Goodbody Stockbrokers (trading as Goodbody) is regulated by the Central Bank of Ireland. For the attention of US clients of Goodbody Securities Inc, this third-party research report has been produced by our affiliate Goodbody Stockbrokers. Please see the end of this report for analyst certifications and other important disclosures. Irish Property A detailed analysis of the prospects for Irish Property Foundations of recovery Economic Research 27 Sep 2013 New property cycle begins as domestic demand starts to recover Following record falls in property prices (commercial -67%, residential -50%) and construction output (-80%), we believe the property market is set for better times. This will be driven by domestic demand returning to growth in 2014 and continued strength in FDI. As a result, supply-demand imbalances will start to emerge in some segments of the property market, especially in Greater Dublin. Commercial property assets, particularly offices, offer significant value Our analysis shows that the office market, particularly in Dublin, offers the best investment prospects. This is based on limited availability of quality stock in key locations, with no new builds on the horizon and increasing demand from the IT/Financial sectors as Dublin becomes a hub for such activities. All of which will put upward pressure on rents which remain at half of peak 2007 levels. Returns are also attractive in other commercial market segments, but also face more fundamental challenges, particularly in the retail sector. Dublin to lead housing recovery with total completions of 25k by 2020 Based on relatively conservative assumptions, Irish housing demand is expected to increase from the current level of less than 10k p.a. to 26-36k by 2026, with over a third of this in Dublin. These demand projections underpin our house completion forecasts of c.25k by 2020 and 33k in 2026. The strong demand for housing in Greater Dublin, coupled with limited supply, means that prices will experience the most upward pressure in the capital. Indeed, recent pricing trends suggest that this has already begun. Market conditions in other parts of Ireland will be more challenging given excess supply, especially in the West & Border counties. Scope for Irish construction sector to grow strongly Construction activity in Ireland now represents only 7% of GNP, down from 25% at the peak and versus a European LT average of 12%. The strong demand that we see in both the housing and office markets, coupled with a recovery in other segments of the construction sector, underpins our forecast for construction output growth of 10% p.a. which implies the sector accounting for 11% of GNP by 2020. Opportunity knocks on playing the Irish property recovery Our detailed analysis gives us increasing comfort that the Irish property sector has turned the corner. From an investment perspective, this can be played a number of ways : (i) directly through the underlying asset, especially Dublin Offices where we see returns of circa 10% p.a; (ii) via a REIT; (iii) construction related stocks, especially Grafton as it has the biggest exposure at over 20% of sales, (iv) Financials stocks, particularly Bank of Ireland, where risks to forecasts are to the upside; (v) the balance sheet of the banks, in particular the BKIR cocos and covered bonds, and;(vi) through the sovereign, as a general play on Ireland. 0 50 100 150 200 250 300 350 400 450 Index (1983=100) GDP Housebuilding Comm property prices (real) Resi prices (real) GNP Source: CSO, DoELG, IPD, Goodbody Ireland's property crash in an historical context Residential prices have halved Real commercial property prices are 25% below 1983 levels Housebuilding at record lows -6 -4 -2 0 2 4 6 8 10 12 14 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 % Commercial yield 10-year bond yield Spread Average spread Source: IPD, FactSet, Goodbody Commercial yields at a record high relative to bond yields 0% 5% 10% 15% 20% 25% 30% 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 % of GNP Base case Conservative Optimistic EU historical average Source: CSO, Euroconstruct, Goodbody Scope for significant growth in construction - scenario analysis Economists Dermot O'Leary +353-1-641-9167 [email protected] Juliet Tennent +353-1-641-9469 [email protected]

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Goodbody Stockbrokers (trading as Goodbody) is regulated by the Central Bank of Ireland. For the attention of US clients of Goodbody

Securities Inc, this third-party research report has been produced by our affiliate Goodbody Stockbrokers. Please see the end of this

report for analyst certifications and other important disclosures.

Irish Property A detailed analysis of the prospects for Irish Property

Foundations of recovery

Economic Research 27 Sep 2013

New property cycle begins as domestic demand starts to recover

Following record falls in property prices (commercial -67%, residential -50%) and

construction output (-80%), we believe the property market is set for better times.

This will be driven by domestic demand returning to growth in 2014 and continued

strength in FDI. As a result, supply-demand imbalances will start to emerge in

some segments of the property market, especially in Greater Dublin.

Commercial property assets, particularly offices, offer significant value

Our analysis shows that the office market, particularly in Dublin, offers the best

investment prospects. This is based on limited availability of quality stock in key

locations, with no new builds on the horizon and increasing demand from the

IT/Financial sectors as Dublin becomes a hub for such activities. All of which will

put upward pressure on rents which remain at half of peak 2007 levels. Returns

are also attractive in other commercial market segments, but also face more

fundamental challenges, particularly in the retail sector.

Dublin to lead housing recovery with total completions of 25k by 2020

Based on relatively conservative assumptions, Irish housing demand is expected to

increase from the current level of less than 10k p.a. to 26-36k by 2026, with over

a third of this in Dublin. These demand projections underpin our house completion

forecasts of c.25k by 2020 and 33k in 2026. The strong demand for housing in

Greater Dublin, coupled with limited supply, means that prices will experience the

most upward pressure in the capital. Indeed, recent pricing trends suggest that

this has already begun. Market conditions in other parts of Ireland will be more

challenging given excess supply, especially in the West & Border counties.

Scope for Irish construction sector to grow strongly

Construction activity in Ireland now represents only 7% of GNP, down from 25% at

the peak and versus a European LT average of 12%. The strong demand that we

see in both the housing and office markets, coupled with a recovery in other

segments of the construction sector, underpins our forecast for construction output

growth of 10% p.a. which implies the sector accounting for 11% of GNP by 2020.

Opportunity knocks on playing the Irish property recovery

Our detailed analysis gives us increasing comfort that the Irish property sector has

turned the corner. From an investment perspective, this can be played a number

of ways : (i) directly through the underlying asset, especially Dublin Offices where

we see returns of circa 10% p.a; (ii) via a REIT; (iii) construction related stocks,

especially Grafton as it has the biggest exposure at over 20% of sales, (iv)

Financials stocks, particularly Bank of Ireland, where risks to forecasts are to the

upside; (v) the balance sheet of the banks, in particular the BKIR cocos and

covered bonds, and;(vi) through the sovereign, as a general play on Ireland.

0

50

100

150

200

250

300

350

400

450

Index (

1983=

100)

GDP Housebuilding Comm property prices (real) Resi prices (real) GNP

Source: CSO, DoELG, IPD, Goodbody

Ireland's property crash in an historical context

Residential prices have halved

Real commercial property prices

are 25% below 1983 levels

Housebuilding at record lows

-6

-4

-2

0

2

4

6

8

10

12

14

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

%

Commercial yield 10-year bond yield Spread Average spread

Source: IPD, FactSet, Goodbody

Commercial yields at a record high relative to bond yields

0%

5%

10%

15%

20%

25%

30%

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

% o

f G

NP

Base case Conservative Optimistic EU historical average

Source: CSO, Euroconstruct, Goodbody

Scope for significant growth in construction - scenario analysis

Economists

Dermot O'Leary

+353-1-641-9167

Juliet Tennent

+353-1-641-9469

Goodbody Economy - Ireland

Page 2 27 Sep. 2013

Key Themes

The property industry has arguably played the most influential role in the Irish economy over recent

years. Between 2002 and 2007, it played a crucial role in growth in employment, tax revenues, credit

and output. From 2007 onwards, the industry collapse triggered knock-on implications for the banks,

household wealth and the depth of the recession. Prices and output in the sector now appear to be

stabilising. This report provides a comprehensive analysis of the prospects for the sector. Given the

importance of the economic cycle to developments in the sector, the report begins with an updated view

on the economic outlook. This is followed by a detailed appraisal of the prospects for the commercial

property market as well as a forecast of potential construction output.

Ireland & Property – beginning a new cycle

Property cycles have been an important feature of Irish economic history. The reasons for their

frequency in Ireland may partly be explained by both government intervention (property tax

reliefs for example) and, in some cases, a lack thereof. In the most recent instance,

inappropriately low interest rates stoked an unprecedented boom that government policy did

little to counteract until it was too late, thus sowing the seeds for a bust of equally

unprecedented magnitude.

While Ireland is still dealing with the after-effects of this crash, it is important to recognise the

inherent cyclical nature of property. Historical analysis of price and output changes, coupled

with evidence of an improvement in the wider economy, suggests that a new cycle may be

taking hold. On the former, commercial property prices are now 25% below 1983 levels in real

terms. Growth in house prices is now in line with the growth in incomes over the last thirty

years, while housebuilding is back at levels last seen in the early 1960s. A gradual economic

recovery should be enough to maintain a new property cycle in the coming years.

An urban-led recovery

Ireland is in the midst of a gradual recovery from a very painful recession. The severity of the

recession was a function of the very unbalanced position of the Irish economy prior to the

international financial crisis. At that time, investment accounted for 31% of GNP, relative to a

long-term average of 23%. Within this, construction investment was the key outlier,

representing 25% of GNP, relative to a long-term average of 14%. A rebalancing was overdue.

This rebalancing has now fully played out. Investment currently accounts for just 13% of GNP,

the lowest since at least 1970. Construction investment stands at just 7% of GNP, half its long-

term average. Recent evidence suggests that both business investment and construction are

growing again and are forecast, in 2014, to contribute to the first year of growth in domestic

demand since 2007.

By historical standards, the recovery in the Irish economy is expected to be a muted one, due

to the ongoing deleveraging in the household sector. Recovery is also not anticipated to be

evenly balanced across the Irish economy for two reasons. Firstly, the collapse in construction

will have longer lasting effects in some parts of the country due to the oversupply of properties

and the lingering impact of unemployment. Secondly, urban areas have been taking a

disproportionate share of the foreign direct investment coming into Ireland, thus contributing to

a recovery in labour markets and overall economic output in these areas. Prospects for recovery

in property markets must be seen in this context

Commercial property – a classic cyclical industry

Commercial property is highly correlated with the economic cycle. Over the past thirty years,

commercial property values have tended to lead cycles in domestic demand, while commercial

construction has tended to lag. Although the most recent cycle was the fourth in the last thirty

years, it was the most severe by far. Commercial property values fell by a total of 67% from

the peak, returning values to 1998 levels in nominal terms.

Goodbody Economy - Ireland

27 Sep. 2013 Page 3

From an investment point of view, there are three ingredients in determining the likely medium

term performance of commercial property: (1) Income; (2) Flows and; (3) Timing. The average

equivalent yield on commercial property in Ireland currently stands at 8.8%. Relative to Irish

government bonds, commercial property yields are at the highest level in at least thirty years.

While some of this reflects expectations of falling rents once leases come to an end (market

rents have fallen by 50% over recent years), even allowing for this, a reversionary yield of

6.8% remains attractive. Investors obviously perceive value, based on investment in Irish

commercial property of over €1bn this year. Historical precedence suggests that the market has

reached a turning point in terms of values and rents.

