Alex Spiroglou, DipTA (ATAA) ECF Securities Derivatives Dept

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

��������������� � ��������������� � ��������������������������� ������������������������������������� ����������

Alex Spiroglou, DipTA (ATAA)ECF SecuritiesDerivatives Dept

Speaker BackgroundMr Spiroglou is working in the Derivatives Dept of Energon Capital Finance.Performing Advisory Derivatives Portfolio Management for a private client base,and also produces the “Daily Market Strategies” report , covering the commodities, equity, currency and fixed income markets based on quantitative, intermarket and technical criteria.He holds a Bsc in “Banking and International Finance” from City Univercity, LondonHe also has the following professional qualification titles :- Investment Management Certificate (U.K. Society of Investment Professionals)- Diploma in Technical Analysis (Australian Technical Analysts Association)- Market Maker Certificate (ADEX)- Client Consultant Certificate (ADEX)- Investment Consultant Certificate (HCMC)

If you interested in the Notes accompanying this Presentation , feel free to email me at : [email protected]

q PART I ………….……………………………..…..2

- Introduction

- The Necessity for Intermarket Analysis

- Basic Principles

- Asset Allocation & Market Timing Uses

q PART II ………….……………………………..…..17

- Comparison to Technical & Fundamental Analysis

- Limitations of Intermarket Research

q PART III ………….…………………………….…..25

- Systemizing Intermarket Analysis

- Mechanical Trading

- SemiMechanical Trading

Stocks

Bonds

Commodites

Forex

� What is Intermarket Analysis ?

� What is the Markets’ Message ?

� Is it just another Theory ?

� Think like a Fundamentalist , Trade like a Tehnician

PART I (Introduction)

� What is so “New” about the New Global Economy ?

PART I (The Necessity of a Global View)

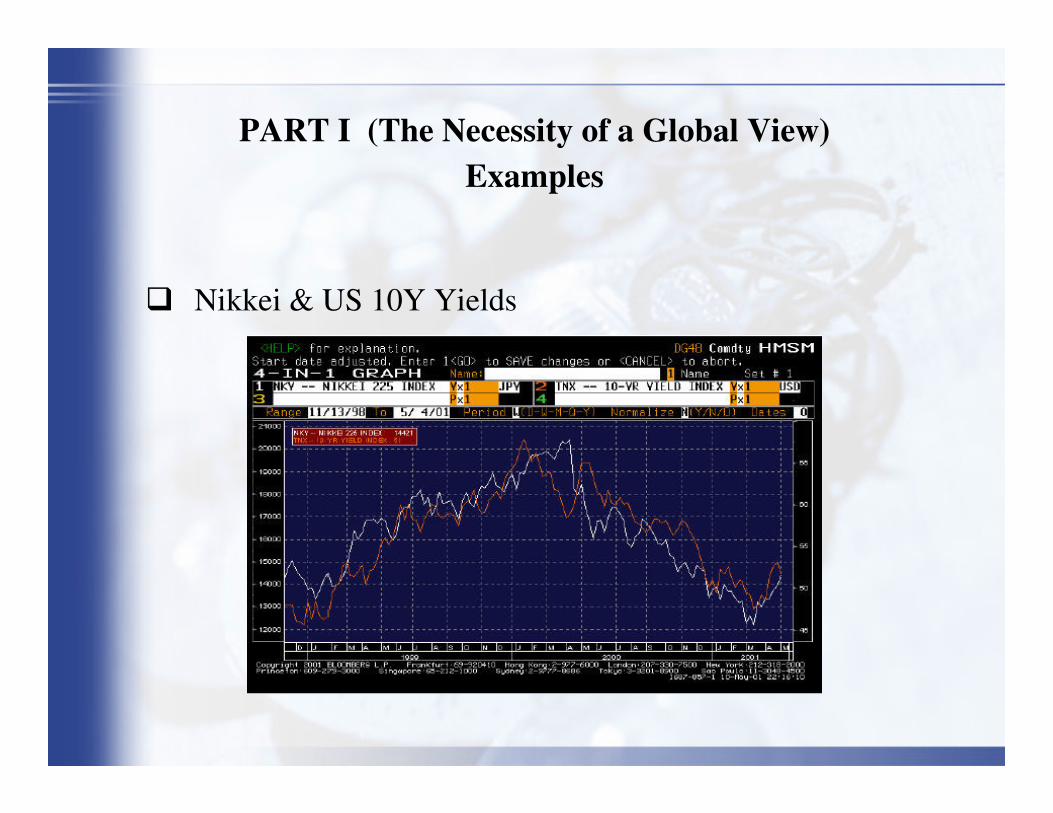

� Nikkei & US 10Y Yields

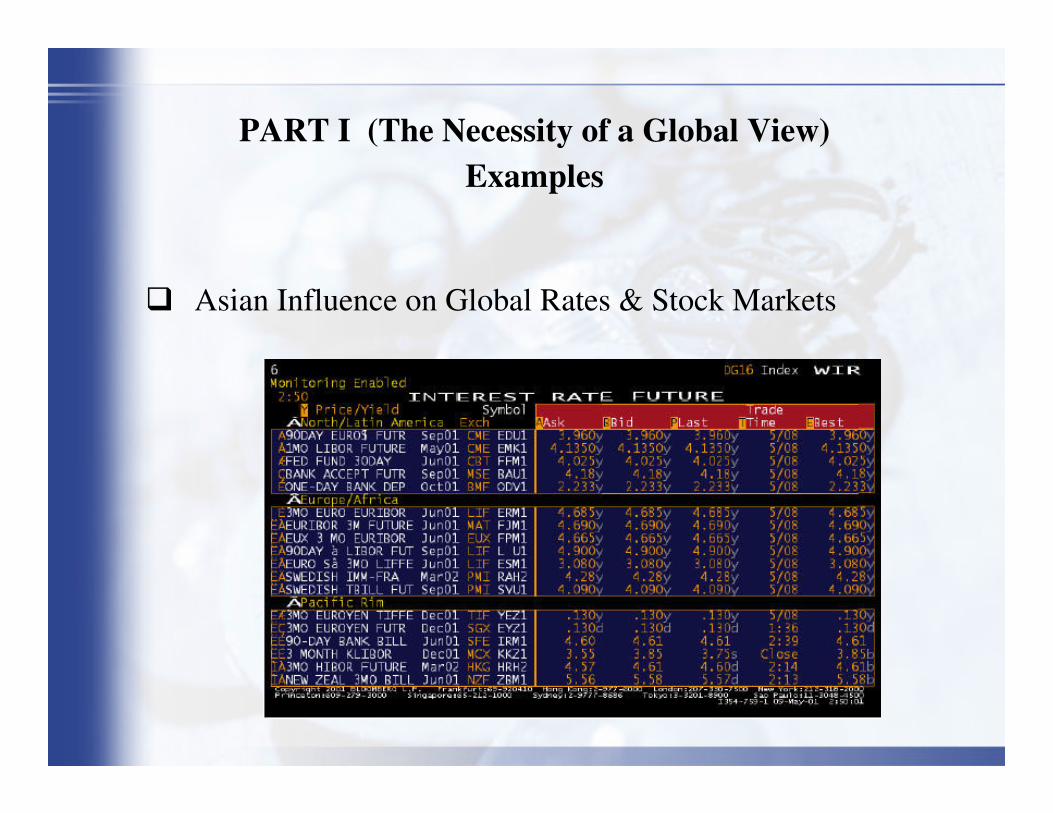

PART I (The Necessity of a Global View)Examples

� Asian Influence on Global Rates & Stock Markets

PART I (The Necessity of a Global View)Examples

The Assumptions behind Intermarket Analysis

� All markets are interrelated, they don’t move in isolation.

