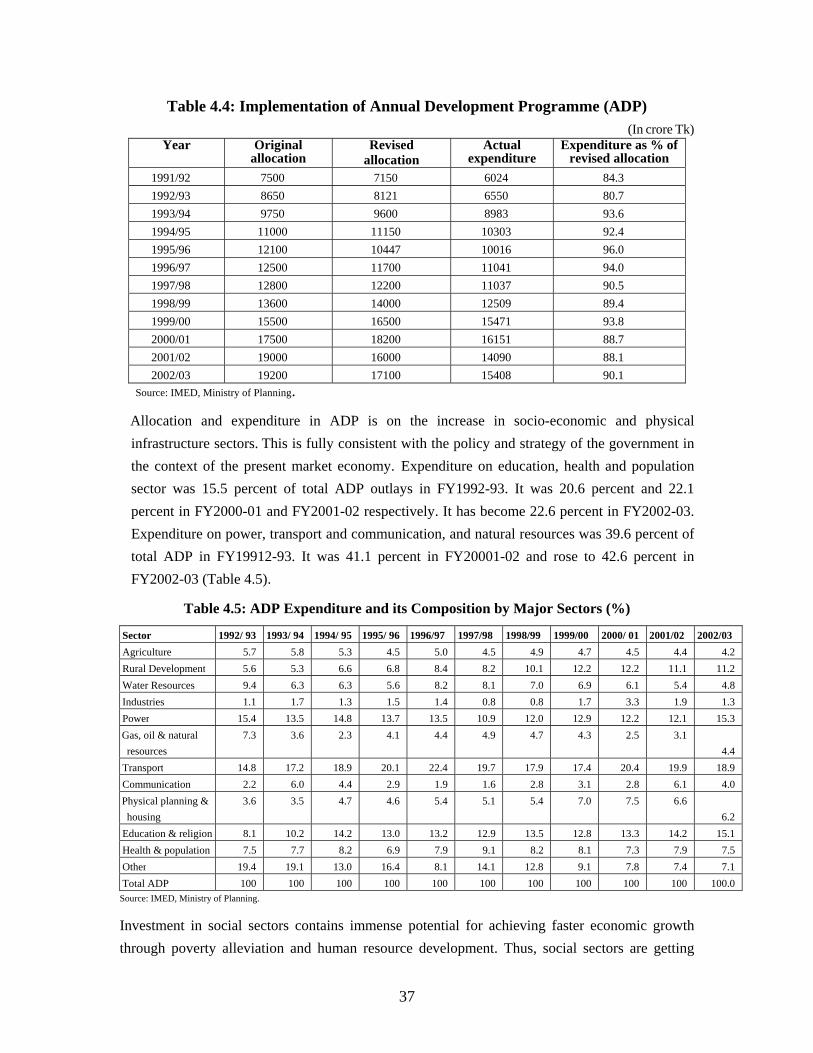

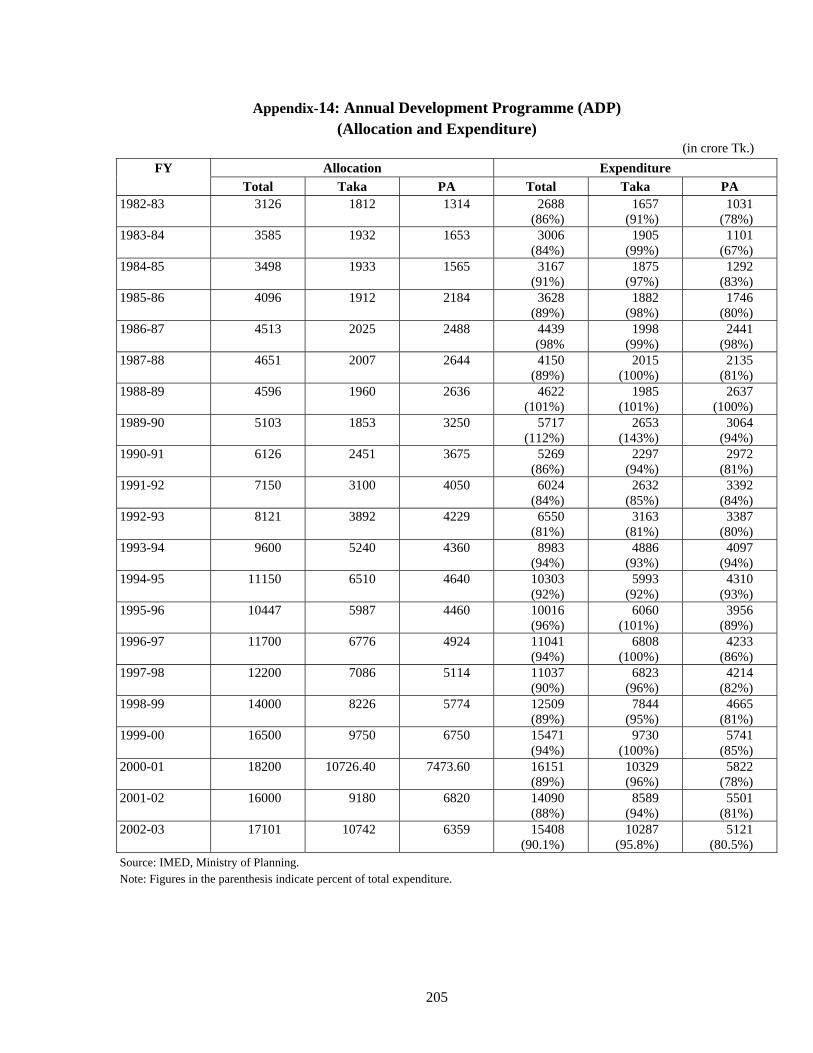

4.4 Implementation of Annual Development Programme (ADP) 37

4.5 ADP Expenditure and its Composition by Major Sectors (%) 37

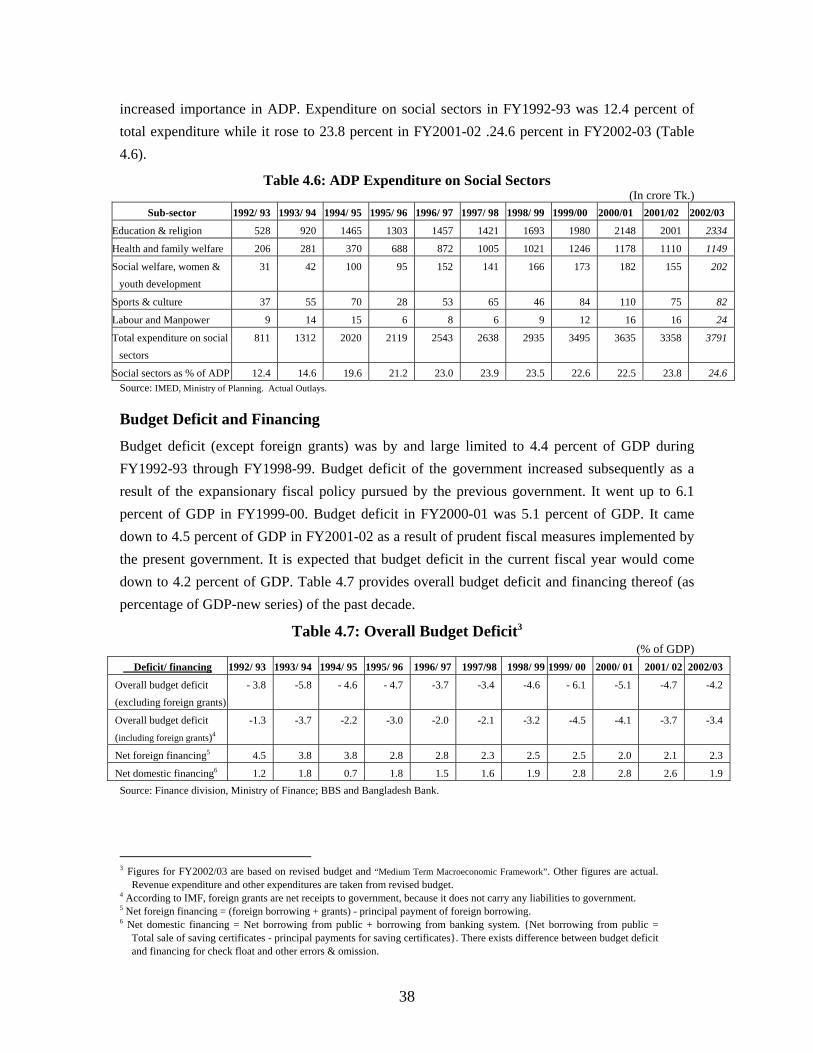

4.6 ADP Expenditure on Social Sectors 38

4.7 Overall Budget Deficit 38

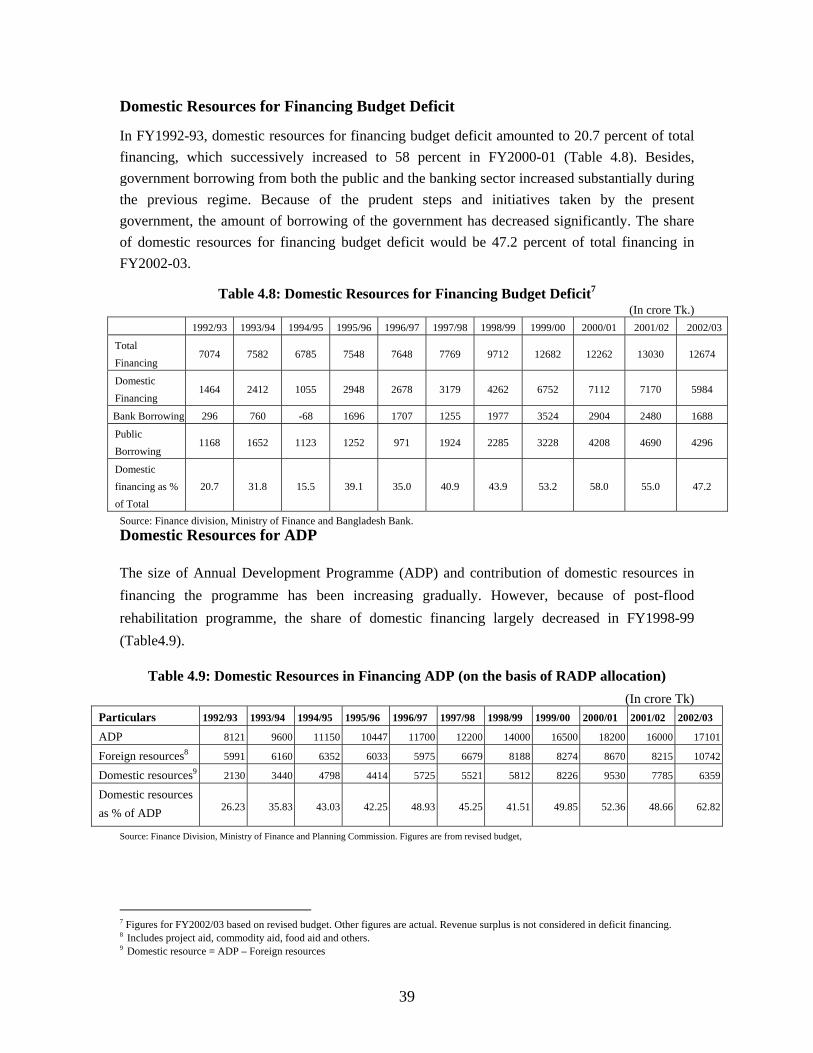

4.8 Domestic Resources for Financing Budget Deficit 39

4.9 Domestic Resources in Financing ADP (on the basis of RADP allocation) 39

5.1 Broad Money (M2) and Its Causative Factors 41

5.2 Reserve Money and Its Sources of Change 42

5.3 Summary of Trading Operations of Dhaka Stock Exchange 46

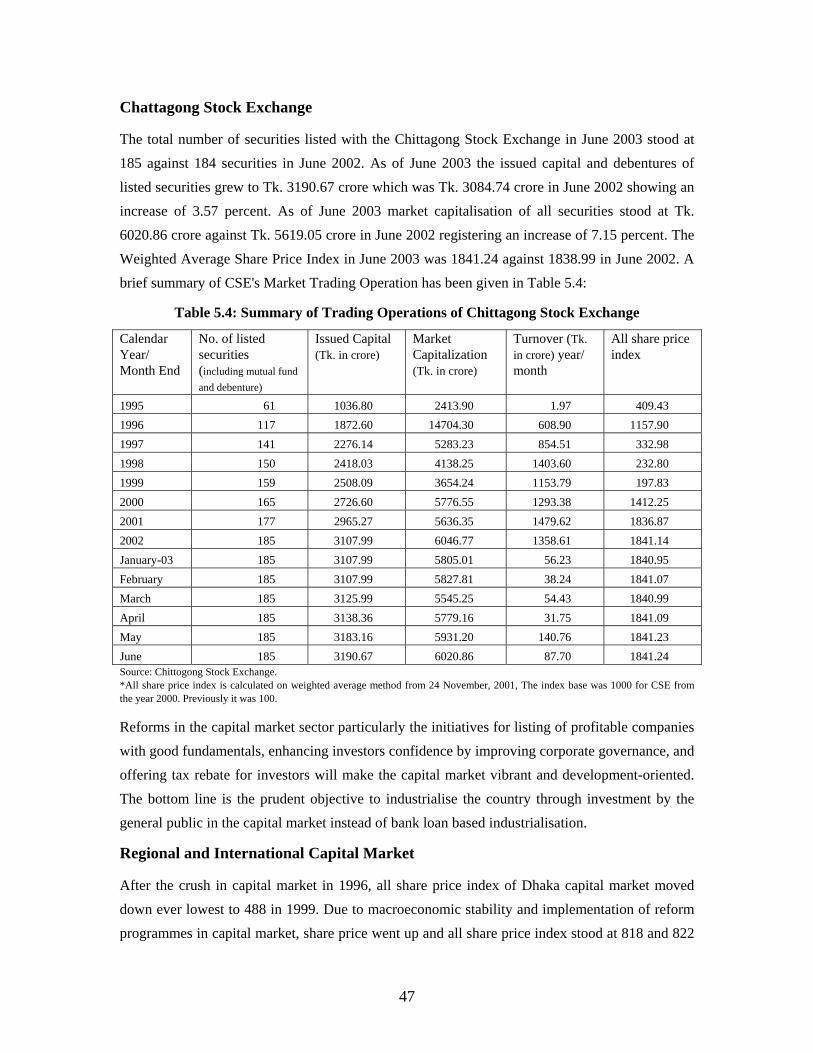

5.4 Summary of Trading Operations of Chittagong Stock Exchange 47

5.5 Important Regional and International Share Price Indices 48

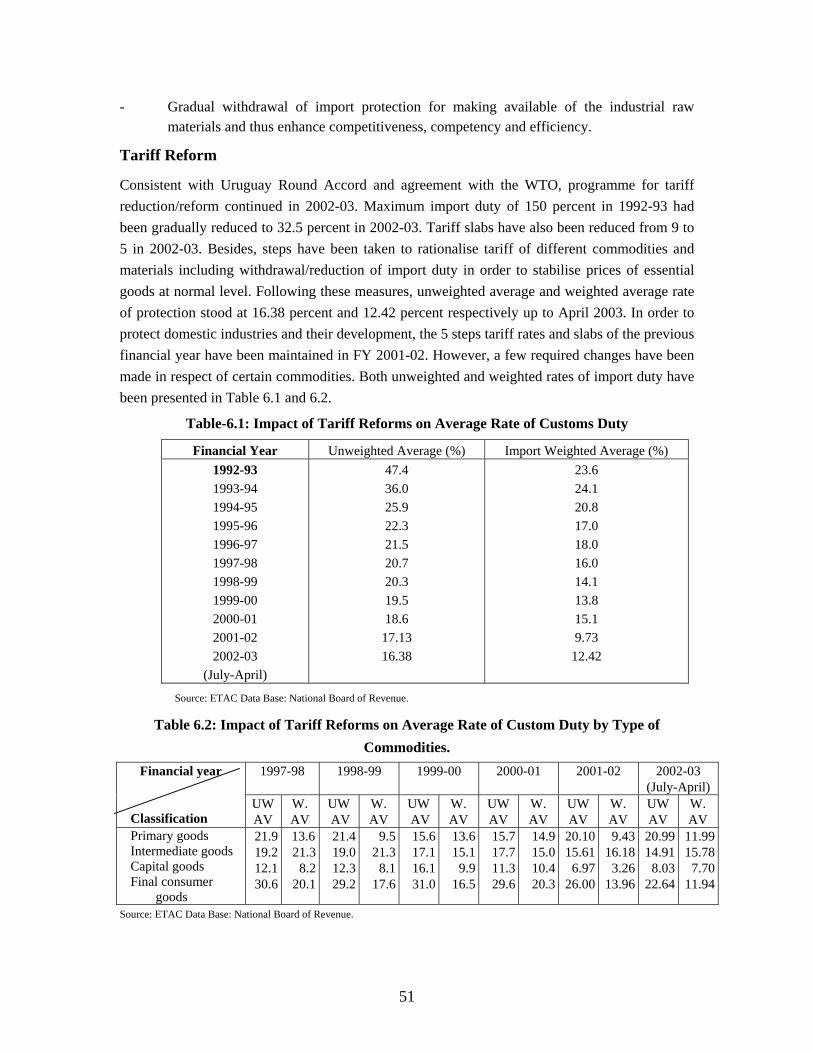

6.1 Impact of Tariff Reforms on Average Rate of Customs Duty 51

6.2 Impact of Tariff Reforms on Average Rate of Customs Duty by Type of Commodities

51

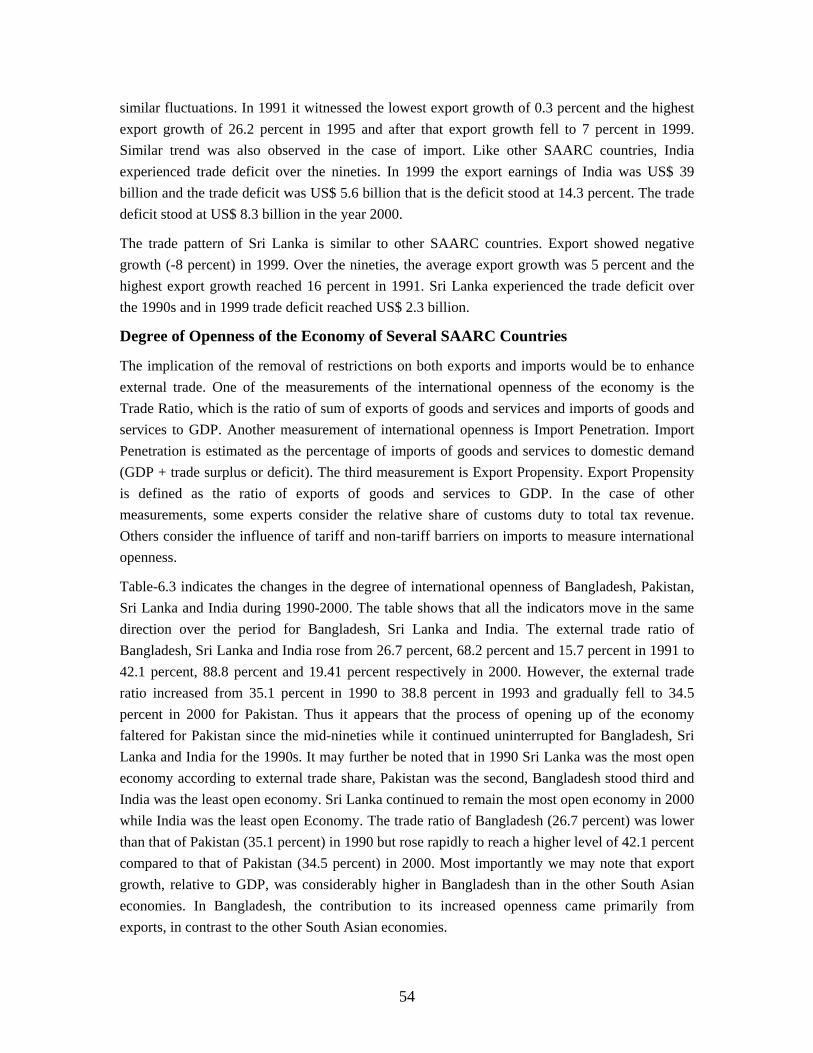

6.3 Degree of International Openness for Bangladesh, Pakistan, Sri Lanka

and India.

55

6.4 Average Exchange Rate (Taka per US$) 56

6.5 Foreign Exchange Reserves 56

viii

Table Title Page

6.6 Import Growth and Composition 57

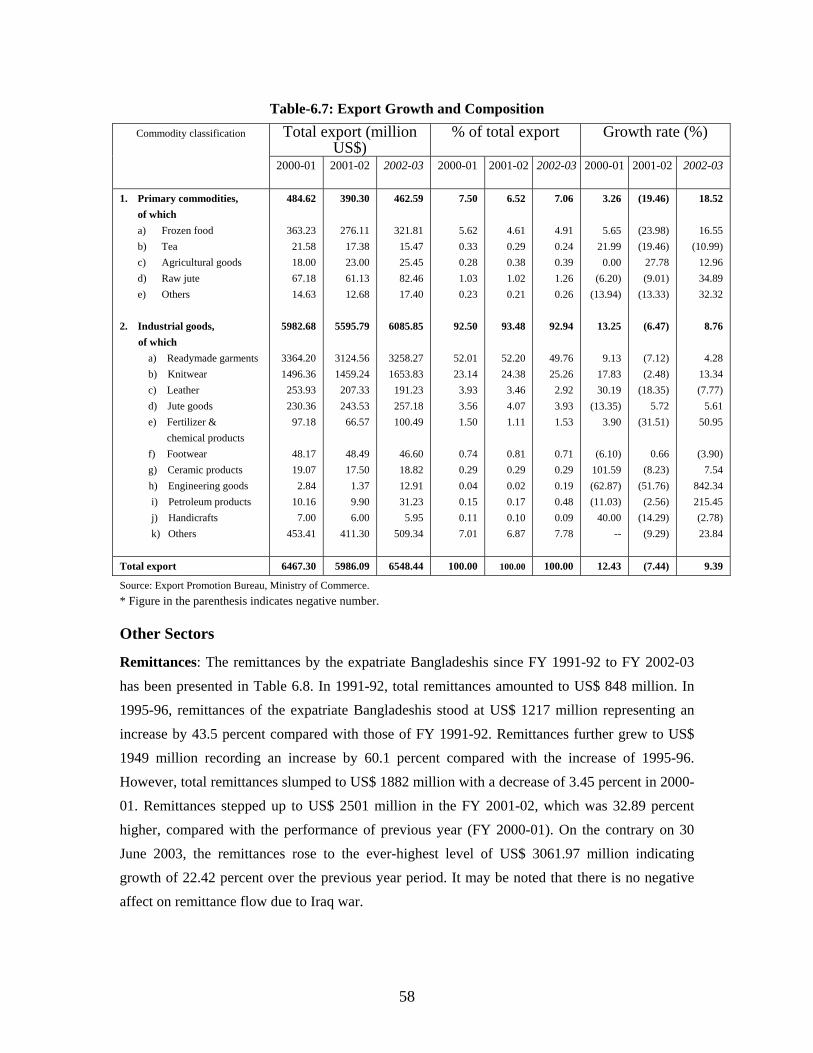

6.7 Export Growth and Composition 58

6.8 Annual Amount of Remittances 59

6.9 Balance of Payments 60

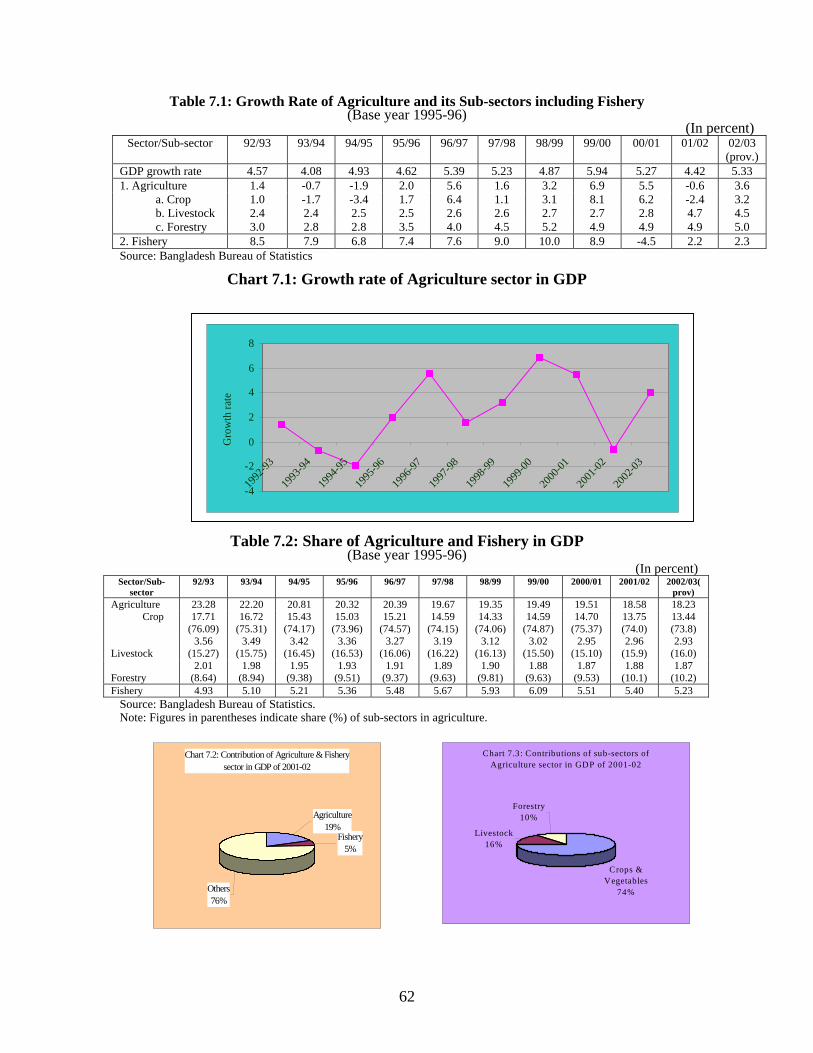

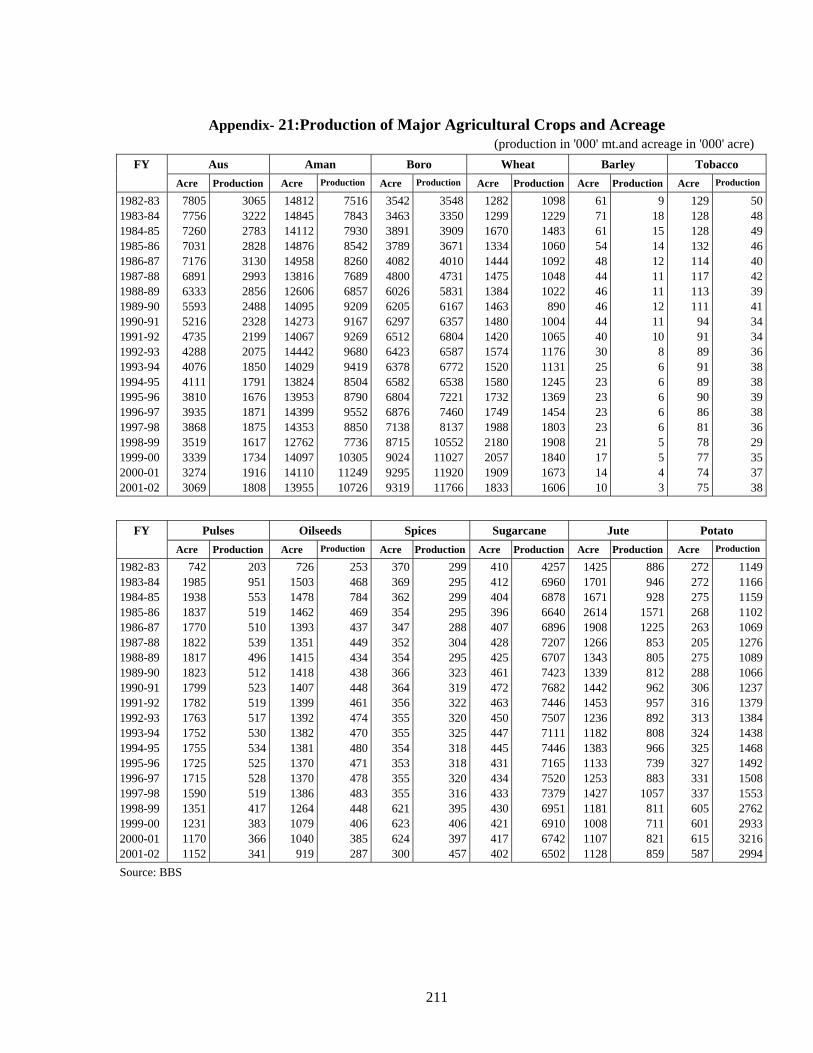

7.1 Growth Rate of Agriculture and its Sub-sectors including Fishery (Base year 1995-96)

62

7.2 Share of Agriculture and Fishery in GDP (Base year 1995-96) 62

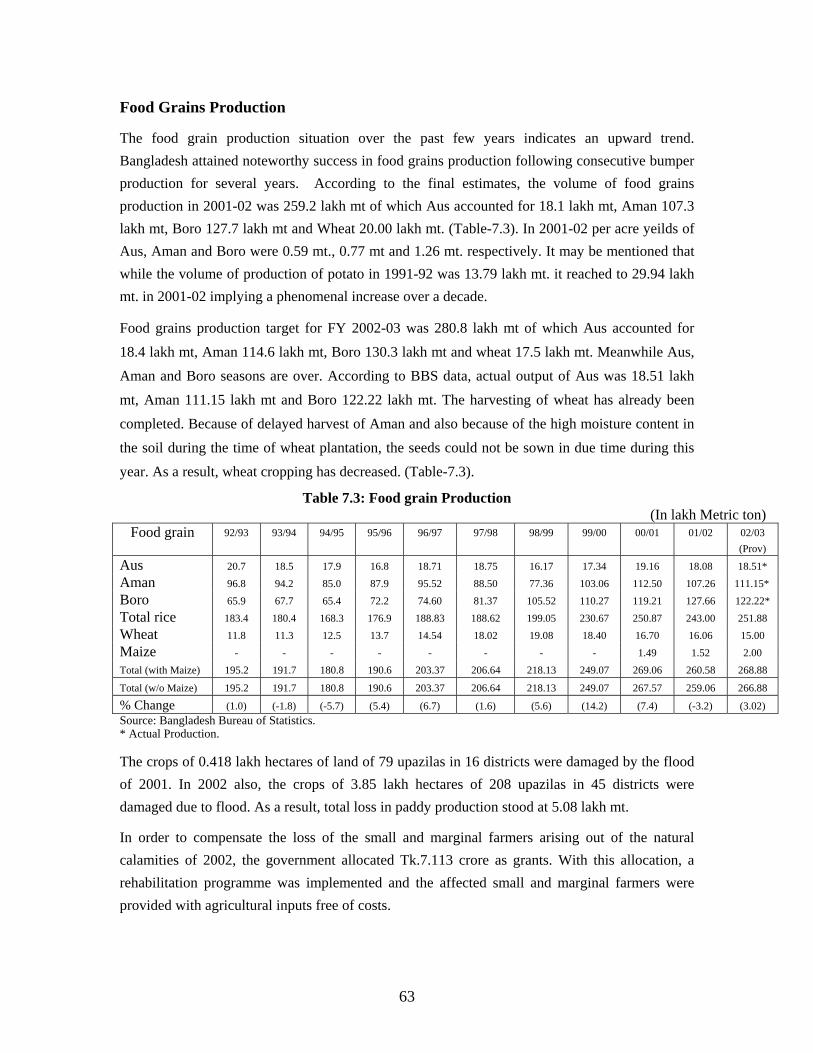

7.3 Food Grain Production 63

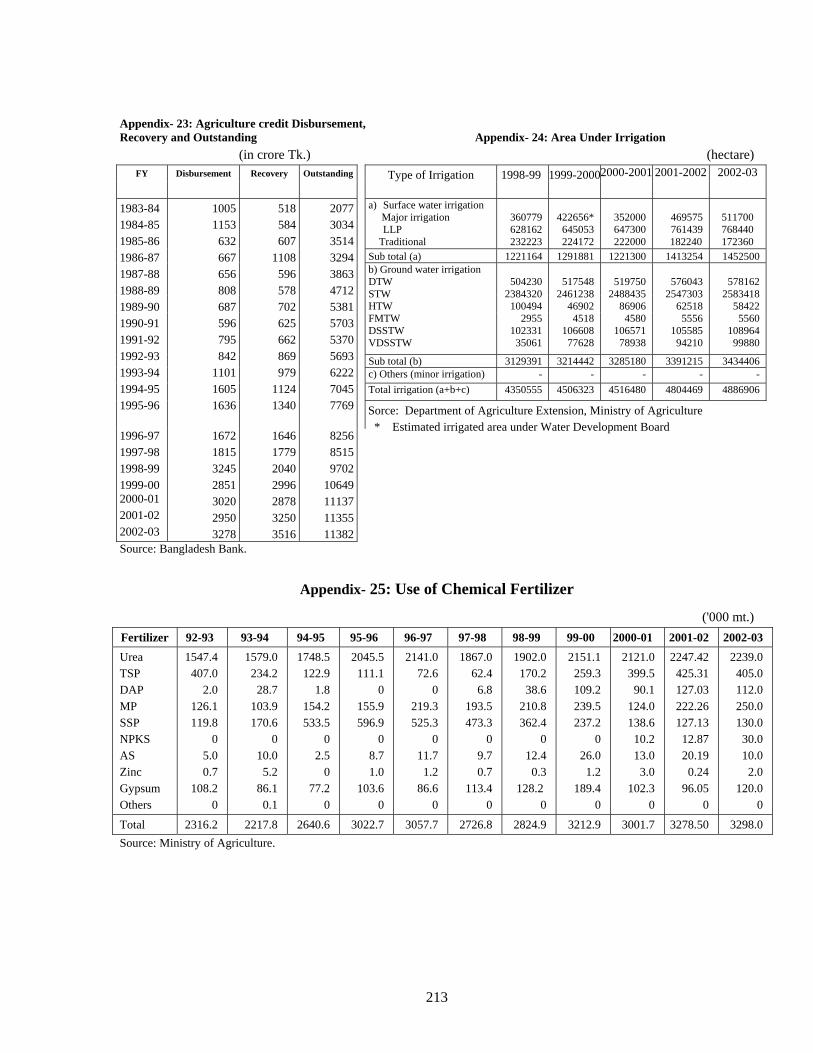

7.4 Area Under Irrigation 66

7.5 Uses of Chemical Fertilizer 67

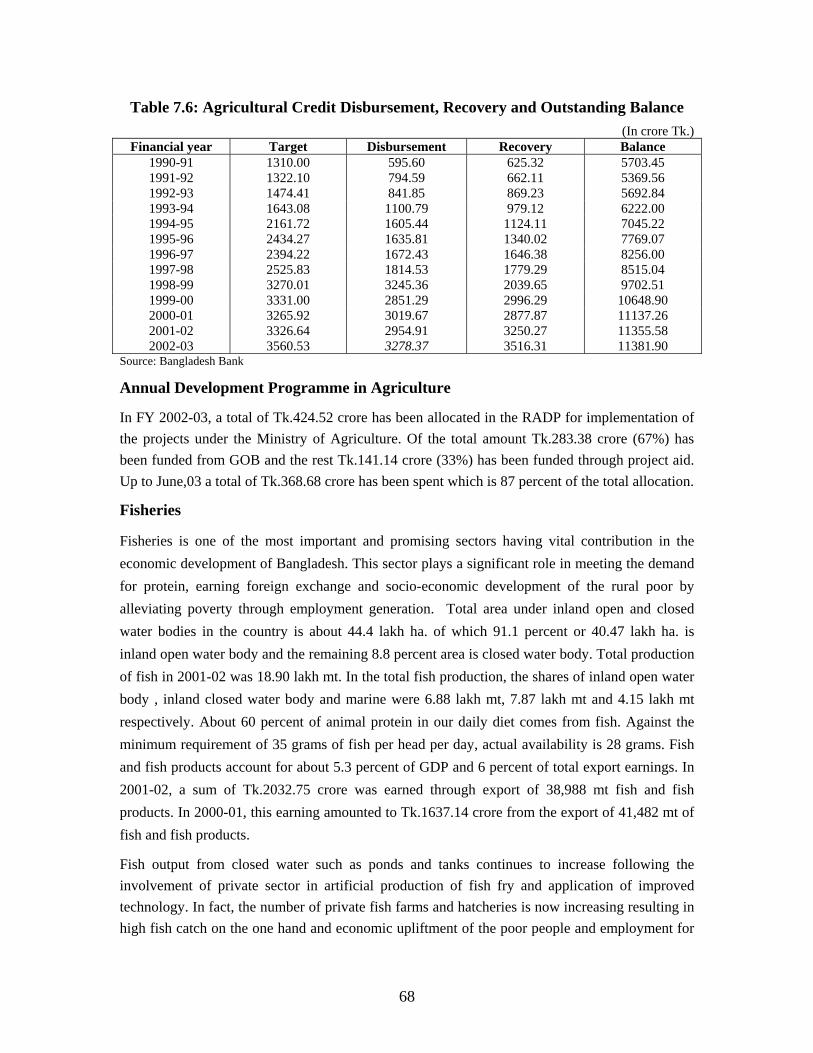

7.6 Agricultural Credit Disbursement, Recovery and Outstanding Balance 68

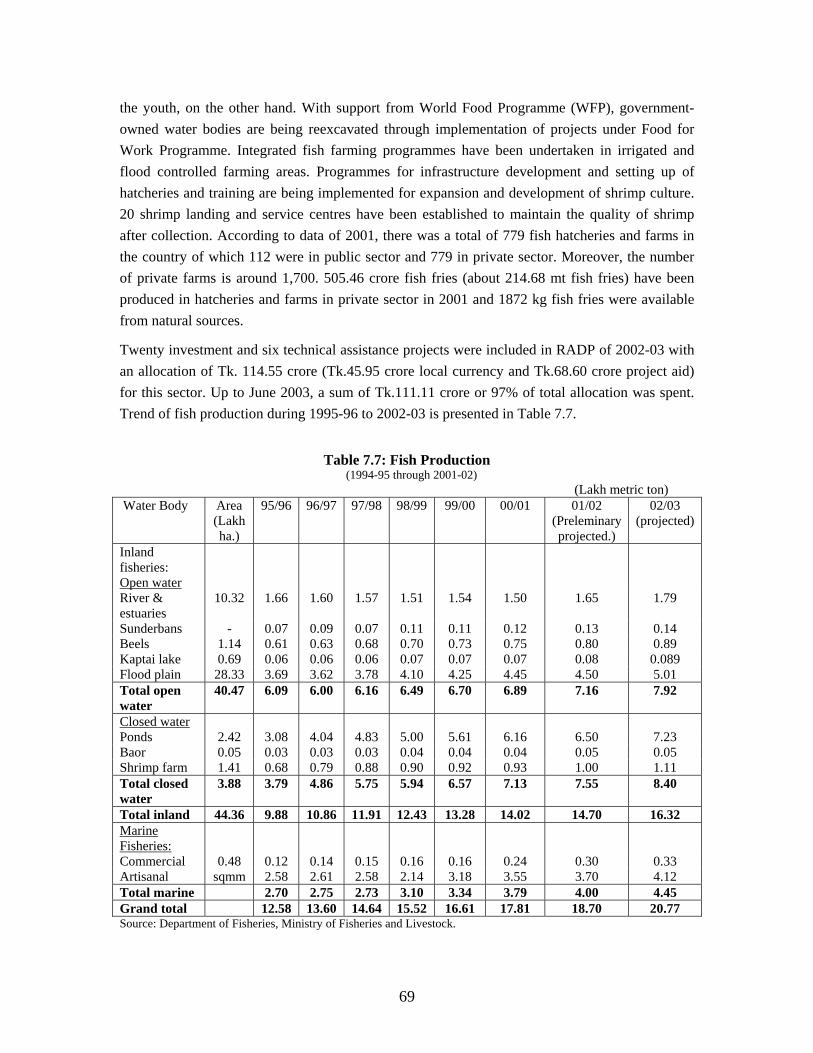

7.7 Fish Production (1994-95 through 2001-02) 69

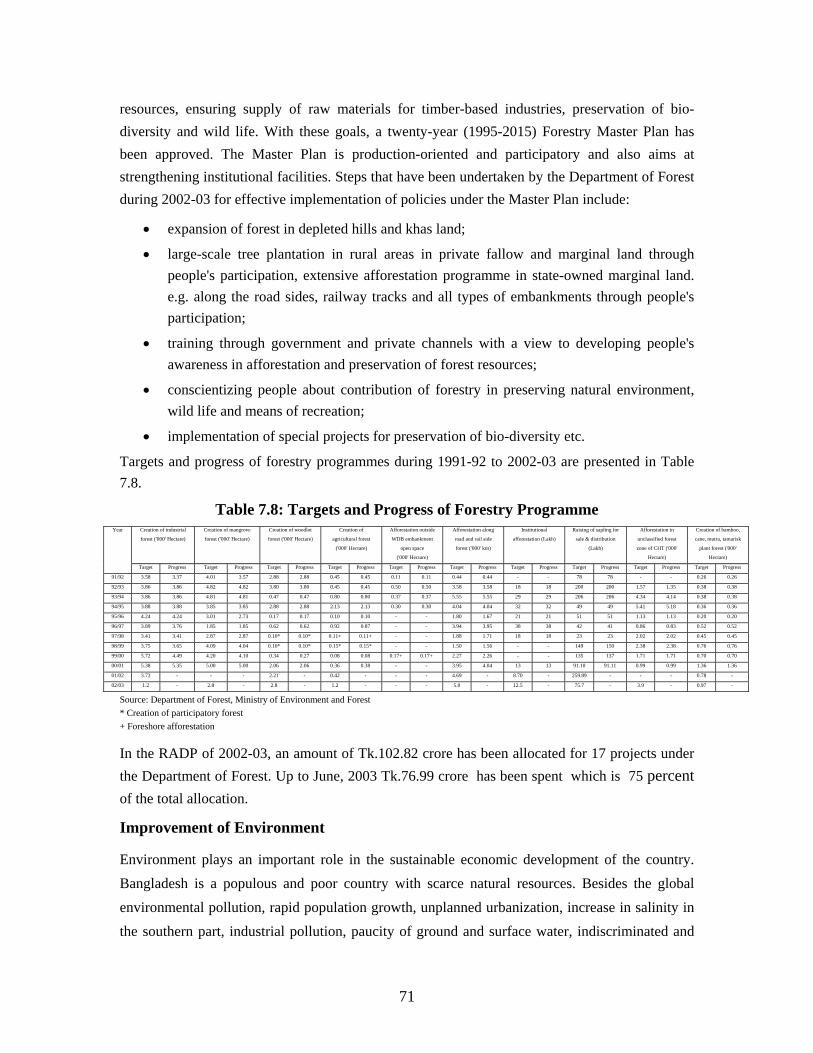

7.8 Targets and Progress of Forestry Programme 71

8.1 Contribution of Manufacturing Sector in GDP and Growth Rate (at constant prices of 1995-96)

74

8.2 Quantum Index of Production for Medium to Large-scale Industries (1988-89=100)

75

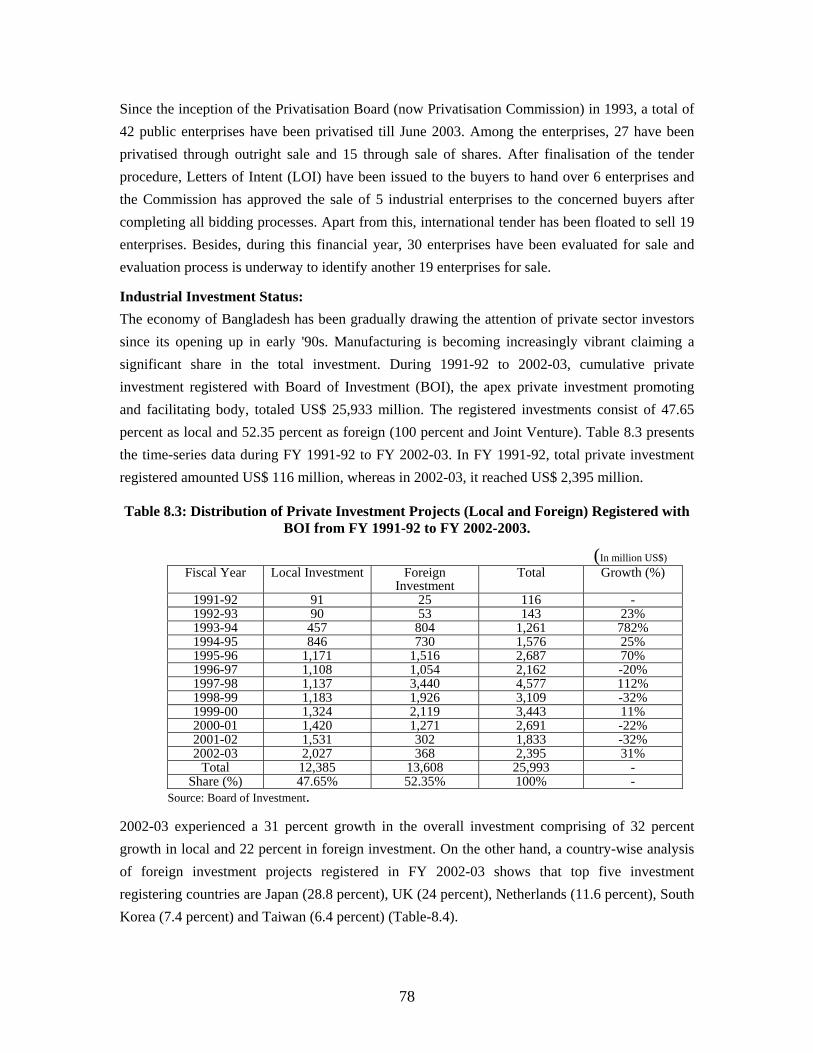

8.3 Distribution of Private Investment Projects (Local and Foreign) Registered with the BOI from FY1991-92 to FY2002-03.

78

8.4 Country-wise Distribution of Foreign Private Investment Registered with BOI from FY1996-97 to FY2002-03.

79

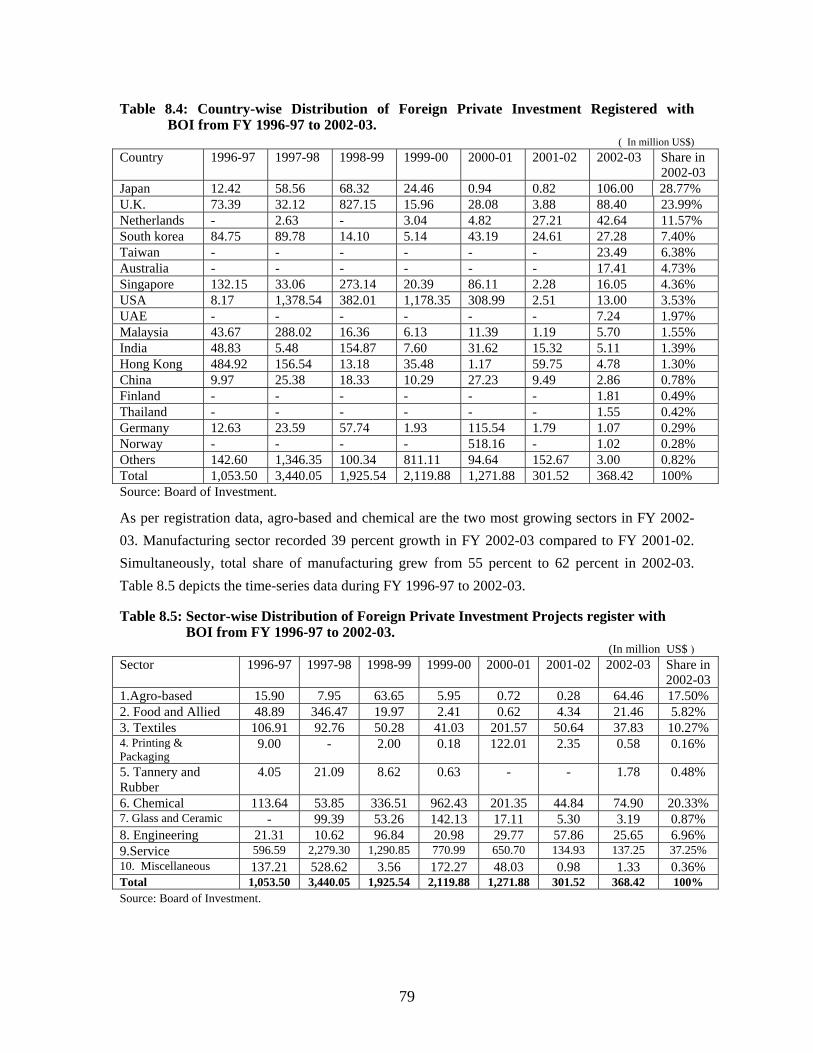

8.5 Sector-wise Distribution of Foreign Private Investment Projects Registered with BOI from FY1996-97 to FY2002-03.

79

8.6 Comparative Statement of Sector-wise Distribution of Local Private Investment Registered with BOI from FY2001-02 to FY2002-03.