Given the scale and nature of foreign direct investment coming into the country and the

expected ongoing reduction in vacancy rates, the office sector offers the best prospects for

growth over the coming years. The Dublin office market is no stranger to boom and bust cycles,

with one typically occurring every decade. No new office building is expected until at least

2016, while the last completion occurred in early 2011. While headline vacancy rates are high,

there is a limited amount of large office accommodation available in the capital. The latest data

show that rents and capital values have started to increase and we expect a further reduction in

vacancy rates will lead to a continuation of this trend.

Retail remains the weakest sector of the commercial property market, with rents and capital

values continuing to fall sharply in 2013. While yields are at attractive levels, the industry faces

continuing difficulties with low levels of consumer spending, “strategic examinerships” and a

continued shift to online and out of city centre locations. Industrial rents have grown for two

consecutive quarters and there is a notable pick-up in transactions. There are reasons to be

cautiously optimistic on the sector.

Residential property – A regional story

One must be careful in assessing the prospects for the “Irish housing market”. More than any

other market, the prospects differ depending on the geographic location and the type of

property in question. National statistics suggest that prices rose on an annual basis in June

2013 for the first time in five and a half years. However, this is being driven by Dublin, where

prices are rising at an annual pace of 11%, whereas prices continue to fall outside the capital.

Based on our analysis of supply and demand, we believe this multi-speed market will continue.

After a 50% fall, residential property prices are below long-term averages (based on various

valuation metrics), but not dramatically so. Relative to disposable income per capita, house

prices are estimated to be 10% below the long-term average, while rental yields are modestly

above the long-term spread to government bond yields. Historical analysis suggests that

Ireland’s crash is the largest in any developed economy since 1970. That same historical

evidence also suggests that real price growth averages 6% per annum in the five years

following the trough. A similar occurrence in Ireland would mean that 40% of the drop in prices

would be recovered within five years, leaving prices still down 30% from the peak.

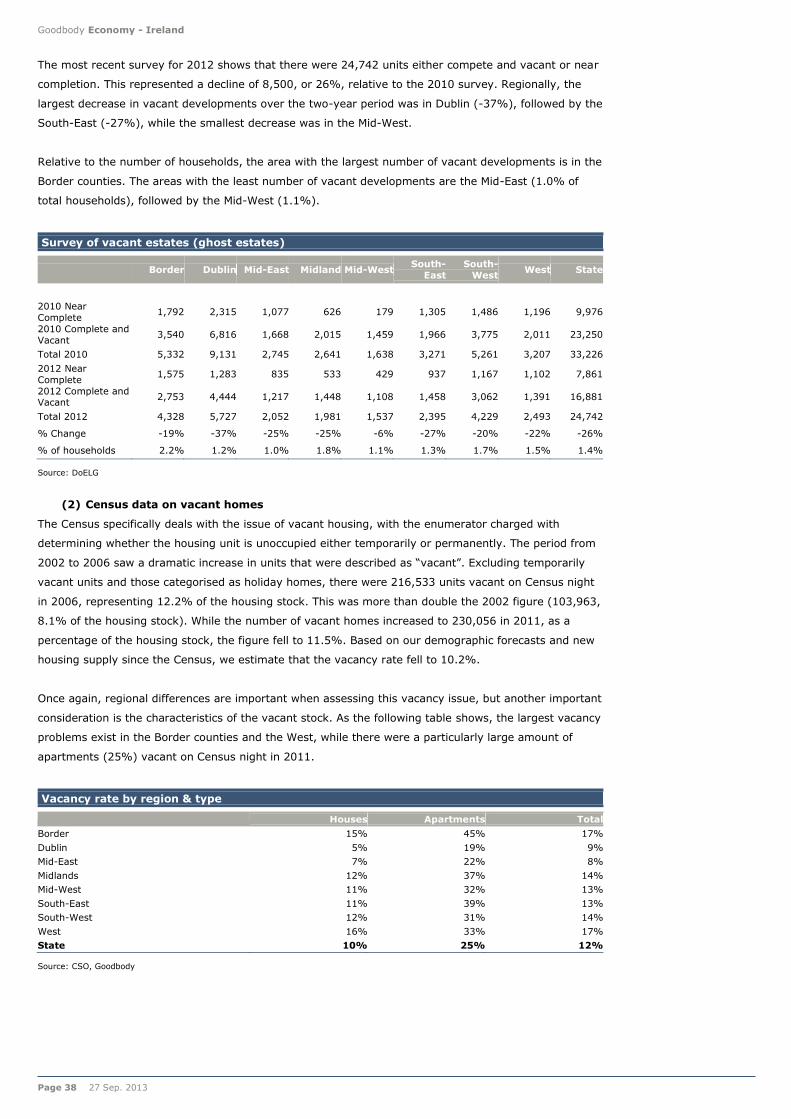

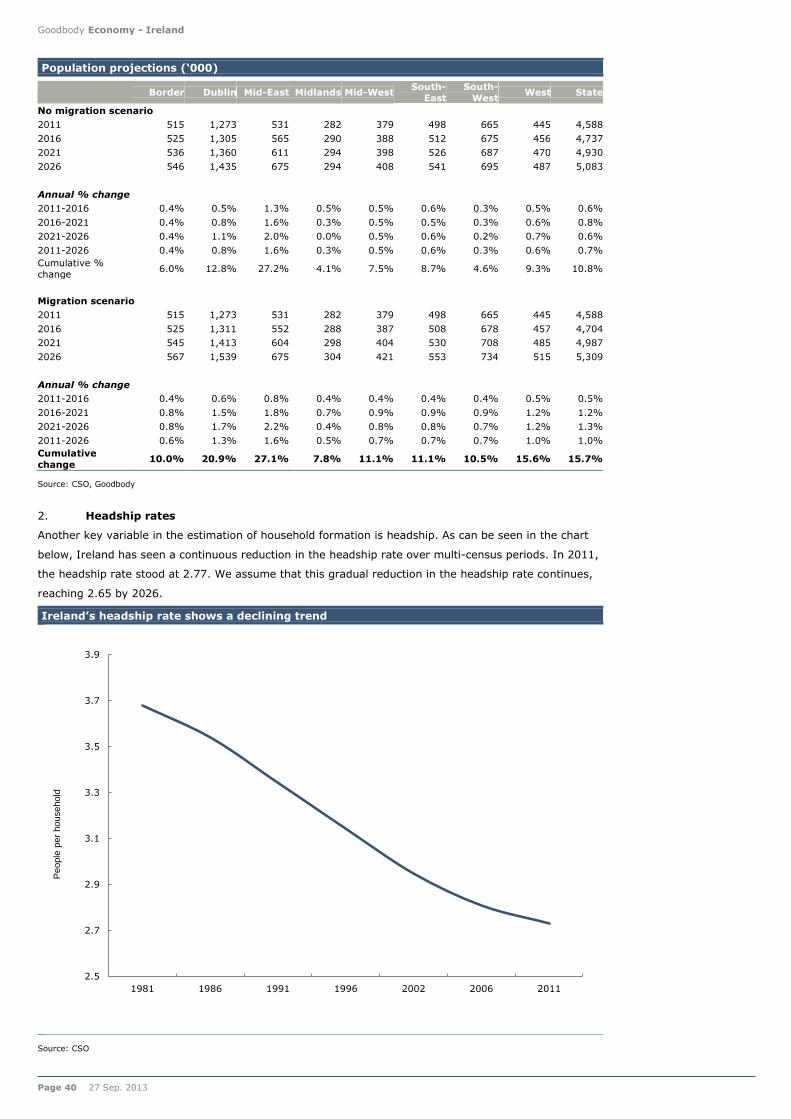

Census 2011 revealed that 12% of homes were vacant, with significant variations by location

and type (25% for apartments & 10% for houses). Based on assumptions for household

formation, we have estimated the time required to work off excess stock and thus recommence

building. The Greater Dublin area requires building to start immediately, while in parts of the

country (Border counties), no net new building will be required until the end of the decade.

Combining household formation and the likely evolution of the vacant stock, the period from

2011-2016 requires new build in the range of 9,000-10,000, in line with current output levels.

However, we estimate that all of this supply should be within in the Greater Dublin area. As

supply is worked through and the number of households continues to rise, we estimate that

housing demand will rise to 21,000-26,000 units in the period from 2016 to 2021, before rising

further to 26,000-36,000 in 2021-2026. This underpins our forecast for 25,000 completions by

2021 and 33,000 by 2026.

Goodbody Economy - Ireland

Page 4 27 Sep. 2013

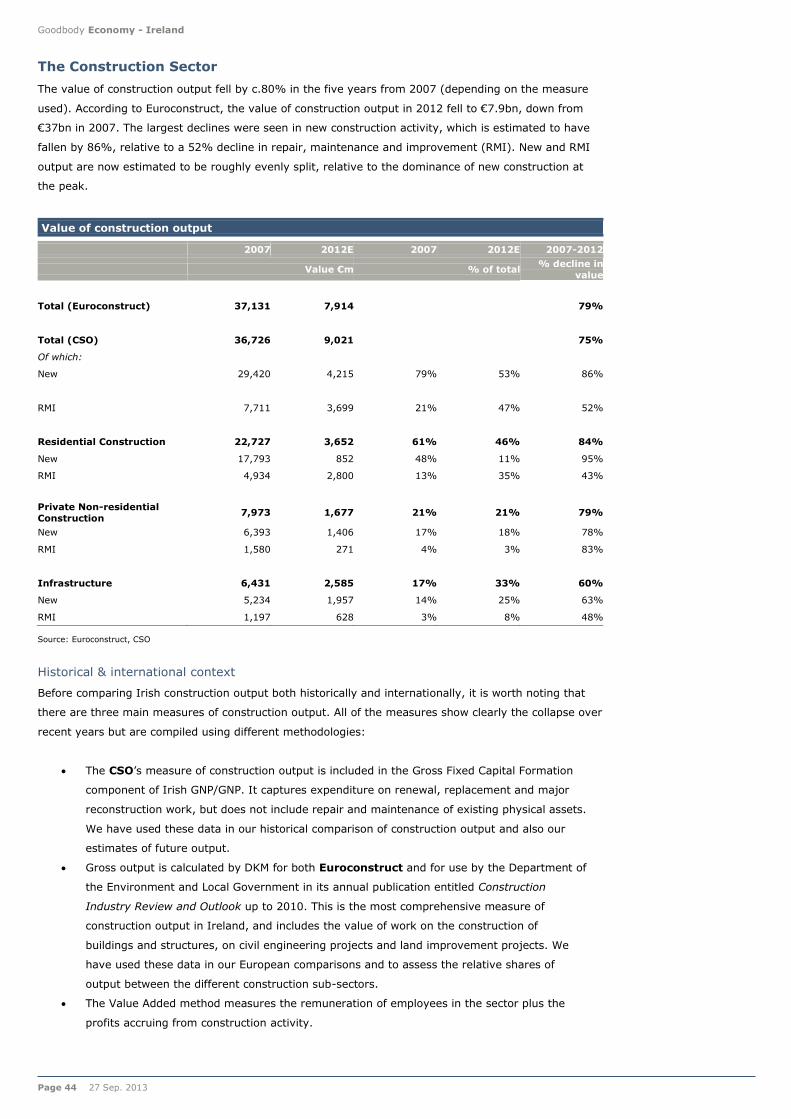

Strong growth potential in construction sector from here

The value of construction output has fallen by 80% since 2007. As a result, construction output

now amounts to just 7% of GNP, half its long-term average. While a period of undershoot was

required following the boom of the 2000s, there is scope for significant growth from this level

over the medium term. As a comparison, construction accounts for 10% of GDP on average

across Europe, while the long term average stands at 11%-12%.