� Intermaket work provides background data.

� Intermarket work uses external , as opposed to internal data.

� Heavy emphasis is placed on the futures market

PART I (Basic Principles)

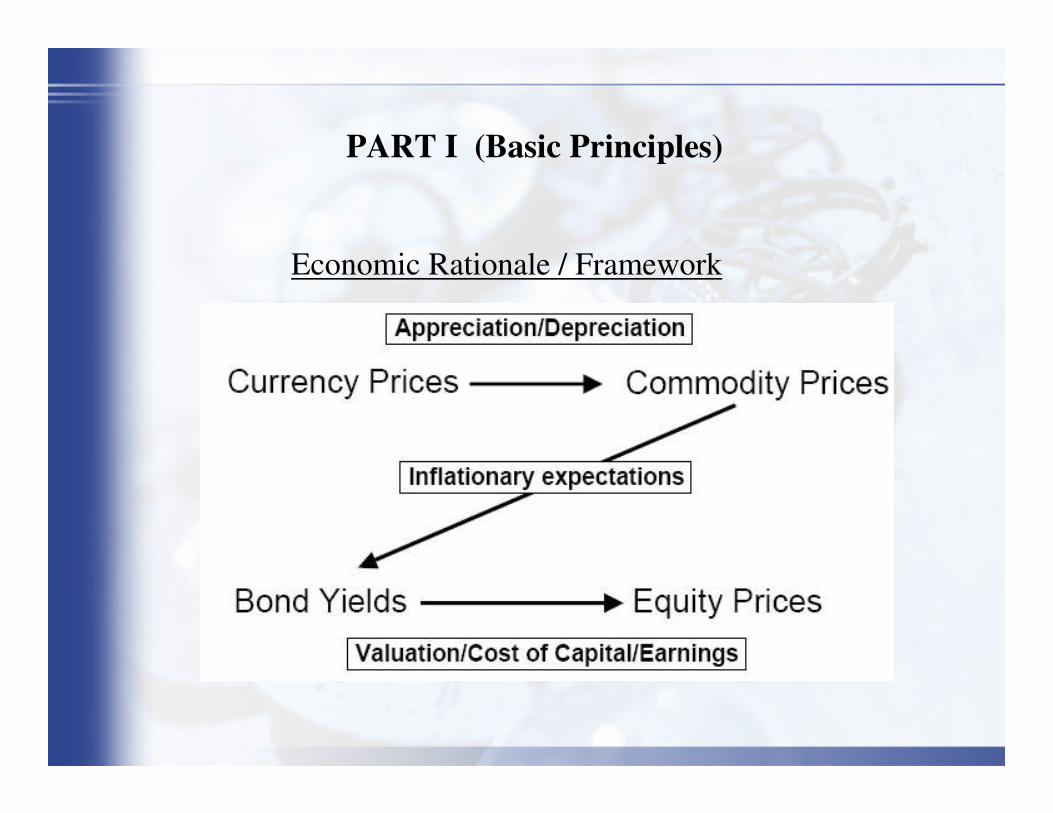

Economic Rationale / Framework

PART I (Basic Principles)

PART I (Basic Principles)

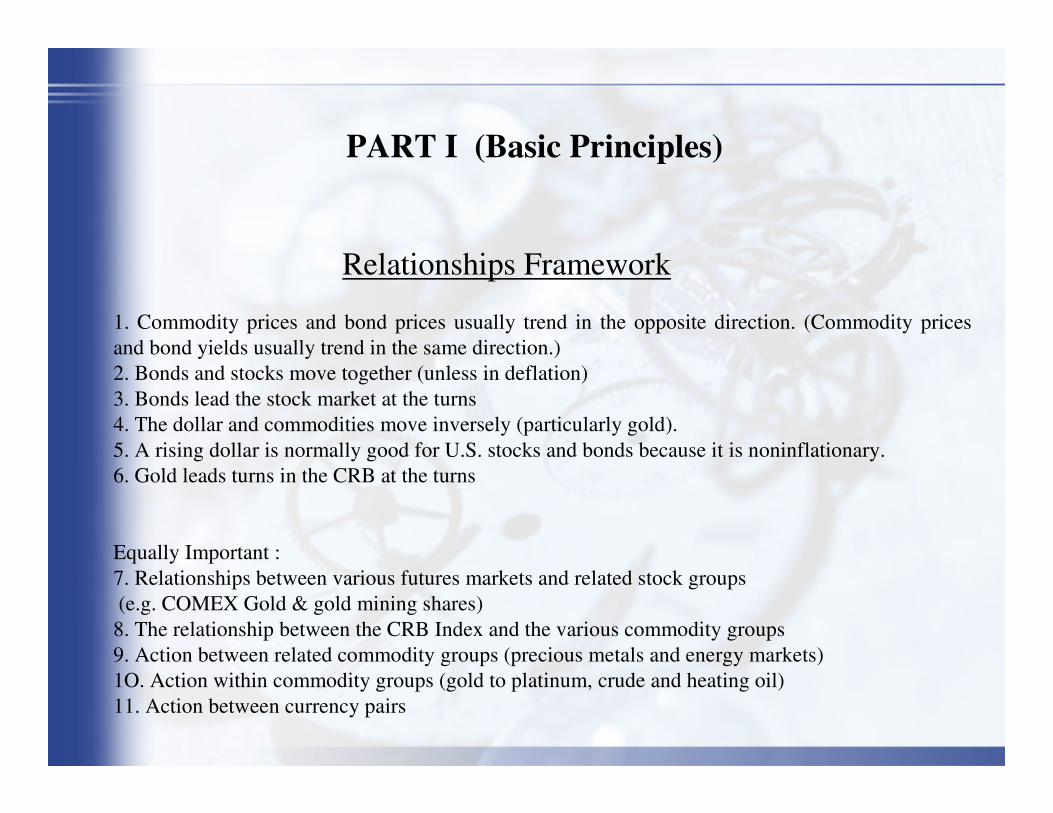

Relationships Framework

1. Commodity prices and bond prices usually trend in the opposite direction. (Commodity prices and bond yields usually trend in the same direction.) 2. Bonds and stocks move together (unless in deflation)3. Bonds lead the stock market at the turns4. The dollar and commodities move inversely (particularly gold).5. A rising dollar is normally good for U.S. stocks and bonds because it is noninflationary.6. Gold leads turns in the CRB at the turns