80

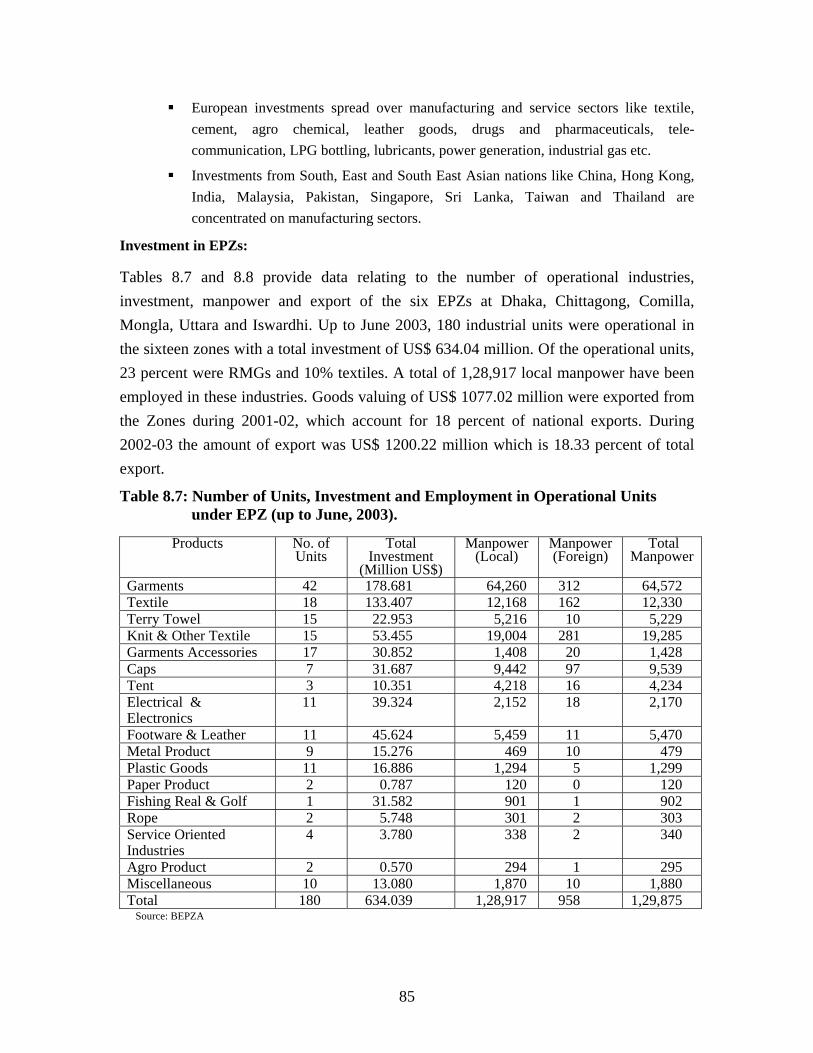

8.7 Number of Units, Investment and Employment in the Operational Units under EPZ (up to June, 2003)

85

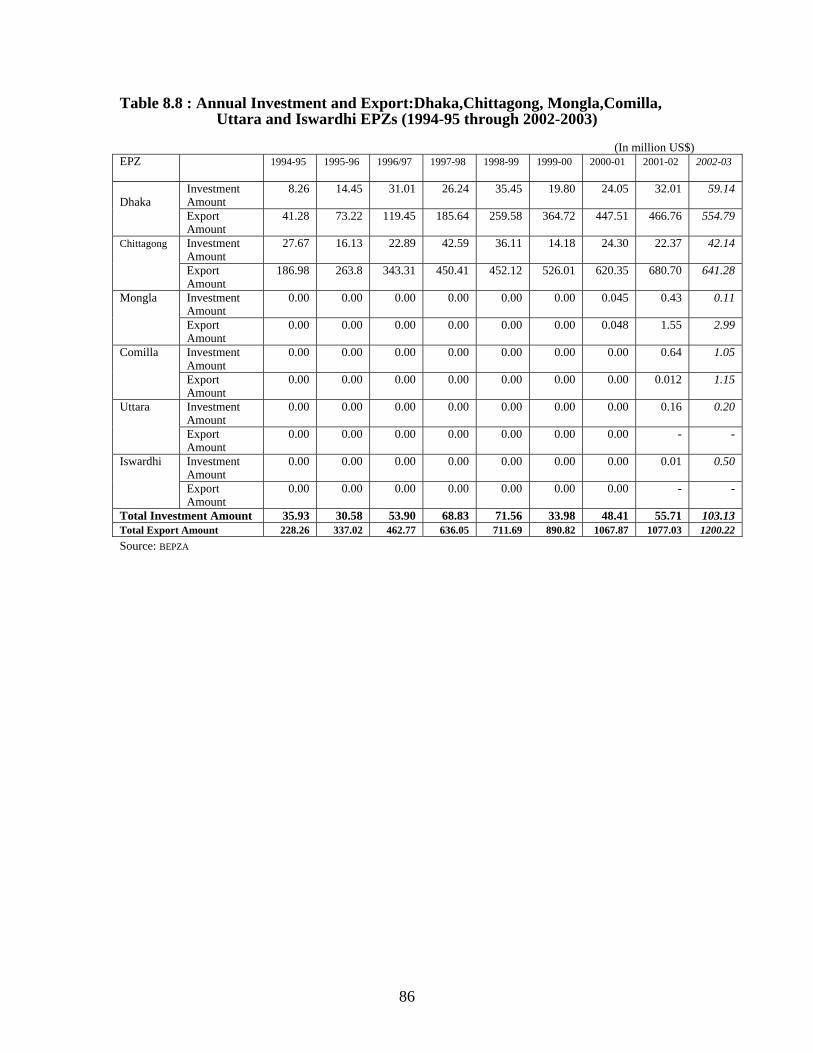

8.8 Annual Investment and Export: Dhaka, Chittagong, Mongla, Comilla, Uttara and Iswardhi EPZs (1994-95 through 2002-03)

86

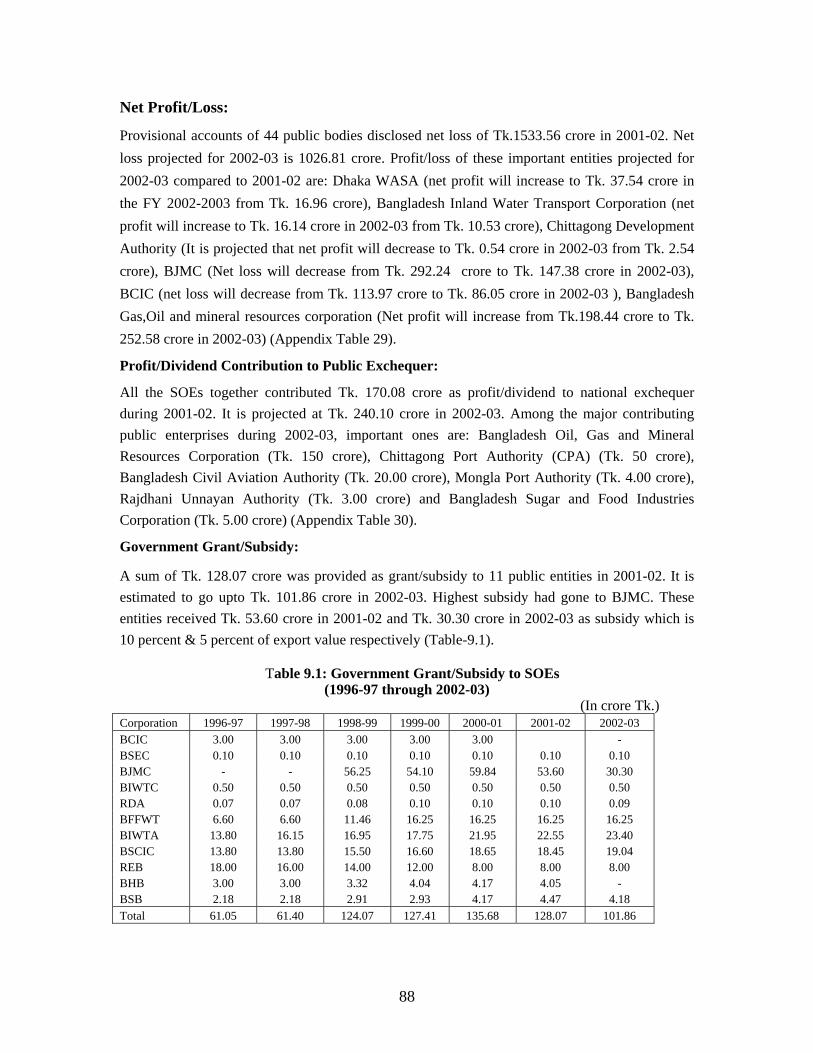

9.1 Government Grant/Subsidy to SOEs (1996-97 through 2002-03) 88

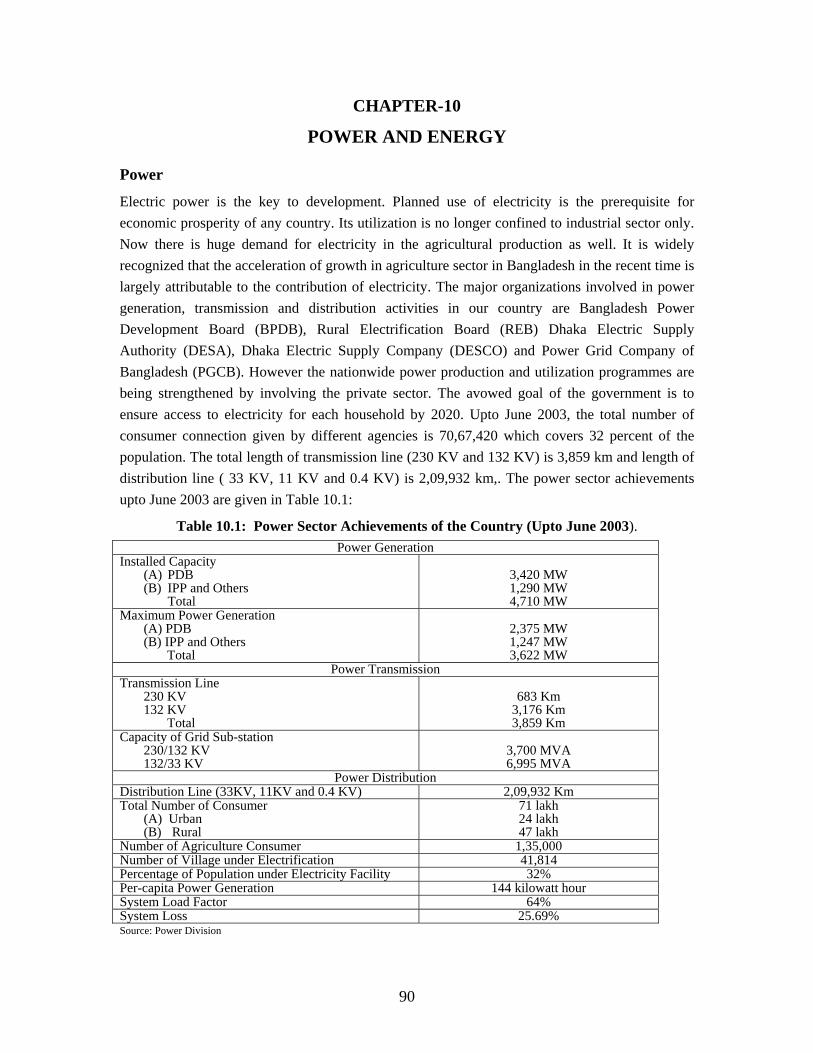

10.1 Power Sector Achievements of the Country (up to June 2003) 90

10.2 Installed Capacity, Dependable Production Capacity and Maximum

Production

91

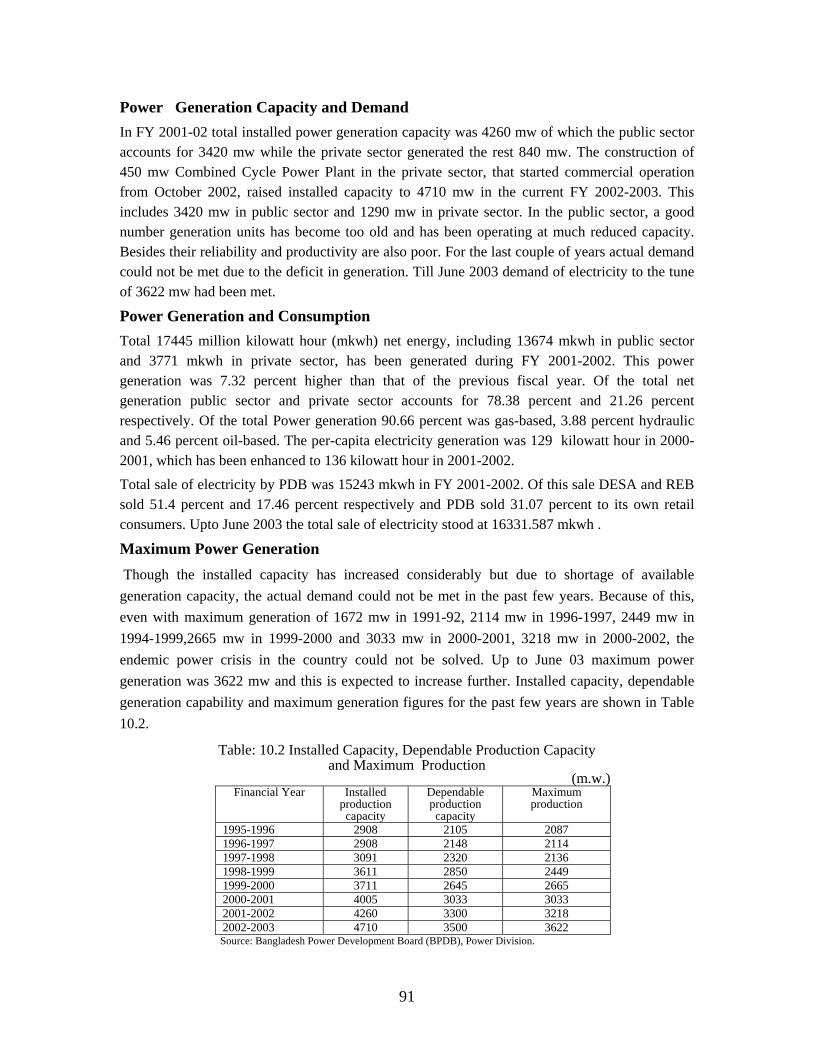

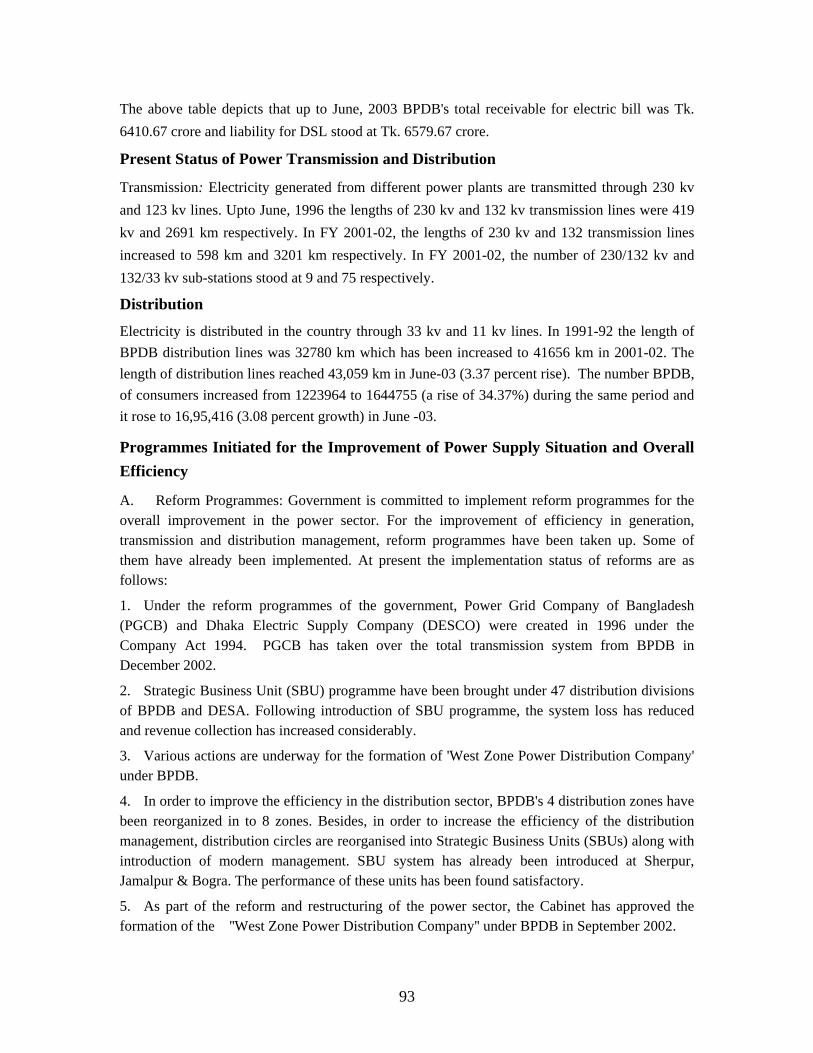

10.3 Accounts Receivable and Payable of BPDB 92

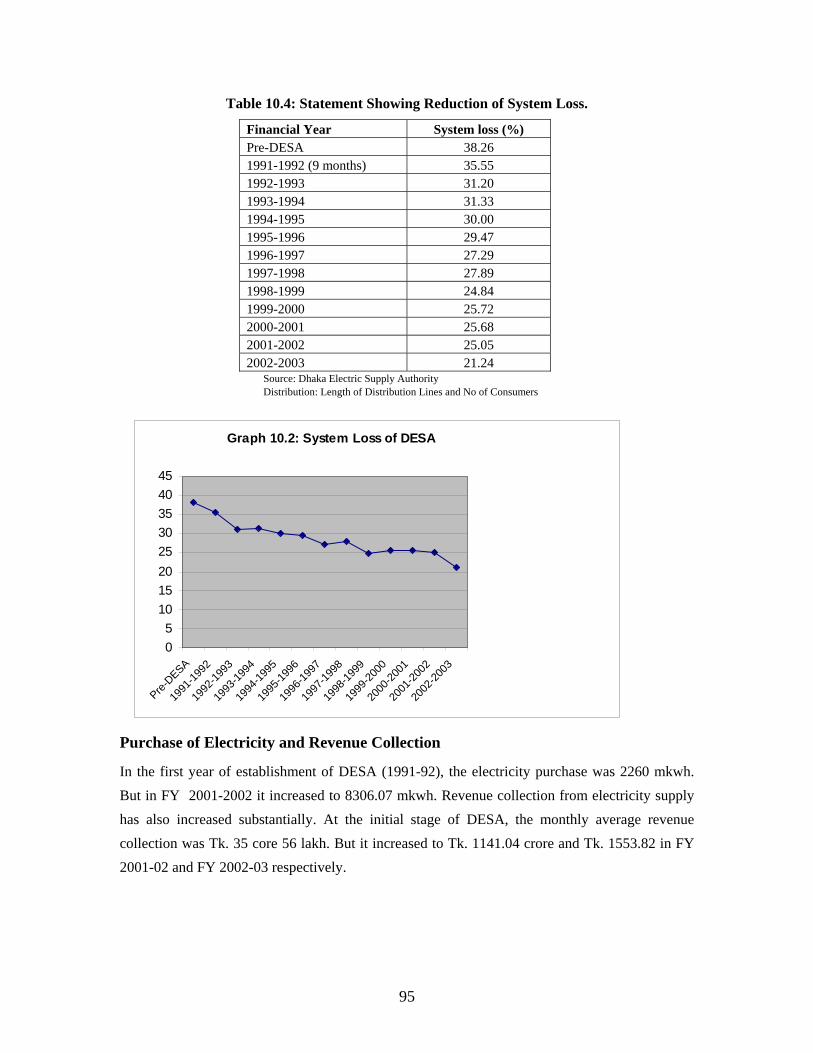

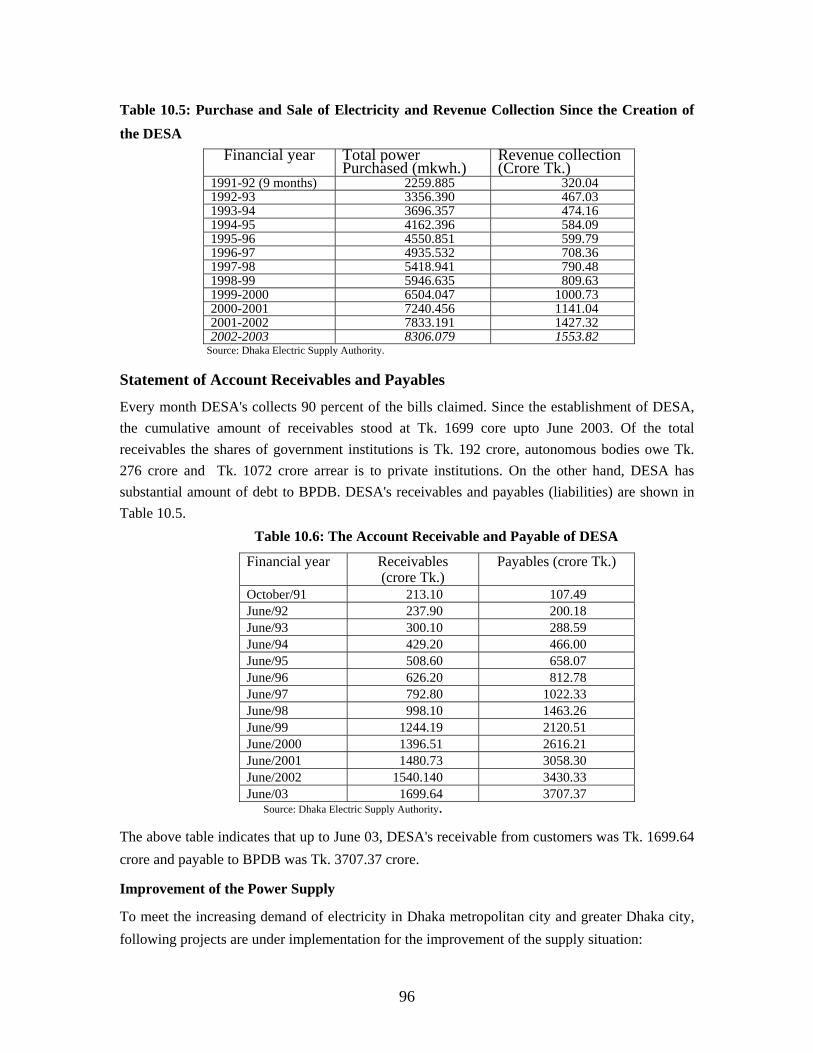

10.4 Statement Showing Reduction of System Loss 95

10.5 Purchase and Sale of Electricity and Revenue Collection since the

Creation of the DESA

96

10.6 The Accounts Receivable and Payable of DESA 96

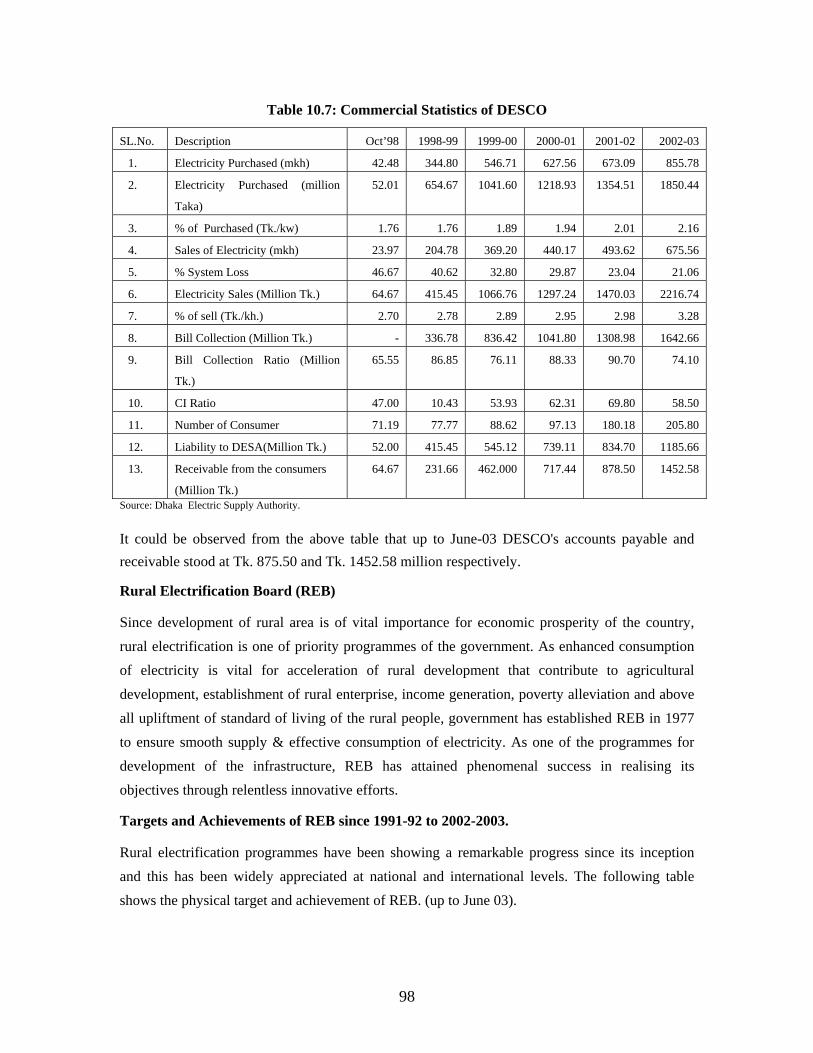

10.7 Commercial Statistics of DESCO 98

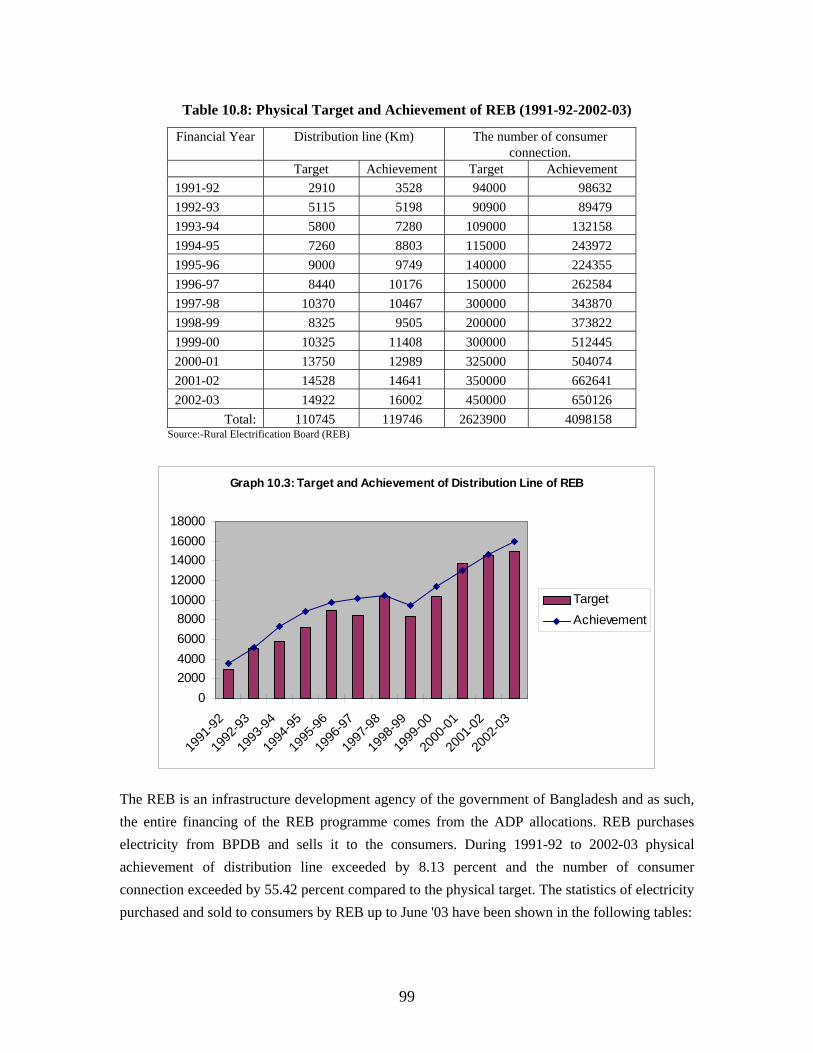

10.8 Physical Target and Achievement of REB (1991-92 to 2002-03) 99

ix

Table Title Page

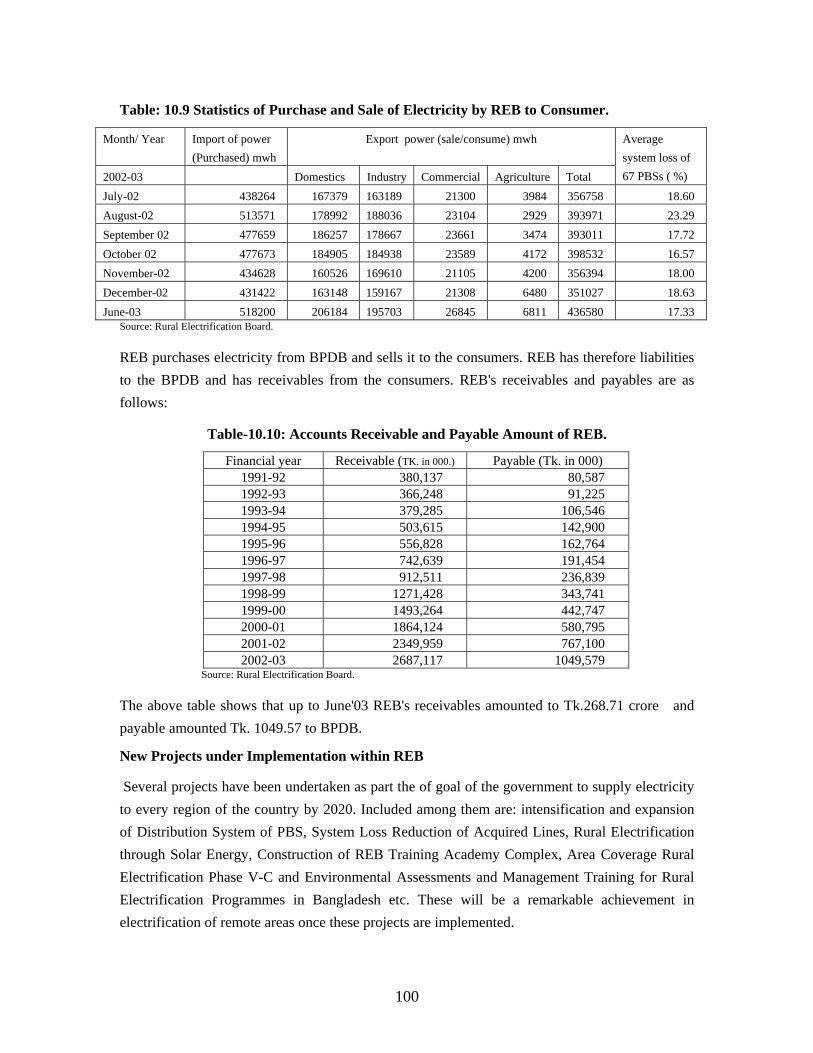

10.9 Statistics of Purchase and Sale of Electricity by REB to Consumer 100

10.10 Accounts Receivable and Payable Amount of REB 100

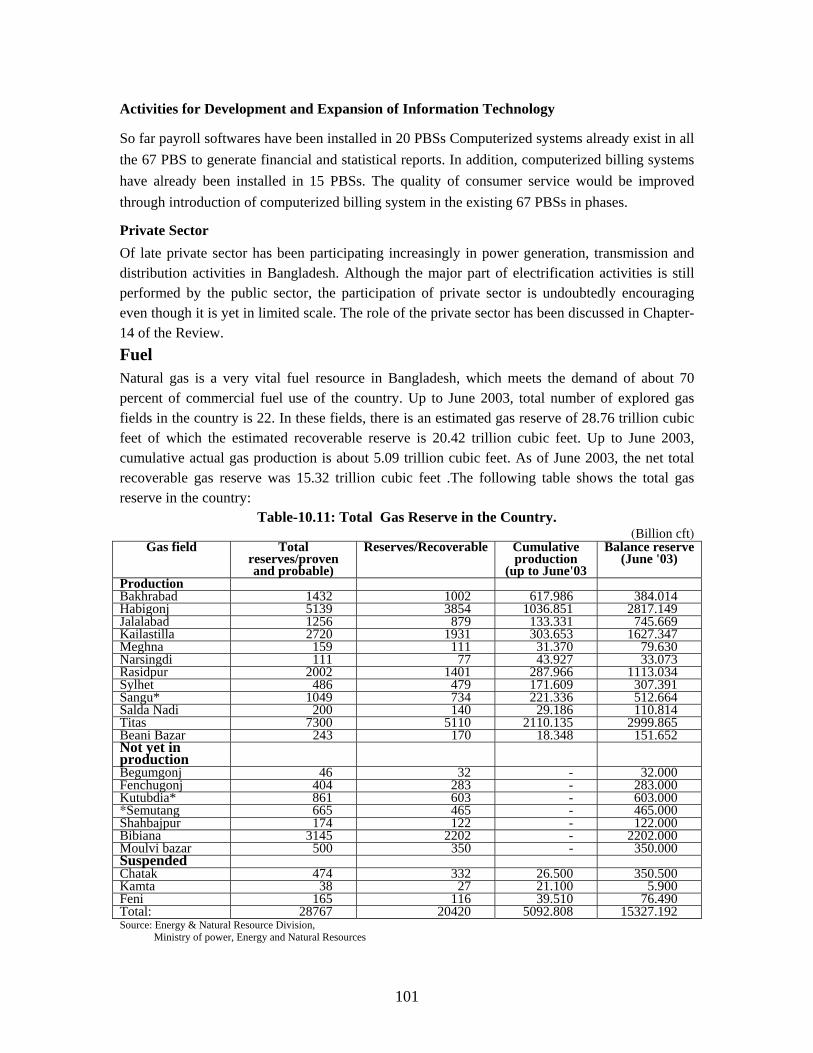

10.11 Total Gas Reserve in the Country 101

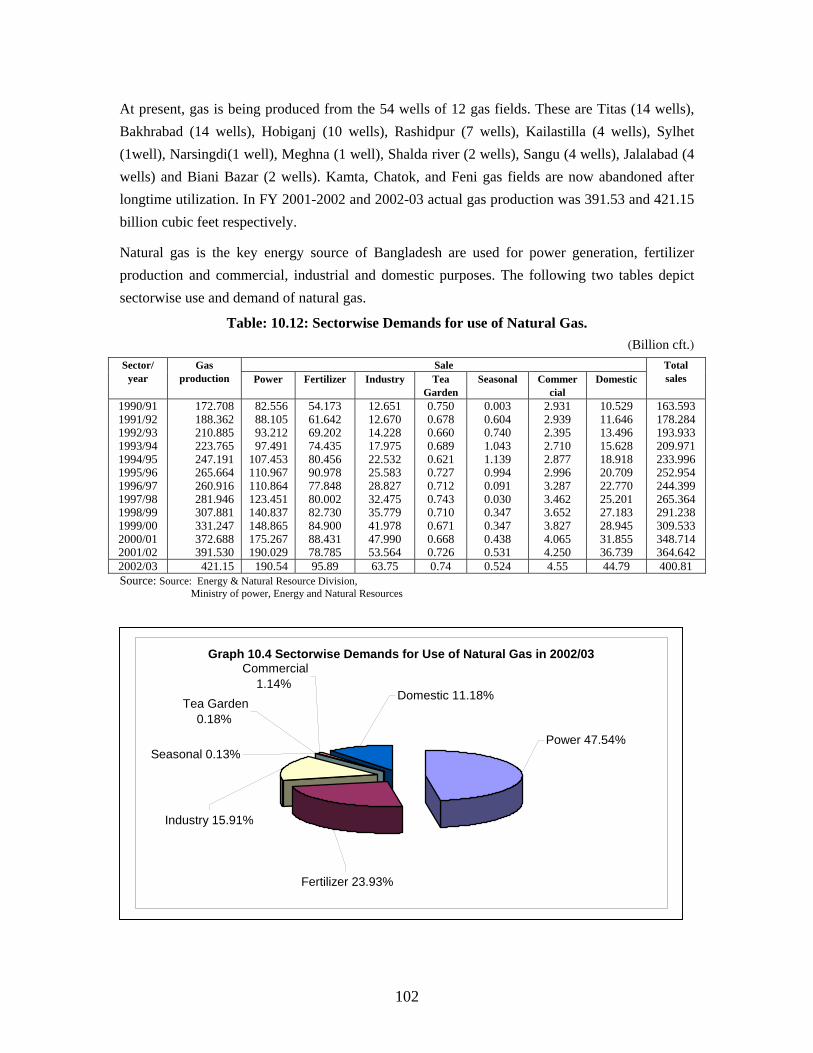

10.12 Sector-wise Demands for Use of Natural Gas 102

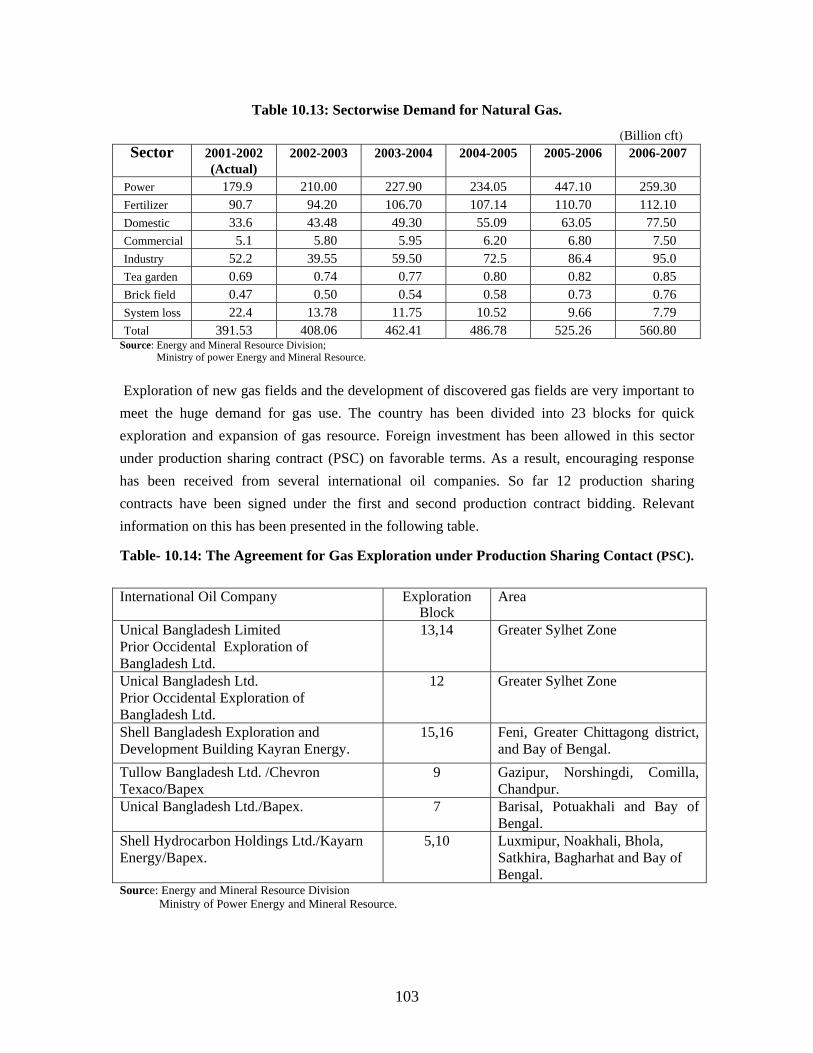

10.13 Sector-wise Demand for Natural Gas 103

10.14 The Agreement for Gas Exploration under Production Sharing Contract 103

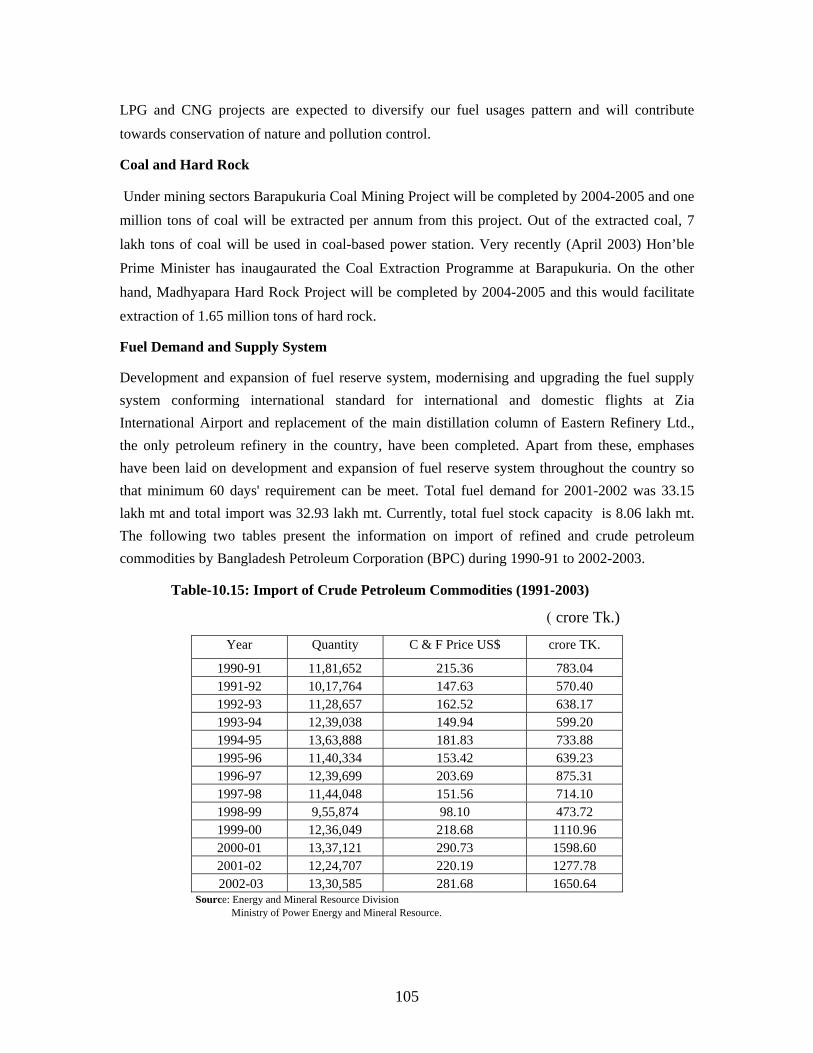

10.15 Import of Crude Petroleum Commodities (1991-2003) 105

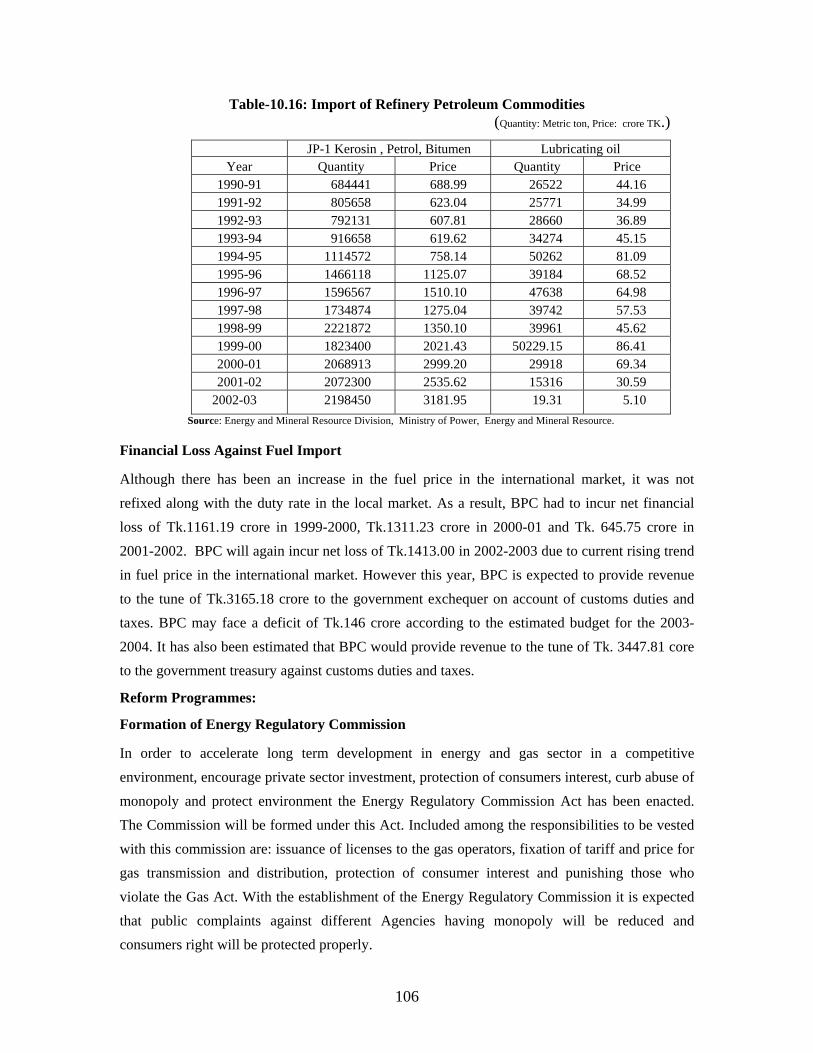

10.16 Import of Refinery Petroleum Commodities 106

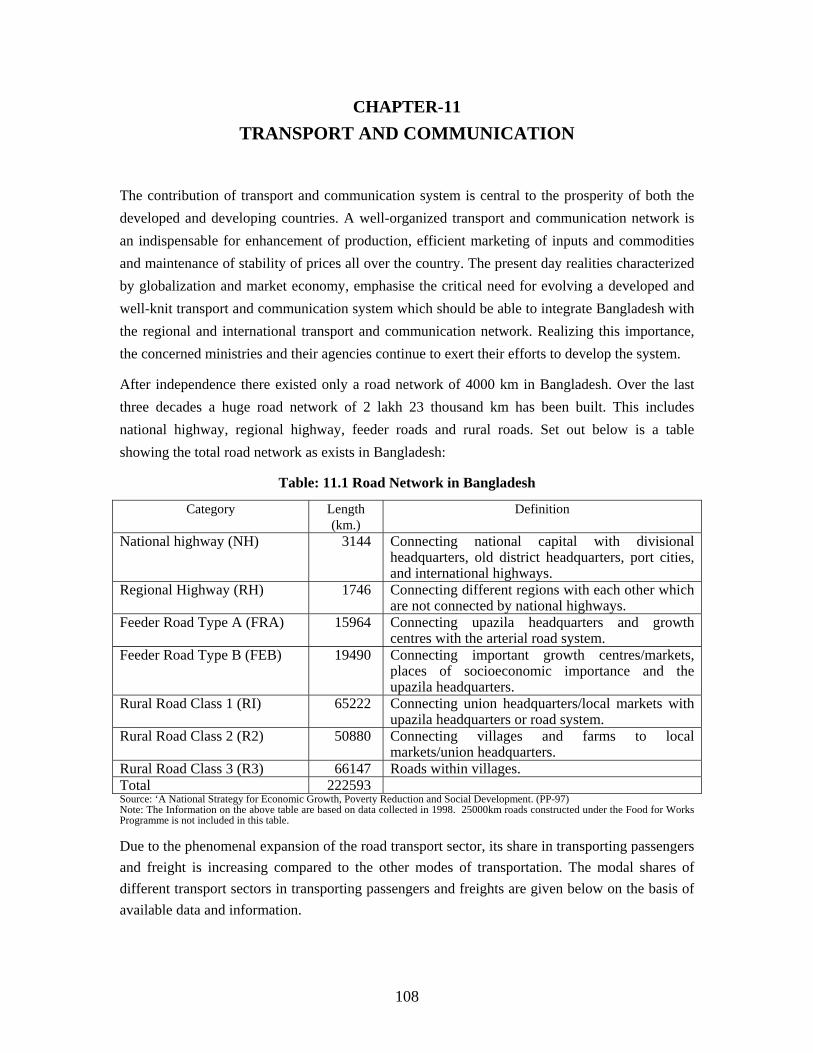

11.1 Road Network in Bangladesh 108

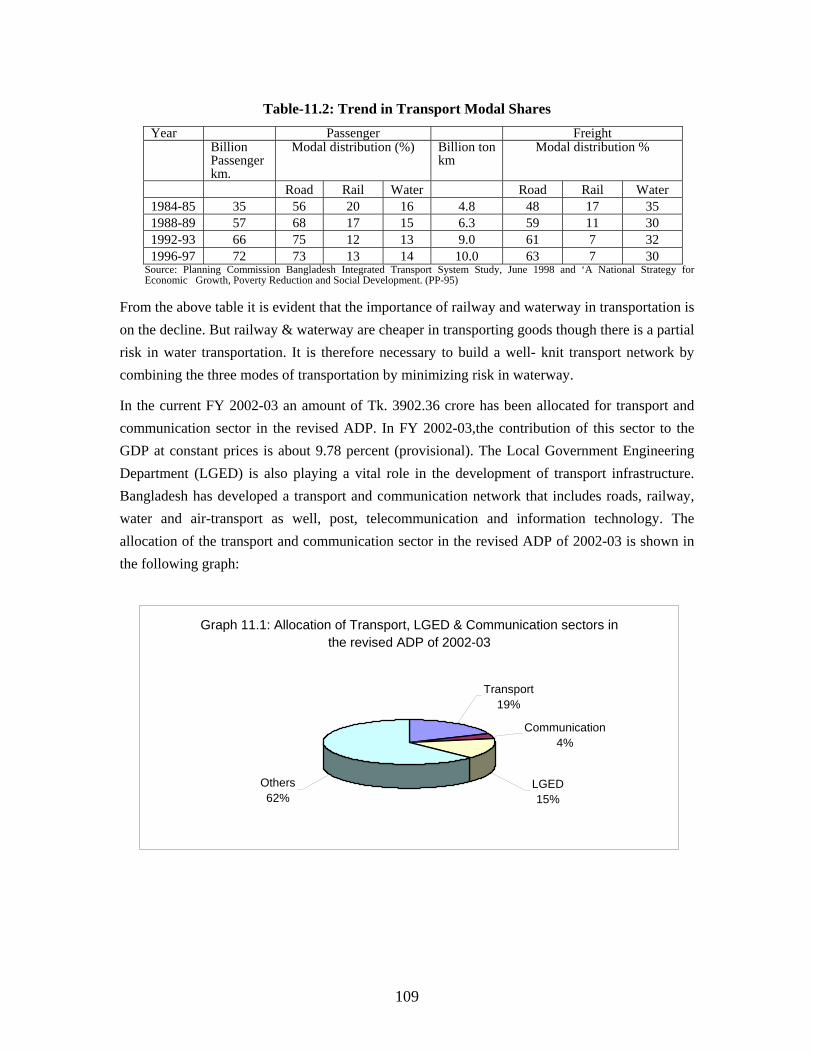

11.2 Trend in Transport Modal Shares 109

11.3 Various Categories of Roads under Roads and Highways Department 110

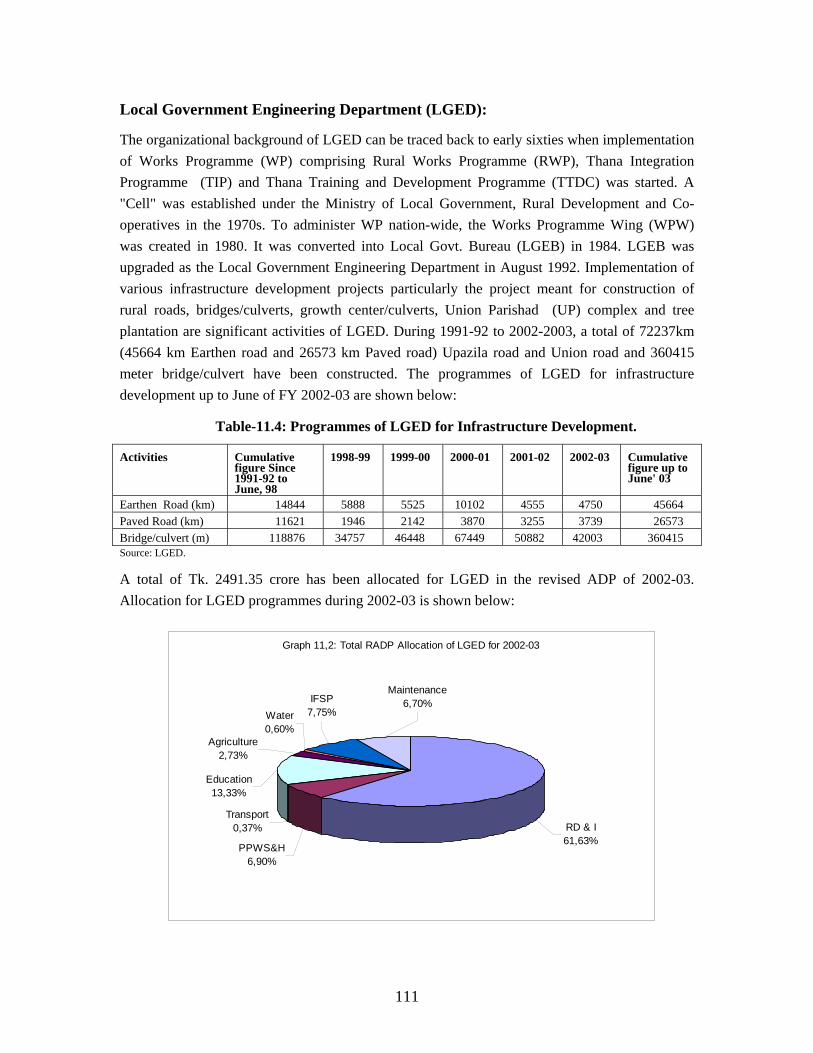

11.4 Programmes of LGDE for Infrastructure Development 111

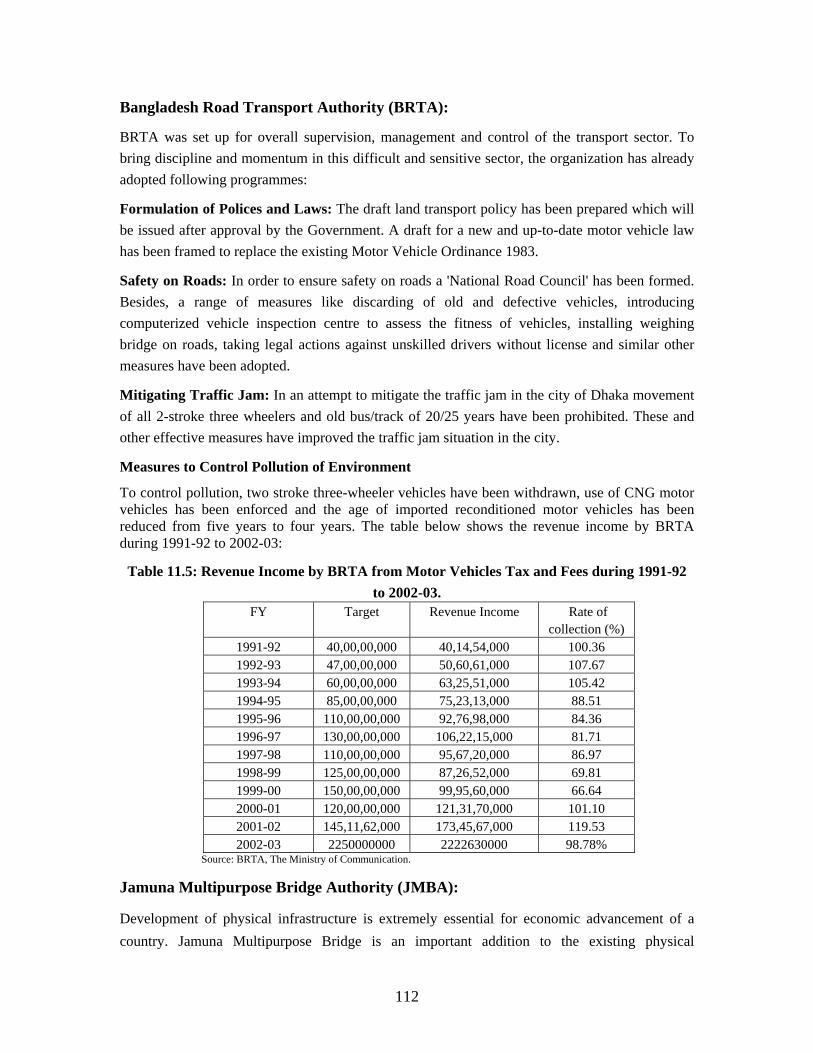