All components of construction output have fallen sharply over recent years, but the collapse in

residential construction output has had the biggest effect on total output, falling from 14% of

GNP to just 4%. Non-residential activity is estimated at 1% of GNP, relative to a European

average of 3%, while civil engineering represents just 1.7% of GNP (2.5% in Europe).

We posit three scenarios for construction output over the period to 2020. In the base case,

construction output rises to 11% of GDP, translating into 10% annual growth in output. Under a

more conservative scenario, which may come about due to continuing capital constraints in the

sector for example, output grows to just 9% of GNP by 2020. Even under this scenario, output

would grow at an annual pace of 7%. A more optimistic scenario that sees construction back to

13% of GNP, would see 13% per annum compound growth over the period

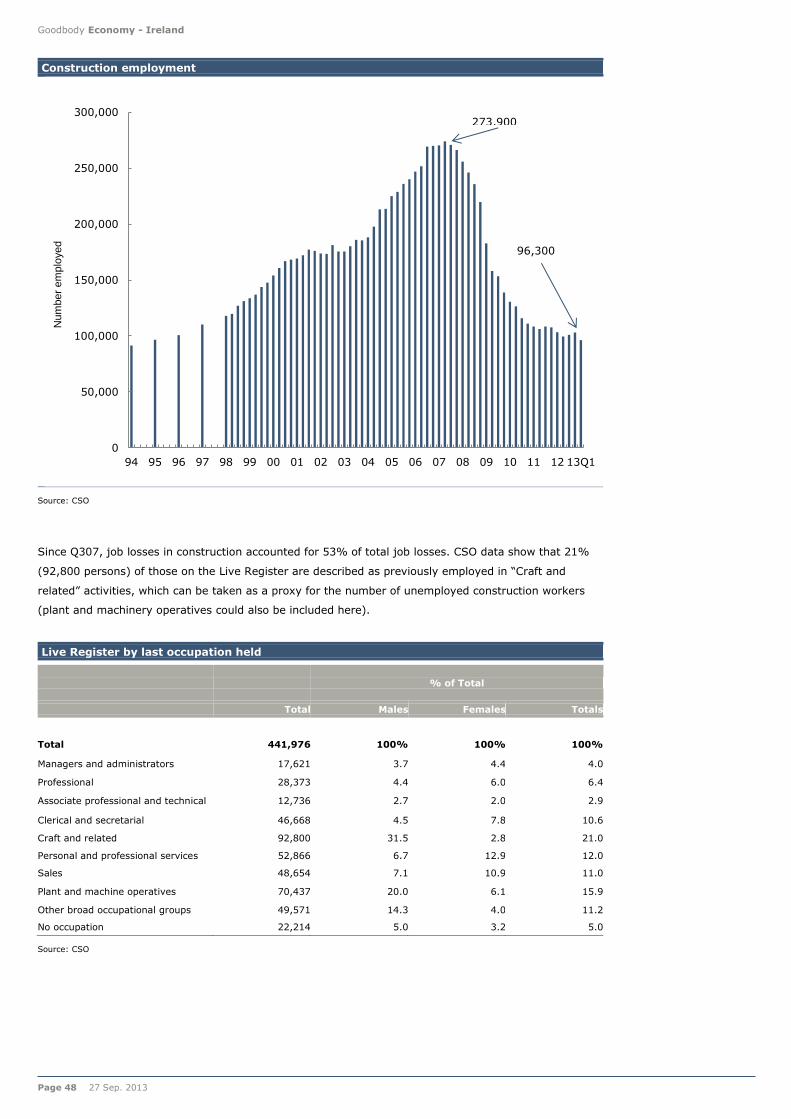

Returning the construction sector to “normal” levels could have a profound impact on

employment in the sector. A normal level of output could lead to construction employment

growing to 157,000, relative to the current level of c.100,000.

How to play Irish property

There are a number of ways for investors to play the recovery in Irish property, ranging from

low income/low risk approaches like covered bonds to direct property or direct equity exposure.

Equity: REITs, introduced to Ireland for the first time earlier this year, are the purest play on

recovery in the Irish property market. At the current time, there is only one REIT on the market

(Green). The banks also offer a leveraged play on recovery in the sector. Improving property

trends provide more comfort on credit loss forecasts, strengthening our positive Bank of Ireland

investment case. We have upgraded our PT from 23c to 26c. Among the construction stocks,

Grafton has the largest exposure to an Irish recovery, which represents 20% of group sales.

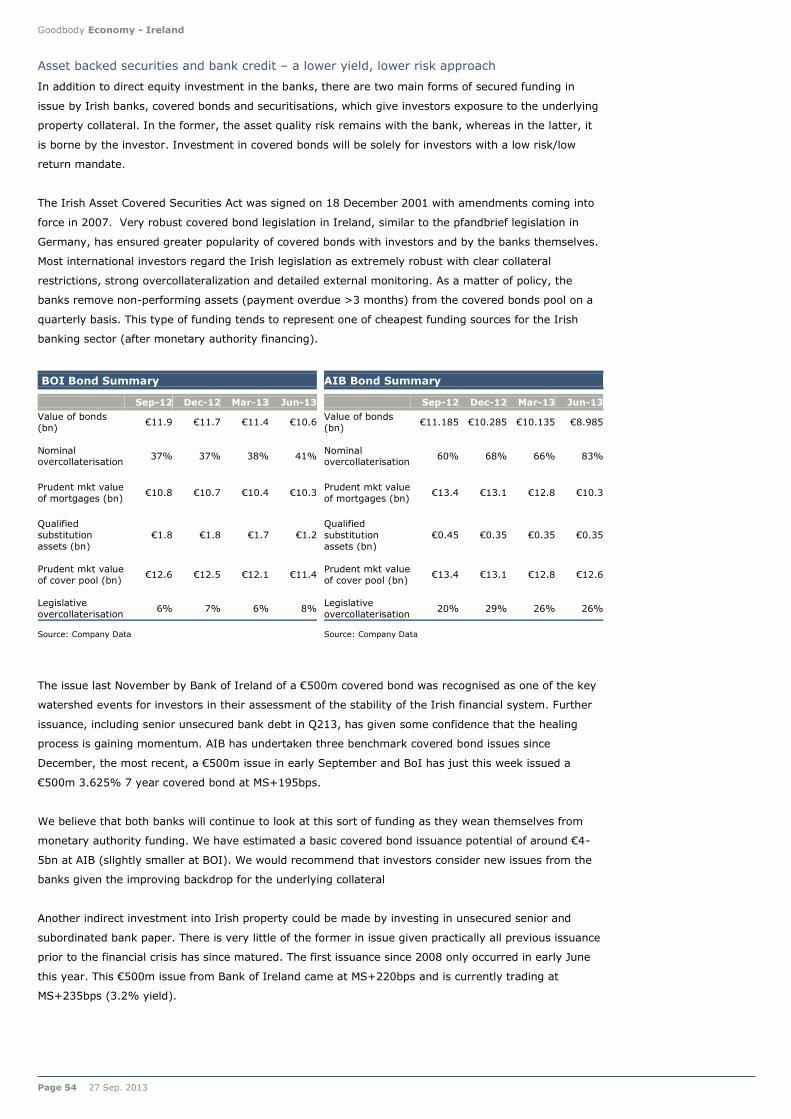

Credit: We would recommend that investors consider new ACS issues from the banks given the

improving backdrop for the underlying collateral. We particularly like Bank of Ireland’s 2016

contingent convertible securities which are yielding 7.5%. Basel III transition rules Core Equity

Tier 1 ratios provide almost €3.5-4.0bn of capital protection to the 8.25% trigger on the cocos.

Direct Property & Loans: In this instance, most focus will be on the commercial side given

the larger bite-size, especially Dublin Offices where we see returns of circa 10% p.a. Disposals

from deleveraging banks will also provide opportunities.

Sovereign: The collapse in the property market has played a significant role in the

deterioration in the public finances over recent years, whether in relation to collapse in tax

revenues coming from the sector or the recapitalisation of the banking system. A recovery in

the sector should reduce contingent liabilities in the banking system and also in NAMA. It should

also help to improve the government fiscal position.

Goodbody Economy - Ireland

27 Sep. 2013 Page 5

Contents

Key Themes 2

Introduction - Ireland & property – A volatile relationship 7

Macroeconomic backdrop 9

Commercial property 16

The office market 19

When will building start again? 25

Retail Market 27

The Industrial Market - Showing signs of stabilisation 29

Irish residential property market 31

Estimating medium-term housing demand 39

The Construction Sector 44

Where next for the construction sector? 49

How to play Irish Property 51

Appendix – Glossary of Property Terms 56

Goodbody Economy - Ireland

Page 6 27 Sep. 2013

Goodbody Economy - Ireland

27 Sep. 2013 Page 7

Introduction - Ireland & property – A volatile relationship

Ireland has a long and colourful history with property. The country boasts one of the highest home

ownership rates in the world, partly reflecting cultural legacies but also due to government policy that

encourages ownership of property over rental. Government policy also incentivised construction of a

whole array of residential and non-residential building in the period from the mid-1980s to 2006

(property tax incentives). Public infrastructure spending has also been through a number of cycles,

ranging from the boom of the early 2000s to the recent dearth in activity.

Property cycles have been an important and frequent feature of Irish economic history. The reasons for

their scale and frequency may partly be explained by both government intervention and the lack thereof.

For instance, the most recent boom and bust episode in the Irish property market was partly fuelled by

inappropriate interest rates, but also government policy which did little to counteract this buoyancy. This

led to a boom in property construction, values, property-related taxation and speculation of epic

proportions. The subsequent collapse has been equally spectacular.

The following chart illustrates longer-term developments for five main variables in the Irish property

market – economic growth (GDP & GNP), house-building, commercial property prices and house prices.

We have rebased all variables to 1983. The scale of recent decline is stark when put in this context.

House building is at the lowest level during this time period, despite continued growth in the population

over recent years. Commercial prices, in real terms, are now more that 25% below 1983 levels, while

real residential property prices have fallen to 1998 levels. All variables have fallen below the growth in

real GDP over the period, while house price growth is now exactly in line with real GNP growth (a more

appropriate variable for income growth for Ireland).