Equally Important :7. Relationships between various futures markets and related stock groups (e.g. COMEX Gold & gold mining shares)8. The relationship between the CRB Index and the various commodity groups 9. Action between related commodity groups (precious metals and energy markets)1O. Action within commodity groups (gold to platinum, crude and heating oil)11. Action between currency pairs

PART I (Basic Principles)Rising Bond Prices are Usually Good for Stock Prices

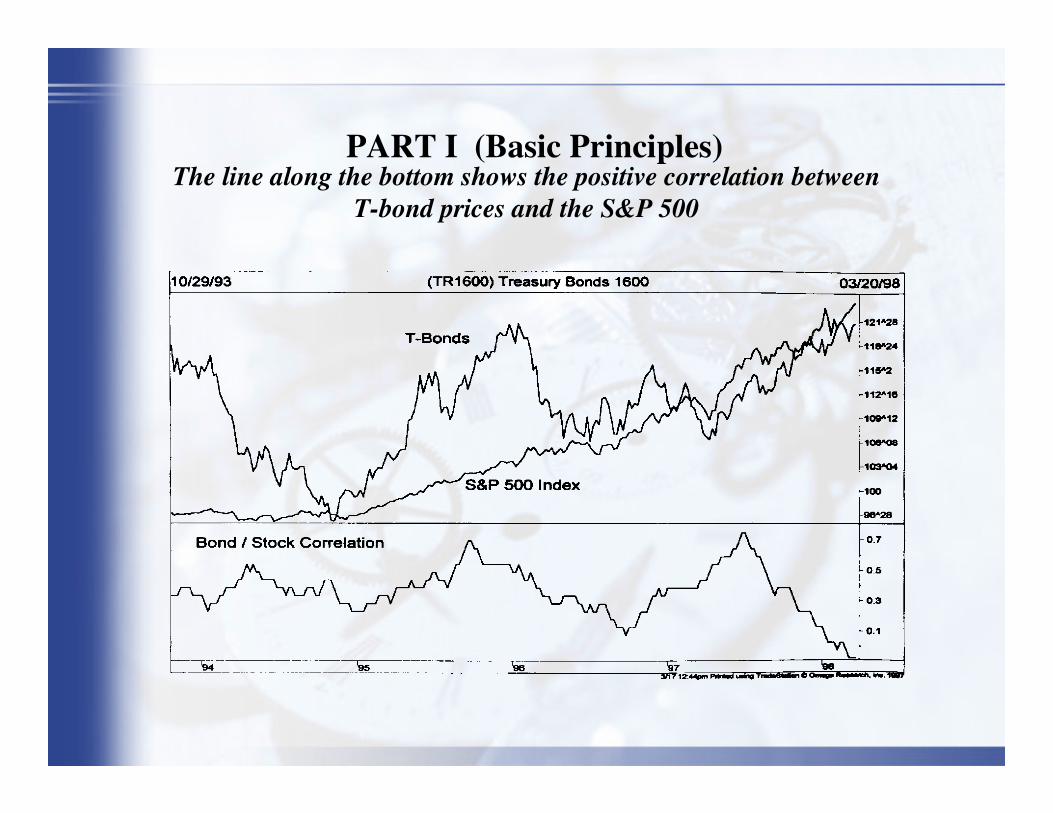

PART I (Basic Principles)The line along the bottom shows the positive correlation between

T-bond prices and the S&P 500

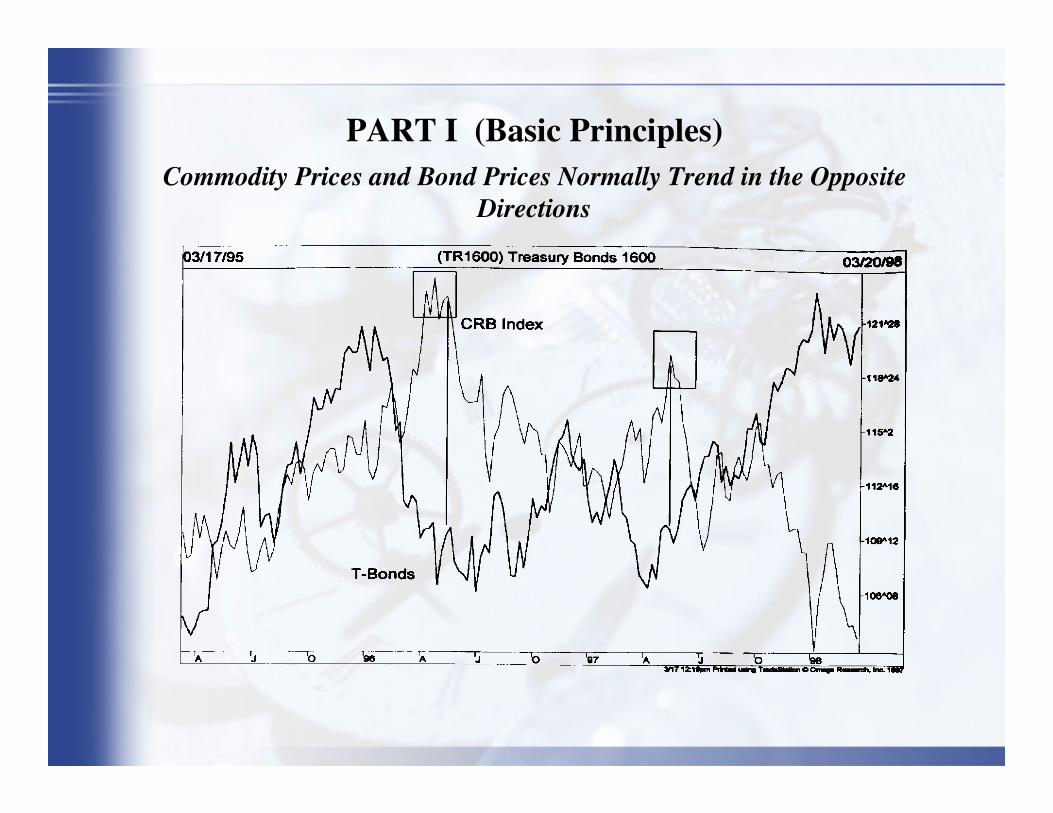

PART I (Basic Principles)Commodity Prices and Bond Prices Normally Trend in the Opposite

Directions

PART I (Basic Principles)

