January 6, 2013 Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision. For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report. * = This Research Report has been partially prepared by analysts employed by non-U.S. affiliates of the member. Please see page 2 for the name of each non-U.S. affiliate contributing to this Research Report and the names of the analysts employed by each contributing affiliate. += Analysts employed by non-U.S. affiliates are not registered with FINRA, may not be associated persons of the member and may not be subject to NASD/NYSE restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account. MORGAN STANLEY BLUE PAPER eCommerce Disruption: A Global Theme Transforming Traditional Retail Fulfillment execution is key to realizing eCommerce’s disruptive potential. By 2016, our AlphaWise survey and global eCommerce model suggest a nearly 50% increase in penetration of retail sales, to 9.3% (from 6.5% today), surpassing $1 trillion. As the key disruptors of the past 10 years become incumbents, their continued success hinges on building scale and brand equity. Which companies will benefit? Amazon, eBay, MercadoLibre, and Rakuten should benefit as the scale-based eCommerce platform companies. Traditional retail beneficiaries include Nordstrom, Sun Art, Williams-Sonoma, and eventually Walmart. Niche online players like ASOS and Blue Nile could also prosper from the global, disruptive, long runway trend of eCommerce. For some, eCommerce is a relatively minor issue. High-end apparel and footwear, price clubs, and specialty food retailers have business models that seem less vulnerable to market share erosion from eCommerce. We put Costco in this category. This Blue Paper leverages insights from Morgan Stanley retail and internet analysts from all over the world to arrive at five key conclusions: 1) fulfillment infrastructure is critical, 2) some categories remain resistant to change, 3) third-party marketplaces can prosper, 4) the mobile opportunity is promising, and 5) scale / brand favors incumbents. Driving those conclusions are the competitive advantages successful eCommerce players enjoy: price, selection, convenience, distribution, and cost structure. MORGAN STANLEY RESEARCH Global Scott Devitt 1 Andrew Ruud 1 David Gober 1 Joseph Parkhill 1 Kimberly Greenberger 1 Mark Wiltamuth 1 Richard Ji 2 Philip Wan 2 Timothy Chan 2 Robert Lin 2 Angela Moh 2 Geoff Ruddell 3 Edouard Aubin 3 Anisha Singhal 3 Louise Singlehurst 3 Edward Hill-Wood 3 Nicholas Ashworth 3 Maryia Berasneva 3 Loredana Serra 1 Tom Kierath 5 Crystal Wang 5 Tetsuro Tsusaka 6 Zachary Arrick 1 Nishant Verma 1 *See page 2 for all contributors to this report 1 Morgan Stanley & Co. LLC 2 Morgan Stanley Asia Limited+ 3 Morgan Stanley & Co. International plc+ 4 Morgan Stanley C.T.V.M. S.A+ 5 Morgan Stanley Australia Limited + 6 Morgan Stanley MUFG Securities Co., Ltd.+ Morgan Stanley Blue Papers focus on critical investment themes that require coordinated perspectives across industry sectors, regions, or asset classes.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

January 6, 2013

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision.

For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report.

* = This Research Report has been partially prepared by analysts employed by non-U.S. affiliates of the member. Please see page 2 for the name of each non-U.S. affiliate contributing to this Research Report and the names of the analysts employed by each contributing affiliate.

+= Analysts employed by non-U.S. affiliates are not registered with FINRA, may not be associated persons of the member and may not be subject to NASD/NYSE restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

M O R G A N S T A N L E Y B L U E P A P E R

eCommerce Disruption: A Global Theme Transforming Traditional Retail

Fulfillment execution is key to realizing eCommerce’s disruptive potential. By 2016, our AlphaWise survey and global eCommerce model suggest a nearly 50% increase in penetration of retail sales, to 9.3% (from 6.5% today), surpassing $1 trillion. As the key disruptors of the past 10 years become incumbents, their continued success hinges on building scale and brand equity.

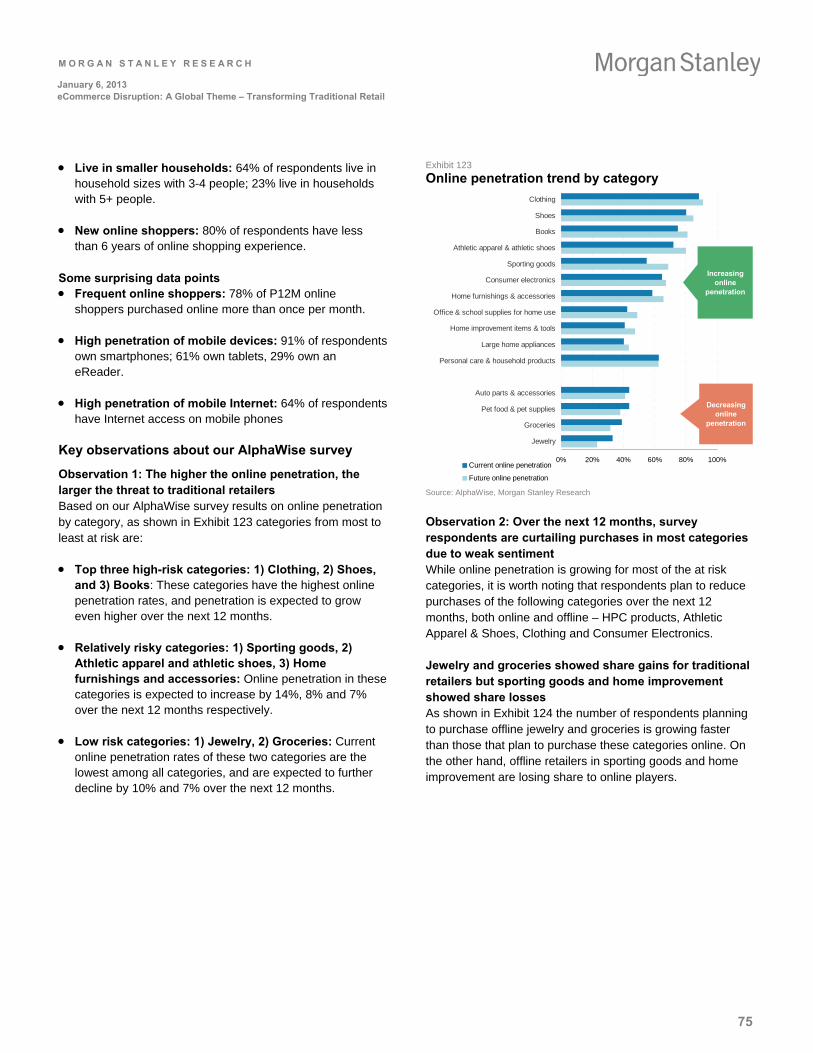

Which companies will benefit? Amazon, eBay, MercadoLibre, and Rakuten should benefit as the scale-based eCommerce platform companies. Traditional retail beneficiaries include Nordstrom, Sun Art, Williams-Sonoma, and eventually Walmart. Niche online players like ASOS and Blue Nile could also prosper from the global, disruptive, long runway trend of eCommerce. For some, eCommerce is a relatively minor issue. High-end apparel and footwear, price clubs, and specialty food retailers have business models that seem less vulnerable to market share erosion from eCommerce. We put Costco in this category.

This Blue Paper leverages insights from Morgan Stanley retail and internet analysts from all over the world to arrive at five key conclusions: 1) fulfillment infrastructure is critical, 2) some categories remain resistant to change, 3) third-party marketplaces can prosper, 4) the mobile opportunity is promising, and 5) scale / brand favors incumbents. Driving those conclusions are the competitive advantages successful eCommerce players enjoy: price, selection, convenience, distribution, and cost structure.

M O R G A N S T A N L E Y R E S E A R C H

G l o b a l

Scott Devitt1

Andrew Ruud1

David Gober1

Joseph Parkhill1

Kimberly Greenberger1

Mark Wiltamuth1

Richard Ji2

Philip Wan2

Timothy Chan2

Robert Lin2

Angela Moh2

Geoff Ruddell3

Edouard Aubin3

Anisha Singhal3

Louise Singlehurst3

Edward Hill-Wood3

Nicholas Ashworth3

Maryia Berasneva3

Loredana Serra1

Tom Kierath5

Crystal Wang5

Tetsuro Tsusaka6

Zachary Arrick1

Nishant Verma1

*See page 2 for all contributors to this report

1 Morgan Stanley & Co. LLC

2 Morgan Stanley Asia Limited+ 3 Morgan Stanley & Co. International plc+ 4 Morgan Stanley C.T.V.M. S.A+ 5 Morgan Stanley Australia Limited + 6 Morgan Stanley MUFG Securities Co., Ltd.+

Morgan Stanley Blue Papers focus on critical investment themes that require coordinated perspectives across industry sectors, regions, or asset classes.

M O R G A N S T A N L E Y R E S E A R C H

2

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

Global Internet and Retail Teams

Contributors to This Report

US Internet

Scott Devitt1 +1 (212) 761-3365 [email protected] Andrew Ruud1 +1 (212) 761-5978 [email protected] Zachary Arrick1 +1 (212) 761-4226 [email protected] Nishant Verma1 +1 (212) 761-6320 [email protected]

US Retail

Hardlines David Gober1 +1 (212) 761-6616 [email protected]

Branded Apparel & Footwear Joseph Parkhill1 +1 (212) 761-0766 [email protected]

Softlines Kimberly Greenberger1 +1 (212) 761-6284 [email protected]

Food, Drug and Discounters Mark Wiltamuth1 +1 (212) 761-8589 [email protected]

China Internet

Richard Ji2 +852 2848-6926 [email protected] Philip Wan2 +852 2848-8227 [email protected] Timothy Chan2 +852 2239-7107 [email protected]

China Retail

Robert Lin2 +852 2848-5835 [email protected] Angela Moh2 +852 2848-5405 [email protected]

Western Europe Retail

Geoff Ruddell3 +44 20 7425-8954 [email protected] Edouard Aubin3 +44 20 7425-3160 [email protected] Anisha Singhal3 +44 20 7425-7526 [email protected] Louise Singlehurst3 +44 20 7425-7239 [email protected]

Europe Internet

Edward Hill-Wood3 +44 20 7425-9224 [email protected] Nicholas Ashworth3 +44 20 7425-7770 [email protected] Maryia Berasneva3 +44 20 7425-7502 [email protected] Liz A. Rich3 +44 20 7425-7082 [email protected]

Brazil Retail

Loredana Serra1 +1 (212) 761-7954 [email protected] Jeronimo De Guzman1 +1 (212) 761-7084 [email protected] Franco Abelardo4 +55 11 3048-9609 [email protected]

Australia Retail

Tom Kierath5 +61 2 9770-1578 [email protected] Crystal Wang5 +61 2 9770-1195 [email protected]

Japan Internet

Tetsuro Tsusaka6 +81 3 5424-5901 [email protected]

1 Morgan Stanley & Co. LLC 2 Morgan Stanley Asia Limited+

3 Morgan Stanley & Co. International plc+ 4 Morgan Stanley C.T.V.M. S.A+

5 Morgan Stanley Australia Limited + 6 Morgan Stanley MUFG Securities Co., Ltd.+

See page 145 for recent Blue Paper reports.

M O R G A N S T A N L E Y R E S E A R C H

3

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

Table of Contents

Executive Summary: Retail Transformed .......................................................................................................................... 4

Five Key Conclusions: Where Does eCommerce Go from Here?.................................................................................... 5

Disruptive Forces and Key Stock Calls............................................................................................................................... 7

Takeaways by Region ........................................................................................................................................................... 8

Key AlphaWise Conclusions ................................................................................................................................................ 12

Segment Analysis by Region

United States

Internet ........................................................................................................................................................................ 14

Retail............................................................................................................................................................................ 23

Food, Drug and Discounters ................................................................................................................................. 27

Branded Apparel & Footwear ................................................................................................................................ 28

Hardlines ................................................................................................................................................................. 31

Softlines .................................................................................................................................................................. 33

Western Europe

Retail............................................................................................................................................................................ 43

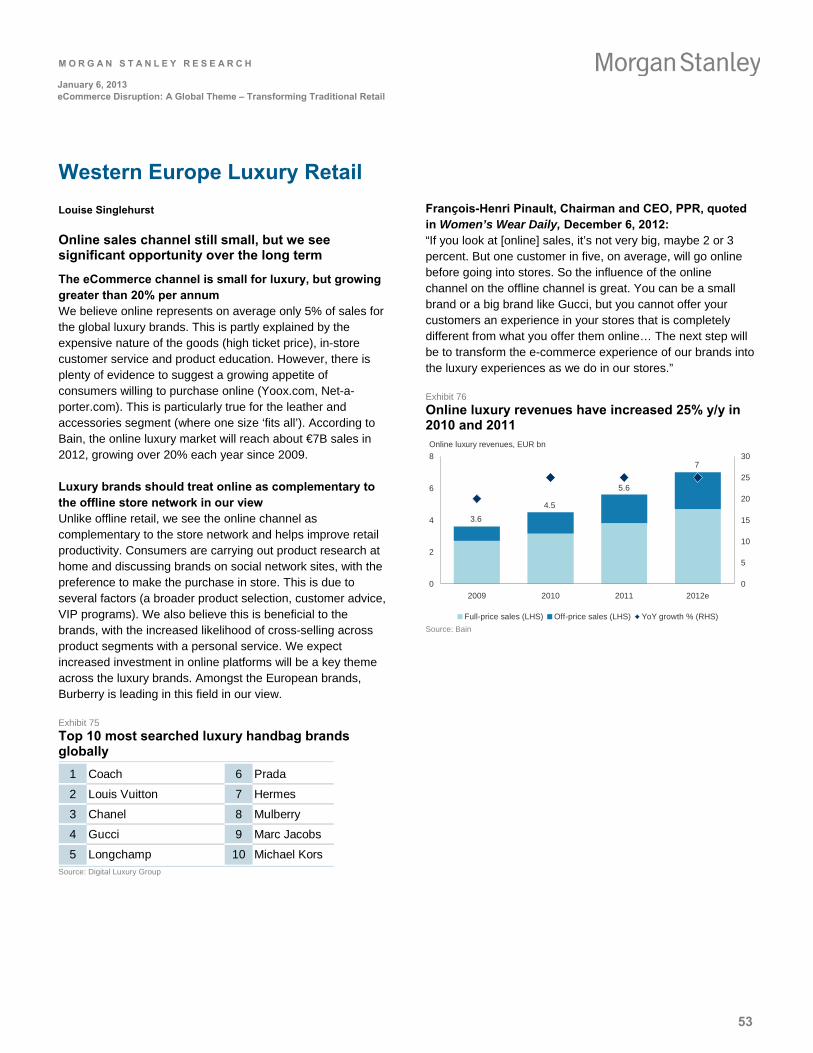

Retail – Luxury............................................................................................................................................................ 53

Brazil: Internet and Retail ................................................................................................................................ 54

China

Internet..................................................................................................................................................................... 61

Retail ........................................................................................................................................................................ 68

Russia

Internet..................................................................................................................................................................... 78

Australia

Retail ........................................................................................................................................................................ 84

Japan

Internet..................................................................................................................................................................... 89

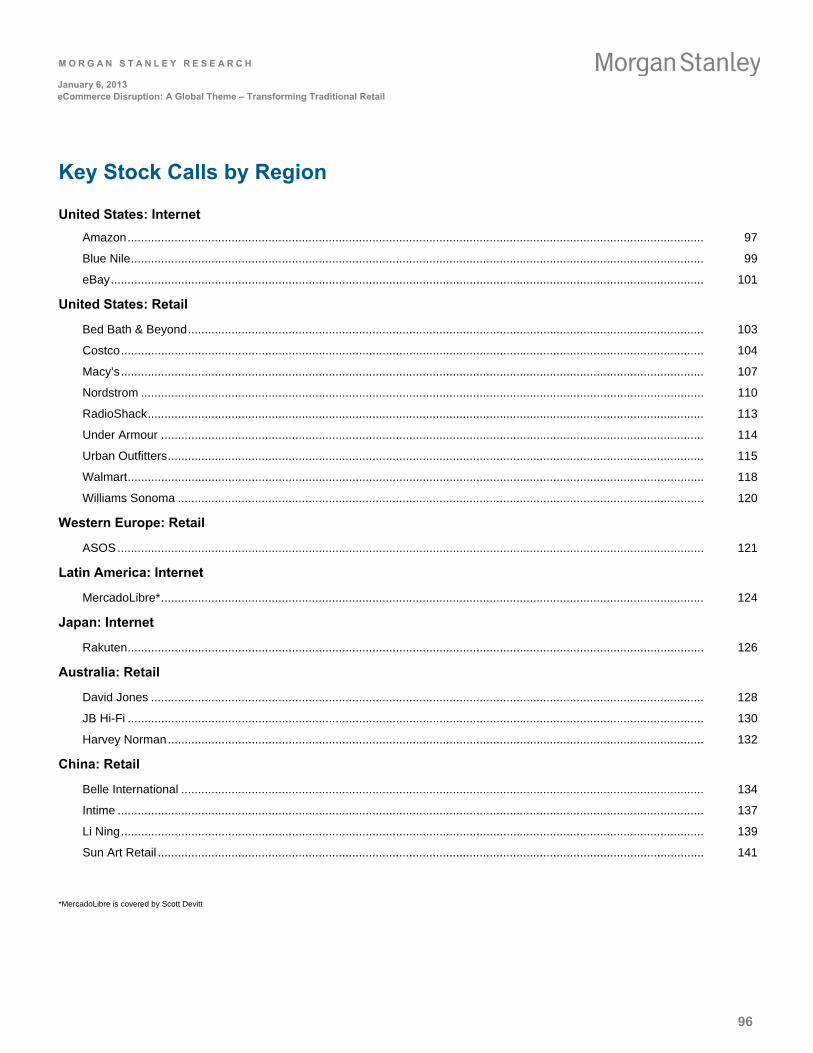

Key Stock Calls by Region ................................................................................................................................................... 95

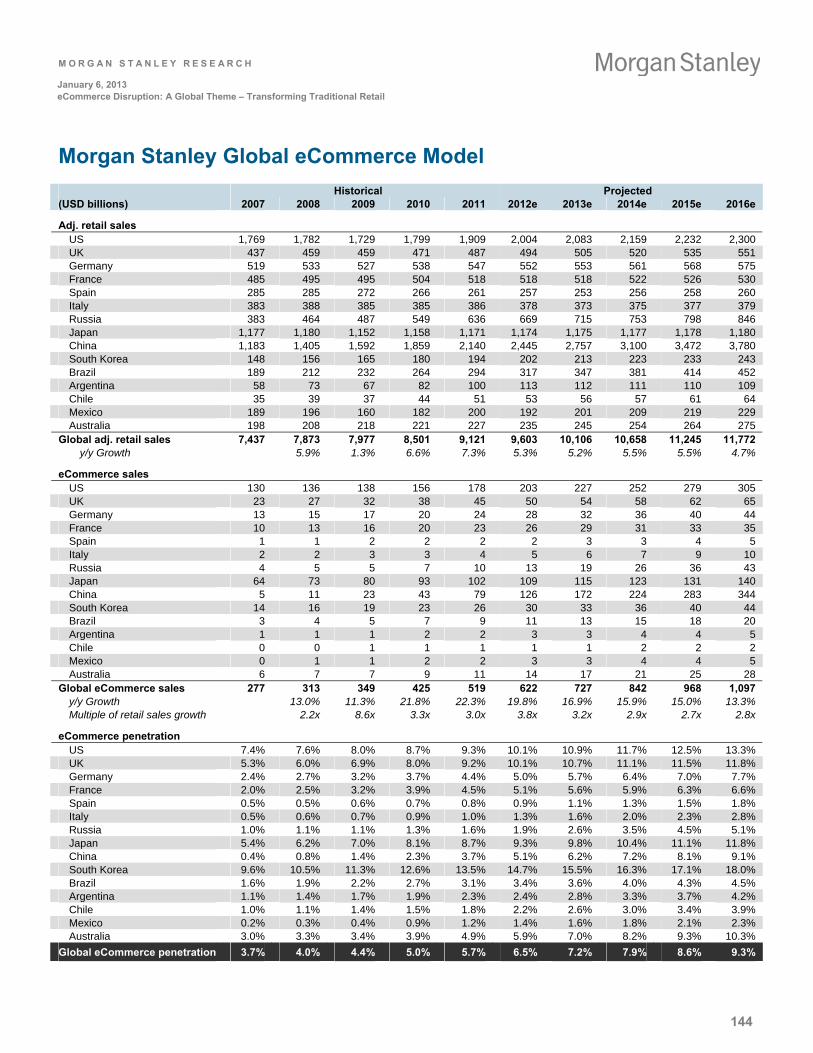

Morgan Stanley Global eCommerce Model......................................................................................................................... 143

