Manufacturing Competitiveness Investment Trends and What That Means for You 4 December 2015 Sarah Raehl Deloitte Consulting LLP

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Manufacturing Competitiveness Investment Trends and What That Means for You 4 December 2015 Sarah Raehl Deloitte Consulting LLP

#ED411 Copyright © 2015 Deloitte Development LLC. All rights reserved.

The US continues to be a recipient of significant Foreign Direct Investment (FDI) • Annual FDI in the US has averaged $200B / year for

the last 8 years

• The continued expansion of the global market is creating a more competitive investment climate

World inflows of FDI

United States 2007 $221B, 11% 2013 $193B, 14%

Europe 2007 $856B, 44% 2013 $239B, 17%

China 2007 $156B, 8% 2013 $258B, 19%

Attractiveness to expanding businesses – both foreign and domestic – is key to economic growth within the global market

Source: OECD international direct investment database

Note: Percentages indicate each country/region’s percentage of total global FDI

Asia European Union

Rest of World

United States

#ED411 Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Total US FDI has risen steadily over time, increasing 38.7% between 2007 and 2013 to $2.8 Trillion

• During that time manufacturing rose over 44% to $936B, accounting for over a third of total US FDI

Manufacturing continues to be the largest FDI sector

0

100

200

300

400

500

600

700

800

900

1000 2013 MFG by Segment $ billion

US total FDI by sector (historical cost basis)

Source: US Bureau of Economic Analysis

Electrical equipment Computers & Electronics

Metals

Food

Machinery

Transportation Equipment

Chemicals

Other Manufacturing

What is driving these trends?

#ED411 Copyright © 2015 Deloitte Development LLC. All rights reserved.

A new generation of digital design and collaboration tools is enabling manufacturers to save time and money in product development and manufacturing, potentially freeing up funds for such things as innovation

Advanced materials with superior performance characteristics, such as carbon fiber composites, ceramics, and nanomaterials are increasingly finding uses in large consumer-oriented industries, which may impact supply chains to streamline access

New processes such as additive manufacturing (e.g. 3D printing) are influencing everything from product design to material selection, to supply chain configuration

Increased push for product customization in less time, while balancing cost and risk demands

Focus is shifting from manufacturing as a cost to be minimized to a strategic lever to drive long term success through product differentiation

New technologies are shaping the future of manufacturing and offering companies new ways to compete, innovate, and grow

New Uses of IT

New Materials

New Production Processes

Shifting Demand Patterns

Where is next?

#ED411 Copyright © 2015 Deloitte Development LLC. All rights reserved.

• 50+ companies responded to the survey • Fabricated Metal Products and Machinery Manufacturing were the top segments represented in the survey • Average revenue of participant organizations was $500M to $10B while the employee count was 1,000 to 10,000

Deloitte, in partnership with MAPI, conducted a survey of US manufacturers regarding the evolution of their global footprint through 2020

25%

23%

18%

8%

8%

4% 4%

10% • Fabricated Metal Products • Machinery • Miscellaneous • Transportation Equipment • Electrical Equipment, Appliance

and Component Manufacturing • Chemicals • Plastics and Rubber Products • Other

9%

26%

14%

46%

0% 6%

$10M to $100M

$100M to $500M

$500M to $1B

$1B to $10B

$10B to $30B

> $30B

Primary Industry of Survey Respondents Annual Revenues of Survey Respondents

#ED411 Copyright © 2015 Deloitte Development LLC. All rights reserved.