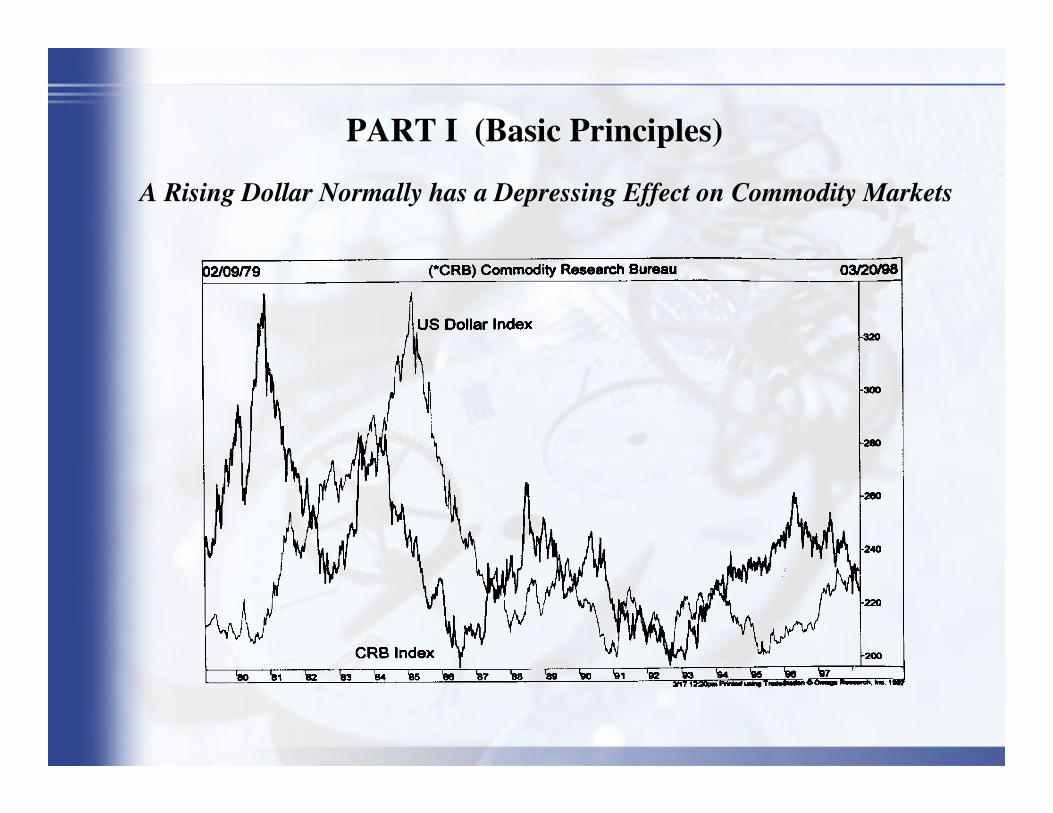

A Rising Dollar Normally has a Depressing Effect on Commodity Markets

PART I (Basic Principles)