11.5 Revenue Income by BRTA from Motor Vehicles Tax and Fees during 1991-92 to 2002-03

112

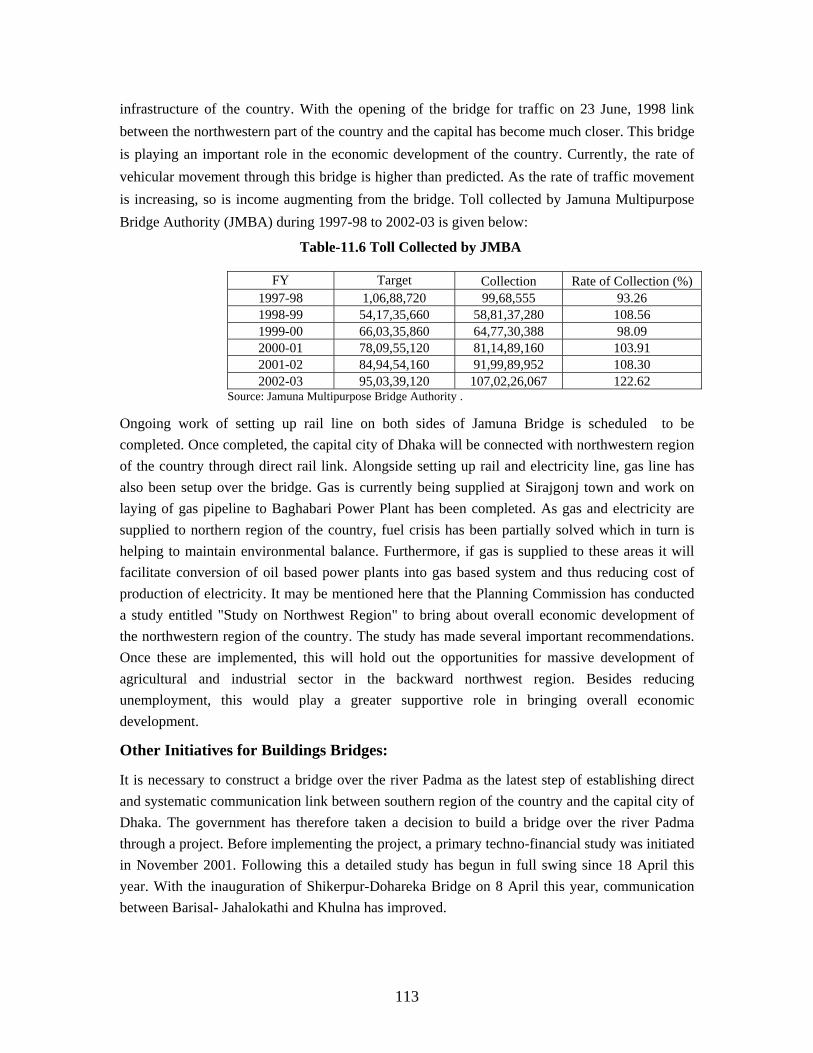

11.6 Toll Collected by JMBA 113

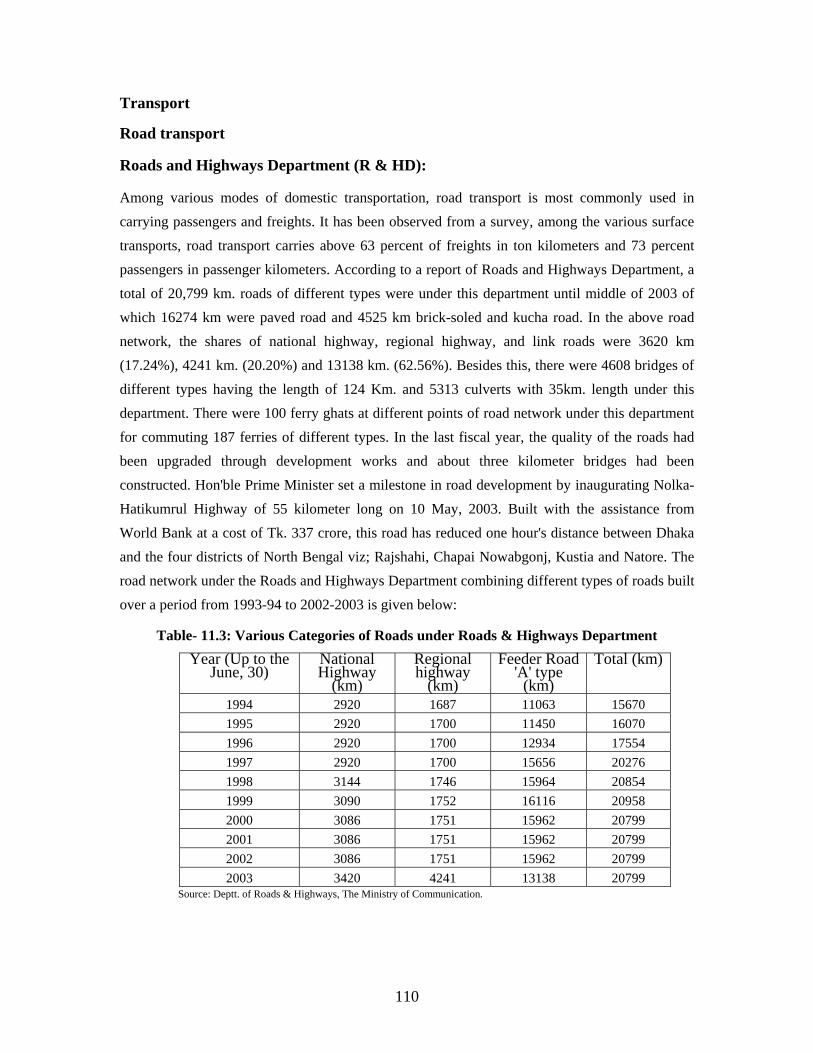

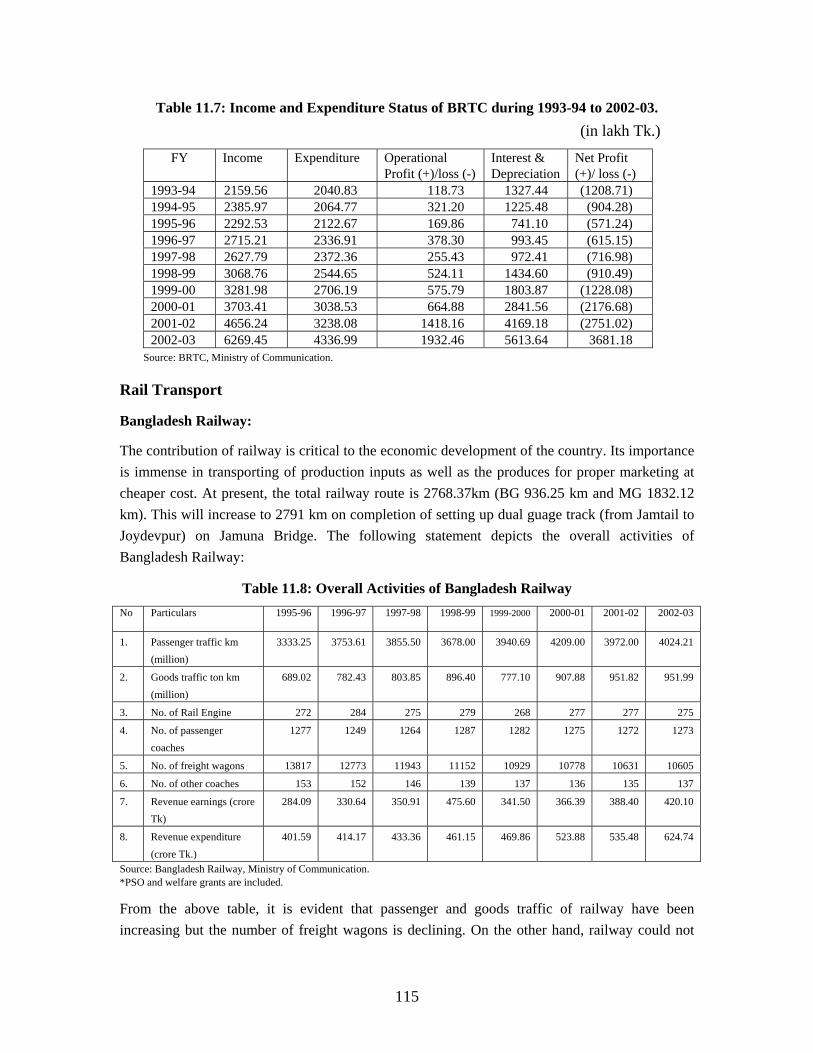

11.7 Income and Expenditure Status of BRTC during 1993-94 to 2002-03 115

11.8 Overall Activities of Bangladesh Railway 115

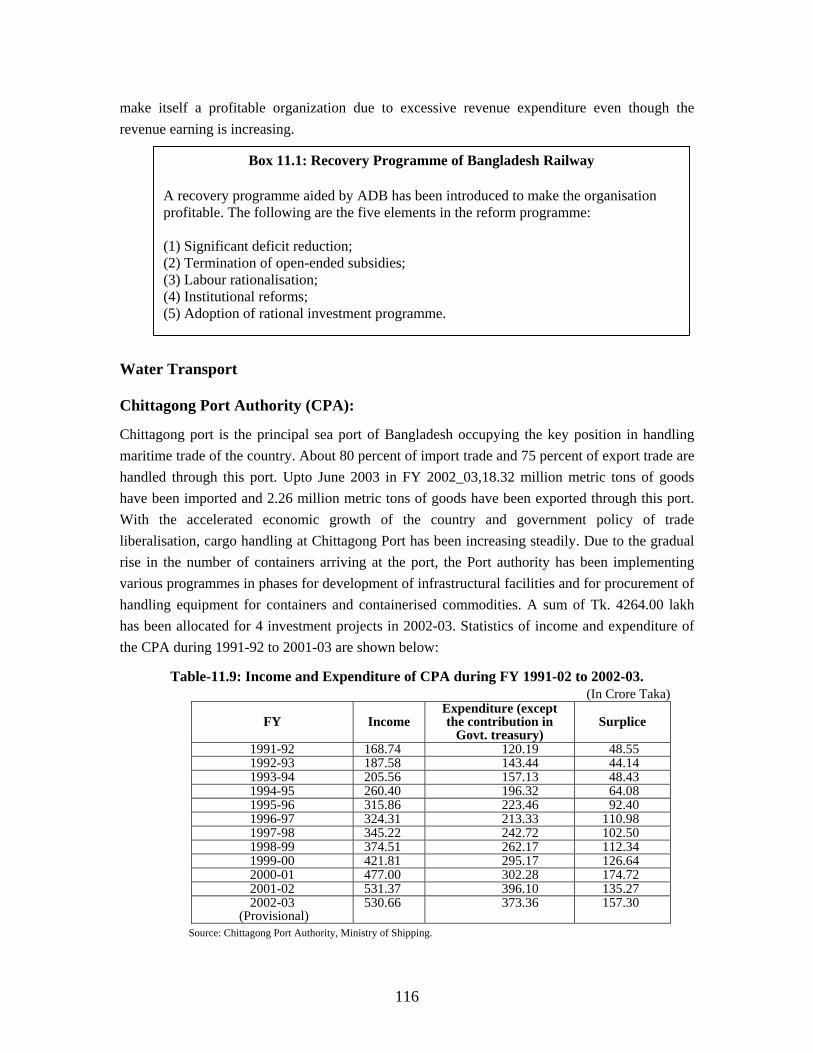

11.9 Income and Expenditure of CPA during 1991-92 to 2002-03 116

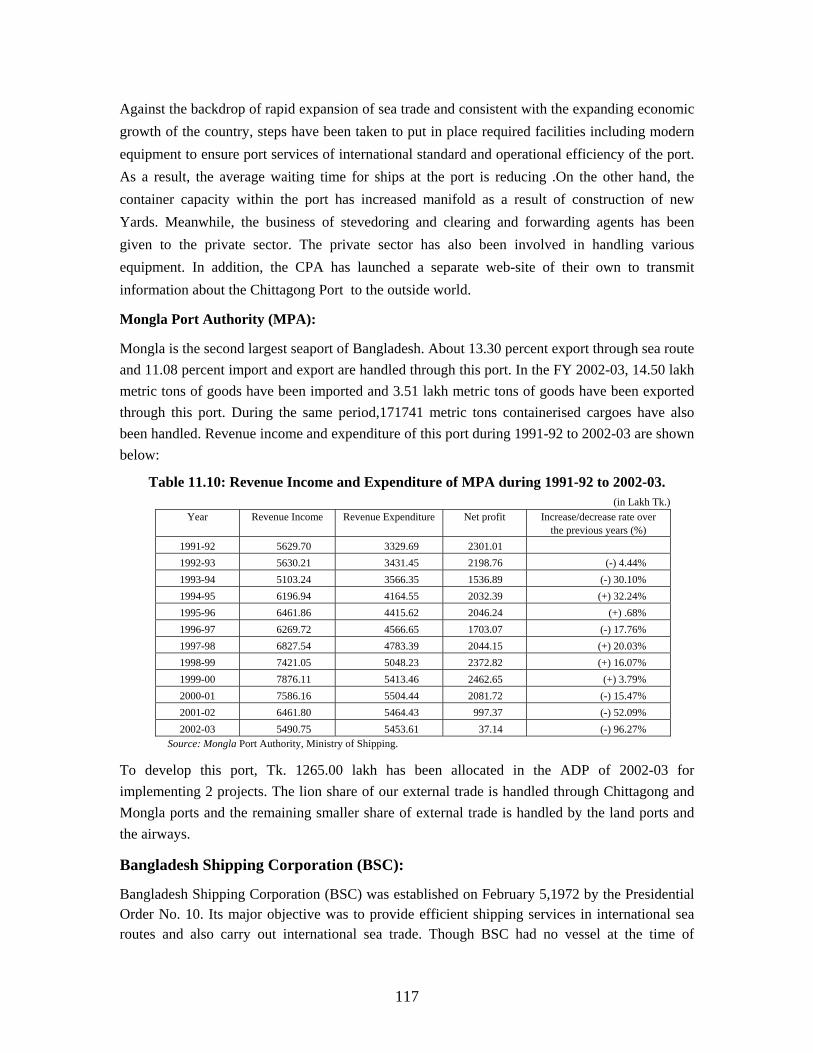

11.10 Revenue, Income and Expenditure of MPA during 1991-92 to 2002-03 117

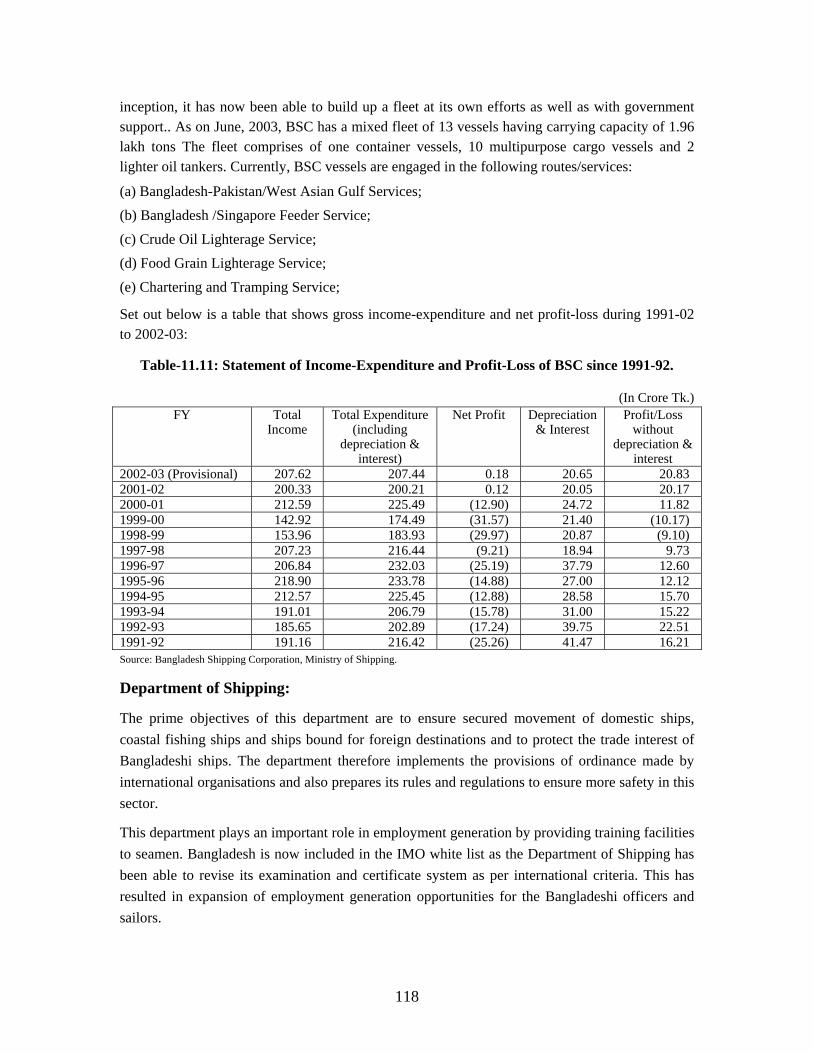

11.11 Statement of Income-Expenditure and Profit-Loss of BSC since 1991-92 118

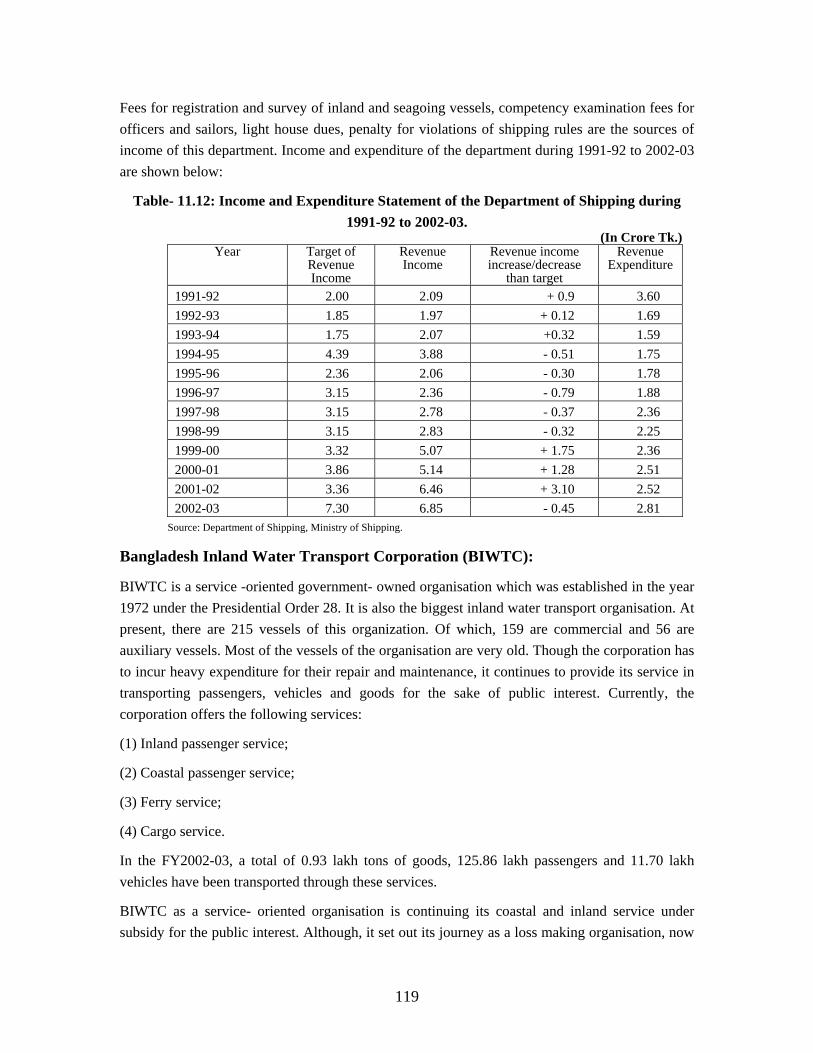

11.12 Income and Expenditure Statement of the Department of Shipping

during 1991-92 to 2002-03

119

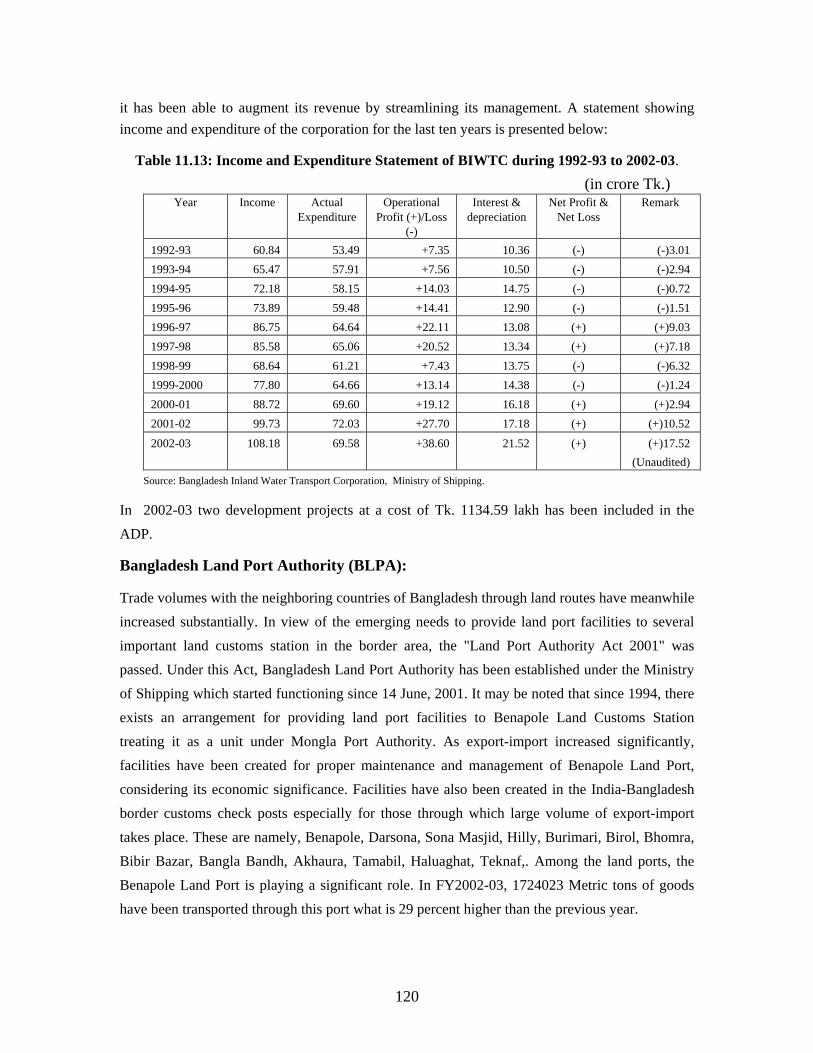

11.13 Income and Expenditure Statement of BIWTC during 1992-93 to 2002-

03

120

11.14 Statistics on Movement of Aircrafts, Passengers and Cargoes in the Airports during 1993 to 2003.

122

11.15 Income/Expenditure of Biman Bangladesh Airlines during 1991-92 to

2002-03

123

11.16 Statement of the Number of Telephone, NWD Circuits and Foreign

Circuits of BTTB since 1991-92

124

11.17 Revenue Target, Collection, Expenditure and Surplus of BTTB during

1991-92 to 2002-2993

125

12.1 Rate of Generation of Value Addition in the Social Sectors 129

12.2 Allocation in Social Sectors under ADP 130

12.3 Allocation under Revenue Budget for Social Sectors 130

12.4 Student Enrolment at Primary Level (1990-2002) 133

12.5 Recent Trend in Literacy (15 years and above) 134

12.6 Recent Trends in Health Indices 136

x

Table Title Page

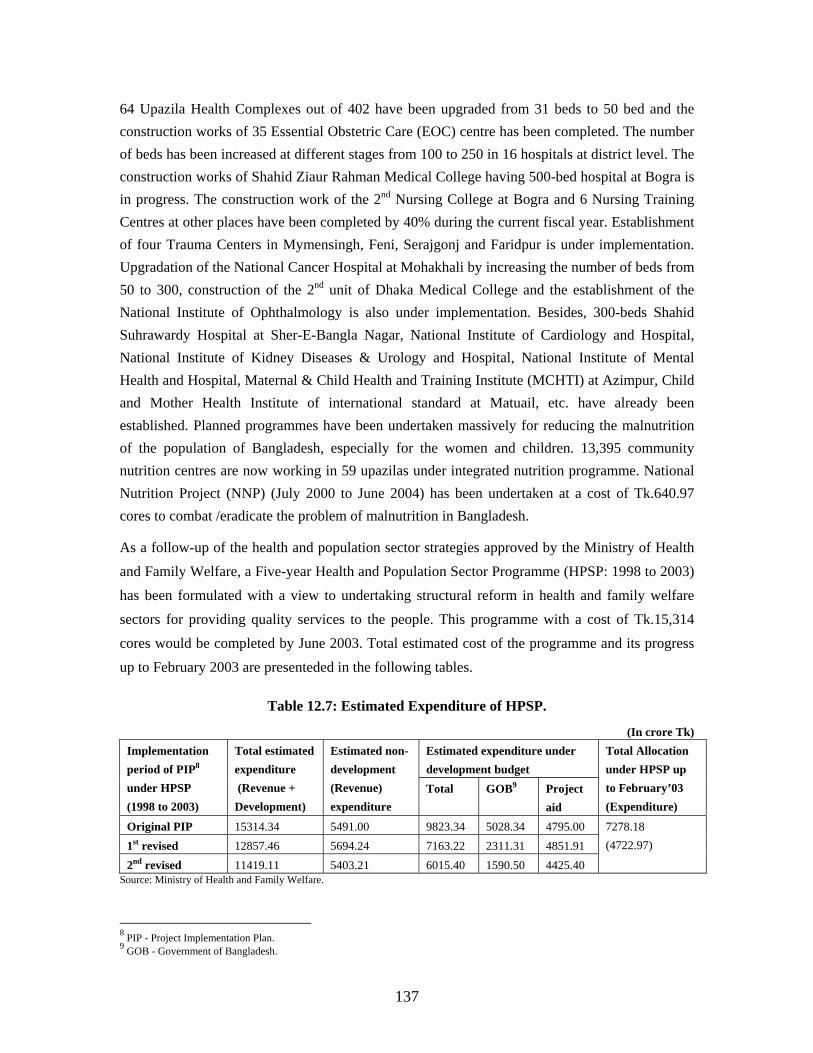

12.7 Estimated Expenditure of Health and Population Sector Programme (HPSP)

137

12.8 Progress of HPSP 138

12.9 Government Expenditure in Education, Health and Social Sectors in

1980 and 2000.

139

12.10 Allocations and Expenditures in RADP 140

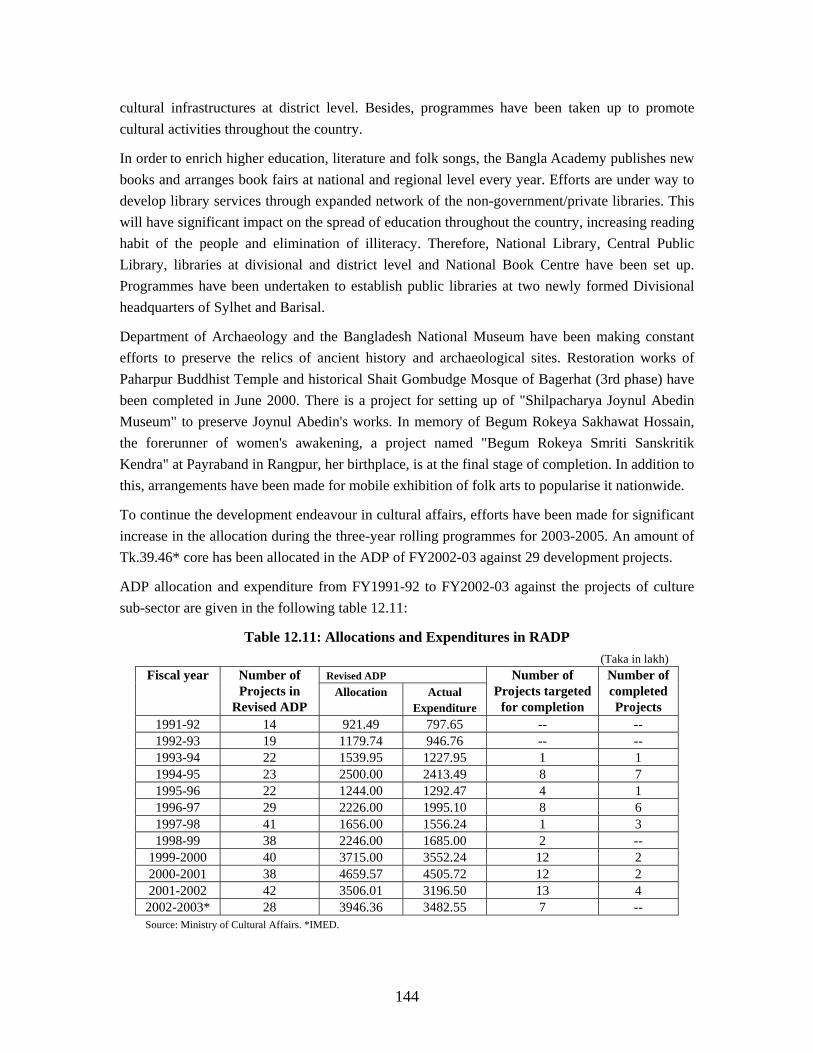

12.11 Allocations and Expenditures in RADP 144

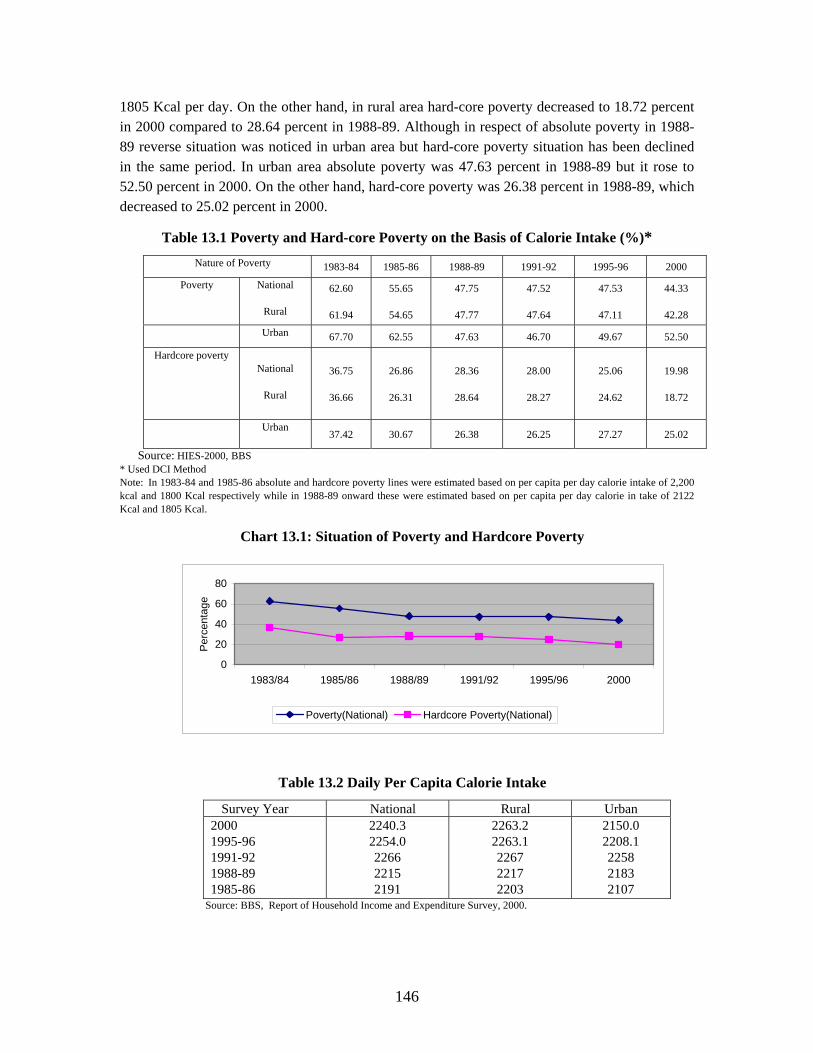

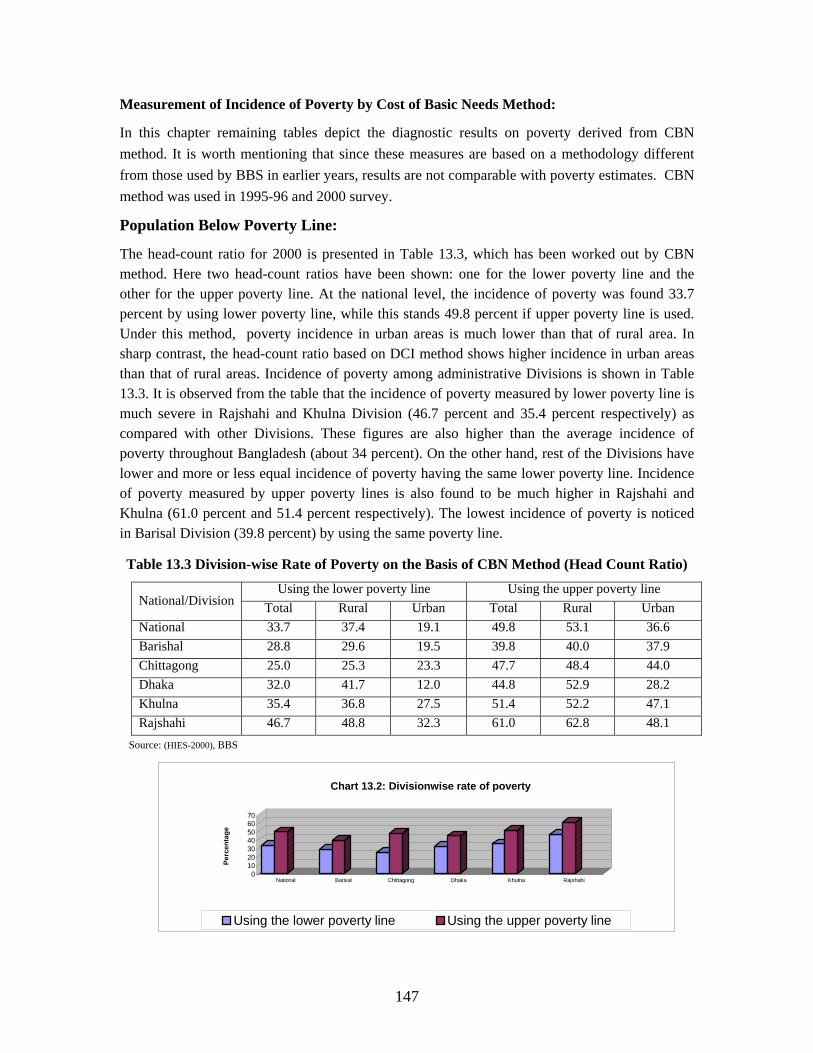

13.1 Poverty and Hard-core Poverty on the Basis of Calorie Intake (%) 146

13.2 Daily Per Capita Calorie Intake 146

13.3 Division-wise Rate of Poverty on the Basis of CBN Method (Head Count

Ratio)