Ireland’s property crash in a historical context

Source: CSO, DoELG, IPD, Goodbody

0

50

100

150

200

250

300

350

400

450

Index (

1983=

100)

GDP Housebuilding Comm property prices (real) Resi prices (real) GNP

Residential prices have halved

Real commercial property prices are 25% below 1983 levels

Housebuilding at record lows

Goodbody Economy - Ireland

Page 8 27 Sep. 2013

The nature of property markets is that they are inherently prone to cycles. These cycles differ in scale

and duration, but typically follow a consistent pattern. At first, low interest rates and economic growth

fuel an increase in demand for property. This pushes prices upwards, increasing the incentive to build.

Expectations of a continued rise in prices fuel an increase in speculation. At this stage, policymakers,

particularly central bankers, step in to slow the economy. This reduces the profit on speculation and

building, which leads to a slowdown in investment. Demand for property also falls and consequently

prices begin to decline. Eventually, they reach a level that is attractive once again, economic growth

resumes and a new cycle begins.

Calling turning points in property cycles is difficult, but it is clear from our historical analysis that

property prices and activity have fallen well below the decline in economic activity generally, as

measured by GDP. Relative to GNP, commercial prices, non-residential building and residential

construction remain substantially below levels justified by the developments in the broader economy.

Although the Irish economy is still dealing with the after-effects of the property collapse, particularly in

relation to unemployment and household debt, there are strong indications that the economic cycle has

turned. The recovery will be uneven, a backdrop likely to be mirrored in the property sector. While not

uniform across the country, our analysis suggests that a new property cycle has begun.

Goodbody Economy - Ireland

27 Sep. 2013 Page 9

Macroeconomic backdrop

A recovery is in train but it is uneven

Ireland is in the midst of a shallow recovery from a very painful recession. While supply-side drivers

(population, productivity, competitiveness) remain supportive of growth, the economy continues to be

held back by a combination of deleveraging, fiscal consolidation and low levels of new bank lending.

Nevertheless, significant progress has been made since the arrival of the Troika in November 2010 to

return public finances to health, rehabilitate the banking system and improve the competitive position of

the Irish economy. While this period of restructuring and reform has been painful, the country is set to

reap the benefits over the coming years.

Post strong export-led growth in the 1995-2001 period, Irish economic growth was driven by domestic

factors from 2003 to 2007. A rapid expansion in credit was a key ingredient, which fuelled growth in

household debt, construction activity and speculation. The resultant boom meant that the Irish economy

become very unbalanced in the period immediately prior to the international financial crisis. This is

illustrated in the chart below, which shows that investment accounted for 31% of GNP at the peak,

relative to a long-term average of 23% of GNP. Construction investment was key in this; construction

output grew to a peak of 25% of GNP (long-term average is 14% of GNP). The rebalancing witnessed

since the peak was necessary, and extremely painful. However, recent trends suggest that this

rebalancing has now been completed and both construction and non-construction investment is on the

increase again and will contribute to growth overall. History suggests that investment recoveries can be

quite vigorous in the aftermath of a collapse.

Rebalancing Act – Investment & Construction to GNP

Source: CSO, Goodbody

Private sector deleveraging remains both the biggest constraint on domestic spending and the key risk

to bank balance sheets. However, while this is likely to restrain growth, deleveraging does not preclude

a modest growth outturn.

0%

5%

10%

15%

20%

25%

30%

35%

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012

% o

f G

NP

Investment/GNP Construction/GNP Average Average

Goodbody Economy - Ireland

Page 10 27 Sep. 2013

Excessive growth in prices relative to euro area peers during this period led to a deterioration in

competitiveness that the country has been trying to regain over recent years. In this regard, Ireland has

seen the most rapid reduction in unit labour costs since the beginning of the crisis in the euro area.

Allied to permanent attractions like an English-speaking, well-educated workforce, a business-friendly

climate and an attractive corporation tax rate, Ireland has been able to return to export-led growth.

Although exports have slowed in 2013 on the back of industry-specific issues in the pharmaceutical

sector (the “patent cliff”), we expect that net exports will continue to be a key contributor to growth in

the coming years, albeit with a small contribution from domestic demand, starting in 2014.

Economic recovery now in train

Source: Goodbody

Irish economic growth forecasts

2010 2011 2012 2013f 2014f 2015f

Consumption 0.9% -1.6% -0.3% -0.7% 0.8% 1.1%

Government -6.9% -2.8% -3.7% -1.9% -1.5% -1.3%

Investment -22.6% -9.5% -1.0% -3.9% 6.4% 7.7%

Domestic Demand -5.0% -3.0% -1.1% -1.4% 1.1% 1.5%

Exports 6.4% 5.4% 1.6% 0.6% 3.7% 3.9%

Imports 3.6% -0.4% 0.0% 0.5% 2.4% 3.0%

GDP -1.1% 2.2% 0.2% 0.5% 2.4% 2.6%

GNP 0.5% -1.6% 1.8% 2.9% 1.9% 1.9%

Source: CSO, Goodbody estimates

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

2005 2006 2007 2008 2009 2010 2011 2012 2013f 2014f 2015f

% Y

oY

GDP Domestic demand

Goodbody Economy - Ireland

27 Sep. 2013 Page 11

Recent evidence suggests that recovery is being driven by the urban centres, particularly Dublin. There

are two main reasons for this trend:

The collapse in construction has had a disproportionate impact in rural locations. In Q4 2006,

one in seven workers (15%) was employed in the construction sector outside the Greater

Dublin area, relative to 10% in Greater Dublin.

Dublin has been able to attract a disproportionate amount of the FDI coming into Ireland,

mainly due to the growth in the Information and Communications Technology (ICT) sector in

the capital.

The second point here is key, as economic policy in Ireland is geared towards putting in place the

conditions to engineer an export-led recovery. The IDA is the body responsible for attracting FDI into

Ireland and has been instrumental in the substantial growth in multinationals based in the country. As

the Irish economy has developed over the last three decades, the focus for the IDA has changed too.

The following chart shows how this focus has shifted from manufacturing in the 1970s and 1980s to the

internet activities of the early 2000s. The current focus for the IDA is now the so-called “Smart

Economy” industries including ICT, medical technologies and finance.

Evolution of FDI focus in Ireland

Source: IDA

It is no surprise that the regional employment patterns reflect the shifts seen above as well as the

general increase in wealth levels. Specifically, the Irish economy has become predominately a service

economy. As of the second quarter of 2013, 76% of those employed in Ireland worked in the services

sector, relative to 66% ten years earlier. In Greater Dublin, the services sector is even more important,

representing 85% of the total (75% ten years earlier). This compares to just 70% outside of the Greater

Dublin area.

Goodbody Economy - Ireland

Page 12 27 Sep. 2013

Services employment as a % of total

Source: CSO

This is by no means unique to Ireland. On the contrary, a trend towards services output as economies

develop is a recognised fact. It is also accepted that urban areas will continue to drive population

growth, as empirical studies have shown a positive correlation between the growth in the urban share of

the population and income growth.

The lure of the city

The question then is how important are the cities, particularly Dublin, in a national context and can they

be the driver of growth. Our analysis suggests that Dublin represents a large share of the population and

an even larger share of economic output. Our demographic forecasts suggest that the Greater Dublin

area is expected to see population growth of 19% between 2011 and 2026, compared to just 5% growth

outside the Greater Dublin area. This reflects some natural increase in the population, but predominately

the role of migration, both from within Ireland and abroad.

The table below shows the relative importance of Dublin to the national economy. The Greater Dublin

Area (GDA, which includes the commuting counties of Kildare, Meath and Wicklow) accounts for 39% of

the population in the State, 42% of total employment and 50% of economic activity (as measured by

gross value added). In addition, Dublin contributes 56% of total tax take, 62% of Corporation tax

receipts and 51% of total PAYE. Disposable income per head in Dublin is also 11% ahead of the national

average.

50%

55%

60%

65%

70%

75%

80%

85%

90%

Q1

98

Q3

98

Q1

99

Q3

99

Q1

00

Q3

00

Q1

01

Q3

01

Q1

02

Q3

02

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

Q1

12

Q3

12

Q1

13

% o

f T

ota

l

National Greater Dublin Ireland excl Greater Dublin

Goodbody Economy - Ireland

27 Sep. 2013 Page 13

Regional analysis of the Irish economy (% of Total)

Population GVA Employment Unemployed Labour force

Disp. Income

per head*

Dublin 28 42 30 24 29 111

Mid East 12 8 12 13 12 100

Greater Dublin 39 50 42 37 41 108

Mid-West 8 7 8 9 8 99

South East 11 7 10 14 11 94

South West 14 18 15 12 15 99

Southern & Eastern 73 82 75 72 74 103

Border 11 7 10 11 10 90

Midland 6 4 6 8 6 89

West 10 8 10 9 10 96

Border, Midland & West 27 18 25 28 26 92

Source: Goodbody, CSO

*% of state average

Dublin is also the most attractive location for foreign direct investment into the country. The following

table is taken from a study completed for the Dublin Regional Authority (Dublin’s Role in the Irish and

Global Economy 2012, Brendan Williams et al). It shows that while Dublin’s share of IDA-supported

businesses is high at 47%, the capital particularly dominates in certain sectors, namely in the areas of

financial services (86% of total) and entertainment and media (83% of total). In an answer to a recent

Dail question, the Minister for Jobs, Enterprise & Innovation Richard Bruton confirmed that the FDI bias

towards Dublin has continued in 2013. Of a total of 275 site visits conducted by potential investors to

the end of August 2013, 152 or 55% had been to Dublin. This was in line with the trends seen in 2012,

when 52% of the 379 site visits conducted were to Dublin. Other urban centres of Cork (10%), Limerick

(7%) and Galway (4%) account for a further 20% of visits in 2013 with Waterford seeing almost 5% of

visits.

IDA site locations by sector type

Total Dublin Cork Galway Limerick Waterford Other

Financial Services 219 86% 2% 1% 1% 1% 8%

ICT 159 48% 19% 10% 5% 1% 18%

Industrial products &

services 96 15% 16% 7% 4% 5% 53%

Pharma 82 29% 27% 0% 0% 6% 38%

Medical Technologies 76 11% 11% 17% 7% 3% 53%

Consumer goods 56 25% 11% 0% 4% 9% 52%

Business services 40 48% 25% 3% 5% 3% 17%

Chemicals 20 30% 25% 0% 15% 0% 30%

Entertainment & media 6 83% 17% 0% 0% 0% 0%

Total 754 47% 13% 5% 3% 3% 29%

Source: Dublin Regional Authority

We believe that Dublin will continue to benefit from what is described as clustering or agglomeration

effects. This is the process by which commercial activity tends to cluster together, thus enjoying

economies of scale and access to a pool of skilled labour and complementary services and infrastructure.

This process tends to be self-reinforcing (i.e. success breeds success). In Dublin, the process could be

described as the Google-effect; multinationals in the IT sector have been attracted to Dublin due to the

success of Google, among others. Dublin, being the only city in Ireland of global scale, is also able to

attract highly skilled migrants to work in these industries.