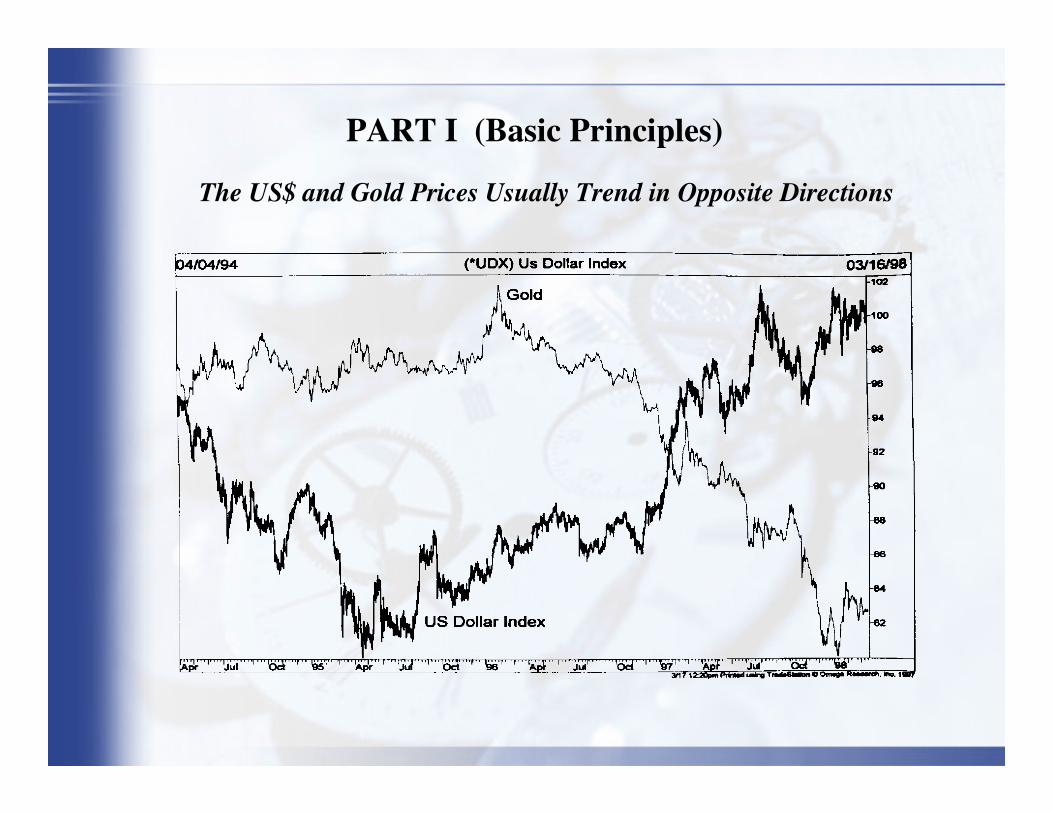

The US$ and Gold Prices Usually Trend in Opposite Directions

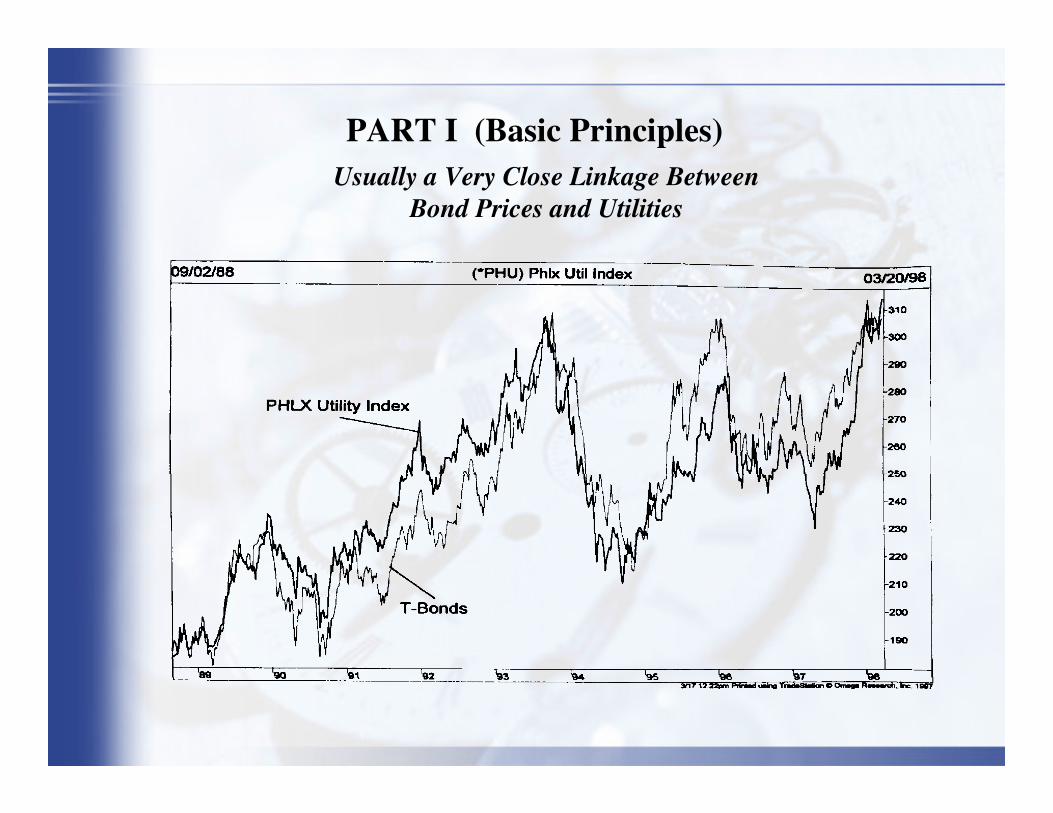

PART I (Basic Principles)Usually a Very Close Linkage Between

Bond Prices and Utilities

PART I (Basic Principles)

Chronological Framework

PART I ( Asset Allocation & Market Timing Uses)

Economic Forecasting

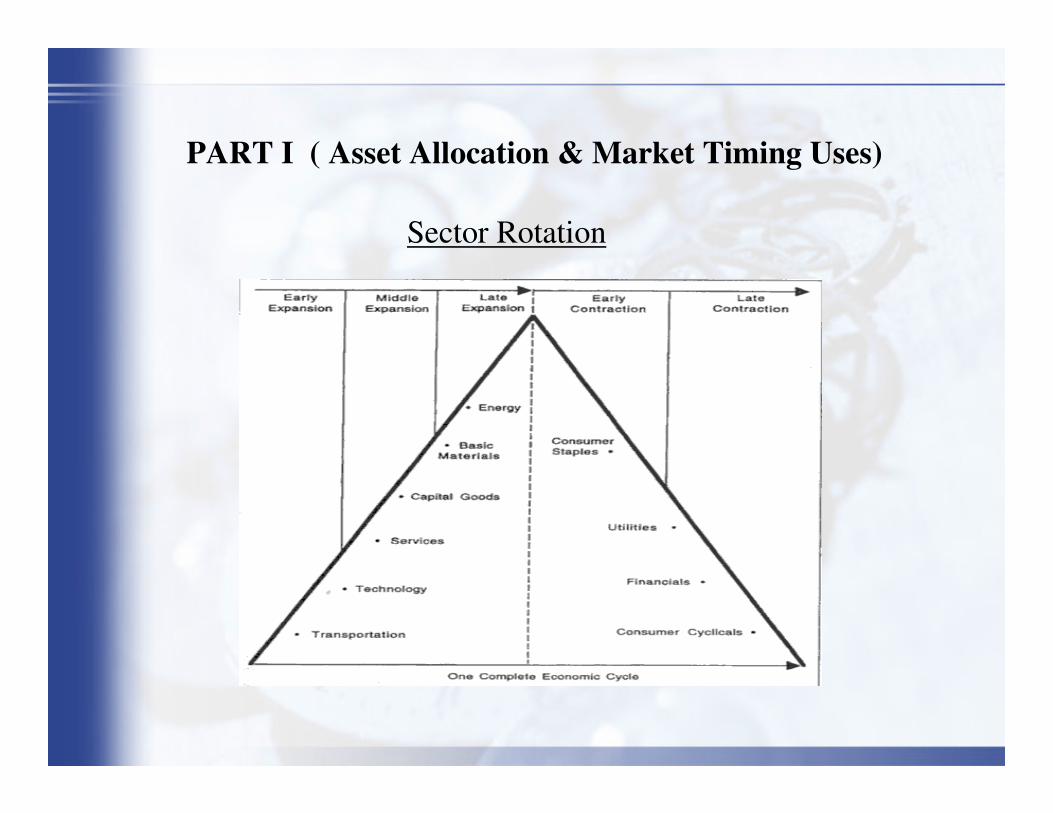

PART I ( Asset Allocation & Market Timing Uses)

Sector Rotation

PART I ( Asset Allocation & Market Timing Uses)

Market Timing

Leading Market Relationships“Leading” markets, could pinpoint potential trading

opportunities, as they are about to unfold-“Leading” markets could help identify trends so traders could catch a bigger portion of each move

Coincident Market Relationships-False signals could be minimized because the full picture is taken into consideration, not just a small piece of it-Stops could be placed on how related markets are affecting the market being traded.-Divergences between correlated markets can help spot short / medium / long term price disclocations.

PART I ( Asset Allocation & Market Timing Uses)

What other Strategies can be devised and Opportunities exploited ?

Ø Intermarket Spreads

Ø Intramarket Spreads

Ø Pairs Trading

PART II (Comparison to Single Market TA )

Single Market Technical analysis (on its own) is incomplete , as an exclusive technical focus is counter-productive. Reliance on price based indicators (solely) may limit our understanding of what drives the markets. In other words, by obsessing about price, we might be sacrificing deeper insight into the root causes of price behaviour.Intermarket Analysis - by turning the focus of the technical analyst outward instead of inward- provides a more rational understanding of technical forces at work in the marketplace. It is impossible to do intermarket work without understanding of the fundamental forces behind those moves.

By incorporating “exogenous” factors – say interest rates – we add a helpful causative dimension to our treatment.This way the timing logic takes into account not only price action – which can be deceptive – but some of the defining properties that help shape and determine price behaviour

PART II (Comparison to Fundamental Analysis )