M O R G A N S T A N L E Y R E S E A R C H

4

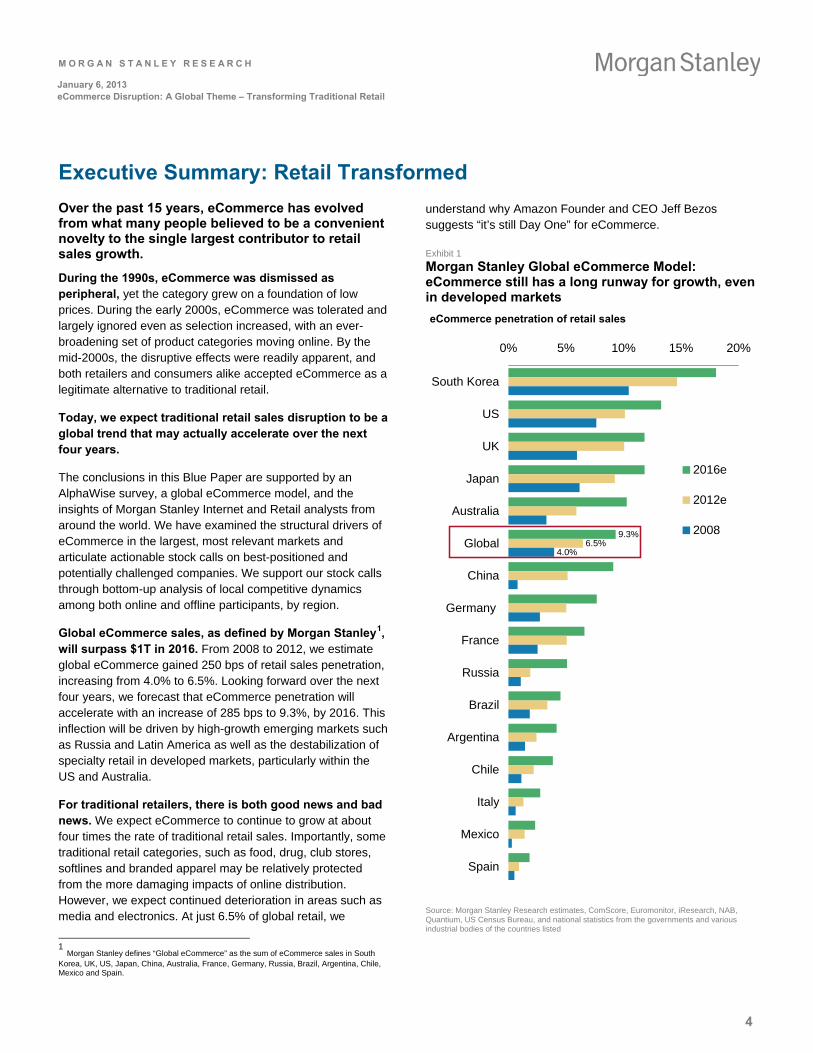

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

Executive Summary: Retail Transformed

Over the past 15 years, eCommerce has evolved from what many people believed to be a convenient novelty to the single largest contributor to retail sales growth.

During the 1990s, eCommerce was dismissed as peripheral, yet the category grew on a foundation of low prices. During the early 2000s, eCommerce was tolerated and largely ignored even as selection increased, with an ever- broadening set of product categories moving online. By the mid-2000s, the disruptive effects were readily apparent, and both retailers and consumers alike accepted eCommerce as a legitimate alternative to traditional retail.

Today, we expect traditional retail sales disruption to be a global trend that may actually accelerate over the next four years.

The conclusions in this Blue Paper are supported by an AlphaWise survey, a global eCommerce model, and the insights of Morgan Stanley Internet and Retail analysts from around the world. We have examined the structural drivers of eCommerce in the largest, most relevant markets and articulate actionable stock calls on best-positioned and potentially challenged companies. We support our stock calls through bottom-up analysis of local competitive dynamics among both online and offline participants, by region.

Global eCommerce sales, as defined by Morgan Stanley1, will surpass $1T in 2016. From 2008 to 2012, we estimate global eCommerce gained 250 bps of retail sales penetration, increasing from 4.0% to 6.5%. Looking forward over the next four years, we forecast that eCommerce penetration will accelerate with an increase of 285 bps to 9.3%, by 2016. This inflection will be driven by high-growth emerging markets such as Russia and Latin America as well as the destabilization of specialty retail in developed markets, particularly within the US and Australia.

For traditional retailers, there is both good news and bad news. We expect eCommerce to continue to grow at about four times the rate of traditional retail sales. Importantly, some traditional retail categories, such as food, drug, club stores, softlines and branded apparel may be relatively protected from the more damaging impacts of online distribution. However, we expect continued deterioration in areas such as media and electronics. At just 6.5% of global retail, we

1 Morgan Stanley defines “Global eCommerce” as the sum of eCommerce sales in South Korea, UK, US, Japan, China, Australia, France, Germany, Russia, Brazil, Argentina, Chile, Mexico and Spain.

understand why Amazon Founder and CEO Jeff Bezos suggests “it’s still Day One” for eCommerce.

Exhibit 1

Morgan Stanley Global eCommerce Model: eCommerce still has a long runway for growth, even in developed markets eCommerce penetration of retail sales

9.3%6.5%

4.0%

0% 5% 10% 15% 20%

South Korea

US

UK

Japan

Australia

Global

China

Germany

France

Russia

Brazil

Argentina

Chile

Italy

Mexico

Spain

2016e

2012e

2008

Source: Morgan Stanley Research estimates, ComScore, Euromonitor, iResearch, NAB, Quantium, US Census Bureau, and national statistics from the governments and various industrial bodies of the countries listed

M O R G A N S T A N L E Y R E S E A R C H

5

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

Five Key Conclusions: Where Does eCommerce Go from Here?

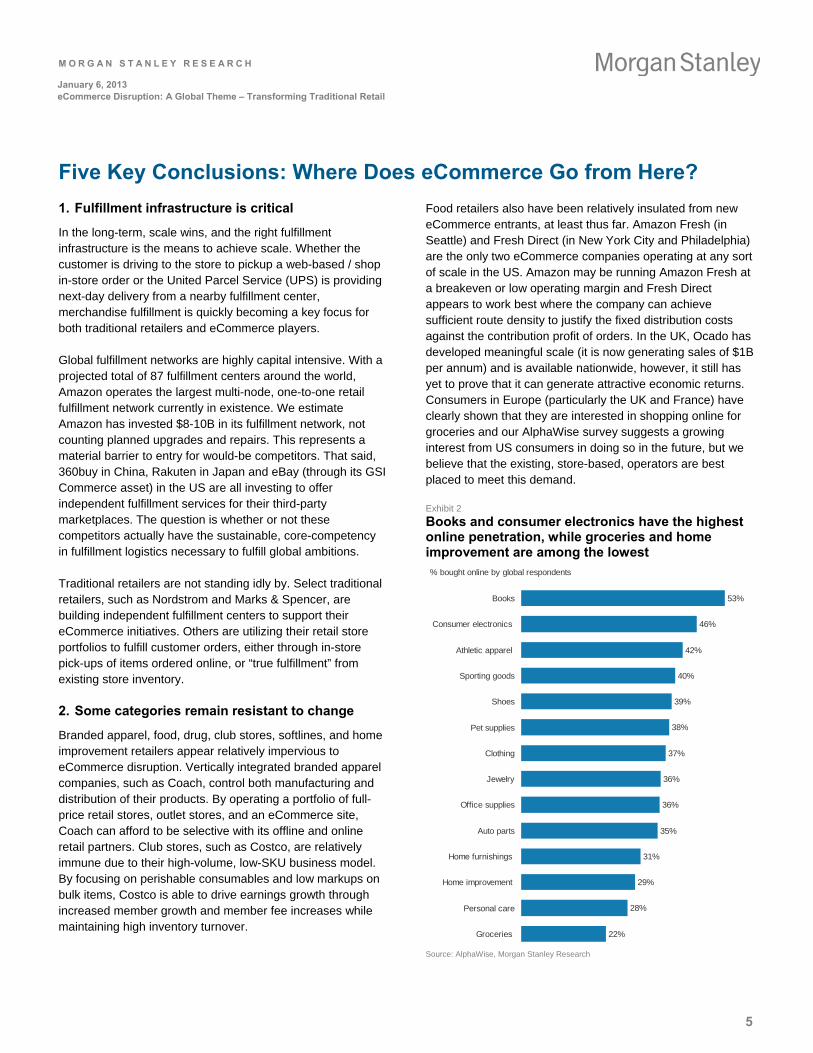

1. Fulfillment infrastructure is critical

In the long-term, scale wins, and the right fulfillment infrastructure is the means to achieve scale. Whether the customer is driving to the store to pickup a web-based / shop in-store order or the United Parcel Service (UPS) is providing next-day delivery from a nearby fulfillment center, merchandise fulfillment is quickly becoming a key focus for both traditional retailers and eCommerce players.

Global fulfillment networks are highly capital intensive. With a projected total of 87 fulfillment centers around the world, Amazon operates the largest multi-node, one-to-one retail fulfillment network currently in existence. We estimate Amazon has invested $8-10B in its fulfillment network, not counting planned upgrades and repairs. This represents a material barrier to entry for would-be competitors. That said, 360buy in China, Rakuten in Japan and eBay (through its GSI Commerce asset) in the US are all investing to offer independent fulfillment services for their third-party marketplaces. The question is whether or not these competitors actually have the sustainable, core-competency in fulfillment logistics necessary to fulfill global ambitions.

Traditional retailers are not standing idly by. Select traditional retailers, such as Nordstrom and Marks & Spencer, are building independent fulfillment centers to support their eCommerce initiatives. Others are utilizing their retail store portfolios to fulfill customer orders, either through in-store pick-ups of items ordered online, or “true fulfillment” from existing store inventory.

2. Some categories remain resistant to change

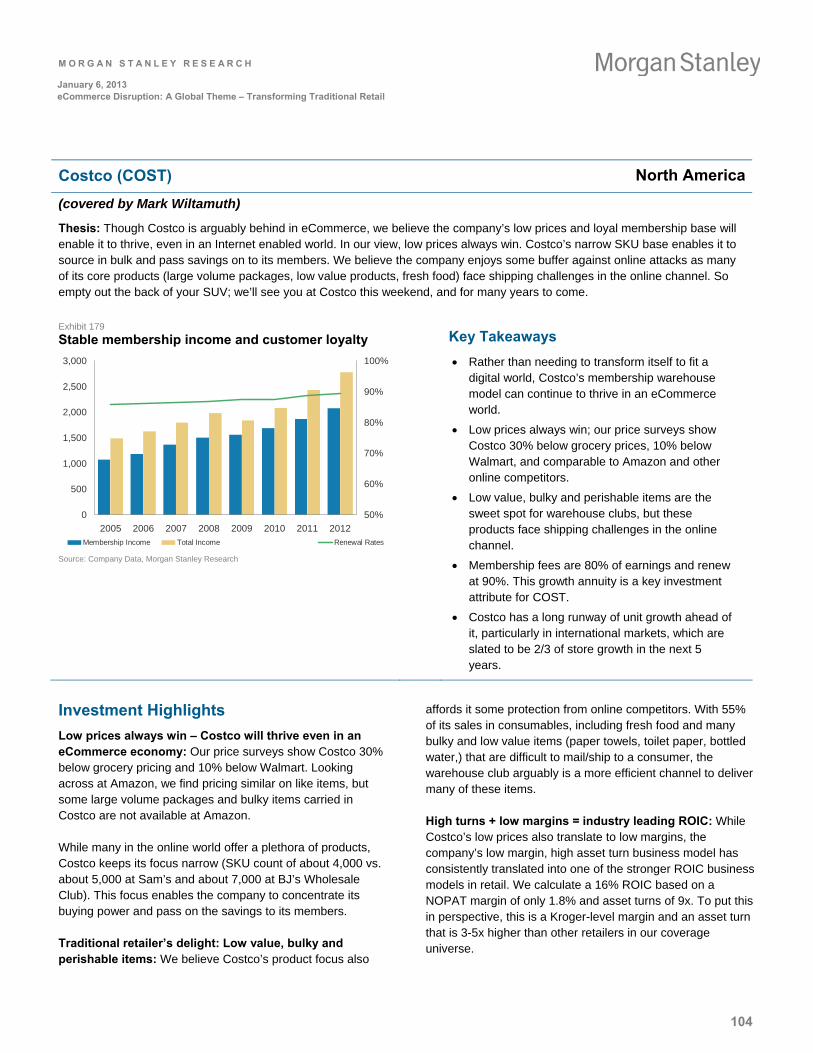

Branded apparel, food, drug, club stores, softlines, and home improvement retailers appear relatively impervious to eCommerce disruption. Vertically integrated branded apparel companies, such as Coach, control both manufacturing and distribution of their products. By operating a portfolio of full-price retail stores, outlet stores, and an eCommerce site, Coach can afford to be selective with its offline and online retail partners. Club stores, such as Costco, are relatively immune due to their high-volume, low-SKU business model. By focusing on perishable consumables and low markups on bulk items, Costco is able to drive earnings growth through increased member growth and member fee increases while maintaining high inventory turnover.

Food retailers also have been relatively insulated from new eCommerce entrants, at least thus far. Amazon Fresh (in Seattle) and Fresh Direct (in New York City and Philadelphia) are the only two eCommerce companies operating at any sort of scale in the US. Amazon may be running Amazon Fresh at a breakeven or low operating margin and Fresh Direct appears to work best where the company can achieve sufficient route density to justify the fixed distribution costs against the contribution profit of orders. In the UK, Ocado has developed meaningful scale (it is now generating sales of $1B per annum) and is available nationwide, however, it still has yet to prove that it can generate attractive economic returns. Consumers in Europe (particularly the UK and France) have clearly shown that they are interested in shopping online for groceries and our AlphaWise survey suggests a growing interest from US consumers in doing so in the future, but we believe that the existing, store-based, operators are best placed to meet this demand.

Exhibit 2

Books and consumer electronics have the highest online penetration, while groceries and home improvement are among the lowest % bought online by global respondents

53%

46%

42%

40%

39%

38%

37%

36%

36%

35%

31%

29%

28%

22%

Books

Consumer electronics

Athletic apparel

Sporting goods

Shoes

Pet supplies

Clothing

Jewelry

Office supplies

Auto parts

Home furnishings

Home improvement

Personal care

Groceries

Source: AlphaWise, Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H

6

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

3. Third-party marketplaces can prosper

The success of owned-inventory eCommerce sites (“first party,” or 1P) versus third-party marketplaces (3P) varies by region. The US and Western Europe have seen success in integrated eCommerce platforms, 1P+3P, dominated by Amazon, although eBay has re-emerged as a capable 3P-only competitor. While one could argue that selling owned inventory alongside third-party sellers creates a conflict of interest, there are benefits to being a market maker. Amazon’s owned inventory business helps it set market pricing for third-party sellers. While this could mean lower profits on a unit basis for third-party sellers, it drives lower prices in the marketplace, which drives greater customer adoption, leading to increased third-party sell-through.

In markets like South Korea, China and Japan, 3P continues to lead. However, third-party marketplaces in these markets tend to have an inability to bundle orders (meaning products are delivered from a variety of sellers) making it tough to compete with owned inventory players on delivery speed and consistency of experience. Therefore 3P marketplaces, particularly Rakuten, are aggressively investing in building a fulfillment network. While MercadoLibre management recognizes the value of offering fulfillment, the company does not have plans to do so in the near-term.

4. Mobile eCommerce: A promising opportunity – for both online and traditional retailers

While mobile can represent an extra layer of convenience, via the ability to purchase anytime / anywhere, it can also have the opposite effect, as 1) entering billing and shipping information can be cumbersome and 2) given smaller screen size, the app must be highly intuitive. We believe larger companies, with the resources to develop well-designed apps that integrate customers’ existing account information can generate incremental sales.

Exhibit 3

Smartphone penetration by geography Smartphone installed base as a % of mobile subscriber base

Smartphone penetration by region

37%

47%

55%

66%

74%

'05 '06 '07 '08 '09 '10 '11 '12e '13e '14e '15e

North America

Western Europe

China

Latin America

Eastern Europe

Source: Company data, Gartner, IDC, Nielsen, Morgan Stanley Research

Smartphone penetration is highest in the US and UK. Not-surprisingly, eCommerce sales through mobile devices represent 10-12% of all eCommerce purchases in those countries, which is at least 2-3x the rate for emerging markets. According to comScore, US mobile eCommerce penetration has grown from 2% in 2Q10 to 10% in 3Q12.

eCommerce companies are beginning to disclose their own smartphone eCommerce penetration. eBay, for example, estimates about 13% of GMV will be purchased via a smartphone in 2012, of which the company estimates 1/3 is incremental to desktop GMV. The company has also developed an app that simplifies the listing process, which enables the company to gain traction with sellers, as well.

Exhibit 4

comScore estimates 10% of eCommerce sales in the US were made on a mobile device

$0

$10

$20

$30

$40

$50

$60

2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12

0%

2%

4%

6%

8%

10%

12%

US eCommerce ($B) Percentage Spent via Mobile Devices

Source: comScore, Morgan Stanley Research

Mobile can also benefit traditional retailers. By equipping clerks with mobile devices, shoppers can speed up purchasing by skipping the checkout line. It can also help provide better inventory management when combined with technologies like radio frequency identification.

5. Scale / Brand: The big should get bigger

Traditional retailers benefit from legacy brand and store footprint. Online retailers that can achieve scale (which is rare) benefit from brand awareness, effective online customer service, and a more variable cost structure. The admittedly small number of instances of scale success, albeit with significant economic value creation, include Alibaba, Amazon, eBay, MercadoLibre, and Rakuten. Our scale / brand conclusion is that online retail may ultimately have more consolidated market share than offline retail favoring large players. In this context, traditional discount retailers may be best positioned to participate in the consolidation of specialty retailers. Companies such as Costco and Walmart represent material distribution points for many global brands, and it may be difficult for eCommerce to disrupt the scale advantages of larger, established traditional retailers.