Goodbody Economy - Ireland

Page 14 27 Sep. 2013

A “smart” economy needs an educated workforce…

In December 2008, the Irish government of the time set out its strategy for the development of the Irish

economy over the medium-term. While it included measures to stabilise the economy and the public

finances, it also to build a “Smart Economy” with a “thriving enterprise sector, high quality employment,

secure energy supplies, an attractive environment, and first-class infrastructure”. The strategy focuses

on four forms of capital accumulation that will drive economic growth – (i) human capital; (ii) physical

capital; (iii) environmental capital, and; (iv) social capital. The development of human capital is key

within this, as it is recognised that innovation will be vital to growth. Education is pivotal in achieving

this goal. The OECD ranks Ireland’s younger workforce as one of the best educated; in 2011, 47% of 25-

34 year olds attained at least tertiary education, relative to the OECD average of 39%. As the following

chart shows, this put Ireland among the top-five countries in the world on this measure. More recent

events, such as the cuts to the education budget have not been helpful, but there is a recognition that if

Ireland is to attract high-value add investment, it will have to ensure that the labour pool is suitably

qualified. Increasingly, sector-specific skills gaps have had to be filled by immigrants in recent years.

Proportion of population aged 25-34 with a tertiary eduction

Source: OECD

…which further supports the case for growth led by the cities

The strategic plan for the Irish economy very much plays into the strength of the cities for a number of

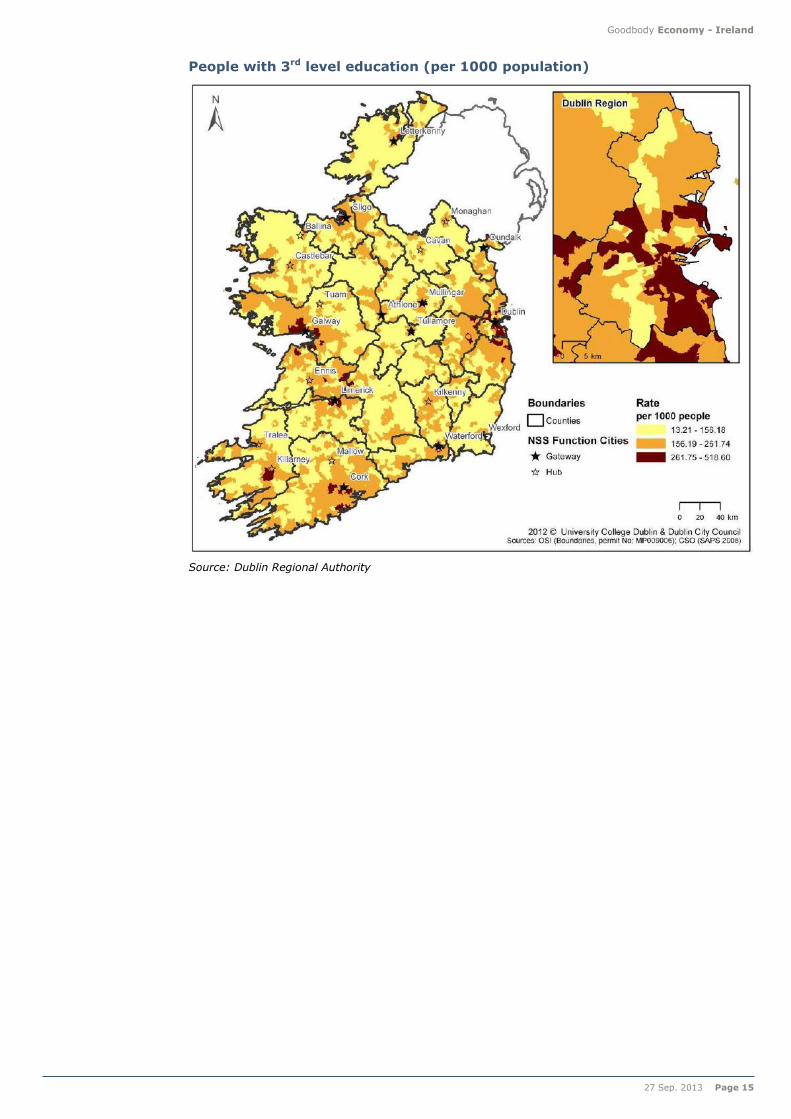

reasons. Firstly, as Census data show, educational attainment is particularly high in the cities,

particularly in Dublin (as the chart on the next page shows). Secondly, these locations are able to attract

a skilled workforce. Third, scale allows for the development of physical infrastructure in the cities.

Finally, city locations allow for the generation and sharing of ideas, thus driving innovation.

0

10

20

30

40

50

60

70

% o

f P

opula

tion (

25

-34)

Goodbody Economy - Ireland

27 Sep. 2013 Page 15

People with 3rd level education (per 1000 population)

Source: Dublin Regional Authority

Goodbody Economy - Ireland

Page 16 27 Sep. 2013

Commercial property

A play on the economic cycle

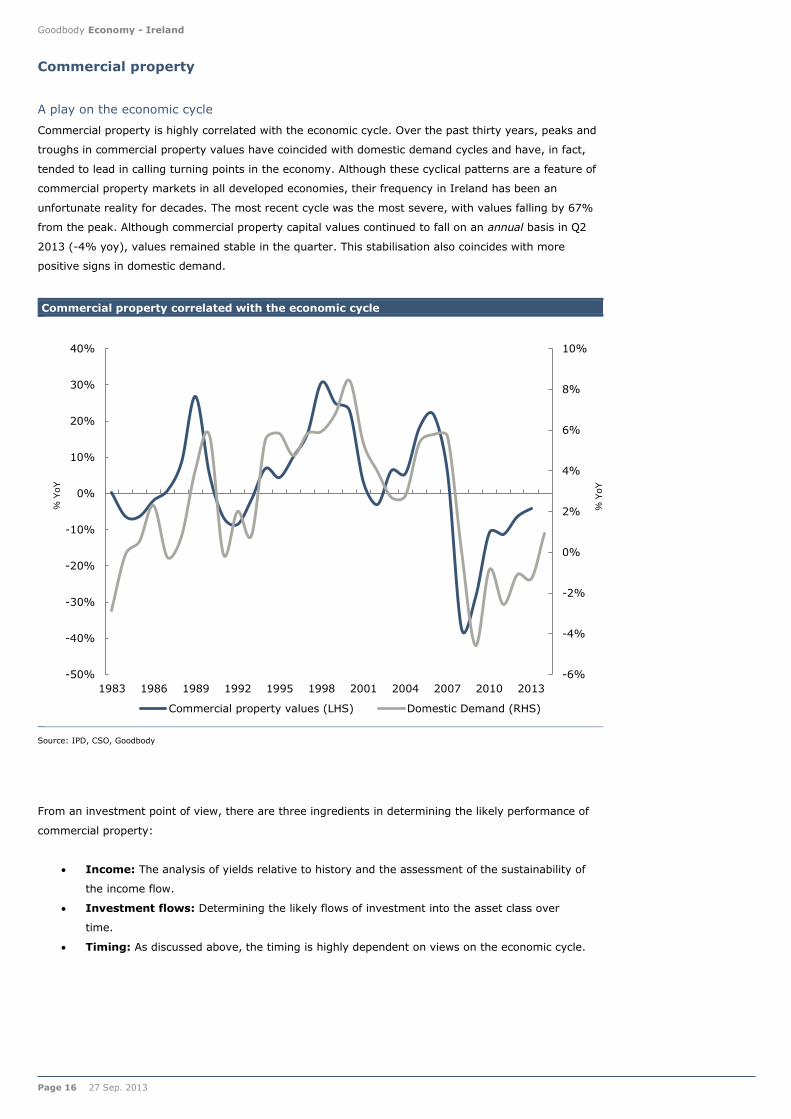

Commercial property is highly correlated with the economic cycle. Over the past thirty years, peaks and

troughs in commercial property values have coincided with domestic demand cycles and have, in fact,

tended to lead in calling turning points in the economy. Although these cyclical patterns are a feature of

commercial property markets in all developed economies, their frequency in Ireland has been an

unfortunate reality for decades. The most recent cycle was the most severe, with values falling by 67%

from the peak. Although commercial property capital values continued to fall on an annual basis in Q2

2013 (-4% yoy), values remained stable in the quarter. This stabilisation also coincides with more

positive signs in domestic demand.

Commercial property correlated with the economic cycle

Source: IPD, CSO, Goodbody

From an investment point of view, there are three ingredients in determining the likely performance of

commercial property:

Income: The analysis of yields relative to history and the assessment of the sustainability of

the income flow.

Investment flows: Determining the likely flows of investment into the asset class over

time.

Timing: As discussed above, the timing is highly dependent on views on the economic cycle.

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

1983 1986 1989 1992 1995 1998 2001 2004 2007 2010 2013

% Y

oY

% Y

oY

Commercial property values (LHS) Domestic Demand (RHS)

Goodbody Economy - Ireland

27 Sep. 2013 Page 17

Income – Yields are at attractive levels

Total returns (see Glossary in Appendix for definitions of these commercial property terms) on Irish

property for the year to June 2013 were 5.3% with attractive income returns of approx. 9.9% off-setting

declines in capital values.

The recent stabilisation in capital values is being led by yield movements, which reflect the current

strong demand for property assets. Property Equivalent Yields have reached a turning point and have

now decreased by 20bp from a peak of 9.0% at end Q1 2013, having increased by 500bp from 4% at

the end of the property boom. At 8.8%, property equivalent yields compare favourably with yields on

other asset classes, with Irish 10 year bond yields now down to 4%. Even allowing for a risk premium of

4% over bond yields, current market pricing means hurdle rates for property investment will be

exceeded.

Commercial yields at a record high relative to bond yields

Source: IPD, FactSet, Goodbody

An initial yield (Rental Income/Gross Capital Value) of c.9.2% is clearly attractive, and is the primary

reason for the strong interest in the market. Investors, however, are not only concerned about the initial

level of income but also the sustainability of this income. With rents down by 50% since 2008, current

rental levels will not be sustained when leases come up for renewal. The Reversionary Yield (Rental

Value/Gross Capital Value) captures this phenomenon, but, at 6.8%, even this yield suggests that

commercial property represents a good investment.

The decline in rental values is likely to continue to impact on property market returns over the next few

years as existing leases approach expiry or break options. To gauge underlying yield movements since

the market peak, the chart below shows CBRE calculations of the yield on prime properties on the basis

of current market values and current market rents. There has been a substantial increase in income

yields, but the majority of markets are now seeing a hardening of yields.