� Transferable

� Global , not Local

� Market Driven

� Focal Points

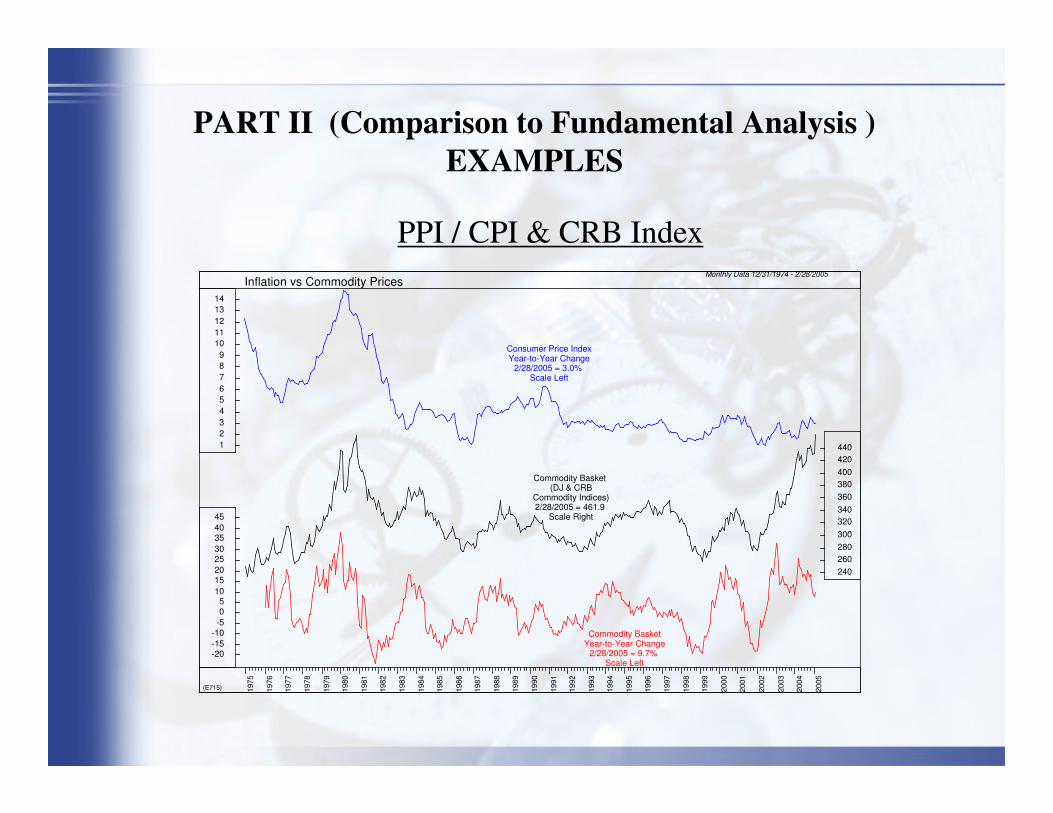

PART II (Comparison to Fundamental Analysis )EXAMPLES

(E715)

Monthly Data 12/31/1974 - 2/28/2005

Consumer Price IndexYear-to-Year Change

2/28/2005 = 3.0% Scale Left

123456789

1011121314

Commodity Basket (DJ & CRB

Commodity Indices)2/28/2005 = 461.9

Scale Right

240260280300320340360380400420440

Commodity BasketYear-to-Year Change

2/28/2005 = 9.7% Scale Left

-20-15-10-505

1015202530354045

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Inflation vs Commodity Prices

PPI / CPI & CRB Index

PART II (Limitations of Intermarket Research)

� Information Overflow

� Limited Historical Data

PART III ( Systemizing Intermarket Analysis )

� We have no choice

� Structure , Discipline & Risk Values

� Markets provide enormous amounts of information

� Our Competitors do it…

Why Systemize ?

PART III ( Systemizing Intermarket Analysis )

� Can be…

� Can be classified as…

� Can be used as…

� Can be used in…

Market Correlations…

PART III ( Systemizing Intermarket Analysis )

Mechanical Trading Discretionary Trading

Semi- Mechanical Trading

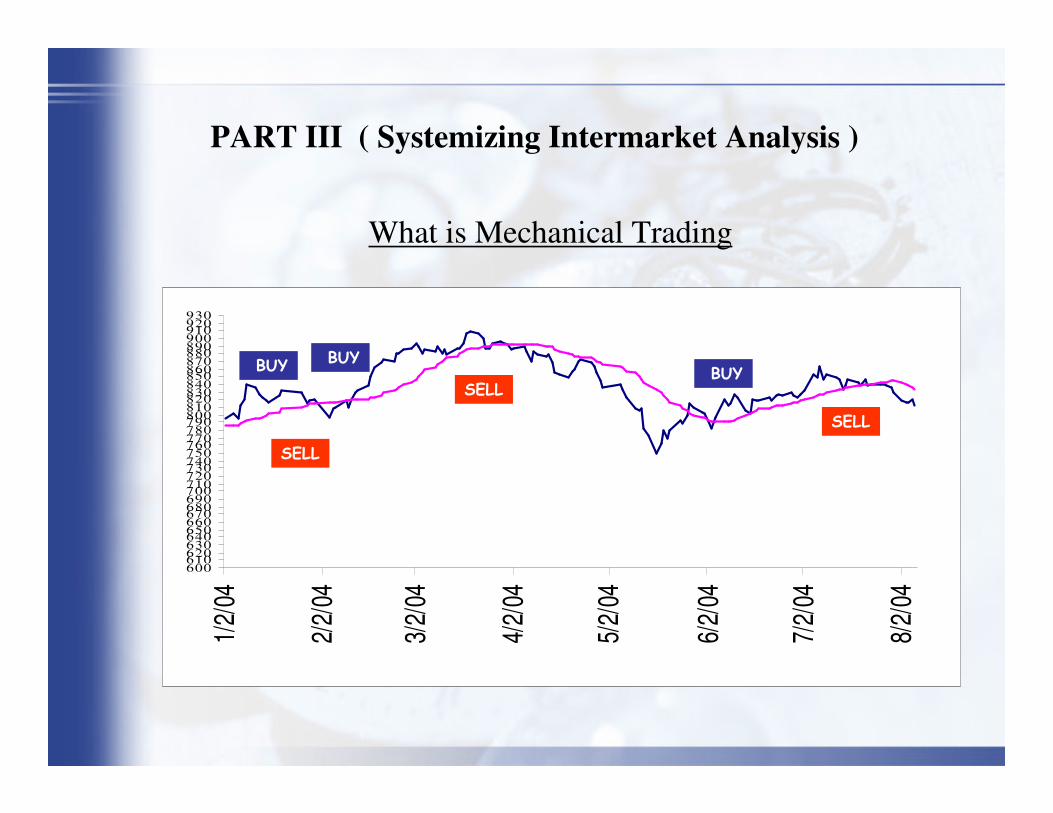

PART III ( Systemizing Intermarket Analysis )

What is Mechanical Trading

600610620630640650660670680690700710720730740750760770780790800810820830840850860870880890900910920930

1/2/

04

2/2/

04

3/2/

04

4/2/

04

5/2/

04

6/2/

04

7/2/

04

8/2/

04

������

� ���

� ���

� ���

���

PART III ( Systemizing Intermarket Analysis )

Why not go completely Mechanical ?

� Not everything can be modelled

� Experience cannot be “pigeon-holed”

� No (modelled) Strategy works across all time frames

� Systems are often over-optimised

PART III ( Systemizing Intermarket Analysis )

Semi – Mechanical Trading

The essence of the Semi-Mechanical Trading approach is not to “forecast” & predict the

future (unlike discretionary trading), but to objectively identify substantially different

average return / risk characteristics of the present.

Mechanical Entry / Exit Rules (signals) can be overiden and are usually combined with the

underlying technical picture in order to align our investment position with the specific

market characteristis that we identify at any given point in time.

Objective Models / Ranking Systems are devised (providing weight of the evidence) in

order to facilitate a disciplined yet flexible decision – making process.