M O R G A N S T A N L E Y R E S E A R C H

7

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

Five Disruptive Forces Summary of Top Stock Calls

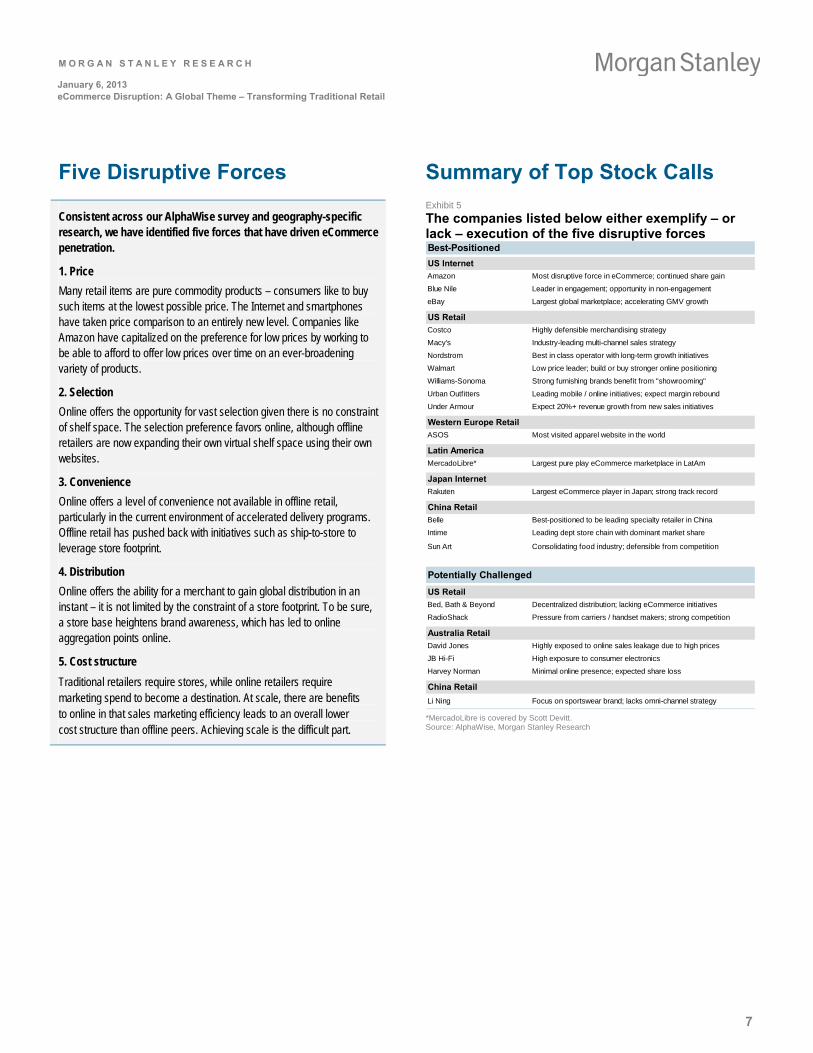

Consistent across our AlphaWise survey and geography-specific research, we have identified five forces that have driven eCommerce penetration.

1. Price

Many retail items are pure commodity products – consumers like to buy such items at the lowest possible price. The Internet and smartphones have taken price comparison to an entirely new level. Companies like Amazon have capitalized on the preference for low prices by working to be able to afford to offer low prices over time on an ever-broadening variety of products.

2. Selection

Online offers the opportunity for vast selection given there is no constraint of shelf space. The selection preference favors online, although offline retailers are now expanding their own virtual shelf space using their own websites.

3. Convenience

Online offers a level of convenience not available in offline retail, particularly in the current environment of accelerated delivery programs. Offline retail has pushed back with initiatives such as ship-to-store to leverage store footprint.

4. Distribution

Online offers the ability for a merchant to gain global distribution in an instant – it is not limited by the constraint of a store footprint. To be sure, a store base heightens brand awareness, which has led to online aggregation points online.

5. Cost structure

Traditional retailers require stores, while online retailers require marketing spend to become a destination. At scale, there are benefits to online in that sales marketing efficiency leads to an overall lower cost structure than offline peers. Achieving scale is the difficult part.

Exhibit 5

The companies listed below either exemplify – or lack – execution of the five disruptive forces Best-Positioned

US Internet

Amazon Most disruptive force in eCommerce; continued share gain

Blue Nile Leader in engagement; opportunity in non-engagement

eBay Largest global marketplace; accelerating GMV growth

US Retail

Costco Highly defensible merchandising strategy

Macy's Industry-leading multi-channel sales strategy

Nordstrom Best in class operator with long-term growth initiatives

Walmart Low price leader; build or buy stronger online positioning

Williams-Sonoma Strong furnishing brands benefit from "showrooming"

Urban Outfitters Leading mobile / online initiatives; expect margin rebound

Under Armour Expect 20%+ revenue growth from new sales initiatives

Western Europe Retail

ASOS Most visited apparel website in the world

Latin America

MercadoLibre* Largest pure play eCommerce marketplace in LatAm

Japan Internet

Rakuten Largest eCommerce player in Japan; strong track record

China Retail

Belle Best-positioned to be leading specialty retailer in China

Intime Leading dept store chain with dominant market share

Sun Art Consolidating food industry; defensible from competition

Potentially Challenged

US Retail

Bed, Bath & Beyond Decentralized distribution; lacking eCommerce initiatives

RadioShack Pressure from carriers / handset makers; strong competition

Australia Retail

David Jones Highly exposed to online sales leakage due to high prices

JB Hi-Fi High exposure to consumer electronics

Harvey Norman Minimal online presence; expected share loss

China Retail

Li Ning Focus on sportswear brand; lacks omni-channel strategy *MercadoLibre is covered by Scott Devitt. Source: AlphaWise, Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H

8

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

Summary of Key Takeaways:

United States

Internet

Key stock calls: Amazon, Blue Nile, eBay (best-positioned)

1. Over the next five years, logistics and fulfillment innovation should determine the level of disruption of traditional retail.

2. Structural and socioeconomic demographics determine the company-specific strategy an eCommerce retailer will have to lead with in a specific market; in the US, fulfillment is crucial.

3. Investments that improve an eCommerce retailer’s ability to offer low prices, broad selection and increased convenience will likely lead to higher sales growth, albeit at a potentially lower margin.

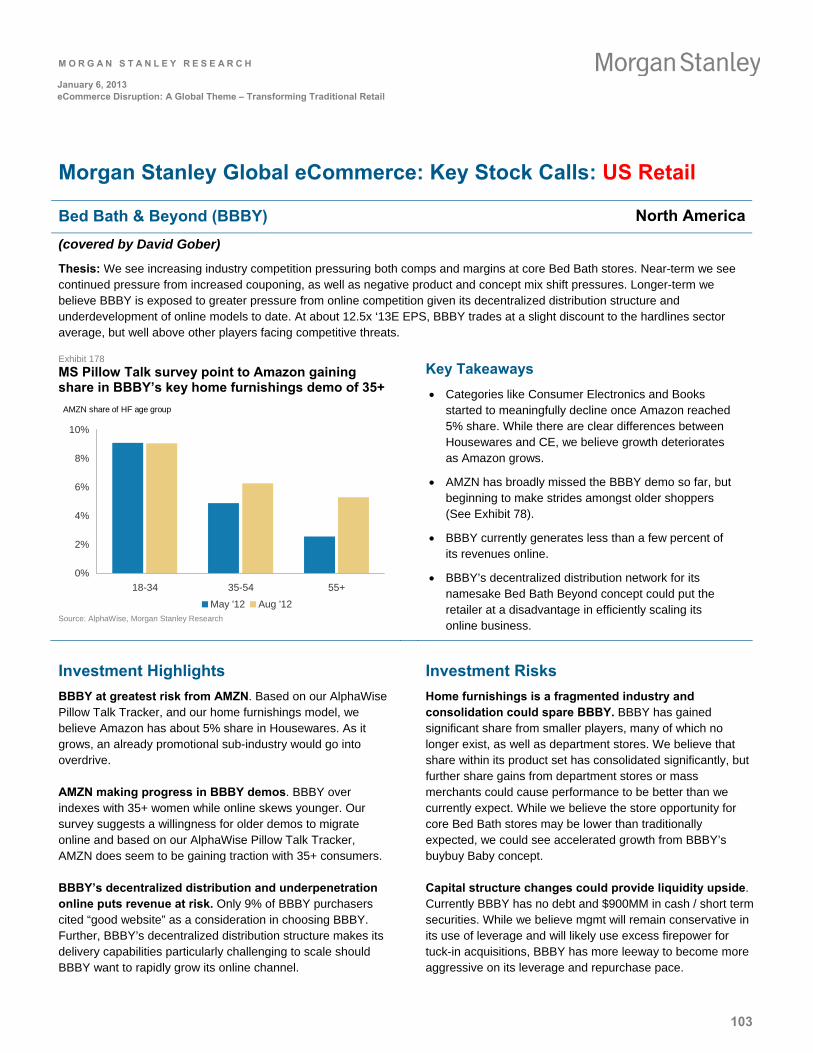

Retail – Hardlines

Key stock calls: Williams-Sonoma (best-positioned), and Bed Bath & Beyond and RadioShack (potentially challenged)

1. eCommerce penetration for the consumer electronics category is high (47%), and likely to keep increasing.

2. About 30% of home furnishings buyers shop online. Williams-Sonoma is well-positioned (33% of total sales online) while Bed Bath & Beyond is not, given 1% of revenue online, decentralized distribution, and high skew of branded, easily price-comparable products.

Retail – Branded Apparel

Key stock calls: Under Armour (best-positioned)

1. As brands control their own distribution, they remain largely insulated from typical pressures from pure online competition.

2. eCommerce provides a key means to enter markets internationally and elevate brand awareness with new users.

Retail – Softlines

Key stock calls: Macy’s, Nordstrom, and Urban Outfitters (best-positioned)

1. A secular shift towards eCommerce has compelled apparel retailers to develop, expand, and enhance their online platforms.

2. Softlines retail is one of the most defensible retail categories against online-only competition.

Retail – Food, Drug and Discounters

Key stock calls: Costco and Walmart (well-positioned)

1. Costco and the club stores can still thrive due to low prices and focus on perishables that are not easy to ship.

2. We believe Walmart has the potential to become a global leader in eCommerce sales, due to its buying power and ability to buy or build its way to a stronger competitive position.

M O R G A N S T A N L E Y R E S E A R C H

9

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

Western Europe

Retail

Key stock calls: ASOS (best-positioned)

1. Online penetration varies significantly across Western Europe. About 15% of non-food sales and 5% of food sales now occur online in the UK (one of the highest rates in the world), but in Southern Europe, online spending remains minimal.

2. "Click and Collect" services are proving very popular in both the UK and France, though it is not yet clear whether this is merely because these services are offered for free by most retailers.

3. The impact of the online shopping revolution in the UK goes well beyond the retail industry. It is beginning to have a profound impact on the property industry and, increasingly, on the very fabric of society.

Latin America

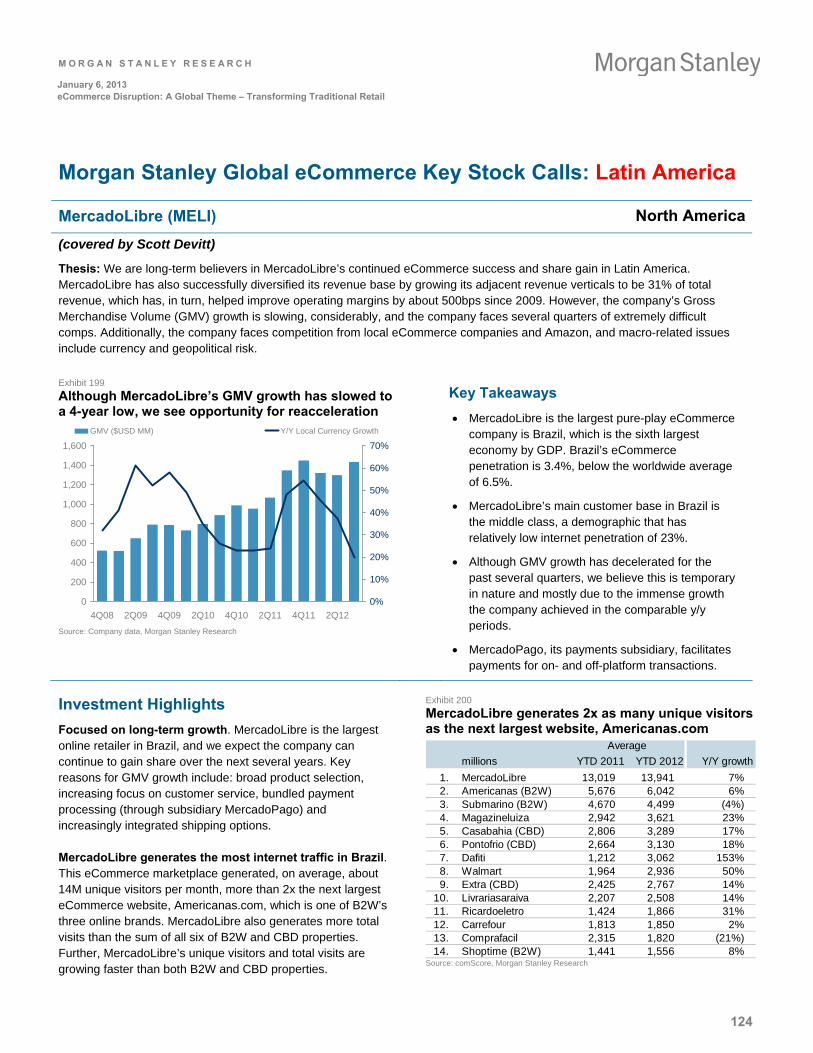

Internet and Retail

Key stock calls: MercadoLibre (best-positioned)

1. Growing middle class penetration should drive future eCommerce growth.

2. Price and convenience have been the main drivers of adoption so far; shipping, payment terms, and security can drive further growth.

3. High penetration of high-ticket electronics/appliances currently but significant room for growth in new lower-ticket categories.

4. Traditional linked retailers dominate eCommerce space in Brazil; core customers vary significantly by site.

M O R G A N S T A N L E Y R E S E A R C H

10

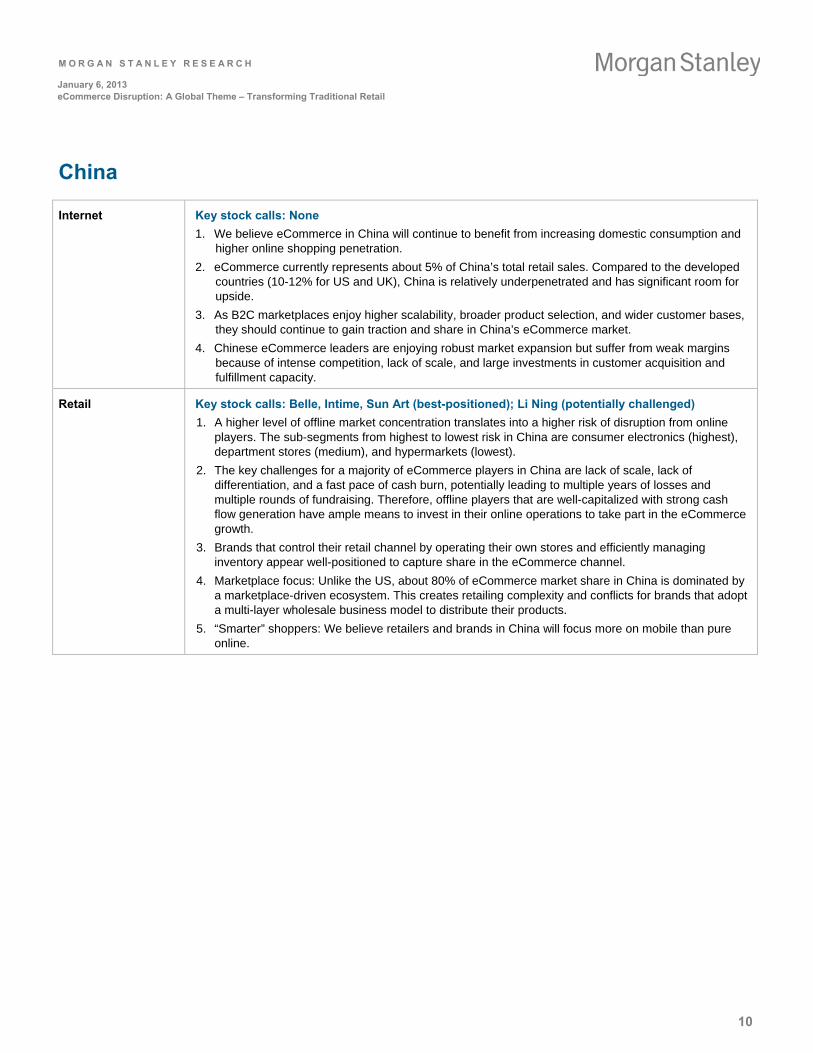

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

China

Internet

Key stock calls: None

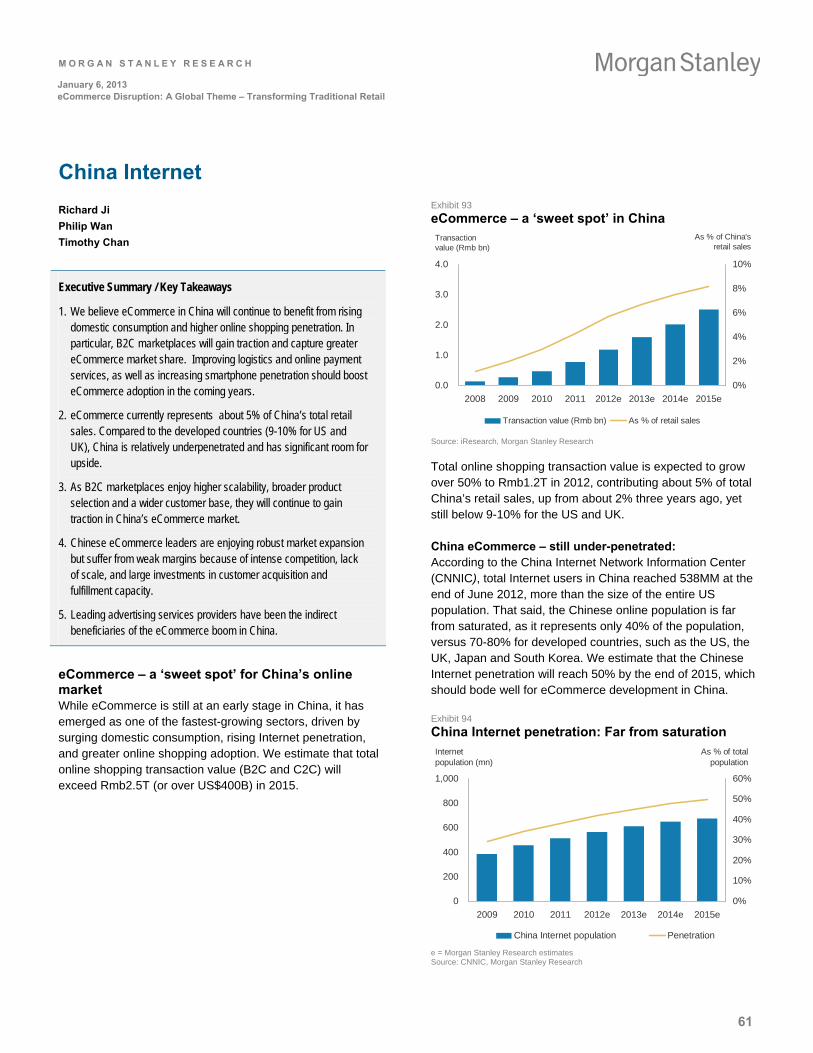

1. We believe eCommerce in China will continue to benefit from increasing domestic consumption and higher online shopping penetration.

2. eCommerce currently represents about 5% of China’s total retail sales. Compared to the developed countries (10-12% for US and UK), China is relatively underpenetrated and has significant room for upside.

3. As B2C marketplaces enjoy higher scalability, broader product selection, and wider customer bases, they should continue to gain traction and share in China’s eCommerce market.

4. Chinese eCommerce leaders are enjoying robust market expansion but suffer from weak margins because of intense competition, lack of scale, and large investments in customer acquisition and fulfillment capacity.