147

13.4 Distribution of Poor by Residence in Percentage 148

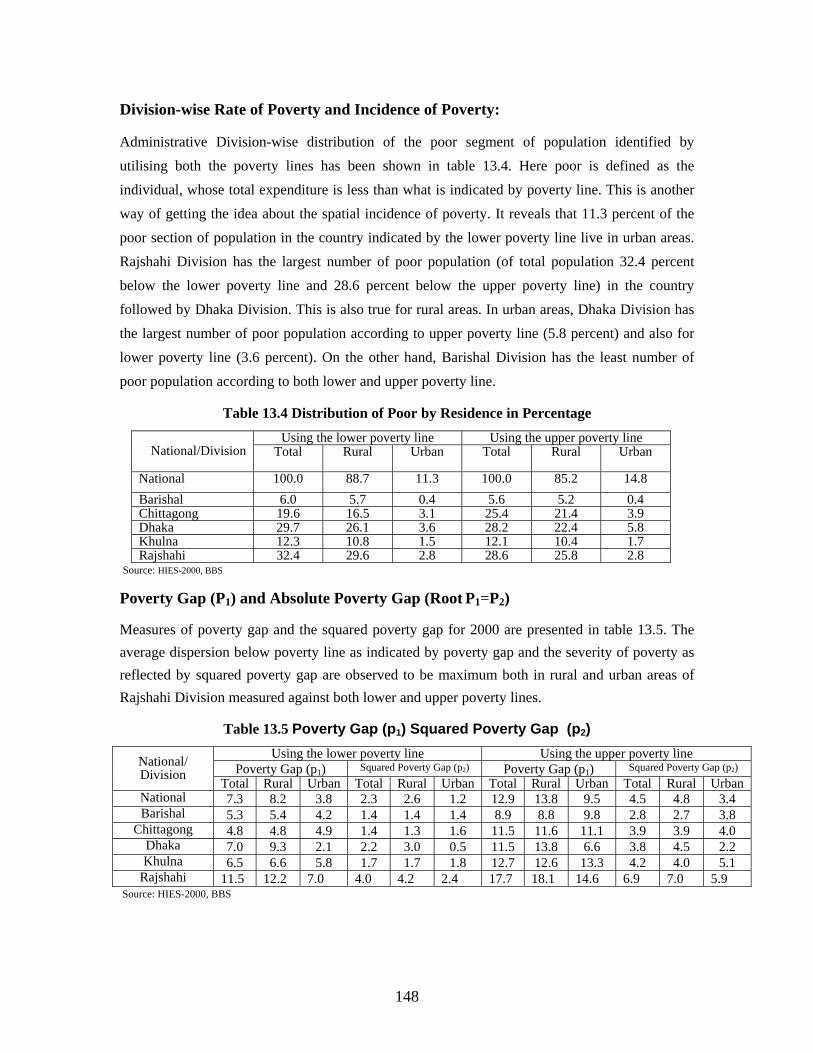

13.5 Poverty Gap (P1), Squared Poverty Gap (P2) 148

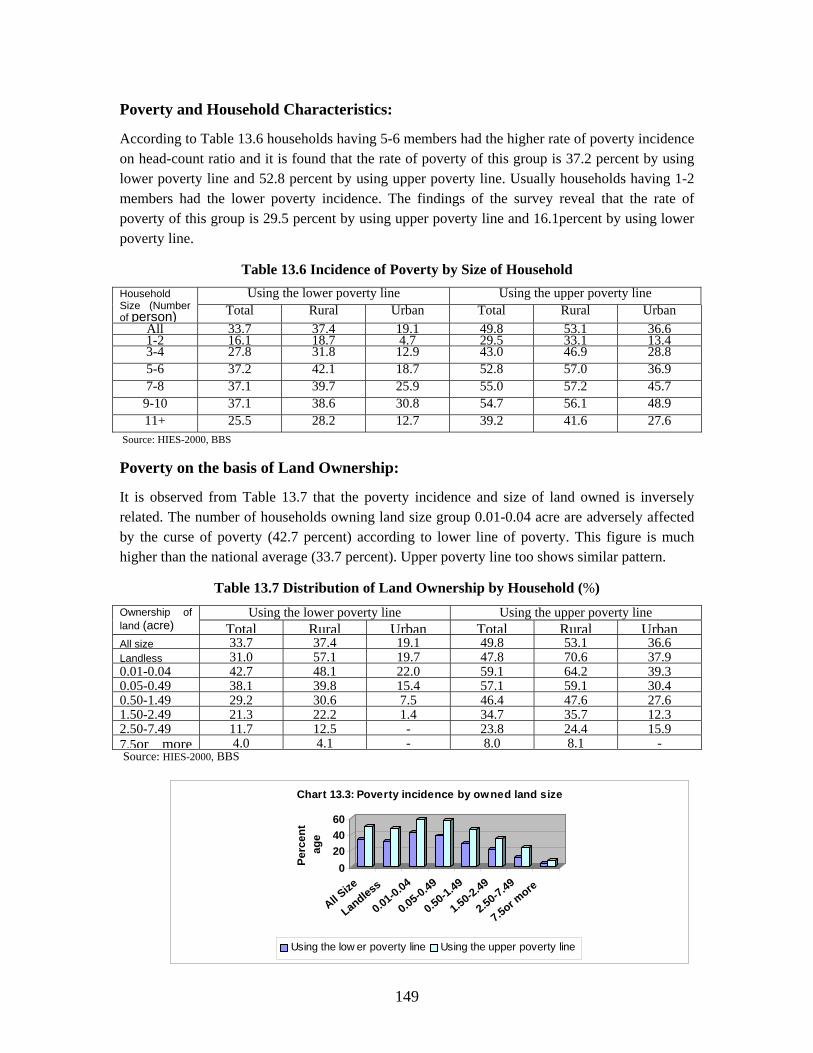

13.6 Incidence of Poverty by Size of Household 149

13.7 Distribution of Land Ownership by Household (%) 149

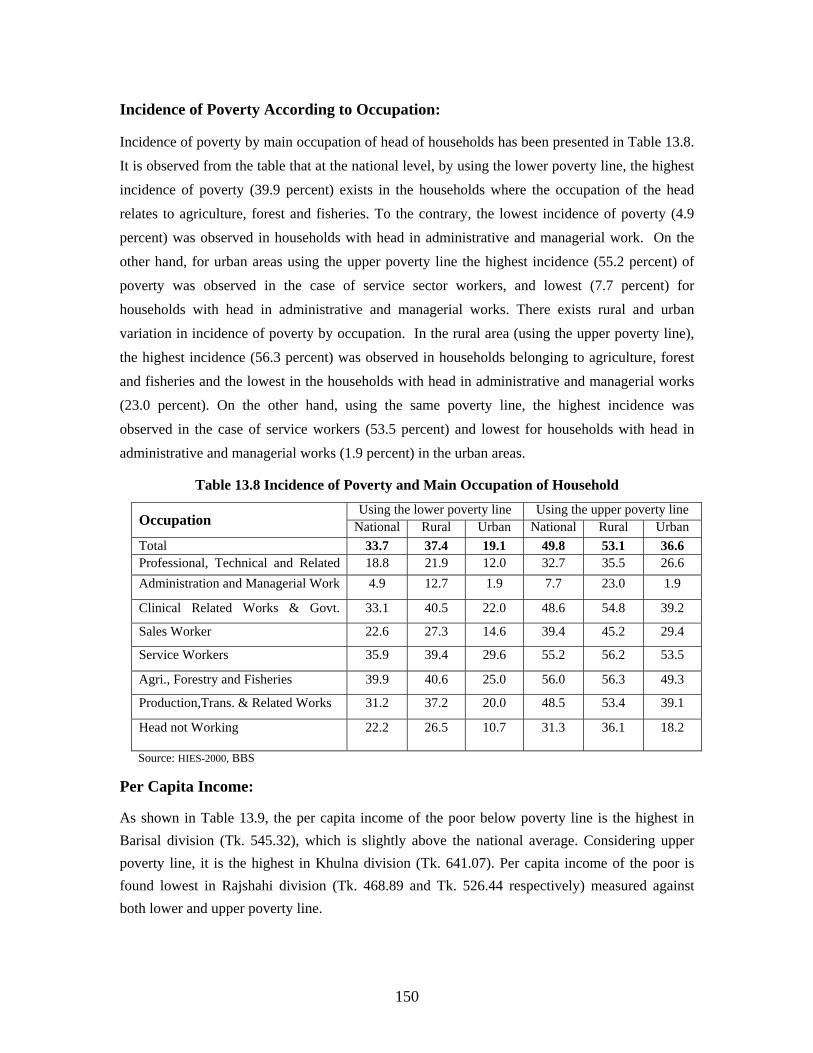

13.8 Incidence of Poverty and Main Occupation of Household 150

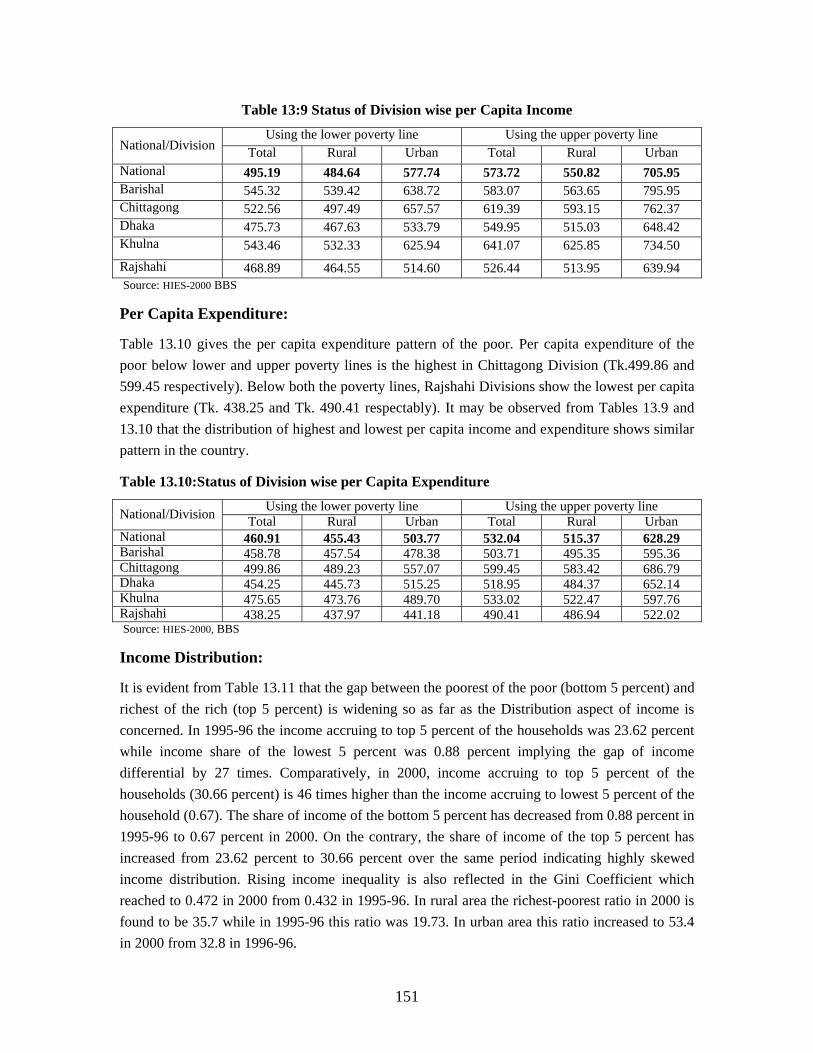

13.9 Status of Division-wise Per Capita Income 151

13.10 Status of Division-wise Per Capita Expenditure 151

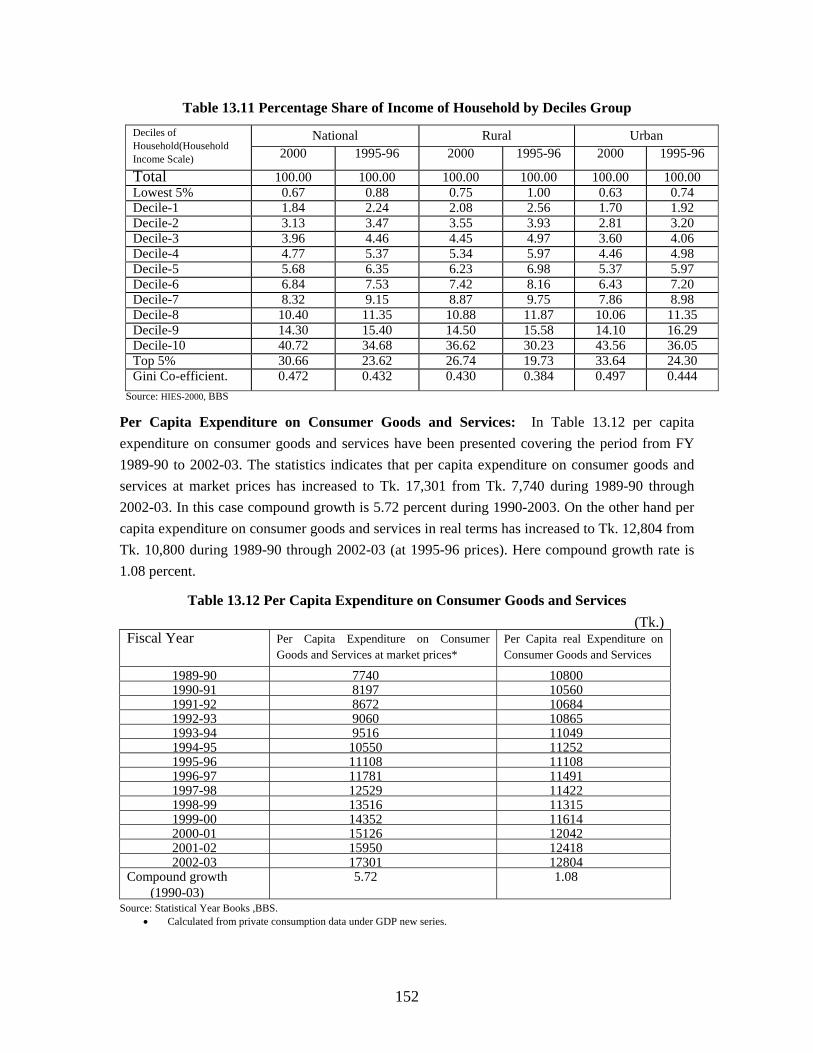

13.11 Percentage Share of Income of Household by Deciles Group 152

13.12 Per Capita Expenditure on Consumer Goods and Services 152

13.13 Simulating Trends in Poverty under Alternative Growth Scenario,

Bangladesh: 2000-2020

153

13.14 Major Goal Posts in Poverty and Social Targets Set against the 1990

Benchmark

154

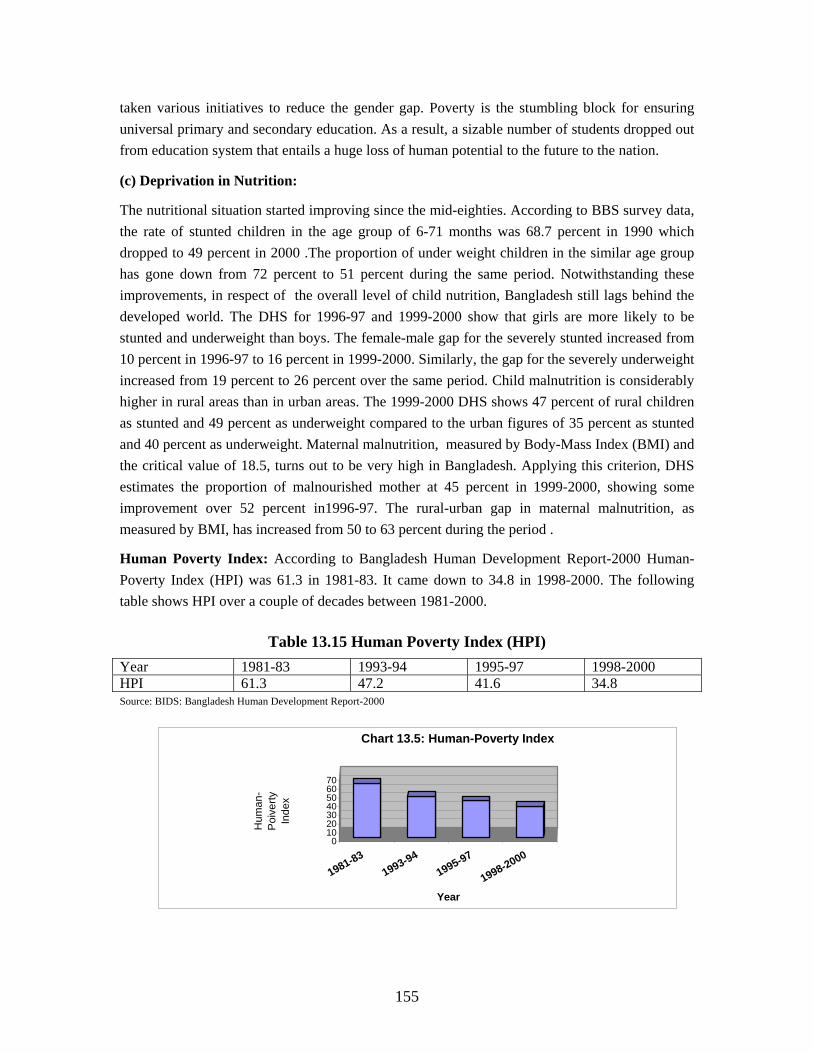

13.15 Human Poverty Index (HPI) 155

13.16 Poverty Alleviation Effects by Sectors 156

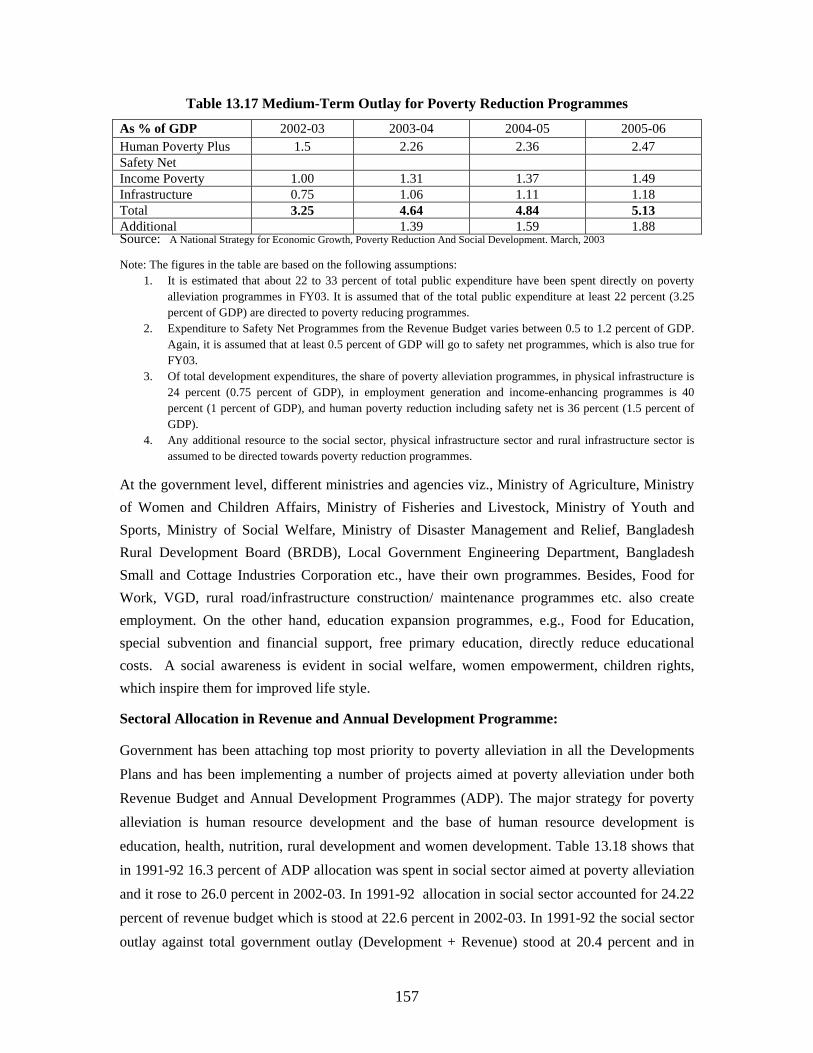

13.17 Medium-Term Outlay for Poverty Reduction Programmes 157

13.18 Allocation in Social Sector in the Revenue and Annual Development

Programmes

158

13.19 Safety Net Programmes 159

13.20 Status of Grihayan Tahabil 162

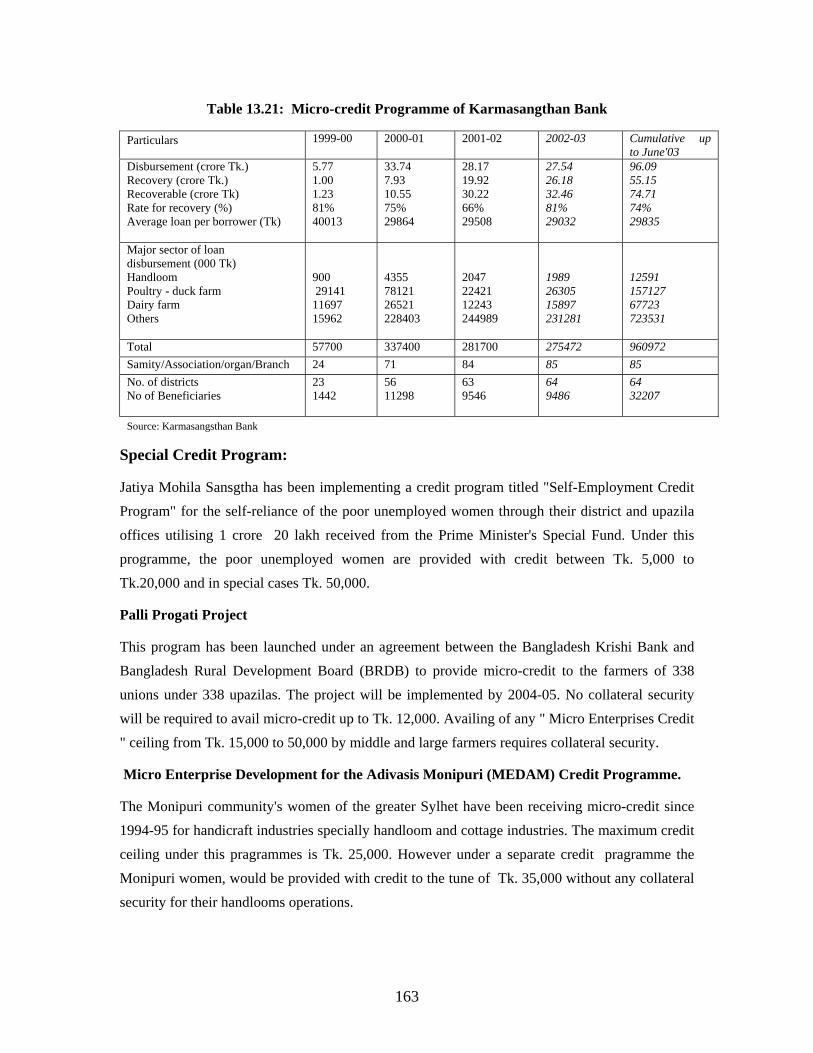

13.21 Micro-credit Programme of Karmasangthan Bank 163

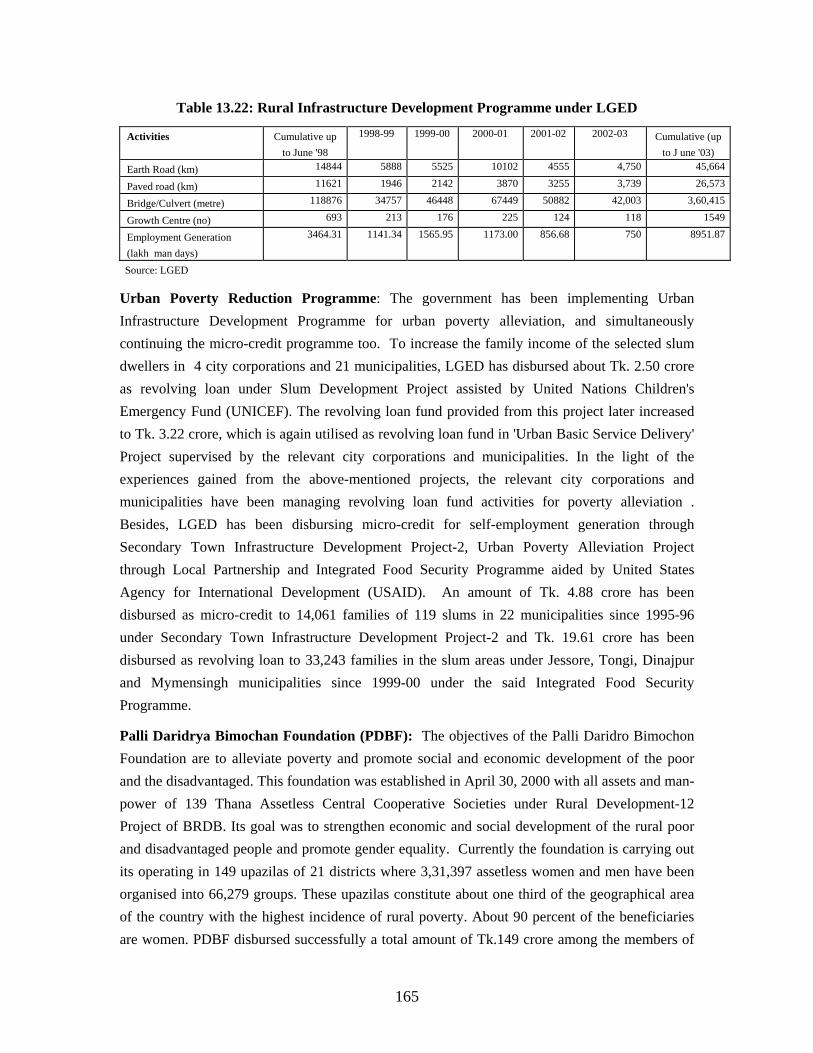

13.22 Rural Infrastructure Development Programme under LGED 165

13.23 Micro Credit Disbursement Programme of Four Major NGOs (up to June'

02)

168

13.24 Sources of Micro Credit and Revolving Loan Fund of NGOs 168

13.25 Status of Micro Credit Programmes of Major NGOs 169

13.26 Micro Credit Programme of three Specialised Institutions 172

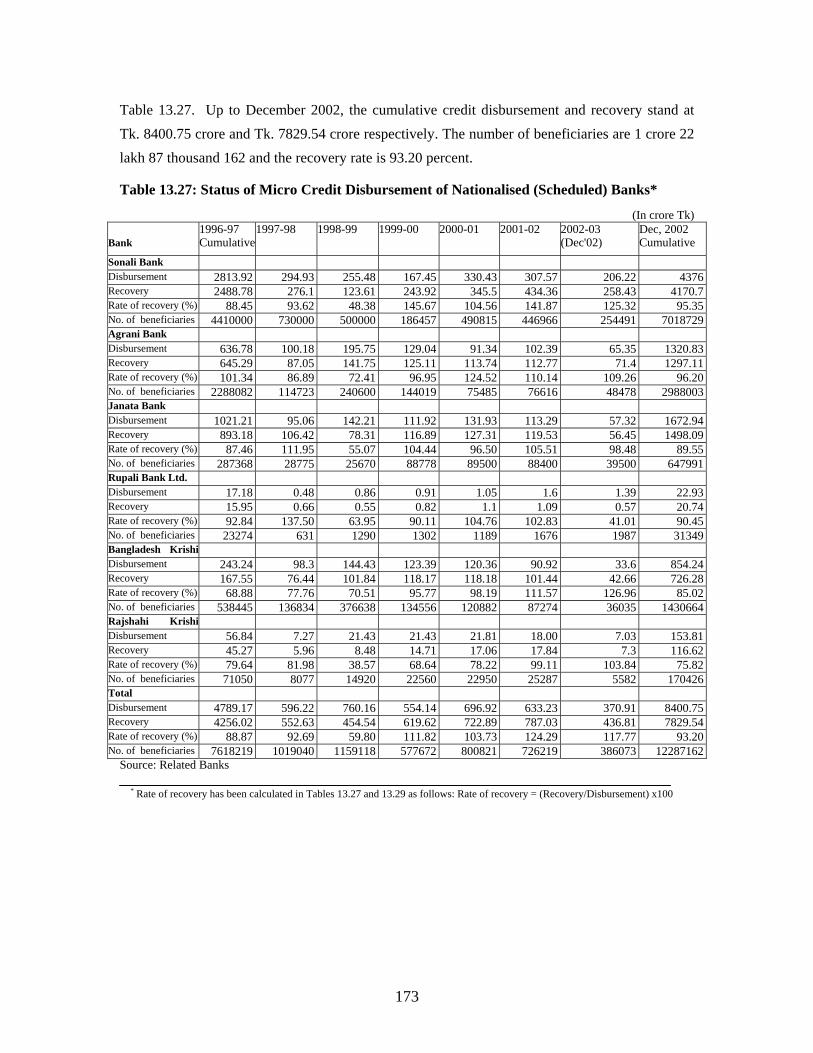

13.27 Status of Micro Credit Disbursement of Nationalized (Scheduled) Banks 173

xi

Table Title Page

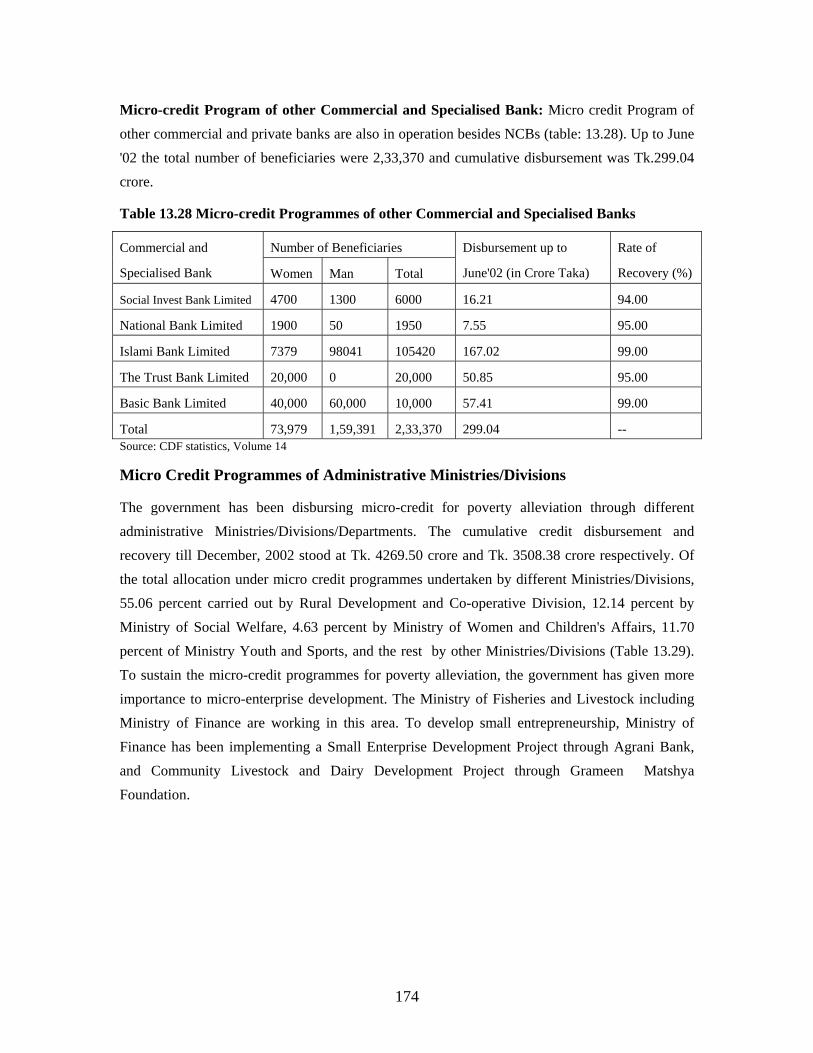

13.28 Micro Credit Programmes of other Commercial and Specialised Banks 174

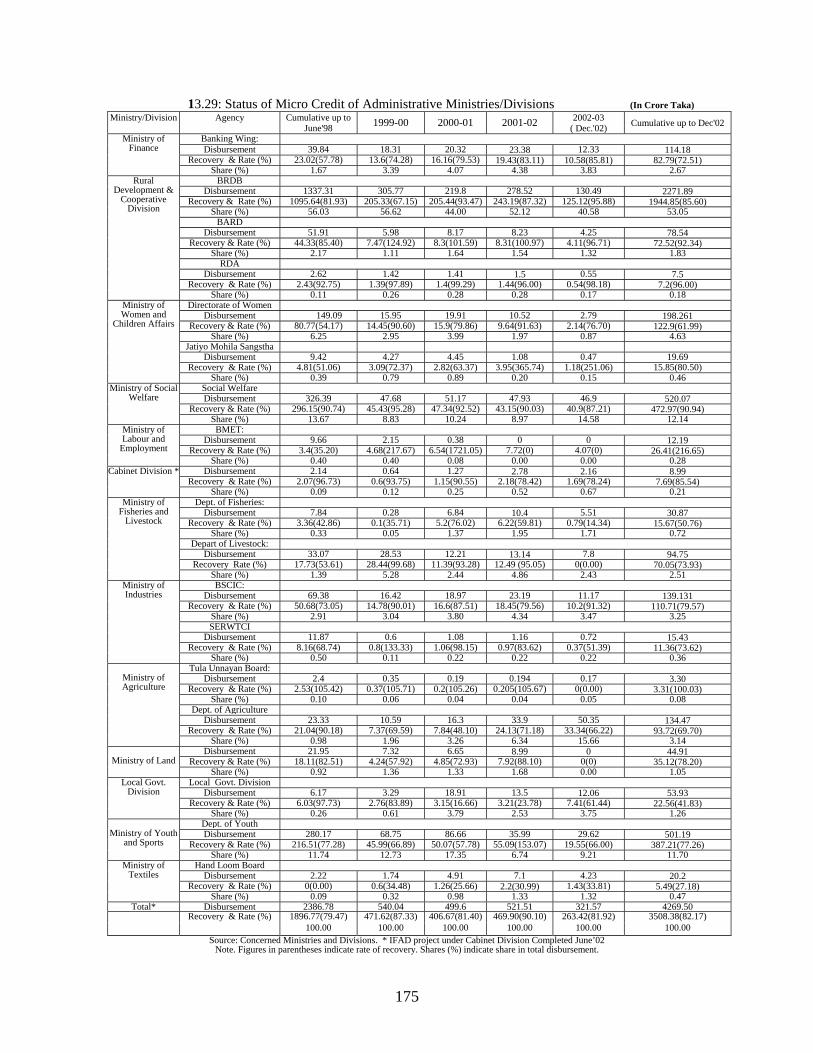

13.29 Status of Micro Credit of Administrative Ministires/Divisions 175

14.1 Number of Primary Schools in the Government and Private Sector 187

LIST OF GRAPHS

Graph Title Page

2.1 Growth Rate of GDP at Constant Price 19

2.2.1 Contribution of Broad Sectors in GDP of 1991-92 23

2.2.2 Contribution of Broad Sectors in GDP of 2002-03 23

2.3 Saving as Percentage of GDP 24

2.4 Investment as Percentage of GDP 25

3.1 National Inflation Rate 26

3.2 Point-to-Point Rate of Inflation (National) 27

3.3 Wage Rate Index 28

3.4 Share of Employed Labour Force by Broad Sector in Bangladesh

Labour Force Survey, 1999-00

29

3.5 Number of Expatriates Bangladeshi and their Remittances 30

3.6 Number of Expatriates Classified by Skill 30

3.7 Rate of Expatriates Bangladeshi by Country in 2002 31

5.1 Trend of the Money Supply 43

5.2 Composition of the Money Supply 43

6.1 Foreign Exchange Reserve 56

6.2 Trade Deficit and Current Account Balance 59

7.1 Growth Rate of Agriculture Sector in GDP 62

7.2 Contribution of Agriculture and Fishery Sector in GDP of

2001-02

62

7.3 Contribution of Sub-sectors of Agriculture Sector in GDP of

2001-02

62

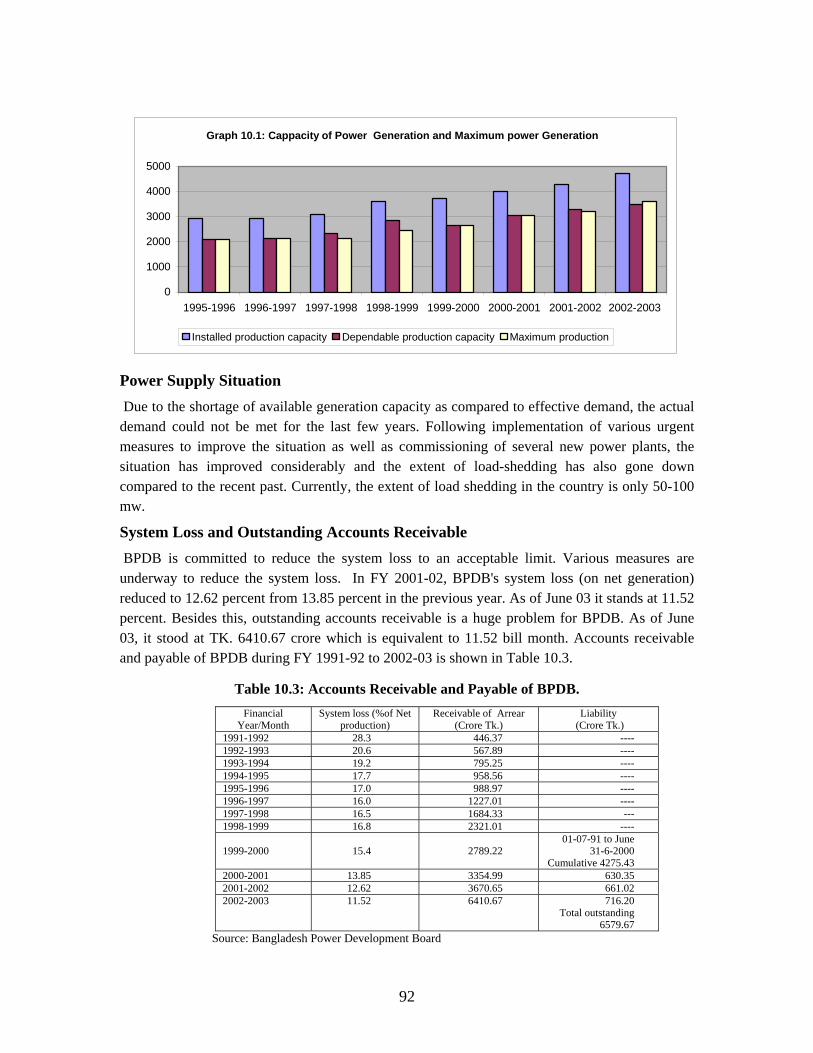

10.1 Capacity of Power Generation and Maximum Power Generation 92

10.2 System Loss of DESA 95

10.3 Target and Achievement of Distribution Line for Rural

Electrification

99

xii

Graph Title Page

10.4 Sector-wise Demands for the Use of Natural Gas 102

11.1 Allocation of Transport, LGED and Communication Sectors in

the RADP of 2002-03

109

11.2 Total RADP Allocation of LBED for 2002-03 111

11.3 The Number of Telephones of BTTB Over the Years 124

12.1 Government Allocation for Social Sectors since 1991-92 to

2002-03

130

12.2 Trend of Maternal and Child Mortality 136

13.1 Situation of Poverty and Hardcore Poverty 146

13.2 Division wise Rate of Poverty 147

13.3 Poverty Incidence by Owned Land Size 149

13.4 Per Capita Expenditure on Consumer Goods and Services 153

13.5 Human Poverty Index 155

14.1 Customer Distribution of Different Private Cellular Mobile

Companies (in Thousands)