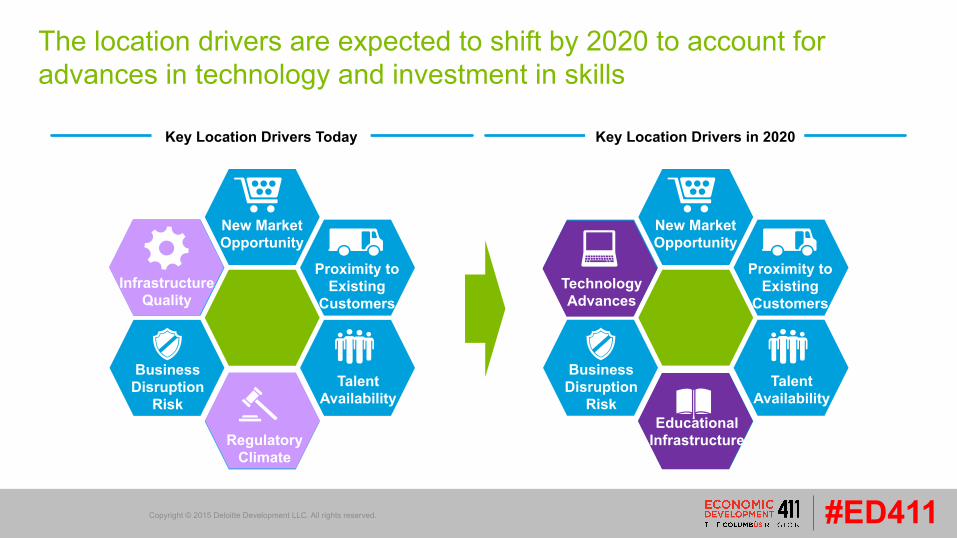

Market opportunities, the search for talent, and concerns with business disruption risk have historically been primary location decision drivers

Regulatory Climate Favorable government support

Talent Availability Search for engineers and skilled production workers, particularly welders and machinists

Business Disruption Risk Minimize exposure to natural, political, economic, and infrastructure risks that can disrupt production

Infrastructure Quality Robust and reliable infrastructure to minimize production disruptions

Proximity to Existing Customers Reduce time and cost to get products to end market

New Market Opportunity Growing purchasing power and sheer size of markets such as China and Brazil

#ED411 Copyright © 2015 Deloitte Development LLC. All rights reserved.

The location drivers are expected to shift by 2020 to account for advances in technology and investment in skills

Key Location Drivers Today Key Location Drivers in 2020

New Market Opportunity

Proximity to Existing

Customers

Talent Availability

Business Disruption

Risk

Infrastructure Quality

Regulatory Climate

New Market Opportunity

Proximity to Existing

Customers

Talent Availability

Business Disruption

Risk

Technology Advances

Educational Infrastructure

#ED411 Copyright © 2015 Deloitte Development LLC. All rights reserved.

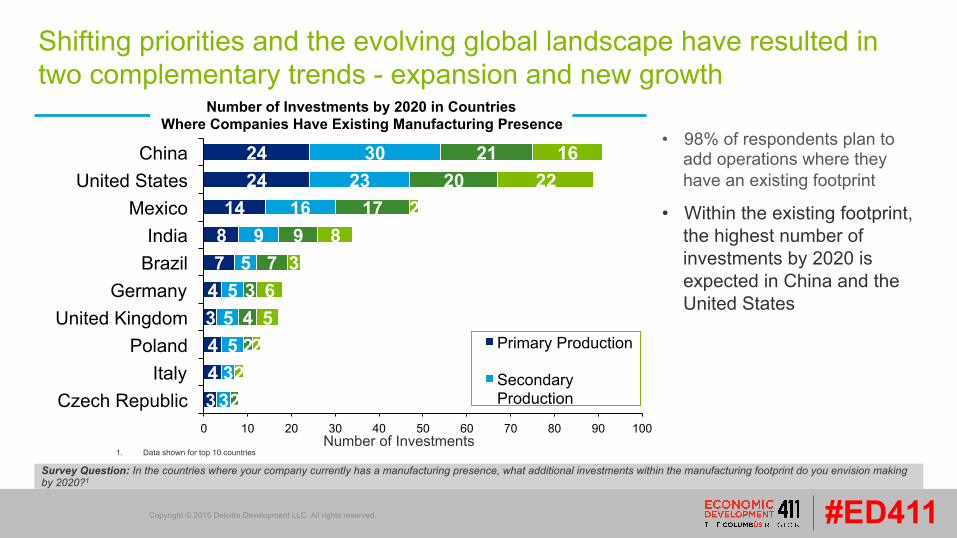

Shifting priorities and the evolving global landscape have resulted in two complementary trends - expansion and new growth