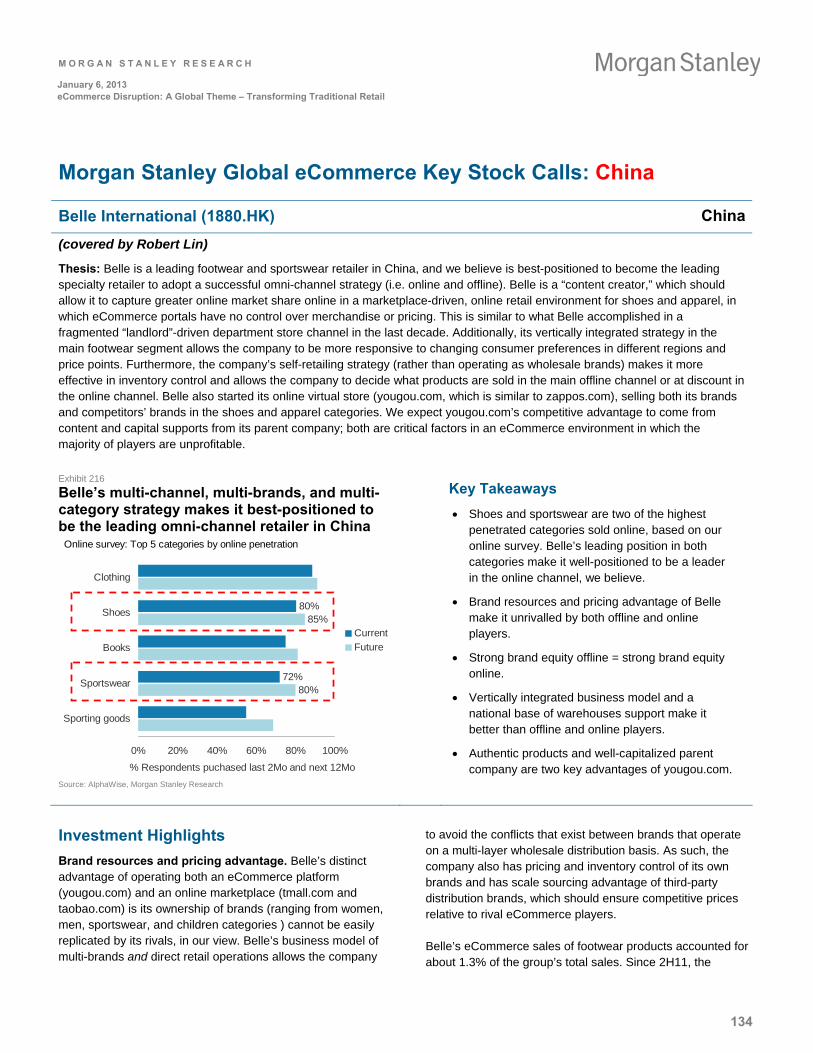

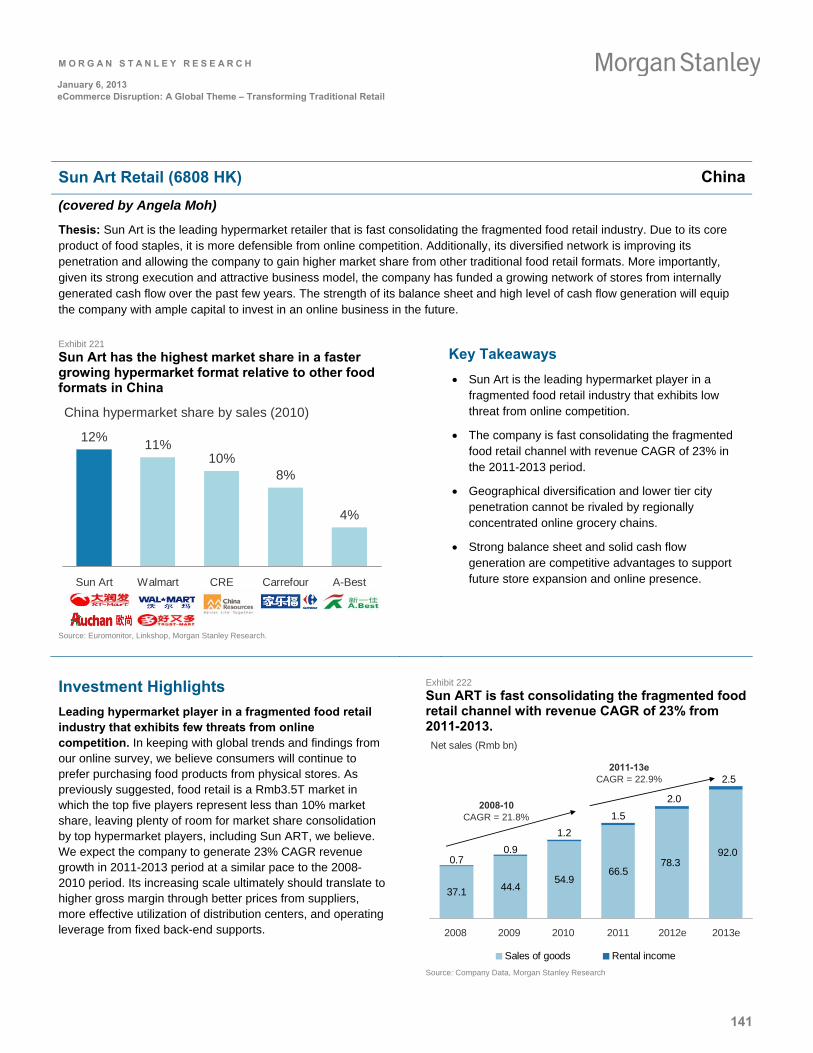

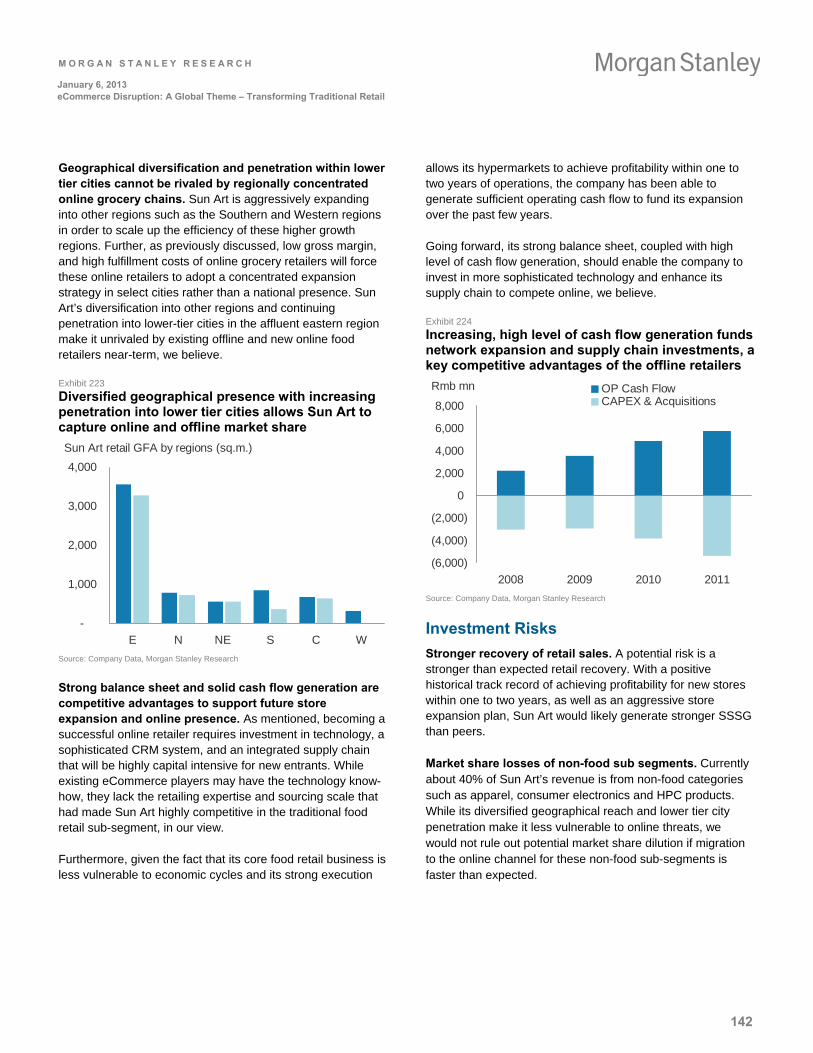

Retail Key stock calls: Belle, Intime, Sun Art (best-positioned); Li Ning (potentially challenged)

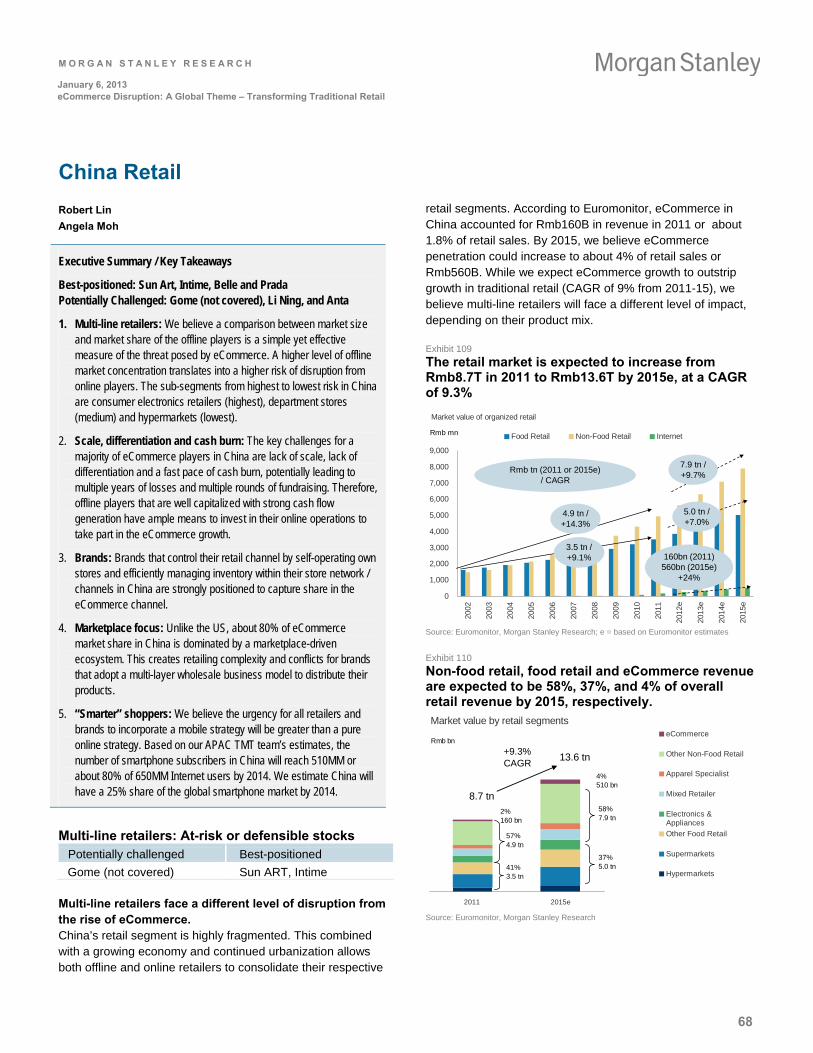

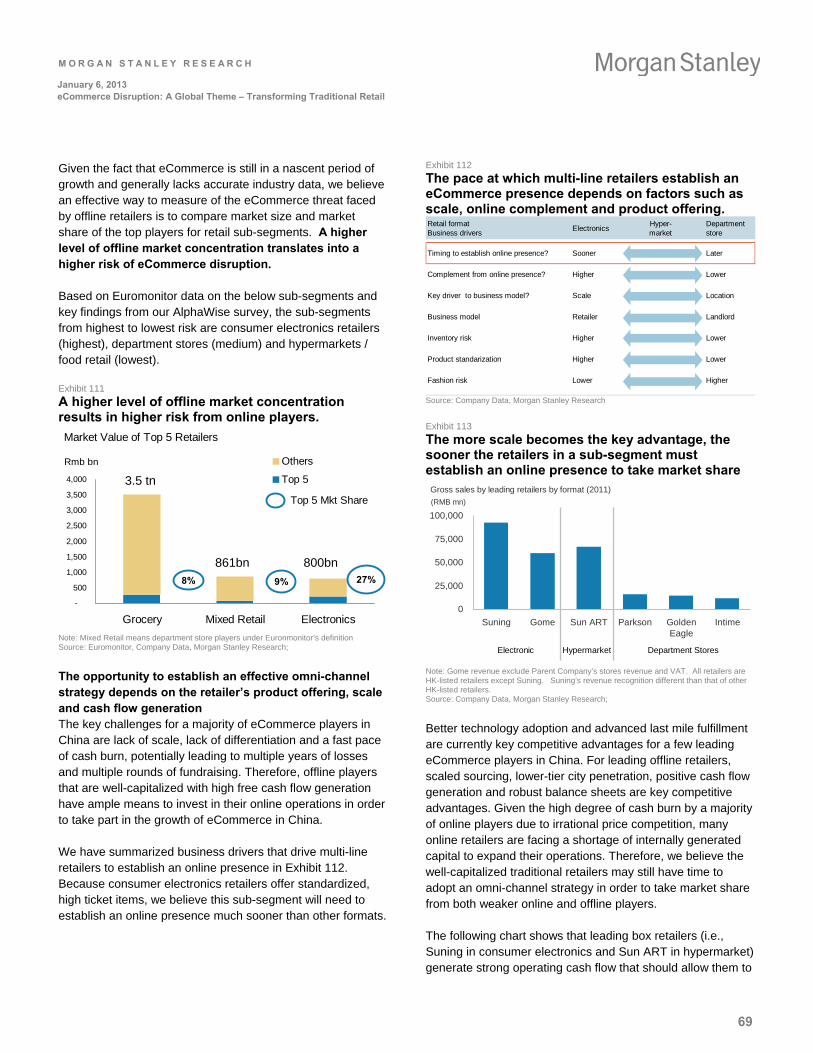

1. A higher level of offline market concentration translates into a higher risk of disruption from online players. The sub-segments from highest to lowest risk in China are consumer electronics (highest), department stores (medium), and hypermarkets (lowest).

2. The key challenges for a majority of eCommerce players in China are lack of scale, lack of differentiation, and a fast pace of cash burn, potentially leading to multiple years of losses and multiple rounds of fundraising. Therefore, offline players that are well-capitalized with strong cash flow generation have ample means to invest in their online operations to take part in the eCommerce growth.

3. Brands that control their retail channel by operating their own stores and efficiently managing inventory appear well-positioned to capture share in the eCommerce channel.

4. Marketplace focus: Unlike the US, about 80% of eCommerce market share in China is dominated by a marketplace-driven ecosystem. This creates retailing complexity and conflicts for brands that adopt a multi-layer wholesale business model to distribute their products.

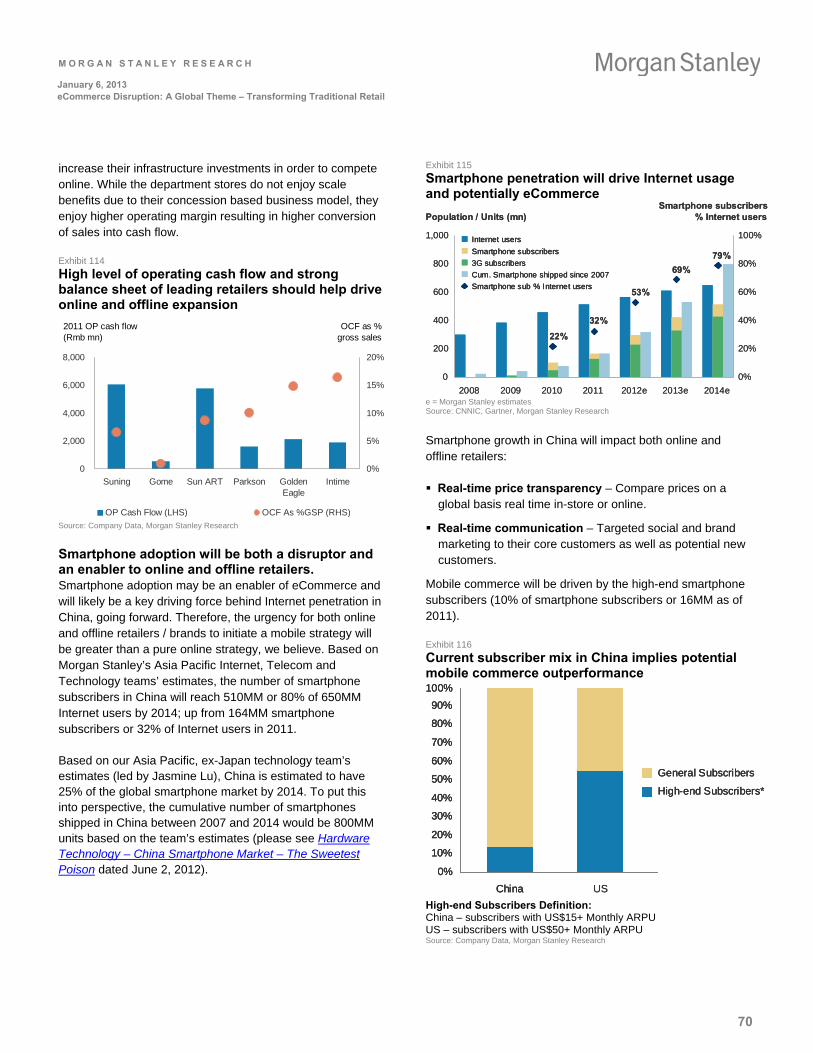

5. “Smarter” shoppers: We believe retailers and brands in China will focus more on mobile than pure online.