PART III ( Systemizing Intermarket Analysis )Examples

ISM & the S&P 500

(S1100)

Monthly Data 7/31/1950 - 2/28/2005 (Log Scale)

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

Signals Generated When ISM Index:Declines by 7 Points = BuyRises by 22 Points = Sell

Profitable Trades: 78%Gain/Annum: 9.7%Buy-Hold Gain/Annum: 8.0%Latest Signal 7/31/2004 = 1101.72

1318233040526990

118155203267350459602790

103613591784

1318233040526990

118155203267350459602790

103613591784

Declining = Bullish

Rising =Bearish

333639424548525660657075818794

333639424548525660657075818794

Standard & Poor's 500 Stock Index

Source: Institute for Supply ManagementISM Report on BusinessInstitute for Supply Management Price Index

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

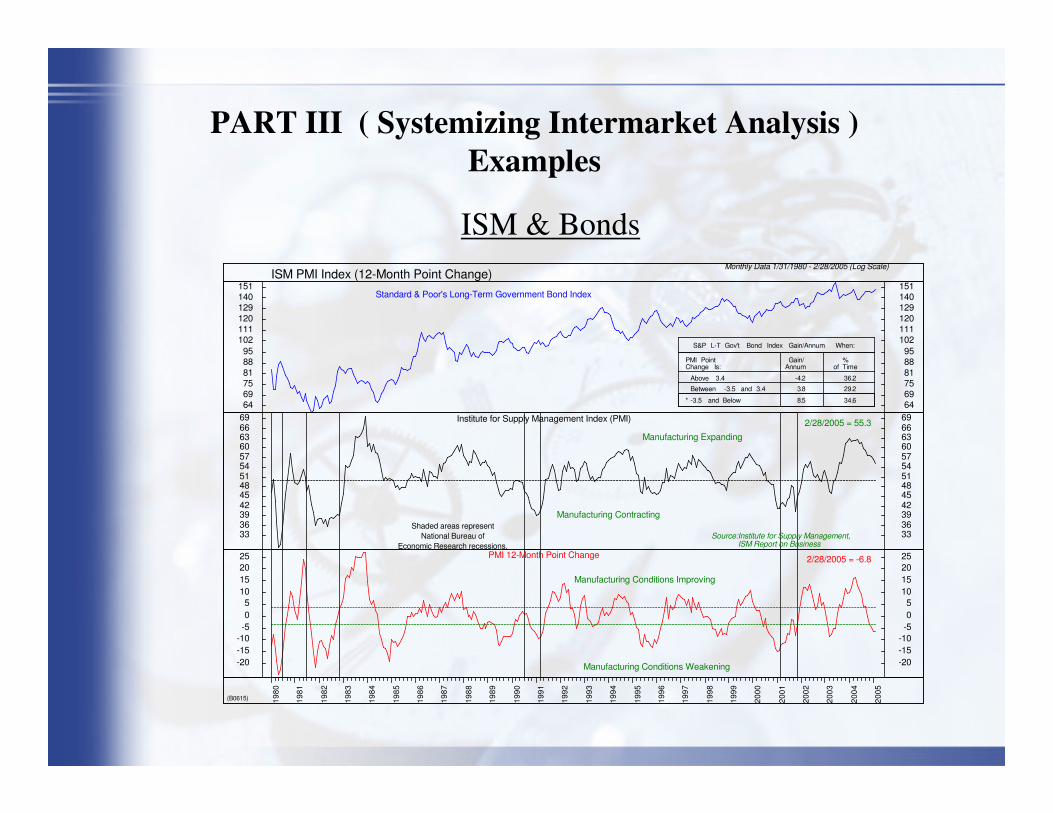

PART III ( Systemizing Intermarket Analysis )Examples

ISM & BondsMonthly Data 1/31/1980 - 2/28/2005 (Log Scale)

(B0615)

Standard & Poor's Long-Term Government Bond Index

S&P L-T Gov't Bond Index Gain/Annum When:

PMI Point Gain/ %Change Is: Annum of Time

Above 3.4 -4.2 36.2

Between -3.5 and 3.4 3.8 29.2

* -3.5 and Below 8.5 34.6646975818895

102111120129140151

646975818895

102111120129140151

Institute for Supply Management Index (PMI)

Shaded areas representNational Bureau of

Economic Research recessions.Source:Institute for Supply Management,

ISM Report on Business

2/28/2005 = 55.3

Manufacturing Expanding

Manufacturing Contracting

33363942454851545760636669

33363942454851545760636669

Manufacturing Conditions Improving

Manufacturing Conditions Weakening

2/28/2005 = -6.8PMI 12-Month Point Change

-20-15-10-505

10152025

-20-15-10-505

10152025

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

ISM PMI Index (12-Month Point Change)

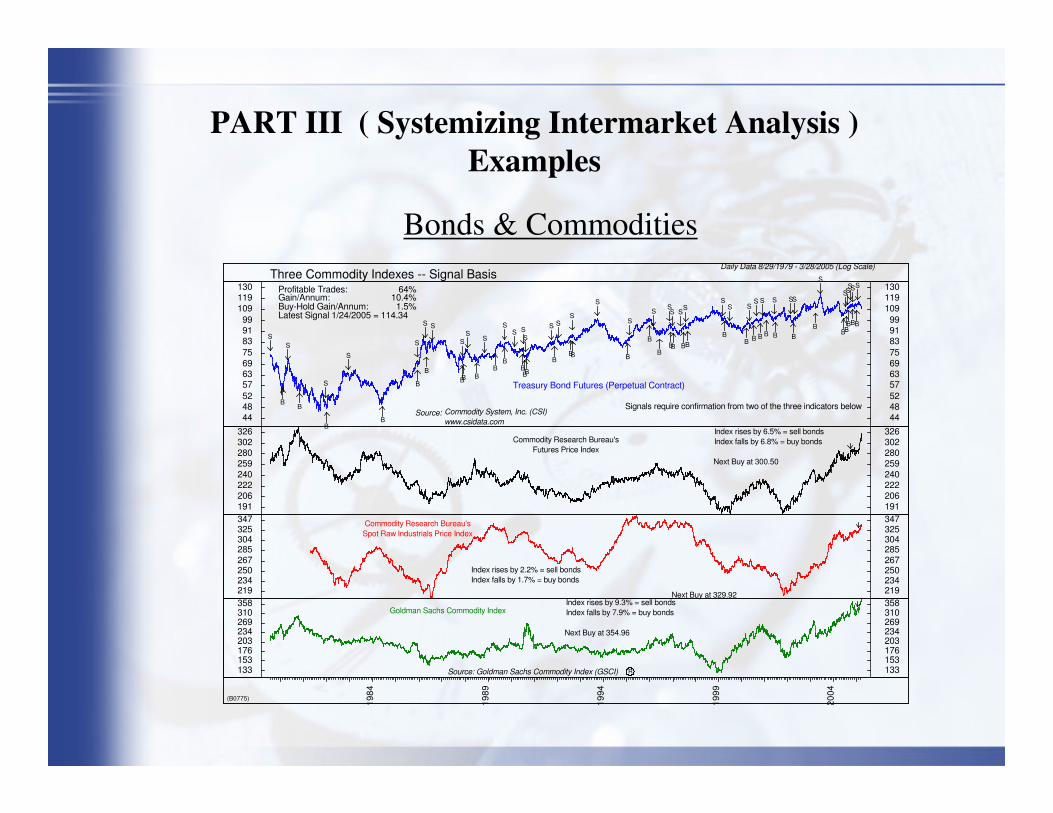

PART III ( Systemizing Intermarket Analysis )Examples

Bonds & Commodities

(B0775)