-6

-4

-2

0

2

4

6

8

10

12

14

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

%

Commercial yield 10-year bond yield Spread Average spread

Goodbody Economy - Ireland

Page 18 27 Sep. 2013

CBRE Ireland Equivalent Yield Series (%)

Peak Jul-13 Trending

Retail

Shops

Prime High Street 2.50 5.75 Stronger

Good Secondary High Street 3.50 7.00 Stronger

Prime Provincial 3.25 8.00 Stronger

Shopping Centres

Prime High Street 3.50 7.50 Stronger

Secondary 4.25 9.50 Stronger

Offices

Prime City Centre Dublin 4.25 6.25 Stronger

Secondary City Centre Dublin 4.25 7.50 Stronger

Suburban Dublin 5.00 8.50 Stronger

Primes Provincial 5.75 9.50 Stronger

Industrial

Prime Dublin 4.75 8.75 Stronger

Secondary Dublin 4.75 10.75 Stronger

Prime Provincial 5.75 12.00 Stable

Source: CBRE

Investment flows picking up strongly

Following an almost complete cessation in 2011, commercial property investment has picked up strongly

since the second half of 2012. Total investment in commercial property (not including loan sales) was

estimated by Savills to be €575m in 2011. The total for the first half of 2013 (€610m) already exceeds

this level and is expected to well over €1bn by the end of this year. Highlighting the preference for

offices, over 60% of the total investment since 2011 has been into this sector.

Investment in commercial property

Source: Savills

0

100

200

300

400

500

600

700

2009 2010 2011 2012 2013 (H1)

Euro

(m

)

Domestic Non-Domestic Unknown

Goodbody Economy - Ireland

27 Sep. 2013 Page 19

Occupier analysis

Unlike the much improved official dataset of the Irish residential market, the Irish non-residential

property market suffers from a lack of detailed data. This makes analysis of the sector more difficult, but

the in-house analysis and data within the various commercial property companies, along with yield and

rental data from IPD enables us to paint a relatively detailed picture of the commercial property market

in Ireland. Our analysis is divided in to the three main components of the commercial market:

Office

Retail

Industrial

The office market

A brief description

Ireland’s office market is dominated by the Dublin region, with the capital accounting for between 75%-

80% of the total office stock in the country (source: DTZ Sherry Fitzgerald & DKM). Given this, we focus

on the underlying supply and demand fundamentals, as well as trends and prospects for the capital in

our assessment of the office sector.

Location of Dublin office space

Source: Lisney

According to Lisney, the Dublin office market currently consists of 3.6m square metres of space.

Reflecting the boom in office construction since the upturn in the Irish economy from the mid-1990s

onwards, the majority (73%) of this space was built since 1990 and over half (53%) built since 2000.

From a geographical perspective, 63% of the space is located in the city centre, with the South Suburbs

at 18%, the North Suburbs at 18% and the West Suburbs at 8%.

Historical review of the Dublin office construction market reveals a series of volatile cycles that follow

economic cycles with a lag of 12-24 months. Since the 1960s, peaks are observed approximately every

ten years (1964, 1972/1973, 1982, 1991, 2001 and 2008). This is not uncommon in office markets

internationally, with studies showing that typical office market cycles last between 10-12 years.

City Region

63%

South Suburbs

18%

North Suburbs

11%

West Suburbs

8%

Goodbody Economy - Ireland

Page 20 27 Sep. 2013

Booms & busts in Dublin office construction

Source: Lisney

Rents

Office rents experienced similarly volatile cycles, with annual growth of 20% achieved in the ten years

since 1970. These peaks were closely aligned with economic cycle. Since 1970, office rents have

endured four periods of declines, with the most severe by far being the most recent cycle, where rents

declined by 50%. In previous cycles, rents declined for three to four years before growing modestly at

first and then accelerating quite dramatically thereafter. This is a reflection of the lagged nature of new

commercial building construction, whereby new activity is triggered by actual increased demand and

rental levels, but reflecting the time involved in planning, developing, finishing and letting, supply does

not immediately follow.

-50.0

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

Thousands (

sqm

)

1st boom (1971-1975)

2nd boom (1980-1982)

3rd boom (1990-1991)

4th boom (1996-2001)

5th boom (2006-2008)

Goodbody Economy - Ireland

27 Sep. 2013 Page 21

Real office rents* (1970-2012)

Source: Lisney, CSO *deflated by CPI

Current rental levels

After peaking at €670 per square metre in 2007, prime office rents fell to a trough of €320 per square

metre by early 2012. Recently, rents have trended above this level but remain more than 50% below

the 2007 peak. Indeed, prime office rents remain at levels last seen in 1998.

Rental growth from this point will be driven by supply and demand. In relation to the latter, one of the

determinants of office space demand will be cost. At the peak of the boom, Ireland was one of the most

expensive locations in Europe for office space. This is no longer the case.

In 2008, Ireland was listed as the 14th most expensive office location in the world according to CBRE. In

the latest CBRE report, Ireland has fallen out of the top 50. Among European locations, Ireland is mid-

table, ranking 21st out of the fifty cities analysed. This puts Ireland on a par with Leeds in the UK and

Munich in Germany. In 2008, office costs in Ireland were on a par with Hong Kong, Abu Dhabi, Paris and

Midtown Manhattan. In other words, Ireland is now a much more attractive location from a cost

perspective relative to five years ago.

0

50

100

150

200

250

300

Dec

70

Dec

72

Dec

74

Dec

76

Dec

78

Dec

80

Dec

82

Dec

84

Dec

86

Dec

88

Dec

90

Dec

92

Dec

94

Dec

96

Dec

98

Dec

00

Dec

02

Dec

04

Dec

06

Dec

08

Dec

10

Dec

12

Index (

1970=

100)

Goodbody Economy - Ireland

Page 22 27 Sep. 2013

Total office occupancy costs* (€ per sqm) – Europe Q1 2013

Rank City Cost Rank City Cost Rank City Cost

1 London Central 1,869 18 Jersey 485 35 Hamburg 350

2 London City 1,117 19 Leeds 479 36 Copenhagen 340

3 Paris 1,002 20 Munich 465 37 Budapest 323

4 Geneva 875 21 Dublin 445 38 Berlin 312

5 Zurich 732 22 Warsaw 440 39 Bratislava 306

6 Istanbul 718 23 Brussels 436 40 Lisbon 297

7 Stockholm 644 24 Helsinki 426 41 Barcelona 293

8 Milan 599 25 Madrid 424 42 Lille 280

9 Manchester 581 26 Amsterdam 413 43 Bucharest 279

10 Aberdeen 571 27 Liverpool 408 44 Belfast 274

11 Edinburgh 568 28 Lyon 400 45 Rotterdam 273

12 Oslo 563 29 Prague 399 46 Sofia 218

13 Birmingham 558 30 Southampton 373 47 Valencia 211

14 Frankfurt 555 31 Athens 368 48 Malaga 205

15 Bristol 530 32 Gothenburg 365 49 Oporto 187

16 Glasgow 523 33 Marseille 360 50 Thessaloniki 185

17 Rome 495 34 Vienna 360 51 Mallorca 180

Source: CBRE *includes all charges (rents, service charges etc.)

Vacant stock – Still high not as alarming as headline statistics would suggest

A major concern of observers of the office market is the very high vacancy rate. Vacancy rates can vary

depending on definitions employed by the commercial agents. Using data from Lisney, the vacancy rate

stood at 18.9% at the end of Q2 2013. From a historical and international perspective this is a very high

level of vacancy. Most assume that a “normal” level of vacancy is of the order of 7%, so the logical

conclusion is that the Dublin market is grossly oversupplied and that rents are likely to be under

pressure for some time to come as vacancy levels converge towards that 7% level.

Such a conclusion is too simplistic. Academic studies have shown that the “natural” vacancy rate in

Ireland may be substantially higher than the 7% level suggested. A paper by John McCartney (Predicting

Turning Points in the Rent Cycle Using the Natural Vacancy Rate – An Applied Study of the Dublin Office

Market) calculates, using econometric techniques, that the natural vacancy rate for the Dublin market

may currently be as high as 15%. The paper suggests that the natural vacancy rate experienced a

distinct step change from 1999 onwards, citing a number of possible reasons including the new low

interest rate environment at the start of the euro and a move to suburban office locations.

It is also important to note that the vacant stock in the Dublin market varies significantly by location

within the city and, importantly, by the quality of the stock. Among the regions, the west suburbs have a

vacancy rate of 33%, with the north suburbs at 18%, the south suburbs at 19% and the city region

below 17%.

Again, although rates vary due to definitional issues across the agencies, it is uniformly accepted that

the city centre has the lowest vacancy rate. CBRE states that the city centre vacancy rate stood at

16.4% in the city centre in Q2 2013 (which, on its definition comprises the Dublin postcodes 1 to 8,

including the IFSC), relative to 17.2% for Dublin overall. CBRE recently undertook a more granular

analysis of the vacancy levels in the city centre, with the results shown in the chart below.

Goodbody Economy - Ireland

27 Sep. 2013 Page 23

Vacancy in Dublin offices varies significantly

Source: Lisney

Vacancy rates by quality of office space

Source: CBRE

Lisney has analysed Dublin city centre in even more detail by drilling down into what is considered as

the Central Business District (CBD) comprising of Dublin postal codes 1, 2 and 4, which accounts for

over 80% of the available office space in the city. Analysis of this area is key, as recent trends suggest

that occupiers prefer to take up the quality locations in the CBD first. In this regard, there is 309,450

sqm of space available in the CBD, accounting for 46% of the total available space in the capital.

However, almost one-third (29%) of this space is described as Grade C or obsolete, relative to 16% that

is described as obsolete for Dublin as a whole.

Vacant office space in Dublin

Grade A Grade B Grade C Total

Dublin 1 39,050 40,800 2,900 82,750

Dublin 2 31,250 58,750 57,600 147,600

Dublin 4 34,000 16,500 28,600 79,100

Total city centre 104,300 116,050 89,100 309,450

Non-city centre 215,700 128,950 15,900 360,550

Total Dublin 320,000 245,000 105,000 670,000

% of Total

% of Total Dublin

Dublin 1 47% 49% 4% 12%

Dublin 2 21% 40% 39% 22%

Dublin 4 43% 21% 36% 12%

Total city centre 34% 38% 29% 46%

Non-city centre 60% 36% 4% 54%

Total Dublin 48% 37% 16% 100%

Source: Lisney

Grade A: New modern accommodation, Grade B: Modern, previously occupied and of an acceptable standard, Grade C: Obsolete

Take-up levels

Take-up in the Dublin market is usually calculated on a gross basis (i.e. does not include those offices

that have been vacated in the period). Average annual take-up over the 1994-2012 period amounted to

163,500 sqm. Excluding the boom years of 2005-2007, this average drops to 153,000 sqm (Lisney).

Take up in the first half of 2013 amounted to 61,000 sqm, slightly ahead of the same period of 2012.

For the whole of 2012, take-up amounted to 142,000 sqm, only slightly below the long-term average.

Take-up for 2013 is expected to amount to close to last year’s level.

As one might expect, take-up has been dominated by Grade A and Grade B space over the recent years.

In 2012, these two categories accounted for 97% of the total take-up. Dublin city centre has been the

favoured location for tenants, with 61% of total take-up in 2012 and 55% in 2011, albeit helped by a

small number of large transactions (for example, Google in 2011 and the Central Bank in 2012).