M O R G A N S T A N L E Y R E S E A R C H

11

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

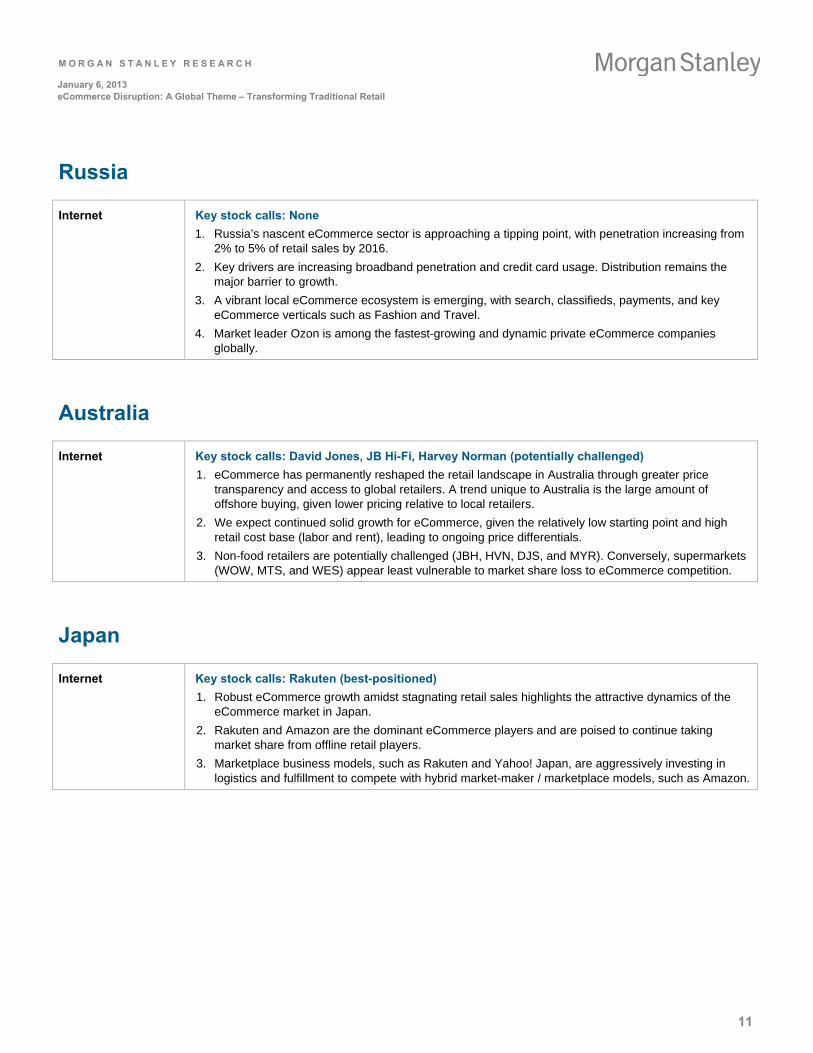

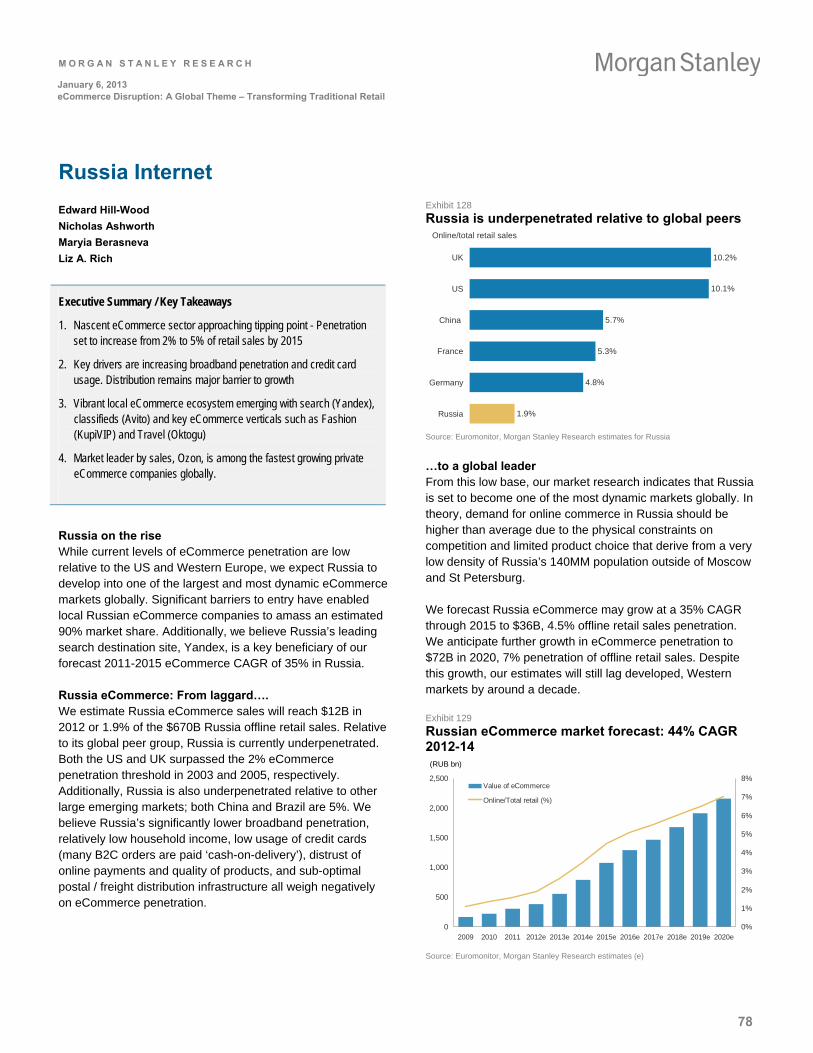

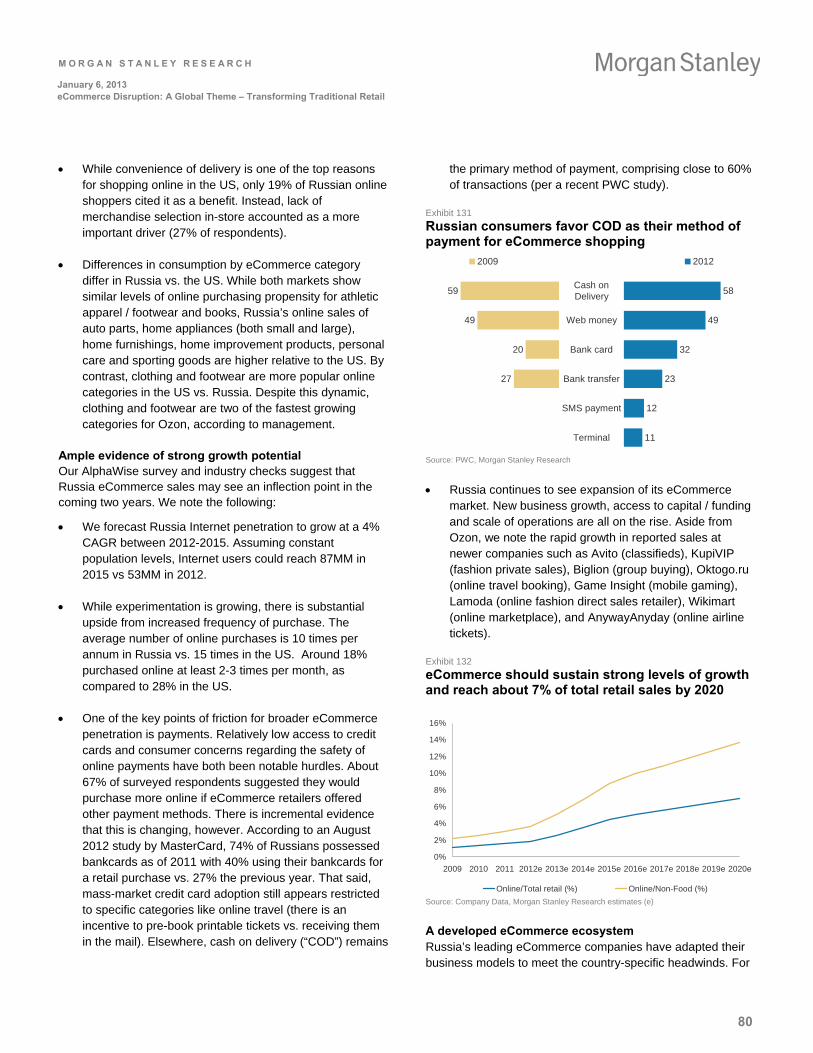

Russia

Internet

Key stock calls: None

1. Russia’s nascent eCommerce sector is approaching a tipping point, with penetration increasing from 2% to 5% of retail sales by 2016.

2. Key drivers are increasing broadband penetration and credit card usage. Distribution remains the major barrier to growth.

3. A vibrant local eCommerce ecosystem is emerging, with search, classifieds, payments, and key eCommerce verticals such as Fashion and Travel.

4. Market leader Ozon is among the fastest-growing and dynamic private eCommerce companies globally.

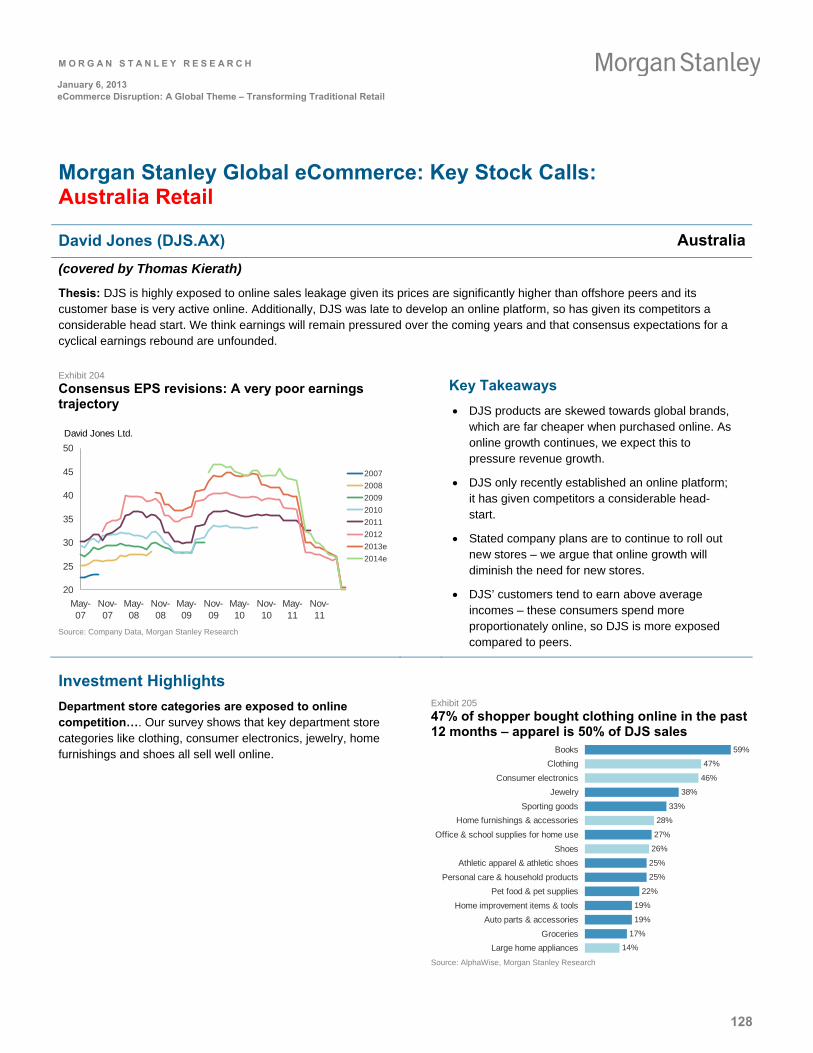

Australia

Internet

Key stock calls: David Jones, JB Hi-Fi, Harvey Norman (potentially challenged)

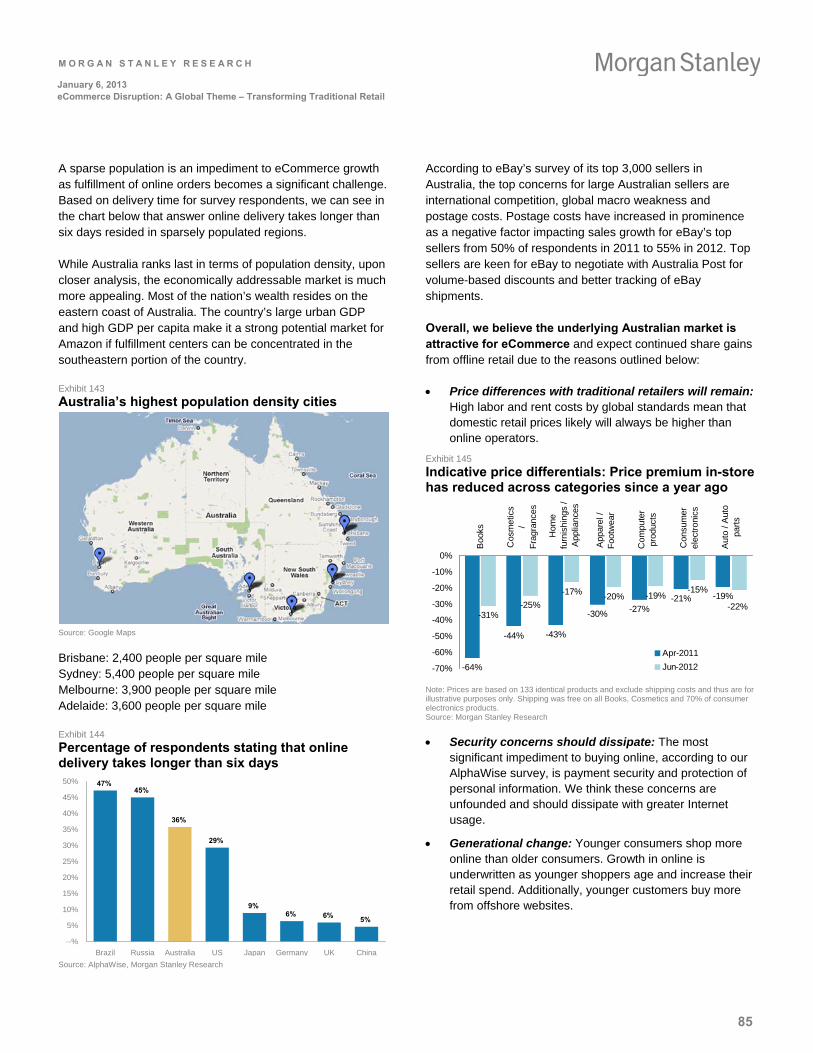

1. eCommerce has permanently reshaped the retail landscape in Australia through greater price transparency and access to global retailers. A trend unique to Australia is the large amount of offshore buying, given lower pricing relative to local retailers.

2. We expect continued solid growth for eCommerce, given the relatively low starting point and high retail cost base (labor and rent), leading to ongoing price differentials.

3. Non-food retailers are potentially challenged (JBH, HVN, DJS, and MYR). Conversely, supermarkets (WOW, MTS, and WES) appear least vulnerable to market share loss to eCommerce competition.

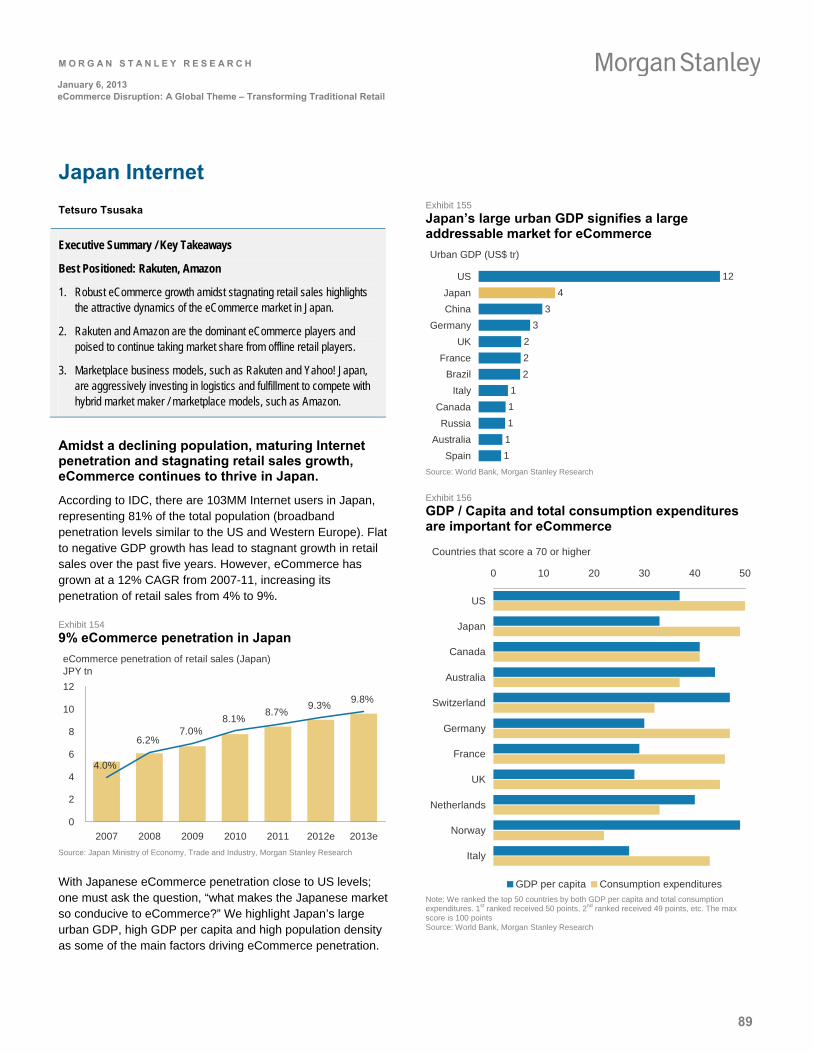

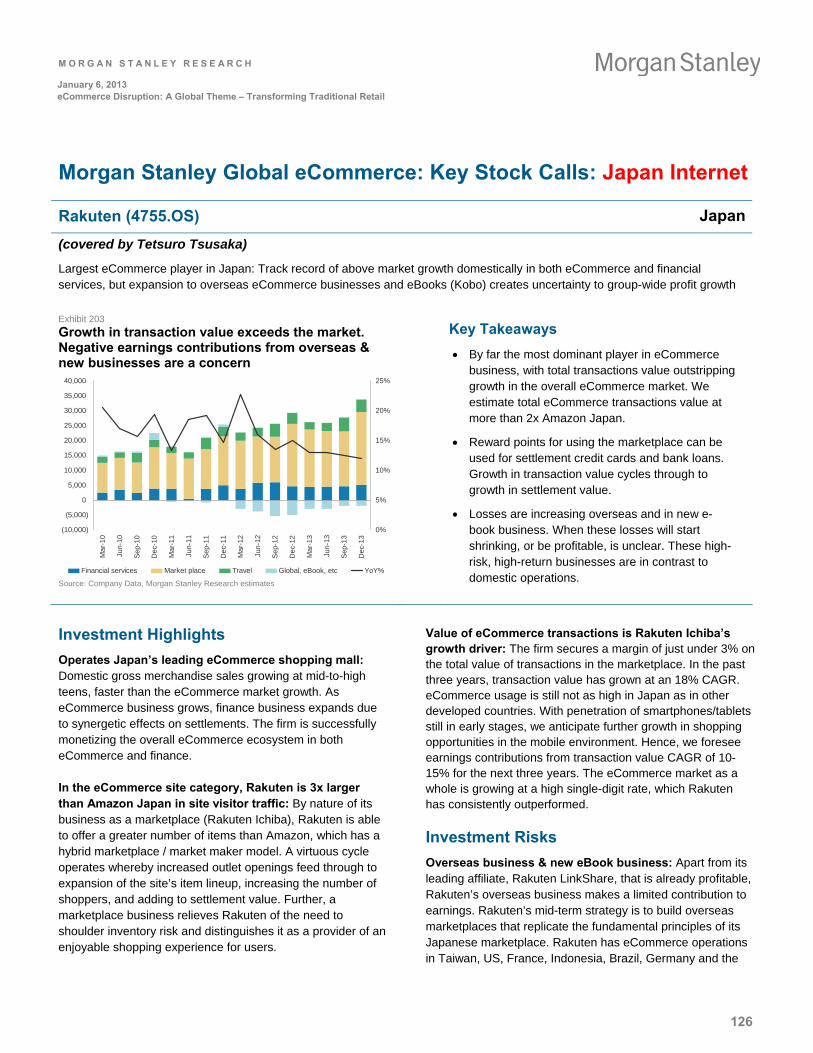

Japan

Internet

Key stock calls: Rakuten (best-positioned)

1. Robust eCommerce growth amidst stagnating retail sales highlights the attractive dynamics of the eCommerce market in Japan.

2. Rakuten and Amazon are the dominant eCommerce players and are poised to continue taking market share from offline retail players.

3. Marketplace business models, such as Rakuten and Yahoo! Japan, are aggressively investing in logistics and fulfillment to compete with hybrid market-maker / marketplace models, such as Amazon.