183

14.2 Year-wise Information on the Number of Government and

Private Primary School

187

LIST OF BOXES

Box Title Page

1.1 Millennium Development Goals 4

1.2 Medium-Term Macroeconomic Framework: Key Indicators 12

4.1 Measures under Direct Taxes 34

4.2 Measures under Indirect Taxes 34

7.1 Main Objectives of the National Agriculture Policy 61

11.1 Recovery Programme of Bangladesh Railway 116

11.2 Cost Reduction Measures of Biman 123

11.3 Special Services of the Postal Department 126

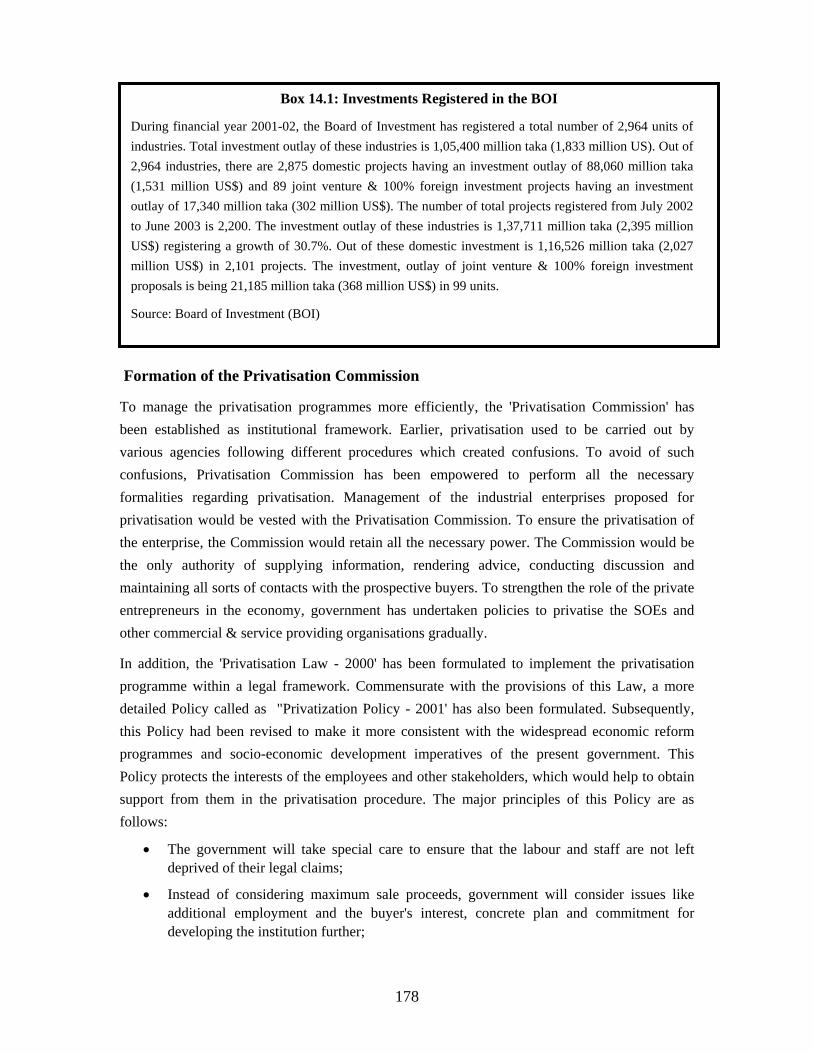

14.1 Investments Registered in the BOI 178

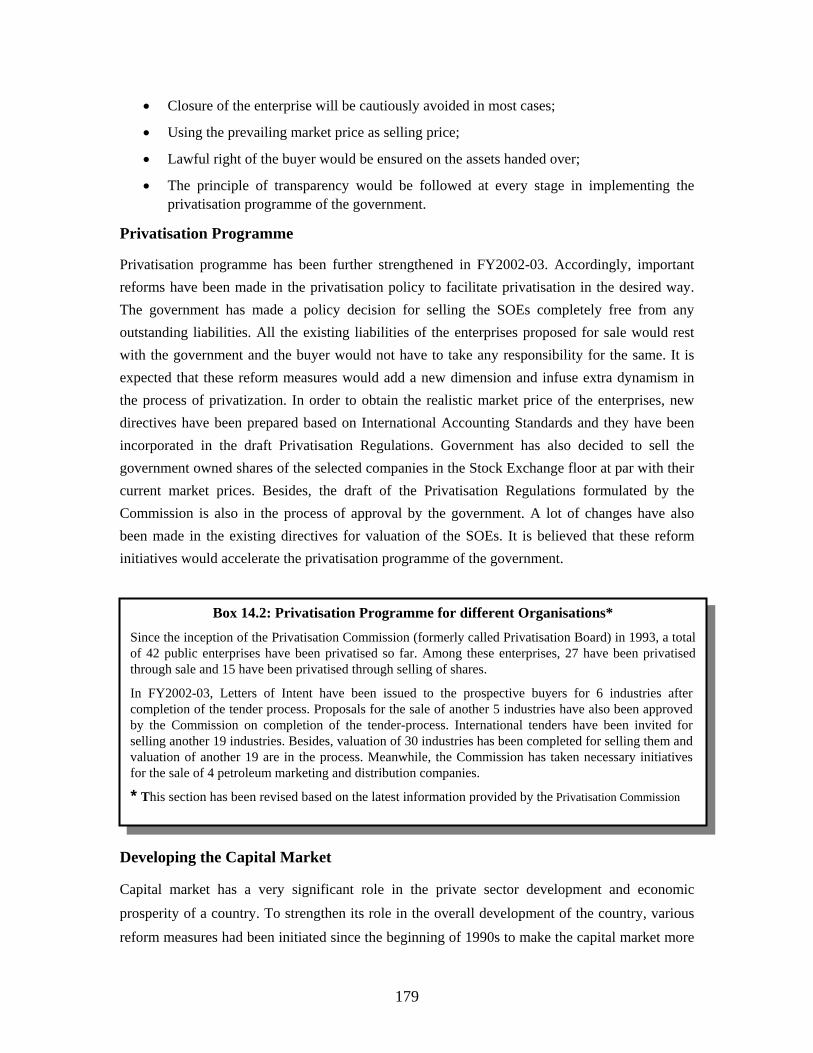

14.2 Privatisation Programme for Different Organisations 179

14.3 General Objectives of Bangladesh Telecommunication

Regulatory Commission

184

xiii

LIST OF STATISTICAL APPENDICES

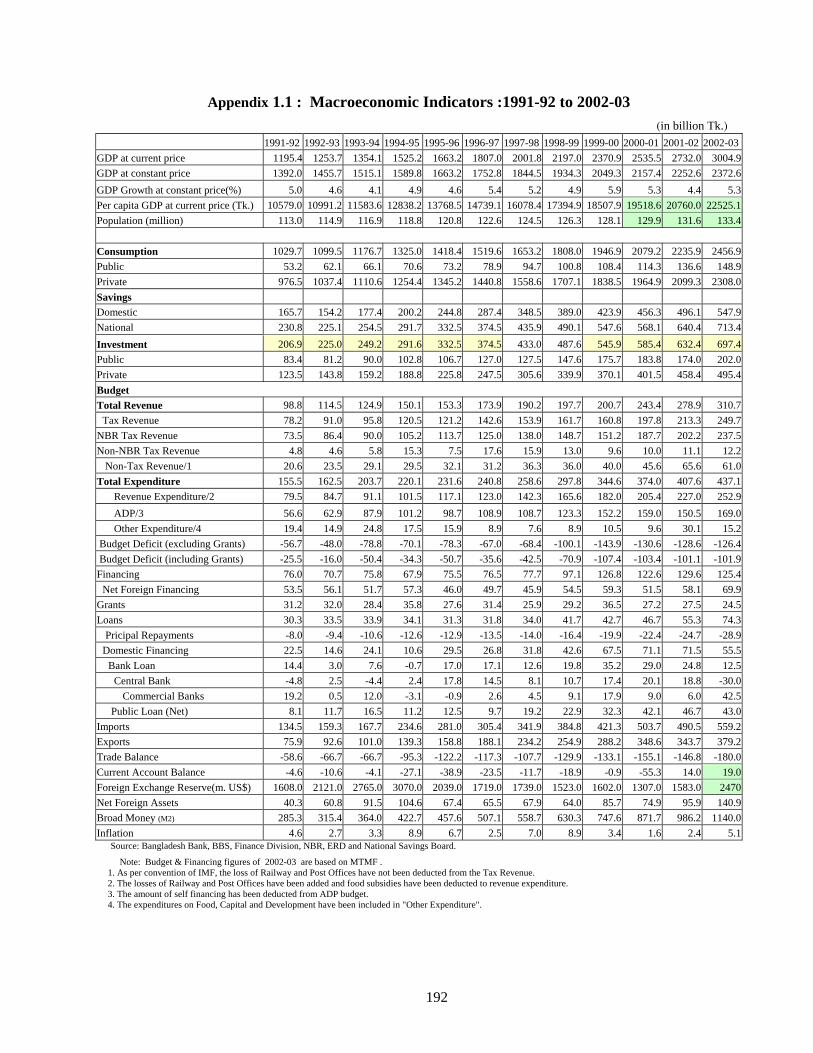

Appendix Title Page 1.1 Macroeconomic Indicators: 1991-92-2002-03 192

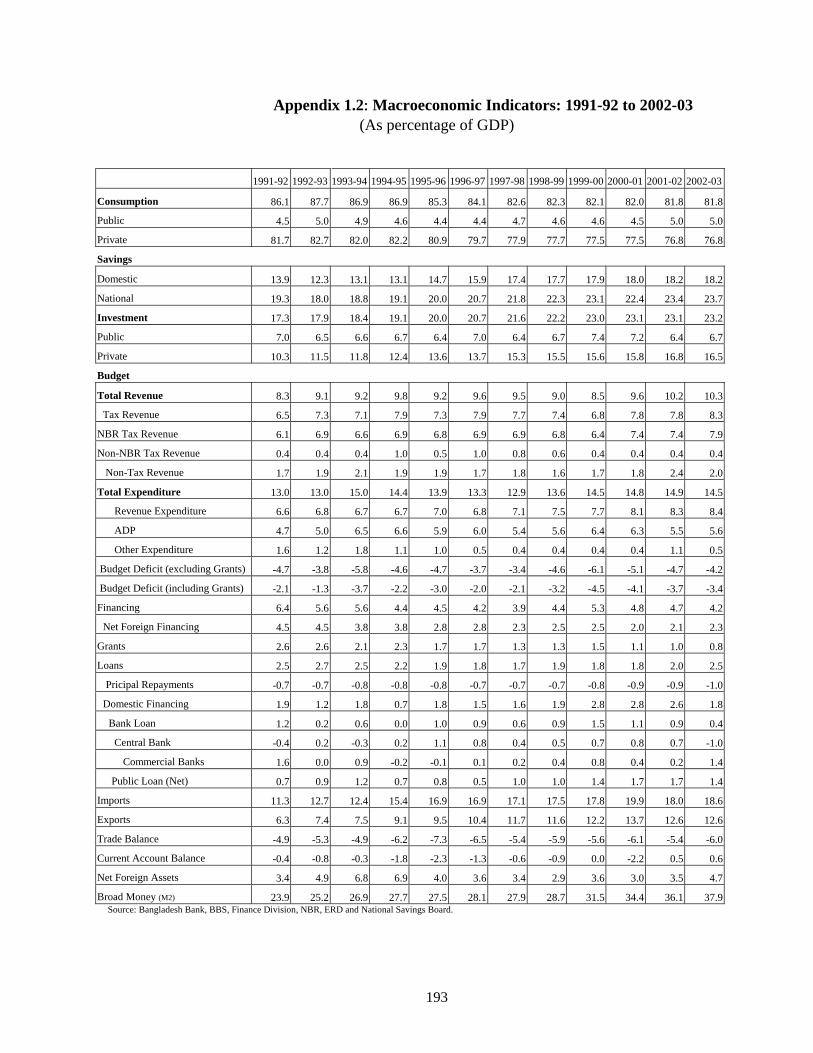

1.2 Macroeconomic Indicators: 1991-92-2002-03 (As Percentage of GDP) 193

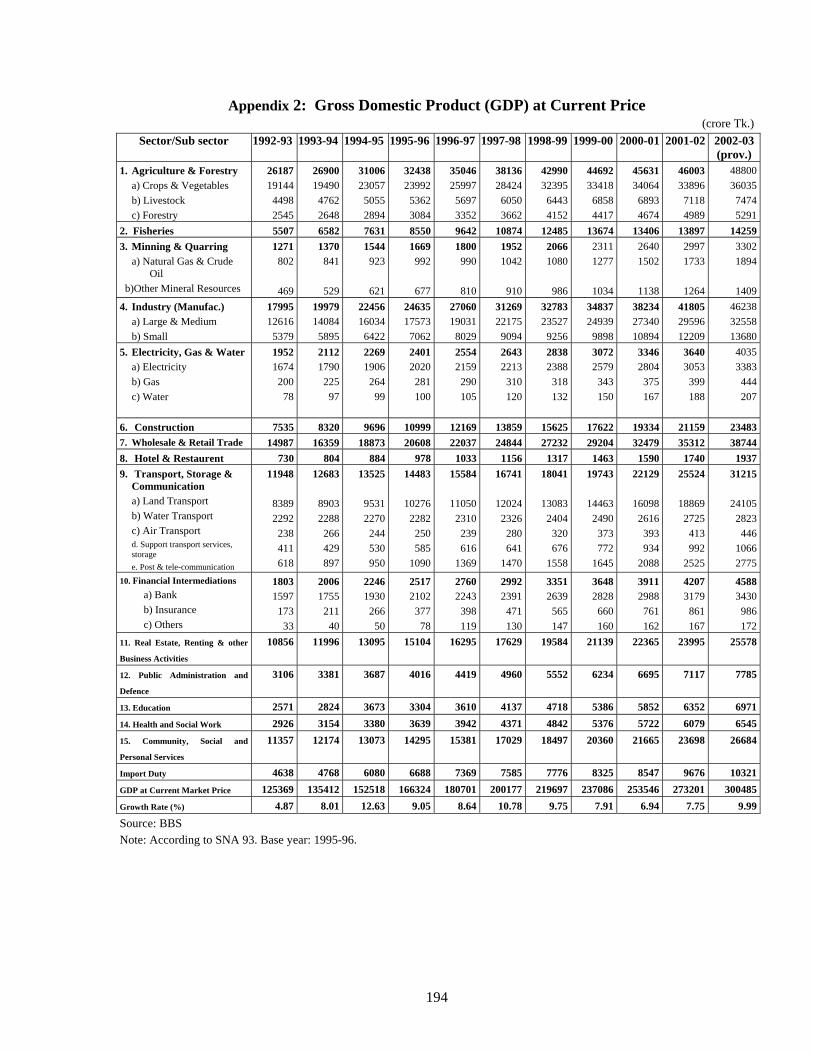

2. Gross Domestic Product (GDP) at Current Price 194

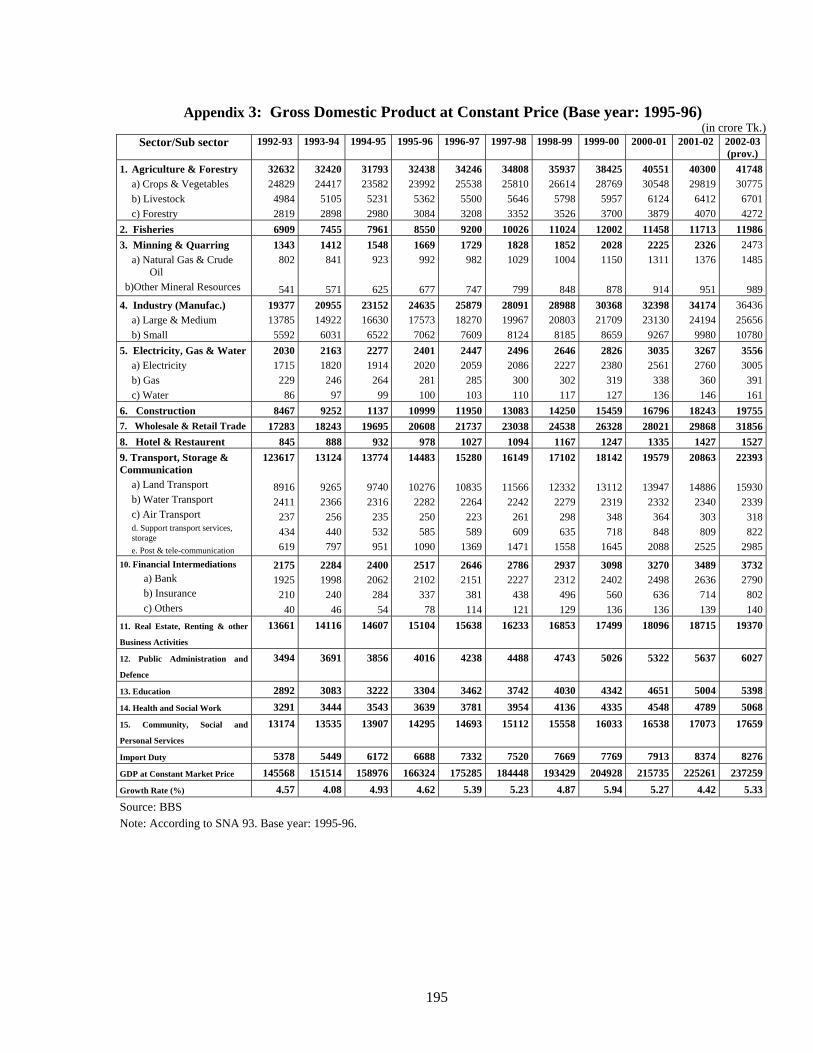

3. Gross Domestic Product at Constant Price (Base Year: 1995-96) 195

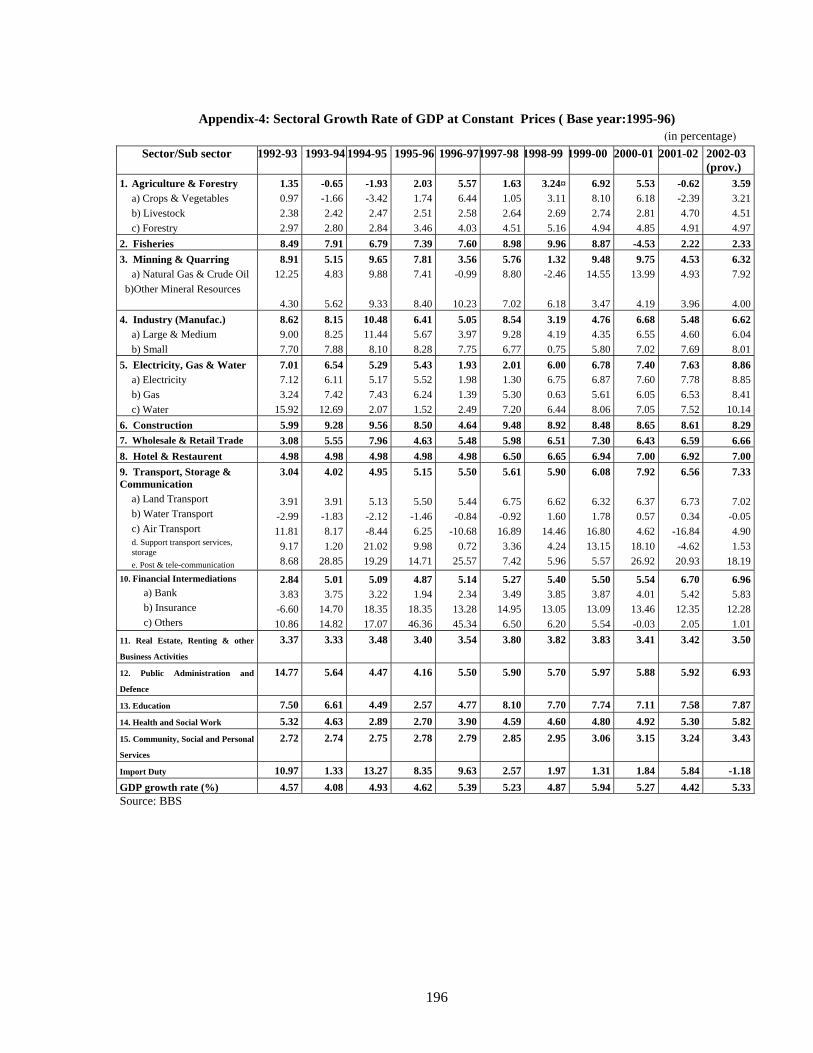

4. Sectoral Growth Rate of GDP [at Constant (1995-96) Prices] 196

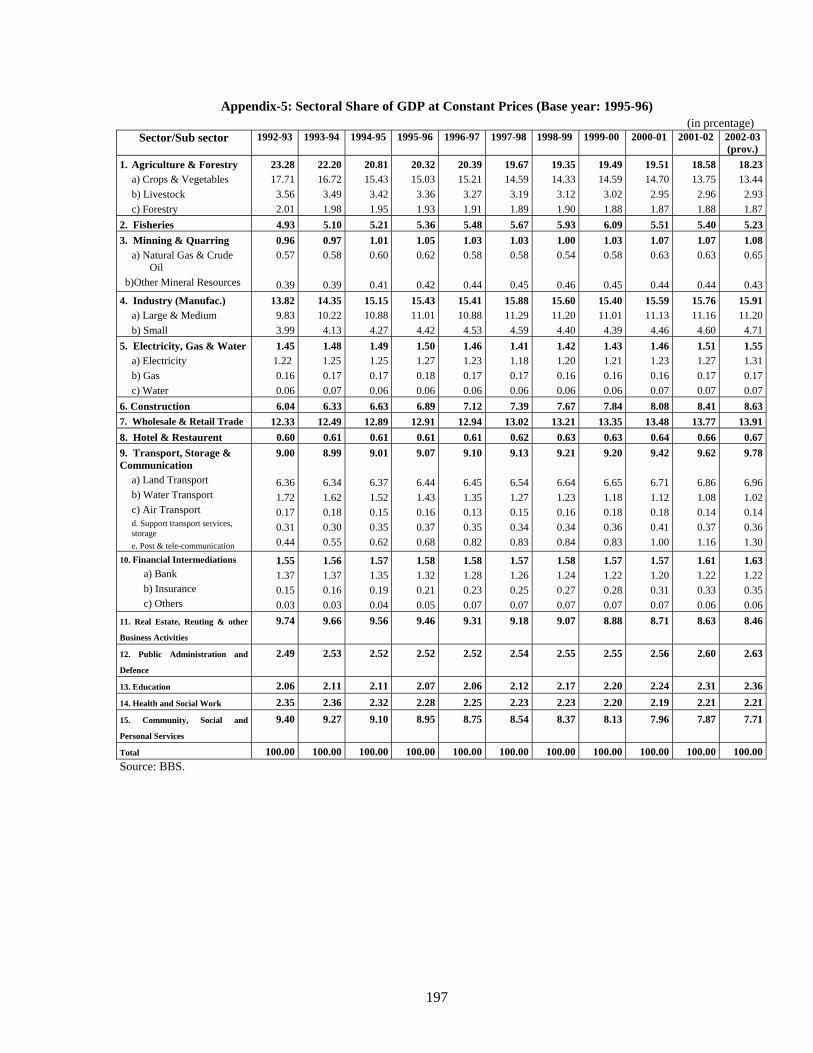

5. Sectoral Share of GDP (%) at Constant Prices (1995-96) 197

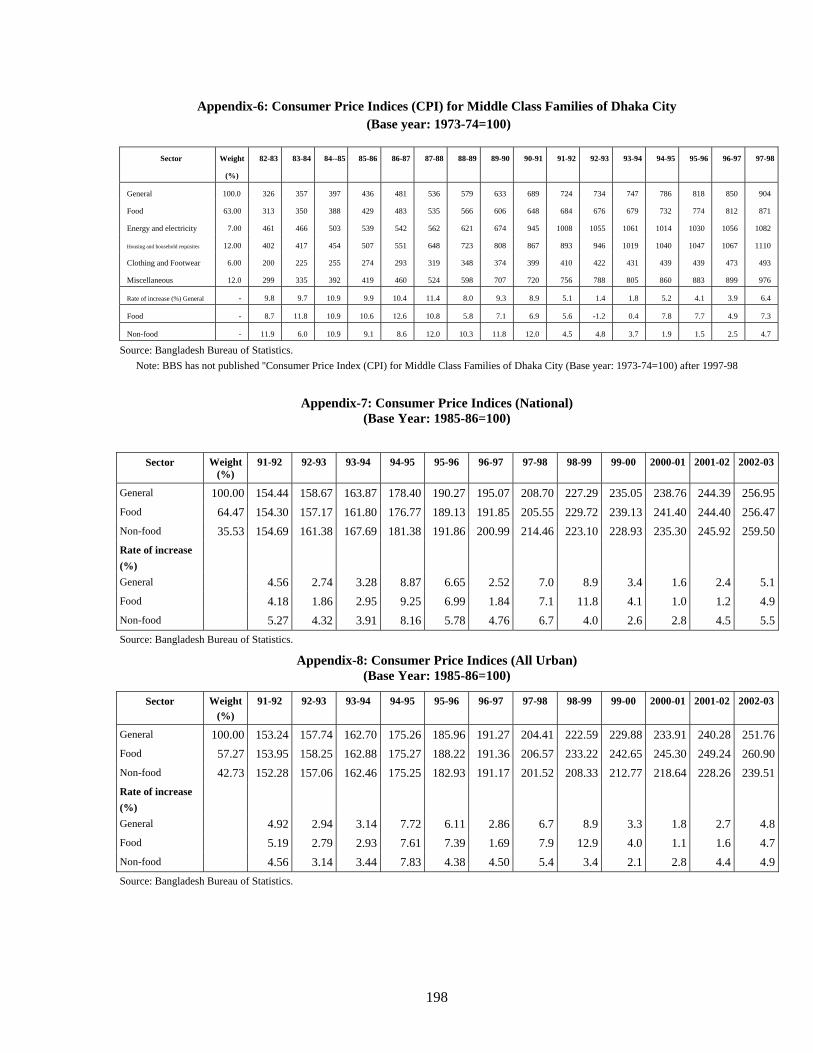

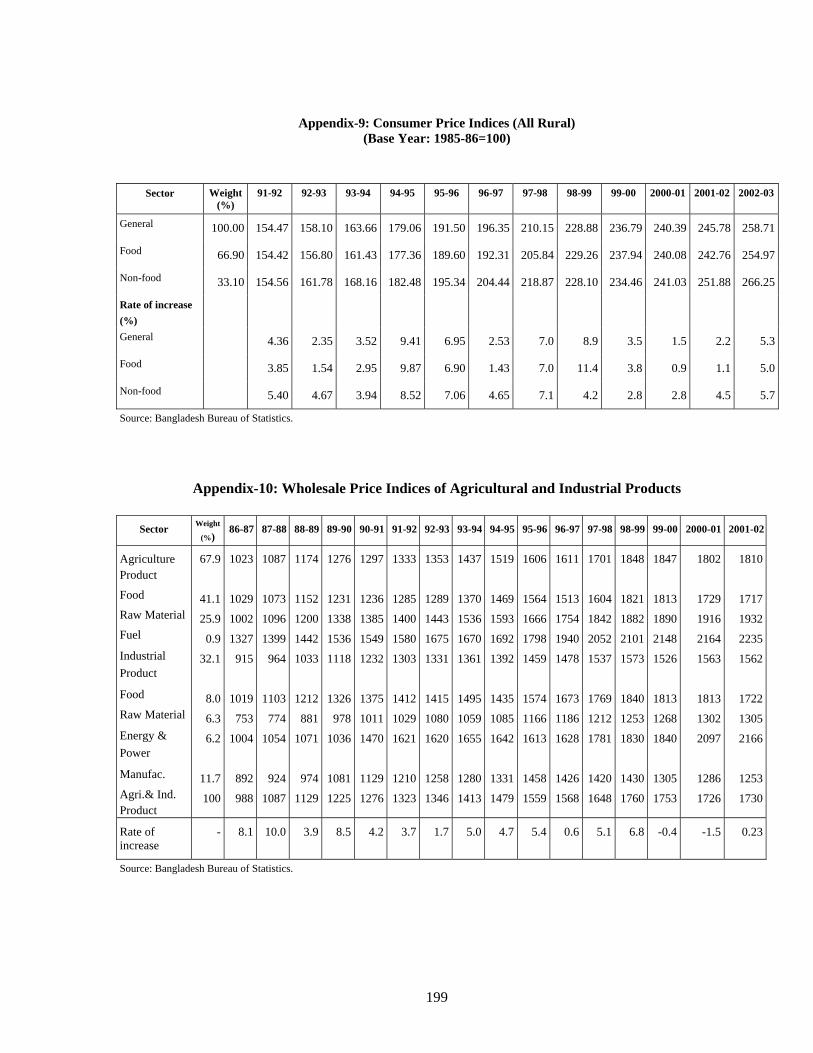

6. Consumer Price Indices (CPI) for Middle Class Families of Dhaka City (Base year: 1973-74=100)

198

7. Consumer Price Indices-National (Base Year: 1985-86=100) 198

8. Consumer Price Indices-All Urban (Base Year: 1985-86=100) 198

9. Consumer Price Indices-All Rural (Base Year: 1985-86=100) 199

10. Wholesale Price Indices of Agricultural and Industrial Products 199

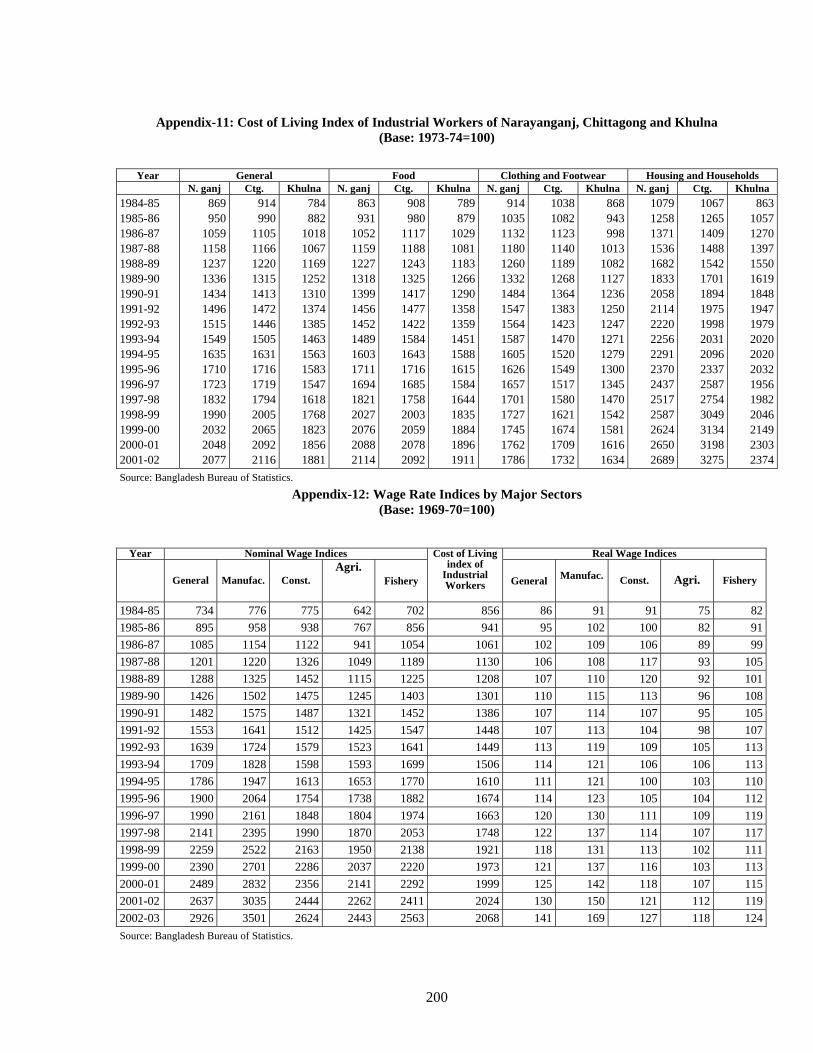

11. Cost of Living Index of Industrial Workers of Narayanganj, Chittagong and Khulna (Base Year: 1973-74=100)

200

12. Wage Rate Indices by Major Sectors (Base Year: 1969-70=100) 200

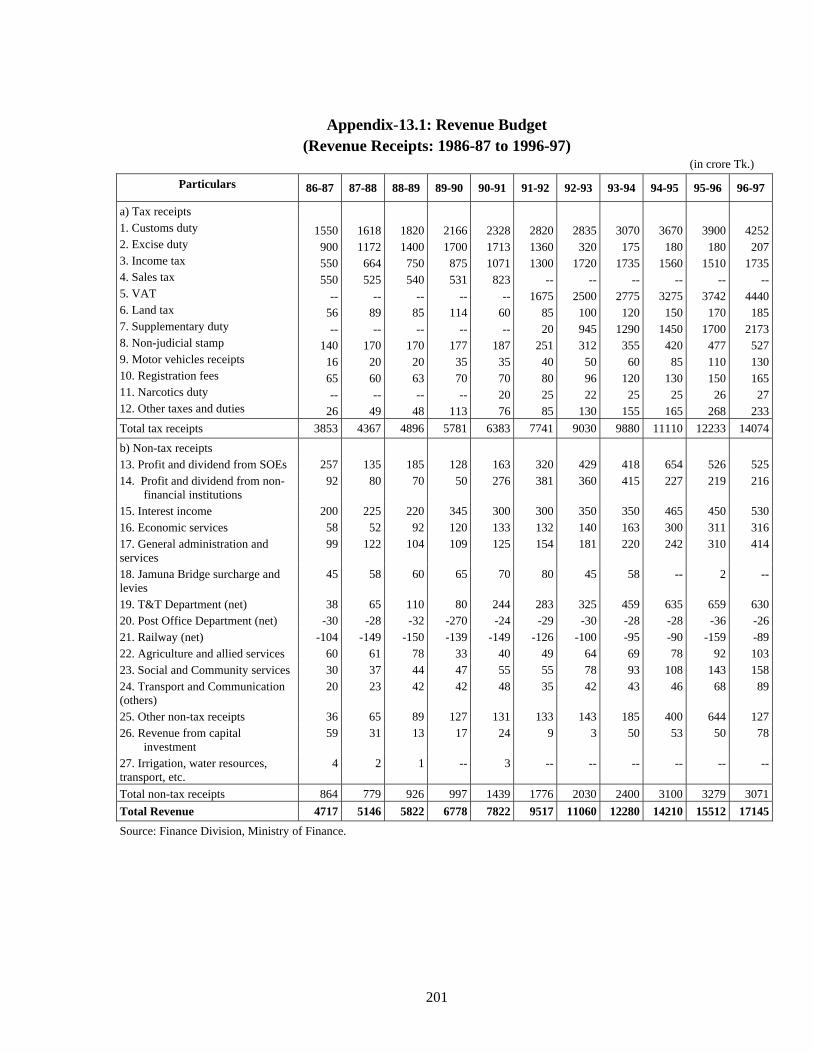

13.1. Revenue Budget (Revenue Receipts 1986-87 to 1996-97) 201

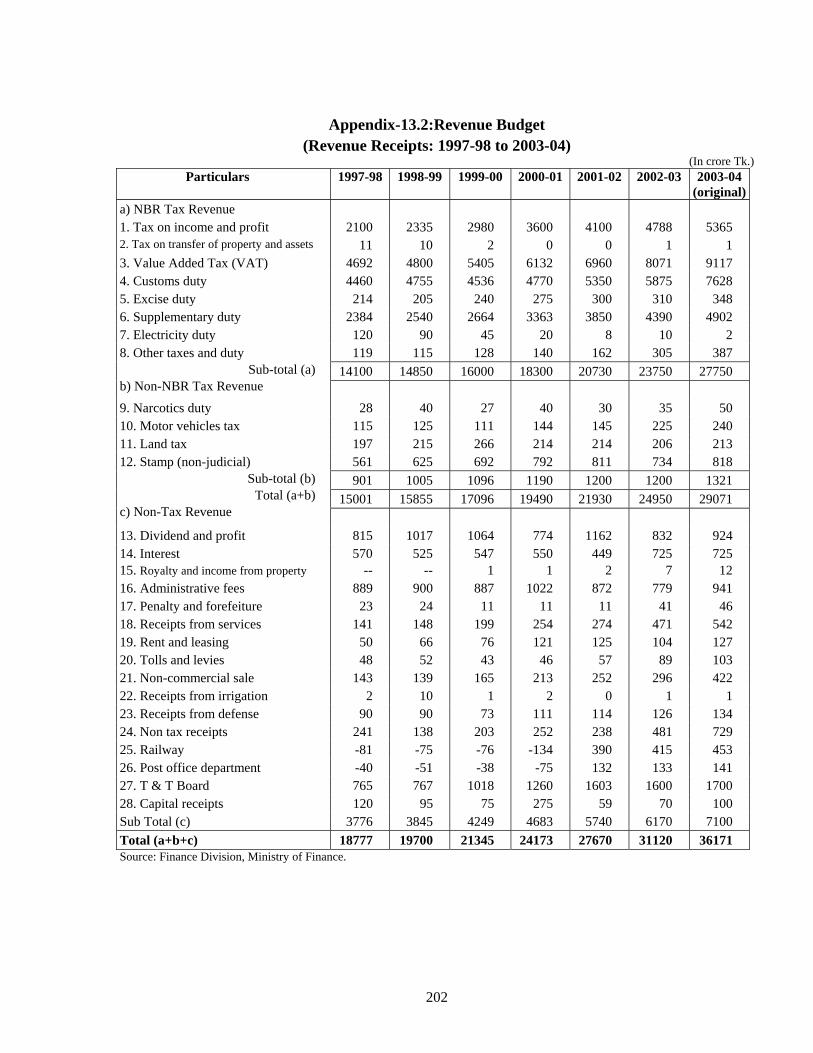

13.2. Revenue Budget (Revenue Receipts 1997-98 to 2003-04) 202

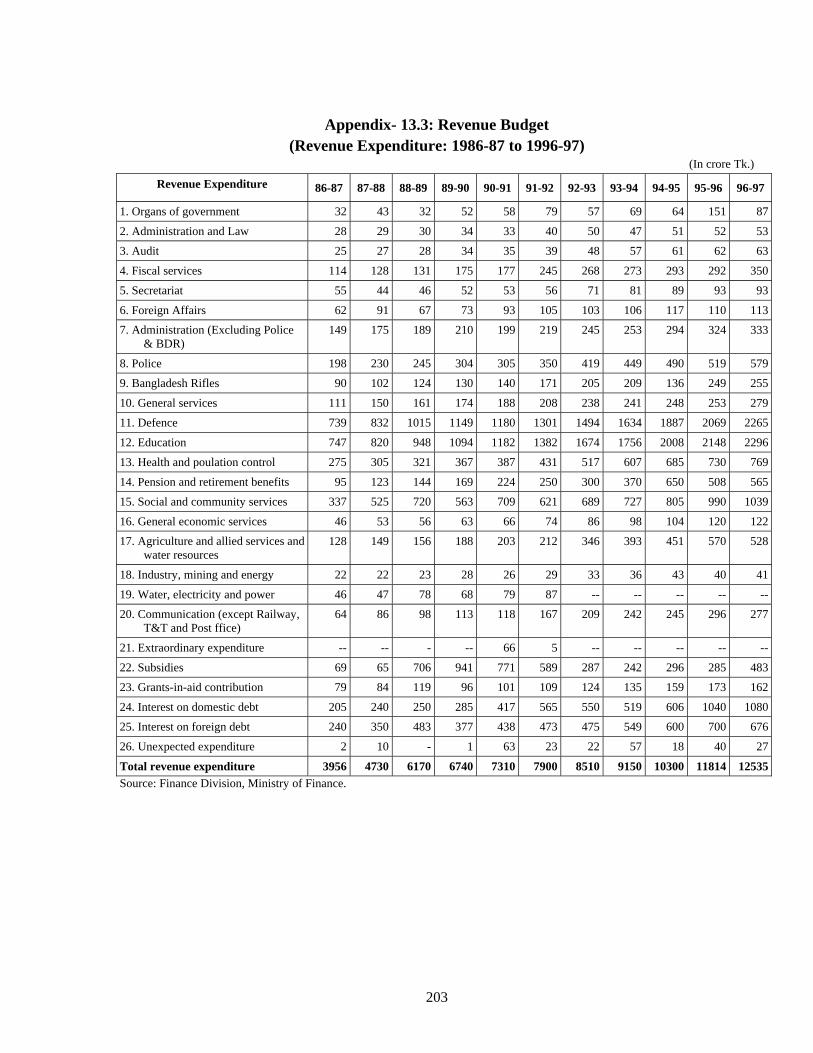

13.3. Revenue Budget (Revenue Expenditure 1986-87 to 1996-97) 203

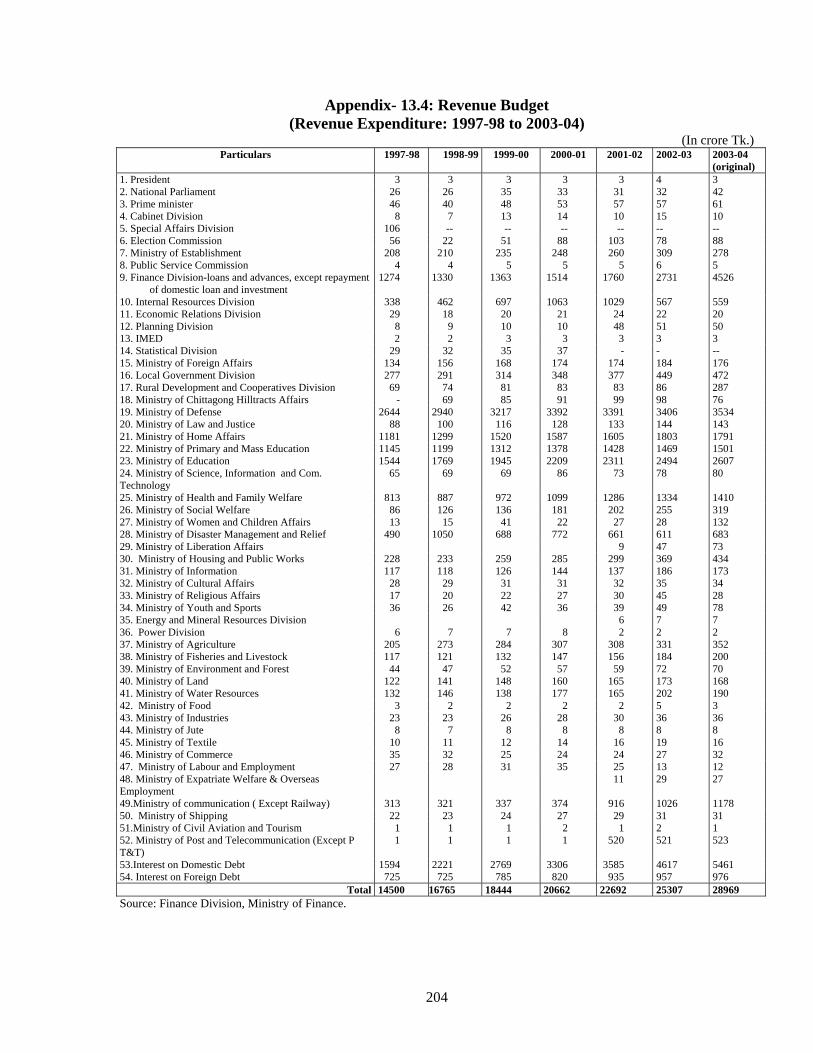

13.4. Revenue Budget (Revenue Expenditure 1997-98 to 2003-04) 204

14. Annual Development Programme (ADP) (Allocation and Expenditure) 205

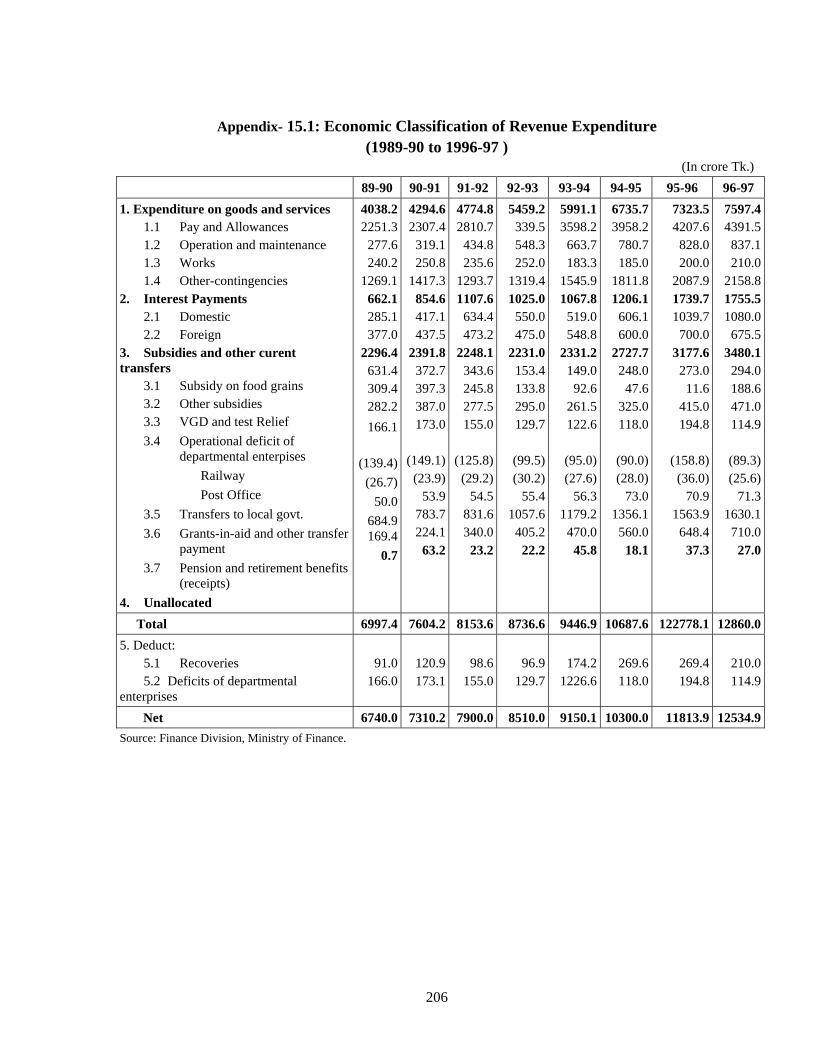

15.1. Economic Classification of Revenue Expenditure (1989-90 to 1996-97) 206

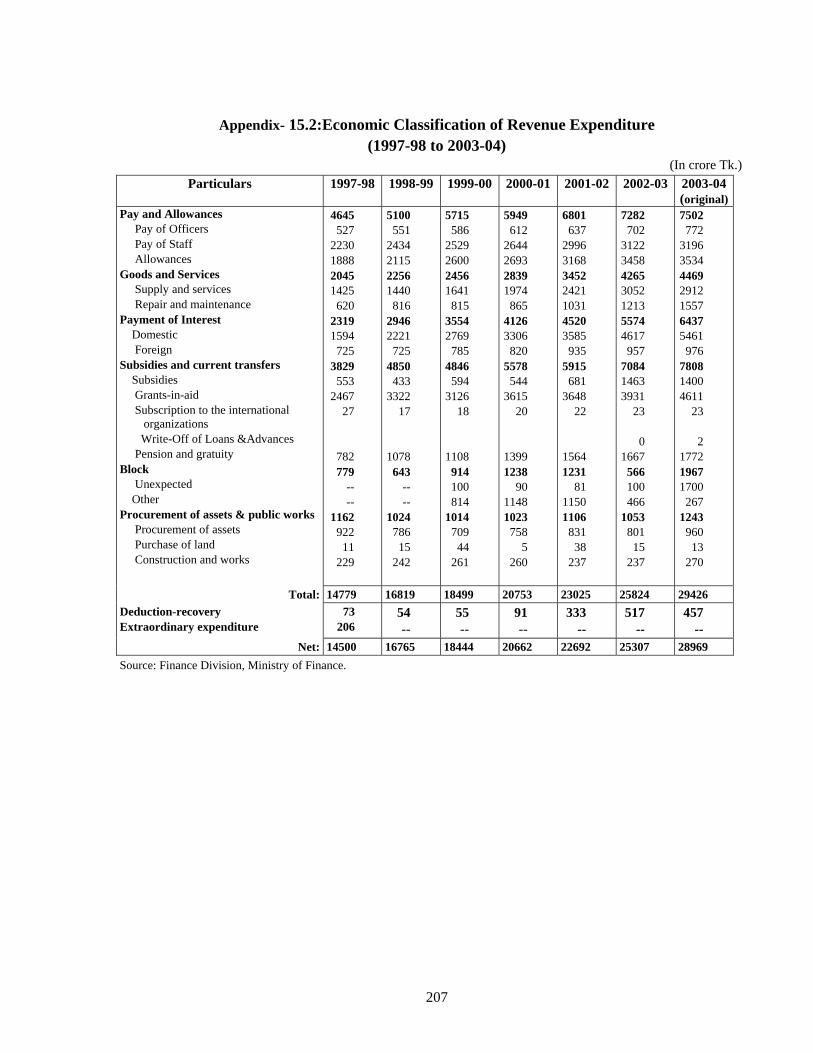

15.2. Economic Classification of Revenue Expenditure (1997-98 to 2003-04) 207

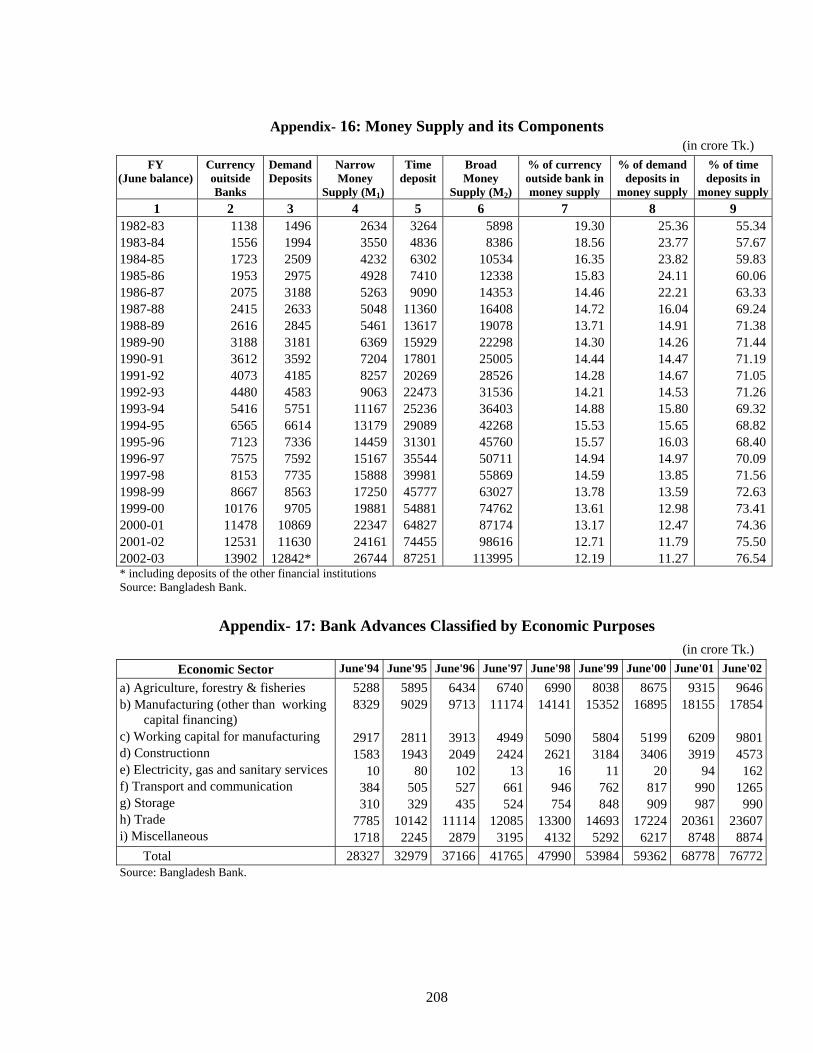

16. Money Supply and Its Components 208

17. Bank Advances Classified by Economic Purposes 208

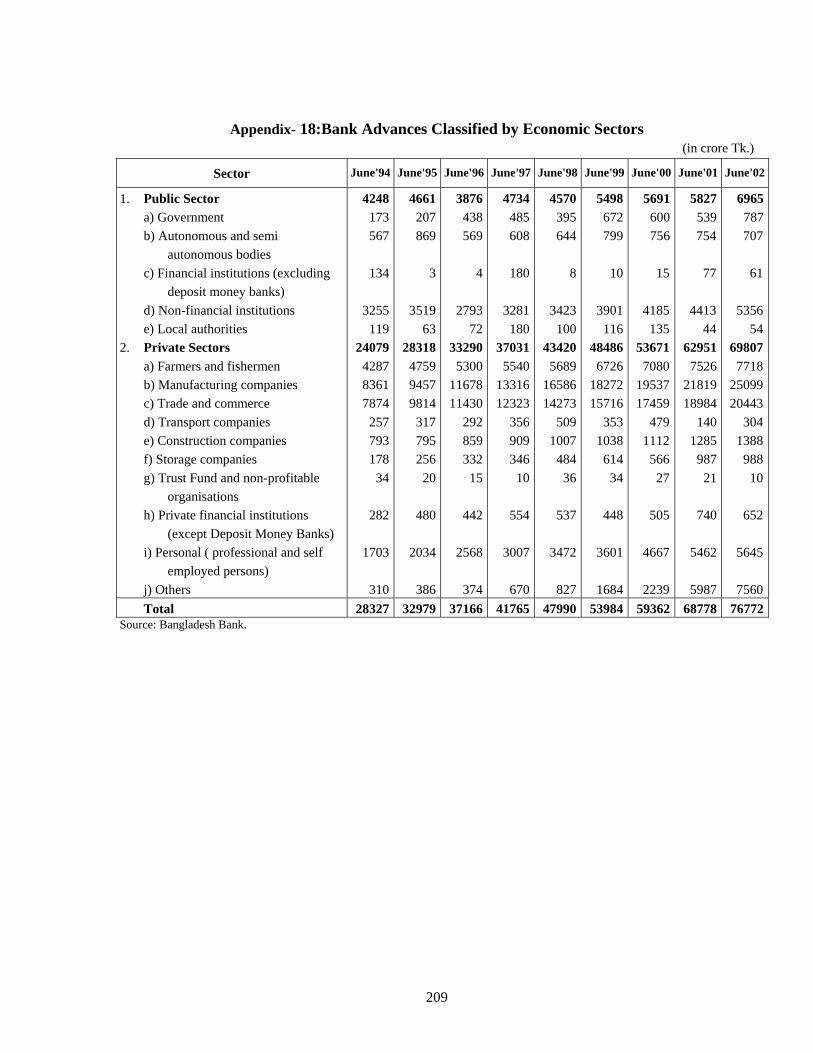

18. Bank Advances Classified by Economic Sectors 209

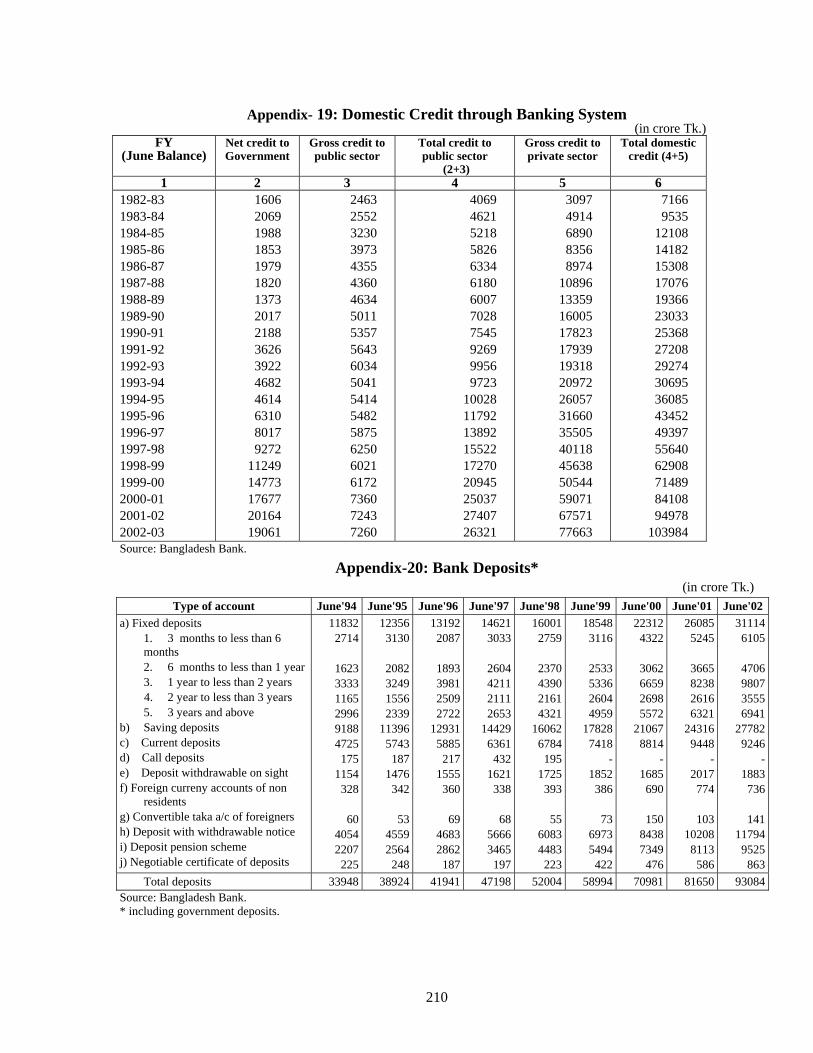

19. Domestic Credit through Banking System 210

20. Bank Deposits 210

21. Production of Major Agricultural Crops and Acreage 211

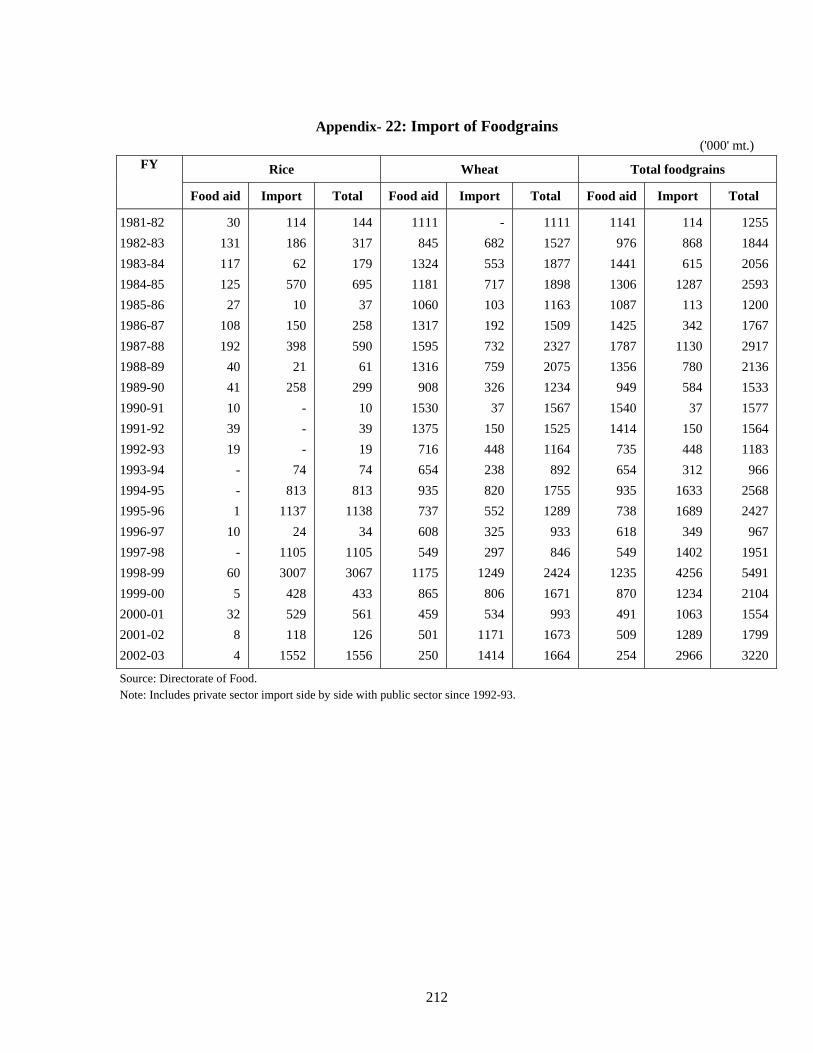

22. Import of Foodgrains 212

23. Agricultural Credit Disbursement, Recovery and Outstanding 213

24. Area Under Irrigation 213

25. Use of Chemical Fertilizer 213

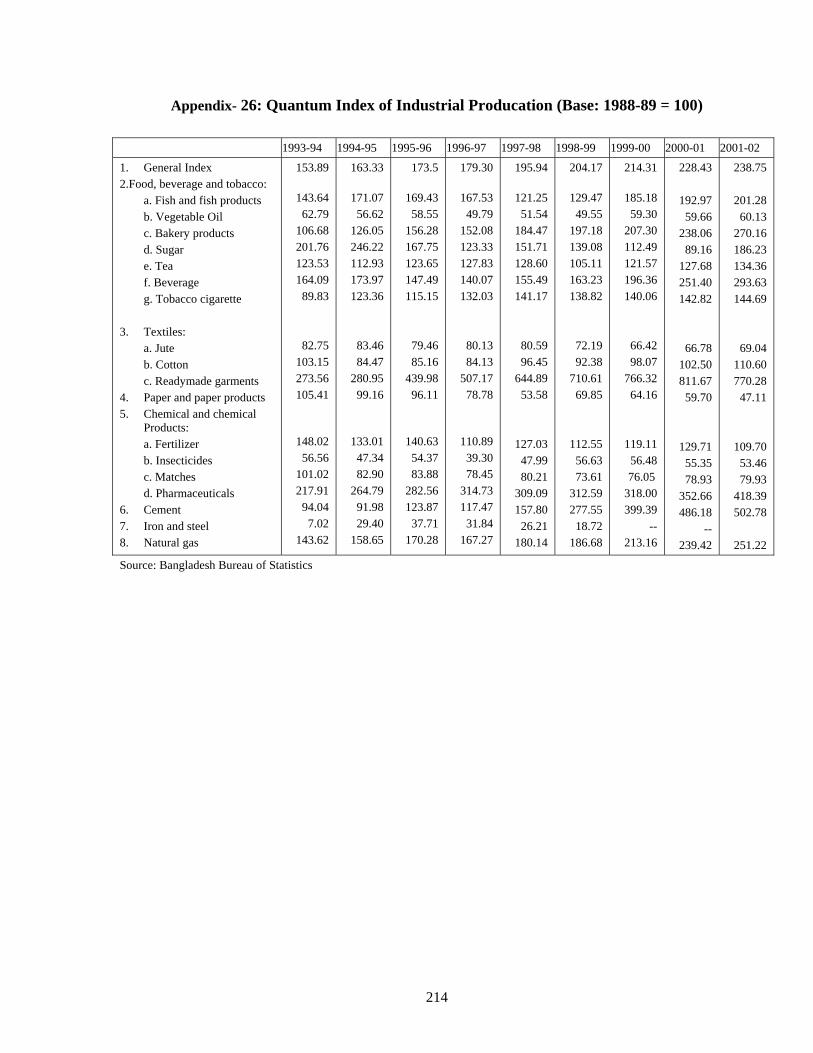

26. Quantum Index of Industrial Production (Base: 1988-89=100) 214

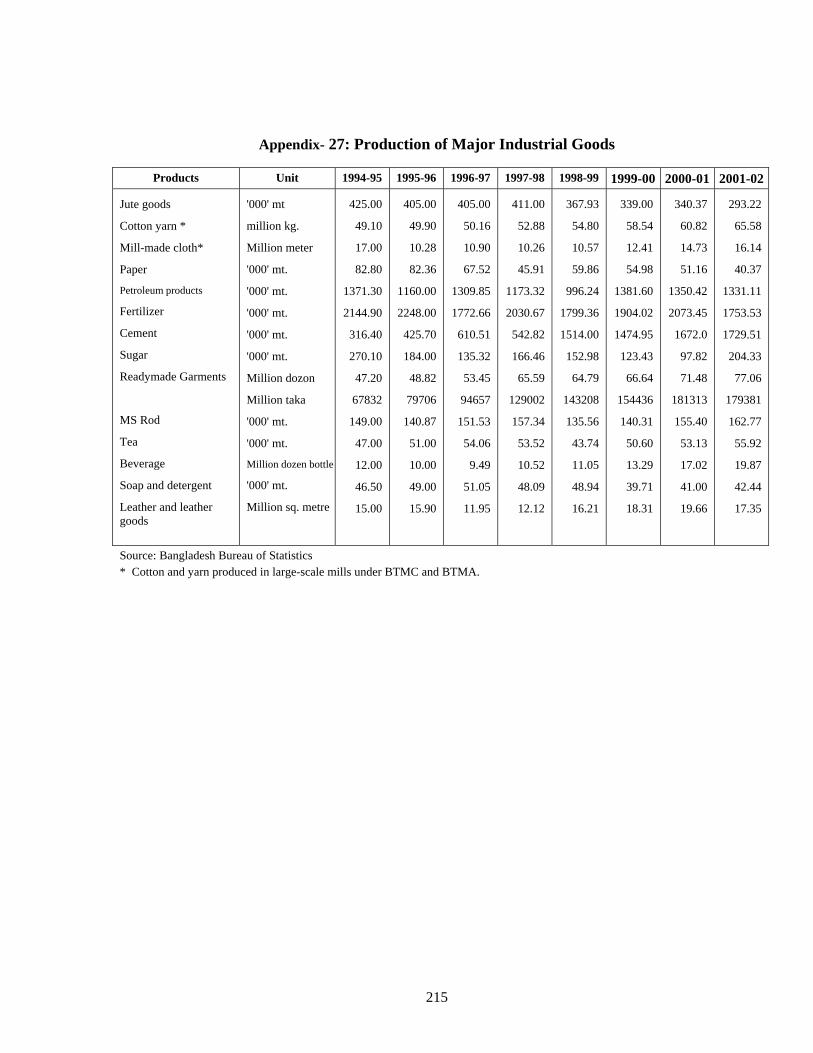

27. Production of Major Industrial Goods 215

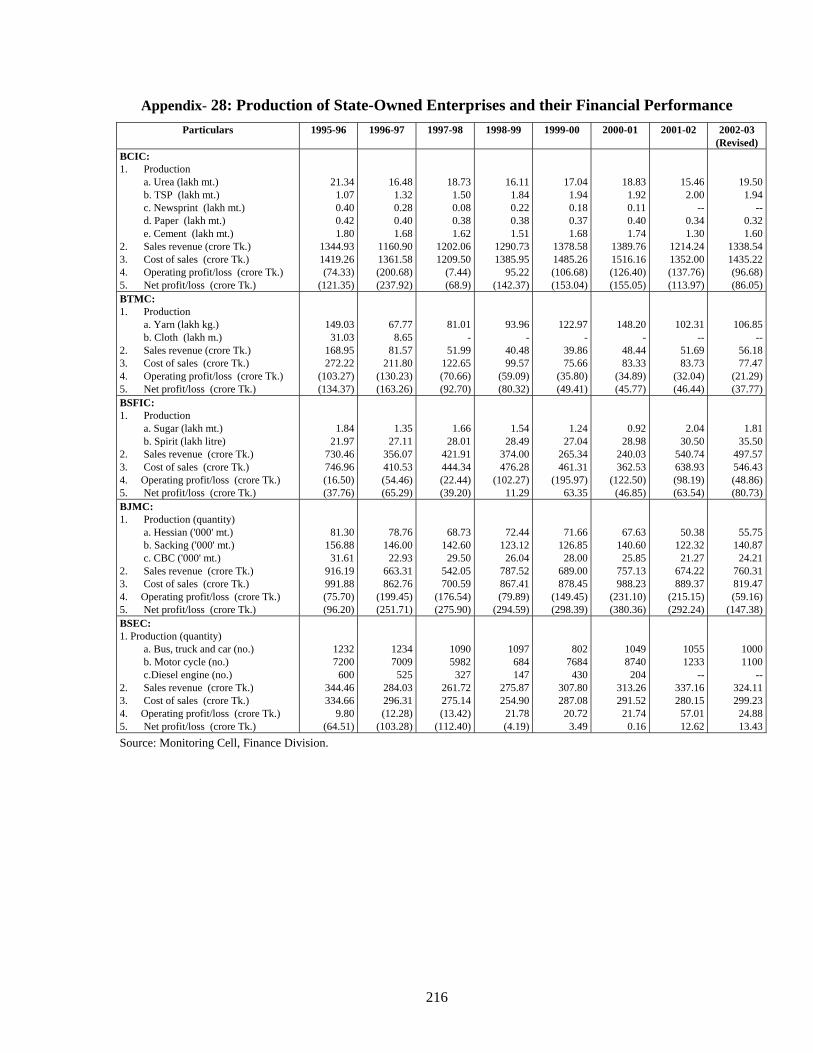

28. Production of State-Owned Enterprises (SOEs) and their Financial Performance 216

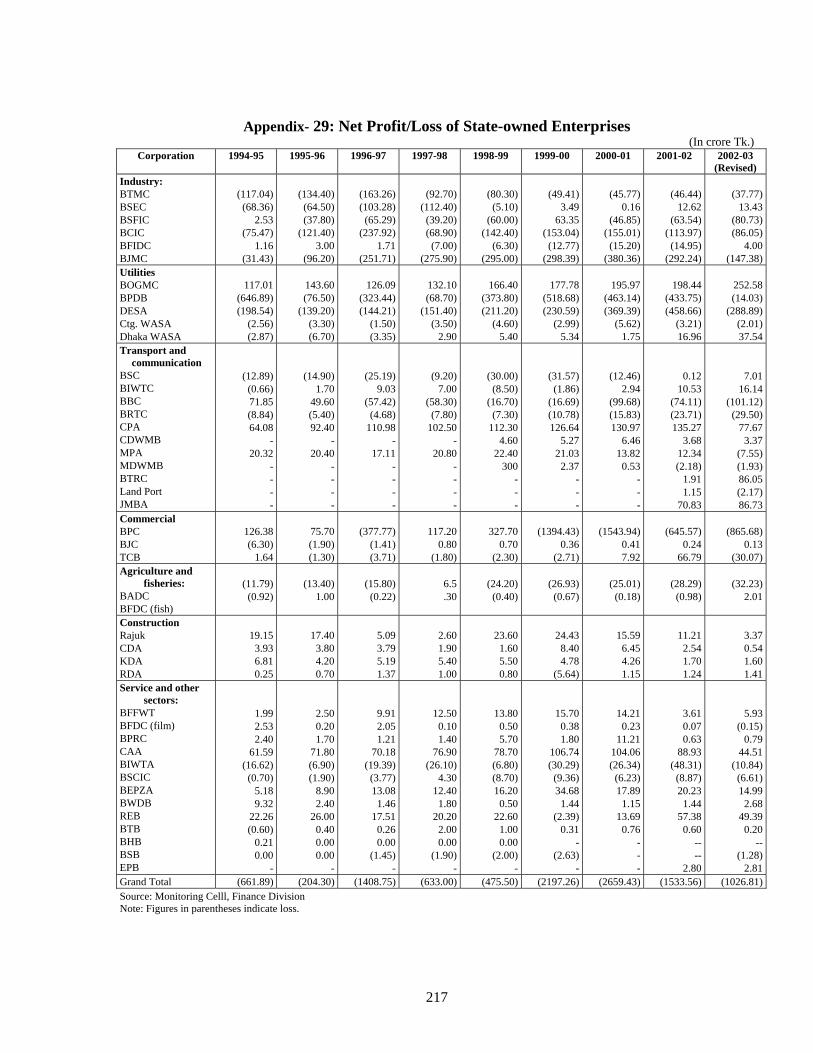

29. Net Profit/Loss of SOEs 217

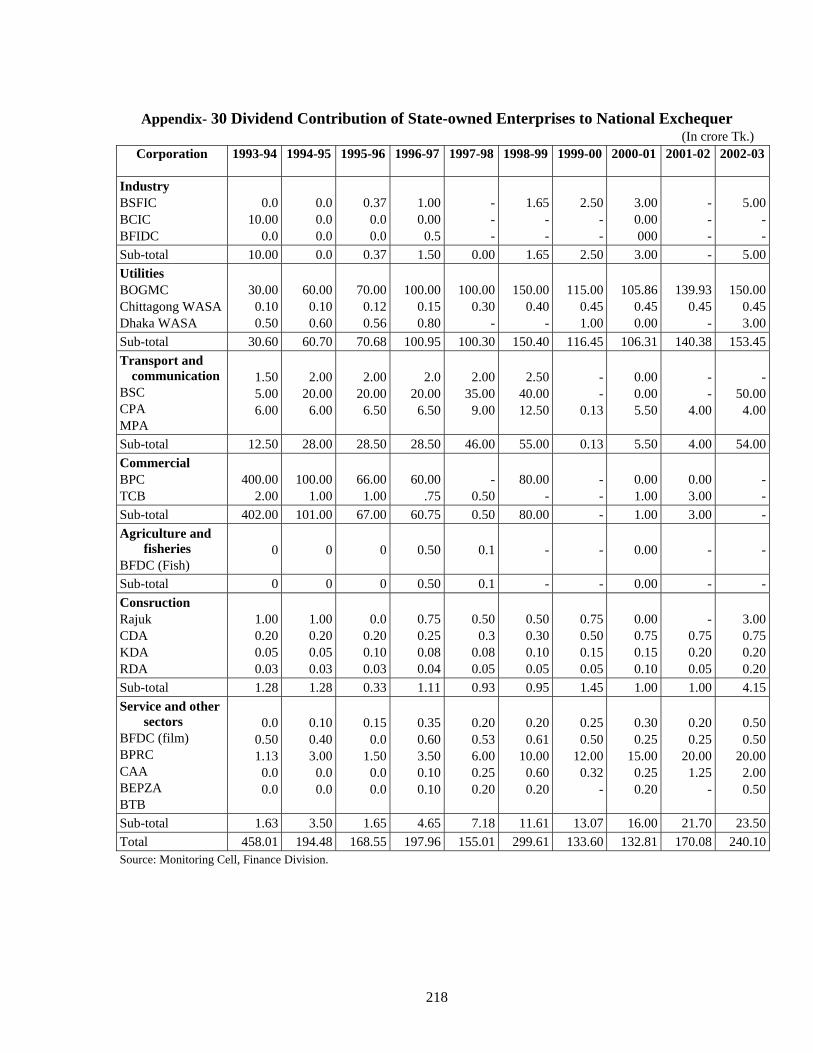

30. Dividend Contribution of SOEs 218

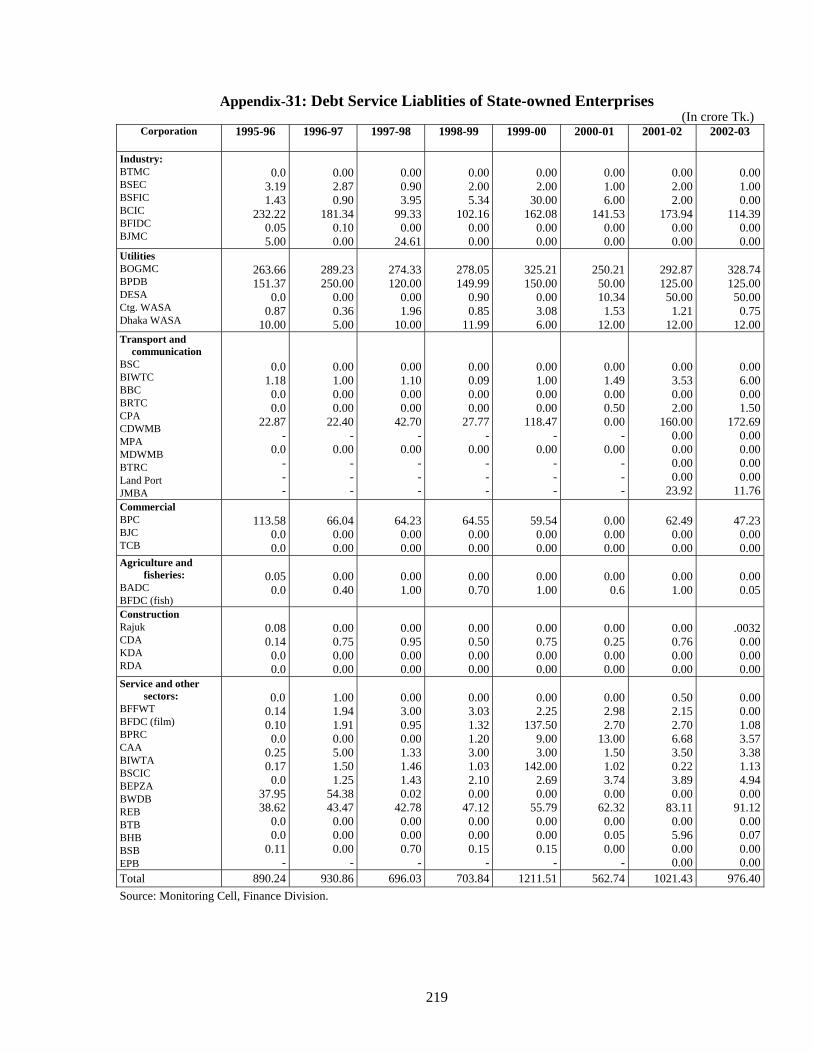

31. Debt Service Liabilities of SOEs 219

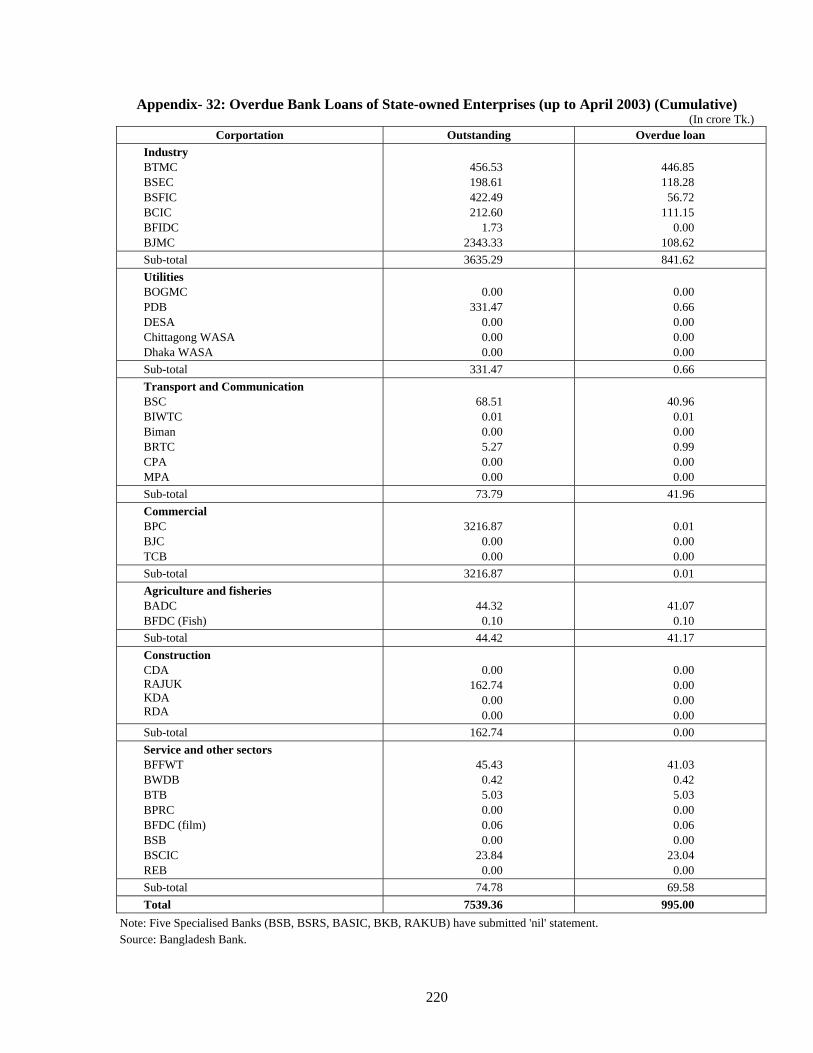

32. Overdue Bank Loans of SOEs (Up to April'03, cumulative) 220

xiv

Table Title Page