0%

5%

10%

15%

20%

25%

30%

35%

40%

City

Region

North

Suburbs

Dublin

overall

South

Suburbs

West

Suburbs

Va

ca

ncy r

ate

(e

nd

-20

12

)

Sourc

e:

Lisne

y

Dublin

1/3/7 Dublin 2/4 Dublin 6/8 IFSC City Centre

overall

0%

5%

10%

15%

20%

25%

30%

Va

ca

ncy r

ate

Total Grade A

Sourc

e:

CBRE

Goodbody Economy - Ireland

Page 24 27 Sep. 2013

Office take-up by location

Source: Lisney

Given the emergence of the IT hub in Dublin, it is no surprise that the IT sector has been the biggest

source of demand. This was particularly the case in 2011 with the 19,000 sqm lease by Google, with a

more broad-based demand seen in 2012 across the different business sectors. More recently, the IT and

financial sectors dominated take-up in Q2 2013, accounting for 39% and 26% respectively.

Dublin office take-up by sector (% of total)

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Professional

Services 10% 35% 27% 11% 11% 21% 17% 13% 6% 4%

Financial 28% 9% 26% 33% 45% 24% 17% 17% 18% 19%

State 18% 4% 5% 16% 10% 11% 8% 6% 6% 17%

IT 12% 19% 21% 11% 14% 20% 26% 32% 39% 26%

Pharmaceutical/

Health/life

sciences

6% 3% 4% 4% 9% 5% 5% 9% 5% 8%

Media

2% 0% 4%

Education

11% 3%

Other 26% 30% 18% 25% 10% 19% 27% 21% 16% 19%

Total ('000

sqm) 149 189 206 234 299 181 84 124 164 142

Source: Lisney

0

50

100

150

200

250

300

350

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

'000 s

qm

City Centre North Suburbs South Suburbs West Suburbs

Goodbody Economy - Ireland

27 Sep. 2013 Page 25

When will building start again?

No new office buildings have emerged in the capital since the first half of 2011. This marks the most

prolonged period of drought in the new office construction sector in history. With no plans in the public

domain as yet, it is likely that no new space will come on stream until at least 2016. This is because of

the time lag involved in commercial construction activity. As a comparison, in the ten years to 1999

annual office completions amounted to an average 43 buildings per year in Dublin at an average size of

4,000 sqm.

The key reason for the complete absence of new construction is that at current rents, it is not

economical to build. Based on the vacant stock analysis, one could conclude that there is little need for

new building until this stock is used up. However, there are a number of reasons to believe that new

developments could be needed sooner than one would think:

Time lag – Given the time lag involved in completing a commercial building, the market

dynamics are often very different at the end of the process relative to the start.

A higher “natural” vacancy rate – We have shown that while the current vacancy rate

may appear high at a headline level, it is in fact closer to the “natural rate” for Dublin than

one would assume.

Lack of large spaces – While there is a relatively large amount of office space available in

the city, there is only limited choice if tenants are looking for particularly large space. CBRE

recently noted that there are just 17 buildings across Dublin that could accommodate space

requirements over 7,000 sqm. In total, this space accounts for just a quarter of the total

vacant space available. The IDA has recently stated that the availability of large office space

in the CBD may indeed act as a constraint towards attracting inward foreign direct

investment.

Vacancy rates could fall quite quickly in the absence of new building activity

Although agents tend to focus on “take-up” when discussing occupancy in the office market, a more

relevant variable in assessing trends in the vacancy rate is net absorption. This measures the change in

occupied office space and thus takes into account movement by companies to alternative office

accommodation which leads to no net change in occupied space and the closure of businesses, thus

adding to the available office stock. .

Office take-up versus net absorption

Source: Lisney, Goodbody

Vacancy rate forecasts

Source: Lisney, Goodbody

We have assumed that take-up runs at the twenty-year average of 150,000 sqm over the four years to

2016. Under this assumption, net absorption amounts to 70,000 sqm on average. With no new office

space assumed over the period, the vacancy rate is forecast to fall to 10.5% by the end of 2016. If take-

up was to exceed the long-term average and rise to 200,000 sqm per annum, the vacancy rate would

fall much quicker to 4.9% at the end of 2016. If take-up was to slow significantly to just 100,000sqm

per annum, the vacancy rate would fall to just 16% by the end of the period.

-50

0

50

100

150

200

250

300

350

1992 1996 2000 2004 2008 2012 2016f

'000 s

qm

Take-up Net absorption0%

5%

10%

15%

20%

25%

1987 1991 1995 1999 2003 2007 2011 2015f

Vacancy r

ate

150,000sqm annual take-up

100,000sqm annual take-up

200,000sqm annual take-up

Sourc

Goodbody Economy - Ireland

Page 26 27 Sep. 2013

Building viability

So when will it be financially viable to build in the capital. Lisney has developed a very useful matrix,

which using current building costs and allowing for current market terms, including a two-year rent-free

period, calculates the appropriate rental level based on varying assumptions for the yield and the cost of

land.

At current rental values (c.€320 per sqm) and at the current rental yield of 6.25% in the city centre

region, it is not financially viable to develop and build an office location in the capital. However, as our

analysis of historical cycles shows, rental values can move up quite quickly, meaning that a viable rental

level can be achieved even prior to the completion of the building if the planning stage was to be

commenced straight away.

Lisney suggest that a headline rent of c.€360 per sqm is required to justify development. The

assumptions underlying this calculation include prevailing lease terms (including a 24-month rent-free

period), developer profit on costs at 15%, a yield of 6.25% and a site value of €10m per acre. Rents,

therefore, must increase by just 12% to make building viable (recent transactions suggest a €10m per

acre site cost is a reasonable assumption even though a recent transaction in Ballsbridge took place at a

price of €11.5m per acre).

Office market conclusions

Given the likely trajectory of the economy, particularly in Dublin, and the expected downward trend in

vacancy rates, the office market offers the best risk/reward investment prospects in the short-term.

High-single digit total returns are expected from this asset class, but the risk bias is to the upside, given

the expected continued high level of interest in the sector.

Office-building viability matrix (rent per sqm)

5.50% 5.75% 6.00% 6.25% 6.50% 6.75% 7.00%

5,000,000 274 290 305 320 335 351 367

7,000,000 288 304 320 336 352 369 385

8,000,000 295 311 327 344 361 378 395

9,000,000 302 319 335 352 369 386 404

10,000,000 309 326 343 360 377 395 413

11,000,000 316 333 350 368 386 404 422

12,000,000 322 340 358 376 394 412 431

13,000,000 329 348 365 384 403 422 440

14,000,000 336 355 372 392 411 431 449

15,000,000 343 362 381 400 420 440 459

Source: Lisney

Note: Green areas are financially viable combinations of yield and land cost, Red areas are unviable

Pric

e p

er a

cre

Yield

Goodbody Economy - Ireland

27 Sep. 2013 Page 27

Retail Market

Conditions in the Retail Market remain challenging with retailers continuing to face a weak economic

backdrop in the domestic economy. The most recent figures show core retail sales (ex-motor trades)

remain 18% below the peak levels of 2007. Broader consumption data display similar trends with the Q2

national accounts showing consumption rising by a modest 0.3% yoy in nominal terms (-1.3% yoy in

real terms), which is 14% lower than peak 2007 levels. The severity of the collapse in consumer

spending has seen retail rents fall almost 50% from 2008 peak levels and capital values fall 70% from

peak 2007 levels. This has translated into equivalent rental yields, which recovered as capital values fell,

averaging c.8% since H2 2009 from a low of 3.4% during the boom years. This recovery in equivalent

yields has seen Dublin’s ranking on the Cushman & Wakefield Most Expensive Retail Location fall

consistently since 2008 when it peaked at number 5, ahead of London, Tokyo and Sydney. It now stands

at 17.

Most expensive retail locations

Rank 2008 2012

1 New York Hong Kong

2 Hong Kong New York

3 Paris Paris

4 Milan Tokyo

5 Dublin Sydney

6 London London

7 Tokyo Zurich

8 Zurich Milan

9 Sydney Seoul

10 Seoul Munich

11 Athens Vienna

12 Munich Sao Paulo

13 Vienna Moscow

14 Moscow Beijing

15 Madrid Barcelona

16 Singapore Singapore

17 New Delhi Dublin

18 Amsterdam Amsterdam

19 Copenhagen Kuala Lumper

20 Prague Toronto

Source: Cushman & Wakefield

Despite this recovery in rental yields and valuations in retail property, actual rents and capital values

remain under pressure, with the latest set of data from IPD showing rentals (-6% yoy) and capital

values (-8% yoy) continuing to fall on an annual basis in Q2. While there are some sectors of the retail

market showing tentative signs of stabilisation, thus far this is confined to prime high street sites and

larger shopping centres particularly in the capital, where prime rents are bottoming. Activity levels and

rental yields in secondary locations outside the capital remain weak with vacancy levels high. This

reflects the challenging conditions and uncertain outlook that the retail sector in Ireland still faces with

consumer spending yet to initiate a recovery.

Goodbody Economy - Ireland

Page 28 27 Sep. 2013

Retail rents and capital values remain under pressure

Source: IPD

Rents followed retails sales lower

Source: IPD

The most recent retail figures show that core retail sales (ex-motor trades) remain 18% below the peak

levels seen in 2007. Broader consumption data display similar trends, with the Q2 national accounts

showing consumption rising by a modest 0.3% yoy in nominal terms (-1.3% yoy in real terms), which is

14% lower than peak 2007 levels. Against this negative backdrop retailers are continuing to struggle

and liquidation, receiverships and the exit of non-domestic retailers from the Irish market has continued.

There has also been an increase in strategic examinerships, which has seen some larger retail players

successfully securing rent reductions.

Regional high street vacancy

Source: CBRE

Bouncing along the bottom

The outlook for the retail property market is closely correlated with the consumer. Here underlying

drivers are showing tentative signs of stability. The most important of these are in relation to the labour

market where employments grew at 1.8% yoy in Q2 and unemployment has fallen to 13.7% from a high

of 15% in Q1 2012. However, the high debt burden being carried by households (203% of disposable

income) will continue to weigh on Irish consumers in the medium term and we expect consumption to

remain negative for the rest of 2013, prior to very slowly recovering in 2015. This will see retail rents

and valuations remain under pressure.