M O R G A N S T A N L E Y R E S E A R C H

12

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

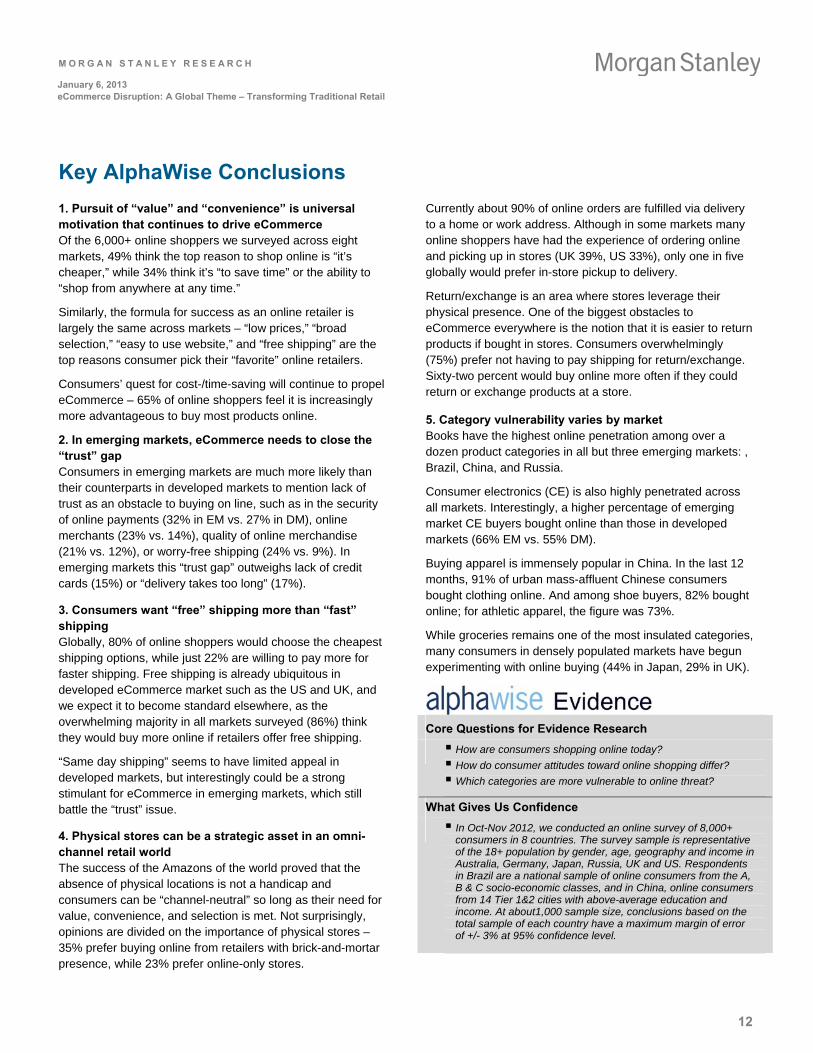

Key AlphaWise Conclusions

1. Pursuit of “value” and “convenience” is universal motivation that continues to drive eCommerce Of the 6,000+ online shoppers we surveyed across eight markets, 49% think the top reason to shop online is “it’s cheaper,” while 34% think it’s “to save time” or the ability to “shop from anywhere at any time.”

Similarly, the formula for success as an online retailer is largely the same across markets – “low prices,” “broad selection,” “easy to use website,” and “free shipping” are the top reasons consumer pick their “favorite” online retailers.

Consumers’ quest for cost-/time-saving will continue to propel eCommerce – 65% of online shoppers feel it is increasingly more advantageous to buy most products online.

2. In emerging markets, eCommerce needs to close the “trust” gap Consumers in emerging markets are much more likely than their counterparts in developed markets to mention lack of trust as an obstacle to buying on line, such as in the security of online payments (32% in EM vs. 27% in DM), online merchants (23% vs. 14%), quality of online merchandise (21% vs. 12%), or worry-free shipping (24% vs. 9%). In emerging markets this “trust gap” outweighs lack of credit cards (15%) or “delivery takes too long” (17%).

3. Consumers want “free” shipping more than “fast” shipping Globally, 80% of online shoppers would choose the cheapest shipping options, while just 22% are willing to pay more for faster shipping. Free shipping is already ubiquitous in developed eCommerce market such as the US and UK, and we expect it to become standard elsewhere, as the overwhelming majority in all markets surveyed (86%) think they would buy more online if retailers offer free shipping.

“Same day shipping” seems to have limited appeal in developed markets, but interestingly could be a strong stimulant for eCommerce in emerging markets, which still battle the “trust” issue.

4. Physical stores can be a strategic asset in an omni-channel retail world The success of the Amazons of the world proved that the absence of physical locations is not a handicap and consumers can be “channel-neutral” so long as their need for value, convenience, and selection is met. Not surprisingly, opinions are divided on the importance of physical stores – 35% prefer buying online from retailers with brick-and-mortar presence, while 23% prefer online-only stores.

Currently about 90% of online orders are fulfilled via delivery to a home or work address. Although in some markets many online shoppers have had the experience of ordering online and picking up in stores (UK 39%, US 33%), only one in five globally would prefer in-store pickup to delivery.

Return/exchange is an area where stores leverage their physical presence. One of the biggest obstacles to eCommerce everywhere is the notion that it is easier to return products if bought in stores. Consumers overwhelmingly (75%) prefer not having to pay shipping for return/exchange. Sixty-two percent would buy online more often if they could return or exchange products at a store.

5. Category vulnerability varies by market Books have the highest online penetration among over a dozen product categories in all but three emerging markets: , Brazil, China, and Russia.

Consumer electronics (CE) is also highly penetrated across all markets. Interestingly, a higher percentage of emerging market CE buyers bought online than those in developed markets (66% EM vs. 55% DM).

Buying apparel is immensely popular in China. In the last 12 months, 91% of urban mass-affluent Chinese consumers bought clothing online. And among shoe buyers, 82% bought online; for athletic apparel, the figure was 73%.

While groceries remains one of the most insulated categories, many consumers in densely populated markets have begun experimenting with online buying (44% in Japan, 29% in UK).

Core Questions for Evidence Research

How are consumers shopping online today?

How do consumer attitudes toward online shopping differ?

Which categories are more vulnerable to online threat?

What Gives Us Confidence

In Oct-Nov 2012, we conducted an online survey of 8,000+ consumers in 8 countries. The survey sample is representative of the 18+ population by gender, age, geography and income in Australia, Germany, Japan, Russia, UK and US. Respondents in Brazil are a national sample of online consumers from the A, B & C socio-economic classes, and in China, online consumers from 14 Tier 1&2 cities with above-average education and income. At about1,000 sample size, conclusions based on the total sample of each country have a maximum margin of error of +/- 3% at 95% confidence level.

M O R G A N S T A N L E Y R E S E A R C H

13

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

eCommerce Disruption: A Global Theme

Segment Analysis by Region

M O R G A N S T A N L E Y B L U E P A P E R

M O R G A N S T A N L E Y R E S E A R C H

14

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

US Internet

Scott Devitt

Andrew Ruud

Zachary Arrick

Nishant Verma

Executive Summary / Key Takeaways

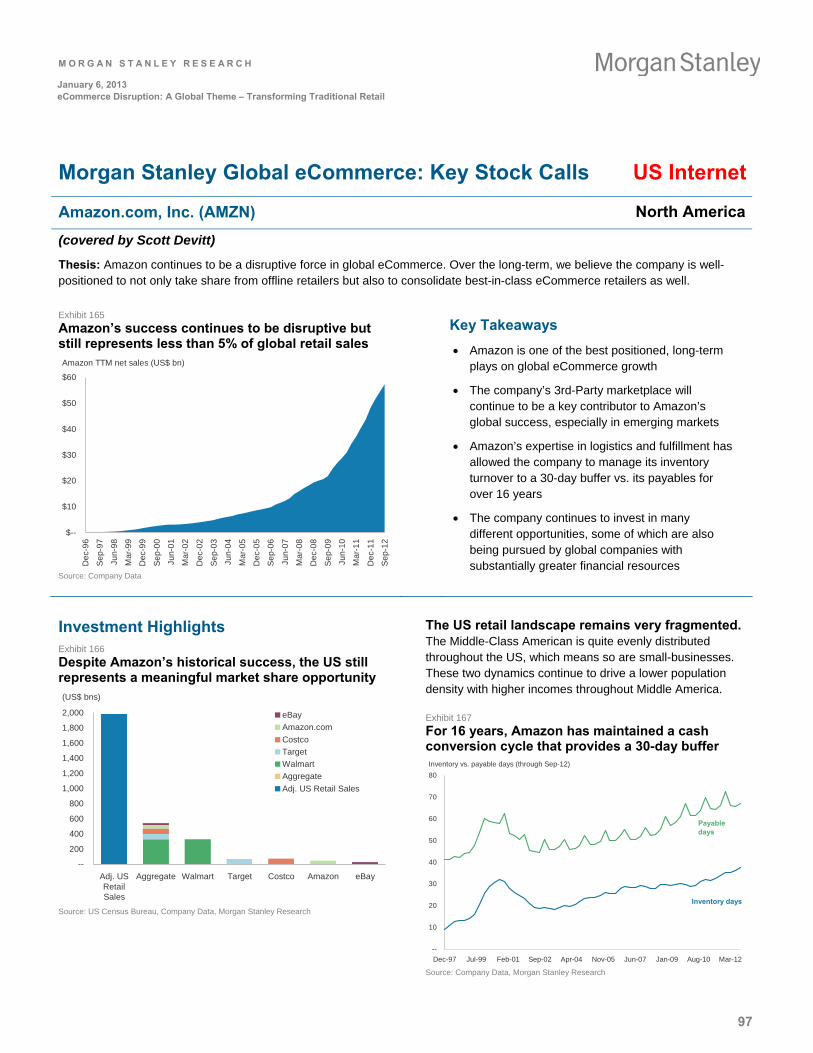

Best Positioned: Amazon, eBay, and Blue Nile

1. Over the next five years, logistics and fulfillment innovation will determine the level of disruption of traditional retail; Amazon is best-positioned to breakaway from competing traditional retailers and eCommerce players that do not have a vertically integrated fulfillment network.

2. Structural and socio-economic demographics predetermine the company-specific strategy an eCommerce retailer will have to lead with in a specific market; in the US, fulfillment is crucial.

3. Investments that improve an eCommerce retailer’s ability to offer low prices, broad selection and increased convenience will likely lead to higher sales growth; albeit at a potentially lower margin. Amazon has traditionally led the way – so far there has been no proof of any competing eCommerce or traditional retailer that is willing to do so at that level.

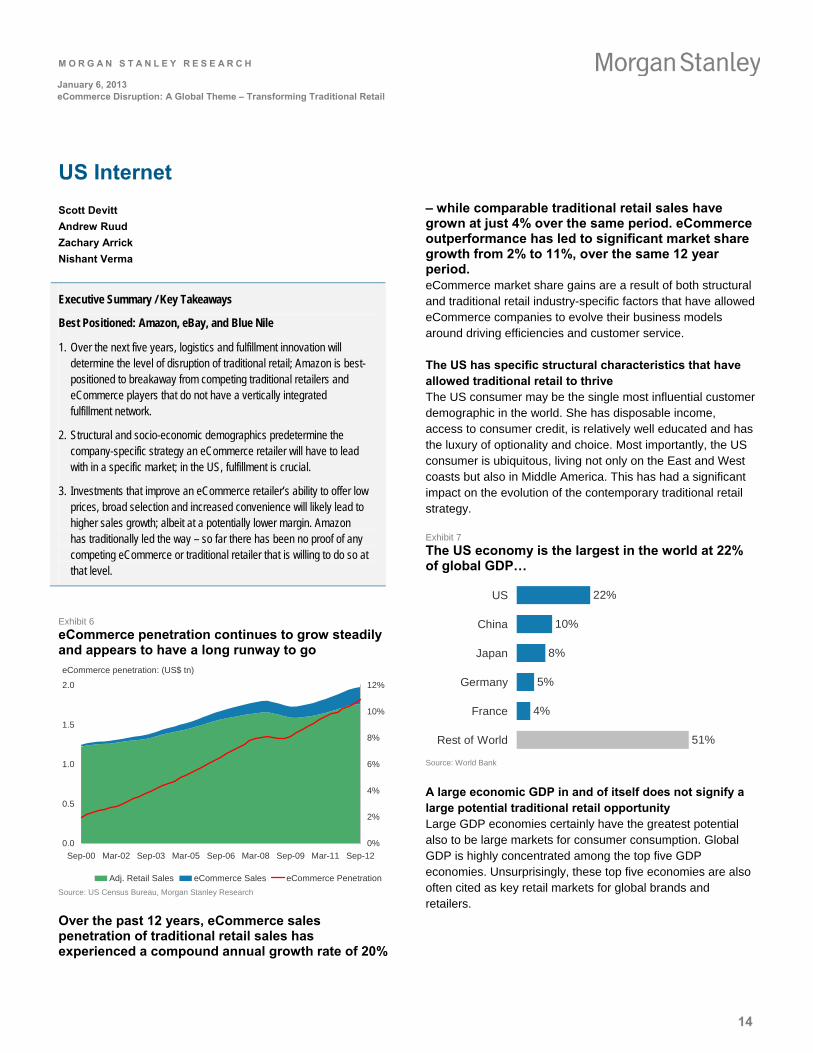

Exhibit 6

eCommerce penetration continues to grow steadily and appears to have a long runway to go

eCommerce penetration: (US$ tn)

0.0

0.5

1.0

1.5

2.0

Sep-00 Mar-02 Sep-03 Mar-05 Sep-06 Mar-08 Sep-09 Mar-11 Sep-12

0%

2%

4%

6%

8%

10%

12%

Adj. Retail Sales eCommerce Sales eCommerce Penetration Source: US Census Bureau, Morgan Stanley Research

Over the past 12 years, eCommerce sales penetration of traditional retail sales has experienced a compound annual growth rate of 20%

– while comparable traditional retail sales have grown at just 4% over the same period. eCommerce outperformance has led to significant market share growth from 2% to 11%, over the same 12 year period. eCommerce market share gains are a result of both structural and traditional retail industry-specific factors that have allowed eCommerce companies to evolve their business models around driving efficiencies and customer service.

The US has specific structural characteristics that have allowed traditional retail to thrive The US consumer may be the single most influential customer demographic in the world. She has disposable income, access to consumer credit, is relatively well educated and has the luxury of optionality and choice. Most importantly, the US consumer is ubiquitous, living not only on the East and West coasts but also in Middle America. This has had a significant impact on the evolution of the contemporary traditional retail strategy.

Exhibit 7

The US economy is the largest in the world at 22% of global GDP…

22%

10%

8%

5%

4%

51%

US

China

Japan

Germany

France

Rest of World

Source: World Bank

A large economic GDP in and of itself does not signify a large potential traditional retail opportunity Large GDP economies certainly have the greatest potential also to be large markets for consumer consumption. Global GDP is highly concentrated among the top five GDP economies. Unsurprisingly, these top five economies are also often cited as key retail markets for global brands and retailers.

M O R G A N S T A N L E Y R E S E A R C H

15

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

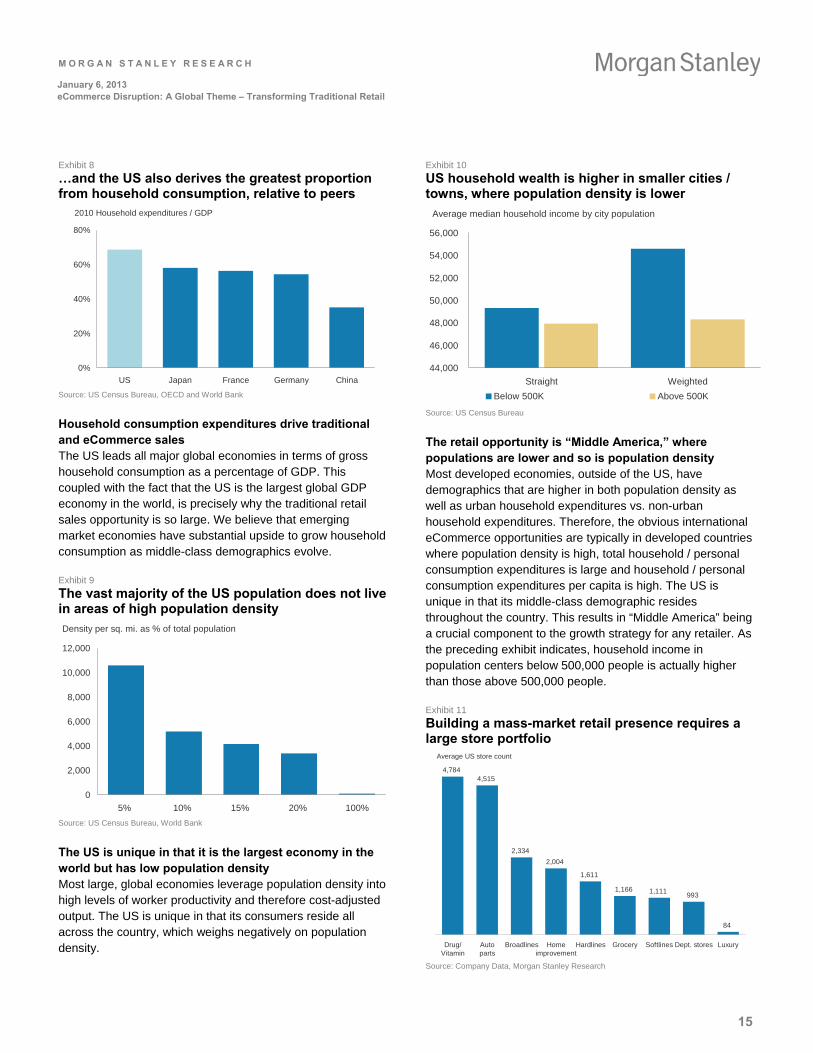

Exhibit 8

…and the US also derives the greatest proportion from household consumption, relative to peers

2010 Household expenditures / GDP

0%

20%

40%

60%

80%

US Japan France Germany China Source: US Census Bureau, OECD and World Bank

Household consumption expenditures drive traditional and eCommerce sales The US leads all major global economies in terms of gross household consumption as a percentage of GDP. This coupled with the fact that the US is the largest global GDP economy in the world, is precisely why the traditional retail sales opportunity is so large. We believe that emerging market economies have substantial upside to grow household consumption as middle-class demographics evolve.

Exhibit 9

The vast majority of the US population does not live in areas of high population density

Density per sq. mi. as % of total population

0

2,000

4,000

6,000

8,000

10,000

12,000

5% 10% 15% 20% 100% Source: US Census Bureau, World Bank

The US is unique in that it is the largest economy in the world but has low population density Most large, global economies leverage population density into high levels of worker productivity and therefore cost-adjusted output. The US is unique in that its consumers reside all across the country, which weighs negatively on population density.

Exhibit 10

US household wealth is higher in smaller cities / towns, where population density is lower

Average median household income by city population

44,000

46,000

48,000

50,000

52,000

54,000

56,000

Straight Weighted

Below 500K Above 500K

Source: US Census Bureau

The retail opportunity is “Middle America,” where populations are lower and so is population density Most developed economies, outside of the US, have demographics that are higher in both population density as well as urban household expenditures vs. non-urban household expenditures. Therefore, the obvious international eCommerce opportunities are typically in developed countries where population density is high, total household / personal consumption expenditures is large and household / personal consumption expenditures per capita is high. The US is unique in that its middle-class demographic resides throughout the country. This results in “Middle America” being a crucial component to the growth strategy for any retailer. As the preceding exhibit indicates, household income in population centers below 500,000 people is actually higher than those above 500,000 people.