Daily Data 8/29/1979 - 3/28/2005 (Log Scale)

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

B

S

Treasury Bond Futures (Perpetual Contract)

Profitable Trades: 64%Gain/Annum: 10.4%Buy-Hold Gain/Annum: 1.5%Latest Signal 1/24/2005 = 114.34

Signals require confirmation from two of the three indicators belowSource: Commodity System, Inc. (CSI)

www.csidata.com44485257636975839199

109119130

44485257636975839199

109119130

Commodity Research Bureau'sFutures Price Index

Index rises by 6.5% = sell bondsIndex falls by 6.8% = buy bonds

Next Buy at 300.50

191206222240259280302326

191206222240259280302326

Commodity Research Bureau'sSpot Raw Industrials Price Index

Index rises by 2.2% = sell bondsIndex falls by 1.7% = buy bonds

Next Buy at 329.92219234250267285304325347

219234250267285304325347

Goldman Sachs Commodity IndexIndex rises by 9.3% = sell bondsIndex falls by 7.9% = buy bonds

Next Buy at 354.96

Source: Goldman Sachs Commodity Index (GSCI) R133153176203234269310358

133153176203234269310358

1984

1989

1994

1999

2004

Three Commodity Indexes -- Signal Basis

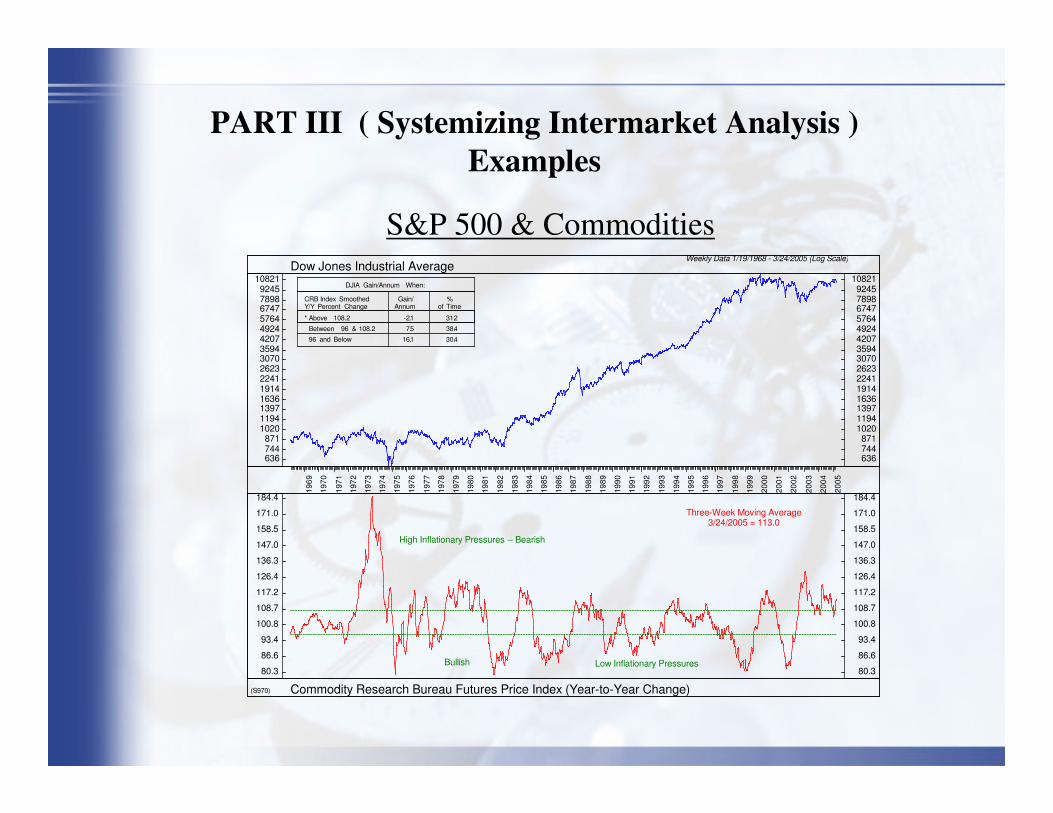

PART III ( Systemizing Intermarket Analysis )Examples

S&P 500 & CommoditiesWeekly Data 1/19/1968 - 3/24/2005 (Log Scale)

(S970)

DJIA Gain/Annum When:

CRB Index Smoothed Gain/ %Y/Y Percent Change Annum of Time

* Above 108.2 -2.1 31.2

Between 96 & 108.2 7.5 38.4

96 and Below 16.1 30.4

636744871

102011941397163619142241262330703594420749245764674778989245

10821

636744871

102011941397163619142241262330703594420749245764674778989245

10821

High Inflationary Pressures -- Bearish

Low Inflationary PressuresBullish

Three-Week Moving Average3/24/2005 = 113.0

80.3

86.6

93.4

100.8

108.7

117.2

126.4

136.3

147.0

158.5

171.0

184.4

80.3

86.6

93.4

100.8

108.7

117.2

126.4

136.3

147.0

158.5

171.0

184.4

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Commodity Research Bureau Futures Price Index (Year-to-Year Change)

Dow Jones Industrial Average

Concluding Remarks

“Although the scope of intemarket analysis is broad, forcing us to stretch our

imaginations and expand our vision, the potential benefit is well worth the

extra effort. I am excited about the prospects of intermarket analysis …. The

question is no longer whether or not we should take intermarket comparisons

into consideration, but rather how soon we should begin..”

John J. Murphy

Market Correlations…

NOTES

This presentation is largely informational and by no means exhaustive.

More advanced strategies (that have been developed based on the ideas pioneered by

Mr Murphy ) have not been presented as they are :

(i) beyond the scope of the presentation

(ii) are proprietary

Charts : Some charts are courtesy of Ned Davis Research

Commentary : parts of the presentation include excerpts of Mr. Murphy’s books

REFERENCES & RECOMMENDED READING

John J. Murphy “ Intermarket Technical Analysis ”

John J. Murphy “ Intermarket Analysis, Profiting from Global Market Relationships ”

Martin Pring “ The All –Season Investor ”

Murray Ruggiero “ Cybernetic Trading Strategies ”

Mark Boucher “ The Hedge Fund Edge ”

Ned Davis “ Being Right or Making Money”

Ned Davis “The Triumph of Contrarian Investing”

Geoffrey Moore “Leading Indicators for the 1990’s”

Stephen Leeb “ Market Timing for the Nineties ”

Marty Zweig “Winning on Wall Street ”

Timothy Hays : “ The Research Driven Investor “

George Dagnino “ Profiting in Bull or Bear Markets “

Related Documents

![[Derivatives Consulting Group] Introduction to Equity Derivatives](https://static.cupdf.com/doc/110x72/5525eed15503467c6f8b4b12/derivatives-consulting-group-introduction-to-equity-derivatives.jpg)