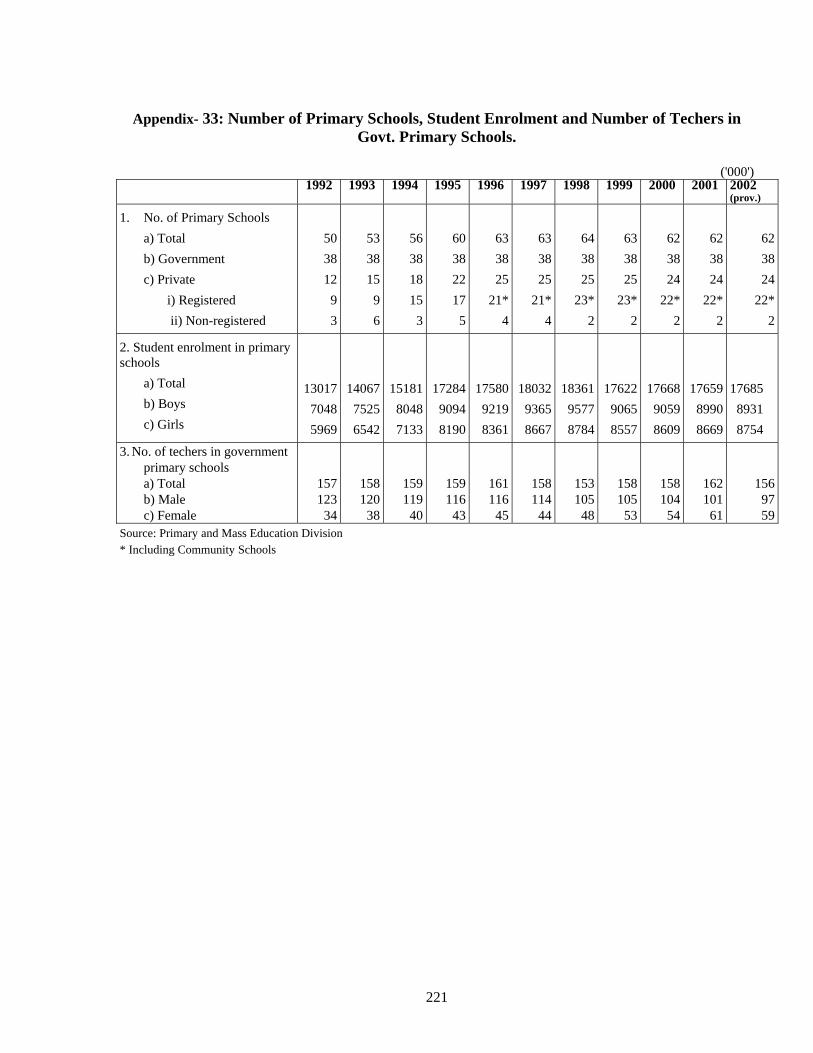

33. Number of Primary Schools, Student Enrolment and Number of Teachers in Govt. Primary Schools

221

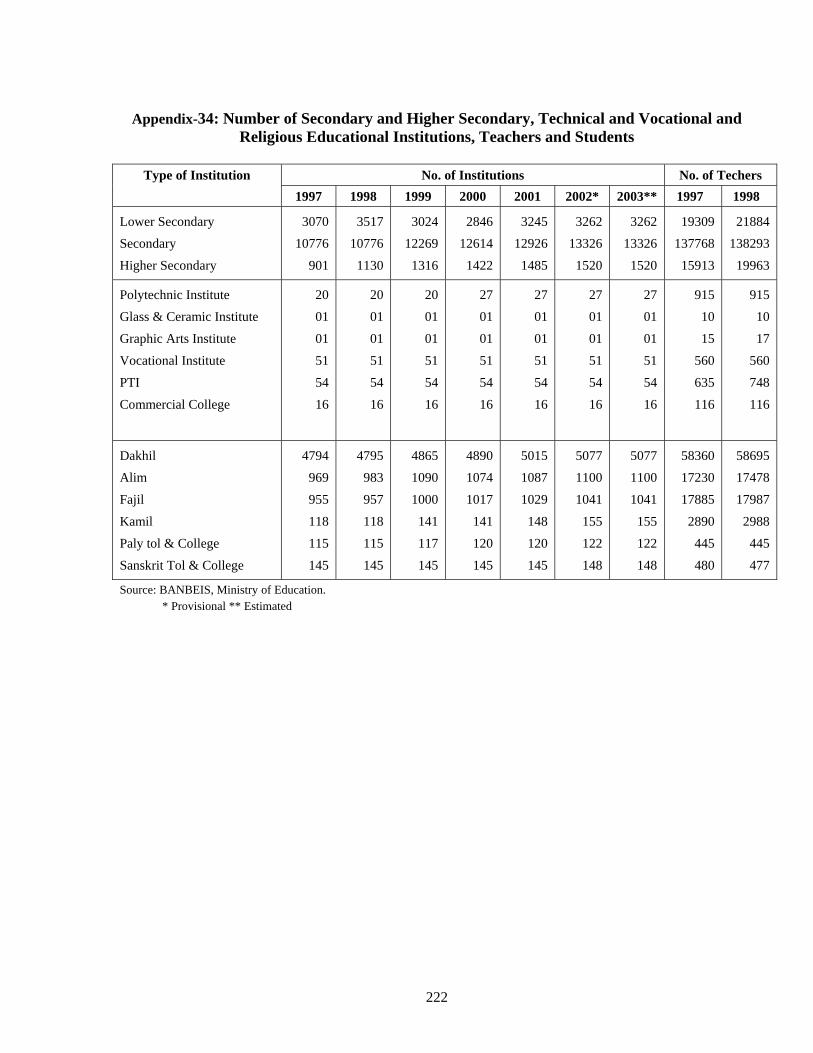

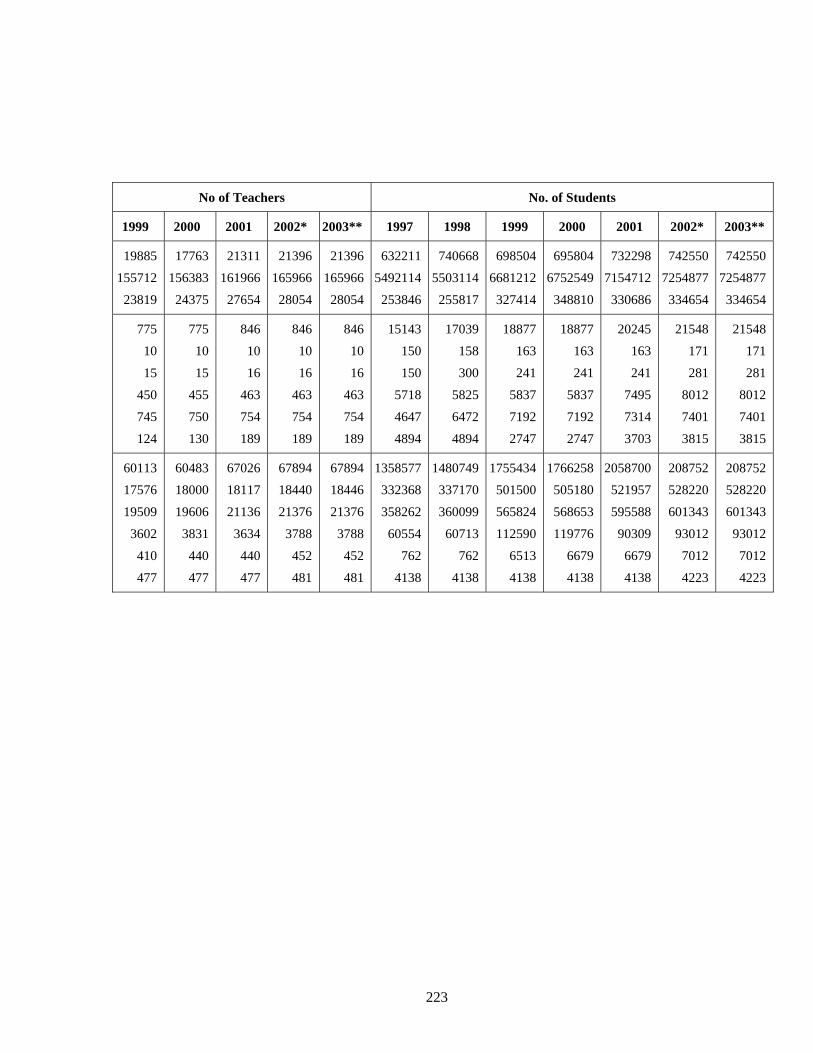

34. Number of Secondary and Higher Secondary, Technical and Vocational and Religious Educational Institutions, Teachers and Students

222-223

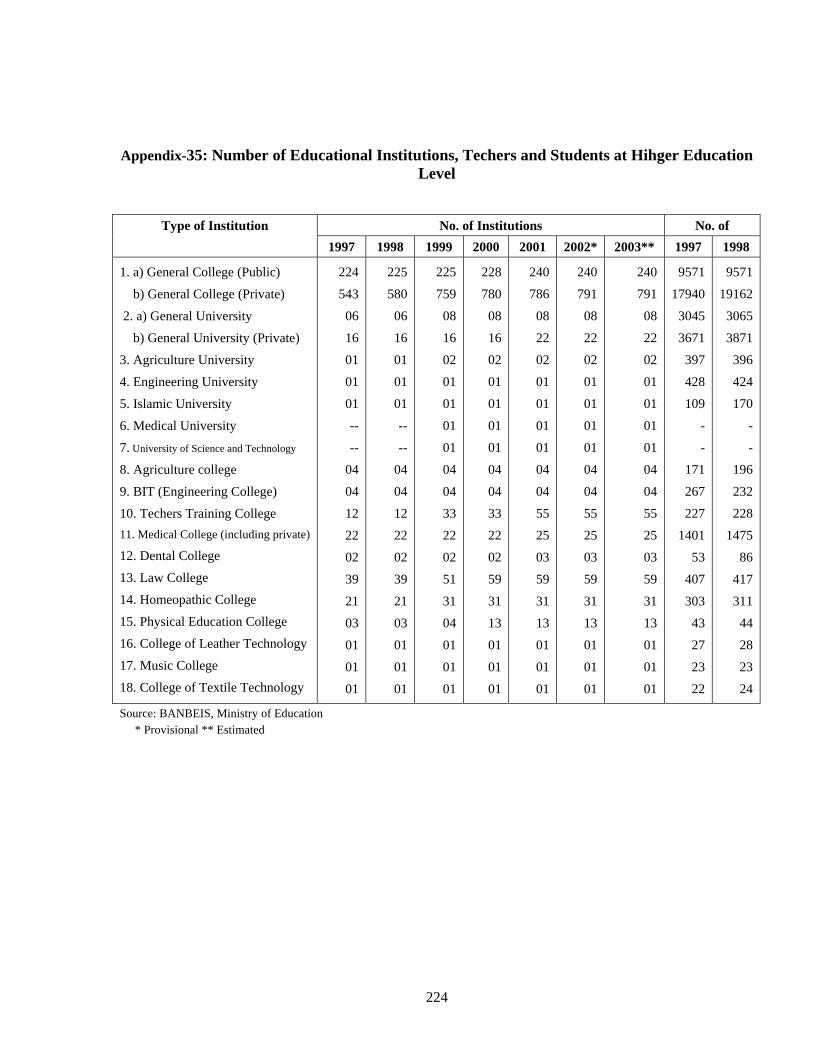

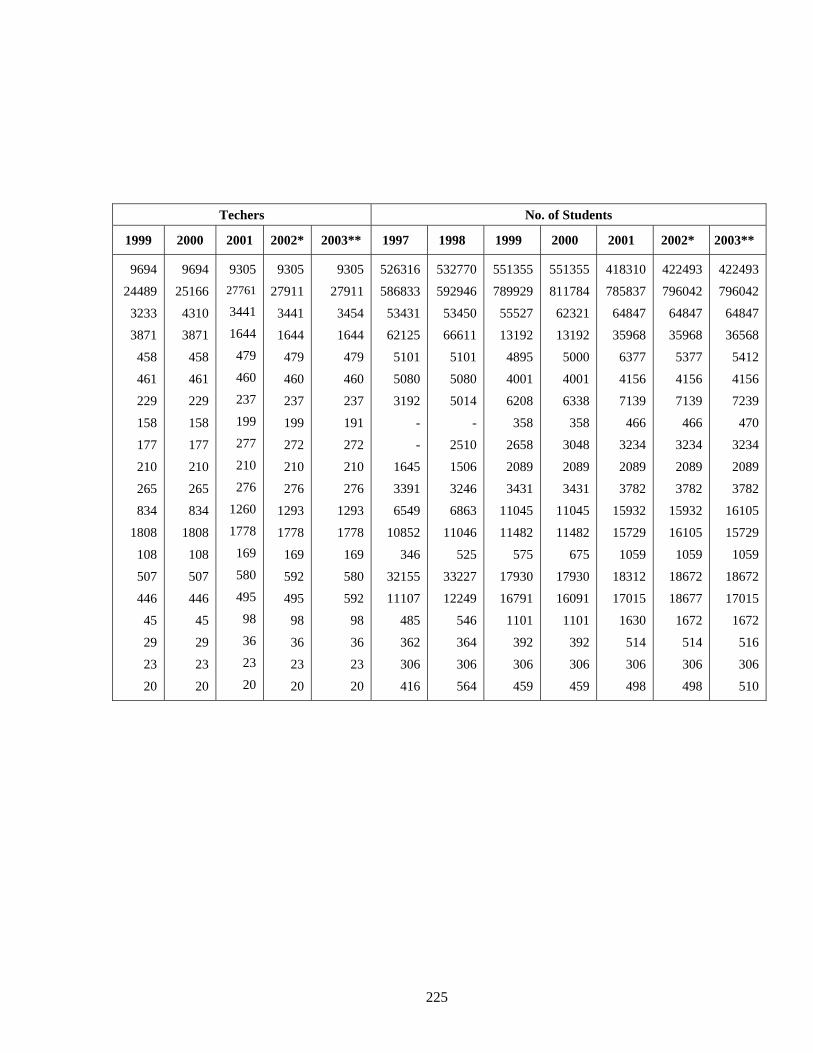

35. Number of Educational Institutions, Teachers and Students at Higher Education Level

224-225

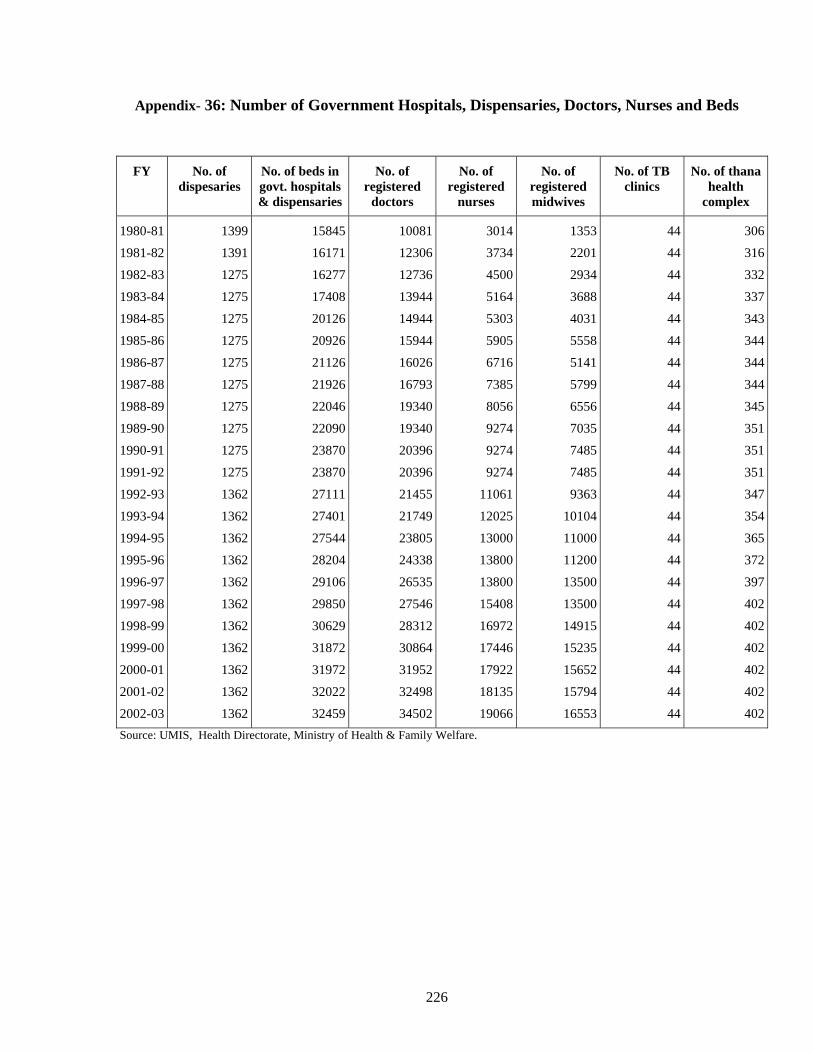

36. Number of Govt. Hospitals, Dispensaries, Doctors, Nurses and Beds 226

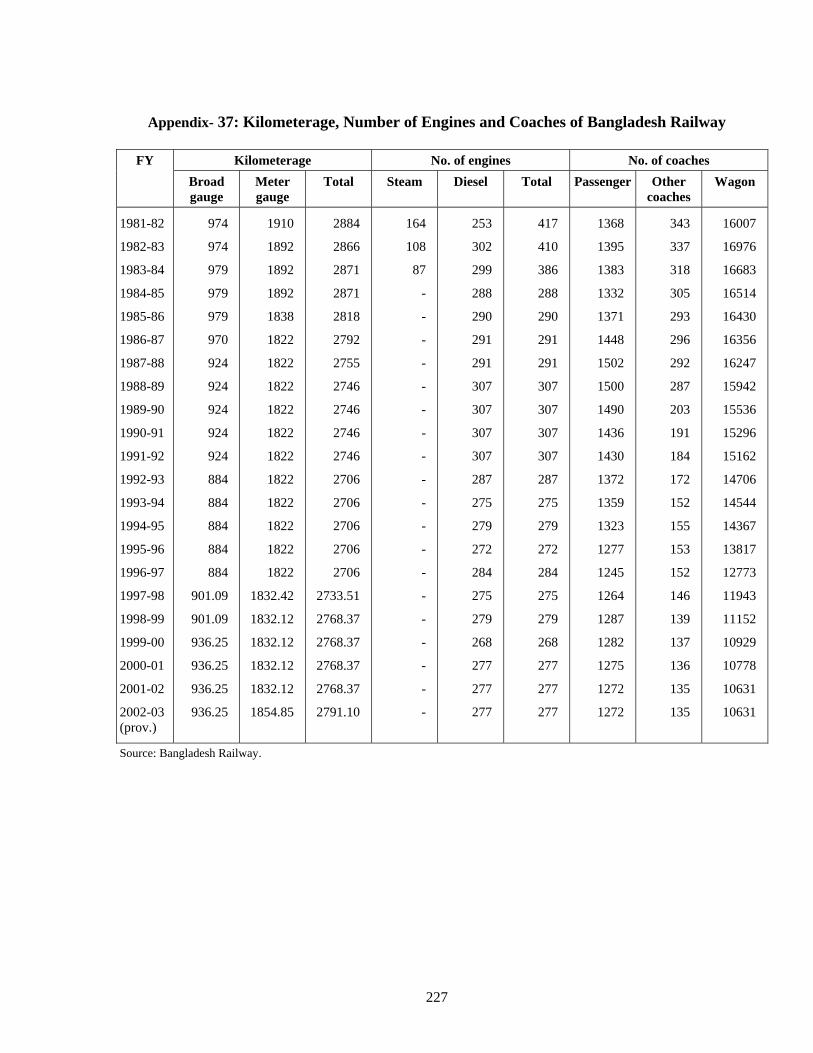

37. Kilometerage, Number of Engines and Coaches of Bangladesh Railway 227

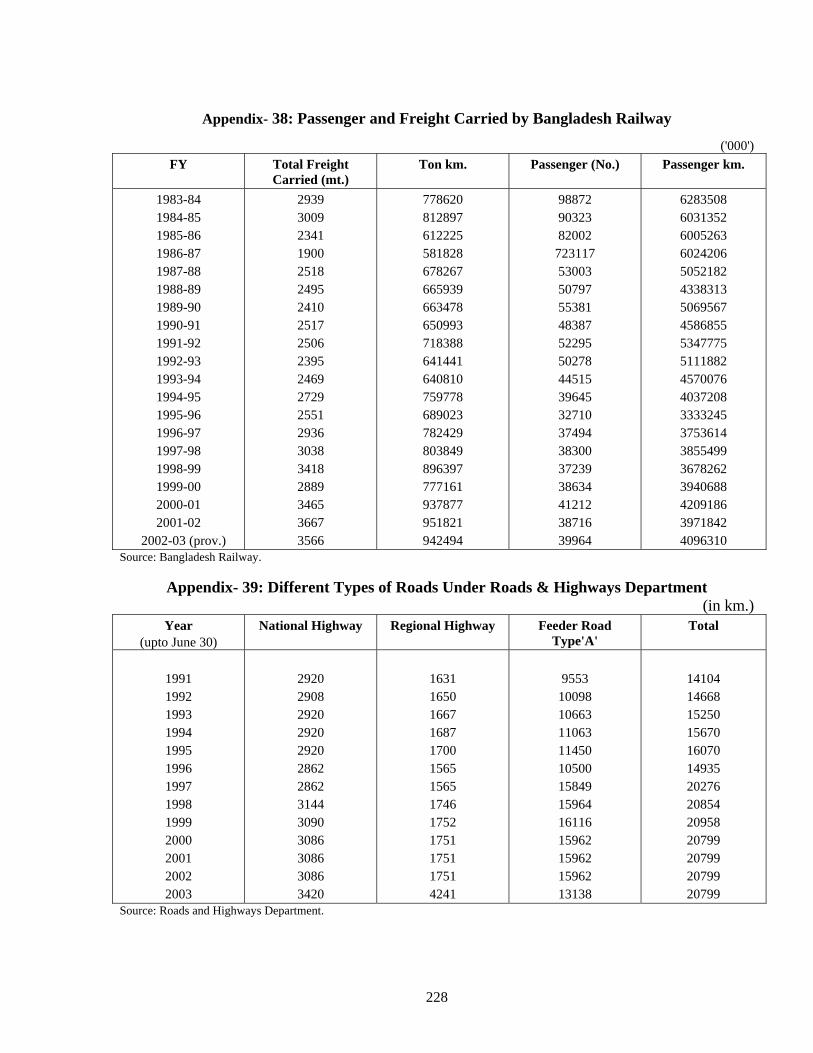

38. Passenger and Freight Carried by Bangladesh Railway 228

39. Different Type of Roads under Roads and Highways Department 228

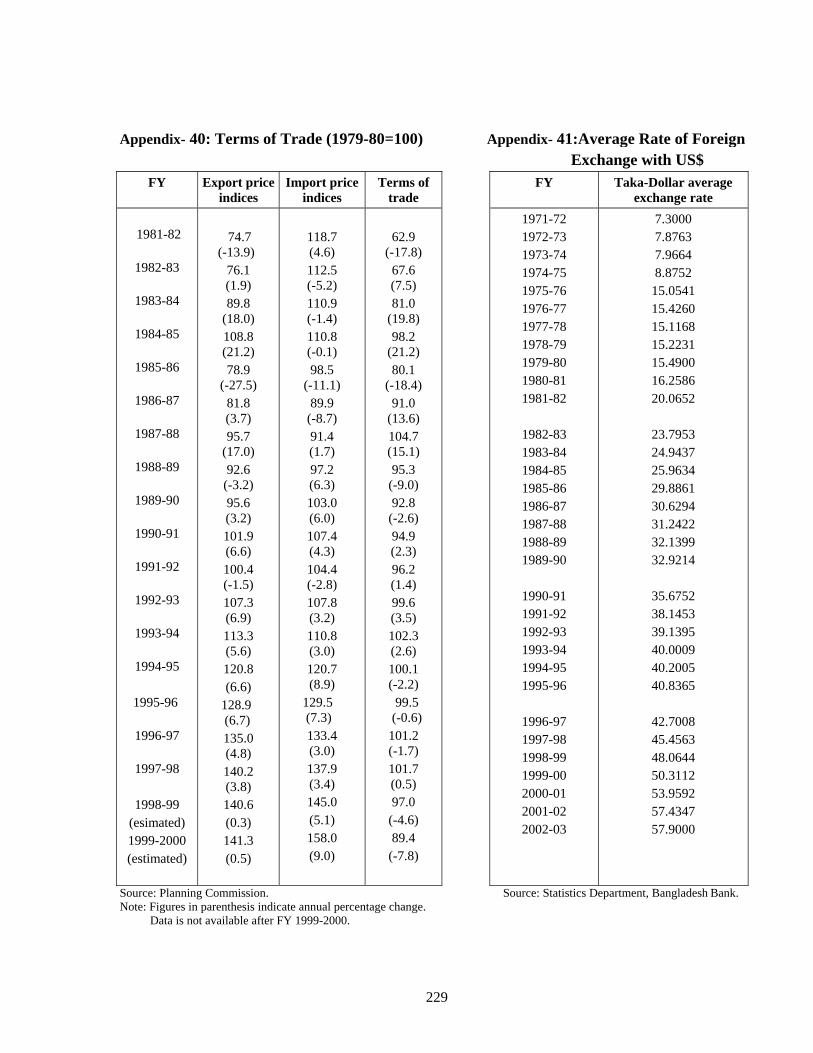

40. Terms of Trade (Base: 1979-80=100) 229

41. Average Rates of Foreign Exchange with US Dollar 229

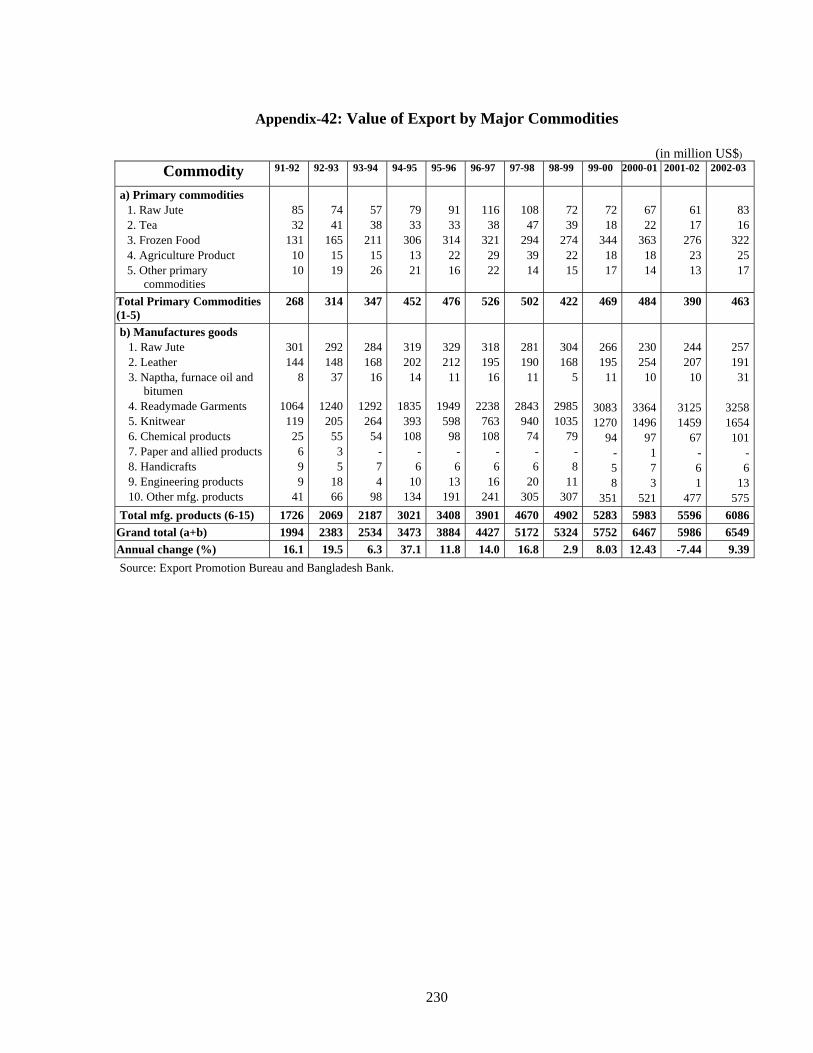

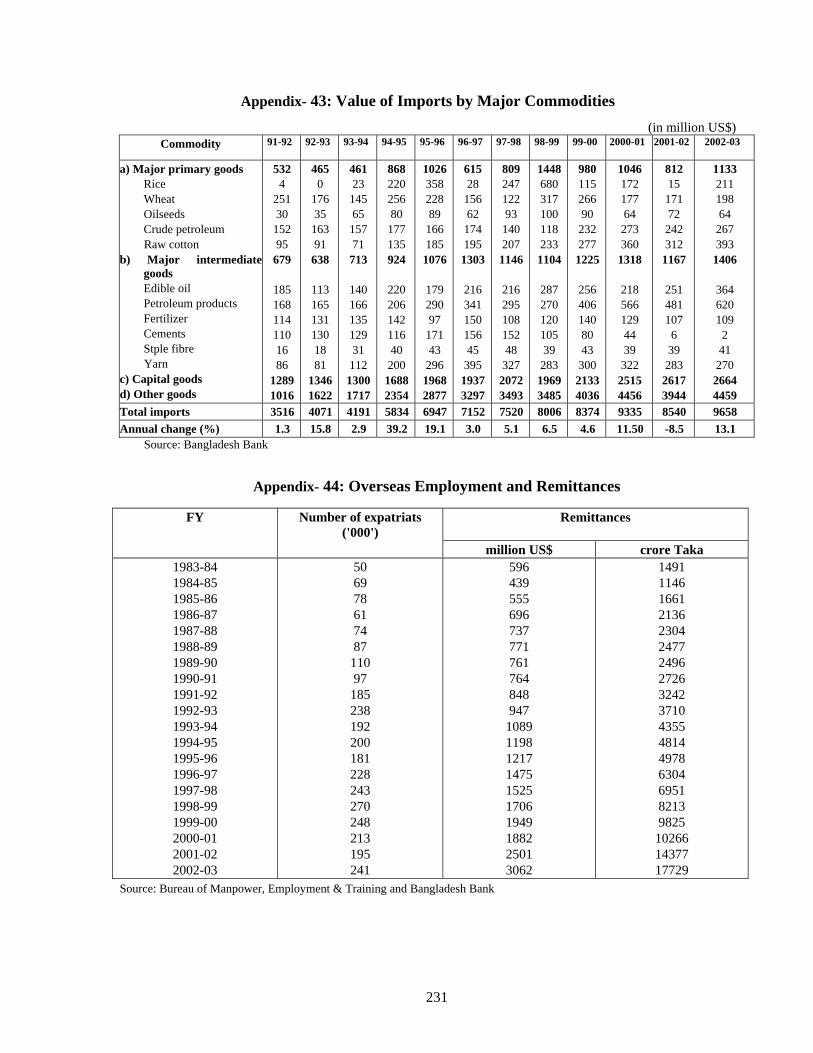

42. Value of Exports by Major Commodities 230

43. Value of Imports by Major Commodities 231

44. Overseas Employment and Remittances 231

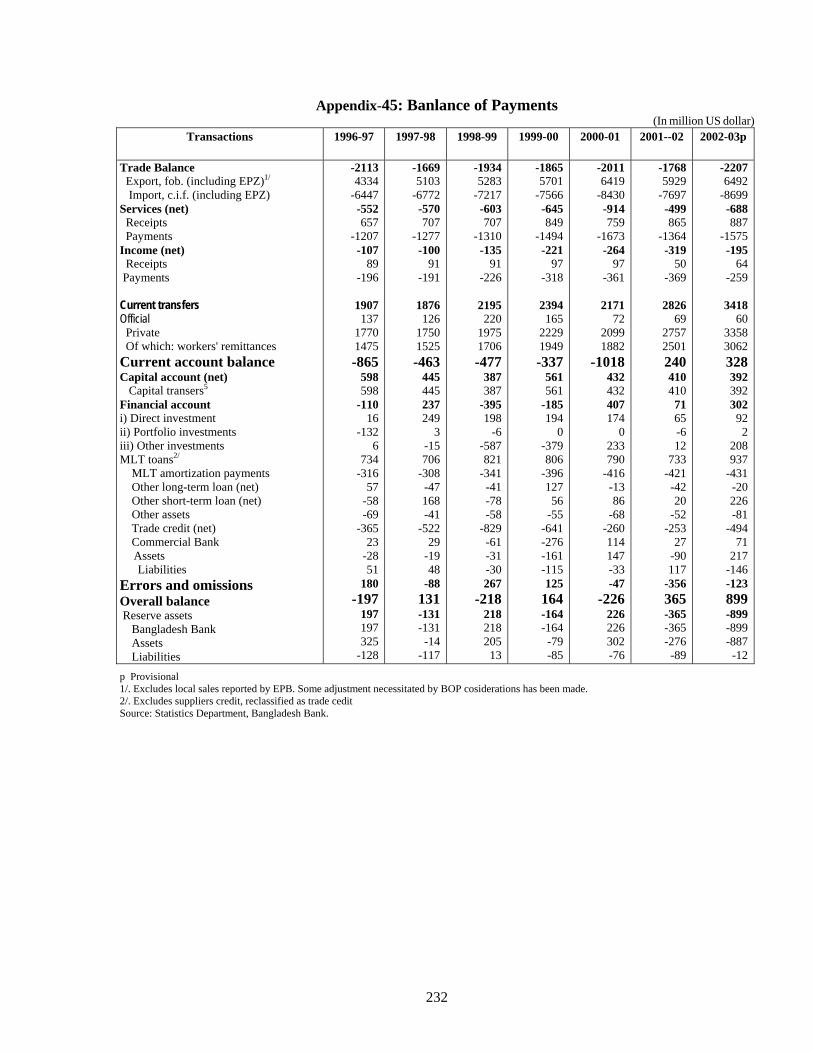

45. Balance of Payments 232

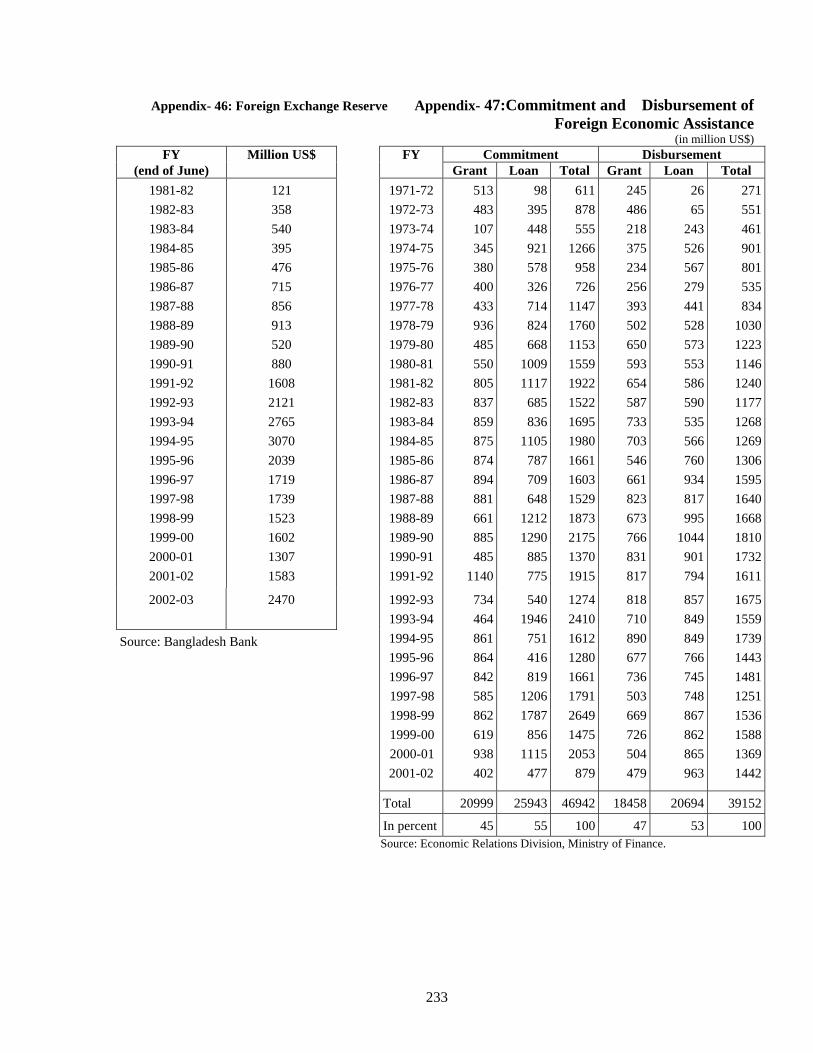

46. Foreign Exchange Reserves 233

47. Commitment and Disbursement of Foreign Economic Assistance 233

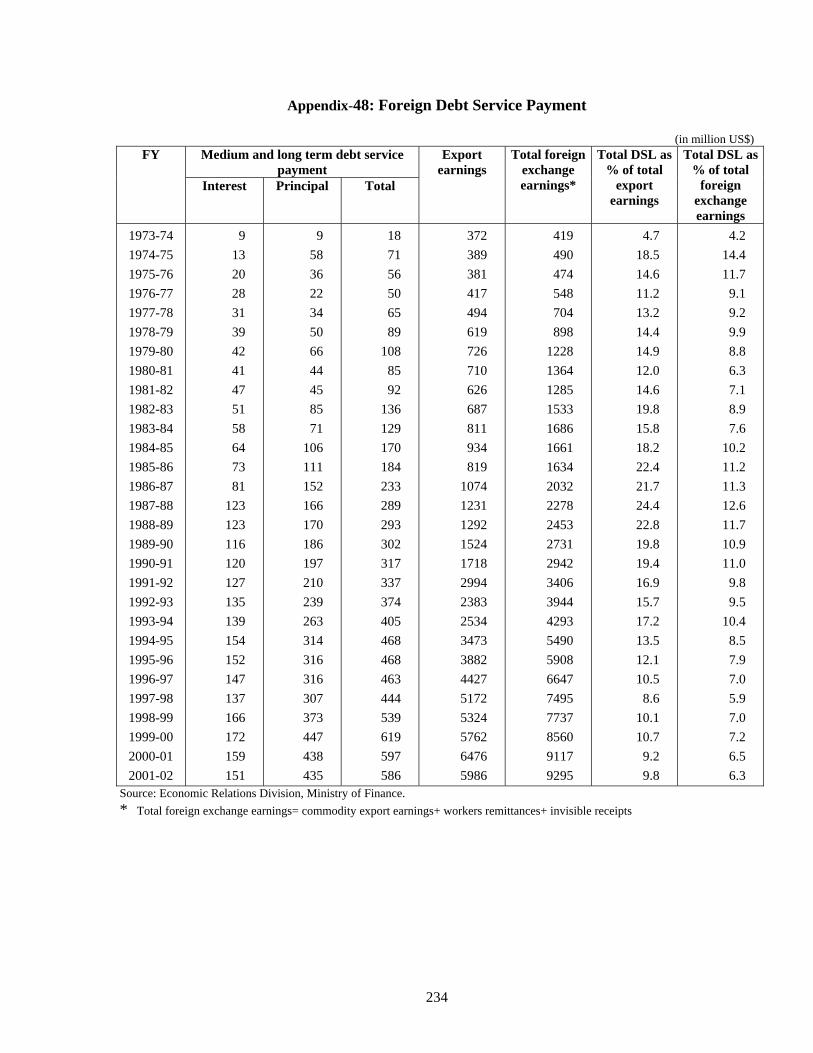

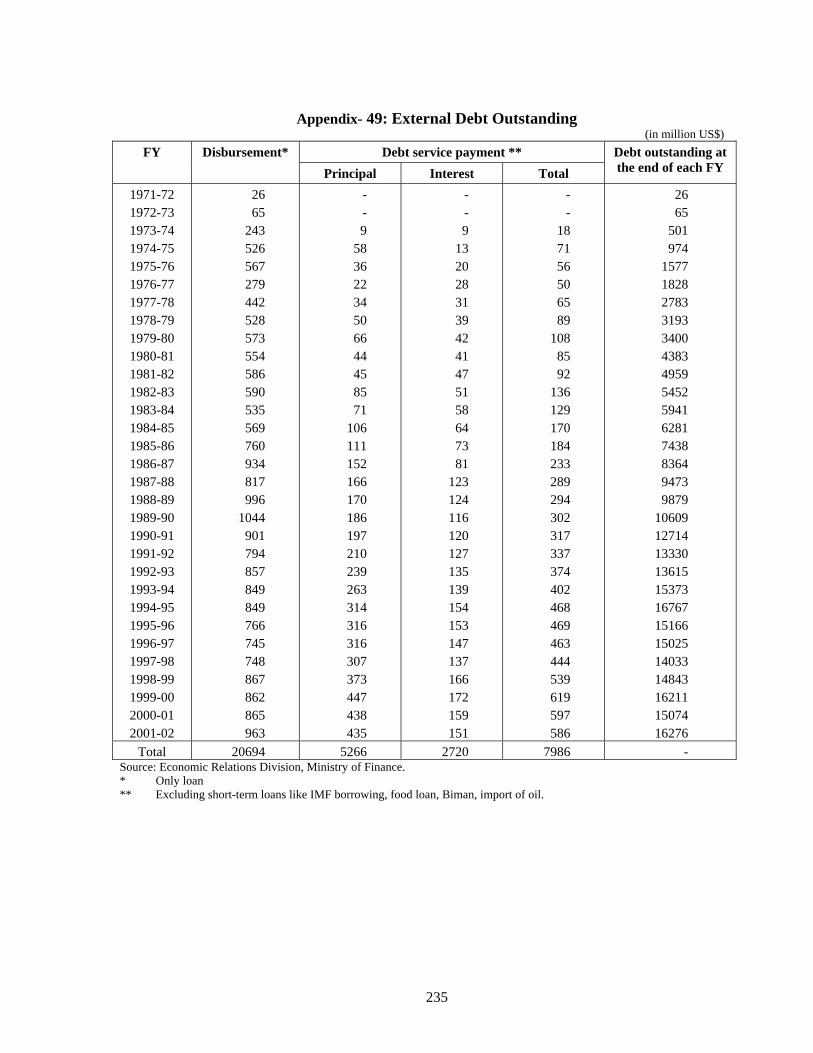

48. Foreign Debt Service Payment 234

49. External Debt Outstanding 235

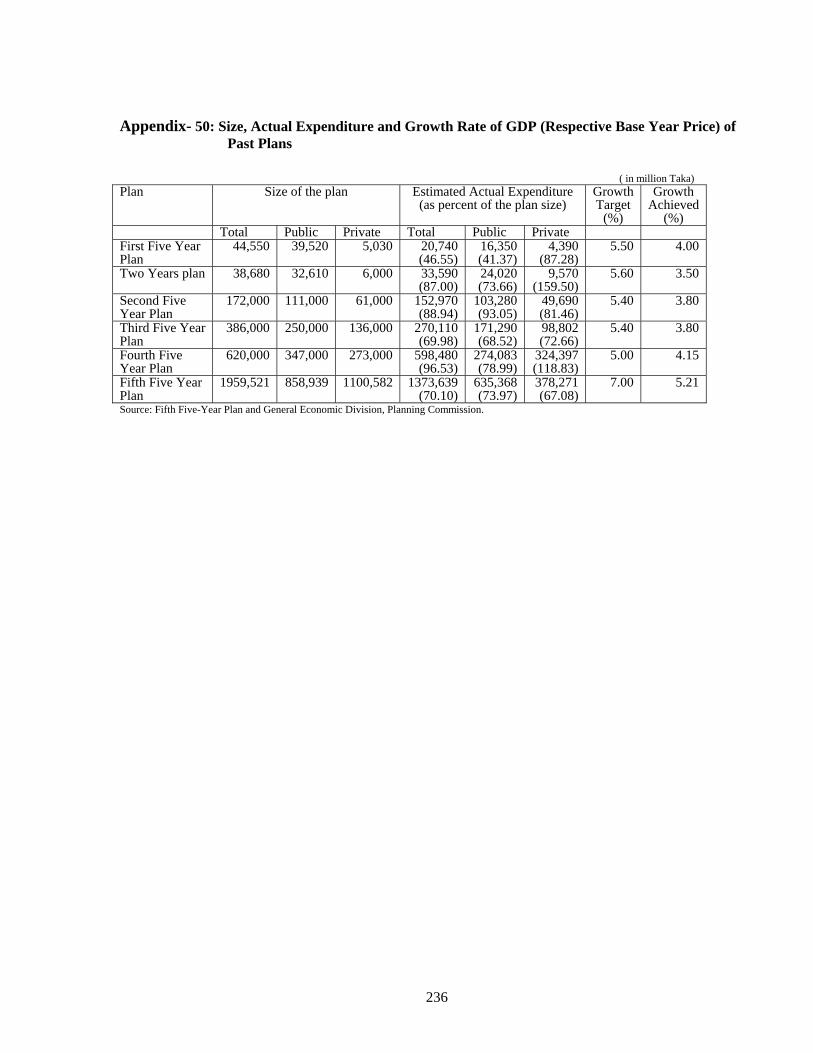

50. Size, Actual Expenditure and Growth Rate of GDP (Respective Base Year Price) of Past Plans

236

xv

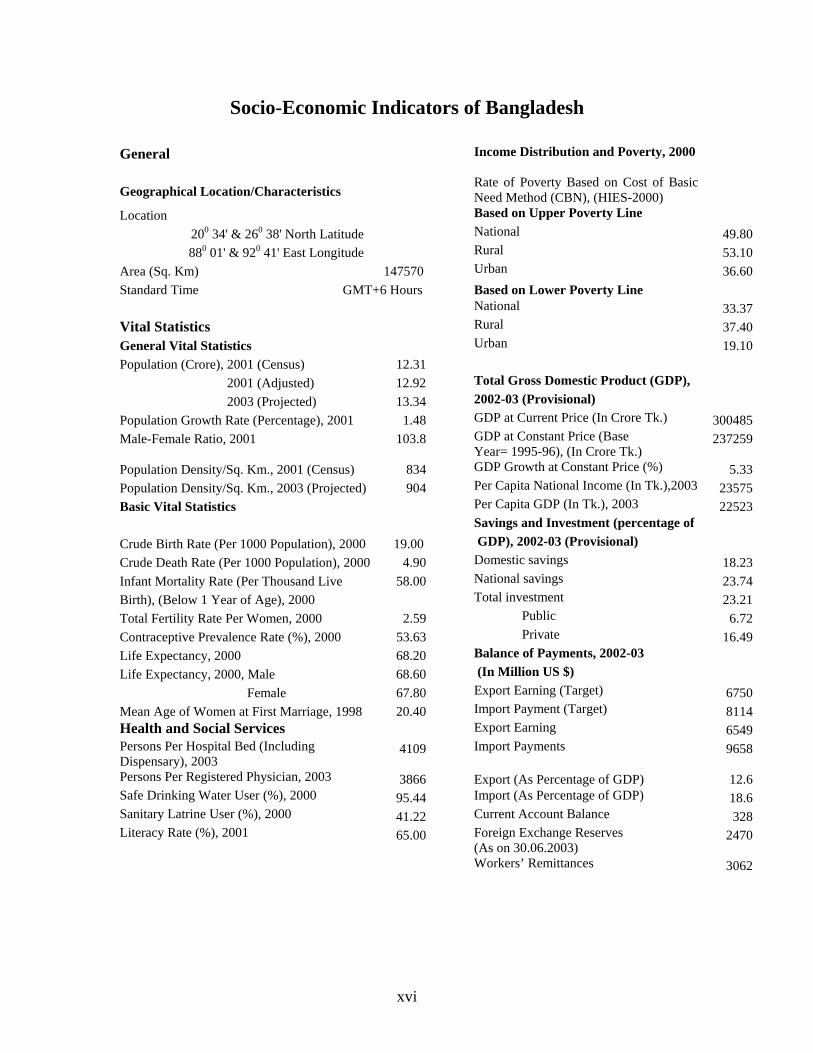

Socio-Economic Indicators of Bangladesh

General Geographical Location/Characteristics

Income Distribution and Poverty, 2000 Rate of Poverty Based on Cost of Basic Need Method (CBN), (HIES-2000)

Location Based on Upper Poverty Line 200 34' & 260 38' North Latitude National 49.80 880 01' & 920 41' East Longitude Rural 53.10

Area (Sq. Km) 147570 Urban 36.60 Standard Time GMT+6 Hours Based on Lower Poverty Line

National 33.37 Vital Statistics Rural 37.40 General Vital Statistics Population (Crore), 2001 (Census) 12.31

Urban 19.10

2001 (Adjusted) 12.92 Total Gross Domestic Product (GDP), 2003 (Projected) 13.34 2002-03 (Provisional) Population Growth Rate (Percentage), 2001 1.48 GDP at Current Price (In Crore Tk.) 300485 Male-Female Ratio, 2001 103.8 GDP at Constant Price (Base

Year= 1995-96), (In Crore Tk.) 237259

Population Density/Sq. Km., 2001 (Census) 834 GDP Growth at Constant Price (%) 5.33 Population Density/Sq. Km., 2003 (Projected) 904 Per Capita National Income (In Tk.),2003 23575 Basic Vital Statistics Per Capita GDP (In Tk.), 2003 22523 Savings and Investment (percentage of Crude Birth Rate (Per 1000 Population), 2000 19.00 GDP), 2002-03 (Provisional) Crude Death Rate (Per 1000 Population), 2000 4.90 Domestic savings 18.23 Infant Mortality Rate (Per Thousand Live 58.00 National savings 23.74 Birth), (Below 1 Year of Age), 2000 Total investment 23.21 Total Fertility Rate Per Women, 2000 2.59 Public 6.72 Contraceptive Prevalence Rate (%), 2000 53.63 Private 16.49 Life Expectancy, 2000 68.20 Balance of Payments, 2002-03 Life Expectancy, 2000, Male 68.60 (In Million US $) Female 67.80 Export Earning (Target) 6750 Mean Age of Women at First Marriage, 1998 20.40 Import Payment (Target) 8114 Health and Social Services Export Earning 6549 Persons Per Hospital Bed (Including Dispensary), 2003

4109 Import Payments 9658

Persons Per Registered Physician, 2003 3866 Export (As Percentage of GDP) 12.6 Safe Drinking Water User (%), 2000 95.44 Import (As Percentage of GDP) 18.6 Sanitary Latrine User (%), 2000 41.22 Current Account Balance 328 Literacy Rate (%), 2001 65.00 Foreign Exchange Reserves

(As on 30.06.2003) 2470

Workers’ Remittances 3062

xvi

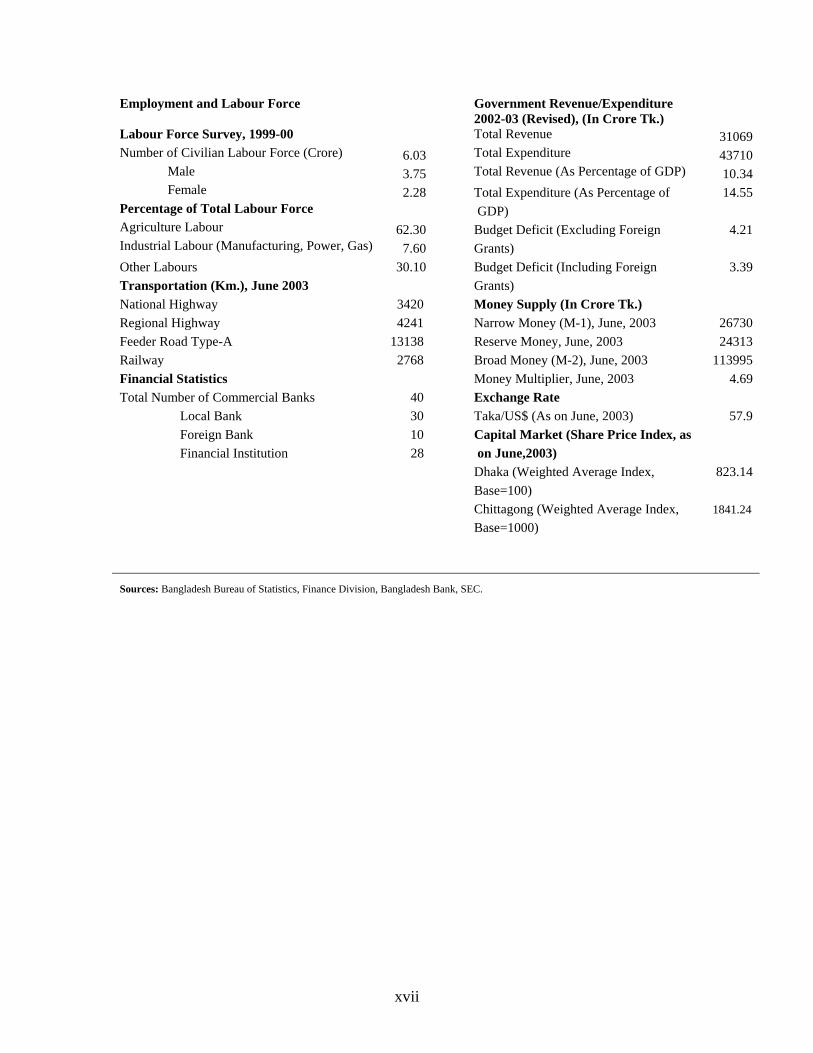

Employment and Labour Force Government Revenue/Expenditure 2002-03 (Revised), (In Crore Tk.)