Exhibit 11

Building a mass-market retail presence requires a large store portfolio

Average US store count

4,7844,515

2,334

2,004

1,611

1,166 1,111993

84

Drug/Vitamin

Autoparts

Broadlines Homeimprovement

Hardlines Grocery Softlines Dept. stores Luxury

Source: Company Data, Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H

16

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

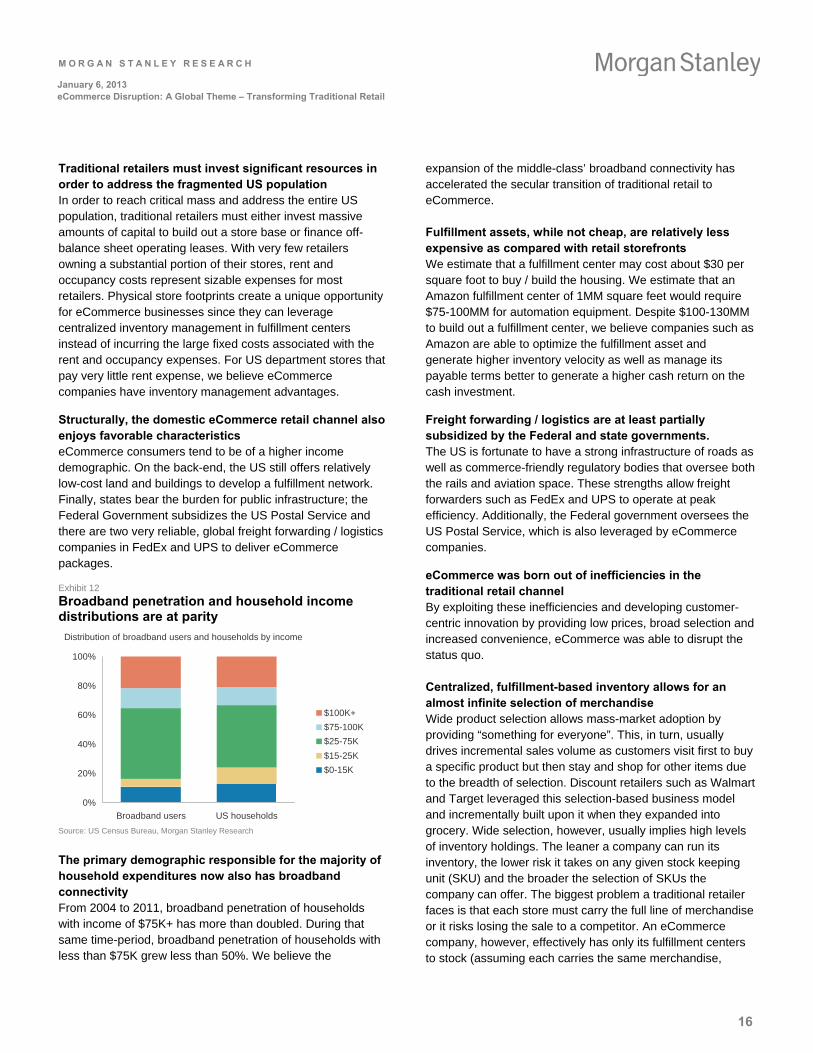

Traditional retailers must invest significant resources in order to address the fragmented US population In order to reach critical mass and address the entire US population, traditional retailers must either invest massive amounts of capital to build out a store base or finance off-balance sheet operating leases. With very few retailers owning a substantial portion of their stores, rent and occupancy costs represent sizable expenses for most retailers. Physical store footprints create a unique opportunity for eCommerce businesses since they can leverage centralized inventory management in fulfillment centers instead of incurring the large fixed costs associated with the rent and occupancy expenses. For US department stores that pay very little rent expense, we believe eCommerce companies have inventory management advantages.

Structurally, the domestic eCommerce retail channel also enjoys favorable characteristics eCommerce consumers tend to be of a higher income demographic. On the back-end, the US still offers relatively low-cost land and buildings to develop a fulfillment network. Finally, states bear the burden for public infrastructure; the Federal Government subsidizes the US Postal Service and there are two very reliable, global freight forwarding / logistics companies in FedEx and UPS to deliver eCommerce packages.

Exhibit 12

Broadband penetration and household income distributions are at parity

Distribution of broadband users and households by income

0%

20%

40%

60%

80%

100%

Broadband users US households

$100K+

$75-100K

$25-75K

$15-25K

$0-15K

Source: US Census Bureau, Morgan Stanley Research

The primary demographic responsible for the majority of household expenditures now also has broadband connectivity From 2004 to 2011, broadband penetration of households with income of $75K+ has more than doubled. During that same time-period, broadband penetration of households with less than $75K grew less than 50%. We believe the

expansion of the middle-class’ broadband connectivity has accelerated the secular transition of traditional retail to eCommerce.

Fulfillment assets, while not cheap, are relatively less expensive as compared with retail storefronts We estimate that a fulfillment center may cost about $30 per square foot to buy / build the housing. We estimate that an Amazon fulfillment center of 1MM square feet would require $75-100MM for automation equipment. Despite $100-130MM to build out a fulfillment center, we believe companies such as Amazon are able to optimize the fulfillment asset and generate higher inventory velocity as well as manage its payable terms better to generate a higher cash return on the cash investment.

Freight forwarding / logistics are at least partially subsidized by the Federal and state governments. The US is fortunate to have a strong infrastructure of roads as well as commerce-friendly regulatory bodies that oversee both the rails and aviation space. These strengths allow freight forwarders such as FedEx and UPS to operate at peak efficiency. Additionally, the Federal government oversees the US Postal Service, which is also leveraged by eCommerce companies.

eCommerce was born out of inefficiencies in the traditional retail channel By exploiting these inefficiencies and developing customer-centric innovation by providing low prices, broad selection and increased convenience, eCommerce was able to disrupt the status quo.

Centralized, fulfillment-based inventory allows for an almost infinite selection of merchandise Wide product selection allows mass-market adoption by providing “something for everyone”. This, in turn, usually drives incremental sales volume as customers visit first to buy a specific product but then stay and shop for other items due to the breadth of selection. Discount retailers such as Walmart and Target leveraged this selection-based business model and incrementally built upon it when they expanded into grocery. Wide selection, however, usually implies high levels of inventory holdings. The leaner a company can run its inventory, the lower risk it takes on any given stock keeping unit (SKU) and the broader the selection of SKUs the company can offer. The biggest problem a traditional retailer faces is that each store must carry the full line of merchandise or it risks losing the sale to a competitor. An eCommerce company, however, effectively has only its fulfillment centers to stock (assuming each carries the same merchandise,

M O R G A N S T A N L E Y R E S E A R C H

17

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

which is often not the case). Amazon operates the largest domestic fulfillment network, by far, totaling 30-35 fulfillment centers. By comparison, the average discount retailer has about 2,000 stores.

Exhibit 13

Amazon’s centralized inventory appears to drive more efficiencies vs. Target’s decentralized model Inventory turnover (through FQ3:2012)

--x

5x

10x

15x

20x

25x

30x

35x

40x

45x

1997 1999 2000 2002 2003 2005 2006 2008 2009 2011

Amazon Target Source: Company Data, Morgan Stanley Research

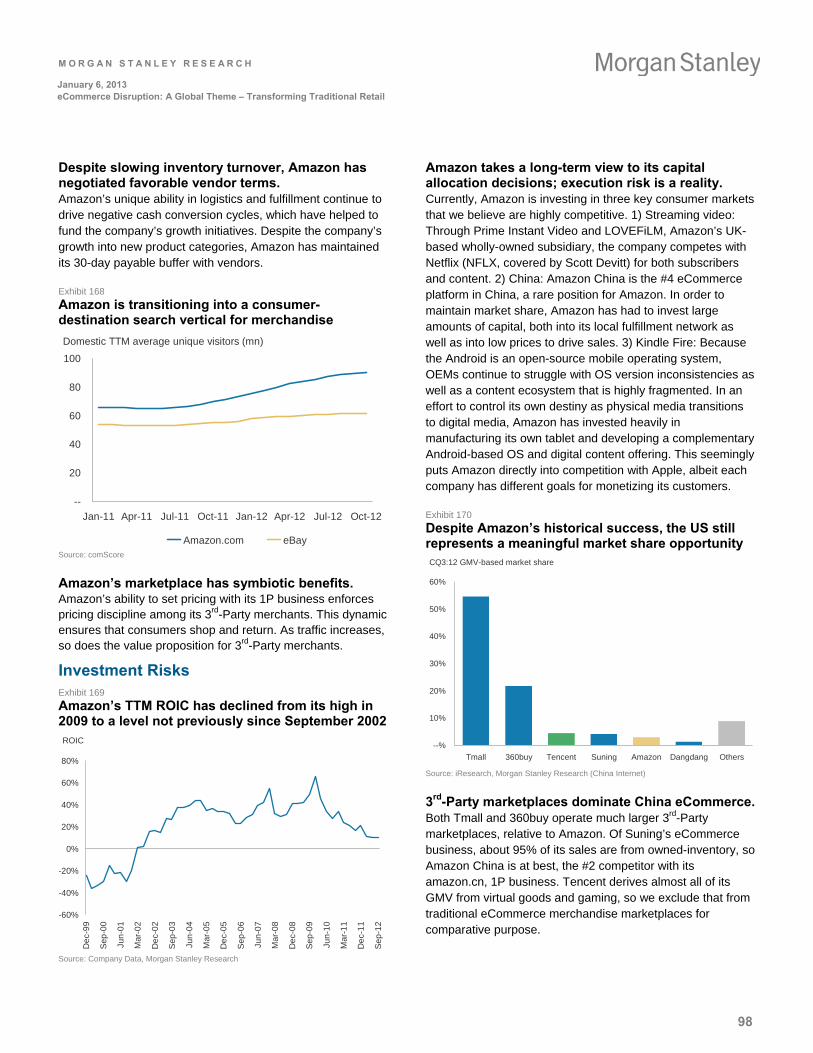

Amazon has enjoyed high inventory velocity over time, but “growing pains” are evident It is difficult to argue against Amazon’s ability to drive inventory management efficiencies through its fulfillment network. The chart above compares Amazon to one of the more efficient discount retailers in the US, Target. One cannot help but notice the degradation in inventory turnover through the course of Amazon’s reported history. We do not believe this is in and of itself a bad thing; in fact, we see this as a natural side effect of the company growing into a broader set of product verticals. Going forward, we expect Amazon’s inventory turnover to stabilize or even inflect upward as the company continues to build fulfillment centers closer to the end-customer.

Best-in-class eCommerce retailers tend to generate cash through negative cash conversion cycles Because of their relatively fewer fulfillment centers (vs. retail stores) and the benefits of centralized inventory, eCommerce retailers have the opportunity to generate very high levels of inventory velocity while maintaining comparable payment terms to those of a traditional retailer. If managed correctly, this can generate a positive cash float that increases so long as sales growth continues and the spread between inventory and payable days stays negative (days inventory, minus days payable).

Exhibit 14

Amazon’s working capital spread, measured in days, has been extremely stable for over 15 years Inventory vs. payable days (through Sep-12)

--

10

20

30

40

50

60

70

80

Dec-97 Jul-99 Feb-01 Sep-02 Apr-04 Nov-05 Jun-07 Jan-09 Aug-10 Mar-12

Payable days

Inventory days

Source: Company Data

Amazon has negotiated favorable payment terms, offsetting the inventory-related “growing pains” Despite inventory turns declining over time, it is apparent that the company does not necessarily manage to working capital metrics, but rather to a level of operating risk management. For over 15 years, Amazon has consistently managed its cash conversion cycle to a negative 30 days. We believe investors and business operators alike would be hard-pressed to find another example of such a stable cash conversion cycle for over 15 years, given the level of growth the company experienced in that timeframe.

eCommerce is not limited to owned-inventory models; third-party marketplaces also succeed It is economically impractical for an eCommerce retailer to always have every SKU in stock. A third-party marketplace allows an eCommerce company to “carry” an infinitely scalable selection of merchandise and may operate as a standalone business in the case of eBay or a complementary business in the case of Amazon.

M O R G A N S T A N L E Y R E S E A R C H

18

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

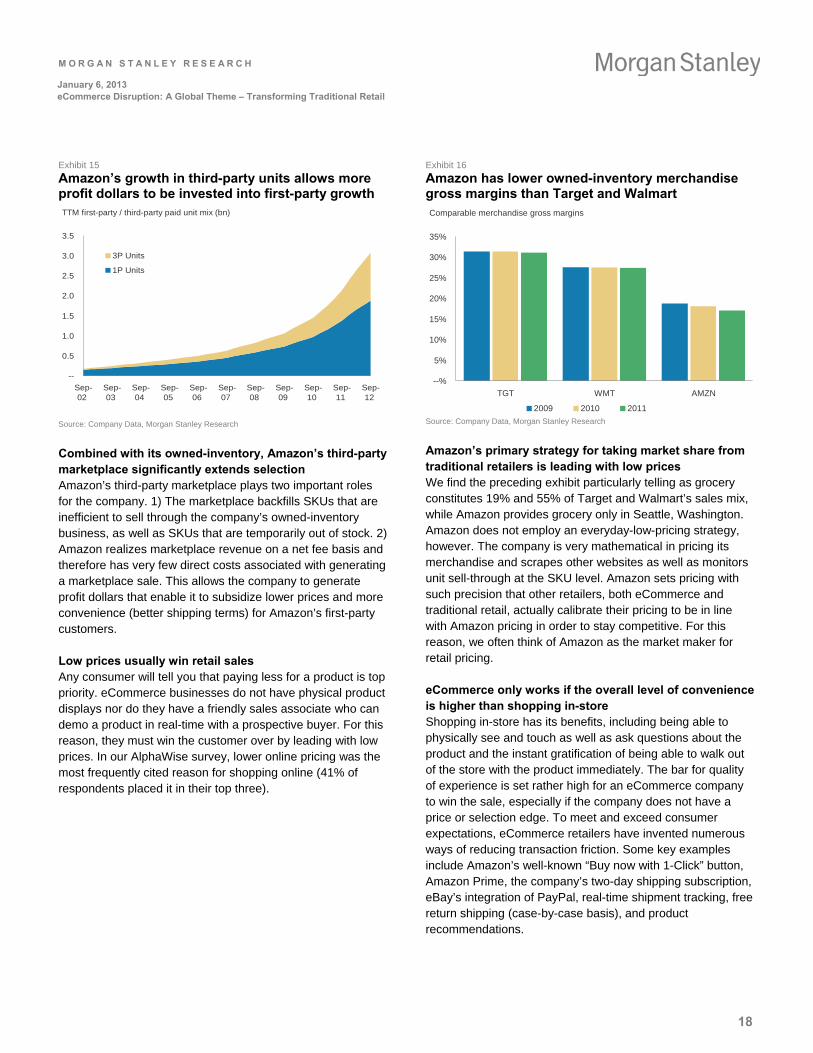

Exhibit 15

Amazon’s growth in third-party units allows more profit dollars to be invested into first-party growth TTM first-party / third-party paid unit mix (bn)

--

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Sep-02

Sep-03

Sep-04

Sep-05

Sep-06

Sep-07

Sep-08

Sep-09

Sep-10

Sep-11

Sep-12

3P Units

1P Units

Source: Company Data, Morgan Stanley Research

Combined with its owned-inventory, Amazon’s third-party marketplace significantly extends selection Amazon’s third-party marketplace plays two important roles for the company. 1) The marketplace backfills SKUs that are inefficient to sell through the company’s owned-inventory business, as well as SKUs that are temporarily out of stock. 2) Amazon realizes marketplace revenue on a net fee basis and therefore has very few direct costs associated with generating a marketplace sale. This allows the company to generate profit dollars that enable it to subsidize lower prices and more convenience (better shipping terms) for Amazon’s first-party customers.

Low prices usually win retail sales Any consumer will tell you that paying less for a product is top priority. eCommerce businesses do not have physical product displays nor do they have a friendly sales associate who can demo a product in real-time with a prospective buyer. For this reason, they must win the customer over by leading with low prices. In our AlphaWise survey, lower online pricing was the most frequently cited reason for shopping online (41% of respondents placed it in their top three).

Exhibit 16

Amazon has lower owned-inventory merchandise gross margins than Target and Walmart Comparable merchandise gross margins

--%

5%

10%

15%

20%

25%

30%

35%

TGT WMT AMZN

2009 2010 2011 Source: Company Data, Morgan Stanley Research

Amazon’s primary strategy for taking market share from traditional retailers is leading with low prices We find the preceding exhibit particularly telling as grocery constitutes 19% and 55% of Target and Walmart’s sales mix, while Amazon provides grocery only in Seattle, Washington. Amazon does not employ an everyday-low-pricing strategy, however. The company is very mathematical in pricing its merchandise and scrapes other websites as well as monitors unit sell-through at the SKU level. Amazon sets pricing with such precision that other retailers, both eCommerce and traditional retail, actually calibrate their pricing to be in line with Amazon pricing in order to stay competitive. For this reason, we often think of Amazon as the market maker for retail pricing.

eCommerce only works if the overall level of convenience is higher than shopping in-store Shopping in-store has its benefits, including being able to physically see and touch as well as ask questions about the product and the instant gratification of being able to walk out of the store with the product immediately. The bar for quality of experience is set rather high for an eCommerce company to win the sale, especially if the company does not have a price or selection edge. To meet and exceed consumer expectations, eCommerce retailers have invented numerous ways of reducing transaction friction. Some key examples include Amazon’s well-known “Buy now with 1-Click” button, Amazon Prime, the company’s two-day shipping subscription, eBay’s integration of PayPal, real-time shipment tracking, free return shipping (case-by-case basis), and product recommendations.

M O R G A N S T A N L E Y R E S E A R C H

19

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

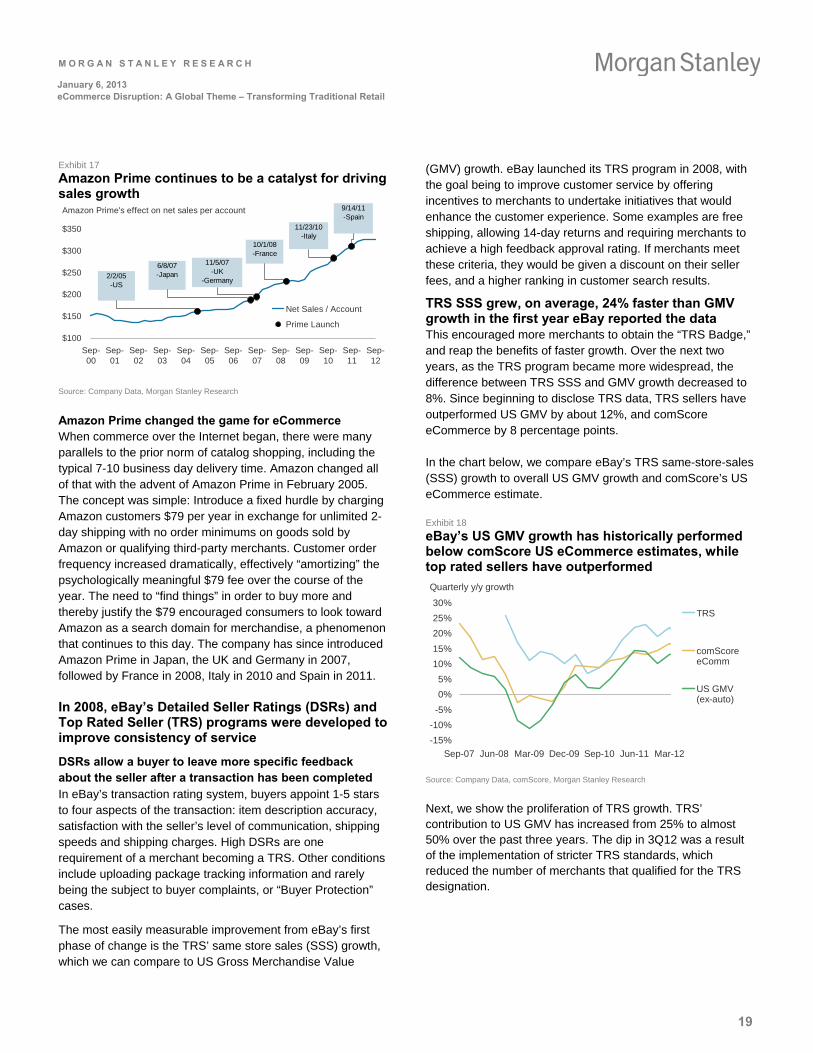

Exhibit 17

Amazon Prime continues to be a catalyst for driving sales growth Amazon Prime's effect on net sales per account

$100

$150

$200

$250

$300

$350

Sep-00

Sep-01

Sep-02

Sep-03

Sep-04

Sep-05

Sep-06

Sep-07

Sep-08

Sep-09

Sep-10

Sep-11

Sep-12

Net Sales / Account

Prime Launch

2/2/05-US

6/8/07-Japan

11/5/07-UK

-Germany

10/1/08-France

11/23/10-Italy

9/14/11-Spain

Source: Company Data, Morgan Stanley Research

Amazon Prime changed the game for eCommerce When commerce over the Internet began, there were many parallels to the prior norm of catalog shopping, including the typical 7-10 business day delivery time. Amazon changed all of that with the advent of Amazon Prime in February 2005. The concept was simple: Introduce a fixed hurdle by charging Amazon customers $79 per year in exchange for unlimited 2-day shipping with no order minimums on goods sold by Amazon or qualifying third-party merchants. Customer order frequency increased dramatically, effectively “amortizing” the psychologically meaningful $79 fee over the course of the year. The need to “find things” in order to buy more and thereby justify the $79 encouraged consumers to look toward Amazon as a search domain for merchandise, a phenomenon that continues to this day. The company has since introduced Amazon Prime in Japan, the UK and Germany in 2007, followed by France in 2008, Italy in 2010 and Spain in 2011.