0

100

200

300

400

500

600

700

800

900

2Q

1983

4Q

1986

2Q

1990

4Q

1993

2Q

1997

4Q

2000

2Q

2004

4Q

2007

2Q

2011

Index levle

RENTAL INDEX CAPITAL GROWTH

50

60

70

80

90

100

110

120

130

1Q

2005

1Q

2006

1Q

2007

1Q

2008

1Q

2009

1Q

2010

1Q

2011

1Q

2012

1Q

2013

Index level

Rental Index Retail Index (Value)

0% 5% 10% 15% 20% 25%

Sligo - Grafton/Castle…

Limerick - O'Connell…

Sligo - O'Connell Street

Cork - St Patricks Street

Dublin - Grafton Street

Dublin - Henry/Mary…

Galway - Wiliam Street

Kilarney - New Street

Kilkenny - High Street

Galway - High Street

Kilarney - Main Street

Galway - Shop Street

Galway - Main Guard…

Q3 2012 Q1 2013

Goodbody Economy - Ireland

27 Sep. 2013 Page 29

In conjunction with the weak consumer, retail property faces other challenges. The 6 year slump in

retailing has seen a number of structural changes to the overall retail landscape that also negatively

impact the outlook for rental and capital growth. Amongst these are (i) turnover based rents; (ii) shorter

lease length, (iii) pop-up shops on temporary, low rent, leases and (iv) further strategic examinerships

by large retailers attempting to force rents down. On a broader basis the expansion of online retailing

also poses a threat to the sector

The Industrial Market - Showing signs of stabilisation

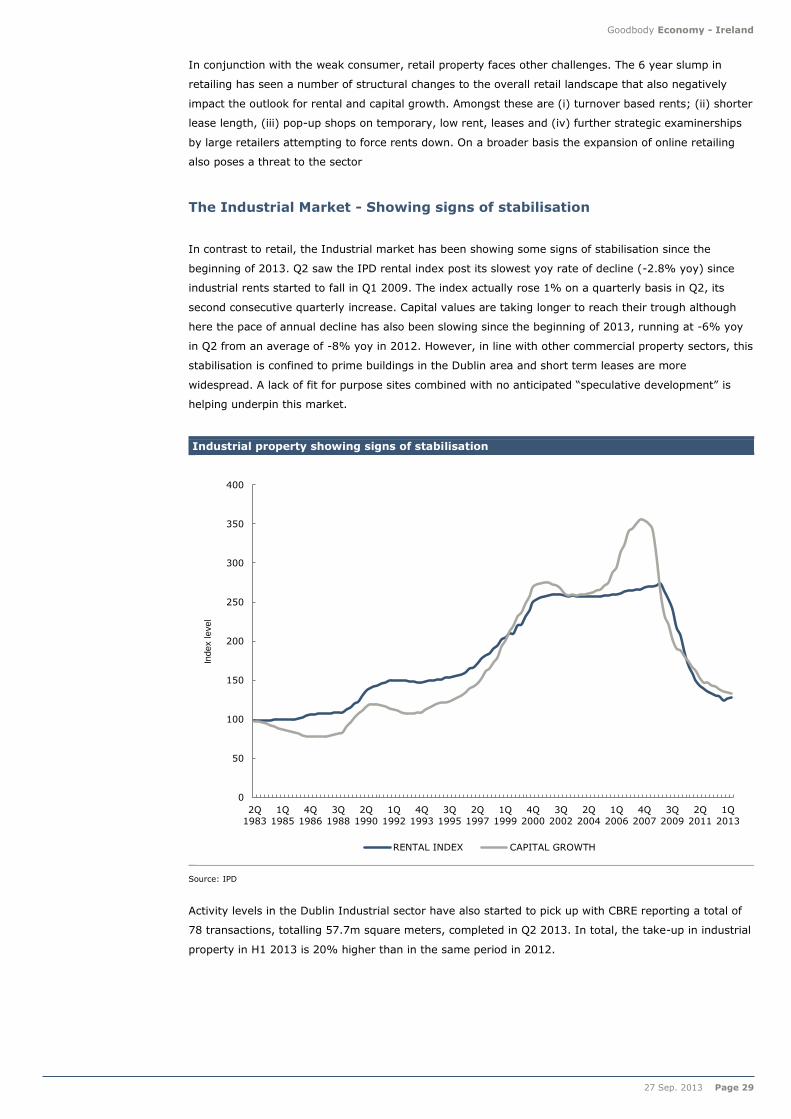

In contrast to retail, the Industrial market has been showing some signs of stabilisation since the

beginning of 2013. Q2 saw the IPD rental index post its slowest yoy rate of decline (-2.8% yoy) since

industrial rents started to fall in Q1 2009. The index actually rose 1% on a quarterly basis in Q2, its

second consecutive quarterly increase. Capital values are taking longer to reach their trough although

here the pace of annual decline has also been slowing since the beginning of 2013, running at -6% yoy

in Q2 from an average of -8% yoy in 2012. However, in line with other commercial property sectors, this

stabilisation is confined to prime buildings in the Dublin area and short term leases are more

widespread. A lack of fit for purpose sites combined with no anticipated “speculative development” is

helping underpin this market.

Industrial property showing signs of stabilisation

Source: IPD

Activity levels in the Dublin Industrial sector have also started to pick up with CBRE reporting a total of

78 transactions, totalling 57.7m square meters, completed in Q2 2013. In total, the take-up in industrial

property in H1 2013 is 20% higher than in the same period in 2012.

0

50

100

150

200

250

300

350

400

2Q

1983

1Q

1985

4Q

1986

3Q

1988

2Q

1990

1Q

1992

4Q

1993

3Q

1995

2Q

1997

1Q

1999

4Q

2000

3Q

2002

2Q

2004

1Q

2006

4Q

2007

3Q

2009

2Q

2011

1Q

2013

Index l

evel

RENTAL INDEX CAPITAL GROWTH

Goodbody Economy - Ireland

Page 30 27 Sep. 2013

Industrial take-up

Source: CBRE

Capital values, which are 63% below peak levels, are attracting a growing number of occupiers who

want to purchase buildings. This will provide some support for capital values. CBRE reports that almost

half (47%) of transactions in 2013 were property sales, with the remainder being lease agreements, an

increase from the 32% seen in H1 2012.

CBRE also reports that activity is being driven by large corporate transactions, many of which are part of

the multi-national sector, suggesting that the industrial market is benefitting from the solid performance

of the external sector in a way that the retail market is not. The continued success of the IDA and

Enterprise Ireland in attracting and retaining FDI and domestic exporters provides support. The shift to

non-store retailing and the resulting distribution requirements provides further opportunities for the

industrial market.

0

10

20

30

40

50

60

70

Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013

'000s S

quare

M

Goodbody Economy - Ireland

27 Sep. 2013 Page 31

Irish residential property market

While housing booms and busts have featured in a whole swathe of developed economies during the

2003-2012 period, the magnitude of Ireland’s has few, if any, precedents. Official data show that after

increasing by almost three-fold (270%) in the ten years to 2007, house prices halved over the following

five years. There is also reason to believe that the price declines have been even more severe, given the

increasing prevalence of cash transactions, which are not included in the official statistics. Following this

unprecedented crash, house prices in Ireland started to stabilise in the third quarter of 2012 and

registered a first annual increase in five years in June 2013.

Peak to trough price declines in recent housing busts

Source: ECB, Case-Shiller

Is residential property now cheap?

After a halving of prices, is residential property in Ireland now cheap? To assess this question, we look at

two long-term valuation metrics.

The first is house prices relative to incomes. While this is complicated by the lack of a consistent long-

term average earnings series, we have used the national accounts on disposable incomes and divided it

by the total population to get a per capita disposable income metric. This has the disadvantage of

biasing the house price to income ratio upwards, but the advantage of a consistent series back to 1970.

For the house price data, we have used Department of the Environment and Local Government (DoELG)

data on new house prices from 1975 to 1995, permanent tsb from 1996 to 2004 and the CSO from 2005

to 2013.

Between 1970 and 2013, Irish house prices averaged 11 times average per capita disposable income.

However, if the peak is excluded, the true long-term average is closer to 10 times. During that time

period, the ratio troughed at 8 times in 1996 and reached a peak of 16 times in 2007. The ratio

currently stands at 9 times. While the ratio is at its lowest level since 1997, it is just 10% below its long-

term average, so cheap but only modestly so. For the ratio to return to its long-term average over the

next five years, under the assumption of a modest 1% average annual growth in per capita disposable

income, house prices would have to grow by 5% per annum over the period.

-60%

-50%

-40%

-30%

-20%

-10%

0%

Portugal Netherlands Cyprus UK US Spain Ireland

Goodbody Economy - Ireland

Page 32 27 Sep. 2013

Average price/disposable income per capita

Source: CSO, ptsb, DoELG, Goodbody

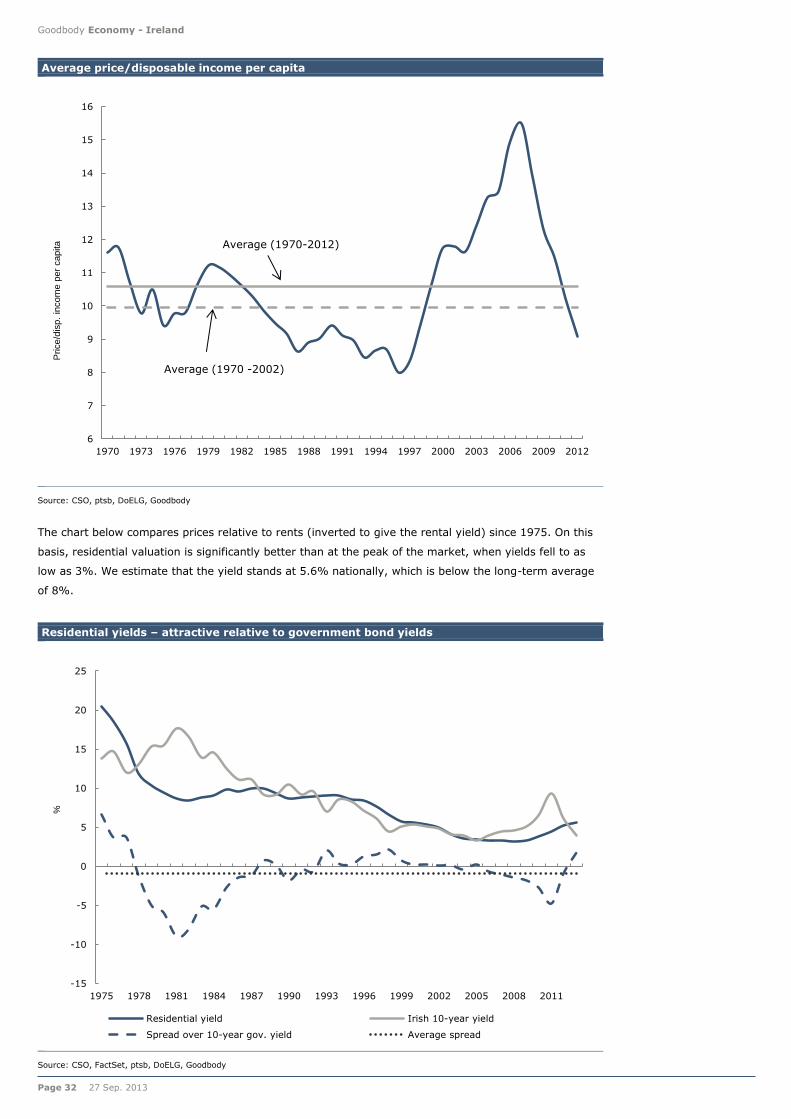

The chart below compares prices relative to rents (inverted to give the rental yield) since 1975. On this

basis, residential valuation is significantly better than at the peak of the market, when yields fell to as

low as 3%. We estimate that the yield stands at 5.6% nationally, which is below the long-term average

of 8%.

Residential yields – attractive relative to government bond yields

Source: CSO, FactSet, ptsb, DoELG, Goodbody

6

7

8

9

10

11

12

13

14

15

16