Labour Force Survey, 1999-00 Total Revenue 31069 Number of Civilian Labour Force (Crore) 6.03 Total Expenditure 43710

Male 3.75 Total Revenue (As Percentage of GDP) 10.34 Female 2.28 Total Expenditure (As Percentage of 14.55

Percentage of Total Labour Force GDP) Agriculture Labour 62.30 Budget Deficit (Excluding Foreign 4.21 Industrial Labour (Manufacturing, Power, Gas) 7.60 Grants) Other Labours 30.10 Budget Deficit (Including Foreign 3.39 Transportation (Km.), June 2003 Grants) National Highway 3420 Money Supply (In Crore Tk.) Regional Highway 4241 Narrow Money (M-1), June, 2003 26730 Feeder Road Type-A 13138 Reserve Money, June, 2003 24313 Railway 2768 Broad Money (M-2), June, 2003 113995 Financial Statistics Money Multiplier, June, 2003 4.69 Total Number of Commercial Banks 40 Exchange Rate Local Bank 30 Taka/US$ (As on June, 2003) 57.9 Foreign Bank 10 Capital Market (Share Price Index, as Financial Institution 28 on June,2003) Dhaka (Weighted Average Index, 823.14 Base=100) Chittagong (Weighted Average Index, 1841.24 Base=1000) Sources: Bangladesh Bureau of Statistics, Finance Division, Bangladesh Bank, SEC.

xvii

CHAPTER-1

MACROECONOMIC REVIEW AND DEVELOPMENT STRATEGIES

In its journey towards prosperity Bangladesh economy passed a crucially important phase during FY 2001-02 and 2002-03. During this period the country's economy regained stability following a process of recovery. The present Government had to confront the onerous task of managing an economy that became increasingly fragile due to economic mismanagement of the previous regime. In addition, the faltering global economy and the adverse impact of the September 11 shock further deepened the economy's fragility and instability. Against this backdrop, the Government implemented a set of pragmatic recovery programmes and restored stability in the economy. Still the prevailing imperatives dictate the need for deepening and expanding the already initiated reforms for infusion of dynamism in the economy. In the socio-political context of Bangladesh, though implementation of these reforms presented a formidable challenge, the Government faced it successfully through its relentless efforts over the past one and a half year.

Economic Growth

Over the past two decades, particularly during the 1990's, the economic growth in Bangladesh registered a remarkable progress. The average growth rate of Gross Domestic Product (GDP) was around 5 percent in this decade. Implementation of a wide array of reforms during the early 1990s made it possible to achieve this higher rate of growth. Four percent growth rate on an average over a period of the last two decades brought an opportunity for transition to a higher growth path. Attaining of per capita GDP growth at 3.3 percent during the 1990's is an impressive achievement. This was possible due to a sharp fall in birth rate. Success in attaining such a higher growth, elevated Bangladesh's position among the developing countries. Infusion of further momentum in the economy in FY 2002-03, caused to make projection of GDP at 5.33 percent which is 0.91 percent higher than the growth rate of last fiscal year. In FY 2002-03, the growth in agriculture and industries (manufacturing) sectors has been projected at 3.59 and 6.62 percent respectively. Moreover, the current year's growth in all other sectors barring the construction sector has been projected to be higher than those of the previous fiscal year.

Saving and Investment

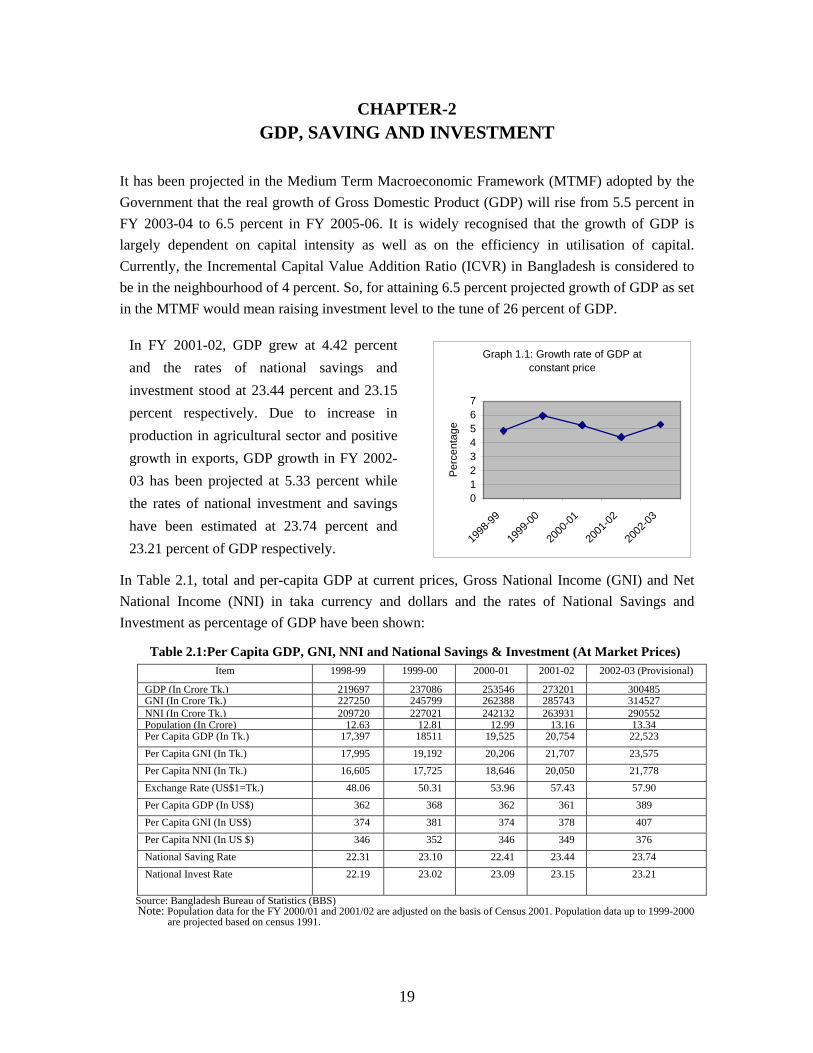

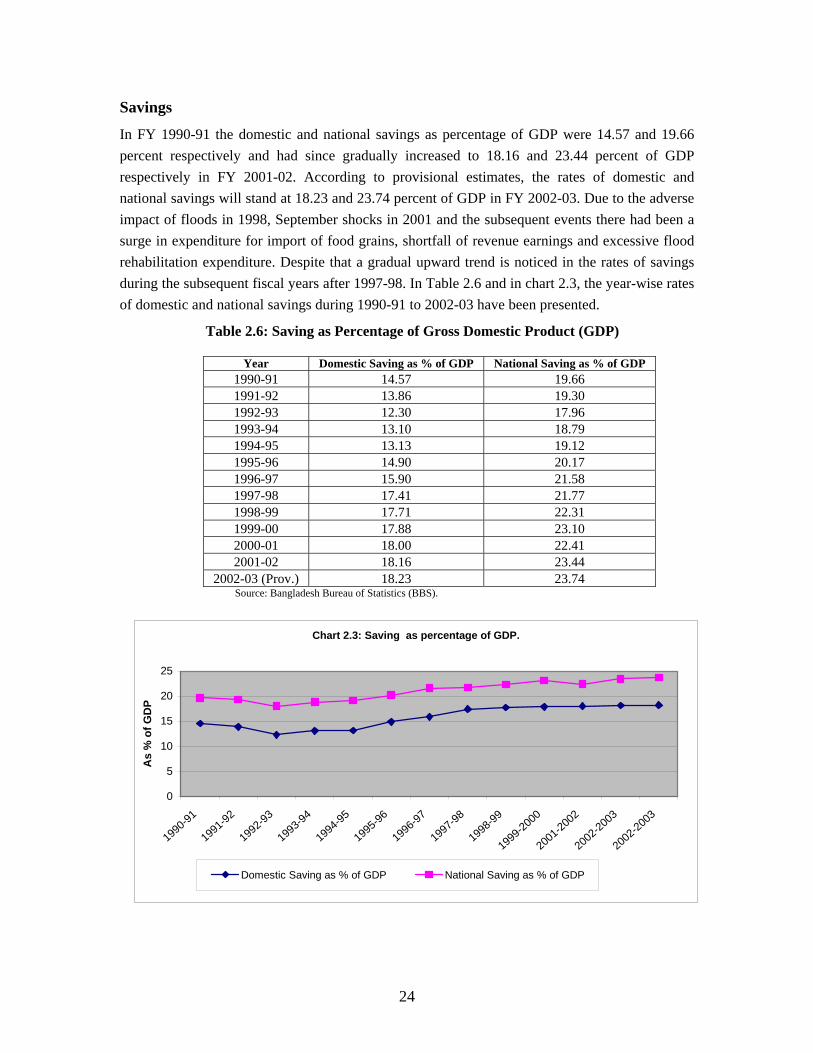

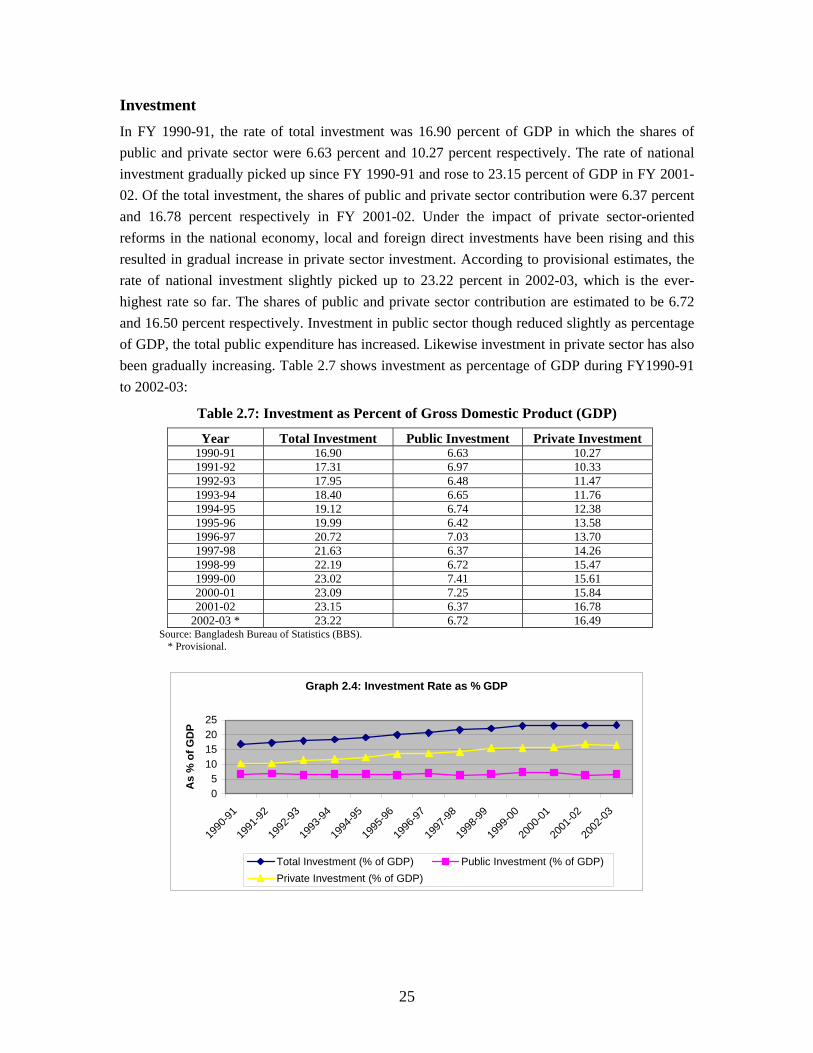

Based on provisional estimates, domestic and national savings during the current fiscal year have been projected at 18.23 and 23.74 percent of GDP. In FY 1991-92 the rates of savings stood at 13.86 and 19.30 percent reflecting a secular rise in savings over the decade. Provisional estimates show that the rate of investment in FY 2002-03 will be 23.22 percent of GDP consisting of shares of public and private sector at 6.72 percent and 16.49 percent respectively. The rate of investment too registered a rising trend over the past decade.

1

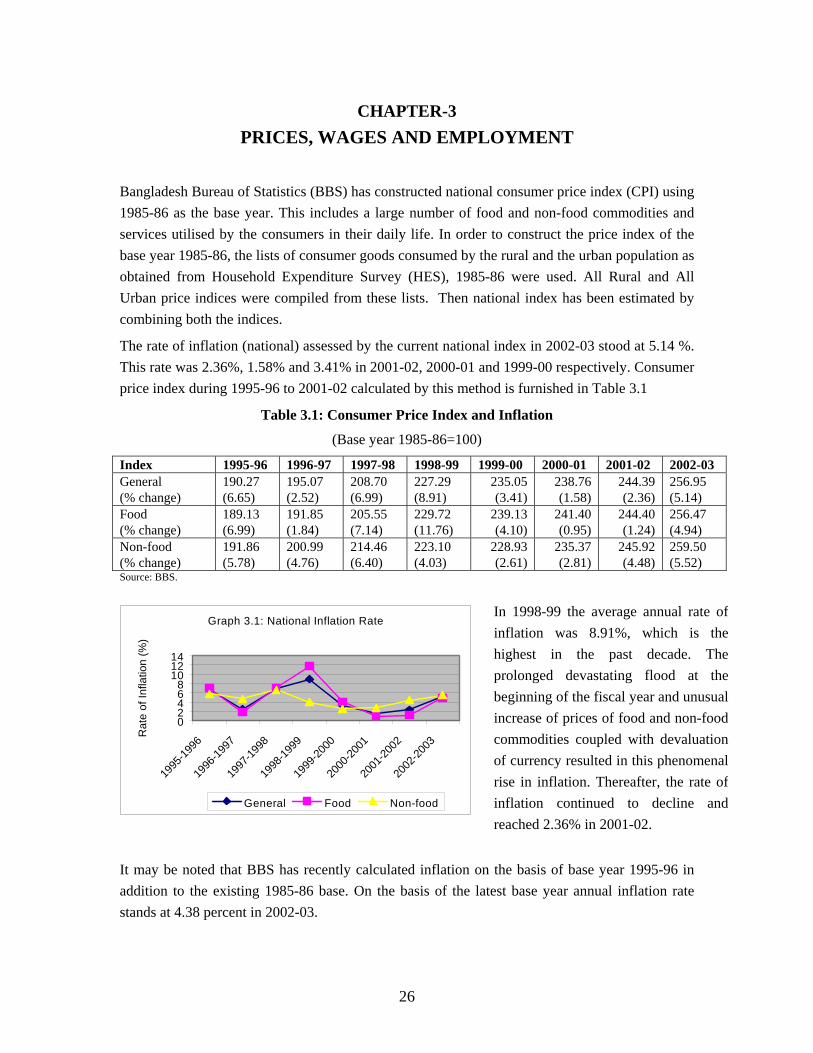

Inflation

According to consumer price index, constructed on the basis of 1985-86 as the base year, the rate of inflation in FY 2002-03 stood at 5.14 percent. In food and non-food sectors, inflation stood at 4.94 and 5.52 percent respectively. In a growing economy such inflationary trend is considered tolerable. It is however to be noted that, the rate of inflation remained low in Bangladesh since the 1990s. Maintaining this low rate of inflation has largely been possible due to rise in food production and downward trend in prices of consumer goods in the international market.

Fiscal policy and fiscal Management

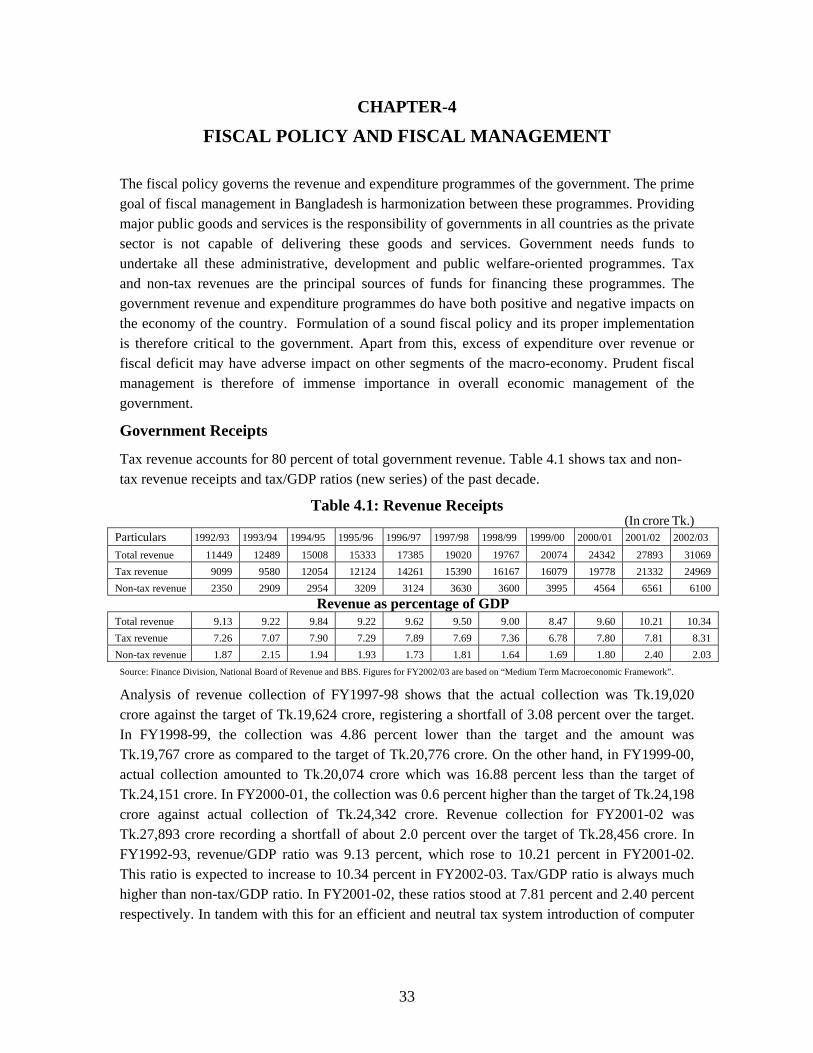

Following restoration of stability in macroeconomic management of the country, the deficit in the last two fiscal years came down to a sustainable level. Whereas in FY 1999-2000 the budget deficit was 6.1 percent, it came down to 4.7 percent in the previous fiscal and 4.2 percent in the FY 2002-03. This has been achieved through a combination of policies aimed at rationalization of Government expenditure and augmentation of domestic resources mobilization. In the Government's efforts to establish macroeconomic stability in the economy, this achievement is a significant milestone. While announcing budget for FY2002-03, a number of steps were proposed to augment both tax and non-tax revenue. In the backdrop of declining foreign aid, enhanced domestic revenue mobilization was an imperative for our fiscal sustainability. NBR revenue has increased by 17.53 percent in FY 2003, which is much higher than the actual collection of the last year. The Government total revenue has exceeded Tk.31000 core which is the highest so far. This has raised the revenue-GDP ratio to 10.4 percent. It is to be noted that the growth of revenue was 7.0 percent during the 1990s while it was only 3 percent during the 1980s. In Bangladesh, expenditure-GDP rose to 15 percent FY03. In the 1980s, the growth of expenditure was 3.1 percent which rose to 6.6 percent during the 1990s. Despite saddled with resource constraints, the trend in Government spending in the priority social sectors like human development, building rural infrastructure and poverty reduction has been consistently on the increase. According to the revised ADP, the expenditure in social sector stands at 24.6 percent and the revenue outlays on social sector stands at 22.7 percent in FY03.

Monetary Policy and Monetary Management

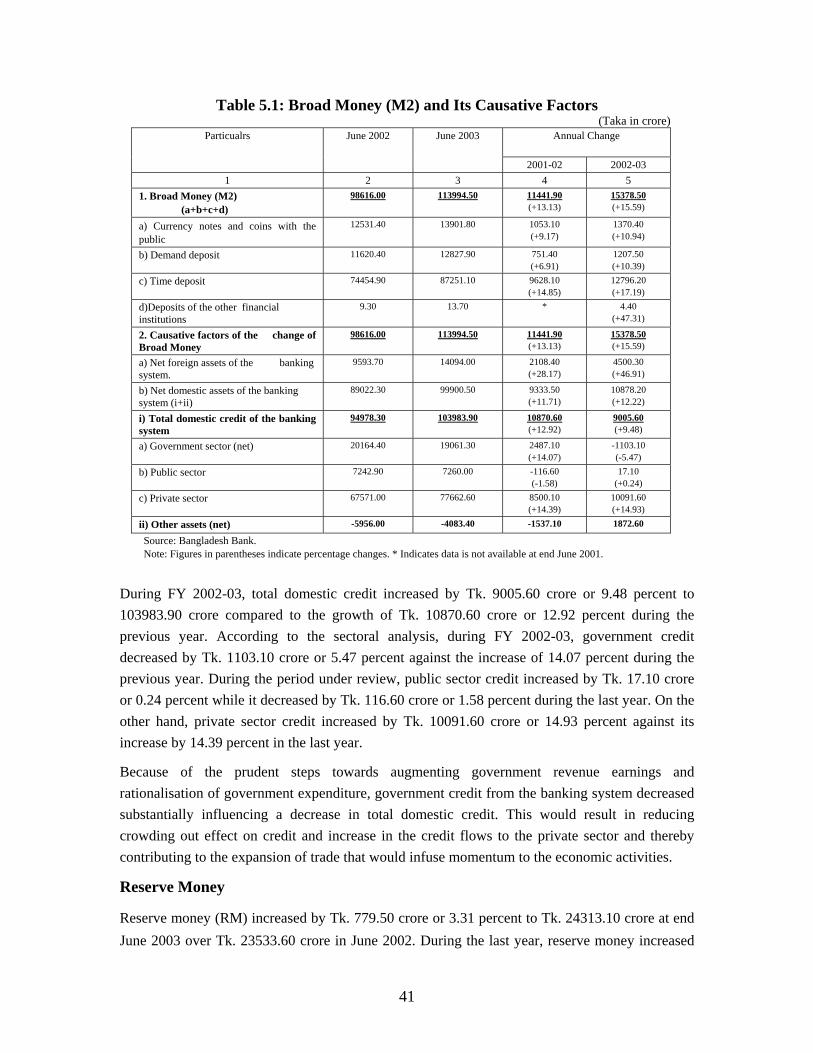

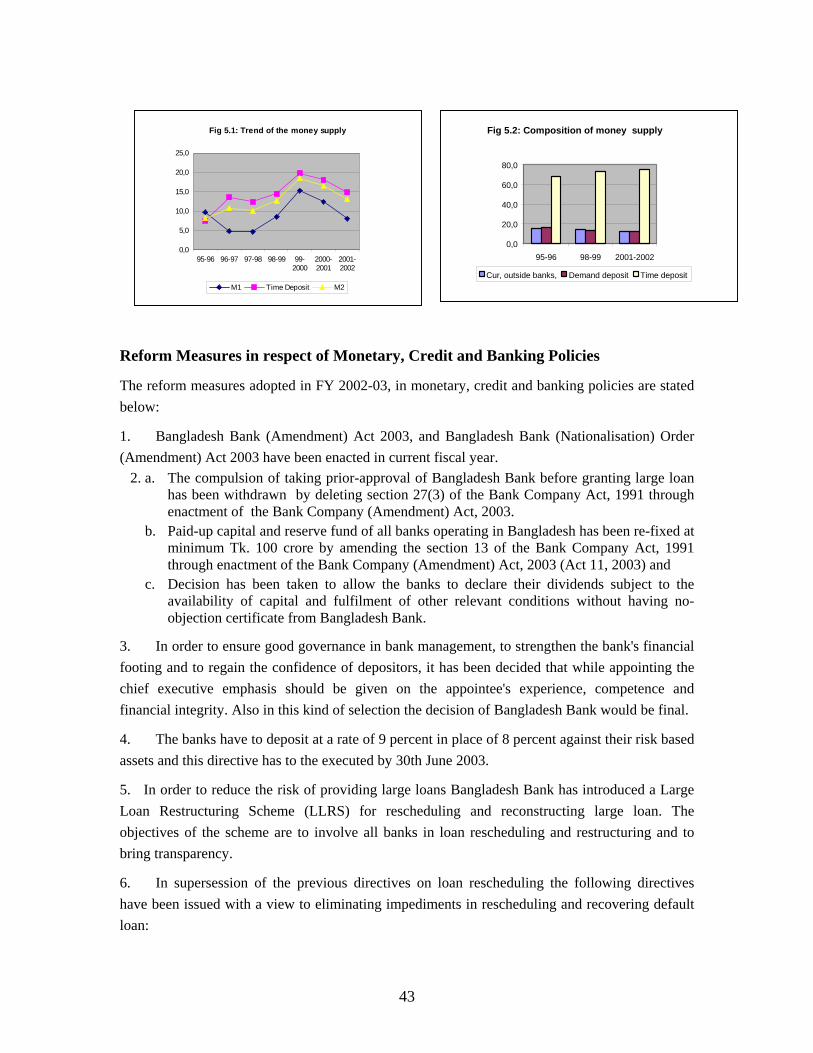

Monetary policy for FY 2002-03 was formulated to accelerate the pace of economic activities of the country and to maintain the trend of economic growth. As the country's monetary management was steered in the light of a moderately expansionary monetary policy, the money supply and credit expansion remained slightly expansionary during FY2002-03. During this period the broad money supply registered 15.59 percent increase compared to that of the corresponding period of the previous fiscal year. On the other hand, the domestic credit expansion

2

registered a slightly lower increase by 9.48 percent compared to 12.92 percent increase during the corresponding period of the previous fiscal year. During this period credit flows to the public sector decreased (5.47%) while it registered an increase by 14.93 in the case of private sector. Because of the measures taken by the Government to improve revenue collection and to rationalize public expenditure, the rate of borrowing by the Government from the banking system reduced which had an important impact on the reduction of growth of domestic borrowing. This resulted in minimizing crowding out effect of public borrowing and caused increased flow of credit to the private sector that brought about expansion of trade and commerce and infused dynamism in the economic activities. Besides, a number of important steps were taken in the areas of banking and monetary and credit policy to ensure transparency in monetary and credit management. Several measures have been taken for development and expansion of capital market. This would result in restoration of investor's confidence in capital market.

External Sector

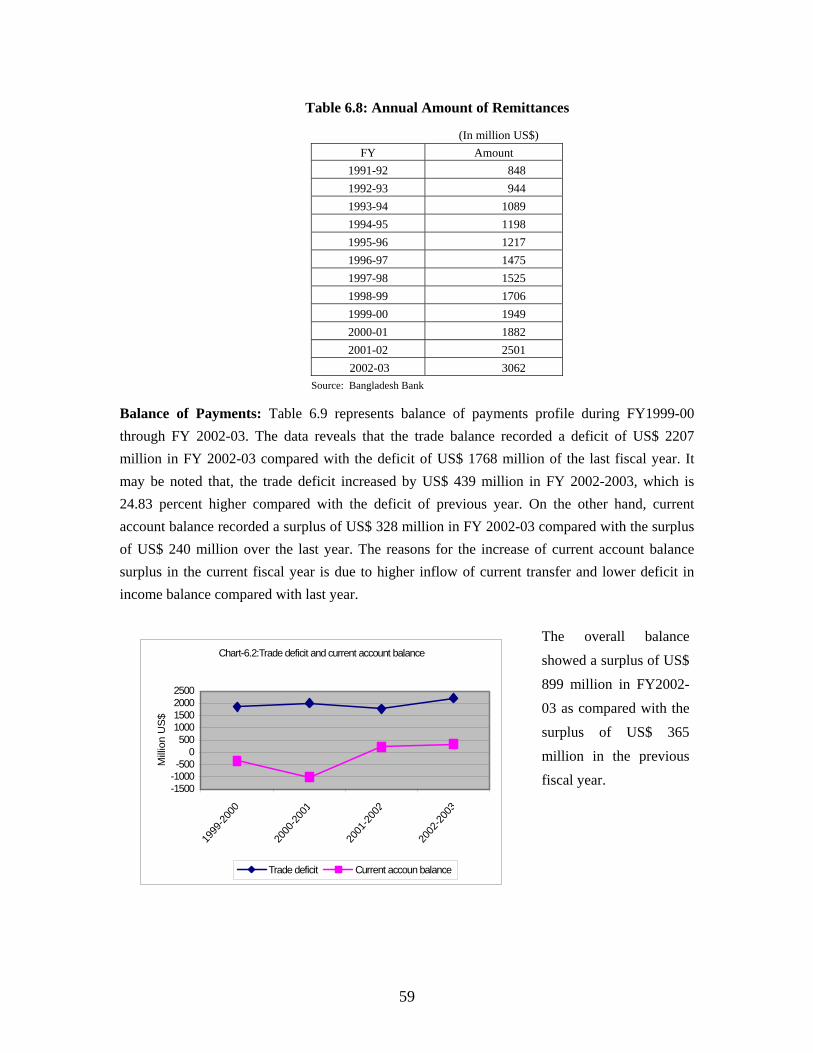

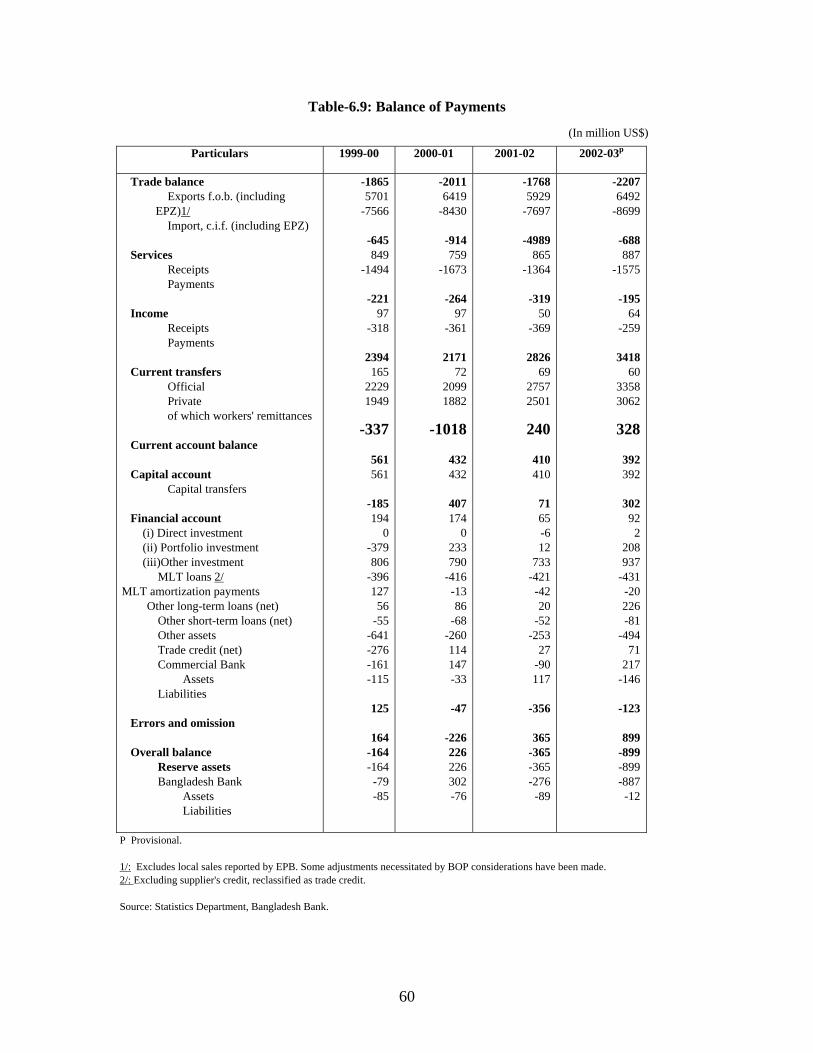

Despite prevailing adverse global economic situation, the current account balance of the balance of payment in Bangladesh registered a surplus of US$240 million in 2001-02, which was 0.5 percent of GDP. This trend continued in FY 2002-03 and the surplus stood at US$ 328 million, which was 0.63 percent of GDP. Notably, excepting India and Pakistan none of the least developed countries in South Asia achieved this surplus in the recent past. On the other hand, the trade-deficit situation is also improving gradually. According to available statistics, where the trade deficit in FY 1999-2000 and 2000-2001 stood at US$ 1865 and 2011 million respectively, it declined to US$ 1768 million in 2001-02. However the trade deficit in FY 2002-03 rose to US$ 2207 million, which is 24.83 percent higher than the deficit of the previous fiscal year. Because of the prudent and timely steps taken by the Government, the remittance flow of the expatriate Bangladeshi workers increased by 33 percent in FY 2001-02 and it increased from US$ 1.9 billion in FY 2000-01 to US$ 2.5 billion in the previous fiscal year. The trend continued during the current year. As a result, the remittance reached the US$3.06 billion mark in June 2003 and also the overall balance of payment situation improved further. It is to be noted that the foreign exchange reserve plummeted to US$ 1.09 billion when the present Government took office in October 2001.

3

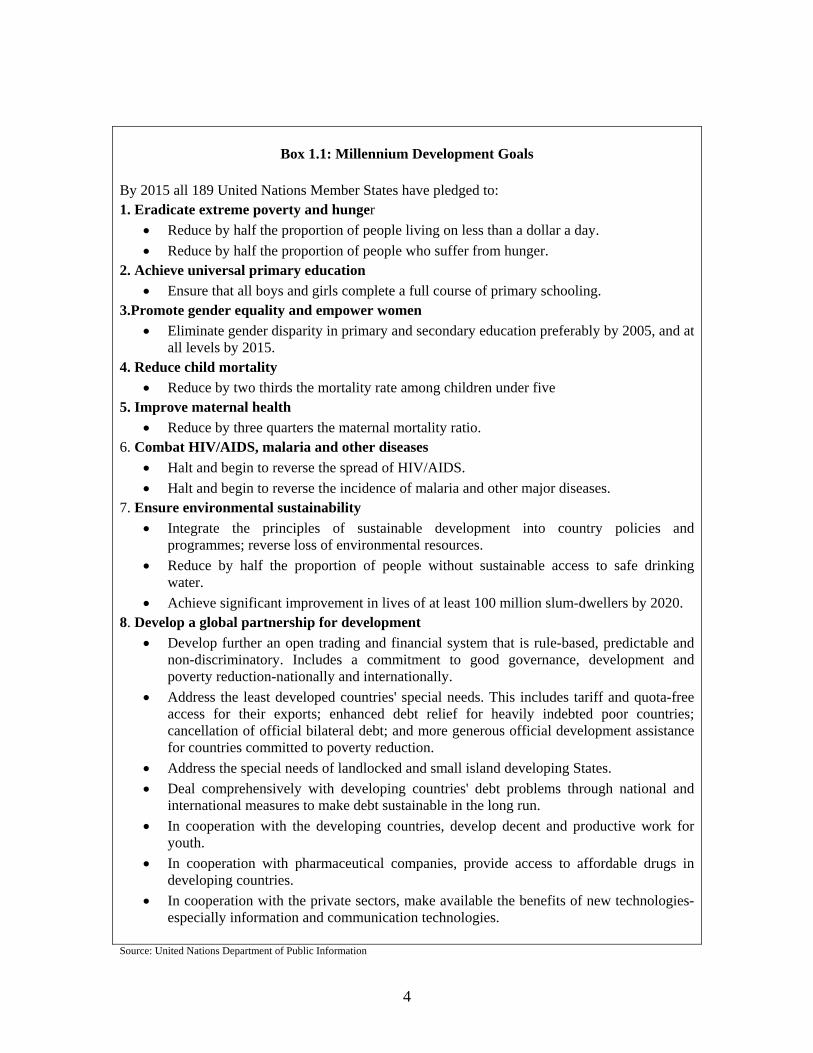

Box 1.1: Millennium Development Goals

By 2015 all 189 United Nations Member States have pledged to: 1. Eradicate extreme poverty and hunger

• Reduce by half the proportion of people living on less than a dollar a day. • Reduce by half the proportion of people who suffer from hunger.

2. Achieve universal primary education • Ensure that all boys and girls complete a full course of primary schooling.

3.Promote gender equality and empower women • Eliminate gender disparity in primary and secondary education preferably by 2005, and at

all levels by 2015. 4. Reduce child mortality

• Reduce by two thirds the mortality rate among children under five 5. Improve maternal health

• Reduce by three quarters the maternal mortality ratio. 6. Combat HIV/AIDS, malaria and other diseases

• Halt and begin to reverse the spread of HIV/AIDS. • Halt and begin to reverse the incidence of malaria and other major diseases.

7. Ensure environmental sustainability • Integrate the principles of sustainable development into country policies and

programmes; reverse loss of environmental resources. • Reduce by half the proportion of people without sustainable access to safe drinking

water. • Achieve significant improvement in lives of at least 100 million slum-dwellers by 2020.

8. Develop a global partnership for development • Develop further an open trading and financial system that is rule-based, predictable and

non-discriminatory. Includes a commitment to good governance, development and poverty reduction-nationally and internationally.

• Address the least developed countries' special needs. This includes tariff and quota-free access for their exports; enhanced debt relief for heavily indebted poor countries; cancellation of official bilateral debt; and more generous official development assistance for countries committed to poverty reduction.

• Address the special needs of landlocked and small island developing States. • Deal comprehensively with developing countries' debt problems through national and

international measures to make debt sustainable in the long run. • In cooperation with the developing countries, develop decent and productive work for

youth. • In cooperation with pharmaceutical companies, provide access to affordable drugs in

developing countries. • In cooperation with the private sectors, make available the benefits of new technologies-

especially information and communication technologies. Source: United Nations Department of Public Information

4

Reforms Initiatives

A Public Expenditure Review Commission and a Revenue Reforms Commission were constituted for streamlining and improving the effectiveness of public expenditures and enhancing revenue efforts. Their interim recommendations, already submitted, were taken into consideration in formulating budget for FY2003-04. For the first time, the Government carried out a mid-term review of the budget for FY2002-03 and the results of this review were incorporated in the revised budget for FY2002-03.

The Government has undertaken a series of reform measures in the energy and power sector in order to create an appropriate enabling environment for improved public sector performance, attract multi-lateral and private investment, rationalize tariff rates and improve collections, and the consumers get 'value for money'. In order to promote efficient energy use, the government is going to adopt an interim electricity, gas and petroleum pricing framework to ensure efficiency and financial viability of this sector.

The trade regime has been further liberalized by reducing the maximum tariff rate by 5 percent. Supplementary duty scheme has been rationalized by reducing the number of rates from 31 to 5. Import license fee on all imports has been withdrawn. Consequently, the average nominal tariff protection further declined. This liberalization trend was continued in the budget for 2003-04. The Government has designed an integrated policy framework for effective participation in globalisation process in the post -MFA period.

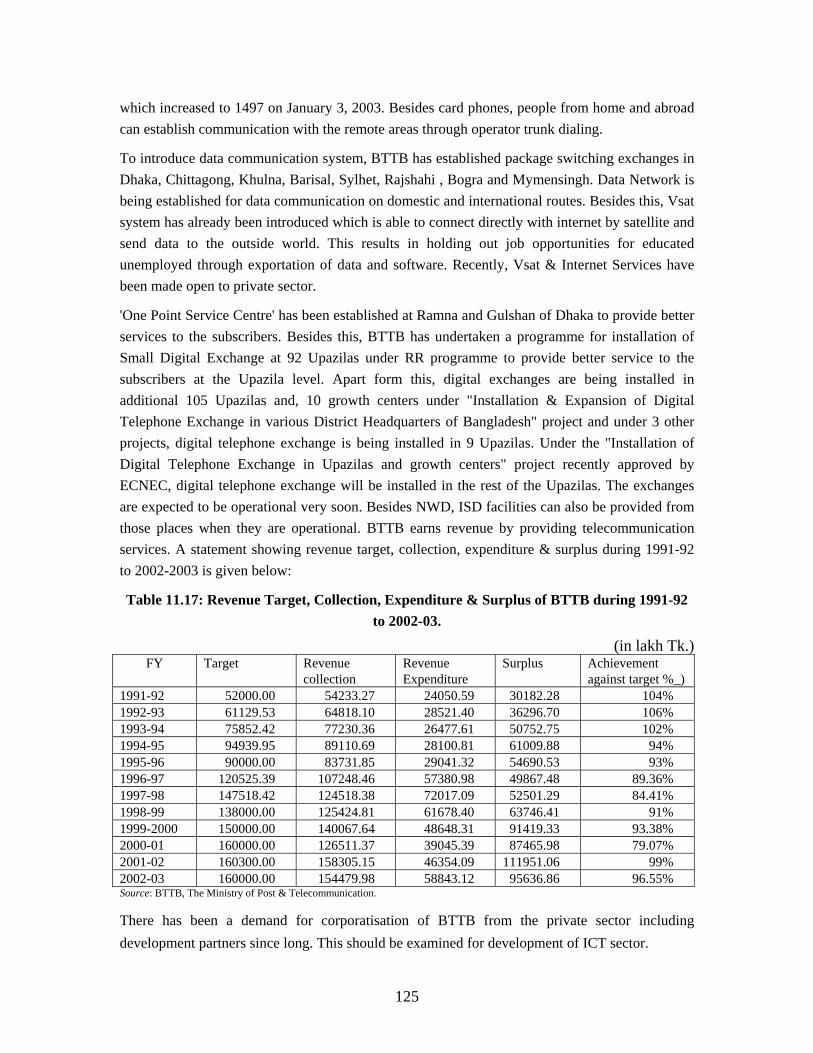

In view of the positive impact of telecommunication and the new information and communication technology on poverty alleviation and growth, the Government has been undertaking reforms in the telecommunication sector. Corporatization of BTTB is under active consideration of the Government. Moreover, the Bangladesh Telecommunication Act, 2001 has already been enacted and made operational to ensure fair play to multi- operators.

To bring more discipline in the financial sector and increase operational autonomy of the Bangladesh Bank necessary amendments to the Bangladesh Bank Order, Banking Companies Act and Banks (Nationalization) Order have been enacted by the Parliament. Several Task Forces have been set up to enforce the Money Laundering Prevention Act.

In order to develop capital market on a sound footing and to protect the interest of local investors a number of reforms has been introduced in current fiscal which include enactment of Central Depository System (CDS Amendment) Bill, 2002, introducing web-site of capital market and reduction of corporate tax rate. These reforms resulted in increase in average daily transactions in the capital market and rise in overall share price index in FY 2002-03 compared to 2001-02. In addition, there has been an investment to tune of Tk.1943.76 million up to June, 2003 through Initial Public Offer (IPO). There have been comprehensive reforms in foreign exchange management too. The Government has introduced floating exchange rate since 31 May, 2003. If

5

the newly introduced system brings in any instability, Bangladesh Bank will intervene through buying and selling of dollars directly to restore discipline.

The Government has passed a revised Privatisation Policy signalling its commitment to SOE reform. All SOEs have been put on hard budget constraint. In July, 2002, the Hon'ble Prime Minister took a politically bold decision and closed down the Adamjee Jute Mills, the largest jute mill of the World employing about 25,000 workers and accounting for about 10 percent of total annual SOE losses. Since then about 24 SOEs have already been either closed or downsized. They represent over 41 percent of aggregate SOE losses engaged in manufacturing. Employees retrenched from these SOEs have been reduced by 30 percent last year and we expect to reduce this loss further this year. The government is committed to continue reforms in the SOE sector keeping in view the interest of the economy; but this will have to be accompanied by satisfactory compensation and safety net programmes.

Adequate allocation has been made in the revised budget of FY 2002-03 to defray the severance benefits payable to the retrenched employees of the SOEs selected for privatization and to clear up arrears. More allocation is also being provided in the Revenue budget for FY 04 for operation and Maintenance expenditure. Recognizing the need to strengthen the governance of targeted food transfer programs, the Food for Education Program, and the Primary Education Stipends Program have been discontinued and have been replaced by a cash stipend program for primary school students. It may be noted here that to ensure transparency the government has already monetized most of its Food for Work (FFW) programs. The Government is determined to continue supporting the secondary education of girls and has decided to extend the Female stipends Program to Class 12. Controlling environmental pollution will get the priority it deserves for sustainable development. The Government has meanwhile banned the use and marketing of the polythene bags and has also phased out two stroke three wheelers from Dhaka city to eliminate one of the major sources of air pollution.

New incentive scheme has been introduced for improving performance of NCB's including collection of non-performing loans. Loan recovery departments have been strengthened. Necessary amendment to the Money Loan Courts have been enacted by the Parliament. Effective internal control is being set up in banks. To control default loan, Bangladesh Bank has issued necessary regulations. A Committee on default Loans was set up to suggest measures for reducing the burden of debt default and for improved loan management performance of the banking sector. A loan write off policy has been introduced by Bangladesh Bank for the first time.

Development Strategy

Since independence, the Government of Bangladesh has endeavoured to improve the quality of life of the people through planned development. Bangladesh has so far implemented 5 Five-Year

6

Plans including one Two-Year Plan. Allocation and expenditure of these plans together with the rate of growth achieved have been shown at Appendix-50.

The Plans could not achieve desired success against targeted objectives because of a host of factors including resource constraints. Bangladesh has, however, gained enviable success in terms of achieving improvements in most of the socio-economic indicators. Consistent with the market economy and the global context, required changes have been introduced in the development strategy of Bangladesh.

In the socio-economic realities of Bangladesh, the pursuit of medium-term development plan would be best suited for the desired growth of the country. Poverty reduction will be at the heart of such plan. The medium-term Plan will emphasise on detailed action plans against individual goals so that it can be achieved at the lowest level. If the medium-term plan is implemented within the vision of the long-term perspective, it would facilitate refixing of targets, inputs and objectives.

The Government has finalised a three-year 'National strategy for Economic Growth, Poverty Reduction and Social Development' to implement its medium-term plan. In the light of this strategy document, the Government will also prepare a three-year 'Rolling Investment Programme' which would form the basis of executing future plans.

National Strategy for Economic Growth, Poverty Reduction and Social Development

Immediately after taking office, the present Government, besides identifying the priority areas of reform, took up the task of preparing a 'National strategy for Economic Growth, Poverty Reduction and Social Development' in line with the UN Millennium Development Goals (MDG). In preparing this strategy document a wide consultation process was undertaken at the national level and local level including consultation with the experts and stakeholders. A preliminary draft of the document, was put in place in April, 2002. Based on this draft a comprehensive dialogue took place with the Government and non-government organisations, representatives from the civil society and the development partners. In the light of the feedback received a revised draft was prepared in January 2003. In March 2003, the draft was finalised after certain amendments.

The cardinal objective of the development strategy articulated in the document will be to make sure that benefits of growth are shared by the poor. The strategy document lays emphasis on the following five major strategies:

♦ Acceleration of pro-poor growth. ♦ Promotion of good governance ♦ Investment in human development ♦ Women development; and ♦ Ensuring social security.

7

Acceleration of Pro-poor Growth

In the strategy document, a target of raising economic growth from 5.0 percent to 6-7 percent has

been set so that the proportion of poor people can be reduced by half by 2015. The other

important segments of the strategy include:

♦ a stable macroeconomic framework

♦ development of private sector

♦ sound and effective financial systems

♦ strengthening institutional capacity

♦ rural development

♦ expansion of productive sectors

♦ improvement of existing capacity and quality of infrastructure development.

Promotion of Good Governance

The second important element of the strategy is establishing good governance in all spheres. With this end in view, the Government has planned to bring in judicial reforms to infuse dynamism in the judicial process, to bring about basic reforms in police administration and to ensure transparency and accountability in the use of public resources.

Investment in Human Development

As the development of human resources has strong poverty reducing effects, the Government lays special emphasis on enhancing the basic capacity of the poor by way of strengthening the health, education and nutrition programmes. To implement the strategy, the Government has already allocated substantial resources for expansion of education, particularly the primary education. As a result, there has been quantitative expansion in education but the health and nutrition programmes relatively lag behind. In the present strategy pursued by the Government, these two areas are having greater importance. Overall, the Government will divert and allocate more resources to all the programmes relating human resource development.

Women Development

The burden of poverty falls disproportionately on women due to a numbers of factors such as literacy rate, low nutrition, low and discriminatory wages and high mortality. Empowering women is critically important for socio-economic development. The degree of women empowerment is measured in terms of their access to education, participation in workforce, property rights, participation in politics and access to credit. Although Bangladesh has made much progress in this area, it leaves much to be desired. Against this backdrop, the strategy paper lays emphasis on:

♦ policies and institutional actions to close the gender gap

8

♦ reduce violence against women

♦ reduce high maternal mortality

♦ remove hindrances to women's employment and economic opportunities

♦ implement policies to ensure formal equality

♦ support affirmative actions at all levels and in all spheres

♦ create women-friendly institutional environment.