In 2008, eBay’s Detailed Seller Ratings (DSRs) and Top Rated Seller (TRS) programs were developed to improve consistency of service

DSRs allow a buyer to leave more specific feedback about the seller after a transaction has been completed In eBay’s transaction rating system, buyers appoint 1-5 stars to four aspects of the transaction: item description accuracy, satisfaction with the seller’s level of communication, shipping speeds and shipping charges. High DSRs are one requirement of a merchant becoming a TRS. Other conditions include uploading package tracking information and rarely being the subject to buyer complaints, or “Buyer Protection” cases.

The most easily measurable improvement from eBay’s first phase of change is the TRS’ same store sales (SSS) growth, which we can compare to US Gross Merchandise Value

(GMV) growth. eBay launched its TRS program in 2008, with the goal being to improve customer service by offering incentives to merchants to undertake initiatives that would enhance the customer experience. Some examples are free shipping, allowing 14-day returns and requiring merchants to achieve a high feedback approval rating. If merchants meet these criteria, they would be given a discount on their seller fees, and a higher ranking in customer search results.

TRS SSS grew, on average, 24% faster than GMV growth in the first year eBay reported the data This encouraged more merchants to obtain the “TRS Badge,” and reap the benefits of faster growth. Over the next two years, as the TRS program became more widespread, the difference between TRS SSS and GMV growth decreased to 8%. Since beginning to disclose TRS data, TRS sellers have outperformed US GMV by about 12%, and comScore eCommerce by 8 percentage points.

In the chart below, we compare eBay’s TRS same-store-sales (SSS) growth to overall US GMV growth and comScore’s US eCommerce estimate.

Exhibit 18

eBay’s US GMV growth has historically performed below comScore US eCommerce estimates, while top rated sellers have outperformed

Quarterly y/y growth

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Sep-07 Jun-08 Mar-09 Dec-09 Sep-10 Jun-11 Mar-12

TRS

comScoreeComm

US GMV(ex-auto)

Source: Company Data, comScore, Morgan Stanley Research

Next, we show the proliferation of TRS growth. TRS’ contribution to US GMV has increased from 25% to almost 50% over the past three years. The dip in 3Q12 was a result of the implementation of stricter TRS standards, which reduced the number of merchants that qualified for the TRS designation.

M O R G A N S T A N L E Y R E S E A R C H

20

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

Exhibit 19

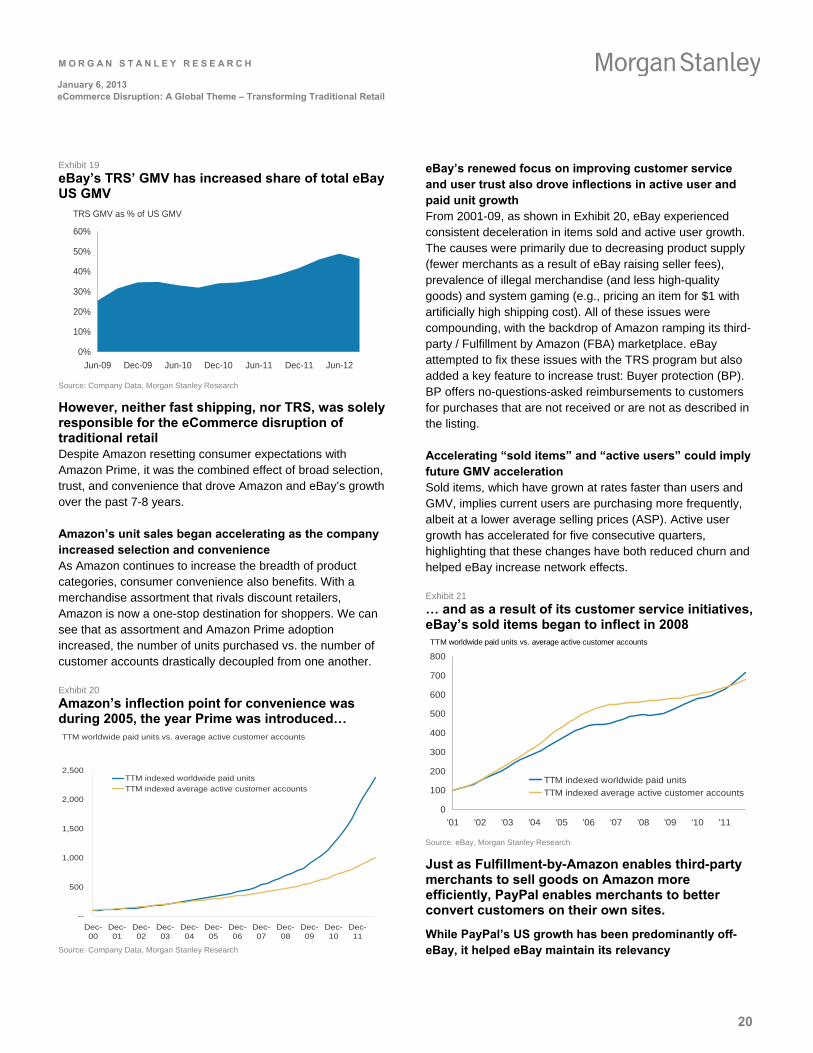

eBay’s TRS’ GMV has increased share of total eBay US GMV

TRS GMV as % of US GMV

0%

10%

20%

30%

40%

50%

60%

Jun-09 Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 Jun-12

Source: Company Data, Morgan Stanley Research

However, neither fast shipping, nor TRS, was solely responsible for the eCommerce disruption of traditional retail Despite Amazon resetting consumer expectations with Amazon Prime, it was the combined effect of broad selection, trust, and convenience that drove Amazon and eBay’s growth over the past 7-8 years.

Amazon’s unit sales began accelerating as the company increased selection and convenience As Amazon continues to increase the breadth of product categories, consumer convenience also benefits. With a merchandise assortment that rivals discount retailers, Amazon is now a one-stop destination for shoppers. We can see that as assortment and Amazon Prime adoption increased, the number of units purchased vs. the number of customer accounts drastically decoupled from one another.

Exhibit 20

Amazon’s inflection point for convenience was during 2005, the year Prime was introduced… TTM worldwide paid units vs. average active customer accounts

--

500

1,000

1,500

2,000

2,500

Dec-00

Dec-01

Dec-02

Dec-03

Dec-04

Dec-05

Dec-06

Dec-07

Dec-08

Dec-09

Dec-10

Dec-11

TTM indexed worldwide paid units

TTM indexed average active customer accounts

Source: Company Data, Morgan Stanley Research

eBay’s renewed focus on improving customer service and user trust also drove inflections in active user and paid unit growth From 2001-09, as shown in Exhibit 20, eBay experienced consistent deceleration in items sold and active user growth. The causes were primarily due to decreasing product supply (fewer merchants as a result of eBay raising seller fees), prevalence of illegal merchandise (and less high-quality goods) and system gaming (e.g., pricing an item for $1 with artificially high shipping cost). All of these issues were compounding, with the backdrop of Amazon ramping its third-party / Fulfillment by Amazon (FBA) marketplace. eBay attempted to fix these issues with the TRS program but also added a key feature to increase trust: Buyer protection (BP). BP offers no-questions-asked reimbursements to customers for purchases that are not received or are not as described in the listing.

Accelerating “sold items” and “active users” could imply future GMV acceleration Sold items, which have grown at rates faster than users and GMV, implies current users are purchasing more frequently, albeit at a lower average selling prices (ASP). Active user growth has accelerated for five consecutive quarters, highlighting that these changes have both reduced churn and helped eBay increase network effects.

Exhibit 21

… and as a result of its customer service initiatives, eBay’s sold items began to inflect in 2008

0

100

200

300

400

500

600

700

800

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11

TTM indexed worldwide paid units

TTM indexed average active customer accounts

TTM worldwide paid units vs. average active customer accounts

Source: eBay, Morgan Stanley Research

Just as Fulfillment-by-Amazon enables third-party merchants to sell goods on Amazon more efficiently, PayPal enables merchants to better convert customers on their own sites.

While PayPal’s US growth has been predominantly off-eBay, it helped eBay maintain its relevancy

M O R G A N S T A N L E Y R E S E A R C H

21

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

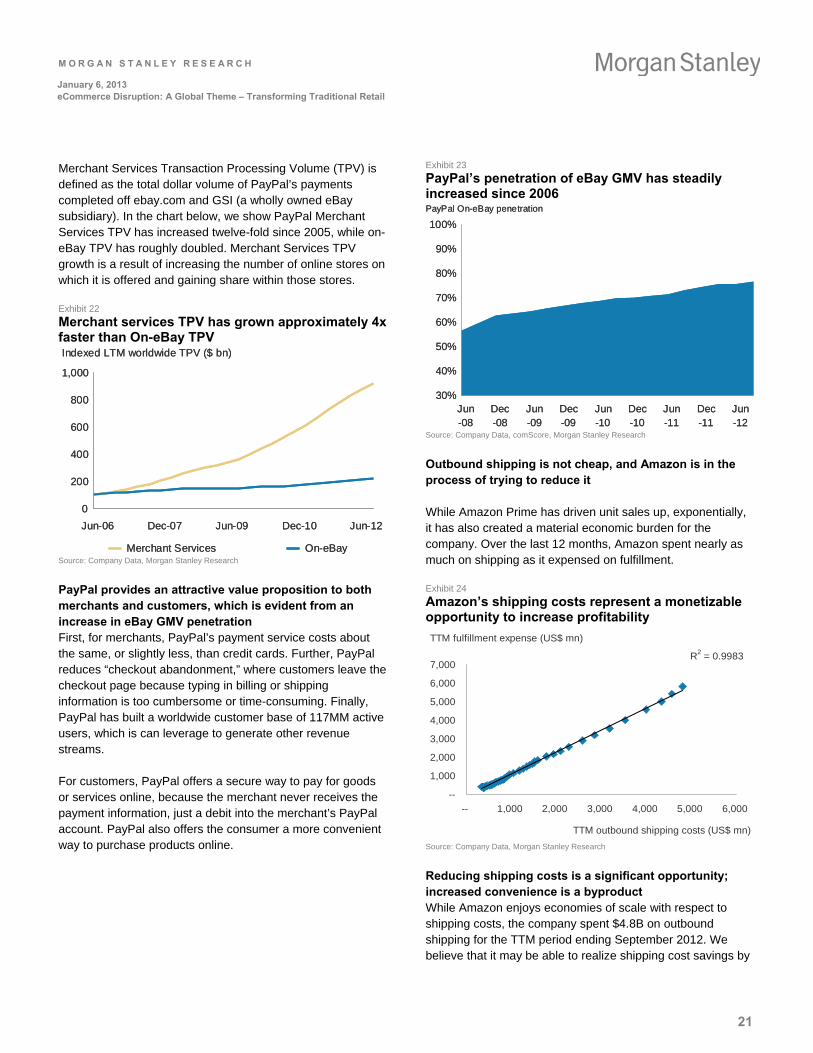

Merchant Services Transaction Processing Volume (TPV) is defined as the total dollar volume of PayPal’s payments completed off ebay.com and GSI (a wholly owned eBay subsidiary). In the chart below, we show PayPal Merchant Services TPV has increased twelve-fold since 2005, while on-eBay TPV has roughly doubled. Merchant Services TPV growth is a result of increasing the number of online stores on which it is offered and gaining share within those stores.

Exhibit 22

Merchant services TPV has grown approximately 4x faster than On-eBay TPV Indexed LTM worldwide TPV ($ bn)

0

200

400

600

800

1,000

Jun-06 Dec-07 Jun-09 Dec-10 Jun-12

Merchant Services On-eBay

Indexed LTM worldwide TPV ($ bn)

0

200

400

600

800

1,000

Jun-06 Dec-07 Jun-09 Dec-10 Jun-12

Merchant Services On-eBay Source: Company Data, Morgan Stanley Research

PayPal provides an attractive value proposition to both merchants and customers, which is evident from an increase in eBay GMV penetration First, for merchants, PayPal’s payment service costs about the same, or slightly less, than credit cards. Further, PayPal reduces “checkout abandonment,” where customers leave the checkout page because typing in billing or shipping information is too cumbersome or time-consuming. Finally, PayPal has built a worldwide customer base of 117MM active users, which is can leverage to generate other revenue streams.

For customers, PayPal offers a secure way to pay for goods or services online, because the merchant never receives the payment information, just a debit into the merchant’s PayPal account. PayPal also offers the consumer a more convenient way to purchase products online.

Exhibit 23

PayPal’s penetration of eBay GMV has steadily increased since 2006 PayPal On-eBay penetration

30%

40%

50%

60%

70%

80%

90%

100%

Jun-08

Dec-08

Jun-09

Dec-09

Jun-10

Dec-10

Jun-11

Dec-11

Jun-12

PayPal On-eBay penetration

30%

40%

50%

60%

70%

80%

90%

100%

Jun-08

Dec-08

Jun-09

Dec-09

Jun-10

Dec-10

Jun-11

Dec-11

Jun-12

Source: Company Data, comScore, Morgan Stanley Research

Outbound shipping is not cheap, and Amazon is in the process of trying to reduce it

While Amazon Prime has driven unit sales up, exponentially, it has also created a material economic burden for the company. Over the last 12 months, Amazon spent nearly as much on shipping as it expensed on fulfillment.

Exhibit 24

Amazon’s shipping costs represent a monetizable opportunity to increase profitability

TTM fulfillment expense (US$ mn)

R2 = 0.9983

--

1,000

2,000

3,000

4,000

5,000

6,000

7,000

-- 1,000 2,000 3,000 4,000 5,000 6,000

TTM outbound shipping costs (US$ mn)

Source: Company Data, Morgan Stanley Research

Reducing shipping costs is a significant opportunity; increased convenience is a byproduct While Amazon enjoys economies of scale with respect to shipping costs, the company spent $4.8B on outbound shipping for the TTM period ending September 2012. We believe that it may be able to realize shipping cost savings by

M O R G A N S T A N L E Y R E S E A R C H

22

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

building fulfillment centers closer to its end customers. While the cost of doing so is not insignificant, the company will likely be able to run these “last-mile” fulfillment centers much more efficiently by curating the merchandise mix toward the fastest turning SKUs. The preceding chart implies that fulfillment costs are variable in nature. Due to Amazon’s growth curve into new product categories and geographies, inventory turnover has come down steadily, which in turn has limited Amazon’s ability to show consolidated efficiency in leveraging its fulfillment network. If Amazon is able to reduce the per-unit variable costs (shipping being one of them) and increase its inventory turnover within new fulfillment centers, we should see fulfillment expense leverage.

Exhibit 25

comScore estimates 10% of eCommerce sales were purchased on a mobile device in 3Q12, up from 3% in 3Q10

$0

$10

$20

$30

$40

$50

$60

2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12

0%

2%

4%

6%

8%

10%

12%US eCommerce ($bn) Percentage spent via mobile devices

Source: comScore, Morgan Stanley Research

Mobile shopping is also an eCommerce growth driver – it adds a layer of convenience – by offering the ability for a customer shop anywhere / anytime comScore estimates 10% of US eCommerce was purchased on a mobile device in 3Q12, and expects that to rise to 13% in the 2012 holiday season. This compares similarly to mobile eCommerce penetration of the UK of 11.6%.

eBay as a mobile case study eBay has built at least eight unique mobile apps, focused on different verticals (general interest, fashion, auto, classifieds,

pets, bar code scanning, etc), which have generated 100MM+ downloads. A well designed app that is additive to the customer experience can be incremental.

eBay estimates it will generate over $10B of mobile GMV in 2012, up from $5B in 2011. This translates to about 13% of total GMV (including autos). Company management has implied about 1/3 of this mobile GMV is incremental, which means eBay generated about 4% of incremental GMV from mobile, or $3.3B.

Exhibit 26

In 2012, Mobile GMV would represent 13% of eBay’s total GMV Source of eBay GMV (including auto)

100% 99% 97% 93% 87%

9%5%

4%2%

--%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012e

IncrementalMobile GMV

Mobile GMV(Cannibalizedfrom Desktop)

Desktop GMV

Source: eBay, Morgan Stanley Research

Amazon and eBay have led the large-scale innovation cycle for the eCommerce category, both in the United States and Internationally While eCommerce, as a category, certainly extends beyond the scope of just Amazon and eBay, these two eCommerce retailers have built sustainable business models on a foundation of innovation. They continue to lead the disruption of traditional retailers by maintaining acute focus on low price, broad selection and increased convenience. We believe both Amazon and eBay will continue to lead the transition from traditional to eCommerce sales for years to come.

M O R G A N S T A N L E Y R E S E A R C H

23

January 6, 2013 eCommerce Disruption: A Global Theme – Transforming Traditional Retail

US Retail

Mark Wiltamuth (Food, Drug and Discounters)

Joseph Parkhill (Branded Apparel & Footwear)

David Gober (Hardlines)

Kimberly Greenberger (Softlines)

Executive Summary / Key Takeaways

Best-positioned: Williams-Sonoma, Under Armour, Macy’s Nordstrom, Urban Outfitters, Costco, and Walmart Challenged: Bed Bath & Beyond, RadioShack

Food, Drug and Discounters

1. Costco and the club stores can still win in the Internet era due to their low prices and focus on the food / perishables that are not easy to ship.

2. We believe Walmart has the potential to become a global leader in eCommerce sales. Walmart’s buying power ensures it will not be beaten on price, and we expect it to buy or build its way to a stronger competitive position in this channel.

Branded Apparel

1. As brands control their own distribution, they remain largely insulated from typical pressures from pure online competition.

2. eCommerce provides a key avenue to enter markets internationally and elevate brand awareness with new consumers.

Hardlines

1. Consumer Electronics – eCommerce penetration is high (47%), and likely to keep growing. Best Buy and Radio Shack are negatively impacted, but Radio Shack least prepared with 1% of total revenue generated online.

2. Home Furnishings – about 30% of furnishings buyers shop online. Williams-Sonoma is well positioned (33% of total sales online) while Bed Bath and Beyond is not, given 1% of revenue online, decentralized distribution and high skew of branded, easily price comparable products.

Softlines

1. A secular shift towards eCommerce has compelled apparel retailers to develop, expand and enhance their online platforms.

2. Softlines retail is one of the most defensible retail categories against online only competition.

eCommerce Key Trends for Retailers:

Exhibit 27

Online penetration varies across the retail industry

0%

20%

40%

60%

80%

Bo

oks

Clo

thin

g

Co

ns.e

lect

ron

ics

Jew

elry

Sh

oes

Ath

letic

we

ar

Sp

ort

ing

go

ods

Ho

me

furn

ish

ing

s

Off

ice

su

ppl

ies

Pe

rs.

Ca

re &

HH

LD

pro

d

Ho

me

impr

ove

me

nt

Pe