• 98% of respondents plan to add operations where they have an existing footprint

• Within the existing footprint, the highest number of investments by 2020 is expected in China and the United States

1. Data shown for top 10 countries

3 4 4 3 4 7 8 14

24 24

3 3 5 5 5

5 9

16 23

30

2

2 4 3

7 9

17 20

21

2 2

5 6

3 8

2 22

16

0 10 20 30 40 50 60 70 80 90 100

Czech Republic Italy

Poland United Kingdom

Germany Brazil India

Mexico United States

China

Primary Production

Secondary Production

Number of Investments

Number of Investments by 2020 in Countries Where Companies Have Existing Manufacturing Presence

Survey Question: In the countries where your company currently has a manufacturing presence, what additional investments within the manufacturing footprint do you envision making by 2020?1

#ED411 Copyright © 2015 Deloitte Development LLC. All rights reserved.

• While Brazil, China and India continue to be leading candidates for new manufacturing investments, countries such as South Africa, Turkey and Vietnam are also being considered

54% of respondents plan to invest outside of their existing footprint, with a focus in Asia and South America

2 2

3 4 4 4

6 7 7 7

0 2 4 6 8

Saudi Arabia Russia Poland

Vietnam Turkey Mexico

South Africa India

China Brazil

1. Data shown for top 10 countries

Number of Companies

Survey Question: What countries do you anticipate your company will enter (or are considering for entry) by 2020? 1

Number of Companies Looking to Enter New Markets

Country Talent Access

Serve New

Markets

Cost Reduction

Opportunity

Proximity to Resources /

Suppliers Incentives

Favorable Logistics /

Supply Chain

Brazil

China

India

Mexico

Poland

Russia

Saudi Arabia

South Africa

Turkey

Vietnam

High Importance Moderate Importance Limited Importance

Reasons for Expanding Footprint

How can you compete?

#ED411 Copyright © 2015 Deloitte Development LLC. All rights reserved.

Demonstrating a deep talent pool, robust ecosystem, and supportive business environment will be key to competing for manufacturing investment Talent Availability

• Existing talent availability • Pipeline of talent • Relevant industry concentration

Timing to Market • Development ready real estate options

• Site readiness – prepped and ready to go • Utilities – in place, reliable, scalable, and sustainable • Road access – in place • Permitting & environmental studies – complete or able to be expedited

Attractive Cost Structure • One-Time (land/building, construction, site prep, capital, permits) • Ongoing (labor, logistics, taxes, utilities, facility) • Incentives (Upfront, Ongoing)

Fit • United front for attracting business (regional level) • Brand image and company culture • Desirable place to live (expats & Americans)

Enabling Manufacturing

Talent Availability

Timing to Market Cost

Fit

#ED411 Copyright © 2015 Deloitte Development LLC. All rights reserved.

Proactively identifying and addressing challenges within your target ecosystems can be a key differentiator in the long-term

Manufacturers

Universities/ tech colleges

Growth fundin

g

Growth

funding

Investment return

3D printing service

providers

• Software developers • Material providers

Industry trade groups

Startups

Financers

Support

services

Talent

Training

Talent

Research

Research funding

Mentorship

Leadership

Shared research

Development Partnerships/ Research

Training input

Shared research

Jobs / internships

Mfg input / partnerships

Jobs

Training

Training

3D Printing

Representative 3D Printing Ecosystem

Locations that excel at demonstrating favorable talent pools, ecosystems, and supportive business

environments are likely to be the big winners in the race to attract manufacturing investments in the future

Copyright © 2015 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited

Related Documents