The Government in order to ensure greater participation of women in all spheres of development

within the framework of poverty reduction strategy, will actively promote appropriate policies

and programmes.

Ensuring Social Protection

Four sets of policies would be emphasised for the poor to cope better with various income shocks. These policies would increase the crisis -coping capacity of the poor. ♦ The first set of policies will focus on the social safety net for the poor through food for works

and income transfer programmes (e.g. VGD/IG-VGD, FFW/TR, old-age pension schemes in rural areas, support for the female destitutes and traditional relief programmes) to address the specific problems of chronic poverty and socially disadvantaged groups (e.g. street children, elderly poor, the disabled population etc.).

♦ The second set of policies will address the vulnerabilities of 'new poor' like the retrenched workers. This form an increasingly important component of the social protection policies in the backdrop of privatization, labour restructuring, market.

♦ The third set of policies will put emphasis on the development of social solidarity as an increasingly important route for social interventions. The newly set up umbrella support organization such as the Social Development Foundation (SDF) will play an important role in fostering social capital formation by promoting CBOs and local associations in building and maintenance of small-scale community infrastructures.

♦ The fourth set of policies will relate to risks insurance covering four categories: (a) providing access to credit to the poor in times of emergency to ease the burden of shocks; (b) ensuring good public health services to reduce health hazard related income and consumption shocks; (c) strengthening disaster preventing and mitigating mechanisms to enhance the coping capability of the poor in times of natural disasters; and (d) introducing effective measures to minimize suffering from violence and personal insecurity.

In the strategy document, there is an elaborate framework for monitoring and assessing the poverty reduction programmes. Within this framework a National Poverty Alleviation Council' headed by the Hon'ble Prime Minister has been formed. Besides this, a Focal Point has been

9

established in the General Economics Division of the Planning Commission which has been entrusted with the task of collecting all data and information on the progress of poverty reduction programmes.

Medium Term Macroeconomic Framework

To facilitate the implementation of the 'National Strategy for Economic Growth, Poverty Reduction and Social Development', a Medium Term Macroeconomic Framework (MTMF) has been specified. The framework has been worked out on the basis of the estimated values of FY 2002-03 as the benchmark. The purpose is to comprehend the dynamics of the economy identifying key macroeconomic fundamentals and formulate and implement realistic budgets.

The Framework envisages a stable macroeconomic environment during the period. It seeks to achieve an accelerated growth rate of GDP in real terms rising from 5.5 percent in FY2003- 04 to 6.5 percent in FY 06. The target rate of growth has been set to ensure a real breakthrough in poverty reduction in the medium term. The economy's average growth rate in the recent past, has been higher than the historic trend growth rate of 4 percent. Because of the adoptation and implementation of policies for structural reforms by the Government, it is expected that the growth momentum will be regained in FY 03, which will provide the basis for a new era of higher growth from FY 2003-04.

As high and variable inflation inhibits growth, worsens income distribution and the poverty situation, the framework envisages low and stable rate of inflation in the economy. A tight rein will be put on inflation so that the positive impact on poverty reduction achieved through higher growth is not frustrated. The rate of inflation is expected to be 4.0 percent in FY2004-05 and stable afterwards.

By the 1990s Bangladesh has made a transition from a situation of low saving and investment ratios to moderate saving and investment ratios. It is expected that the trend will continue and investment rates will increase further in the coming years. Moreover, the poverty reduction strategy would require higher growth which can be achieved through higher investment. Better management of public capital and more efficient provisioning of infrastructure leading to better utilization of private capital would be ensured such that the productivity of capital is enhanced and higher growth is achieved.

Accelerated poverty reduction would require higher amount of Government revenue which can be spent on programs benefiting the poor. The revenue-GDP ratio as well as the tax-GDP ratio are still low in Bangladesh compared with similar ratios in other developing countries. The Government plans to mobilize larger amount of domestic revenue so that the revenue-GDP ratio would rise from 10.6 percent in FY 2002-03 to 11.9 percent in FY 2005-06 and the tax GDP ratio from 8.3 percent to 9.7 percent during the same period. The government has already implemented some short term measures for increasing domestic resources in FY 2001-02. Several additional

10

measures have also been proposed in the FY2002-03 budget which have started to yield positive results. The government has also been rationalizing the prices of public goods and services to improve non-tax revenue collection. Future measures to increase revenue collections will focus on further reforms in the revenue system.

A significant increase in public expenditure is needed to reduce the incidence of poverty at a faster rate. Within the medium term framework, total government expenditure as a proportion of GDP will increase from 15.2 per cent in FY 2002-03 to 16.4 per cent in FY 2005-06. The rise in expenditure-GDP ratio would largely reflect the additional public expenditures required to finance new poverty reduction projects. The size of ADP will grow from 5.8 per cent of GDP in FY 2002-03 to 6.9 per cent in FY 2005-06 indicating expanded and improved absorption capacity of the key sectors in utilizing additional development resources.

The budget deficit will be kept under control in the neighborhood of 3.8 to 4.0 per cent (4.5 to 4.7 per cent excluding grants) of GDP and will be financed by both domestic and foreign resources. To avoid pressure on scarce budgetary resources it would be expedient to rely on foreign loans at concessionary interest rates to finance deficit. It is expected that increased volume of foreign resources will be forthcoming to finance the poverty reduction agenda under the strategy. Consequently, net foreign financing (excluding grants) as proportion of GDP would increase from 1.6 percent in FY 2002-03 to 1.8 percent in FY 2005-06. Net domestic financing has been projected at 1.9 per cent of GDP in FY 2005-06. The monetary and credit program for the medium term has been designed to ensure higher growth of GDP as well as price stability. Broad money growth rate would decline from 12.5 per cent in FY 2002-03 to 11.9 per cent in FY 2005-06. The reserves money will be used as an operating target to keep broad money growth within reasonable limit.

The balance of payments (BOP) situation would also improve during the program period. The assumption underlying the projected behavior is the steady growth of exports along with enhanced inflow of multilateral and bilateral inflows to finance new poverty reduction programs. The gross official reserves would increase to US$ 3.3 billion (3.2 months import equivalence) in FY 2005-06.

11

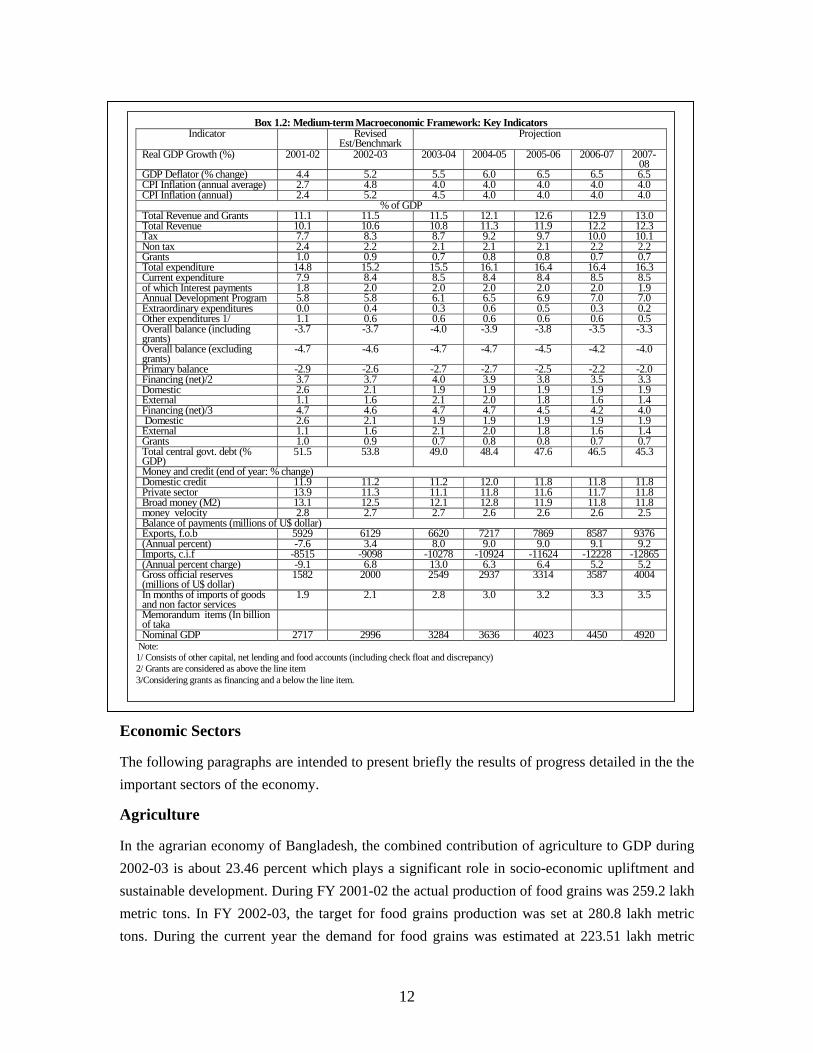

Box 1.2: Medium-term Macroeconomic Framework: Key Indicators

Indicator Revised Est/Benchmark

Projection

Real GDP Growth (%) 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08

GDP Deflator (% change) 4.4 5.2 5.5 6.0 6.5 6.5 6.5 CPI Inflation (annual average) 2.7 4.8 4.0 4.0 4.0 4.0 4.0 CPI Inflation (annual) 2.4 5.2 4.5 4.0 4.0 4.0 4.0

% of GDP Total Revenue and Grants 11.1 11.5 11.5 12.1 12.6 12.9 13.0 Total Revenue 10.1 10.6 10.8 11.3 11.9 12.2 12.3 Tax 7.7 8.3 8.7 9.2 9.7 10.0 10.1 Non tax 2.4 2.2 2.1 2.1 2.1 2.2 2.2 Grants 1.0 0.9 0.7 0.8 0.8 0.7 0.7 Total expenditure 14.8 15.2 15.5 16.1 16.4 16.4 16.3 Current expenditure 7.9 8.4 8.5 8.4 8.4 8.5 8.5 of which Interest payments 1.8 2.0 2.0 2.0 2.0 2.0 1.9 Annual Development Program 5.8 5.8 6.1 6.5 6.9 7.0 7.0 Extraordinary expenditures 0.0 0.4 0.3 0.6 0.5 0.3 0.2 Other expenditures 1/ 1.1 0.6 0.6 0.6 0.6 0.6 0.5 Overall balance (including grants)

-3.7 -3.7 -4.0 -3.9 -3.8 -3.5 -3.3

Overall balance (excluding grants)

-4.7 -4.6 -4.7 -4.7 -4.5 -4.2 -4.0

Primary balance -2.9 -2.6 -2.7 -2.7 -2.5 -2.2 -2.0 Financing (net)/2 3.7 3.7 4.0 3.9 3.8 3.5 3.3 Domestic 2.6 2.1 1.9 1.9 1.9 1.9 1.9 External 1.1 1.6 2.1 2.0 1.8 1.6 1.4 Financing (net)/3 4.7 4.6 4.7 4.7 4.5 4.2 4.0 Domestic 2.6 2.1 1.9 1.9 1.9 1.9 1.9 External 1.1 1.6 2.1 2.0 1.8 1.6 1.4 Grants 1.0 0.9 0.7 0.8 0.8 0.7 0.7 Total central govt. debt (% GDP)

51.5 53.8 49.0 48.4 47.6 46.5 45.3

Money and credit (end of year: % change) Domestic credit 11.9 11.2 11.2 12.0 11.8 11.8 11.8 Private sector 13.9 11.3 11.1 11.8 11.6 11.7 11.8 Broad money (M2) 13.1 12.5 12.1 12.8 11.9 11.8 11.8 money velocity 2.8 2.7 2.7 2.6 2.6 2.6 2.5 Balance of payments (millions of U$ dollar) Exports, f.o.b 5929 6129 6620 7217 7869 8587 9376 (Annual percent) -7.6 3.4 8.0 9.0 9.0 9.1 9.2 Imports, c.i.f -8515 -9098 -10278 -10924 -11624 -12228 -12865 (Annual percent charge) -9.1 6.8 13.0 6.3 6.4 5.2 5.2 Gross official reserves (millions of U$ dollar)

1582 2000 2549 2937 3314 3587 4004

In months of imports of goods and non factor services

1.9 2.1 2.8 3.0 3.2 3.3 3.5

Memorandum items (In billion of taka

Nominal GDP 2717 2996 3284 3636 4023 4450 4920 Note: 1/ Consists of other capital, net lending and food accounts (including check float and discrepancy) 2/ Grants are considered as above the line item 3/Considering grants as financing and a below the line item.

Economic Sectors

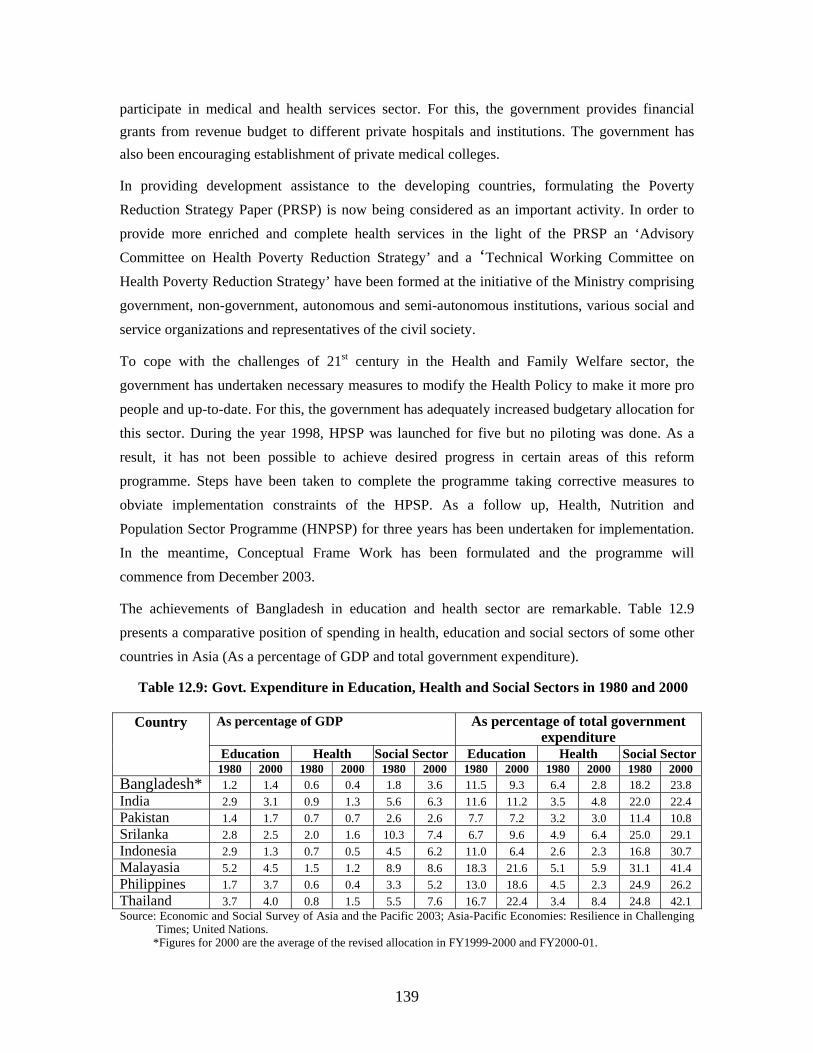

The following paragraphs are intended to present briefly the results of progress detailed in the the important sectors of the economy.

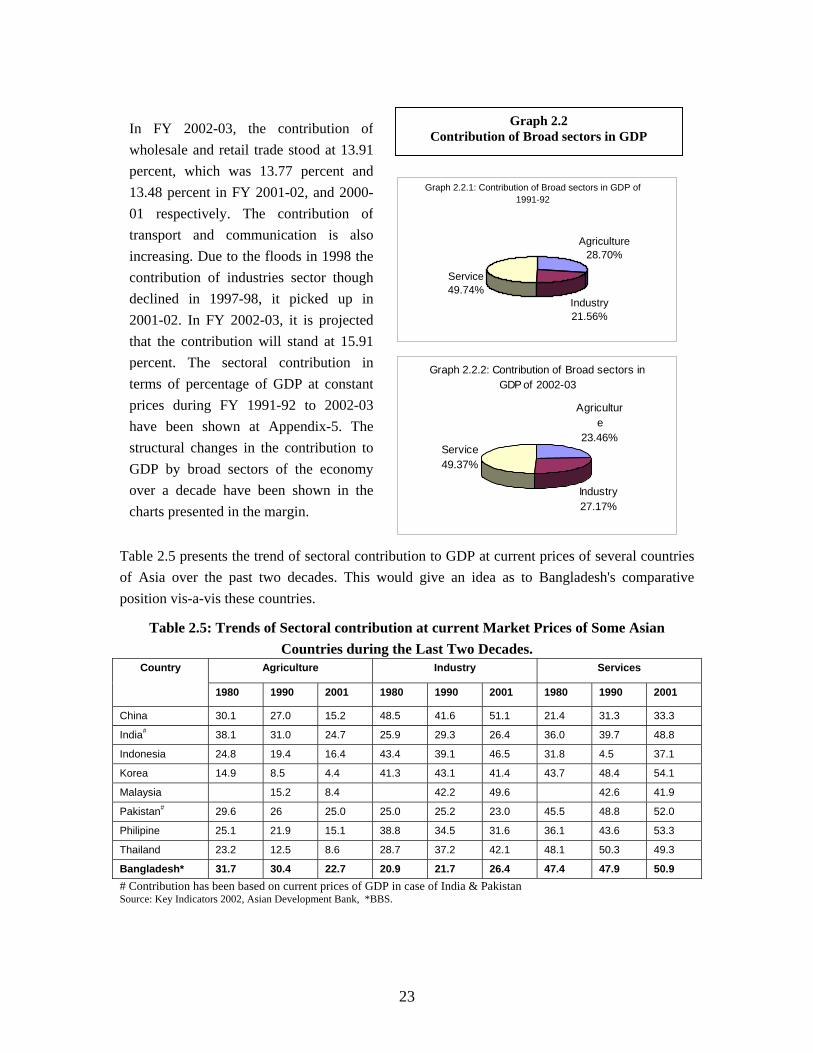

Agriculture

In the agrarian economy of Bangladesh, the combined contribution of agriculture to GDP during 2002-03 is about 23.46 percent which plays a significant role in socio-economic upliftment and sustainable development. During FY 2001-02 the actual production of food grains was 259.2 lakh metric tons. In FY 2002-03, the target for food grains production was set at 280.8 lakh metric tons. During the current year the demand for food grains was estimated at 223.51 lakh metric

12

tons. During this year the growth in agriculture and fisheries sectors has been projected at 3.6 and 2.3 percent respectively. As agriculture is the mainstay of the economy, besides reducing poverty it contributes significantly to ensuring food security for a vast population, together with improving their standard of living and augmenting employment opportunities. There have been continued efforts from Government for development of agriculture. Included among them are management of irrigation water, availability of fertilizer, introducing commercial orientation to livestock sub-sector, massive afforestation throughout the country and preservation of forest, meeting the deficiencies in forest resources, ensuring supply of raw materials for forest-based industries, conservation of bio-diversity and wild-life and protection of environment and control of air-pollution for sustainable development.

Industry

The role of industry (manufacturing) sector is central to the economic development of a country. During FY 2002-03, the contribution of this sector to GDP has been estimated at 15.91 percent while its growth has been projected at 6.62 percent. All industries excepting those relate to national security have been made open for local and foreign investors. An inspired and dynamic private sector's role will be critical for industrialisation of Bangladesh. And this should be made competitive in a deregulated domestic and international market. Included in the vision of industrialisation, there is a goal of having 25 percent contribution of manufacturing sector to GDP. It has also been envisioned that this sector will absorb 20 percent of workforce. In order to encourage industrial growth, the rate of interest for all industries under the thrust sector have been reduced from 10-12.5 percent to 9 percent. The interest rate of shipment and packing credit has also been reduced from 8-10 percent to 7 percent. In addition, the bank rate has been reduced from 7 percent to 6 percent to reduce the interest rate of bank loan. Since establishment of Privatisation Board (Now Privatisation Commission), up to June, 2003 a total of 42 industrial entities have been privatised. Much wider initiatives are in place to accelerate the pace of privatisation. In FY 2001-02 the net loss of 44 SOEs amounted to Tk.1533.56 crore. In FY 2002-03, the net loss has been estimated at Tk.1026.81 crore. Foreign Direct Investment in the country has now increased substantially. In FY 1991-92 the foreign investment stood at US$ 25 million. In FY 2002-03 it stood at US$368 million. The Government has already declared a range of facilities for foreign investment. Currently, six Export Processing Zones (EPZs) are operating in the country. Up to June 2003, 180 industries were operational in these zones which had a total investment to the tune of US$ 634.04 million.

Power and Energy

During the current year, the total power generation capacity increased to 4680 mw following commercial operation of the 450 mw Combined Cycle Power Plant set up under the private sector initiative since October, 2002. Against this installed capacity, 3622 mw power is being generated.

13

The present Government has taken up a set of comprehensive development and reform programmes to attract private sector investment to supplement the Government investment to increase power generation. In the current year, out of the total power generated, the public sector's share is 78.38 percent while the private sector accounts for 21.26 percent share. Of the total power generated, 90.66 percent is gas-based, 3.88 percent is hydraulic and 5.46 percent is oil-based. Bangladesh Power Development Board (BPDB) is playing one of the major roles in power generation. Besides, Bangladesh Rural Electrification Board (BREB), Dhaka Electric Supply Company (DESCO) and Power Grid Company of Bangladesh (PGCB) are also working for managing transmission and distribution system of power. Through the PDB system, power is distributed through 33 kv and 11 kv lines. Power generated in different plants is distributed through 230 kv and 123 kv lines. A total of 22 gas fields has been discovered in the country so far. Out of the total extractable reserve of gas, 391.53 billion cft have been extracted during FY 2001-02. The whole country has been divided into 23 blocs for special exploration of gas resources and also for expansion of the use of gas. So far Production Sharing Contract (PSC) has been concluded for 12 blocs. In order to meet the increasing demand for gas, the private sector is coming up side by side with the public sector. In order to contain environment pollution, the process of converting vehicles into CNG is under way. Under the 'Dhaka Clean Fuel Project' the petrol-driven auto rickshaws and cars are being converted into CNG at both public and private sector levels. Bangladesh Petroleum Corporation has taken measures to make the storage facilities at different sites in Bangladesh developed, expanded and also internationally acceptable in terms of quality and standard. The companies under Petrobangla are being awarded administrative and financial autonomy for exercising more powers.

Transport and Communication

The system of transport and communication is of immense importance for development of Bangladesh. The contribution of this sector to GDP at constant price is 9.78 percent (provisional). The transport and communication network in Bangladesh consists of road transport, railways, water and airways, post and telecommunication and information technology. Although immediately after independence there was a road network of 4000 kilometres only; it increased, according to the estimates of 1998, to a huge road network of 2 lakh 23 thousand kilometres with national highways, regional highways, feeder roads and rural roads. Bangladesh Road Transport Authority was set up to take care of overall supervision, management and supervision of the transport sector. As a cheap mode of transportation, the importance of Bangladesh Railway is immense. Despite the fact that Bangladesh Railway had been a loss-making entity for many years, it has introduced recently a set of reform programmes that aim to reduce the deficit of Railway, abolish the system of open ended subsidy and rationalise manpower, among others. In maritime-trade of the country, Chittagong and Mongla Port Authorities play critical role. A small part of the remaining external trade is performed through land ports and air routes. Bangladesh

14

Shipping Corporation has built-up a mixed fleet of 13 vessels in order to provide efficient shipping services as well as to perform properly most of the external trade activities linked to international maritime trade. In addition, there is a Directorate of Shipping to ensure accident-free movements of all kinds of ships that include ships operating in inland waterways, coastal fishing trawlers, ships bound for foreign destination and ships coming into Bangladesh ports and also to protect commercial interests of Bangladeshi ships. Bangladesh Inland Water Transport Corporation is a service-oriented organisation. This entity, as a public utility service, is playing an important role in transporting commodities, passengers and vehicles. In order to enhance trade activies with the neighbouring countries, 13 land ports have been established at the Bangladesh-India border under Bangladesh Land Port Authority. Biman Bangladesh Airlines is the only public sector organisation engaged in the task of managing air travels. Amidst global recession in aviation business, Biman is continuing its operational activities in the competitive market with its limited resources. In the socio-economic development of Bangladesh, the role of telecommunication is significant. In view of the increasing public demand, as the number of telephones, NWD circuits and overseas circuits increased, so the revenue augmented over the last ten years. Opening up of cellular phones to private sector has increased teledensity significantly. Bangladesh Postal Department is a service-oriented organisation. The department makes arrangements for speedy dispatch of mails throughout the country through Biman, Railway, Bus and Launch. In addition, the department provides quite a few special services through which valuable articles, documents etc. can be sent to and from the country. In the current context of globalisation and market economy, economic development is not possible without achieving progress in information technology. In order to bring about improvement in this sector, the Government has taken up a comprehensive development programme.

Poverty Reduction

Poverty is a multi-faceted problem. The primary goal of the overall development efforts of Bangladesh government is the reduction of poverty. Poverty reduction, has, therefore, been given the top-most priority in the development plans of the country and a range of programmes are being implemented. According to the report on Household Income and Expenditure Survey 2000, (HIES) published by Bangladesh Bureau of Statistics (BBS), the absolute poverty at national level on the basis of daily calorie intake of 2122 k. cal. was 47.75 percent in 1998-99 and 44.33 percent in 2000. During the same period the hardcore poverty measured against 1805 k. cal was 28.36 and 19.98 percent. The poverty trend has been calculated according to Cost of Basic Needs (CBN) methodology introduced in 1995-96. According to this methodology, using high and low poverty lines the impact of poverty at national level are 49.8 percent and 33.7 percent. According to Bangladesh Human Development Report 2000, Human Development Index was 16.3 percent in 1981-83 and 34.8 percent in 1998-2000. In a recent meeting with the Secretaries, the Hon'ble Prime Minister emphasised the need for implementing programmes having poverty reducing

15

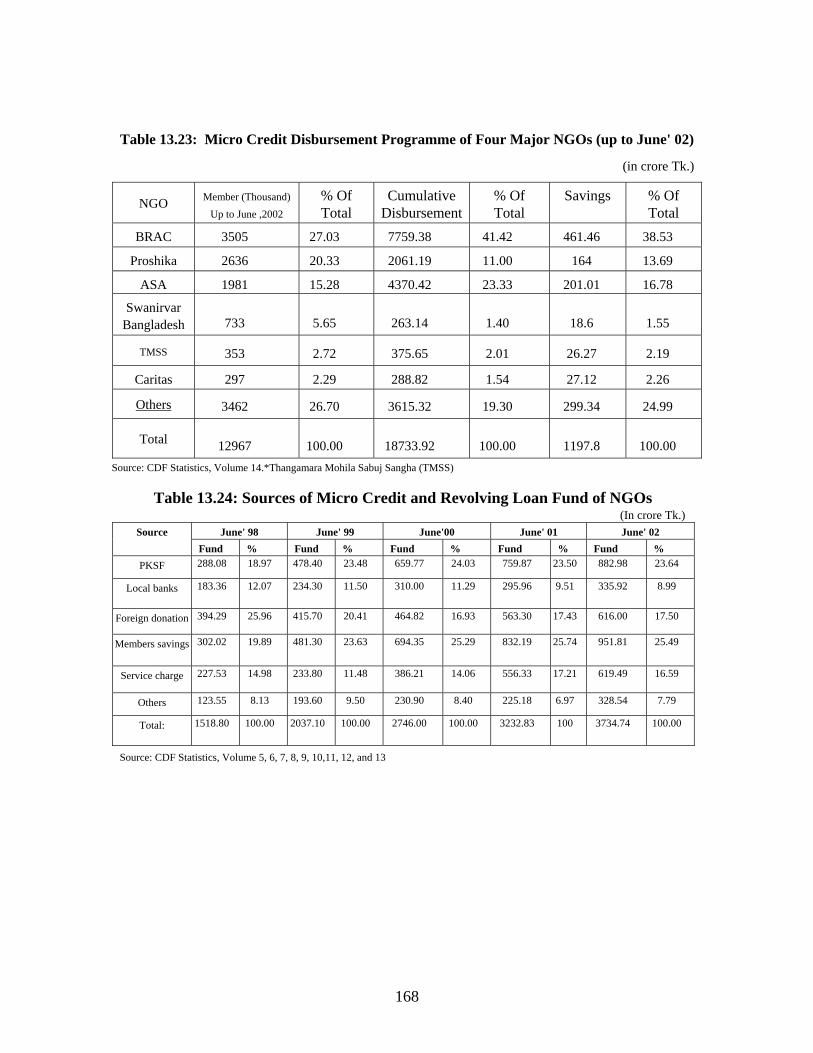

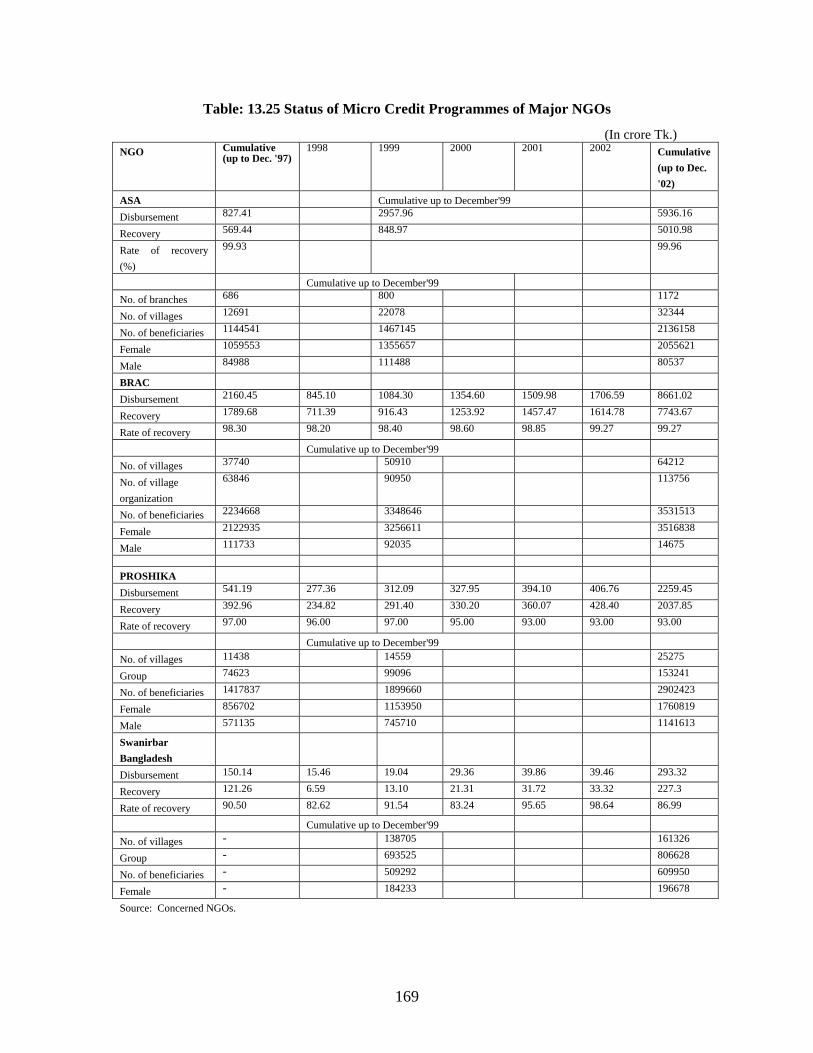

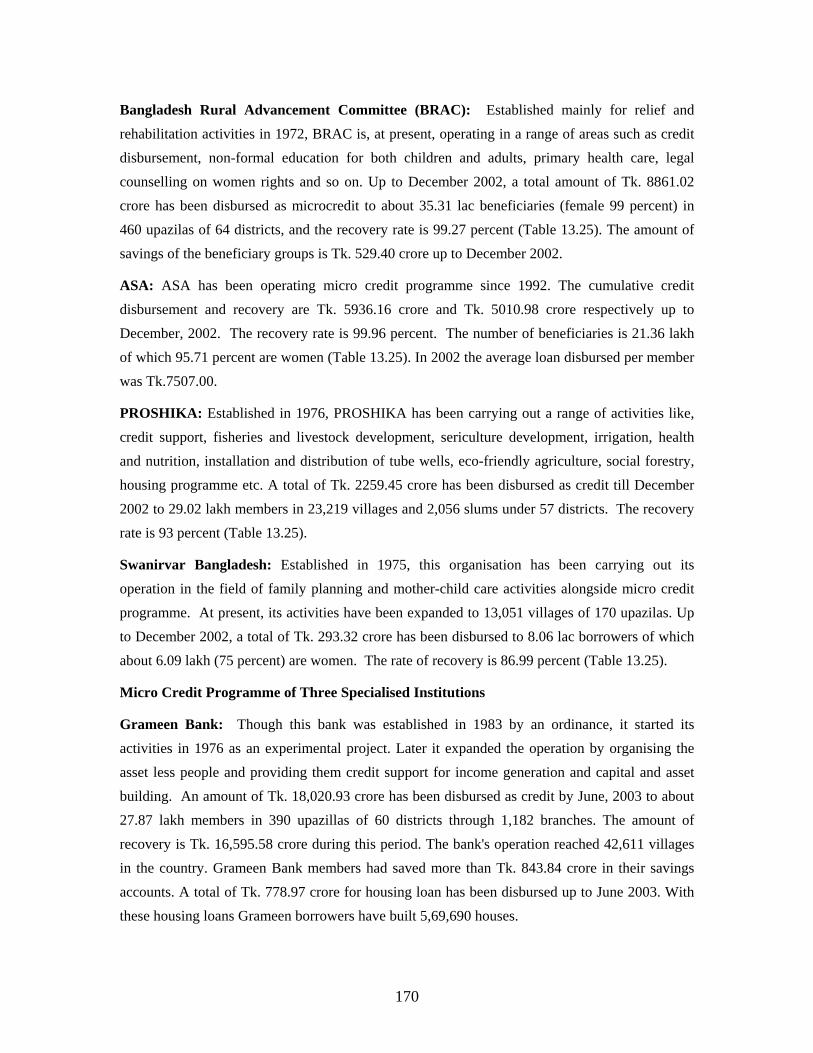

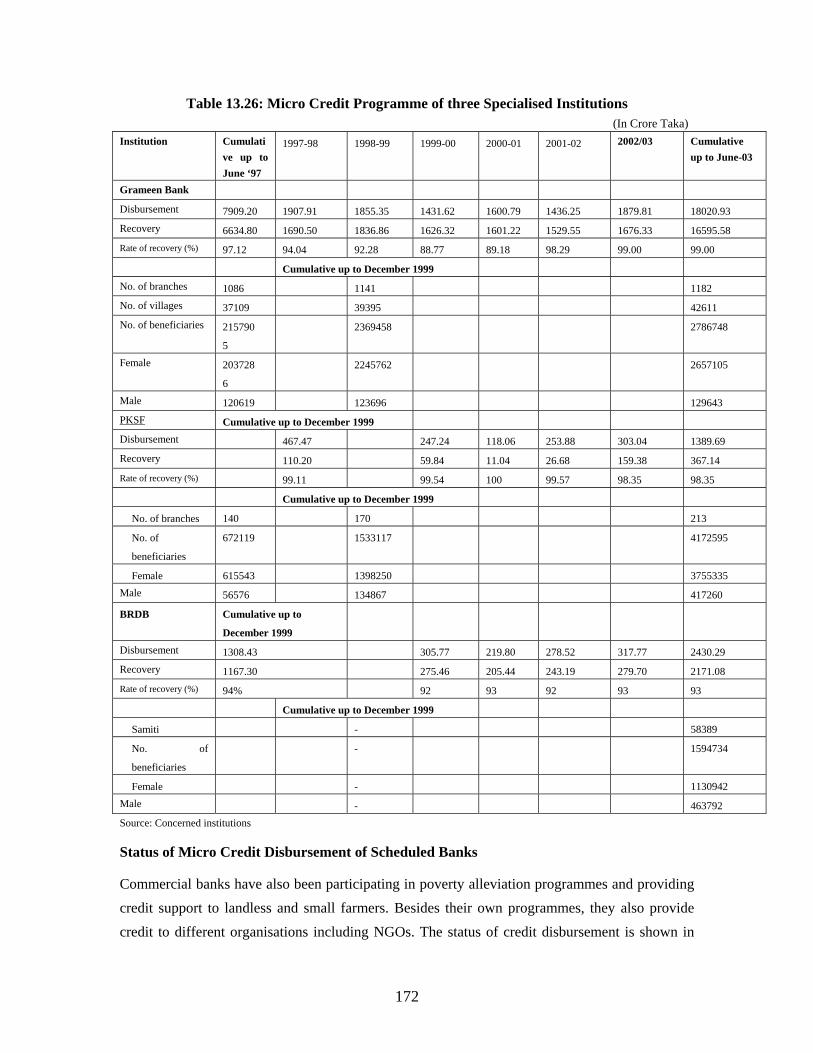

effects on a priority basis. Included among them are plantation of trees, fish cultivation, goat rearing, primary and women education, information and communication technology, library development, children's right, vocational and technical education and housing for the poor. In addition, a project has been taken up at the initiative of the Hon'ble Prime Minister at a cost of Tk. 447.00 crore for reduction of poverty. The implementation of the project will be completed by June, 2006. The role of micro-credit in reducing poverty is widely recognised. Bangladesh Rural Development Board (BRDB), Palli Karma Shahayask Foundation (PKSF) and a number of Government Agencies are engaged in distributing micro credit. Besides Grameen Bank, the scheduled banks are also participating in micro-credit distribution programme. Alongside the Government organisations, the Non-government organizations (NGOs) are also carrying out micro-credit operations. Among the NGOs, ASA, BRAC, PROSHIKA and SWANIRVHAR are playing significant role in this area.

Human Resource Development

The fundamental objective of economic upliftment is human development. The role of literate, healthy and efficient human resources is critical to the intended development of a country by achieving sustainable and higher growth. Education training, health and social services as tools for human resources development are gaining increasing importance. Realising this importance, the government in response is channeling increased resources to social sectors for human resource development. In FY 2002-03, the share of social sector in total public outlay has been estimated at 24 percent. The primary education has been made compulsory since 1990. Stipends for female students have been introduced to promote women education. A system of informal education for adult and illiterate learners has also been introduced. The outcome of these initiatives is that the current rate of literacy now rises to 62.66 percent. In order to build a system of quality education, a number of programmes has been introduced including teachers' training, revision of curriculum and infrastructure development. Greater emphasis has been laid on science & technology and vocational education. Efforts are under way to build an effective and sound health services to ensure sound public health alongside education. The Five-Year Health and Population Sector Programme (HPSP) was scheduled to be terminated in June 2003 but eventually completed in December 2003. A Health, Nutrition and Population Sector Programme (HNPSP) will commence from January 2004. Government is taking a range of measures through the Ministry of Women and Children's Affairs for women and children development. With a view to removing the gender inequality and to involve women with the mainstream of development activities, a variety of programmes has been adopted at governmental level. Elaborate programmes are being implemented to convert the youth force of the country into a productive force. In order to ensure utilisation of youth force in the developmental pursuit of the Government, adequate provisions have been made for training and efficiency enhancement of the unemployed youth, credit support, motivation and grants. To ensure welfare for the landless,

16

destitute, vagabonds, orphans, retarded and other disadvantaged classes, a variety of development programmes has been adopted. In addition a number of programmes aimed to develop sports and culture are being implemented. Implementation of these programmes are resulting in gradual development of human resources.

Private Sector Development

In market economy, private sector is the main engine of growth and development. The present Government continues its efforts for increased participation of private sector in the overall development activities of the country. It is trying to create an investment-friendly environment in the one hand, and taking initiatives for involving private sector for sustainable development on the other. Among the many initiatives of the Government, significant ones are formulation of different policies, reform of industrial policies, setting up Bangladesh Investment Board, (BOI) constituting Privatization Commission and strengthening of capital market. Private initiatives in the power and energy sector are being particularly encouraged. In FY2002-03, with the commissioning of two power plants under the private sector, the total power generation increased to 3622mw from 3218mw earlier. In telecommunication sector, two private companies are making significant contribution. Up to June 2003, 4 private companies provided 13 lakh 79 thousand cellular mobile connections which was 7 lakh in the previous year. In addition, 2 private companies have installed 25,348 fixed lines. Because of a range of initiatives in the transport sector, involvement of private sector is increasing in air-transport, water-transport and railway. GMG Air Lines are now operating in domestic and international air-routes. In construction and operation of container terminal for water-transport, in development and operation of landing station, private sector initiatives are being encouraged. In addition, decision has been taken to place different land ports under the private sector. Currently 40 banks, 60 insurance companies and 28 other financial institutions are operating under the private sector. These institutions, besides providing sound and efficient services, are supporting to make investment easy and competitive. Up to 2002 a total 24736 registered non-government primary schools has been established under the private initiative. In addition, a significant number of secondary schools, colleges and universities has also been established. In the health sector currently 642 private hospitals and clinics are operating. It has been made possible to save valuable foreign currencies by way of providing higher education and specialised health services. A comprehensive programme is in existence under the private sector initiative in the agriculture sector. The private sector is making special contributions in the areas of selling of shallow tube-wells, production and marketing of quality seeds, improvement of irrigation systems etc. Private initiatives are making special contributions to the jute and textile sectors too. Currently there are as many as 182 cotton mills in the country of which 156 cotton mills are under private sector. There are 3800 export-oriented garment industries that absorb a work force of 1.8 million. Consequent on a range of measures taken by the Government, private sector investment increased gradually which now

17

accounts for 71 percent of the total investment. During July 2002 to June 2003, the total number of industries registered with the Board of Investment stood at 2200 and the total investment proposed amounted to Tk.137,711 million. During the corresponding period of the previous year, the proposed investment of the registered industries amounted to Tk.105,400 million. As the rise in private investment will contribute to rise in production and attaining efficiency, so will it contribute to reduction of revenue expenditure for infrastructure and human resource development.

World Economic Outlook

In 2002 the world economy started recovering from the ills of severe recession in 2001. As a result, in the early part of 2002, the signs of achieving higher growth became evident in the global economy. But amidst continuation of adverse impact of the bursting of equity market bubble, rising political uncertainty, low market confidence and the escalation of oil prices, the pace of recovery slowed towards the end of 2002. Despite that the world output grew by 3.3 percent in 2002 from its dismal 2.3 percent registered in 2001. However, consistent monetary and fiscal policy pursued by the industrialised developed countries, improved macroeconomic management with accelerated structural reform in developing countries were the major contributing factors for the growth recovery. As the two major economic blocs, the Euro area and Japan remained relatively weak, a faster global recovery during the year was stalled. Due to the economic uncertainty throughout the world and the Iraq war, the projection of global economic growth for 2003 had to be adjusted. According to the IMF projection as presented in 'World Economic Outlook' published in February this year, the world output was estimated at 3.3 percent. But in the changed scenario, this projection has been revised to 3.2 percent in April 2003. In this projection, the rate of growth in developed countries has been estimated at 1.9 percent. In the case of the developing countries, this has been projected at 5.0 percent. Again among the developing countries, the growth of the developing Asia might be around 6.3 percent. According to revised projection of IMF, the growth of world trade in 2003 would be 4.3 percent which is 0.3 percent less than the projection of February 2003. But the impact of the realities emerging during post-Iraq war would call for a fresh projection of world economic growth in 2003.

18

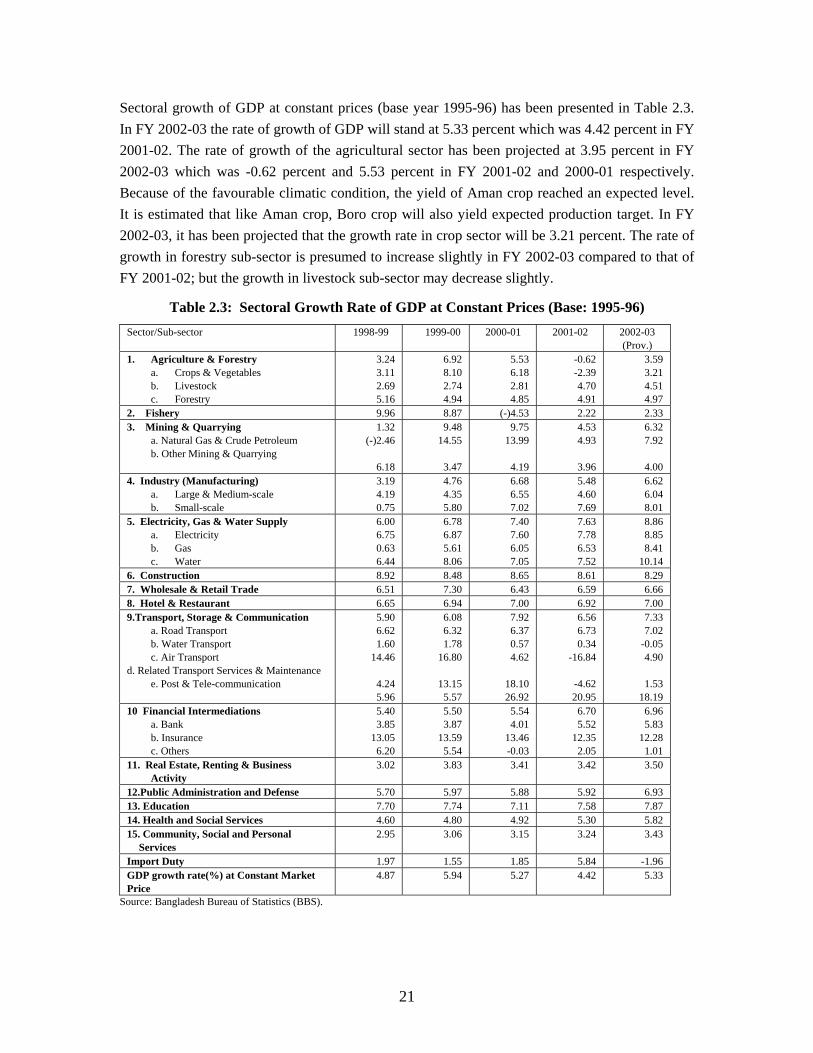

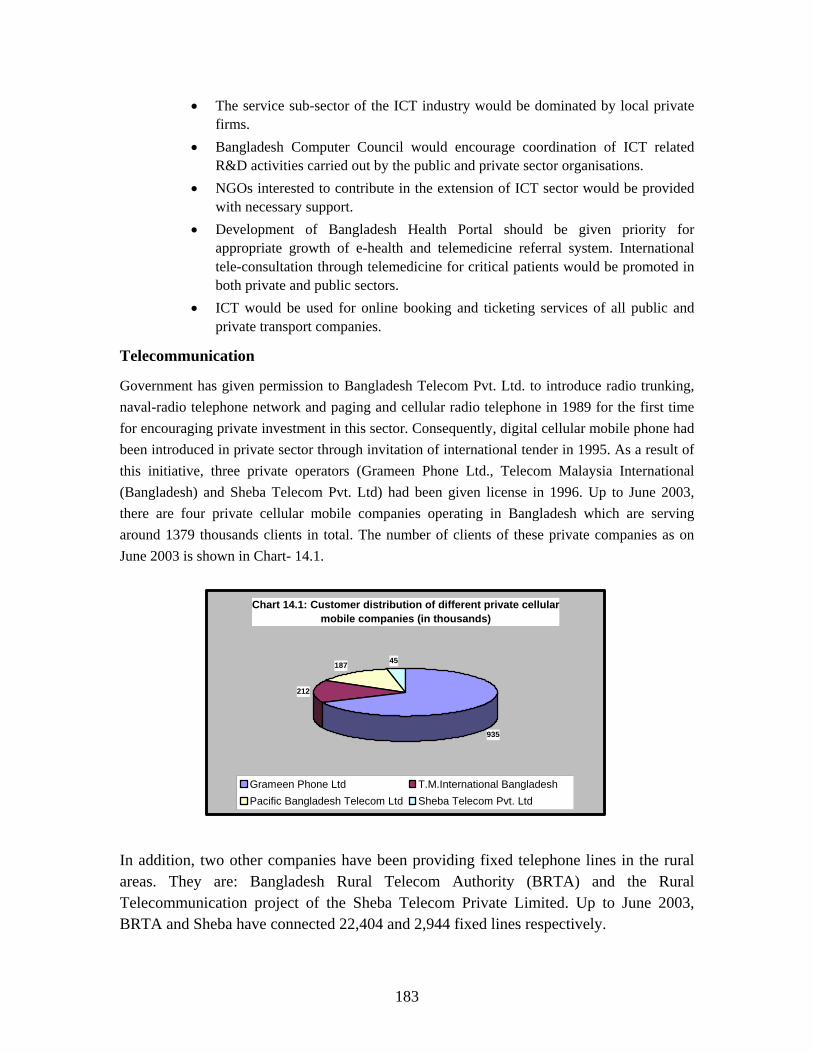

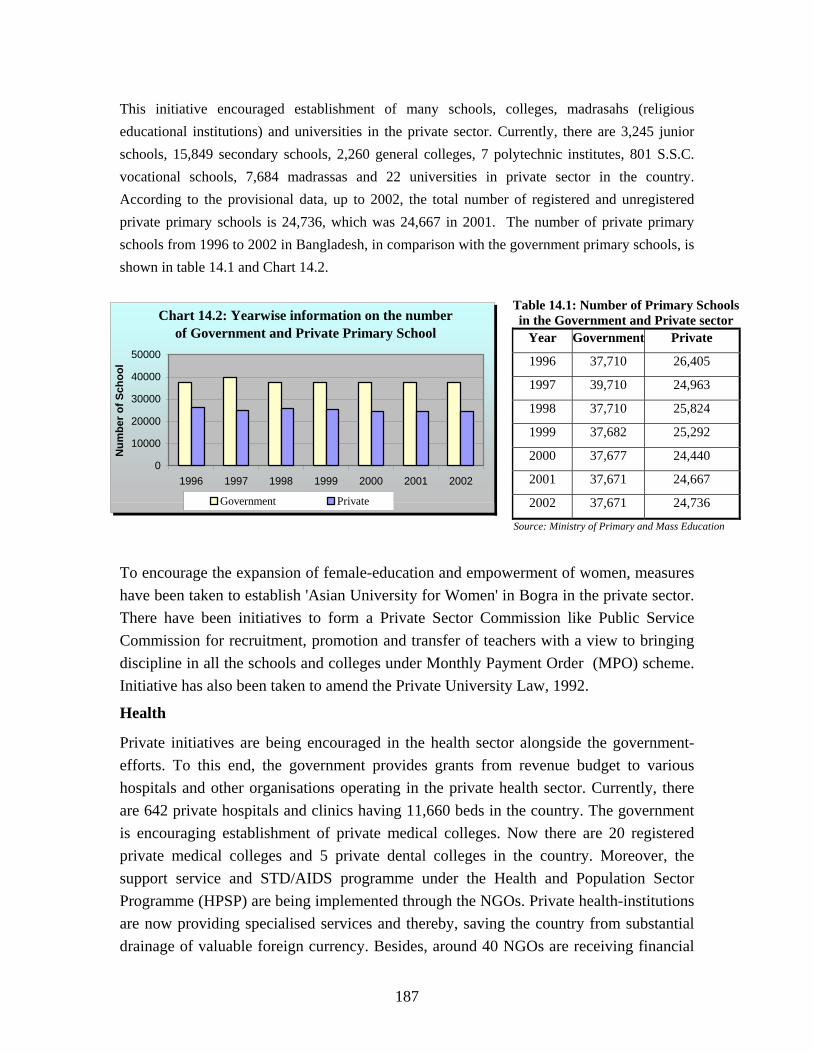

CHAPTER-2 GDP, SAVING AND INVESTMENT